☑ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the Quarterly Period Ended September 30, 2024

OR

☐TRANSITION REPORT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the Transition Period From __________ to __________

Commission File Number: 1-09720

PAR TECHNOLOGY CORPORATION

(Exact name of registrant as specified in its charter)

Delaware

16-1434688

(State or other jurisdiction of incorporation or organization)

(I.R.S. Employer Identification No.)

PAR Technology Park, 8383 Seneca Turnpike, New Hartford, New York13413-4991

(Address of principal executive offices, including zip code)

(315) 738-0600

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class

Trading Symbol

Name of each exchange on which registered

Common Stock, $0.02 par value

PAR

New York Stock Exchange

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company”, and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer ☑

Accelerated Filer ☐

Non-Accelerated Filer ☐

Smaller Reporting Company ☐

Emerging Growth Company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☑

As of November 7, 2024, 36,305,087 shares of the registrant’s common stock, $0.02 par value, were outstanding.

“PAR®,” “PAR POS®” (formerly “Brink POS®”), “Punchh®,” “PAR OrderingTM” (formerly “MENUTM”), “Data Central®,” "Open Commerce®,” "PAR® Pay”, “PAR® Payment Services”, "StuzoTM," "PAR RetailTM," and other trademarks identifying our products and services appearing in this Quarterly Report belong to us. This Quarterly Report may also contain trade names and trademarks of other companies. Our use of such other companies’ trade

names or trademarks is not intended to imply any endorsement or sponsorship by these companies of us or our products or services.

Unless the context indicates otherwise, references in this Quarterly Report to "we," "us," "our," the "Company," and "PAR" mean PAR Technology Corporation and its consolidated subsidiaries.

FORWARD-LOOKING STATEMENTS

This Quarterly Report contains “forward-looking statements” within the meaning of Section 21E of the Securities and Exchange Act of 1934, as amended (the “Exchange Act”), Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and the Private Securities Litigation Reform Act of 1995. Forward-looking statements are not historical in nature, but rather are predictive of PAR's future operations, financial condition, financial results, business strategies and prospects. Forward-looking statements are generally identified by words such as “believe,” “could”, “continue,” “expect,” “estimate,” “future”, “may,” “will,” “would,” and similar expressions.

Forward-looking statements are based on management's current expectations and assumptions and are inherently uncertain. Actual results and outcomes could differ materially from those expressed in or implied by forward-looking statements, including statements relating to and PAR's expectations regarding:

•the plans, strategies and objectives of management for future operations, including PAR’s service and product offerings, its go-to-market strategies and the expected development, demand, performance, market share, or competitive performance of its products and services;

•PAR's ability to achieve and sustain profitability;

•projections of net revenue, margins, expenses, cash flows, or other financial items;

•PAR's annual recurring revenue, active sites, subscription service margins, net loss, net loss per share, and other key performance indicators and non-GAAP financial measures;

•PAR's expectations about the availability and terms of product and component supplies for our hardware;

•the timing and expected benefits of acquisitions, divestitures, and capital markets transactions;

•PAR’s human capital strategies and engagement;

•current or future macroeconomic trends or geopolitical events and the impact of those trends and events on PAR and its business, financial condition, and results of operations;

•claims, disputes, or other litigation matters; and

•assumptions underlying any of the foregoing.

Factors, risks, trends, and uncertainties that could cause PAR’s actual results to differ materially from those expressed in or implied by forward-looking statements include:

•PAR's ability to successfully develop or acquire and transition new products and services and enhance existing products and services to meet evolving customer needs and respond to emerging technological trends, including artificial intelligence;

•PAR's ability to add and maintain active sites, retain and manage suppliers, secure alternative suppliers, and manage inventory levels, navigate manufacturing disruptions or logistics challenges, shipping delays and shipping costs;

•the effects, costs and timing of acquisitions, divestitures, and capital markets transactions;

•PAR's ability to integrate acquisitions into its operations and the timing, complexity and costs associated with integrations, including the acquisitions of Stuzo Holdings, LLC and TASK Group Holdings Limited;

•macroeconomic trends, such as a recession or slowed economic growth, fluctuating interest rates, inflation, and changes in consumer confidence and discretionary spending;

•geopolitical events, such as effects of the Russia-Ukraine war, tensions with China and between China and Taiwan, hostilities in the Middle East, including the Israel conflict(s), and uncertainty relating to the U.S. presidential transition and the Trump administration's policies and regulations, including potential changes to trade agreements or tariffs;

•PAR's ability to successfully attract, develop and retain necessary qualified employees to develop and expand its business, execute product installations and respond to customer service level needs;

•the protection of PAR's intellectual property;

•PAR's ability to retain and add integration partners, and its success in acquiring and developing relevant technology for current, new, and potential customers for its service and product offerings;

•risks associated with PAR's international operations;

•PAR’s ability to generate sufficient cash flow or access additional financing sources as needed to repay its outstanding debts, including amounts owed under its outstanding convertible notes and credit facility;

•the effects of global pandemics, such as COVID-19 or other public health crises;

•changes in estimates and assumptions PAR makes in connection with the preparation of its financial statements, or in building its business and operational plans and in executing PAR's strategies;

•disruptions in operations from data breaches and cyberattacks, including heightened risks due to the rapid development and adoption of artificial intelligence technologies globally;

•PAR's ability to maintain proper and effective internal control over financial reporting;

•PAR's ability to execute its business, operational plans, and strategies and manage its business continuity risks, including disruptions or delays in product assembly and fulfillment;

•potential impacts, liabilities and costs from pending or potential investigations, claims and disputes; and

•other factors, risks, trends and uncertainties disclosed in our filings with the Securities and Exchange Commission ("SEC"), particularly those listed under the heading "Risk Factors" in our Annual Report on Form 10-K for the fiscal year ended December 31, 2023, in our Quarterly Report for the quarter ended March 31, 2024, and in this Quarterly Report.

Given these risks and uncertainties, readers are cautioned not to place undue reliance on forward-looking statements. We undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events, or otherwise, except as may be required under applicable securities law.

Preferred stock, $0.02 par value, 1,000,000 shares authorized

—

—

Common stock, $0.02 par value, 116,000,000 shares authorized, 37,773,764 and 29,386,234 shares issued, 36,303,459 and 28,029,915 outstanding at September 30, 2024 and December 31, 2023, respectively

749

584

Additional paid in capital

972,811

625,154

Accumulated deficit

(258,886)

(274,956)

Accumulated other comprehensive loss

(118)

(939)

Treasury stock, at cost, 1,470,305 shares and 1,356,319 shares at September 30, 2024 and December 31, 2023, respectively

(21,849)

(16,778)

Total shareholders’ equity

692,707

333,065

Total Liabilities and Shareholders’ Equity

$

1,299,274

$

802,606

See accompanying notes to unaudited interim condensed consolidated financial statements

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (Continued)

(In thousands)

(unaudited)

Nine Months Ended September 30,

2024

2023

Effect of exchange rate changes on cash and cash equivalents

933

(508)

Net increase (decrease) in cash and cash equivalents and cash held on behalf of customers

73,531

(25,639)

Cash and cash equivalents and cash held on behalf of customers at beginning of period

47,539

77,533

Cash and cash equivalents and cash held on behalf of customers at end of period

$

121,070

$

51,894

Reconciliation of cash and cash equivalents and cash held on behalf of customers

Cash and cash equivalents

$

105,804

$

43,136

Cash held on behalf of customers

15,266

8,758

Total cash and cash equivalents and cash held on behalf of customers

$

121,070

$

51,894

Supplemental disclosures of cash flow information:

Cash paid for interest

$

3,713

$

4,022

Cash paid for income taxes

1,543

2,392

Capitalized software recorded in accounts payable

36

468

Capital expenditures in accounts payable

62

98

Common stock issued for acquisition

133,181

—

Cash flows are presented on a consolidated basis and include $0.2 million of cash and cash equivalents presented in current assets of discontinued operations in the condensed consolidated balance sheets as of December 31, 2023. Refer to “Note 4 – Discontinued Operations” for additional information related to cash flows from discontinued operations.

See accompanying notes to unaudited interim condensed consolidated financial statements

NOTES TO INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

Note 1 — Summary of Significant Accounting Policies

Nature of Business

PAR Technology Corporation (the “Company” or “PAR,” “we,” or “us”), through its consolidated subsidiaries, operates in one segment, Restaurant/Retail. We report aggregate financial information on a consolidated basis to our Chief Executive Officer, who is the Company’s chief operating decision maker. The Restaurant/Retail segment provides leading omnichannel cloud-based software and hardware solutions to the restaurant and retail industries.

Our product and service offerings include point-of-sale, customer engagement and loyalty, digital ordering and delivery, operational intelligence technologies, payment processing, hardware, and related technologies, solutions, and services. We provide enterprise restaurants, franchisees, and other foodservice outlets with operational efficiencies through a data-driven network with integration capabilities from point-of-sale to the kitchen, to fulfillment. Our subscription services are grouped into two product lines: Engagement Cloud, which includes Punchh and PAR Retail (formerly Stuzo) products and services for customer loyalty and engagement, Plexure for international customer loyalty and engagement, and PAR Ordering (formerly MENU) for omnichannel digital ordering and delivery; and Operator Cloud, which includes PAR POS (formerly Brink POS) and TASK for front-of-house, PAR Payment Services and PAR Pay for payments, and Data Central for back-of-house. The accompanying consolidated financial statements include the Company's accounts and those of its consolidated subsidiaries. All intercompany transactions have been eliminated in consolidation.

Basis of Presentation

The accompanying financial statements of PAR Technology Corporation and its consolidated subsidiaries have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”) for interim financial statements and the instructions to Form 10-Q and Regulation S-X pertaining to interim financial statements as promulgated by the SEC. In the opinion of management, the Company's financial statements include all normal and recurring adjustments necessary in order to make the financial statements not misleading and to provide a fair presentation of the Company's financial results for the interim period included in this Quarterly Report. Interim results are not necessarily indicative of results for the full year or any future periods. The information included in this Quarterly Report should be read in conjunction with the Company's audited consolidated financial statements and notes thereto included in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2023 (the “2023 Annual Report”).

The results of operations of the Company's Government segment are reported as discontinued operations in the condensed consolidated statements of operations for all periods presented and the related assets and liabilities associated with the discontinued operations are classified as assets and liabilities of discontinued operations in the condensed consolidated balance sheet as of December 31, 2023. All results and information in the condensed consolidated financial statements are presented as continuing operations and exclude the Government segment unless otherwise noted specifically as discontinued operations.

Use of Estimates

The preparation of the financial statements requires management of the Company to make a number of estimates and assumptions relating to the reported amount of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the period. Significant items subject to these estimates and assumptions include revenue recognition, stock-based compensation, the recognition and measurement of assets acquired and liabilities assumed in business combinations at fair value, the carrying amount of property, plant, and equipment including right-to-use assets and liabilities, identifiable intangible assets and goodwill, valuation allowances for receivables, valuation of excess and obsolete inventories, and measurement of contingent consideration at fair value. Actual results could differ from those estimates.

Cash and Cash Equivalents and Cash Held on Behalf of Customers

Cash and cash equivalents and cash held on behalf of customers consist of the following:

(in thousands)

September 30, 2024

December 31, 2023

Cash and cash equivalents

Cash

$

103,643

$

37,143

Money market funds

2,161

40

Cash held on behalf of customers

15,266

10,170

Total cash and cash equivalents and cash held on behalf of customers

$

121,070

$

47,353

The Company maintained bank balances that, at times, exceeded the federally insured limit during the nine months ended September 30, 2024. The Company did not experience losses relating to these deposits and management does not believe that the Company is exposed to any significant credit risk with respect to these amounts.

Short-Term Investments

The carrying value of investment securities consist of the following:

(in thousands)

September 30, 2024

December 31, 2023

Short-term investments

Treasury bills and notes

$

11,985

$

37,194

Short-term deposits

593

—

Total short-term investments

$

12,578

$

37,194

The Company did not have any material gains or losses on these securities during the nine months ended September 30, 2024. The estimated fair value of these securities approximated their carrying value as of September 30, 2024 and December 31, 2023.

Discontinued Operations

In determining whether a group of assets disposed of (or is to be disposed of) should be presented as a discontinued operation, the Company analyzes whether the group of assets disposed of represented a component of the entity; that is, whether it had historic operations and cash flows that were discrete both operationally and for financial reporting purposes. In addition, the Company considers whether the disposal represents a strategic shift that has or will have a major effect on the Company’s operations and financial results.

The assets and liabilities of a discontinued operation, other than goodwill, are measured at the lower of carrying amount or fair value, less cost to sell. When a portion of a reporting unit that constitutes a business is to be disposed of, the goodwill associated with that business is included in the carrying amount of the business based on the relative fair values of the business to be disposed of and the portion of the reporting unit that will be retained. Interest is allocated to discontinued operations if the interest is directly attributable to the discontinued operations or is interest on debt that is required to be repaid as a result of the disposal.

Other Assets

Other assets include deferred implementation costs of $7.9 million and $8.8 million and deferred commissions of $3.6 million and $2.6 million at September 30, 2024 and December 31, 2023, respectively.

The following table summarizes amortization expense for deferred implementation costs and deferred commissions:

Three Months Ended September 30,

Nine Months Ended September 30,

(in thousands)

2024

2023

2024

2023

Amortization of deferred implementation costs

$

1,569

$

1,271

$

4,612

$

3,409

Amortization of deferred commissions

430

226

1,235

617

Other assets include the cash surrender value of life insurance related to the Company’s deferred compensation plan eligible to certain employees. The cash surrender value of the deferred compensation plan was cashed out during the three months ended September 30, 2024. The balance of the life insurance policies was zero and $3.3 million at September 30, 2024 and December 31, 2023, respectively.

Other Long-Term Liabilities

Other long-term liabilities include deferred tax liabilities of $22.7 million and $0.8 million at September 30, 2024 and December 31, 2023, respectively.

Other long-term liabilities include amounts owed to employees that participated in the Company’s deferred compensation plan. Amounts owed to employees who participated in the deferred compensation plan were $0.1 million and $0.4 million at September 30, 2024 and December 31, 2023, respectively.

Gain on Insurance Proceeds

During the nine months ended September 30, 2024, and 2023 the Company received $0.1 million and $0.5 million, respectively, of insurance proceeds in connection with the settlement of legacy claims.

Related Party Transactions

During the nine months ended September 30, 2023, Ronald Shaich, the sole member of Act III Management LLC ("Act III Management"), served as a strategic advisor to the Company's board of directors pursuant to a strategic advisor agreement, which terminated on June 1, 2023. Keith Pascal, a director of the Company, is an employee of Act III Management and serves as its vice president and secretary. Mr. Pascal does not have an ownership interest in Act III Management.

As of September 30, 2024 and December 31, 2023, the Company had zero accounts payable owed to Act III Management. During the three months ended September 30, 2024 and 2023, the Company paid Act III Management zero and during the nine months ended September 30, 2024 and 2023 the Company paid Act III Management zero and $0.1 million, respectively, for services performed under the strategic advisor agreement.

In connection with the acquisition of TASK Group Holdings Limited (“TASK Group” and such acquisition, the "TASK Group Acquisition"), the Company leases an Australian office from the Houden Superannuation Fund. The trustees and beneficiaries of the Houden Superannuation Fund include two executives of TASK Group. The Australian office has been occupied by the TASK Group since 2005 with the last rent increase occurring in March 2021 based on an independent review of comparable market rent. During the three months ended September 30, 2024, the Company paid the Houden Superannuation Fund $0.1 million in rent. The Company had zero accounts payable owed to the Houden Superannuation Fund as of September 30, 2024.

Impairment of Long-Lived Assets

During the three months ended September 30, 2024, the Company recorded an impairment loss of $0.2 million included in general and administrative expense in the condensed consolidated statements of operations related to the discontinuance of the Brink POS trade name.

Recently Adopted Accounting Pronouncements

There were no recent accounting pronouncements or changes in accounting pronouncements during the nine months ended September 30, 2024 that are of significance or potential significance to the Company.

Most performance obligations greater than one year relate to service and support contracts that the Company expects to fulfill within 36 months. The Company expects to fulfill 100% of service and support contracts within 60 months.

The changes in deferred revenue, inclusive of both current and long-term, are as follows:

(in thousands)

2024

2023

Beginning balance - January 1

$

11,454

$

13,584

Acquired deferred revenue (Note 3)

12,391

—

Recognition of deferred revenue

(73,706)

(19,074)

Deferral of revenue

79,911

17,889

Impact of foreign currency translation on deferred revenue

460

—

Ending balance - September 30

$

30,510

$

12,399

The above tables exclude customer deposits of $1.7 million and $2.0 million as of the nine months ended September 30, 2024 and 2023, respectively. During the three months ended September 30, 2024 and 2023, the Company recognized revenue included in deferred revenue at the beginning of each respective period of $1.4 million and $2.7 million. During the nine months ended September 30, 2024 and 2023, the Company recognized revenue included in deferred revenue at the beginning of each respective period of $6.3 million and $8.7 million.

Disaggregated Revenue

The Company disaggregates revenue from contracts with customers by major product line because the Company believes it best depicts how the nature, amount, timing and uncertainty of revenue and cash flows are affected by contract terms and economic factors.

On July 18, 2024 (New York Time), July 19, 2024 (Sydney Time) (the "TASK Closing Date"), the Company completed its acquisition of TASK Group, pursuant to a court-approved scheme of arrangement. On the TASK Closing Date, the Company paid TASK Group's shareholders approximately $131.5 million in cash consideration, and issued 2,163,393 shares of common stock at a price of $52.70 per share of Company common stock, for a total purchase consideration of $245.5 million. The Company acquired TASK Group to expand its footprint in the international foodservice vertical with TASK Group's Australia-based global foodservice transaction platform that offers international unified commerce solutions and loyalty and engagement solutions.

The Company incurred acquisition expenses related to the TASK Group Acquisition of approximately $2.9 million which are included in general and administrative in the condensed consolidated statements of operations.

The TASK Group Acquisition was accounted for as a business combination in accordance with Accounting Standards Codification ("ASC") Topic 805, Business Combinations. Accordingly, assets acquired and liabilities assumed have been accounted for at their preliminarily determined respective fair values as of the TASK Closing Date. The fair value determinations were based on management's estimates and assumptions, with the assistance of independent valuation and tax consultants. Preliminary fair values are subject to measurement period adjustments within the permitted measurement period (up to one year from the TASK Closing Date) as management finalizes its procedures and net working capital adjustments (if any) are settled.

The following table presents management's preliminary purchase price allocation:

(in thousands)

Purchase price allocation

Cash

$

4,179

Short-term investments

562

Accounts receivable

7,105

Property and equipment

1,030

Lease right-of-use assets

3,418

Developed technology

32,100

Customer relationships

48,000

Trade names

1,800

Prepaid and other acquired assets

1,916

Goodwill

181,442

Total assets

281,552

Accounts payable

4,212

Accrued expenses

3,502

Lease right-of-use liabilities

3,397

Deferred revenue

4,710

Deferred taxes

20,263

Consideration paid

$

245,468

Intangible Assets

The Company identified three acquired intangible assets in the TASK Group Acquisition: developed technology; customer relationships; and trade names split across the TASK and Plexure product lines. The preliminary fair values of developed technology and customer relationship intangible assets were determined utilizing the “multi-period excess earnings method”, which method is predicated upon the calculation of the net present value of after-tax net cash flows respectively attributable to each asset. The Company applied a seven-year economic life and discount rate of 12.5% in determining the Plexure developed technology and a seven-year economic life and discount rate of 14.0% in determining the TASK developed technology preliminary intangible fair values. The Company applied a 10.0% estimated annual attrition rate and a discount rate of 14.0% for the TASK customer relationships and applied a 95.0% probability of renewal factor and a discount rate of 12.5% for the

Plexure customer relationships intangible preliminary fair values. The preliminary fair value of trade names intangible was determined utilizing the “relief from royalty” approach, which is a form of the income approach that attributes savings recognized from not having to pay a royalty for the use of an asset. The Company applied a fair and reasonable royalty rate of 0.5% and a discount rate of 12.5% for the TASK trade name and a fair and reasonable royalty rate of 0.5% and a discount rate of 14.0% in determining the Plexure trade name intangible preliminary fair values. The estimated useful life of each of the foregoing identifiable intangible assets was preliminarily determined to be: seven years for developed technology; thirteen years for customer relationships; and eight years for the trade names.

Goodwill

Goodwill represents the excess of consideration transferred for the fair value of net identifiable assets acquired and is tested for impairment at least annually. The goodwill value represents expected synergies from the product acquired and other benefits. It is not deductible for income tax purposes.

Deferred Taxes

The Company determined the deferred tax position to be recorded at the time of the TASK Group Acquisition in accordance with ASC Topic 740, Income Taxes, resulting in recognition of $20.3 million in deferred tax liabilities for future reversal of taxable temporary differences primarily for intangible assets.

Stuzo Acquisition

On March 8, 2024, the Company acquired 100% of the outstanding equity interests of Stuzo Blocker, Inc., Stuzo Holdings, LLC and their subsidiaries (collectively, “Stuzo” and such acquisition, the “Stuzo Acquisition”), a digital engagement software provider to convenience and fuel retailers ("C-Stores"), for purchase consideration of approximately $170.5 million paid in cash (the "Cash Consideration"), subject to certain adjustments (including customary adjustments for Stuzo cash, debt, debt-like items, and net working capital), and $19.2 million paid in shares of Company common stock. 441,598 shares of common stock were issued as purchase consideration, determined using a fair value share price of $43.41. The Company acquired Stuzo to expand its footprint in the C-Stores market vertical with Stuzo's industry-leading guest engagement platform (PAR Retail) serving major brands in the space.

$1.5 million of the Cash Consideration was deposited into an escrow account administered by a third party to fund potential post-closing adjustments and obligations. During the three months ended September 30, 2024, the escrow account was released in full.

The Company incurred acquisition expenses related to the Stuzo Acquisition of approximately $2.9 million which are included in general and administrative in the condensed consolidated statements of operations.

The Stuzo Acquisition was accounted for as a business combination in accordance with ASC Topic 805, Business Combinations. Accordingly, assets acquired and liabilities assumed have been accounted for at their preliminarily determined respective fair values as of March 8, 2024, (the "Stuzo Acquisition Date"). The fair value determinations were based on management's estimates and assumptions, with the assistance of independent valuation and tax consultants. Preliminary fair values are subject to measurement period adjustments within the permitted measurement period (up to one year from the Stuzo Acquisition Date) as management finalizes its procedures and net working capital adjustments (if any) are settled.

During the three months ended September 30, 2024, preliminary fair values of assets and liabilities as of the Stuzo Acquisition Date were adjusted to reflect ongoing acquisition valuation analyses and net working capital adjustments. These adjustments included changes to accrued expenses and goodwill to reflect changes in underlying fair value assumptions. The Company is in the process of finalizing valuation assumptions for the intangibles and the sales tax liability exposure as of the Stuzo Acquisition Date.

The following table presents management's current purchase price allocation and the initial purchase price allocation:

(in thousands)

Current purchase price allocation

Initial purchase price allocation

Cash

$

4,244

$

4,244

Accounts receivable

1,262

2,208

Property and equipment

307

307

Developed technology

18,200

18,200

Customer relationships

39,400

39,000

Trademarks

5,400

6,600

Non-competition agreements

3,500

4,800

Prepaid and other acquired assets

774

774

Goodwill

136,602

132,140

Total assets

209,689

208,273

Accounts payable

317

317

Accrued expenses

4,053

4,459

Deferred revenue

7,680

5,443

Deferred taxes

7,934

8,349

Consideration paid

$

189,705

$

189,705

Intangible Assets

The Company identified four acquired intangible assets in the Stuzo Acquisition: developed technology; customer relationships; trademarks; and non-competition agreements. The preliminary fair values of developed technology and customer relationship intangible assets were determined utilizing the “multi-period excess earnings method”, which method is predicated upon the calculation of the net present value of after-tax net cash flows respectively attributable to each asset. The Company applied a seven-year economic life and discount rate of 12.5% in determining the Stuzo developed technology preliminary intangible fair value and applied a 7.0% estimated annual attrition rate and discount rate of 12.5% in determining the Stuzo customer relationships intangible preliminary fair value. The preliminary fair value of trademarks intangible was determined utilizing the “relief from royalty” approach, which is a form of the income approach that attributes savings recognized from not having to pay a royalty for the use of an asset. The Company applied a fair and reasonable royalty rate of 1.0% and discount rate of 12.5% in determining the trademarks intangible preliminary fair value. The preliminary fair value of the Stuzo non-competition agreements was determined utilizing the discounted earnings method. The estimated useful life of each of the foregoing identifiable intangible assets was preliminarily determined to be: seven years for developed technology; fifteen years for customer relationships related to SaaS platform and related support; five years for customer relationships related to managed platform development services; indefinite for the trademarks; and five years for the non-competition agreements.

Goodwill

Goodwill represents the excess of consideration transferred for the fair value of net identifiable assets acquired and is tested for impairment at least annually. The goodwill value represents expected synergies from the product acquired and other benefits. It is not deductible for income tax purposes.

Deferred Taxes

The Company determined the deferred tax position to be recorded at the time of the Stuzo Acquisition in accordance with ASC Topic 740, Income Taxes, resulting in recognition of $7.9 million in deferred tax liabilities for future reversal of taxable temporary differences primarily for intangible assets.

The net deferred tax liability relating to the Stuzo Acquisition was determined by the Company to provide future taxable temporary differences that allow for the Company to utilize certain previously fully reserved deferred

tax assets. Accordingly, the Company recognized a reduction to its valuation allowance resulting in a net tax benefit of $7.7 million for the nine months ended September 30, 2024.

Pro Forma Financial Information - unaudited

For the three and nine months ended September 30, 2024, the Stuzo Acquisition resulted in additional revenues of $10.7 million and $23.4 million, respectively, and income before income taxes of $1.6 million and $3.4 million, respectively; and the TASK Group Acquisition resulted in additional revenues of $9.6 million and $9.6 million, respectively, and loss before income taxes of $(0.1) million and $(0.1) million, respectively.

The following table summarizes the Company's unaudited pro forma results of operations for the three and nine months ended September 30, 2024 and 2023 as if the TASK Group Acquisition and Stuzo Acquisition had occurred on January 1, 2023:

Three Months Ended September 30,

Nine Months Ended September 30,

(in thousands)

2024

2023

2024

2023

Total revenue

$

98,999

$

90,968

$

279,094

$

273,100

Net loss from continuing operations

(29,862)

(19,642)

(82,960)

(51,922)

The unaudited pro forma results presented above are for illustrative purposes only and do not reflect the realization of actual cost savings or any related integration costs. The unaudited pro forma results do not purport to be indicative of the results that would have been obtained, or to be a projection of results that may be obtained in the future. These unaudited pro forma results include certain adjustments, primarily due to increases in amortization expense due to the fair value adjustments of intangible assets, acquisition related costs and the impact of income taxes on the pro forma adjustments. $5.4 million of acquisition costs have been reflected in the 2023 pro forma results.

Note 4 — Discontinued Operations

On June 7, 2024 (the “PGSC Closing Date”), the Company entered into a Stock Purchase Agreement (the “Purchase Agreement”) with Booz Allen Hamilton Inc. ("Booz Allen Hamilton") for the sale of PAR Government Systems Corporation ("PGSC"), a wholly owned subsidiary of the Company. Pursuant to the Purchase Agreement, on the Closing Date, Booz Allen Hamilton acquired 100% of the issued and outstanding shares of common stock of PGSC for a cash purchase price of $95.0 million, before customary post-closing adjustments based on PGSC’s indebtedness, working capital, cash, and transaction expenses at closing. At closing we entered into a transition services agreement with Booz Allen Hamilton pursuant to which the Company and Booz Allen Hamilton provide certain transitional services to each other as contemplated by and subject to the Purchase Agreement. The service period for the transitional services generally ends during the third quarter of 2025.

On July 1, 2024 (the "RRC Closing Date"), the Company sold 100% of the issued and outstanding equity interests of Rome Research Corporation ("RRC"), a wholly-owned subsidiary of the Company, to NexTech Solutions Holdings, LLC ("NexTech") for a cash purchase price of $7.0 million, before customary post-closing adjustments based on RRC’s indebtedness, working capital, cash, and transaction expenses at closing. At closing we entered into a transition services agreement with NexTech pursuant to which the Company and NexTech provide certain transitional services to each other as contemplated by and subject to the transition services agreement. The service period for the transitional services generally ends during the third quarter of 2025.

The sale of PGSC and RRC comprise the sale of 100% of the Company's Government segment. The Company recognized a pre-tax gain on sale of $77.2 million from the sale of PGSC and RRC in the nine months ended September 30, 2024.

Pursuant to the Purchase Agreement, within 120 days following the PGSC Closing Date Booz Allen Hamilton is required to deliver to the Company a closing statement setting forth its determination of net working capital and any resulting net working capital surplus or deficit. To the extent there is an adjustment to net working capital, as agreed to by the Company and Booz Allen Hamilton pursuant to the Purchase Agreement, any such change will be recorded as an adjustment to the gain on sale of discontinued operations for the period such change occurs.

Pursuant to the sale of RRC, $0.7 million of the cash purchase price was deposited into an escrow account administered by a third party to fund potential post-closing adjustments and obligations. As of September 30, 2024, the balance in the escrow account remained at $0.7 million. Within 90 days following the RRC Closing Date NexTech is required to deliver to the Company a closing statement setting forth its determination of net working capital and any resulting net working capital surplus or deficit. To the extent there is an adjustment to net working capital, as agreed to by the Company and NexTech pursuant to the sale, any such change will be recorded as an adjustment to the gain on sale of discontinued operations for the period such change occurs.

As of September 30, 2024, the Company estimated the federal taxable gain on sale for PGSC and RRC to be $74.6 million, however, we expect to offset the taxable gain through the utilization of several tax benefits including $41.8 million of our net operating loss carryforwards, $22.4 million of our Section 163(j) interest expense limitation carryforwards, and $1.6 million of our research and development tax credits. Additionally, the income tax associated with the gain will be impacted by the final allocation of the sales price, which may be materially different from the Company’s estimates. The impact of changes in estimated income tax (if any) will be recorded as an adjustment to discontinued operations in the period such change in estimate occurs.

The Company incurred expenses related to its disposition of PGSC and RRC of approximately $6.9 million which are included in net income from discontinued operations in the condensed consolidated statements of operations.

The accounting requirements for reporting the disposition of PGSC and RRC as discontinued operations were met when the disposition of PGSC was completed and the sale of RRC was deemed probable. Accordingly, the historical results of PGSC and RRC have been presented as discontinued operations and, as such, have been excluded from continuing operations for all periods presented.

The following table presents the major classes of assets and liabilities of discontinued operations for PGSC and RRC as of December 31, 2023:

The following table presents the major categories of income from discontinued operations:

Three Months Ended September 30,

Nine Months Ended September 30,

(in thousands)

2024

2023

2024

2023

Contract revenue

$

—

$

38,433

$

66,540

$

101,301

Contract cost of sales

—

(34,506)

(60,218)

(91,970)

Operating income from discontinued operations

—

3,927

6,322

9,331

General and administrative expense

177

(67)

(693)

(80)

Other expense, net

—

(111)

—

(221)

Gain on sale of discontinued operations

451

—

77,205

—

Income from discontinued operations before provision for income taxes

628

3,749

82,834

9,030

Benefit from (provision for) income taxes

204

(31)

(2,147)

(57)

Net income from discontinued operations

$

832

$

3,718

$

80,687

$

8,973

In accordance with ASC Topic 205, Presentation of Financial Statements, the Company adjusted contract cost of sales to exclude corporate overhead allocated to discontinued operations for all periods presented.

The following table presents select non-cash operating and investing activities related to cash flows from discontinued operations:

Three Months Ended September 30,

Nine Months Ended September 30,

(in thousands)

2024

2023

2024

2023

Depreciation and amortization

$

—

$

116

$

200

$

347

Capital expenditures

—

156

233

370

Stock-based compensation

50

37

1,004

98

Note 5 — Accounts Receivable, net

At September 30, 2024 and December 31, 2023, the Company had current expected credit losses of $3.6 million and $1.9 million, respectively, against accounts receivable.

Changes in the current expected credit loss for the nine months ended September 30 were:

The components of inventory, adjusted for reserves, consisted of the following:

(in thousands)

September 30, 2024

December 31, 2023

Finished goods

$

15,389

$

13,530

Work in process

185

216

Component parts

7,793

9,147

Service parts

548

667

Inventories, net

$

23,915

$

23,560

At September 30, 2024 and December 31, 2023, the Company had excess and obsolescence reserves of $8.9 million and $9.0 million, respectively, against inventories.

Note 7 — Identifiable Intangible Assets and Goodwill

The Company's identifiable intangible assets represent intangible assets acquired in acquisitions and software development costs. The components of identifiable intangible assets are:

(in thousands)

September 30, 2024

December 31, 2023

Estimated Useful Life

Weighted-Average Amortization Period

Acquired developed technology

$

173,889

$

119,800

3 - 7 years

5.40 years

Internally developed software costs

37,913

34,735

3 years

2.76 years

Customer relationships

101,910

14,510

5 - 15 years

11.26 years

Trade names

3,210

1,410

2 - 8 years

7.73 years

Non-competition agreements

3,530

30

1 - 5 years

4.5 years

320,452

170,485

Impact of currency translation on intangible assets

1,376

1,399

Less: accumulated amortization

(110,900)

(87,001)

210,928

84,883

Internally developed software costs not meeting general release threshold

3,923

2,886

Trademarks, trade names (non-amortizable)

11,200

6,200

Indefinite

$

226,051

$

93,969

Software costs placed into service during the three months ended September 30, 2024 and 2023, were $1.3 million and $0.3 million, respectively. Software costs placed into service during the nine months ended September 30, 2024 and 2023, were $3.2 million and $2.4 million, respectively.

The following table summarizes amortization expense for acquired developed technology and internally developed software:

Three Months Ended September 30,

Nine Months Ended September 30,

(in thousands)

2024

2023

2024

2023

Amortization of acquired developed technology

$

5,660

$

4,020

$

14,628

$

12,160

Amortization of internally developed software

1,168

1,460

3,591

4,606

Amortization of identifiable intangible assets recorded in cost of sales

6,828

5,480

18,219

16,766

Amortization expense recorded in operating expenses

2,699

464

5,577

1,393

Impact of foreign currency translation on intangible assets

The expected future amortization of intangible assets, assuming straight-line amortization of capitalized software development costs and acquisition related intangibles, excluding software development costs not meeting the general release threshold is:

(in thousands)

2024, remaining

$

9,910

2025

38,423

2026

36,411

2027

32,163

2028

22,123

Thereafter

71,898

Total

$

210,928

Goodwill carried is as follows:

(in thousands)

2024

2023

Beginning balance - January 1

$

488,918

$

486,026

Stuzo Acquisition

136,602

—

TASK Group Acquisition

181,442

—

Foreign currency translation

(3,878)

311

Ending balance - September 30

$

803,084

$

486,337

Note 8 — Debt

In connection with, and to partially fund the TASK Group Acquisition, on July 5, 2024, the Company entered into a credit agreement (the "Credit Agreement"), as the borrower, with certain of its U.S. subsidiaries, as guarantors, the lenders party thereto, Blue Owl Capital Corporation, as administrative agent and collateral agent, and Blue Owl Credit Advisors, LLC, as lead arranger and bookrunner, that provides for a term loan in an initial aggregate principal amount of $90.0 million (the "Credit Facility" and, the loans thereunder, the “Term Loans”).

The Credit Facility matures on the earlier of (i) July 5, 2029 and (ii) the date on which the Company's 1.50% Convertible Senior Notes due 2027 (the "2027 Notes") become due and payable in accordance with their terms. The Term Loans bear interest at a rate equal to either of the following, as selected by the Company: (i) an alternate base rate plus an applicable margin of 4.50%, 4.00% or 3.50% based on a total net recurring revenue leverage ratio, or (ii) a secured overnight financing rate plus an applicable margin of 5.50%, 5.00% or 4.50% based on a total net recurring revenue leverage ratio. Voluntary prepayments of the Term Loans, as well as certain mandatory prepayments of the Term Loans, require payment of a prepayment premium of 4.0% during the first year of the Credit Facility, 3.0% during the second year of the Credit Facility, and 1.0% during the third year of the Credit Facility. Under the Credit Agreement, on a quarterly basis commencing with the fiscal quarter ended December 31, 2024, the Company is required to maintain liquidity of at least $20.0 million and a total net annual recurring revenue leverage ratio of no greater than 1.25 to 1.00.

The following table summarizes information about the net carrying amounts of long-term debt as of September 30, 2024:

(in thousands)

2026 Notes

2027 Notes

Credit Facility

Total

Principal amount of notes outstanding

$

120,000

$

265,000

$

90,000

$

475,000

Unamortized debt issuance cost

(1,251)

(4,551)

(1,164)

(6,966)

Unamortized discount

—

—

(1,299)

(1,299)

Total notes payable

$

118,749

$

260,449

$

87,537

$

466,735

The following table summarizes information about the net carrying amounts of long-term debt as of December 31, 2023:

(in thousands)

2026 Notes

2027 Notes

Total

Principal amount of notes outstanding

$

120,000

$

265,000

$

385,000

Unamortized debt issuance cost

(1,811)

(5,542)

(7,353)

Total notes payable

$

118,189

$

259,458

$

377,647

The following table summarizes interest expense recognized on the long-term debt:

Three Months Ended September 30,

Nine Months Ended September 30,

(in thousands)

2024

2023

2024

2023

Contractual interest expense

$

3,963

$

2,554

$

7,676

$

6,016

Amortization of debt issuance costs

623

541

1,647

1,594

Amortization of discount

108

—

108

—

Total interest expense

$

4,694

$

3,095

$

9,431

$

7,610

The following table summarizes the future principal payments as of September 30, 2024:

(in thousands)

2024, remaining

$

—

2025

—

2026

120,000

2027

355,000

2028

—

Thereafter

—

Total

$

475,000

Note 9 — Common Stock

In connection with, and to partially fund the Cash Consideration related to the Stuzo Acquisition, on March 7, 2024, the Company entered into a Securities Purchase Agreement (the "Securities Purchase Agreement") with funds and accounts advised by T. Rowe Price Investment Management, Inc., ADW Capital, Voss Capital, Greenhaven Road Capital, Jane Street, Progeny 3, Fund 1 Investments LLC, Newtyn Capital, Ghisallo Capital Management and Burkehill Global Management (collectively, the “Purchasers”) to raise approximately $200 million through a private placement of PAR common stock. Pursuant to the Securities Purchase Agreement, PAR issued and sold 5,174,638 shares of its common stock at a 10% discount to the Purchasers for a gross purchase price of approximately $200 million ($38.65 per share). Net proceeds from the Securities Purchase Agreement were approximately $194.4 million, net of issuance costs of $5.5 million.

On January 2, 2024, the Company entered into a consulting agreement with PAR Act III, LLC ("PAR Act III") pursuant to which PAR Act III provides the Company with strategic consulting, merger and acquisition technology due diligence, and other professional and expert services that may be requested from time to time by the Company’s Chief Executive Officer through April 8, 2026. In consideration for the services provided under the consulting agreement, the Company amended its common stock purchase warrant issued to PAR Act III on April 8,

2021 (the "Warrant") to extend the termination date of the Warrant to April 8, 2028, subject to the consulting agreement remaining in effect through April 8, 2026.

The issuance date fair value of the Warrant extension was determined to be $4.5 million based on using the Black-Scholes model with the following assumptions as of January 2, 2024:

Original Warrant

Modified Warrant

Expected term

2.25 years

4.25 years

Risk free interest rate

4.33

%

3.93

%

Expected volatility

55.01

%

63.39

%

Expected dividend yield

None

None

Fair value (per warrant)

$

7.36

$

16.21

In connection with the Company's private placement of its common stock on March 7, 2024 to partially fund the Stuzo Acquisition, an additional 6,312 shares of common stock are available for purchase under the Warrant, increasing the total to 510,287 shares of common stock available for purchase at an exercise price of $74.96 per share.

The Warrant is accounted for as stock-based compensation to non-employees pursuant to ASC Topic 718, Stock Compensation, by way of ASC Topic 815, Derivatives and Hedging, due to the Warrant extension being in exchange for consulting services. The issuance date fair value of the Warrant extension of $4.5 million will be recognized as stock-based compensation expense ratably over the requisite service period for the Warrant extension ending April 8, 2026.

Note 10 — Stock-Based Compensation

Stock-based compensation expense, net of forfeitures and adjustments of zero and $0.1 million, was $5.9 million and $3.9 million for the three months ended September 30, 2024 and 2023, respectively. Stock-based compensation expense, net of forfeitures and adjustments of $0.2 million and $0.4 million, was $16.6 million and $10.5 million for the nine months ended September 30, 2024 and 2023, respectively.

At September 30, 2024, the aggregate unrecognized compensation expense related to unvested equity awards was $32.3 million, which is expected to be recognized as compensation expense in fiscal years 2024 through 2027.

A summary of stock option activity for the nine months ended September 30, 2024 is below:

(in thousands, except for weighted average exercise price)

Options outstanding

Weighted average exercise price

Outstanding at January 1, 2024

920

$

13.04

Exercised

(174)

12.03

Canceled/forfeited

(16)

13.22

Outstanding at September 30, 2024

730

$

13.28

A summary of unvested restricted stock units activity for the nine months ended September 30, 2024 is below:

(in thousands, except for weighted average award value)

A total of 330,000 shares of Company common stock were made available for purchase under the Company's 2021 Employee Stock Purchase Plan ("ESPP"), subject to adjustment as provided for in the ESPP. As of September 30, 2024, 15,251 shares of common stock were purchased.

Note 11 — Net Income (Loss) Per Share

Net income (loss) per share is calculated in accordance with ASC Topic 260, Earnings per Share, which specifies the computation, presentation and disclosure requirements for earnings per share (“EPS”). It requires the presentation of basic and diluted EPS. Basic EPS excludes all dilution and is based upon the weighted average number of shares of common stock outstanding during the period. Diluted EPS reflects the potential dilution that would occur if convertible securities or other contracts to issue common stock were exercised. At September 30, 2024, there were 730,000 anti-dilutive stock options outstanding compared to 929,000 as of September 30, 2023. At September 30, 2024, there were 925,000 anti-dilutive restricted stock units outstanding compared to 862,000 as of September 30, 2023.

Note 12 — Commitments and Contingencies

From time to time, the Company is party to legal proceedings arising in the ordinary course of business. Based on information currently available, and based on its evaluation of such information, the Company believes the legal proceedings in which it is currently involved are not material or are not likely to result in a material adverse effect on the Company’s business, financial condition or results of operations, or cannot currently be estimated.

Note 13 — Geographic Information and Customer Concentration

The following table represents revenues by country based on the location of the revenue:

Three Months Ended September 30,

Nine Months Ended September 30,

(in thousands)

2024

2023

2024

2023

United States

$

81,638

$

62,279

$

219,353

$

190,223

International

15,116

6,422

25,624

16,591

Total

$

96,754

$

68,701

$

244,977

$

206,814

The following table represents assets by country based on the location of the assets:

(in thousands)

September 30, 2024

December 31, 2023

United States

$

984,773

$

767,894

International

314,501

34,712

Total

$

1,299,274

$

802,606

Customers comprising 10% or more of the Company’s total revenues are summarized as follows:

Three Months Ended September 30,

Nine Months Ended September 30,

2024

2023

2024

2023

McDonald’s Corporation

18

%

11

%

13

%

12

%

Yum! Brands, Inc.

8

%

14

%

9

%

14

%

Dairy Queen

7

%

10

%

8

%

11

%

All Others

67

%

65

%

70

%

63

%

Total

100

%

100

%

100

%

100

%

No other customer within "All Others" represented 10% or more of the Company’s total revenue for the three and nine months ended September 30, 2024 or 2023.

The Company’s financial instruments have been recorded at fair value using available market information and valuation techniques. The fair value hierarchy is based upon three levels of input, which are:

Level 1 — quoted prices in active markets for identical assets or liabilities (observable)

Level 2 — inputs other than Level 1 that are observable, either directly or indirectly, such as quoted prices for similar assets or liabilities, quoted prices in inactive markets, or other inputs that are observable market data for essentially the full term of the asset or liability (observable)

Level 3 — unobservable inputs that are supported by little or no market activity, but are significant to determining the fair value of the asset or liability (unobservable)

The Company’s financial instruments primarily consist of cash and cash equivalents, cash held on behalf of customers, short-term investments, debt instruments and deferred compensation assets and liabilities. The carrying amounts of cash and cash equivalents, cash held on behalf of customers, and short-term investments as of September 30, 2024 and December 31, 2023 were considered representative of their fair values because of their short-term nature and are classified as Level 1 of the fair value hierarchy. Debt instruments are recorded at principal amount net of unamortized debt issuance cost and discount (refer to "Note 8 - Debt" for additional information). The estimated fair value of the 2.875% Convertible Senior Notes due 2026 (the "2026 Notes"), 1.50% Convertible Senior Notes due 2027 (the "2027 Notes"), and the Credit Facility at September 30, 2024 was $161.5 million, $264.4 million, and $88.7 millionrespectively. As the Credit Facility has a variable interest rate and has no equity component, the book value of the Credit Facility is equal to the fair value. The estimated fair value of the 2026 Notes and 2027 Notes at December 31, 2023 was $145.6 million and $236.1 million respectively. The valuation techniques used to determine the fair value of the Company's long-term debt are classified in Level 2 of the fair value hierarchy as they are derived from broker quotations.

Deferred compensation assets and liabilities primarily relate to the Company’s deferred compensation plan, which allows for pre-tax salary deferrals for certain employees. Changes in the fair value of the deferred compensation liabilities are derived using quoted prices in active markets of the asset selections made by plan participants. Deferred compensation liabilities are classified in Level 2, the fair value classification as defined under FASB ASC Topic 820, Fair Value Measurements, because their inputs are derived principally from observable market data by correlation to the hypothetical investments. The Company holds insurance investments to partially offset the Company’s liabilities under its deferred compensation plan, which are recorded at fair value each period using the cash surrender value of the insurance investments.

The cash surrender value of the life insurance policy was zero and $3.3 million at September 30, 2024 and December 31, 2023, respectively, and is included in other assets on the condensed consolidated balance sheets. Amounts owed to employees participating in the deferred compensation plan at September 30, 2024 were $0.1 million compared to $0.4 million at December 31, 2023 and are included in other long-term liabilities on the condensed consolidated balance sheets.

The Company uses a Monte Carlo simulation of a discounted cash flow model to determine the fair value of the earn-out liability associated with the acquisition of MENU Technologies AG (the "MENU Acquisition"). Significant inputs used in the simulation are not observable in the market and thus the liability represents a Level 3 fair value measurement as defined in ASC 820. Ultimately, the liability will be equivalent to the amount paid, and the difference between the fair value estimate and amount paid will be recorded in earnings. The amount paid that is less than or equal to the liability on the acquisition date will be reflected as cash used in financing activities in the Company's condensed consolidated statements of cash flows. Any amount paid in excess of the liability on the acquisition date will be reflected as cash used in operating activities.

During the three months ended June 30, 2024, the Company determined that there would be no earn-out payment related to the MENU Acquisition. As such, the Company reduced the fair value of the earn-out liability to zero. The earn-out period expired on July 31, 2024 with no payment made.

The following table presents the changes in the estimated fair values of the Company’s liabilities for contingent consideration measured using significant unobservable inputs (Level 3) for the nine months ended September 30:

(in thousands)

2024

2023

Balance at January 1

$

600

$

9,800

Change in fair value of contingent consideration

(600)

(7,500)

Balance at September 30

$

—

$

2,300

The balance of the fair value of the liability was recorded within "Accrued expenses" in the condensed consolidated balance sheets. The change in fair value of contingent consideration was recorded within "Adjustment to contingent consideration liability" in the condensed consolidated statements of operations.

The following table provides quantitative information associated with the fair value measurement of the Company’s liabilities for contingent consideration as of December 31, 2023:

Contingency Type

Maximum Payout (1) (undiscounted) (in thousands)

Fair Value

Valuation Technique

Unobservable Inputs

Weighted Average or Range

Revenue based payments

$

5,600

$

600

Monte Carlo

Revenue volatility

25.0

%

Discount rate

11.5

%

Projected year of payments

2024

(1) Maximum payout as determined by Monte Carlo valuation simulation; the disclosed contingency is not subject to a contractual maximum payout.

Item 2. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion and analysis of our financial condition and results of operations should be read in conjunction with our financial statements and the notes thereto included under "Part I, Item 1. Financial Statements (unaudited)" of this Quarterly Report and our audited consolidated financial statements and the notes thereto included under "Part II, Item 8. Financial Statements and Supplementary Data" of the 2023 Annual Report. This discussion contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from the results contemplated by these forward-looking statements due to a number of factors, including those discussed under "Forward-Looking Statements".

OVERVIEW

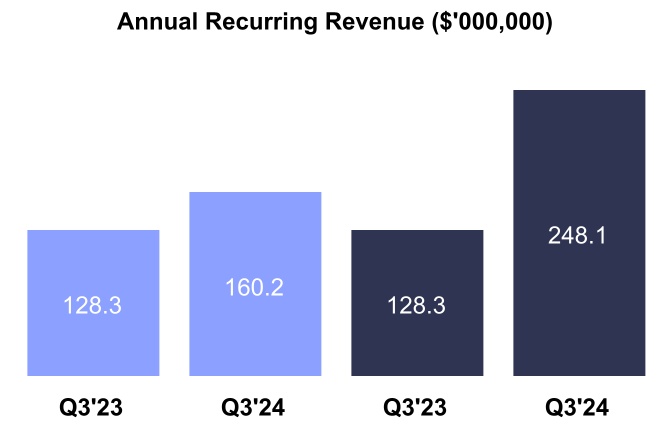

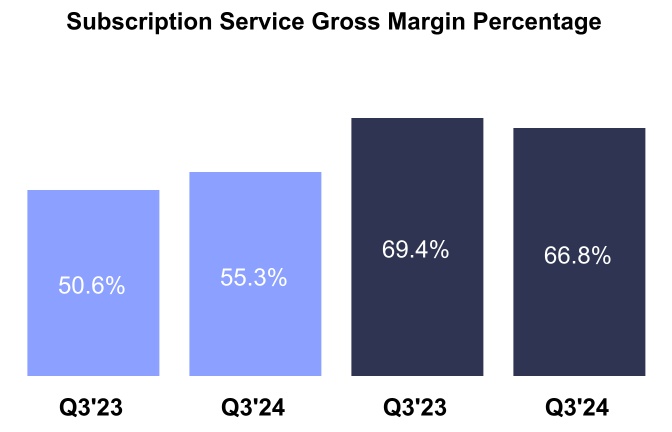

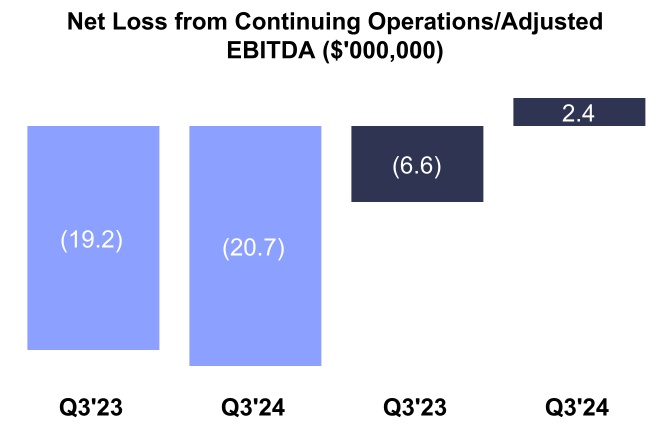

Q3 2024 Operating Performance Highlights

Organic -Year-over-year

growth of 24.8%

Total - Year-over-year

growth of 93.3%

GAAP - Year-over-year 4.7% improvement

Non-GAAP - Year-over-year 2.6% decline

Net Loss from Cont. Ops.

Year-over-year decline of $1.4 million

Adjusted EBITDA

Year-over-year improvement of $9.0 million

Refer to "Key Performance Indicators and Non-GAAP Financial Measures" below for important information on key performance indicators and non-GAAP financial measures, including annual recurring revenue ("ARR"), non-GAAP subscription service gross margin percentage, and adjusted EBITDA. We use these key performance indicators and non-GAAP financial measures to evaluate our performance.

•Sale of Rome Research Corporation: On July 1, 2024, the Company sold Rome Research Corporation for $7.0 million, before customary post-closing adjustments, completing the divestiture of PAR's Government segment.

•Acquisition of TASK Group: In July 2024, the Company secured a term loan of $90.0 million under the Credit Facility which was used in connection with its acquisition of TASK Group. TASK Group, an Australia-based entity, offers international unified commerce solutions, including interactive customer engagement and seamless integration, tailored for major brands worldwide. The TASK Group’s transaction management platform, TASK, is used by some of the world’s largest foodservice brands including, Starbucks and Guzman Y Gomez, while its loyalty customer engagement platform, Plexure, is used by McDonald’s Corporation in 65 markets. With the addition of TASK Group, the Company will be able to serve the top enterprise foodservice brands across the globe with a unified commerce approach from front-of-house to back-of-house.

Refer to “Note 3 – Acquisitions”, “Note 4 – Discontinued Operations”, and “Note 8 – Debt” of the notes to interim condensed consolidated financial statements in "Part I, Item 1. Financial Statements (unaudited)" of this Quarterly Report for additional information about the sale of RRC, the Credit Facility, and the acquisition of TASK Group.

million or 40.8% compared to $68.7 million for the three months ended September 30, 2023.

Subscription service revenues were $59.9 million for the three months ended September 30, 2024, an increase of $28.5 million or 91.0% compared to $31.4 million for the three months ended September 30, 2023. The increase was substantially driven by increased Engagement Cloud subscription service revenues of $21.8 million, of which $18.5 million was driven by inorganic increases in revenues of $10.7 million and $7.8 million stemming from the post-acquisition operations of the PAR Retail and Plexure product lines, respectively. The residual increase of $3.3 million from Engagement Cloud subscription services was driven by a 21.9% organic increase in active sites and an 8.4% organic increase in average revenue per site equally driven by cross-selling initiatives, upselling, and price increases. Operator Cloud subscription services increased $6.5 million of which $1.4 million was driven by an inorganic increase in revenues stemming from the post-acquisition operations of the TASK product line. The residual increase of $5.1 million from Operator Cloud subscription services was driven by a 16.8%increase in organic active sites and a 12.2% increase in average revenue per site equally driven by cross-selling initiatives, upselling, and price increases.

Hardware revenues were $22.7 million for the three months ended September 30, 2024, a decrease of $3.2 million or 12.3% compared to $25.8 million for the three months ended September 30, 2023. The decrease primarily consists of decreases in hardware revenues from international hardware sales of $1.3 million, peripherals (scanners, printers, and components) of $0.8 million, and tablets of $0.6 million. These decreases were substantially driven by the timing of tier one enterprise customer hardware refresh cycles and timing of onboarding of Operator Cloud customers buying hardware.

Professional service revenues were $14.2 million for the three months ended September 30, 2024, an increase of $2.7 million or 23.3% from $11.5 million for the three months ended September 30, 2023. The increase was substantially driven by a $1.1 million increase in hardware repair services, a $0.8 million increase in field operations, and a $0.5 million increase in installation services.

Nine Months Ended September 30,

Percentage of total revenue

Increase (decrease)

(in thousands)

2024

2023

2024

2023

2024 vs 2023

Subscription service

$

143,160

$

89,700

58.4

%

43.4

%

59.6

%

Hardware

60,992

78,991

24.9

%

38.2

%

(22.8)

%

Professional service

40,825

38,123

16.7

%

18.4

%

7.1

%

Total revenues, net

$

244,977

$

206,814

100.0

%

100.0

%

18.5

%

For the nine months ended September 30, 2024 compared to the nine months ended September 30, 2023

Total revenues were $245.0 million for the nine months ended September 30, 2024, an increase of $38.2 million or 18.5% compared to $206.8 million for the nine months ended September 30, 2023.

Subscription service revenues were $143.2 million for the nine months ended September 30, 2024, an increase of $53.5 million or 59.6% compared to $89.7 million for the nine months ended September 30, 2023. The increase was substantially driven by increased Engagement Cloud subscription service revenues of $35.5 million, of which $31.2 million was driven by inorganic increases in revenues of $23.4 million and $7.8 million stemming from the post-acquisition operations of the PAR Retail and Plexure product lines, respectively. The residual increase of $4.3 million from Engagement Cloud subscription services was driven by an 8.5% organic increase in active sites. Operator Cloud subscription services increased $17.7 million of which revenues of $1.4 million was driven by an inorganic increase in revenues stemming from the post-acquisition operations of the TASK product line. The residual increase of $16.3 million from Operator Cloud subscription services was driven by an 18.3%increase in organic active sites and a 13.1% increase in average revenue per site equally driven by cross-selling initiatives, upselling, and price increases.

Hardware revenues were $61.0 million for the nine months ended September 30, 2024, a decrease of $18.0 million or 22.8% compared to $79.0 million for the nine months ended September 30, 2023. The decrease primarily consists of decreases in hardware revenues from terminals of $6.2 million, peripherals of $4.2 million, and kitchen display systems of $3.7 million. These decreases were substantially driven by the timing of tier one enterprise

customer hardware refresh cycles and timing of onboarding of Operator Cloud customers buying hardware.

Professional service revenues were $40.8 million for the nine months ended September 30, 2024, an increase of $2.7 million or 7.1% from $38.1 million for the nine months ended September 30, 2023. The increase was substantially driven by a $3.1 million increase in hardware repair services and a $1.6 million increase in field operations, partially offset by a $1.7 million decrease in installation services.

Gross Margin

Three Months Ended September 30,

Gross Margin Percentage

Increase (decrease)

(in thousands)

2024

2023

2024

2023

2024 vs 2023

Subscription service

$

33,120

$

15,866

55.3

%

50.6

%

4.7

%

Hardware

5,772

6,529

25.5

%

25.3

%

0.2

%

Professional service

4,139

2,739

29.2

%

23.8

%

5.4

%

Total gross margin

$

43,031

$

25,134

44.5

%

36.6

%

7.9

%

For the three months ended September 30, 2024 compared to the three months ended September 30, 2023

Total gross margin as a percentage of revenue for the three months ended September 30, 2024, increased to 44.5% as compared to 36.6% for the three months ended September 30, 2023.

Subscription service margin as a percentage of subscription service revenue for the three months ended September 30, 2024, increased to 55.3% as compared to 50.6% for the three months ended September 30, 2023. The increase was substantially driven by a continued focus on efficiency improvements with our hosting and customer support costs as well as improved margins stemming from post-acquisition operations of PAR Retail and TASK Group.

Hardware margin as a percentage of hardware revenue for the three months ended September 30, 2024, was relatively unchanged at 25.5% as compared to 25.3% for the three months ended September 30, 2023.

Professional service margin as a percentage of professional service revenue for the three months ended September 30, 2024, increased to 29.2% as compared to 23.8% for the three months ended September 30, 2023. The increase primarily consists of increased margins for field operations and installations substantially driven by improved cost management.

Nine Months Ended September 30,

Gross Margin Percentage

Increase (decrease)

(in thousands)

2024

2023

2024

2023

2024 vs 2023

Subscription service

$

76,736

$

43,045

53.6

%

48.0

%

5.6

%

Hardware

14,405

15,989

23.6

%

20.2

%

3.4

%

Professional service

9,976

6,198

24.4

%

16.3

%

8.1

%

Total gross margin

$

101,117

$

65,232

41.3

%

31.5

%

9.8

%

For the nine months ended September 30, 2024 compared to the nine months ended September 30, 2023

Total gross margin as a percentage of revenue for the nine months ended September 30, 2024, increased to 41.3% as compared to 31.5% for the nine months ended September 30, 2023.

Subscription service margin as a percentage of subscription service revenue for the nine months ended September 30, 2024, increased to 53.6% as compared to 48.0% for the nine months ended September 30, 2023. The increase was substantially driven by a continued focus on efficiency improvements with our hosting and customer support costs as well as improved margins stemming from post-acquisition operations of PAR Retail and TASK Group.

Hardware margin as a percentage of hardware revenue for the nine months ended September 30, 2024, increased to 23.6% as compared to 20.2% for the nine months ended September 30, 2023. The increase in margin primarily consists of improved inventory management resulting in lower excess and obsolescent inventory charges and improved margins from terminals and kitchen display systems primarily driven by price increases.

Professional service margin as a percentage of professional service revenue for the nine months ended September 30, 2024, increased to 24.4% as compared to 16.3% for the nine months ended September 30, 2023. The increase primarily consists of increased margins for hardware service repair and field operations substantially driven by improved cost management.

Sales and Marketing Expense ("S&M")

Three Months Ended September 30,

Percentage of total revenue

Increase (decrease)

(in thousands)

2024

2023

2024

2023

2024 vs 2023

Sales and marketing

$

10,500

$

9,532

10.9

%

13.9

%

10.2

%