.2 Somnigroup to Acquire Leggett & Platt A pr i l 13, 2026 1

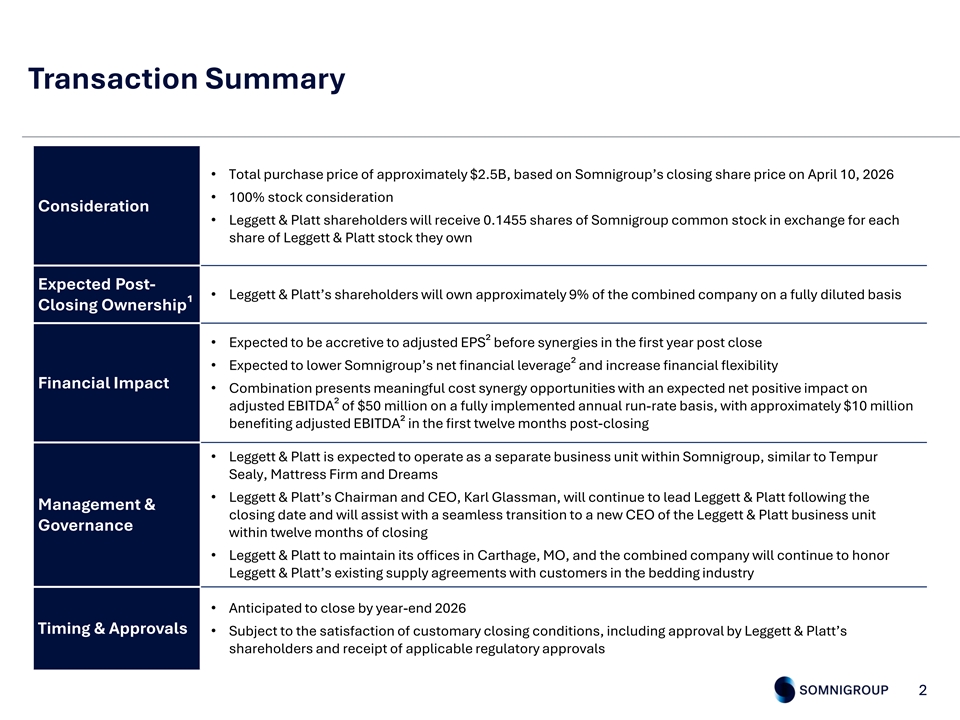

Transaction Summary • Total purchase price of approximately $2.5B, based on Somnigroup’s closing share price on April 10, 2026 • 100% stock consideration Consideration • Leggett & Platt shareholders will receive 0.1455 shares of Somnigroup common stock in exchange for each share of Leggett & Platt stock they own Expected Post- • Leggett & Platt’s shareholders will own approximately 9% of the combined company on a fully diluted basis Closing Ownership¹ • Expected to be accretive to adjusted EPS² before synergies in the first year post close • Expected to lower Somnigroup’s net financial leverage² and increase financial flexibility Financial Impact • Combination presents meaningful cost synergy opportunities with an expected net positive impact on adjusted EBITDA² of $50 million on a fully implemented annual run-rate basis, with approximately $10 million benefiting adjusted EBITDA² in the first twelve months post-closing • Leggett & Platt is expected to operate as a separate business unit within Somnigroup, similar to Tempur Sealy, Mattress Firm and Dreams • Leggett & Platt’s Chairman and CEO, Karl Glassman, will continue to lead Leggett & Platt following the Management & closing date and will assist with a seamless transition to a new CEO of the Leggett & Platt business unit Governance within twelve months of closing • Leggett & Platt to maintain its offices in Carthage, MO, and the combined company will continue to honor Leggett & Platt’s existing supply agreements with customers in the bedding industry • Anticipated to close by year-end 2026 Timing & Approvals • Subject to the satisfaction of customary closing conditions, including approval by Leggett & Platt’s shareholders and receipt of applicable regulatory approvals 2 2

The Somnigroup Investment Thesis: “The Stage Is Set – the Best Is Yet to Come” Global Scale, Vertical Integration: A leading international bedding company with leading, end-to-end capabilities from design and manufacturing to retail Omnichannel Reach & Iconic Brands: Portfolio of trusted brands and products, reaching consumers wherever they shop – online, in 2,800+ stores, and through a robust wholesale network Relentless Innovation & Consumer Insight: Industry-leading R&D, marketing investment and consumer access fuel product differentiation and demand as sleep becomes ever more central to health and wellness Operational Excellence & Leverage: Structural advantages drive superior efficiency and cash flow Resilient Cash Generation & Disciplined Capital Allocation: Robust free cash flow and strong balance sheet supports business reinvestment, acquisitions and shareholder returns Connected, Proven Leadership: Seasoned management team with track record of driving execution and growth across all business units Poised for Industry Recovery: 3 Uniquely positioned to drive value as the $120 billion global bedding market rebounds 3

High-level Strategic Direction | Corporate Governance | Capital Allocation Leading global Leading U.S. Leading U.K. Leading global bedding manufacturer bedding retailer bedding retailer components designer & manufacturer Tactical Go-to-market Strategy | Operational Excellence | Passionate Customer Service 4

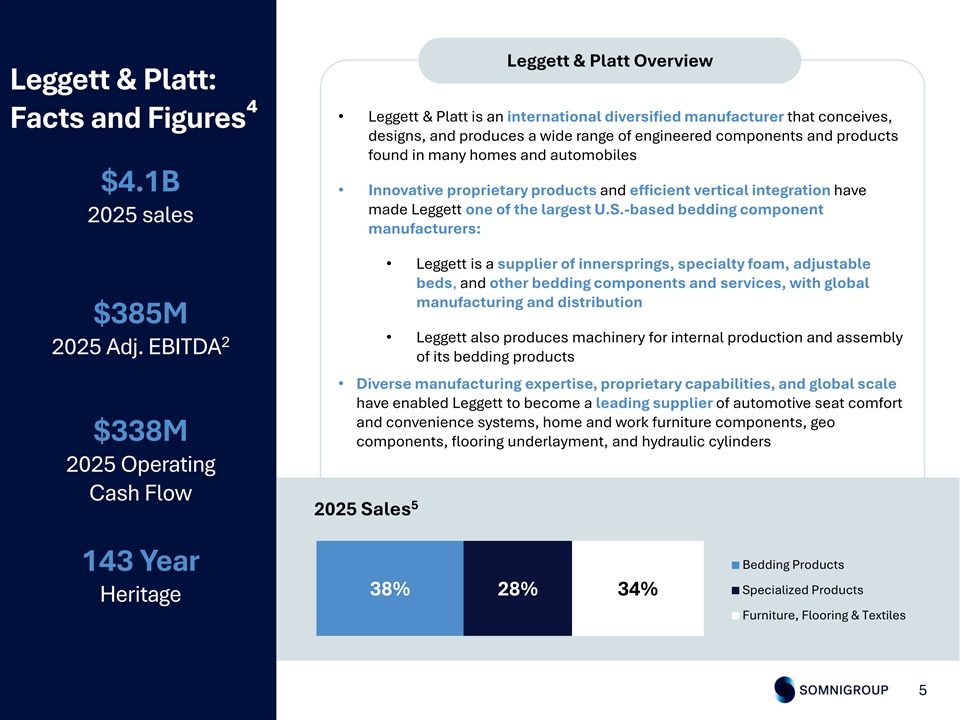

Leggett & Platt Overview Leggett & Platt: • Leggett & Platt is an international diversified manufacturer that conceives, Facts and Figures⁴ designs, and produces a wide range of engineered components and products found in many homes and automobiles $4.1B • Innovative proprietary products and efficient vertical integration have made Leggett one of the largest U.S.-based bedding component 2025 sales manufacturers: • Leggett is a supplier of innersprings, specialty foam, adjustable beds, and other bedding components and services, with global manufacturing and distribution $385M • Leggett also produces machinery for internal production and assembly 2 2025 Adj. EBITDA of its bedding products • Diverse manufacturing expertise, proprietary capabilities, and global scale have enabled Leggett to become a leading supplier of automotive seat comfort and convenience systems, home and work furniture components, geo $338M components, flooring underlayment, and hydraulic cylinders 2025 Operating Cash Flow 5 2025 Sales Bedding Products 143 Year Specialized Products 38% 28% 34% Heritage Furniture, Flooring & Textiles 5

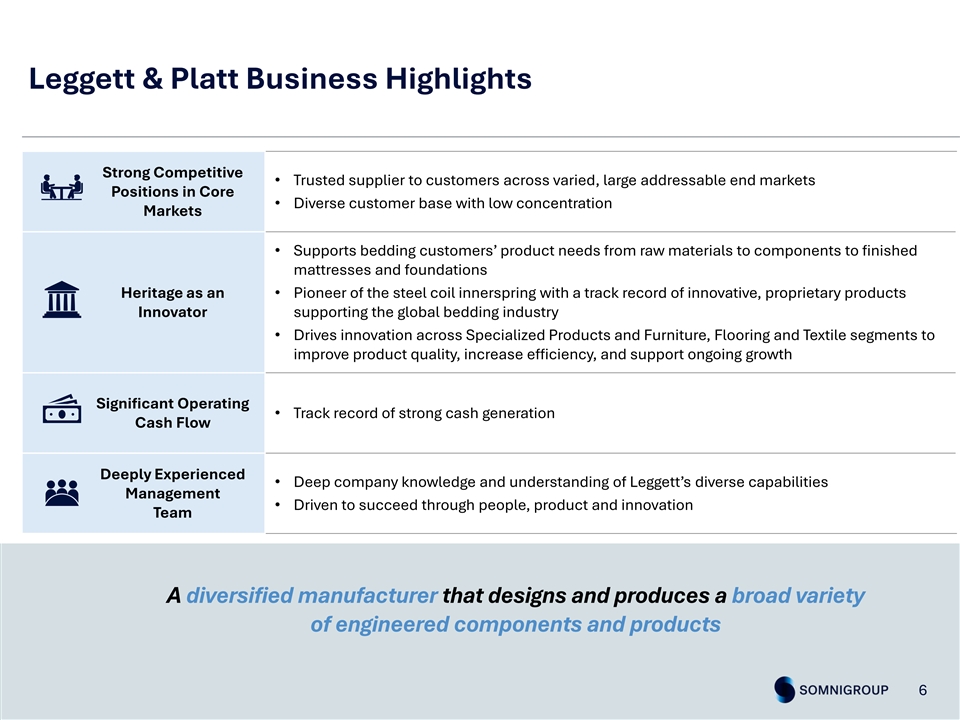

Leggett & Platt Business Highlights Strong Competitive • Trusted supplier to customers across varied, large addressable end markets Positions in Core • Diverse customer base with low concentration Markets • Supports bedding customers’ product needs from raw materials to components to finished mattresses and foundations Heritage as an • Pioneer of the steel coil innerspring with a track record of innovative, proprietary products Innovator supporting the global bedding industry • Drives innovation across Specialized Products and Furniture, Flooring and Textile segments to improve product quality, increase efficiency, and support ongoing growth Significant Operating • Track record of strong cash generation Cash Flow Deeply Experienced • Deep company knowledge and understanding of Leggett’s diverse capabilities Management • Driven to succeed through people, product and innovation Team A diversified manufacturer that designs and produces a broad variety of engineered components and products 6 6

Transaction Rationale 1 Continues Vertical Integration Strategy, Enhancing Consumer-Centric Innovation 2 Expands Addressable Market in Bedding and into Non-Bedding Industries 2 3 Reduces Financial Leverage and Drives Operating Cash Flow 2 Drives Immediate Adjusted EPS Accretion Before Synergies 4 Creates Meaningful Synergy Opportunities 5 7

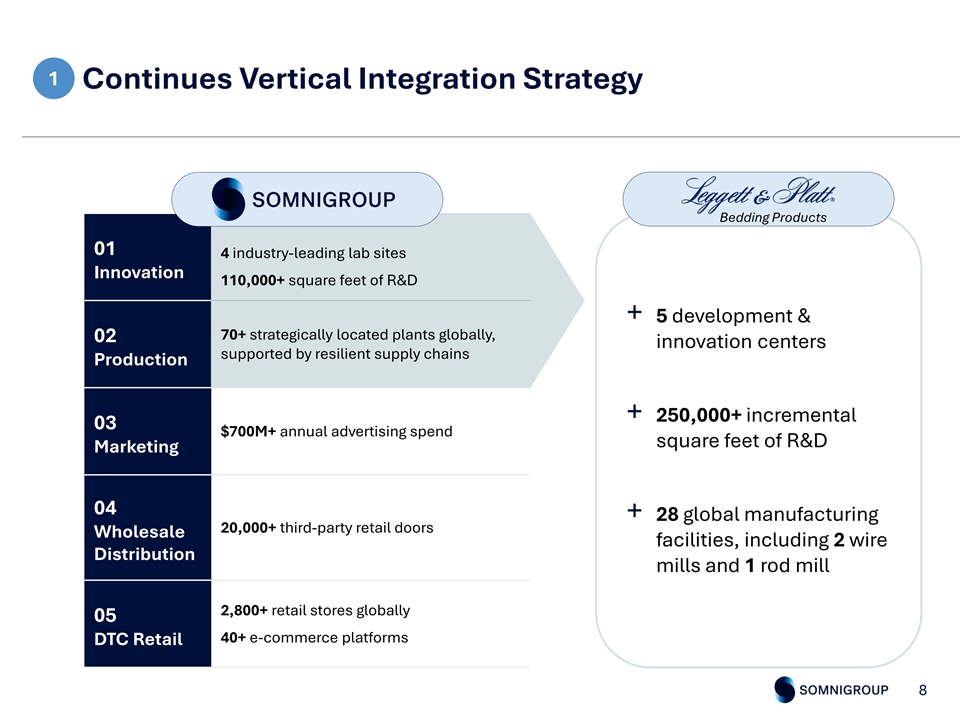

1 Continues Vertical Integration Strategy Bedding Products 01 4 industry-leading lab sites Innovation 110,000+ square feet of R&D + 5 development & 70+ strategically located plants globally, 02 innovation centers supported by resilient supply chains Production + 250,000+ incremental 03 $700M+ annual advertising spend square feet of R&D Marketing 04 + 28 global manufacturing 20,000+ third-party retail doors Wholesale facilities, including 2 wire Distribution mills and 1 rod mill 2,800+ retail stores globally 05 40+ e-commerce platforms DTC Retail 8

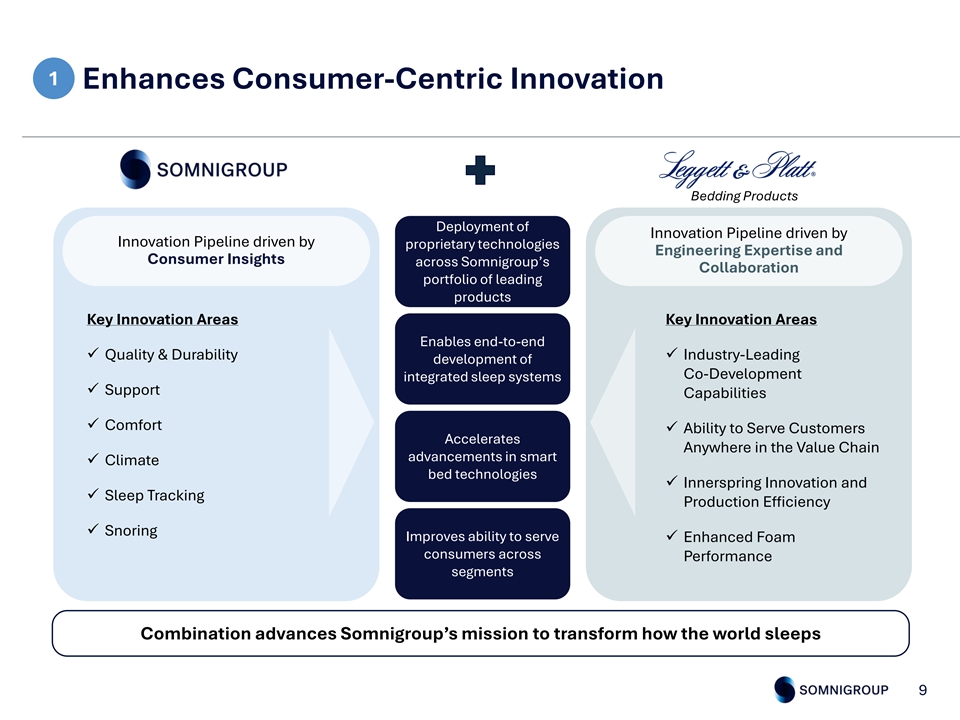

1 Enhances Consumer-Centric Innovation Bedding Products Deployment of Innovation Pipeline driven by Innovation Pipeline driven by proprietary technologies Engineering Expertise and Consumer Insights across Somnigroup’s Collaboration portfolio of leading products Key Innovation Areas Key Innovation Areas Enables end-to-end ü Quality & Durabilityü Industry-Leading development of Co-Development integrated sleep systems ü Support Capabilities ü Comfort ü Ability to Serve Customers Accelerates Anywhere in the Value Chain advancements in smart ü Climate bed technologies ü Innerspring Innovation and ü Sleep Tracking Production Efficiency ü Snoring Improves ability to serve ü Enhanced Foam consumers across Performance segments Combination advances Somnigroup’s mission to transform how the world sleeps 9

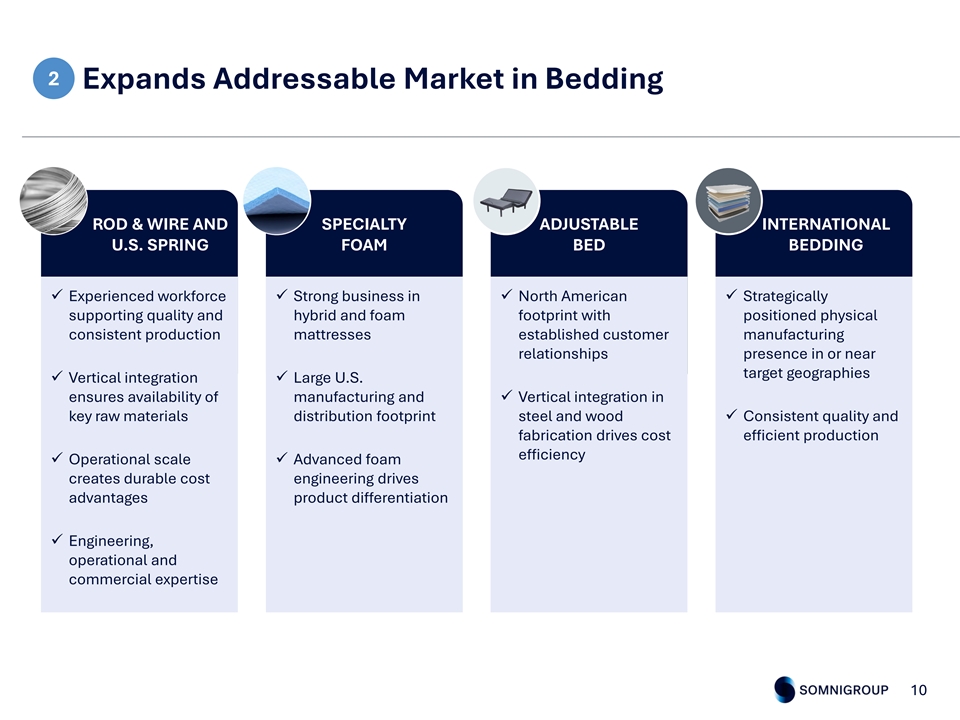

2 Expands Addressable Market in Bedding ROD & WIRE AND SPECIALTY ADJUSTABLE INTERNATIONAL U.S. SPRING FOAM BED BEDDING ü Experienced workforce ü Strong business in ü North American ü Strategically supporting quality and hybrid and foam footprint with positioned physical consistent production mattresses established customer manufacturing relationships presence in or near target geographies ü Vertical integration ü Large U.S. ensures availability of manufacturing and ü Vertical integration in key raw materials distribution footprint steel and wood ü Consistent quality and fabrication drives cost efficient production efficiency ü Operational scale ü Advanced foam creates durable cost engineering drives advantages product differentiation ü Engineering, operational and commercial expertise 10

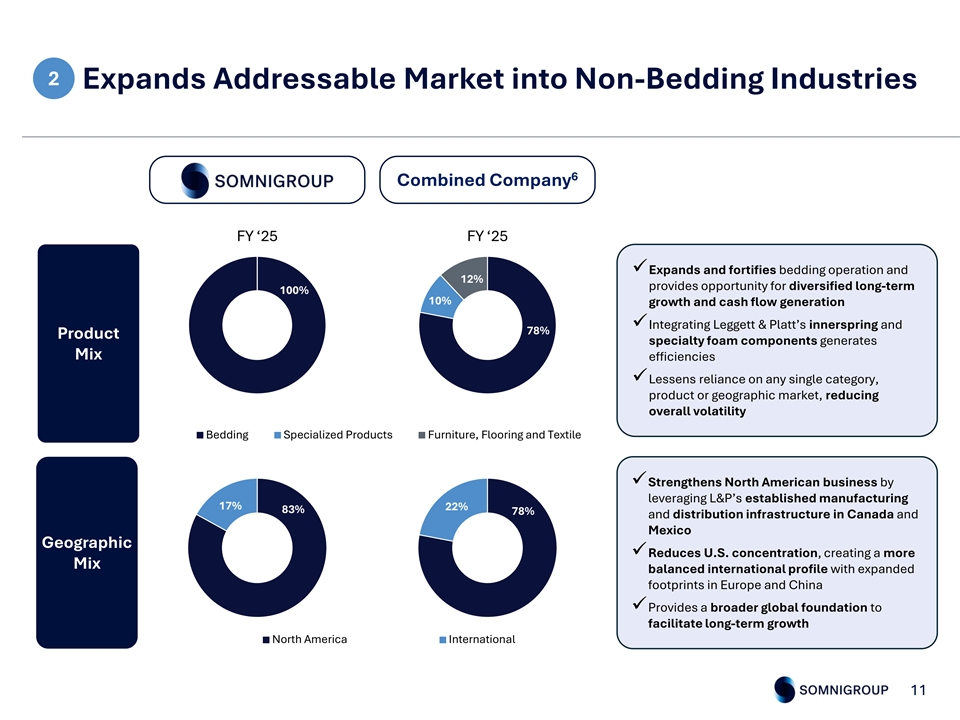

2 Expands Addressable Market into Non-Bedding Industries 6 Combined Company FY ‘25 FY ‘25 üExpands and fortifies bedding operation and 12% provides opportunity for diversified long-term 100% 10% growth and cash flow generation üIntegrating Leggett & Platt’s innerspring and 78% Product specialty foam components generates Mix efficiencies üLessens reliance on any single category, product or geographic market, reducing overall volatility Bedding Specialized Products Furniture, Flooring and Textile üStrengthens North American business by leveraging L&P’s established manufacturing 17% 22% 83% 78% and distribution infrastructure in Canada and Mexico Geographic üReduces U.S. concentration, creating a more Mix balanced international profile with expanded footprints in Europe and China üProvides a broader global foundation to facilitate long-term growth North America International 11

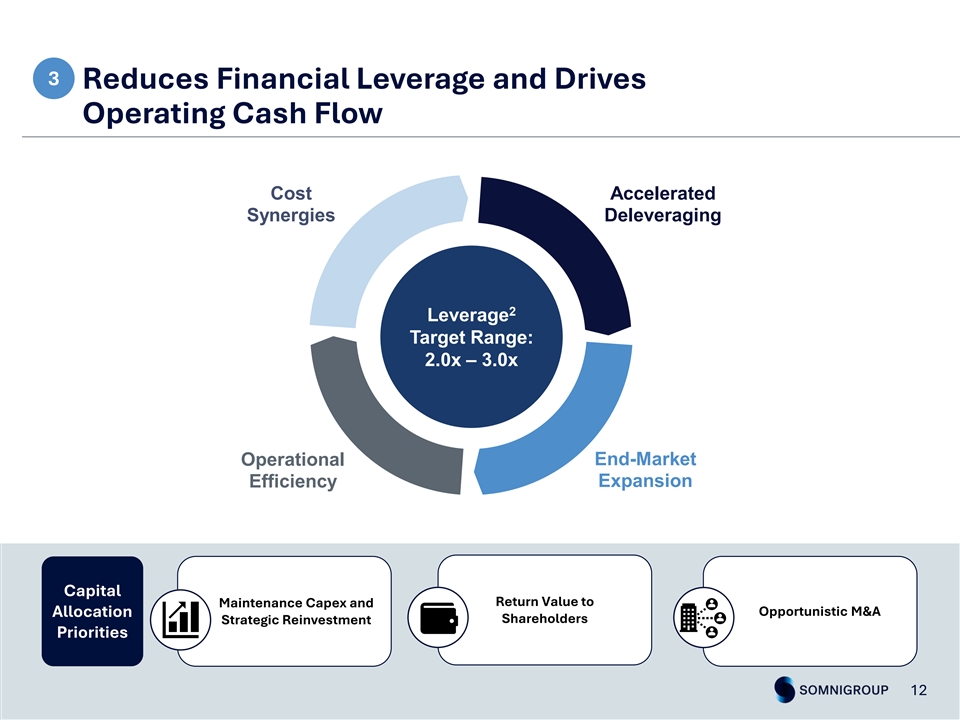

3 Reduces Financial Leverage and Drives Operating Cash Flow Cost Accelerated Synergies Deleveraging 2 Leverage Target Range: 2.0x – 3.0x End-Market Operational Expansion Efficiency Capital Return Value to Maintenance Capex and Opportunistic M&A Allocation Shareholders Strategic Reinvestment Priorities 12 12

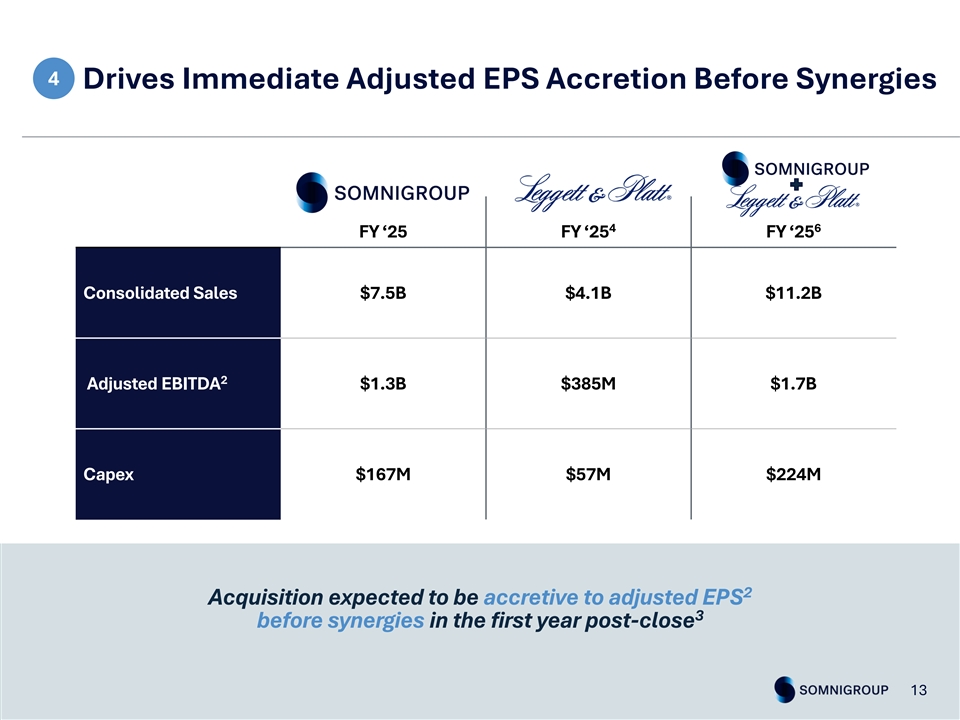

4 Drives Immediate Adjusted EPS Accretion Before Synergies 4 6 FY ‘25 FY ‘25 FY ‘25 Consolidated Sales $7.5B $4.1B $11.2B 2 Adjusted EBITDA $1.3B $385M $1.7B Capex $167M $57M $224M 2 Acquisition expected to be accretive to adjusted EPS 3 before synergies in the first year post-close 13 13

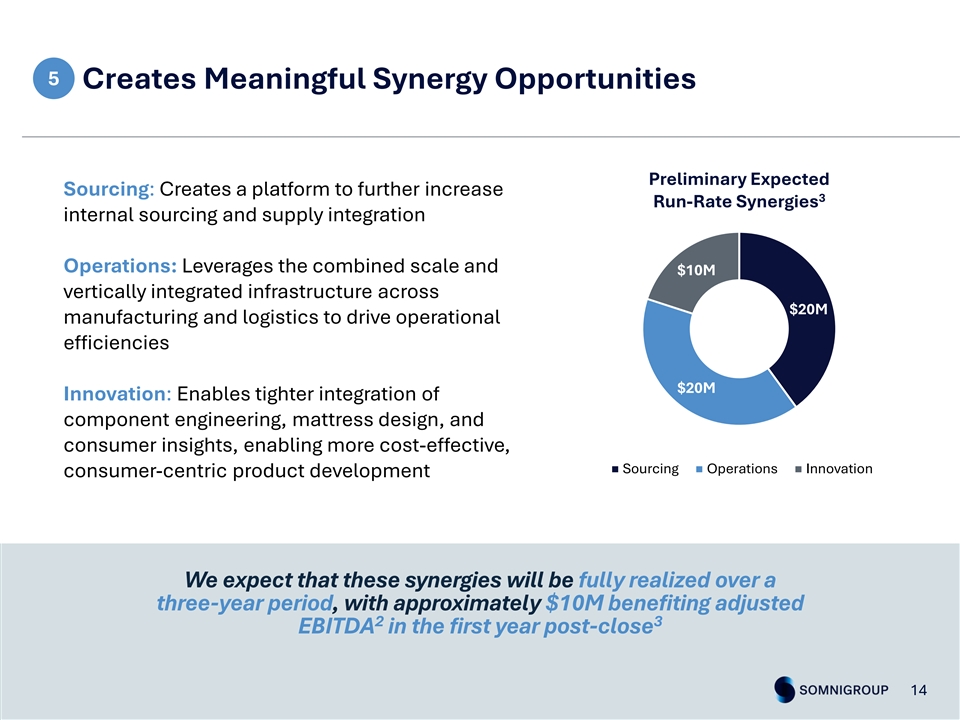

5 Creates Meaningful Synergy Opportunities Preliminary Expected Sourcing: Creates a platform to further increase 3 Run-Rate Synergies internal sourcing and supply integration Operations: Leverages the combined scale and $10M vertically integrated infrastructure across $20M manufacturing and logistics to drive operational efficiencies $20M Innovation: Enables tighter integration of component engineering, mattress design, and consumer insights, enabling more cost-effective, Sourcing Operations Innovation consumer-centric product development We expect that these synergies will be fully realized over a three-year period, with approximately $10M benefiting adjusted 2 3 EBITDA in the first year post-close 14 14

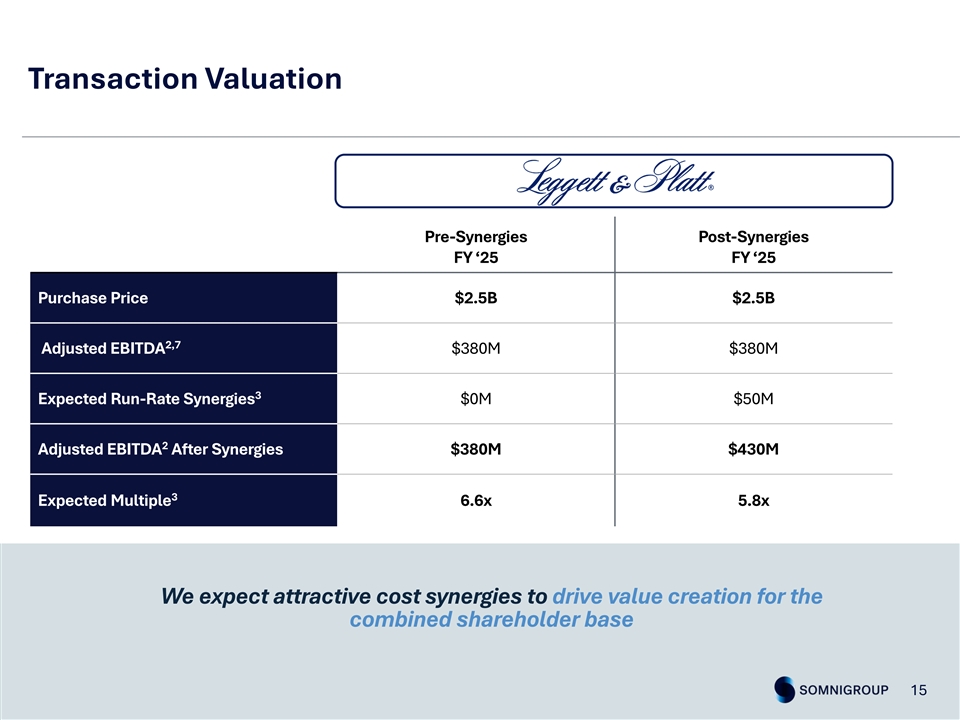

Transaction Valuation Pre-Synergies Post-Synergies FY ‘25 FY ‘25 Purchase Price $2.5B $2.5B 2,7 Adjusted EBITDA $380M $380M 3 Expected Run-Rate Synergies $0M $50M 2 Adjusted EBITDA After Synergies $380M $430M 3 Expected Multiple 6.6x 5.8x We expect attractive cost synergies to drive value creation for the combined shareholder base 15 15

The Somnigroup Investment Thesis: “The Stage Is Set – the Best Is Yet to Come” Global Scale, Vertical Integration: A leading international bedding company with leading, end-to-end capabilities from design and manufacturing to retail Omnichannel Reach & Iconic Brands: Portfolio of trusted brands and products, reaching consumers wherever they shop – online, in 2,800+ stores, and through a robust wholesale network Relentless Innovation & Consumer Insight: Industry-leading R&D, marketing investment and consumer access fuel product differentiation and demand as sleep becomes ever more central to health and wellness Operational Excellence & Leverage: Structural advantages drive superior efficiency and cash flow Resilient Cash Generation & Disciplined Capital Allocation: Robust free cash flow and strong balance sheet supports business reinvestment, acquisitions and shareholder returns Connected, Proven Leadership: Seasoned management team with track record of driving execution and growth across all business units Poised for Industry Recovery: 3 Uniquely positioned to drive value as the $120 billion global bedding market rebounds 16

APPENDIX 17

Forward Looking Statements This investor presentation contains statements that may be characterized as “forward-looking” within the meaning of the federal securities laws. Such statements might include information concerning one or more of Somnigroup International Inc.’s (“Somnigroup”) and Leggett & Platt, Incorporated’s (“Leggett”) plans, guidance, objectives, goals, strategies, and other information that is not historical information. When used in this communication, the words “will,” “targets,” “expects,” “anticipates,” “plans,” “proposed,” “intends,” “outlook,” and variations of such words or similar expressions are intended to identify forward-looking statements. These forward-looking statements include, without limitation, statements relating to Somnigroup’s expectations regarding the impact of the proposed transaction on Somnigroup's brands, products, customer base, results of operations, or financial position, its share repurchases, adjusted EPS, net leverage, operating cash flow, net income, future performance, cost and run-rate synergies, funding sources, expected capital structure, the financial impact of Leggett’s existing long-term debt, ability to deleverage after the proposed transaction, the expected timing and likelihood of completion of the proposed transaction, the integration of Leggett with Somnigroup’s business and personnel and Somnigroup's and Leggett's post-acquisition financial reporting. Any forward-looking statements contained herein are based upon current expectations and beliefs and various assumptions. There can be no assurance that these expectations and these beliefs will prove correct. Numerous factors, many of which are beyond Somnigroup’s and Leggett's control, could cause actual results to differ materially from any that may be expressed herein as forward-looking statements. These potential risks include risks associated with Leggett’s ongoing operations; the ability to obtain the requisite Leggett shareholder approval; the risk that Somnigroup or Leggett may be unable to obtain governmental and regulatory approvals required for the proposed transaction (and the risk that such approvals may result in the imposition of conditions that could adversely affect the combined company or the expected benefits of the proposed transaction); the risk that an event, change or other circumstance could give rise to the termination of the proposed transaction; the risk of delays in completing the proposed transaction; the ability to successfully integrate Leggett into Somnigroup's operations and realize synergies from the proposed transaction and the expected run-rate of such synergies; the possibility that the expected benefits of the acquisition are not realized when expected or at all; the risk that any announcement relating to the proposed transaction could have adverse effects on the market price of Somnigroup’s or Leggett’s common stock; the risk of litigation related to the proposed transaction; the diversion of management time from ongoing business operations and opportunities as a result of the proposed transaction; the risk of adverse reactions or changes to business or employee relationships, including those resulting from the announcement or completion of the proposed transaction; general economic, financial and industry conditions, particularly conditions relating to the financial performance and related credit issues present in the retail sector, as well as consumer confidence and the availability of consumer financing; the impact of the macroeconomic environment in both the U.S. and internationally on Somnigroup and Leggett; uncertainties arising from national and global events; industry competition; the effects of consolidation of retailers on revenues and costs; consumer acceptance and changes in demand for Somnigroup’s and Leggett's products; and other risks inherent in Somnigroup’s and Leggett’s businesses. All such factors are difficult to predict, are beyond Somnigroup’s and Leggett’s control, and are subject to additional risks and uncertainties, including those detailed in Somnigroup’s annual report on Form 10-K for the year ended December 31, 2025, and those detailed in Leggett’s annual report on Form 10-K for the year ended December 31, 2025. These risks, as well as other risks related to the proposed transaction, will be included in the Form S-4 and proxy statement/prospectus (as defined below) that Somnigroup and Leggett intend to file with the United States Securities and Exchange Commission (the “SEC”) in connection with the proposed transaction. There may be other factors that may cause Somnigroup’s and Leggett's actual results to differ materially from the forward-looking statements. Neither Somnigroup nor Leggett undertakes any obligation to publicly update any forward-looking statement, whether as a result of new information, future events or otherwise, except as required by law. 18

Forward Looking Statements Note Regarding Historical Financial Information: In this investor presentation we provide or refer to certain historical information for Somnigroup and Leggett. For a more detailed discussion of Somnigroup’s and Leggett’s financial performance, please refer to Somnigroup’s and Leggett’s SEC filings. Note Regarding Trademarks, Trade Names, and Service Marks: TEMPUR®, Tempur-Pedic®, the Tempur-Pedic & Reclining Figure Design®, Tempur Breeze, ActiveBreeze®, TEMPUR-Adapt®, TEMPUR-ProAdapt®, TEMPUR-LuxeAdapt®, TEMPUR-ProBreeze®, TEMPURLuxeBreeze®, TEMPUR-Cloud®, TEMPUR-Contour , TEMPUR-Rhapsody , TEMPUR-Flex®, THE GRANDBED BY Tempur-Pedic®, TEMPUR- Ergo®, TEMPUR-UP , TEMPUR-Neck , TEMPUR-Symphony, TEMPUR-Comfort , TEMPUR-Traditional , TEMPUR-Home , Sealy®, Sealy Posturepedic®, Stearns & Foster®, Intellicoil , PrecisionFit , COCOON by Sealy , SealyChill , Mattress Firm®, and Sleepy’s® are trademarks, trade names, or service marks of Somnigroup International Inc., and/or its subsidiaries. All other trademarks, trade names, and service marks in this presentation are the property of the respective owners. 19

Legends No Offer or Solicitation This investor presentation is not intended to be, and shall not constitute, an offer to sell, buy or exchange or the solicitation of an offer to sell, buy or exchange any securities, or a solicitation of any vote or approval, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offering of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933, as amended. Additional Information and Where to Find It In connection with the proposed transaction, Somnigroup intends to file with the SEC a registration statement on Form S-4 (the “Form S-4”) that will include a proxy statement of Leggett and that will also constitute a prospectus of Somnigroup with respect to the shares of Somnigroup common stock to be issued in the proposed transaction (the “proxy statement/prospectus”). The definitive proxy statement/prospectus (if and when available) will be filed with the SEC by, and mailed to shareholders of, Leggett. Each of Somnigroup and Leggett may also file other relevant documents with the SEC regarding the proposed transaction. This investor presentation is not a substitute for the Form S-4, the proxy statement/prospectus or any other document that Somnigroup or Leggett may file with the SEC in connection with the proposed transaction. INVESTORS AND SECURITY HOLDERS OF SOMNIGROUP AND LEGGETT ARE URGED TO READ THE FORM S-4, THE PROXY STATEMENT/PROSPECTUS AND ANY OTHER RELEVANT DOCUMENTS FILED WITH THE SEC, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THOSE DOCUMENTS, CAREFULLY IN THEIR ENTIRETY IF AND WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED TRANSACTION. Investors and security holders will be able to obtain copies of these documents (if and when available), as well as other filings containing information about Somnigroup and Leggett, free of charge on the SEC's website at www.sec.gov. Copies of the documents filed with, or furnished to, the SEC by Somnigroup will be available free of charge on Somnigroup's website at https://somnigroup.com/investor-resources/financials/sec-filings/default.aspx. Copies of the documents filed with, or furnished to, the SEC by Leggett will be available free of charge on Leggett’s website at https://leggett.gcs-web.com/financials/sec-filings. The information included on, or accessible through, Somnigroup’s or Leggett’s website is not incorporated by reference into this investor presentation. Participants in Solicitation Somnigroup, Leggett and certain of their respective directors and executive officers may be deemed to be participants in the solicitation of proxies with respect to the proposed transaction under the rules of the SEC. You can find information about Somnigroup's executive officers and directors in Somnigroup's definitive proxy statement filed with the SEC on March 31, 2026, under the section entitled “Proposal No. 1 — Election of Directors – Executive Officers,” “Proposal No. 1 — Election of Directors - Nominees to Board of Directors,” “Stock Ownership – Stock Ownership of Certain Beneficial Owners and Directors and Executive Officers,” “Executive Compensation and Related Information - Compensation of Executive Officers” and “Director Compensation.” You can find information about Leggett’s executive officers and directors in Leggett’s Annual Report on Form 10-K for the year ended December 31, 2025, under the sections entitled “Supplemental Information: Information about our Executive Officers” and “Directors, Executive Officers and Corporate Governance,” and in Leggett’s definitive proxy statement filed with the SEC on April 7, 2026, under the sections entitled “Corporate Governance and Board Matters - Director Compensation,” “Proposals to be Voted On at the Annual Meeting - Proposal One: Election of Directors,” “Executive Compensation and Related Matters - Compensation Discussion & Analysis” and “Security Ownership - Security Ownership of Directors and Executive Officers.” Additional information regarding the interests of the participants in the solicitation of proxies will be included in the Form S-4, the proxy statement/prospectus and other relevant materials to be filed with the SEC if and when they become available. You should read the Form S-4 and the proxy statement/prospectus carefully when available before making any voting or investment decisions. You may obtain free copies of these documents using the sources indicated above. 20

Use of Non-GAAP Financial Measures Information In this investor presentation and certain of its press releases and SEC filings, Somnigroup provides information regarding EBITDA, adjusted EBITDA, and leverage, which are not recognized terms under U.S. Generally Accepted Accounting Principles (“GAAP”) and do not purport to be alternatives to net income and earnings per share as a measure of operating performance, an alternative to cash provided by operating activities as a measure of liquidity, or an alternative to total debt. Also, Leggett provides information regarding Adjusted EBITDA, which is not recognized term under GAAP and does not purport to be an alternative to net income. Somnigroup and Leggett believe these non-GAAP measures provide investors with performance measures that better reflect Somnigroup’s and Leggett’s underlying operations and trends, including trends in changes in margin and operating expenses, providing a perspective not immediately apparent from net income and operating income. The adjustments each company’s management makes to derive the non-GAAP measures include adjustments to exclude items that may cause short-term fluctuations in the nearest GAAP measure, but which management does not consider to be the fundamental attributes or primary drivers of Somnigroup’s or Leggett’s businesses, as applicable. Somnigroup and Leggett believe that exclusion of these items assists in providing a more complete understanding of their respective underlying results from continuing operations and trends, and each company’s management uses these measures along with the corresponding GAAP financial measures to manage their respective businesses, to evaluate its consolidated and business segment performance compared to prior periods and the marketplace, to establish operational goals and management incentive goals, and to provide continuity to investors for comparability purposes. Limitations associated with the use of these non-GAAP measures include that these measures do not present all the amounts associated with Somnigroup’s or Leggett’s results as determined in accordance with GAAP. These non-GAAP measures should be considered supplemental in nature and should not be construed as more significant than comparable measures defined by GAAP. Because not all companies use identical calculations, these presentations may not be comparable to other similarly titled measures of other companies. For more information regarding the use of these non-GAAP financial measures, please refer to the reconciliations on the following pages and Somnigroup’s and Leggett’s SEC filings. EBITDA and Adjusted EBITDA A reconciliation of Somnigroup’s GAAP net income to EBITDA and adjusted EBITDA per credit facility is provided on the subsequent slides. Somnigroup management believes that the use of EBITDA and adjusted EBITDA per credit facility provides investors with useful information with respect to Somnigroup’s operating performance and comparisons from period to period as well as Somnigroup’s compliance with requirements under its credit agreement. A reconciliation of Leggett’s GAAP net income to EBITDA and adjusted EBITDA is provided on the subsequent slides. Leggett management believes that the use of EBITDA and adjusted EBITDA provides investors with useful information with respect to Leggett’s operating performance and comparisons from period to period. Leverage Consolidated indebtedness less netted cash to adjusted EBITDA per credit facility, which Somnigroup may refer to as leverage, is provided on a subsequent slide and is calculated by dividing consolidated indebtedness less netted cash, as defined by Somnigroup’s senior secured credit facility, by adjusted EBITDA per credit facility. Somnigroup provides this as supplemental information to investors regarding Somnigroup’s operating performance and comparisons from period to period, as well as general information about Somnigroup 's progress in managing its leverage. 21

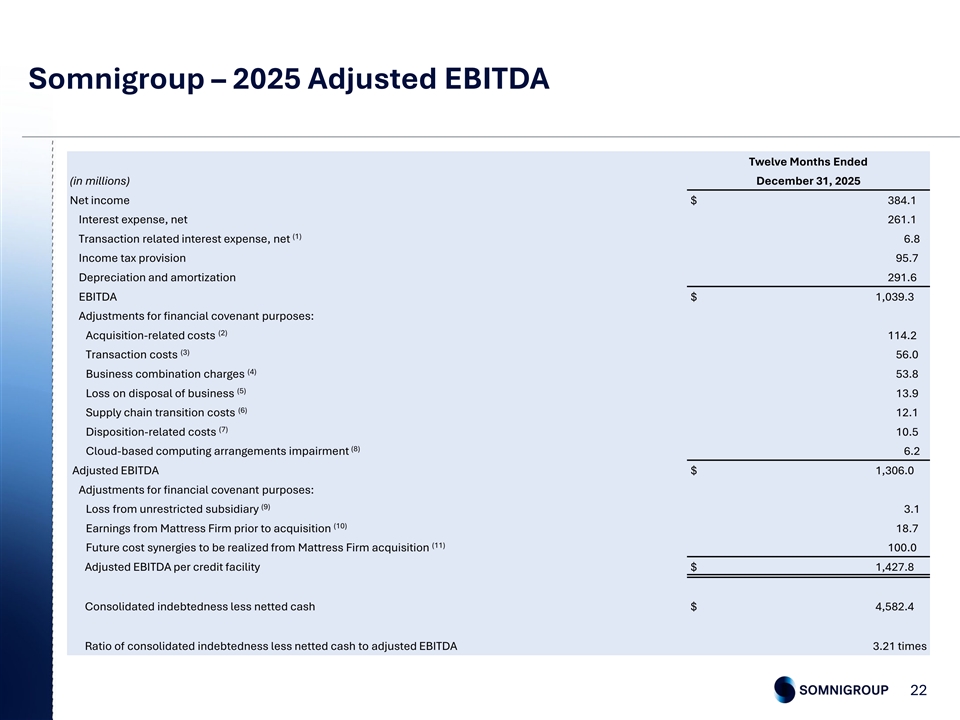

Somnigroup – 2025 Adjusted EBITDA Twelve Months Ended (in millions) December 31, 2025 Net income $ 384.1 Interest expense, net 261.1 (1) Transaction related interest expense, net 6.8 Income tax provision 95.7 Depreciation and amortization 291.6 EBITDA $ 1,039.3 Adjustments for financial covenant purposes: (2) Acquisition-related costs 114.2 (3) Transaction costs 56.0 (4) Business combination charges 53.8 (5) Loss on disposal of business 13.9 (6) Supply chain transition costs 12.1 (7) Disposition-related costs 10.5 (8) Cloud-based computing arrangements impairment 6.2 Adjusted EBITDA $ 1,306.0 Adjustments for financial covenant purposes: (9) Loss from unrestricted subsidiary 3.1 (10) Earnings from Mattress Firm prior to acquisition 18.7 (11) Future cost synergies to be realized from Mattress Firm acquisition 100.0 Adjusted EBITDA per credit facility $ 1,427.8 Consolidated indebtedness less netted cash $ 4,582.4 Ratio of consolidated indebtedness less netted cash to adjusted EBITDA 3.21 times 22

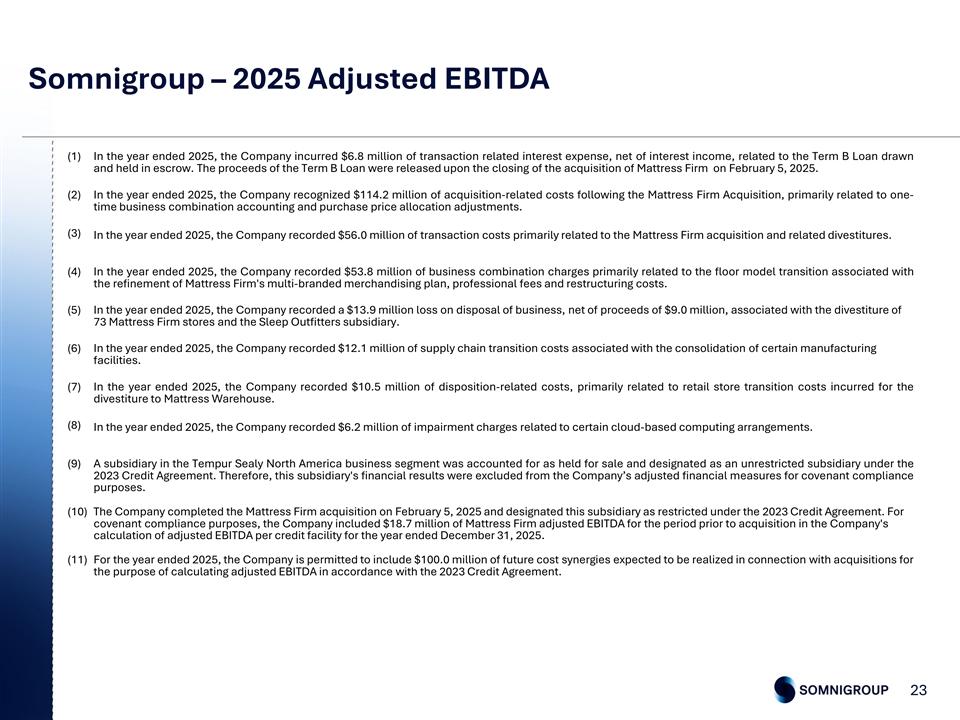

Somnigroup – 2025 Adjusted EBITDA (1) In the year ended 2025, the Company incurred $6.8 million of transaction related interest expense, net of interest income, related to the Term B Loan drawn and held in escrow. The proceeds of the Term B Loan were released upon the closing of the acquisition of Mattress Firm on February 5, 2025. (2) In the year ended 2025, the Company recognized $114.2 million of acquisition-related costs following the Mattress Firm Acquisition, primarily related to one- time business combination accounting and purchase price allocation adjustments. (3) In the year ended 2025, the Company recorded $56.0 million of transaction costs primarily related to the Mattress Firm acquisition and related divestitures. (4) In the year ended 2025, the Company recorded $53.8 million of business combination charges primarily related to the floor model transition associated with the refinement of Mattress Firm's multi-branded merchandising plan, professional fees and restructuring costs. (5) In the year ended 2025, the Company recorded a $13.9 million loss on disposal of business, net of proceeds of $9.0 million, associated with the divestiture of 73 Mattress Firm stores and the Sleep Outfitters subsidiary. (6) In the year ended 2025, the Company recorded $12.1 million of supply chain transition costs associated with the consolidation of certain manufacturing facilities. (7) In the year ended 2025, the Company recorded $10.5 million of disposition-related costs, primarily related to retail store transition costs incurred for the divestiture to Mattress Warehouse. (8) In the year ended 2025, the Company recorded $6.2 million of impairment charges related to certain cloud-based computing arrangements. (9) A subsidiary in the Tempur Sealy North America business segment was accounted for as held for sale and designated as an unrestricted subsidiary under the 2023 Credit Agreement. Therefore, this subsidiary's financial results were excluded from the Company’s adjusted financial measures for covenant compliance purposes. (10) The Company completed the Mattress Firm acquisition on February 5, 2025 and designated this subsidiary as restricted under the 2023 Credit Agreement. For covenant compliance purposes, the Company included $18.7 million of Mattress Firm adjusted EBITDA for the period prior to acquisition in the Company's calculation of adjusted EBITDA per credit facility for the year ended December 31, 2025. (11) For the year ended 2025, the Company is permitted to include $100.0 million of future cost synergies expected to be realized in connection with acquisitions for the purpose of calculating adjusted EBITDA in accordance with the 2023 Credit Agreement. 23

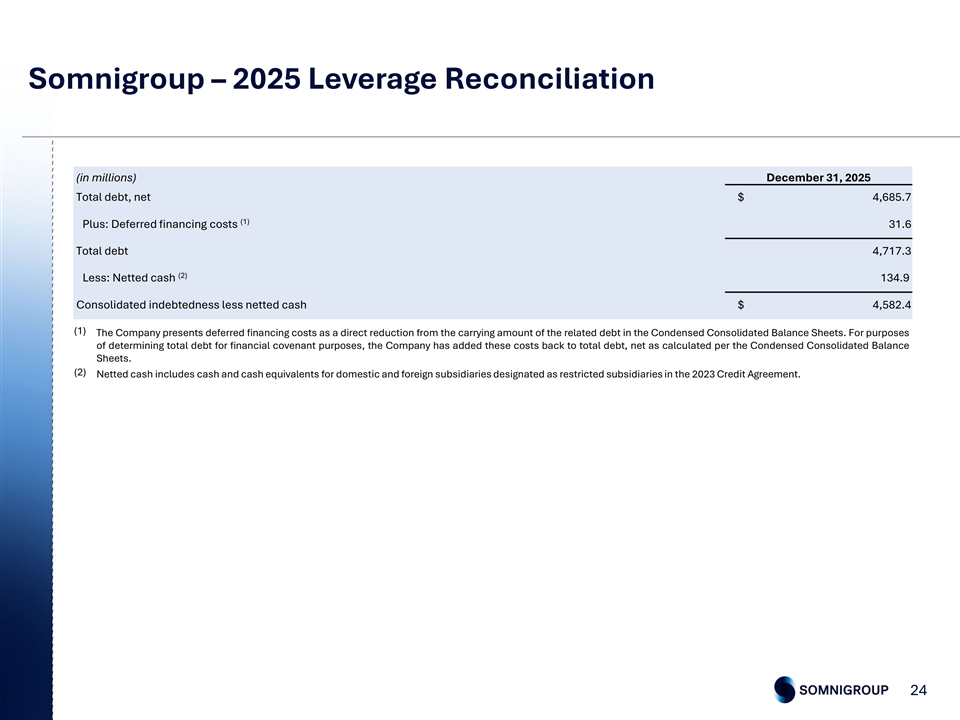

Somnigroup – 2025 Leverage Reconciliation (in millions) December 31, 2025 Total debt, net $ 4,685.7 (1) Plus: Deferred financing costs 31.6 Total debt 4,717.3 (2) Less: Netted cash 134.9 Consolidated indebtedness less netted cash $ 4,582.4 (1) The Company presents deferred financing costs as a direct reduction from the carrying amount of the related debt in the Condensed Consolidated Balance Sheets. For purposes of determining total debt for financial covenant purposes, the Company has added these costs back to total debt, net as calculated per the Condensed Consolidated Balance Sheets. (2) Netted cash includes cash and cash equivalents for domestic and foreign subsidiaries designated as restricted subsidiaries in the 2023 Credit Agreement. 24

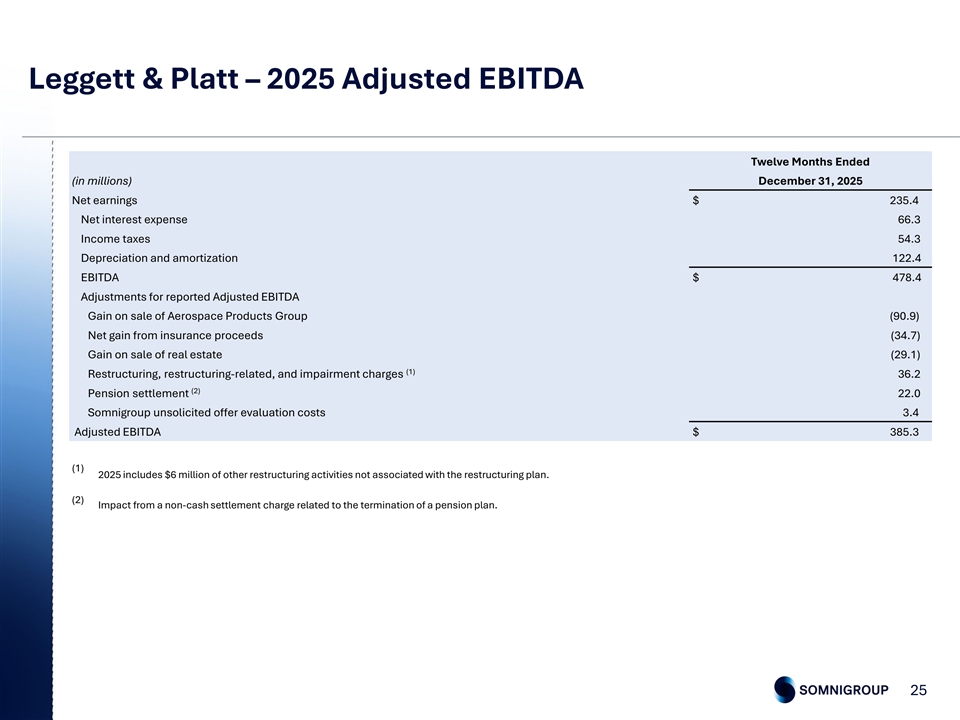

Leggett & Platt – 2025 Adjusted EBITDA Twelve Months Ended (in millions) December 31, 2025 Net earnings $ 235.4 Net interest expense 66.3 Income taxes 54.3 Depreciation and amortization 122.4 EBITDA $ 478.4 Adjustments for reported Adjusted EBITDA Gain on sale of Aerospace Products Group (90.9) Net gain from insurance proceeds (34.7) Gain on sale of real estate (29.1) (1) Restructuring, restructuring-related, and impairment charges 36.2 (2) Pension settlement 22.0 Somnigroup unsolicited offer evaluation costs 3.4 Adjusted EBITDA $ 385.3 (1) 2025 includes $6 million of other restructuring activities not associated with the restructuring plan. (2) Impact from a non-cash settlement charge related to the termination of a pension plan. 25

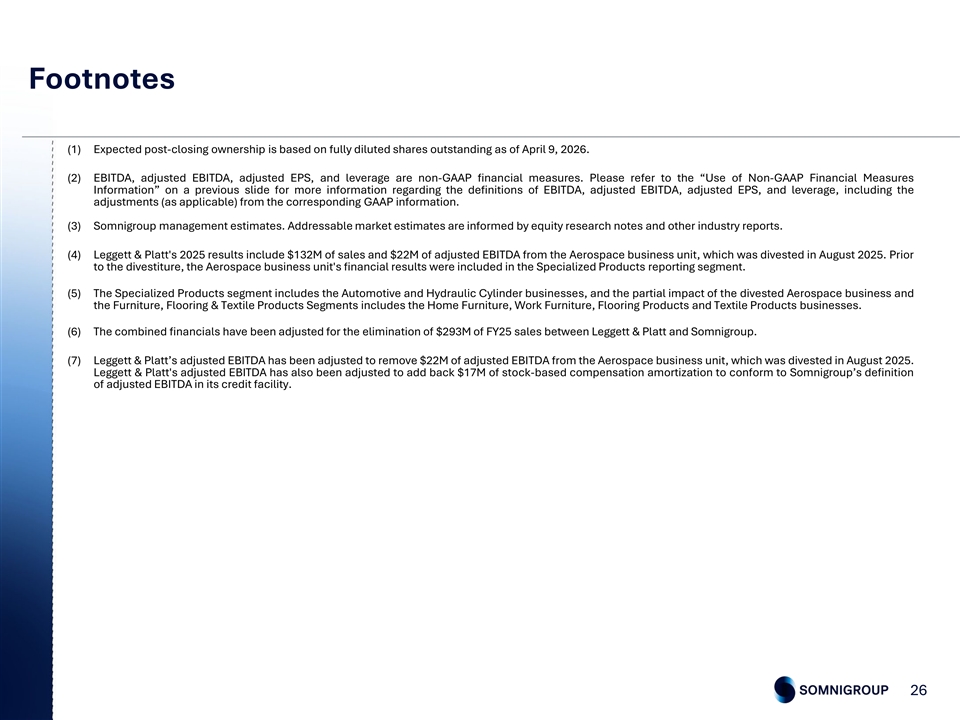

Footnotes (1) Expected post-closing ownership is based on fully diluted shares outstanding as of April 9, 2026. (2) EBITDA, adjusted EBITDA, adjusted EPS, and leverage are non-GAAP financial measures. Please refer to the “Use of Non-GAAP Financial Measures Information” on a previous slide for more information regarding the definitions of EBITDA, adjusted EBITDA, adjusted EPS, and leverage, including the adjustments (as applicable) from the corresponding GAAP information. (3) Somnigroup management estimates. Addressable market estimates are informed by equity research notes and other industry reports. (4) Leggett & Platt's 2025 results include $132M of sales and $22M of adjusted EBITDA from the Aerospace business unit, which was divested in August 2025. Prior to the divestiture, the Aerospace business unit's financial results were included in the Specialized Products reporting segment. (5) The Specialized Products segment includes the Automotive and Hydraulic Cylinder businesses, and the partial impact of the divested Aerospace business and the Furniture, Flooring & Textile Products Segments includes the Home Furniture, Work Furniture, Flooring Products and Textile Products businesses. (6) The combined financials have been adjusted for the elimination of $293M of FY25 sales between Leggett & Platt and Somnigroup. (7) Leggett & Platt’s adjusted EBITDA has been adjusted to remove $22M of adjusted EBITDA from the Aerospace business unit, which was divested in August 2025. Leggett & Platt's adjusted EBITDA has also been adjusted to add back $17M of stock-based compensation amortization to conform to Somnigroup’s definition of adjusted EBITDA in its credit facility. 26