☑QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended June 30, 2024

or

☐TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from __________to__________

Commission File Number 1-2256

Exxon Mobil Corporation

(Exact name of registrant as specified in its charter)

New Jersey

13-5409005

(State or other jurisdiction of incorporation or organization)

(I.R.S. Employer Identification Number)

22777 Springwoods Village Parkway,Spring,Texas77389-1425

(Address of principal executive offices) (Zip Code)

(972)940-6000

(Registrant's telephone number, including area code)

_______________________

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class

Trading Symbol

Name of Each Exchange on Which Registered

Common Stock, without par value

XOM

New York Stock Exchange

0.524% Notes due 2028

XOM28

New York Stock Exchange

0.835% Notes due 2032

XOM32

New York Stock Exchange

1.408% Notes due 2039

XOM39A

New York Stock Exchange

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.Yes ☑No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).Yes ☑No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer

☑

Accelerated filer

☐

Non-accelerated filer

☐

Smaller reporting company

☐

Emerging growth company

☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes☐No ☑

Indicate the number of shares outstanding of each of the issuer's classes of common stock, as of the latest practicable date.

Class

Outstanding as of June 30, 2024

Common stock, without par value

4,442,826,580

EXXON MOBIL CORPORATION

FORM 10-Q

FOR THE QUARTERLY PERIOD ENDED JUNE 30, 2024

TABLE OF CONTENTS

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements

Condensed Consolidated Statement of Income - Three and six months ended June 30, 2024 and 2023

Amortization and settlement of postretirement benefits reserves adjustment included in net periodic benefit costs

17

7

26

13

Total other comprehensive income (loss)

(69)

538

(1,369)

736

Comprehensive income (loss) including noncontrolling interests

9,502

8,691

16,768

20,732

Comprehensive income (loss) attributable to noncontrolling interests

280

373

506

809

Comprehensive income (loss) attributable to ExxonMobil

9,222

8,318

16,262

19,923

The information in the Notes to Condensed Consolidated Financial Statements is an integral part of these statements.

4

CONDENSED CONSOLIDATED BALANCE SHEET

(millions of dollars, unless noted)

June 30, 2024

December 31, 2023

ASSETS

Current assets

Cash and cash equivalents

26,460

31,539

Cash and cash equivalents – restricted

28

29

Notes and accounts receivable – net

43,071

38,015

Inventories

Crude oil, products and merchandise

19,685

20,528

Materials and supplies

4,818

4,592

Other current assets

2,176

1,906

Total current assets

96,238

96,609

Investments, advances and long-term receivables

47,948

47,630

Property, plant and equipment – net

298,283

214,940

Other assets, including intangibles – net

18,238

17,138

Total Assets

460,707

376,317

LIABILITIES

Current liabilities

Notes and loans payable

6,621

4,090

Accounts payable and accrued liabilities

60,107

58,037

Income taxes payable

4,035

3,189

Total current liabilities

70,763

65,316

Long-term debt

36,565

37,483

Postretirement benefits reserves

10,398

10,496

Deferred income tax liabilities

40,080

24,452

Long-term obligations to equity companies

1,612

1,804

Other long-term obligations

25,023

24,228

Total Liabilities

184,441

163,779

Commitments and contingencies (Note 3)

EQUITY

Common stock without par value

(9,000 million shares authorized, 8,019 million shares issued)

46,781

17,781

Earnings reinvested

463,294

453,927

Accumulated other comprehensive income

(13,187)

(11,989)

Common stock held in treasury

(3,576 million shares at June 30, 2024 and

4,048 million shares at December 31, 2023)

(228,483)

(254,917)

ExxonMobil share of equity

268,405

204,802

Noncontrolling interests

7,861

7,736

Total Equity

276,266

212,538

Total Liabilities and Equity

460,707

376,317

The information in the Notes to Condensed Consolidated Financial Statements is an integral part of these statements.

5

CONDENSED CONSOLIDATED STATEMENT OF CASH FLOWS

(millions of dollars)

Six Months Ended June 30,

2024

2023

CASH FLOWS FROM OPERATING ACTIVITIES

Net income (loss) including noncontrolling interests

18,137

19,996

Depreciation and depletion (includes impairments)

10,599

8,486

Changes in operational working capital, excluding cash and debt

(2,608)

(3,885)

All other items – net

(904)

1,127

Net cash provided by operating activities

25,224

25,724

CASH FLOWS FROM INVESTING ACTIVITIES

Additions to property, plant and equipment

(11,309)

(10,771)

Proceeds from asset sales and returns of investments

1,629

2,141

Additional investments and advances

(744)

(834)

Other investing activities including collection of advances

224

183

Cash acquired from mergers and acquisitions

754

0

Net cash used in investing activities

(9,446)

(9,281)

CASH FLOWS FROM FINANCING ACTIVITIES

Additions to long-term debt

217

136

Reductions in long-term debt

(1,142)

(6)

Reductions in short-term debt

(2,771)

(172)

Additions/(reductions) in debt with three months or less maturity

(6)

(172)

Contingent consideration payments

(27)

(68)

Cash dividends to ExxonMobil shareholders

(8,093)

(7,439)

Cash dividends to noncontrolling interests

(397)

(293)

Changes in noncontrolling interests

16

11

Common stock acquired

(8,337)

(8,680)

Net cash used in financing activities

(20,540)

(16,683)

Effects of exchange rate changes on cash

(318)

132

Increase/(decrease) in cash and cash equivalents

(5,080)

(108)

Cash and cash equivalents at beginning of period

31,568

29,665

Cash and cash equivalents at end of period

26,488

29,557

SUPPLEMENTAL DISCLOSURES

Income taxes paid

6,968

8,841

Cash interest paid

Included in cash flows from operating activities

321

295

Capitalized, included in cash flows from investing activities

590

561

Total cash interest paid

911

856

Noncash right of use assets recorded in exchange for lease liabilities

Operating leases

647

1,036

Finance leases

53

438

Non-Cash Transaction: The Corporation acquired Pioneer Natural Resources in an all-stock transaction on May 3, 2024, having issued 545 million shares of ExxonMobil common stock having a fair value of $63 billion and assumed debt with a fair value of $5 billion. See Note 2 for additional information.

The information in the Notes to Condensed Consolidated Financial Statements is an integral part of these statements.

6

CONDENSED CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

ExxonMobil Share of Equity

(millions of dollars, unless noted)

Common Stock

Earnings Reinvested

Accumulated Other Comprehensive Income

Common Stock Held in Treasury

ExxonMobil Share of Equity

Non-controlling Interests

Total Equity

Balance as of March 31, 2023

15,904

440,552

(13,095)

(244,676)

198,685

7,729

206,414

Amortization of stock-based awards

130

—

—

—

130

—

130

Other

(5)

—

—

—

(5)

27

22

Net income (loss) for the period

—

7,880

—

—

7,880

273

8,153

Dividends - common shares

—

(3,701)

—

—

(3,701)

(178)

(3,879)

Other comprehensive income (loss)

—

—

438

—

438

100

538

Share repurchases, at cost

—

—

—

(4,383)

(4,383)

—

(4,383)

Dispositions

—

—

—

2

2

—

2

Balance as of June 30, 2023

16,029

444,731

(12,657)

(249,057)

199,046

7,951

206,997

Balance as of March 31, 2024

17,971

458,339

(13,169)

(257,891)

205,250

7,802

213,052

Amortization of stock-based awards

178

—

—

—

178

—

178

Other

(117)

—

—

—

(117)

10

(107)

Net income (loss) for the period

—

9,240

—

—

9,240

331

9,571

Dividends - common shares

—

(4,285)

—

—

(4,285)

(231)

(4,516)

Other comprehensive income (loss)

—

—

(18)

—

(18)

(51)

(69)

Share repurchases, at cost

—

—

—

(5,310)

(5,310)

—

(5,310)

Issued for acquisitions

28,749

—

—

34,603

63,352

—

63,352

Dispositions

—

—

—

115

115

—

115

Balance as of June 30, 2024

46,781

463,294

(13,187)

(228,483)

268,405

7,861

276,266

Three Months Ended June 30, 2024

Three Months Ended June 30, 2023

Common Stock Share Activity

(millions of shares)

Issued

Held in Treasury

Outstanding

Issued

Held in Treasury

Outstanding

Balance as of March 31

8,019

(4,076)

3,943

8,019

(3,976)

4,043

Share repurchases, at cost

—

(45)

(45)

—

(40)

(40)

Issued for acquisitions

—

545

545

—

—

—

Dispositions

—

—

—

—

—

—

Balance as of June 30

8,019

(3,576)

4,443

8,019

(4,016)

4,003

The information in the Notes to Condensed Consolidated Financial Statements is an integral part of these statements.

7

CONDENSED CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

ExxonMobil Share of Equity

(millions of dollars, unless noted)

Common Stock

Earnings Reinvested

Accumulated Other Comprehensive Income

Common Stock Held in Treasury

ExxonMobil Share of Equity

Non-controlling Interests

Total Equity

Balance as of December 31, 2022

15,752

432,860

(13,270)

(240,293)

195,049

7,424

202,473

Amortization of stock-based awards

288

—

—

—

288

—

288

Other

(11)

—

—

—

(11)

11

—

Net income (loss) for the period

—

19,310

—

—

19,310

686

19,996

Dividends - common shares

—

(7,439)

—

—

(7,439)

(293)

(7,732)

Other comprehensive income (loss)

—

—

613

—

613

123

736

Share repurchases, at cost

—

—

—

(8,768)

(8,768)

—

(8,768)

Dispositions

—

—

—

4

4

—

4

Balance as of June 30, 2023

16,029

444,731

(12,657)

(249,057)

199,046

7,951

206,997

Balance as of December 31, 2023

17,781

453,927

(11,989)

(254,917)

204,802

7,736

212,538

Amortization of stock-based awards

375

—

—

—

375

—

375

Other

(124)

—

—

—

(124)

16

(108)

Net income (loss) for the period

—

17,460

—

—

17,460

677

18,137

Dividends - common shares

—

(8,093)

—

—

(8,093)

(397)

(8,490)

Other comprehensive income (loss)

—

—

(1,198)

—

(1,198)

(171)

(1,369)

Share repurchases, at cost

—

—

—

(8,288)

(8,288)

—

(8,288)

Issued for acquisitions

28,749

—

—

34,603

63,352

—

63,352

Dispositions

—

—

—

119

119

—

119

Balance as of June 30, 2024

46,781

463,294

(13,187)

(228,483)

268,405

7,861

276,266

Six Months Ended June 30, 2024

Six Months Ended June 30, 2023

Common Stock Share Activity

(millions of shares)

Issued

Held in Treasury

Outstanding

Issued

Held in Treasury

Outstanding

Balance as of December 31

8,019

(4,048)

3,971

8,019

(3,937)

4,082

Share repurchases, at cost

—

(73)

(73)

—

(79)

(79)

Issued for acquisitions

—

545

545

—

—

—

Dispositions

—

—

—

—

—

—

Balance as of June 30

8,019

(3,576)

4,443

8,019

(4,016)

4,003

The information in the Notes to Condensed Consolidated Financial Statements is an integral part of these statements.

8

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

Note 1. Basis of Financial Statement Preparation

These unaudited condensed consolidated financial statements should be read in the context of the consolidated financial statements and notes thereto filed with the Securities and Exchange Commission in the Corporation's 2023 Annual Report on Form 10-K. In the opinion of the Corporation, the information furnished herein reflects all known accruals and adjustments necessary for a fair statement of the results for the periods reported herein. All such adjustments are of a normal recurring nature.

The Corporation's exploration and production activities are accounted for under the "successful efforts" method.

Note 2. Pioneer Natural Resources Merger

On May 3, 2024, the Corporation acquired Pioneer Natural Resources Company ("Pioneer"), an independent oil and gas exploration and production company. The acquisition included over 850 thousand net acres in the Midland Basin of West Texas and proved reserves in excess of 2 billion oil-equivalent barrels. In connection with the acquisition, we issued 545 million shares of ExxonMobil common stock having a fair value of $63 billion on the acquisition date, and assumed debt with a fair value of $5 billion.

The transaction was accounted for as a business combination in accordance with ASC 805, which requires that assets acquired and liabilities assumed be recognized at their fair values as of the acquisition date. The following table summarizes the provisional fair values of the assets acquired and liabilities assumed.

(billions of dollars)

Pioneer

Current assets (1)

3

Other non-current assets

1

Property, plant & equipment (2)

84

Total identifiable assets acquired

88

Current liabilities (1)

3

Long-term debt (3)

5

Deferred income tax liabilities (4)

16

Other non-current liabilities

2

Total liabilities assumed

26

Net identifiable assets acquired

62

Goodwill (5)

1

Net assets (6)

63

(1) Current assets and current liabilities consist primarily of accounts receivable and payable, with their respective fair values approximating historical values given their short-term duration, expectation of insignificant bad debt expense, and our credit rating.

(2) Property, plant and equipment was preliminarily valued using the income approach. Significant inputs and assumptions used in the income approach included estimates for commodity prices, future oil and gas production profiles, operating expenses, capital expenditures, and a risk-adjusted discount rate. Collectively, these inputs are Level 3 inputs.

(3) Long-term debt was valued using market prices as of the acquisition date, which reflects the use of Level 1 inputs.

(4) Deferred income taxes represent the tax effects of differences in the tax basis and acquisition date fair values of assets acquired and liabilities assumed.

(5) Goodwill was allocated to the Upstream segment.

(6) Provisional fair value measurements were made for assets acquired and liabilities assumed. Adjustments to those measurements may be made in subsequent periods, up to one year from the date of acquisition, as we continue to evaluate the information necessary to complete the analysis.

9

Debt Assumed in the Merger

The following table presents long-term debt assumed at closing:

(millions of dollars)

Par Value

Fair Value as of May 2, 2024

0.250% Convertible Senior Notes due May 2025 (1)

450

1,327

1.125% Senior Notes due January 2026

750

699

5.100% Senior Notes due March 2026

1,100

1,096

7.200% Senior Notes due January 2028

241

252

4.125% Senior Notes due February 2028

138

130

1.900% Senior Notes due August 2030

1,100

914

2.150% Senior Notes due January 2031

1,000

832

(1) In June 2024, the Corporation redeemed in full all of the Convertible Senior Notes assumed from Pioneer for an amount consistent with the acquisition date fair value.

Actual and Pro Forma Impact of Merger

The following table presents revenues and earnings for Pioneer since the acquisition date (May 3, 2024), for the periods presented:

(millions of dollars)

Three Months Ended June 30, 2024

Six Months Ended June 30, 2024

Sales and other operating revenues

4,372

4,372

Net income (loss) attributable to ExxonMobil

398

398

The following table presents unaudited pro forma information for the Corporation as if the merger with Pioneer had occurred at the beginning of January 1, 2023:

Unaudited

(millions of dollars)

Three Months Ended June 30,

Six Months Ended June 30,

2024

2023

2024

2023

Sales and other operating revenues

92,167

86,076

178,557

175,425

Net income (loss) attributable to ExxonMobil

9,265

8,577

18,256

20,663

The historical financial information was adjusted to give effect to the pro forma events that were directly attributable to the merger and factually supportable. The unaudited pro forma consolidated results are not necessarily indicative of what the consolidated results of operations actually would have been had the merger been completed on January 1, 2023. In addition, the unaudited pro forma consolidated results reflect pro forma adjustments primarily related to conforming Pioneer's accounting policies to ExxonMobil, additional depreciation expense related to the fair value adjustment of the acquired property, plant and equipment, our capital structure, Pioneer's transaction-related costs, and applicable income tax impacts of the pro forma adjustments.

Our transaction costs to effect the acquisition were immaterial.

10

Note 3. Litigation and Other Contingencies

Litigation

A variety of claims have been made against ExxonMobil and certain of its consolidated subsidiaries in a number of pending lawsuits. Management has regular litigation reviews, including updates from corporate and outside counsel, to assess the need for accounting recognition or disclosure of these contingencies. The Corporation accrues an undiscounted liability for those contingencies where the incurrence of a loss is probable and the amount can be reasonably estimated. If a range of amounts can be reasonably estimated and no amount within the range is a better estimate than any other amount, then the minimum of the range is accrued. The Corporation does not record liabilities when the likelihood that the liability has been incurred is probable but the amount cannot be reasonably estimated or when the liability is believed to be only reasonably possible or remote. For contingencies where an unfavorable outcome is reasonably possible and which are significant, the Corporation discloses the nature of the contingency and, where feasible, an estimate of the possible loss. For purposes of our contingency disclosures, “significant” includes material matters, as well as other matters which management believes should be disclosed.

State and local governments and other entities in various jurisdictions across the United States and its territories have filed a number of legal proceedings against several oil and gas companies, including ExxonMobil, requesting unprecedented legal and equitable relief for various alleged injuries purportedly connected to climate change. These lawsuits assert a variety of novel, untested claims under statutory and common law. Additional such lawsuits may be filed. We believe the legal and factual theories set forth in these proceedings are meritless and represent an inappropriate attempt to use the court system to usurp the proper role of policymakers in addressing the societal challenges of climate change.

Local governments in Louisiana have filed unprecedented legal proceedings against a number of oil and gas companies, including ExxonMobil, requesting compensation for the restoration of coastal marsh erosion in the state. We believe the factual and legal theories set forth in these proceedings are meritless.

While the outcome of any litigation can be unpredictable, we believe the likelihood is remote that the ultimate outcomes of these lawsuits will have a material adverse effect on the Corporation’s operations, financial condition, or financial statements taken as a whole. We will continue to defend vigorously against these claims.

Other Contingencies

The Corporation and certain of its consolidated subsidiaries were contingently liable at June 30, 2024, for guarantees relating to notes, loans and performance under contracts. Where guarantees for environmental remediation and other similar matters do not include a stated cap, the amounts reflect management’s estimate of the maximum potential exposure. Where it is not possible to make a reasonable estimation of the maximum potential amount of future payments, future performance is expected to be either immaterial or have only a remote chance of occurrence.

June 30, 2024

(millions of dollars)

Equity Company

Obligations(1)

Other Third-Party Obligations

Total

Guarantees

Debt-related

1,070

135

1,205

Other

678

5,896

6,574

Total

1,748

6,031

7,779

(1) ExxonMobil share

Additionally, the Corporation and its affiliates have numerous long-term sales and purchase commitments in their various business activities, all of which are expected to be fulfilled with no adverse consequences material to the Corporation’s operations or financial condition.

Current period change excluding amounts reclassified from accumulated other comprehensive income (1)

570

35

605

Amounts reclassified from accumulated other comprehensive income

—

8

8

Total change in accumulated other comprehensive income

570

43

613

Balance as of June 30, 2023

(14,021)

1,364

(12,657)

Balance as of December 31, 2023

(13,056)

1,067

(11,989)

Current period change excluding amounts reclassified from accumulated other comprehensive income (1)

(1,197)

(21)

(1,218)

Amounts reclassified from accumulated other comprehensive income

—

20

20

Total change in accumulated other comprehensive income

(1,197)

(1)

(1,198)

Balance as of June 30, 2024

(14,253)

1,066

(13,187)

(1) Cumulative Foreign Exchange Translation Adjustment includes net investment hedge gain/(loss) net of taxes of $123 million and $(70) million in 2024 and 2023, respectively.

Amounts Reclassified Out of Accumulated Other

Comprehensive Income - Before-tax Income/(Expense)

(millions of dollars)

Three Months Ended June 30,

Six Months Ended June 30,

2024

2023

2024

2023

Amortization and settlement of postretirement benefits reserves adjustment included in net periodic benefit costs

(Statement of Income line: Non-service pension and postretirement benefit expense)

Amortization and settlement of postretirement benefits reserves adjustment included in net periodic benefit costs

(5)

1

(8)

(1)

Total

54

106

(20)

163

12

Note 5. Earnings Per Share

Earnings per common share

Three Months Ended June 30,

Six Months Ended June 30,

2024

2023

2024

2023

Net income (loss) attributable to ExxonMobil (millions of dollars)

9,240

7,880

17,460

19,310

Weighted-average number of common shares outstanding (millions of shares)(1)

4,317

4,066

4,158

4,084

Earnings (loss) per common share (dollars)(2)

2.14

1.94

4.20

4.73

Dividends paid per common share (dollars)

0.95

0.91

1.90

1.82

(1) Includes restricted shares not vested as well as 545 million shares issued for the Pioneer merger on May 3, 2024.

(2) Earnings (loss) per common share and earnings (loss) per common share – assuming dilution are the same in each period shown.

Note 6. Pension and Other Postretirement Benefits

(millions of dollars)

Three Months Ended June 30,

Six Months Ended June 30,

2024

2023

2024

2023

Components of net benefit cost

Pension Benefits - U.S.

Service cost

117

122

230

242

Interest cost

168

165

336

331

Expected return on plan assets

(181)

(133)

(362)

(266)

Amortization of actuarial loss/(gain)

21

21

42

42

Amortization of prior service cost

(8)

(7)

(16)

(14)

Net pension enhancement and curtailment/settlement cost

14

7

17

15

Net benefit cost

131

175

247

350

Pension Benefits - Non-U.S.

Service cost

86

81

169

163

Interest cost

198

232

425

466

Expected return on plan assets

(230)

(172)

(491)

(346)

Amortization of actuarial loss/(gain)

24

14

49

28

Amortization of prior service cost

12

13

25

25

Net benefit cost

90

168

177

336

Other Postretirement Benefits

Service cost

19

20

37

40

Interest cost

62

69

125

139

Expected return on plan assets

(5)

(3)

(10)

(7)

Amortization of actuarial loss/(gain)

(26)

(31)

(52)

(61)

Amortization of prior service cost

(15)

(11)

(31)

(21)

Net benefit cost

35

44

69

90

13

Note 7. Financial Instruments and Derivatives

The estimated fair value of financial instruments and derivatives at June 30, 2024 and December 31, 2023, and the related hierarchy level for the fair value measurement was as follows:

June 30, 2024

Fair Value

(millions of dollars)

Level 1

Level 2

Level 3

Total Gross Assets & Liabilities

Effect of Counterparty Netting

Effect of Collateral Netting

Difference in Carrying Value and Fair Value

Net Carrying Value

Assets

Derivative assets (1)

4,790

1,187

—

5,977

(5,510)

(24)

—

443

Advances to/receivables from equity companies (2)(6)

—

2,475

4,206

6,681

—

—

476

7,157

Other long-term financial assets (3)

1,400

—

1,515

2,915

—

—

237

3,152

Liabilities

Derivative liabilities(4)

4,996

1,457

—

6,453

(5,510)

(230)

—

713

Long-term debt(5)

28,874

1,469

—

30,343

—

—

4,063

34,406

Long-term obligations to equity companies(6)

—

—

1,680

1,680

—

—

(68)

1,612

Other long-term financial liabilities(7)

—

—

516

516

—

—

49

565

December 31, 2023

Fair Value

(millions of dollars)

Level 1

Level 2

Level 3

Total Gross Assets & Liabilities

Effect of Counterparty Netting

Effect of Collateral Netting

Difference in Carrying Value and Fair Value

Net Carrying Value

Assets

Derivative assets (1)

4,544

1,731

—

6,275

(5,177)

(528)

—

570

Advances to/receivables from equity companies (2)(6)

—

2,517

4,491

7,008

—

—

519

7,527

Other long-term financial assets (3)

1,389

—

944

2,333

—

—

202

2,535

Liabilities

Derivative liabilities(4)

4,056

1,608

—

5,664

(5,177)

(40)

—

447

Long-term debt(5)

30,556

2,004

—

32,560

—

—

3,102

35,662

Long-term obligations to equity companies(6)

—

—

1,896

1,896

—

—

(92)

1,804

Other long-term financial liabilities (7)

—

—

697

697

—

—

45

742

(1) Included in the Balance Sheet lines: Notes and accounts receivable - net and Other assets, including intangibles - net.

(2) Included in the Balance Sheet line: Investments, advances and long-term receivables.

(3) Included in the Balance Sheet lines: Investments, advances and long-term receivables and Other assets, including intangibles - net.

(4) Included in the Balance Sheet lines: Accounts payable and accrued liabilities and Other long-term obligations.

(5) Excluding finance lease obligations.

(6) Advances to/receivables from equity companies and long-term obligations to equity companies are mainly designated as hierarchy level 3 inputs. The fair value is calculated by discounting the remaining obligations by a rate consistent with the credit quality and industry of the company.

(7) Included in the Balance Sheet line: Other long-term obligations. Includes contingent consideration related to a prior year acquisition where fair value is based on expected drilling activities and discount rates.

14

At June 30, 2024 and December 31, 2023, respectively, the Corporation had $675 million and $800 million of collateral under master netting arrangements not offset against the derivatives on the Condensed Consolidated Balance Sheet, primarily related to initial margin requirements.

The Corporation may use non-derivative financial instruments, such as its foreign currency-denominated debt, as hedges of its net investments in certain foreign subsidiaries. Under this method, the change in the carrying value of the financial instruments due to foreign exchange fluctuations is reported in accumulated other comprehensive income. As of June 30, 2024, the Corporation has designated $3.2 billion of its Euro-denominated debt and related accrued interest as a net investment hedge of its European business. The net investment hedge is deemed to be perfectly effective.

The Corporation had undrawn short-term committed lines of credit of $237 million and undrawn long-term committed lines of credit of $1,795 million as of second quarter 2024.

Derivative Instruments

The Corporation’s size, strong capital structure, geographic diversity, and the complementary nature of its business segments reduce the Corporation’s enterprise-wide risk from changes in commodity prices, currency rates and interest rates. In addition, the Corporation uses commodity-based contracts, including derivatives, to manage commodity price risk and to generate returns from trading. Commodity contracts held for trading purposes are presented in the Condensed Consolidated Statement of Income on a net basis in the line “Sales and other operating revenue" and in the Consolidated Statement of Cash Flows in “Cash Flows from Operating Activities”. The Corporation’s commodity derivatives are not accounted for under hedge accounting. At times, the Corporation also enters into currency and interest rate derivatives, none of which are material to the Corporation’s financial position as of June 30, 2024 and December 31, 2023, or results of operations for the periods ended June 30, 2024 and 2023.

Credit risk associated with the Corporation’s derivative position is mitigated by several factors, including the use of derivative clearing exchanges and the quality of and financial limits placed on derivative counterparties. The Corporation maintains a system of controls that includes the authorization, reporting, and monitoring of derivative activity.

The net notional long/(short) position of derivative instruments at June 30, 2024 and December 31, 2023, was as follows:

(millions)

June 30, 2024

December 31, 2023

Crude oil (barrels)

6

(7)

Petroleum products (barrels)

(44)

(43)

Natural gas (MMBTUs)

(568)

(560)

Realized and unrealized gains/(losses) on derivative instruments that were recognized in the Condensed Consolidated Statement of Income are included in the following lines on a before-tax basis:

(millions of dollars)

Three Months Ended June 30,

Six Months Ended June 30,

2024

2023

2024

2023

Sales and other operating revenue

(103)

332

(895)

983

Crude oil and product purchases

(5)

5

(2)

(20)

Total

(108)

337

(897)

963

15

Note 8. Disclosures about Segments and Related Information

(millions of dollars)

Three Months Ended June 30,

Six Months Ended June 30,

2024

2023

2024

2023

Earnings (Loss) After Income Tax

Upstream

United States

2,430

920

3,484

2,552

Non-U.S.

4,644

3,657

9,250

8,482

Energy Products

United States

450

1,528

1,286

3,438

Non-U.S.

496

782

1,036

3,055

Chemical Products

United States

526

486

1,030

810

Non-U.S.

253

342

534

389

Specialty Products

United States

447

373

851

824

Non-U.S.

304

298

661

621

Corporate and Financing

(310)

(506)

(672)

(861)

Corporate total

9,240

7,880

17,460

19,310

Sales and Other Operating Revenue

Upstream

United States

6,729

1,673

8,919

4,443

Non-U.S.

3,317

3,739

6,843

9,126

Energy Products

United States

26,415

26,128

51,218

51,052

Non-U.S.

43,014

38,945

82,423

78,921

Chemical Products

United States

2,213

1,992

4,407

4,021

Non-U.S.

3,620

3,678

7,266

7,370

Specialty Products

United States

1,538

1,542

3,007

3,110

Non-U.S.

3,115

3,095

6,265

6,384

Corporate and Financing

25

3

49

12

Corporate total

89,986

80,795

170,397

164,439

Intersegment Revenue

Upstream

United States

5,545

5,044

11,533

10,000

Non-U.S.

11,043

8,412

21,023

17,811

Energy Products

United States

6,537

5,074

13,095

10,525

Non-U.S.

6,395

6,988

13,147

13,957

Chemical Products

United States

1,950

2,084

3,815

3,872

Non-U.S.

998

977

2,023

1,754

Specialty Products

United States

634

684

1,289

1,364

Non-U.S.

151

169

315

268

Corporate and Financing

71

64

150

128

16

Geographic Sales and Other Operating Revenue

(millions of dollars)

Three Months Ended June 30,

Six Months Ended June 30,

2024

2023

2024

2023

United States

36,895

31,335

67,551

62,626

Non-U.S.

53,091

49,460

102,846

101,813

Total

89,986

80,795

170,397

164,439

Significant Non-U.S. revenue sources include: (1)

Canada

8,126

6,825

15,182

13,546

United Kingdom

5,036

5,242

10,196

12,253

Singapore

3,985

3,758

8,003

7,489

France

3,512

3,494

6,985

6,978

Australia

2,450

2,392

4,875

4,820

Germany

2,448

2,256

4,795

4,549

Belgium

2,302

2,410

4,709

5,059

(1)Revenue is determined by primary country of operations. Excludes certain sales and other operating revenues in non-U.S. operations where attribution to a specific country is not practicable.

Revenue from Contracts with Customers

Sales and other operating revenue include both revenue within the scope of ASC 606 and outside the scope of ASC 606. Trade receivables in Notes and accounts receivable – net reported on the Balance Sheet also includes both receivables within the scope of ASC 606 and those outside the scope of ASC 606. Revenue and receivables outside the scope of ASC 606 primarily relate to physically settled commodity contracts accounted for as derivatives. Contractual terms, credit quality, and type of customer are generally similar between those revenues and receivables within the scope of ASC 606 and those outside it.

Sales and other operating revenue

(millions of dollars)

Three Months Ended June 30,

Six Months Ended June 30,

2024

2023

2024

2023

Revenue from contracts with customers

64,181

63,322

122,600

127,626

Revenue outside the scope of ASC 606

25,805

17,473

47,797

36,813

Total

89,986

80,795

170,397

164,439

17

Note 9. Divestment Activities

Through June 30, 2024, the Corporation realized proceeds of approximately $1.6 billion and net after-tax earnings of $0.4 billion from its divestment activities. This included the sale of the Santa Ynez Unit and associated facilities in California, certain conventional and unconventional assets in the United States, as well as other smaller divestments.

In 2023, the Corporation realized proceeds of approximately $4.1 billion and recognized net after-tax earnings of approximately $0.6 billion from its divestment activities. This included the sale of the Aera Energy joint venture, Esso Thailand Ltd., the Billings Refinery, certain unconventional assets in the United States, as well as other smaller divestments.

In February 2022, the Corporation signed an agreement with Seplat Energy Offshore Limited for the sale of Mobil Producing Nigeria Unlimited. The agreement is subject to certain conditions precedent and government approvals. In mid-2022, a Nigerian court issued an order to halt transition activities and enter into arbitration with the Nigerian National Petroleum Company. In June 2024, the court order was lifted and arbitration suspended. The closing date and any loss on sale will depend on resolution of the conditions precedent and government approvals.

18

ITEM 2. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Overview

Second quarter crude prices were essentially unchanged versus the first quarter, near the middle of the 10-year historical range (2010-2019), as the market remains relatively balanced. Natural gas prices declined due to lower demand from milder weather, though remained toward the middle of the 10-year range. Industry refining margins declined from the top of the 10-year range to the lower half of the range, as increased supply more than met record global demand in the second quarter. Chemical margins showed a slight improvement compared to the first quarter of 2024, although margins remained at bottom-of-cycle conditions and well below the 10-year range, as capacity additions outpaced demand growth.

Recent Mergers and Acquisitions

On May 3, 2024, ExxonMobil acquired Pioneer Natural Resources Company (Pioneer), an independent oil and gas exploration and production company. See "Note 2. Pioneer Natural Resources Merger" of the Condensed Consolidated Financial Statements for additional information.

Selected Earnings Factor Definitions

The updated earnings factors introduced in the first quarter 2024 provide additional visibility into drivers of our business results. The company evaluates these factors periodically to determine if any enhancements may provide helpful insights to the market. Listed below are descriptions of the earnings factors:

Advantaged Volume Growth. Earnings impacts from change in volume/mix from advantaged assets, strategic projects, and high-value products.

•Advantaged Assets (Advantaged growth projects). Includes Permian (heritage Permian (1) and Pioneer), Guyana, Brazil, and LNG.

•Strategic Projects. Includes (i) the following completed projects: Rotterdam Hydrocracker, Corpus Christi Chemical Complex, Baton Rouge Polypropylene, Beaumont Crude Expansion, Baytown Chemical Expansion, Permian Crude Venture, and the 2022 Baytown advanced recycling facility; and (ii) the following projects still to be completed: Fawley Hydrofiner, China Chemical Complex, Singapore Resid Upgrade, Strathcona Renewable Diesel, ProxximaTM Venture, USGC Reconfiguration, additional advanced recycling projects under evaluation worldwide, and additional projects in plan yet to be publicly announced.

•High-Value Products. Includes performance products and lower-emission fuels. Performance products (performance chemicals, performance lubricants) refers to products that provide differentiated performance for multiple applications through enhanced properties versus commodity alternatives and bring significant additional value to customers and end-users. Lower-emission fuels refers to fuels with lower life cycle emissions than conventional transportation fuels for gasoline, diesel and jet transport.

Base Volume. Includes all volume/mix factors not included in Advantaged Volume Growth defined above.

Structural Cost Savings. After-tax earnings effect of Structural Cost Savings as defined on page 21, including cash operating expenses related to divestments that were previously in the "volume/mix" factor.

Expenses. Includes all expenses otherwise not included in other earnings factors.

Timing Effects. Timing effects are primarily related to unsettled derivatives (mark-to-market) and other earnings impacts driven by timing differences between the settlement of derivatives and their offsetting physical commodity realizations (due to LIFO inventory accounting).

(1)Heritage Permian basin assets exclude assets acquired as part of the acquisition of Pioneer that closed May 3, 2024.

19

Earnings (loss) excluding Identified Items

Earnings (loss) excluding Identified Items (non-GAAP) are earnings (loss) excluding individually significant non-operational events with, typically, an absolute corporate total earnings impact of at least $250 million in a given quarter. The earnings (loss) impact of an Identified Item for an individual segment in a given quarter may be less than $250 million when the item impacts several periods or several segments. Earnings (loss) excluding identified items does include non-operational earnings events or impacts that are generally below the $250 million threshold utilized for Identified Items. Management uses these figures to improve comparability of the underlying business across multiple periods by isolating and removing significant non-operational events from business results. The Corporation believes this view provides investors increased transparency into business results and trends and provides investors with a view of the business as seen through the eyes of management. Earnings (loss) excluding Identified Items is not meant to be viewed in isolation or as a substitute for net income (loss) attributable to ExxonMobil as prepared in accordance with U.S. GAAP.

References in this discussion to Corporate earnings (loss) mean net income (loss) attributable to ExxonMobil (U.S. GAAP) from the Condensed Consolidated Statement of Income. Unless otherwise indicated, references to earnings (loss); Upstream, Energy Products, Chemical Products, Specialty Products, and Corporate and Financing earnings (loss); and earnings (loss) per share are ExxonMobil's share after excluding amounts attributable to noncontrolling interests.

Due to rounding, numbers presented may not add up precisely to the totals indicated.

20

Structural Cost Savings

Structural Cost Savings describes decreases in cash opex excluding energy and production taxes as a result of operational efficiencies, workforce reductions, divestment-related reductions, and other cost-savings measures that are expected to be sustainable compared to 2019 levels. Relative to 2019, estimated cumulative Structural Cost Savings totaled $10.7 billion, which included an additional $1.0 billion in the first six months of 2024. The total change between periods in expenses below will reflect both Structural Cost Savings and other changes in spend, including market factors, such as inflation and foreign exchange impacts, as well as changes in activity levels and costs associated with new operations, mergers and acquisitions, new business venture development, and early-stage projects. Estimates of cumulative annual structural savings may be revised depending on whether cost reductions realized in prior periods are determined to be sustainable compared to 2019 levels. Structural Cost Savings are stewarded internally to support management's oversight of spending over time. This measure is useful for investors to understand the Corporation's efforts to optimize spending through disciplined expense management.

Dollars in billions (unless otherwise noted)

Twelve Months Ended December 31,

Six Months Ended June 30,

2019

2023

2023

2024

Components of Operating Costs

From ExxonMobil’s Consolidated Statement of Income (U.S. GAAP)

Production and manufacturing expenses

36.8

36.9

18.3

18.9

Selling, general and administrative expenses

11.4

9.9

4.8

5.1

Depreciation and depletion (includes impairments)

19.0

20.6

8.5

10.6

Exploration expenses, including dry holes

1.3

0.8

0.3

0.3

Non-service pension and postretirement benefit expense

1.2

0.7

0.3

0.1

Subtotal

69.7

68.9

32.2

34.9

ExxonMobil’s share of equity company expenses (non-GAAP)

9.1

10.5

5.0

4.7

Total Adjusted Operating Costs (non-GAAP)

78.8

79.4

37.2

39.6

Total Adjusted Operating Costs (non-GAAP)

78.8

79.4

37.2

39.6

Less:

Depreciation and depletion (includes impairments)

19.0

20.6

8.5

10.6

Non-service pension and postretirement benefit expense

1.2

0.7

0.3

0.1

Other adjustments (includes equity company depreciation and depletion)

3.6

3.7

1.5

1.7

Total Cash Operating Expenses (Cash Opex) (non-GAAP)

55.0

54.4

26.9

27.2

Energy and production taxes (non-GAAP)

11.0

14.9

7.5

6.8

Total Cash Operating Expenses (Cash Opex) excluding Energy and Production Taxes (non-GAAP)

44.0

39.5

19.4

20.4

Change vs 2019

Change vs 2023

Estimated Cumulative vs 2019

Total Cash Operating Expenses (Cash Opex) excluding Energy and Production Taxes (non-GAAP)

-4.5

+1.0

Market

+3.6

+0.2

Activity/Other

+1.6

+1.8

Structural Cost Savings

-9.7

-1.0

-10.7

Due to rounding, numbers presented may not add up precisely to the totals indicated.

21

REVIEW OF SECOND QUARTER 2024 RESULTS

ExxonMobil’s second quarter 2024 earnings were $9.2 billion, or $2.14 per share assuming dilution, compared with earnings of $7.9 billion a year earlier. The increase in earnings was mainly driven by improved realizations and increased volumes for advantaged Upstream investments in the Permian and Guyana, partially offset by weaker industry refining margins and higher scheduled maintenance. Capital and exploration expenditures were $7.0 billion, up $0.9 billion from second quarter 2023.

Earnings for the first six months of 2024 were $17.5 billion, or $4.20 per diluted share, compared with $19.3 billion a year earlier. Capital and exploration expenditures were $12.9 billion, up $0.3 billion from the first six months of 2023. The Corporation distributed $8.1 billion in dividends to shareholders and repurchased $8.3 billion of common stock.

(1) Refer to page 20 for definition of Identified Items and earnings (loss) excluding Identified Items.

22

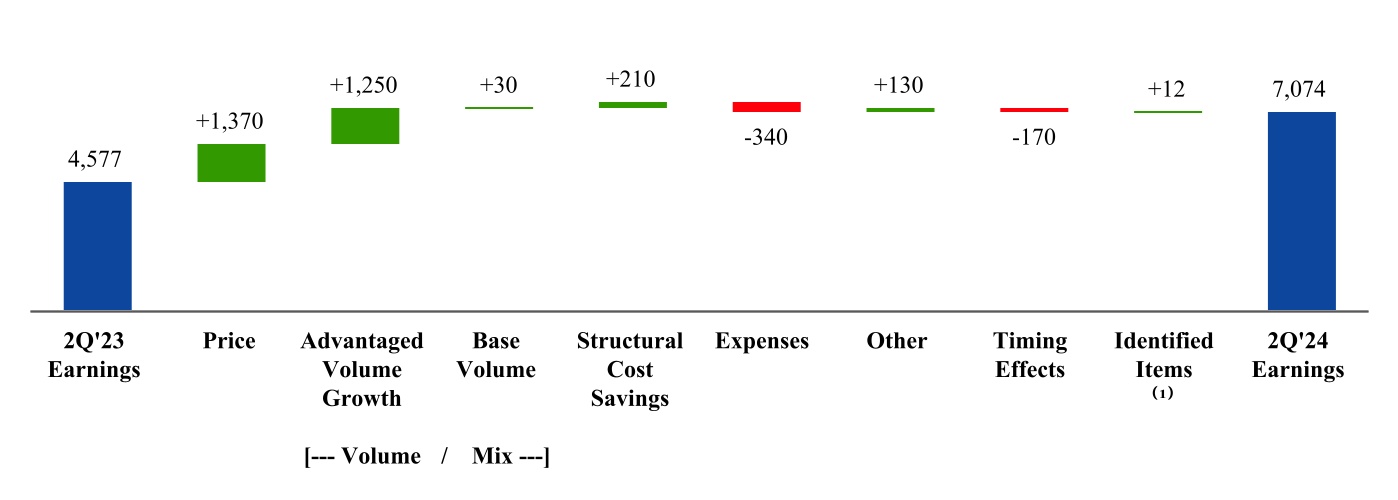

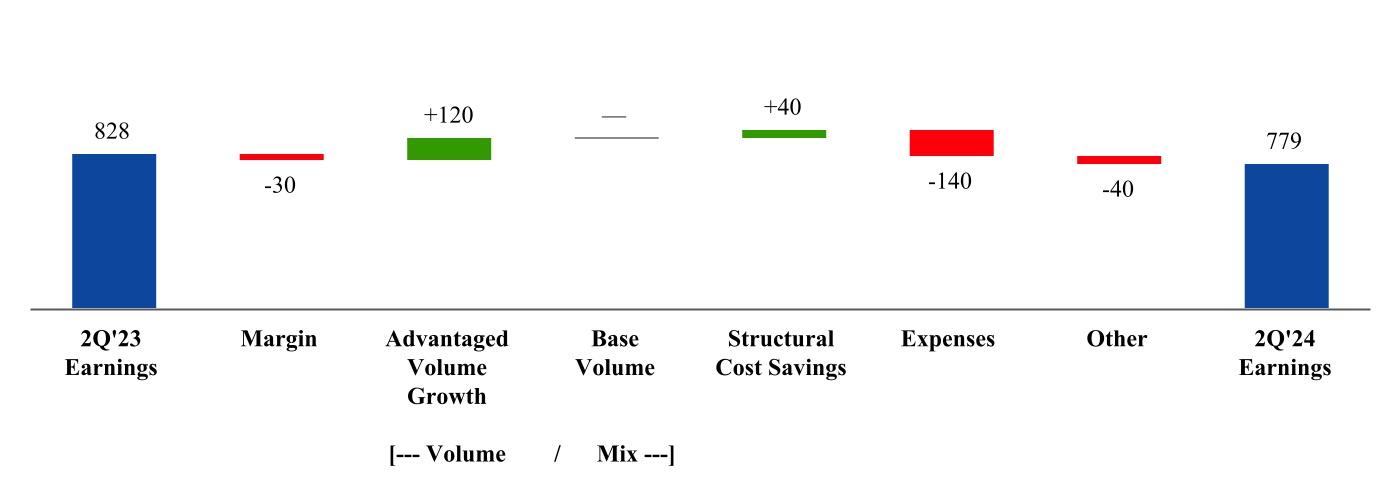

Upstream Second Quarter Earnings Factor Analysis

(millions of dollars)

Price– Price impacts increased earnings by $1,370 million, driven by an increase in liquids realizations, partly offset by a decrease in natural gas realizations.

Advantaged Volume Growth – Higher volumes from advantaged assets increased earnings by $1,250 million, driven by record production from Guyana, growth in heritage Permian (2), and the Pioneer acquisition.

Base Volume – Higher base volumes increased earnings by $30 million.

Structural Cost Savings – Increased earnings by $210 million.

Expenses – Higher expenses decreased earnings by $340 million, primarily from depreciation.

Other – All other items increased earnings by $130 million, driven by favorable impacts from divestments, partly offset by Pioneer-related transaction costs.

Timing Effects – Less favorable timing effects from derivatives mark-to-market impacts decreased earnings by $170 million.

Identified Items (1) –2Q2023 $(12) million loss driven by additional European taxes.

(1) Refer to page 20 for definition of Identified Items and earnings (loss) excluding Identified Items.

(2) Heritage Permian basin assets exclude assets acquired as part of the acquisition of Pioneer that closed May 3, 2024.

23

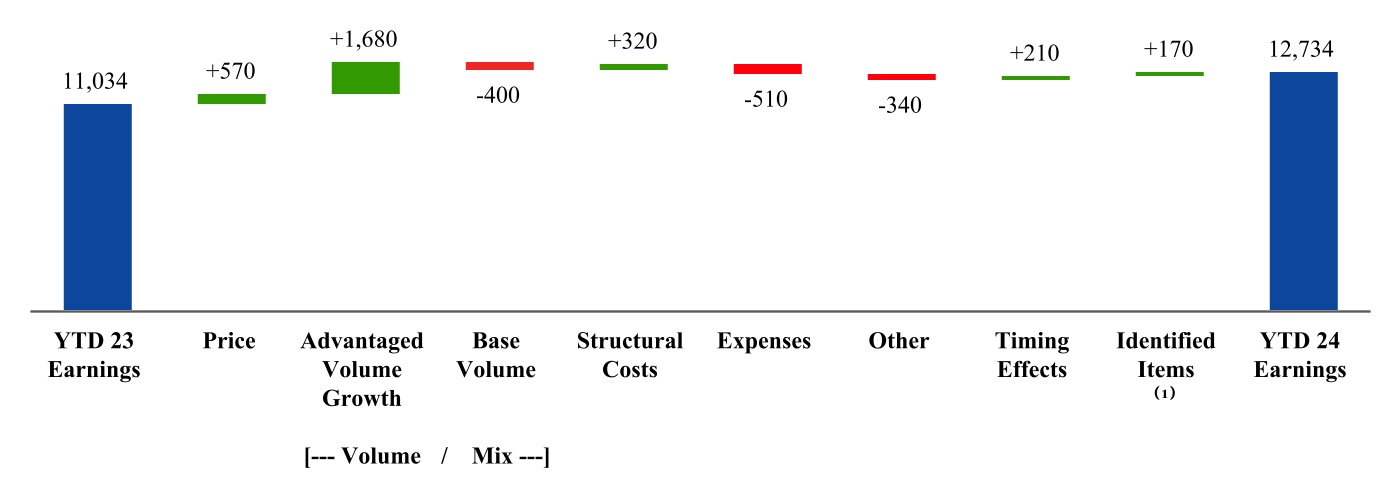

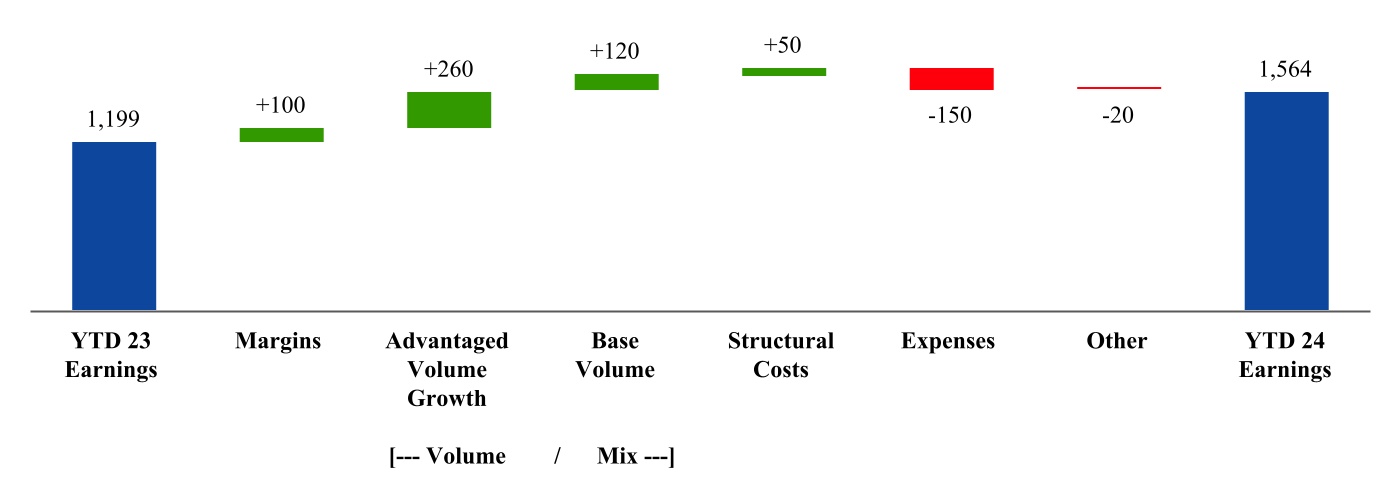

Upstream Year-to-Date Earnings Factor Analysis

(millions of dollars)

Price– Price impacts increased earnings by $570 million, driven by an increase in average realizations for crude oil, partially offset by a decrease in average natural gas realizations.

Advantaged Volume Growth – Higher volumes from advantaged assets increased earnings by $1,680 million, driven by record production from Guyana, growth in heritage Permian (2), and the Pioneer acquisition.

Base Volume – Lower base volumes decreased earnings by $400 million, mainly driven by divestments and government-mandated curtailments.

Structural Cost Savings – Increased earnings by $320 million, due to operational efficiencies and divestments.

Expenses – Higher expenses decreased earnings by $510 million, primarily from depreciation.

Other – All other items, including costs related to the Pioneer transaction, decreased earnings by $340 million.

Timing Effects – Less unfavorable timing effects from derivatives mark-to-market impacts increased earnings by $210 million.

Identified Items (1) –2023 $(170) million loss driven by additional European taxes.

(1) Refer to page 20 for definition of Identified Items and earnings (loss) excluding Identified Items.

(2) Heritage Permian basin assets exclude assets acquired as part of the acquisition of Pioneer that closed May 3, 2024.

24

Upstream Operational Results

Three Months Ended June 30,

Six Months Ended June 30,

2024

2023

2024

2023

Net production of crude oil, natural gas liquids, bitumen and synthetic oil

(thousands of barrels daily)

United States

1,261

785

1,038

802

Canada/Other Americas

760

618

767

645

Europe

4

4

4

4

Africa

215

206

220

213

Asia

714

702

712

725

Australia/Oceania

30

38

30

35

Worldwide

2,984

2,353

2,771

2,424

Net natural gas production available for sale

(millions of cubic feet daily)

United States

2,900

2,346

2,570

2,357

Canada/Other Americas

114

97

104

94

Europe

331

375

354

461

Africa

167

86

158

110

Asia

3,486

3,350

3,380

3,473

Australia/Oceania

1,245

1,275

1,236

1,276

Worldwide

8,243

7,529

7,802

7,771

Oil-equivalent production (1)

(thousands of oil-equivalent barrels daily)

4,358

3,608

4,071

3,719

(1) Natural gas is converted to an oil-equivalent basis at six million cubic feet per one thousand barrels.

(1) Natural gas is converted to an oil-equivalent basis at six million cubic feet per one thousand barrels.

2Q 2024

versus

2Q 2023

2Q 2024 production of 4.4 million oil-equivalent barrels per day increased 750 thousand oil-equivalent barrels per day from 2Q 2023, driven by the Pioneer acquisition and record production in Guyana and heritage Permian (1).

YTD 2024

versus

YTD 2023

4.1 million oil-equivalent barrels per day in 2024 increased 352 thousand oil-equivalent barrels per day from 2023, driven by the Pioneer acquisition and record production in Guyana and heritage Permian (1).

(1) Heritage Permian basin assets exclude assets acquired as part of the acquisition of Pioneer that closed May 3, 2024.

Listed below are descriptions of ExxonMobil’s volumes reconciliation factors which are provided to facilitate understanding of the terms.

Entitlements - Net Interest are changes to ExxonMobil’s share of production volumes caused by non-operational changes to volume-determining factors. These factors consist of net interest changes specified in Production Sharing Contracts (PSCs), which typically occur when cumulative investment returns or production volumes achieve defined thresholds, changes in equity upon achieving pay-out in partner investment carry situations, equity redeterminations as specified in venture agreements, or as a result of the termination or expiry of a concession. Once a net interest change has occurred, it typically will not be reversed by subsequent events, such as lower crude oil prices.

Entitlements - Price, Spend and Other are changes to ExxonMobil’s share of production volumes resulting from temporary changes to non-operational volume-determining factors. These factors include changes in oil and gas prices or spending levels from one period to another. According to the terms of contractual arrangements or government royalty regimes, price or spending variability can increase or decrease royalty burdens and/or volumes attributable to ExxonMobil. For example, at higher prices, fewer barrels are required for ExxonMobil to recover its costs. These effects generally vary from period to period with field spending patterns or market prices for oil and natural gas. Such factors can also include other temporary changes in net interest as dictated by specific provisions in production agreements.

Government Mandates are changes to ExxonMobil's sustainable production levels as a result of production limits or sanctions imposed by governments.

Divestments are reductions in ExxonMobil’s production arising from commercial arrangements to fully or partially reduce equity in a field or asset in exchange for financial or other economic consideration.

Growth and Other comprise all other operational and non-operational factors not covered by the above definitions that may affect volumes attributable to ExxonMobil. Such factors include, but are not limited to, production enhancements from project and work program activities, acquisitions including additions from asset exchanges, downtime, market demand, natural field decline, and any fiscal or commercial terms that do not affect entitlements.

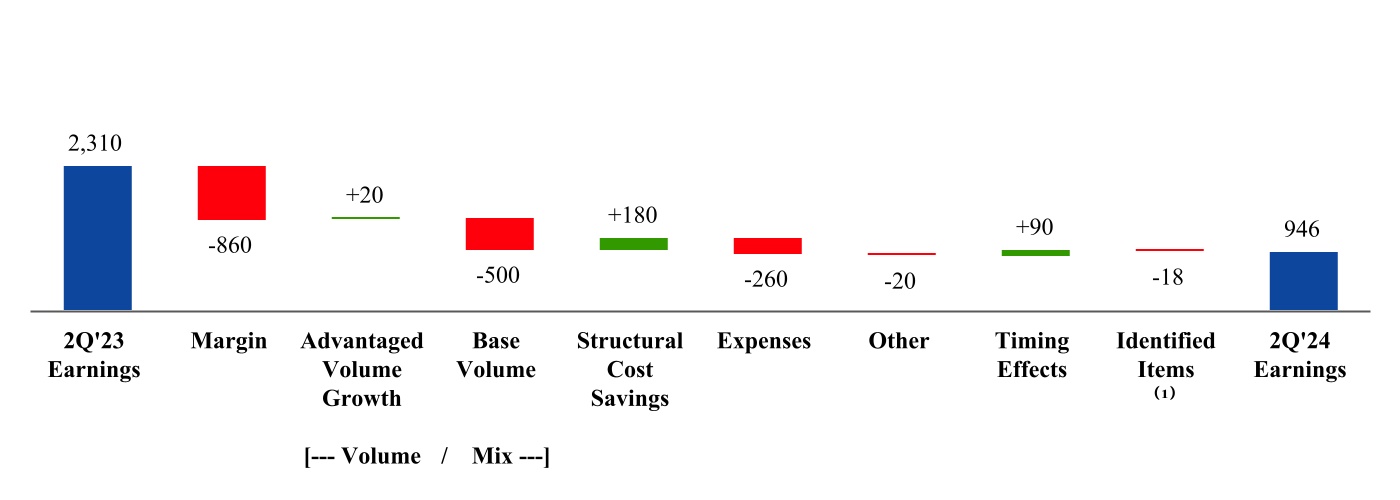

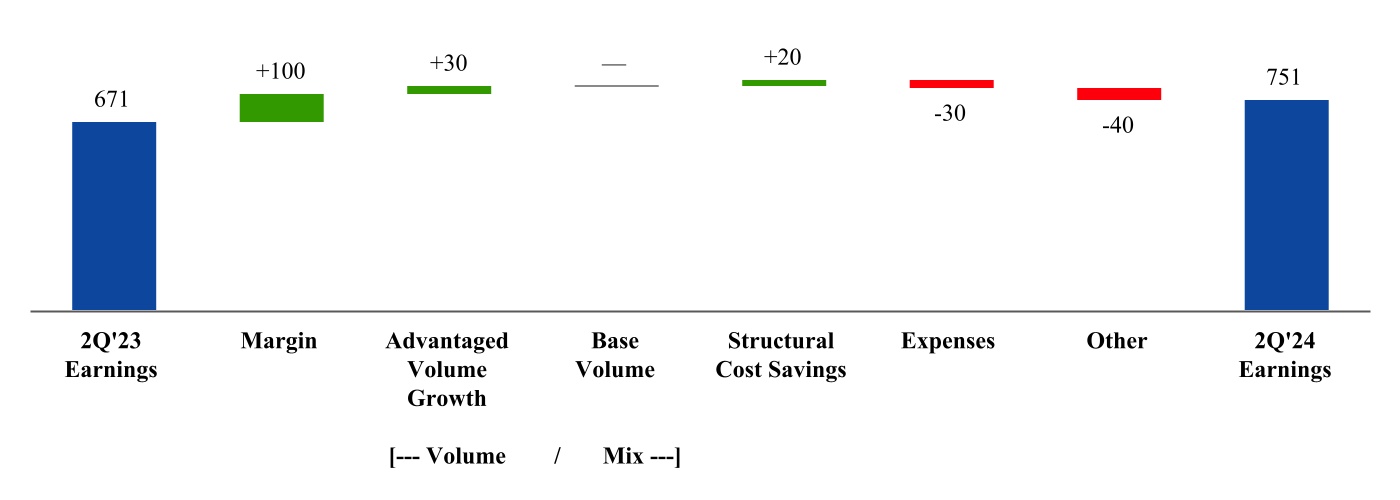

Energy Products Second Quarter Earnings Factor Analysis

(millions of dollars)

Margin – Margins decreased earnings by $860 million, driven by weaker industry refining margins.

Advantaged Volume Growth – Higher volumes from strategic projects increased earnings by $20 million.

Base Volume – Lower base volumes decreased earnings by $500 million, driven by higher scheduled maintenance and divestments.

Structural Cost Savings– Increased earnings by $180 million.

Expenses– Higher expenses decreased earnings by $260 million from higher planned maintenance and turnaround activity.

Other – All other items decreased earnings by $20 million.

Timing Effects – Favorable timing effects from derivatives mark-to-market impacts increased earnings by $90 million.

Identified Items (1) – 2Q 2023 $18 million gain related to European taxes.

(1)Refer to page 20 for definition of Identified Items and earnings (loss) excluding Identified Items.

27

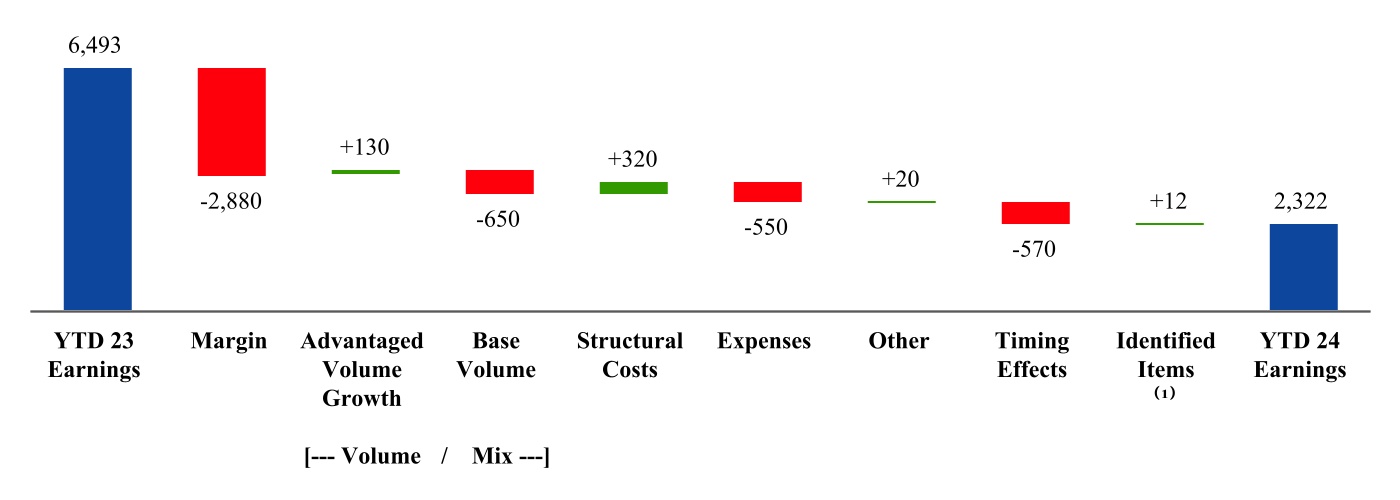

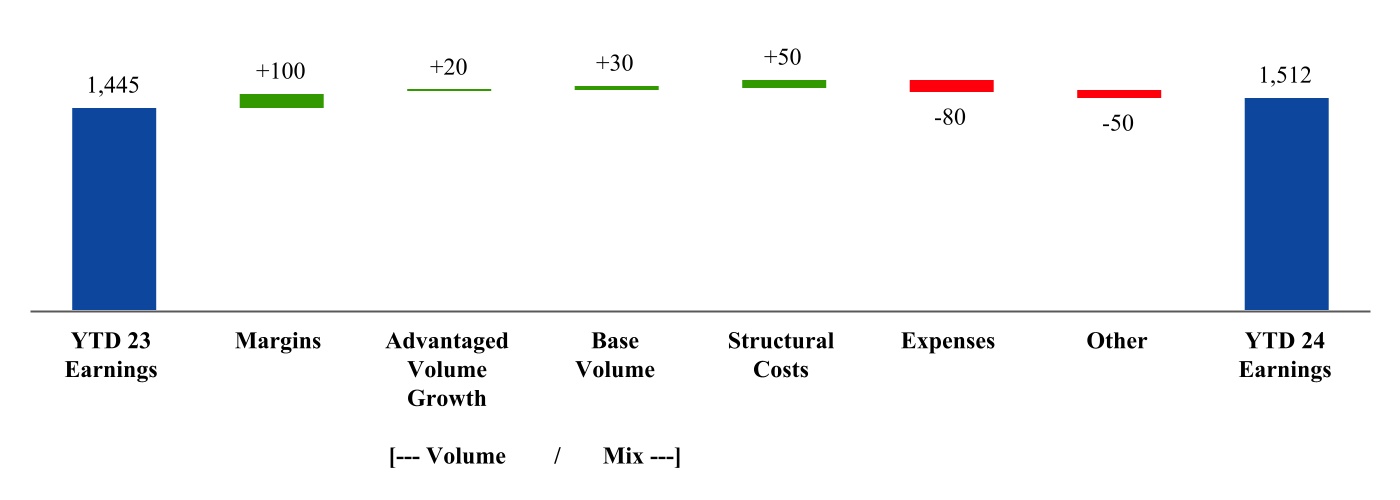

Energy Products Year-to-Date Earnings Factor Analysis

(millions of dollars)

Margins– Margins decreased earnings by $2,880 million, driven by significantly weaker industry refining margins, which normalized from the historically high levels in early 2023.

Advantaged Volume Growth – Higher volumes from the Beaumont refinery expansion increased earnings by $130 million.

Base Volume – Lower base volumes from divestments and higher scheduled maintenance decreased earnings by $650 million.

Structural Cost Savings– Increased earnings by $320 million due primarily to divestments and maintenance related efficiencies.

Expenses– Higher expenses decreased earnings by $550 million, driven by increased turnaround and higher planned maintenance activity.

Other – All other items increased earnings by $20 million.

Timing Effects – Unfavorable timing effects mainly from derivatives mark-to-market impacts decreased earnings by $570 million.

Identified Items (1) – 2023 $(12) million loss from additional European taxes.

(1) Refer to page 20 for definition of Identified Items and earnings (loss) excluding Identified Items.

28

Energy Products Operational Results

(thousands of barrels daily)

Three Months Ended June 30,

Six Months Ended June 30,

2024

2023

2024

2023

Refinery throughput

United States

1,746

1,944

1,823

1,794

Canada

387

388

397

403

Europe

987

1,209

970

1,199

Asia Pacific

446

463

424

514

Other

174

169

177

176

Worldwide

3,740

4,173

3,791

4,086

Energy Products sales(1)

United States

2,639

2,743

2,607

2,601

Non-U.S.

2,681

2,916

2,669

2,867

Worldwide

5,320

5,658

5,276

5,469

Gasoline, naphthas

2,243

2,401

2,210

2,290

Heating oils, kerosene, diesel

1,718

1,842

1,730

1,806

Aviation fuels

344

344

342

328

Heavy fuels

181

228

197

221

Other energy products

834

844

797

823

(1) Data reported net of purchases/sales contracts with the same counterparty.

Due to rounding, numbers presented may not add up precisely to the totals indicated.

Structural Cost Savings– Increased earnings by $40 million.

Expenses– Higher expenses, including increased project and maintenance costs, decreased earnings by $140 million.

Other – All other items decreased earnings by $40 million.

30

Chemical Products Year-to-Date Earnings Factor Analysis

(millions of dollars)

Margins– Despite weaker global industry margins, overall margins increased earnings by $100 million, driven by North American feed advantage, lower energy costs, and stronger high-value product margins.

Advantaged Volume Growth – Growth in high-value product sales increased earnings by $260 million.

Base Volume – Higher base volumes increased earnings by $120 million, driven by modest demand growth and lower turnaround impacts.

Structural Cost Savings– Increased earnings by $50 million, primarily from operational efficiencies.

Expenses– Higher growth projects spend and maintenance decreased earnings by $150 million.

Other – All other items decreased earnings by $20 million.

Chemical Products Operational Results

(thousands of metric tons)

Three Months Ended June 30,

Six Months Ended June 30,

2024

2023

2024

2023

Chemical Products sales (1)

United States

1,802

1,725

3,649

3,286

Non-U.S.

3,071

3,124

6,278

6,212

Worldwide

4,873

4,849

9,927

9,498

(1) Data reported net of purchases/sales contracts with the same counterparty.

(1) Refer to page 20 for definition of Identified Items and earnings (loss) excluding Identified Items.

Corporate and Financing expenses were $310 million for the second quarter of 2024, $196 million lower than the second quarter of 2023, mainly due to lower financing costs.

Corporate and Financing expenses were $672 million for the first six months of 2024, $189 million lower than 2023, mainlydue to lower financing costs, partially offset by Pioneer-related costs.

34

LIQUIDITY AND CAPITAL RESOURCES

(millions of dollars)

Three Months Ended June 30,

Six Months Ended June 30,

2024

2023

2024

2023

Net cash provided by/(used in)

Operating activities

25,224

25,724

Investing activities

(9,446)

(9,281)

Financing activities

(20,540)

(16,683)

Effect of exchange rate changes

(318)

132

Increase/(decrease) in cash and cash equivalents

(5,080)

(108)

Cash and cash equivalents (at end of period)

26,488

29,557

Cash flow from operations and asset sales

Net cash provided by operating activities (U.S. GAAP)

10,560

9,383

25,224

25,724

Proceeds associated with sales of subsidiaries, property, plant & equipment, and sales and returns of investments

926

1,287

1,629

2,141

Cash flow from operations and asset sales (Non-GAAP)

11,486

10,670

26,853

27,865

Because of the ongoing nature of our asset management and divestment program, we believe it is useful for investors to consider proceeds associated with asset sales together with cash provided by operating activities when evaluating cash available for investment in the business and financing activities, including shareholder distributions.

Cash flow from operations and asset sales in the second quarter of 2024 was $11.5 billion, an increase of $0.8 billion from the comparable 2023 period primarily reflectinghigherearnings.

Cash provided by operating activities totaled $25.2 billion for the first six months of 2024, $0.5 billion lower than 2023. Net income including noncontrolling interests was $18.1 billion, a decrease of $1.9 billion from the prior year period. The adjustment for the noncash provision of $10.6 billion for depreciation and depletion was up $2.1 billion from 2023. Changes in operational working capital were a reduction of $2.6 billion during the period. All other items net decreased cash flows by $0.9 billion in 2024 versus a contribution of $1.1 billion in 2023. See the Condensed Consolidated Statement of Cash Flows for additional details.

Investing activities for the first six months of 2024 used net cash of $9.4 billion, an increase of $0.2 billion compared to the prior year. Spending for additions to property, plant and equipment of $11.3 billion was $0.5 billion higher than 2023. Proceeds from asset sales were $1.6 billion, a decrease of $0.5 billion compared to the prior year. Net investments and advances decreased $0.1 billion from $0.7 billion in 2023. Cash acquired from mergers and acquistions during the first six months of 2024 was $0.8 billion.

Net cash used in financing activities was $20.5 billion in the first six months of 2024, including $8.3 billion for the purchase of 72.1 million shares of ExxonMobil stock, as part of the previously announced buyback program, and $1.3 billion to repay Pioneer convertible debt. This compares to net cash used in financing activities of $16.7 billion in the prior year. Total debt at the end of the second quarter of 2024 was $43.2 billion compared to $41.6 billion at year-end 2023. The Corporation's debt to total capital ratio was 13.5 percent at the end of the second quarter of 2024 compared to 16.4 percent at year-end 2023. The net debt to capital ratio (1) was 5.7 percent at the end of the second quarter, an increase of 1.2 percentage points from year-end 2023. The Corporation's capital allocation priorities are investing in competitively advantaged, high-return projects; maintaining a strong balance sheet; and sharing our success with our shareholders through more consistent share repurchases and a growing dividend. The Corporation distributed a total of $8.1 billion to shareholders in the first six months of 2024 through dividends.

The Corporation has access to significant capacity of long-term and short-term liquidity. Internally generated funds are expected to cover the majority of financial requirements, supplemented by long-term and short-term debt. The Corporation had undrawn short-term committed lines of credit of $0.2 billion and undrawn long-term committed lines of credit of $1.8 billion as of second quarter 2024.

The Corporation, as part of its ongoing asset management program, continues to evaluate its mix of assets for potential upgrade. Because of the ongoing nature of this program, dispositions will continue to be made from time to time which will result in either gains or losses. Additionally, the Corporation continues to evaluate opportunities to enhance its business portfolio through acquisitions of assets or companies, and enters into such transactions from time to time. Key criteria for evaluating acquisitions include strategic fit, cost synergies, potential for future growth, low cost of supply, and attractive valuations. Acquisitions may be made with cash, shares of the Corporation’s common stock, or both.

Litigation and other contingencies are discussed in Note 3 to the unaudited condensed consolidated financial statements.

(1) Net debt is total debt of $43.2 billion less $26.5 billion of cash and cash equivalents excluding restricted cash . Net debt to capital ratio is net debt divided by net debt plus total equity of $276.3 billion. Total debt is the sum of notes and loans payable and long-term debt, as reported in the consolidated balance sheet.

35

Contractual Obligations

The Corporation and its affiliates have numerous long-term sales and purchase commitments in their various business activities, all of which are expected to be fulfilled with no adverse consequences material to the Corporation’s operations or financial condition. Through the second quarter of 2024, the Corporation entered into two long-term purchase agreements with an estimated total obligation of approximately $3.0 billion. The Corporation assumed take-or-pay obligations of $4.9 billion associated with the Pioneer acquisition that include long-term purchase, gathering, processing, and transportation commitments.

TAXES

(millions of dollars)

Three Months Ended June 30,

Six Months Ended June 30,

2024

2023

2024

2023

Income taxes

4,094

3,503

7,897

8,463

Effective income tax rate

34

%

33

%

35

%

34

%

Total other taxes and duties (1)

7,531

8,328

14,691

16,423

Total

11,625

11,831

22,588

24,886

(1) Includes “Other taxes and duties” plus taxes that are included in “Production and manufacturing expenses” and “Selling, general and administrative expenses”.

Total taxes were $11.6 billion for the second quarter of 2024, a decrease of $0.2 billion from 2023. Income tax expense was $4.1 billion compared to $3.5 billion in the prior year. The effective income tax rate, which is calculated based on consolidated company income taxes and Exxonmobil's share of equity company income taxes, was 34 percent. This increased from the 33 percent rate in the prior year period due primarily to a change in mix of results in jurisdictions with varying tax rates. Total other taxes and duties decreased by $0.8 billion to $7.5 billion.

Total taxes were $22.6 billion for the first six months of 2024, a decrease of $2.3 billion from 2023. Income tax expense decreased by $0.6 billion to $7.9 billion reflecting lower refining margins. The effective income tax rate of 35 percent was up compared to the prior year period due primarily to a change in mix of results in jurisdictions with varying tax rates. Total other taxes and duties decreased by $1.7 billion to $14.7 billion.

CAPITAL AND EXPLORATION EXPENDITURES

(millions of dollars)

Three Months Ended June 30,

Six Months Ended June 30,

2024

2023

2024

2023

Upstream (including exploration expenses)

5,747

4,609

10,329

9,190

Energy Products

552

731

1,079

1,416

Chemical Products

502

659

935

1,490

Specialty Products

94

103

170

194

Other

144

64

365

256

Total

7,039

6,166

12,878

12,546

Capital and exploration expenditures in the second quarter of 2024 were $7.0 billion, up 14% from the second quarter of 2023.

Capital and exploration expenditures in the first six months of 2024 were $12.9 billion, up 3% from the first six months of 2023. The Corporation anticipates an investment level of approximately $28 billion in 2024. Actual spending could vary depending on the progress of individual projects and property acquisitions.

36

FORWARD-LOOKING STATEMENTS

Statements related to future events; projections; descriptions of strategic, operating, and financial plans and objectives; statements of future ambitions and plans; and other statements of future events or conditions, are forward-looking statements. Similarly, discussion of roadmaps or future plans related to carbon capture, transportation and storage, biofuel, hydrogen, ammonia, direct air capture, and other future plans to reduce emissions and emission intensity of ExxonMobil, its affiliates, and third parties, are dependent on future market factors, such as continued technological progress, policy support and timely rule-making and permitting, and represent forward-looking statements.

Actual future results, including financial and operating performance; potential earnings, cash flow, dividends or shareholder returns, including the timing and amounts of share repurchases; total capital expenditures and mix, including allocations of capital to low carbon investments; realization and maintenance of structural cost reductions and efficiency gains, including the ability to offset inflationary pressure; plans to reduce future emissions and emissions intensity, including ambitions to reach Scope 1 and Scope 2 net zero from operated assets by 2050, to reach Scope 1 and 2 net zero in heritage Upstream Permian Basin (1) unconventional operated assets by 2030 and in Pioneer assets by 2035, to eliminate routine flaring in-line with World Bank Zero Routine Flaring, and to reach near-zero methane emissions from operated assets and other methane initiatives; meeting ExxonMobil’s divestment and start-up plans, and associated project plans as well as technology advances, including the timing and outcome of projects to capture, transport and store CO2, produce hydrogen and ammonia, produce biofuels, produce lithium, create new advanced carbon materials, and use plastic waste as a feedstock for advanced recycling; timely granting of governmental permits and certifications; future debt levels and credit ratings; business and project plans, timing, costs, capacities and profitability; resource recoveries and production rates; and planned Denbury and Pioneer integrated benefits could differ materially due to a number of factors.