ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2025 Commission file number: 1-3579

PITNEY BOWES INC.

State of incorporation:

Delaware

I.R.S. Employer Identification No.

06-0495050

Address:

27 Waterview Drive,

Shelton,

Connecticut

06484

Telephone Number:

(203)

922-4000

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class

Trading Symbol(s)

Name of Each Exchange on Which Registered

Common Stock, $1 par value per share

PBI

New York Stock Exchange

6.7% Notes due 2043

PBI.PRB

New York Stock Exchange

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yesþ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ Noþ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yesþ No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files) Yesþ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definition of "large accelerated filer,""accelerated filer,""smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer

þ

Accelerated filer

o

Non-accelerated filer

o

Smaller reporting company

☐

Emerging growth company

☐

If an emerging growth company, indicate by check mark whether the registrant has elected not to use the extended transition period for complying with new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. Yes ☑ No ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No þ

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. þ

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ¨

As of June 30, 2025, the aggregate market value of the registrant's common stock held by non-affiliates of the registrant was $2 billion based on the closing sale price as reported on the New York Stock Exchange. At January 31, 2026, there were 149,942,698 outstanding shares of common stock, $1 par value.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's proxy statement to be filed within 120 days after our fiscal year end in connection with the Annual Meeting of Stockholders, are incorporated by reference in Part III of this Form 10-K.

This Annual Report on Form 10-K (Annual Report) contains statements that are forward-looking. We believe that these forward-looking statements are reasonable based on our current expectations and assumptions. However, we caution readers that any forward-looking statement within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934 are subject to risks and uncertainties and actual results could differ materially. Words such as "estimate," "project," "plan," "believe," "expect," "anticipate," "intend" and similar expressions may identify such forward-looking statements. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise, except as required by law. Forward-looking statements in this Annual Report speak only as of the date hereof, and forward-looking statements in documents attached that are incorporated by reference speak only as of the date of those documents.

Forward-looking statements are subject to inherent risks and uncertainties and subject to change. Accordingly, actual results of operations, financial condition and cash flows could differ materially from those projected or assumed in our forward-looking statements. Certain factors which could cause future financial performance to differ materially from expectations include, without limitation:

•changes in postal regulations or the operations and financial health of posts in the U.S. or other major markets, or changes to the broader postal or shipping markets

•accelerated or sudden decline in physical mail or shipping volumes

•the loss of some of our larger clients

•periods of difficult economic conditions impacting the company and our clients, including inflation and rising prices, changes in interest rates and a slow-down in economic activity, including a global recession, or a prolonged U.S. government shutdown

•our ability to compete successfully

•changes in banking regulations, major bank failures, the loss of our Industrial Bank charter or limitations on our banking activities

•changes in government contracting regulations and compliance challenges

•changes in labor and transportation availability and costs

•global supply chain issues adversely impacting our third party suppliers' ability to provide us with products and services

•changes in trade policies, tariffs and regulations

•changes in senior management and Board of Directors, loss of key employees and ability to attract and retain employees

•expenses and potential impacts resulting from cyber-attacks or other cybersecurity incidents affecting us or our suppliers

•inability to comply with data privacy and protection laws and regulations

•interruptions or difficulties in the operation of our cloud-based applications and systems or those of our suppliers

•changes in credit ratings, capital market disruptions, decline in cash flows, noncompliance with debt covenants or future interest rate increases that may adversely impact our ability to access capital markets at reasonable costs

•our indebtedness, including Convertible Notes, and the impact of any conversion, repurchase or redemption of the Convertible Notes

•our success at managing customer credit risk

•changes in foreign currency exchange rates

•the risks and uncertainties associated with the Ecommerce Restructuring

•changes in tax rates, laws or regulations

•inability to protect our intellectual property rights and intellectual property infringement claims

•our success in developing and marketing new products and services and obtaining regulatory approvals, if required

•acts of nature and the impact of a pandemic on the Company and the services and solutions we offer

•shareholder activism

Further information about factors that could materially affect us, including our results of operations and financial condition, is contained in Item 1A. "Risk Factors" in this Annual Report.

3

ITEM 1. BUSINESS

General

Pitney Bowes Inc. ("we, us, our, or the company") is a technology-driven company that provides digital shipping solutions, mailing innovation, and financial services to clients around the world - including more than 90 percent of the Fortune 500. Small businesses to large enterprises, and government entities rely on Pitney Bowes to reduce the complexity of sending mail and parcels.

Business Segments

SendTech Solutions

SendTech Solutions provides clients with physical and digital shipping and mailing technology solutions and other applications to help simplify and save on the sending, tracking and receiving of letters, parcels and flats, as well as supplies and maintenance services for these offerings. We offer financing alternatives that enable clients to finance equipment. Digital delivery services enables clients to reduce transportation and logistics costs, select the best carrier based on need and cost, improve delivery times and track packages in real-time. Powered by our shipping APIs, clients can purchase postage, print shipping labels and access shipping and tracking services from multiple carriers that can be easily integrated into any web application such as online shopping carts or ecommerce sites and provide guaranteed delivery times and flexible payment options.

Through our wholly owned subsidiary, The Pitney Bowes Bank ("the Bank"), we offer financing alternatives that enable clients to finance other manufacturers' equipment and product purchases, a revolving credit solution that allows clients to make meter rental payments and purchase postage, services and supplies, an interest-bearing deposit solution to clients that prefer to prepay postage and meet working capital needs.

Presort Services

We are the largest workshare partner of the United States Postal Service ("USPS") and national outsource provider of mail sortation services that allow clients to qualify volumes of First-Class Mail, First Class Flats, Marketing Mail and Marketing Mail Flats/Bound Printed Matter for postal workshare discounts. Using our proprietary technology, we provide clients with end-to-end solutions from pick up to delivery into the postal system network, improving mail delivery and enhancing total mail value including optimizing postage savings.

Other

Other represents amounts of the prior Global Ecommerce segment that did not qualify for discontinued operations treatment, primarily related to operations that were dissolved or sold and certain shared services functions. In August 2024, we exited from the Global Ecommerce business through an orderly wind-down of these operations. See Note 4 to the Consolidated Financial Statements for further information.

Sales and Services

We market our products, solutions and services through a direct and inside sales force, global and regional partner channels, direct mailings and digital channels. We provide call-center, online and on-site support services for our products and solutions. Support services are primarily provided under maintenance contracts.

Competition

SendTech Solutions

We face competition from other mail equipment and solutions providers and those that offer online shipping and mailing products and services solutions. We differentiate ourselves through the breadth of our physical and digital offerings, including cloud-based software platforms designed to support complex, high-volume, multi-carrier shipping and mailing operations, an open platform architecture; competitive pricing; available financing and payment solutions; product reliability; support services; and our extensive knowledge of the shipping and mailing industry.

Our financing operations face competition, in varying degrees, from large, diversified financial institutions, leasing companies, commercial finance companies, commercial banks and smaller specialized firms. We believe what differentiates us from our competitors is the breadth of our financing and payment solutions and our ability to seamlessly integrate these solutions into our clients' shipping and mailing operations.

Presort Services

We face competition from regional and local presort providers, cooperatives of multiple local presort providers, consolidators and service bureaus that offer presort solutions as part of a larger bundle of outsourcing services. We also face competition from large mailers that have sufficient volumes and the capability to sort their own mailings in-house and could use excess capacity to offer presort services to others. The principal competitive factors include price, innovative service, delivery speed, tracking and reporting, industry expertise and economies of scale. Our competitive advantages include our national network of processing centers handling

4

upwards of 15 billion mail pieces annually including a proprietary Mail Exchange program affording clients maximized postage discounts, improved deliverability, and proven business continuity protocols. Clients benefit from our industry expertise at all levels through local Mail Design Professional certified support resources, allowing greater access to programs like United States Postal Service ("USPS") Promotions and Incentives, saving additional costs on mailing and increasing impact of their mail. Additionally, a dedicated postal relations team ensures rapid resolution for quality and compliance. With a fleet of over 350 drivers and vehicles, we provide clients flexible logistics including a unique USPS long-haul partnership made possible by our significant scale and processing volumes, ensuring improved delivery performance and additional safeguards for participating mail, particularly during peak seasons. Our proprietary Presort Services Account offers mail management capabilities from pick-up to invoicing including tracking, reporting, and data ingestion assuring mailers complete visibility and chain of custody. Our competitive capabilities collectively result in unexpected value for mailers.

Also see Item 1A. Risk Factors for further details regarding the competition our businesses face.

Research and Development

We invest in research and development activities to develop new products and solutions, enhance the effectiveness and functionality of existing products and solutions and deliver high value technology and differentiated services in high value segments of the market.

Third Party Suppliers

SendTech Solutions depends on third party suppliers and outsource providers for a variety of services and product components and the hosting of our SaaS offerings. Presort Services relies on third party suppliers to help equip our facilities, provide warehouse support and assist with logistical operations. All of our businesses and corporate functions depend on third party providers for a variety of data analytics, sales, reporting and other functions. In certain instances, we rely on single-sourced or limited-sourced suppliers and outsourcing vendors around the world because doing so is advantageous due to quality, price or lack of alternative sources. We have risk mitigation programs to monitor conditions affecting our suppliers' ability to fulfill expected commitments. We believe that our available sources for services, components, supplies, logistics and manufacturing are adequate.

Regulatory Matters

We are subject to the regulations of the USPS and other postal authorities worldwide, including requirements applicable to our mailing, shipping and related services. We are also subject to regulations as a U.S. government contractor, including applicable procurement and compliance requirements, as well as transportation regulations for various parts of our business, worldwide customs, trade and export regulations related to our domestic and cross-border logistics operations. In addition, our businesses that use, process, transmit or store personal, confidential or proprietary data are subject to evolving data privacy and security regulations in the United States and internationally. The Bank is chartered as an Industrial Bank under the laws of the State of Utah. As such, the Bank is subject to the regulations of the Utah Department of Financial Institutions and the Federal Deposit Insurance Corporation, and to applicable banking laws and regulations, including those relating to capital and liquidity, consumer compliance, and anti-money laundering and sanctions compliance. Certain company affiliates that provide services to the Bank are also subject to regulatory requirements applicable to those services.

Climate Change

Although climate change has not had a material impact on our operations to date, the risk of increasingly severe climate events or the risk that those events happen more frequently could affect one or more of our facilities and our ability to conduct daily operations or impact our clients and their ability to do business with us. Changes in regulation relating to climate change and other aspects of sustainability and governance of ESG, including different regulatory requirements in different locations where we operate, may change the cost of compliance for collecting, assuring and reporting information regarding these impacts and risk management.

Human Capital

Employee Profile

We have approximately 6,600 employees, with 75% located in the United States. We also rely on a contingent hourly workforce to supplement our full-time workforce to meet fluctuating demand.

We seek to create a high-performance culture that will drive and sustain enhanced long-term value for all our shareholders. To attract, retain and engage the talent needed, we provide competitive compensation designed to reward performance and contribution. We regularly assess the business environments and labor markets in the areas we operate to ensure our compensation programs reflect best practices and are market competitive. Depending on position and level, elements of our compensation packages include base salary, variable compensation based on individual and company objectives and equity. We provide a competitive benefits package, including medical, dental, life and disability insurance, and benefits that provide additional support for our employees’ mental, physical, financial and social well-being.

5

Employee Engagement and Development

We are committed to creating a culture where our employees feel supported and valued. We offer employees many opportunities to advance their skills, learn new skills and achieve career goals through virtual and in-person development and training programs, professional development initiatives, experiential learning, mentoring and coaching programs. Through multiple platforms, we offer employees and candidates varied opportunities to find development opportunities and stay informed about key changes to our business. We conduct periodic employee engagement surveys and benchmark the results both internally and against other high performing organizations. We consider feedback from employees and we make changes where possible and financially prudent.

Health and Safety

We are committed to providing a safe workplace that protects against and limits personal injury and environmental harm. Through regular evaluations of site safety performance, sharing of successes, and creating projects to engage employees in safety improvements, we identify risks, provide guidance and training, review and learn from accidents, and reduce injuries. We also report monthly to both local site management and senior leadership on safety metrics, trends, risks and regulatory activity.

Available Information

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and any amendments thereto filed with, or furnished to, the SEC, are available, free of charge, through the Investor Relations section of our website at www.investorrelations.pitneybowes.com or from the SEC's website at www.sec.gov, as soon as reasonably practicable after these reports are electronically filed with, or furnished to, the SEC. The other information found on our website is not part of this or any other report we file with or furnish to the SEC and is not incorporated herein or therein by reference.

Information About Our Executive Officers

Name

Age

Title

Executive Officer Since

Kurt Wolf

52

Chief Executive Officer

2025

Paul Evans

57

Executive Vice President, Chief Financial Officer and Treasurer

2025

Lauren Freeman-Bosworth

51

Executive Vice President, General Counsel and Corporate Secretary

2024

Debbie Pfeiffer

65

Executive Vice President and President, Presort Services

2024

Todd Everett

52

Executive Vice President and President, Sending Technology Solutions

2025

There are no family relationships among the above officers.

Mr. Wolf was appointed Chief Executive Officer in May 2025 and has served on our Board of Directors since May 2023. Prior to joining the Company, he served as Managing Member and Chief Investment Officer of Hestia Capital Management, a deep value hedge fund, since 2009.

Mr. Evans was appointed Executive Vice President, Chief Financial Officer and Treasurer in July 2025 and served on our Board of Directors since 2024. Previously, he served as Chief Operating Officer at America's Auto Auction Group, Interim Chief Executive Officer at Hill International, Inc. and Chief Financial Officer of Sevan Multi-Site Solutions.

Ms. Freeman-Bosworth was appointed Executive Vice President, General Counsel and Corporate Secretary in April 2024. Prior to this appointment, she was the Company's Vice President and Deputy General Counsel, Litigation, Governance and Compliance since June 2014.

Ms. Pfeiffer was appointed Executive Vice President and President, Presort Services in January 2024. Prior to this appointment, she served as the Company's President, Presort Services since November 2015.

Mr. Everett was appointed Executive Vice President and President, Sending Technology Solutions in September 2025 and served on our Board of Directors since 2023. He also is currently an independent advisor to several ecommerce companies and a board member of a private technology shipping company. Mr. Everett also held various roles at Newgistics, Inc., including President and Chief Executive Officer from 2015 until February 2018, prior to Pitney Bowes' acquisition of Newgistics.

6

ITEM 1A. RISK FACTORS

Our operations face certain risks that should be considered in evaluating our business. We manage and mitigate these risks on a proactive basis, using an enterprise risk management program. Nevertheless, the following risk factors, some of which may be beyond our control, could materially affect our business, financial condition, results of operations, brand and reputation, and may cause future results to be materially different from our current expectations. These risk factors are not intended to be all inclusive.

Mailing and Shipping Industry Risks

The financial condition and governance model of the USPS, or the national posts in our other major markets, has affected, and could, in the future, adversely affect client demand for our offerings and thus our financial performance.

We are dependent on financially viable national posts in the geographic markets where we operate, particularly in the United States. A significant portion of our revenue depends upon the ability of these posts, especially the USPS, to provide reliable, competitive mail and package delivery services to our clients. Their ability to provide high quality reliable service at affordable rates relates to their ongoing financial strength. The USPS and other national posts continue to face financial challenges which could lead to changes in governance models. If these challenges or changes interfere with these posts’ ability to provide the services they currently provide, our financial performance may be adversely affected.

We are subject to postal regulations and processes, which could adversely affect our financial performance.

A significant portion of our business is subject to regulation and oversight by the USPS, posts in other major markets, and the governmental bodies that regulate the posts themselves. These postal authorities have the power to regulate some of our current products and services and to establish guidelines for postage rates. They also must approve many of our new product and service offerings before we can bring them to market. If new product and service offerings are not approved or there are significant conditions to approval, our ability to grow the business and in turn, our financial performance, could be adversely affected. Additionally, if favorable postage rates are reversed, regulations on existing products, rates or services are changed, legal or regulatory changes cause posts to change their operating models in a way that disadvantages our business, posts utilize their position in the market or their role as product regulator to limit competition in areas where the posts themselves offer solutions, or if we fall out of compliance with the posts’ regulations, our financial performance could be adversely affected.

If we are not able to respond to the continuing decline in the volume of physical mail delivered via traditional postal services, our financial performance could be adversely affected.

Continuing declines in traditional mail volumes impact our financial results. An accelerated or sudden decline in mail volumes could result from one or more of the following factors: changes in communication technologies and their use; changes in frequency and quality of mail delivery from national posts; changes in law that favor alternative means of communication, burden mail, or limit how the mail may be used; significant rate increases; or other external events affecting physical mail delivery. If we are not successful at meeting the continuing challenges faced in our mailing business, or if physical mail volumes experience an accelerated or sudden decline, our financial performance could be adversely affected.

Our ability to compete in the shipping market in the United States depends upon certain contractual relationships we have with the USPS and other carriers, as well as their service.

Our SendTech Solutions offerings depend upon certain contractual relationships with the USPS and other carriers to enable us to offer these services profitably. Should the USPS or other carriers make changes to how they contract with us for our solutions, our profitability could be adversely affected.

Business Operational Risks

The markets for our products and services are highly competitive.

SendTech Solutions faces competition from other mail equipment and solutions providers, companies that offer products and services as alternative means of message communications and those that offer online shipping and mailing products and services solutions. SendTech Solutions’ digital shipping business competes with technology providers ranging from large, established companies and national posts to smaller companies offering negotiated carrier rates. In addition, our financing operations face competition, in varying degrees, from large, diversified financial institutions, leasing companies, commercial finance companies, commercial banks and smaller specialized firms. Presort Services faces competition from regional and local presort providers, cooperatives of multiple local presort providers, consolidators and service bureaus that offer presort solutions as part of a larger bundle of outsourcing services and large volume mailers that have sufficient volumes and the capability to presort their own mailings in-house and could use excess capacity to offer presort services to others. We compete on the basis of a variety of factors, including price and the breadth and quality of our products and services. If we are not able to differentiate ourselves from our competitors or effectively compete with them, we may lose clients and the financial results of these segments may be adversely affected.

7

If we fail to effectively manage our third party suppliers, or if their ability to perform were negatively impacted, our business, financial performance and reputation could be adversely affected.

SendTech Solutions operations rely on third party suppliers for services and components for our mailing equipment, spare parts, supplies and services and for the hosting of our SaaS offerings. Presort Services relies on third party suppliers to help equip our facilities, provide warehouse support and assist with logistical operations. In certain instances, we rely on single-sourced or limited-sourced suppliers around the world because of advantages in quality, price or lack of alternative sources. Like many other companies, we and our suppliers have experienced interruptions, delays and increased supply costs in the past, due to, among other things, volatility in the semiconductor industry, threats of strikes, rising inflation, tariffs and geopolitical instability. If we experience supply chain constraints in the future or these constraints were to worsen, or if other unknown events cause our suppliers to not be able to provide their services, components or equipment to us in a timely and cost-effective manner, and we were not able to find alternate suppliers, we could lose clients, incur significant disruptions in manufacturing and operations and increased costs.

Fluctuations in transportation costs or disruptions to transportation services in Presort Services could adversely affect client satisfaction or our financial performance.

In addition to our reliance on the USPS, Presort Services relies upon third party transportation service providers to transport a significant portion of our mail volumes. The use of these providers is subject to risks, including our ability to negotiate acceptable terms due to, increased competition during peak periods, capacity issues, increased fuel costs, labor shortages, performance problems, extreme weather, natural or man-made disasters, pandemics, or other unforeseen difficulties. Given our reliance upon these providers, any unforeseen disruptions affecting the availability of these services or any dramatic increase in the cost of these services (each of which we have experienced, at times), could adversely affect client satisfaction and our financial performance.

Our business depends on our ability to attract, retain, and engage with, employees at a reasonable cost to meet the needs of our business and to consistently deliver highly differentiated, competitive offerings.

During the second half of 2025, we approved a voluntary, early retirement initiative in the U.S. and a globally targeted, involuntary restructuring initiative (together, the “2025 Plan”). Such actions may cause us to experience a loss of continuity, experience and institutional knowledge, a reduction in productivity and efficiency, the unexpected loss of key employees and/or other retention issues during transitional periods. Such actions may also make it more difficult to attract and retain qualified employees.

There is also significant competition for the talent needed for research and development of new products and services and talent needed to sell and service our other products and services within all our business units.

At times, Presort Services has experienced increased demand and competition for labor, driving up costs. We supplement our workforce with contingent hourly workers from staffing agencies on an as-needed basis; however, if we experience labor shortages, and are unable to attract and utilize contingent workers, or if our staffing agencies terminate their relationship with us and we cannot find alternative providers, we could incur higher costs and our operations could be adversely affected. Moreover, given the nature of our Presort Services employee base, if we cannot continue to maintain good relationships, we could experience increased employee dissatisfaction and turnover, which could result in increased operating costs and reduced operational flexibility.

If we fail to comply with government contracting regulations, our financial performance, brand name and reputation could suffer.

We have a significant number of contracts with governmental entities. Government contracts are subject to extensive and complex procurement laws and regulations, along with regular audits and investigations by government agencies. If we were subjected to a claim of contractual noncompliance by a government agency and were found noncompliant, then we could be subject to various civil or criminal penalties and administrative sanctions, which could include the termination of the contract, reimbursement of payments received, fines and debarment from doing business with other government agencies. Any of these events could not only affect our financial performance, but also adversely affect our brand and reputation.

Difficulty in obtaining and protecting our intellectual property, and the risk of infringement claims by others may negatively impact our financial performance.

Our business success depends in part upon protecting our intellectual property rights, including proprietary technology developed (internally or by third party partners and subcontractors) or obtained through acquisitions. We rely on copyrights, patents, trademarks, trade secrets and other intellectual property laws to establish and protect our proprietary rights. If we are unable to protect our intellectual property rights, our competitive position may suffer, which could adversely affect our revenue and profitability. The continued evolution of patent law and the nature of our innovation work may affect the number of patents we are able to receive for our development efforts. As we continue to transition our business to more software and service-based offerings, patent protection of these innovations will be more difficult to obtain. As a result, we will rely more on copyrights and, when appropriate, trade secret protection for those software and service-based offerings. In addition, from time to time, third parties may claim that we, our clients, or our suppliers, have infringed their intellectual property rights. Although third parties also face the same difficulties in patenting software and service-based offerings, these claims, if successful, may require us to redesign affected products, enter into costly settlement or license agreements, pay damage awards, or face a temporary or permanent injunction prohibiting us from marketing or selling certain products.

8

Our capital investments to develop new products and offerings may not yield the anticipated benefits.

We make significant capital investments in new products and services to meet the evolving needs of our customers, improve and grow our business and remain competitive. If we are not successful in these new product or service introductions, or if our past capital investments do not yield the results anticipated when making the investments, there may be an adverse effect on our financial performance.

We are subject to risks relating to claims arising from the Ecommerce Restructuring and related transactions.

On August 8, 2024, we entered into a series of transactions designed to facilitate an orderly wind-down of a majority of our Global Ecommerce reporting segment, including the sale of 81% of the voting interests of DRF Logistics, LLC (“DRF Logistics”), which owned a majority of the Global Ecommerce segment’s net assets and operations (the “GEC Sale”). Following the GEC Sale, DRF Logistics and DRF LLC, a subsidiary of DRF Logistics (together, the “Ecommerce Debtors”), at the direction of their own governing bodies, filed voluntary petitions to commence Chapter 11 bankruptcy cases. We refer to the GEC Sale, the Chapter 11 cases and any associated transactions collectively as the “Ecommerce Restructuring.” On November 25, 2024, the Bankruptcy Court entered an order confirming the liquidation plan, and the timely and orderly wind-down of the Ecommerce Debtors is ongoing. Risks and uncertainties may continue to be associated with the Ecommerce Restructuring, including, among others, continuing claims asserted against the Company or its affiliates related to the Ecommerce Restructuring as described in Part I, Item 3, “Legal Proceedings.”

Changes within our senior management and our Board of Directors could create uncertainties and impact our business.

We have undergone recent changes in our senior management and in the composition of our Board of Directors. Leadership transitions may create continuity risks and operational challenges and could adversely affect our ability to execute our strategy. These changes also may create uncertainty among investors, customers, employees, and other stakeholders regarding our future direction and performance, and could make it more difficult to attract and retain qualified personnel. Our senior management team is focused on initiatives to strengthen our business and improve long-term value for our shareholders. If we fail to effectively implement any of these initiatives or to do so on a timely basis, our business, results of operations, financial condition and cash flows could be adversely affected.

Cybersecurity and Technology Risks

Our financial performance and our reputation could be adversely affected, and we could be subject to legal liability or regulatory enforcement actions, if we or our suppliers are unable to protect against, or effectively respond to, cyberattacks or other cybersecurity incidents.

We depend on the security and integrity of our information technology systems and those of certain third-party service providers and suppliers to support numerous business processes and activities, to service our clients, and to enable consumer transactions and postal services. There are numerous cybersecurity risks to these systems, including, but not limited to, individual and group criminal hackers, industrial espionage, denial of service attacks, ransomware and malware attacks, attacks on the software supply chain, and employee errors and/or malfeasance, phishing and other social engineering attacks, credential theft, insider threats and exploitation of vulnerabilities in third-party software and systems. These cyber threats are diverse and constantly evolving, especially given the advances in, and the rise of the use of, artificial intelligence, thereby increasing the difficulty of preventing, detecting, and successfully defending against themand may be more difficult to detect and mitigate, including as threat actors use artificial intelligence and other advanced tools to enhance attacks and impersonation tactics. Successful cybersecurity breaches could, among other things, disrupt our operations or degrade service delivery or result in the unauthorized disclosure, theft and misuse of company, client, consumer and employee sensitive and confidential information, all of which could adversely affect our financial performance. Cybersecurity breaches could result in legal claims or proceedings, financial liability to other parties, governmental investigations, regulatory enforcement actions and penalties, and damage to our brand and reputation. Although we maintain insurance coverage relating to cybersecurity incidents, we may incur costs or financial losses that are either not insured against or not fully covered through our insurance and such insurance may be subject to exclusions, sub-limits and retentions and may become more expensive or less available on acceptable terms. We and certain of our suppliers have experienced cybersecurity incidents in the past, and may experience additional incidents in the future. Despite the implementation of our cybersecurity processes, our security measures cannot guarantee that a significant cyberattack will not occur or that we will be able to prevent, detect or respond to all incidents in a timely and effective manner. Our goal is to prevent meaningful incursions and minimize the overall impact of those that occur. For more information on how the Company handles cybersecurity, see Item 1C. Cybersecurity.

Failure to comply with data privacy and protection laws and regulations could subject us to legal liability and adversely affect our reputation and our financial performance.

Our businesses use, process, and store proprietary information and personal, sensitive, or confidential data relating to our business, clients, and employees. Privacy laws and similar regulations in many jurisdictions where we do business require that we take significant steps to safeguard that information, and these laws and regulations continue to evolve. The scope of the laws that may be applicable to us is often uncertain and may be conflicting, and the growth of our cloud-based services increases the scope and

9

complexity of laws that might apply. In addition, new laws may add an array of requirements on how we handle or use information and increase our compliance obligations. For example,India's Digital Personal Data Protection Act of 2023, and implemented rules notified in 2025, established a framework regulating the processing of digital personal data. The European Union’s Artificial Intelligence Act, which entered into force in August 2024, introduces additional requirements for certain AI systems and practices and will apply on a phased timeline, and may increase compliance obligations for organizations that develop, deploy or use AI-enabled tools. In the United States, a growing number of states have enacted different laws regarding personal information, privacy and artificial intelligence that impose significant new requirements on consumer personal information. In some instances (e.g., California), these laws also expand the definition of consumer personal information to include information related to employees and business contacts. Some of these state laws have established independent agencies with rule making and enforcement authority, whose initial guidance, actions, and regulations continue to evolve and may be adopted or become effective on a phased basis. Other countries or states have enacted and will continue to enact and amend laws or regulations in the future that have similar or additional requirements. Although we endeavor to continually monitor and assess the impact of these laws and regulations, and continually update our systems to protect our data and comply with these laws, their interpretation and enforcement are uncertain, subject to change, and may require substantial costs to monitor and implement. Failure to comply with data privacy and protection laws and regulations could also result in government enforcement actions (which could result in substantial civil and/or criminal penalties) and private litigation, which could adversely affect our reputation and financial performance.

If we or our third party service providers and suppliers encounter interruptions or difficulties in the operation of our cloud-based applications, our business could be disrupted, our reputation and relationships may be harmed, and our financial performance could be adversely affected.

Our business relies upon the continuous and uninterrupted performance of our cloud-based applications and systems and those of certain third-party service providers and suppliers to support numerous business processes, to service our clients and to support their transactions with their customers and postal services. Our applications and systems, and those of our third-party service providers and suppliers, may be subject to interruptions due to technological errors, system capacity constraints, software errors or defects, human errors, computer or communications failures, power loss, adverse acts of nature and other unexpected events. We have business continuity and disaster recovery plans in place designed to reduce the impact on our business operations in case of such events and we also require our suppliers to have the same .and, where appropriate, contractually obligate certain third-party service providers and suppliers to maintain similar plans. Nonetheless, there can be no guarantee that these plans will function as designed or will be sufficient to address all contingencies. If we are unable to limit interruptions or successfully correct them in a timely manner or at all, such interruptions could result in lost revenue, loss of critical data, significant expenditures of capital, a delay or loss in market acceptance of our services and damage to our reputation, brand and relationships, any of which could have an adverse effect on our business and our financial performance.

Macroeconomic and General Regulatory Risks

Periods of difficult economic conditions, other macroeconomic events, or a public health crisis could adversely affect our business.

Our operations and financial performance are impacted by economic conditions in the United States and the other countries where we and our clients do business. Any significant or perceived weakening of these economies, reduction in business confidence, change in business or consumer spending habits, concerns of a domestic or global recession, rising inflation or interest rates, limited availability of credit, or other macroeconomic events (including public health crises, severe weather events, government shutdowns or other disruptions in government operations), not within our control, may impact our clients’ businesses or reduce our clients’ demand for shipping and mailing products and services and thus, negatively affect our financial performance. These economic conditions, at times, have arisen and can arise suddenly, and the duration and full impact of such conditions can be difficult to predict, which could adversely impact our business, financial condition, and results of operations.

A significant decline in cash flows, changes in our credit ratings, capital market disruptions, noncompliance with any of our debt covenants, or significant withdrawals by depositors at the Bank, could adversely affect our ability to maintain adequate liquidity, provide competitive financing services and to fund various discretionary priorities.

We provide competitive finance offerings and fund discretionary priorities, such as capital investments, strategic acquisitions, dividend payments and share repurchases through a combination of cash generated from operations, and access to capital markets. Our ability to access U.S. capital markets and the associated cost of borrowing is dependent upon our credit ratings and is subject to capital market volatility. We maintain a revolving credit facility to provide funding as needed, however, our ability to borrow under this facility is subject to compliance with the covenants set forth in the credit agreement governing the revolving credit facility.

A significant decline in cash flows, or changes in our credit ratings, material capital market disruptions or noncompliance with any of our debt covenants that adversely affects our ability to access capital markets, could impact our ability to maintain adequate liquidity, continue to provide competitive finance offerings, repay or refinance maturing debt, and fund other strategic or discretionary activities, and adversely affect our operational and financial performance.

10

Changes in tax rates, laws or regulations could adversely impact our financial results.

We are subject to taxes in the U.S. and in the foreign jurisdictions where we do business. Due to continuing global fiscal challenges and political conditions, tax laws and enforcement approaches have been and may continue to be subject to significant change. Changes in tax laws may be on a prospective or retroactive basis and could have a material impact on our tax expense and cash flows. The Organization for Economic Co-operation and Development (OECD) has set forth a Two-Pillar Solution fundamentally overhauling the international tax rules. Pillar One focuses on reallocation of profits while Pillar Two applies a global minimum corporate tax. The OECD has issued Model Rules and ongoing administrative guidance to support implementation and coordination of these initiatives, and a number of jurisdictions have enacted or are implementing rules based on the OECD framework, including the Pillar Two global minimum tax. Although some jurisdictions have issued guidance or passed tax laws based on the OECD Model Rules, the final nature, timing and extent of any such tax reforms or other legislative or regulatory actions (including their scope, interpretation, implementation, enforcement and interaction with other jurisdictions’ rules) are evolving and it is difficult to assess their overall effect. These developments could increase our compliance and reporting obligations and, depending on the jurisdictions in which we operate and the interaction among applicable rules, could result in incremental tax expense (including “top-up” taxes), potential double taxation and adversely impact our financial results and cash flows. We continuously monitor developments and evaluate the impact these new rules are anticipated to have on our tax rate.

We are subject to tax audits in the various jurisdictions in which we operate. Given the complexity of the current and changing tax laws and regulations, tax authorities may disagree with certain positions we have taken and assess additional taxes. We regularly review the strength of our positions based on current law, court cases, rulings and proposed legislative changes to determine the appropriateness of our tax provision, however, there can be no assurance that we will accurately predict the outcomes of these audits, which could have a material impact on our effective tax rate and adversely impact our financial results and cash flows.

Our operations and financial performance may be negatively affected by changes in trade policies, tariffs and regulations.

In recent years, the United States increased tariffs for certain goods, which triggered other nations to also increase tariffs on certain of their goods. These increased tariffs resulted in additional costs on certain components used in SendTech products. In addition, there continues to be significant uncertainty about the future relationship between the United States and various other countries with respect to trade policies, treaties, tariffs, taxes, and other limitations on cross-border operations. Changes in tariffs, trade barriers, price and exchange controls and other regulatory requirements could have an adverse effect on our business, prospects, financial condition and operating results, the extent of which cannot be predicted with certainty at this time.

Our business could be negatively affected as a result of shareholder activism.

We value constructive input from investors and regularly engage with our stockholders regarding strategy and performance. Our Board of Directors and management team are committed to acting in the best interests of all our stockholders; however, there is no assurance that the results of actions taken by our Board of Directors and management team will be successful.

We have been and may continue to be subject to shareholder activism in the future.Such activism or perceived uncertainties as to our future direction could adversely affect our results of operations and financial condition, as well as the market performance of our securities, including fluctuations in our stock price based on temporary or speculative market perceptions or other factors that do not necessarily reflect the underlying fundamentals and prospects of our business.

We also face evolving and diverging requirements and expectations from investors, regulators, customers and other stakeholders across the jurisdictions in which we operate, including on environmental, social, governance and sustainability matters. Any actual or perceived failure to meet any expectations of our key stakeholders, including any regulatory requirements or expectations, could expose us to legal, operational and reputational risks, which could negatively impact our business.

Our indebtedness and the terms of our debt agreements could limit our financial and operating flexibility and adversely affect our

Business.

As of December 31, 2025, we had total debt of approximately $2 billion. Our debt service obligations could require us to dedicate a portion of our cash flows from operations to interest and principal payments. This could reduce the funds available to support operations, capital expenditures, and strategic initiatives and could increase our vulnerability to adverse business, industry, or economic conditions.

In addition, the agreements governing our indebtedness contain financial covenants and other restrictions that may limit our ability to take actions that could be in our best interests, including limitations on incurring additional indebtedness, granting liens, making certain investments, selling assets, entering into certain strategic transactions, or making certain restricted payments. For example, under our senior secured credit agreement, we are required to satisfy quarterly tested maintenance covenants, including a minimum interest coverage ratio and maximum secured net leverage and total net leverage ratios. Our ability to comply with these covenants and restrictions may be affected by events beyond our control. If we fail to comply, we may be required to seek waivers or amendments, which may not be available on acceptable terms, and a default could result in acceleration of amounts due and other remedies (including pursuant to any cross-default or cross-acceleration provisions).

We may need to refinance, redeem, or repay indebtedness as it matures (or in certain circumstances earlier than scheduled), and we

11

cannot guarantee that we will be able to do so on acceptable terms, or at all. In particular, our senior secured credit agreement contains provisions pursuant to which, if the notes due March 2027 have not been redeemed in full by specified dates and liquidity falls below

specified levels, certain of our term loans and any borrowings under our revolving credit facility could become due earlier than their

stated maturities. Further, a portion of our indebtedness bears interest at variable rates and increases in interest rates could increase our borrowing costs and adversely affect our cash flows.

The conditional conversion feature of the Convertible Notes, if triggered, may adversely affect our financial condition and operating results.

In the event the conditional conversion feature of the Convertible Notes is triggered, holders of Convertible Notes will be entitled to convert the Convertible Notes at any time during specified periods at their option. If one or more holders elect to convert their Convertible Notes, the conversion would be settled through the payment of cash, which could adversely affect our liquidity. In addition, even if holders do not elect to convert their Convertible Notes, we could be required to reclassify all or a portion of the outstanding principal of the Convertible Notes as a current rather than long-term liability, which could result in a reduction of our net working capital.

Certain provisions in the Indenture governing the Convertible Notes could delay or prevent an otherwise beneficial takeover or takeover attempt of us.

Certain provisions in the Convertible Notes and the Indenture could make it more difficult or expensive for a third party to acquire us. For example, if an attempted acquisition constitutes a fundamental change, holders of the Convertible Notes will have the right to require us to repurchase their Convertible Notes in cash. In addition, if an attempted acquisition constitutes a make-whole fundamental change, we may be required to increase the conversion rate for holders who convert their Convertible Notes. In either case, our obligations under the Convertible Notes and the Indenture could increase the cost of acquiring us or otherwise discourage a third party from acquiring us, including in a transaction that holders of the Convertible Notes or holders of our common stock may view as favorable.

The Capped Call Transactions may affect the value of the Convertible Notes and the market price of our common stock.

In connection with the pricing of the Convertible Notes, we entered into privately negotiated Capped Call Transactions with the option counterparties. The Capped Call Transactions are expected to reduce potential dilution to our common stock upon conversion of any Convertible Notes, with such reduction subject to a cap. If the market price per share of our common stock, as measured under the terms of the Capped Call Transactions, exceeds the cap price of the Capped Call Transactions, there would nevertheless be dilution to the extent that such market price exceeds the cap price of the Capped Call Transactions. In addition, to the extent any observation period for any Convertible Notes does not correspond to the period during which the market price of our common stock is measured under the terms of the Capped Call Transactions, there could also be dilution and/or a reduced offset of any such cash payments as a result of the different measurement periods.

The option counterparties or their respective affiliates may modify their hedge positions by entering into or unwinding various derivatives with respect to our common stock and/or purchasing or selling our common stock or other securities of ours in secondary market transactions following the pricing of the Convertible Notes and prior to the maturity of the Convertible Notes (and may do so on each exercise date for the Capped Call Transactions or following any termination of any portion of the Capped Call Transactions in connection with any repurchase, redemption or early conversion of the Convertible Notes). This activity could also cause an increase or a decrease in the market price of our common stock or the Convertible Notes, which could affect holders’ ability to convert the Convertible Notes and, to the extent the activity occurs following conversion or during any observation period related to a conversion of Convertible Notes, it could affect the amount and value of the consideration that holders will receive upon conversion of such Convertible Notes.

We are subject to counterparty risk with respect to the Capped Call Transactions.

The option counterparties are financial institutions, and we are subject to the risk that any or all of them might default under the Capped Call Transactions. Our exposure to the credit risk of the option counterparties will not be secured by any collateral. Global economic conditions from time to time have resulted in the actual or perceived failure or financial difficulties of many financial institutions. If an option counterparty were to default under the Capped Call Transactions, we would become an unsecured creditor with a claim equal to our exposure at that time under the Capped Call Transactions with such option counterparty. Our exposure will depend on many factors but, generally, an increase in our exposure will be correlated to an increase in the market price and in the volatility of our common stock. In addition, upon a default by an option counterparty, we may suffer adverse tax consequences and more dilution than we currently anticipate with respect to our common stock. We can provide no assurance as to the financial stability or viability of the option counterparties.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

12

ITEM 1C. CYBERSECURITY

A comprehensive cybersecurity program is critical to achieving our business goals. Like all companies in today’s world, we face a multitude of cybersecurity threats that range from ransomware, and denial-of-service, to attacks from more advanced nation state actors, and even insider threats. Likewise, our customers, suppliers, subcontractors and partners face similar cybersecurity threats, and a cybersecurity incident impacting us or any of these entities could materially adversely affect our business operations and financial performance. These cybersecurity threats and related risks make it imperative that we expend considerable resources to safeguard our organization’s assets and to prevent service disruptions or minimize the impact should an incident occur. Our processes for assessing, identifying, and managing material risks from cybersecurity threats are described below.

The Audit Committee of the Board of Directors oversees the Company's cybersecurity risk management program, including management’s processes for identifying and mitigating risks, including cybersecurity risks, to help align our risk exposure with our strategic objectives.Senior technology leadership, including our Senior Vice President of IT and Security, briefs the Audit Committee and the full Board of Directors on our cybersecurity and information security posture on a regular cadence. In addition to this regular reporting, cybersecurity risks or threats may also be escalated to the Audit Committee on an as-needed basis. In the event of an incident, we strive to follow our detailed incident response playbook, which outlines the steps to be taken from incident detection to mitigation, recovery, escalation to senior management, the Board of Directors, and functional areas, and notification to customers and employees as appropriate.

Our information security organization is led by the Senior Vice President of IT and Security, who is responsible for our overall information security strategy, policy, security engineering, product security, operations and cybersecurity threat detection and response.The Senior Vice President of IT and Security has more than 33 years of experience serving in various information technology roles. The information security organization manages and continually enhances an enterprise security structure with the goal of preventing cybersecurity incidents to the extent feasible, while simultaneously increasing our system and product resilience in an effort to minimize the business impact should an incident occur. Our cybersecurity program attempts to follow the National Institute of Standards and Technology (NIST) Cybersecurity Framework principles. We also seek to maintain certain ISO certification and obtain AICPA SOC2 reports for certain of our systems and products. We have adopted a risk-based management process to define, manage, and prioritize controls required to maintain the confidentiality, integrity and availability of our digital assets. Employees outside of our information security organization also have a role in our cybersecurity defenses and are required to receive periodic cybersecurity training, which we believe improves our overall cybersecurity posture.

We have also extended our cybersecurity governance to our operational business executives. Technical leadership periodically presents an assessment of mission critical information assets, those that would cause significant business, customer, or employee impact to the appropriate senior management executives. This is a formal assessment which describes the underlying cyber posture, mitigation plan, and commitments. It ensures that the cybersecurity program in the business unit is progressing against its goals and new risks are operationally prioritized. In addition, the Senior Vice President of IT and Security meets with leaders from the Company's legal, IT, and internal audit organizations to ensure alignment with privacy, regulations, legal compliance and audit plans.

We rely heavily on third party partners (i.e. suppliers, subcontractors, consultants, etc.) to support our products, business operations and technology services, and a cybersecurity incident at a partner could materially adversely impact us. Where possible, we include information security provisions, audit rights and insurance requirements, in contracts with these partners based on their level of access to our systems and data. For our most critical partners, where possible, we attempt to pursue an annual attestation of ongoing compliance to our standard policies and practices. For select partners, we engage third party cybersecurity monitoring and alerting services, and seek to work directly with those partners to address potential deficiencies identified.

Given the constantly evolving cyber-threat landscape, we continuously test and evolve our cybersecurity program. We engage internal security team experts who perform ‘ethical hacking’ against our information assets to uncover risks. As part of its risk based annual audit plan, our internal audit team reviews a number of components of our information technology operations, which taken together, comprise our cybersecurity defenses. A report of its findings is distributed to certain members of management and completion of the auditor's comments is tracked and reported up to the Audit Committee. We also engage third party service providers to conduct evaluations of our security controls, whether through penetration testing, independent audits or consulting on best practices to address new challenges. These evaluations include testing both the design and operational effectiveness of security controls.

Assessing, identifying, and managing cybersecurity related risks are integrated into our overall enterprise risk management (ERM) process. Cybersecurity related risks are included in the risk universe that our ERM process evaluates to assess top risks to the enterprise on an annual basis. To the extent the ERM process identifies a heightened cybersecurity related risk, risk owners are assigned to develop risk mitigation plans, which are then tracked to completion. The ERM process annual risk assessment is presented to the Audit Committee.

As of the date of this report, we have not identified any cybersecurity threats or incidents that have materially affected or are reasonably likely to materially affect the Company. We and certain of our service providers have experienced cyberattacks and attempted cyberattacks in the past, which we believe have thus far been mitigated by preventative, detective, and responsive measures put in place. Notwithstanding the cybersecurity protections we have in place, we may not be successful in preventing or mitigating a cybersecurity incident that could have a material adverse effect on us. See Item 1A. “Risk Factors” for a discussion of cybersecurity risks.

13

ITEM 2. PROPERTIES

We lease numerous facilities worldwide, including administrative offices, mail sortation facilities, service locations, data centers and call centers. We conduct our research and development activities in facilities located in Noida and Pune, India and Shelton, Connecticut. Effective January 1, 2026, we relocated our corporate headquarters to Shelton, Connecticut.

Presort Services conducts mail sortation operations through a network of 34 operating centers throughout the United States. SendTech Solutions leases a manufacturing and distribution facility in Indiana. This facility is significant as it stores a majority of the SendTech Solutions products, supplies and inventories.

Should any facility be unable to function as intended for an extended period of time, our ability to service our clients and operating results could be impacted. Management believes that our facilities are in good operating condition, materially utilized and adequate for our current business needs.

ITEM 3. LEGAL PROCEEDINGS

See Note 16 Commitments and Contingencies to the Consolidated Financial Statements for additional information.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

14

PART II

ITEM 5. MARKET FOR THE COMPANY'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our common stock is principally traded on the New York Stock Exchange (NYSE) under the symbol "PBI". At January 31, 2026, we had 10,580 common stockholders of record.

Dividends and Share Repurchases

During 2025, we paid quarterly dividends totaling $51 million, or $0.30 per share. We expect to continue to pay a quarterly dividend; however, the Board of Directors may decide to increase, decrease or not approve the payment of a dividend at any time.

Throughout 2025, the Board of Directors authorized a new $500 million share repurchase program. On February 16, 2026, the Board of Directors authorized an increase to the share repurchase program of $250 million. Subject to limitations in our New Credit Agreement (as defined below), common stock repurchases may be made from time to time in open market or private transactions in such manner as may be deemed advisable from time to time (including, without limitation, pursuant to one or more 10b5-1 trading plans, accelerated share repurchase programs, and any other method that the Company may deem advisable) and may be discontinued at any time. The following table provides information about common stock purchases during the three months ended December 31, 2025:

Total number of shares purchased

Average price paid per share

Total number of shares purchased as part of publicly announced plans or programs

Approximate dollar value of shares that may yet be purchased under the plans or programs (in thousands)

Beginning balance

$148,226

October 2025

3,203,100

$

11.30

3,203,100

$212,031

November 2025

7,926,090

$

9.52

7,926,090

$136,553

December 2025

1,484,407

$

10.05

1,484,407

$121,639

12,613,597

$

10.04

12,613,597

During 2025, we purchased 35,853,442 shares at an aggregate cost of $378 million. From January 1, 2026 through February 13, 2026 we purchased an aggregate additional 1,204,679 shares at a cost of $12 million.

15

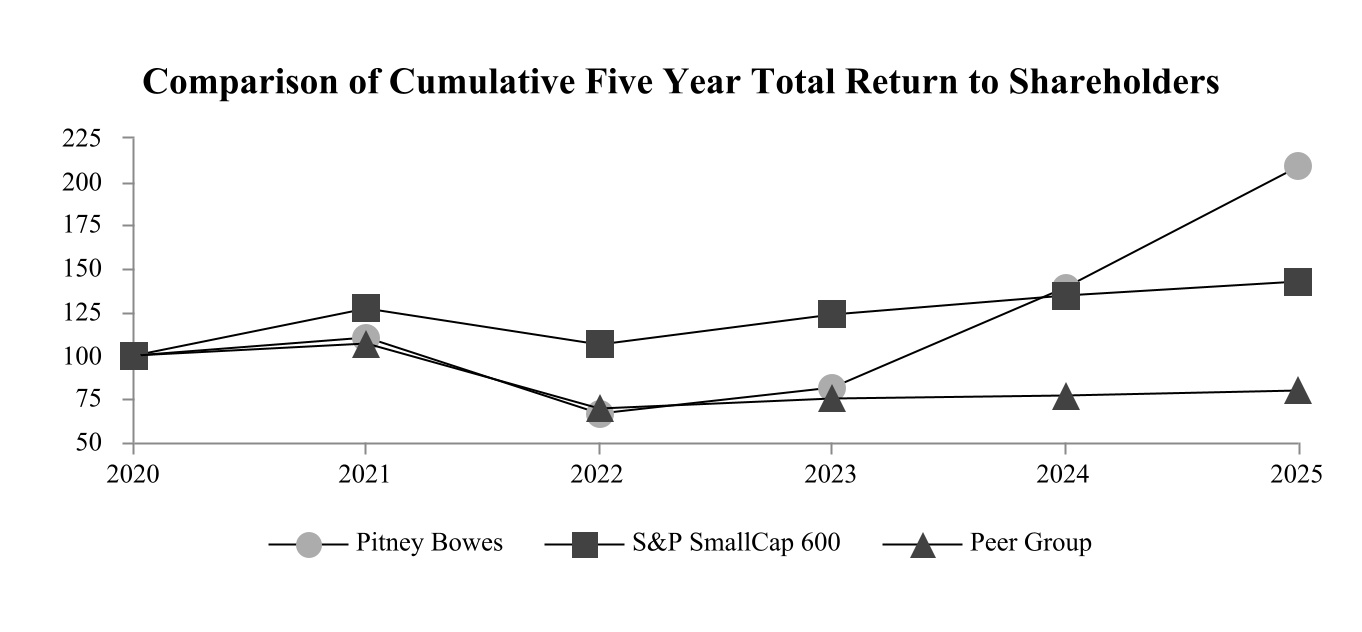

Stock Performance Graph

Our peer group is comprised of: ACCO Brands Corporation, Bread Financial Holdings, Inc., Cimpress plc, CSG Systems International, Inc., Deluxe Corporation, Diebold Nixdorf, Incorporated, E2open Parent Holdings, Inc., HNI Corporation, Matthews International Corporation, McGrath RentCorp, Quad/Graphics, Inc., Sabre Corporation, TTEC Holdings, Inc. and Unisys Corporation.

The accompanying graph shows the annual change in the value of a $100 investment in Pitney Bowes Inc., the Standard and Poor's (S&P) SmallCap 600 Composite Index and a peer group over a five-year period assuming the reinvestment of dividends. The composition of our peer group is developed by our Compensation Committee based on recommendations from their independent compensation consultant.

The above graph was determined by an independent third party. On a total return basis, a $100 investment on December 31, 2020, in Pitney Bowes Inc., the S&P SmallCap 600 Composite Index and our peer group would have been worth $209, $142 and $80, respectively, on December 31, 2025.

Total return for the S&P SmallCap 600 Composite Index and our peer group is based on market capitalization, weighted for each year. The stock price performance is not necessarily indicative of future stock price performance.

ITEM 6. [RESERVED]

16

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS

The following discussion of our financial condition and operating results should be read in conjunction with our risk factors, consolidated financial statements and related notes. This discussion includes forward-looking statements based on management's current expectations, estimates and projections and involves risks and uncertainties. Actual results may differ significantly from those currently expressed. A detailed discussion of risks and uncertainties that could cause actual results to differ materially from such forward-looking statements is outlined under "Forward-Looking Statements" and "Item 1A. Risk Factors" in this Form 10-K. All table amounts are presented in thousands of dollars.

RESULTS OF OPERATIONS

Years Ended December 31,

Favorable/(Unfavorable)

2025

2024

Actual % Change

Total revenue

$

1,892,629

$

2,026,598

(7)

%

Total cost of revenue

868,767

964,298

10

%

Selling, general and administrative

621,567

717,894

13

%

Research and development

15,278

31,957

52

%

Restructuring charges

58,660

76,915

24

%

Interest expense, net

101,460

110,094

8

%

Other components of net pension and postretirement cost

7,543

89,044

92

%

Other expense

26,830

88,723

70

%

Income (loss) from continuing operations before income taxes

192,524

(52,327)

>100%

Provision (benefit) for income taxes

47,827

(154,829)

>(100%)

Income from continuing operations

144,697

102,502

41

%

Loss from discontinued operations, net of tax

—

(306,099)

100

%

Net income (loss)

$

144,697

$

(203,597)

>100%

Years Ended December 31,

Favorable/(Unfavorable)

2024

2023

Actual % Change

Total revenue

$

2,026,598

$

2,078,925

(3)

%

Total cost of revenue

964,298

1,048,315

8

%

Selling, general and administrative

717,894

781,609

8

%

Research and development

31,957

29,486

(8)

%

Restructuring charges

76,915

52,412

(47)

%

Goodwill impairment

—

123,574

100

%

Interest expense, net

110,094

98,769

(11)

%

Other components of net pension and postretirement cost

89,044

(8,256)

>(100%)

Other expense (income)

88,723

(3,064)

>(100%)

Loss from continuing operations before income taxes

(52,327)

(43,920)

(19)

%

(Benefit) provision for income taxes

(154,829)

17,347

>100%

Income (loss) from continuing operations

102,502

(61,267)

>100%

Loss from discontinued operations, net of tax

(306,099)

(324,360)

6

%

Net loss

$

(203,597)

$

(385,627)

47

%

Refer to Segment Results and Consolidated Expenses sections for detailed information.

17

CHANGES IN REPORTING

We recast our reporting presentation of revenue and cost of revenue to better align with our offerings. We now report Services revenue and Cost of services, which includes the previously reported Business services and Support services, Products revenue and Cost of products, which includes the previously reported Equipment sales and Supplies, and Financing and other revenue and Cost of financing and other, which includes the previously reported Financing and Rentals.

We recast our corporate expense allocation methodology to allocate all marketing and innovation expenses to our SendTech Solutions segment due to a change in how these functions are now managed.

We recast our segment reporting to report the revenue and related expenses of a cross-border services contract in our SendTech Solutions reporting segment, which was previously reported in Other operations.

Prior periods presented in this Form 10-K have been recast to conform to the current period presentation.

SEGMENT RESULTS

We operate in two segments: SendTech Solutions and Presort Services. Management measures segment profitability and performance as segment revenues less the related costs and expenses attributable to the segment. Segment results exclude interest, taxes, corporate expenses, restructuring charges and other items not allocated to the segments.

In the Consolidated Statements of Operations, we allocate a portion of total interest expense to finance interest expense, included in Cost of financing and other. For segment reporting, we exclude the allocated finance interest expense from the determination of adjusted segment EBIT.

SendTech Solutions

SendTech Solutions provides clients with physical and digital shipping and mailing technology solutions and other applications to help simplify and save on the sending, tracking and receiving of letters, parcels and flats, as well as supplies and maintenance services for these offerings. We offer financing alternatives that enable clients to finance Company and other manufacturers' equipment and product purchases, a revolving credit solution that allows clients to make meter rental payments and purchase postage, services and supplies, an interest-bearing deposit solution to clients that prefer to prepay postage and meet working capital needs.

Financial performance for the SendTech Solutions segment was as follows:

Years Ended December 31,

Favorable/(Unfavorable)

2025

2024

% change

Services

$

569,403

$

588,046

(3)

%

Products

364,709

430,845

(15)

%

Financing and other

321,889

335,141

(4)

%

Total revenue

1,256,001

1,354,032

(7)

%

Cost of services

196,143

218,108

10

%

Cost of products

212,366

244,203

13

%

Cost of financing and other

13,807

17,461

21

%

Total costs of revenue

422,316

479,772

12

%

Gross margin

833,685

874,260

(5)

%

Gross margin %

66.4

%

64.6

%

Selling, general and administrative

398,230

461,737

14

%

Research and development

15,968

29,883

47

%

Other components of pension and post retirement costs

7,298

(2,111)

>(100%)

Adjusted Segment EBIT

$

412,189

$

384,751

7

%

SendTech Solutions revenue decreased $98 million in 2025 compared to 2024. Products revenue declined $66 million primarily due to customers opting to extend leases of their existing advanced-technology equipment rather than purchase new equipment, the impact of

18