•Delivered industry-leading results, earnings of $7.1 billion and cash flow from operations of $11.5 billion1

•Returned industry-leading $9.2 billion to shareholders, on pace to purchase $20 billion in shares this year2

•Repurchased approximately 40% of shares issued to acquire Pioneer Natural Resources since May 2024

•Commenced start-up of Singapore Resid Upgrade, Fawley Hydrofiner and Strathcona Renewable Diesel projects

Results Summary

2Q25

1Q25

Change vs 1Q25

Dollars in millions (except per share data)

YTD 2025

YTD 2024

Change vs YTD 2024

7,082

7,713

-631

Earnings (U.S. GAAP)

14,795

17,460

-2,665

7,082

7,713

-631

Earnings Excluding Identified Items (non-GAAP)

14,795

17,460

-2,665

1.64

1.76

-0.12

Earnings Per Common Share ³

3.40

4.20

-0.80

1.64

1.76

-0.12

Earnings Excluding Identified Items Per Common Share (non-GAAP) ³

3.40

4.20

-0.80

SPRING, Texas – August 1, 2025 – Exxon Mobil Corporation today announced second-quarter 2025 earnings of $7.1 billion, or $1.64 per share assuming dilution. Cash flow from operating activities was $11.5 billion and free cash flow was $5.4 billion. Shareholder distributions totaled $9.2 billion, including $4.3 billion of dividends and $5.0 billion of share repurchases, consistent with the company's announced plans.

“The second quarter, once again, proved the value of our strategy and competitive advantages, which continue to deliver for our shareholders no matter the market conditions or geopolitical developments,” said Darren Woods, ExxonMobil chairman and chief executive officer.

“We achieved our highest second-quarter Upstream production since the merger of Exxon and Mobil more than 25 years ago. It was also our best quarter yet for high-value product sales volumes in Product Solutions. Since 2019, we've delivered $13.5 billion in structural cost savings, more than all other IOCs combined.4 And our 2030 structural cost savings plan exceeds their cumulative cost savings targets.4 We began start-up operations for the first six of ten key projects this year and remain on track to start up the remaining four. Collectively, these projects are expected to improve our earnings power by more than $3 billion in 2026 at constant prices and margins.5 These results demonstrate how our competitive advantages are delivering industry-leading value today and providing a long runway of profitable growth far into the future.”

1 Earnings and cash flow from operations, adjusted for consistency on items reported under U.S. GAAP for the IOCs with actual reported results on or before July 31, 2025, or using reported FactSet consensus as of July 31, 2025. IOCs includes each of BP, Chevron, Shell and TotalEnergies.

2 Shareholder distributions for the IOCs are actuals for companies that reported results on or before July 31, 2025, or estimated using FactSet consensus as of July 31, 2025. IOCs includes each of BP, Chevron, Shell and TotalEnergies.

3 Assuming dilution.

4 IOC structural cost savings reflect reported cost savings as of July 31, 2025. Sourced from IOC disclosures.

5 Earnings contributions are adjusted to 2024 $65/bbl real Brent (assumes annual inflation of 2.5%) and 10-year average Energy, Chemical, and Specialty Product margins, which refer to the average of annual margins from 2010-2019.

1

Year-to-date Earnings Driver Analysis

YE24 Cash (U.S. GAAP) to 2Q25 Cash Flow

Financial Highlights

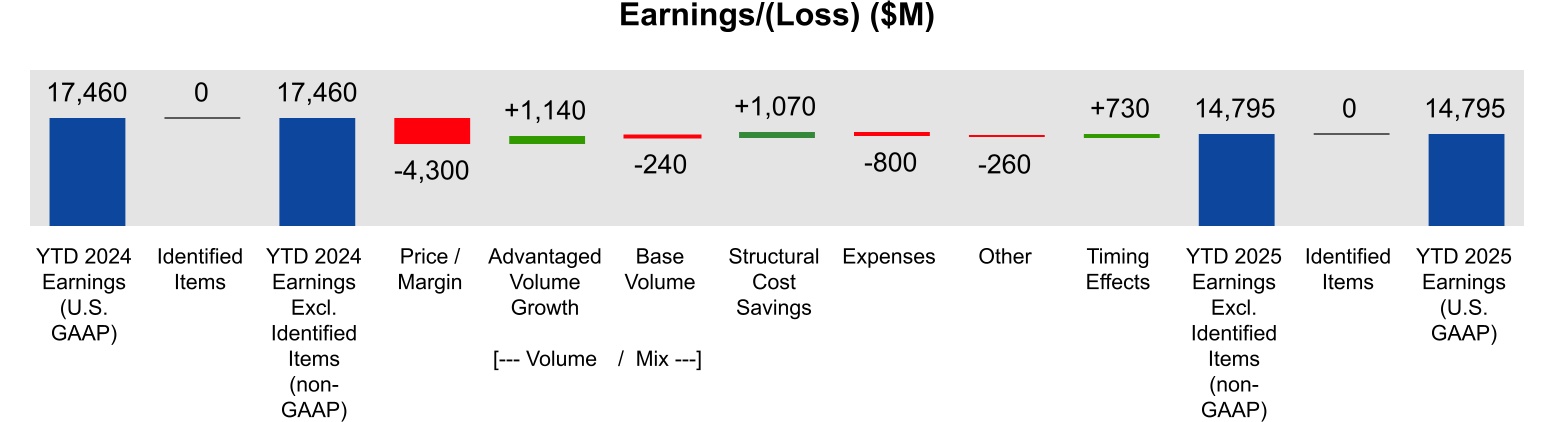

•Year-to-date earnings were $14.8 billion versus $17.5 billion in the first half of 2024. Advantaged volume growth in the Permian and Guyana, additional structural cost savings and favorable timing effects partially offset lower earnings due to weaker crude prices, a decline in industry refining margins, higher depreciation costs and lower base volumes from strategic divestments.

•The company achieved year-to-date Structural Cost Savings of $1.4 billion. Since 2019, the company has delivered $13.5 billion of cumulative Structural Cost Savings, more than all cost savings reported by other IOCs combined. The company expects to deliver $18 billion of cumulative savings through the end of 2030 versus 2019, also exceeding the total targets disclosed by other IOCs.

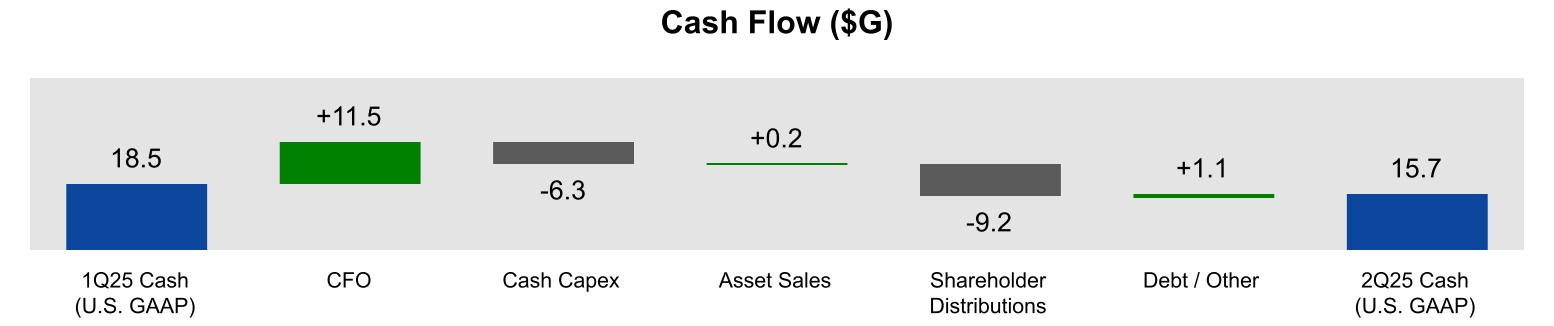

•Generated strong cash flow from operations of $24.5 billion and free cash flow of $14.2 billion in the first half of the year. Industry-leading year-to-date shareholder distributions of $18.4 billion included $8.6 billion of dividends and $9.8 billion of share repurchases, consistent with the company's plan to deliver $20 billion of share repurchases this year. The company has repurchased approximately 40% of shares issued to acquire Pioneer Natural Resources since May of 2024.

•The Corporation declared a third-quarter dividend of $0.99 per share, payable on September 10, 2025, to shareholders of record of Common Stock at the close of business on August 15, 2025.

•The company's industry-leading debt-to-capital and net-debt-to-capital ratio was 13% and 8%, respectively, reflecting debt repayment of $4.7 billion year-to-date. The period-end cash balance was $15.7 billion.1

•Cash capital expenditures were $6.3 billion in the second quarter, bringing year-to-date spending to $12.3 billion. This includes $12.2 billion of additions to property, plant and equipment during the first half of 2025. The company expects full-year cash capital expenditures of $27 billion to $29 billion, consistent with previous guidance.

1 Net debt is total debt of $39.0 billion less $14.4 billion of cash and cash equivalents excluding restricted cash. Net-debt to-capital ratio is net debt divided by the sum of net debt and total equity of $270.0 billion. Period-end cash balance includes cash and cash equivalents including restricted cash. ExxonMobil has lower net debt-to-capital and debt-to-capital than all IOCs. Net debt-to-capital and debt-to-capital are sourced from Bloomberg. Figures are actuals for IOCs that reported results on or before July 31, 2025, or estimated using Bloomberg consensus as of July 31, 2025.

•Upstream year-to-date earnings were $12.2 billion, a decrease of $576 million compared to the first half of 2024. Advantaged assets volume growth in the Permian and Guyana, structural cost savings, favorable foreign exchange, tax impacts and timing effects contributed to earnings. These gains were more than offset by weaker crude realizations and higher depreciation. Year-to-date net production increased 13%, or 520,000 oil-equivalent barrels per day, to 4.6 million oil-equivalent barrels per day driven by the acquisition of Pioneer, partly offset by non-core asset divestments.

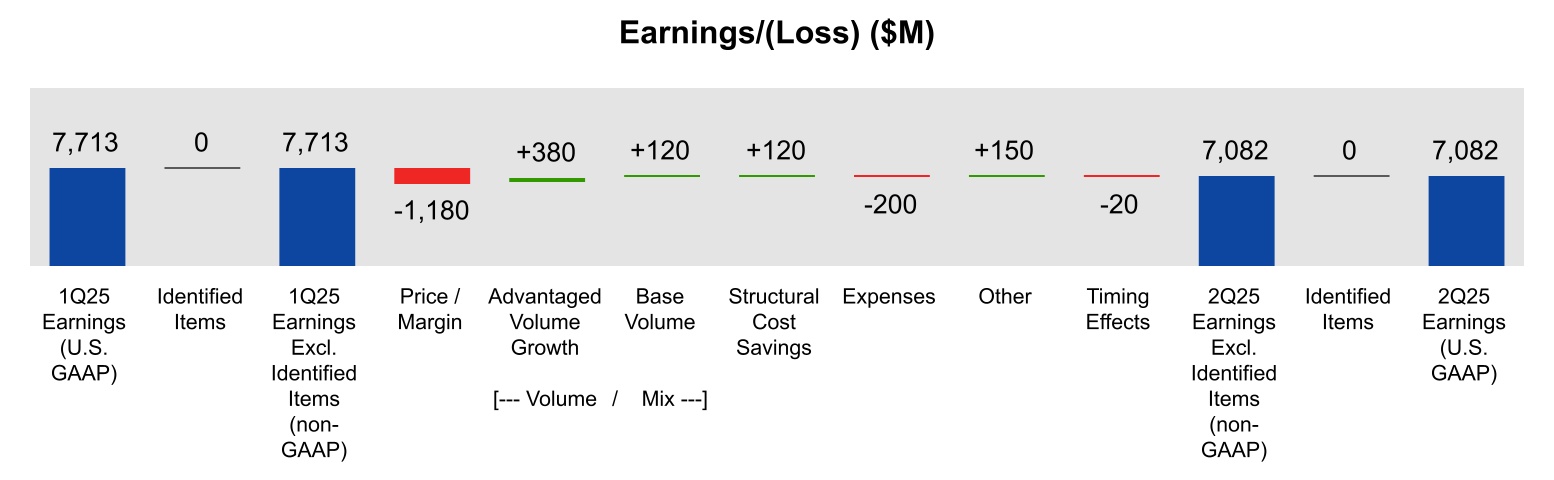

•Second-quarter earnings were $5.4 billion, a decrease of $1.4 billion from the first quarter. Lower crude and natural gas realizations were partially offset by volume growth from advantaged assets, which included record Permian production of 1.6 million oil-equivalent barrels per day, along with structural cost savings. Second-quarter net production was 4.6 million oil-equivalent barrels per day, the highest second-quarter output since the Exxon and Mobil merger more than 25 years ago, and an increase of 79,000 oil-equivalent barrels per day compared to the first quarter.

•Energy Products year-to-date 2025 earnings were $2.2 billion, a decrease of $129 million versus the first half of 2024. Weaker industry refining margins were mostly offset by structural cost savings, lower scheduled maintenance, favorable timing effects and the absence of unfavorable inventory impacts.

•Second-quarter earnings were $1.4 billion, an increase of $539 million from the first quarter driven by stronger industry refining margins from higher seasonal demand and higher volumes from lower scheduled maintenance, partially offset by unfavorable foreign exchange.

•The company recently commenced start-up operations at its Fawley Hydrofiner in the United Kingdom. Once fully operational, the facility will upgrade high-sulfur, lower-value distillates to produce an additional 37,000 barrels per day of ultra-low sulfur diesel, growing the company's portfolio of higher value products.

•The company's Strathcona Renewable Diesel project, Canada's largest renewable diesel facility, has commenced operations, contributing to the growth of higher value products by adding 20,000 barrels per day of capacity.1

•Chemical Products year-to-date earnings were $566 million, a decrease of $998 million versus the first half of 2024. Results were affected by weaker margins and higher project-driven expenses related to the China Chemical Complex, partially offset by structural cost savings.

•Second-quarter earnings of $293 million were comparable to the first quarter. Higher sales volumes driven by the China Chemical Complex ramp-up offset weaker margins from lower North America feed advantage.

1 Optimizing current production based on product demand, compliance requirements and supplier capabilities for both the renewable feedstock and also the required hydrogen for processing.

•Specialty Products continued to deliver strong earnings from its portfolio of high-value products. Year-to-date earnings were $1.4 billion, a decrease of $77 million compared to the first half of the prior year. Higher expenses, including spending on ProxximaTM systems and carbon materials market development, and unfavorable foreign exchange were partially offset by stronger margins and structural cost savings.

•Earnings increased $125 million versus the first quarter. Stronger basestock margins and record high-value product sales volumes were partially offset by higher new market development costs.

•The company began start-up of the Singapore Resid Upgrade project during the quarter. Once fully operational, the facility will convert 80,000 barrels per day of lower value fuel oil to higher value products, including 20,000 barrels per day of performance lubricant basestocks for Specialty Products and 50,000 barrels per day of distillates for Energy Products.

•Corporate and Financing year-to-date net charges of $1.6 billion increased $885 million compared to the first half of 2024 mainly due to lower interest income, unfavorable foreign exchange and increased pension-related expenses.

•Second-quarter net charges of $759 million decreased $39 million versus the first quarter.

5

CASH FLOW FROM OPERATIONS AND ASSET SALES EXCLUDING WORKING CAPITAL

2Q25

1Q25

Dollars in millions (unless otherwise noted)

YTD 2025

YTD 2024

7,354

8,033

Net income/(loss) including noncontrolling interests

15,387

18,137

6,101

5,702

Depreciation and depletion (includes impairments)

11,803

10,599

(3,970)

(878)

Changes in operational working capital, excluding cash and debt

(4,848)

(2,608)

2,065

96

Other

2,161

(904)

11,550

12,953

Cash Flow from Operating Activities (U.S. GAAP)

24,503

25,224

176

1,823

Proceeds from asset sales and returns of investments

1,999

1,629

11,726

14,776

Cash Flow from Operations and Asset Sales (non-GAAP)

26,502

26,853

3,970

878

Less: Changes in operational working capital, excluding cash and debt

4,848

2,608

15,696

15,654

Cash Flow from Operations and Asset Sales excluding Working Capital (non-GAAP)

31,350

29,461

(176)

(1,823)

Less: Proceeds from asset sales and returns of investments

(1,999)

(1,629)

15,520

13,831

Cash Flow from Operations excluding Working Capital (non-GAAP)

29,351

27,832

FREE CASH FLOW

2Q25

1Q25

Dollars in millions (unless otherwise noted)

YTD 2025

YTD 2024

11,550

12,953

Cash Flow from Operating Activities (U.S. GAAP)

24,503

25,224

(6,283)

(5,898)

Additions to property, plant and equipment

(12,181)

(11,309)

(319)

(153)

Additional investments and advances

(472)

(744)

246

93

Other investing activities including collection of advances

339

224

176

1,823

Proceeds from asset sales and returns of investments

1,999

1,629

23

22

Inflows from noncontrolling interest for major projects

45

12

5,393

8,840

Free Cash Flow (non-GAAP)

14,233

15,036

6

CASH CAPITAL EXPENDITURES

2Q25

1Q25

Dollars in millions (unless otherwise noted)

YTD 2025

YTD 2024

6,283

5,898

Additions to property, plant and equipment

12,181

11,309

319

153

Additional investments and advances

472

744

(246)

(93)

Other investing activities including collection of advances

(339)

(224)

(23)

(22)

Inflows from noncontrolling interests for major projects

(45)

(12)

6,333

5,936

Total Cash Capital Expenditures (non-GAAP)

12,269

11,817

2Q25

1Q25

Dollars in millions (unless otherwise noted)

YTD 2025

YTD 2024

Upstream

3,407

2,983

United States

6,390

5,251

2,262

2,010

Non-U.S.

4,272

4,205

5,669

4,993

Total

10,662

9,456

Energy Products

154

127

United States

281

297

8

251

Non-U.S.

259

687

162

378

Total

540

984

Chemical Products

171

154

United States

325

228

108

137

Non-U.S.

245

579

279

291

Total

570

807

Specialty Products

43

52

United States

95

24

54

58

Non-U.S.

112

139

97

110

Total

207

163

Other

126

164

Other

290

407

6,333

5,936

Worldwide

12,269

11,817

7

CALCULATION OF STRUCTURAL COST SAVINGS

Dollars in billions (unless otherwise noted)

Twelve Months Ended December 31,

Six Months Ended June 30,

2019

2024

2024

2025

Components of Operating Costs

From ExxonMobil’s Consolidated Statement of Income (U.S. GAAP)

Production and manufacturing expenses

36.8

39.6

18.9

20.2

Selling, general and administrative expenses

11.4

10.0

5.1

5.1

Depreciation and depletion (includes impairments)

19.0

23.4

10.6

11.8

Exploration expenses, including dry holes

1.3

0.8

0.3

0.3

Non-service pension and postretirement benefit expense

1.2

0.1

0.1

0.2

Subtotal

69.7

74.0

34.9

37.6

ExxonMobil’s share of equity company expenses (non-GAAP)

9.1

9.6

4.7

5.2

Total Adjusted Operating Costs (non-GAAP)

78.8

83.6

39.6

42.8

Total Adjusted Operating Costs (non-GAAP)

78.8

83.6

39.6

42.8

Less:

Depreciation and depletion (includes impairments)

19.0

23.4

10.6

11.8

Non-service pension and postretirement benefit expense

1.2

0.1

0.1

0.2

Other adjustments (includes equity company depreciation and depletion)

3.6

3.7

1.7

2.4

Total Cash Operating Expenses (Cash Opex) (non-GAAP)

55.0

56.4

27.2

28.4

Energy and production taxes (non-GAAP)

11.0

13.9

6.8

7.6

Total Cash Operating Expenses (Cash Opex) excluding Energy and Production Taxes (non-GAAP)

44.0

42.5

20.4

20.8

Change vs 2019

Change vs 2024

Estimated Cumulative vs 2019

Total Cash Operating Expenses (Cash Opex) excluding Energy and Production Taxes (non-GAAP)

-1.5

+0.4

Market

+4.0

+0.3

Activity / Other

+6.6

+1.5

Structural Cost Savings

-12.1

-1.4

-13.5

This press release references Structural Cost Savings, which describes decreases in cash opex excluding energy and production taxes as a result of operational efficiencies, workforce reductions, divestment-related reductions, and other cost-saving measures, that are expected to be sustainable compared to 2019 levels. Relative to 2019, estimated cumulative Structural Cost Savings totaled $13.5 billion, which included an additional $1.4 billion in the first six months of 2025. The total change between periods in expenses above will reflect both Structural Cost Savings and other changes in spend, including market drivers, such as inflation and foreign exchange impacts, as well as changes in activity levels and costs associated with new operations, mergers and acquisitions, new business venture development, and early-stage projects. Structural Cost Savings from new operations, mergers and acquisitions, and new business venture developments are included in the cumulative Structural Cost Savings. Estimates of cumulative annual Structural Cost Savings may be revised depending on whether cost reductions realized in prior periods are determined to be sustainable compared to 2019 levels. Structural Cost Savings are stewarded internally to support management's oversight of spending over time. This measure is useful for investors to understand the Corporation's efforts to optimize spending through disciplined expense management.

8

ExxonMobil will discuss financial and operating results and other matters during a webcast at 8:30 a.m. Central Time on August 1, 2025. To listen to the event or access an archived replay, please visit www.exxonmobil.com.

Selected Earnings Driver Definitions

Advantaged volume growth. Represents earnings impact from change in volume/mix from advantaged assets, advantaged projects, and high-value products. See frequently used terms on page 11 for definitions of advantaged assets, advantaged projects, and high-value products.

Base volume. Represents and includes all volume/mix drivers not included in advantaged volume growth driver defined above.

Structural cost savings. Represents after-tax earnings effect of Structural Cost Savings as defined on page 8, including cash operating expenses related to divestments.

Expenses. Represents and includes all expenses otherwise not included in other earnings drivers.

Timing effects. Represents timing effects that are primarily related to unsettled derivatives (mark-to-market) and other earnings impacts driven by timing differences between the settlement of derivatives and their offsetting physical commodity realizations (due to LIFO inventory accounting).

Cautionary Statement

Statements related to future events; projections; descriptions of strategic, operating, and financial plans and objectives; statements of future ambitions, future earnings power, potential addressable markets, or plans; and other statements of future events or conditions in this release, are forward-looking statements. Similarly, discussion of future carbon capture, transportation and storage, as well as lower-emission fuels, hydrogen, ammonia, lithium, direct air capture, ProxximaTM systems, carbon materials, low-carbon data centers, and other low carbon and new business plans to reduce emissions of ExxonMobil, its affiliates, and third parties, are dependent on future market factors, such as continued technological progress, stable policy support and timely rule-making and permitting, and represent forward-looking statements. Actual future results, including financial and operating performance; potential earnings, cash flow, or rate of return; total capital expenditures and mix, including allocations of capital to low carbon and other new investments; realization and maintenance of structural cost reductions and efficiency gains, including the ability to offset inflationary pressure; plans to reduce future emissions and emissions intensity; ambitions to reach Scope 1 and Scope 2 net zero from operated assets by 2050, to reach Scope 1 and 2 net zero in heritage Permian Basin unconventional operated assets by 2030 and in Pioneer Permian assets by 2035, to eliminate routine flaring in-line with World Bank Zero Routine Flaring, to reach near-zero methane emissions from its operated assets and other methane initiatives, and to meet ExxonMobil’s emission reduction goals and plans, divestment and start-up plans, and associated project plans as well as technology advances, including the timing and outcome of projects to capture and store CO2, produce hydrogen and ammonia, produce lower-emission fuels, produce lithium, produce ProxximaTM systems, create new advanced carbon materials, and use plastic waste as feedstock for advanced recycling; cash flow, dividends and shareholder returns, including the timing and amounts of share repurchases; future debt levels and credit ratings; business and project plans, timing, costs, capacities and returns; resource recoveries and production rates; and planned Pioneer and Denbury integrated benefits, could differ materially due to a number of factors. These include global or regional changes or imbalances in the supply and demand for oil, natural gas, petrochemicals, and feedstocks and other market factors, economic conditions and seasonal fluctuations that impact prices, differentials, and volume/mix for our products; changes in any part of the world in laws, taxes, or regulations including environmental and tax regulations, trade sanctions, and timely granting of governmental permits and certifications; developments or changes in government policies supporting lower carbon and new market investment opportunities or policies limiting the attractiveness of future investment such as the additional European taxes on the energy sector and unequal support for different methods of emissions reduction; variable impacts of trading activities on our margins and results each quarter; changes in interest and exchange rates; actions of competitors and commercial counterparties; the outcome of commercial negotiations, including final agreed terms and conditions; the ability to access debt markets; the ultimate impacts of public health crises, including the effects of government responses on people and economies; reservoir performance, including variability and timing factors applicable to unconventional resources, the success of new unconventional technologies, and the ability of new technologies to improve the recovery relative to competitors; the level and outcome of exploration projects and decisions to invest in future reserves; timely completion of development and other construction projects and commencement of start-up operations, including reliance on third-party suppliers and service providers; final management approval of future projects and any changes in the scope, terms, or costs of such projects as approved; government regulation of our growth opportunities; war, civil unrest, attacks against the company or industry and other political or security disturbances; expropriations, seizure, or capacity, insurance, export, import or shipping limitations by foreign governments or laws; changes in market, national or regional tariffs or realignment of global trade and supply chain networks; opportunities for potential acquisitions, investments or divestments and satisfaction of applicable conditions to closing, including timely regulatory approvals; the capture of efficiencies within and between business lines and the ability to maintain near-term cost reductions as ongoing efficiencies without impairing our competitive positioning; unforeseen technical or operating difficulties and unplanned maintenance; the development and competitiveness of alternative energy and emission reduction technologies; the results of research programs and the ability to bring new technologies to commercial scale on a cost-competitive basis; and other factors discussed under Item 1A. Risk Factors of ExxonMobil’s 2024 Form 10-K.

Actions needed to advance ExxonMobil’s 2030 greenhouse gas emission-reductions plans are incorporated into its medium-term business plans, which are updated annually. The reference case for planning beyond 2030 is based on ExxonMobil’s Global Outlook (Outlook) research and publication. The Outlook is reflective of the existing global policy environment and an

9

assumption of increasing policy stringency and technology improvement to 2050. Current trends for policy stringency and deployment of lower-emission solutions are not yet on a pathway to achieve net-zero by 2050. As such, the Outlook does not project the degree of required future policy and technology advancement and deployment for the world, or ExxonMobil, to meet net zero by 2050. As future policies and technology advancements emerge, they will be incorporated into the Outlook, and ExxonMobil's business plans will be updated accordingly. References to projects or opportunities may not reflect investment decisions made by ExxonMobil or its affiliates. Individual projects or opportunities may advance based on a number of factors, including availability of stable and supportive policy, permitting, technological advancement for cost-effective abatement, insights from the company planning process, and alignment with our partners and other stakeholders. Capital investment guidance in lower-emission investments is based on our corporate plan; however, actual investment levels will be subject to the availability of the opportunity set and public policy support, and focused on returns.

Frequently Used Terms and Non-GAAP Measures

This press release includes cash flow from operations and asset sales (non-GAAP). Because of the regular nature of our asset management and divestment program, the company believes it is useful for investors to consider proceeds associated with the sales of subsidiaries, property, plant and equipment, and sales and returns of investments together with cash provided by operating activities when evaluating cash available for investment in the business and financing activities. A reconciliation to net cash provided by operating activities for the 2024 and 2025 periods is shown on page 6.

This press release also includes cash flow from operations excluding working capital (non-GAAP), and cash flow from operations and asset sales excluding working capital (non-GAAP). The company believes it is useful for investors to consider these numbers in comparing the underlying performance of the company's business across periods when there are significant period-to-period differences in the amount of changes in working capital. A reconciliation to net cash provided by operating activities for the 2024 and 2025 periods is shown on page 6.

This press release also includes Earnings/(Loss) Excluding Identified Items (non-GAAP), which are earnings/(loss) excluding individually significant non-operational events with, typically, an absolute corporate total earnings impact of at least $250 million in a given quarter. The earnings/(loss) impact of an identified item for an individual segment may be less than $250 million when the item impacts several periods or several segments. Earnings/(loss) excluding Identified Items does include non-operational earnings events or impacts that are generally below the $250 million threshold utilized for identified items. When the effect of these events is significant in aggregate, it is indicated in analysis of period results as part of quarterly earnings press release and teleconference materials. Management uses these figures to improve comparability of the underlying business across multiple periods by isolating and removing significant non-operational events from business results. The Corporation believes this view provides investors increased transparency into business results and trends and provides investors with a view of the business as seen through the eyes of management. Earnings excluding Identified Items is not meant to be viewed in isolation or as a substitute for net income/(loss) attributable to ExxonMobil as prepared in accordance with U.S. GAAP. A reconciliation to each of corporate earnings and segment earnings are shown for 2025 and 2024 periods in Attachments II-a and II-b. Earnings per share amounts are shown on page 1 and in Attachment II-a, including a reconciliation to earnings/(loss) per common share – assuming dilution (U.S. GAAP).

This press release also includes total taxes including sales-based taxes. This is a broader indicator of the total tax burden on the Corporation’s products and earnings, including certain sales and value-added taxes imposed on and concurrent with revenue-producing transactions with customers and collected on behalf of governmental authorities (“sales-based taxes”). It combines “Income taxes” and “Total other taxes and duties” with sales-based taxes, which are reported net in the income statement. The company believes it is useful for the Corporation and its investors to understand the total tax burden imposed on the Corporation’s products and earnings. A reconciliation to total taxes is shown in Attachment I-a.

This press release also references free cash flow (non-GAAP). Free cash flow is the sum of net cash provided by operating activities, net cash flow used in investing activities excluding cash acquired from mergers and acquisitions, and inflows from noncontrolling interests for major projects from financing activities. This measure is useful when evaluating cash available for financing activities, including shareholder distributions, after investment in the business. Free cash flow is not meant to be viewed in isolation or as a substitute for net cash provided by operating activities. A reconciliation to net cash provided by operating activities for the 2024 and 2025 periods is shown on page 6.

This press release also references total cash capital expenditures (non-GAAP). Cash capital expenditures are the sum of additions to property, plant and equipment; additional investments and advances; and other investing activities including collection of advances; reduced by inflows from noncontrolling interests for major projects, each from the Consolidated Statement of Cash Flows. The company believes it is a useful measure for investors to understand the cash impact of investments in the business, which is in line with standard industry practice. A breakdown of cash capex is shown on page 7.

References to resources or resource base may include quantities of oil and natural gas classified as proved reserves, as well as quantities that are not yet classified as proved reserves, but that are expected to be ultimately recoverable. The term “resource base” or similar terms are not intended to correspond to SEC definitions such as “probable” or “possible” reserves. A reconciliation of production excluding divestments, entitlements, and government mandates to actual production is contained in the Supplement to this release included as .2 to the Form 8-K filed the same day as this news release.

The term “project” as used in this news release can refer to a variety of different activities and does not necessarily have the same meaning as in any government payment transparency reports. Projects or plans may not reflect investment decisions made by the company. Individual opportunities may advance based on a number of factors, including availability of supportive

10

policy, technology for cost-effective abatement, and alignment with our partners and other stakeholders. The company may refer to these opportunities as projects in external disclosures at various stages throughout their progression.

Advantaged assets (Advantaged growth projects) when used in reference to the Upstream business, includes Permian, Guyana, and LNG.

Advantaged projects refers to capital projects and programs of work that contribute to Energy, Chemical, and/or Specialty Products segments that drive integration of segments/businesses, increase yield of higher value products, or deliver higher than average returns.

Base portfolio (Base) in our Upstream segment, refers to assets (or volumes) other than advantaged assets (or volumes from advantaged assets). In our Energy Products segment, refers to assets (or volumes) other than advantaged projects (or volumes from advantaged projects). In our Chemical Products and Specialty Products segments refers to volumes other than high-value products volumes.

Compound annual growth rate (CAGR) represents the consistent rate at which an investment or business result would have grown had the investment or business result compounded at the same rate each year.

Debt-to-capital ratio is total debt divided by the sum of total debt and equity. Total debt is the sum of notes and loans payable and long-term debt, as reported in the Consolidated Balance Sheet.

Government mandates (curtailments) are changes to ExxonMobil’s sustainable production levels as a result of production limits or sanctions imposed by governments.

High-value products includes performance products and lower-emission fuels.

Lower-emission fuels are fuels with lower life cycle emissions than conventional transportation fuels for gasoline, diesel and jet transport.

Net-debt-to-capital ratio is net debt divided by the sum of net debt and total equity, where net debt is total debt net of cash and cash equivalents, excluding restricted cash. Total debt is the sum of notes and loans payable and long-term debt, as reported in the consolidated balance sheet.

Performance products (performance chemicals, performance lubricants) refers to products that provide differentiated performance for multiple applications through enhanced properties versus commodity alternatives and bring significant additional value to customers and end-users.

Total shareholder return (TSR) is defined by FactSet and measures the change in value of an investment in common stock over a specified period of time, assuming dividend reinvestment. FactSet assumes dividends are reinvested in stock at market prices on the ex-dividend date. Unless stated otherwise, total shareholder return is quoted on an annualized basis.

This press release also references Structural Cost Savings, for more details see page 8.

Unless otherwise indicated, year-to-date (“YTD”) means as of the last business day of the most recent fiscal quarter.

Reference to Earnings

References to corporate earnings mean net income attributable to ExxonMobil (U.S. GAAP) from the consolidated income statement. Unless otherwise indicated, references to earnings, Upstream, Energy Products, Chemical Products, Specialty Products and Corporate and Financing earnings, and earnings per share are ExxonMobil’s share after excluding amounts attributable to noncontrolling interests.

Exxon Mobil Corporation has numerous affiliates, many with names that include ExxonMobil, Exxon, Mobil, Esso, and XTO. For convenience and simplicity, those terms and terms such as Corporation, company, our, we, and its are sometimes used as abbreviated references to specific affiliates or affiliate groups. Similarly, ExxonMobil has business relationships with thousands of customers, suppliers, governments, and others. For convenience and simplicity, words such as venture, joint venture, partnership, co-venturer, and partner are used to indicate business and other relationships involving common activities and interests, and those words may not indicate precise legal relationships. ExxonMobil's ambitions, plans and goals do not guarantee any action or future performance by its affiliates or Exxon Mobil Corporation's responsibility for those affiliates' actions and future performance, each affiliate of which manages its own affairs.

Throughout this press release, both as well as .2, due to rounding, numbers presented may not add up precisely to the totals indicated.

11

ATTACHMENT I-a

CONDENSED CONSOLIDATED STATEMENT OF INCOME

(Preliminary)

Dollars in millions (unless otherwise noted)

Three Months Ended June 30,

Six Months Ended June 30,

2025

2024

2025

2024

Revenues and other income

Sales and other operating revenue

79,477

89,986

160,535

170,397

Income from equity affiliates

1,462

1,744

2,831

3,586

Other income

567

1,330

1,270

2,160

Total revenues and other income

81,506

93,060

164,636

176,143

Costs and other deductions

Crude oil and product purchases

45,327

54,199

92,115

101,800

Production and manufacturing expenses

10,102

9,804

20,185

18,895

Selling, general and administrative expenses

2,528

2,568

5,068

5,063

Depreciation and depletion (includes impairments)

6,101

5,787

11,803

10,599

Exploration expenses, including dry holes

251

153

315

301

Non-service pension and postretirement benefit expense

90

34

203

57

Interest expense

145

271

350

492

Other taxes and duties

6,257

6,579

12,292

12,902

Total costs and other deductions

70,801

79,395

142,331

150,109

Income/(Loss) before income taxes

10,705

13,665

22,305

26,034

Income tax expense/(benefit)

3,351

4,094

6,918

7,897

Net income/(loss) including noncontrolling interests

7,354

9,571

15,387

18,137

Net income/(loss) attributable to noncontrolling interests

272

331

592

677

Net income/(loss) attributable to ExxonMobil

7,082

9,240

14,795

17,460

OTHER FINANCIAL DATA

Dollars in millions (unless otherwise noted)

Three Months Ended June 30,

Six Months Ended June 30,

2025

2024

2025

2024

Earnings per common share (U.S. dollars)

1.64

2.14

3.40

4.20

Earnings per common share - assuming dilution (U.S. dollars)

1.64

2.14

3.40

4.20

Dividends on common stock

Total

4,288

4,285

8,623

8,093

Per common share (U.S. dollars)

0.99

0.95

1.98

1.90

Millions of common shares outstanding

Average - assuming dilution

4,331

4,317

4,351

4,158

Taxes

Income taxes

3,351

4,094

6,918

7,897

Total other taxes and duties

7,204

7,531

14,270

14,691

Total taxes

10,555

11,625

21,188

22,588

Sales-based taxes

5,289

6,339

10,759

11,888

Total taxes including sales-based taxes

15,844

17,964

31,947

34,476

ExxonMobil share of income taxes of equity companies (non-GAAP)

486

907

1,143

1,905

12

ATTACHMENT I-b

CONDENSED CONSOLIDATED BALANCE SHEET

(Preliminary)

Dollars in millions (unless otherwise noted)

June 30, 2025

December 31, 2024

ASSETS

Current assets

Cash and cash equivalents

14,352

23,029

Cash and cash equivalents – restricted

1,359

158

Notes and accounts receivable – net

41,792

43,681

Inventories

Crude oil, products and merchandise

21,364

19,444

Materials and supplies

4,007

4,080

Other current assets

2,234

1,598

Total current assets

85,108

91,990

Investments, advances and long-term receivables

46,092

47,200

Property, plant and equipment – net

295,356

294,318

Other assets, including intangibles – net

21,041

19,967

Total Assets

447,597

453,475

LIABILITIES

Current liabilities

Notes and loans payable

5,419

4,955

Accounts payable and accrued liabilities

59,725

61,297

Income taxes payable

3,017

4,055

Total current liabilities

68,161

70,307

Long-term debt

33,570

36,755

Postretirement benefits reserves

10,352

9,700

Deferred income tax liabilities

39,368

39,042

Long-term obligations to equity companies

1,113

1,346

Other long-term obligations

25,071

25,719

Total Liabilities

177,635

182,869

EQUITY

Common stock without par value

(9,000 million shares authorized, 8,019 million shares issued)

46,629

46,238

Earnings reinvested

477,061

470,903

Accumulated other comprehensive income

(12,436)

(14,619)

Common stock held in treasury

(3,756 million shares at June 30, 2025, and 3,666 million shares at December 31, 2024)

(248,661)

(238,817)

ExxonMobil share of equity

262,593

263,705

Noncontrolling interests

7,369

6,901

Total Equity

269,962

270,606

Total Liabilities and Equity

447,597

453,475

13

ATTACHMENT I-c

CONDENSED CONSOLIDATED STATEMENT OF CASH FLOWS

(Preliminary)

Dollars in millions (unless otherwise noted)

Six Months Ended June 30,

2025

2024

CASH FLOWS FROM OPERATING ACTIVITIES

Net income/(loss) including noncontrolling interests

15,387

18,137

Depreciation and depletion (includes impairments)

11,803

10,599

Changes in operational working capital, excluding cash and debt

(4,848)

(2,608)

All other items – net

2,161

(904)

Net cash provided by operating activities

24,503

25,224

CASH FLOWS FROM INVESTING ACTIVITIES

Additions to property, plant and equipment

(12,181)

(11,309)

Proceeds from asset sales and returns of investments

1,999

1,629

Additional investments and advances

(472)

(744)

Other investing activities including collection of advances

339

224

Cash acquired from mergers and acquisitions

—

754

Net cash used in investing activities

(10,315)

(9,446)

CASH FLOWS FROM FINANCING ACTIVITIES

Additions to long-term debt

883

217

Reductions in long-term debt

(13)

(1,142)

Additions to short-term debt

172

—

Reductions in short-term debt

(4,676)

(2,771)

Additions/(Reductions) in debt with three months or less maturity

257

(6)

Contingent consideration payments

(79)

(27)

Cash dividends to ExxonMobil shareholders

(8,623)

(8,093)

Cash dividends to noncontrolling interests

(452)

(397)

Changes in noncontrolling interests

(10)

4

Inflows from noncontrolling interests for major projects

45

12

Common stock acquired

(9,768)

(8,337)

Net cash provided by (used in) financing activities

(22,264)

(20,540)

Effects of exchange rate changes on cash

600

(318)

Increase/(Decrease) in cash and cash equivalents (including restricted)

(7,476)

(5,080)

Cash and cash equivalents at beginning of period (including restricted)

23,187

31,568

Cash and cash equivalents at end of period (including restricted)