☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Quarterly Period Ended March 31, 2026

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Transition Period from to

COMMISSION FILE NUMBER: 000-16509

CITIZENS, INC.

(Exact name of registrant as specified in its charter)

Colorado

84-0755371

(State or other jurisdiction of incorporation or organization)

(I.R.S. Employer Identification No.)

11815 Alterra Pkwy, Floor 15, Austin, TX78758

(Current Address)

Registrant's telephone number, including area code: (512) 837-7100

Securities registered pursuant to Section 12(b) of the Act

Class A Common Stock

CIA

NYSE

(Title of each class)

(Trading symbol(s))

(Name of each exchange on which registered)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.xYeso No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). xYesoNo

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act:

Large accelerated filer

☐

Accelerated filer

☒

Non-accelerated filer

☐

Smaller reporting company

☒

Emerging growth company

☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes x No

As of May 1, 2026, the Registrant had 50,553,564 shares of Class A common stock outstanding.

Class A, no par value, 100,000,000 shares authorized, 54,662,129 and 54,625,652 shares issued and outstanding in 2026 and 2025, respectively, including shares in treasury of 4,327,810 in 2026 and 2025

272,771

272,294

Class B, no par value, 2,000,000 shares authorized, 1,001,714 shares issued and outstanding in 2026 and 2025, including shares in treasury of 1,001,714 in 2026 and 2025

3,184

3,184

Retained earnings

73,921

71,653

Accumulated other comprehensive income (loss)

(87,483)

(88,421)

Treasury stock, at cost

(23,725)

(23,725)

Total stockholders' equity

238,668

234,985

Total liabilities and stockholders' equity

$

1,739,500

1,754,760

See accompanying Notes to Consolidated Financial Statements.

Net increase (decrease) in cash and cash equivalents

(4,456)

(10,916)

Cash and cash equivalents at beginning of year

22,976

29,271

Cash and cash equivalents at end of period

$

18,520

18,355

SUPPLEMENTAL DISCLOSURES OF NONCASH INVESTING AND FINANCING ACTIVITIES:

During the three months ended March 31, 2025, various fixed maturity issuers exchanged securities with book values of $5.7 million for securities of equal value and none during the three months ended March 31, 2026.

The Company had $1.9 million net unsettled security trades at March 31, 2026 and $0.3 million at March 31, 2025.

See accompanying Notes to Consolidated Financial Statements.

The consolidated financial statements include the accounts and operations of Citizens, Inc. ("Citizens" or the "Company"), a Colorado corporation, and its wholly-owned subsidiaries, CICA Life Insurance Company of America ("CLOA"), CICA Life Ltd. ("CICA Bermuda"), Security Plan Life Insurance Company ("SPLIC"), Magnolia Guaranty Life Insurance Company ("MGLIC"), Computing Technology, Inc. ("CTI"), and Nexo Global Services LLC, a Puerto Rico holding company ("Nexo") and its wholly-owned subsidiaries, CICA Life A.I., a Puerto Rico company ("CICA International") and Nexo Enrollment Services LLC, a Puerto Rico service company ("NES"). All significant inter-company accounts and transactions have been eliminated. Citizens and its wholly-owned subsidiaries are collectively referred to as the "Company," "it," "we," "us" or "our".

The consolidated balance sheet as of March 31, 2026, the consolidated statements of operations and comprehensive income (loss) and stockholders' equity for the three months ended March 31, 2026 and March 31, 2025 and the consolidated statements of cash flows for the three months ended March 31, 2026 and March 31, 2025 have been prepared by the Company without audit and are not subject to audit. In the opinion of management, all normal and recurring adjustments to present fairly the financial position, results of operations, and changes in cash flows at March 31, 2026 and for comparative periods have been made. The consolidated financial statements have been prepared in accordance with U.S. generally accepted accounting principles ("U.S. GAAP") for interim financial information and with the instructions to Form 10-Q adopted by the Securities and Exchange Commission ("SEC"). Accordingly, the consolidated financial statements do not include all the information and footnotes required for complete financial statements and should be read in conjunction with the Company’s consolidated financial statements and notes thereto included in our Annual Report on Form 10-K for the year ended December 31, 2025 ("2025 Form 10-K"). Operating results for the interim periods disclosed herein are not necessarily indicative of the results that may be expected for a full year or any future period.

The Company operates through two segments: International Insurance and Domestic Insurance.

International Insurance. All International policies are issued by CICA International. CICA International offers U.S. dollar-denominated products to non-U.S. residents/citizens internationally, including endowment products, which are principally accumulation contracts that incorporate an element of life insurance protection and whole life insurance. These contracts are designed to provide a fixed amount of insurance coverage over the life of the insured and may utilize rider benefits to provide additional increasing or decreasing coverage and annuity benefits to enhance accumulations.

NES provides services to policyholders of CICA International.

Domestic Insurance. Our Domestic Insurance segment operates through our subsidiaries CLOA, which issues whole life, final expense and life products with living benefits throughout the U.S. and SPLIC and MGLIC, which focus on the life insurance needs of the lower-income markets, primarily in Louisiana, Mississippi and Arkansas. Our products in this segment consist primarily of small face amount whole life, industrial life and pre-need policies, which are designed to fund final expenses for the insured, primarily relating to funeral and burial costs. SPLIC also issues critical illness policies.

CTI provides data processing systems and services to the Company.

USE OF ESTIMATES

The preparation of consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent

assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ materially from these estimates.

Significant estimates include those used in the evaluation of credit losses on fixed maturity securities, valuation allowances on deferred tax assets, and actuarially determined assets and liabilities. Certain of these estimates are particularly sensitive to market conditions, and deterioration and/or volatility in the worldwide debt or equity markets could have a material impact on the consolidated financial statements.

SIGNIFICANT ACCOUNTING POLICIES

For a description of all significant accounting policies, see Part IV, Item 15, Note 1. Summary of Significant Accounting Policies in the notes to our consolidated financial statements included in our 2025 Form 10-K, which should be read in conjunction with these accompanying consolidated financial statements.

(2) ACCOUNTING PRONOUNCEMENTS

ACCOUNTING STANDARDS NOT YET ADOPTED

In November 2024, the Financial Accounting Standards Board ("FASB") issued Accounting Standards Update ("ASU") 2024-03, "Income Statement - Reporting Comprehensive Income - Expense Disaggregation Disclosures (Subtopic 220-40): Disaggregation of Income Statement Expenses", which is intended to enhance expense disclosures by requiring additional disaggregation of certain costs and expenses, on an interim and annual basis, within the footnotes to the financial statements. ASU 2024-03 is effective for annual periods beginning after December 15, 2026, and interim reporting periods beginning after December 15, 2027. Early adoption is permitted, and the amendments may be applied either prospectively or retrospectively. This ASU will impact only our disclosures and not our financial condition or results of operations. We are currently evaluating the impact of adopting this pronouncement on the notes to the consolidated financial statements.

No other new accounting pronouncements issued or effective during the year had, or is expected to have, a material impact on our consolidated financial statements.

(3) INVESTMENTS

The Company invests primarily in fixed maturity securities as shown below.

The following tables represent the amortized cost, gross unrealized gains and losses and fair value of fixed maturity securities as of the dates indicated.

The Company's investments in equity securities are shown below.

Fair Value

(In thousands)

March 31, 2026

December 31, 2025

Equity securities:

Bond mutual funds

$

217

219

Common stocks

1,227

1,130

Non-redeemable preferred stock

7

7

Total equity securities

$

1,451

1,356

VALUATION OF INVESTMENTS

Available-for-sale ("AFS") fixed maturity securities are reported in the consolidated financial statements at fair value with the change in fair value recorded through other comprehensive income (loss). Equity securities are also measured at fair value in the consolidated financial statements with the change in fair value recorded through net income (loss). The Company recognized net investment related gains of $0.1 million and $47 thousand for the three months ended March 31, 2026 and 2025, respectively, on equity securities held.

The Company considers several factors in its review and evaluation of individual investments, using the process described in Part IV, Item 15, Note 2. Investments in the notes to the consolidated financial statements of our 2025 Form 10-K to determine whether a credit valuation loss exists. For the three months ended March 31, 2026 and 2025, the Company recorded no credit valuation losses on fixed maturity securities.

For fixed maturity security investments that have unrealized losses as of March 31, 2026 and December 31, 2025, the gross unrealized losses and related fair values that have been in a continuous unrealized loss position by timeframe are as follows.

In each category of our fixed maturity securities described above, we do not intend to sell our investments, and it is not more likely than not that the Company will be required to sell the investments before recovery of their amortized cost bases. As of March 31, 2026 and December 31, 2025, 98.8% and 98.7% of the fair value of our fixed maturity securities portfolio, respectively, were rated investment grade. While the losses are currently unrealized, we continue to monitor all fixed maturity securities on an on-going basis as future information may become available which could result in an allowance being recorded.

These unrealized losses on fixed maturity securities are due to noncredit-related factors, including changes in credit spreads and rising interest rates since purchase, which have little bearing on the recoverability of our investments, hence they are not recognized as credit losses. The fair value is expected to recover as the securities approach maturity or if market yields for such investments decline.

The amortized cost and fair value of fixed maturity securities at March 31, 2026 by contractual maturity are shown in the table below. Actual maturities may differ from contractual maturities because borrowers may have the right to call or prepay obligations with or without call or prepayment penalties. Securities not due at a single maturity date have been reflected based upon final stated maturity.

The Company uses the specific identification method of the individual security to determine the cost basis used in the calculation of realized gains and losses related to security sales.

Three Months Ended

March 31,

(In thousands)

2026

2025

Fixed maturity securities, available-for-sale:

Proceeds

$

11,761

65

Gross realized gains

$

55

1

Gross realized losses

$

368

4

(4) FAIR VALUE MEASUREMENTS

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. We hold AFS fixed maturity securities, which are carried at fair value with changes in fair value reported through other comprehensive income (loss). We also report our equity securities and certain other long-term investments at fair value with changes in fair value reported through the consolidated statements of operations and comprehensive income (loss).

Fair value measurements are generally based upon observable and unobservable inputs. Observable inputs reflect market data obtained from independent sources, while unobservable inputs reflect our view of market assumptions in the absence of observable market information. We utilize valuation techniques that maximize the use of observable inputs and minimize the use of unobservable inputs. All assets and liabilities carried at fair value are required to be classified and disclosed in one of the following three categories.

•Level 1 - Quoted prices for identical instruments in active markets.

•Level 2 - Quoted prices for similar instruments in active markets; quoted prices for identical or similar instruments in markets that are not active; and model-derived valuations whose inputs or whose significant value drivers are observable.

•Level 3 - Instruments whose significant value drivers are unobservable.

Level 1 primarily consists of financial instruments whose value is based on quoted market prices such as U.S. Treasury securities and actively traded mutual fund and stock investments.

Level 2 includes those financial instruments that are valued by independent pricing services or broker quotes. These pricing models are primarily industry-standard models that consider various inputs, such as interest rates, credit spreads and foreign exchange rates for the underlying financial instruments. All significant inputs are observable or derived from observable information in the marketplace or are supported by observable levels at which transactions are executed in the marketplace. Financial instruments in this category primarily include corporate securities, U.S. Government-sponsored enterprise securities, securities issued by states and political subdivisions and certain mortgage and asset-backed securities.

Level 3 is comprised of financial instruments whose fair value is estimated based on non-binding broker prices utilizing significant inputs not based on or corroborated by readily available market information. We have no investments in this category.

The following tables set forth our assets measured at fair value on a recurring basis as of the dates indicated.

March 31, 2026

Level 1

Level 2

Level 3

Total Fair Value

(In thousands)

Financial assets:

Fixed maturity securities:

U.S. Treasury and U.S. Government-sponsored enterprises

$

5,607

1,335

—

6,942

States and political subdivisions

—

262,058

—

262,058

Corporate

40

862,808

—

862,848

Commercial mortgage-backed

—

9,042

—

9,042

Residential mortgage-backed

—

97,639

—

97,639

Asset-backed

—

32,582

—

32,582

Total fixed maturity securities

5,647

1,265,464

—

1,271,111

Equity securities:

Bond mutual funds

217

—

—

217

Common stocks

1,227

—

—

1,227

Non-redeemable preferred stock

7

—

—

7

Total equity securities

1,451

—

—

1,451

Other long-term investments (1)

—

—

—

86,308

Total financial assets

$

7,098

1,265,464

—

1,358,870

(1) In accordance with Subtopic 820-10, certain investments that are measured at fair value using the net asset value per share (or its equivalent) practical expedient are not classified in the fair value hierarchy. The fair value amounts presented in this table are intended to permit reconciliation of the fair value hierarchy to the amounts presented in the consolidated balance sheets.

U.S. Treasury and U.S. Government-sponsored enterprises

$

5,654

1,354

—

7,008

States and political subdivisions

—

268,792

—

268,792

Corporate

42

866,828

—

866,870

Commercial mortgage-backed

—

8,894

—

8,894

Residential mortgage-backed

—

103,088

—

103,088

Asset-backed

—

33,209

—

33,209

Total fixed maturity securities

5,696

1,282,165

—

1,287,861

Equity securities:

Bond mutual funds

219

—

—

219

Common stocks

1,130

—

—

1,130

Non-redeemable preferred stock

7

—

—

7

Total equity securities

1,356

—

—

1,356

Other long-term investments (1)

—

—

—

85,157

Total financial assets

$

7,052

1,282,165

—

1,374,374

(1) In accordance with Subtopic 820-10, certain investments that are measured at fair value using the net asset value per share (or its equivalent) practical expedient are not classified in the fair value hierarchy. The fair value amounts presented in this table are intended to permit reconciliation of the fair value hierarchy to the amounts presented in the consolidated balance sheets.

FINANCIAL INSTRUMENTS VALUATION

FINANCIAL INSTRUMENTS CARRIED AT FAIR VALUE

Fixed maturity securities, available-for-sale. At March 31, 2026, fixed maturity securities, valued using a third-party pricing source, totaled $1.3 billion for Level 2 assets and comprised 93.1% of total reported fair value of our financial assets. The Level 1 and Level 2 valuations are reviewed and updated quarterly through testing by comparisons to separate pricing models, other third-party pricing services, and back tested to recent trades. In addition, we obtain information annually relative to the third-party pricing models and review model parameters for reasonableness. There were no Level 3 assets as of March 31, 2026. For the three months ended March 31, 2026, there were no material changes to the valuation methods or assumptions used to determine fair values, and no broker or third-party prices were changed from the values received.

Equity securities. Our equity securities are classified as Level 1 assets as their fair values are based upon quoted market prices.

Structured note.At March 31, 2026, the Company held an investment in a structured note, which includes components classified as fixed maturity securities and other long-term investments on the consolidated balance sheets. The partner interest is included in other long-term investments and is measured at its net asset value ("NAV") of $2.6 million as a practical expedient, which approximates fair value. The Company recognized investment related losses of $0.1 million for the three months ended March 31, 2026. These investments are included in other long-term investments on the consolidated balance sheets. As of March 31, 2026, we are committed to funding this structured note investment up to $4.1 million over the next nine years.

Limited partnerships. The Company considers the NAV to represent the value of the investment fund and is measured by the total value of assets minus the total value of liabilities. The following table includes information

related to our investments in limited partnerships that calculate NAV per share. For these investments, which are measured at fair value on a recurring basis, we use the NAV per share to measure fair value. The Company recognized net investment related gains of $1.8 million and losses of $1.5 million on limited partnerships held for the three months ended March 31, 2026 and 2025, respectively. These investments are included in other long-term investments on the consolidated balance sheets.

March 31, 2026

December 31, 2025

(In thousands, except for years)

Fair Value Using NAV Per Share

Unfunded Commit- ments

Range

(In years)

Fair Value Using NAV Per Share

Unfunded Commit- ments

Range

(In years)

Description

Limited partnerships:

Middle market

Investments in privately-originated, performing senior secured debt primarily in North America-based companies

$

29,385

—

2

$

30,956

—

2

Late-stage growth

Investments in private late-stage, established companies seeking capital to accelerate growth prior to an IPO or sale

39,603

1,558

2 to 4

36,623

2,232

2 to 4

Infrastructure

Investments in environmental infrastructure and related technology, focusing on renewable power generation and distribution

14,738

2,638

8

15,013

4,052

8

Total limited partnerships

$

83,726

4,196

$

82,592

6,284

The majority of our limited partnership investments are not redeemable because distributions from the funds will be received when the underlying investments of the funds are liquidated. The life spans indicated above may be shortened or extended at the fund manager's discretion, typically in one or two-year increments.

FINANCIAL INSTRUMENTS NOT CARRIED AT FAIR VALUE

Estimates of fair values are made at a specific point in time, based on relevant market prices and information about the financial instruments. The estimated fair values of financial instruments presented below are not necessarily indicative of the amounts the Company might realize in actual market transactions.

The carrying amount and fair value for the financial assets and liabilities on the consolidated financial statements not otherwise disclosed for the periods indicated were as follows:

March 31, 2026

December 31, 2025

(In thousands)

Carrying Value

Fair Value

Carrying Value

Fair Value

Financial assets:

Policy loans

$

67,217

67,217

67,455

67,455

Residential mortgage loan

22

22

24

24

Cash and cash equivalents

18,520

18,520

22,976

22,976

Financial liabilities:

Annuity - investment contracts

69,134

63,098

68,975

64,066

Policy loans. Policy loans had a weighted average annual interest rate of 7.7% at both March 31, 2026 and December 31, 2025 and no specified maturity dates. Policy loans are an integral part of the life insurance policies we have in force, cannot be valued separately and are not marketable. Therefore, the fair value of policy loans

approximates the carrying value reflected on the consolidated balance sheets are considered Level 3 assets in the fair value hierarchy.

Residential mortgage loan. The mortgage loan is secured by a residential property. The interest rate for this loan was 7.0% at both March 31, 2026 and December 31, 2025. At March 31, 2026, the remaining loan matures in two years. Management estimated the fair value using an annual interest rate of 6.25% at both March 31, 2026 and December 31, 2025. Our mortgage loan is considered a Level 3 asset in the fair value hierarchy and is included in other long-term investments on the consolidated balance sheets.

Cash and cash equivalents. The fair value of cash and cash equivalents approximates carrying value and these assets are characterized as Level 1 assets in the fair value hierarchy.

Annuity liabilities. The fair value of the Company's liabilities under annuity contracts, which are considered Level 3 liabilities, was estimated at March 31, 2026 and December 31, 2025 using discounted cash flows based upon spot rates adjusted for various risk adjustments ranging from 3.63% to 5.10% and 3.31% to 4.98%, respectively. The fair value of liabilities under all insurance contracts are taken into consideration in the overall management of interest rate risk, which seeks to minimize exposure to changing interest rates through the matching of investment maturities with amounts due under insurance contracts.

Other long-term investments.Financial instruments included in other long-term investments are classified in various levels of the fair value hierarchy. The following table summarizes the carrying amounts of these investments.

Carrying Value

(In thousands)

March 31, 2026

December 31, 2025

Other long-term investments:

Limited partnerships

$

83,726

82,592

Structured note

2,582

2,565

FHLB common stock

224

222

All other investments

58

60

Total other long-term investments

$

86,590

85,439

We are a member of the Federal Home Loan Bank ("FHLB") of Dallas and such membership requires members to own stock in the FHLB. Our FHLB stock is carried at amortized cost, which approximates fair value.

(5) DEFERRED POLICY ACQUISITION COSTS AND COST OF INSURANCE ACQUIRED

DAC

The following tables roll forward the deferred policy acquisition costs ("DAC") and cost of insurance acquired ("COIA") balances for the three months ended March 31, 2026 and 2025 by reporting cohort. Our reporting cohorts are Permanent, which summarizes insurance policies with premiums payable over the lifetime of the policy, and

Permanent Limited Pay, which summarizes insurance policies with premiums payable for a limited time after which the policy is fully paid up. Both reporting cohorts include whole life and endowment policies.

The Domestic Insurance segment is the only segment that recognizes COIA; therefore, the balances for the three months ended March 31, 2026 and 2025 on a consolidated basis by reporting cohort are shown below.

(In thousands)

Permanent

Permanent Limited Pay

Other Business

Total

Three Months Ended March 31, 2026

Balance, beginning of year

$

7,036

764

1,195

8,995

Amortization expense

(93)

(9)

(86)

(188)

Balance, end of year

$

6,943

755

1,109

8,807

Three Months Ended March 31, 2025

Balance, beginning of year

$

7,424

809

1,213

9,446

Amortization expense

(99)

(13)

14

(98)

Balance, end of year

$

7,325

796

1,227

9,348

(6) POLICYHOLDERS’ LIABILITIES

LIABILITY FOR FUTURE POLICY BENEFITS

The following tables summarize balances of and changes in the liability for future policy benefits for our reporting cohorts: Permanent, which summarizes insurance policies with premiums payable over the lifetime of the policy,

and Permanent Limited Pay, which summarizes insurance policies with premiums payable for a limited time after which the policy is fully paid up. Both reporting cohorts include whole life and endowment policies.

March 31, 2026

(In thousands)

International Insurance

Domestic Insurance

Permanent

Permanent Limited Pay

Total

Permanent

Permanent Limited Pay

Total

Present Value of Expected Net Premiums:

Balance, beginning of year

$

241,394

20,592

261,986

189,845

13,052

202,897

Beginning balance at original discount rate

$

242,912

20,405

263,317

192,071

13,446

205,517

Effect of actual variances from expected experience

937

11

948

(13,394)

(690)

(14,084)

Adjusted beginning of year balance

243,849

20,416

264,265

178,677

12,756

191,433

Issuances

6,319

782

7,101

24,866

483

25,349

Interest accrual

2,466

201

2,667

2,080

122

2,202

Net premiums collected

(9,853)

(1,460)

(11,313)

(6,646)

(103)

(6,749)

Derecognition and other

190

44

234

(1,462)

(50)

(1,512)

Ending balance at original discount rate

242,971

19,983

262,954

197,515

13,208

210,723

Effect of changes in discount rates

(4,106)

23

(4,083)

(4,967)

(493)

(5,460)

Balance, end of period

$

238,865

20,006

258,871

192,548

12,715

205,263

Present Value of Expected Future Policy Benefits:

Balance, beginning of year

$

910,575

166,327

1,076,902

324,382

139,220

463,602

Beginning balance at original discount rate

$

932,243

174,075

1,106,318

339,821

152,775

492,596

Effect of actual variances from expected experience

1,845

721

2,566

(13,531)

(516)

(14,047)

Adjusted beginning of year balance

934,088

174,796

1,108,884

326,290

152,259

478,549

Issuances

6,433

773

7,206

24,867

482

25,349

Interest accrual

10,158

1,734

11,892

3,813

1,788

5,601

Benefit payments

(25,408)

(4,762)

(30,170)

(5,699)

(1,819)

(7,518)

Derecognition and other

75

168

243

(1,472)

8

(1,464)

Ending balance at original discount rate

925,346

172,709

1,098,055

347,799

152,718

500,517

Effect of changes in discount rates

(34,522)

(10,100)

(44,622)

(20,930)

(16,000)

(36,930)

Balance, end of period

$

890,824

162,609

1,053,433

326,869

136,718

463,587

Net liability for future policy benefits

$

651,959

142,603

794,562

134,321

124,003

258,324

Plus: Flooring impact

2

—

2

—

—

—

Less: Reinsurance recoverable

—

—

—

7,705

—

7,705

Net liability for future policy benefits, after reinsurance recoverable

The following table reconciles the net liability for future policy benefits shown above to the liability for future policy benefits reported in the consolidated balance sheets.

March 31, 2026

March 31, 2025

(In thousands)

International

Insurance

Domestic

Insurance

Consolidated

International

Insurance

Domestic Insurance

Consolidated

Life Insurance:

Permanent

$

651,961

126,616

778,577

675,686

125,167

800,853

Permanent limited pay

142,603

124,003

266,606

143,245

126,640

269,885

Deferred profit liability

27,650

39,332

66,982

25,011

36,878

61,889

Other

30,549

24,672

55,221

27,595

16,864

44,459

Total life insurance

852,763

314,623

1,167,386

871,537

305,549

1,177,086

Accident & Health Insurance:

Other

718

681

1,399

529

584

1,113

Total future policy benefit reserves

$

853,481

315,304

1,168,785

872,066

306,133

1,178,199

The following table provides the amount of undiscounted and discounted expected gross premiums and expected future benefit payments for long-term duration contracts.

The following tables summarize the amount of revenue and interest related to long-term duration contracts recognized in the consolidated statement of operations and comprehensive income (loss).

Three Months Ended March 31,

2026

2025

(In thousands)

Gross Premiums

Interest Expense

Gross Premiums

Interest Expense

International Insurance:

Life Insurance:

Permanent

$

21,242

7,692

21,767

8,081

Permanent Limited Pay

4,771

1,767

4,461

1,764

Other

(584)

—

(336)

—

Less:

Reinsurance

384

—

471

—

Total, net of reinsurance

25,045

9,459

25,421

9,845

Accident & Health Insurance:

Other

153

—

187

—

Total

$

25,198

9,459

25,608

9,845

Domestic Insurance:

Life Insurance:

Permanent

$

15,666

1,733

13,389

1,652

Permanent Limited Pay

1,973

2,133

2,123

2,107

Other

453

—

497

—

Less:

Reinsurance

3,610

—

2,082

—

Total, net of reinsurance

14,482

3,866

13,927

3,759

Accident & Health Insurance:

Other

258

—

262

—

Total

$

14,740

3,866

14,189

3,759

The following table provides the weighted-average durations of the liability for future policy benefits.

The following table provides the weighted-average interest rates for the liability for future policy benefits.

March 31, 2026

March 31, 2025

International

Insurance

Domestic

Insurance

International

Insurance

Domestic

Insurance

Permanent:

Interest rate at original discount rate

4.81

%

4.96

%

4.84

%

4.91

%

Interest rate at current discount rate

5.07

%

5.64

%

5.12

%

5.50

%

Permanent Limited Pay:

Interest rate at original discount rate

4.21

%

4.84

%

4.16

%

4.83

%

Interest rate at current discount rate

5.10

%

5.60

%

5.09

%

5.46

%

LIABILITY FOR POLICYHOLDERS’ ACCOUNT BALANCES

The following table presents the policyholders' account balances by range of guaranteed minimum crediting rates and the related range of the difference, in basis points, between rates being credited and the respective guaranteed minimums.

The following table reconciles policyholders' account balances shown above to the policyholders' account balance liability in the consolidated balance sheets.

As of March 31,

(In thousands)

2026

2025

Annuities:

Supplemental contracts without life contingencies

$

91,260

67,838

Fixed annuity

88,423

88,708

Unearned revenue reserve

1,492

1,488

Total annuities

$

181,175

158,034

Premiums paid in advance:

Premiums paid in advance

$

27,141

29,973

Other

2,539

1,991

Total premiums paid in advance

$

29,680

31,964

(7) REINSURANCE

In the normal course of business, the Company reinsures portions of certain policies that we underwrite to mitigate exposure to potential losses and/or to provide additional capacity for growth. In CICA International, prior to April 1, 2025, we retained up to $100,000 on any one individual life insurance policy and reinsured the death benefit amount. For new policies beginning on such date, we increased our retention amount to $250,000 and reinsure amounts above that. We also reinsure 100% of our accidental death benefit rider coverage. In CLOA, we have a coinsurance agreement with RGA Reinsurance Company ("RGA"). Under this agreement, CLOA has elected RGA to reinsure 50% of its final expense business. The Company remains contingently liable in the event that any of the reinsurers are unable to meet their obligations under any reinsurance agreement.

Our amounts recoverable from reinsurers represent receivables from and reserves ceded to reinsurers. We obtain reinsurance from multiple reinsurers and monitor our reinsurance concentration as well as the financial strength ratings of our reinsurers. Their ratings by A.M. Best Company range from A- (Excellent) to A+ (Superior).

A summary of life insurance in force, along with assumed and ceded reinsurance activity, is summarized below as of the periods indicated.

The Company's reinsurance recoverable on ceded reinsurance was $12.9 million and $10.9 million as of March 31, 2026 and December 31, 2025, respectively. Premiums, claims and surrenders assumed and ceded, and expenses ceded for all lines of business are summarized for the periods indicated below.

Three Months Ended

March 31,

(In thousands)

2026

2025

Premiums from short duration contracts:

Direct

$

412

449

Ceded

(1)

(1)

Net premiums earned

411

448

Premiums from long duration contracts:

Direct

43,520

41,901

Assumed

15

11

Ceded

(4,008)

(2,563)

Net premiums earned

39,527

39,349

Total premiums earned

$

39,938

39,797

Claims and surrenders assumed

$

20

(40)

Claims and surrenders ceded

$

(744)

(677)

Commissions assumed and ceded

$

(2,971)

(3,125)

Other general expenses ceded

$

(803)

(588)

(8) COMMITMENTS AND CONTINGENCIES

LITIGATION AND REGULATORY ACTIONS

From time to time, we are subject to legal and regulatory actions relating to our business. We may incur defense costs, including attorneys' fees, and other direct litigation costs associated with defending claims. If we suffer an adverse judgment as a result of litigation claims, it could have a material adverse effect on our business, results of operations and financial condition. Part I. Item 3. Legal Proceedings and Part IV. Item 1. Note 8. Commitments and Contingencies of our consolidated financial statements and notes thereto included in the 2025 Form 10-K includes a discussion of our legal proceedings. There have been no material developments in the three months ended March 31, 2026 from the legal proceedings described in our consolidated financial statements and notes thereto included in the 2025 Form 10-K.

CONTRACTUAL OBLIGATIONS

As of March 31, 2026, we committed to funding investments up to $8.3 million related to limited partnership and structured note investments previously described.

CREDIT FACILITY

On May 3, 2024, the Company renewed its $20 million senior secured revolving credit facility (the “Credit Facility”) with Regions Bank ("Regions"). The Credit Facility has a three-year term, maturing on May 5, 2027, and allows the Company to borrow up to $20 million for working capital purposes, capital expenditures and other corporate purposes.

Revolving loans may be requested by the Company in aggregate minimum principal amounts of $0.5 million per loan. At the Company's election, the revolving loans may either bear a rate (a fluctuating rate per annum) equal to

the greatest of (a) Regions' prime rate, (b) the federal funds rate plus 0.50%, (c) the index rate plus 1.00% or (d) 0.75%. The Company is required to pay Regions an annual commitment fee of 0.375% of the unused portion of the Credit Facility in quarterly installments, which the Company expenses as it is incurred.

Obligations under the Credit Facility are secured by substantially all of the assets of the Company other than the equity interests in its subsidiaries, real estate owned by the Company, and other limited exceptions. The Credit Facility contains customary events of default and financial, affirmative and negative covenants including, but not limited to, restrictions on indebtedness, liens, investments, asset dispositions and restricted payments. As of March 31, 2026, the Company had not borrowed any funds against the Credit Facility and was not in violation of any covenants.

(9) STOCKHOLDERS' EQUITY AND RESTRICTIONS

STOCK

Our Restated and Amended Articles of Incorporation authorize the issuance of 127,000,000 shares, of which 100,000,000 shares shall be Class A common stock, 2,000,000 shares shall be Class B common stock, and 25,000,000 shall be preferred stock. Both authorized classes of common stock are equal in all respects, except (a) each share of Class A common stock is entitled to receive twice the cash dividends paid on a per share basis to the Class B common stock, if any; and (b) the holders of the Class B common stock have the exclusive right to elect a simple majority of the Board of Directors of Citizens. Citizens currently has no outstanding preferred stock or Class B common stock.

A summary of the change in the number of shares of Class A common stock and treasury stock issued is as follows:

2026

2025

Three Months Ended March 31,

(In thousands)

Common Stock Class A

Treasury Stock

Common Stock Class A

Treasury Stock

Balance at beginning of year

54,626

5,330

54,235

5,330

Stock issued for compensation

36

—

1

—

Balance at end of period

54,662

5,330

54,236

5,330

EARNINGS PER SHARE

The following table sets forth the computation of basic and diluted earnings per share of Class A common stock.

Three Months Ended March 31,

2026

2025

(In thousands, except per share amounts)

Basic and diluted earnings per share:

Net income (loss)

$

2,268

(1,623)

Weighted average shares of Class A outstanding - basic

50,308

49,908

Weighted average shares of Class A outstanding - diluted(1)

51,580

50,912

Basic earnings (loss) per share of Class A common stock

$

0.05

(0.03)

Diluted earnings (loss) per share of Class A common stock

0.04

(0.03)

(1) Because the Company reported a net loss for the three months ended March 31, 2025, the effect of all potentially dilutive securities was excluded from the calculation of diluted earnings per share as it would be anti-dilutive.

Each of our domestic regulated insurance subsidiaries is required to meet stipulated regulatory capital requirements imposed by the U.S. National Association of Insurance Commissioners ("NAIC"). All domestic insurance subsidiaries exceeded the minimum capital requirements at March 31, 2026. On March 27, 2024, Citizens and the Colorado Division of Insurance entered into a capital maintenance agreement that specifies that Citizens will infuse capital as needed to ensure that CLOA's RBC remains above 350%. As CLOA's RBC exceeded 350% at March 31, 2026, no capital contribution was necessary.

CICA International is a Puerto Rico domiciled company. The Insurance Code of Puerto Rico does not specifically set forth minimum capital and surplus standards but rather requires that an insurer submit a business plan for approval to the Office of the Commissioner of Insurance ("OIC") that includes proposed minimum capital and surplus. CICA International is required to maintain a minimum of $750,000 in capital and maintain a premium to surplus ratio of 7 to 1. At March 31, 2026, CICA International's capital exceeds both the required minimum capital and related ratio.

(10) SEGMENT AND OTHER OPERATING INFORMATION

The Company's segments are defined by management's reporting structure and operating activities. The chief operating decision maker ("CODM"), our President and Chief Executive Officer, reviews and analyzes income statement information by segment to make decisions, assess financial performance and allocate resources across the Company in order to meet the overall strategic objectives of the Company. The Company has two reportable segments: International Insurance and Domestic Insurance.

Our International Insurance segment issues endowment contracts, which are principally accumulation contracts that incorporate an element of life insurance protection, and whole life insurance to non-U.S. residents through CICA International. These contracts are designed to provide a fixed amount of insurance coverage over the life of the insured and may utilize rider benefits to provide additional coverage and annuity benefits to enhance accumulations.

Our Domestic Insurance segment operates through our subsidiaries: CLOA, which issues whole life, final expense and life products with living benefits throughout the U.S.; and SPLIC and MGLIC, which focus on the life insurance needs of the lower-income markets, primarily in Louisiana, Mississippi, and Arkansas. SPLIC also issues critical illness policies. Our policies are sold and serviced through independent agents.

The International Insurance and Domestic Insurance portions of the Company constitute separate businesses. In addition to the International Insurance and Domestic Insurance business, the Company also operates other non-insurance portions of the Company ("Other Non-Insurance Enterprises"), which primarily include the Company’s IT and corporate-support functions.

The accounting policies of the reportable segments and Other Non-Insurance Enterprises are presented in accordance with U.S. GAAP and are the same as those described in the summary of significant accounting policies in our 2025 Form 10-K. The CODM evaluates profit and loss performance based on U.S. GAAP income (loss) before federal income tax for its two reportable segments. The Company's Other Non-Insurance Enterprises represents the only reportable difference between segments and consolidated operations.

Increase (decrease) in future policy benefit reserves

(6,856)

3,210

—

(3,646)

Policyholder liability remeasurement (gain) loss

93

(265)

—

(172)

Policyholders' dividends

1,185

110

—

1,295

Total insurance benefits paid or provided

27,456

10,119

—

37,575

Commissions

5,103

6,172

—

11,275

Other general expenses

5,295

5,060

2,338

12,693

Capitalization of deferred policy acquisition costs

(4,787)

(4,062)

—

(8,849)

Amortization of deferred policy acquisition costs

3,466

1,181

—

4,647

Amortization of cost of insurance acquired

—

98

—

98

Total benefits and expenses

36,533

18,568

2,338

57,439

Income (loss) before federal income tax

$

(195)

558

(2,150)

(1,787)

The Company categorizes premiums in two categories - first year premiums are premiums received within the first 12 months of a policy's issuance and any premiums received thereafter are renewal premiums. A summary of the premiums for the International Insurance segment is detailed below.

A summary of the Domestic Insurance segment premium breakout is detailed below.

(In thousands)

Three Months Ended March 31,

2026

2025

Direct premiums:

First year

$

5,680

5,425

Renewal

12,670

10,846

Total direct premiums

18,350

16,271

Reinsurance

(3,610)

(2,082)

Total premiums

$

14,740

14,189

The table below summarizes assets by segment.

(In thousands)

March 31, 2026

December 31, 2025

Assets:

Segments:

International Insurance

$

1,178,768

1,190,736

Domestic Insurance

529,478

529,357

Total Segments

1,708,246

1,720,093

Other Non-Insurance Enterprises

31,254

34,667

Total assets

$

1,739,500

1,754,760

GEOGRAPHIC INFORMATION

The following table sets forth the Company's annual total of earned premiums by country of policyholder residence for the periods indicated.

Three Months Ended March 31,

(In thousands)

2026

2025

Area:

United States

$

18,521

16,500

Colombia

6,825

6,554

Taiwan

3,406

3,886

Venezuela

3,178

3,350

Ecuador

2,996

3,200

Argentina

2,602

2,096

Other foreign countries

9,125

9,702

Reinsurance and change in premium accruals

(6,715)

(5,491)

Total premiums

$

39,938

39,797

(11) INCOME TAXES

The effective tax rate is the ratio of tax expense or tax benefit over pre-tax income. The tax effective rate was 4.5% for the three months ended March 31, 2026, compared to an effective tax benefit rate of 9.2% for the same period in

2025. CICA International is considered a controlled foreign corporation for federal income tax purposes. As a result, the insurance activity of CICA International is subject to Subpart F of the Internal Revenue Code and is included in Citizens’ taxable income. The Government of Puerto Rico approved a tax exemption decree for CICA International which freezes the income tax rate at 0% on taxable earnings up to $1.2 million and 4% on taxable earnings in excess of $1.2 million for a minimum of 15 years. The effective tax rate varies from the prevailing corporate federal income tax rate of 21% mainly due to the impact of Subpart F and the reduced Puerto Rico income tax rate.

At March 31, 2026 and 2025, we determined it was more likely than not that a portion of our capital deferred tax assets would not be realized in their entirety. The Company recorded valuation allowances of $4.7 million at March 31, 2026 and 2025, in accumulated other comprehensive income (loss) on the consolidated balance sheets.

(12) OTHER COMPREHENSIVE INCOME (LOSS)

The changes in the components of other comprehensive income (loss) are reported net of the effects of income taxes of 21% for domestic entities and 4% for Puerto Rican entities for the three months ended March 31, 2026 and 2025. The following table provides a rollforward of accumulated other comprehensive income (loss) for the periods indicated below.

(In thousands)

Unrealized Gains and Losses on Available for Sale Securities

Discount Rate for Liability for Future Policy Benefits

Other Comprehensive Income (Loss)

Balance at December 31, 2025, net of tax

$

(136,344)

47,923

(88,421)

Other comprehensive income (loss) before reclassification, before tax

(16,295)

17,135

840

Amounts reclassified from other comprehensive income (loss), before tax

412

—

412

Income tax benefit (expense)

1,191

(1,505)

(314)

Balance at March 31, 2026, net of tax

$

(151,036)

63,553

(87,483)

Balance at December 31, 2024, net of tax

$

(169,599)

73,634

(95,965)

Other comprehensive income (loss) before reclassification, before tax

18,334

(8,589)

9,745

Amounts reclassified from other comprehensive income (loss), before tax

83

—

83

Income tax benefit (expense)

(1,379)

442

(937)

Balance at March 31, 2025, net of tax

$

(152,561)

65,487

(87,074)

(13) RELATED PARTY TRANSACTIONS

The Company has various routine related party transactions in conjunction with our holding company structure, such as management service agreements related to costs incurred, a tax sharing agreement between entities, and inter-company dividends and capital contributions. There were no changes related to these relationships during the three months ended March 31, 2026. See our 2025 Form 10-K for a comprehensive discussion of related party transactions.

(14) SUBSEQUENT EVENTS

The Company has evaluated the impact of subsequent events as defined by the accounting guidance through the date this report was issued and determined that no other significant subsequent events need to be recognized or disclosed at this time.

Item 2. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

FORWARD-LOOKING STATEMENTS

This section and other parts of this Quarterly Report on Form 10-Q ("Form 10-Q") contain forward-looking statements, within the meaning of the Private Securities Litigation Reform Act of 1995, that involve risks and uncertainties. Forward-looking statements provide current expectations of future events based on certain assumptions and include any statement that does not directly relate to any historical or current fact. Forward-looking statements can also be identified by words such as “future,” “anticipates,” “believes,” “estimates,” “expects,” “intends,” “plans,” “predicts,” “will,” “would,” “could,” “can,” “may,” and similar terms. Forward-looking statements are not guarantees of future performance and the Company’s actual results may differ significantly from the results discussed in the forward-looking statements. These forward-looking statements are subject to a number of risks, uncertainties and assumptions including those factors discussed in the "Risk Factors" contained in our Annual Report on Form 10-K for the year ended December 31, 2025, which is incorporated herein by reference.

The following discussion should be read in conjunction with the consolidated financial statements and accompanying notes included in Part I, Item 1 of this Form 10-Q, as well as in conjunction with MD&A and the consolidated financial statements and notes thereto that are included in our Form 10-K. The Company assumes no obligation to revise or update any forward-looking statements for any reason, except as required by law.

The U.S. Securities and Exchange Commission ("SEC") maintains a website at www.sec.gov that contains reports, proxy statements, and other information regarding issuers, including the Company, that file electronically with the SEC. Our own website, www.citizensinc.com, provides free access to the Company's Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, Section 16 filings made by our executive officers and directors, and any amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934. These materials are made available on our website as soon as reasonably practicable after we file them with, or furnish them to, the SEC. Information contained on, or accessible through, our website is not incorporating by reference into, and should not be considered part of, this Form 10-Q.

OBJECTIVE OF OUR MANAGEMENT'S DISCUSSION AND ANALYSIS

We refer to our Management’s Discussion and Analysis of Financial Condition and Results of Operations as our “MD&A”. The objective of our MD&A is to provide investors with information in order to assess the material changes in our financial condition from December 31, 2025 to March 31, 2026 and the material changes in our results of operations for the three months ended March 31, 2026 as compared to the same period in 2025. We also discuss in the MD&A any trends that we believe may materially affect our future operations or financial condition.

OVERVIEW

For over 55 years, Citizens has been fulfilling the needs of our policyholders and their families by providing insurance products that offer both living and death benefits. We conduct insurance related operations through our insurance subsidiaries, which provide benefits to policyholders globally. We specialize in offering primarily individual whole life insurance, endowment products and final expense insurance in niche markets where we believe we can optimize our competitive position.

As an insurance provider, we collect premiums on an ongoing basis from our policyholders and invest the majority of the premiums to pay future benefits, including claims, surrenders and policyholder dividends. Accordingly, the Company derives its revenues principally from: (1) life insurance premiums earned for insurance coverages provided to insureds in our two operating segments – International Insurance and Domestic Insurance; and (2) net investment income. In addition to reserving for and paying insurance benefits to our policyholders, our expenses consist primarily of the costs of selling our insurance products (e.g., commissions, underwriting, marketing expenses), operating expenses and income taxes.

We operate in two segments - International Insurance and Domestic Insurance. Our International Insurance segment operates through CICA Life, A.I., a Puerto Rican insurer, referred to as "CICA International". Our Domestic

Insurance segment operates through our subsidiaries CICA Life Insurance Company of America ("CLOA"), Security Plan Life Insurance Company ("SPLIC") and Magnolia Guaranty Life Insurance Company ("MGLIC").

EVENTS THAT IMPACTED OUR BUSINESS

From time-to-time, certain events may affect our business in ways that cause current or future results to differ from past results. See (1) the factors described in Part 1. Item 1A. Risk Factors in our Annual Report on Form 10-K for the period ended December 31, 2025 ("2025 Form 10-K"); and (2) the events described in Part 1. Item 7. "Management's Discussion and Analysis of Financial Condition and Results of Operations - Events that Impacted Our Business" in the 2025 Form 10-K.

FINANCIAL HIGHLIGHTS

Summary

Income before federal income tax increased by $4.2 million in the three months ended March 31, 2026 compared to the same period in 2025, to $2.4 million from a loss of $1.8 million, respectively. The primary factor that drove this was a $3.9 million increase in investment related gains and losses, reflecting the absence of the BlackRock write-down recorded in the prior year period.

Financial Condition at March 31, 2026

•Total assets of $1.7 billion

•Total direct insurance in force of $5.5 billion

•Total investments of $1.4 billion; fixed maturity securities comprised 89% of total investments

•No debt

•Book value per share of Class A common stock of $4.74

•Adjusted book value per share of Class A common stock of $6.481

•Diluted earnings per share of Class A common stock for the three months ended of $0.04

The Factors that Drive our Operating Results

We see the following as the primary factors that drive our operating results.

•Sales of our products and the premiums we receive from these sales

•Investments and the income that they generate

•Claims and surrenders

•Operating expenses

•Actuarial assumptions

Sales of our Products. We believe sales statistics are meaningful to gain an understanding of, among other things, the attractiveness of our products, how expansion of our distribution channels affects our revenue, customer retention and the performance of our business from period-to-period. Throughout the MD&A, we describe the actions and initiatives we are taking to increase sales and improve retention, sales performance in each period and as compared to prior year period, and how we view trends with respect to sales and retention.

One sales factor that is key to our profitability is product mix. We offer a competitive product mix designed to meet the needs of our specific customer demographics and actively manage new product margins and in-force profitability. Product mix can have an impact on profitability; when we sell a higher volume of lower-margin products, we may receive more premiums but may not be as profitable as in periods when we sell a greater percentage of higher-margin products. Our product mix has been trending towards sales of our newer whole life products, which have a smaller margin than sales of our international endowment products. We expect this trend in our International

1 Adjusted book value per of Class A common share is a non-GAAP measure that is calculated by dividing actual Class A common stockholders’ equity, excluding AOCI, by the number of Class A common shares outstanding at the end of the period.

Insurance segment to continue due to the anticipated volumes of endowment maturities being replaced by higher volumes of whole life products.

Premium Revenues. Premium revenues consist of all money deposited by customers into new and existing insurance policies. We view these premiums in two categories - first year premiums are premiums received within the first 12 months of a policy's issuance and any premiums received thereafter are renewal premiums.

Throughout the MD&A, we refer to "direct" premiums as all premiums received and "net" or "total" premiums as all premiums received less premiums ceded to our reinsurers. Direct premium revenue increased 4% in the three months ended March 31, 2026 to $43.9 million from $42.4 million in the three months ended March 31, 2025. This increase was driven by sales and renewal premiums in our Domestic Insurance segment.

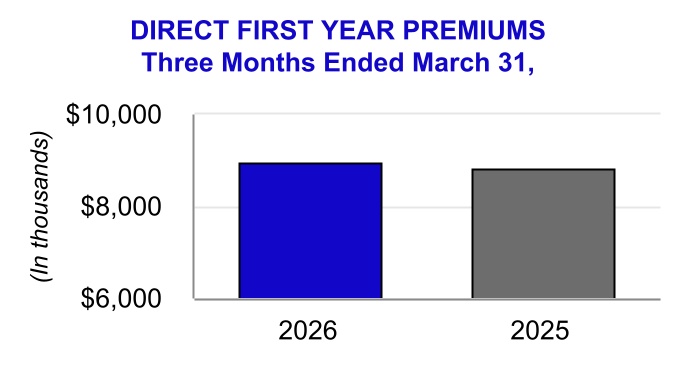

First Year Premiums. Direct first year premiums increased 2% in the three months ended March 31, 2026 to $9.0 million from $8.8 million in the three months ended March 31, 2025, driven by sales in our Domestic Insurance segment and an increased number of producing agents. First year premium growth primarily resulted from our CLOA final expense business.

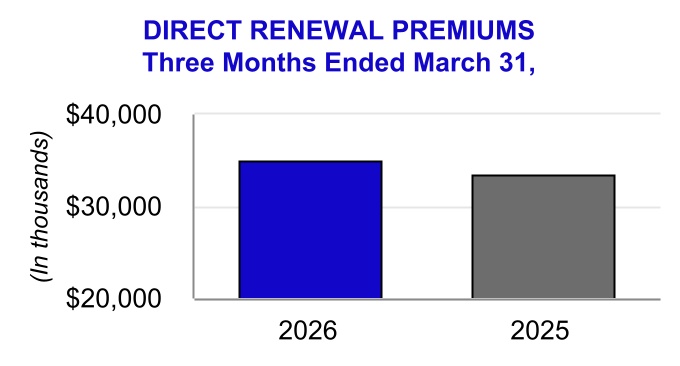

Renewal Premiums. Our direct renewal premiums in the three months ended March 31, 2026 increased primarily due to strong sales in 2025 in our Domestic Insurance segment, leading to higher number of policies paying renewal premiums in the current period. Premium growth was constrained by the high level of surrenders and matured endowments in our International Insurance segment during the last few years, which has lowered the number of policies remaining in force and paying renewal premiums in this segment.

Investment Income. Our net investment income decreased for the three months ended March 31, 2026 compared to the same prior year period. Total investment income increased for the three months ended March 31, 2026 compared to the same prior year period as we began investing in investment grade private placement credit, where we expect higher returns. This increase was outweighed by non-recurring fund fees due to the underperformance of the BlackRock middle market limited partnership. Excluding one time and unanticipated events, we expect our

net investment income to increase, as we have begun investing in investment grade private placement credit, where we expect higher returns.

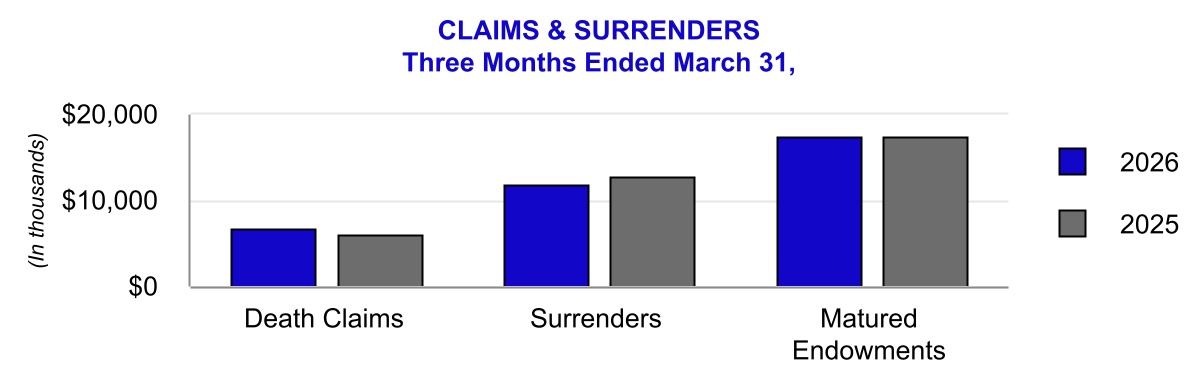

Claims and Surrenders.Payment of policyholder benefits for claims and surrenders is our largest expense and thus key to our profitability. The three largest components of this expense are reflected in the graph below.

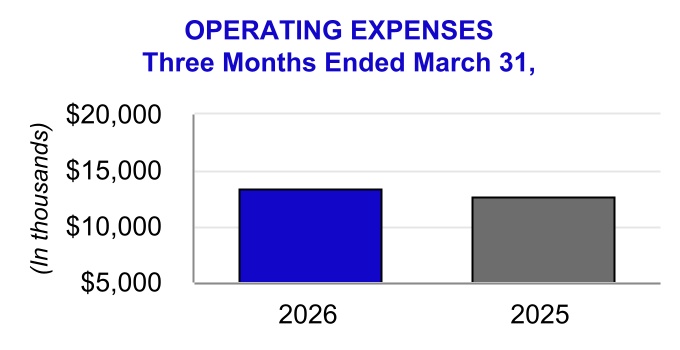

Operating Expenses. Operating expenses are our second largest expense and thus also drive our operating results. These operating expenses are meaningful to gain an understanding of how we manage our business, including among other things, salaries, benefits, and spending on growth initiatives. Our operating expenses increased by $0.7 million in the three months ended March 31, 2026, as compared to the prior year period due to continued investment in supporting the growth of our business.

Actuarial Assumptions. The actuarial assumptions that underlie our reserves are based upon our best estimates of certain factors such as mortality, lapses, morbidity and discount rates. Our results will be affected to the extent there is a variance between our actuarial assumptions and actual experience. This is reflected in our Consolidated Statements of Operations and Comprehensive Income as increase (decrease) in future policy benefit reserves and policyholder liability remeasurement (gain) loss.

Recently, we have experienced a rebalancing in our business mix due to the volume of maturities in our international endowment business and continued growth in the Domestic Insurance segment. Our current profitability is affected by how closely actual experience matches our actuarial assumptions for these shifts, and by the amount of reserves we must hold. Updated assumptions to policyholder liability remeasurement (gain) loss negatively affected our operating results by $1.0 million compared to the same prior year quarter due to unfavorable experience in our International Insurance segment. Actuarial assumptions are continually monitored and updated at least annually to reflect overall experience as well as emerging trends.

INSURANCE ISSUED AND INFORCE

The amount of direct insurance, number of policies, and average face amounts for life policies issued during the periods indicated are shown below.

Three Months Ended March 31,

2026

2025

Amount of Insurance Issued

Number of Policies Issued

Average Policy Face Amount Issued

Amount of Insurance Issued

Number of Policies Issued

Average Policy Face Amount Issued

International

$

88,357,208

870

$

101,560

$

106,875,869

942

$

113,456

Domestic

147,347,717

17,017

8,659

148,285,315

14,819

10,006

Total

$

235,704,925

17,887

$

255,161,184

15,761

In the first three months of 2026, we issued $235.7 million in new direct insurance.

The number of insurance policies issued, average policy face amount and total insurance issued in our International Insurance segment decreased in the three months ended March 31, 2026 as compared to the prior year period due to lower volume and product mix. During the first three months of 2026, a larger proportion of our sales was comprised of our single premium product aimed at replacing maturing endowments, which has a $100,000 maximum face value, as well as other endowment products. Our endowment products generally have lower policy face amounts than our whole life product.

In our Domestic Insurance segment, we continue to experience strong sales and increased number of policies issued of our final expense products. The use of information to enhance underwriting decisions with additional medical and lab data from third parties is resulting in issuance of policies with lower face amounts, as expected. We also believe this segment is being impacted by inflation on the cost of living, which has affected new sales since the customer demographic is primarily lower-income individuals.

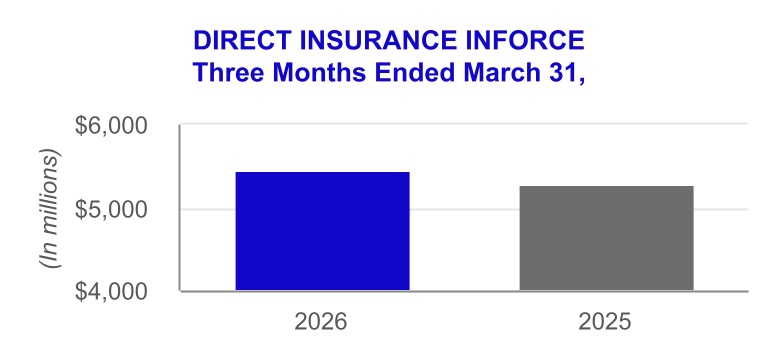

The amount of direct insurance inforce for the periods indicated is shown below.

Overall insurance inforce has grown due to the issuance of new business, but growth has been and will be impacted by persistency rates, policy maturities and surrenders.

Our revenues are generated primarily by life insurance premiums and investment income from invested assets.

Three Months Ended

March 31,

(In thousands)

2026

2025

Revenues:

Premiums

$

39,938

39,797

Net investment income

17,304

17,377

Investment related gains (losses), net

984

(2,894)

Other income

1,494

1,372

Total revenues

$

59,720

55,652

Three Months Ended

March 31,

(In thousands)

2026

2025

Direct premiums:

First year

$

8,970

8,817

Renewal

34,962

33,533

Total direct premiums

43,932

42,350

Reinsurance

(3,994)

(2,553)

Total premiums

$

39,938

39,797

Our first year direct premiums increased 2% in the three months ended March 31, 2026 compared to the same period in 2025, due to sales and expanded distribution in our Domestic Insurance segment. Renewal premiums also increased from strong first year sales in 2025 in our Domestic Insurance segment, leading to higher number of policies paying renewal premiums in the current period, which more than offset the impact from the high level of surrenders during the last few years and increasing matured endowment benefits paid in our International Insurance segment which has lowered the number of policies paying renewal premiums in this segment.

Reinsurance premiums ceded increased in the three months ended March 31, 2026 compared to the same period in 2025. We have a coinsurance agreement with RGA Reinsurance Company ("RGA") in order to provide more capacity for growth in our Domestic Insurance segment. Since we cede 50% of the direct premiums we receive for our CLOA final expense products to RGA, as sales of these products increase, reinsurance ceded to RGA also increases.

Net Investment Income. Asummary of our net investment income performance is as follows:

Three Months Ended

March 31,

(In thousands, except for %)

2026

2025

Gross investment income:

Fixed maturity securities

$

16,358

15,428

Equity securities

11

75

Policy loans

1,267

1,369

Other long-term investments

821

1,164

Total investment income

18,457

18,036

Investment expenses

(1,153)

(659)

Net investment income

$

17,304

17,377

Net investment income, annualized

$

70,445

69,508

Average invested assets, at amortized cost

$

1,552,656

1,537,288

Annualized yield on average invested assets

4.54

%

4.52

%

Fixed maturity securities constitute the vast majority, or 89%, of our investment portfolio based on fair value and thus provide the majority of our net investment income. Our fixed maturity investment portfolio, primarily invested in callable securities, has faced challenges due to the sustained low interest rate environment for the 10 years prior to 2021. Many securities were called between 2019 and 2021, which required us to reinvest in lower interest rate fixed maturity assets, which impacts net investment income and yields. In order to enhance yields, we are investing in new opportunities, including investment grade private placement fixed income securities and other asset classes, while maintaining a prudent risk profile. As discussed above, net investment income is down slightly for the three months ended March 31, 2026 as a result of higher investment expenses when compared to prior year quarter.

Investment Related Gains (Losses), Net. We recorded investment related gains of $1.0 million during the three months ended March 31, 2026 compared to investment related losses of $2.9 million during the same prior year period. The losses in the prior year period are primarily related to the non-cash write-down of our BlackRock investment. We did not sell this investment; however, the changes in fair values of our equity securities are reflected as investment related gains or losses in our Consolidated Statements of Operations and Comprehensive Income, in addition to executed transactions that result in a gain or loss.

Other Income. Other income consists primarily of supplemental contracts issued to policyholders in our International Insurance segment upon the surrender or maturity of their original policies. Supplemental contracts offer our policyholders the opportunity to leave their cash with us and be paid interest at a guaranteed rate or receive an annuity, at their option.

Increase (decrease) in future policy benefit reserves

(4,703)

(3,646)

Policyholder liability remeasurement (gain) loss

875

(172)

Policyholders' dividends

1,102

1,295

Total insurance benefits paid or provided

36,927

37,575

Commissions

10,824

11,275

Other general expenses

13,372

12,693

Capitalization of deferred policy acquisition costs

(8,944)

(8,849)

Amortization of deferred policy acquisition costs

4,979

4,647

Amortization of cost of insurance acquired

188

98

Total benefits and expenses

$

57,346

57,439

Payments of claims and surrenders benefits constitute the vast majority of our expenses.

Claims and Surrenders.

Three Months Ended

March 31,

(In thousands)

2026

2025

Claims and surrenders:

Death claim benefits

$

6,669

6,067

Surrender benefits

11,859

12,901

Endowment benefits

1,448

1,679

Matured endowment benefits

17,448

17,351

A&H and other policy benefits

2,229

2,100

Total claims and surrenders

$

39,653

40,098

Death claim benefits increased in the three months ended March 31, 2026 compared to the same period in 2025 due to a higher volume of claims. While we maintain diligent oversight of claims activities, we expect a rise in line with the expansion of our business. Many of these death claims are expected to be partially offset by our reinsurance coverage.

The vast majority of our surrender benefits payments are made on policies surrendered in our International Insurance segment. These policies are generally policies that have been in place for many years, built up cash values, and have little or no surrender charges remaining. Surrender benefits decreased 8% in the three months ended March 31, 2026 compared to the prior year period and can vary from one period to another. We continue to focus efforts on retention initiatives.

Many of our endowment policies are reaching their contractual maturity dates and thus matured endowment benefits increased slightly in the three months ended March 31, 2026 compared to the prior year period. Compared to peak endowment activity in 2025, we expect maturity benefits to decrease throughout 2026.

Increase (Decrease) in Future Policy Benefit Reserves. Future policy benefit reserves reflect the liability established to provide for the future payment of policy benefits and thus they generally increase when we have a larger in force block of business due to higher sales and persistency (i.e., more policies on which we expect to pay future benefits) and decrease when we have lower sales and persistency. In the three months ended March 31, 2026, the change in future policy benefit reserves decreased compared to the prior year period despite the increase in our inforce business, driven by reserves released in connection with policyholder benefits payouts.

Policyholder Liability Remeasurement (Gain) Loss. Most of our products are long-duration contracts that provide a specified, fixed amount of insurance benefit in exchange for a fixed premium. When a policy is initially issued, we establish a "net premium ratio" ("NPR") using assumptions regarding expected premiums and policyholder benefit liabilities. On a quarterly basis, we review actual versus expected experience in such quarter, which is reported as a policyholder liability remeasurement gain (if better performance than assumptions) or loss (if lower performance than assumptions). Additionally, the best estimate assumptions are updated every year in our third quarter and are reflected on our income statement as a policyholder liability remeasurement gain or loss. In the three months ended March 31, 2026, the remeasurement (gain) loss was negatively affected by unfavorable experience in our International Insurance segment.

Commissions. Commission expenses are a cost of acquiring business, as commissions are the primary compensation paid to our independent agents for selling our products. First year commission rates are higher than renewal commission rates and thus commissions fluctuate directly in relation to first year sales. Although first year sales increased in the three months ended March 31, 2026 as compared to the same period in 2025, commissions decreased in the three months ended March 31, 2026 due to more sales of our single premium product offered to policyholders with maturing endowments in the International Insurance segment, which has a lower commission rate than other products.