.2

2026 First Quarter Results & Outlook April 28 , 2026

2 Enter “so what” if necessary – Century Gothic, Bold, Size 18 or smaller This presentation is made as of the date hereof and contains “forward - looking statements” as defined in Rule 3b - 6 of the Securit ies Exchange Act of 1934, Rule 175 of the Securities Act of 1933, and relevant legal decisions. The forward - looking statements are subject to risks and uncertainties. All forward - lo oking statements should be considered in the context of the risk and other factors detailed from time to time in CMS Energy’s and Consumers Energy’s Securities and Exchange Commissi on filings. Forward - looking statements should be read in conjunction with “FORWARD - LOOKING STATEMENTS AND INFORMATION” and “RISK FACTORS” sections of CMS Energy’s and Consumers Energy’s most recent Form 10 - K and as updated in reports CMS Energy and Consumers Energy file with the Securities and Exchange Commission. CMS Energy’s and Cons ume rs Energy’s “FORWARD - LOOKING STATEMENTS AND INFORMATION” and “RISK FACTORS” sections are incorporated herein by reference and discuss important factors th at could cause CMS Energy’s and Consumers Energy’s results to differ materially from those anticipated in such statements. CMS Energy and Consumers Energy undertake no ob ligation to update any of the information presented herein to reflect facts, events or circumstances after the date hereof. The presentation also includes non - GAAP measures when describing CMS Energy’s results of operations and financial performance. A reconciliation of each of these measures to the most directly comparable GAAP measure is included in the appendix and posted on our website at www.cmsenergy.com . Investors and others should note that CMS Energy routinely posts important information on its website and considers the Inves tor Relations section, www.cmsenergy.com/investor - relations , a channel of distribution. Presentation endnotes are included after the appendix. 2

3 Investment Thesis . . . . . . o ver two decades of industry - leading financial performance. Strong Cash Flow & Balance Sheet Attractive & Diversified Growth Long Capital Runway Top - Tier Regulatory Jurisdiction Affordability driven by the CE Way + Digital Long Capital Runway Top - Tier Regulatory Jurisdiction a Clean Energy Leader Presentation endnotes are included at the end of the presentation.

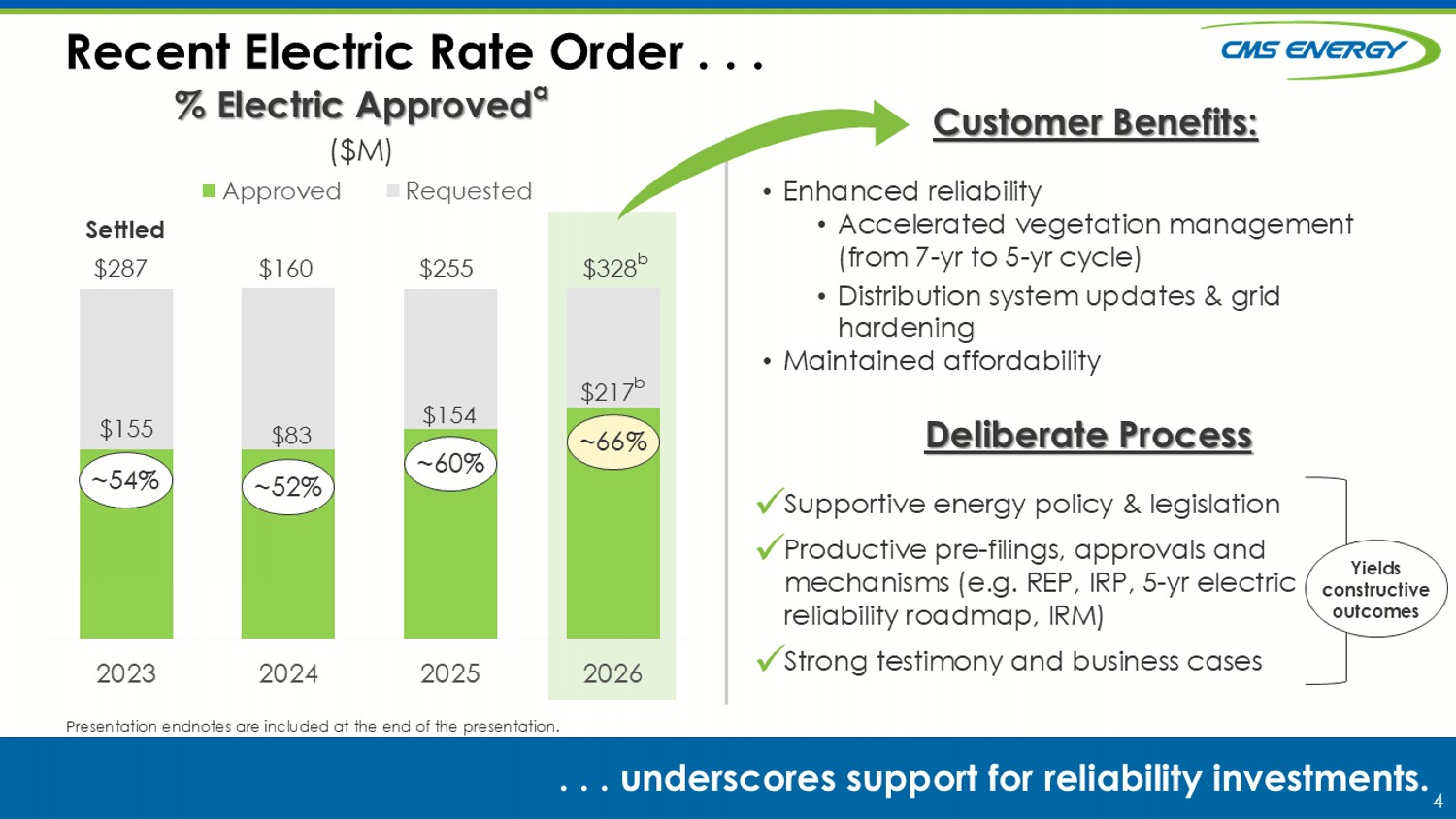

4 v Recent Electric Rate Order . . . . . . u nderscores support for reliability investments. Presentation endnotes are included at the end of the presentation. 2023 2024 2025 2026 Approved Requested ~52% ~54% ~60% ~ 66 % % Electric Approved a ($M) $287 $155 $160 $83 $255 $154 $328 b $217 b Customer Benefits: • Enhanced reliability • Accelerated vegetation management (from 7 - yr to 5 - yr cycle ) • Distribution system updates & grid hardening • Maintained affordability Deliberate Process S upportive energy policy & l egislation Productive pre - filings, approvals and mechanisms (e.g. REP, IRP, 5 - yr electric reliability roadmap, IRM) Strong testimony and business cases x x x Yields constructive outcomes Settled

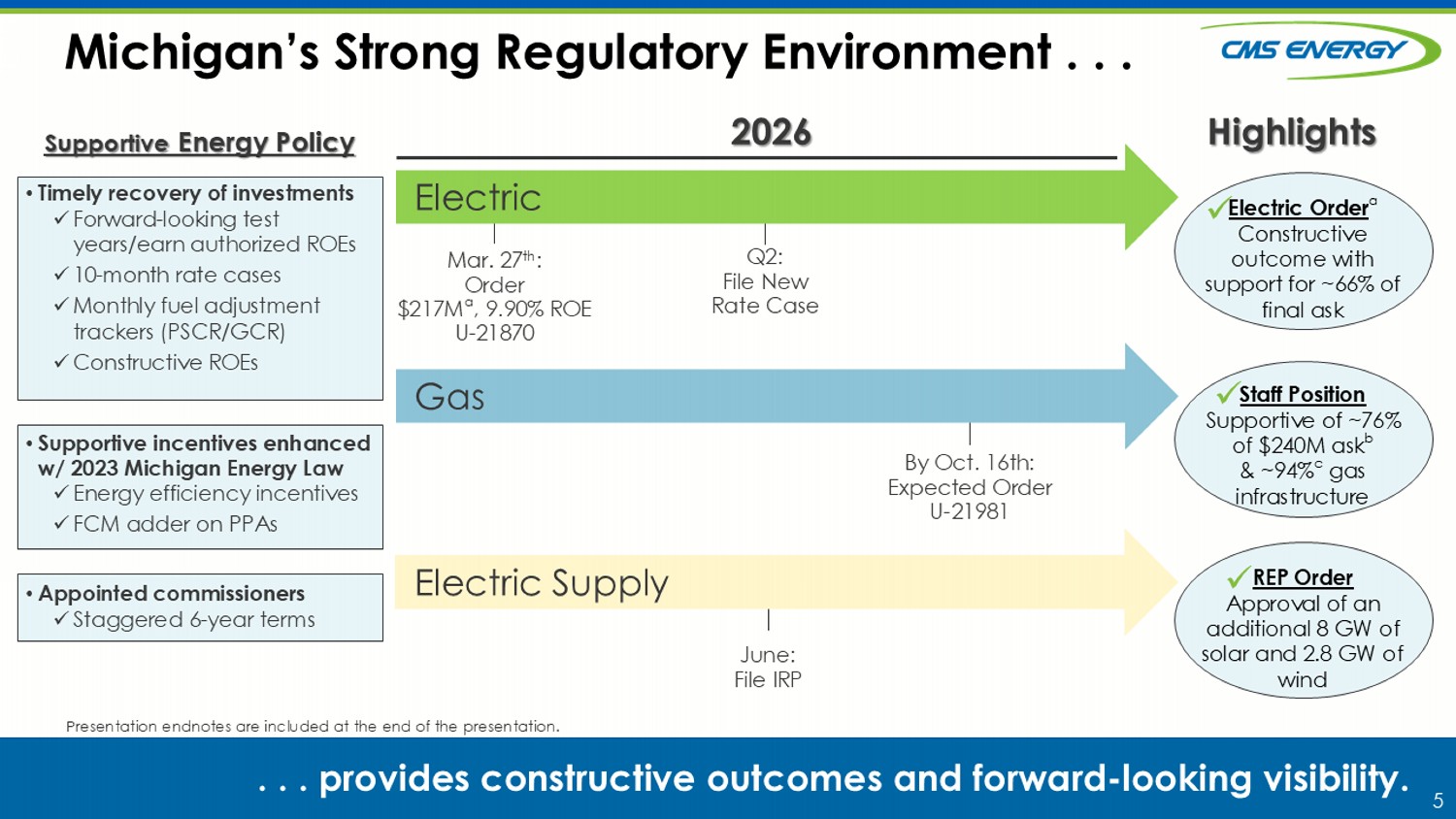

5 Q2: File New Rate Case By Oct. 16th: Expected Order U - 21981 Michigan’s Strong Regulatory Environment . . . . . . provides constructive outcomes and forward - looking visibility. Electric Gas Supportive Energy Policy • Timely recovery of investments x Forward - looking test years/earn authorized ROEs x 10 - month rate cases x Monthly fuel adjustment trackers (PSCR/GCR) x Constructive ROEs • Supportive incentives enhanced w/ 2023 Michigan Energy Law x Energy efficiency incentives x FCM adder on PPAs • Appointed commissioners x Staggered 6 - year terms Electric Supply 2026 June : File IRP Presentation endnotes are included at the end of the presentation. Mar. 27 th : Order $217M a , 9.90 % ROE U - 21870 Highlights Electric Order a Constructive outcome with support for ~ 66 % of final ask x Staff Position Supportive of ~76% of $240M ask b & ~94% c gas infrastructure x REP Order Approval of an additional 8 GW of solar and 2.8 GW of wind x

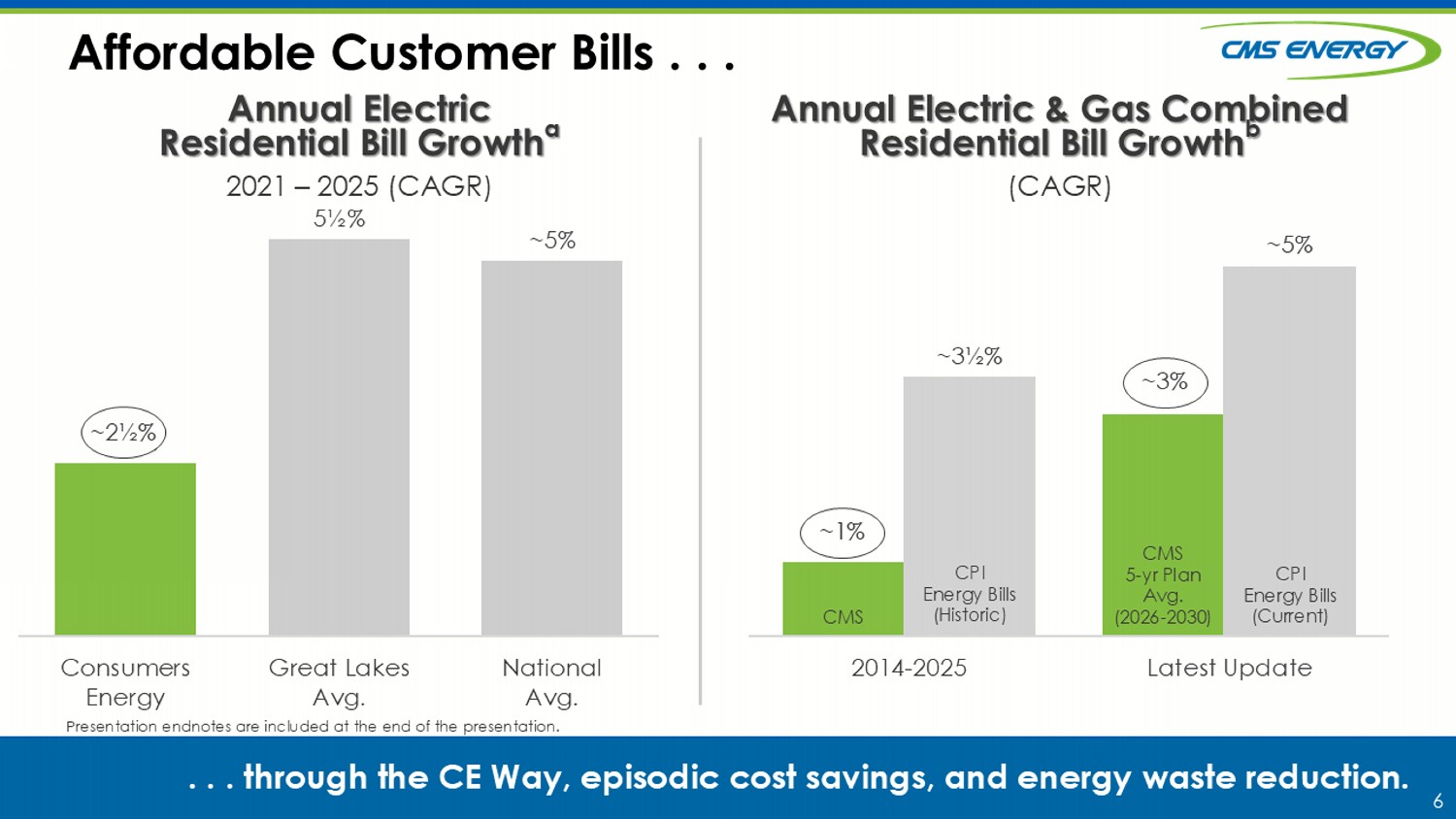

6 Affordable Customer Bills . . . . . . through the CE Way, episodic cost savings, and energy waste reduction. Presentation endnotes are included at the end of the presentation. ~1% ~ 3% ~3½% ~5% 2014-2025 Latest Update Annual Electric & Gas Combined Residential Bill Growth b (CAGR) CMS 5 - yr Plan Avg. (2026 - 2030) CPI Energy Bills (Current) CPI Energy Bills (Historic) CMS ~2½% 5½% ~5% Consumers Energy Great Lakes Avg. National Avg. Annual Electric Residential Bill Growth a 2021 – 2025 (CAGR) ~ 2½ % ~ 1 % ~3%

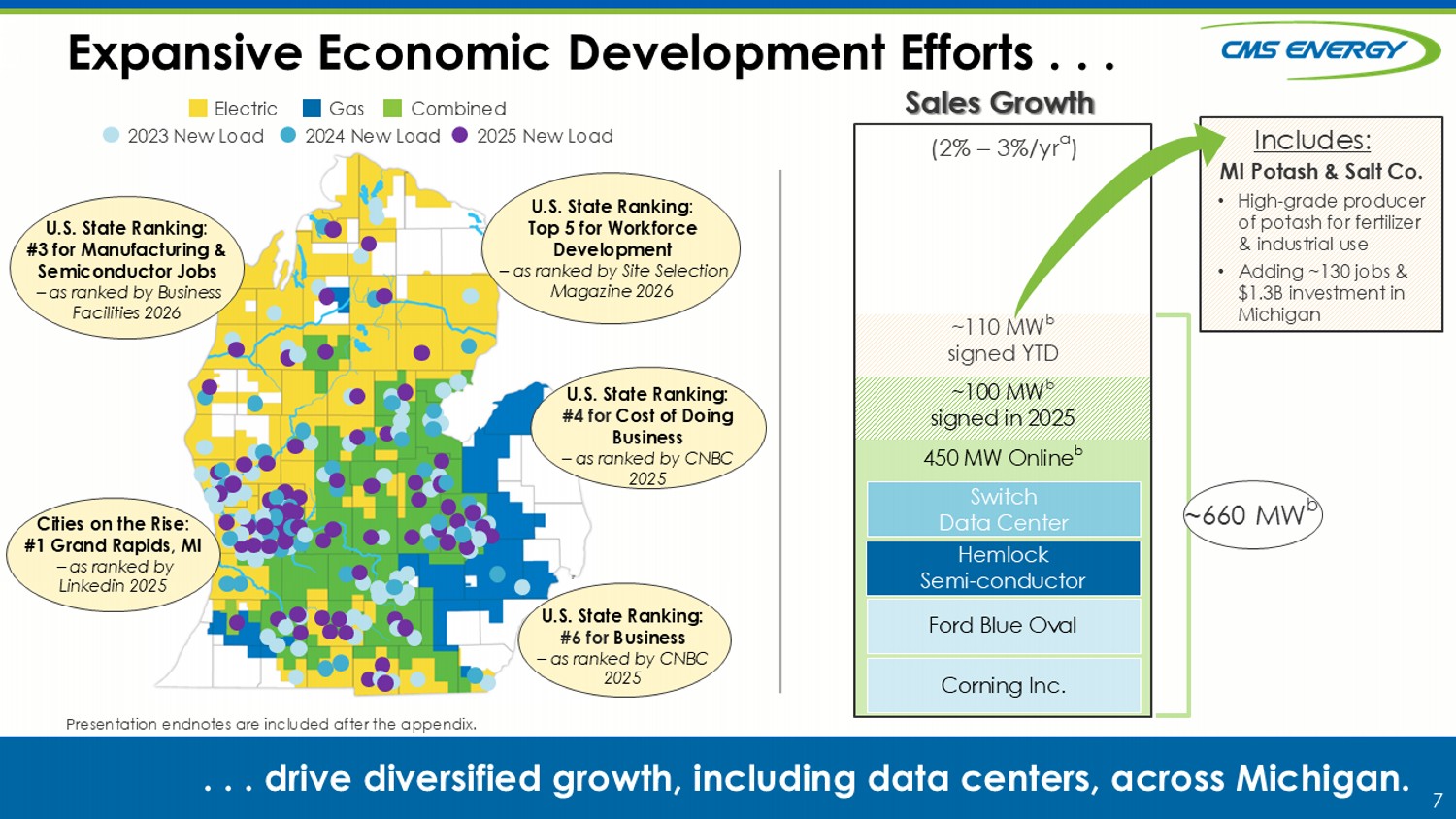

7 Expansive Economic Development Efforts . . . . . . drive diversified growth, including data centers, across Michigan. Electric Gas Combined 2023 New Load 2024 New Load 2025 New Load • Adding ~130 jobs & $1.3B investment in Michigan MI Potash & Salt Co. Hemlock Semi - conductor Switch Data Center Ford Blue Oval (2% – 3%/ yr a ) Corning Inc. ~660 MW b ~100 MW b signed in 2025 450 MW Online b ~110 MW b signed YTD Sales Growth Cities on the Rise : #1 Grand Rapids, MI – as ranked by Linkedin 2025 U.S. State Ranking: #6 for B usiness – as ranked by CNBC 2025 U.S. State Ranking: #4 for C ost of Doing B usiness – as ranked by CNBC 2025 U.S. State Ranking : Top 5 for Workforce Development – as ranked by Site Selection Magazine 2026 U.S. State Ranking : #3 for Manufacturing & Semiconductor Jobs – as ranked by Business Facilities 2026 • H igh - grade producer of potash for fertilizer & industrial use Includes: Presentation endnotes are included after the appendix.

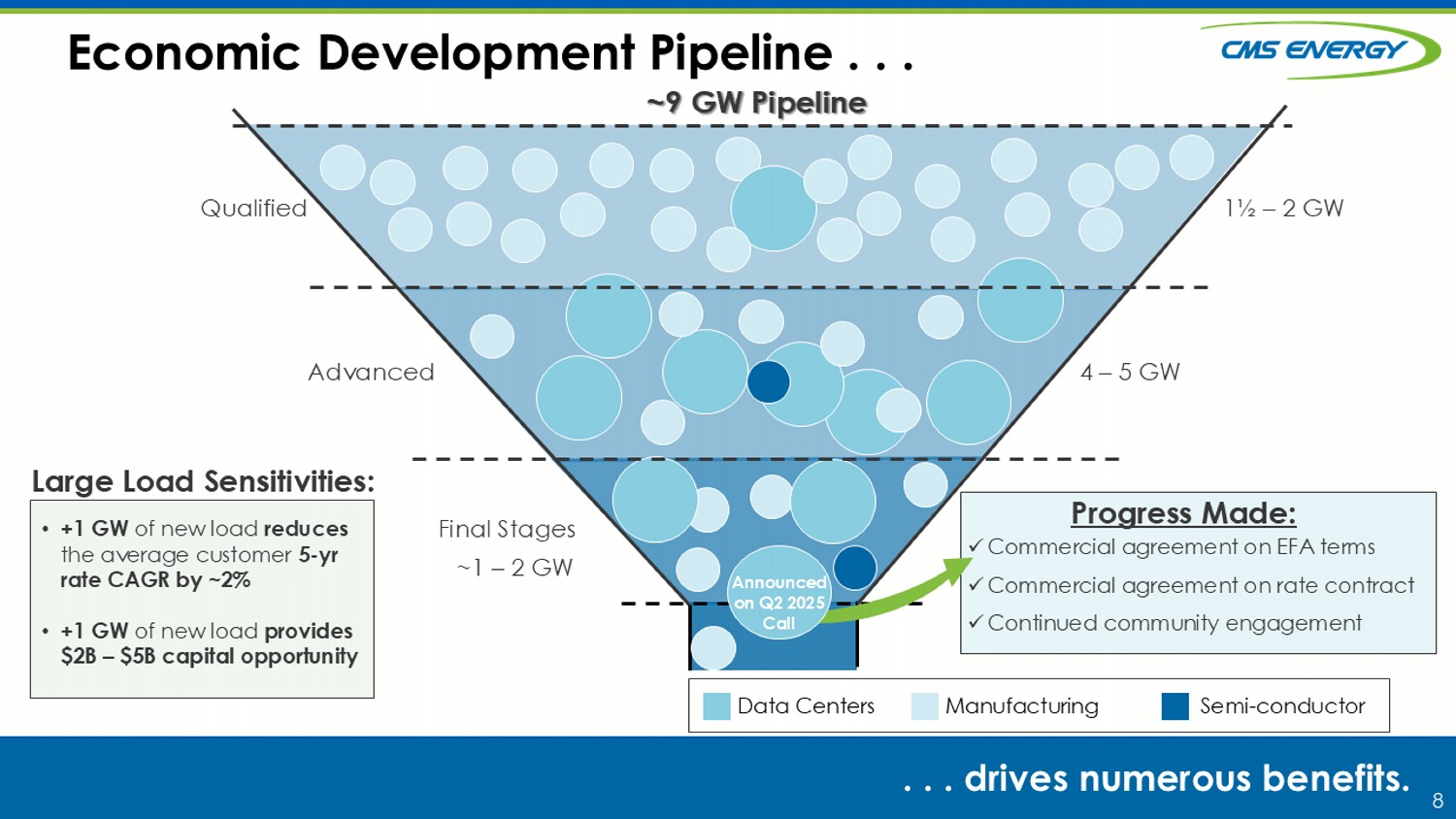

8 Economic Development Pipeline . . . . . . drives numerous benefits. ~9 GW Pipeline Semi - conductor Advanced Final Stages 4 – 5 GW 1½ – 2 GW Qualified Data Centers Manufacturing ~1 – 2 GW • +1 GW of new load reduces the average customer 5 - yr rate CAGR by ~2% • +1 GW of new load provides $2B – $5B capital opportunity Progress Made: x Commercial agreement on EFA terms x Commercial agreement on rate contract x Continued community engagement Large Load Sensitivities: Announced on Q2 2025 Call

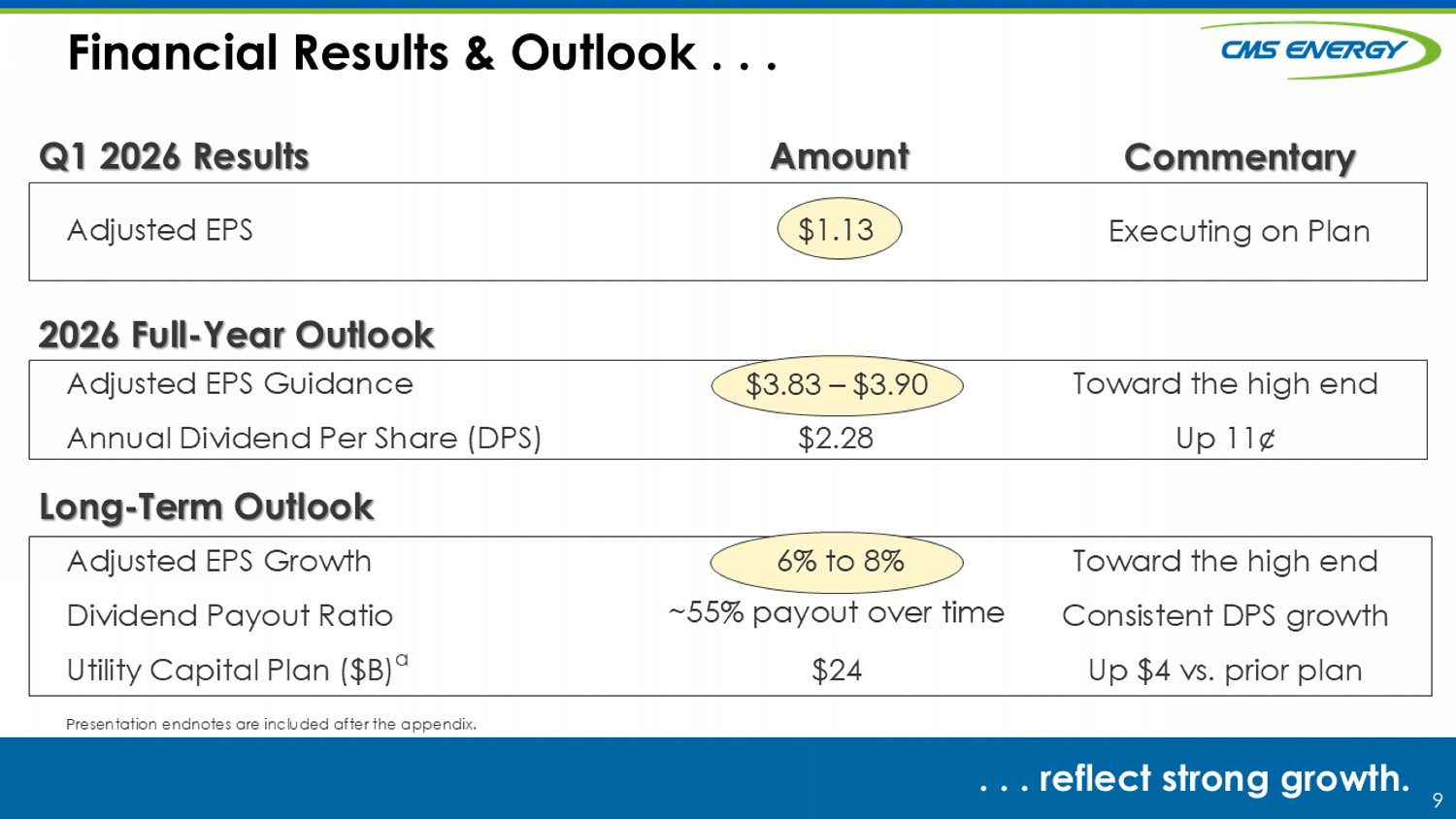

9 Commentary Amount Financial Results & Outlook . . . . . . reflect strong growth. Long - Term Outlook 2026 Full - Year Outlook Q1 2026 Results $1.13 Adjusted EPS Toward the high end Up 11¢ $3.06 – $3.12 $2.28 Adjusted EPS Guidance Annual Dividend Per Share (DPS) Toward the high end Consistent DPS growth Up $4 vs. prior plan 6% to 8%+ Adjusted EPS Growth Dividend Payout Ratio Utility Capital Plan ($B) a $24 $3.83 – $3.90 Executing on Plan ~55% payout over time Presentation endnotes are included after the appendix. 6% to 8%

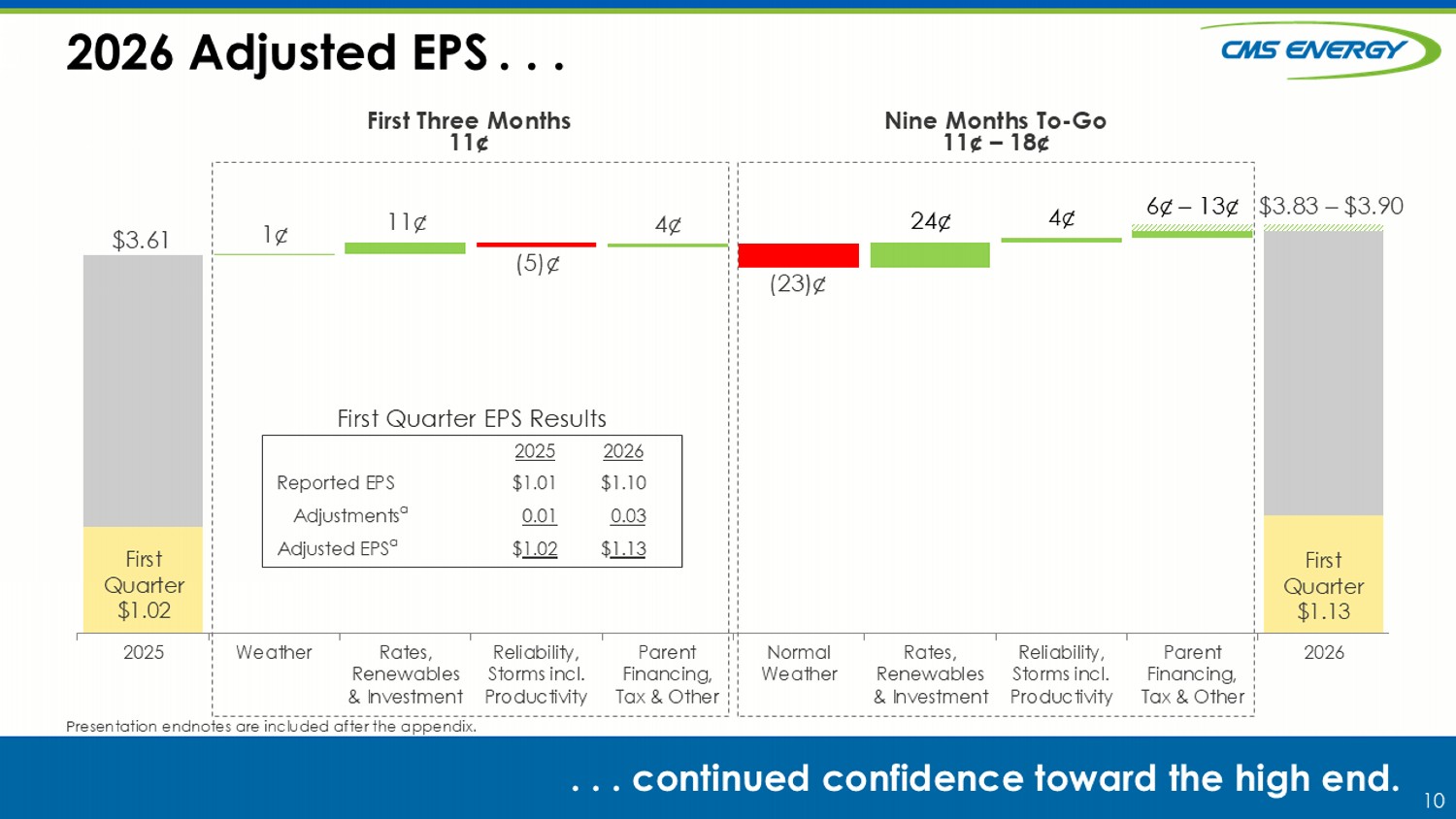

10 2025 Weather Rates, Renewables & Investment Reliability, Storms incl. Productivity Parent Financing, Tax & Other Normal Weather Rates, Renewables & Investment Reliability, Storms incl. Productivity Parent Financing, Tax & Other 2026 2026 Adjusted EPS . . . . . . continued confidence toward the high end. First Three Months 11¢ Nine Months To - Go 11¢ – 18 ¢ Presentation endnotes are included after the appendix. $3.83 – $3.90 1¢ $3.61 11¢ 4 ¢ (23)¢ 24¢ 6 ¢ – 13 ¢ (5)¢ 4 ¢ First Quarter $1. 13 First Quarter $1.02 2026 2025 $1.10 $1.01 Reported EPS 0.03 0.01 Adjustments a $ 1.13 $ 1.02 Adjusted EPS a First Quarter EPS Results

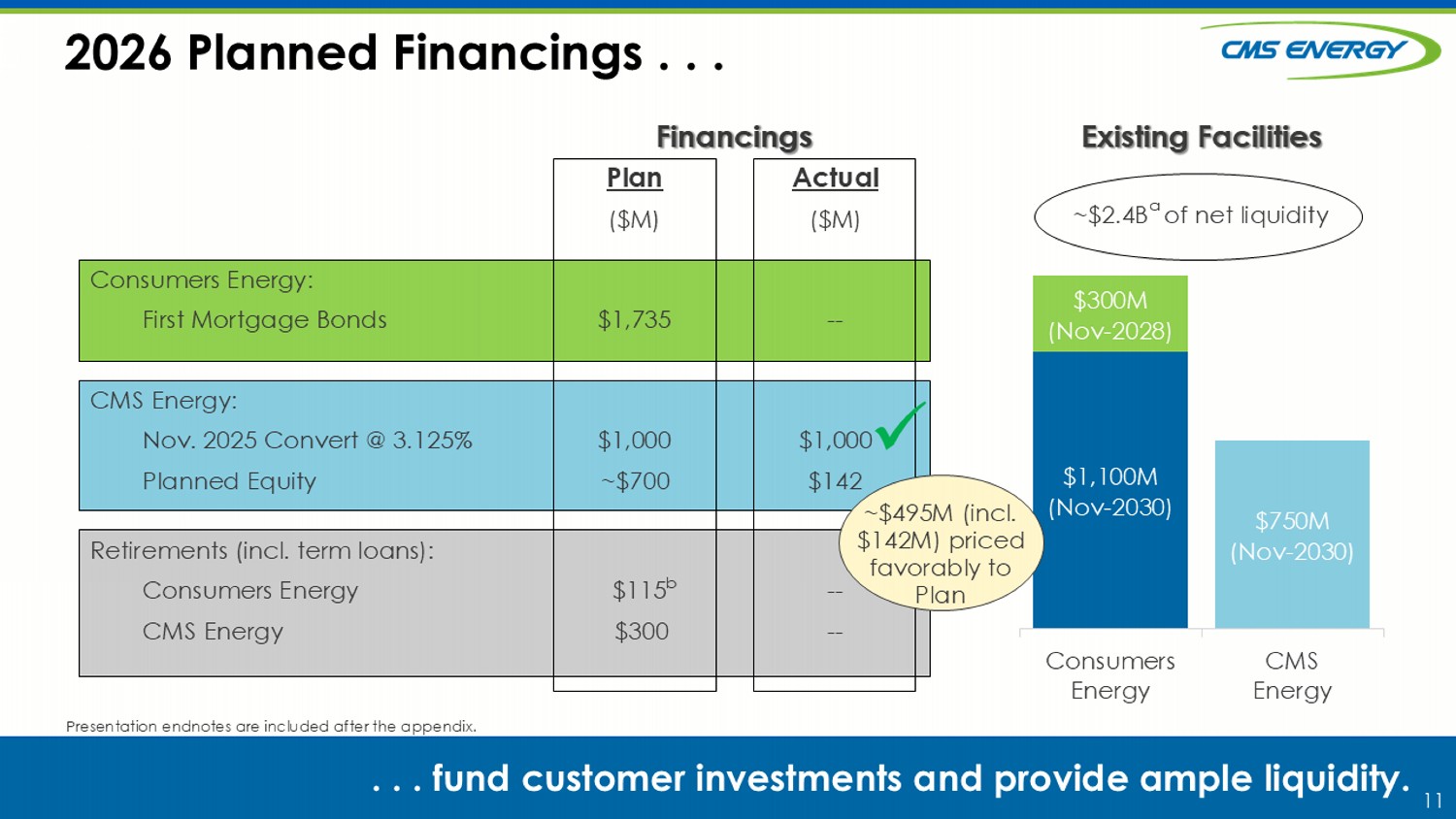

11 Actual Plan ($M) ($M) Consumers Energy: -- $1,735 First Mortgage Bonds CMS Energy: $1,000 $1,000 Nov. 2025 Convert @ 3.125% $142 ~$700 Planned Equity Retirements (incl. term loans): -- $115 b Consumers Energy -- $300 CMS Energy Existing Facilities $1,100M (Nov - 2030) $750M (Nov - 2030) $300M (Nov - 2028) Consumers Energy CMS Energy Financings 2026 Planned Financings . . . . . . fund customer investments and provide ample liquidity. Presentation endnotes are included after the appendix. ~$ 2.4 B a of net liquidity x ~$495M (incl. $142M) priced favorably to Plan

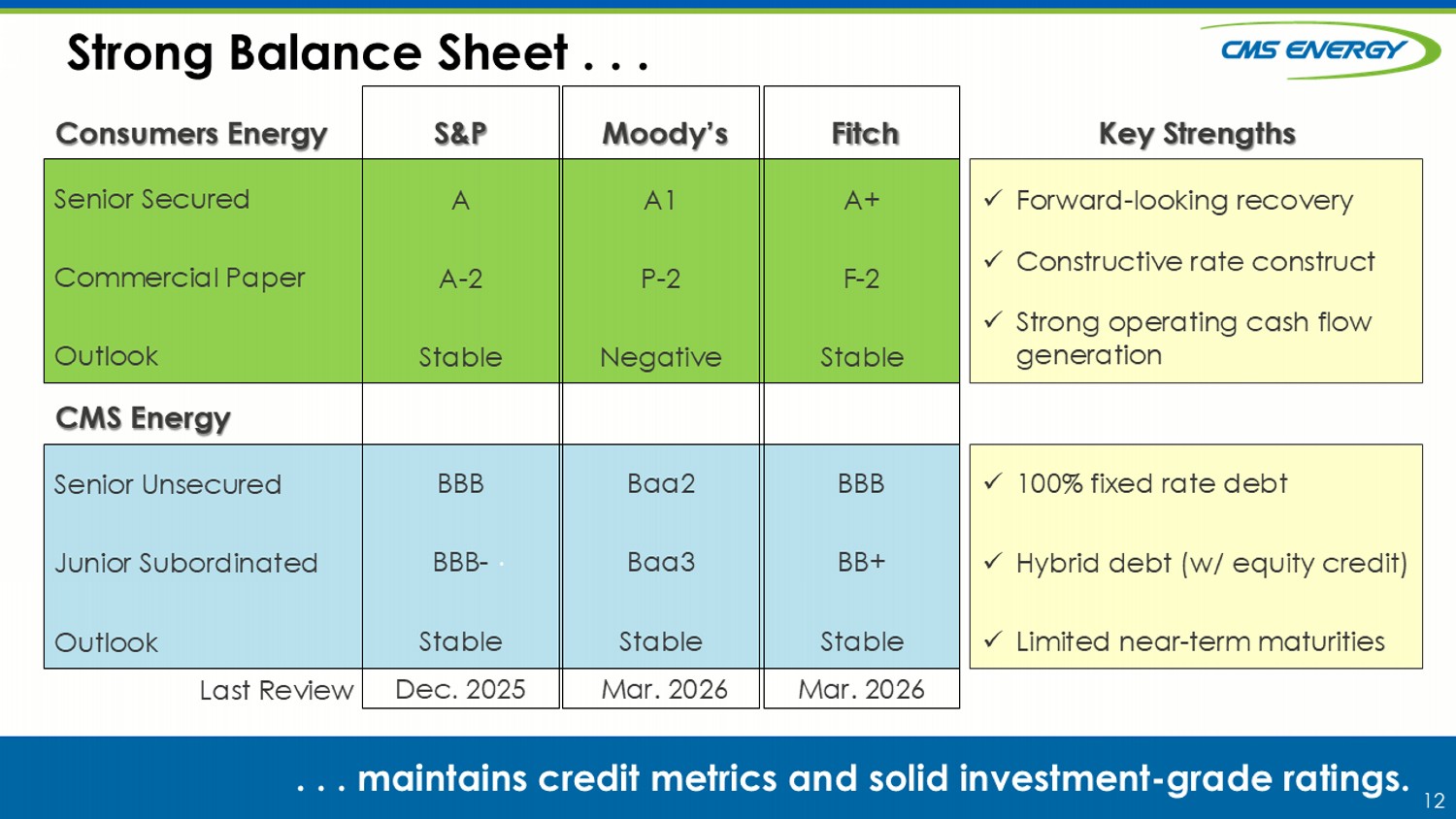

12 . Strong Balance Sheet . . . . . . m aintains credit metrics and solid investment - grade ratings. Consumers Energy CMS Energy Senior Secured Commercial Paper Outlook Senior Unsecured Junior Subordinated Outlook Last Review A1 P - 2 Negative Baa2 Baa3 Stable Mar. 2026 A+ F - 2 Stable BBB BB+ Stable Mar. 2026 S&P Moody’s Fitch x Forward - looking recovery x Constructive rate construct x Strong operating cash flow generation x 100% fixed rate debt x Hybrid debt (w/ equity credit) x Limited near - term maturities Key Strengths A A - 2 Stable BBB BBB - Stable Dec . 2025

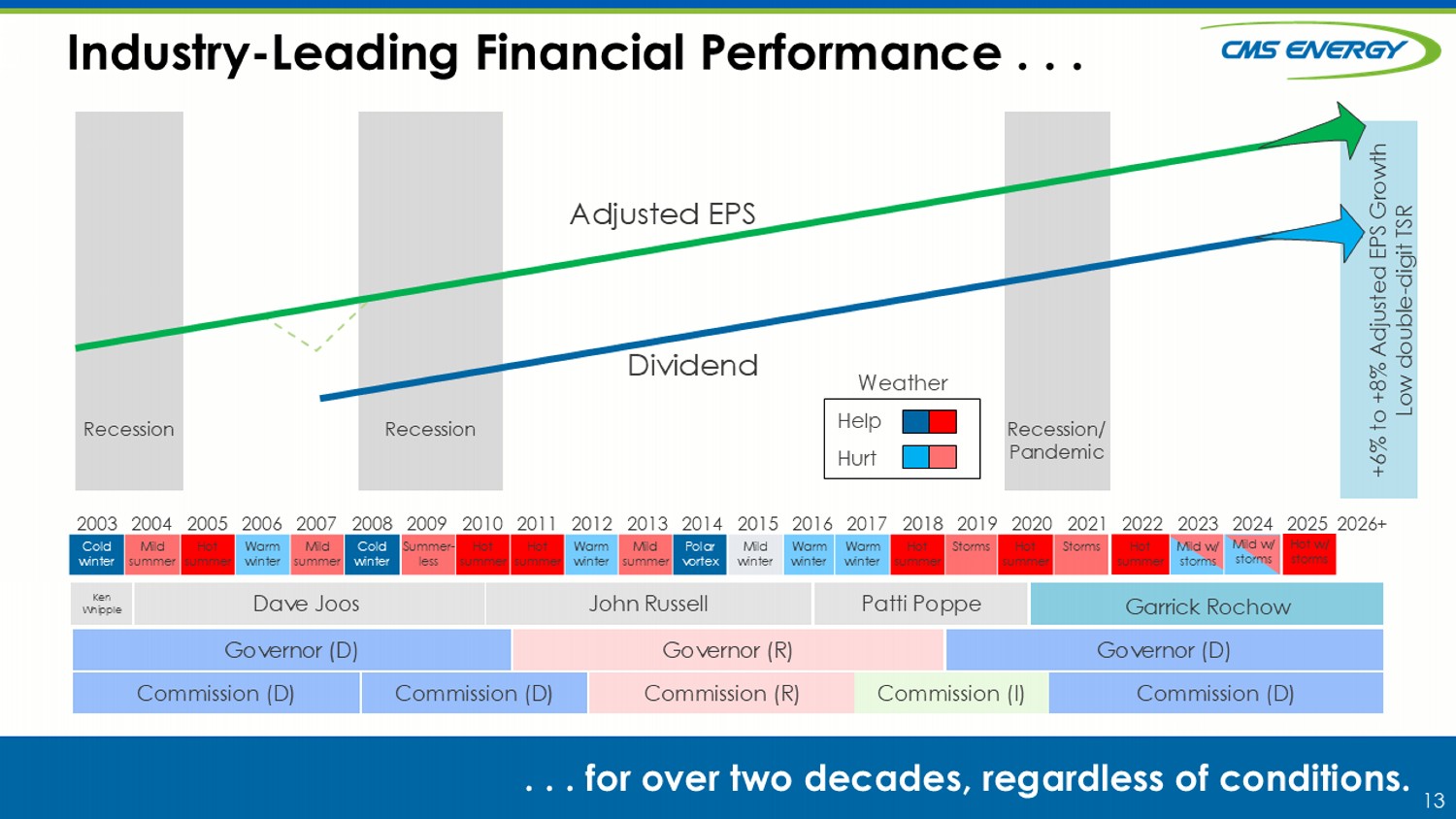

13 Recession Industry - Leading Financial Performance . . . . . . for over two decades, regardless of conditions. 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026+ Recession Adjusted EPS Dividend Weather Help Hurt Cold winter Mild summer Warm winter Hot summer Mild summer Cold winter Polar vortex Mild summer Warm winter Hot summer Hot summer Summer - less Storms Hot summer Storms Hot summer Warm winter Warm winter Mild winter Governor (D) Governor (R) Governor (D) Commission (D) Commission (D) Commission (R) Commission (I) Commission (D) Dave Joos John Russell Patti Poppe Ken Whipple Recession/ Pandemic Garrick Rochow Mild w/ storms Hot summer Mild w/ storms Hot w/ s torms +6% to +8% Adjusted EPS Growth Low double - digit TSR

14 14 Q&A Thank You!

15 Appendix

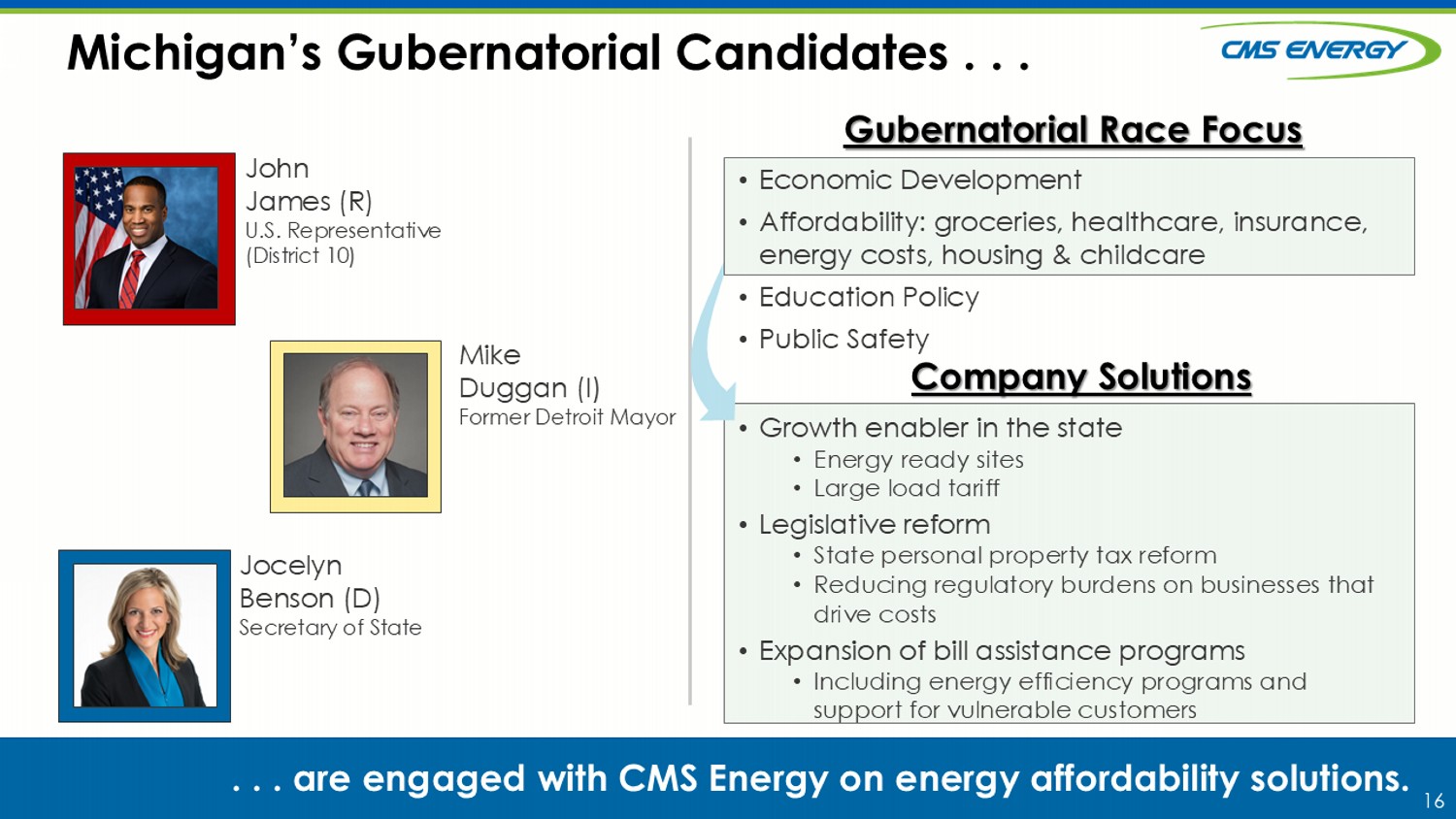

16 Michigan’s Gubernatorial Candidates . . . . . . a re engaged with CMS Energy on energy a ffordability solutions. John James (R) U.S. Representative (District 10) Jocelyn Benson (D) Secretary of State Mike Duggan (I) Former Detroit Mayor Gubernatorial Race Focus • Growth enabler in the state • Energy ready sites • Large load tariff • Legislative reform • State personal property tax reform • Reducing regulatory burdens on businesses that drive costs • Expansion of bill assistance programs • Including energy efficiency programs and support for vulnerable customers Company Solutions • Economic Development • Affordability: groceries, healthcare, insurance, energy costs, housing & childcare • Education Policy • Public Safety

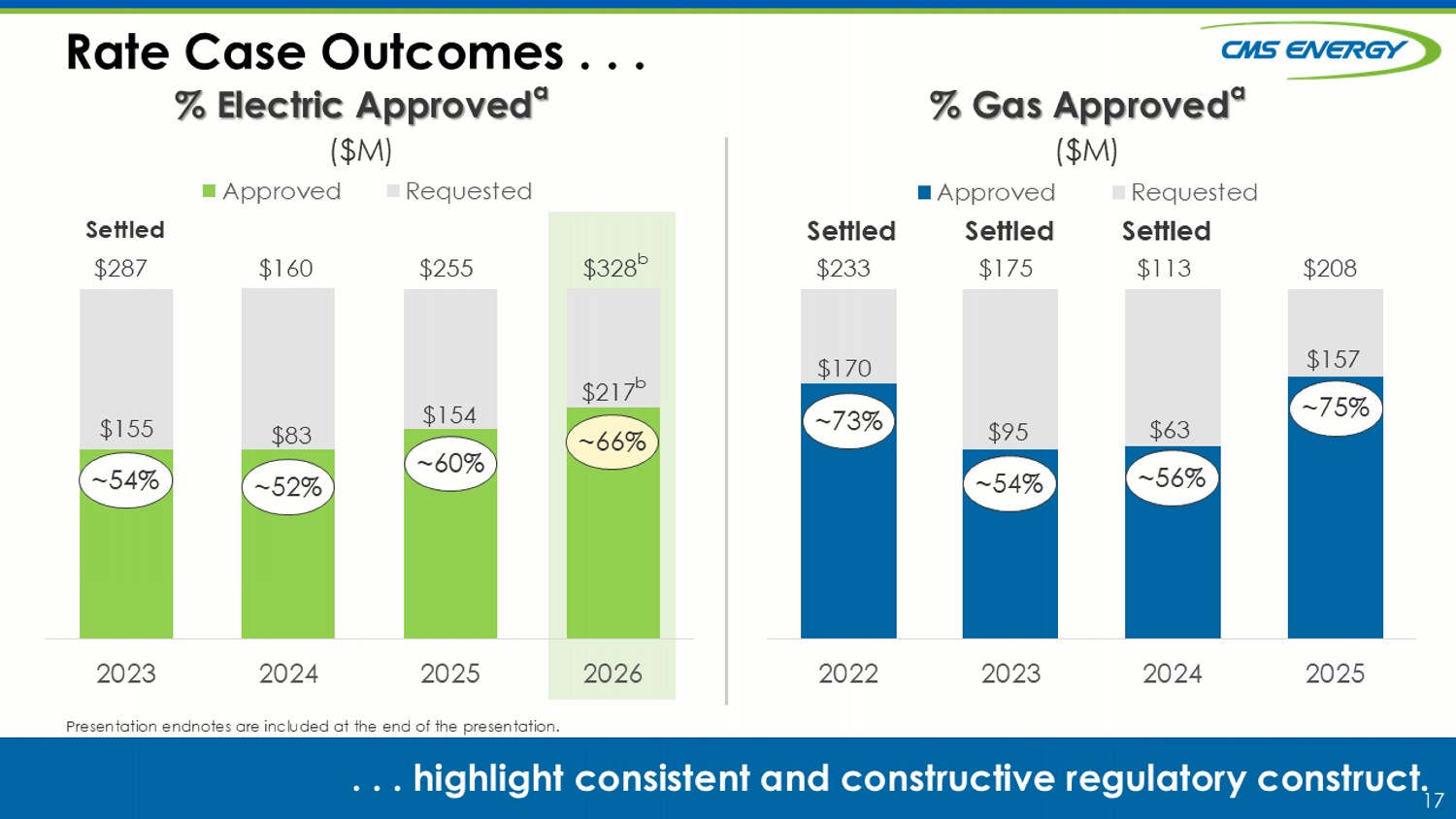

17 Rate Case Outcomes . . . . . . highlight consistent and constructive regulatory construct. Presentation endnotes are included at the end of the presentation. % Electric Approved a ($M) % Gas Approved a ($M) 2022 2023 2024 2025 Approved Requested ~56% ~54% ~75% $175 Settled $95 $113 $63 $208 $157 Settled v 2023 2024 2025 2026 Approved Requested ~52% ~54% ~60% ~66% $287 Settled $155 $160 $83 $255 $154 $328 b $217 b ~73% $233 $170 Settled

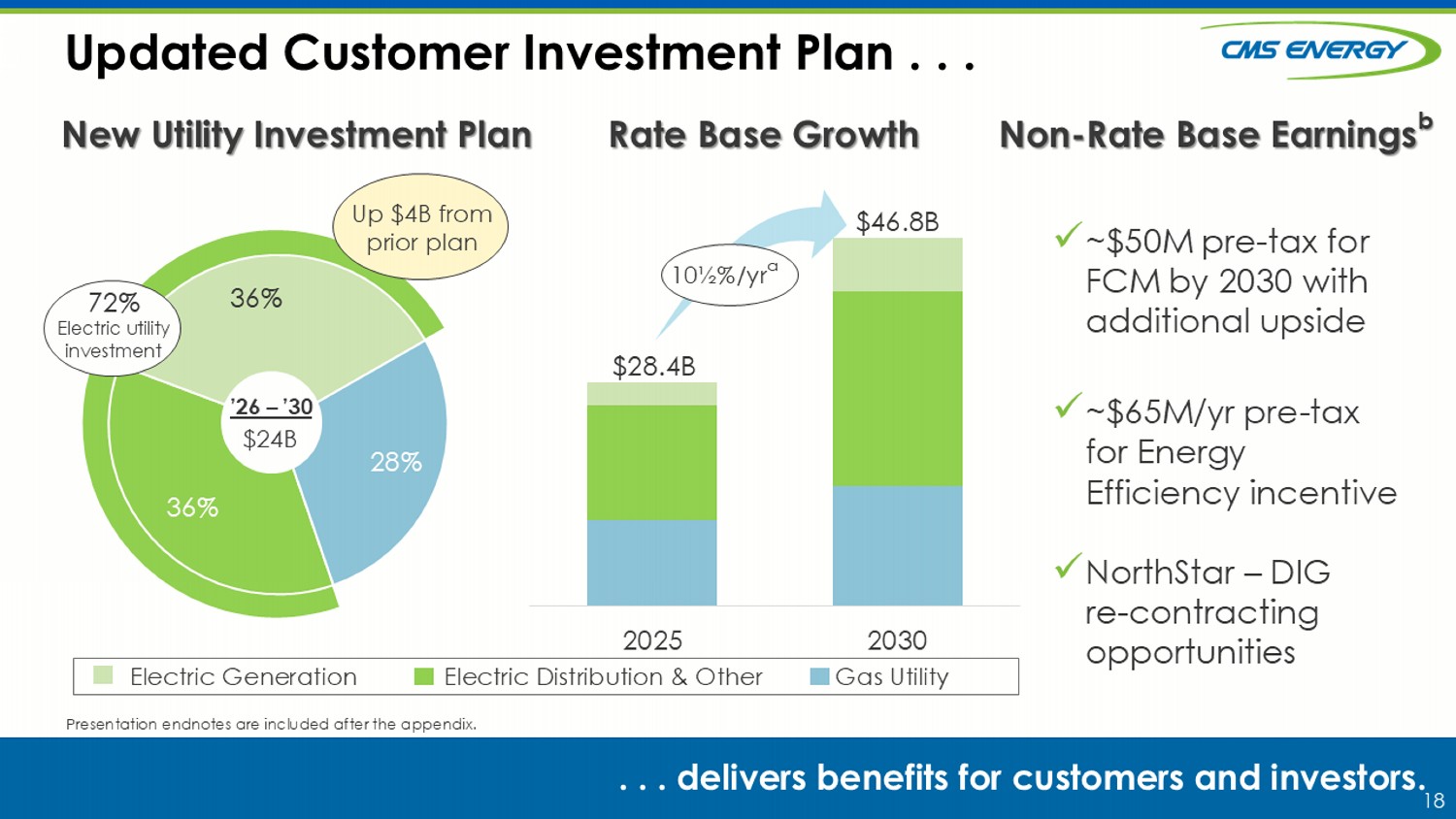

18 36% 36% 28% Updated Customer Investment Plan . . . . . . delivers benefits for customers and investors. New Utility Investment Plan Rate Base Growth Presentation endnotes are included after the appendix. E lectric Generation Electric Distribution & Other Gas Utility $24B ’26 – ’30 72% Electric utility investment x ~$50M pre - tax for FCM by 2030 with additional upside x ~$65M/yr pre - tax for Energy Efficiency incentive x NorthStar – DIG re - contracting opportunities Non - Rate Base Earnings b 2025 2030 $28.4B $ 46 .8B 10½%/ yr a Up $4B from prior plan

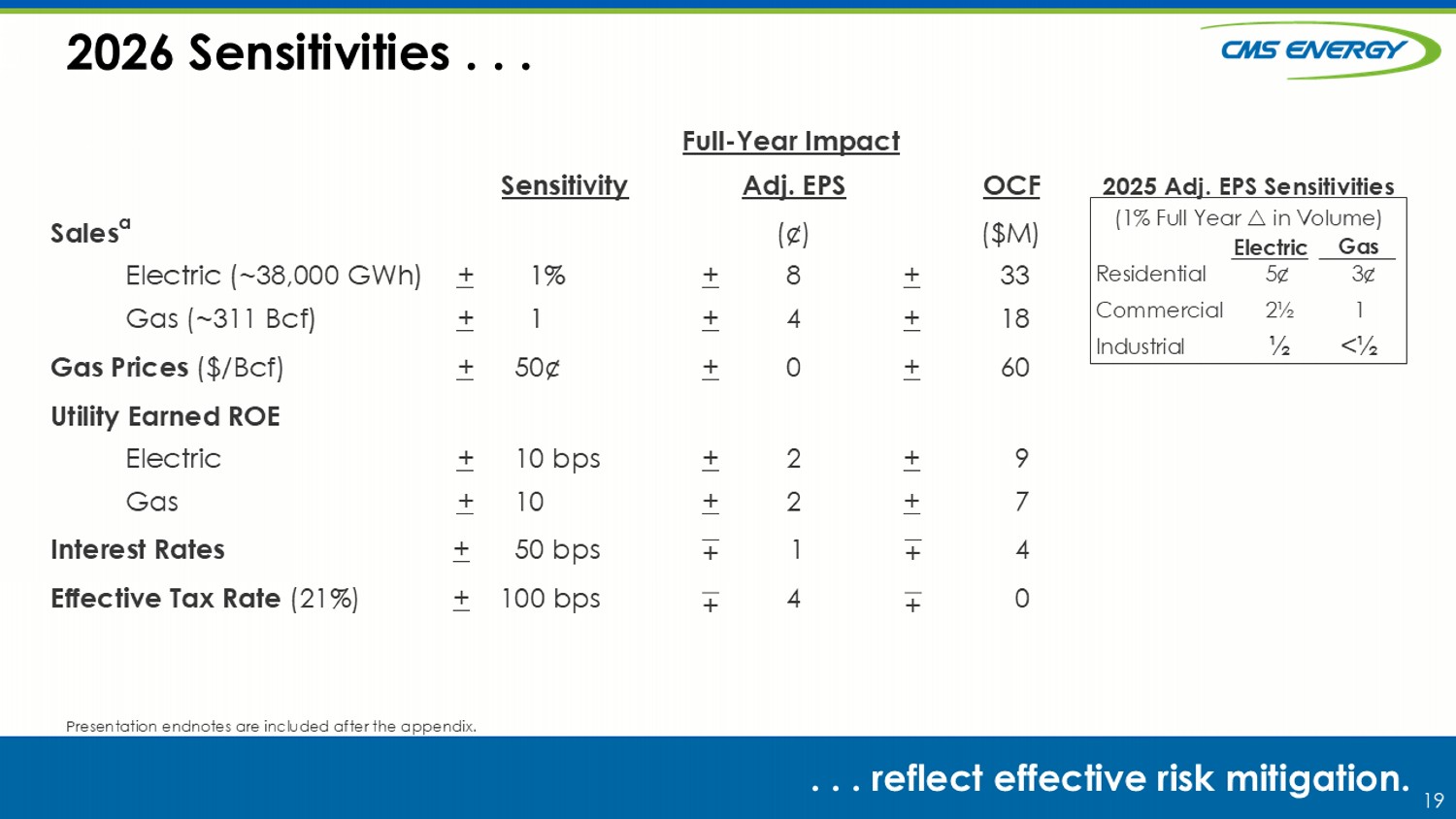

19 2026 Sensitivities . . . . . . r eflect effective risk mitigation. Presentation endnotes are included after the appendix. Full - Year Impact OCF Adj. EPS Sensitivity ($M) 33 18 + + ( ¢) 8 4 + + 1% 1 + + Sales a Electric (~38,000 GWh) Gas (~311 Bcf) 60 + 0 + 50 ¢ + Gas Prices ($/Bcf) 9 7 + + 2 2 + + 10 bps 10 + + Utility Earned ROE Electric Gas 4 1 50 bps + Interest Rates 0 4 100 bps + Effective Tax Rate (21%) + + + + Electric Residential Commercial Industrial 5 ¢ 2 ½ 3¢ (1% Full Year in Volume) 2025 Adj. EPS Sensitivities Gas ½ 1 < ½

20 Endnotes

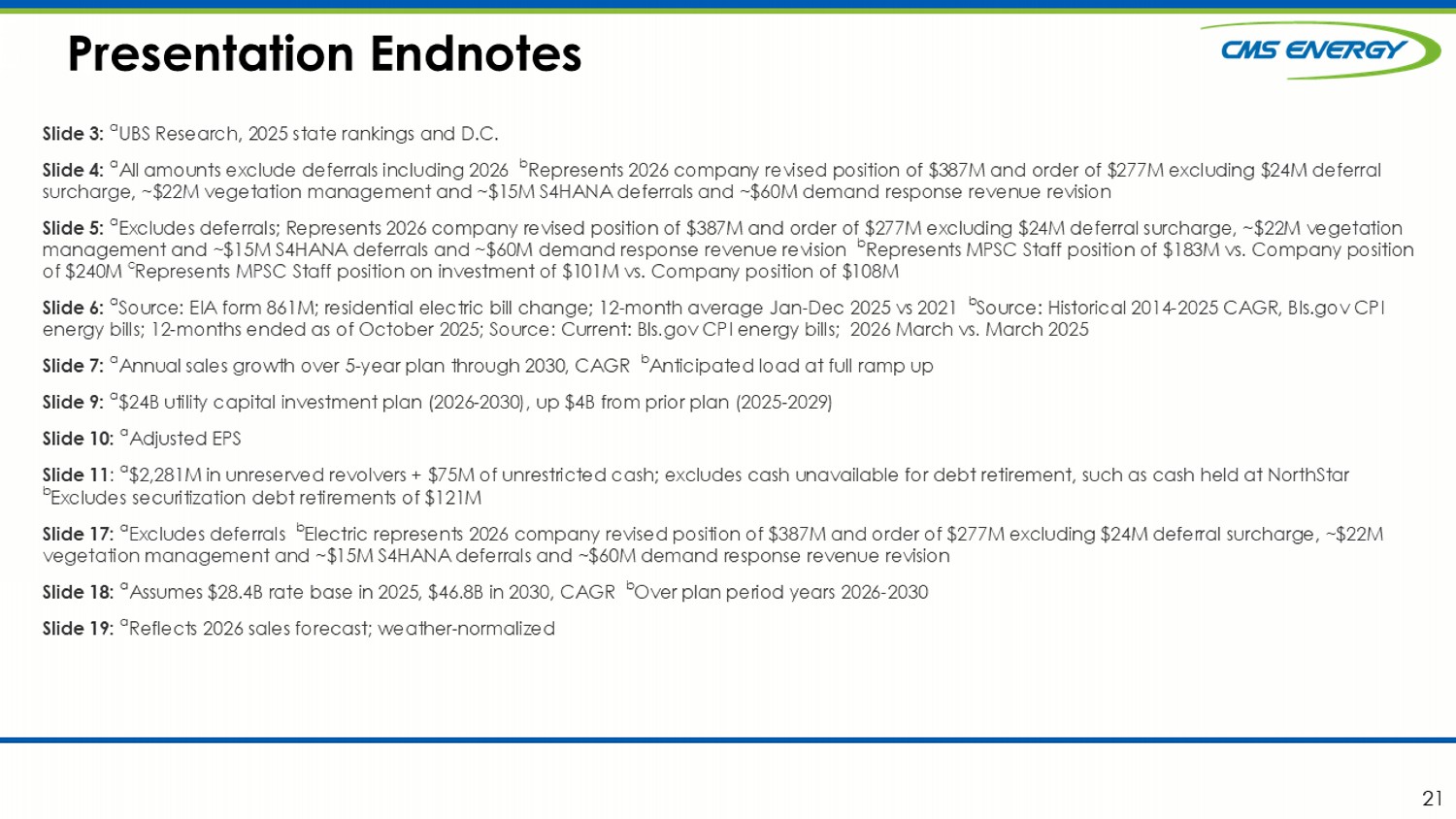

21 Presentation Endnotes Slide 3: a UBS Research, 2025 state rankings and D.C. Slide 4: a All amounts exclude deferrals including 2026 b Represents 2026 company revised position of $387M and order of $277M excluding $24M deferral surcharge, ~$22M vegetation management and ~$15M S4HANA deferrals and ~$60M demand response revenue revision Slide 5: a Excludes deferrals; Represents 2026 company revised position of $387M and order of $277M excluding $24M deferral surcharge, ~$22M vege ta tion management and ~$15M S4HANA deferrals and ~$60M demand response revenue revision b Represents MPSC Staff position of $183M vs. Company position of $240M c Represents MPSC Staff position on investment of $101M vs. Company position of $108M Slide 6: a Source : EIA form 861M; residential electric bill change; 12 - month average Jan - Dec 2025 vs 2021 b Source : Historical 2014 - 2025 CAGR, Bls.gov CPI energy bills; 12 - months ended as of October 2025; Source: Current: Bls.gov CPI energy bills; 2026 March vs. March 2025 Slide 7: a Annual sales growth over 5 - year plan through 2030, CAGR b Anticipated load at full ramp up Slide 9: a $24B utility capital investment plan (2026 - 2030), up $4B from prior plan (2025 - 2029) Slide 10: a Adjusted EPS Slide 11 : a $2,281M in unreserved revolvers + $75M of unrestricted cash; excludes cash unavailable for debt retirement, such as cash held at NorthStar b Excludes securitization debt retirements of $121M Slide 17: a Excludes deferrals b Electric represents 2026 company revised position of $387M and order of $277M excluding $24M deferral surcharge, ~$22M vegetation management and ~$15M S4HANA deferrals and ~$60M demand response revenue revision Slide 18: a Assumes $28.4B rate base in 2025, $46.8B in 2030, CAGR b Over plan period years 2026 - 2030 Slide 19: a Reflects 2026 sales forecast; weather - normalized 21

22 GAAP Reconciliation CMS Energy provides historical financial results on both a reported (GAAP) and adjusted (non - GAAP) basis and provides forward - lo oking guidance on an adjusted basis. During an oral presentation, references to “earnings” are on an adjusted basis. All references to net income ref er to net income available to common stockholders and references to earnings per share are on a diluted basis. Adjustments could include items such as disc ont inued operations, asset sales, impairments, restructuring costs, business optimization initiative, major enterprise resource planning software implementatio ns, changes in accounting principles, voluntary separation program, changes in federal and state tax policy, regulatory items from prior years, unrealized gains or lo sses from mark - to - market adjustments, recognized in net income related to NorthStar Clean Energy's interest expense, or other items. Management views adj usted earnings as a key measure of the company’s present operating financial performance and uses adjusted earnings for external communications with ana lysts and investors. Internally, the company uses adjusted earnings to measure and assess performance. Because the company is not able to estimate th e impact of specific line items, which have the potential to significantly impact, favorably or unfavorably, the company's reported earnings in future per iods, the company is not providing reported earnings guidance nor is it providing a reconciliation for the comparable future period earnings. The adju ste d earnings should be considered supplemental information to assist in understanding our business results, rather than as a substitute for the reported earnin gs. 22

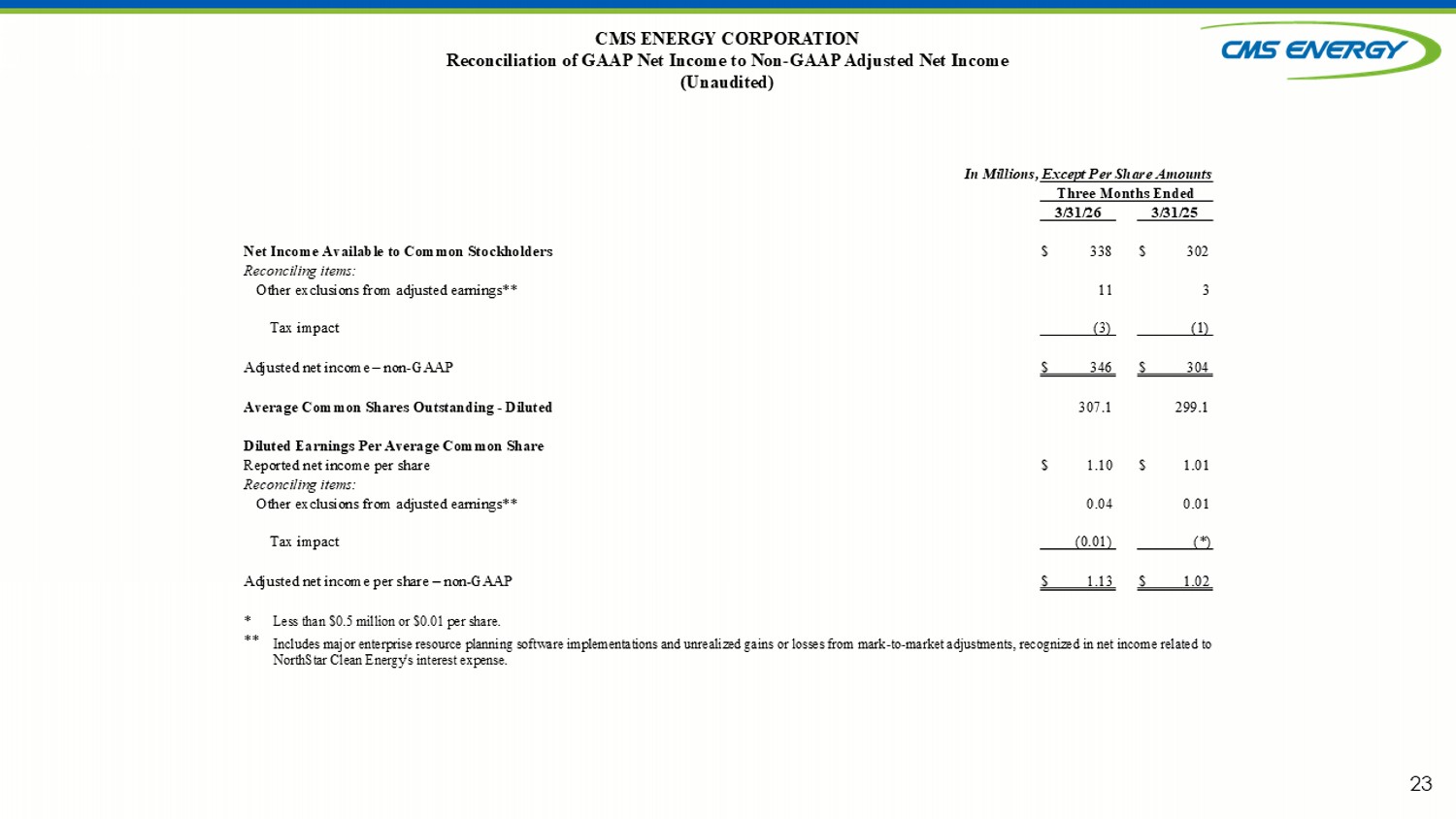

23 CMS ENERGY CORPORATION Reconciliation of GAAP Net Income to Non - GAAP Adjusted Net Income (Unaudited) In Millions, Except Per Share Amounts Three Months Ended 3/31/25 3/31/26 302 $ 338 $ Net Income Available to Common Stockholders Reconciling items: 3 11 Other exclusions from adjusted earnings** (1) (3) Tax impact 304 $ 346 $ Adjusted net income – non - GAAP 299.1 307.1 Average Common Shares Outstanding - Diluted Diluted Earnings Per Average Common Share 1.01 $ 1.10 $ Reported net income per share Reconciling items: 0.01 0.04 Other exclusions from adjusted earnings** (*) (0.01) Tax impact 1.02 $ 1.13 $ Adjusted net income per share – non - GAAP Less than $0.5 million or $0.01 per share. * Includes major enterprise resource planning software implementations and unrealized gains or losses from mark - to - market adjustme nts, recognized in net income related to NorthStar Clean Energy's interest expense. **