1 MD&A Overview

| 1 | Overview |

| 1.1 | Introduction |

At a glance

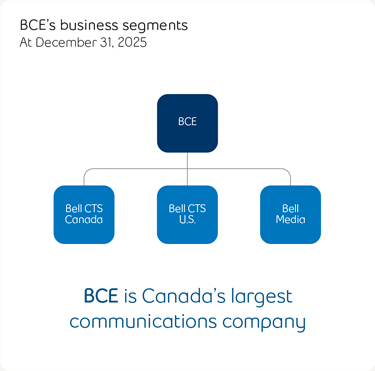

BCE is Canada’s largest communications company,(1) leading the way in advanced fibre and wireless networks, enterprise services and digital media. BCE delivers next-generation technology that leverages cloud-based and AI-driven solutions. BCE provides residential, business and wholesale customers with a wide range of solutions for all their communications needs. BCE’s shares are publicly traded on the Toronto Stock Exchange and on the New York Stock Exchange (TSX, NYSE: BCE).

On August 1, 2025, BCE acquired Ziply Fiber, the leading fibre Internet provider in the Pacific Northwest of the U.S. providing wireline, Internet and TV services to residential, business and wholesale customers in this region. The results from the acquired Ziply Fiber operations are included in a new segment, Bell Communication and Technology Services (Bell CTS) U.S., from the date of acquisition.

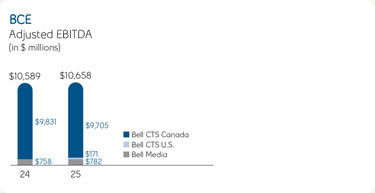

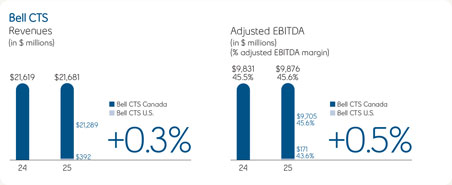

Our results are subsequently reported in three segments: Bell CTS Canada, Bell CTS U.S. and Bell Media. Our segments reflect how we manage our business and how we classify our operations for planning and measuring performance.

Bell CTS Canada provides a wide range of communication products and services to consumer, business and government customers across Canada. Wireless products and services include mobile data and voice plans, streaming services, and devices and are available nationally. Wireline products and services comprise data (including Internet access, Internet protocol television (IPTV), cloud-based services, AI-driven solutions and business solutions), voice, streaming services, and other communication services and products, which are available to our residential, small and medium-sized business and large enterprise customers primarily in Ontario, Québec, the Atlantic provinces and Manitoba, while satellite TV service and connectivity to business customers are available nationally across Canada. In addition, this segment includes our wholesale business, which buys and sells local telephone, long distance, data and other services from or to resellers and other carriers, as well as, in 2024, the results of operations of our national consumer electronics retailer, The Source (Bell) Electronics Inc. (The Source). In 2024, Bell wound down The Source head office and back office operations, as well as closed 107 The Source stores.

Bell CTS U.S., comprised of Ziply Fiber, provides wireline communication products and services over a combined fibre-based and copper-based network, to residential, business and wholesale customers in the Pacific Northwest of the U.S. Wireline products and services consist of data (including broadband Internet with varying speeds and value-added features, commercial ethernet, dedicated Internet-non-switched access and other data transport networking options) and voice (traditional and voice over Internet protocol (VoIP) voice services, including local, long distance, and unified communications as a service (UCaaS) and Video (IPTV)).

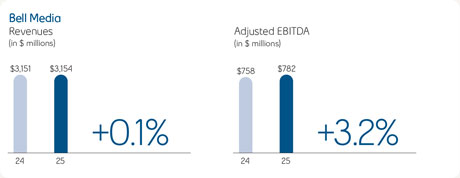

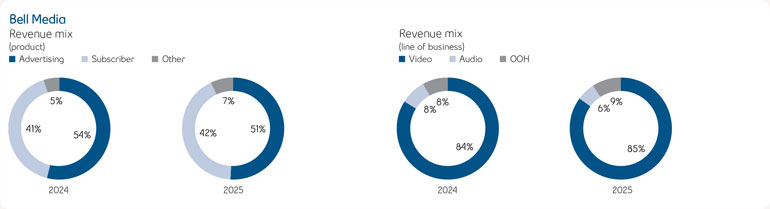

Bell Media holds a portfolio of assets providing premium video, audio, out-of-home (OOH) advertising, and digital media services to customers nationally across Canada.

We also hold investments in a number of other assets, including:

| • | a 50% indirect equity interest in Glentel Inc. (Glentel) |

| • | a 20.2% indirect equity interest in entities that operate the Montréal Canadiens Hockey Club, evenko and the Bell Centre in Montréal, Québec, as well as Place Bell in Laval, Québec |

| (1) | Based on total revenue and total combined customer connections. |

| BCE INC. 2025 ANNUAL FINANCIAL REPORT | 9 |