(7) Represents various federal and local reimbursement programs in the United Kingdom and Canada.

1

Portfolio

(dollars in thousands at Welltower pro rata ownership)

In-Place NOI Diversification(1)

By Partner:

Total Properties

Seniors Housing Operating

Seniors Housing Triple-net

Outpatient Medical

Long-Term/ Post-Acute Care

Total

% of Total

Barchester

261

$

217,296

$

264,552

$

—

$

—

$

481,848

11.0

%

Cogir Senior Living

180

379,984

—

—

—

379,984

8.7

%

Care UK

170

262,408

—

—

—

262,408

6.0

%

Sunrise Senior Living

85

238,200

—

—

—

238,200

5.5

%

Avir Health Group

131

—

—

—

211,772

211,772

4.9

%

Oakmont Management Group

72

202,772

—

—

—

202,772

4.6

%

Avery Healthcare

95

109,356

78,700

—

—

188,056

4.3

%

StoryPoint Senior Living

117

179,624

—

—

—

179,624

4.1

%

HC-One

215

126,940

—

—

—

126,940

2.9

%

Sagora Senior Living

71

126,792

—

—

—

126,792

2.9

%

Remaining

1,139

1,196,120

279,840

117,408

372,680

1,966,048

45.1

%

Total

2,536

$

3,039,492

$

623,092

$

117,408

$

584,452

$

4,364,444

100.0

%

By Country:

United States

1,610

$

2,019,500

$

237,196

$

117,408

$

577,744

$

2,951,848

67.6

%

United Kingdom

794

742,300

382,636

—

—

1,124,936

25.8

%

Canada

132

277,692

3,260

—

6,708

287,660

6.6

%

Total

2,536

$

3,039,492

$

623,092

$

117,408

$

584,452

$

4,364,444

100.0

%

By MSA:

Greater London

143

$

187,988

$

81,912

$

—

$

—

$

269,900

6.2

%

New York / New Jersey

70

111,212

24,396

12,128

17,292

165,028

3.8

%

Los Angeles

50

132,068

19,524

284

3,400

155,276

3.6

%

Dallas

79

106,008

968

1,212

30,708

138,896

3.2

%

Houston

54

28,200

—

74,220

20,068

122,488

2.8

%

Montréal

26

93,768

—

—

—

93,768

2.1

%

Washington D.C.

32

71,492

6,632

—

15,488

93,612

2.1

%

Boston

27

71,748

14,412

168

—

86,328

2.0

%

San Francisco

23

65,996

6,212

—

3,876

76,084

1.7

%

Chicago

34

58,852

7,164

—

—

66,016

1.5

%

Philadelphia

36

36,100

5,480

368

10,964

52,912

1.2

%

Seattle

25

43,616

1,268

264

—

45,148

1.0

%

Raleigh

11

11,204

31,428

—

—

42,632

1.0

%

Charlotte

25

21,576

10,580

10,404

—

42,560

1.0

%

San Antonio

16

26,108

952

228

15,256

42,544

1.0

%

Cleveland

24

33,100

2,548

—

5,084

40,732

0.9

%

Tampa

26

9,368

2,540

—

27,912

39,820

0.9

%

San Diego

14

27,148

7,532

—

3,116

37,796

0.9

%

Minneapolis

23

37,156

—

552

—

37,708

0.9

%

Birmingham UK

16

24,668

11,896

—

—

36,564

0.8

%

Remaining

1,782

1,842,116

387,648

17,580

431,288

2,678,632

61.4

%

Total

2,536

$

3,039,492

$

623,092

$

117,408

$

584,452

$

4,364,444

100.0

%

Notes:

(1) Represents current quarter annualized In-Place NOI. See page 16 for reconciliation.

2

Portfolio

(dollars, units and occupancy at Welltower pro rata ownership; dollars in thousands)

Seniors Housing Operating

Total Portfolio Performance(1)

1Q25

2Q25

3Q25

4Q25

1Q26

Properties

1,113

1,171

1,199

1,659

1,689

Units

124,742

129,758

131,792

160,218

163,618

Total occupancy

85.1

%

85.6

%

86.9

%

87.4

%

87.3

%

Total revenues

$

1,901,227

$

2,007,567

$

2,109,690

$

2,607,559

$

2,823,788

Operating expenses

1,410,579

1,464,457

1,530,131

1,902,889

2,042,868

NOI

$

490,648

$

543,110

$

579,559

$

704,670

$

780,920

NOI margin

25.8

%

27.1

%

27.5

%

27.0

%

27.7

%

Recurring cap-ex

$

68,359

$

63,937

$

78,803

$

116,560

$

67,924

Other cap-ex

$

135,045

$

118,646

$

131,668

$

166,439

$

165,031

Same Store Performance(2)

1Q25

2Q25

3Q25

4Q25

1Q26

Properties

921

921

921

921

921

Units

104,508

104,523

104,522

104,525

104,484

Occupancy

85.3

%

86.4

%

87.9

%

88.9

%

89.0

%

Same store revenues

$

1,572,867

$

1,611,726

$

1,652,555

$

1,680,617

$

1,722,576

Compensation

668,246

677,882

689,648

701,603

698,682

Utilities

77,066

64,899

74,637

71,067

78,661

Food

61,729

64,375

66,019

68,450

64,596

Repairs and maintenance

42,473

42,841

45,786

45,310

45,498

Property taxes

52,905

53,030

53,250

49,234

54,611

All other

234,789

240,323

240,550

248,522

248,711

Same store operating expenses

1,137,208

1,143,350

1,169,890

1,184,186

1,190,759

Same store NOI

$

435,659

$

468,376

$

482,665

$

496,431

$

531,817

Same store NOI margin %

27.7

%

29.1

%

29.2

%

29.5

%

30.9

%

Year over year NOI growth rate

22.1

%

Year over year revenue growth rate

9.5

%

Partners(3)

Properties

Pro Rata Units

Welltower Ownership %(4)

Top Markets

1Q26 NOI

% of Total

Cogir Senior Living

180

27,246

94.3

%

Greater London

$

53,982

6.9

%

Care UK

170

10,938

100.0

%

Southern California

49,692

6.4

%

Sunrise Senior Living

85

7,767

90.7

%

Northern California

39,704

5.1

%

Barchester

111

6,814

100.0

%

New York / New Jersey

27,667

3.5

%

Oakmont Management Group

72

7,099

100.0

%

Dallas

26,701

3.4

%

StoryPoint Senior Living

117

11,927

94.2

%

Montreal

23,568

3.0

%

HC-One

215

12,348

100.0

%

Washington D.C.

20,487

2.6

%

Sagora Senior Living

71

8,174

100.0

%

Boston

17,793

2.3

%

Legend Senior Living

59

5,057

89.2

%

Chicago

14,693

1.9

%

Avery Healthcare

45

3,377

94.4

%

Seattle

11,184

1.4

%

Belmont Village

21

2,803

95.0

%

Top markets

285,471

36.5

%

Clover Management

69

7,811

94.2

%

All other

495,449

63.5

%

Discovery Senior Living

73

5,844

59.6

%

Total

$

780,920

100.0

%

Quality Senior Living

46

5,195

90.9

%

Remaining

342

40,258

Total

1,676

162,658

Notes:

(1) Properties, units, occupancy and cap-ex exclude land parcels, properties under development/redevelopment, leased properties and nonoperational properties.

(3) Represents partner concentration based on annualized In-Place NOI for the quarter ended March 31, 2026. Property count and pro rata units represent the In-Place portfolio.

(4) Welltower ownership percentage weighted based on In-Place NOI. See page 16 for reconciliation.

3

Portfolio

(dollars in thousands at Welltower pro rata ownership)

Payment Coverage Stratification

EBITDARM Coverage(1)

EBITDAR Coverage(1)

% of In-Place NOI

Seniors Housing Triple-net

Long-Term/ Post- Acute Care

Total

Weighted Average Maturity

Number of Leases

Seniors Housing Triple-net

Long-Term/ Post- Acute Care

Total

Weighted Average Maturity

Number of Leases

<.85x

0.1

%

0.1

%

0.2

%

11

3

0.1

%

0.1

%

0.2

%

11

3

.85x-.95x

—

%

—

%

—

%

—

—

—

%

—

%

—

%

—

—

.95x-1.05x

—

%

—

%

—

%

—

—

0.4

%

3.4

%

3.8

%

11

3

1.05x-1.15x

—

%

—

%

—

%

—

—

0.4

%

—

%

0.4

%

6

2

1.15x-1.25x

0.3

%

—

%

0.3

%

4

1

4.7

%

1.2

%

5.9

%

10

7

1.25x-1.35x

1.0

%

1.3

%

2.3

%

9

3

—

%

—

%

—

%

—

—

>1.35

5.7

%

6.1

%

11.8

%

11

24

1.5

%

2.8

%

4.3

%

11

16

Total

7.1

%

7.5

%

14.6

%

10

31

7.1

%

7.5

%

14.6

%

10

31

Revenue and Lease Maturity(2)

Rental Income

Year

Seniors Housing Triple-net

Outpatient Medical

Long-Term / Post-Acute Care

Interest Income

Total Revenues

% of Total

2026

$

2,613

$

1,509

$

9,313

$

33,252

$

46,687

2.9

%

2027

—

1,517

1,287

52,514

55,318

3.5

%

2028

—

3,197

6,669

2,505

12,371

0.8

%

2029

1,115

5,068

—

79,933

86,116

5.4

%

2030

12,525

5,954

30,543

3,646

52,668

3.3

%

2031

—

4,886

4,686

12,603

22,175

1.4

%

2032

99,706

3,052

55,255

359

158,372

9.9

%

2033

63,175

817

1,070

—

65,062

4.1

%

2034

433

3,987

—

274

4,694

0.3

%

2035

36,868

5,653

15,007

1,024

58,552

3.7

%

Thereafter

391,907

86,438

465,451

95,279

1,039,075

64.7

%

$

608,342

$

122,078

$

589,281

$

281,389

$

1,601,090

100.0

%

Weighted Avg Maturity Years

15

12

15

8

14

Notes:

(1) Represents trailing twelve month coverage metrics as of December 31, 2025 for stable portfolio only. Agreements included represent 53% of total Seniors Housing Triple-net and Long-Term/Post-Acute Care In-Place NOI. See page 16 for a reconciliation. Agreements with mixed units use the predominant type based on investment balance.

(2) Excludes all land parcels, developments and investments classified as held for sale, as well as Seniors Housing Triple-net and Long-Term / Post-Acute Care leases accounted for on a cash basis where substantially all contractual rental income during the most recent period was not collected. Rental income represents annualized cash base rent for effective lease agreements. The amounts are derived from the current contracted monthly cash base rent, net of collectability reserves, if applicable. Rental income does not include common area maintenance charges, the amortization of above/below market lease intangibles or other non-cash income. Interest income represents the annualized contractual rate of interest for loans, net of collectability reserves, if applicable.

4

Portfolio

(dollars, square feet and occupancy at Welltower pro rata ownership; dollars in thousands except per square feet)

Outpatient Medical

Total Portfolio Performance(1)

1Q25

2Q25

3Q25

4Q25

1Q26

Properties

433

434

437

194

135

Square feet

21,775,061

21,914,499

22,073,485

8,801,545

5,576,683

Occupancy

94.5

%

94.4

%

94.2

%

95.5

%

96.9

%

Total revenues

$

214,693

$

215,718

$

219,238

$

148,862

$

76,524

Operating expenses

66,804

65,197

65,851

45,000

20,184

NOI

$

147,889

$

150,521

$

153,387

$

103,862

$

56,340

NOI margin

68.9

%

69.8

%

70.0

%

69.8

%

73.6

%

Revenues per square foot

$

39.44

$

39.37

$

39.73

$

67.65

$

54.89

NOI per square foot

$

27.17

$

27.47

$

27.80

$

47.20

$

40.41

Recurring cap-ex

$

6,191

$

13,221

$

19,324

$

4,298

$

1,550

Other cap-ex

$

9,742

$

9,297

$

14,051

$

1,963

$

920

Same Store Performance(2)

1Q25

2Q25

3Q25

4Q25

1Q26

Properties

86

86

86

86

86

Occupancy

97.5

%

97.7

%

97.8

%

97.7

%

97.7

%

Same store revenues

$

26,977

$

27,277

$

25,569

$

26,990

$

27,466

Same store operating expenses

3,692

3,602

1,941

3,200

3,624

Same store NOI

$

23,285

$

23,675

$

23,628

$

23,790

$

23,842

NOI margin

86.3

%

86.8

%

92.4

%

88.1

%

86.8

%

Year over year NOI growth rate

2.4

%

Portfolio Diversification

by Tenant(3)

Rental Income

% of Total

Quality Indicators

Kelsey-Seybold

$

73,996

60.6

%

Health system affiliated properties as % of NOI(3)

99.6

%

UnitedHealth

15,420

12.6

%

Health system affiliated tenants as % of rental income(3)

93.5

%

Atrium Health

10,456

8.6

%

Investment grade tenants as % of rental income(3)

94.8

%

Norman Regional Health

6,789

5.6

%

Retention (trailing twelve months)(3)

90.2

%

Baylor Scott & White Health

2,234

1.8

%

Average remaining lease term (years)(3)

12.1

Remaining portfolio

13,183

10.8

%

Average building size (square feet)(3)

71,557

Total

$

122,078

100.0

%

Average age (years)

15

Expirations(3)

2026

2027

2028

2029

2030

Thereafter

Occupied square feet

65,924

60,858

128,406

188,154

258,094

3,315,032

% of occupied square feet

1.6

%

1.5

%

3.2

%

4.7

%

6.4

%

82.6

%

Notes:

(1) Properties, square feet, occupancy and cap-ex exclude land parcels, properties under development/redevelopment and nonoperational properties. Per square foot amounts are annualized.

(2) Includes 86 same store properties representing 3,362,256 square feet. See pages 16 and 17 for reconciliation.

(3) Excludes all land parcels, developments and investments held for sale. Rental income represents annualized cash base rent for effective lease agreements. The amounts are derived from the current contracted monthly cash base rent, net of collectability reserves, if applicable. Rental income does not include common area maintenance charges, the amortization of above/below market lease intangibles or other non-cash income. Retention includes month-to-month tenants retained.

5

Investment

(dollars in thousands at Welltower pro rata ownership)

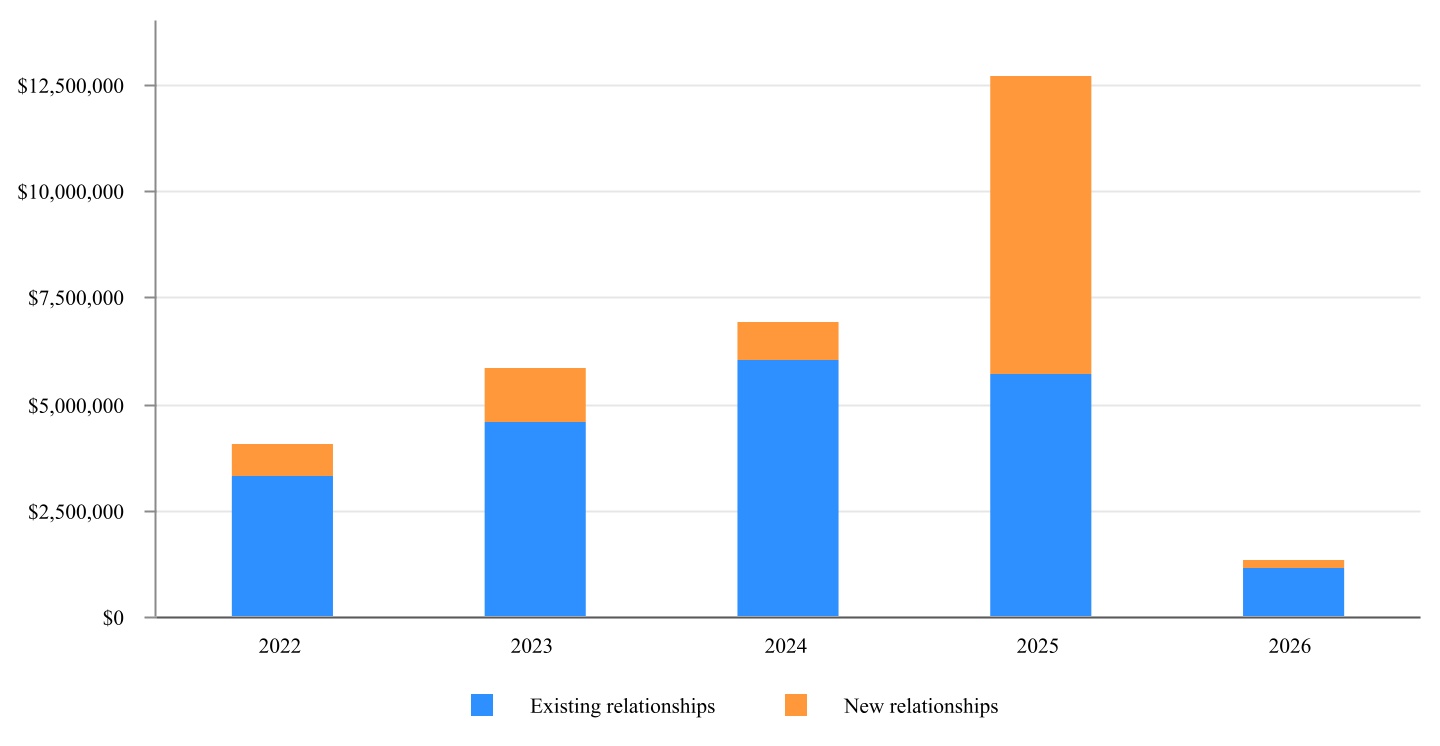

Relationship Investment History

Detail of Acquisitions/JVs(1)

2022

2023

2024

2025

1Q26

22-26 Total

Count

27

52

54

90

34

257

Total

$

2,785,739

$

4,222,706

$

5,287,140

$

17,566,127

$

1,374,866

$

31,236,578

Low

6,485

2,950

970

4,825

259

259

Median

66,074

65,134

39,863

52,894

26,904

48,899

High

389,149

644,443

936,814

6,644,176

206,230

6,644,176

Investment Timing

Acquisitions and Loan Funding(2)

Yield

Construction Conversions(3)

Year 1 Yield

Dispositions and Loan Repayments

Yield

January

$

421,410

8.6

%

$

10,242

1.0

%

$

554,763

6.3

%

February

930,790

7.5

%

57,317

(1.6)

%

1,163,973

7.6

%

March

1,863,160

7.4

%

—

—

%

1,060,809

8.3

%

Total

$

3,215,360

7.6

%

$

67,559

(1.2)

%

$

2,779,545

7.6

%

Notes:

(1) Includes non-yielding asset acquisitions.

(2) Includes advances for non-real estate loans. Excludes land acquisitions and advances for development loans.

(3) Includes expansion conversions and excludes in substance real estate investments.

6

Investment

(dollars in thousands at Welltower pro rata ownership, except per bed / unit / square foot)

Gross Investment Activity

First Quarter 2026

Properties

Beds / Units / Square Feet

Investment Per Bed / Unit / SqFt

Pro Rata Amount

Yield

Acquisitions and Loan Funding(1)

Seniors Housing Operating

32

4,105

units

$

254,971

$

1,069,602

Seniors Housing Triple-net

6

414

units

326,649

135,233

Outpatient Medical

1

134,307

sf

729

97,919

Long-Term/Post-Acute Care

1

116

beds

81,466

72,112

Loan funding

1,840,494

Total acquisitions and loan funding(2)

40

3,215,360

7.6

%

Development Funding(3)

Development projects:

Seniors Housing Operating

44

4,233

units

63,066

Outpatient Medical

—

—

sf

8,291

Total development projects

44

71,357

Redevelopment and expansion projects:

Seniors Housing Operating

1

28

units

2,327

Total development funding

45

73,684

9.6

%

Total gross investments

3,289,044

7.6

%

Dispositions and Loan Repayments(4)

Seniors Housing Operating

4

217

units

62,722

13,611

Seniors Housing Triple-net

2

107

units

44,860

4,800

Outpatient Medical

64

3,393,449

sf

402

1,364,133

Long-Term/Post-Acute Care

35

4,823

beds

111,195

524,397

Loan repayments

872,604

Total dispositions and loan repayments(5)

105

2,779,545

7.6

%

Net investments (dispositions)

$

509,499

Notes:

(1) Acquisitions represent purchase price excluding accounting adjustments pursuant to U.S. GAAP, for all consolidated and unconsolidated property acquisitions. Pro rata amounts include joint venture real estate loans receivable. Loan advances represent cash funded for real estate and non-real estate loans receivable, excluding development loans. Includes acquisition of leaseholds and additional ownership interest in properties, which are both excluded from property, unit and per unit metrics.

(2) Acquisition yields represents annualized contractual or projected cash rent/NOI to be generated divided by investment amount, excluding land parcels. Loan funding yield represents annualized contractual interest divided by investment amount.

(3) Amounts represent cash funded for all developments/expansions including construction in progress, loans and in substance real estate. Yield represents projected annualized cash rent/NOI to be generated upon conversion/stabilization divided by commitment amount.

(4) Amounts represent proceeds received for loan repayments and consolidated and unconsolidated property sales. Includes disposition of partial ownership interest in properties which are excluded from property, unit and per unit metrics.

(5) Yield represents annualized cash rent/interest/NOI that was being generated pre-disposition divided by proceeds. Pro rata amounts include joint venture real estate loans receivable.

7

Investment

(dollars in thousands at Welltower pro rata ownership)

Development Funding Projections(1)

Projected Future Funding

Projects

Beds / Units / Square Feet

Stable Yields(2)

2026 Funding

Funding Thereafter

Total Unfunded Commitments

Committed Balances

Seniors Housing Operating

39

3,686

10.8

%

$

294,679

$

273,164

$

567,843

$

1,214,720

Development Project Conversion Estimates(1)

Quarterly Conversions

Annual Conversions

Amount

Year 1 Yields(2)

Stable Yields(2)

Amount

Year 1 Yields(2)

Stable Yields(2)

1Q26 actual

$

68,348

(1.2)

%

10.4

%

2026 actual

$

68,348

(1.2)

%

10.4

%

2Q26 estimate

202,788

(2.3)

%

10.8

%

2026 estimate

397,708

(1.6)

%

11.1

%

3Q26 estimate

104,110

(0.3)

%

9.7

%

2027 estimate

385,901

(1.2)

%

9.5

%

4Q26 estimate

90,810

(1.7)

%

13.3

%

Thereafter estimate

431,111

0.5

%

11.6

%

Total

$

466,056

(1.6)

%

11.0

%

Total

$

1,283,068

(0.8)

%

10.7

%

Unstabilized Properties

12/31/2025 Properties

Stabilizations

Construction Conversions(1)

Acquisitions/ Dispositions

3/31/2026 Properties

Beds / Units

Seniors Housing Operating

68

(6)

2

3

67

10,012

Seniors Housing Triple-net

7

—

—

—

7

499

Total

75

(6)

2

3

74

10,511

Occupancy

12/31/2025 Properties

Stabilizations

Construction Conversions(3)

Acquisitions/ Dispositions

Progressions

3/31/2026 Properties

0% - 50%

32

—

—

3

(7)

28

50% - 70%

20

(1)

—

—

5

24

70% +

23

(5)

2

—

2

22

Total

75

(6)

2

3

—

74

Occupancy

3/31/2026 Properties

Months In Operation

Revenues

% of Total Revenues(4)

Gross Investment Balance

% of Total Gross Investment

0% - 50%

28

9

$

114,499

0.8

%

$

1,134,147

1.7

%

50% - 70%

24

23

240,239

1.8

%

1,063,887

1.6

%

70% +

22

35

245,563

1.8

%

1,187,599

1.8

%

Total

74

22

$

600,302

4.4

%

$

3,385,633

5.1

%

(1) Includes development projects (construction in progress, development loans and in substance real estate) and excludes expansion projects. Projects expected to be delivered in phases over multiple quarters are reflected in the last quarter.

(2) Actual yields may vary.

(3) Includes expansion and development loan conversions.

(4) Percent of total revenues based on current quarter annualized pro rata total revenues on page 10.

8

Financial

(dollars in thousands at Welltower pro rata ownership)

Components of NAV

Stabilized NOI

Pro rata beds/units/square feet

Seniors Housing Operating(1)

$

3,039,492

162,658

units

Seniors Housing Triple-net

623,092

29,111

units

Outpatient Medical

117,408

4,130,660

square feet

Long-Term/Post-Acute Care

584,452

40,240

beds

Total In-Place NOI(2)

4,364,444

Incremental stabilized NOI(3)

141,896

Total stabilized NOI

$

4,506,340

Obligations

Lines of credit and commercial paper(4)

$

—

Senior unsecured notes(4)

15,203,031

Secured debt(4)

3,532,517

Financing lease liabilities

527,174

Total debt

19,262,722

Add (Subtract):

Other liabilities (assets), net(5)

306,448

Cash and cash equivalents and restricted cash

(4,861,519)

Net obligations

$

14,707,651

Other Assets

Land parcels(6)

423,515

Effective Interest Rate(9)

Real estate loans receivable(7)

4,131,005

8.8%

Non-real estate loans receivable(8)

231,974

10.0%

Joint venture real estate loans receivables(10)

227,219

5.7%

Property dispositions(11)

1,144,138

Development properties:(12)

Current balance

653,352

Unfunded commitments

578,262

Committed balances

$

1,231,614

Projected yield

10.8

%

Projected NOI

$

133,014

Common shares outstanding(13)

726,394

Notes:

(1) Includes $18,894,000 attributable to our proportional share of income (loss) from unconsolidated management company investments.

(3) Represents incremental NOI from Seniors Housing Operating unstabilized properties.

(4) Represents principal amounts due and does not include unamortized premiums/discounts, deferred loan expenses or other fair value adjustments as reflected on the balance sheet. Includes $850,566,000 of foreign secured debt and $370,880,000 of failed sale-leaseback financing obligations.

(5) Includes liabilities / (assets) that impact cash or NOI and excludes non-real estate loans and non-cash items such as straight-line rent receivable, unearned revenues, intangible assets and above/below market lease intangibles.

(6) Includes land parcels and predevelopment projects.

(7) Represents $4,150,715,000 of real estate loans, excluding development loans and including certain in substance real estate developments and held to maturity debt securities, net of $19,710,000 of credit allowances.

(8) Represents $238,580,000 of non-real estate loans, net of $6,606,000 of credit allowances.

(9) Average cash-pay interest rates are 8.2%, 3.3% and 5.7% for real estate, non-real estate loans and joint venture real estate loans, respectively. Rates exclude non-accrual/interest-free loans.

(10) Represents our partners' share of Welltower loans made to select joint ventures secured by the joint venture owned properties.

(11) Represents proceeds from expected property dispositions in the next twelve months.

(12) Includes expansion projects. Includes partial conversions to date.

(13) Includes March 31, 2026 common shares, OP Units and DownREIT Units outstanding and the dilutive impact of exchangeable senior unsecured notes.

9

Financial

(dollars in thousands at Welltower pro rata ownership)

Net Operating Income(1)

1Q25

2Q25

3Q25

4Q25

1Q26

Revenues:

Seniors Housing Operating

Resident fees and services

$

1,897,810

$

2,003,039

$

2,100,724

$

2,588,078

$

2,814,403

Other income

3,417

4,528

8,966

19,481

9,385

Total revenues

1,901,227

2,007,567

2,109,690

2,607,559

2,823,788

Seniors Housing Triple-net

Rental income

103,399

104,360

99,423

167,485

191,086

Interest income

2,111

—

—

—

—

Other income

32

346

91

537

40

Total revenues

105,542

104,706

99,514

168,022

191,126

Outpatient Medical

Rental income

212,554

213,552

217,188

147,701

75,430

Other income

2,139

2,166

2,050

1,161

1,094

Total revenues

214,693

215,718

219,238

148,862

76,524

Long-Term/Post-Acute Care

Rental income

145,439

165,214

184,261

211,841

191,595

Interest income

—

—

—

—

8,077

Other income

199

14

194

5

192

Total revenues

145,638

165,228

184,455

211,846

199,864

Corporate

Interest income

63,572

65,256

70,477

56,158

85,414

Other income

34,179

30,512

52,439

31,513

41,225

Total revenues

97,751

95,768

122,916

87,671

126,639

Total

Resident fees and services

1,897,810

2,003,039

2,100,724

2,588,078

2,814,403

Rental income

461,392

483,126

500,872

527,027

458,111

Interest income

65,683

65,256

70,477

56,158

93,491

Other income

39,966

37,566

63,740

52,697

51,936

Total revenues

2,464,851

2,588,987

2,735,813

3,223,960

3,417,941

Property operating expenses:

Seniors Housing Operating

1,410,579

1,464,457

1,530,131

1,902,889

2,042,868

Seniors Housing Triple-net

5,190

4,817

4,496

4,490

4,827

Outpatient Medical

66,804

65,197

65,851

45,000

20,184

Long-Term/Post-Acute Care

3,495

3,705

3,609

2,974

2,893

Corporate

4,054

4,740

6,025

6,261

14,208

Total property operating expenses

1,490,122

1,542,916

1,610,112

1,961,614

2,084,980

Net operating income:

Seniors Housing Operating

490,648

543,110

579,559

704,670

780,920

Seniors Housing Triple-net

100,352

99,889

95,018

163,532

186,299

Outpatient Medical

147,889

150,521

153,387

103,862

56,340

Long-Term/Post-Acute Care

142,143

161,523

180,846

208,872

196,971

Corporate

93,697

91,028

116,891

81,410

112,431

Net operating income

$

974,729

$

1,046,071

$

1,125,701

$

1,262,346

$

1,332,961

Note:

(1) Please see discussion of Supplemental Reporting Measures on page 15. Includes amounts from investments sold or held for sale. NOI related to OP Unit and DownREIT ownership included at 100%.

10

Financial

(dollars in thousands)

Leverage and EBITDA Reconciliations(1)

Twelve Months Ended

Three Months Ended

March 31, 2026

March 31, 2026

Net income (loss)

$

1,456,895

$

752,324

Interest expense

699,708

192,715

Income tax expense (benefit)

10,036

11,633

Depreciation and amortization

2,221,751

622,752

EBITDA

4,388,390

1,579,424

Loss (income) from unconsolidated entities

17,246

1,686

Stock-based compensation

1,555,786

17,434

Loss (gain) on extinguishment of debt, net

3,816

727

Loss (gain) on real estate dispositions and acquisitions of controlling interests, net

(1,817,666)

(420,400)

Impairment of assets

73,707

4,826

Provision for loan losses, net

(5,777)

1,632

Loss (gain) on derivatives and financial instruments, net

25,617

—

Other expenses

248,278

61,137

Casualty losses, net of recoveries

10,565

3,040

Other impairment(2)

604

—

Total adjustments

112,176

(329,918)

Adjusted EBITDA

$

4,500,566

$

1,249,506

Interest Coverage Ratios

Interest expense

$

699,708

$

192,715

Capitalized interest

30,728

8,449

Non-cash interest expense

(49,166)

(10,162)

Total interest

$

681,270

$

191,002

EBITDA

$

4,388,390

$

1,579,424

Interest coverage ratio

6.44

x

8.27

x

Adjusted EBITDA

$

4,500,566

$

1,249,506

Adjusted Interest coverage ratio

6.61

x

6.54

x

Fixed Charge Coverage Ratios

Total interest

$

681,270

$

191,002

Secured debt principal amortization

67,019

17,056

Total fixed charges

$

748,289

$

208,058

EBITDA

$

4,388,390

$

1,579,424

Fixed charge coverage ratio

5.86

x

7.59

x

Adjusted EBITDA

$

4,500,566

$

1,249,506

Adjusted Fixed charge coverage ratio

6.01

x

6.01

x

Net Debt to EBITDA Ratios

Total debt(3)

$

18,455,978

Less: cash and cash equivalents and restricted cash

(4,819,293)

Net debt

$

13,636,685

EBITDA Annualized

$

6,317,696

Net debt to EBITDA ratio

2.16

x

Adjusted EBITDA Annualized

$

4,998,024

Net debt to Adjusted EBITDA ratio

2.73

x

Notes:

(1) Please see discussion of Supplemental Reporting Measures on page 15.

(2) Represents the write-off of straight-line rent receivable and unamortized lease incentive balances related to leases placed on cash recognition.

(3) Includes unamortized premiums/discounts, other fair value adjustments, financing lease liabilities of $522,410,000 and failed sale-leaseback financing obligations of $370,880,000. Excludes operating lease liabilities of $1,528,863,000 related to ASC 842.

11

Financial

(in thousands except share price)

Leverage and Current Capitalization(1)

% of Total

Book capitalization

Lines of credit and commercial paper(2)

$

—

—

%

Long-term debt obligations(2)(3)

18,455,978

31.51

%

Cash and cash equivalents and restricted cash

(4,819,293)

(8.23)

%

Net debt to consolidated book capitalization

$

13,636,685

23.28

%

Total equity and noncontrolling interests(4)

44,929,270

76.72

%

Consolidated book capitalization

$

58,565,955

100.00

%

Joint venture debt, net(5)

528,442

Total book capitalization

$

59,094,397

Undepreciated book capitalization

Lines of credit and commercial paper(2)

$

—

—

%

Long-term debt obligations(2)(3)

18,455,978

26.60

%

Cash and cash equivalents and restricted cash

(4,819,293)

(6.95)

%

Net debt to consolidated undepreciated book capitalization

$

13,636,685

19.65

%

Accumulated depreciation and amortization

10,822,151

15.60

%

Total equity and noncontrolling interests(4)

44,929,270

64.75

%

Consolidated undepreciated book capitalization

$

69,388,106

100.00

%

Joint venture debt, net(5)

528,442

Total undepreciated book capitalization

$

69,916,548

Enterprise value

Lines of credit and commercial paper(2)

$

—

—

%

Long-term debt obligations(2)(3)

18,455,978

11.98

%

Cash and cash equivalents and restricted cash

(4,819,293)

(3.13)

%

Net debt to consolidated enterprise value

$

13,636,685

8.85

%

Common shares outstanding

704,687

Period end share price

197.71

Common equity market capitalization

$

139,323,667

90.41

%

Noncontrolling interests(4)

1,135,595

0.74

%

Consolidated enterprise value

$

154,095,947

100.00

%

Joint venture debt, net(5)

528,442

Total enterprise value

$

154,624,389

Secured debt as % of total assets

Secured debt(2)

$

2,773,856

3.55

%

Gross asset value(6)

$

78,042,707

Total debt as % of gross asset value

Total debt(2)(3)

$

18,455,978

23.65

%

Gross asset value(6)

$

78,042,707

Unsecured debt as % of unencumbered assets

Unsecured debt(2)

$

15,159,712

21.18

%

Unencumbered gross assets(7)

$

71,578,405

Notes:

(1) Please see discussion of Supplemental Reporting Measures on page 15.

(2) Amounts include unamortized premiums/discounts and other fair value adjustments as reflected on the balance sheet.

(3) Includes financing lease liabilities of $522,410,000 and failed sale-leaseback financing obligations of $370,880,000. Excludes operating lease liabilities of $1,528,863,000 related to ASC 842.

(4) Includes all noncontrolling interests (redeemable and permanent) as reflected on our balance sheet.

(5) Net of Welltower's share of unconsolidated debt and minority partners' share of Welltower consolidated debt.

(6) Gross asset value equals total assets plus accumulated depreciation as reflected on the balance sheet.

(7) Unencumbered gross assets equal gross asset value for consolidated properties that are not financed with secured debt.

12

Financial

(dollars in thousands)

Debt Maturities and Scheduled Principal Amortization(1)

Year

Lines of Credit and Commercial Paper(2)

Senior Unsecured Notes(3)

Consolidated Secured Debt

Noncontrolling Interests' Share of Consolidated Debt

Share of Unconsolidated Secured Debt

Combined Debt(4)

% of Total

Wtd. Avg. Interest Rate (5)

2026

$

—

$

2,668,941

$

227,324

$

(2,305)

$

39,579

$

2,933,539

15.97

%

4.35

%

2027

—

714,980

351,366

(2,344)

133,541

1,197,543

6.52

%

3.31

%

2028

—

2,525,010

189,887

(328)

32,130

2,746,699

14.96

%

3.83

%

2029

—

2,179,674

416,690

(95,567)

22,657

2,523,454

13.74

%

3.39

%

2030

—

1,750,000

157,587

(326)

1,473

1,908,734

10.39

%

3.86

%

2031

—

1,350,000

59,306

(343)

373,220

1,782,183

9.70

%

3.47

%

2032

—

1,050,000

70,974

(354)

49,728

1,170,348

6.37

%

3.49

%

2033

—

—

419,389

(36,866)

649

383,172

2.09

%

4.82

%

2034

—

659,100

204,165

(8,051)

679

855,893

4.66

%

4.41

%

2035

—

1,250,000

42,236

(551)

21,961

1,313,646

7.15

%

5.06

%

Thereafter

—

1,150,000

399,598

(140)

—

1,549,458

8.45

%

4.98

%

Totals

$

—

$

15,297,705

$

2,538,522

$

(147,175)

$

675,617

$

18,364,669

100.00

%

Weighted Avg. Interest Rate(5)

—

%

3.94

%

4.04

%

4.46

%

5.32

%

4.00

%

Weighted Avg. Maturity Years

—

4.8

6.7

4.5

4.2

5.0

% Floating Rate Debt(5)

—

%

17.18

%

9.39

%

64.33

%

0.04

%

15.10

%

Debt by Local Currency(1)

Lines of Credit and Commercial Paper(2)

Senior Unsecured Notes(3)

Consolidated Secured Debt

Noncontrolling Interests' Share of Consolidated Debt

Share of Unconsolidated Secured Debt

Combined Debt(4)

Investment Hedges(6)

United States

$

—

$

11,729,674

$

1,721,942

$

(131,959)

$

626,415

$

13,946,072

$

—

United Kingdom

—

1,384,110

—

—

—

1,384,110

11,640,639

Canada

—

2,183,921

816,580

(15,216)

49,202

3,034,487

6,505,742

Totals

$

—

$

15,297,705

$

2,538,522

$

(147,175)

$

675,617

$

18,364,669

$

18,146,381

Notes:

(1) Represents principal amounts due excluding unamortized premiums/discounts or other fair value adjustments as reflected on the balance sheet.

(2) Our unsecured commercial paper program and our unsecured revolving credit facility had a zero balance as of March 31, 2026. The unsecured revolving credit facility is comprised of a $2,000,000,000 tranche that matures on July 24, 2029 and a $4,250,000,000 tranche that matures on March 6, 2030. The $4,250,000,000 tranche may be extended for two successive terms of six months at our option. Commercial paper borrowings are backstopped by the unsecured revolving credit facility.

(3) Senior Unsecured Notes include the following:

•2026 includes CAD $2,747,615,000 of unsecured term loans (approximately $1,968,941,000 USD at March 31, 2026) that mature on October 9, 2026, and bear interest at adjusted CORRA + 0.70%.

•2027 includes CAD $300,000,000 of 2.95% senior unsecured notes (approximately $214,980,000 USD at March 31, 2026) that mature on January 15, 2027.

•2028 includes $1,035,000,000 of 2.75% exchangeable senior unsecured notes that mature on May 15, 2028 unless earlier exchanged, purchased or redeemed.

•2028 also includes £550,000,000 of 4.80% senior unsecured notes (approximately $725,010,000 USD at March 31, 2026). The notes mature on November 20, 2028.

•2029 includes $1,035,000,000 of 3.125% exchangeable senior unsecured notes that mature on July 15, 2029 unless earlier exchanged, purchased or redeemed.

•2034 includes £500,000,000 of 4.50% senior unsecured notes (approximately $659,100,000 USD at March 31, 2026). The notes mature on December 1, 2034.

(4) Excludes operating lease liabilities of $1,528,863,000, finance lease liabilities of $522,410,000 and failed sale-leaseback financing obligations of $370,880,000 related to ASC 842.

(5) Based on variable interest rates and foreign currency exchange rates in effect as of March 31, 2026. The interest rate on the unsecured revolving credit facility is SOFR + 0.655%. Commercial paper, senior notes and secured debt average interest rate represents the face value note rate. Includes the impact of notional swaps and caps to convert fixed rate debt to SOFR-based floating rate debt, and SOFR-based floating rate debt and CORRA-based floating rate debt to fixed rate debt.

(6) Represents notional value of foreign currency derivative contracts at end of period spot FX rates. The fair market value of the gains (losses) of these contracts is currently USD $(74,239,000), as represented in other assets (liabilities) on the balance sheet. We supplement our local currency debt with foreign currency derivative contracts to offset the translation and economic exposures related to our international investments. Currently, our foreign currency derivatives are comprised of cross-currency swaps.

13

Glossary

Age: Current year, less the year built, adjusted for major renovations. Average age is weighted by pro rata NOI.

Cap-ex, Tenant Improvements, Leasing Commissions: Represents amounts incurred for: 1) recurring and non-recurring capital expenditures required to maintain and re-tenant our properties; 2) second generation tenant improvements; and 3) leasing commissions paid to third party leasing agents to secure new tenants. Excludes sustainability investments.

Construction Conversion: Represents completed construction projects that were placed into service and began generating NOI.

EBITDAR: Earnings before interest, taxes, depreciation, amortization and rent. The company uses unaudited, periodic financial information provided solely by tenants/borrowers to calculate EBITDAR and has not independently verified the information.

EBITDAR Coverage: Represents the ratio of EBITDAR to contractual rent for leases or interest and principal payments for loans. EBITDAR coverage is a measure of a property’s ability to generate sufficient cash flows for the operator/borrower to pay rent and meet other obligations. The coverage shown excludes properties that are unstabilized, closed or for which data is not available or meaningful.

EBITDARM: Earnings before interest, taxes, depreciation, amortization, rent and management fees. The company uses unaudited, periodic financial information provided solely by tenants/borrowers to calculate EBITDARM and has not independently verified the information.

EBITDARM Coverage: Represents the ratio of EBITDARM to contractual rent for leases or interest and principal payments for loans. EBITDARM coverage is a measure of a property’s ability to generate sufficient cash flows for the operator/borrower to pay rent and meet other obligations, assuming that management fees are not paid. The coverage shown excludes properties that are unstabilized, closed or for which data is not available or meaningful.

Health System - Affiliated: Outpatient medical properties are considered affiliated with a health system if one or more of the following conditions are met: 1) the land parcel is contained within the physical boundaries of a hospital campus; 2) the land parcel is located adjacent to the campus; 3) the building is physically connected to the hospital regardless of the land ownership structure; 4) a ground lease is maintained with a health system entity; 5) a master lease is maintained with a health system entity; 6) significant square footage is leased to a health system entity; 7) the property includes an ambulatory surgery center with a hospital partnership interest; or 8) a significant square footage is leased to a physician group that is either employed, directly or indirectly by a health system, or has a significant clinical and financial affiliation with the health system.

Long-Term/Post-Acute Care: Includes all skilled nursing, rehabilitation and long-term/post-acute care facilities where the majority of individuals require 24-hour nursing or medical care. Generally, these properties are licensed for Medicaid and/or Medicare reimbursement and are subject to triple-net operating leases. Most of these facilities focus on higher acuity patients and offer rehabilitation units specializing in cardiac, orthopedic, dialysis, neurological or pulmonary rehabilitation.

MSA: For the United States and Canada, we use the Metropolitan Statistical Area as defined by the U.S. Census Bureau and the Census Metropolitan Areas as defined by Statistics Canada, respectively. For the United Kingdom, we generally use the Metro Region as defined by EuroStat with Greater London defined as a 55-mile radius around the city’s center.

Occupancy: Outpatient Medical occupancy represents the percentage of total rentable square feet leased and occupied, including month-to-month leases, as of the date reported. Occupancy for all other property types represents average quarterly operating occupancy based on the most recent quarter of available data and excludes properties that are unstabilized, closed or for which data is not available or meaningful. The company uses unaudited, periodic financial information provided solely by tenants/borrowers to calculate occupancy and has not independently verified the information. Occupancy metrics are reflected at our pro rata share.

Outpatient Medical: Outpatient medical buildings include properties offering ambulatory medical services such as primary and secondary care, outpatient surgery, diagnostic procedures and rehabilitation. These properties are typically affiliated with a health system and may be located on a hospital campus. They are specifically designed and constructed for use by healthcare professionals to provide services to patients. They also include medical office buildings that typically contain sole and group physician practices and may provide laboratory and other specialty services.

Seniors Housing Operating (SHO): Includes independent, assisted living and dementia care properties in the U.S. and Canada and all care homes in the U.K. generally structured to take advantage of the REIT Investment Diversification and Empowerment Act of 2007, as well as Wellness Housing properties.

Seniors Housing Triple-net (SH-NNN): Includes independent, assisted living and dementia care properties in the U.S. and Canada and all care homes in the U.K. subject to triple-net operating leases.

Square Feet: Net rentable square feet calculated utilizing Building Owners and Managers Association measurement standards.

Stable: Generally, a triple-net rental property is considered stable (versus unstabilized or under development) when it has achieved EBITDAR coverage of 1.00x or greater for three consecutive months or, if targeted performance has not been achieved, 12 months following the budgeted stabilization date. Triple-net properties for which income is recognized on a cash basis and for which substantially all contractual rent during the period has not been collected are excluded from the stable portfolio. A Seniors Housing Operating facility is considered stable upon the earliest of 90% occupancy, NOI at or above the underwritten target or 12 months past the underwritten stabilization date. Excludes assets held for sale and assets disposed of during the current quarter.

Unstabilized: An acquisition that does not meet the stable criteria upon closing or a construction property that has opened but not yet reached stabilization.

14

Supplemental Reporting Measures

We believe that revenues and net income, as defined by U.S. generally accepted accounting principles ("U.S. GAAP"), are the most appropriate earnings measurements. However, we consider EBITDA, Adjusted EBITDA, RevPOR, ExpPOR, SS RevPOR, SS ExpPOR, NOI, In-Place NOI ("IPNOI") and Same Store NOI ("SSNOI") to be useful supplemental measures of our operating performance. Excluding EBITDA and Adjusted EBITDA, these supplemental measures are disclosed on our pro rata ownership basis. Pro rata amounts are derived by reducing consolidated amounts for minority partners’ noncontrolling ownership interests and adding our minority ownership share of unconsolidated amounts. We do not control unconsolidated investments. While we consider pro rata disclosures useful, they may not accurately depict the legal and economic implications of our joint venture arrangements and should be used with caution.

We define NOI as total revenues, including tenant reimbursements, less property operating expenses. Property operating expenses represent costs associated with managing, maintaining and servicing tenants for our properties. These expenses include, but are not limited to, property-related payroll and benefits, property management fees paid to managers, marketing, housekeeping, food service, maintenance, utilities, property taxes and insurance. General and administrative expenses represent general overhead costs that are unrelated to property operations and are unallocable to the properties. These expenses include, but are not limited to, payroll and benefits related to corporate employees, professional services, office expenses and depreciation of corporate fixed assets. IPNOI represents cash NOI excluding interest income, other income and non-IPNOI and adjusted for timing of current quarter portfolio changes such as acquisitions, development conversions, segment transitions and dispositions. Properties classified as held for sale and leased properties are excluded from IPNOI. SSNOI is used to evaluate the operating performance of our properties using a consistent population which controls for changes in the composition of our portfolio. As used herein, same store is generally defined as those revenue-generating properties in the portfolio for the relevant year-over-year reporting periods. Acquisitions and development conversions are included in the same store amounts five full quarters after acquisition or being placed into service. Land parcels, loans and leased properties, as well as any properties sold or classified as held for sale during the period, are excluded from the same store amounts. Redeveloped properties (including major refurbishments of a Seniors Housing Operating property where 20% or more of units are simultaneously taken out of commission for 30 days or more or Outpatient Medical properties undergoing a change in intended use) are excluded from the same store amounts until five full quarters post completion of the redevelopment. Properties undergoing operator transitions and/or segment transitions are also excluded from the same store amounts until five full quarters post completion of the operator transition or segment transition. In addition, properties significantly impacted by force majeure, acts of God or other extraordinary adverse events are excluded from same store amounts until five full quarters after the properties are placed back into service. SSNOI excludes non-cash NOI and includes adjustments to present consistent property ownership percentages and to translate Canadian properties and UK properties using a consistent exchange rate. Normalizers include adjustments that in management’s opinion are appropriate in considering SSNOI, a supplemental, non-GAAP performance measure. None of these adjustments, which may increase or decrease SSNOI, are reflected in our financial statements prepared in accordance with U.S. GAAP. Significant normalizers (defined as any that individually exceed 0.50% of SSNOI growth per property type) are separately disclosed and explained. We believe NOI, IPNOI and SSNOI provide investors relevant and useful information because they measure the operating performance of our properties at the property level on an unleveraged basis. We use NOI, IPNOI and SSNOI to make decisions about resource allocations and to assess the property level performance of our portfolio.

RevPOR represents the average revenues generated per occupied room per month and ExpPOR represents the average expenses per occupied room per month at our Seniors Housing Operating properties. These metrics are calculated as our pro rata share of total resident fees and services revenues or property operating expenses from the income statement, divided by average monthly occupied room days. SS RevPOR and SS ExpPOR are used to evaluate the RevPOR and ExpPOR performance of our properties under a consistent population, which eliminates changes in the composition of our portfolio. They are based on the same pool of properties used for SSNOI and include any revenue and expense normalizations used for SSNOI. We use RevPOR, ExpPOR, SS RevPOR and SS ExpPOR to evaluate the revenue-generating capacity and profit potential of our Seniors Housing Operating portfolio independent of fluctuating occupancy rates. They are also used in comparison against industry and competitor statistics, if known, to evaluate the quality of our Seniors Housing Operating portfolio.

We measure our credit strength both in terms of leverage ratios and coverage ratios. The leverage ratios indicate how much of our balance sheet capitalization is related to long-term debt, net of cash and restricted cash. We expect to maintain capitalization ratios and coverage ratios sufficient to maintain a capital structure consistent with our current profile. The ratios are based on EBITDA and Adjusted EBITDA. EBITDA is defined as earnings (net income per income statement) before interest expense, income taxes, depreciation and amortization. Adjusted EBITDA is defined as EBITDA excluding unconsolidated entities and including adjustments for stock-based compensation expense, provision for loan losses, gains/losses on extinguishment of debt, gains/losses on disposition of properties and acquisitions of controlling interests, impairment of assets, gains/losses on derivatives and financial instruments, other expenses, other impairment charges and other adjustments deemed appropriate in management's opinion. We believe that EBITDA and Adjusted EBITDA, along with net income, are important supplemental measures because they provide additional information to assess and evaluate the performance of our operations. We primarily use these measures to determine our interest coverage ratio, which represents EBITDA and Adjusted EBITDA divided by total interest, and our fixed charge coverage ratio, which represents EBITDA and Adjusted EBITDA divided by fixed charges. Fixed charges include total interest and secured debt principal amortization. Our leverage ratios include net debt to Adjusted EBITDA, book capitalization, undepreciated book capitalization and consolidated enterprise value. Book capitalization represents the sum of net debt (defined as total long-term debt, excluding operating lease liabilities, less cash and cash equivalents and restricted cash), total equity and redeemable noncontrolling interests. Undepreciated book capitalization represents book capitalization adjusted for accumulated depreciation and amortization. Consolidated enterprise value represents book capitalization adjusted for the fair market value of our common stock. Our leverage ratios are defined as the proportion of net debt to total capitalization.

Our supplemental reporting measures and similarly entitled financial measures are widely used by investors, equity and debt analysts and rating agencies in the valuation, comparison, rating and investment recommendations of companies. Our management uses these financial measures to facilitate internal and external comparisons to historical operating results and in making operating decisions. Additionally, these measures are utilized by the Board of Directors to evaluate management performance. None of the supplemental reporting measures represent net income or cash flow provided from operating activities as determined in accordance with U.S. GAAP and should not be considered as alternative measures of profitability or liquidity. Finally, the supplemental reporting measures, as defined by us, may not be comparable to similarly entitled items reported by other real estate investment trusts or other companies. Multi-period amounts may not equal the sum of the individual quarterly amounts due to rounding.

15

Supplemental Reporting Measures

(dollars in thousands)

Non-GAAP Reconciliations

NOI Reconciliation

1Q25

2Q25

3Q25

4Q25

1Q26

Net income (loss)

$

257,266

$

304,618

$

282,186

$

117,767

$

752,324

Loss (gain) on real estate dispositions and acquisitions of controlling interests, net

(51,777)

(14,850)

(4,025)

(1,378,391)

(420,400)

Loss (income) from unconsolidated entities

(1,263)

7,392

12,610

(4,442)

1,686

Income tax expense (benefit)

(5,519)

1,053

2,335

(4,985)

11,633

Other expenses

14,060

16,598

44,699

125,844

61,137

Impairment of assets

52,402

19,876

3,081

45,924

4,826

Provision for loan losses, net

(2,007)

(1,113)

1,088

(7,384)

1,632

Loss (gain) on extinguishment of debt, net

6,156

—

—

3,089

727

Loss (gain) on derivatives and financial instruments, net

(3,210)

(409)

31,682

(5,656)

—

General and administrative expenses

63,758

64,175

63,124

1,557,378

67,474

Depreciation and amortization

485,869

495,036

509,812

594,151

622,752

Interest expense

144,962

141,157

162,052

203,784

192,715

Consolidated net operating income

960,697

1,033,533

1,108,644

1,247,079

1,296,506

NOI attributable to unconsolidated investments(1)

28,316

26,069

29,337

26,430

48,240

NOI attributable to noncontrolling interests(2)

(14,284)

(13,531)

(12,280)

(11,163)

(11,785)

Pro rata net operating income (NOI)(3)

$

974,729

$

1,046,071

$

1,125,701

$

1,262,346

$

1,332,961

In-Place NOI Reconciliation

At Welltower pro rata ownership

Seniors Housing Operating

Seniors Housing Triple-net

Outpatient Medical

Long-Term /Post-Acute Care

Corporate

Total

Revenues

$

2,823,788

$

191,126

$

76,524

$

199,864

$

126,639

$

3,417,941

Property operating expenses

(2,042,868)

(4,827)

(20,184)

(2,893)

(14,208)

(2,084,980)

NOI(3)

780,920

186,299

56,340

196,971

112,431

1,332,961

Adjust:

Interest income

—

—

—

(8,077)

(85,414)

(93,491)

Other income

(2,020)

(40)

(164)

(192)

(34,444)

(36,860)

Sold / held for sale

(2,359)

(29)

(23,178)

(4,159)

—

(29,725)

Nonoperational(4)

1,259

5

8

(319)

—

953

Non In-Place NOI(5)

(26,419)

(30,491)

(3,654)

(38,242)

7,427

(91,379)

Timing adjustments(6)

8,492

29

—

131

—

8,652

Total adjustments

(21,047)

(30,526)

(26,988)

(50,858)

(112,431)

(241,850)

In-Place NOI

759,873

155,773

29,352

146,113

—

1,091,111

Annualized In-Place NOI

$

3,039,492

$

623,092

$

117,408

$

584,452

$

—

$

4,364,444

Same Store Property Reconciliation

Seniors Housing Operating

Seniors Housing Triple-net

Outpatient Medical

Long-Term /Post-Acute Care

Total

Total properties

1,917

431

141

349

2,838

Recent acquisitions and development conversions(7)

(591)

(174)

(7)

(141)

(913)

Under development

(40)

—

—

—

(40)

Under redevelopment(8)

(2)

—

—

—

(2)

Current held for sale

(16)

—

(42)

(2)

(60)

Land parcels, loans and leased properties

(176)

(4)

(6)

(6)

(192)

Transitions(9)

(163)

(1)

—

(2)

(166)

Other(10)

(8)

—

—

(2)

(10)

Same store properties

921

252

86

196

1,455

Notes:

(1) Represents Welltower's interests in joint ventures where Welltower is the minority partner.

(2) Represents minority partners' interests in joint ventures where Welltower is the majority partner.

(3) Represents Welltower's pro rata share of NOI. See page 10 for more information.

(4) Primarily includes development properties and land parcels.

(5) Primarily represents non-cash NOI and NOI associated with leased properties.

(6) Represents timing adjustments for current quarter acquisitions, construction conversions and segment or operator transitions.

(7) Acquisitions and development conversions will enter the same store pool five full quarters after acquisition or certificate of occupancy.

(8) Redevelopment properties will enter the same store pool after five full quarters of operations post redevelopment completion.

(9) Transitioned properties will enter the same store pool after five full quarters of operations with the new operator in place or under the new structure.

(10) Represents properties that are either closed or being closed.

16

Supplemental Reporting Measures

(dollars in thousands at Welltower pro rata ownership)

Same Store NOI Reconciliation

1Q25

2Q25

3Q25

4Q25

1Q26

Y/o/Y

Seniors Housing Operating

NOI

$

490,648

$

543,110

$

579,559

$

704,670

$

780,920

Non-cash NOI on same store properties

(4,423)

(1,632)

(1,956)

(2,153)

(1,479)

NOI attributable to non-same store properties

(57,288)

(77,535)

(97,717)

(208,753)

(248,830)

Currency and ownership adjustments(1)

6,273

632

(65)

528

(1,500)

Other normalizing adjustments(2)

449

3,801

2,844

2,139

2,706

SSNOI

435,659

468,376

482,665

496,431

531,817

22.1

%

Seniors Housing Triple-net

NOI

100,352

99,889

95,018

163,532

186,299

Non-cash NOI on same store properties

(10,687)

(10,120)

(8,966)

(8,053)

(6,055)

NOI attributable to non-same store properties

(14,996)

(13,588)

(8,781)

(77,489)

(100,016)

Currency and ownership adjustments(1)

3,259

1,859

327

—

(337)

Normalizing adjustments for joint venture recapitalization(3)

(1,394)

(1,394)

(465)

—

—

Other normalizing adjustments(2)

—

—

—

(240)

(353)

SSNOI

76,534

76,646

77,133

77,750

79,538

3.9

%

Outpatient Medical

NOI

147,889

150,521

153,387

103,862

56,340

Non-cash NOI on same store properties

(2,857)

(2,783)

(2,592)

(2,507)

(2,442)

NOI attributable to non-same store properties

(121,744)

(123,951)

(127,151)

(77,562)

(30,000)

Other normalizing adjustments(2)

(3)

(112)

(16)

(3)

(56)

SSNOI

23,285

23,675

23,628

23,790

23,842

2.4

%

Long-Term/Post-Acute Care

NOI

142,143

161,523

180,846

208,872

196,971

Non-cash NOI on same store properties

(16,554)

(16,997)

(16,728)

(16,227)

(16,249)

NOI attributable to non-same store properties

(42,179)

(61,111)

(79,861)

(107,311)

(89,906)

Currency and ownership adjustments(1)

185

126

118

94

(21)

Normalizing adjustment for lease restructure(4)

—

—

—

—

(4,031)

Normalizing adjustments for service agreement termination(5)

970

970

647

—

—

SSNOI

84,565

84,511

85,022

85,428

86,764

2.6

%

Corporate

NOI

93,697

91,028

116,891

81,410

112,431

NOI attributable to non-same store properties

(93,697)

(91,028)

(116,891)

(81,410)

(112,431)

SSNOI

—

—

—

—

—

Total

NOI

974,729

1,046,071

1,125,701

1,262,346

1,332,961

Non-cash NOI on same store properties

(34,521)

(31,532)

(30,242)

(28,940)

(26,225)

NOI attributable to non-same store properties

(329,904)

(367,213)

(430,401)

(552,525)

(581,183)

Currency and ownership adjustments(1)

9,717

2,617

380

622

(1,858)

Normalizing adjustments, net

22

3,265

3,010

1,896

(1,734)

SSNOI

$

620,043

$

653,208

$

668,448

$

683,399

$

721,961

16.4

%

Notes:

(1) Includes adjustments to reflect consistent property ownership percentages, to translate Canadian properties at a USD/CAD rate of 1.43 and to translate UK properties at a GBP/USD rate of 1.23.

(2) Represents aggregate normalizing adjustments which are individually less than 0.50% of SSNOI growth per property type.

(3) Represents normalizing adjustment related to a joint venture recapitalization associated with one Seniors Housing Triple-net lease.

(4) Represents normalizing adjustment related to lease restructures with two Long-Term/Post-Acute Care leases.

(5) Represents normalizing adjustment related to the termination of a service agreement related to one Long-Term/Post-Acute Care lease.

17

Supplemental Reporting Measures

(dollars in thousands, except RevPOR, SS RevPOR and SSNOI/unit)

SHO RevPOR Reconciliation

United States

United Kingdom

Canada

Total

Consolidated SHO revenues

$

1,642,960

$

962,582

$

184,832

$

2,790,374

Unconsolidated SHO revenues attributable to Welltower(1)

46,106

6,965

2,257

55,328

SHO revenues attributable to noncontrolling interests(2)

(19,206)

—

(2,708)

(21,914)

Pro rata SHO revenues(3)

1,669,860

969,547

184,381

2,823,788

Non-cash and non-RevPOR revenues

(3,203)

(772)

(235)

(4,210)

Revenues attributable to non in-place properties

(5,332)

(215,543)

(8,442)

(229,317)

SHO local revenues

1,661,325

753,232

175,704

2,590,261

Average occupied units/month

91,106

29,635

19,676

140,417

RevPOR/month in USD

$

6,163

$

8,590

$

3,018

$

6,234

RevPOR/month in local currency(4)

£

6,984

$

4,311

Reconciliations of SHO SS RevPOR Growth, SSNOI Growth and SSNOI/Unit

United States

United Kingdom

Canada

Total

1Q25

1Q26

1Q25

1Q26

1Q25

1Q26

1Q25

1Q26

SHO SS RevPOR Growth

Consolidated SHO revenues

$

1,396,502

$

1,642,960

$

322,505

$

962,582

$

148,864

$

184,832

$

1,867,871

$

2,790,374

Unconsolidated SHO revenues attributable to WELL(1)

41,589

46,106

4,337

6,965

10,504

2,257

56,430

55,328

SHO revenues attributable to noncontrolling interests(2)

(20,799)

(19,206)

—

—

(2,275)

(2,708)

(23,074)

(21,914)

SHO pro rata revenues(3)

1,417,292

1,669,860

326,842

969,547

157,093

184,381

1,901,227

2,823,788

Non-cash and non-RevPOR revenues on same store properties

(4,912)

(2,275)

—

—

(170)

(241)

(5,082)

(2,516)

Revenues attributable to non-same store properties

(176,782)

(308,226)

(130,012)

(738,669)

(37,042)

(47,154)

(343,836)

(1,094,049)

Currency and ownership adjustments(4)

4,912

—

10,998

(2,994)

4,072

(1,725)

19,982

(4,719)

Other normalizing adjustments(5)

—

(419)

—

—

—

—

—

(419)

SHO SS RevPOR revenues(6)

$

1,240,510

$

1,358,940

$

207,828

$

227,884

$

123,953

$

135,261

$

1,572,291

$

1,722,085

Avg. occupied units/month(7)

67,813

70,912

6,980

7,310

14,326

14,765

89,119

92,987

SHO SS RevPOR(8)

$

6,182

$

6,477

$

10,063

$

10,536

$

2,924

$

3,096

$

5,963

$

6,259

SS RevPOR YOY growth

4.8

%

4.7

%

5.9

%

5.0

%

SHO SSNOI Growth

Consolidated SHO NOI

$

363,213

$

495,848

$

66,561

$

205,996

$

53,413

$

73,169

$

483,187

$

775,013

Unconsolidated SHO NOI attributable to WELL(1)

15,696

17,194

708

1,636

4,142

1,175

20,546

20,005

SHO NOI attributable to noncontrolling interests(2)

(12,024)

(12,761)

—

—

(1,061)

(1,337)

(13,085)

(14,098)

SHO pro rata NOI(3)

366,885

500,281

67,269

207,632

56,494

73,007

490,648

780,920

Non-cash NOI on same store properties

(4,414)

(1,511)

(9)

45

—

(13)

(4,423)

(1,479)

NOI attributable to non-same store properties

(27,127)

(85,790)

(16,336)

(143,205)

(13,825)

(19,835)

(57,288)

(248,830)

Currency and ownership adjustments(4)

2,006

—

2,803

(823)

1,464

(677)