☑QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended June 30, 2025

or

☐TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from __________to__________

Commission File Number 1-2256

Exxon Mobil Corporation

(Exact name of registrant as specified in its charter)

New Jersey

13-5409005

(State or other jurisdiction of incorporation or organization)

(I.R.S. Employer Identification Number)

22777 Springwoods Village Parkway,Spring,Texas77389-1425

(Address of principal executive offices) (Zip Code)

(972)940-6000

(Registrant's telephone number, including area code)

_______________________

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class

Trading Symbol

Name of Each Exchange on Which Registered

Common Stock, without par value

XOM

New York Stock Exchange

0.524% Notes due 2028

XOM28

New York Stock Exchange

0.835% Notes due 2032

XOM32

New York Stock Exchange

1.408% Notes due 2039

XOM39A

New York Stock Exchange

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.Yes ☑No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).Yes ☑No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer

☑

Accelerated filer

☐

Non-accelerated filer

☐

Smaller reporting company

☐

Emerging growth company

☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes☐No ☑

Indicate the number of shares outstanding of each of the issuer's classes of common stock, as of the latest practicable date.

Class

Outstanding as of June 30, 2025

Common stock, without par value

4,263,247,021

EXXON MOBIL CORPORATION

FORM 10-Q

FOR THE QUARTERLY PERIOD ENDED JUNE 30, 2025

TABLE OF CONTENTS

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements

Condensed Consolidated Statement of Income - Three and six months ended June 30, 2025 and 2024

Non-service pension and postretirement benefit expense

90

34

203

57

Interest expense

145

271

350

492

Other taxes and duties

6,257

6,579

12,292

12,902

Total costs and other deductions

70,801

79,395

142,331

150,109

Income (loss) before income taxes

10,705

13,665

22,305

26,034

Income tax expense (benefit)

3,351

4,094

6,918

7,897

Net income (loss) including noncontrolling interests

7,354

9,571

15,387

18,137

Net income (loss) attributable to noncontrolling interests

272

331

592

677

Net income (loss) attributable to ExxonMobil

7,082

9,240

14,795

17,460

Earnings (loss) per common share (dollars)

1.64

2.14

3.40

4.20

Earnings (loss) per common share - assuming dilution (dollars)

1.64

2.14

3.40

4.20

(1) Includes $40 million related to the write-off of exploratory well costs in 2025 that were previously capitalized for greater than one year at December 31, 2024.

The information in the Notes to Condensed Consolidated Financial Statements is an integral part of these statements.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

Note 1. Basis of Financial Statement Preparation

These unaudited Condensed Consolidated Financial Statements should be read in the context of the Consolidated Financial Statements and notes thereto filed with the Securities and Exchange Commission in the Corporation's 2024 Annual Report on Form 10-K. In the opinion of the Corporation, the information furnished herein reflects all known accruals and adjustments necessary for a fair statement of the results for the periods reported herein. All such adjustments are of a normal recurring nature.

Restricted cash represents sale proceeds required to be set aside by a contractual arrangement for any potential like-kind exchange. The restriction will lapse upon the earlier of completion of the exchange or the expiry of the underlying time period, which is less than one year.

The Corporation's exploration and production activities are accounted for under the "successful efforts" method.

Note 2. Pioneer Natural Resources Merger

On May 3, 2024, the Corporation acquired Pioneer Natural Resources Company ("Pioneer"), an independent oil and gas exploration and production company. In connection with the acquisition, we issued 545 million shares of ExxonMobil common stock having a fair value of $63 billion on the acquisition date, and assumed debt with a fair value of $5 billion.

The transaction was accounted for as a business combination in accordance with ASC 805, which requires that assets acquired and liabilities assumed be recognized at their fair values as of the acquisition date. The following table summarizes the fair values of the assets acquired and liabilities assumed.

(billions of dollars)

Pioneer

Current assets (1)

3

Other non-current assets

1

Property, plant & equipment (2)

84

Total identifiable assets acquired

88

Current liabilities (1)

3

Long-term debt (3)

5

Deferred income tax liabilities (4)

16

Other non-current liabilities

2

Total liabilities assumed

26

Net identifiable assets acquired

62

Goodwill (5)

1

Net assets

63

(1) Current assets and current liabilities consist primarily of accounts receivable and payable, with their respective fair values approximating historical values given their short-term duration, expectation of insignificant bad debt expense, and our credit rating.

(2) Property, plant and equipment, of which a significant portion relates to crude oil and natural gas properties, was primarily valued using the income approach. Significant inputs and assumptions used in the income approach included estimates for commodity prices, future oil and gas production volumes, drilling and development costs, and risk-adjusted discount rates. Collectively, these inputs are level 3 inputs.

(3) Long-term debt was valued using market prices as of the acquisition date, which reflects the use of level 1 inputs.

(4) Deferred income taxes represent the tax effects of differences in the tax basis and acquisition date fair values of assets acquired and liabilities assumed.

(5) Goodwill was allocated to the Upstream segment.

The following table presents long-term debt assumed at closing:

(millions of dollars)

Par Value

Fair Value as of May 2, 2024

0.250% Convertible Senior Notes due May 2025 (1)

450

1,327

1.125% Senior Notes due January 2026

750

699

5.100% Senior Notes due March 2026

1,100

1,096

7.200% Senior Notes due January 2028

241

252

4.125% Senior Notes due February 2028

138

130

1.900% Senior Notes due August 2030

1,100

914

2.150% Senior Notes due January 2031

1,000

832

(1) In June 2024, the Corporation redeemed in full all of the Convertible Senior Notes assumed from Pioneer for an amount consistent with the acquisition date fair value.

Actual and Pro Forma Impact of Merger

The following table presents revenues and earnings included in the Consolidated Statement of Income for Pioneer since the acquisition date (May 3, 2024) through June 30, 2024:

(millions of dollars)

Three Months Ended June 30, 2024

Six Months Ended June 30, 2024

Sales and other operating revenues

4,372

4,372

Net income (loss) attributable to ExxonMobil

398

398

The following table presents unaudited pro forma information for the Corporation as if the merger with Pioneer had occurred at the beginning of January 1, 2023:

Unaudited

(millions of dollars)

Three Months Ended June 30, 2024

Six Months Ended June 30, 2024

Sales and other operating revenues

92,167

178,557

Net income (loss) attributable to ExxonMobil

9,265

18,256

The historical financial information was adjusted to give effect to the pro forma events that were directly attributable to the merger and factually supportable. The unaudited pro forma consolidated results are not necessarily indicative of what the consolidated results of operations actually would have been had the merger been completed on January 1, 2023. In addition, the unaudited pro forma consolidated results reflect pro forma adjustments primarily related to conforming Pioneer's accounting policies to ExxonMobil, additional depreciation expense related to the fair value adjustment of the acquired property, plant and equipment, our capital structure, Pioneer's transaction-related costs, and applicable income tax impacts of the pro forma adjustments.

Our transaction costs to effect the acquisition were immaterial.

A variety of claims have been made against ExxonMobil and certain of its consolidated subsidiaries in a number of pending lawsuits. Management has regular litigation reviews, including updates from corporate and outside counsel, to assess the need for accounting recognition or disclosure of these contingencies. The Corporation accrues an undiscounted liability for those contingencies where the incurrence of a loss is probable and the amount can be reasonably estimated. If a range of amounts can be reasonably estimated and no amount within the range is a better estimate than any other amount, then the minimum of the range is accrued. The Corporation does not record liabilities when the likelihood that the liability has been incurred is probable but the amount cannot be reasonably estimated or when the liability is believed to be only reasonably possible or remote. For contingencies where an unfavorable outcome is reasonably possible and which are significant, the Corporation discloses the nature of the contingency and, where feasible, an estimate of the possible loss. For purposes of our contingency disclosures, “significant” includes material matters, as well as other matters, which management believes should be disclosed.

State and local governments and other entities in various jurisdictions across the United States and its territories have filed a number of legal proceedings against several oil and gas companies, including ExxonMobil, requesting unprecedented legal and equitable relief for various alleged injuries purportedly connected to climate change. These lawsuits assert a variety of novel, untested claims under statutory and common law. Additional such lawsuits may be filed. We believe the legal and factual theories set forth in these proceedings are meritless and represent an inappropriate attempt to use the court system to usurp the proper role of policymakers in addressing the societal challenges of climate change.

Local governments in Louisiana have filed unprecedented legal proceedings against a number of oil and gas companies, including ExxonMobil, requesting compensation for the restoration of coastal marsh erosion in the state. We believe the factual and legal theories set forth in these proceedings are meritless.

While the outcome of any litigation can be unpredictable, we believe the likelihood is remote that the ultimate outcomes of these lawsuits will have a material adverse effect on the Corporation’s operations, financial condition, or financial statements taken as a whole. We will continue to defend vigorously against these claims.

Other Contingencies

The Corporation and certain of its consolidated subsidiaries were contingently liable at June 30, 2025, for guarantees relating to notes, loans and performance under contracts. Where guarantees for environmental remediation and other similar matters do not include a stated cap, the amounts reflect management’s estimate of the maximum potential exposure. Where it is not possible to make a reasonable estimation of the maximum potential amount of future payments, future performance is expected to be either immaterial or have only a remote chance of occurrence.

June 30, 2025

(millions of dollars)

Equity Company

Obligations(1)

Other Third-Party Obligations

Total

Guarantees

Debt-related

991

157

1,148

Other

674

6,359

7,033

Total

1,665

6,516

8,181

(1) ExxonMobil share.

Additionally, the Corporation and its affiliates have numerous long-term sales and purchase commitments in their various business activities, all of which are expected to be fulfilled with no adverse consequences material to the Corporation’s operations or financial condition.

Current period change excluding amounts reclassified from accumulated other comprehensive income (1)

(1,197)

(21)

(1,218)

Amounts reclassified from accumulated other comprehensive income

—

20

20

Total change in accumulated other comprehensive income

(1,197)

(1)

(1,198)

Balance as of June 30, 2024

(14,253)

1,066

(13,187)

Balance as of December 31, 2024

(16,166)

1,547

(14,619)

Current period change excluding amounts reclassified from accumulated other comprehensive income (1)

2,200

(46)

2,154

Amounts reclassified from accumulated other comprehensive income

—

29

29

Total change in accumulated other comprehensive income

2,200

(17)

2,183

Balance as of June 30, 2025

(13,966)

1,530

(12,436)

(1) Cumulative Foreign Exchange Translation Adjustment includes net investment hedge gain/(loss) net of taxes of $(293) million and $123 million in 2025 and 2024, respectively.

Amounts Reclassified Out of Accumulated Other

Comprehensive Income - Before-tax Income/(Expense)

(millions of dollars)

Three Months Ended June 30,

Six Months Ended June 30,

2025

2024

2025

2024

Amortization and settlement of postretirement benefits reserves adjustment included in net periodic benefit costs

(Statement of Income line: Non-service pension and postretirement benefit expense)

The estimated fair value of financial instruments and derivatives at June 30, 2025 and December 31, 2024, and the related hierarchy level for the fair value measurement was as follows:

June 30, 2025

Fair Value

(millions of dollars)

Level 1

Level 2

Level 3

Total Gross Assets & Liabilities

Effect of Counterparty Netting

Effect of Collateral Netting

Difference in Carrying Value and Fair Value

Net Carrying Value

Assets

Derivative assets (1)

8,022

1,423

—

9,445

(8,585)

(62)

—

798

Advances to/receivables from equity companies (2)(6)

—

2,458

4,290

6,748

—

—

325

7,073

Other long-term financial assets (3)

1,517

—

1,538

3,055

—

—

214

3,269

Liabilities

Derivative liabilities(4)

8,271

1,271

—

9,542

(8,585)

(311)

—

646

Long-term debt(5)

25,560

2,517

—

28,077

—

—

3,374

31,451

Long-term obligations to equity companies(6)

—

—

1,156

1,156

—

—

(43)

1,113

Other long-term financial liabilities(7)

—

—

404

404

—

—

56

460

December 31, 2024

Fair Value

(millions of dollars)

Level 1

Level 2

Level 3

Total Gross Assets & Liabilities

Effect of Counterparty Netting

Effect of Collateral Netting

Difference in Carrying Value and Fair Value

Net Carrying Value

Assets

Derivative assets (1)

3,223

1,206

—

4,429

(3,913)

(3)

—

513

Advances to/receivables from equity companies (2)(6)

—

2,466

4,167

6,633

—

—

451

7,084

Other long-term financial assets (3)

1,468

—

1,504

2,972

—

—

247

3,219

Liabilities

Derivative liabilities(4)

3,561

1,416

—

4,977

(3,913)

(341)

—

723

Long-term debt(5)

28,884

1,813

—

30,697

—

—

3,935

34,632

Long-term obligations to equity companies(6)

—

—

1,393

1,393

—

—

(47)

1,346

Other long-term financial liabilities (7)

—

—

583

583

—

—

57

640

(1) Included in the Balance Sheet lines: Notes and accounts receivable - net and Other assets, including intangibles - net.

(2) Included in the Balance Sheet line: Investments, advances and long-term receivables.

(3) Included in the Balance Sheet lines: Investments, advances and long-term receivables and Other assets, including intangibles - net.

(4) Included in the Balance Sheet lines: Accounts payable and accrued liabilities and Other long-term obligations.

(5) Excluding finance lease obligations.

(6) Advances to/receivables from equity companies and long-term obligations to equity companies are mainly designated as hierarchy level 3 inputs. The fair value is calculated by discounting the remaining obligations by a rate consistent with the credit quality and industry of the equity company.

(7) Included in the Balance Sheet line: Other long-term obligations. Includes contingent consideration related to a prior year acquisition where fair value is based on expected drilling activities and discount rates.

At June 30, 2025 and December 31, 2024, respectively, the Corporation had $849 million and $491 million of collateral under master netting arrangements not offset against the derivatives on the Condensed Consolidated Balance Sheet, primarily related to initial margin requirements.

The Corporation may use non-derivative financial instruments, such as its foreign currency-denominated debt, as hedges of its net investments in certain foreign subsidiaries. Under this method, the change in the carrying value of the financial instruments due to foreign exchange fluctuations is reported in accumulated other comprehensive income. As of June 30, 2025, the Corporation has designated $3.5 billion of its Euro-denominated debt and related accrued interest as a net investment hedge of its European business. The net investment hedge is deemed to be perfectly effective.

The Corporation had undrawn short-term committed lines of credit of $0.2 billion and undrawn long-term committed lines of credit of $0.7 billion as of the end of second quarter 2025.

Derivative Instruments

The Corporation’s size, strong capital structure, geographic diversity, and the complementary nature of its business segments reduce the Corporation’s enterprise-wide risk from changes in commodity prices, currency rates and interest rates. In addition, the Corporation uses commodity-based contracts, including derivatives, to manage commodity price risk and to generate returns from trading. Commodity contracts held for trading purposes are presented in the Condensed Consolidated Statement of Income on a net basis in the line “Sales and other operating revenue" and in the Consolidated Statement of Cash Flows in “Cash Flows from Operating Activities”. The Corporation’s commodity derivatives are not accounted for under hedge accounting. At times, the Corporation also enters into currency and interest rate derivatives, none of which are material to the Corporation’s financial position as of June 30, 2025 and December 31, 2024, or results of operations for the periods ended June 30, 2025 and 2024.

The Corporation operates a program to hedge certain of its fixed-rate debt instruments against changes in fair value due to changes in the designated benchmark interest rate. This program utilizes fair value hedge accounting. The derivative (hedging) instruments are fixed-for-floating interest rate swaps, with settlement dates that correspond to the interest payments associated with the fixed-rate debt (hedged item). Changes in the fair values of the hedging instruments are perfectly offset by changes in the fair values of the hedged items; the effects of these changes in fair values are recorded in "Interest expense" in the Consolidated Statement of Income. This program was not material to the Consolidated Financial Statements as of the end of second quarter 2025.

Credit risk associated with the Corporation’s derivative position is mitigated by several factors, including the use of derivative clearing exchanges and the quality of and financial limits placed on derivative counterparties. The Corporation maintains a system of controls that includes the authorization, reporting, and monitoring of derivative activity.

The net notional long/(short) position of derivative instruments at June 30, 2025 and December 31, 2024, was as follows:

(millions)

June 30, 2025

December 31, 2024

Crude oil (barrels)

—

13

Petroleum products (barrels)

(26)

(32)

Natural gas (MMBTUs)

(647)

(675)

Realized and unrealized gains/(losses) on derivative instruments that were recognized in the Condensed Consolidated Statement of Income are included in the following lines on a before-tax basis:

Note 8. Disclosures about Segments and Related Information

(millions of dollars)

Upstream

Energy Products

Chemical Products

Specialty Products

Segment Total

U.S.

Non-U.S.

U.S.

Non-U.S.

U.S.

Non-U.S.

U.S.

Non-U.S.

Three Months Ended June 30, 2025

Revenues and other income

Sales and other operating revenue

5,939

3,286

25,072

34,917

1,970

3,700

1,438

3,134

79,456

Income from equity affiliates

5

1,300

36

28

38

129

3

(10)

1,529

Intersegment revenue

6,230

8,824

4,502

6,512

1,668

790

551

113

29,190

Other income

93

23

26

54

—

3

2

31

232

Segment revenues and other income

12,267

13,433

29,636

41,511

3,676

4,622

1,994

3,268

110,407

Costs and other items

Crude oil and product purchases

4,533

2,006

25,515

33,551

2,136

3,204

1,073

2,025

74,043

Operating expenses, excl. depreciation and depletion (1)

2,716

2,480

1,940

2,272

1,096

1,194

510

556

12,764

Depreciation and depletion (includes impairments)

3,356

1,733

198

170

148

138

27

43

5,813

Interest expense

22

16

(1)

1

—

—

—

2

40

Other taxes and duties

49

531

830

4,744

18

39

1

44

6,256

Total costs and other deductions

10,676

6,766

28,482

40,738

3,398

4,575

1,611

2,670

98,916

Segment income (loss) before income taxes

1,591

6,667

1,154

773

278

47

383

598

11,491

Income tax expense (benefit)

379

2,332

264

159

23

3

91

106

3,357

Segment net income (loss) incl. noncontrolling interests

1,212

4,335

890

614

255

44

292

492

8,134

Net income (loss) attributable to noncontrolling interests

—

145

65

73

—

6

1

3

293

Segment income (loss)

1,212

4,190

825

541

255

38

291

489

7,841

Reconciliation of consolidated revenues

Segment revenues and other income

110,407

Other revenues (2)

289

Elimination of intersegment revenues

(29,190)

Total consolidated revenues and other income

81,506

Reconciliation of income (loss) attributable to ExxonMobil

Total segment income (loss)

7,841

Corporate and Financing income (loss)

(759)

Net income (loss) attributable to ExxonMobil

7,082

(millions of dollars)

Upstream

Energy Products

Chemical Products

Specialty Products

Segment Total

U.S.

Non-U.S.

U.S.

Non-U.S.

U.S.

Non-U.S.

U.S.

Non-U.S.

Three Months Ended June 30, 2025

Additions to property, plant and equipment (3)

3,047

2,022

145

258

161

101

39

50

5,823

As of June 30, 2025

Investments in equity companies

5,107

19,846

462

983

3,008

2,598

—

793

32,797

Total assets

152,661

134,033

32,412

46,120

17,456

18,433

2,674

8,476

412,265

Reconciliation to Corporate Total

Segment Total

Corporate and Financing

Corporate Total

Three Months Ended June 30, 2025

Additions to property, plant and equipment (3)

5,823

532

6,355

As of June 30, 2025

Investments in equity companies

32,797

(140)

32,657

Total assets

412,265

35,332

447,597

(1) Operating expenses, excl. depreciation and depletion includes the following GAAP line items, as reflected on the Income Statement: Production and manufacturing expenses; Selling, general and administrative expenses; Exploration expenses, including dry holes; and Non-service pension and postretirement benefit expense.

(2) Primarily Corporate and Financing Interest revenue of $312 million.

(3) Includes non-cash additions.

Due to rounding, numbers presented may not add up precisely to the totals indicated.

Operating expenses, excl. depreciation and depletion (1)

2,605

2,710

2,033

2,176

1,194

1,120

467

547

12,852

Depreciation and depletion (includes impairments)

2,792

2,039

197

178

144

110

22

34

5,516

Interest expense

46

18

2

1

—

1

—

—

68

Other taxes and duties

104

687

873

4,841

2

20

—

51

6,578

Total costs and other deductions

9,866

7,992

32,459

48,780

3,522

4,446

1,592

2,939

111,596

Segment income (loss) before income taxes

3,165

7,807

609

649

673

341

584

338

14,166

Income tax expense (benefit)

735

2,954

104

92

147

76

136

31

4,275

Segment net income (loss) incl. noncontrolling interests

2,430

4,853

505

557

526

265

448

307

9,891

Net income (loss) attributable to noncontrolling interests

—

209

55

61

—

12

1

3

341

Segment income (loss)

2,430

4,644

450

496

526

253

447

304

9,550

Reconciliation of consolidated revenues

Segment revenues and other income

125,762

Other revenues (2)

551

Elimination of intersegment revenues

(33,253)

Total consolidated revenues and other income

93,060

Reconciliation of income (loss) attributable to ExxonMobil

Total segment income (loss)

9,550

Corporate and Financing income (loss)

(310)

Net income (loss) attributable to ExxonMobil

9,240

(millions of dollars)

Upstream

Energy Products

Chemical Products

Specialty Products

Segment Total

U.S.

Non-U.S.

U.S.

Non-U.S.

U.S.

Non-U.S.

U.S.

Non-U.S.

Three Months Ended June 30, 2024

Additions to property, plant and equipment (3)

86,884

2,474

160

345

104

298

44

64

90,373

As of December 31, 2024

Investments in equity companies

4,884

21,396

444

915

3,016

2,649

—

814

34,118

Total assets

154,914

134,609

32,143

43,399

17,445

17,692

2,882

8,040

411,124

Reconciliation to Corporate Total

Segment Total

Corporate and Financing

Corporate Total

Three Months Ended June 30, 2024

Additions to property, plant and equipment (3)

90,373

431

90,804

As of December 31, 2024

Investments in equity companies

34,118

(108)

34,010

Total assets

411,124

42,351

453,475

(1) Operating expenses, excl. depreciation and depletion includes the following GAAP line items, as reflected on the Income Statement: Production and manufacturing expenses; Selling, general and administrative expenses; Exploration expenses, including dry holes; and Non-service pension and postretirement benefit expense.

(2) Primarily Corporate and Financing Interest revenue of $433 million.

(3) Includes non-cash additions.

Due to rounding, numbers presented may not add up precisely to the totals indicated.

Operating expenses, excl. depreciation and depletion (1)

5,479

4,761

4,022

4,431

2,159

2,278

982

1,126

25,238

Depreciation and depletion (includes impairments)

6,394

3,422

393

343

293

260

54

81

11,240

Interest expense

59

22

(1)

2

—

—

—

2

84

Other taxes and duties

113

1,070

1,617

9,306

34

61

3

88

12,292

Total costs and other deductions

22,007

14,542

56,652

82,679

6,776

8,818

3,109

5,401

199,984

Segment income (loss) before income taxes

4,003

14,322

1,585

1,606

621

67

801

1,011

24,016

Income tax expense (benefit)

921

4,930

358

346

111

(3)

187

183

7,033

Segment net income (loss) incl. noncontrolling interests

3,082

9,392

1,227

1,260

510

70

614

828

16,983

Net income (loss) attributable to noncontrolling interests

—

316

105

189

—

14

1

6

631

Segment income (loss)

3,082

9,076

1,122

1,071

510

56

613

822

16,352

Reconciliation of consolidated revenues

Segment revenues and other income

224,000

Other revenues (2)

605

Elimination of intersegment revenues

(59,969)

Total consolidated revenues and other income

164,636

Reconciliation of income (loss) attributable to ExxonMobil

Total segment income (loss)

16,352

Corporate and Financing income (loss)

(1,557)

Net income (loss) attributable to ExxonMobil

14,795

(millions of dollars)

Upstream

Energy Products

Chemical Products

Specialty Products

Segment Total

U.S.

Non-U.S.

U.S.

Non-U.S.

U.S.

Non-U.S.

U.S.

Non-U.S.

Six Months Ended June 30, 2025

Additions to property, plant and equipment (3)

5,827

4,044

261

486

306

218

88

103

11,333

As of June 30, 2025

Investments in equity companies

5,107

19,846

462

983

3,008

2,598

—

793

32,797

Total assets

152,661

134,033

32,412

46,120

17,456

18,433

2,674

8,476

412,265

Reconciliation to Corporate Total

Segment Total

Corporate and Financing

Corporate Total

Six Months Ended June 30, 2025

Additions to property, plant and equipment (3)

11,333

1,051

12,384

As of June 30, 2025

Investments in equity companies

32,797

(140)

32,657

Total assets

412,265

35,332

447,597

(1) Operating expenses, excl. depreciation and depletion includes the following GAAP line items, as reflected on the Income Statement: Production and manufacturing expenses; Selling, general and administrative expenses; Exploration expenses, including dry holes; and Non-service pension and postretirement benefit expense.

(2) Primarily Corporate and Financing Interest revenue of $675 million.

(3) Includes non-cash additions.

Due to rounding, numbers presented may not add up precisely to the totals indicated.

Operating expenses, excl. depreciation and depletion (1)

4,332

5,340

4,047

4,314

2,185

2,180

895

1,082

24,375

Depreciation and depletion (includes impairments)

4,634

4,074

393

367

303

219

44

73

10,107

Interest expense

74

33

3

3

—

1

—

1

115

Other taxes and duties

202

1,300

1,693

9,544

19

39

2

103

12,902

Total costs and other deductions

16,554

15,768

62,766

94,163

6,980

8,985

3,190

5,851

214,257

Segment income (loss) before income taxes

4,511

15,382

1,739

1,471

1,332

683

1,113

763

26,994

Income tax expense (benefit)

1,027

5,779

340

230

302

126

261

94

8,159

Segment net income (loss) incl. noncontrolling interests

3,484

9,603

1,399

1,241

1,030

557

852

669

18,835

Net income (loss) attributable to noncontrolling interests

—

353

113

205

—

23

1

8

703

Segment income (loss)

3,484

9,250

1,286

1,036

1,030

534

851

661

18,132

Reconciliation of consolidated revenue

Segment revenues and other income

241,251

Other revenues (2)

1,132

Elimination of intersegment revenues

(66,240)

Total consolidated revenues and other income

176,143

Reconciliation of income (loss) attributable to ExxonMobil

Total segment income (loss)

18,132

Corporate and Financing income (loss)

(672)

Net income (loss) attributable to ExxonMobil

17,460

(millions of dollars)

Upstream

Energy Products

Chemical Products

Specialty Products

Segment Total

U.S.

Non-U.S.

U.S.

Non-U.S.

U.S.

Non-U.S.

U.S.

Non-U.S.

Six Months Ended June 30, 2024

Additions to property, plant and equipment (3)

88,912

4,138

302

666

204

533

58

122

94,935

As of December 31, 2024

Investments in equity companies

4,884

21,396

444

915

3,016

2,649

—

814

34,118

Total assets

154,914

134,609

32,143

43,399

17,445

17,692

2,882

8,040

411,124

Reconciliation to Corporate Total

Segment Total

Corporate and Financing

Corporate Total

Six Months Ended June 30, 2024

Additions to property, plant and equipment (3)

94,935

943

95,878

As of December 31, 2024

Investments in equity companies

34,118

(108)

34,010

Total assets

411,124

42,351

453,475

(1) Operating expenses, excl. depreciation and depletion includes the following GAAP line items, as reflected on the Income Statement: Production and manufacturing expenses; Selling, general and administrative expenses; Exploration expenses, including dry holes; and Non-service pension and postretirement benefit expense.

(2) Primarily Corporate and Financing Interest revenue of $907 million.

(3) Includes non-cash additions.

Due to rounding, numbers presented may not add up precisely to the totals indicated.

Sales and other operating revenue include both revenue within the scope of ASC 606 and outside the scope of ASC 606. Trade receivables in Notes and accounts receivable – net reported on the Balance Sheet also includes both receivables within the scope of ASC 606 and those outside the scope of ASC 606. Revenue and receivables outside the scope of ASC 606 primarily relate to physically settled commodity contracts accounted for as derivatives. Contractual terms, credit quality, and type of customer are generally similar between those revenues and receivables within the scope of ASC 606 and those outside it.

Sales and other operating revenue

(millions of dollars)

Three Months Ended June 30,

Six Months Ended June 30,

2025

2024

2025

2024

Revenue from contracts with customers

56,680

64,181

113,611

122,600

Revenue outside the scope of ASC 606

22,797

25,805

46,924

47,797

Total

79,477

89,986

160,535

170,397

Geographic Sales and Other Operating Revenue

(millions of dollars)

Three Months Ended June 30,

Six Months Ended June 30,

2025

2024

2025

2024

United States

34,436

36,895

69,043

67,551

Non-U.S.

45,041

53,091

91,492

102,846

Total

79,477

89,986

160,535

170,397

Significant Non-U.S. revenue sources include: (1)

Canada

6,804

8,126

13,794

15,182

(1)Revenue is determined by primary country of operations. Excludes certain sales and other operating revenues in non-U.S. operations where attribution to a specific country is not practicable.

Note 9. Divestment Activities

Through June 30, 2025, the Corporation realized proceeds of approximately $2.0 billion and net after-tax earnings of approximately $0.2 billion from its divestment activities. This included the sale of select conventional assets in Texas and New Mexico, Mobil Argentina S.A., as well as other smaller divestments.

In 2024, the Corporation realized proceeds of approximately $5.0 billion and recognized net after-tax earnings of approximately $1.0 billion from its divestment activities. This included the sale of the Santa Ynez Unit and associated facilities in California, Mobil Producing Nigeria Unlimited, ExxonMobil Exploration Argentina, the Fos-sur-Mer Refinery (France), the Adriatic LNG terminal (Italy), and certain conventional and unconventional assets in the United States, as well as other smaller divestments.

ITEM 2. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Overview

During the second quarter of 2025, the price of crude oil decreased slightly relative to first quarter 2025, remaining near the middle of the 10-year historical range (2010-2019) supported by strong demand which helped to offset increased OPEC supply. Natural gas prices remained above the 10-year range on strong global demand. Global industry refining margins improved in the second quarter, moving back to the middle of the 10-year historical range driven by strong seasonal demand. Chemical margins remained at bottom of cycle, well below the 10-year range, with continued industry oversupply.

During 2025, the U.S. announced a variety of trade-related actions, including the imposition of tariffs on imports from several countries. In response, many countries announced their own retaliatory tariffs. Certain tariffs were paused for a period of time but have not been withdrawn, while others have been revised. The global trade environment continues to be volatile. The likelihood of the U.S. or its trading partners resuming tariffs, imposing new or revised reciprocal tariffs, export restrictions, or other forms of trade-related sanctions is highly uncertain. Despite the current uncertainty as to what effects these actions will ultimately have on the Corporation, our suppliers and our customers, as well as on the overall macroeconomic environment, we do not anticipate any material near-term financial impacts.

Selected Earnings Driver Definitions

The earnings drivers provide additional visibility into our business results. The Corporation evaluates these drivers periodically to determine if any enhancements may provide helpful insights to the market. Listed below are descriptions of the earnings drivers:

Advantaged Volume Growth. Represents earnings impacts from change in volume/mix from advantaged assets, advantaged projects, and high-value products.

•Advantaged Assets (Advantaged growth projects). Includes Permian, Guyana, and LNG.

•Advantaged Projects. Includes capital projects and programs of work that contribute to Energy, Chemical, and/or Specialty Products segments that drive integration of segments/businesses, increase yield of higher value products, or deliver higher than average returns.

•High-Value Products. Includes performance products and lower-emission fuels. Performance products (performance chemicals, performance lubricants) refers to products that provide differentiated performance for multiple applications through enhanced properties versus commodity alternatives and bring significant additional value to customers and end-users. Lower-emission fuels refers to fuels with lower life cycle emissions than conventional transportation fuels for gasoline, diesel and jet transport.

Base Volume. Represents all volume/mix drivers not included in Advantaged Volume Growth defined above.

Structural Cost Savings. Represents after-tax earnings effects of Structural Cost Savings as defined on page 23, including cash operating expenses related to divestments.

Expenses. Represents all expenses otherwise not included in other earnings drivers.

Timing Effects. Represents timing effects that are primarily related to unsettled derivatives (mark-to-market) and other earnings impacts driven by timing differences between the settlement of derivatives and their offsetting physical commodity realizations (due to LIFO inventory accounting).

Earnings (loss) excluding Identified Items are earnings (loss) excluding individually significant non-operational events with, typically, an absolute corporate total earnings impact of at least $250 million in a given quarter. The earnings (loss) impact of an Identified Item for an individual segment may be less than $250 million when the item impacts several segments or several periods. Earnings (loss) excluding Identified Items does include non-operational earnings events or impacts that are generally below the $250 million threshold utilized for Identified Items. Management uses these figures to improve comparability of the underlying business across multiple periods by isolating and removing significant non-operational events from business results. The Corporation believes this view provides investors increased transparency into business results and trends, and provides investors with a view of the business as seen through the eyes of management. Earnings (loss) excluding Identified Items is not meant to be viewed in isolation or as a substitute for net income (loss) attributable to ExxonMobil as prepared in accordance with U.S. GAAP.

References in this discussion to Corporate earnings (loss) mean net income (loss) attributable to ExxonMobil (U.S. GAAP) from the Condensed Consolidated Statement of Income. Unless otherwise indicated, references to earnings (loss); Upstream, Energy Products, Chemical Products, Specialty Products, and Corporate and Financing earnings (loss); and earnings (loss) per share are ExxonMobil's share after excluding amounts attributable to noncontrolling interests.

Due to rounding, numbers presented may not add up precisely to the totals indicated.

Structural Cost Savings describes decreases in cash opex excluding energy and production taxes as a result of operational efficiencies, workforce reductions, divestment-related reductions, and other cost-savings measures that are expected to be sustainable compared to 2019 levels. Relative to 2019, estimated cumulative Structural Cost Savings totaled $13.5 billion, which included an additional $1.4 billion in the first six months of 2025. The total change between periods in expenses below will reflect both Structural Cost Savings and other changes in spend, including market factors, such as inflation and foreign exchange impacts, as well as changes in activity levels and costs associated with new operations, mergers and acquisitions, new business venture development, and early-stage projects. Structural Cost Savings from new operations, mergers and acquisitions, and new business venture developments are included in the cumulative Structural Cost Savings. Estimates of cumulative annual structural savings may be revised depending on whether cost reductions realized in prior periods are determined to be sustainable compared to 2019 levels. Structural Cost Savings are stewarded internally to support management's oversight of spending over time. This measure is useful for investors to understand the Corporation's efforts to optimize spending through disciplined expense management.

Dollars in billions (unless otherwise noted)

Twelve Months Ended December 31,

Six Months Ended June 30,

2019

2024

2024

2025

Components of Operating Costs

From ExxonMobil’s Consolidated Statement of Income (U.S. GAAP)

Production and manufacturing expenses

36.8

39.6

18.9

20.2

Selling, general and administrative expenses

11.4

10.0

5.1

5.1

Depreciation and depletion (includes impairments)

19.0

23.4

10.6

11.8

Exploration expenses, including dry holes

1.3

0.8

0.3

0.3

Non-service pension and postretirement benefit expense

1.2

0.1

0.1

0.2

Subtotal

69.7

74.0

34.9

37.6

ExxonMobil’s share of equity company expenses (Non-GAAP)

9.1

9.6

4.7

5.2

Total Adjusted Operating Costs (Non-GAAP)

78.8

83.6

39.6

42.8

Total Adjusted Operating Costs (Non-GAAP)

78.8

83.6

39.6

42.8

Less:

Depreciation and depletion (includes impairments)

19.0

23.4

10.6

11.8

Non-service pension and postretirement benefit expense

1.2

0.1

0.1

0.2

Other adjustments (includes equity company depreciation and depletion)

3.6

3.7

1.7

2.4

Total Cash Operating Expenses (Cash Opex) (Non-GAAP)

55.0

56.4

27.2

28.4

Energy and production taxes (Non-GAAP)

11.0

13.9

6.8

7.6

Total Cash Operating Expenses (Cash Opex) excluding Energy and Production Taxes (Non-GAAP)

44.0

42.5

20.4

20.8

Change

vs

2019

Change

vs

2024

Estimated Cumulative vs

2019

Total Cash Operating Expenses (Cash Opex) excluding Energy and Production Taxes (Non-GAAP)

-1.5

+0.4

Market

+4.0

+0.3

Activity / Other

+6.6

+1.5

Structural Cost Savings

-12.1

-1.4

-13.5

Due to rounding, numbers presented may not add up precisely to the totals indicated.

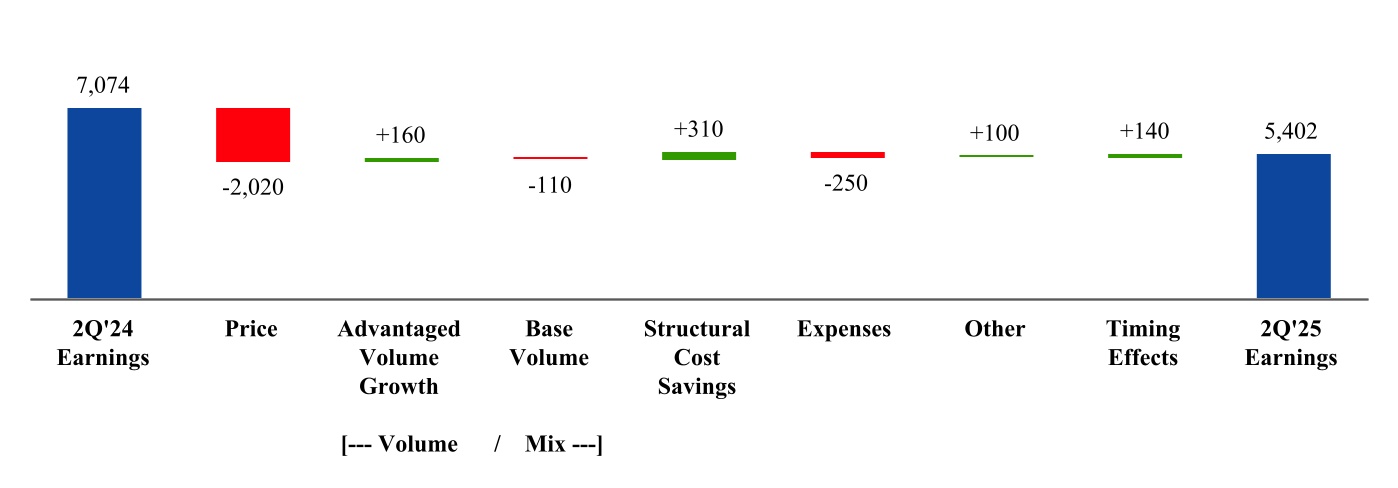

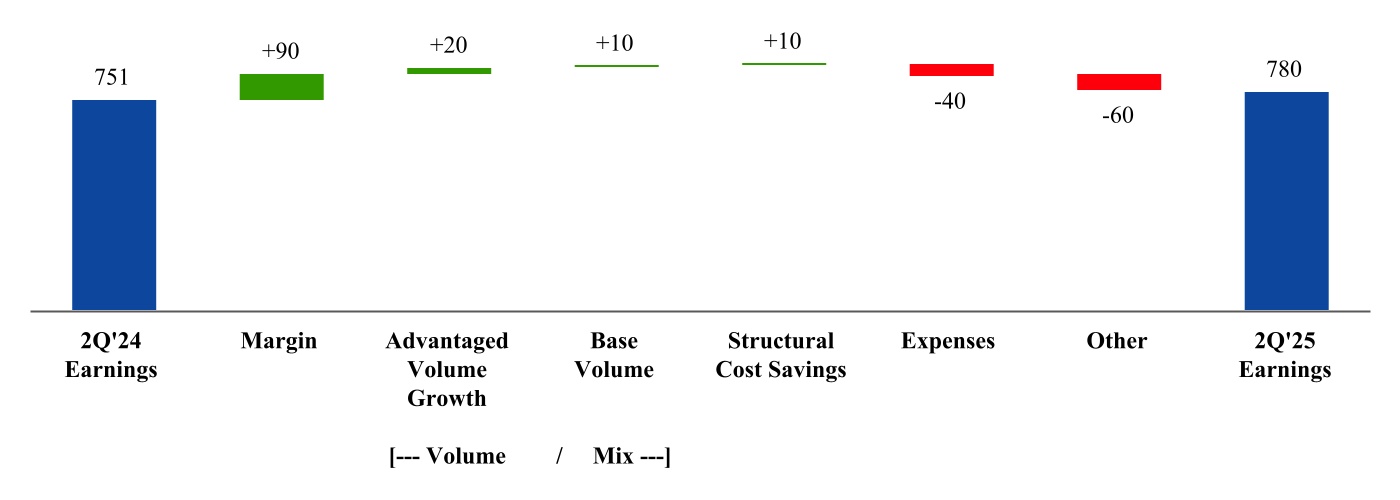

ExxonMobil’s second quarter 2025 earnings were $7.1 billion, compared to $9.2 billion a year earlier. The decrease in earnings was mainly driven by weaker crude prices, lower chemical realizations, and higher expenses from growth initiatives; partly offset by increased volumes from advantaged Upstream investments in the Permian and Structural Cost Savings. Cash capital expenditures were $6.3 billion, down $0.2 billion from second quarter 2024.

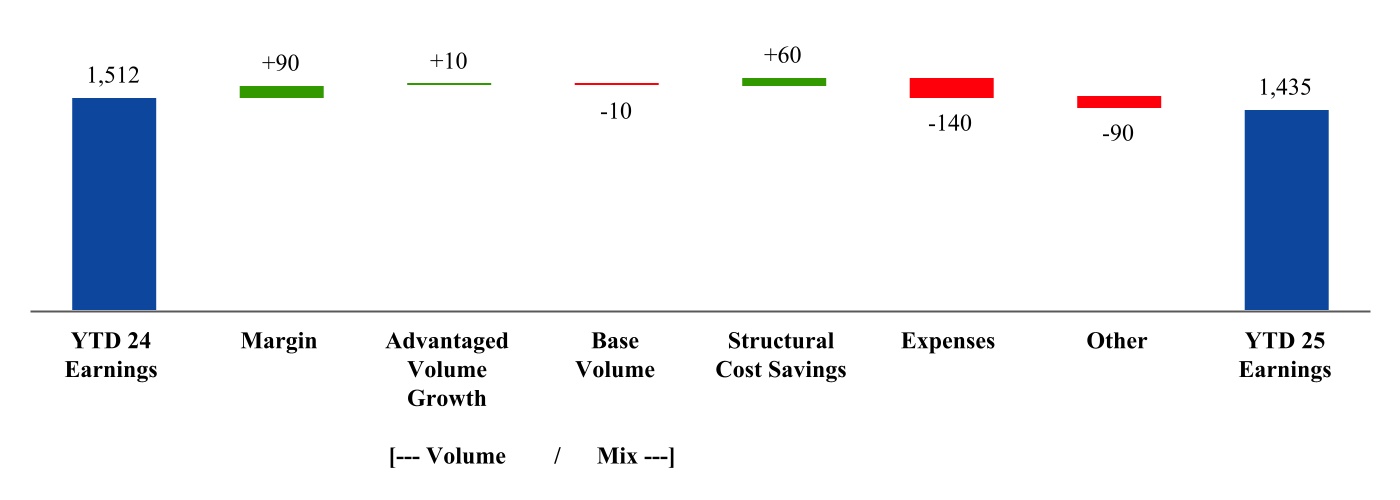

Earnings for the first six months of 2025 were $14.8 billion, compared to $17.5 billion a year earlier. Cash capital expenditures were $12.3 billion, up $0.5 billion from the first six months of 2024. The Corporation distributed $8.6 billion in dividends to shareholders and repurchased $9.8 billion of common stock.

Price – Price impacts decreased earnings by $2,020 million, mainly driven by lower liquids realizations.

Advantaged Volume Growth – Volumes from advantaged assets increased earnings by $160 million, mainly driven by Permian growth, including the Pioneer acquisition.

Base Volume – Decreased earnings by $110 million as a result of divestments.

Structural Cost Savings – Increased earnings by $310 million.

Expenses – Decreased earnings by $250 million from higher depreciation.

Other – Increased earnings by $100 million, driven by favorable foreign exchange and tax items, partially offset by lower divestment gains.

Timing Effects – Increased earnings by $140 million, mainly from favorable derivatives mark-to-market impacts.

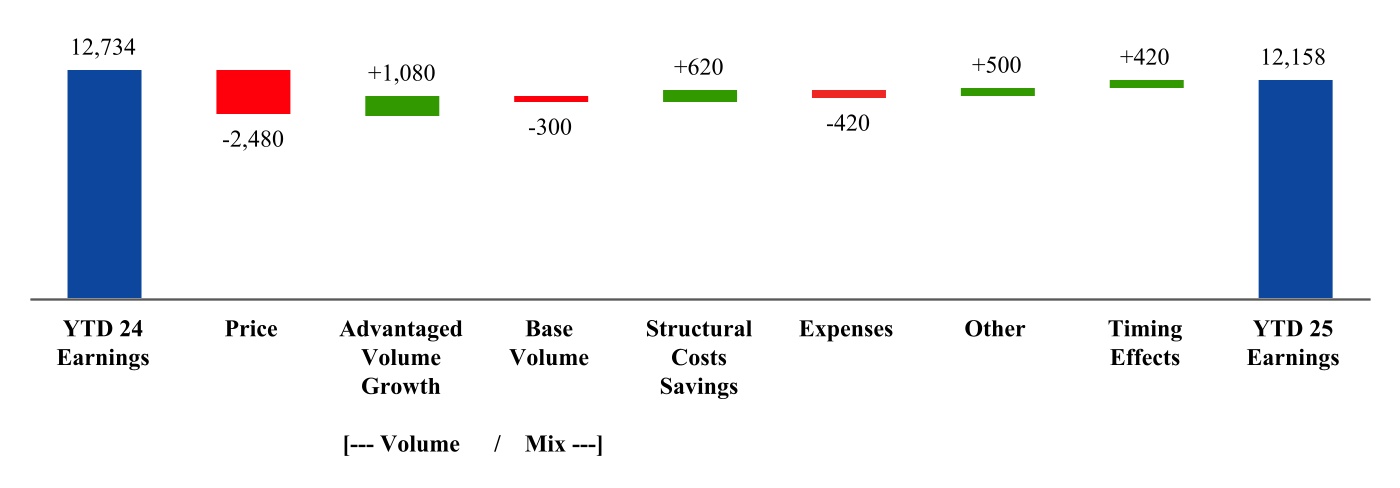

Upstream Year-to-Date Earnings Driver Analysis

(millions of dollars)

Price– Price impacts decreased earnings by $2,480 million, driven by lower liquids realizations.

Advantaged Volume Growth – Volumes from advantaged assets increased earnings by $1,080 million, driven by the Permian and Guyana.

Base Volume – Divestments of non-strategic assets decreased earnings by $300 million, partially offset by the Tengiz expansion.

Structural Cost Savings – Increased earnings by $620 million.

Expenses – Decreased earnings by $420 million, primarily from higher depreciation.

Other – Increased earnings by $500 million, driven by favorable foreign exchange and tax items.

Timing Effects – Increased earnings by $420 million from favorable derivatives mark-to-market impacts.

(1) Natural gas is converted to an oil-equivalent basis at six million cubic feet per one thousand barrels.

Due to rounding, numbers presented may not add up precisely to the totals indicated.

2Q 2025

versus

2Q 2024

2Q 2025 production of 4.6 million oil-equivalent barrels per day increased 272 thousand oil-equivalent barrels per day from 2Q 2024, driven by the Pioneer acquisition.

YTD 2025

versus

YTD 2024

4.6 million oil-equivalent barrels per day in 2025 increased 520 thousand oil-equivalent barrels per day from 2024, driven by Permian production.

Listed below are descriptions of ExxonMobil’s volumes reconciliation drivers which are provided to facilitate understanding of the terms.

Entitlements - Net Interest are changes to ExxonMobil’s share of production volumes caused by non-operational changes to volume-determining drivers. These drivers consist of net interest changes specified in Production Sharing Contracts (PSCs), which typically occur when cumulative investment returns or production volumes achieve defined thresholds, changes in equity upon achieving pay-out in partner investment carry situations, equity redeterminations as specified in venture agreements, or as a result of the termination or expiry of a concession. Once a net interest change has occurred, it typically will not be reversed by subsequent events, such as lower crude oil prices.

Entitlements - Price / Spend / Other are changes to ExxonMobil’s share of production volumes resulting from temporary changes to non-operational volume-determining drivers. These drivers include changes in oil and gas prices or spending levels from one period to another. According to the terms of contractual arrangements or government royalty regimes, price or spending variability can increase or decrease royalty burdens and/or volumes attributable to ExxonMobil. For example, at higher prices, fewer barrels are required for ExxonMobil to recover its costs. These effects generally vary from period to period with field spending patterns or market prices for oil and natural gas. Such drivers can also include other temporary changes in net interest as dictated by specific provisions in production agreements.

Government Mandates are changes to ExxonMobil's sustainable production levels as a result of production limits or sanctions imposed by governments.

Divestments are reductions in ExxonMobil’s production arising from commercial arrangements to fully or partially reduce equity in a field or asset in exchange for financial or other economic consideration.

Growth and Other comprise all other operational and non-operational drivers not covered by the above definitions that may affect volumes attributable to ExxonMobil. Such drivers include, but are not limited to, production enhancements from project and work program activities, acquisitions including additions from asset exchanges, downtime, market demand, natural field decline, and any fiscal or commercial terms that do not affect entitlements.

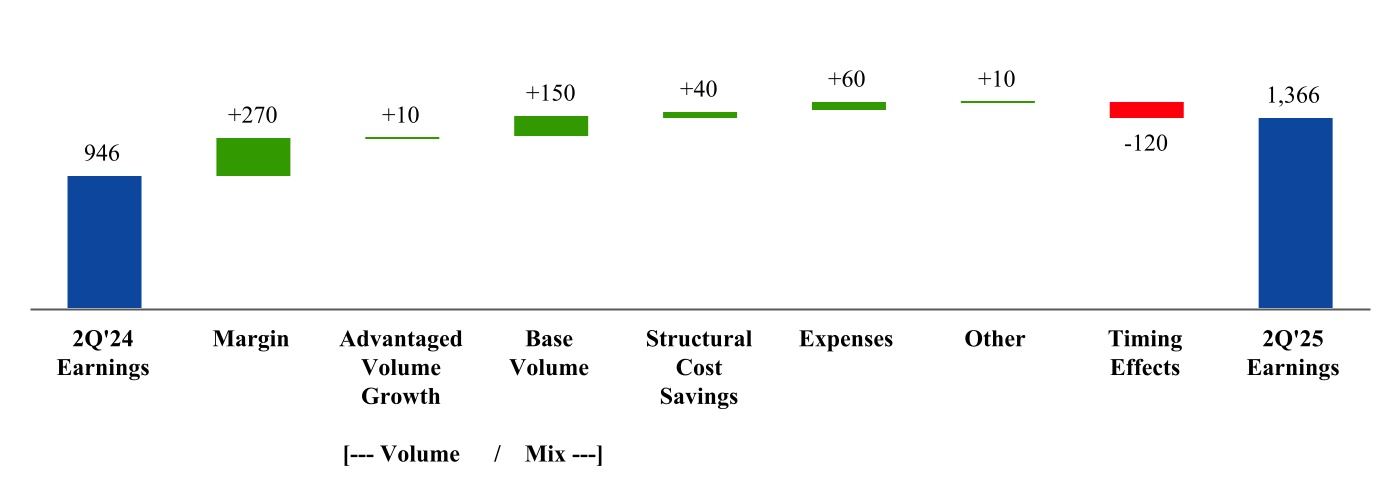

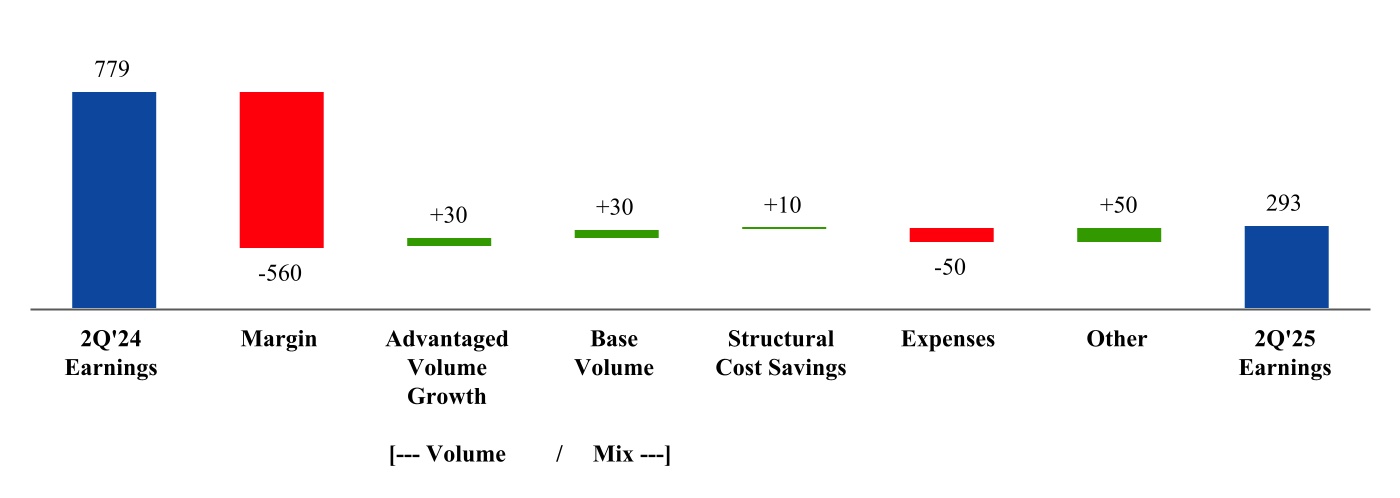

Energy Products Second Quarter Earnings Driver Analysis

(millions of dollars)

Margin – Industry refining margins increased earnings by $270 million, on higher fuel demand and industry supply outages.

Advantaged Volume Growth – Volumes from advantaged projects increased earnings by $10 million.

Base Volume – Increased earnings by $150 million, driven by lower scheduled maintenance.

Structural Cost Savings– Increased earnings by $40 million.

Expenses– Increased earnings by $60 million.

Other – Increased earnings by $10 million.

Timing Effects – Decreased earnings by $120 million, mainly from the absence of prior year favorable derivatives mark-to-market impacts.

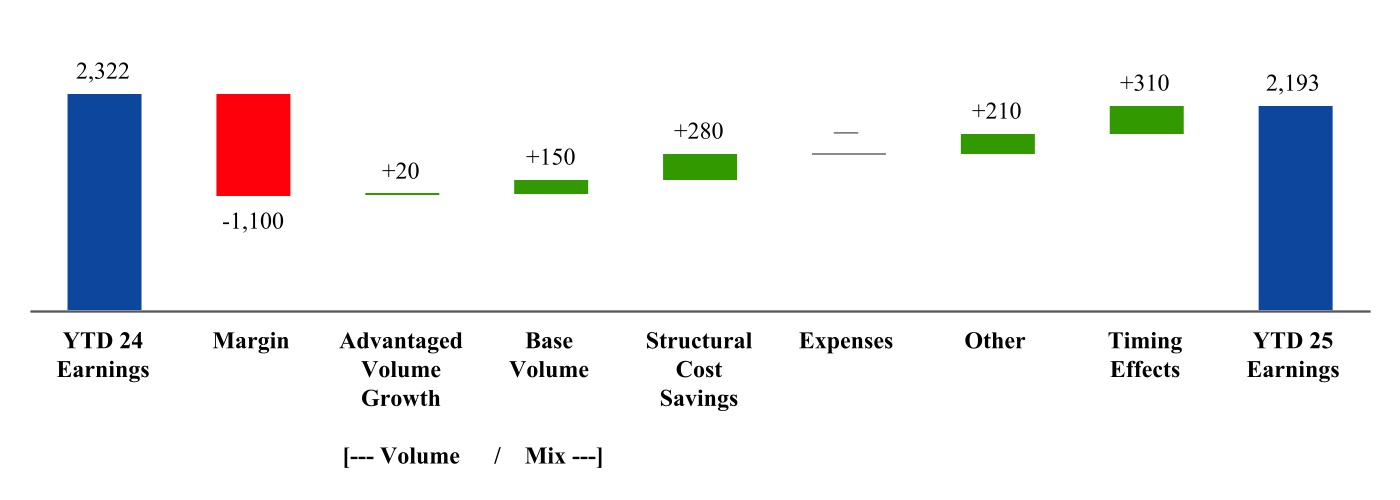

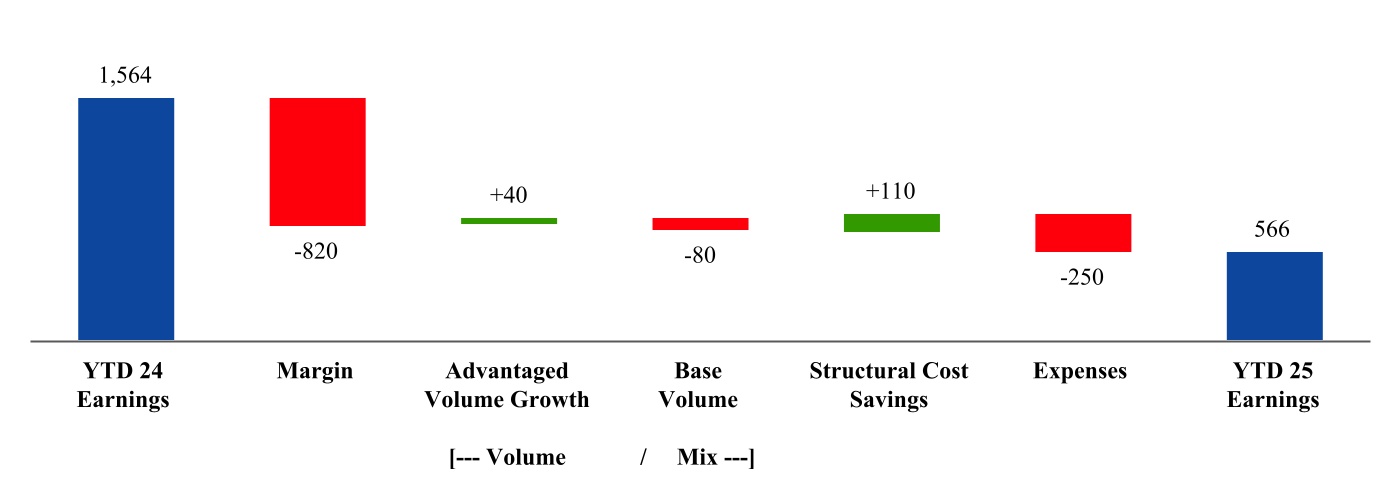

Energy Products Year-to-Date Earnings Driver Analysis

(millions of dollars)

Margins– Industry refining margins decreased earnings by $1,100 million, as the increased supply from industry capacity additions outpaced higher global demand.

Advantaged Volume Growth – Volumes from advantaged projects increased earnings by $20 million.

Base Volume – Higher base volumes increased earnings by $150 million, driven by lower scheduled maintenance.

Structural Cost Savings– Increased earnings by $280 million.

Expenses– Remained flat.

Other – All other items, mainly driven by the absence of unfavorable inventory impacts, increased earnings by $210 million.

Timing Effects – Increased earnings by $310 million, mainly from the absence of prior year unfavorable derivatives mark-to-market impacts.

(2) Refer to page 22 for definition of Identified Items and earnings (loss) excluding Identified Items.

Corporate and Financing expenses were $759 million for the second quarter of 2025, $449 million higher than the second quarter of 2024, due to lower interest income, unfavorable foreign exchange and increased pension-related expenses.

Corporate and Financing expenses were $1,557 million for the first six months of 2025, $885 million higher than 2024, due to lower interest income, unfavorable foreign exchange and increased pension-related expenses.

Net cash provided by operating activities (U.S. GAAP)

11,550

10,560

24,503

25,224

Proceeds associated with sales of subsidiaries, property, plant & equipment, and sales and returns of investments

176

926

1,999

1,629

Cash flow from operations and asset sales (Non-GAAP)

11,726

11,486

26,502

26,853

Because of the ongoing nature of our asset management and divestment program, we believe it is useful for investors to consider proceeds associated with asset sales together with cash provided by operating activities when evaluating cash available for investment in the business and financing activities, including shareholder distributions.

Cash flow from operations and asset sales in the second quarter of 2025 was $11.7 billion, an increase of $0.2 billion from the comparable 2024 period.

Cash provided by operating activities totaled $24.5 billion for the first six months of 2025, $0.7 billion lower than 2024. Net income including noncontrolling interests was $15.4 billion, a decrease of $2.8 billion from the prior year period. The adjustment for the noncash provision of $11.8 billion for depreciation and depletion was up $1.2 billion from 2024. Changes in operational working capital were a reduction of $4.8 billion during the period. All other items net increased cash flows by $2.2 billion in 2025 versus a decrease of $0.9 billion in 2024. See the Condensed Consolidated Statement of Cash Flows for additional details.

Investing activities for the first six months of 2025 used net cash of $10.3 billion, an increase of $0.9 billion compared to the prior year. Spending for additions to property, plant and equipment of $12.2 billion was $0.9 billion higher than 2024. Proceeds from asset sales were $2.0 billion, an increase of $0.4 billion compared to the prior year. Net investments and advances decreased $0.4 billion from $0.5 billion in 2024.

Net cash used in financing activities was $22.3 billion in the first six months of 2025, including $9.8 billion for the purchase of 89.9 million shares of ExxonMobil stock, as part of the previously announced buyback program. This compares to net cash used in financing activities of $20.5 billion in the prior year. Total debt at the end of the second quarter of 2025 was $39.0 billion compared to $41.7 billion at year-end 2024. The Corporation's debt to total capital ratio was 12.6 percent at the end of the second quarter of 2025 compared to 13.4 percent at year-end 2024. The net debt to capital ratio (1) was 8.4 percent at the end of the second quarter, an increase of 1.9 percentage points from year-end 2024. The Corporation's capital allocation priorities are investing in competitively advantaged, high-return projects; maintaining a strong balance sheet; and sharing our success with our shareholders through more consistent share repurchases and a growing dividend. The Corporation distributed a total of $8.6 billion to shareholders in the first six months of 2025 through dividends.

The Corporation has access to significant capacity of long-term and short-term liquidity. Internally generated funds are expected to cover the majority of financial requirements, supplemented by long-term and short-term debt. The Corporation had undrawn short-term committed lines of credit of $0.2 billion and undrawn long-term committed lines of credit of $0.7 billion as of the end of second quarter 2025.

The Corporation, as part of its ongoing asset management program, continues to evaluate its mix of assets for potential upgrade. Because of the ongoing nature of this program, dispositions will continue to be made from time to time which will result in either gains or losses. Additionally, the Corporation continues to evaluate opportunities to enhance its business portfolio through acquisitions of assets or companies, and enters into such transactions from time to time. Key criteria for evaluating acquisitions include strategic fit, cost synergies, potential for future growth, low cost of supply, and attractive valuations. Acquisitions may be made with cash, shares of the Corporation’s common stock, or both.

Litigation and other contingencies are discussed in Note 3 to the unaudited Condensed Consolidated Financial Statements.

(1) Net debt is total debt of $39.0 billion less $14.4 billion of cash and cash equivalents excluding restricted cash . Net debt to capital ratio is net debt divided by net debt plus total equity of $270.0 billion. Total debt is the sum of notes and loans payable and long-term debt, as reported in the Consolidated Balance Sheet.

(1) Includes “Other taxes and duties” plus taxes that are included in “Production and manufacturing expenses” and “Selling, general and administrative expenses”, each from the Consolidated Statement of Income.

Total taxes were $10.6 billion for the second quarter of 2025, a decrease of $1.1 billion from 2024. Income tax expense was $3.4 billion compared to $4.1 billion in the prior year. The effective income tax rate, which is calculated based on consolidated company income taxes and ExxonMobil's share of equity company income taxes, was 34 percent, comparable with the prior year period. Total other taxes and duties decreased by $0.3 billion to $7.2 billion.

Total taxes were $21.2 billion for the first six months of 2025, a decrease of $1.4 billion from 2024. Income tax expense decreased by $1.0 billion to $6.9 billion reflecting lower commodity prices. The effective income tax rate of 34 percent was down compared to the prior year period due primarily to favorable one-time items. Total other taxes and duties decreased by $0.4 billion to $14.3 billion.

CASH CAPITAL EXPENDITURES (Non-GAAP)

Cash capital expenditures (Cash Capex) is the sum of "Additions to property, plant and equipment"; "Additional investments and advances"; and "Other investing activities including collection of advances"; reduced by "Inflows from noncontrolling interests for major projects", each from the Consolidated Statement of Cash Flows. This measure is useful for investors to understand the current period cash impact of investments in the business.

(millions of dollars)

Three Months Ended June 30,

Six Months Ended June 30,

2025

2024

2025

2024

Additions to property, plant and equipment

6,283

6,235

12,181

11,309

Additional investments and advances

319

323

472

744

Other investing activities including collection of advances

(246)

(9)

(339)

(224)

Inflows from noncontrolling interests for major projects

(23)

—

(45)

(12)

Total Cash Capex (Non-GAAP)

6,333

6,549

12,269

11,817

Cash capex in the second quarter of 2025 was $6.3 billion, down $0.2 billion from the second quarter of 2024.

(millions of dollars)

Three Months Ended June 30,

Six Months Ended June 30,

2025

2024

2025

2024

Upstream

5,669

5,351

10,662

9,456

Energy Products

162

467

540

984

Chemical Products

279

468

570

807

Specialty Products

97

82

207

163

Other

126

181

290

407

Total Cash Capex (Non-GAAP)

6,333

6,549

12,269

11,817

The Corporation plans to invest in the range of $27 billion to $29 billion in 2025. Actual spending could vary depending on the progress of individual projects and property acquisitions.

Statements related to future events; projections; descriptions of strategic, operating, and financial plans and objectives; statements of future ambitions and plans; future earnings power; potential addressable markets; and other statements of future events or conditions are forward-looking statements. Similarly, discussion of future plans related to carbon capture, transportation and storage, lower-emission fuels, hydrogen, ammonia, direct air capture, ProxximaTM systems, carbon materials, lithium, low-carbon data centers, and other future plans to reduce emissions and emission intensity of ExxonMobil, its affiliates, and third parties are dependent on future market factors, such as continued technological progress, stable policy support and timely rule-making and permitting, and represent forward-looking statements.

Actual future results, including financial and operating performance; potential earnings, cash flow, dividends or shareholder returns, including the timing and amounts of share repurchases; total capital expenditures and mix, including allocations of capital to low carbon and other new investments; realization and maintenance of structural cost reductions and efficiency gains, including the ability to offset inflationary pressure; plans to reduce future emissions and emissions intensity, including ambitions to reach Scope 1 and Scope 2 net zero from operated assets by 2050, to reach Scope 1 and 2 net zero in heritage Permian Basinunconventional operated assets by 2030 and in Pioneer Permian assets by 2035, to eliminate routine flaring in-line with World Bank Zero Routine Flaring, to reach near-zero methane emissions from operated assets and other methane initiatives; and to meet ExxonMobil’s emission reduction plans and goals, divestment and start-up plans, and associated project plans as well as technology advances, including the timing and outcome of projects to capture, transport and store CO2, produce hydrogen and ammonia, produce lower-emission fuels, produce ProxximaTM systems, produce carbon materials, produce lithium, and use plastic waste as feedstock for advanced recycling; future debt levels and credit ratings; business and project plans, timing, costs, capacities and profitability; resource recoveries and production rates; and planned Denbury and Pioneer integrated benefits, could differ materially due to a number of factors.

These include global or regional changes or imbalances in the supply and demand for oil, natural gas, petrochemicals, and feedstocks and other market factors; economic conditions and seasonal fluctuations that impact prices, differentials, and volume/mix for our products; developments or changes in local, national, or international laws, regulations, taxes, trade sanctions, trade tariffs, or policies affecting our business, such as government policies supporting lower carbon and new market investment opportunities, the punitive European taxes on the oil and gas sector and unequal support for different technological methods of emissions reduction or evolving, ambiguous and unharmonized standards imposed by various jurisdictions related to sustainability and greenhouse gas reporting; timely granting of governmental permits and certifications; uncertain impacts of deregulation on the legal and regulatory environment; changes in interest and exchange rates; variable impacts of trading activities on our margins and results each quarter; actions of co-venturers, competitors and commercial counterparties; the outcome of commercial negotiations, including final agreed terms and conditions; the outcome of competitive bidding and project awards; the ability to access debt markets on favorable terms or at all; the occurrence, pace, rate of recovery and effects of public health crises; adoption of regulatory incentives consistent with law; reservoir performance, including variability and timing factors applicable to unconventional resources, the success of new unconventional technologies, and the ability of new technologies to improve recovery relative to competitors; the level, outcome, and timing of exploration and development projects and decisions to invest in future reserves and resources; timely completion of construction projects and commencement of start-up operations, including reliance on third-party suppliers and service providers; final management approval of future projects and any changes in the scope, terms, costs or assumptions of such projects as approved; the actions of government or other actors against our core business activities and acquisitions, divestitures or financing opportunities; war, civil unrest, attacks against the company or industry, and other geopolitical or security disturbances, including disruption of land or sea transportation routes; decoupling of economies, realignment of global trade and supply chain networks, and disruptions in military alliances; expropriations, seizure, or capacity, insurance, shipping, import or export limitations imposed directly or indirectly by governments or laws; opportunities for potential acquisitions, investments or divestments and satisfaction of applicable conditions to closing, including timely regulatory approvals; the capture of efficiencies within and between business lines and the ability to maintain near-term cost reductions as ongoing efficiencies without impairing our competitive positioning; unforeseen technical or operating difficulties and unplanned maintenance; the development and competitiveness of alternative energy and emission reduction technologies; consumer preferences including willingness and ability to pay for reduced emission products; the results of research programs and the ability to bring new technologies to commercial scale on a cost-competitive basis; and other factors discussed under "Item 1A. Risk Factors" of ExxonMobil’s 2024 Form 10-K.

Forward-looking and other statements regarding environmental and other sustainability efforts and aspirations are not an indication that these statements are material to investors or require disclosure in our filing with the SEC or any other regulatory authority. In addition, historical, current, and forward-looking environmental and other sustainability-related statements may be based on standards for measuring progress that are still developing, internal controls and processes that continue to evolve, and assumptions that are subject to change in the future, including future rule-making.

Actions needed to advance ExxonMobil’s 2030 greenhouse gas emission-reductions plans are incorporated into its medium-term business plans, which are updated annually. The reference case for planning beyond 2030 is based on ExxonMobil’s Global Outlook (Outlook) research and publication. The Outlook is reflective of the existing global policy environment and an assumption of increasing policy stringency and technology improvement to 2050. Current trends for policy stringency and development of lower-emission solutions are not yet on a pathway to achieve net-zero by 2050. As such, the Outlook does not project the degree of required future policy and technology advancement and deployment for the world, or ExxonMobil, to meet net zero by 2050. As future policies and technology advancements emerge, they will be incorporated into the Outlook, and ExxonMobil’s business plans will be updated accordingly. References to projects or opportunities may not reflect investment decisions made by ExxonMobil or its affiliates. Individual projects or opportunities may advance based on a number of factors, including availability of stable and supportive policy, permitting, technological advancement for cost-effective abatement, insights from the Corporate planning process, and alignment with our partners and other stakeholders. Capital investment guidance in lower-emission investments is based on our Corporate plan; however, actual investment levels will be subject to the availability of the opportunity set and public policy support, and focused on returns.

The term “project” as used in this report can refer to a variety of different activities and does not necessarily have the same meaning as in any government payment transparency reports.

ITEM 3. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Information about market risks for the six months ended June 30, 2025, does not differ materially from that discussed under Item 7A of the registrant's Annual Report on Form 10-K for 2024.

ITEM 4. CONTROLS AND PROCEDURES

As indicated in the certifications in Exhibit 31 of this report, the Corporation’s Chief Executive Officer, Chief Financial Officer and Principal Accounting Officer have evaluated the Corporation’s disclosure controls and procedures as of June 30, 2025. Based on that evaluation, these officers have concluded that the Corporation’s disclosure controls and procedures are effective in ensuring that information required to be disclosed by the Corporation in the reports that it files or submits under the Securities Exchange Act of 1934, as amended, is accumulated and communicated to them in a manner that allows for timely decisions regarding required disclosures and are effective in ensuring that such information is recorded, processed, summarized and reported within the time periods specified in the Securities and Exchange Commission’s rules and forms. There were no changes during the Corporation’s last fiscal quarter that materially affected, or are reasonably likely to materially affect, the Corporation’s internal control over financial reporting.

PART II. OTHER INFORMATION

ITEM 1. LEGAL PROCEEDINGS

ExxonMobil has elected to use a $1 million threshold for disclosing environmental proceedings.

As reported in the Corporation’s Form 10-Q for the first quarter of 2025, on December 11, 2024, the Fifth Circuit affirmed the judgment of the United States District Court for the Southern District of Texas assessing a $14.25 million penalty against ExxonMobil related to alleged Clean Air Act and other violations at the Baytown complex. On March 11, 2025, ExxonMobil filed a petition for review with the U.S. Supreme Court. On June 30, 2025, the U.S. Supreme Court denied ExxonMobil’s petition for review. The penalty award is now final and will be paid to the United States Treasury.

Refer to the relevant portions of Note 3 of this Quarterly Report on Form 10-Q for further information on legal proceedings.

ITEM 2. UNREGISTERED SALES OF EQUITY SECURITIES AND USE OF PROCEEDS

Issuer Purchases of Equity Securities for Quarter Ended June 30, 2025

Total Number

of Shares

Purchased (1)

Average

Price Paid

per Share (2)

Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs(3)

Approximate Dollar Value of Shares that May Yet Be Purchased Under the Program

(Billions of dollars) (4)

April 2025

15,755,246

$106.66

15,753,442

$33.5

May 2025

15,966,137

$105.40

15,942,442

$31.8

June 2025

14,766,153

$108.39

14,764,209

$30.2

Total

46,487,536

$106.78

46,460,093

(1) Includes shares withheld from participants in the Corporation's incentive program for personal income taxes.

(2) Excludes 1% U.S. excise tax on stock repurchases.

(3) Purchases were made under terms intended to qualify for exemption under Rules 10b-18 and 10b5-1.

(4) The Corporation continued its share repurchase program, originally initiated in 2022. In its 2024 Corporate Plan Update released December 11, 2024, the Corporation stated that it expects to continue its share repurchase program with a $20 billion repurchase pace per year through 2026, assuming reasonable market conditions.

During the second quarter, the Corporation did not issue or sell any unregistered equity securities.

ITEM 5. OTHER INFORMATION

During the three months ended June 30, 2025, none of the Corporation’s directors or officers adopted or terminated a “Rule 10b5-1 trading arrangement” or “non-Rule 10b5-1 trading arrangement,” as each term is defined in Item 408(a) of Regulation S-K.

Section 1350 Certification (pursuant to Sarbanes-Oxley Section 906) by Principal Accounting Officer.

101*

Interactive Data Files (formatted as Inline XBRL).

104*

Cover Page Interactive Data File (formatted as Inline XBRL and contained in Exhibit 101).

* Filed herewith.

** Furnished herewith.

39

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

EXXON MOBIL CORPORATION

Date: August 4, 2025

By:

/s/ LEN M. FOX

Len M. Fox

Vice President, Controller and Tax (Principal Accounting Officer)