| Feldman Financial Advisors, Inc. | ||

| 8804 Mirador Place | ||

| McLean, VA 22102 | ||

| (202) 467-6862 | ||

|

Everett Cash Mutual Insurance Company Everett, Pennsylvania

Conversion Valuation Appraisal Report Valued as of September 17, 2025

Prepared By

Feldman Financial Advisors, Inc. McLean, Virginia

|

| Feldman Financial Advisors, Inc. | ||

| 8804 Mirador Place | ||

| McLean, VA 22102 | ||

| (202) 467-6862 | ||

September 17, 2025

Board of Directors

Everett Cash Mutual Insurance Company

10591 Lincoln Highway

Everett, Pennsylvania 61201

Members of the Board:

At your request, we have completed and hereby provide an independent appraisal (the “Appraisal”) of the estimated consolidated pro forma market value of Everett Cash Mutual Insurance Company (“ECM” or the “Company”) as of September 17, 2025 (the “Valuation Date”). Pursuant to a Plan of Conversion from the Mutual to Stock Form (the “Plan of Conversion”) to be adopted by ECM’s Board of Directors, ECM plans to convert from a Pennsylvania mutual insurance company to a Pennsylvania stock insurance company (the “Conversion”) under the Pennsylvania Insurance Company Mutual-to-Stock Conversion Act (the “Act”). Simultaneously, ECM will issue and sell all of its common stock to Old Republic Specialty Insurance Group, Inc. (“Old Republic Specialty”), a wholly owned subsidiary of Old Republic International Corporation (“Old Republic”). Old Republic Specialty will acquire all of the authorized common stock of the converted ECM for an amount of cash equal to at least the minimum of the valuation range (“Valuation Range”) established herein by the statutorily required and independently determined Appraisal. As a result of the foregoing, ECM will become an indirect wholly owned subsidiary of Old Republic.

ECM’s eligible policyholders and other eligible subscribers will receive the right to purchase shares of Old Republic common stock in a stock offering (the “Offering”) in an aggregate amount between the minimum and maximum of the Valuation Range at a purchase price per share discount of from 30% to 35% of the volume-weighted average trading price of Old Republic common stock. In the event that the aggregate amount of stock sold in the Offering is less than the minimum of the Valuation Range, Old Republic will contribute cash equal to not less than the difference between the minimum of the Valuation Range and the aggregate amount of stock sold in the Offering to fund the acquisition of all of the common stock of ECM as converted.

In accordance with Section 914(A)-d of the Act, the aggregate price of the capital stock issued in the Conversion shall be equal to the estimated pro forma market value of the converted stock company based upon an independent evaluation by a qualified expert. Furthermore, as permitted by Section 914(A)-d of the Act, the pro forma market value may be that value that is estimated to be necessary to attract full subscription for the shares and may be stated as a range of pro forma market value. Pursuant to the requirement in Section 913-A(b)(1), the Appraisal must be included as part of the Plan of Conversion filed with the Commissioner of the Pennsylvania Insurance Department.

FELDMAN FINANCIAL ADVISORS, INC.

Board of Directors

Everett Cash Mutual Insurance Company

September 17, 2025

Page Two

Feldman Financial Advisors, Inc. (“Feldman Financial”) is a financial consulting and advisory firm that specializes in financial valuations and analyses of business enterprises and securities in the financial services industry. The background of Feldman Financial is presented in Exhibit I. In preparing the Appraisal, we conducted an analysis of ECM that included discussions with the Company’s management. We reviewed the unaudited financial statements of ECM as prepared under generally accepted accounting principles (“GAAP”) for the years ended December 31, 2023 and 2024. We also reviewed statutory financial data of ECM for the years ended December 31, 2023 and 2024 and the six months ended June 30, 2025. In addition, where appropriate, we considered information based on other available published sources that we believe are reliable; however, we cannot guarantee the accuracy and completeness of such information.

In preparing the Appraisal, we also reviewed and analyzed: (i) financial and operating information with respect to the business, operations, and prospects of ECM as furnished to us by the Company; (ii) publicly available information concerning the Company that we believe to be relevant to our analysis; (iii) a comparison of the historical financial results and present financial condition of the Company with those of selected publicly traded insurance companies that we deemed relevant; and (iv) financial performance and market valuation data of certain publicly traded insurance industry aggregates as provided by industry sources.

The Appraisal is based on the Company’s representation that the information and financial data furnished to us by the Company and its independent auditors are truthful, accurate, and complete. We did not independently verify the financial statements and other information provided by the Company and its independent auditors, nor did we independently value the assets or liabilities of the Company. The Appraisal considers the Company only as a going concern on a standalone basis and should not be considered as an indication of the liquidation value of the Company.

It is our opinion that, as of September 17, 2025, the estimated consolidated pro forma market value of the Company was $180,000,000 with a corresponding Valuation Range of $153,000,000 to $207,000,000. The Valuation Range was based upon a 15% decrease from the midpoint of $180,000,000 to determine the minimum and a 15% increase from the midpoint to establish the maximum.

Our Appraisal is not intended, and must not be construed, to be a recommendation of any kind as to the advisability of purchasing shares of Old Republic common stock in the Offering. The Appraisal considers the Company only as a going concern and should not be considered as an indication of its liquidation value. The Appraisal is necessarily based upon estimates of a number of matters, all of which are subject to change from time to time.

FELDMAN FINANCIAL ADVISORS, INC.

Board of Directors

Everett Cash Mutual Insurance Company

September 17, 2025

Page Three

The Appraisal reflects only the Valuation Range, as of the Valuation Date, of the estimated consolidated pro forma market value of the Company as converted and does not take into account any trading activity with respect to the purchase and sale of Old Republic common stock in the secondary market on the date of issuance of such securities or at any time thereafter following the completion of the Offering. Feldman Financial is not a seller of securities within the meaning of any federal or state securities laws, and any report prepared by Feldman Financial shall not be used as an offer or solicitation with respect to the purchase or sale of any securities.

The Valuation Range reported herein may be updated as necessary and required. These updates will consider, among other factors, any developments or changes in the Company’s operating performance, financial condition, or management policies, and current conditions in the securities markets for insurance company common stocks. Should any such new developments or changes be material, in our opinion, to the estimated consolidated pro forma market value of the Company, appropriate adjustments to the Valuation Range will be made. The reasons for any such adjustments will be explained in detail at that time.

| Respectfully submitted, | |

| Feldman Financial Advisors, Inc. | |

| /s/ Trent R. Feldman | |

| Trent R. Feldman, President | |

| /s/ Peter W. L. Williams | |

| Peter W. L. Williams, Principal |

FELDMAN FINANCIAL ADVISORS, INC.

TABLE OF CONTENTS

| CHAPTER | PAGE | |||

| INTRODUCTION | 1 | |||

| I. | BUSINESS OF EVERETT CASH MUTUAL INSURANCE COMPANY | 2 | ||

| General Overview | 2 | |||

| Financial Condition | 8 | |||

| Income and Expense Trends | 10 | |||

| II. | INDUSTRY FUNDAMENTALS | 19 | ||

| Financial Strength Ratings by A.M. Best | 19 | |||

| Industry Performance and Investment Outlook | 20 | |||

| III. | COMPARISONS WITH PUBLICLY TRADED COMPANIES | 21 | ||

| General Overview | 21 | |||

| Selection Criteria | 22 | |||

| Summary Profiles of the Comparative Group Companies | 25 | |||

| Recent Financial Comparisons | 30 | |||

| IV. | MARKET VALUE ADJUSTMENTS | 34 | ||

| General Overview | 34 | |||

| Earnings Prospects | 34 | |||

| Management | 35 | |||

| Liquidity of the Issue | 35 | |||

| Dividend Policy | 36 | |||

| Subscription Interest | 36 | |||

| Stock Market Conditions | 36 | |||

| New Issue Discount | 38 | |||

| Adjustments Conclusion | 40 | |||

| Valuation Approach | 40 | |||

| Valuation Conclusion | 41 | |||

| APPENDIX – EXHIBITS | ||||

| I | Background of Feldman Financial Advisors, Inc. | I-1 | ||

| II | Statement of Contingent and Limiting Conditions | II-1 | ||

| III-1 | Consolidated Balance Sheets | III-1 | ||

| III-2 | Consolidated Income Statements | III-2 | ||

| III-3 | Consolidated Investments and Cash Portfolio | III-3 | ||

| IV-1 | Statutory Financial Data – Everett Cash Mutual Insurance Company | IV-1 | ||

| IV-1 | Statutory Financial Data – American Reliable Insurance Company | IV-6 | ||

| IV-1 | Statutory Financial Data – 1st Choice Advantage Insurance Company, Inc. | IV-11 | ||

| IV-1 | Statutory Financial Data – Ever-Greene Mutual Insurance Company | IV-16 | ||

| V-1 | Financial Performance Data for Public P&C Insurance Companies | V-1 | ||

| V-2 | Market Valuation Data for Public P&C Insurance Companies | V-3 | ||

| VI-1 | Pro Forma Assumptions for Conversion Valuation | VI-1 | ||

| VI-2 | Pro Forma Conversion Valuation Range | VI-2 | ||

i

FELDMAN FINANCIAL ADVISORS, INC.

LIST OF TABLES

| CHAPTER | PAGE | ||||

| I. | BUSINESS OF EVERETT CASH MUTUAL INSURANCE COMPANY | ||||

| Table 1 | Corporate Organizational Structure | 3 | |||

| Table 2 | Selected Financial Condition Data | 8 | |||

| Table 3 | Consolidated Income Statement Data | 11 | |||

| Table 4 | Consolidated Underwriting Performance Data | 12 | |||

| Table 5 | Consolidated Direct Premiums Written by Line of Business | 13 | |||

| Table 6 | Consolidated Direct Premiums Written by State | 14 | |||

| Table 7 | Statutory Financial Overview | 18 | |||

| III. | COMPARISONS WITH PUBLICLY TRADED COMPANIES | ||||

| Table 8 | General Operating Summary of the Comparative Group | 24 | |||

| Table 9 | Comparative Financial Condition Data | 31 | |||

| Table 10 | Comparative Operating Performance Data | 33 | |||

| IV. | MARKET VALUE ADJUSTMENTS | ||||

| Table 11 | Selected Stock Market Index Performance | 37 | |||

| Table 12 | Subscription-Based Insurance Company Demutualizations | 39 | |||

| Table 13 | Comparative Market Valuation Analysis | 42 | |||

ii

FELDMAN FINANCIAL ADVISORS, INC.

INTRODUCTION

At your request, we have completed and hereby provide an independent appraisal (the “Appraisal”) of the estimated consolidated pro forma market value of Everett Cash Mutual Insurance Company (“ECM” or the “Company”) as of September 17, 2025 (the “Valuation Date”). Pursuant to a Plan of Conversion from the Mutual to Stock Form (the “Plan of Conversion”) to be adopted by the Company’s Board of Directors (the “Board”), ECM plans to convert from a Pennsylvania mutual insurance company to a Pennsylvania stock insurance company (the “Conversion”) under the Pennsylvania Insurance Company Mutual-to-Stock Conversion Act (the “Act”). Simultaneously, ECM will issue and sell all of its common stock to Old Republic Specialty Insurance Group, Inc. (“Old Republic Specialty”), a wholly owned subsidiary of Old Republic International Corporation (“Old Republic”). Old Republic Specialty will acquire all of the authorized common stock of the converted ECM for an amount of cash equal to at least the minimum of the valuation range (“Valuation Range”) established herein by the statutorily required and independently determined Appraisal. As a result of the foregoing, ECM will become an indirect wholly owned subsidiary of Old Republic.

ECM’s eligible policyholders and other eligible subscribers will receive the right to purchase shares of Old Republic common stock in a stock offering (the “Offering”) in an aggregate amount between the minimum and maximum of the Valuation Range at a purchase price per share discount of from 30% to 35% of the volume-weighted average trading price of Old Republic common stock. In the event that the aggregate amount of stock sold in the Offering is less than the minimum of the Valuation Range, Old Republic will contribute cash equal to not less than the difference between the minimum of the Valuation Range and the aggregate amount of stock sold in the Offering to fund the acquisition of all of the common stock of the ECM as converted.

In accordance with Section 914(A)-d of the Act, the aggregate price of the capital stock issued in the Conversion shall be equal to the estimated pro forma market value of the converted stock company based upon an independent evaluation by a qualified expert. Furthermore, as permitted by Section 914(A)-d of the Act, the pro forma market value may be that value that is estimated to be necessary to attract full subscription for the shares and may be stated as a range of pro forma market value.

Feldman Financial Advisors, Inc. (“Feldman Financial”) is a financial consulting and advisory firm that specializes in financial valuations and analyses of business enterprises and securities in the financial services industries. The background of Feldman Financial is presented in Exhibit I. In preparing the Appraisal, we conducted an analysis of ECM that included discussions with the Company’s management. We reviewed the unaudited financial statements of ECM as prepared under generally accepting accounting principles (“GAAP”) for the years ended December 31, 2023 and 2024. We also reviewed statutory financial data of ECM for the years ended December 31, 2023 and 2024 and the six months ended June 30, 2025. In addition, where appropriate, we considered information based on other available published sources that we believe are reliable; however, we cannot guarantee the accuracy and completeness of such information.

In preparing the Appraisal, we also reviewed and analyzed: (i) financial and operating information with respect to the business, operations, and prospects of ECM as furnished to us by the Company; (ii) publicly available information concerning the Company that we believe to be relevant to our analysis; (iii) a comparison of the historical financial results and present financial condition of the Company with those of selected publicly traded insurance companies that we deemed relevant; and (iv) financial performance and market valuation data of certain publicly traded insurance industry aggregates as provided by industry sources.

The Appraisal is based on the Company’s representation that the information and financial data furnished to us by the Company and its independent auditors are truthful, accurate, and complete. We did not independently verify the financial statements and other information provided by the Company and its independent auditors, nor did we independently value the assets or liabilities of the Company. The Appraisal considers the Company only as a going concern on a standalone basis and should not be considered as an indication of the liquidation value of the Company.

Our Appraisal is not intended, and must not be construed, to be a recommendation of any kind as to the advisability of purchasing shares of Old Republic common stock in the Offering. The Appraisal considers the Company only as a going concern and should not be considered as an indication of its liquidation value. The Appraisal is necessarily based upon estimates of a number of matters, all of which are subject to change from time to time.

The Valuation Range reported herein may be updated as necessary and required. These updates will consider, among other factors, any developments or changes in the Company’s operating performance, financial condition, or management policies, and current conditions in the securities markets for insurance company common stocks. Should any such new developments or changes be material, in our opinion, to the estimated consolidated pro forma market value of the Company, appropriate adjustments to the Valuation Range will be made. The reasons for any such adjustments will be explained in detail at that time.

1

FELDMAN FINANCIAL ADVISORS, INC.

I. BUSINESS OF EVERETT CASH MUTUAL INSURANCE COMPANY

General Overview

ECM is a mutual insurance company domiciled in Pennsylvania. ECM operates as a property and casualty insurance carrier specializing in farmowners and agribusiness coverage. ECM also offers certain commercial insurance products that complement its farm/agricultural focus. The Company was established originally in 1913. The executive offices of ECM are located in Everett, Pennsylvania. At December 31, 2024, on a consolidated GAAP basis, the Company had total assets of $513.0 million and total equity capital of $130.7 million. For the year ended December 31, 2024, ECM had direct premiums written of $237.2 million, net premiums earned of $177.1 million, and GAAP net income of $11.1 million.

ECM is organized as a group of companies, including various subsidiary companies and an affiliate. ECM markets its products through a network of independent agents in 48 states and the District of Columbia. Approximately 14.3%, 11.2%, 7.5%, and 6.7% of consolidated direct premiums written were from Pennsylvania, North Carolina, Texas, and Arkansas, respectively, for the year ended December 31, 2024. ECM is the fourth largest writer of farmowners insurance in Pennsylvania and the second largest writer of farmowners insurance in North Carolina.

ECM has expanded its geographic footprint to cover the continental United States through a combination of organic growth and the acquisition in 2022 of American Reliable Insurance Company (“ARIC”). ARIC is domiciled in Arizona and writes farm, ranch, and equine insurance coverage in 48 states and the District of Columbia. Following the acquisition of ARIC, ECM’s direct premiums written more than doubled from $107.8 million in 2021 to $249.7 million in 2023. The acquisition of ARIC accomplished, among other things, extraordinary geographic diversification and spread of risk for ECM and positioned the Company on a national scale.

Business Strategy

ECM seeks to be a leading provider of insurance solutions to the farm, ranch, and agricultural business sector. ECM has focused on growing its statutory surplus and premium revenue with a consistent theme of “narrow but deep” market penetration in the farm/agricultural insurance sector. An integral part of ECM’s business strategy is to own multiple insurance carriers that can target different market segments and geographical areas. Numerous states prevent an insurance carrier from offering multiple rating plans for a particular product. Through its subsidiary and affiliate group of companies, ECM utilizes different carriers to carve a product niche in profitable operating segments. ECM has also emphasized expanding its commercial insurance business, particularly in areas that are logical extensions of its agricultural niches. ECM’s focus on commercial lines has included small contractors, restaurants, wineries, breweries, and other “Main Street” small businesses.

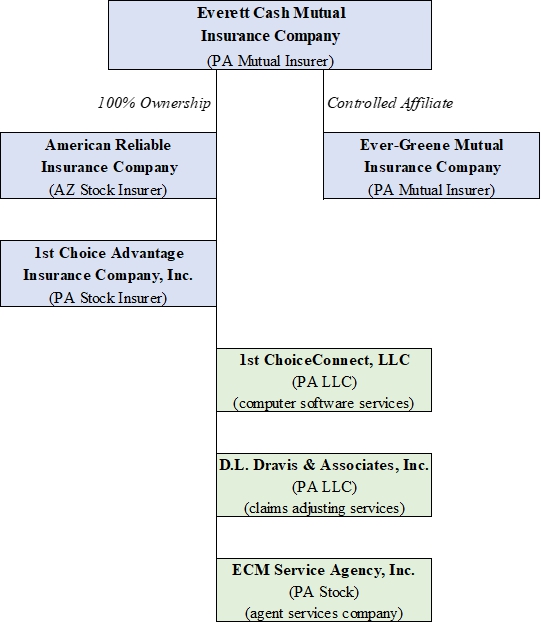

Corporate Operating Structure

ECM is the ultimate controlling entity of its group of subsidiary companies. The corporate organizational chart on the next page depicts the direct ownership and affiliated relationships within the group of ECM businesses. ECM has 100% ownership of ARIC and 1st Choice Advantage Insurance Company, Inc. (“1CA”). ECM controls Ever-Greene Mutual Insurance Company (“EGM”) through a common board of directors at both companies. ECM is also party to reinsurance agreements and cost-sharing agreements with 1CA, EGM, and ARIC. Non-insurance carrier entities owned by ECM include 1st ChoiceConnect, LCC (“1CC”), D.L. Dravis and Associates, Inc. (“Dravis”), and ECM Service Agency, Inc. (“ECMSA”). ECM, ARIC, 1CA, and EGM share a common board of directors, employees, software, and office space. ECMSA operates as a retail insurance agency. Dravis provides claims adjusting and appraisal services to insurance companies. 1CC provides policy and claims software solutions to insurance companies. ARIC, 1CA, EGM, 1CC, and Dravis reimburse ECM under a cost-sharing agreement that stipulates the allocation of personnel costs, along with specific overhead expenses, based upon predetermined factors.

2

FELDMAN FINANCIAL ADVISORS, INC.

Table 1

ECM Insurance Group

Corporate Organizational Structure

3

FELDMAN FINANCIAL ADVISORS, INC.

Descriptions of the companies within the ECM Insurance Group are summarized below:

ECM (Everett, Pennsylvania) writes primarily property and liability insurance in 16 states, including Arkansas, Georgia, Illinois, Indiana, Iowa, Kansas, Kentucky, Maryland, Missouri, Nebraska, North Carolina, Ohio, Pennsylvania, South Dakota, Tennessee, and Virginia. ECM is also licensed but is not currently writing in five additional states. ECM provides insurance coverages primarily in the farmowners and commercial lines of business through a network of independent insurance agencies. ECM began non-renewing its personal automobile line of business in August 2024. ECM’s unconsolidated direct written premiums amounted to $107.2 million for the year ended December 31, 2024, with approximately 25.4%, 13.8%, and 12.8% generated in Pennsylvania, North Carolina, and Arkansas, respectively.

ARIC (Phoenix, Arizona) was acquired by ECM effective as of December 31, 2022. ARIC is licensed to write primarily property and liability insurance in all U.S. states and the District of Columbia, and writes insurance in all states except Alaska and Hawaii. ARIC provides insurance coverages primarily in the farmowners and commercial lines of business through a network of independent insurance agencies. ARIC concentrates on agribusiness, farms, ranches, and all aspects of the equine industry, including equine mortality. ARIC’s direct written premiums amounted to $100.7 million for the year ended December 31, 2024, with 8.3%, 5.2%, and 4.3% written in North Carolina, Texas, and Oklahoma, respectively.

1CA (Everett, Pennsylvania) is licensed to write automobile insurance in Pennsylvania, North Carolina, Kentucky, Ohio, Virginia, Tennessee, Georgia, Indiana, and Texas. 1CA also writes property insurance in Texas and Georgia. 1CA was initially established in 2000 to write automobile insurance in support of ECM’s primary property offering. Starting in 2017, 1CA began to diversify its product offerings to include other product lines consistent with ECM’s product offerings. During 2024, 1CA initiated a planned exit from private passenger automobile lines in all states. Products are offered by 1CA through a network of independent insurance agents. 1CA’s direct written premiums amounted to $29.3 million for the year ended December 31, 2024, with 39.7%, 16.2%, and 12.1% written in Texas, Pennsylvania, and North Carolina, respectively

EGM (Everett, Pennsylvania) is licensed in Pennsylvania. EGM is affiliated with ECM through common management and board control. Effective January 1, 2023, EGM assumed an increased strategic role within the ECM Insurance Group and entered into a quota share reinsurance agreement with ECM, whereby EGM began assuming 60% participation on risks written on a direct basis by ECM within Pennsylvania and classified as perils. EGM wrote no direct business in 2024 and reported $12.7 million in net premiums earned. In connection with the Conversion, EGM plans to merge into ECM and surrender its operating license.

1CC (Everett, Pennsylvania) functions as the technology arm of the ECM Insurance Group. ECM licensed its internally developed policy and claims systems to other insurance carriers, converting what is typically a cost center into a profit center. 1CC provides clients with innovative and cost-effective information management software, strategic management systems, and business intelligence models and dashboards for policy and claims administration, rate assessments and quotes, and payment access.

Dravis (Everett, Pennsylvania) operates as the independent claims adjusting division for the ECM Insurance Group. Dravis is a collection of employee adjusters and independent contractors, primarily overseeing the field investigation for ECM, ARIC, and other insurance carriers. Dravis has provided multi-line claims services since 1982. The staff of adjusters and appraisers at Dravis is equipped to handle a full spectrum of claims needs, including conducting full investigations and processing claims through completion, determination of value, settlement, and any mediation.

4

FELDMAN FINANCIAL ADVISORS, INC.

Product Offerings

ECM’s core competency lies in offering insurance products to farm/agriculture and selected commercial businesses. ECM has emphasized financial strength and growth in evolving into a multi-line, multi-state insurance carrier. ECM writes a variety of personal and commercial lines packages, specializing in farmowners coverage. ARIC concentrates on agribusiness, farms, ranches, and all aspects of the equine industry, including equine mortality. 1CA provides personal and commercial automobile coverage for farmowners and commercial policyholders in good standing with ECM. EGM’s current business consists of inland marine business assumed from ECM. ECM and 1CA are exiting the personal automobile market as personal automobile will be non-renewed starting with September 1, 2024 renewals. ECM, 1CA, and ARIC will continue to offer commercial automobile coverage as this segment is viewed as a key product to round out the farm/agriculture business model.

ECM provides niche programs for a wide variety of distinct businesses, including equine, poultry (along with avian influenza), confinement operations, commercial farms, wineries and vineyards, as well as farm bed and breakfast lodging. ECM has remained focused on expanding its niche through new product line offerings and expansion of its geographic footprint. ECM has gradually shifted its business mix by de-emphasizing homeowners accounts, which now only compose a nominal percentage of its overall premium business. In addition, personal automobile (which only makes up a modest portion of overall premium writings) non-renewals began September 1, 2024 and are expected to be completed by September 1, 2025. Management has also established new commercial coverage products, including agribusiness, liquor liability, car washes, wineries/breweries, and equipment breakdown, and has been expanding its commercial automobile program to support its niche farm/agriculture products. Overall, the Company’s prospective business plan includes maintaining focus on farm/agribusiness, continued integration of ARIC, and placing greater emphasis on pricing sophistication, rate adequacy and risk selection.

Marketing and Distribution

ECM’s marketing plan is aimed at delivering a top-quality insurance product to agents who are able to appreciate and sell the quality of the Company’s product in a price-sensitive marketplace. Having made a long-term commitment to a narrow market niche, ECM seeks to maintain pricing stability throughout the insurance market pricing cycles. The Company realizes there are always competitors who will offer an insurance product at a lower price, and there are always customers actively seeking the lowest-priced product. ECM strives to align itself with the segment of the market that does appreciate the coverages and services provided by the Company as an industry specialist. The Company recognizes that this segment requires competitive pricing but is willing to pay for needed coverages and services. ECM focuses on marketing its products through independent agents who are especially committed to the farmowners/agribusiness niche. ECM’s multiple distribution channel approach allows the Company to adjust pricing based on market conditions in various states.

The marketing efforts of ECM are further supported by the Company’s claims, underwriting, and billings operations. As an industry specialist, ECM is able to offer expertise in all interactions with agents and/or policyholders. ECM believes that these positive experiences result in higher policyholder retention and create new business opportunities for the Company’s agents. While it relies on independent agents for the front-line distribution and customer support, underwriting, billing, loss control, and claim handling responsibilities are retained by ECM. Many of the Company’s agents have had direct relationships with ECM for a number of years.

Executive Officers

ECM is managed by an experienced group of executives led by Randy F. Shaw, its President and Chief Executive Officer. Mr. Shaw joined ECM in 1987 and has served in many senior positions at ECM. Summary biographies of ECM’s executive officers are included below:

Randy F. Shaw serves as the President and Chief Executive Officer of ECM and also serves on the Board of Directors. He joined the Company in July 1987 and formerly served as Treasurer, Chief Financial Officer, and Chief Operating Officer of ECM. Mr. Shaw has more than 40 years of experience in the insurance and finance industry and holds a Certified Public Accountant designation. Prior to joining ECM, he was employed with Grumman Systems Support Corporation and Arthur Andersen & Company. Mr. Shaw received his B.S. in Accounting from Penn State University.

5

FELDMAN FINANCIAL ADVISORS, INC.

David E. Eppinger serves as Executive Vice President/Chief Operating Officer, a position he has held since January 2020. He also serves as Secretary of the Company. Previously, he served as the Vice President of Research and Development at ECM. Mr. Eppinger joined ECM originally in August 1998. He received his B.S. in Quantitative Business Analysis from Penn State University.

Steven S. Merrill serves as the Chief Financial Officer and Treasurer of the Company. He joined the Company in August 2022. Mr. Merrill is a Certified Public Accountant and was formerly employed by the independent accounting firms of Brown Schultz Sheridan & Fritz, Buffamante Whipple Buttafaro, P.C., and KPMG LLP. Mr. Merrill received his B.S. in Accounting from the University of Delaware.

Dennis R. Fraley serves as Executive Vice President of Underwriting of ECM. He joined the Company in April 2018. Mr. Fraley was employed previously by American Reliable Insurance Company since 2003 in various positions as National Sales Manager, Underwriting Manager of Commercial Operations, and Director of Commercial Operations and Underwriting. Mr. Fraley is a graduate of the University of Illinois Urbana-Champaign.

Plan of Conversion

As a mutual insurance company, ECM does not have shareholders. It has members. The members of ECM are the policyholders of ECM. The members of ECM are entitled to the right to elect directors and to approve fundamental transactions such as the Conversion. In an insurance company organized as a stock institution, policyholders have no governance rights, which reside with shareholders, and instead have only contractual rights under their insurance policies.

The Plan of Conversion is subject to the approval of the Board of ECM and subject to the approval of the Commissioner of the Pennsylvania Insurance Department. The Plan of Conversion is also subject to the approval of the members of ECM by the affirmative vote of at least two-thirds of the votes to be cast at a special meeting. The Plan of Conversion provides that Old Republic will offer shares of its common stock for sale in the Offering to Eligible Members of ECM and the directors, officers, and employees of ECM. The maximum amount of Old Republic common stock that any person, together with any associate or group of persons acting in concert, may directly or indirectly acquire in the Offering shall not exceed $350,000.

The Board of ECM regularly undertakes strategic review and assessment of its operations, business plans, enterprise risk management, and market position generally. The Board has also engaged in ongoing efforts to identify strategic alternatives to achieve ECM’s goals and address significant challenges currently facing it, including exceedingly high reinsurance costs, limited capacity to write new farmowners business, and needed technology and infrastructure investments. Ultimately, the Board determined that ECM’s future success, its ability to continue to serve its policyholders and other stakeholders, and ECM’s mission to become a preeminent writer of farmowners business, would all be enhanced by expanding its writing capacity, expanding geographically, augmenting its capital position, and achieving an “A+” rating from A.M. Best Company, Inc. (“A.M. Best”). After careful and thorough study and consideration, ECM concluded that the subscription rights method of demutualization, in a transaction sponsored by Old Republic, best suits ECM under the circumstances. In reaching its conclusion, ECM considered, among other things, that a sponsored demutualization with Old Republic will:

| ● | provide ECM with immediate and long-term access to a significant amount of additional capital and reinsurance capacity; |

| ● | permit ECM to avail itself of Old Republic’s A.M. Best “A+” financial strength rating and Old Republic’s larger A.M. Best financial size category; |

| ● | provide Eligible Members with an opportunity to acquire shares of Old Republic common stock at a significant (between 30% to 35%) discount to market; |

| ● | permit ECM to operate as an indirect wholly owned subsidiary of Old Republic going forward and serve as a platform for developing Old Republic’s specialty farmowners insurance business, thereby maintaining ECM’s existence on a continuing basis; |

6

FELDMAN FINANCIAL ADVISORS, INC.

| ● | permit ECM to continue to serve its existing specialty farmowners insurance customers and increase its product offerings to those customers and new policyholders; |

| ● | permit ECM to maintain its name, headquarters, culture, values, and management team; |

| ● | facilitate the creation of a charitable foundation with a significant $5.0 million contribution for the purpose of supporting the farming community; and |

| ● | provide ECM employees and management with opportunities for career advancement and participation in Old Republic’s existing employee benefits. |

Upon completion of the Conversion, all of the outstanding shares of common stock of the converted ECM will be purchased by Old Republic Specialty and ECM will then become an indirect wholly owned stock subsidiary of Old Republic. The Conversion will be effected only if the combined subscription orders and cash contribution amount from Old Republic equal at least the minimum of the Valuation Range and the members of ECM approve the Plan of Conversion.

The net proceeds from the Conversion will supply additional capital that ECM needs to support future premium growth. The net proceeds will also be used for general corporate purposes, including the repayment of a portion of the surplus notes outstanding. On a short-term basis, the net proceeds will be invested primarily in U.S. Government securities, other federal agency securities, and other securities consistent with the Company’s investment policy.

The remainder of Chapter I examines in more detail the trends addressed in this section, including the impact of changes in the Company’s economic and competitive environment, and ECM’s recent financial performance. The discussion is supplemented by the exhibits in the Appendix. Exhibit III-1 displays the Company’s consolidated GAAP balance sheets as of December 31, 2023 and 2024. Exhibit III-2 presents the Company’s consolidated GAAP income statements for the years ended December 31, 2023 and 2024.

7

FELDMAN FINANCIAL ADVISORS, INC.

Financial Condition

Table 2 presents selected data concerning ECM’s consolidated GAAP financial position as of December 31, 2023 and 2024. Exhibit III-1 presents ECM’s unaudited consolidated GAAP balance sheets as of December 31, 2023 and 2024. Consolidated GAAP financial statements of the Company prior to the years ended December 31, 2023 and 2024 have not been prepared. The recent GAAP financial statements were prepared internally by management of ECM with the assistance of external accountants but were not audited by an independent accounting firm.

Table 2

Selected Financial Condition Data

As of December 31, 2023 and 2024

(Dollars in Thousands)

| December 31, | ||||||||

| 2024 | 2023 | |||||||

| Consolidated Balance Sheet Data | ||||||||

| Total assets | $ | 513,046 | $ | 512,969 | ||||

| Total investments and cash | 240,851 | 229,532 | ||||||

| Uncollected premiums | 42,103 | 37,605 | ||||||

| Reinsurance reoverable (1) | 93,356 | 99,591 | ||||||

| Prepaid reinsurance premiums | 77,136 | 79,458 | ||||||

| Goodwill and other intangibles | 23,891 | 27,047 | ||||||

| Losses and loss adjustment expenses | 154,142 | 159,375 | ||||||

| Unearned premiums | 163,445 | 171,060 | ||||||

| Surplus notes payable | 25,000 | 25,000 | ||||||

| Total liabilities | 382,315 | 388,668 | ||||||

| Total equity | 130,731 | 124,301 | ||||||

| Total equity / total assets | 25.48 | % | 24.23 | % | ||||

| Tangible equity / tangible assets | 21.84 | % | 20.01 | % | ||||

| Total investments and cash / total assets | 46.95 | % | 44.75 | % | ||||

| Policy reserves (2) / total equity | 117.91 | % | 128.22 | % | ||||

| (1) | Includes reinsurance recoverable on unpaid and paid losses and loss adjustment expenses. |

| (2) | Policy reserves equal losses and loss adjustment expenses. |

Source: Everett Cash Mutual Insurance Company, internal GAAP financial statements.

ECM’s consolidated total assets were relatively unchanged from December 31, 2023 to December 31, 2024, measuring approximately $513.0 million at both year-end periods. The largest changes among asset categories in 2024 were an $11.3 million increase in total investment and cash and a $4.5 million increase in uncollected premiums, which were offset partially by a $6.2 million decrease in reinsurance balances recoverable and a $3.2 million decrease in goodwill and other intangibles. Total investments and cash increased from $229.5 million at December 31, 2023 to $240.9 million at December 31, 2024 as a result of continued positive cash flow from operations.

Total investments and cash amounted to 46.9% of total assets at December 31, 2024, compared to 44.7% of total assets as of December 31, 2023. Reinsurance balances recoverable decreased from $99.6 million (19.4% of total assets) at December 31, 2023 to $93.4 million (18.2% of total assets) at December 31, 2024. Reinsurance recoveries are estimates of paid and unpaid losses collectible from ECM’s reinsurers. Prepaid reinsurance premiums declined from $79.5 million (15.5% of total assets) at December 31, 2023 to $77.1 million (15.0% of total assets) at December 31, 2024. Prepaid reinsurance premiums represent amounts ECM has paid or advanced to reinsurers for premiums ceded but not yet earned.

8

FELDMAN FINANCIAL ADVISORS, INC.

Total liabilities decreased by 1.6% or $6.4 million from $388.7 million at December 31, 2023 to $382.3 million at December 31, 2024. The decrease in total liabilities was caused, in part, by the decrease in total policy reserves (losses and loss adjustment expenses), which was reflective of the timing of claims payments and favorable loss reserve development. Total policy reserves decreased by 3.3% or $5.2 million from $159.4 million at December 31, 2023 to $154.1 million at December 31, 2024, while unearned premiums decreased by 4.5% or $7.6 million from $171.1 million at year-end 2023 to $163.4 million at year-end 2024. Premiums are earned over the terms of the related insurance policies and reinsurance contract. Unearned premium reserves are established to cover the unexpired portion of premiums written. Such reserves are computed by monthly pro rata methods for direct business and are based on reports from ceding companies for reinsurance.

ECM maintains policy reserves for the payment of claims (losses) and loss adjustment expenses (“LAE”) related to adjusting those claims. ECM’s loss reserves consist of case reserves, which are reserves for claims that have been reported to it, defense and cost containment (“DCC”) expense reserves, which include all defense and litigation-related expenses, and reserves for claims that have been incurred but have not yet been reported or for case reserve deficiencies or redundancies (“IBNR”). ECM utilizes an independent actuary to assist with the estimation of its loss and LAE reserves. Such reserves are necessarily based on assumptions and estimates, and while management of ECM believes the reserves as established make a reasonable provision for all unpaid losses and settlement expenses, the ultimate liability may differ from that provided.

ECM’s consolidated balance of investments and cash amounted to $240.9 million at December 31, 2024 and constituted 46.9% of total assets. ECM maintains a portion of its investments in relatively short-term and highly liquid assets to ensure the availability of funds for operating purposes. ECM’s cash, cash equivalents, and short-term investments amounted to $23.6 million and investment securities amounted to $217.2 million at December 31, 2024. Exhibit III-3 presents ECM’s consolidated investments and cash portfolio as of December 31, 2023 and 2024. ECM’s investment portfolio comprised $174.6 million of bonds and $40.3 million of common stocks at year-end 2024. The bond portfolio consisted primarily of corporate bonds, U.S. Government and agency obligations, and tax-exempt state and municipal bonds. ECM employs a laddered approach to manage its fixed-income securities to efficiently and effectively manage interest rate risk and return. The common stock portfolio mainly comprised publicly traded stocks, mutual funds, and exchange traded funds. Consistent with its current enterprise risk management strategies, ECM has purposefully reduced the overall investment risk in its securities holdings.

In accordance with insurance industry practice, ECM reinsures a portion of its loss exposure and pays to the reinsurers a portion of the premiums received on all policies reinsured. Insurance policies written by the Company are reinsured with other insurance companies principally to: (i) reduce net liability on individual risks; (ii) mitigate the effect of individual loss occurrences (including catastrophic losses); (iii) stabilize underwriting results; (iv) decrease leverage; and (v) increase underwriting capacity. ECM ceded to reinsurers $76.4 million and $69.7 million of written premiums for the years ended December 31, 2023 and 2024, respectively. ECM’s reinsurance providers, the majority of whom are longstanding partners who understand the Company’s business, are all carefully selected with the help of the Company’s reinsurance broker. ECM monitors the solvency of its reinsurers through regular review of their financial statements and, if available, their A.M. Best ratings. All of the Company’s unaffiliated reinsurance partners currently have at least an “A-” rating from A.M. Best.

As of December 31, 2023 and 2024, ECM had $25.0 million in surplus notes outstanding. The statutory notes are included as regulatory capital for statutory accounting purposes. ECM issued the surplus notes to support its regulatory capital in connection with its steady growth and diversification initiatives. ECM issued a $10.0 million surplus note in February 2019 and an additional $15.0 million surplus note in May 2023. The $10.0 million surplus note bears a current interest rate of 6.50% and matures in February 2039 and the $15.0 million surplus note has a current interest rate of 8.05% and matures in May 2043. Following the completion of the Conversion, ECM plans to repay the $10.0 million surplus note.

ECM’s consolidated GAAP total equity increased from $124.3 million at December 31, 2023 to $130.7 million at December 31, 2024, chiefly as a result of profitable operating results in 2024. ECM’s ratio of total equity to total assets advanced from 24.2% at December 31, 2023 to 25.4% at December 31, 2024. ECM’s consolidated tangible equity increased from $97.3 million at year-end 2023 to $106.8 million at year-end 2024, and the corresponding ratio of tangible equity to tangible assets advanced from 20.8% to 21.8%. ECM had $23.9 million of goodwill on its balance sheet as of December 31, 2024, which original amount of $30.8 million resulted from the acquisition of ARIC in 2022 and is being amortized on a straight-line basis over ten years.

9

FELDMAN FINANCIAL ADVISORS, INC.

Income and Expense Trends

Table 3 displays ECM’s consolidated GAAP earnings results for the years ended December 31, 2023 and 2024. Table 4 presents the Company’s underwriting performance and related ratios. Table 5 presents a summary of consolidated direct premiums written by policy line of business and Table 6 details ECM’s consolidated direct premiums written by state. ECM’s operating results are influenced by factors affecting the property and casualty (“P&C”) insurance industry in general. The performance of the P&C insurance industry is subject to significant variations due to competition, weather, catastrophic events, regulation, general economic conditions, judicial trends, fluctuations in interest rates, and other factors. ECM’s operating results are influenced by factors affecting the P&C insurance industry in general. The operating results of the United States P&C insurance industry are subject to significant variations due to competition, weather, catastrophic events, regulation, general economic conditions, judicial trends, fluctuations in interest rates, and other changes in the investment environment.

ECM’s premium growth and underwriting results have been, and continue to be, influenced by market conditions. Pricing in the P&C insurance industry historically has been cyclical with the financial performance of insurers fluctuating from periods of low premium rates and excess underwriting capacity resulting from increased competition (soft market), followed by periods of high premium rates and a shortage of underwriting capacity resulting from decreased competition (hard market).

ECM recorded GAAP net income of $11.1 million for the year ended December 31, 2024 as compared to GAAP net income of $3.1 million for the year ended December 31, 2023. The Company experienced noticeable improvement in net premiums earned and underwriting profits in 2024. The $8.0 million increase in earnings for 2024 was attributable primarily to a $13.1 million increase in net premiums earned and a $2.9 million increase in net underwriting profits. ECM’s consolidated return on average assets (“ROA”) increased to 2.17% in 2024 and its return on average equity (“ROE”) advanced to 8.73% in 2024.

Total revenue increased to $184.9 million in 2024, which was $21.6 million or 13.2% greater than the $163.3 million of total revenue reported in 2023. Net premiums earned increased by $13.1 million or 8.0% from $164.0 million in 2023 to $177.1 million in 2024, primarily due to a $6.7 million reduction in reinsurance ceded and a $23.4 million positive change in unearned premiums. ECM’s consolidated direct premiums written declined by $12.6 million or 5.1% from $249.7 million in 2023 to $237.2 million in 2024. As shown in Table 5, the decrease in direct premiums written was mainly attributable to a $5.1 million decline in private automobile premiums written and a $4.3 million in homeowners premiums written.

Table 5 illustrates that commercial multi-peril and farmowners multi-peril accounted for 39.7% and 31.7%, respectively, of consolidated direct premiums written in 2024. Commercial multi-peril amounted to $94.3 million and farmowners multi-peril amounted to $75.2 million of direct premiums written in 2024. The next largest categories in 2024 were inland marine ($31.4 million or 9.0%) and commercial automobile ($18.1 million or 7.6%). As a result of the Company’s planned exit from the personal automobile business, personal automobile direct premiums declined by 40.8% or $5.1 million from $12.6 million in 2023 to $7.4 million in 2024.

As shown in Table 6, the states that accounted for the largest amount of consolidated direct premiums written in 2024 included Pennsylvania ($33.8 million or 14.3%), North Carolina ($26.7 million or 11.2%), Texas ($17.9 million or 7.5%), Arkansas ($15.8 million or 6.7%) and Kentucky ($13.3 million or 5.6%). The state that experienced the largest increase between 2023 and 2024 was Iowa, which increased by $2.9 million from $1.7 million in 2023 to $4.6 million in 2024.

10

FELDMAN FINANCIAL ADVISORS, INC.

Table 3

Consolidated Income Statement Data

For the Years Ended December 31, 2023 and 2024

(Dollars in Thousands)

| Year

Ended December 31, | ||||||||

| 2024 | 2023 | |||||||

| Direct premiums written | $ | 237,203 | $ | 249,654 | ||||

| Reinsurance assumed | (20 | ) | 4,634 | |||||

| Reinsurance ceded | (69,729 | ) | (76,434 | ) | ||||

| Change in unearned premiums | 5,293 | (18,116 | ) | |||||

| Other income | 4,388 | 4,275 | ||||||

| Net premiums earned | 177,136 | 164,012 | ||||||

| Losses incurred | 98,727 | 111,905 | ||||||

| Loss adjustment expenses incurred | 10,883 | 10,408 | ||||||

| Other underwriting expenses incurred | 56,037 | 33,529 | ||||||

| Other expenses | 5,195 | 4,801 | ||||||

| Total underwriting expenses | 170,842 | 160,643 | ||||||

| Net underwriting gain | 6,293 | 3,369 | ||||||

| Investment income | 8,912 | 7,258 | ||||||

| Net realized capital gains, net of taxes | 4,402 | 780 | ||||||

| Investment expenses | (1,193 | ) | (1,050 | ) | ||||

| Interest expense | (1,813 | ) | (1,207 | ) | ||||

| Surplus note origination costs | - | (723 | ) | |||||

| Depreciation on real estate | (46 | ) | (46 | ) | ||||

| Net investment gain | 10,263 | 5,013 | ||||||

| Other income, net | 623 | 436 | ||||||

| Goodwill amortization expense | (3,156 | ) | (3,156 | ) | ||||

| Net other income (expense) | (2,532 | ) | (2,719 | ) | ||||

| Net income before income tax expense | 14,024 | 5,662 | ||||||

| Federal income tax expense | 2,898 | 2,547 | ||||||

| Net income | $ | 11,126 | $ | 3,115 | ||||

Source: Everett Cash Mutual Insurance Company, internal GAAP financial statements.

11

FELDMAN FINANCIAL ADVISORS, INC.

Table 4

Consolidated Underwriting Performance Data

For the Years Ended December 31, 2023 and 2024

(Dollars in Thousands)

| Year

Ended December 31, | ||||||||

| 2024 | 2023 | |||||||

| Selected Income Statement Data | ||||||||

| Net premiums earned | $ | 177,136 | $ | 164,012 | ||||

| Losses and loss adjustment expenses incurred | 109,610 | 122,313 | ||||||

| Underwriting expenses | 61,232 | 38,331 | ||||||

| Total underwriting losses and expenses | 170,842 | 160,643 | ||||||

| Net underwriting profit | $ | 6,293 | $ | 3,369 | ||||

| Underwriting Ratios | ||||||||

| Loss ratio (1) | 61.9 | % | 74.6 | % | ||||

| Expense ratio (2) | 34.5 | % | 23.3 | % | ||||

| Combined ratio (3) | 96.4 | % | 97.9 | % | ||||

| (1) | Losses and loss adjustment expenses divided by net premiums earned. |

| (2) | Net underwriting and other expenses divided by net premiums earned. |

| (3) | Sum of the loss ratio and the expense ratio. |

Source: Everett Cash Mutal Insurance Company, unaudited GAAP financial statements.

A key measurement of the profitability of any insurance company for any period is its combined ratio, which is equal to the sum of its loss ratio and its expense ratio. The profitability of property and casualty insurance companies depends on income from underwriting, investment, and service operations. Underwriting results are considered profitable when the combined ratio is under 100% and unprofitable when the combined ratio is over 100%. Table 4 provides additional underwriting performance data for ECM based on GAAP financial data for the years ended December 31, 2023 and 2024.

12

FELDMAN FINANCIAL ADVISORS, INC.

Table 5

Consolidated Direct Premiums Written by Line of Business

For the Years Ended December 31, 2023 and 2024

(Dollars in Thousands; Percent of Total)

| Line of | Year

Ended December 31, 2024 | Year

Ended December 31, 2023 | ||||||||||||||||||||||||||||||

| Business | ECM | ARIC | 1CA | Combined | ECM | ARIC | 1CA | Combined | ||||||||||||||||||||||||

| Fire | $ | 537 | $ | 32 | $ | 0 | $ | 569 | $ | 609 | $ | 3,303 | $ | 0 | $ | 3,913 | ||||||||||||||||

| Allied lines | 161 | 26 | 0 | 188 | 198 | 2,366 | 0 | 2,563 | ||||||||||||||||||||||||

| Farmowners multi-peril | 69,250 | 3,553 | 2,410 | 75,212 | 68,791 | 3,753 | 2,387 | 74,931 | ||||||||||||||||||||||||

| Homeowners multi-peril | 2,556 | 3,864 | 0 | 6,420 | 2,654 | 8,053 | 0 | 10,707 | ||||||||||||||||||||||||

| Commercial multi-peril | 22,368 | 60,778 | 11,120 | 94,266 | 17,074 | 61,741 | 10,306 | 89,120 | ||||||||||||||||||||||||

| Inland marine | 1,536 | 19,816 | 8 | 21,359 | 1,517 | 19,002 | 0 | 20,519 | ||||||||||||||||||||||||

| Workers’ compensation | 1,319 | 0 | 0 | 1,319 | 1,540 | 0 | 0 | 1,540 | ||||||||||||||||||||||||

| Other liability | 5,319 | 3,448 | 542 | 9,309 | 5,830 | 5,759 | 567 | 12,157 | ||||||||||||||||||||||||

| Private automobile | 1,036 | 329 | 6,070 | 7,434 | 1,653 | 1,534 | 9,375 | 12,562 | ||||||||||||||||||||||||

| Commercial automobile | 3,109 | 8,853 | 6,100 | 18,062 | 3,077 | 9,355 | 9,209 | 21,641 | ||||||||||||||||||||||||

| Total | $ | 107,191 | $ | 100,699 | $ | 29,314 | $ | 237,203 | $ | 102,943 | $ | 114,866 | $ | 31,844 | $ | 249,654 | ||||||||||||||||

| Line of | Year

Ended December 31, 2024 | Year

Ended December 31, 2023 | ||||||||||||||||||||||||||||||

| Business | ECM | ARIC | 1CA | Combined | ECM | ARIC | 1CA | Combined | ||||||||||||||||||||||||

| Fire | 0.50 | 0.03 | 0.00 | 0.24 | 0.59 | 2.88 | 0.00 | 1.57 | ||||||||||||||||||||||||

| Allied lines | 0.15 | 0.03 | 0.00 | 0.08 | 0.19 | 2.06 | 0.00 | 1.03 | ||||||||||||||||||||||||

| Farmowners multi-peril | 64.60 | 3.53 | 8.22 | 31.71 | 66.82 | 3.27 | 7.50 | 30.01 | ||||||||||||||||||||||||

| Homeowners multi-peril | 2.38 | 3.84 | 0.00 | 2.71 | 2.58 | 7.01 | 0.00 | 4.29 | ||||||||||||||||||||||||

| Commercial multi-peril | 20.87 | 60.36 | 37.93 | 39.74 | 16.59 | 53.75 | 32.36 | 35.70 | ||||||||||||||||||||||||

| Inland marine | 1.43 | 19.68 | 0.03 | 9.00 | 1.47 | 16.54 | 0.00 | 8.22 | ||||||||||||||||||||||||

| Workers’ compensation | 1.23 | 0.00 | 0.00 | 0.56 | 1.50 | 0.00 | 0.00 | 0.62 | ||||||||||||||||||||||||

| Other liability | 4.96 | 3.42 | 1.85 | 3.92 | 5.66 | 5.01 | 1.78 | 4.87 | ||||||||||||||||||||||||

| Private automobile | 0.97 | 0.33 | 20.71 | 3.13 | 1.61 | 1.34 | 29.44 | 5.03 | ||||||||||||||||||||||||

| Commercial automobile | 2.90 | 8.79 | 20.81 | 7.61 | 2.99 | 8.14 | 28.92 | 8.67 | ||||||||||||||||||||||||

| Total | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | ||||||||||||||||||||||||

Source: S&P Global.

13

FELDMAN FINANCIAL ADVISORS, INC.

Table 6

Consolidated Direct Premiums Written by State

For the Years Ended December 31, 2023 and 2024

(Dollars in Thousands)

| Year Ended December 31, 2024 | Year Ended December 31, 2023 | |||||||||||||||||||||||||||||||

| ECM | ARIC | 1CA | Combined | ECM | ARIC | 1CA | Combined | |||||||||||||||||||||||||

| Alabama | $ | 0 | $ | 1,678 | $ | 0 | $ | 1,678 | $ | 0 | $ | 1,703 | $ | 0 | $ | 1,703 | ||||||||||||||||

| Alaska | 0 | 0 | 0 | 0 | 0 | 138 | 0 | 138 | ||||||||||||||||||||||||

| Arizona | 0 | 3,675 | 0 | 3,675 | 0 | 3,511 | 0 | 3,511 | ||||||||||||||||||||||||

| Arkansas | 13,758 | 2,031 | 0 | 15,789 | 14,022 | 1,678 | 0 | 15,700 | ||||||||||||||||||||||||

| California | 0 | 3,374 | 0 | 3,374 | 0 | 3,538 | 0 | 3,538 | ||||||||||||||||||||||||

| Colorado | 0 | 2,760 | 0 | 2,760 | 0 | 2,720 | 0 | 2,720 | ||||||||||||||||||||||||

| Connecticut | 0 | 1,058 | 0 | 1,058 | 0 | 2,138 | 0 | 2,138 | ||||||||||||||||||||||||

| D.C. | 0 | 2 | 0 | 2 | 0 | 8 | 0 | 8 | ||||||||||||||||||||||||

| Delaware | 0 | 22 | 0 | 22 | 0 | 37 | 0 | 37 | ||||||||||||||||||||||||

| Florida | 0 | 3,866 | 0 | 3,866 | 0 | 4,539 | 0 | 4,539 | ||||||||||||||||||||||||

| Georgia | 2,547 | 3,009 | 3,021 | 8,577 | 2,338 | 3,172 | 3,056 | 8,566 | ||||||||||||||||||||||||

| Hawaii | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | ||||||||||||||||||||||||

| Idaho | 0 | 1,954 | 0 | 1,954 | 0 | 3,045 | 0 | 3,045 | ||||||||||||||||||||||||

| Illinois | 94 | 3,041 | 0 | 3,135 | 85 | 2,779 | 0 | 2,864 | ||||||||||||||||||||||||

| Indiana | 6,361 | 1,608 | 2,069 | 10,038 | 6,628 | 1,773 | 2,826 | 11,227 | ||||||||||||||||||||||||

| Iowa | 3,788 | 849 | 0 | 4,637 | 553 | 1,104 | 0 | 1,658 | ||||||||||||||||||||||||

| Kansas | 7,085 | 1,166 | 0 | 8,252 | 7,071 | 1,432 | 0 | 8,503 | ||||||||||||||||||||||||

| Kentucky | 8,998 | 2,027 | 2,306 | 13,331 | 8,971 | 2,033 | 3,137 | 14,141 | ||||||||||||||||||||||||

| Louisiana | 0 | 3,357 | 0 | 3,357 | 0 | 3,368 | 0 | 3,368 | ||||||||||||||||||||||||

| Maine | 0 | 737 | 0 | 737 | 0 | 928 | 0 | 928 | ||||||||||||||||||||||||

| Maryland | 795 | 840 | 0 | 1,635 | 794 | 1,006 | 0 | 1,800 | ||||||||||||||||||||||||

| Massachusetts | 0 | 2,410 | 0 | 2,410 | 0 | 3,273 | 0 | 3,273 | ||||||||||||||||||||||||

| Michigan | 0 | 1,855 | 0 | 1,855 | 0 | 1,757 | 0 | 1,757 | ||||||||||||||||||||||||

| Minnesota | 0 | 1,880 | 0 | 1,880 | 0 | 2,241 | 0 | 2,241 | ||||||||||||||||||||||||

| Mississippi | 0 | 1,709 | 0 | 1,709 | 0 | 2,233 | 0 | 2,233 | ||||||||||||||||||||||||

| Missouri | 8,200 | 3,592 | 0 | 11,792 | 8,744 | 4,062 | 0 | 12,806 | ||||||||||||||||||||||||

| Montana | 0 | 3,446 | 0 | 3,446 | 0 | 4,086 | 0 | 4,086 | ||||||||||||||||||||||||

| Nebraska | 2,898 | 896 | 0 | 3,794 | 1,385 | 848 | 0 | 2,233 | ||||||||||||||||||||||||

| Nevada | 0 | 1,934 | 0 | 1,934 | 0 | 1,831 | 0 | 1,831 | ||||||||||||||||||||||||

| New Hampshire | 0 | 236 | 0 | 236 | 0 | 492 | 0 | 492 | ||||||||||||||||||||||||

| New Jersey | 0 | 1,827 | 0 | 1,827 | 0 | 2,107 | 0 | 2,107 | ||||||||||||||||||||||||

| New Mexico | 0 | 2,990 | 0 | 2,990 | 0 | 3,154 | 0 | 3,154 | ||||||||||||||||||||||||

| New York | 0 | 1,776 | 0 | 1,776 | 0 | 2,056 | 0 | 2,056 | ||||||||||||||||||||||||

| North Carolina | 14,751 | 8,356 | 3,561 | 26,669 | 14,308 | 12,716 | 3,366 | 30,390 | ||||||||||||||||||||||||

| North Dakota | 0 | 286 | 0 | 286 | 0 | 370 | 0 | 370 | ||||||||||||||||||||||||

| Ohio | 738 | 2,267 | 203 | 3,208 | 682 | 1,957 | 276 | 2,916 | ||||||||||||||||||||||||

| Oklahoma | 0 | 4,330 | 0 | 4,330 | 0 | 4,509 | 0 | 4,509 | ||||||||||||||||||||||||

| Oregon | 0 | 2,672 | 0 | 2,672 | 0 | 3,544 | 0 | 3,544 | ||||||||||||||||||||||||

| Pennsylvania | 27,193 | 1,858 | 4,758 | 33,809 | 27,459 | 1,988 | 6,277 | 35,724 | ||||||||||||||||||||||||

| Rhode Island | 0 | 171 | 0 | 171 | 0 | 752 | 0 | 752 | ||||||||||||||||||||||||

| South Carolina | 0 | 2,588 | 0 | 2,588 | 0 | 2,541 | 0 | 2,541 | ||||||||||||||||||||||||

| South Dakota | 485 | 1,036 | 0 | 1,520 | 520 | 1,138 | 0 | 1,659 | ||||||||||||||||||||||||

| Tennessee | 5,132 | 1,015 | 781 | 6,928 | 4,924 | 1,063 | 856 | 6,843 | ||||||||||||||||||||||||

| Texas | 0 | 6,237 | 11,628 | 17,865 | 0 | 5,592 | 10,837 | 16,429 | ||||||||||||||||||||||||

| Utah | 0 | 516 | 0 | 516 | 0 | 510 | 0 | 510 | ||||||||||||||||||||||||

| Vermont | 0 | 342 | 0 | 342 | 0 | 468 | 0 | 468 | ||||||||||||||||||||||||

| Virginia | 4,367 | 753 | 986 | 6,107 | 4,457 | 1,126 | 1,212 | 6,795 | ||||||||||||||||||||||||

| Washington | 0 | 3,467 | 0 | 3,467 | 0 | 4,347 | 0 | 4,347 | ||||||||||||||||||||||||

| West Virginia | 0 | 89 | 0 | 89 | 0 | 81 | 0 | 81 | ||||||||||||||||||||||||

| Wisconsin | 0 | 2,007 | 0 | 2,007 | 0 | 1,833 | 0 | 1,833 | ||||||||||||||||||||||||

| Wyoming | 0 | 1,103 | 0 | 1,103 | 0 | 1,539 | 0 | 1,539 | ||||||||||||||||||||||||

| Total | $ | 107,191 | $ | 100,699 | $ | 29,314 | $ | 237,203 | $ | 102,943 | $ | 114,866 | $ | 31,844 | $ | 249,654 | ||||||||||||||||

Source: S&P Global.

14

FELDMAN FINANCIAL ADVISORS, INC.

Table 6 (continued)

Consolidated Direct Premiums Written by State

For the Years Ended December 31, 2023 and 2024

(Percent of Total)

| Year Ended December 31, 2024 | Year Ended December 31, 2023 | |||||||||||||||||||||||||||||||

| ECM | ARIC | 1CA | Combined | ECM | ARIC | 1CA | Combined | |||||||||||||||||||||||||

| Alabama | 0.00 | 1.67 | 0.00 | 0.71 | 0.00 | 1.48 | 0.00 | 0.68 | ||||||||||||||||||||||||

| Alaska | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.12 | 0.00 | 0.06 | ||||||||||||||||||||||||

| Arizona | 0.00 | 3.65 | 0.00 | 1.55 | 0.00 | 3.06 | 0.00 | 1.41 | ||||||||||||||||||||||||

| Arkansas | 12.83 | 2.02 | 0.00 | 6.66 | 13.62 | 1.46 | 0.00 | 6.29 | ||||||||||||||||||||||||

| California | 0.00 | 3.35 | 0.00 | 1.42 | 0.00 | 3.08 | 0.00 | 1.42 | ||||||||||||||||||||||||

| Colorado | 0.00 | 2.74 | 0.00 | 1.16 | 0.00 | 2.37 | 0.00 | 1.09 | ||||||||||||||||||||||||

| Connecticut | 0.00 | 1.05 | 0.00 | 0.45 | 0.00 | 1.86 | 0.00 | 0.86 | ||||||||||||||||||||||||

| D.C. | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.01 | 0.00 | 0.00 | ||||||||||||||||||||||||

| Delaware | 0.00 | 0.02 | 0.00 | 0.01 | 0.00 | 0.03 | 0.00 | 0.01 | ||||||||||||||||||||||||

| Florida | 0.00 | 3.84 | 0.00 | 1.63 | 0.00 | 3.95 | 0.00 | 1.82 | ||||||||||||||||||||||||

| Georgia | 2.38 | 2.99 | 10.30 | 3.62 | 2.27 | 2.76 | 9.60 | 3.43 | ||||||||||||||||||||||||

| Hawaii | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | ||||||||||||||||||||||||

| Idaho | 0.00 | 1.94 | 0.00 | 0.82 | 0.00 | 2.65 | 0.00 | 1.22 | ||||||||||||||||||||||||

| Illinois | 0.09 | 3.02 | 0.00 | 1.32 | 0.08 | 2.42 | 0.00 | 1.15 | ||||||||||||||||||||||||

| Indiana | 5.93 | 1.60 | 7.06 | 4.23 | 6.44 | 1.54 | 8.88 | 4.50 | ||||||||||||||||||||||||

| Iowa | 3.53 | 0.84 | 0.00 | 1.95 | 0.54 | 0.96 | 0.00 | 0.66 | ||||||||||||||||||||||||

| Kansas | 6.61 | 1.16 | 0.00 | 3.48 | 6.87 | 1.25 | 0.00 | 3.41 | ||||||||||||||||||||||||

| Kentucky | 8.39 | 2.01 | 7.87 | 5.62 | 8.71 | 1.77 | 9.85 | 5.66 | ||||||||||||||||||||||||

| Louisiana | 0.00 | 3.33 | 0.00 | 1.42 | 0.00 | 2.93 | 0.00 | 1.35 | ||||||||||||||||||||||||

| Maine | 0.00 | 0.73 | 0.00 | 0.31 | 0.00 | 0.81 | 0.00 | 0.37 | ||||||||||||||||||||||||

| Maryland | 0.74 | 0.83 | 0.00 | 0.69 | 0.77 | 0.88 | 0.00 | 0.72 | ||||||||||||||||||||||||

| Massachusetts | 0.00 | 2.39 | 0.00 | 1.02 | 0.00 | 2.85 | 0.00 | 1.31 | ||||||||||||||||||||||||

| Michigan | 0.00 | 1.84 | 0.00 | 0.78 | 0.00 | 1.53 | 0.00 | 0.70 | ||||||||||||||||||||||||

| Minnesota | 0.00 | 1.87 | 0.00 | 0.79 | 0.00 | 1.95 | 0.00 | 0.90 | ||||||||||||||||||||||||

| Mississippi | 0.00 | 1.70 | 0.00 | 0.72 | 0.00 | 1.94 | 0.00 | 0.89 | ||||||||||||||||||||||||

| Missouri | 7.65 | 3.57 | 0.00 | 4.97 | 8.49 | 3.54 | 0.00 | 5.13 | ||||||||||||||||||||||||

| Montana | 0.00 | 3.42 | 0.00 | 1.45 | 0.00 | 3.56 | 0.00 | 1.64 | ||||||||||||||||||||||||

| Nebraska | 2.70 | 0.89 | 0.00 | 1.60 | 1.35 | 0.74 | 0.00 | 0.89 | ||||||||||||||||||||||||

| Nevada | 0.00 | 1.92 | 0.00 | 0.82 | 0.00 | 1.59 | 0.00 | 0.73 | ||||||||||||||||||||||||

| New Hampshire | 0.00 | 0.23 | 0.00 | 0.10 | 0.00 | 0.43 | 0.00 | 0.20 | ||||||||||||||||||||||||

| New Jersey | 0.00 | 1.81 | 0.00 | 0.77 | 0.00 | 1.83 | 0.00 | 0.84 | ||||||||||||||||||||||||

| New Mexico | 0.00 | 2.97 | 0.00 | 1.26 | 0.00 | 2.75 | 0.00 | 1.26 | ||||||||||||||||||||||||

| New York | 0.00 | 1.76 | 0.00 | 0.75 | 0.00 | 1.79 | 0.00 | 0.82 | ||||||||||||||||||||||||

| North Carolina | 13.76 | 8.30 | 12.15 | 11.24 | 13.90 | 11.07 | 10.57 | 12.17 | ||||||||||||||||||||||||

| North Dakota | 0.00 | 0.28 | 0.00 | 0.12 | 0.00 | 0.32 | 0.00 | 0.15 | ||||||||||||||||||||||||

| Ohio | 0.69 | 2.25 | 0.69 | 1.35 | 0.66 | 1.70 | 0.87 | 1.17 | ||||||||||||||||||||||||

| Oklahoma | 0.00 | 4.30 | 0.00 | 1.83 | 0.00 | 3.93 | 0.00 | 1.81 | ||||||||||||||||||||||||

| Oregon | 0.00 | 2.65 | 0.00 | 1.13 | 0.00 | 3.08 | 0.00 | 1.42 | ||||||||||||||||||||||||

| Pennsylvania | 25.37 | 1.85 | 16.23 | 14.25 | 26.67 | 1.73 | 19.71 | 14.31 | ||||||||||||||||||||||||

| Rhode Island | 0.00 | 0.17 | 0.00 | 0.07 | 0.00 | 0.65 | 0.00 | 0.30 | ||||||||||||||||||||||||

| South Carolina | 0.00 | 2.57 | 0.00 | 1.09 | 0.00 | 2.21 | 0.00 | 1.02 | ||||||||||||||||||||||||

| South Dakota | 0.45 | 1.03 | 0.00 | 0.64 | 0.51 | 0.99 | 0.00 | 0.66 | ||||||||||||||||||||||||

| Tennessee | 4.79 | 1.01 | 2.66 | 2.92 | 4.78 | 0.93 | 2.69 | 2.74 | ||||||||||||||||||||||||

| Texas | 0.00 | 6.19 | 39.67 | 7.53 | 0.00 | 4.87 | 34.03 | 6.58 | ||||||||||||||||||||||||

| Utah | 0.00 | 0.51 | 0.00 | 0.22 | 0.00 | 0.44 | 0.00 | 0.20 | ||||||||||||||||||||||||

| Vermont | 0.00 | 0.34 | 0.00 | 0.14 | 0.00 | 0.41 | 0.00 | 0.19 | ||||||||||||||||||||||||

| Virginia | 4.07 | 0.75 | 3.36 | 2.57 | 4.33 | 0.98 | 3.81 | 2.72 | ||||||||||||||||||||||||

| Washington | 0.00 | 3.44 | 0.00 | 1.46 | 0.00 | 3.78 | 0.00 | 1.74 | ||||||||||||||||||||||||

| West Virginia | 0.00 | 0.09 | 0.00 | 0.04 | 0.00 | 0.07 | 0.00 | 0.03 | ||||||||||||||||||||||||

| Wisconsin | 0.00 | 1.99 | 0.00 | 0.85 | 0.00 | 1.60 | 0.00 | 0.73 | ||||||||||||||||||||||||

| Wyoming | 0.00 | 1.09 | 0.00 | 0.46 | 0.00 | 1.34 | 0.00 | 0.62 | ||||||||||||||||||||||||

| Total | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | ||||||||||||||||||||||||

Source: S&P Global.

15

FELDMAN FINANCIAL ADVISORS, INC.

Losses and loss adjustment expenses incurred decreased by 10.4% or $12.7 million from $122.3 million in 2023 to $109.6 million in 2024. Losses and loss adjustment expenses incurred represent the Company’s largest expense item and include: (i) claim payments made; (ii) estimates for future claim payments and changes in those estimates for prior periods; and (iii) costs associated with investigating, defending, and adjusting claims. ECM’s consolidated loss ratio decreased from 74.6% in 2023 to 61.9% in 2024, primarily due to the increase in net premiums earned and favorable development relative to prior years’ loss reserve estimates. Underwriting expenses on a GAAP basis increased from $38.3 million in 2023 to $61.2 million in 2024 and ECM’s consolidated expense ratio increased from 23.3% in 2023 to 34.5% in 2024. ECM’s combined ratio improved from 97.9% in 2023 to 96.4% in 2015, driven largely by the growth in net premiums earned and the decline in losses and loss adjustment expenses incurred.

ECM’s consolidated investment income increased by $1.6 million or 22.8% from $7.3 million in 2023 to $8.9 million in 2024. The increase in investment income reflected the expansion of investment portfolio holdings and a general increase in market rates during 2024. Net realized capital gains increased from $780,000 in 2023 to $4.4 million in 2024 due to the overall appreciation in the equity securities markets. Interest expense, largely representing the interest costs of the surplus notes, increased from $1.2 million in 2023 to $1.8 million in 2024, as 2024 reflected a full year’s cost of the $15.0 million surplus note issued in May 2023. Overall, net investment profits increased from $5.0 million in 2023 to $10.3 million in 2024.

ECM recognized $3.2 million in goodwill amortization expense in both 2023 and 2024. The goodwill resulted from the acquisition of ARIC in 2022 and is being expensed on a straight-line method over ten years. The outstanding balance of goodwill declined from $27.0 million at December 31, 2023 to $23.9 million at December 31, 2024.

The Company’s consolidated income before income taxes increased by $8.4 million from $5.7 million for the year ended December 31, 2023 to $14.0 million for the year ended December 31, 2024. The improvement in pre-tax earnings resulted from the $2.9 million increase in underwriting profits and $5.3 million increase in net investment profits. Federal income tax expense amounted to $2.4 million in 2023 and $2.9 million in 2024. The effective income tax rate was approximately 20.7% in 2024.

Statutory Financial Data Overview

State insurance laws and regulations require ECM (and its subsidiary and affiliate insurance carriers) to file financial statements with state insurance departments in every state where it does business, and the operations of ECM are subject to examination by those departments. ECM prepares statutory financial statements in accordance with accounting practices and procedures prescribed or permitted by these departments. Certain accounting standards differ under statutory accounting practices (“SAP”) as compared to GAAP. For example, premium income is recognized on a pro rata basis over the term covered by the insurance policy, while the related acquisition costs are expensed when incurred under SAP. Under GAAP, both premium income and the related policy acquisition costs are recognized on a pro rata basis over the term of the insurance policy. Therefore, the SAP data for ECM does not correspond to the GAAP presentation.

Table 7 presents summary statutory financial data for ECM over the period from December 31, 2014 to 2024 and for the year-to-date (“YTD”) period ended June 30, 2025. The financial data presented in Table 7 includes combined statutory financial information of ECM, 1CA, EGM, and (effective December 31, 2022) ARIC. Exhibits IV-1, IV-2, IV-3, and IV-4 contain unconsolidated statutory financial summary data for ECM, ARIC, 1CA, and EGM, respectively, for the years ended December 31, 2021 to 2024 and the six months ended June 30, 2025.

16

FELDMAN FINANCIAL ADVISORS, INC.

As reflected in Table 7 on a statutory basis, the Company has experienced significant growth in total assets, capital and surplus, and direct premiums written. ECM’s statutory total assets increased at a compound annual growth rate of 9.5% over the ten-year period from $122.5 million at December 31, 2014 to $303.5 million at December 31, 2024. ECM’s statutory capital and surplus increased at compound annual growth rate of 7.8% from $59.3 million at December 31, 2014 to $126.0 million at December 31, 2024. ECM’s direct premiums written increased at a compound annual growth rate of 13.4% from $67.4 million in 2014 to $237.2 million in 2024.

Historically, ECM’s premium revenue business was generated in a few states, including Pennsylvania, North Carolina, Indiana, and Kentucky, and concentrated primarily on farmowners multi-peril coverage. As part of its strategy to mitigate risk, ECM implemented initiatives to diversify its product offerings and geographic footprint. These diversification efforts led to the acquisition in 2022 of ARIC, which significantly expanded ECM’s geographic presence and product diversification. As a result, ECM’s consolidated direct premiums written expanded from $107.8 million and $160.5 million in 2021 and 2022, respectively, to $249.7 million in 2023. Concurrently, the ratio of ECM’s net premiums written to average capital and surplus increased from 98.6% in 2021 to 129.0% in 2022 and 168.1% in 2023.

ECM experienced a consolidated statutory net loss of $9.7 million for the year ended December 31, 2023, chiefly due to the negative impact of the frequency and severity of weather-related events. ECM’s statutory combined ratio increased from 90.6% in 2022 to 106.5% in 2023. ECM’s statutory expense ratio increased moderately from 29.6% in 2022 to 30.8% in 2023, while its statutory loss ratio increased considerably from 61.0% in 2022 to 75.7% in 2023. ECM’s consolidated statutory earnings rebounded in 2024 to a positive level of $14.8 million. The statutory loss ratio returned to a more normalized level of 62.3% in 2024 and the resulting statutory combined ratio was 96.4%. Benefiting from the integration of ARIC, ECM’s net premiums earned increased steadily from $122.5 million in 2022 to $159.7 million in 2023 and $172.7 million in 2024. ECM’s statutory earnings in 2024 were also boosted by the increase in net investment profits from $3.8 million in 2023 to $9.7 million in 2024.

For the six months ended June 30, 2025, ECM reported a consolidated statutory net loss of $4.2 million. ECM’s profitability is usually cyclical due to weather-related losses with net underwriting profits generally being lower in the first half of the calendar year versus the second half of the year. ECM’s consolidated statutory combined ratio amounted to 107.0% for the first half of 2025, reflecting a 73.6% loss ratio and a 33.4% expense ratio. As a result of the statutory net loss in the first half of 2025, ECM’s consolidated statutory capital and surplus declined from $126.0 million at December 31, 2024 to $122.3 million at June 30, 2025. The ratio of statutory capital and surplus to statutory total assets declined moderately from 41.5% at December 31, 2024 to 39.5% at June 30, 2025.

17

FELDMAN FINANCIAL ADVISORS, INC.

Table 7

Statutory Financial Overview

ECM Insurance Group

As of and For the Years Ended December 31, 2014 to 2024 and

As of and For the Year-to-Date Period Ended June 30, 2025

(Data in Thousands of Dollars, Except Percentages)

| YTD | Year Ended | |||||||||||||||||||||||||||||||||||||||||||||||

| 6/30/25 | 12/31/24 | 12/31/23 | 12/31/22 | 12/31/21 | 12/31/20 | 12/31/19 | 12/31/18 | 12/31/17 | 12/31/16 | 12/31/15 | 12/31/14 | |||||||||||||||||||||||||||||||||||||

| Balance Sheet Data | ||||||||||||||||||||||||||||||||||||||||||||||||

| Total Assets | 309,728 | 303,544 | 280,716 | 262,307 | 224,866 | 198,524 | 173,927 | 155,496 | 152,251 | 142,467 | 133,106 | 122,492 | ||||||||||||||||||||||||||||||||||||

| Total Liabilities | 187,419 | 177,535 | 170,705 | 160,689 | 107,764 | 97,033 | 85,302 | 87,076 | 83,026 | 76,249 | 67,790 | 63,213 | ||||||||||||||||||||||||||||||||||||

| Capital and Surplus | 122,309 | 126,009 | 110,011 | 101,618 | 117,102 | 101,491 | 88,625 | 68,419 | 69,225 | 66,218 | 65,316 | 59,279 | ||||||||||||||||||||||||||||||||||||

| Capital and Surplus Growth (%) | -2.94 | % | 14.54 | % | 8.26 | % | -13.22 | % | 15.38 | % | 14.52 | % | 29.53 | % | -1.16 | % | 4.54 | % | 1.38 | % | 10.18 | % | 12.38 | % | ||||||||||||||||||||||||

| Capital and Surplus / Total Assets | 39.49 | % | 41.51 | % | 39.19 | % | 38.74 | % | 52.08 | % | 51.12 | % | 50.96 | % | 44.00 | % | 45.47 | % | 46.48 | % | 49.07 | % | 48.39 | % | ||||||||||||||||||||||||

| Income Statement Data | ||||||||||||||||||||||||||||||||||||||||||||||||

| Direct Premiums Written (DPW) | 116,120 | 237,203 | 249,654 | 160,451 | 107,791 | 98,211 | 83,078 | 79,926 | 79,865 | 76,942 | 72,822 | 67,376 | ||||||||||||||||||||||||||||||||||||

| Net Premiums Written (NPW) | 94,095 | 167,455 | 177,853 | 141,058 | 107,799 | 98,483 | 80,268 | 77,329 | 77,622 | 74,687 | 71,616 | 64,948 | ||||||||||||||||||||||||||||||||||||

| Net Premiums Earned | 86,964 | 172,748 | 159,737 | 122,545 | 103,153 | 90,147 | 77,814 | 77,607 | 76,276 | 73,291 | 68,432 | 61,153 | ||||||||||||||||||||||||||||||||||||

| Net Loss and LAE Incurred | 64,025 | 107,692 | 120,920 | 74,730 | 60,210 | 53,742 | 51,549 | 57,533 | 56,538 | 58,231 | 41,551 | 38,333 | ||||||||||||||||||||||||||||||||||||

| Net Underwriting Expense | 31,645 | 57,652 | 55,236 | 42,144 | 32,967 | 29,813 | 24,416 | 23,177 | 21,366 | 21,393 | 20,632 | 18,401 | ||||||||||||||||||||||||||||||||||||

| Net Underwriting Gain (Loss) | (8,706 | ) | 7,404 | (16,419 | ) | 5,671 | 9,976 | 6,592 | 1,849 | (3,103 | ) | (1,628 | ) | (6,333 | ) | 6,249 | 4,418 | |||||||||||||||||||||||||||||||

| Net Investment Income | 3,072 | 9,721 | 3,844 | 3,856 | 8,153 | 3,389 | 3,541 | 5,037 | 4,307 | 3,216 | 4,502 | 4,688 | ||||||||||||||||||||||||||||||||||||

| Income Tax Expense (Benefit) | (1,148 | ) | 2,997 | (2,414 | ) | 2,276 | 2,735 | 2,442 | 780 | 125 | 356 | (1,177 | ) | 3,039 | 2,382 | |||||||||||||||||||||||||||||||||

| Net Income (Loss) | (4,219 | ) | 14,750 | (9,725 | ) | 7,616 | 15,786 | 7,917 | 5,010 | 2,213 | 2,721 | (1,493 | ) | 8,107 | 7,096 | |||||||||||||||||||||||||||||||||

| Operating Ratios (%) | ||||||||||||||||||||||||||||||||||||||||||||||||

| Growth Rate - DPW | (10.37 | ) | (4.99 | ) | 55.60 | 48.85 | 9.75 | 18.22 | 3.94 | 0.08 | 3.80 | 5.66 | 8.08 | 13.39 | ||||||||||||||||||||||||||||||||||

| NPW / Avg. Capital and Surplus | 151.57 | 141.90 | 168.08 | 128.99 | 98.63 | 103.60 | 102.22 | 112.36 | 114.62 | 113.56 | 114.96 | 115.95 | ||||||||||||||||||||||||||||||||||||

| Loss and LAE Ratio | 73.62 | 62.34 | 75.70 | 60.98 | 58.37 | 59.62 | 66.25 | 74.13 | 74.12 | 79.45 | 60.72 | 62.68 | ||||||||||||||||||||||||||||||||||||

| Expense Ratio | 33.35 | 34.06 | 30.81 | 29.62 | 30.58 | 30.27 | 30.42 | 29.97 | 27.53 | 28.64 | 28.81 | 28.33 | ||||||||||||||||||||||||||||||||||||