☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THESECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended March 31, 2024

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _____ to ________

Commission File Number: 001-08052

GLOBE LIFE INC.

(Exact name of registrant as specified in its charter)

Delaware

63-0780404

(State or other jurisdiction of incorporation or organization)

(I.R.S. Employer Identification No.)

3700 South Stonebridge Drive, McKinney, Texas75070

(Address of principal executive offices) (Zip Code)

(972) 569-4000

(Registrant’s telephone number, including area code)

NONE

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class

Trading Symbol(s)

Name of each exchange on which registered

Common Stock, $1.00 par value per share

GL

New York Stock Exchange

4.250% Junior Subordinated Debentures

GL PRD

New York Stock Exchange

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer

☒

Accelerated filer

☐

Non-accelerated filer

☐

Smaller reporting company

☐

Emerging growth company

☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

As used in this Form 10-Q, “Globe Life,” the “Company,” “we,” “our” and “us” refer to Globe Life Inc., a Delaware corporation incorporated in 1979, its subsidiaries and affiliates.

(Dollar amounts in thousands, except per share data)

Three Months Ended March 31,

2024

2023

Revenue:

Life premium

$

804,265

$

772,597

Health premium

341,019

322,493

Other premium

—

—

Total premium

1,145,284

1,095,090

Net investment income

282,578

257,105

Realized gains (losses)

(11,799)

(30,927)

Other income

76

50

Total revenue

1,416,139

1,321,318

Benefits and expenses:

Life policyholder benefits(1)

519,871

507,977

Health policyholder benefits(2)

202,327

190,962

Other policyholder benefits

9,595

8,988

Total policyholder benefits

731,793

707,927

Amortization of deferred acquisition costs

99,478

92,322

Commissions, premium taxes, and non-deferred acquisition costs

148,110

137,797

Other operating expense

93,214

84,171

Interest expense

28,621

24,867

Total benefits and expenses

1,101,216

1,047,084

Income before income taxes

314,923

274,234

Income tax benefit (expense)

(60,706)

(50,624)

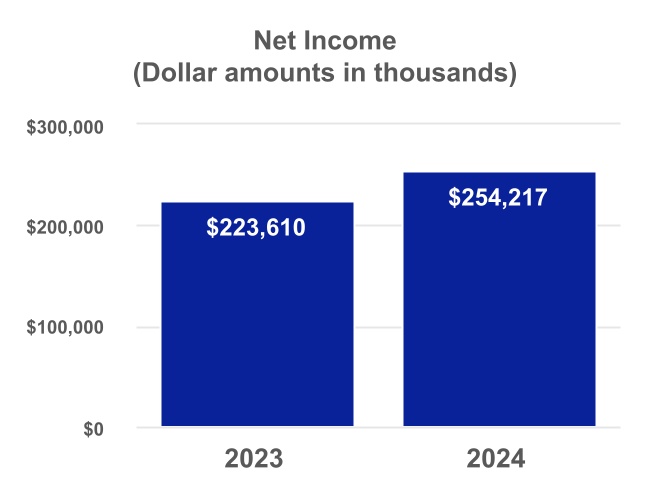

Net income

$

254,217

$

223,610

Basic net income per common share

$

2.71

$

2.32

Diluted net income per common share

$

2.67

$

2.28

(1)Net of a remeasurement gain of $4.9 million for the three months ended March 31, 2024, and a remeasurement gain of $2.7 million for the same period in 2023.

(2)Net of a remeasurement gain of $3.2 million for the three months ended March 31, 2024, and a remeasurement loss of $2.0 million for the same period in 2023.

See accompanying Notes to Condensed Consolidated Financial Statements.

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

Note 1—Significant Accounting Policies

Business: (Globe Life), (the Company), refers to Globe Life Inc., an insurance holding company incorporated in Delaware in 1979, and Globe Life Inc. subsidiaries and affiliates. Globe Life Inc.'s direct or indirect primary subsidiaries are Globe Life And Accident Insurance Company, American Income Life Insurance Company, Liberty National Life Insurance Company, Family Heritage Life Insurance Company of America, and United American Insurance Company. The underwriting companies are owned by their ultimate corporate parent, Globe Life Inc. (Parent Company).

Globe Life provides a variety of life and supplemental health insurance products and annuities to a broad base of customers. The Company is organized into four reportable segments: life insurance, supplemental health insurance, annuities, and investments.

Globe Life markets its insurance products through a number of distribution channels, each of which sells the products of one or more of Globe Life's insurance segments. Our distribution channels consist of the following exclusive agencies: American Income Life Division (American Income), Liberty National Division (Liberty National) and Family Heritage Division (Family Heritage); an independent agency, United American Division (United American); and our Direct to Consumer Division (DTC).

Basis of Presentation: The accompanying condensed consolidated financial statements of Globe Life have been prepared in accordance with the instructions to Form 10-Q. Therefore, they do not include all of the disclosures required by accounting principles generally accepted in the United States of America (GAAP) for annual financial statements. However, in the opinion of management, these statements include all adjustments, consisting of normal recurring adjustments, which are necessary for a fair presentation of the condensed consolidated financial position at March 31, 2024, and the condensed consolidated results of operations, comprehensive income, and cash flows for the periods ended March 31, 2024 and 2023. The interim period condensed consolidated financial statements should be read in conjunction with the Consolidated Financial Statements that are included in the Form 10-K filed with the Securities Exchange Commission (SEC) on February 28, 2024.

Use of Estimates: The preparation of the condensed consolidated financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent liabilities at the date of the condensed consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. See further documentation in the significant accounting policies or the accompanying notes.

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

Note 2—New Accounting Standards

Accounting Pronouncements Adopted in the Current Year

Standard

Description

Effective Date

Effect on the Condensed Consolidated Financial Statements

ASU No. 2022-03,Fair Value Measurement (Topic 820): Fair Value Measurement of Equity Securities Subject to Contractual Sale Restrictions

ASU 2022-03 adds disclosure requirements specific to equity securities subject to contractual sale restrictions. The disclosures clarify the nature of the contractual sale as well as the duration of the restriction and the circumstances that could cause a lapse in the restriction.

This standard is effective for the Company for fiscal years beginning on January 1, 2024 and interim periods within those fiscal years.

The adoption of this standard did not have a material impact on the Condensed Consolidated Financial Statements.

Accounting Pronouncements Yet to be Adopted

Standard

Description

Effective Date

Effect on the Condensed Consolidated Financial Statements

ASU 2023-07 adds disclosure requirements to segment expenses, improving the financial reporting of the entity’s overall performance and assessment of future cash flows. The disclosures will require more detailed information related to the entity’s reportable segments.

This standard is effective for the Company for annual periods beginning on January 1, 2024 and for interim periods beginning on January 1, 2025, and will be implemented on a retrospective basis.

The Company does not expect the standard will have a material impact on the Condensed Consolidated Financial Statements.

ASU No. 2023-09,Income Taxes (Topic 740): Improvements to Income Tax Disclosures

ASU 2023-09 adds disclosure requirements to disaggregated information related to the effective tax rate reconciliation and information on income taxes paid. The disclosures will enhance the assessment of the entity’s operations and related tax risks.

This standard is effective for the Company for annual periods beginning on January 1, 2025, and will be implemented on a prospective basis.

The Company does not expect the standard will have a material impact on the Condensed Consolidated Financial Statements.

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

Note 3—Supplemental Information about Changes to Accumulated Other Comprehensive Income

Components of Accumulated Other Comprehensive Income: An analysis of the change in balance by component of Accumulated Other Comprehensive Income is as follows for the three month periods ended March 31, 2024 and 2023:

Three Months Ended March 31, 2024

Available for Sale Assets

Future Policy Benefits

Foreign Exchange

Pension Adjustments

Total

Balance at January 1, 2024

$

(827,596)

$

(1,947,391)

$

4,719

$

(2,151)

$

(2,772,419)

Other comprehensive income (loss) before reclassifications, net of tax

(239,684)

556,632

(9,951)

—

306,997

Reclassifications, net of tax

(1,905)

—

—

91

(1,814)

Other comprehensive income (loss)

(241,589)

556,632

(9,951)

91

305,183

Balance at March 31, 2024

$

(1,069,185)

$

(1,390,759)

$

(5,232)

$

(2,060)

$

(2,467,236)

Three Months Ended March 31, 2023

Available for Sale Assets

Future Policy Benefits

Foreign Exchange

Pension Adjustments

Total

Balance at January 1, 2023

$

(1,420,672)

$

(1,369,204)

$

(1,681)

$

1,244

$

(2,790,313)

Other comprehensive income (loss) before reclassifications, net of tax

378,162

(569,503)

(5,148)

—

(196,489)

Reclassifications, net of tax

25,746

—

—

(37)

25,709

Other comprehensive income (loss)

403,908

(569,503)

(5,148)

(37)

(170,780)

Balance at March 31, 2023

$

(1,016,764)

$

(1,938,707)

$

(6,829)

$

1,207

$

(2,961,093)

Reclassification Adjustments: Reclassification adjustments out of Accumulated Other Comprehensive Income are presented below for the three month periods ended March 31, 2024 and 2023.

Three Months Ended March 31,

Affected line items in the Statements of Operations

Component Line Item

2024

2023

Unrealized investment (gains) losses on available for sale assets:

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

Note 4—Investments

Portfolio Composition: Summaries of fixed maturities available for sale by amortized cost, fair value, and allowance for credit losses at March 31, 2024 and December 31, 2023, and the corresponding amounts of gross unrealized gains and losses recognized in accumulated other comprehensive income (loss) are as follows. Redeemable preferred stock is included within "Corporates, by sector."

At March 31, 2024

Amortized Cost

Allowance for Credit Losses

Gross Unrealized Gains

Gross Unrealized Losses

Fair

Value(1)

% of Total

Fixed

Maturities(2)

Fixed maturities available for sale:

U.S. Government direct, guaranteed, and government-sponsored enterprises

$

401,859

$

—

$

1

$

(39,039)

$

362,821

2

States, municipalities, and political subdivisions

3,301,276

—

38,251

(454,605)

2,884,922

16

Foreign governments

39,558

—

—

(10,227)

29,331

—

Corporates, by sector:

Industrials

8,297,566

(7,027)

161,482

(667,927)

7,784,094

43

Financial

5,213,973

—

89,584

(416,724)

4,886,833

27

Utilities

2,127,792

—

51,901

(105,623)

2,074,070

11

Total corporates

15,639,331

(7,027)

302,967

(1,190,274)

14,744,997

81

Collateralized debt obligations

36,730

—

3,001

—

39,731

—

Other asset-backed securities

86,030

—

2

(3,481)

82,551

1

Total fixed maturities

$

19,504,784

$

(7,027)

$

344,222

$

(1,697,626)

$

18,144,353

100

(1)Amount reported in the balance sheet.

(2)At fair value.

At December 31, 2023

Amortized Cost

Allowance for Credit Losses

Gross Unrealized Gains

Gross Unrealized Losses

Fair

Value(1)

% of Total

Fixed

Maturities(2)

Fixed maturities available for sale:

U.S. Government direct, guaranteed, and government-sponsored enterprises

$

398,450

$

—

$

7

$

(32,306)

$

366,151

2

States, municipalities, and political subdivisions

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

The Company has exposure to real estate investment trusts with an average rating of BBB+, which had a fair value of $415 million (2% of the total fixed maturity portfolio) and $425 million (2% of the total fixed maturity portfolio) at March 31, 2024 and December 31, 2023, respectively.

A schedule of fixed maturities available for sale by contractual maturity date at March 31, 2024, is shown below on an amortized cost basis, net of allowance for credit losses, and on a fair value basis. Actual disposition dates could differ from contractual maturities due to call or prepayment provisions.

At March 31, 2024

Amortized Cost, net

Fair Value

Fixed maturities available for sale:

Due in one year or less

$

86,769

$

86,518

Due after one year through five years

857,913

862,187

Due after five years through ten years

2,034,083

2,040,670

Due after ten years through twenty years

8,712,181

8,331,022

Due after twenty years

7,684,013

6,701,637

Mortgage-backed and asset-backed securities

122,798

122,319

$

19,497,757

$

18,144,353

Analysis of Investment Operations:"Net investment income" for the three month periods ended March 31, 2024 and 2023 is summarized as follows:

Three Months Ended March 31,

2024

2023

% Change

Fixed maturities available for sale

$

246,098

$

232,299

6

Policy loans

12,816

11,755

9

Mortgage loans

6,760

4,003

69

Other long-term investments(1)

19,663

11,740

67

Short-term investments

1,688

1,595

287,025

261,392

10

Less investment expense

(4,447)

(4,287)

4

Net investment income

$

282,578

$

257,105

10

(1)For the three months ended March 31, 2024 and 2023, the investment funds, accounted for under the fair value option method, recorded $18.9 million and $11.3 million, respectively, in net investment income. Refer to Other Long-Term Investmentsbelowfor further discussion on the investment funds.

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

Selected information about sales of fixed maturities available for sale is as follows:

Three Months Ended March 31,

2024

2023

Fixed maturities available for sale:

Proceeds from sales(1)

$

27,853

$

15,705

Gross realized gains

175

—

Gross realized losses

(35)

(358)

(1)There were no unsettled sales in the periods ended March 31, 2024 and 2023.

An analysis of "Realized gains (losses)" is as follows:

Three Months Ended March 31,

2024

2023

Realized investment gains (losses):

Fixed maturities available for sale:

Sales and other(1)

$

140

$

(357)

Provision for credit losses

88

(32,767)

Fair value option—change in fair value

(15,403)

1,858

Mortgage loans

(874)

(1,280)

Other investments

314

(214)

Realized gains (losses) from investments

(15,735)

(32,760)

Other gains (losses)

3,936

1,833

Total realized gains (losses)

(11,799)

(30,927)

Applicable tax

2,478

6,495

Realized gains (losses), net of tax

$

(9,321)

$

(24,432)

(1)During the three months ended March 31, 2024 and 2023, the Company recorded $66.9 million and $0 of issuer-initiated exchanges of fixed maturities (noncash transactions) that resulted in no realized gains (losses) in either period.

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

Fair Value Measurements:The following tables represent the fair value of fixed maturities measured on a recurring basis at March 31, 2024 and December 31, 2023:

Fair Value Measurement at March 31, 2024:

Quoted Prices in Active Markets for Identical Assets (Level 1)

Significant Other Observable Inputs (Level 2)

Significant Unobservable Inputs (Level 3)

Total Fair Value

Fixed maturities available for sale

U.S. Government direct, guaranteed, and government-sponsored enterprises

$

—

$

362,821

$

—

$

362,821

States, municipalities, and political subdivisions

—

2,884,922

—

2,884,922

Foreign governments

—

29,331

—

29,331

Corporates, by sector:

Industrials

—

7,584,006

200,088

7,784,094

Financial

—

4,756,052

130,781

4,886,833

Utilities

—

1,967,375

106,695

2,074,070

Total corporates

—

14,307,433

437,564

14,744,997

Collateralized debt obligations

—

—

39,731

39,731

Other asset-backed securities

—

82,551

—

82,551

Total fixed maturities

$

—

$

17,667,058

$

477,295

$

18,144,353

Percentage of total

—

%

97

%

3

%

100

%

Fair Value Measurement at December 31, 2023:

Quoted Prices in Active Markets for Identical Assets (Level 1)

Significant Other Observable Inputs (Level 2)

Significant Unobservable Inputs (Level 3)

Total Fair Value

Fixed maturities available for sale

U.S. Government direct, guaranteed, and government-sponsored enterprises

$

—

$

366,151

$

—

$

366,151

States, municipalities, and political subdivisions

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

The following tables represent changes in fixed maturities measured at fair value on a recurring basis using significant unobservable inputs (Level 3):

Analysis of Changes in Fair Value Measurements Using Significant Unobservable Inputs (Level 3)

Asset-

backed Securities

Collateralized Debt Obligations

Corporates

Total

Balance at January 1, 2024

$

—

$

42,146

$

454,733

$

496,879

Included in realized gains / losses

—

—

—

—

Included in other comprehensive income

—

(2,035)

(5,996)

(8,031)

Acquisitions

—

—

7,800

7,800

Sales

—

—

—

—

Amortization

—

1,141

(4)

1,137

Other(1)

—

(1,521)

(18,969)

(20,490)

Transfers into Level 3(2)

—

—

—

—

Transfers out of Level 3(2)

—

—

—

—

Balance at March 31, 2024

$

—

$

39,731

$

437,564

$

477,295

Percent of total fixed maturities

—

%

—

%

3

%

3

%

(1)Includes capitalized interest, foreign exchange adjustments, and principal repayments.

(2)Considered to be transferred at the end of the period. Transfers into Level 3 occur when observable inputs are no longer available. Transfers out of Level 3 occur when observable inputs become available.

Analysis of Changes in Fair Value Measurements Using Significant Unobservable Inputs (Level 3)

Asset-

backed Securities

Collateralized Debt Obligations

Corporates

Total

Balance at January 1, 2023

$

—

$

50,364

$

478,083

$

528,447

Included in realized gains / losses

—

—

—

—

Included in other comprehensive income

—

(4,542)

5,370

828

Acquisitions

—

—

—

—

Sales

—

—

—

—

Amortization

—

1,141

2

1,143

Other(1)

—

(1,461)

(11,816)

(13,277)

Transfers into Level 3(2)

—

—

—

—

Transfers out of Level 3(2)

—

—

—

—

Balance at March 31, 2023

$

—

$

45,502

$

471,639

$

517,141

Percent of total fixed maturities

—

%

—

%

3

%

3

%

(1)Includes capitalized interest, foreign exchange adjustments, and principal repayments.

(2)Considered to be transferred at the end of the period. Transfers into Level 3 occur when observable inputs are no longer available. Transfers out of Level 3 occur when observable inputs become available.

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

The following table presents changes in unrealized gains and losses for the period included in accumulated other comprehensive income for assets held at the end of the reporting period for Level 3 classification:

Changes in Unrealized Gains (Losses) included in Accumulated Other Comprehensive Income for Assets Held at the End of the Period

Asset- backed Securities

Collateralized Debt Obligations

Corporates

Total

At March 31, 2024

$

—

$

(2,035)

$

(5,996)

$

(8,031)

At March 31, 2023

—

(4,542)

5,370

828

Unrealized Loss Analysis: The following table discloses information about fixed maturities available for sale in an unrealized loss position.

Less than Twelve Months

Twelve Months or Longer

Total

Number of issues (CUSIPs) held:

As of March 31, 2024

350

1,654

2,004

As of December 31, 2023

151

1,614

1,765

Globe Life's entire fixed maturity portfolio consisted of 2,551 issues by 991 different issuers at March 31, 2024 and 2,473 issues by 980 different issuers at December 31, 2023. The increase in the number of securities in an unrealized loss position during the period ended March 31, 2024 is due to the increase in interest rates. The weighted-average quality rating of all unrealized loss positions at amortized cost was A- as of March 31, 2024 and December 31, 2023.

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

The following tables disclose unrealized investment losses by class and major sector of fixed maturities available for sale at March 31, 2024 and December 31, 2023.

Analysis of Gross Unrealized Investment Losses

At March 31, 2024

Less than Twelve Months

Twelve Months or Longer

Total

Fair Value

Unrealized Loss

Fair Value

Unrealized Loss

Fair Value

Unrealized Loss

Fixed maturities available for sale:

Investment grade securities:

U.S. Government direct, guaranteed, and government-sponsored enterprises

$

2,033

$

(66)

$

360,438

$

(38,973)

$

362,471

$

(39,039)

States, municipalities, and political subdivisions

479,111

(7,440)

1,648,303

(447,165)

2,127,414

(454,605)

Foreign governments

1,469

(5)

27,862

(10,222)

29,331

(10,227)

Corporates, by sector:

Industrials

692,151

(25,399)

4,221,438

(613,109)

4,913,589

(638,508)

Financial

361,061

(3,813)

2,419,494

(369,671)

2,780,555

(373,484)

Utilities

284,655

(3,438)

681,618

(100,695)

966,273

(104,133)

Total corporates

1,337,867

(32,650)

7,322,550

(1,083,475)

8,660,417

(1,116,125)

Collateralized debt obligations

—

—

—

—

—

—

Other asset-backed securities

—

—

71,424

(2,980)

71,424

(2,980)

Total investment grade securities

1,820,480

(40,161)

9,430,577

(1,582,815)

11,251,057

(1,622,976)

Below investment grade securities:

Corporates, by sector:

Industrials

—

—

146,466

(29,419)

146,466

(29,419)

Financial

8,704

(1,403)

166,838

(41,837)

175,542

(43,240)

Utilities

8,902

(27)

19,713

(1,463)

28,615

(1,490)

Total corporates

17,606

(1,430)

333,017

(72,719)

350,623

(74,149)

Collateralized debt obligations

—

—

—

—

—

—

Other asset-backed securities

—

—

11,079

(501)

11,079

(501)

Total below investment grade securities

17,606

(1,430)

344,096

(73,220)

361,702

(74,650)

Total fixed maturities

$

1,838,086

$

(41,591)

$

9,774,673

$

(1,656,035)

$

11,612,759

$

(1,697,626)

Gross unrealized losses may fluctuate quarter over quarter due to adverse factors in the market that affect our holdings, such as changes in interest rates or credit spreads. The Company considers many factors when determining whether an allowance for a credit loss should be recorded. While the Company holds securities that may be in an unrealized loss position from time to time, Globe Life does not generally intend to sell and it is unlikely that the Company will be required to sell the fixed maturities prior to their anticipated recovery or maturity due to the strong cash flows generated by its insurance operations.

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

Fixed Maturities, Allowance for Credit Losses: A summary of the activity in the allowance for credit losses is as follows.

Three Months Ended March 31,

2024

2023

Allowance for credit losses beginning balance

$

7,115

$

—

Additions to allowance for which credit losses were not previously recorded

—

32,767

Additions (reductions) to allowance for fixed maturities that previously had an allowance

(88)

—

Reduction of allowance for which the Company intends to sell or more likely than not will be required to sell or sold during the period

—

—

Allowance for credit losses ending balance

$

7,027

$

32,767

As of March 31, 2024 and December 31, 2023, the Company did not have any fixed maturities in non-accrual status.

Mortgage Loans (commercial mortgage loans):Summaries of commercial mortgage loans by property type and geographical location at March 31, 2024 and December 31, 2023 are as follows:

March 31, 2024

December 31, 2023

Carrying Value

% of Total

Carrying Value

% of Total

Property type:

Multi-family

$

117,147

36

$

116,299

42

Industrial

81,975

25

57,267

20

Retail

46,822

14

23,925

9

Hospitality

43,634

13

43,897

16

Mixed use

37,267

11

34,749

12

Office

6,734

2

6,734

2

Total recorded investment

333,579

101

282,871

101

Less allowance for credit losses

(4,546)

(1)

(3,672)

(1)

Carrying value, net of allowance for credit losses

$

329,033

100

$

279,199

100

March 31, 2024

December 31, 2023

Carrying Value

% of Total

Carrying Value

% of Total

Geographic location:

Florida

$

60,587

18

$

48,233

17

California

57,093

17

54,721

20

Texas

53,399

16

45,111

16

New Jersey

44,592

14

44,574

16

New York

35,142

11

20,284

7

Washington

14,978

4

14,969

5

Other

67,788

21

54,979

20

Total recorded investment

333,579

101

282,871

101

Less allowance for credit losses

(4,546)

(1)

(3,672)

(1)

Carrying value, net of allowance for credit losses

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

The following tables are reflective of the key factors, debt service coverage ratios, and loan-to-value (LTV) ratios that are utilized by management to monitor the performance of the portfolios. The Company only makes new investments in commercial mortgage loans that have a LTV ratio less than 80%. LTV's that exceed 80% are generally as a result of decreases in the valuation of the underlying property. Generally, a higher LTV ratio and a lower debt service coverage ratio equates to higher risk of loss.

March 31, 2024

Recorded Investment

Debt Service Coverage Ratios(1)

<1.00x

1.00x—1.20x

>1.20x

Total

% of Gross Total

Loan-to-value ratio(2):

Less than 70%

$

35,492

$

155,974

$

125,457

$

316,923

95

70% to 80%

—

—

—

—

—

81% to 90%

9,621

—

—

9,621

3

Greater than 90%

7,035

—

—

7,035

2

Total

$

52,148

$

155,974

$

125,457

333,579

100

Less allowance for credit losses

(4,546)

Total, net of allowance for credit losses

$

329,033

(1)Annual net operating income divided by annual mortgage debt service (principal and interest).

(2)Loan balance divided by appraised value at origination, including planned renovations and stabilized occupancy. Updated internal valuations are used when a loan is materially underperforming.

December 31, 2023

Recorded Investment

Debt Service Coverage Ratios(1)

<1.00x

1.00x—1.20x

>1.20x

Total

% of Gross Total

Loan-to-value ratio(2):

Less than 70%

$

27,091

$

180,761

$

58,364

$

266,216

94

70% to 80%

—

—

—

—

—

81% to 90%

8,468

—

1,153

9,621

3

Greater than 90%

7,034

—

—

7,034

3

Total

$

42,593

$

180,761

$

59,517

282,871

100

Less allowance for credit losses

(3,672)

Total, net of allowance for credit losses

$

279,199

(1)Annual net operating income divided by annual mortgage debt service (principal and interest).

(2)Loan balance divided by appraised value at origination, including planned renovations and stabilized occupancy. Updated internal valuations are used when a loan is materially underperforming.

As of March 31, 2024, the Company evaluated the commercial mortgage loan portfolio on a pool basis to determine the allowance for credit losses. At the end of the period, the Company had 32 loans in the portfolio. For the three months ended March 31, 2024, the allowance for credit losses increased by $874 thousand to $4.5 million. The provision for credit losses is included in "Realized gains (losses)" in the Condensed Consolidated Statements of Operations.

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

There was one delinquent commercial mortgage loan, with an outstanding par value of $3.7 million and outstanding interest due of $116 thousand, as of March 31, 2024. The underlying collateral for this loan is in the process of being sold and the Company expects to recover all interest and principal due as of March 31, 2024. There were no delinquent commercial mortgage loans as of December 31, 2023. As of March 31, 2024, the Company had one commercial mortgage loan in non-accrual status with a principal balance of $4.4 million. As of December 31, 2023, the Company had no commercial mortgage loans in non-accrual status. The Company's unfunded commitment balance to commercial loan borrowers was $29 million as of March 31, 2024.

Other Long-Term Investments: Other long-term investments consist of the following assets:

March 31, 2024

December 31, 2023

Investment funds

$

844,916

$

795,583

Other

54,169

40,295

Total

$

899,085

$

835,878

The following table presents additional information about the Company's investment funds as of March 31, 2024 and December 31, 2023 at fair value:

Fair Value

Unfunded Commitments

Investment Category

March 31, 2024

December 31, 2023

March 31, 2024

Redemption Term/Notice(1)

Commercial mortgage loans

$

459,549

$

411,315

$

489,617

Fully redeemable and non-redeemable with varying terms.

Opportunistic and private credit

180,019

181,410

125,844

Fully redeemable and non-redeemable with varying terms.

Infrastructure

165,441

165,887

16,706

Fully redeemable and non-redeemable with varying terms.

Other

39,907

36,971

53,752

Non-redeemable with varying terms

Total investment funds

$

844,916

$

795,583

$

685,919

(1)Non-redeemable funds generally have an expected life of 7 to 12 years from fund closing with extension options of 1 to 4 years. Redemptions are paid out throughout the life of the funds at the General Partner's discretion. Redeemable funds can generally be redeemed over 6 to 36 months upon request from limited partners.

The Company had $67 million of capital called during the period from existing investment funds. The Company's unfunded commitments were $686 million as of March 31, 2024.

Note 5—Commitments and Contingencies

Guarantees: The Parent Company has guaranteed letters of credit in connection with its credit facility with a group of banks. The letters of credit were issued by TMK Re, Ltd., a wholly-owned subsidiary, to secure TMK Re, Ltd.’s obligation for claims on certain policies reinsured by TMK Re, Ltd. that were sold by other Globe Life insurance subsidiaries. These letters of credit facilitate TMK Re, Ltd.’s ability to reinsure the business of Globe Life's insurance carriers. The agreement was amended on March 29, 2024 and now expires in 2029. The maximum amount of letters of credit available is $250 million. The Parent Company would be liable to the extent that TMK Re, Ltd. does not pay the reinsured party. The amount of letters of credit outstanding at March 31, 2024 was $115 million.

Litigation: Globe Life Inc. and its subsidiaries, in common with the insurance industry in general, are subject to litigation, including: putative class action litigation; alleged breaches of contract; torts, including bad faith and fraud claims based on alleged wrongful or fraudulent acts of agents of the Parent Company's insurance subsidiaries; alleged employment discrimination; alleged worker misclassification; and miscellaneous other causes of action. Based upon information presently available, and in light of legal and other factual defenses available to the Parent Company and its subsidiaries, management does not believe that it is reasonably possible that such litigation will

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

have a material adverse effect on Globe Life's financial condition, future operating results or liquidity; however, assessing the eventual outcome of litigation necessarily involves forward-looking speculation as to judgments to be made by judges, juries and appellate courts in the future. This bespeaks caution, particularly in states with reputations for high punitive damage verdicts.

On September 30, 2022, putative class action litigation was filed against American Income, Giglione-Ackerman Agency, LLC, Eric Giglione and David Ackerman (collectively, “Defendants”) in New Jersey Superior Court (Atiya Bell, et al. v. American Income Life Insurance Company, et al., Case No. MID-L-004928-22). American Income subsequently removed the case to United States District Court for the District of New Jersey (Case No. 2:22-cv-06913-CCC-MAH). Plaintiffs Atiya Bell and Abel Flores (“Plaintiffs”) are former New Jersey independent sales agents who alleged they should have been classified as employees, and asserted claims under New Jersey state law on behalf of (i) a putative class of registered agents in New Jersey who have worked remotely for at least one week since March 9, 2020, and (ii) a putative class of registered agents in New Jersey who trained for at least one week to become sales agents for American Income in New Jersey during the six years prior to September 30, 2022. Plaintiffs made claims under the New Jersey Wage and Hour Law and the New Jersey Wage Payment Law for the alleged failure to pay minimum wages and overtime pay, including for time spent in training, liquidated damages and attorney’s fees and costs. American Income filed a motion to compel this matter to arbitration pursuant to the arbitration clauses found in the agent contracts executed by the claimants. In September 2023, the court denied American Income’s motion, but did so without prejudice, and invited the parties to “conduct limited discovery on the issue of arbitrability,” after which discovery the court would hear a renewed motion from American Income. However, in November 2023, prior to American Income’s filing such motion, the parties agreed in principle to settle the claimants’ claims for a non-material amount.

On September 1, 2023, plaintiff Miné Caglar Cost (“Plaintiff) filed a complaint against American Income Life Insurance Company (“American Income”) in the Superior Court of the State of California for the County of Los Angeles, asserting a single claim for violation of the Private Attorneys General Act (“PAGA”) (Cost v. American Income Life Insurance Company, et al., Case No. 23SMCV04113). Plaintiff is a former California independent insurance sales agent who alleges one cause of action for civil penalties under PAGA arising out of alleged violations of the wage-and-hour provisions of the California Labor Code stemming from American Income’s alleged misclassification of Plaintiff and other California-based sales agents as independent contractors. American Income filed a motion to compel arbitration on an individual basis and stay the representative component of Plaintiff’s claims, to which Plaintiff stipulated. On December 12, 2023, the Court approved the parties’ stipulation to compel the matter to individual arbitration and stayed the case pending the completion of the individual arbitration.

On April 4, 2023, putative class action litigation was filed against National Income Life Insurance Company (“National Income”) in New York Supreme Court by plaintiffs Melissa K. Goppert, Sarah Valente, James O’Neill, Jennifer Abe, and Emily Herendeen (“Plaintiffs”) (Goppert, et al. v. National Income Life Insurance Company, Index No. 153096/2023). Plaintiffs are former National Income independent sales agents who allege they should have been classified as employees and assert claims under New York state law on behalf of a putative class of former independent sales agents and individuals who trained to become independent sale agents since March 2017. Plaintiffs make claims under New York’s Minimum Wage Law (NYLL § 633 and 12 NYCRR § 142-2.1); Overtime Compensation Law (NYLL § 633 and 12 NYCRR § 142-2.2); and “Spread of Hours” Law (12 NYCRR § 142-2.4) for the alleged failure to pay minimum wages and overtime pay, including for time spent in training, and attorney’s fees and costs. National Income filed a motion to compel arbitration of each Plaintiff’s claims on an individual basis, which the Court granted in full on January 11, 2024, and on February 7, 2024, Plaintiffs filed a notice of appeal of the Court’s order.

On November 30, 2023, the Company and our subsidiary, American Income Life Insurance Company, received subpoenas from the U.S. Attorney’s Office for the Western District of Pennsylvania, seeking documents relating to sales practices by certain of our independent sales agents contracted to sell American Income Life Insurance Company policies. The Company and American Income Life Insurance Company are in the preliminary stages of responding to these subpoenas and have been cooperating with the Department of Justice’s investigation. The Department of Justice has not asserted any claims or made allegations against the Company and American Income Life Insurance Company with respect to the foregoing inquiry, and the Company currently is not aware that any legal

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

proceedings are contemplated by governmental authorities. While no assurances can be made, at present management does not believe that it is reasonably possible or probable that this matter will result in a material loss.

A putative securities class action was filed on April 30, 2024 against the Company and six of its current/former senior executives in the United States District Court for the Eastern District of Texas. The case, which is captioned City of Miami Gen. Emp. & Sanitation Emp. Ret. Trust, et al. v. Globe Life Inc., et al., Case No. 4:24-cv-00376, asserts claims under §§ 10(b) and 20(a) of the Securities Exchange Act of 1934 on behalf of a putative class of purchasers of the Company’s securities from May 8, 2019 through April 10, 2024. The Complaint alleges that certain of the Company’s disclosures about financial performance and certain other public statements during the putative class period were materially false or misleading. The Company plans to vigorously defend against the lawsuit.

Pursuant to the Company’s governing documents and indemnification agreements with the named defendants, the Company has agreed to indemnify those defendants for all expenses and losses related to the litigation subject to the terms of those indemnification agreements. The outcome of litigation of this type is inherently uncertain, and there is always the possibility that a court rules in a manner that is adverse to the interests of the Company and the individual defendants. However, the amount of any such loss in that scenario cannot be reasonably estimated at this time. Further, management cannot reasonably estimate whether an outcome on the class action will be resolved in the near term.

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

Note 6—Policy Liabilities

The liability for future policy benefits is determined based on the net level premium method, which requires the liability be calculated as the present value of estimated future policyholder benefits and the related termination expenses, less the present value of estimated future net premiums to be collected from policyholders. The following tables summarize balances and changes in the net liability for future policy benefits, before reinsurance, for traditional life long-duration contracts for the three month periods ended March 31, 2024 and 2023:

Life

Present value of expected future net premiums

American Income

DTC

Liberty National

Other

Total

Balance at January 1, 2023

$

4,273,156

$

5,910,224

$

1,094,407

$

470,741

$

11,748,528

Beginning balance at original discount rates

4,246,723

5,680,864

1,066,123

449,209

11,442,919

Effect of changes in assumptions on future cash flows

—

—

—

—

—

Effect of actual variances from expected experience

(29,981)

(47,988)

(5,590)

(1,886)

(85,445)

Adjusted balance at January 1, 2023

4,216,742

5,632,876

1,060,533

447,323

11,357,474

Issuances(1)

192,555

168,952

30,142

7,241

398,890

Interest accrual(2)

47,898

70,991

13,288

5,670

137,847

Net premiums collected(3)

(127,239)

(153,919)

(33,188)

(11,557)

(325,903)

Effect of changes in the foreign exchange rate

(3,999)

—

—

—

(3,999)

Ending balance at original discount rates

4,325,957

5,718,900

1,070,775

448,677

11,564,309

Effect of change from original to current discount rates

141,680

391,650

57,308

34,379

625,017

Balance at March 31, 2023

$

4,467,637

$

6,110,550

$

1,128,083

$

483,056

$

12,189,326

Balance at January 1, 2024

$

4,681,888

$

6,052,651

$

1,129,716

$

478,052

$

12,342,307

Beginning balance at original discount rates

4,523,329

5,664,259

1,077,831

443,949

11,709,368

Effect of changes in assumptions on future cash flows

—

—

—

—

—

Effect of actual variances from expected experience

(48,248)

(36,229)

(10,448)

(1,851)

(96,776)

Adjusted balance at January 1, 2024

4,475,081

5,628,030

1,067,383

442,098

11,612,592

Issuances(1)

211,847

149,231

26,164

5,931

393,173

Interest accrual(2)

53,823

73,420

13,839

5,764

146,846

Net premiums collected(3)

(135,686)

(152,631)

(33,901)

(11,401)

(333,619)

Effect of changes in the foreign exchange rate

(8,927)

—

—

—

(8,927)

Ending balance at original discount rates

4,596,138

5,698,050

1,073,485

442,392

11,810,065

Effect of change from original to current discount rates

56,533

247,209

28,724

21,777

354,243

Balance at March 31, 2024

$

4,652,671

$

5,945,259

$

1,102,209

$

464,169

$

12,164,308

(1)Issuances represent the present value, using the original discount rate, of the expected net premiums related to new policies issued during each respective period.

(2)The interest accrual is the interest earned on the beginning present value of the expected net premiums, as well as the interest on actual net premiums earned during the period, using the original interest rate.

(3)Net premiums collected represent the product of the current period net premium ratio and the gross premiums collected during the period on the in-force business.

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

Life

Present value of expected future policy benefits

American Income

DTC

Liberty National

Other

Total

Balance at January 1, 2023

$

9,119,104

$

9,225,451

$

3,429,256

$

3,976,150

$

25,749,961

Beginning balance at original discount rates

8,409,761

8,477,892

3,272,980

3,403,704

23,564,337

Effect of changes in assumptions on future cash flows

—

—

—

—

—

Effect of actual variances from expected experience

(31,526)

(48,947)

(7,054)

(2,896)

(90,423)

Adjusted balance at January 1, 2023

8,378,235

8,428,945

3,265,926

3,400,808

23,473,914

Issuances(1)

192,555

168,952

30,142

7,241

398,890

Interest accrual(2)

109,329

112,768

43,256

50,378

315,731

Benefit payments(3)

(96,674)

(147,061)

(54,730)

(30,892)

(329,357)

Effect of changes in the foreign exchange rate

(9,711)

—

—

—

(9,711)

Ending balance at original discount rates

8,573,734

8,563,604

3,284,594

3,427,535

23,849,467

Effect of change from original to current discount rates

1,063,729

1,061,076

274,418

738,992

3,138,215

Balance at March 31, 2023

$

9,637,463

$

9,624,680

$

3,559,012

$

4,166,527

$

26,987,682

Balance at January 1, 2024

$

10,163,627

$

9,714,516

$

3,605,392

$

4,239,623

$

27,723,158

Beginning balance at original discount rates

9,061,833

8,656,752

3,338,252

3,506,859

24,563,696

Effect of changes in assumptions on future cash flows

—

—

—

—

—

Effect of actual variances from expected experience

(52,221)

(36,444)

(10,449)

(2,867)

(101,981)

Adjusted balance at January 1, 2024

9,009,612

8,620,308

3,327,803

3,503,992

24,461,715

Issuances(1)

211,847

149,231

26,164

5,931

393,173

Interest accrual(2)

120,201

117,925

44,554

52,136

334,816

Benefit payments(3)

(104,758)

(159,061)

(58,109)

(34,177)

(356,105)

Effect of changes in the foreign exchange rate

(20,637)

—

—

—

(20,637)

Ending balance at original discount rates

9,216,265

8,728,403

3,340,412

3,527,882

24,812,962

Effect of change from original to current discount rates

741,828

771,812

159,330

576,010

2,248,980

Balance at March 31, 2024

$

9,958,093

$

9,500,215

$

3,499,742

$

4,103,892

$

27,061,942

(1)Issuances represent the present value, using the original discount rate, of the expected future policy benefits related to new policies issued during each respective period.

(2)The interest accrual is the interest earned on the beginning present value of the expected future policy benefits, as well as the interest on actual benefits and expenses paid during the period, using the original interest rate.

(3)Benefit payments represent the release of the present value, using the original discount rate, of the actual future policy benefits incurred during the period due to death, lapse, and maturity benefit payments based on the revised expected assumptions.

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

The following tables summarize balances and changes in the net liability for future policy benefits for long-duration health contracts for the three month periods ended March 31, 2024 and 2023:

Health

Present value of expected future net premiums

United American

Family Heritage

Liberty National

American Income

DTC

Total

Balance at January 1, 2023

$

2,908,501

$

1,594,992

$

423,490

$

190,296

$

90,143

$

5,207,422

Beginning balance at original discount rates

2,941,261

1,729,219

415,442

192,631

87,751

5,366,304

Effect of changes in assumptions on future cash flows

—

—

—

—

—

—

Effect of actual variances from expected experience

(34,132)

(18,758)

(16,585)

(1,621)

(2,573)

(73,669)

Adjusted balance at January 1, 2023

2,907,129

1,710,461

398,857

191,010

85,178

5,292,635

Issuances(1)

75,839

67,787

13,303

10,212

2,392

169,533

Interest accrual(2)

31,587

16,199

4,890

2,036

1,057

55,769

Net premiums collected(3)

(65,914)

(43,979)

(12,403)

(5,424)

(2,661)

(130,381)

Effect of changes in the foreign exchange rate

—

—

—

(388)

—

(388)

Ending balance at original discount rates

2,948,641

1,750,468

404,647

197,446

85,966

5,387,168

Effect of change from original to current discount rates

49,082

(86,054)

16,800

3,220

4,277

(12,675)

Balance at March 31, 2023

$

2,997,723

$

1,664,414

$

421,447

$

200,666

$

90,243

$

5,374,493

Balance at January 1, 2024

$

3,697,771

$

1,711,741

$

358,472

$

206,381

$

115,363

$

6,089,728

Beginning balance at original discount rates

3,625,803

1,783,173

348,570

201,869

109,880

6,069,295

Effect of changes in assumptions on future cash flows

—

—

—

—

—

—

Effect of actual variances from expected experience

(40,531)

(17,092)

(11,410)

(3,550)

(2,316)

(74,899)

Adjusted balance at January 1, 2024

3,585,272

1,766,081

337,160

198,319

107,564

5,994,396

Issuances(1)

104,603

64,008

13,558

9,949

4,609

196,727

Interest accrual(2)

41,822

18,103

4,227

2,283

1,368

67,803

Net premiums collected(3)

(70,249)

(46,400)

(12,780)

(5,839)

(2,678)

(137,946)

Effect of changes in the foreign exchange rate

—

—

—

(862)

—

(862)

Ending balance at original discount rates

3,661,448

1,801,792

342,165

203,850

110,863

6,120,118

Effect of change from original to current discount rates

(8,053)

(107,766)

3,276

(55)

3,016

(109,582)

Balance at March 31, 2024

$

3,653,395

$

1,694,026

$

345,441

$

203,795

$

113,879

$

6,010,536

(1)Issuances represent the present value, using the original discount rate, of the expected net premiums related to new policies issued during each respective period.

(2)The interest accrual is the interest earned on the beginning present value of the expected net premiums, as well as the interest on actual net premiums earned during the period, using the original interest rate.

(3)Net premiums collected represent the product of the current period net premium ratio and the gross premiums collected during the period on the in-force business.

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

Health

Present value of expected future policy benefits

United American

Family Heritage

Liberty National

American Income

DTC

Total

Balance at January 1, 2023

$

3,046,829

$

3,005,664

$

941,574

$

312,750

$

87,532

$

7,394,349

Beginning balance at original discount rates

3,080,633

3,336,344

904,865

303,713

85,212

7,710,767

Effect of changes in assumptions on future cash flows

—

—

—

—

—

—

Effect of actual variances from expected experience

(31,443)

(19,779)

(15,995)

(1,578)

(2,302)

(71,097)

Adjusted balance at January 1, 2023

3,049,190

3,316,565

888,870

302,135

82,910

7,639,670

Issuances(1)

75,683

67,787

13,285

10,212

2,388

169,355

Interest accrual(2)

33,480

32,289

11,840

3,668

1,057

82,334

Benefit payments(3)

(78,563)

(29,261)

(23,976)

(7,137)

(3,354)

(142,291)

Effect of changes in the foreign exchange rate

—

—

—

(708)

—

(708)

Ending balance at original discount rates

3,079,790

3,387,380

890,019

308,170

83,001

7,748,360

Effect of change from original to current discount rates

52,672

(212,708)

59,977

18,363

4,089

(77,607)

Balance at March 31, 2023

$

3,132,462

$

3,174,672

$

949,996

$

326,533

$

87,090

$

7,670,753

Balance at January 1, 2024

$

3,814,328

$

3,315,880

$

865,808

$

335,504

$

109,482

$

8,441,002

Beginning balance at original discount rates

3,741,530

3,506,689

816,819

315,431

104,501

8,484,970

Effect of changes in assumptions on future cash flows

—

—

—

—

—

—

Effect of actual variances from expected experience

(40,325)

(19,049)

(12,821)

(4,002)

(2,321)

(78,518)

Adjusted balance at January 1, 2024

3,701,205

3,487,640

803,998

311,429

102,180

8,406,452

Issuances(1)

104,431

64,008

13,349

9,949

4,598

196,335

Interest accrual(2)

43,444

35,663

10,833

3,937

1,368

95,245

Benefit payments(3)

(82,085)

(33,037)

(23,864)

(6,402)

(3,096)

(148,484)

Effect of changes in the foreign exchange rate

—

—

—

(1,548)

—

(1,548)

Ending balance at original discount rates

3,766,995

3,554,274

804,316

317,365

105,050

8,548,000

Effect of change from original to current discount rates

(10,461)

(282,670)

29,690

11,418

2,725

(249,298)

Balance at March 31, 2024

$

3,756,534

$

3,271,604

$

834,006

$

328,783

$

107,775

$

8,298,702

(1)Issuances represent the present value, using the original discount rate, of the expected future policy benefits related to new policies issued during each respective period.

(2)The interest accrual is the interest earned on the beginning present value of the expected future policy benefits, as well as the interest on actual benefits and expenses paid during the period, using the original interest rate.

(3)Benefit payments represent the release of the present value, using the original discount rate, of the actual future policy benefits incurred during the period due to death, lapse, and maturity benefit payments based on the revised expected assumptions.

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

Health(2)

Net liability for future policy benefits as of March 31, 2023

United American

Family Heritage

Liberty National

American Income

Direct to Consumer

Total

Net liability for future policy benefits at original discount rates

$

131,149

$

1,636,912

$

485,372

$

110,724

$

(2,965)

$

2,361,192

Effect of changes in discount rate assumptions

3,590

(126,654)

43,177

15,143

(188)

(64,932)

Other Adjustments(1)

5,380

490

5,776

333

4,162

16,141

Net liability for future policy benefits, after other adjustments, at current discount rates

140,119

1,510,748

534,325

126,200

1,009

2,312,401

Reinsurance recoverable

(3,609)

(9,852)

(1,428)

—

—

(14,889)

Net liability for future policy benefits, after reinsurance recoverable, at current discount rates

$

136,510

$

1,500,896

$

532,897

$

126,200

$

1,009

$

2,297,512

(1)Other adjustments include the effects of capping and flooring the liability.

(2)Includes the immaterial error correction noted below.

Health

Net liability for future policy benefits as of March 31, 2024

United American

Family Heritage

Liberty National

American Income

Direct to Consumer

Total

Net liability for future policy benefits at original discount rates

105,547

1,752,482

462,151

113,515

(5,813)

2,427,882

Effect of changes in discount rate assumptions

(2,408)

(174,904)

26,414

11,473

(291)

(139,716)

Other Adjustments(1)

14,449

444

11,254

749

6,838

33,734

Net liability for future policy benefits, after other adjustments, at current discount rates

117,588

1,578,022

499,819

125,737

734

2,321,900

Reinsurance recoverable

(3,096)

(10,577)

(1,224)

—

—

(14,897)

Net liability for future policy benefits, after reinsurance recoverable, at current discount rates

$

114,492

$

1,567,445

$

498,595

$

125,737

$

734

$

2,307,003

(1)Other adjustments include the effects of capping and flooring the liability.

Immaterial Correction of Previously Issued Financial Statements—The Company previously presented reinsurance recoverable on a net basis as a component of future policy benefits. In the fourth quarter of 2023, the Company corrected its presentation of reinsurance recoverable to a gross basis as a component of other assets, which resulted in the reclassification of $60 million of reinsurance recoverable at current discount rates from liabilities to assets ($49 million at original discount rates) as of March 31, 2023, with no change to equity, and the related tables in the footnote have been adjusted to reflect such changes.

Remeasurement Gain or Loss—During the three months ended March 31, 2024 and 2023, the Company's results for actual variances from expected experience produced a net reserve remeasurement gain of $8.1 million and a net reserve remeasurement gain of $659 thousand, respectively, in the Condensed Consolidated Statements of Operations. The variance of actual experience from expected experience during the first three months of 2024 was primarily due to favorable variances from our assumptions as compared to actual experience in our life insurance segment (a $4.9 million gain), and favorable variances from our assumptions as compared to actual experience in our health insurance segment (a $3.2 million gain). The variance of actual experience from expected experience during the three months ended 2023 was primarily due to favorable variances from assumptions as compared to actual experience in our life insurance segment (a $2.7 million gain), and unfavorable variances from assumptions as compared to actual experience in our health insurance segment (a $2.0 million loss).

There were no changes to the judgments, assumptions, and methods used in measuring the liability for future policy benefits during the three months ended March 31, 2024 and 2023.

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

The following tables provide the weighted-average original and current discount rates for the liability for future policy benefits and the additional insurance liabilities as of March 31, 2024 and 2023:

As of March 31,

2024

2023

Original discount rate

Current discount rate

Original discount rate

Current discount rate

Life

American Income

5.7

%

5.2

%

5.8

%

4.9

%

Direct to Consumer

6.0

%

5.2

%

6.0

%

5.0

%

Liberty National

5.6

%

5.2

%

5.6

%

5.0

%

Other

6.2

%

5.2

%

6.2

%

5.0

%

Health

United American

5.1

%

5.0

%

5.2

%

4.8

%

Family Heritage

4.2

%

5.1

%

4.3

%

4.9

%

Liberty National

5.8

%

5.2

%

5.8

%

4.9

%

American Income

5.8

%

5.0

%

5.9

%

4.8

%

Direct to Consumer

5.1

%

5.0

%

5.2

%

4.8

%

The following table provides the weighted-average durations of the liability for future policy benefits and the additional insurance liabilities as of March 31, 2024 and 2023:

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

The following tables summarize the amount of gross premiums and interest related to long duration life and health contracts that are recognized in the Condensed Consolidated Statements of Operationsfor the three month periods ended March 31, 2024 and 2023:

Life

Three Months Ended March 31, 2024

Three Months Ended March 31, 2023

Gross Premiums

Interest expense

Gross Premiums

Interest expense

American Income

$

413,759

$

66,379

$

387,145

$

61,431

Direct to Consumer

245,194

44,460

244,707

41,714

Liberty National

89,871

30,542

84,072

29,769

Other

51,069

45,917

51,835

44,275

Total

$

799,893

$

187,298

$

767,759

$

177,189

Health

Three Months Ended March 31, 2024

Three Months Ended March 31, 2023

Gross Premiums

Interest expense

Gross Premiums

Interest expense

United American

$

104,097

$

1,567

$

97,833

$

1,822

Family Heritage

103,391

17,431

96,090

15,977

Liberty National

47,434

6,583

46,745

6,920

American Income

28,919

1,655

28,096

1,632

Direct to Consumer

3,657

—

3,542

—

Total

$

287,498

$

27,236

$

272,306

$

26,351

Gross premiums are included within life and health premium on the Condensed Consolidated Statements of Operations, while the related interest expense is included in life and health policyholder benefits.

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

The following tables provide the undiscounted and discounted expected future net premiums, expected future gross premiums, and expected future policy benefits, at both original and current discount rates, for life and health contracts as of March 31, 2024 and 2023:

Life

As of March 31, 2024

As of March 31, 2023

Not discounted

At original discount rates

At current discount rates

Not discounted

At original discount rates

At current discount rates

American Income

PV of expected future gross premiums

$

24,668,992

$

13,924,819

$

14,181,177

$

23,041,514

$

13,054,486

$

13,575,751

PV of expected future net premiums

8,131,005

4,596,138

4,652,671

7,617,532

4,325,957

4,467,637

PV of expected future policy benefits

31,114,756

9,216,265

9,958,093

28,821,998

8,573,734

9,637,463

DTC

PV of expected future gross premiums

$

17,617,001

$

9,214,360

$

9,597,417

$

17,479,516

$

9,165,113

$

9,773,835

PV of expected future net premiums

10,831,408

5,698,050

5,945,259

10,832,386

5,718,900

6,110,550

PV of expected future policy benefits

25,909,464

8,728,403

9,500,215

25,582,750

8,563,604

9,624,680

Liberty National

PV of expected future gross premiums

$

4,667,397

$

2,725,502

$

2,739,275

$

4,453,139

$

2,599,082

$

2,667,795

PV of expected future net premiums

1,888,084

1,073,485

1,102,209

1,889,419

1,070,775

1,128,083

PV of expected future policy benefits

8,916,134

3,340,412

3,499,742

8,658,766

3,284,594

3,559,012

Other

PV of expected future gross premiums

$

3,701,248

$

1,879,815

$

2,027,187

$

3,798,669

$

1,920,302

$

2,126,949

PV of expected future net premiums

906,921

442,392

464,169

919,924

448,677

483,056

PV of expected future policy benefits

12,437,133

3,527,882

4,103,892

12,392,224

3,427,535

4,166,527

Total

PV of expected future gross premiums

$

50,654,638

$

27,744,496

$

28,545,056

$

48,772,838

$

26,738,983

$

28,144,330

PV of expected future net premiums

21,757,418

11,810,065

12,164,308

21,259,261

11,564,309

12,189,326

PV of expected future policy benefits

78,377,487

24,812,962

27,061,942

75,455,738

23,849,467

26,987,682

As of March 31, 2024, for the life segment using current discount rates, the Company anticipates $28.5 billion of expected future gross premiums and $12.2 billion of expected future net premiums. As of March 31, 2023, using current discount rates, the Company anticipated $28.1 billion of expected future gross premiums and $12.2 billion in expected future net premiums. For each respective period, only expected future net premiums are included in the determination of the liability for future policy benefits on the balance sheet, while the difference between the expected future gross premiums and the expected future net premiums is not.

Notes to Condensed Consolidated Financial Statements

(Dollar amounts in thousands, except per share data)

Health

As of March 31, 2024

As of March 31, 2023

Not discounted

At original discount rates

At current discount rates

Not discounted

At original discount rates

At current discount rates

United American

PV of expected future gross premiums

$

8,757,778

$

5,349,917

$

5,334,881

$

6,783,819

$

4,279,547

$

4,346,007

PV of expected future net premiums

6,002,434

3,661,448

3,653,395

4,685,306

2,948,641

2,997,723

PV of expected future policy benefits

6,186,167

3,766,995

3,756,534

4,909,212

3,079,790

3,132,462

Family Heritage

PV of expected future gross premiums

$

6,854,106

$

4,037,762

$

3,816,256

$

6,442,316

$

3,846,392

$

3,682,300

PV of expected future net premiums

3,039,406

1,801,792

1,694,026

2,908,079

1,750,468

1,664,414

PV of expected future policy benefits

6,769,500

3,554,274

3,271,604

6,358,594

3,387,380

3,174,672

Liberty National

PV of expected future gross premiums

$

2,073,015

$

1,315,879

$

1,353,262

$

2,232,290

$

1,396,334

$

1,468,763

PV of expected future net premiums

509,069

342,165

345,441

634,061

404,647

421,447

PV of expected future policy benefits

1,395,561

804,316

834,006

1,575,745

890,019

949,996

American Income

PV of expected future gross premiums

$

1,768,477

$

991,946

$

1,024,262

$

1,760,671

$

984,216

$

1,037,339

PV of expected future net premiums

362,982

203,850

203,795

351,655

197,446

200,666

PV of expected future policy benefits

644,293

317,365

328,783

626,151

308,170

326,533

Direct to Consumer

PV of expected future gross premiums

$

238,499

$

150,065

$

154,223

$

171,266

$

112,442

$

118,105

PV of expected future net premiums

176,500

110,863

113,879

131,187

85,966

90,243

PV of expected future policy benefits

164,347

105,050

107,775

124,597

83,001

87,090

Total

PV of expected future gross premiums

$

19,691,875

$

11,845,569

$

11,682,884

$

17,390,362

$

10,618,931

$

10,652,514

PV of expected future net premiums

10,090,391

6,120,118

6,010,536

8,710,288

5,387,168

5,374,493

PV of expected future policy benefits

15,159,868

8,548,000

8,298,702

13,594,299

7,748,360

7,670,753