.2 Dana to Combine with Eaton’s Mobility Group June 11, 2026 1 1

Disclaimers Cautionary Notes on Forward-Looking Statements This document is not a substitute for the Form 10, Form S-1/S-4, Schedule TO, Form S-4, prospectus/offer to exchange, proxy statement/prospectus or any other document that Eaton, SpinCo or Dana may file with the SEC. INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE REGISTRATION STATEMENTS, THE SCHEDULE TO; THE PROSPECTUS/OFFER TO EXCHANGE, THE PROXY STATEMENT/PROSPECTUS AND ANY OTHER This communication includes “forward-looking statements” within the meaning of the federal securities laws, including Section 27A of the Securities Act of RELEVANT DOCUMENTS THAT MAY BE FILED WITH THE SEC, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THESE 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended by the Private Securities Litigation Reform Act of DOCUMENTS, CAREFULLY AND IN THEIR ENTIRETY IF AND WHEN THEY BECOME AVAILABLE BECAUSE THEY CONTAIN OR WILL 1995, including statements regarding the proposed transaction between Eaton Corporation plc (“Eaton”), Dana Incorporated (“Dana”) and Mobility (USA) CONTAIN IMPORTANT INFORMATION ABOUT EATON, DANA, SPINCO AND THE PROPOSED TRANSACTION. Investors and security holders will Corporation (“SpinCo”). These forward-looking statements generally are identified by the words “believe,” “project,” “expect,” “anticipate,” “estimate,” be able to obtain free copies of the Form 10, Form S-1/S-4, Schedule TO, Form S-4, the prospectus/offer to exchange and the proxy statement/prospectus (if and “forecast,” “outlook,” “target,” “endeavor,” “seek,” “predict,” “intend,” “strategy,” “plan,” “may,” “could,” “should,” “will,” “would,” or the negative thereof or when available) and other documents containing important information about Eaton, Dana and SpinCo and the proposed transaction, once such documents are variations thereon or similar terminology generally intended to identify forward-looking statements. All statements, other than historical facts, including, but not filed with the SEC through the website maintained by the SEC at http://www.sec.gov. Copies of the documents filed with, or furnished to, the SEC by Eaton and limited to, statements regarding the expected timing and structure of the proposed transaction and financing of the transaction, the ability of the parties to SpinCo will be available free of charge on Eaton’s website at https://www.eaton.com/us/en-us/company/investor-relations.html. Copies of the documents filed complete the proposed transaction, the expected benefits of the proposed transaction, including future financial and operating results and strategic and synergistic with, or furnished to, the SEC by Dana will be available free of charge on Dana’s website at https://danaincorporated.gcs-web.com/. The information included benefits, the tax consequences of the proposed transaction, and the combined company’s plans, objectives, expectations and intentions, legal, economic and on, or accessible through, Eaton or Dana’s website is not incorporated by reference into this communication. regulatory conditions, and any assumptions underlying any of the foregoing, are forward looking statements. Participants in the Solicitation These forward-looking statements are based on Eaton and Dana’s current expectations and are subject to risks and uncertainties. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those indicated or anticipated by such forward-looking statements. The inclusion of such statements should not be regarded as a representation that such plans, estimates or expectations will be Eaton, Dana, SpinCo and certain of their respective directors and executive officers may be deemed to be participants in the solicitation of proxies in respect of achieved. Important factors that could cause actual results to differ materially from such plans, estimates or expectations include, among others, the ability to the proposed transaction. Information about the directors and executive officers of Eaton, including a description of their direct or indirect interests, by security complete the proposed transaction on the timeframe or on the terms currently anticipated or at all, including due to a failure to obtain requisite stockholder and/or holdings or otherwise, is set forth in Eaton’s proxy statement for its 2026 Annual General Meeting of Shareholders, which was filed with the SEC on March 13, regulatory approvals; risks related to difficulties, inabilities or delays in integrating the businesses of Dana and SpinCo; the ability to realize the anticipated 2026. Information about the directors and executive officers of Dana, including a description of their direct or indirect interests, by security holdings or benefits of the proposed transaction, including estimated combined EBITDA, estimated combined revenue and estimated run-rate cost synergies; potential impact otherwise, is set forth in Dana’s proxy statement for its 2026 Annual Meeting of Stockholders, which was filed with the SEC on March 13, 2026. Other of the announcement or consummation of the proposed transaction on Eaton and Dana’s stock prices; restrictions on the conduct of Eaton and Dana’s respective information regarding the participants in the proxy solicitation and a description of their direct and indirect interests, by security holdings or otherwise, will be businesses prior to closing and on each of their ability to pursue alternatives to the proposed transaction; the possibility that the proposed transaction may be contained in the Form S-4 and the proxy statement/prospectus and other relevant materials to be filed with the SEC regarding the proposed transaction when such more expensive to complete than anticipated, including as a result of unexpected factors or events, or unforeseen or unknown liabilities; the ability of the materials become available. Investors should read the Form 10, Form S-1/S-4, Schedule TO, Form S-4, the prospectus/offer to exchange and the proxy combined company to implement its business strategy; the inability of the combined company to retain and hire key personnel; the occurrence of any event that statement/prospectus carefully if and when available before making any voting or investment decisions. You may obtain free copies of these documents from could give rise to termination of the proposed transaction; the risk that stockholder litigation in connection with the proposed transaction or other litigation, Eaton or Dana using the sources indicated above. settlements or investigations may affect the timing or occurrence of the proposed transaction or result in significant costs of defense, indemnification and liability; risks relating to the ability to obtain financing for the transaction upon acceptable terms or at all; evolving legal, regulatory and tax regimes; changes in No Offer or Solicitation general economic and/or industry specific conditions; global economic repercussions related to U.S. and global inflationary pressures and potential recessionary concerns; the risks that the anticipated tax treatment of the proposed transaction is not obtained; the risk of greater than expected difficulty in separating the This communication is not intended to and shall not constitute an offer to sell or the solicitation of an offer to sell or the solicitation of an offer to buy or business of SpinCo from the other businesses of Eaton; risks related to the disruption of management time from ongoing business operations due to the pendency exchange any securities, or a solicitation of any vote or approval, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation, sale of the proposed transaction, or other effects of the pendency of the proposed transaction on the relationship of any of the parties to the transaction with their or exchange would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offer of securities shall be made except employees, customers, suppliers, or other counterparties; and other risk factors detailed from time to time in Eaton and Dana’s reports filed with the Securities by means of a prospectus meeting the requirements of Section 10 of the Securities Act or in a transaction exempt from the registration requirements of the and Exchange Commission (the “SEC”), including Eaton and Dana’s annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K Securities Act. and other documents filed with the SEC, including documents that will be filed with the SEC in connection with the proposed transaction. The foregoing list of important factors is not exclusive. Note Regarding Use of Non-GAAP Financial Measures Any forward-looking statements speak only as of the date of this communication. None of Eaton, Dana or SpinCo undertakes, and each party expressly In addition to the financial measures presented in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”), this communication includes disclaims, any obligation to update any forward-looking statements, whether as a result of new information or development, future events or otherwise, except as certain non-GAAP financial measures (collectively, the “Non-GAAP Measures”), such as adjusted EBITDA, and adjusted EBITDA margin, and adjusted free required by law. Readers are cautioned not to place undue reliance on any of these forward-looking statements. cash flow margin. These Non-GAAP Measures should not be used in isolation or as a substitute or alternative to results determined in accordance with U.S. GAAP. In addition, Dana’s and Eaton’s definitions of these Non-GAAP Measures may not be comparable to similarly titled non-GAAP financial measures It should also be noted that projected financial information for the combined company is based on management’s estimates, assumptions and projections and has reported by other companies. A reconciliation of these Non-GAAP Measures to the most directly comparable financial measures calculated and reported in not been prepared in conformance with the applicable accounting requirements of Regulation S-X relating to pro forma financial information, and the required accordance with U.S. GAAP can be found in Dana’s filings with the SEC except for financial guidance and other forward-looking information since such a pro forma adjustments have not been applied and are not reflected therein. None of this information should be considered in isolation from, or as a substitute for, reconciliation is not practicable without unreasonable effort as Dana is unable to reasonably forecast certain amounts that are necessary for such reconciliation. the historical financial statements of Dana or SpinCo. Important Information About the Transaction and Where to Find It In connection with the proposed transaction, SpinCo may file with the SEC an information statement on Form 10 (“Form 10”) or a registration statement on Form S-1/S-4 (the “Form S-1/S-4”) that constitutes a prospectus with respect to the shares of common stock, par value $0.01 per share, of SpinCo (the “SpinCo shares”) to be issued to Eaton shareholders in the proposed exchange offer (the “prospectus/offer to exchange”). Eaton may also file with the SEC a tender offer statement (the “Schedule TO”) with respect to the offer by Eaton to exchange all SpinCo shares for ordinary shares, par value $0.01 per share, of Eaton that are 2 validly tendered and not properly withdrawn prior to the expiration of the exchange offer (if any). In addition, SpinCo intends to file with the SEC a registration statement on Form S-4 (the “Form S-4”) that will include a proxy statement of Dana and that also constitutes a prospectus of SpinCo with respect to the SpinCo shares to be issued in the proposed merger (the “proxy statement/prospectus”). Each of Eaton, SpinCo and Dana may also file other relevant documents with the SEC regarding the proposed transaction.

Today’s Presenters Bruce McDonald Byron Foster Timothy Kraus Chairman and Incoming Chief Financial Officer Chief Executive Officer Chief Executive Officer 3

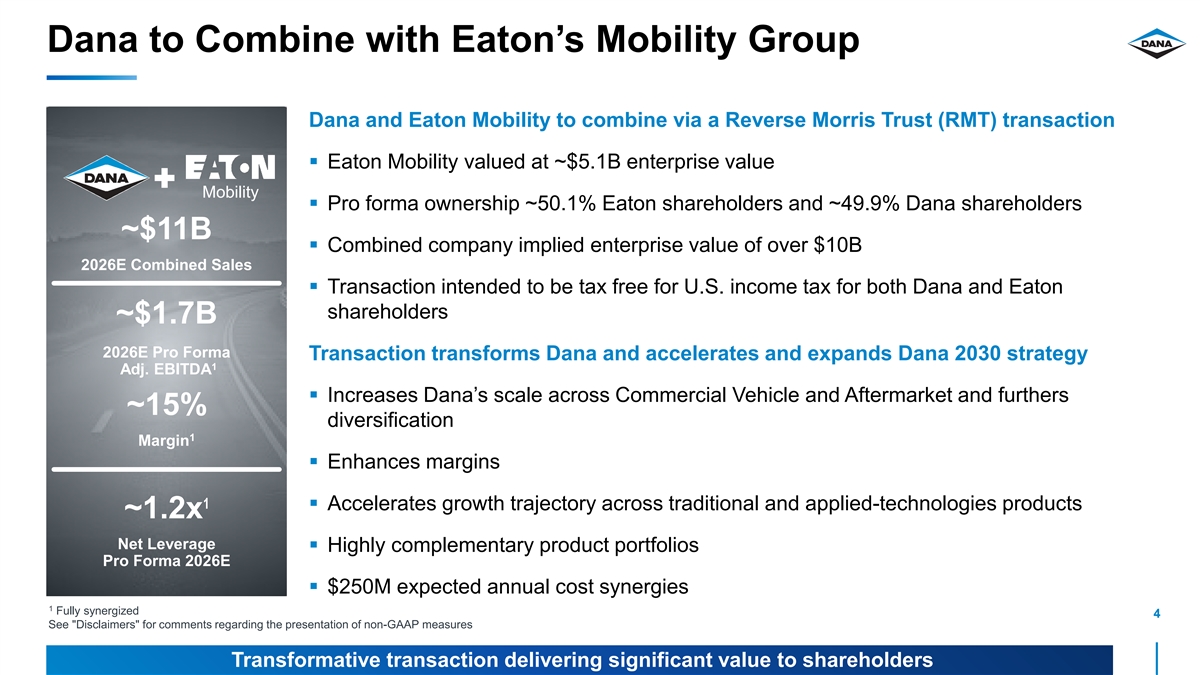

Dana to Combine with Eaton’s Mobility Group Dana and Eaton Mobility to combine via a Reverse Morris Trust (RMT) transaction § Eaton Mobility valued at ~$5.1B enterprise value Mobility § Pro forma ownership ~50.1% Eaton shareholders and ~49.9% Dana shareholders ~$11B § Combined company implied enterprise value of over $10B 2026E Combined Sales § Transaction intended to be tax free for U.S. income tax for both Dana and Eaton shareholders ~$1.7B 2026E Pro Forma Transaction transforms Dana and accelerates and expands Dana 2030 strategy 1 Adj. EBITDA § Increases Dana’s scale across Commercial Vehicle and Aftermarket and furthers ~15% diversification 1 Margin § Enhances margins § Accelerates growth trajectory across traditional and applied-technologies products ~1.2x Net Leverage § Highly complementary product portfolios Pro Forma 2026E § $250M expected annual cost synergies 1 Fully synergized 4 4 See Disclaimers for comments regarding the presentation of non-GAAP measures Values are representative of 100% numbers for the JV. Transformative transaction delivering significant value to shareholders

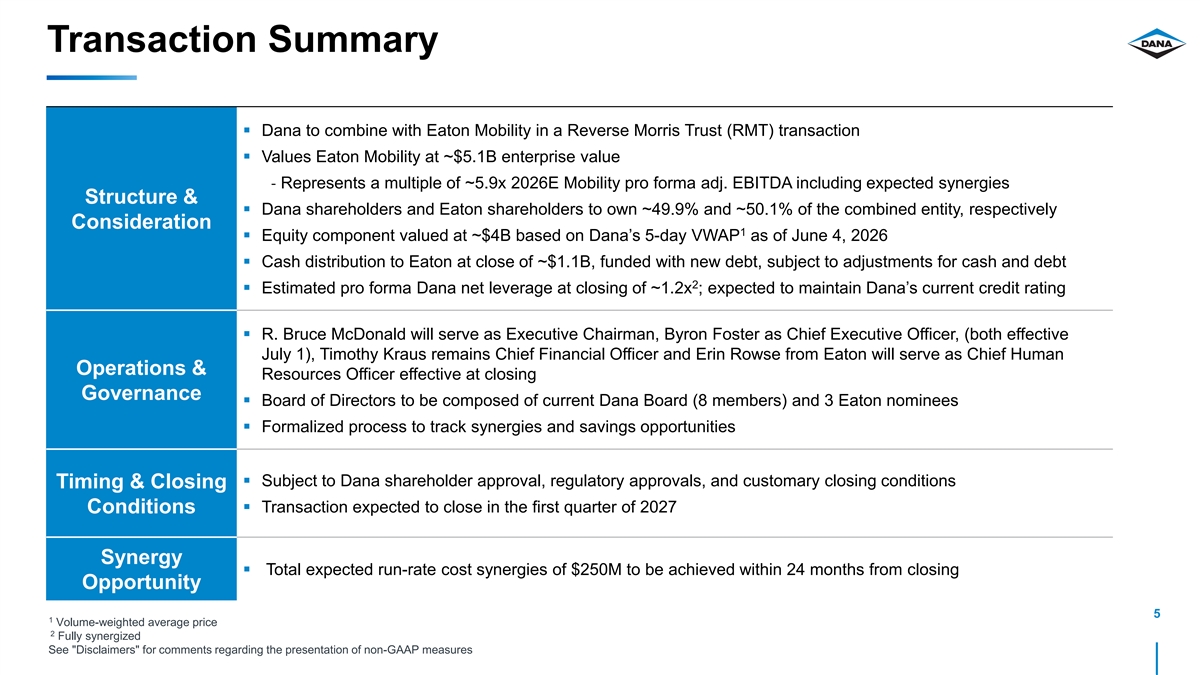

Transaction Summary § Dana to combine with Eaton Mobility in a Reverse Morris Trust (RMT) transaction § Values Eaton Mobility at ~$5.1B enterprise value - Represents a multiple of ~5.9x 2026E Mobility pro forma adj. EBITDA including expected synergies Structure & § Dana shareholders and Eaton shareholders to own ~49.9% and ~50.1% of the combined entity, respectively Consideration 1 § Equity component valued at ~$4B based on Dana’s 5-day VWAP as of June 4, 2026 § Cash distribution to Eaton at close of ~$1.1B, funded with new debt, subject to adjustments for cash and debt 2 § Estimated pro forma Dana net leverage at closing of ~1.2x ; expected to maintain Dana’s current credit rating § R. Bruce McDonald will serve as Executive Chairman, Byron Foster as Chief Executive Officer, (both effective July 1), Timothy Kraus remains Chief Financial Officer and Erin Rowse from Eaton will serve as Chief Human Operations & Resources Officer effective at closing Governance § Board of Directors to be composed of current Dana Board (8 members) and 3 Eaton nominees § Formalized process to track synergies and savings opportunities § Subject to Dana shareholder approval, regulatory approvals, and customary closing conditions Timing & Closing § Transaction expected to close in the first quarter of 2027 Conditions Synergy § Total expected run-rate cost synergies of $250M to be achieved within 24 months from closing Opportunity 5 1 Volume-weighted average price 2 Fully synergized See Disclaimers for comments regarding the presentation of non-GAAP measures

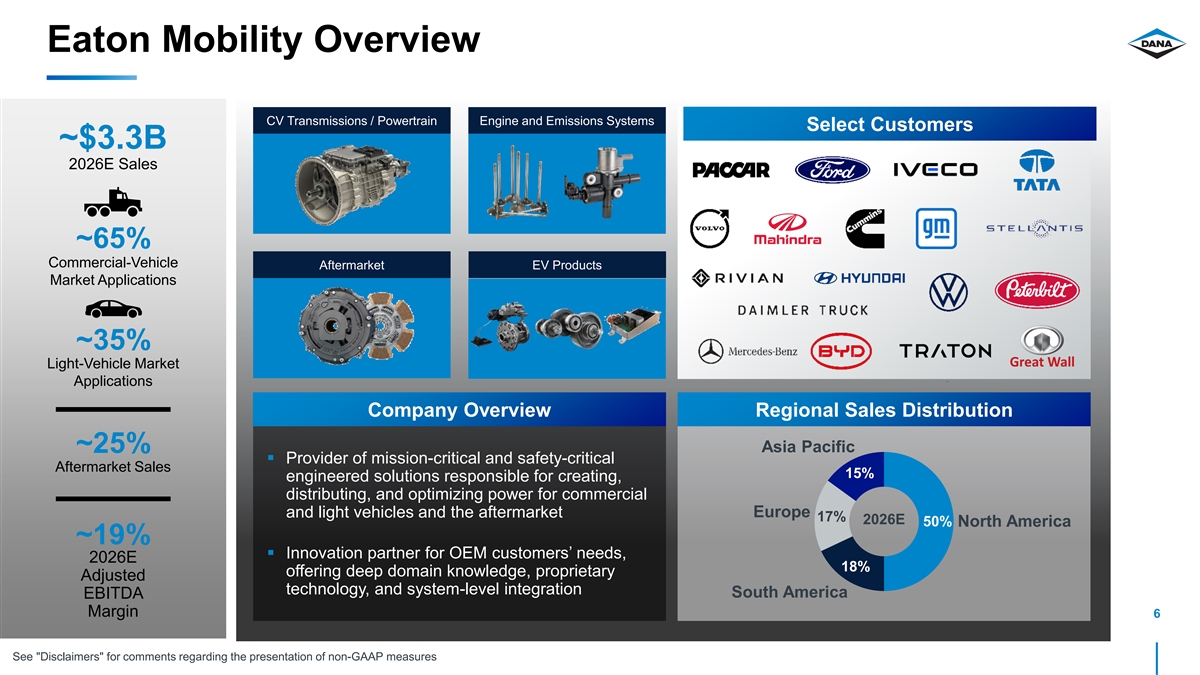

Eaton Mobility Overview CV Transmissions / Powertrain Engine and Emissions Systems Select Customers ~$3.3B 2026E Sales ~65% Commercial-Vehicle Aftermarket EV Products Market Applications ~35% Light-Vehicle Market Applications Company Overview Regional Sales Distribution Asia Pacific ~25% § Provider of mission-critical and safety-critical Aftermarket Sales 15% engineered solutions responsible for creating, distributing, and optimizing power for commercial and light vehicles and the aftermarket Europe 17% 2026E 50% North America ~19% § Innovation partner for OEM customers’ needs, 2026E 18% offering deep domain knowledge, proprietary Adjusted technology, and system-level integration South America EBITDA Margin 6 See Disclaimers for comments regarding the presentation of non-GAAP measures

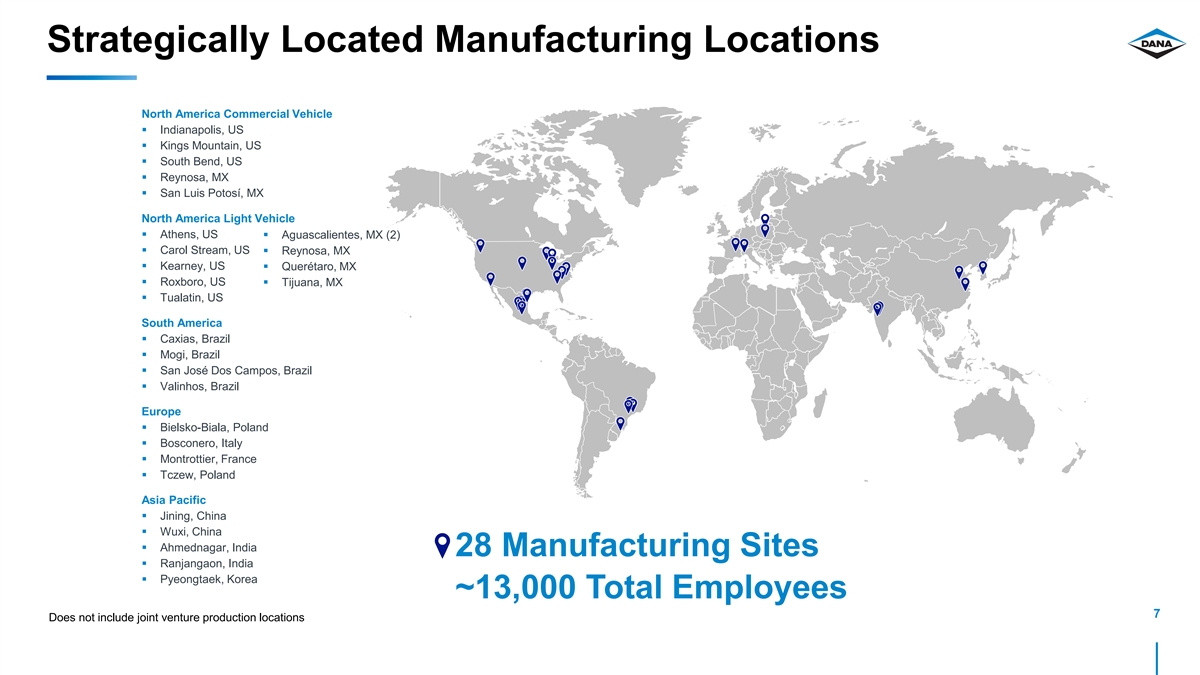

Strategically Located Manufacturing Locations North America Commercial Vehicle § Indianapolis, US § Kings Mountain, US § South Bend, US § Reynosa, MX § San Luis Potosí, MX North America Light Vehicle § Athens, US§ Aguascalientes, MX (2) § Carol Stream, US§ Reynosa, MX § Kearney, US § Querétaro, MX § Roxboro, US § Tijuana, MX § Tualatin, US South America § Caxias, Brazil § Mogi, Brazil § San José Dos Campos, Brazil § Valinhos, Brazil Europe § Bielsko-Biala, Poland § Bosconero, Italy § Montrottier, France § Tczew, Poland Asia Pacific § Jining, China § Wuxi, China § Ahmednagar, India 28 Manufacturing Sites § Ranjangaon, India § Pyeongtaek, Korea ~13,000 Total Employees 7 Does not include joint venture production locations

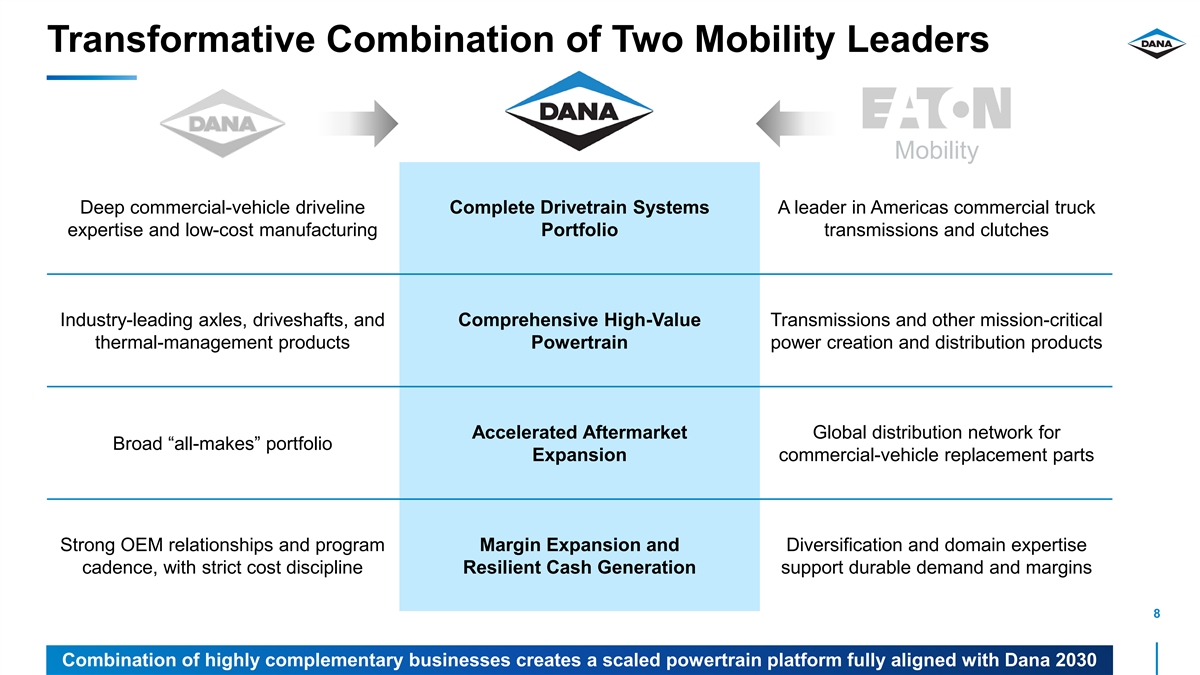

Transformative Combination of Two Mobility Leaders Mobility Deep commercial-vehicle driveline Complete Drivetrain Systems A leader in Americas commercial truck expertise and low-cost manufacturing Portfolio transmissions and clutches Industry-leading axles, driveshafts, and Comprehensive High-Value Transmissions and other mission-critical thermal-management products Powertrain power creation and distribution products Accelerated Aftermarket Global distribution network for Broad “all-makes” portfolio Expansion commercial-vehicle replacement parts Strong OEM relationships and program Margin Expansion and Diversification and domain expertise cadence, with strict cost discipline Resilient Cash Generation support durable demand and margins 8 Combination of highly complementary businesses creates a scaled powertrain platform fully aligned with Dana 2030

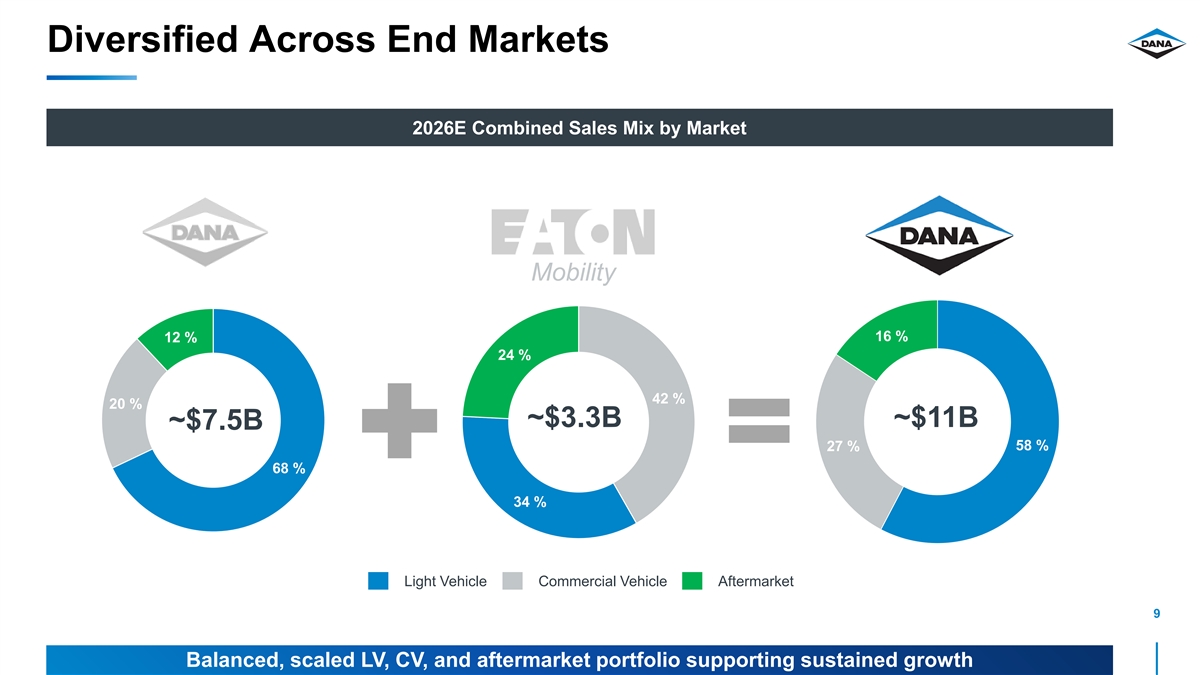

Diversified Across End Markets 2026E Combined Sales Mix by Market Mobility 16 % 12 % 24 % 42 % 20 % ~$3.3B ~$11B ~$7.5B 58 % 27 % 68 % 34 % Light Vehicle Commercial Vehicle Aftermarket 9 Balanced, scaled LV, CV, and aftermarket portfolio supporting sustained growth

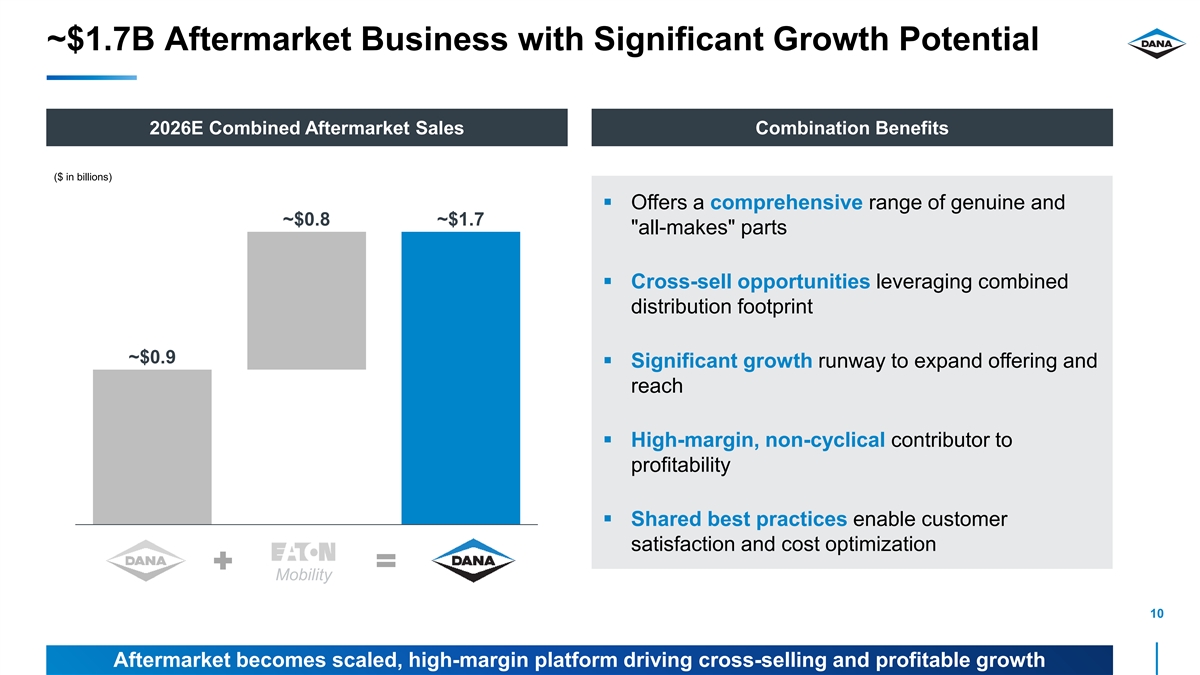

~$1.7B Aftermarket Business with Significant Growth Potential 2026E Combined Aftermarket Sales Combination Benefits ($ in billions) § Offers a comprehensive range of genuine and ~$0.8 ~$1.7 all-makes parts § Cross-sell opportunities leveraging combined distribution footprint ~$0.9 § Significant growth runway to expand offering and reach § High-margin, non-cyclical contributor to profitability § Shared best practices enable customer satisfaction and cost optimization Mobility 10 Aftermarket becomes scaled, high-margin platform driving cross-selling and profitable growth

Combination Expands Dana 2030 Growth Strategy § Additional products will expand scale § Accelerates 2030 growth targets with previous sales target expected to be achieved in 2027… § Broadens scope of traditional products – CV transmissions – Cross-selling opportunity § Aftermarket – Broader breadth and depth of products across all markets § Enhances applied technologies strategy Revised 2030 Sales Target Prior 2030 Sales Target – Complementary EV products and capabilities 11 ~$14-$15 billion billion

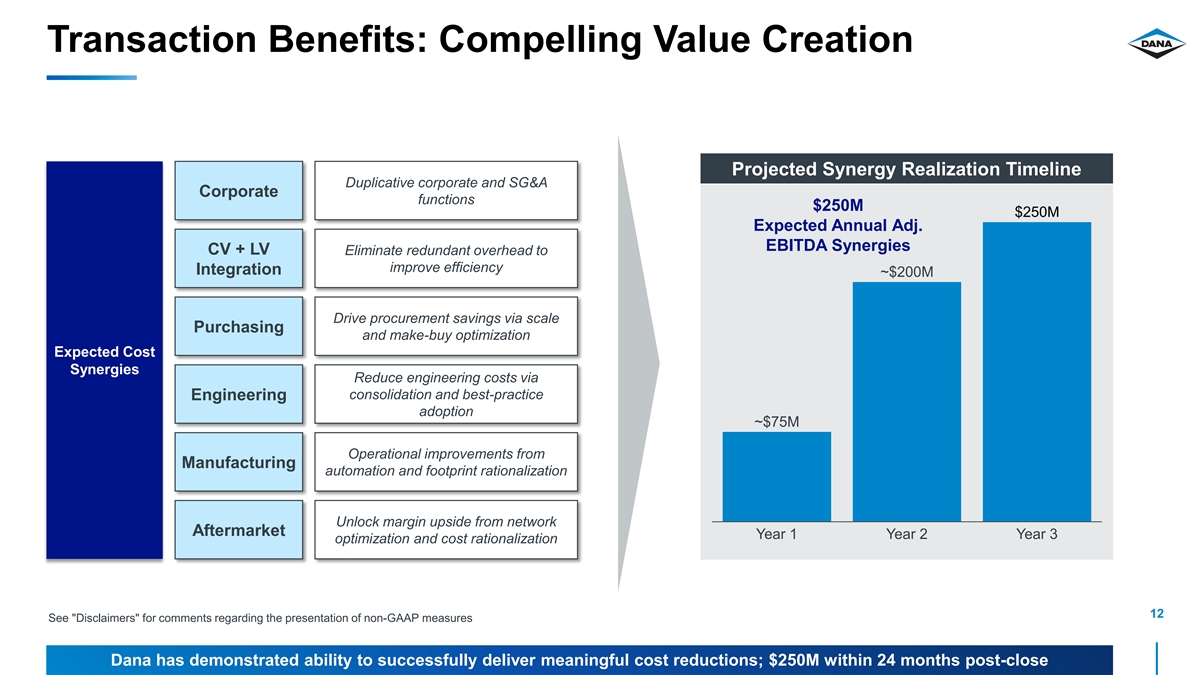

Transaction Benefits: Compelling Value Creation Projected Synergy Realization Timeline Duplicative corporate and SG&A Corporate functions $250M $250M Expected Annual Adj. EBITDA Synergies CV + LV Eliminate redundant overhead to improve efficiency Integration ~$200M Drive procurement savings via scale Purchasing and make-buy optimization Expected Cost Synergies Reduce engineering costs via consolidation and best-practice Engineering adoption ~$75M Operational improvements from Manufacturing automation and footprint rationalization Unlock margin upside from network Aftermarket Year 1 Year 2 Year 3 optimization and cost rationalization 12 See Disclaimers for comments regarding the presentation of non-GAAP measures Dana has demonstrated ability to successfully deliver meaningful cost reductions; $250M within 24 months post-close

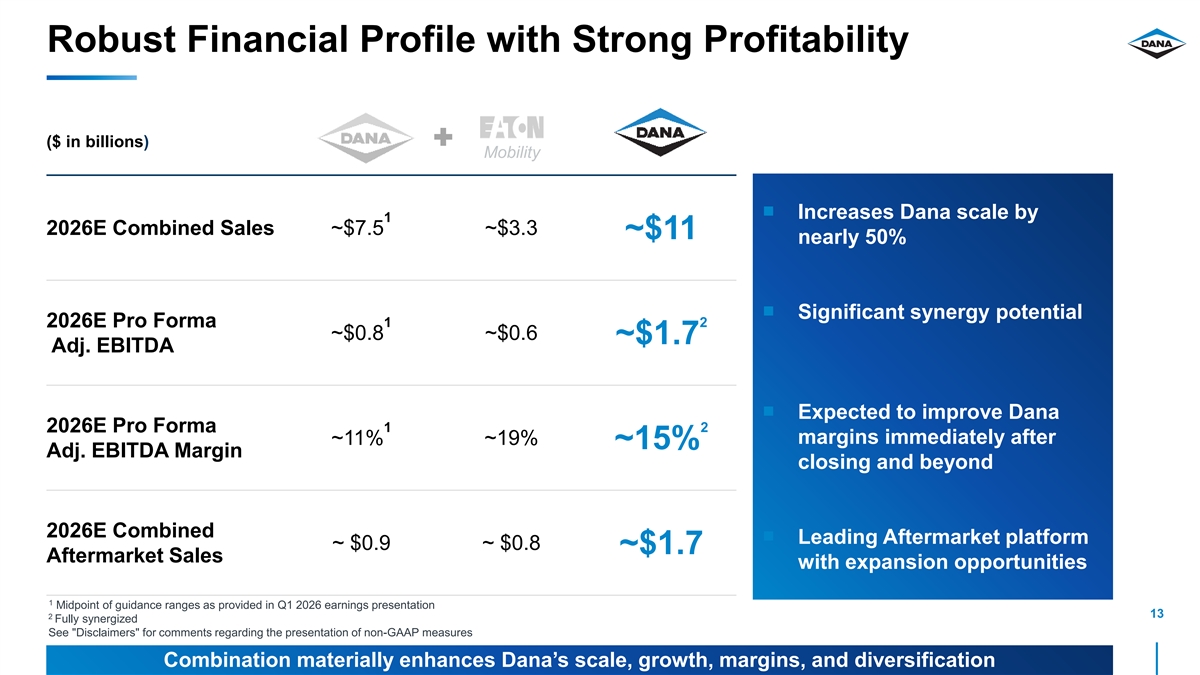

Robust Financial Profile with Strong Profitability ($ in billions) Mobility Increases Dana scale by 1 § 2026E Combined Sales ~$7.5 ~$3.3 ~$11 nearly 50% Significant synergy potential § 2026E Pro Forma 1 2 ~$0.8 ~$0.6 ~$1.7 Adj. EBITDA Expected to improve Dana § 2026E Pro Forma 1 2 margins immediately after ~11% ~19% ~15% Adj. EBITDA Margin closing and beyond 2026E Combined Leading Aftermarket platform § ~ $0.9 ~ $0.8 ~$1.7 Aftermarket Sales with expansion opportunities 1 Midpoint of guidance ranges as provided in Q1 2026 earnings presentation 13 2 Fully synergized See Disclaimers for comments regarding the presentation of non-GAAP measures Combination materially enhances Dana’s scale, growth, margins, and diversification

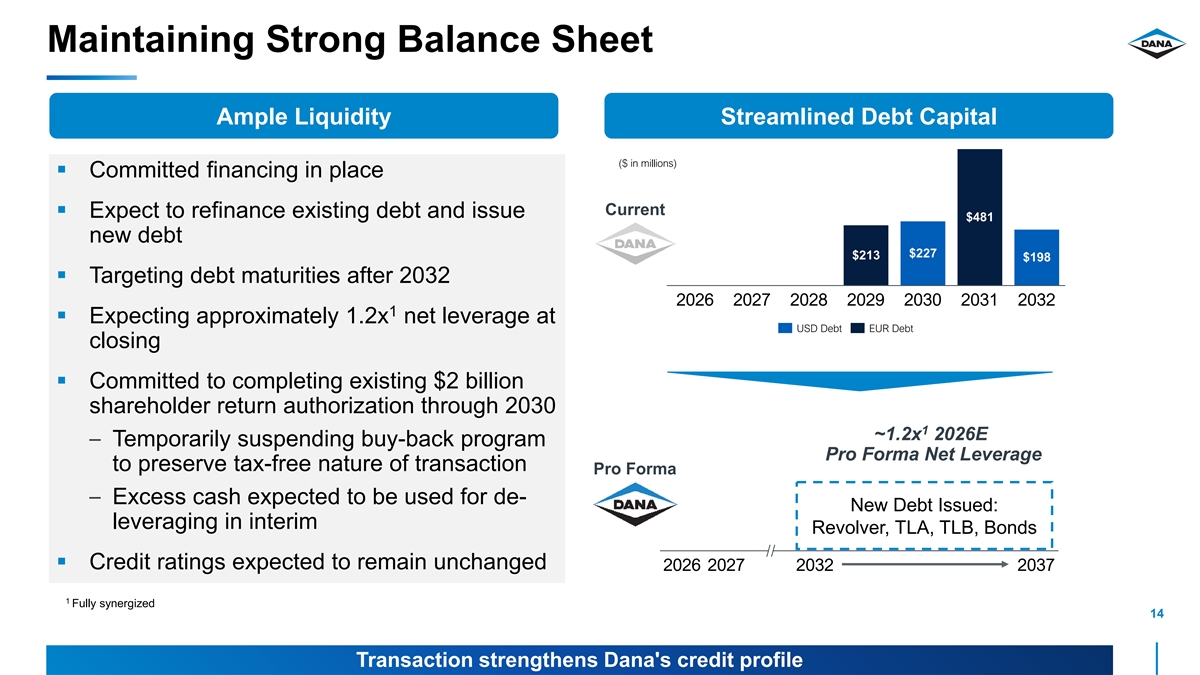

Maintaining Strong Balance Sheet Ample Liquidity Streamlined Debt Capital ($ in millions) § Committed financing in place Current § Expect to refinance existing debt and issue $481 new debt $227 $213 $198 § Targeting debt maturities after 2032 2026 2027 2028 2029 2030 2031 2032 1 § Expecting approximately 1.2x net leverage at USD Debt EUR Debt closing § Committed to completing existing $2 billion shareholder return authorization through 2030 1 ~1.2x 2026E – Temporarily suspending buy-back program Pro Forma Net Leverage to preserve tax-free nature of transaction Pro Forma – Excess cash expected to be used for de- New Debt Issued: leveraging in interim Revolver, TLA, TLB, Bonds § Credit ratings expected to remain unchanged 2026 2027 2032 2037 1 Fully synergized 14 Transaction strengthens Dana's credit profile Source: Dana

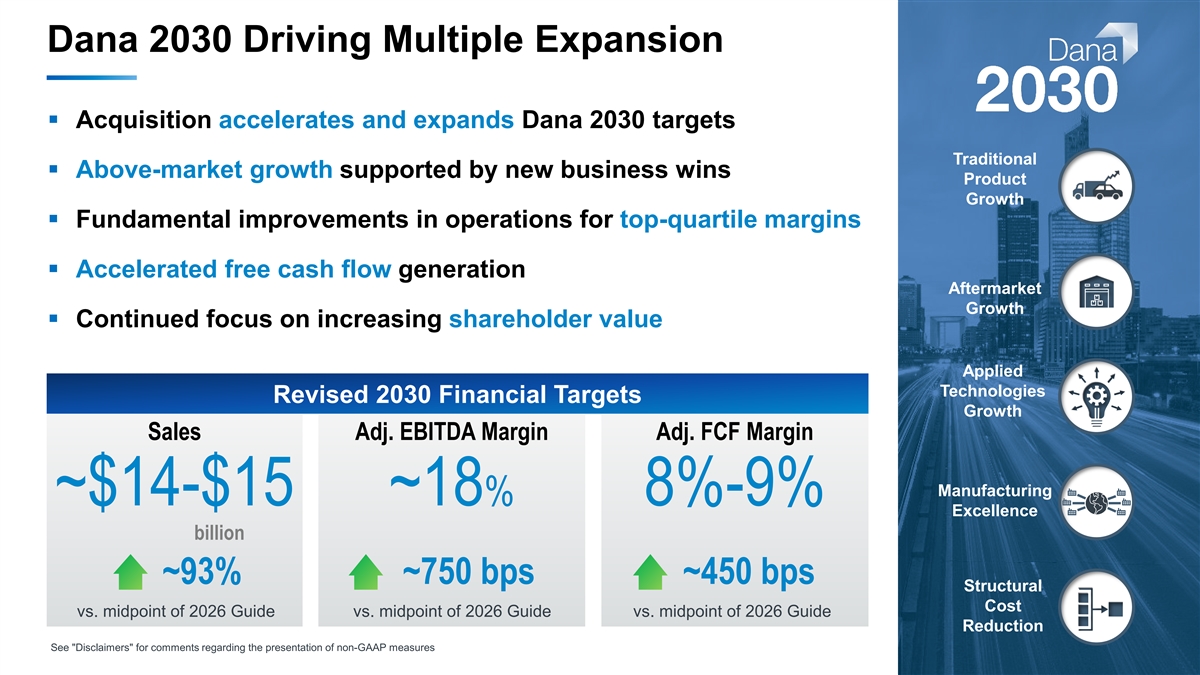

Dana 2030 Driving Multiple Expansion § Acquisition accelerates and expands Dana 2030 targets Traditional § Above-market growth supported by new business wins Product Growth § Fundamental improvements in operations for top-quartile margins § Accelerated free cash flow generation Aftermarket Growth § Continued focus on increasing shareholder value Applied Technologies Revised 2030 Financial Targets Growth Sales Adj. EBITDA Margin Adj. FCF Margin Manufacturing ~$14-$15 ~18% 8%-9% Excellence billion ~93% ~750 bps ~450 bps Structural Cost vs. midpoint of 2026 Guide vs. midpoint of 2026 Guide vs. midpoint of 2026 Guide 15 Reduction See Disclaimers for comments regarding the presentation of non-GAAP measures

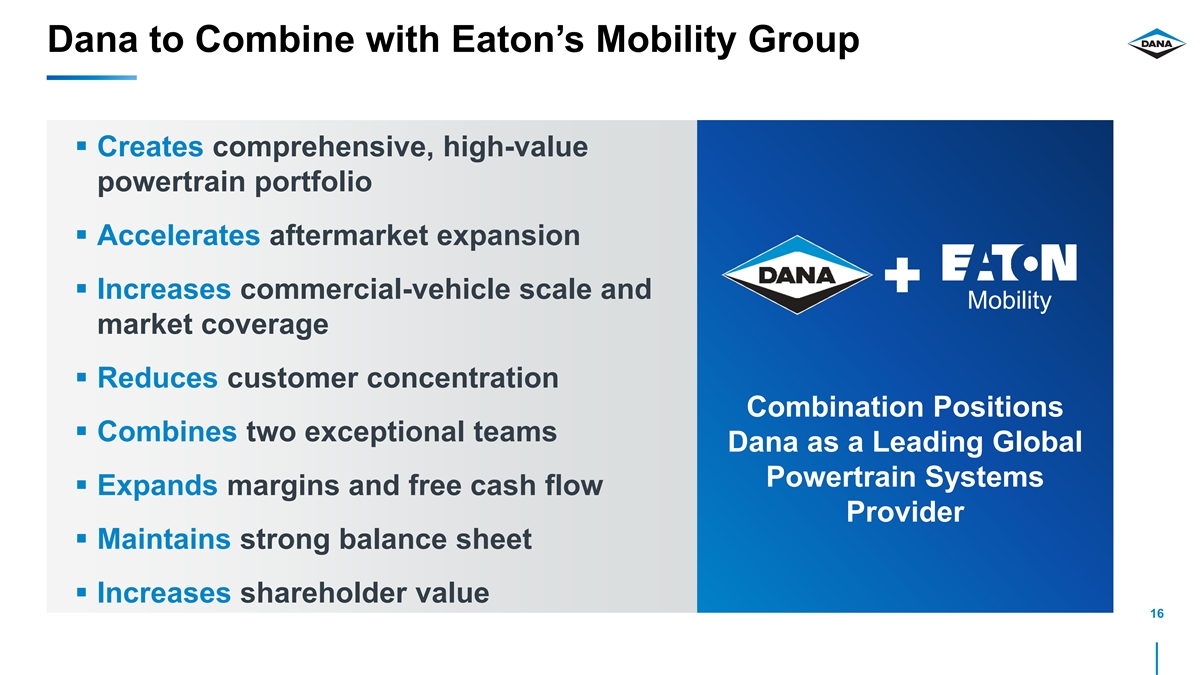

Dana to Combine with Eaton’s Mobility Group § Creates comprehensive, high-value powertrain portfolio § Accelerates aftermarket expansion § Increases commercial-vehicle scale and Mobility market coverage § Reduces customer concentration Combination Positions § Combines two exceptional teams Dana as a Leading Global Powertrain Systems § Expands margins and free cash flow Provider § Maintains strong balance sheet § Increases shareholder value 16

17 17