August 13, 2025

Via EDGAR Transmission

United States Securities and Exchange Commission

Division of Corporation Finance

Office of Life Sciences

100 F Street, N.E.

Washington, D.C. 20549

| Attention: | Lauren Sprague Hamill |

| Jason Drory |

| Re: | Imunon, Inc. |

| Form 10-K for Fiscal Year Ended December 31, 2024 | |

| Filed February 27, 2025 | |

| File No. 001-15911 |

Dear Ms. Hamill and Mr. Drory:

On behalf of Imunon, Inc. (the “Company”), we are writing in response to the letter from the staff (the “Staff”) of the Division of Corporation Finance, Office of Life Sciences, of the U.S. Securities and Exchange Commission (the “Commission”), dated August 4, 2025 (the “Comment Letter”), relating to the Company’s Annual Report on Form 10-K for the year ended December 31, 2024 (the “2024 Form 10-K”), filed with the Commission on February 27, 2025. The Company’s responses to these comments are set forth below.

Please note that for the Staff’s convenience, we have recited the Staff’s comments and provided the Company’s response to such comments immediately thereafter.

2024 Form 10-K

Intellectual Property, page 26

| 1. | In future filings, please revise your intellectual property disclosure in relation to the Company’s material patents as follows: |

● Clearly describe on an individual or patent family basis whether each patent is owned or licensed, the expiration year or expected expiration year of each issued and pending patent, and the jurisdiction, including any foreign jurisdiction, of each material, pending or issued patent.

| Response: | The Company respectfully acknowledges the Staff’s comment and will revise its intellectual property disclosure in future filings as follows: |

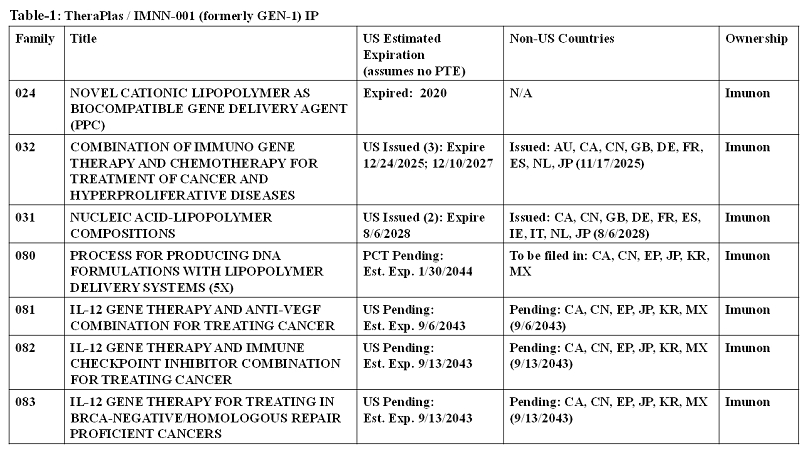

A description of each individual patent belonging to the TheraPlas or PlaCCine technology with respect to patent ownership, expiration/expected expiration year and jurisdiction including foreign jurisdiction will be provided as shown in Table-1 and Table-2, respectively.

● Additionally, it appears that certain of your issued patents pertaining to the TheraPlas and IMNN-001 technologies will expire on dates ranging from 2025 to 2028. Revise your discussion to identify with greater specificity any material patent(s) that will expire in the near term. As appropriate, please provide additional risk factor disclosure discussing the extent to which you face material risk stemming from the expiration of these patents, or otherwise advise.

| Response: | The Company respectfully acknowledges the Staff’s comment, and will revise its intellectual property disclosure in future filings with the following: |

“Patent protection for TheraPlas and IMNN-001 technologies is based upon patent families, that we own, which are directed to composition of matter and methods of use. The first of these patent families have been filed in major markets including the U.S. and Europe. Patents issued in these families expire between 2025 and 2028 (as set forth in Table 1 and Table 2 above). Later-filed patent application families have been filed in major markets including the U.S. and Europe. Any patents issuing in these later-filed families are expected to have a standard 20-year term that will expire between 2043 and 2044, in each instance provided that all appropriate maintenance fees are paid and not including any patent term adjustment, patent term extension, or Supplementary Protection Certificate (SPC) that may be available on a country-by-country basis. Independent of any patent protection, if we obtain FDA regulatory approval of IMNN-001 as a biological product for treating ovarian cancer, it is expected that biologic exclusivity would provide data exclusivity (12 years) and orphan drug exclusivity would provide marketing exclusivity (7 years) against certain competitors during these coextensive regulatory exclusivity periods.”

| 2 |

In future filings, the Company will also revise the section under the heading “Risk Factors” under the subheading “Risks Related to Intellectual Property” to disclose the additional material risks the Company will face upon the anticipated expiration of its patents from 2025 to 2028 by adding the following risk factor:

“Certain of our issued patents pertaining to the TheraPlas and IMNN-001 technologies will expire on dates ranging from 2025 to 2028. If we are unable to obtain issuance of our later-filed, later-expiring patent applications or other means of regulatory exclusivity for our products, the expiration of patents might create opportunities for competitors to enter the market for our target indications, which could have a material negative impact on our financial results. Without patent protection, we are susceptible to competitors bringing similar products to market, obtaining FDA approval, and achieving regulatory exclusivity prior to us.”

| 2. | We refer to your disclosure on page 39 stating that you are party to license agreements with Duke University, under which you have exclusive rights to commercialize medical treatment products and procedures based on Duke’s thermo-sensitive liposome technology. Please revise future filings in an appropriate place to include a discussion of the material terms of these or any other material license agreements, including, as applicable: |

● Nature and scope of intellectual property transferred;

● Each parties’ rights and obligations;

● Duration of agreement and royalty term;

● Termination provisions; and

● Payment provisions, including quantification of any upfront fee and any installments thereof, amounts paid to date, aggregate potential milestone payments segregated by development and commercial milestone payments, and the applicable royalty rates to be paid by each party. In the event a range is provided in place of the actual royalty rate, such range should be within ten percentage points.

Additionally, in future filings, please file the referenced license agreements with Duke University as exhibits, or otherwise provide us with your analysis as to why you believe they are not required to be filed. Refer to Item 601(b)(10) of Regulation S-K.

| Response: | The Company respectfully acknowledges the Staff’s comment, and in future filings, will revise the relevant risk factor as set forth below to delete the reference to the license agreements with Duke University. The Company notes that such license agreements, (which were previously filed as exhibits 10.13 and 10.14 to the Company’s Annual Report on Form 10-K for the year ended December 31, 2022, filed with the Commission on March 30, 2023) are not material contracts for the Company pursuant to Item 601(b)(10) of Regulation S-K because such contracts relate to a development program for ThermoDox, which the Company is no longer pursuing. |

| 3 |

“Our business depends on license agreements with third parties to permit us to use patented technologies. The loss of any of our rights under these agreements could impair our ability to develop and market our products, if approved.

Our success will depend, in a substantial part, on our ability to maintain our rights under license agreements granting us rights to use patented technologies. If we breach any provisions of the license and research agreements, we may lose our ability to use the subject technology, as well as compensation for our efforts in developing or exploiting the technology. Any such loss of rights and access to technology could have a material adverse effect on our business.

Further, we cannot guarantee that any patent or other technology rights licensed to us by others will not be challenged or circumvented successfully by third parties, or that the rights granted will provide adequate protection. We may be required to alter any of our potential products or processes or enter into a license and pay licensing fees to a third party or cease certain activities. There can be no assurance that we can obtain a license to any technology that we determine we need on reasonable terms, if at all, or that we could develop or otherwise obtain alternate technology. If a license is not available on commercially reasonable terms or at all, our business, results of operations, and financial condition could be significantly harmed, and we may be prevented from developing and commercializing the product. Litigation, which could result in substantial costs, may also be necessary to enforce any patents issued to or licensed by us or to determine the scope and validity of another’s claimed proprietary rights.”

* * * *

| 4 |

We appreciate the Staff’s comments and request the Staff contact Susan Eylward, General Counsel and Corporate Secretary, at (917) 538-6811 or by email (seylward@imunon.com) with any questions or comments regarding this letter.

| Very truly yours, | |

| /s/ Susan Eylward | |

| Susan Eylward, General Counsel and Corporate Secretary |

| cc: | Stacy R. Lindborg, Imunon, Inc. |

| 5 |