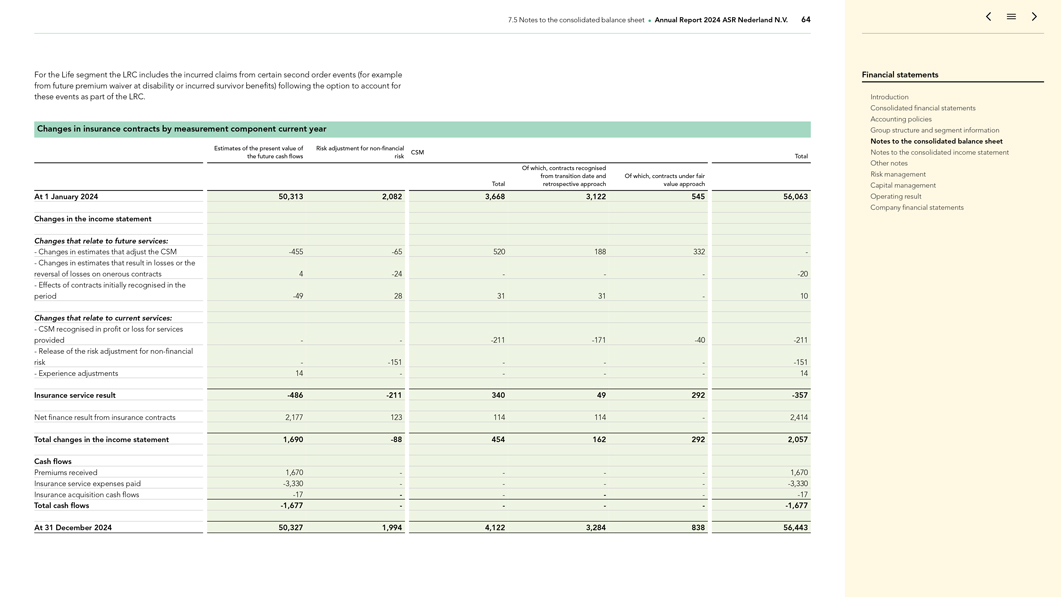

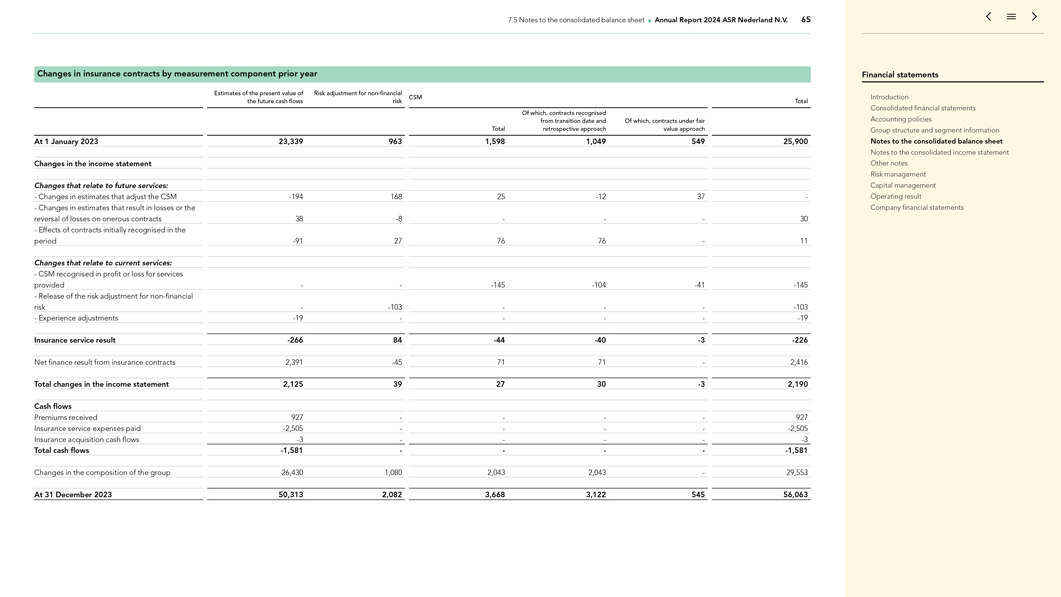

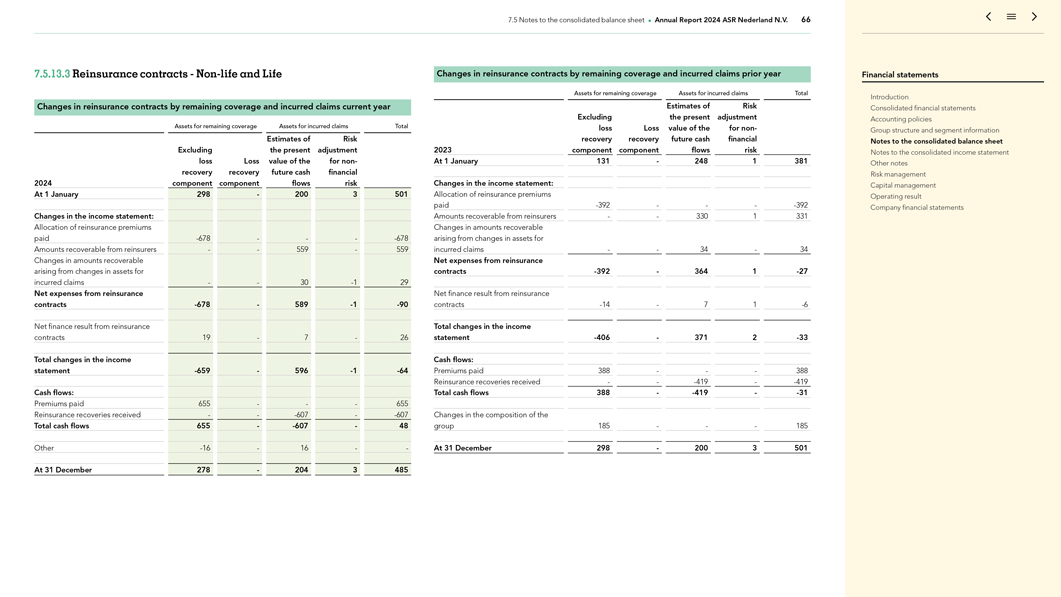

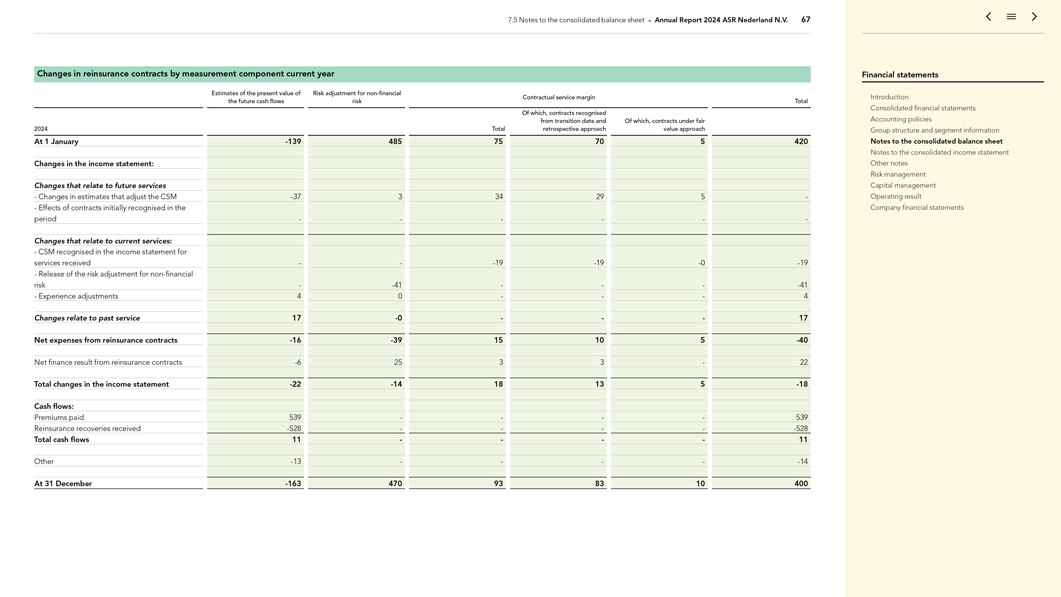

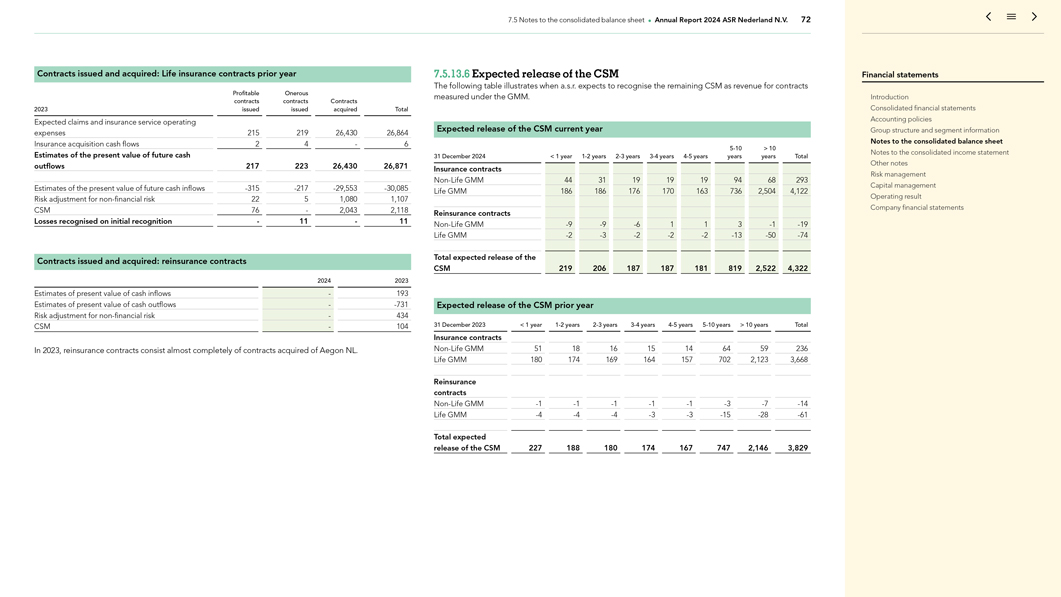

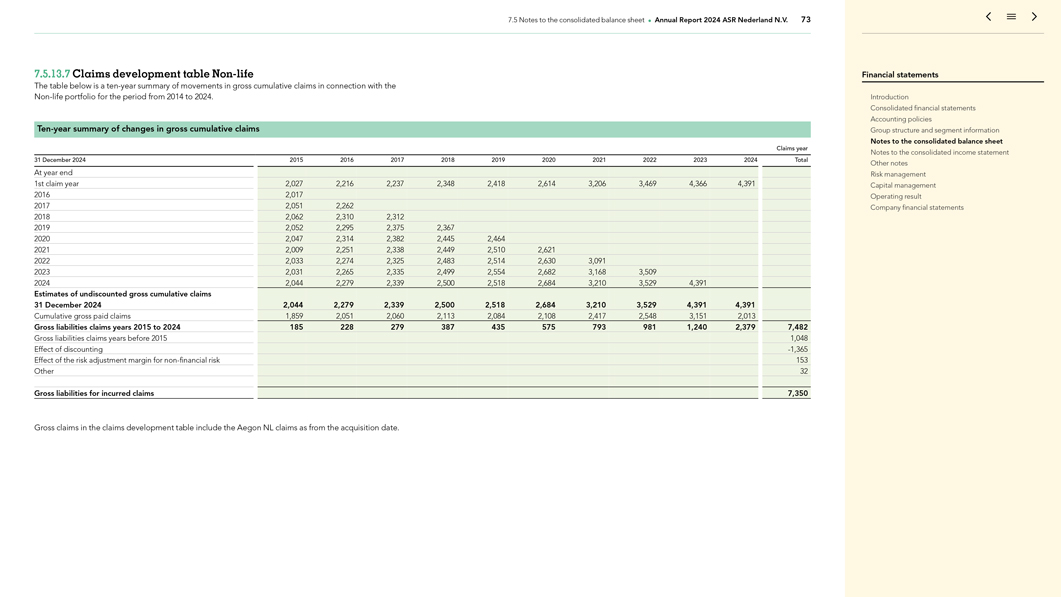

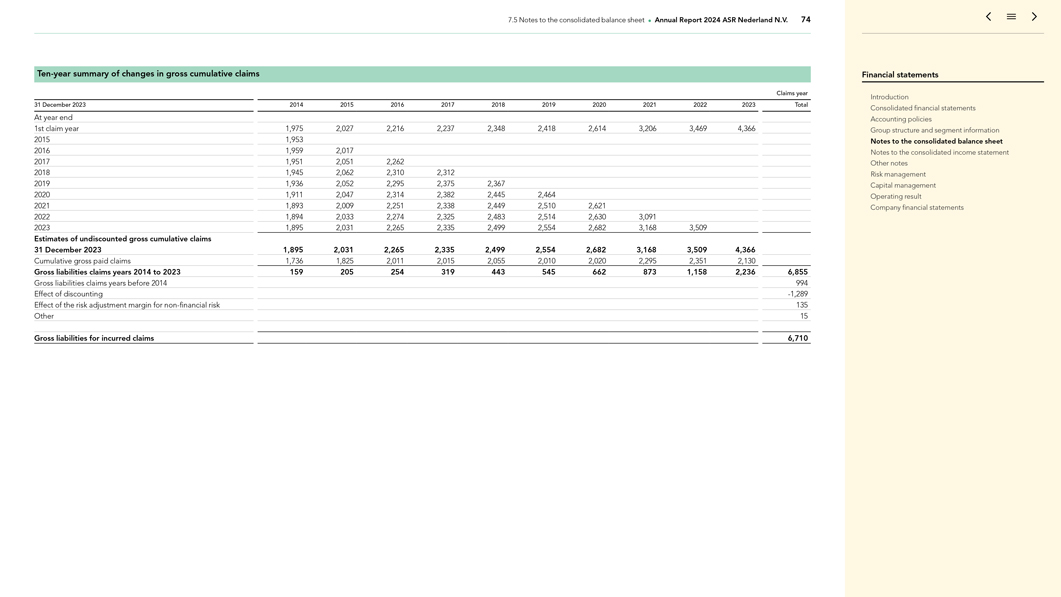

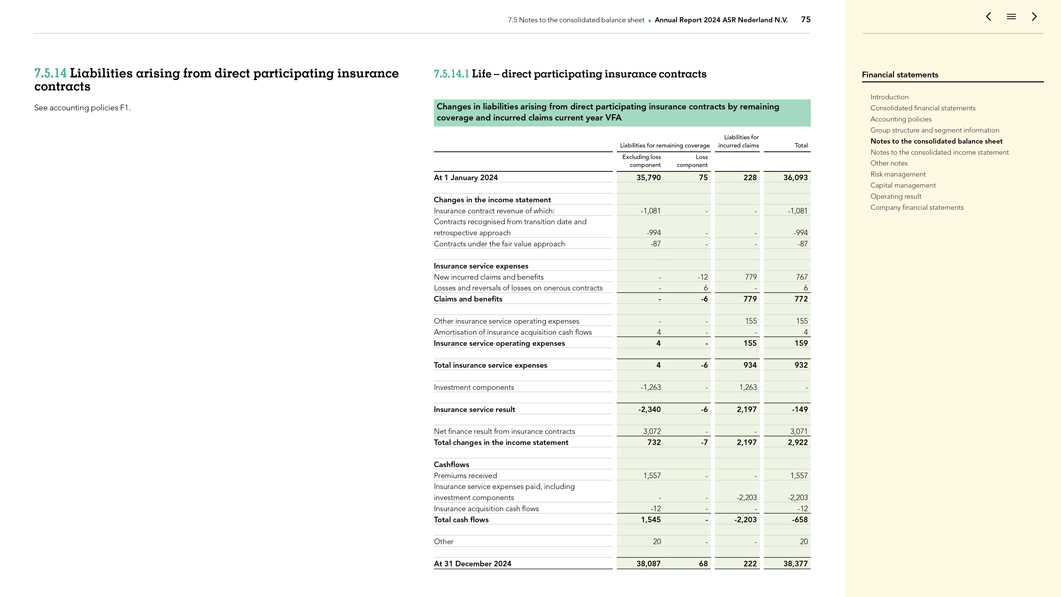

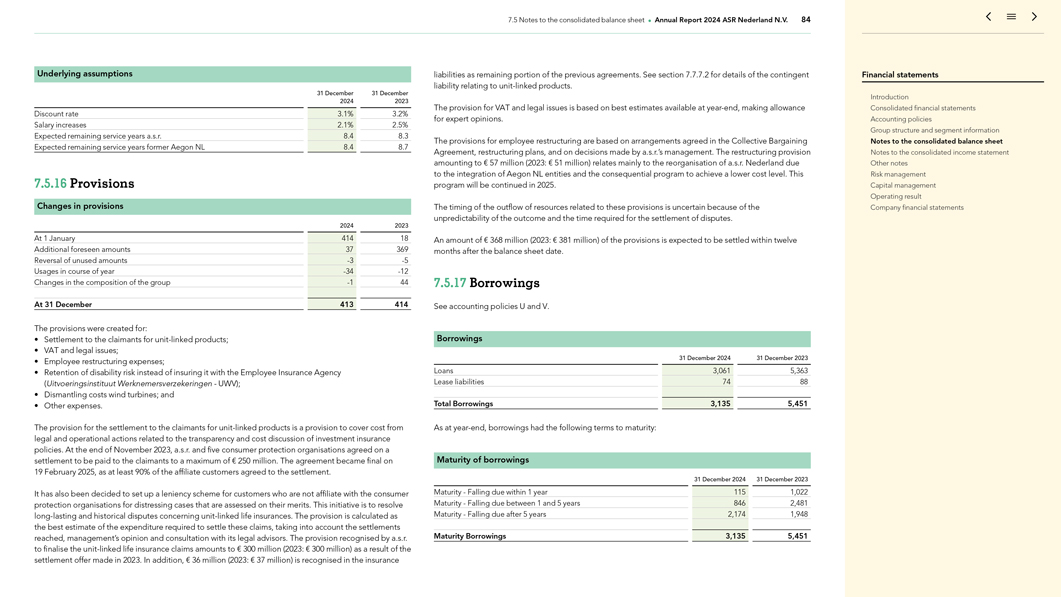

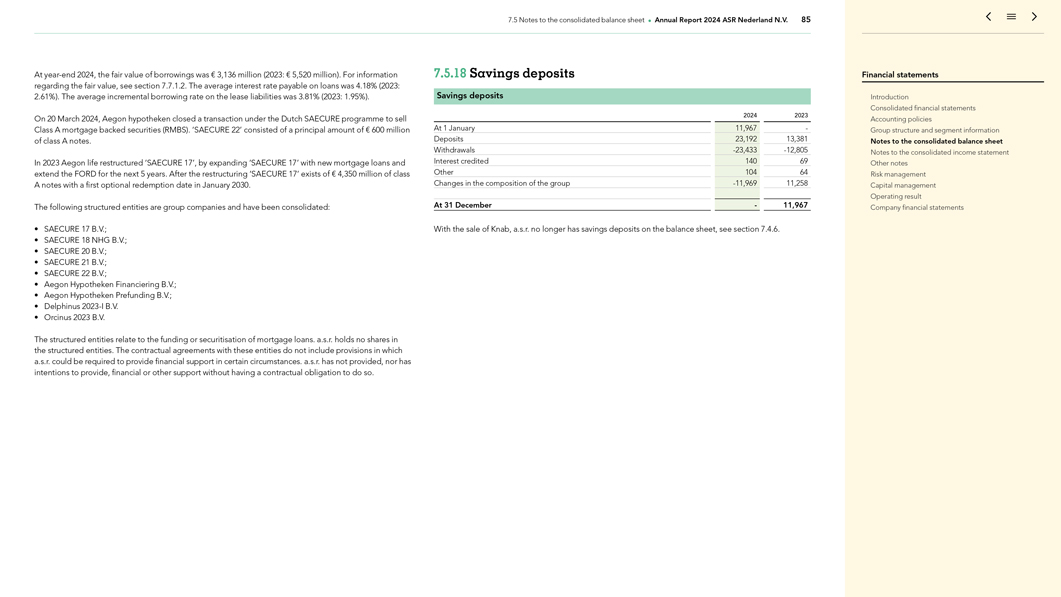

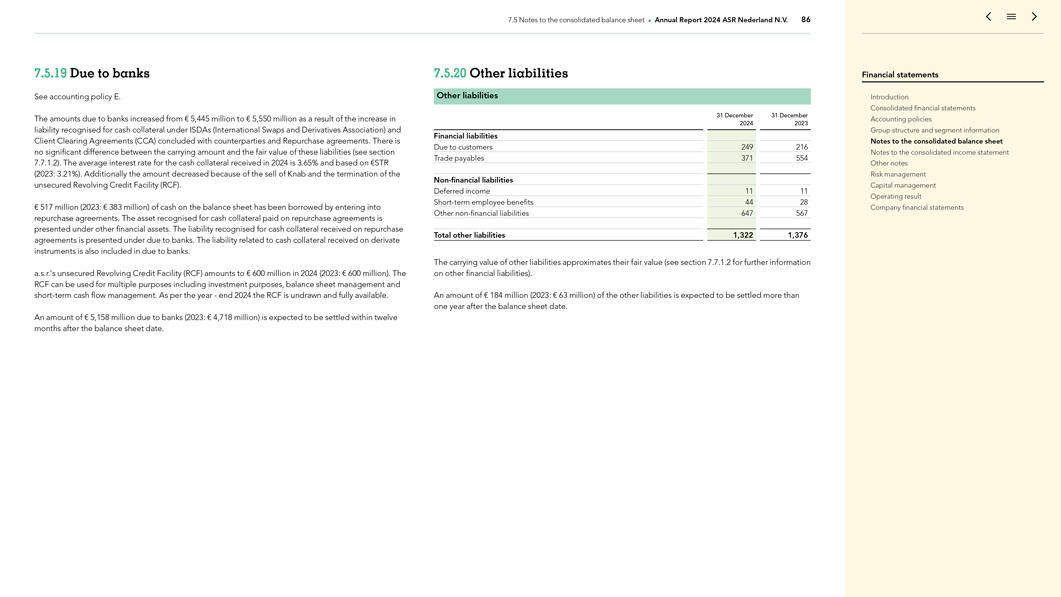

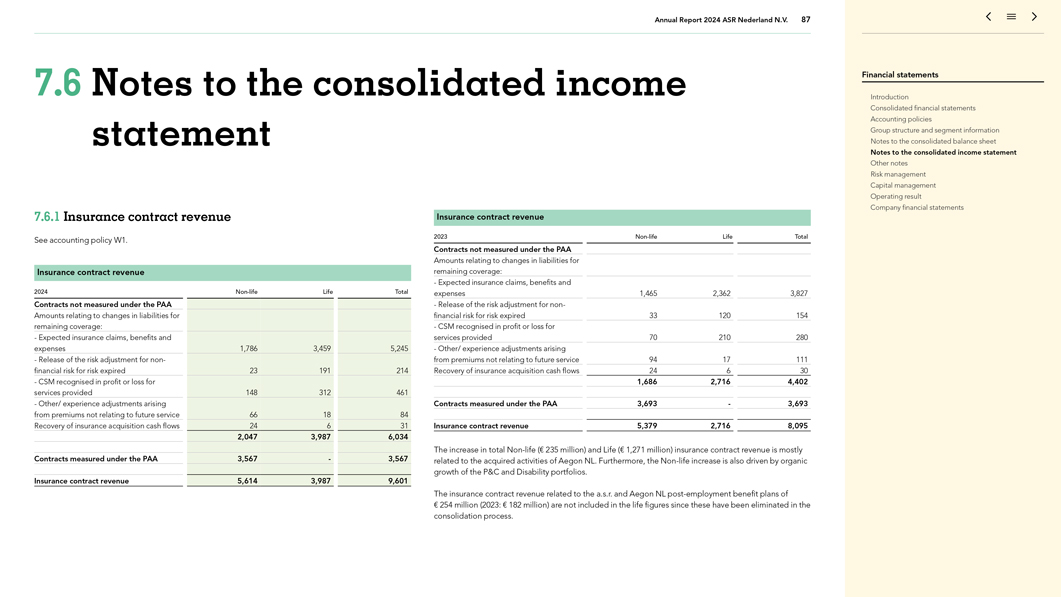

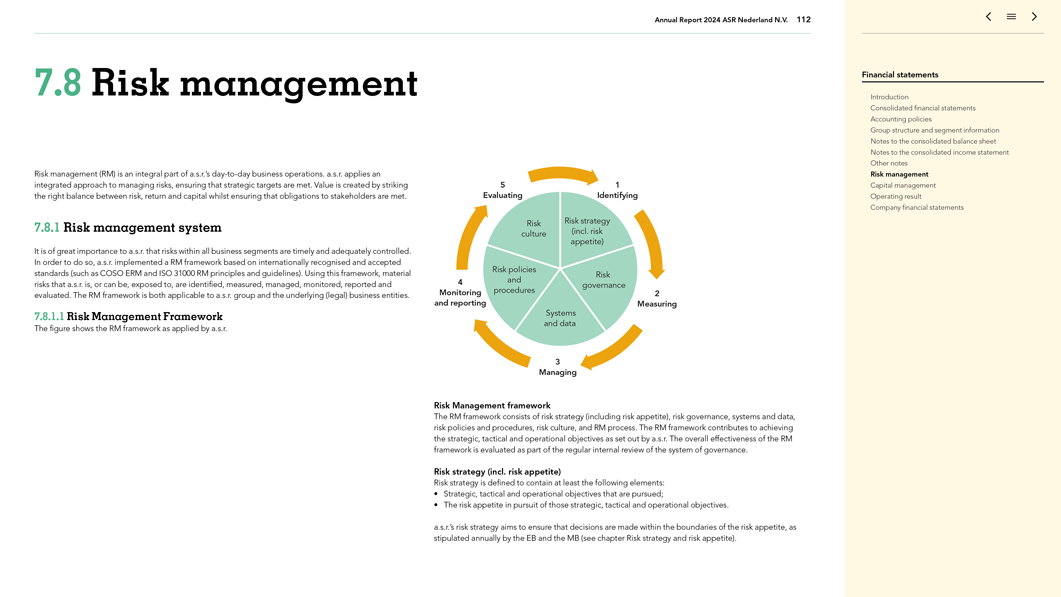

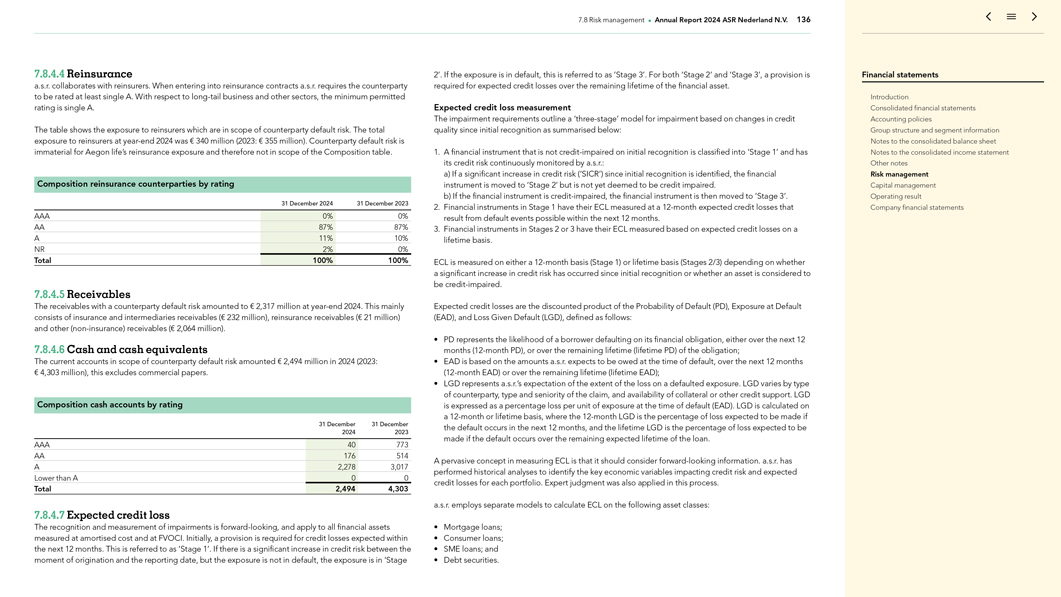

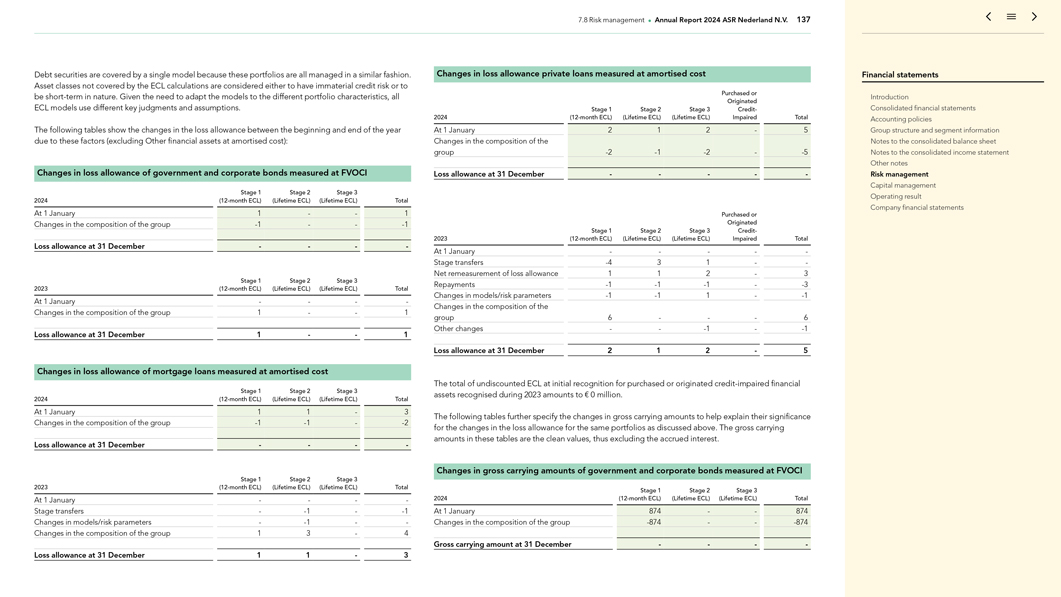

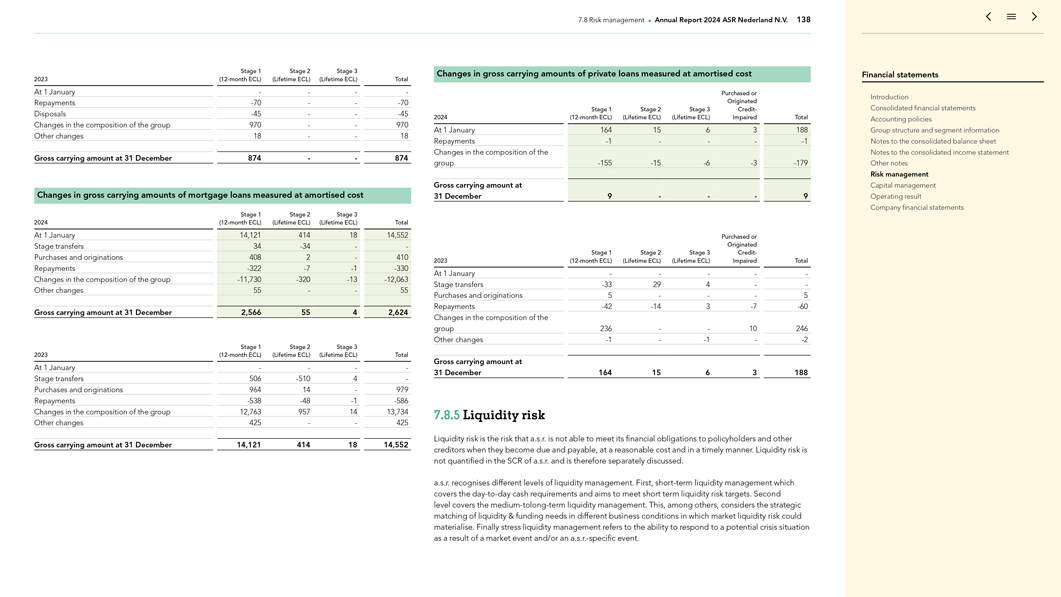

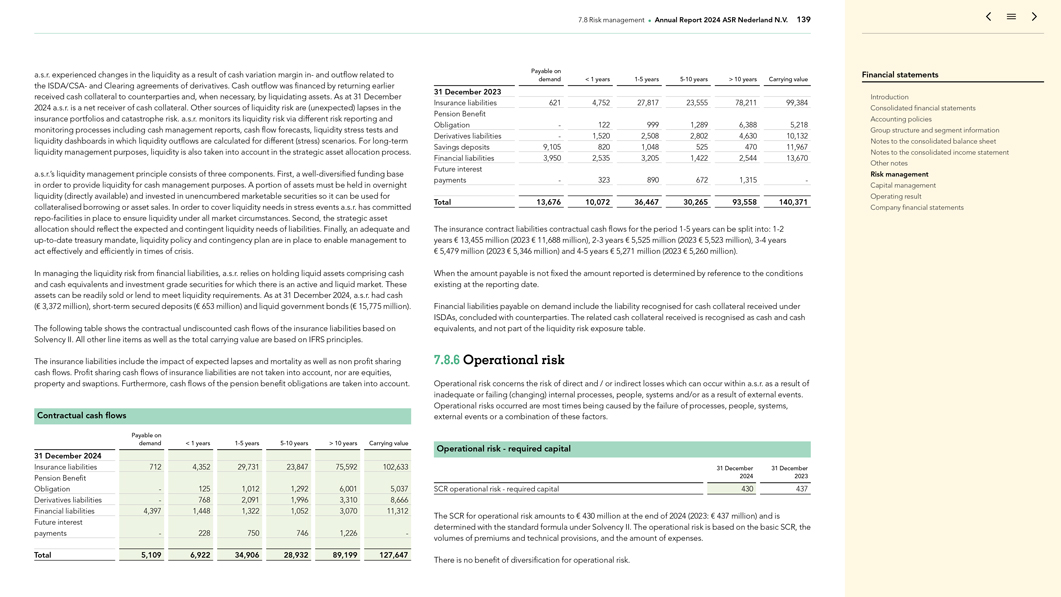

ASR Nederland N.V. Financial statements 7.1 Introduction 2 7.2 Consolidated financial statements 3 7.3 Accounting policies 10 7.4 Group structure and segment information 31 7.5 Notes to the consolidated balance sheet 44 7.6 Notes to the consolidated income statement 87 7.7 Other notes 95 7.8 Risk management 112 7.9 Capital management 142 7.10 Operating result 146 7.11 Company financial statements 149

Annual Report 2024 ASR Nederland N.V. 2 7.1 Introduction 7.1.1 General information ASR Nederland N.V. (a.s.r. or ‘the Group’) is one of the largest insurers in the Netherlands. a.s.r. helps its customers share risks and build up capital for the future. a.s.r. does this with services and products that are good for ‘Nu, later en altijd’, in the fields of insurance, pensions, and mortgages for customers, businesses and employers. a.s.r. is also active as an asset manager for third parties. In 2024, a.s.r. sold insurance products under the following labels: a.s.r., Aegon, and Loyalis. a.s.r. is listed on Euronext Amsterdam and is included in the AEX index. a.s.r. has a total of 7,373 internal FTE’s (2023: 7,994 of which 7,556 excluding Knab). a.s.r. is a public limited company under Dutch law having its registered office located at Archimedeslaan 10, 3584 BA inUtrecht, the Netherlands. Country of incorporation is the Netherlands. a.s.r. has chosen the Netherlands as ‘country of origin’ (land van herkomst) for the issued share capital and some corporate bonds which are listed on Euronext Amsterdam and Euronext Dublin (Ticker: ASRNL). a.s.r. is registered under number 30070695 in the register of the Chamber of Commerce. The consolidated financial statements are presented in euros (€), being the functional currency of a.s.r. and all its group entities. All amounts quoted in these financial statements are in euros and rounded to the nearest million, unless otherwise indicated. Calculations are made using unrounded figures. As a result rounding differences can occur. These statements have been prepared on a going concern basis. The financial statements for 2024 were authorised for issue by the Executive Board (EB) and approved by the Supervisory Board (SB) on 25 March 2025. The financial statements 2024 will be presented to the Annual General Meeting (AGM) of Shareholders for adoption on 21 May 2025. 7.1.2 Statement of compliance The consolidated financial statements of a.s.r. have been prepared in accordance with IFRS – including the International Accounting Standards (IAS) and Interpretations – as adopted by the EU (EU-IFRS), and with the financial reporting requirements included in Title 9, Book 2 of the Dutch Civil Code, where applicable. a.s.r.’s interpretation of EU-IFRS is included in the a.s.r. accounting manual. The accounting policies included in section 7.3 are a summary of the relevant accounting policies of the a.s.r. accounting manual. a.s.r. applies fair value hedge accounting for portfolio hedges of interest rate risk (macro hedging) under the EU ‘carve out’ of IFRS. EU-IFRS differs from International Financial Reporting Standards Accounting Standards as issued by the International Accounting Standards Board (IFRS). Under EU-IFRS, a.s.r. applies fair value hedge accounting for portfolio hedges of interest rate risk (macro hedging) under the EU ‘carve out’ of IFRS. This is the only difference between EU-IFRS as applied by a.s.r. and IFRS. Pursuant to the options offered by Section 362, Book 2 of the Dutch Civil Code, a.s.r. has prepared its company financial statements in accordance with the same principles as those used for the consolidated financial statements. Financial statements Introduction Consolidated financial statements Accounting policies Group structure and segment information Notes to the consolidated balance sheet Notes to the consolidated income statement Other notes Risk management Capital management Operating result Company financial statements

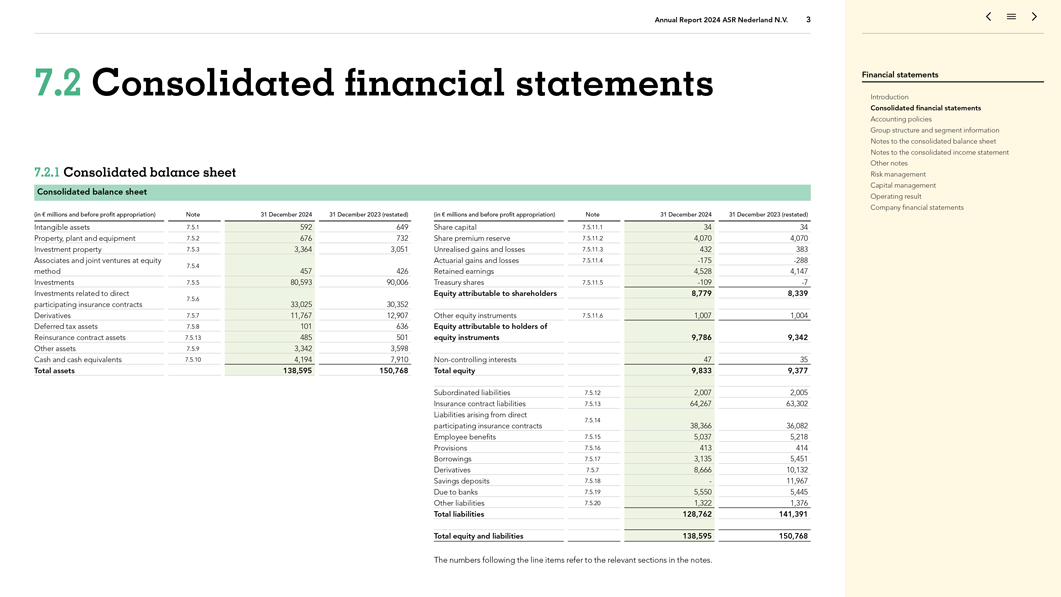

Annual Report 2024 ASR Nederland N.V. 3 7.2 Consolidated financial statements 7.2.1 Consolidated balance sheet Consolidated balance sheet (in € millions and before profit appropriation) Note 31 December 2024 31 December 2023 (restated) Intangible assets 7.5.1 592 649 Property, plant and equipment 7.5.2 676 732 Investment property 7.5.3 3,364 3,051 Associates and joint ventures at equity 7.5.4 method 457 426 Investments 7.5.5 80,593 90,006 Investments related to direct 7.5.6 participating insurance contracts 33,025 30,352 Derivatives 7.5.7 11,767 12,907 Deferred tax assets 7.5.8 101 636 Reinsurance contract assets 7.5.13 485 501 Other assets 7.5.9 3,342 3,598 Cash and cash equivalents 7.5.10 4,194 7,910 Total assets 138,595 150,768 (in € millions and before profit appropriation) Note 31 December 2024 31 December 2023 (restated) Share capital 7.5.11.1 34 34 Share premium reserve 7.5.11.2 4,070 4,070 Unrealised gains and losses 7.5.11.3 432 383 Actuarial gains and losses 7.5.11.4 -175 -288 Retained earnings 4,528 4,147 Treasury shares 7.5.11.5 -109 -7 Equity attributable to shareholders 8,779 8,339 Other equity instruments 7.5.11.6 1,007 1,004 Equity attributable to holders of equity instruments 9,786 9,342 Non-controlling interests 47 35 Total equity 9,833 9,377 Subordinated liabilities 7.5.12 2,007 2,005 Insurance contract liabilities 7.5.13 64,267 63,302 Liabilities arising from direct 7.5.14 participating insurance contracts 38,366 36,082 Employee benefits 7.5.15 5,037 5,218 Provisions 7.5.16 413 414 Borrowings 7.5.17 3,135 5,451 Derivatives 7.5.7 8,666 10,132 Savings deposits 7.5.18—11,967 Due to banks 7.5.19 5,550 5,445 Other liabilities 7.5.20 1,322 1,376 Total liabilities 128,762 141,391 Total equity and liabilities 138,595 150,768 173 The numbers following the line items refer to the relevant sections in the notes. Financial statements Introduction Consolidated financial statements Accounting policies Group structure and segment information Notes to the consolidated balance sheet Notes to the consolidated income statement Other notes Risk management Capital management Operating result Company financial statements

7.2 Consolidated financial statements • Annual Report 2024 ASR Nederland N.V. 4 The 31 December 2023 figures have been restated, see section 7.3.2. Financial statements Introduction Consolidated financial statements Accounting policies Group structure and segment information Notes to the consolidated balance sheet Notes to the consolidated income statement Other notes Risk management Capital management Operating result Company financial statements

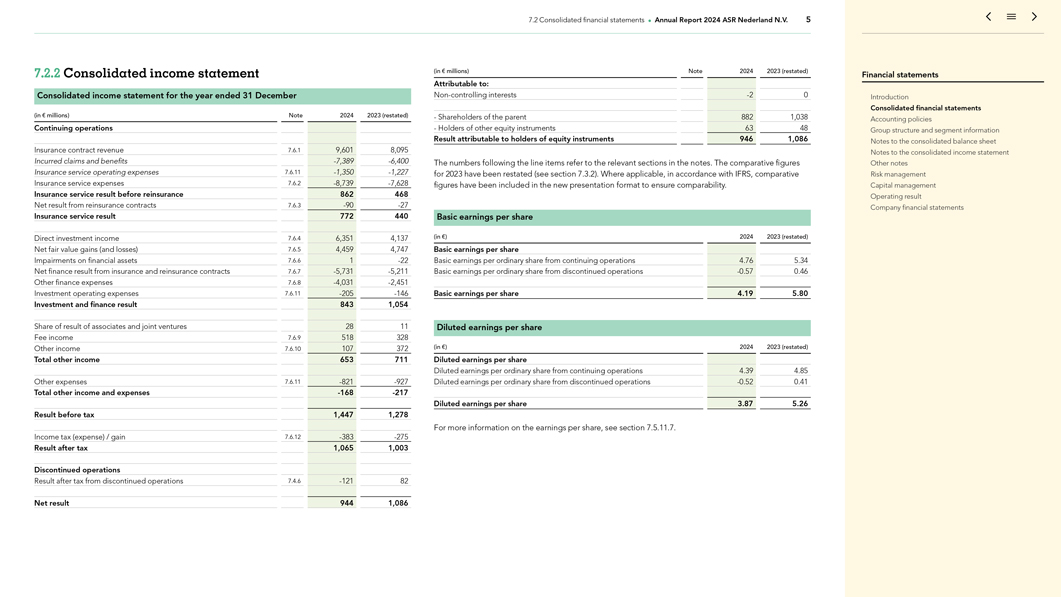

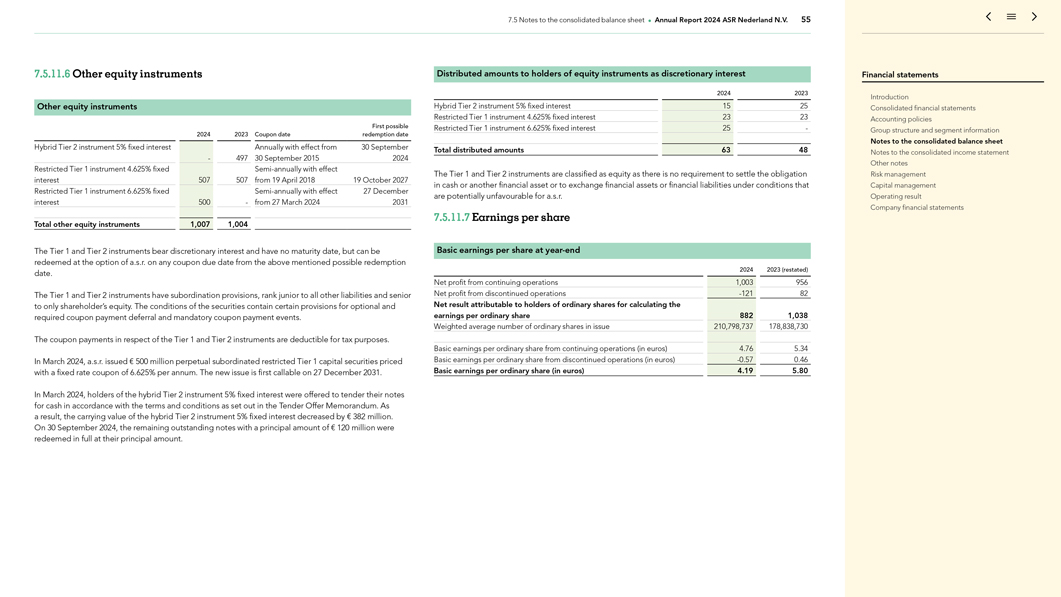

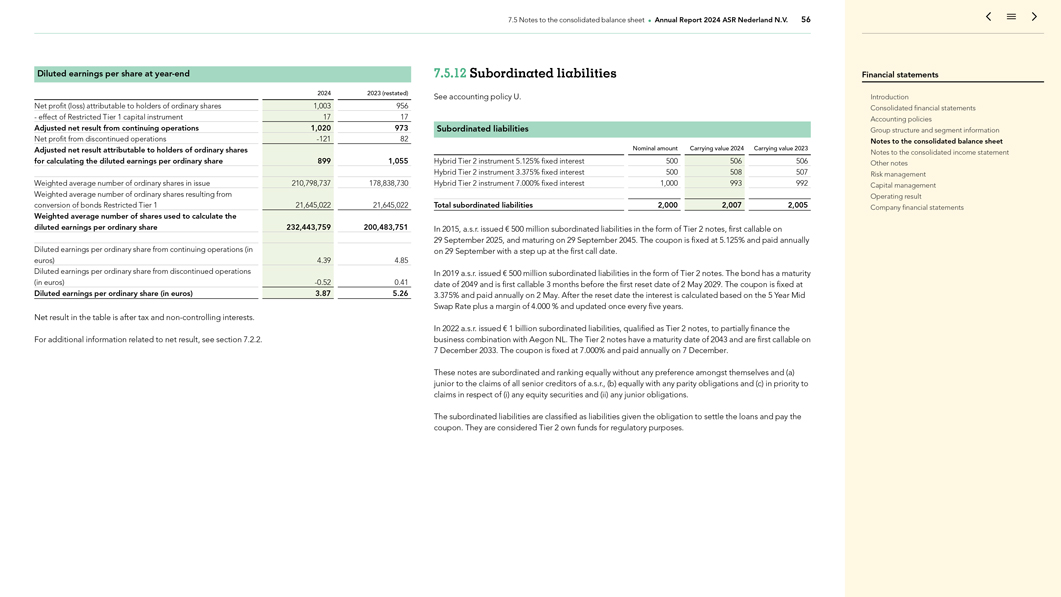

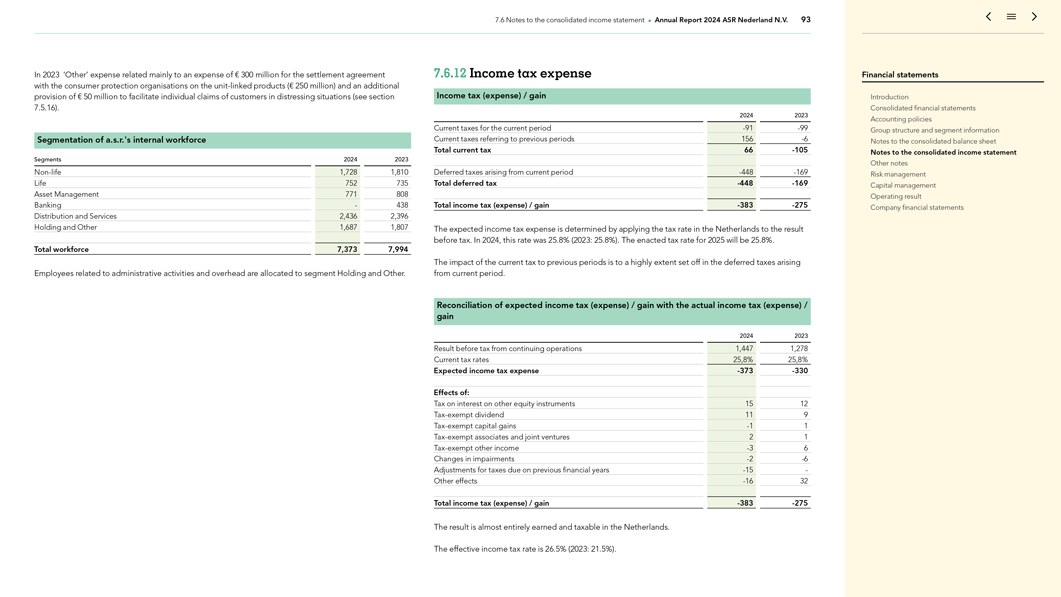

7.2 Consolidated financial statements • Annual Report 2024 ASR Nederland N.V. 5 7.2.2 Consolidated income statement Consolidated income statement for the year ended 31 December (in € millions) Note 2024 2023 (restated) Continuing operations Insurance contract revenue 7.6.1 9,601 8,095 Incurred claims and benefits -7,389 -6,400 Insurance service operating expenses 7.6.11 -1,350 -1,227 Insurance service expenses 7.6.2 -8,739 -7,628 Insurance service result before reinsurance 862 468 Net result from reinsurance contracts 7.6.3 -90 -27 Insurance service result 772 440 Direct investment income 7.6.4 6,351 4,137 Net fair value gains (and losses) 7.6.5 4,459 4,747 Impairments on financial assets 7.6.6 1 -22 Net finance result from insurance and reinsurance contracts 7.6.7 -5,731 -5,211 Other finance expenses 7.6.8 -4,031 -2,451 Investment operating expenses 7.6.11 -205 -146 Investment and finance result 843 1,054 Share of result of associates and joint ventures 28 11 Fee income 7.6.9 518 328 Other income 7.6.10 107 372 Total other income 653 711 Other expenses 7.6.11 -821 -927 Total other income and expenses -168 -217 Result before tax 1,447 1,278 Income tax (expense) / gain 7.6.12 -383 -275 Result after tax 1,065 1,003 Discontinued operations Result after tax from discontinued operations 7.4.6 -121 82 Net result 944 1,086 (in € millions) Note 2024 2023 (restated) Attributable to: Non-controlling interests -2 0—Shareholders of the parent 882 1,038—Holders of other equity instruments 63 48 Result attributable to holders of equity instruments 946 1,086 The numbers following the line items refer to the relevant sections in the notes. The comparative figures for 2023 have been restated (see section 7.3.2). Where applicable, in accordance with IFRS, comparative figures have been included in the new presentation format to ensure comparability. Basic earnings per share (in €) 2024 2023 (restated) Basic earnings per share Basic earnings per ordinary share from continuing operations 4.76 5.34 Basic earnings per ordinary share from discontinued operations -0.57 0.46 Basic earnings per share 4.19 5.80 Diluted earnings per share (in €) 2024 2023 (restated) Diluted earnings per share Diluted earnings per ordinary share from continuing operations 4.39 4.85 Diluted earnings per ordinary share from discontinued operations -0.52 0.41 Diluted earnings per share 3.87 5.26 For more information on the earnings per share, see section 7.5.11.7. Financial statements Introduction Consolidated financial statements Accounting policies Group structure and segment information Notes to the consolidated balance sheet Notes to the consolidated income statement Other notes Risk management Capital management Operating result Company financial statements

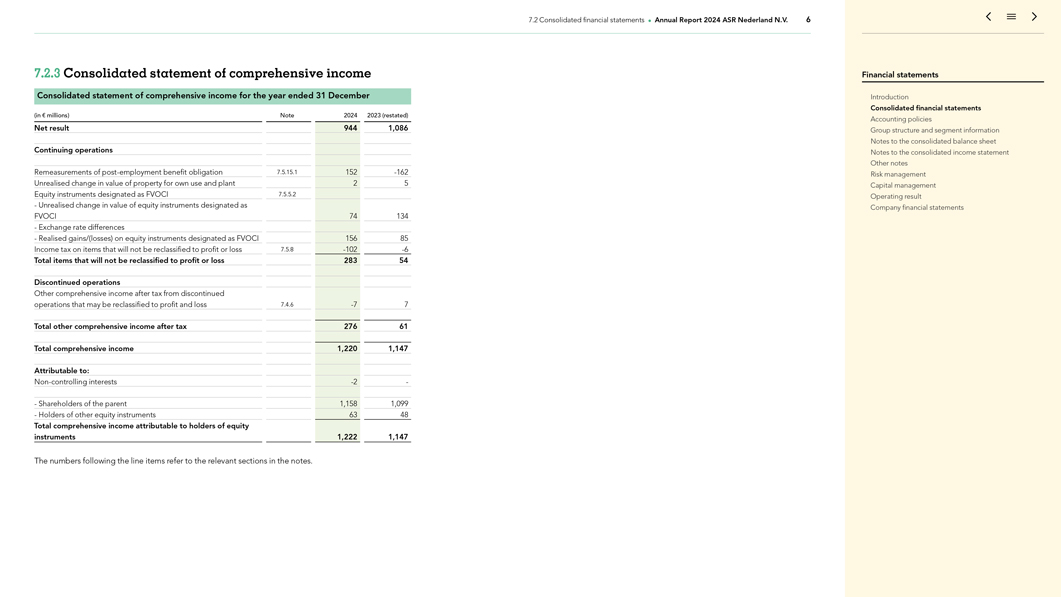

7.2 Consolidated financial statements • Annual Report 2024 ASR Nederland N.V. 6 7.2.3 Consolidated statement of comprehensive income Consolidated statement of comprehensive income for the year ended 31 December (in € millions) Note 2024 2023 (restated) Net result 944 1,086 Continuing operations Remeasurements of post-employment benefit obligation 7.5.15.1 152 -162 Unrealised change in value of property for own use and plant 2 5 Equity instruments designated as FVOCI 7.5.5.2—Unrealised change in value of equity instruments designated as FVOCI 74 134—Exchange rate differences—Realised gains/(losses) on equity instruments designated as FVOCI 156 85 Income tax on items that will not be reclassified to profit or loss 7.5.8 -102 -6 Total items that will not be reclassified to profit or loss 283 54 Discontinued operations Other comprehensive income after tax from discontinued operations that may be reclassified to profit and loss 7.4.6 -7 7 Total other comprehensive income after tax 276 61 Total comprehensive income 1,220 1,147 Attributable to: Non-controlling interests -2 — Shareholders of the parent 1,158 1,099—Holders of other equity instruments 63 48 Total comprehensive income attributable to holders of equity instruments 1,222 1,147 The numbers following the line items refer to the relevant sections in the notes. Financial statements Introduction Consolidated financial statements Accounting policies Group structure and segment information Notes to the consolidated balance sheet Notes to the consolidated income statement Other notes Risk management Capital management Operating result Company financial statements

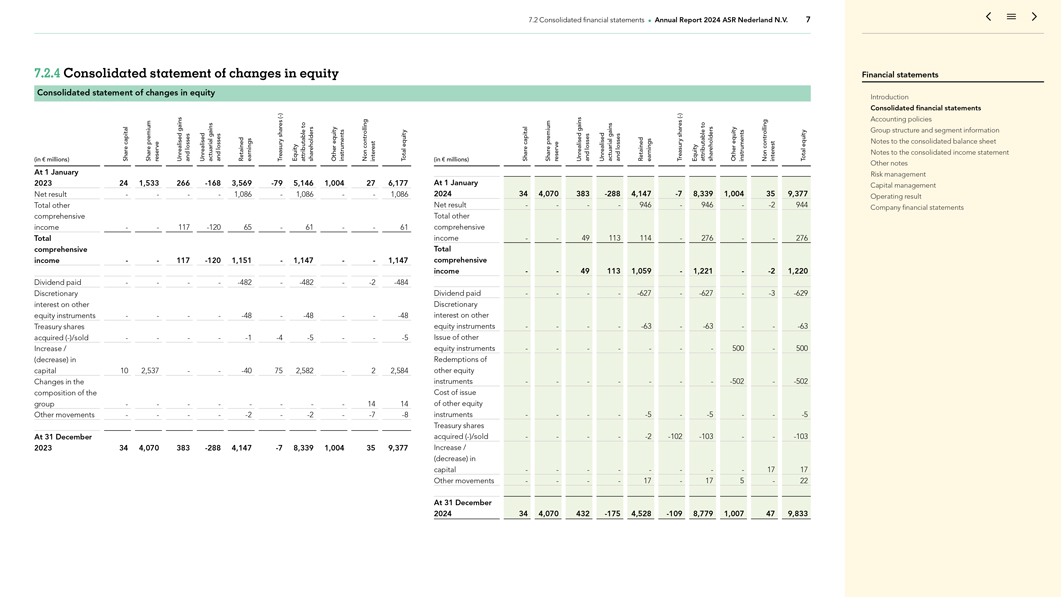

7.2 Consolidated financial statements • Annual Report 2024 ASR Nederland N.V. 7 7.2.4 Consolidated statement of changes in equity Consolidated statement of changes in equity—) ( to gains gains shares equity capital premium losses losses controllingequity (in € millions) Share Share reserve Unrealised and Unrealised actuarial and Retained earnings Treasury Equity attributable shareholders Other instruments Non interest Total At 1 January 2023 24 1,533 266 -168 3,569 -79 5,146 1,004 27 6,177 Net result — — 1,086—1,086 — 1,086 Total other comprehensive income — 117 -120 65—61 — 61 Total comprehensive income — 117 -120 1,151—1,147 — 1,147 Dividend paid — — -482—-482—-2 -484 Discretionary interest on other equity instruments — — -48—-48 — -48 Treasury shares acquired (-)/sold — — -1 -4 -5 — -5 Increase / (decrease) in capital 10 2,537 — -40 75 2,582—2 2,584 Changes in the composition of the group — — — — 14 14 Other movements — — -2—-2—-7 -8 At 31 December 2023 34 4,070 383 -288 4,147 -7 8,339 1,004 35 9,377—) ( to gains gains shares equity capital premium losses losses controllingequity (in € millions) Share Share reserve Unrealised and Unrealised actuarial and Retained earnings Treasury Equity attributable shareholders Other instruments Non interest Total At 1 January 2024 34 4,070 383 -288 4,147 -7 8,339 1,004 35 9,377 Net result — — 946—946—-2 944 Total other comprehensive income — 49 113 114—276 — 276 Total comprehensive income — 49 113 1,059—1,221—-2 1,220 Dividend paid — — -627—-627—-3 -629 Discretionary interest on other equity instruments — — -63—-63 — -63 Issue of other equity instruments — — ——500—500 Redemptions of other equity instruments — — ——-502—-502 Cost of issue of other equity instruments — — -5—-5 — -5 Treasury shares acquired (-)/sold — — -2 -102 -103 — -103 Increase / (decrease) in capital — — — — 17 17 Other movements — — 17—17 5—22 At 31 December 2024 34 4,070 432 -175 4,528 -109 8,779 1,007 47 9,833 Financial statements Introduction Consolidated financial statements Accounting policies Group structure and segment information Notes to the consolidated balance sheet Notes to the consolidated income statement Other notes Risk management Capital management Operating result Company financial statements

7.2 Consolidated financial statements • Annual Report 2024 ASR Nederland N.V. 8 For more information on the share premium reserve, see section 7.5.11.2. For more information on the actuarial gains and losses related to the pension obligation, see section 7.5.11.4. For more information on treasury shares acquired and sold, see section 7.5.11.5. For more information on the issue and redemption of other equity instruments in 2024, see section 7.5.11.6. Financial statements Introduction Consolidated financial statements Accounting policies Group structure and segment information Notes to the consolidated balance sheet Notes to the consolidated income statement Other notes Risk management Capital management Operating result Company financial statements

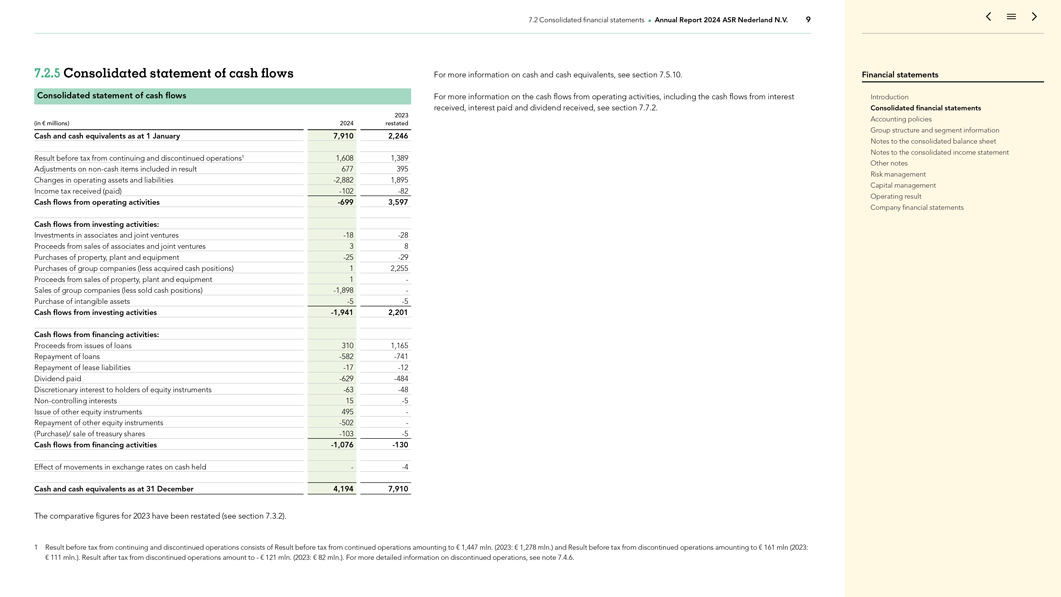

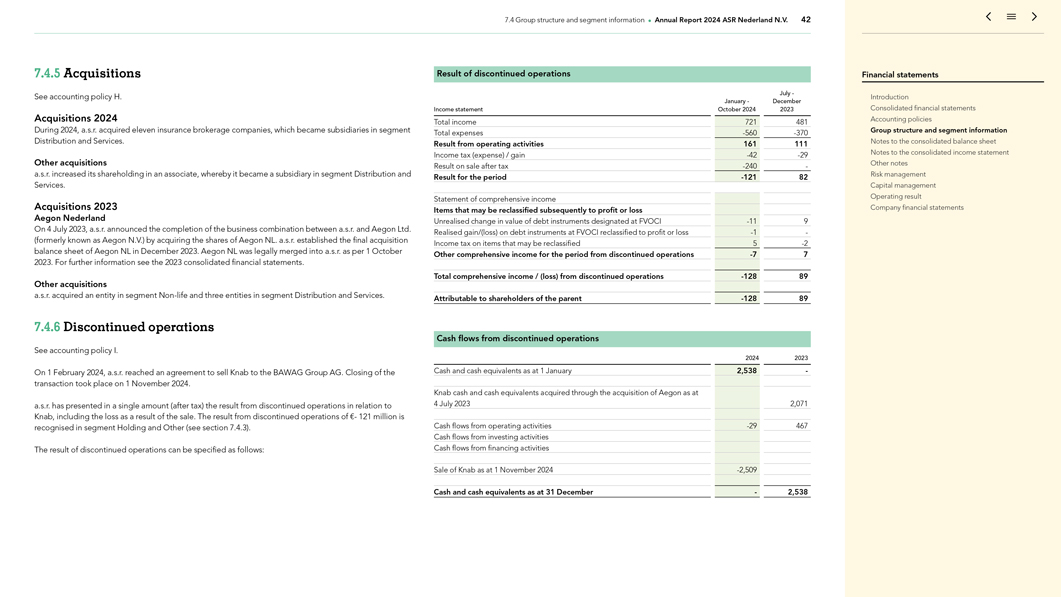

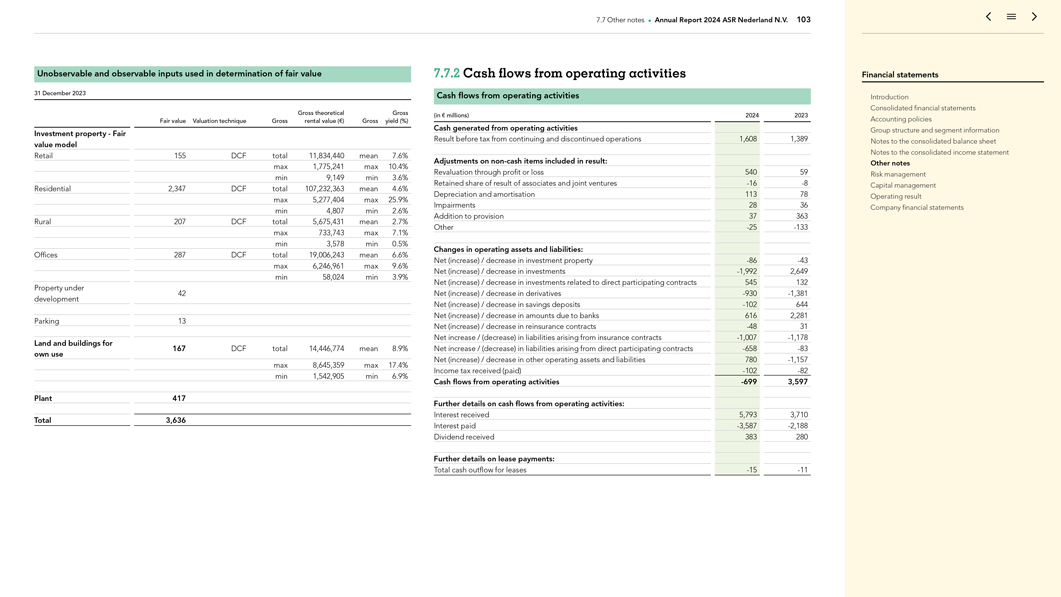

7.2 Consolidated financial statements • Annual Report 2024 ASR Nederland N.V. 9 7.2.5 Consolidated statement of cash flows Consolidated statement of cash flows 2023 (in € millions) 2024 restated Cash and cash equivalents as at 1 January 7,910 2,246 Result before tax from continuing and discontinued operations1 1,608 1,389 Adjustments on non-cash items included in result 677 395 Changes in operating assets and liabilities -2,882 1,895 Income tax received (paid) -102 -82 Cash flows from operating activities -699 3,597 Cash flows from investing activities: Investments in associates and joint ventures -18 -28 Proceeds from sales of associates and joint ventures 3 8 Purchases of property, plant and equipment -25 -29 Purchases of group companies (less acquired cash positions) 1 2,255 Proceeds from sales of property, plant and equipment 1 -Sales of group companies (less sold cash positions) -1,898 -Purchase of intangible assets -5 -5 Cash flows from investing activities -1,941 2,201 Cash flows from financing activities: Proceeds from issues of loans 310 1,165 Repayment of loans -582 -741 Repayment of lease liabilities -17 -12 Dividend paid -629 -484 Discretionary interest to holders of equity instruments -63 -48 Non-controlling interests 15 -5 Issue of other equity instruments 495 -Repayment of other equity instruments -502 -(Purchase)/ sale of treasury shares -103 -5 Cash flows from financing activities -1,076 -130 Effect of movements in exchange rates on cash held—-4 Cash and cash equivalents as at 31 December 4,194 7,910 The comparative figures for 2023 have been restated (see section 7.3.2). For more information on cash and cash equivalents, see section 7.5.10. For more information on the cash flows from operating activities, including the cash flows from interest received, interest paid and dividend received, see section 7.7.2. Financial statements Introduction Consolidated financial statements Accounting policies Group structure and segment information Notes to the consolidated balance sheet Notes to the consolidated income statement Other notes Risk management Capital management Operating result Company financial statements 1 Result before tax from continuing and discontinued operations consists of Result before tax from continued operations amounting to € 1,447 mln. (2023: € 1,278 mln.) and Result before tax from discontinued operations amounting to € 161 mln (2023: € 111 mln 879241 .). Result after- tax 001 from- discontinued Part-2 operations amount28Mar25 to—€ 121 mln. (2023: 13:48 € 82 mln. ). For more detailed Page information 179 on discontinued operations, see note 7.4.6.

Annual Report 2024 ASR Nederland N.V. 10 7.3 Accounting policies 7.3.1 Changes in EU endorsed published IFRS Standards and Harmonisation between a.s.r. and Aegon NL Interpretations effective in 2024 Following further alignment of methodologies and application of policies with Aegon NL, selected comparative figures have also been restated to ensure consistency and comparability. These restatements In 2024, no changes in EU endorsed published IFRS Standards and Interpretations are relevant to a.s.r. are part of the ongoing harmonisation process and reflect the integration of Aegon NL into a.s.r.’s financial reporting framework. 7.3.2 Changes in presentations The current presentation differs from last year’s presentation as recognised in the 2023 financial statements, primarily following the sale of Knab, further harmonisation between a.s.r. and Aegon NL and the refinements related to the implementation of IFRS 17 and IFRS 9. These immaterial (on a qualitative basis) changes in presentation have no impact on a.s.r.’s past or future financial position, financial performance, or cash flows from operating, investing and financing activities. The following restatements, given their nature, are explained in more detail: Reclassification of Knab to discontinued operations On 1 February 2024, a.s.r. reached an agreement to sell Knab to the BAWAG Group AG. Closing of the transaction took place on 1 November 2024. Knab’s results have therefore been reclassified from continuing to discontinued operations, in line with the requirements of IFRS 5. This reclassification has resulted in a single amount of € 82 million presented as result after tax from discontinued operations in the 2023 consolidated income statement and € 7 million presented as other comprehensive income after tax from discontinued operations in the 2023 consolidated statement of comprehensive income. For further details, please refer to section 7.4.6. Changes to the presentation of the Consolidated statement of cash flows: Due to a reassessment of the presentation of the cash flow statement in 2024, the 2023 comparative figures for the cash flows from operating activities were adjusted for the revaluation through profit or loss (€ 357 million) as part of the adjustment for non-cash items included in the result, with a corresponding opposite adjustment in the changes in operating assets and liabilities. 7 interpretations, .3.3 Upcoming changes not yet effective in published in 2024 IFRS standards and The following new standards, amendments to existing standards and interpretations, relevant to a.s.r. and published prior to 1 January 2025 and effective for accounting periods beginning on or after 1 January 2025, were not early adopted by a.s.r.: • IFRS 18: Presentation and Disclosure in Financial Statements (2027); IFRS 18 Presentation and Disclosure in Financial Statements IFRS 18 replaces IAS 1, carrying forward many of the requirements in IAS 1 unchanged and introduces the following key requirements: • present specified categories and defined subtotals in the income statement; • provide disclosures on management-defined performance measures (MPMs) in the notes to the financial statements; • improve aggregation and disaggregation; • the operating profit subtotal is the starting point for the statement of cash flows when presenting the operating cash flows under the direct method. a.s.r. is currently working to identify all impacts the amendments will have on the primary financial statements and notes to the financial statements. IFRS 18 will be applied retrospectively. Cash collateral The presentation of cash collateral paid (2023: €2.3 billion) has been changed to align more with industry practice and is included in other assets and not in investments. 879241-001-Part-2 28Mar25 13:48 Page 180 Financial statements Introduction Consolidated financial statements Accounting policies Group structure and segment information Notes to the consolidated balance sheet Notes to the consolidated income statement Other notes Risk management Capital management Operating result Company financial statements

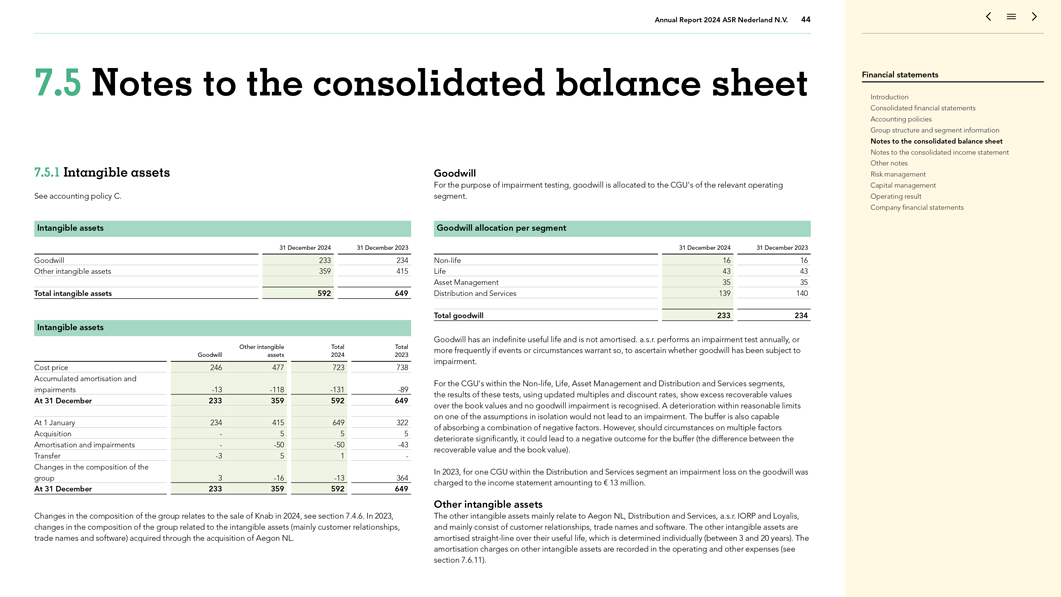

7.3 Accounting policies • Annual Report 2024 ASR Nederland N.V. 11 7.3.4 Key accounting policies A. Estimates and assumptions The preparation of the financial statements requires a.s.r. to make estimates, assumptions and judgements in applying accounting policies that have an effect on the reported amounts in the financial statements. These relate primarily to the following: • The estimated useful life, residual value and fair value of property, plant and equipment, investment property, and intangible assets (see accounting policy C, D and P); • The fair value and impairments of unlisted financial instruments (see accounting policy B and E); • The recoverable amount of impaired assets (see accounting policy B and E ); • The fair value used to determine the net asset value in acquisitions (see section 7.4.5); • The fair value used in measuring the assets held for sale and liabilities related to the assets held for sale (see section 7.4.6); • The measurement of insurance contract liabilities and liabilities arising from direct participating insurance contracts (see section 7.5.13.4); • Actuarial assumptions used for measuring employee benefit obligations (see section 7.5.15); • When forming provisions, the required estimate of existing obligations arising from past events (see section 7.5.16). The estimates and assumptions are based on management’s best knowledge of current facts, actions and events. The actual outcomes may ultimately differ from the results reported earlier on the basis of estimates and assumptions. A detailed explanation of the estimates and assumptions are given in the relevant notes to the consolidated financial statements. As from the date of the Aegon NL business combination, harmonisation of assumptions and methods between Aegon NL and a.s.r. is in progress and is expected to continue in the coming years. a.s.r. takes into account in the expense assumptions the estimated synergy effects from the Aegon NL business combination for the part that can be assessed within the budget period. B. Fair value of assets and liabilities The fair value is the price that a.s.r. would receive to sell an asset or pay to transfer a liability in an orderly transaction between market participants on the transaction date or reporting date in the principal market for the asset or liability, or in the most advantageous market for the asset or liability and assuming the highest and best use for non-financial assets. Where possible, a.s.r. determines the fair value of assets and liabilities on the basis of quoted prices in an active market. In the absence of an active market for a financial instrument, the fair value is determined using valuation techniques. Although valuation techniques are based on observable market data where possible, results are affected by the assumptions used, such as discount rates and estimates of future cash flows. In the unlikely event that the fair value of a financial instrument cannot be measured, it is carried at cost. Fair value hierarchy The following three hierarchical levels are used to determine the fair value of financial instruments and non-financial instruments when accounting for assets and liabilities at fair value and disclosing the comparative fair value of assets and liabilities: Level 1. Fair value based on quoted prices in an active market Level 1 includes assets and liabilities whose value is determined by quoted (unadjusted) prices in the primary active market for identical assets or liabilities. A financial instrument is quoted in an active market if: • Quoted prices are readily and regularly available (from an exchange, dealer, broker, sector organisation, third party pricing service, or a regulatory body); and • These prices represent actual and regularly occurring transactions on an at arm’s length basis. Financial instruments in this category primarily consist of bonds and equities listed in active markets. Cash and cash equivalents (excluding money market instruments), reverse repurchase agreements and cash collateral received are also included as level 1. Level 2. Fair value based on observable market data Determining fair value on the basis of Level 2 involves the use of valuation techniques that use inputs other than quoted prices included within Level 1 that are observable for the asset or liability, either directly (that is, as prices) or indirectly (that is derived from prices of identical or similar assets and liabilities). These observable inputs are obtained from a broker or third party pricing service and include: • Quoted prices in active markets for similar (not identical) assets or liabilities; • Quoted prices for identical or similar assets or liabilities in inactive markets; • Input variables other than quoted prices observable for the asset or liability. These include interest rates and yield curves observable at commonly quoted intervals, volatility, loss ratio, credit risks and default percentages. This category primarily includes: I. Financial instruments: unlisted fixed-interest preference shares and interest rate contracts; II. Financial instruments: loans (excluding mortgage loans and reverse repurchase agreements); III. Other financial assets and liabilities.1 I. Financial instruments: unlisted fixed-interest preference shares and interest rate contracts This category includes unlisted fixed-interest preference shares and interest rate contracts. The valuation techniques for financial instruments use present value calculations and in the case of derivatives, include forward pricing and swap models. The observable market data contains yield curves based on company ratings and characteristics of the unlisted fixed-interest preference shares. Financial statements Introduction Consolidated financial statements Accounting policies Group structure and segment information Notes to the consolidated balance sheet Notes to the consolidated income statement Other notes Risk management Capital management Operating result Company financial statements 1 Not measured 879241 at fair value -001 on the -Part balance- sheet 2 and for which the 28Mar25 fair value is disclosed 13:48 . Page 181

7.3 Accounting policies • Annual Report 2024 ASR Nederland N.V. 12 II. Financial instruments: Loans (excluding mortgage loans and reverse repurchase agreements) The fair value of the loans is based on the discounted cash flow method. It is obtained by calculating the present value based on expected future cash flows and assuming an interest rate curve used in the market that includes an additional spread based on the risk profile of the counterparty. III. Other financial assets and liabilities For other financial assets and liabilities where the fair value is disclosed these fair values are based on observable market inputs, primarily being the price paid to acquire the asset or received to assume the liability on initial recognition, assuming that the transactions have taken place on an at arm’s length basis. Valuation techniques using present value calculations are applied using current interest rates where the payment terms are longer than one year. Level 3. Fair value not based on observable market data The fair value of the level 3 assets and liabilities are determined in whole or in part using a valuation technique based on assumptions that are not supported by prices from observable current market transactions in the same instrument and for which any significant inputs are not based on available observable market data. The financial assets and liabilities in this category are assessed individually. Valuation techniques are used to the extent that observable inputs are not available. The basic principle of fair value measurement is still to determine a fair, at arm’s length price. Unobservable inputs therefore reflect management’s own assumptions about the assumptions that market participants would use in pricing the asset or liability (including assumptions about risk). These inputs are generally based on the available observable data (adjusted for factors that contribute towards the value of the asset) and own source information. This category primarily includes: I. Financial instruments: private equity investments (or private equity partners) and equity funds third parties directly investing in real estate; II. Financial instruments: mortgage loans and mortgage equity funds; III. Investment property, real estate equity funds associates, rural property contracts, buildings for own use and plant (e.g. wind farms); IV. Financial instruments: asset-backed securities. I. Financial instruments: private equity investments and real estate equity funds third parties The main non-observable market input for private equity investments and equity funds third parties directly investing in real estate is the net asset value of the investment as published by the private equity company (or partner) and real estate equity funds respectively. II. Financial instruments: mortgage loans and mortgage equity funds The fair value of the mortgage loan portfolio is based on the discounted cash flow method. It is obtained by calculating the present value based on expected future cash flows and assuming an interest rate curve used in the market that includes an additional spread based on the risk profile of the counterparty. The valuation method used to determine the fair value of the mortgage loan portfolio derives the spread from consumer rates and includes assumptions for originating cost and risks. The method of determining the fair value of the mortgage equity funds is similar to that of mortgage loans. III. Investment property, real estate equity funds associates, rural property contracts, buildings for own use and plant The following categories of investment properties, buildings for own use and plant are recognised and methods of calculating fair value are distinguished: • Residential – based on reference transaction and discounted cash flow method; • Retail – based on reference transaction and income capitalisation method; • Rural – based on reference transaction and discounted cash flow method; • Offices – based on reference transaction and discounted cash flow method (including buildings for own use); • Other investment property – based on reference transaction and discounted cash flow method; • Property under development – based on both discounted cash flow and income capitalisation method; • Plant—based on reference transaction and discounted cash flow method. The following valuation methods are available for the calculation of fair value by the external professional appraisers for investment property, including real estate equity funds associates, rural property contracts, buildings for own use and plant: Reference transactions Independent professional appraisers use transactions in comparable properties and plant as a reference for determining the fair value of the property and plant. The reference transactions of comparable objects are generally based on observable data consisting of the land register ‘Kadaster’ and the rural land price monitor as published by the Dutch government ‘grondprijsmonitor’ in an active property market and in some instances accompanied by own use information. The external professional appraisers valuate the property or plant using the reference transaction in combination with the following valuation methods to ensure the appropriate valuation of the property: • Discounted cash flow method; • Income capitalisation method (property only). Discounted cash flow method Under the discounted cash flow method, fair value is estimated using assumptions regarding the benefits and liabilities of ownership over the asset’s life including an exit or terminal value. This method involves the projection of a series of cash flows on the investment property or plant dependent on the duration of the lease contracts. A market-derived discount rate is applied to these projected cash flow series in order to establish the present value of the cash flows associated with the asset. The exit yield is normally determined separately, and differs from the discount rate. Financial statements Introduction Consolidated financial statements Accounting policies Group structure and segment information Notes to the consolidated balance sheet Notes to the consolidated income statement Other notes Risk management Capital management Operating result Company financial statements 879241-001-Part-2 28Mar25 13:48 Page 182

7.3 Accounting policies • Annual Report 2024 ASR Nederland N.V. 13 The duration of the cash flows and the specific timing of inflows and outflows are determined by events such as rent reviews, lease renewal and related re-letting, redevelopment, or refurbishment. The appropriate duration is typically driven by market behaviour, which depends on the class of investment property. Periodic cash flow is typically estimated as gross rental income less vacancy (apart from the rural category), non-recoverable expenses, collection losses, lease incentives, maintenance costs, agent and commission costs and other operating and management expenses. The series of periodic net operating income, along with an estimate of the terminal value anticipated at the end of the projection period, is then discounted. For the categories residential, offices and other in applying the discounted cash flow method, the significant inputs are the discount rate and market rental value. These inputs are verified with the following market observable data (that are adjusted to reflect the state and condition, location, development potential etc. of the specific property): • Market rent per square meter for renewals and their respective re-letting rates; • Reviewed rent per square meter; • Investment transactions of comparable objects; • 10 Year Dutch Government Bond Yield (%) as published by the DNB. When applying the discounted cash flow method for rural valuations, the significant inputs are the discount rate and market lease values. These inputs are verified with the following market observable data (that are adjusted to reflect the state and condition, location, development potential etc. of the specific property): • Market value per acre per region in accordance with the ‘rural land price monitor’; • 10 Year Dutch Government Bond Yield (%) as published by the DNB. Income capitalisation method Under the income capitalisation method, a property’s fair value is estimated based on the normalised net operating income generated by the property, which is divided by the capitalisation rate (the investor’s rate of return). The difference between gross and net rental income includes the same expense categories as those for the discounted cash flow method with the exception that certain expenses are not measured over time, but included on the basis of a time weighted average, such as the average lease-up costs. Under the income capitalisation method, rents above or below the market rent are capitalised separately. The significant inputs for retail valuations are the reversionary yield and the market or reviewed rental value. These inputs are generally verified with the following observable data (that are adjusted to reflect the state and condition, location, development potential etc. of the specific property): • Market rent per square meter for renewals; • Reviewed rent per square meter (based on the rent reviews performed in accordance with Section 303, Book 7 of the Dutch Civil Code). The fair value of investment properties and buildings for own use, are appraised annually. Valuations are conducted by independent professional appraisers who hold recognised and relevant professional qualifications and have recent experience in the location and category of the property being valued. Market value property valuations were prepared in accordance with the Royal Institution of Chartered Surveyors879241 (RICS) Valuation -001 Standards, -Part 7th -2 Edition (the ‘Red Book’) 28Mar25 . a.s.r. provides 13:48 adequate information to the professional appraisers, in order to conduct a comprehensive valuation. The professional appraisers are changed or rotated at least once every three years. IV. Financial instruments: asset-backed securities The fair value of the asset-backed securities is based on quotes published by an independent data vendor. Transfers between levels The hierarchical level per individual instrument, or group of instruments, is reassessed at every reporting period. If the instrument, or group of instruments, no longer complies with the criteria of the level in question, it is transferred to the hierarchical level that does meet the criteria. A transfer can for instance be when the market becomes less liquid or when quoted market prices for the instrument are no longer available. C. Intangible assets Intangible assets are carried at cost, less any accumulated amortisation and impairment losses. The residual value and the estimated useful life of intangible assets are assessed on each balance sheet date and adjusted where applicable. Goodwill Acquisitions by a.s.r. are accounted for using the acquisition method. Goodwill represents the excess of the cost of an acquisition over the fair value of a.s.r.’s share of the net identifiable assets and liabilities and contingent liabilities of the acquired company at acquisition date. If there is no excess (purchase gain), the carrying amount is directly recognised through the income statement. At the acquisition date, goodwill is allocated to the cash-generating units (CGUs) that are expected to benefit from the business combination. Goodwill has an indefinite useful life and is not amortised. a.s.r. performs an impairment test annually, or more frequently if events or circumstances warrant so, to ascertain whether goodwill has been subject to impairment. As part of this, the carrying amount of the cash-generating unit to which the goodwill has been allocated is compared with its recoverable amount. The recoverable amount is the higher of a CGU’s fair value less costs to sell and value in use. The carrying value is determined as the net asset value including goodwill. The methodologies applied to arrive at the best estimate of the recoverable amount involves two steps. In the first step of the impairment test, the best estimate of the recoverable amount of the CGU to which goodwill is allocated is determined separately based on Price to Earnings or Price to Book ratios (fair value less cost to sell model). The ratio(s) used per CGU depends on the characteristics of the entity in question. The main assumptions in this valuation are the multiples for the aforementioned ratios. These are developed internally but are either derived from or corroborated against market information that is related to observable transactions in the market for comparable businesses. If the outcome of the first step indicates that the difference between the recoverable amount and the carrying value may not be sufficient to support the amount of goodwill allocated to the CGU, step two is performed. In step two an additional analysis is performed in order to determine a recoverable amount in a manner 183 that better addresses the specific characteristics of the relevant CGU. Financial statements Introduction Consolidated financial statements Accounting policies Group structure and segment information Notes to the consolidated balance sheet Notes to the consolidated income statement Other notes Risk management Capital management Operating result Company financial statements

7.3 Accounting policies • Annual Report 2024 ASR Nederland N.V. 14 The additional analysis is based on internal value-in-use models, wherein managements assumptions in relation to cash flow projections for budget periods up to and including five years are used and, if deemed justified, expanded to a longer period given the nature of the insurance activities. Other assumptions, such as the (pre-tax) discount rate and the steady state growth rate, are determined on the advice of an independent external party and are based on a Capital Asset Pricing Model (CAPM). This methodology is based on a risk-free rate plus a risk premium. Operating assumptions are best estimate assumptions and based on historical data where available. Economic assumptions are based on observable market data and projections of future trends. If the recoverable amount is lower than its carrying amount, the difference is directly charged to the income statement as an impairment loss. In the event of impairment, a.s.r. first reduces the carrying amount of the goodwill allocated to the CGU. After that, the carrying amount of the other assets included in the unit is reduced pro rata to the carrying amount of all the assets in the unit. D. Investment property Investment property is property held to earn rent or for capital appreciation or both. Property interests held under operating leases are classified and accounted for as investment property. In some cases, a.s.r. is the owner-occupier of investment properties. If owner-occupied properties cannot be sold separately, they are treated as investment property only if a.s.r. holds an insignificant portion for use in the supply of services or for administrative purposes. Property held for own uses (owner-occupied) is recognised within property, plant and equipment. Investment property is primarily recognised using the fair value model. After initial recognition, a.s.r. remeasures all of its investment property (see accounting policy B) whereby any gain or loss arising from a change in the fair value of the specific investment property is recognised in the income statement under fair value gains and losses. Residential property is generally let for an indefinite period. Other investment property is let for defined periods under leases that cannot be terminated early. Some contracts contain renewal options. Rentals are accounted for as investment income in the period to which they relate. If there is a change in the designation of property, it can lead to: • Reclassification from property, plant and equipment to investment property: at the end of the period of owner-occupation or at inception of an operating lease with a third party; or • Reclassification from investment property to property, plant and equipment: at the commencement of owner-occupation or at the start of developments initiated with a view to selling the property to a third party. The following categories of investment property are recognised by a.s.r. based primarily on the techniques used in determining the fair value of the investment property: • Retail; • Residential; • Rural; • Offices; • Other (consisting primarily of parking); • Investment property under development. Property under development for future use as investment property is recognised as investment property. The valuation of investment property takes (expected) vacancies into account. Borrowing costs directly attributable to the acquisition or development of an asset are capitalised and are part of the cost of that asset. Borrowing costs are capitalised when the following conditions are met: • Expenditures for the asset and borrowing costs are incurred; and • Activities are undertaken that are necessary to prepare an asset for its intended use. Borrowing costs are no longer capitalised when the asset is ready for use or sale. If the development of assets is interrupted for a longer period, capitalisation of borrowing costs is suspended. If the construction is completed in stages and each part of an asset can be used separately, the borrowing costs for each part that reaches completion are no longer capitalised. E. Financial assets and financial liabilities Recognition and initial measurement a.s.r. recognises deposits and loans and borrowings on the date on which they originate. All other financial instruments are recognised at the transaction date, which is the date on which a.s.r. becomes party to the contractual stipulations of the instrument. Financial assets or financial liabilities are initially measured at fair value plus, for a financial asset or financial liability not measured at FVTPL, transaction costs that are directly attributable to its acquisition or issue. Classification and subsequent measurement When a.s.r. becomes party to a financial asset contract, the related assets are classified into one of the following categories: • Amortised cost; • Financial assets at fair value through other comprehensive income (FVOCI); or • Financial assets at fair value through profit or loss (FVTPL). The classification of the financial assets is determined at initial recognition. The classification and measurement of certain financial assets (debt instruments) is based on a.s.r.’s business models in which a financial asset is managed, and its contractual cash flow characteristics. For detailed information on the fair value of the financial assets see accounting policy B. Financial statements Introduction Consolidated financial statements Accounting policies Group structure and segment information Notes to the consolidated balance sheet Notes to the consolidated income statement Other notes Risk management Capital management Operating result Company financial statements

7.3 Accounting policies • Annual Report 2024 ASR Nederland N.V. 15 Financial assets at amortised cost A financial asset (debt instrument) can be measured at amortised cost if it meets both of the following conditions and is not designated as FVTPL: • It is held within a business model whose objective is to hold assets to collect contractual cash flows; and • Its contractual terms give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding. This is known as the SPPI test. Debt instruments at amortised cost include mortgage loans and private loans held by Aegon Bank N.V. (Knab) and Aegon Hypotheken B.V. (Aegon hypotheken). Financial assets that are designated as hedged items are measured in accordance with the requirements for hedge accounting. Financial assets at FVOCI Financial assets at FVOCI can be divided into debt instruments and equity instruments. A debt instrument can be measured at FVOCI if it meets both the following conditions and is not designated as at FVTPL: • It is held within a business model whose objective is achieved by both collecting contractual cash flows and selling financial assets; and • Its contractual terms give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding. Debt instruments at FVOCI are measured at fair value. Unrealised fair value gains and losses are recognised in other comprehensive income, and are subsequently reclassified to profit or loss when realised. Interest income is recognised in profit or loss using the effective interest rate. Debt instruments at FVOCI are subject to the impairment requirements. a.s.r. has only classified the bonds portfolio held by Knab at FVOCI. Equity instruments can be measured at FVOCI if they are not held for trading. There is no subsequent recycling of fair value gains and losses to profit or loss following the derecognition of the investment if elected to measure the equity investments as FVOCI. a.s.r. classifies most equity instruments at FVOCI to reduce volatility in the income statement. Financial assets at FVTPL All financial assets not classified as measured at amortised cost or FVOCI, as described above, are measured at FVTPL. Financial assets at FVTPL include: • Derivatives that do not qualify for hedge accounting; • Financial assets that are managed and whose performance is evaluated on a fair value basis, such as:—Debt instruments for which a.s.r. has identified the business model Other;—Investments related to direct participating contracts;—Financial assets held for trading; • Associates for which a.s.r. elects to measure at FVTPL under IFRS 9. Hedge accounting (see also risk management section in section 7.8) To qualify for hedge accounting, the hedge relationship is designated and formally documented at inception, detailing the particular risk management objective and strategy for the hedge (which includes the item and risk that is being hedged), the derivative that is being used and how hedge effectiveness is being assessed. A derivative has to be effective in accomplishing the objective of offsetting either changes in fair value or cash flows for the risk being hedged. The effectiveness of the hedging relationship is evaluated on a prospective and retrospective basis using qualitative and quantitative measures of correlation. A hedging relationship is considered effective if the results of the hedging instrument are within a ratio of 80% to 125% of the results of the hedged item. a.s.r. has elected to continue to apply the hedge accounting requirements of IAS 39 for macro fair value hedges (EU ‘carve out’) on adoption of IFRS 9. As part of its asset liability management, a.s.r. enters into economic hedges to limit its risk exposure at Knab and Aegon hypotheken. These transactions are assessed to determine whether hedge accounting can and should be applied. a.s.r. currently applies hedge accounting for fair value hedges. Fair value hedges a.s.r. applies fair value hedge accounting to portfolio hedges of interest rate risk (fair value macro hedging) under the EU ‘carve out’ of EU-IFRS. The EU ‘carve out’ macro hedging enables a group of derivatives (or proportions thereof) to be viewed in combination and jointly designated as the hedging instrument and removes some of the limitations in fair value hedge accounting. Under the EU ‘carve out’, ineffectiveness in fair value hedge accounting only arises when the revised projection of the amount of cash flows in scheduled time buckets falls below the designated amount of that bucket. a.s.r. applies fair value hedge accounting for portfolio hedges of interest rate risk (macro hedging) under the EU ‘carve out’ to mortgage loans. Changes in the fair value of the derivatives are recognised in the income statement, together with the fair value adjustment on the mortgage loans (hedged items) insofar as attributable to interest rate risk (the hedged risk). If the hedge relationship no longer meets the criteria for hedge accounting, the cumulative adjustment of the hedged item is, in the case of interest bearing instruments, amortised through the income statement over the remaining term of the original hedge or recognised directly when the hedged item is derecognised. 879241-001-Part-2 28Mar25 13:48 Page 185 Financial statements Introduction Consolidated financial statements Accounting policies Group structure and segment information Notes to the consolidated balance sheet Notes to the consolidated income statement Other notes Risk management Capital management Operating result Company financial statements

7.3 Accounting policies • Annual Report 2024 ASR Nederland N.V. 16 Knab and Aegon hypotheken hold portfolios of long-term fixed rate mortgages and therefore are exposed to changes in fair value due to movements in market interest rates. Knab and Aegon hypotheken manage this risk exposure by entering into pay fixed/receive floating interest rate swaps. Only the interest rate risk element is hedged and therefore other risks, such as credit risk, are managed but not hedged by Knab and Aegon hypotheken. This hedging strategy is applied to the portion of exposure that is not naturally offset against matching positions held by Knab and Aegon hypotheken. Changes in fair value of the long-term fixed rate mortgages arising from changes in interest rate are usually the largest component of the overall change in fair value. This strategy is designated as a fair value hedge and its effectiveness is assessed by comparing changes in the fair value of the loans attributable to changes in the benchmark rate of interest with changes in the fair value of the interest rate swaps. Knab and Aegon hypotheken establish the hedging ratio by matching the notional of the derivatives with the principal of the portfolio being hedged. Possible sources of ineffectiveness are as follows: • Differences between the expected and actual volume of prepayments, as Knab and Aegon hypotheken hedge to the expected repayment date taking into account expected prepayments based on past experience; • Difference in the discounting between the hedged item and the hedging instrument, as cash collateralised interest rate swaps are discounted using Overnight Indexed Swaps (OIS) discount curves, which are not applied to the fixed rate mortgages; • Hedging derivatives with a non-zero fair value at the date of initial designation as a hedging instrument; and • Counterparty credit risk which impacts the fair value of uncollateralised interest rate swaps but not the hedged items. Knab and Aegon hypotheken manage the interest rate risk arising from fixed rate mortgages by entering into interest rate swaps on a monthly basis. The exposure from these portfolios frequently changes due to new loans originated, contractual repayments and early prepayments made by customers in each period. As a result, Knab and Aegon hypotheken adopt a dynamic hedging strategy (sometime referred to as a ‘macro’ or ‘portfolio’ hedge) to hedge the exposure profile by closing and entering into new swap agreements at each month-end. Knab and Aegon hypotheken use the portfolio fair value hedge of interest rate risk to recognise fair value changes related to changes in interest rate risk in the mortgage portfolio, and therefore reduce the profit or loss volatility that would otherwise arise from changes in fair value of the interest rate swaps alone. Accrued interest In line with Solvency II reporting a.s.r. accounts for debt instruments at their “dirty” fair value, thus including any related accrued interest. Business model assessment The business model is determined at a level that reflects how groups of financial assets are managed together to achieve a particular business objective. a.s.r.’s business models refer to how a.s.r. manages its financial assets in order to generate cash flows. a.s.r. identifies the business model Hold to Collect for the mortgage loans and private loans held by Knab and Aegon hypotheken and for its other financial assets, and identifies the business model Hold to Collect & Sell for the bonds portfolio held by Knab. All other debt instruments are mandatorily designated as at FVTPL (business model Other). Assessment whether contractual cash flows are solely payments of principal and interest (SPPI) For the purpose of this assessment, principal is defined as the fair value of the financial asset on initial recognition. However, the principal may change over time – e.g. if there are repayments of principal. Interest is defined as consideration for the time value of money, for the credit risk associated with the principal amount outstanding during a particular period of time and for other basic lending risks (e.g. liquidity risk) and costs (e.g. administrative costs), as well as a profit margin that is consistent with a basic lending arrangement. Financial assets with embedded derivatives are considered in their entirety when determining whether their cash flows are SPPI. a.s.r. assesses the SPPI for the loans and bonds portfolio held by Knab and Aegon hypotheken and for its other financial assets. All other debt instruments are mandatorily designated as at FVTPL (business model Other). Subsequent measurement and gains and losses Financial assets at amortised cost Financial assets at amortised cost are measured at amortised cost using the effective interest method. Interest income, foreign exchange gains and losses and impairment are recognised in profit or loss. Any gain or loss on derecognition is also recognised in profit or loss. Financial assets at FVOCI Equity investments at FVOCI are measured at fair value. All fair value gains and losses are recorded in OCI, without recycling to profit or loss. Dividends from such investments continue to be recognised in profit or loss as Investment income when a.s.r.’s right to receive payments is established. Impairment requirements are not applicable to equity investments measured as FVOCI. Financial assets at FVTPL Financial assets at FVTPL are measured at fair value. Net gains and losses, including any interest or dividend income and foreign exchange gains and losses, are recognised in profit or loss. Impairment requirements are not applicable to financial assets measured at FVTPL. See accounting policy W3. 879241-001-Part-2 28Mar25 13:48 Page 186 Financial statements Introduction Consolidated financial statements Accounting policies Group structure and segment information Notes to the consolidated balance sheet Notes to the consolidated income statement Other notes Risk management Capital management Operating result Company financial statements

7.3 Accounting policies • Annual Report 2024 ASR Nederland N.V. 17 Financial liabilities Classification a.s.r. classifies its liabilities into one of the following categories: • financial liabilities at FVTPL (derivatives); or • financial liabilities at amortised cost (all other financial liabilities). Subsequent measurement and gains and losses Financial liabilities at FVTPL Financial liabilities at FVTPL are measured at fair value. Net gains and losses, including any interest expenses and foreign exchange gains and losses, are recognised in profit or loss. Financial liabilities at amortised cost Financial liabilities at amortised cost are measured at amortised cost using the effective interest method. Interest expenses, foreign exchange gains and losses are recognised in profit or loss. Any gain or loss on derecognition is also recognised in profit or loss. Accrued interest In line with Solvency II reporting a.s.r. accounts for financial liabilities at their “dirty” fair value, thus including any related accrued interest. Interest on financial liabilities Interest expenses are calculated by applying the effective interest rate to the amortised cost of the liability. When calculating the effective interest rate, a.s.r. estimates future cash flows considering all contractual terms of the liability. Derivatives including embedded derivatives Derivatives within the insurance entities are primarily used by a.s.r. for hedging interest rate and exchange rate risks, for hedging future transactions and the exposure to market risks. These derivatives are classified as held-for-trading. Derivatives are measured at fair value with changes in fair value recognised in profit or loss. Derivatives may be embedded in another contractual arrangement (a host contract). For contracts where the host contract is a financial asset in the scope of IFRS 9, the hybrid financial instrument as a whole is assessed for classification and the embedded derivative is not separated from the host contract. • the terms of the embedded derivative would have met the definition of a derivative if they were contained in a separate contract; and • the economic characteristics and risks of the embedded derivative are not closely related to those of the host contract. Impairments in the P&L a.s.r. recognises loss allowances for ECL on debt instruments measured at amortised cost or FVOCI. a.s.r. uses the low credit risk simplification for investment grade debt instruments and recognises a lifetime ECL for other financial assets using the simplified approach. Lifetime ECL are the ECL that result from all possible default events over the expected life of a financial instrument. ECLs are a probability-weighted estimate of credit losses. Credit losses are measured as the present value of all cash shortfalls (i.e. the difference between the cash flows due to a.s.r. in accordance with the contract and the cash flows that a.s.r. expects to receive). The maximum period considered when estimating ECLs is the maximum contractual period over which a.s.r. is exposed to credit risk. Write-off The gross carrying amount of a financial asset is written off (either partially or in full) to the extent that there is no realistic prospect of recovery. This is generally the case when a.s.r. determines that the borrower does not have assets or resources of income that could generate sufficient cash flows to repay the amounts subject to the write-off. However, financial assets that are written off could still be subject to enforcement activities in order to comply with a.s.r.’s procedures for recovery of amounts due. Should amounts be recovered these are then recognised when the payment has been received. Derecognition and contract modification Financial assets a.s.r. derecognises a financial asset when the contractual rights to the cash flows from the financial asset expire, or it transfers the rights to receive the contractual cash flows in a transaction in which substantially all of the risks and rewards of ownership of the financial asset are transferred or in which a.s.r. neither transfers nor retains substantially all of the risks and rewards of ownership and it does not retain control of the financial asset. On derecognition of a financial asset, the difference between the carrying amount at the date of derecognition and the consideration received (including any new asset obtained less any new liability assumed) is recognised in the income statement, unless the financial asset is an equity instrument and is measured at fair value through other comprehensive income. For these instruments any revaluation amount is transferred within equity from unrealised gains and losses to retained earnings. Financial statements Introduction Consolidated financial statements Accounting policies Group structure and segment information Notes to the consolidated balance sheet Notes to the consolidated income statement Other notes Risk management Capital management Operating result Company financial statements A derivative embedded in a host insurance or reinsurance contract is not accounted for separately from the host contract if the embedded derivate itself meets the definition of an insurance or reinsurance contract. For other contracts, a.s.r. accounts for an embedded derivative separately from the host contract when: • the hybrid 879241 contract is—001 not measured -Part at—2 FVTPL; 28Mar25 13:48 a.s.r. enters into transactions whereby it transfers assets recognised in its balance sheet, but retains either all or substantially all of the risks and rewards of the transferred assets. In these cases, the transferred assets are not derecognised. Examples of such transactions are repurchase agreements and securities lending. The asset recognised for cash paid on reverse repurchase agreements is presented under investments. The liability recognised for cash collateral received on repurchase agreements is presented under the line item due 187 to banks .

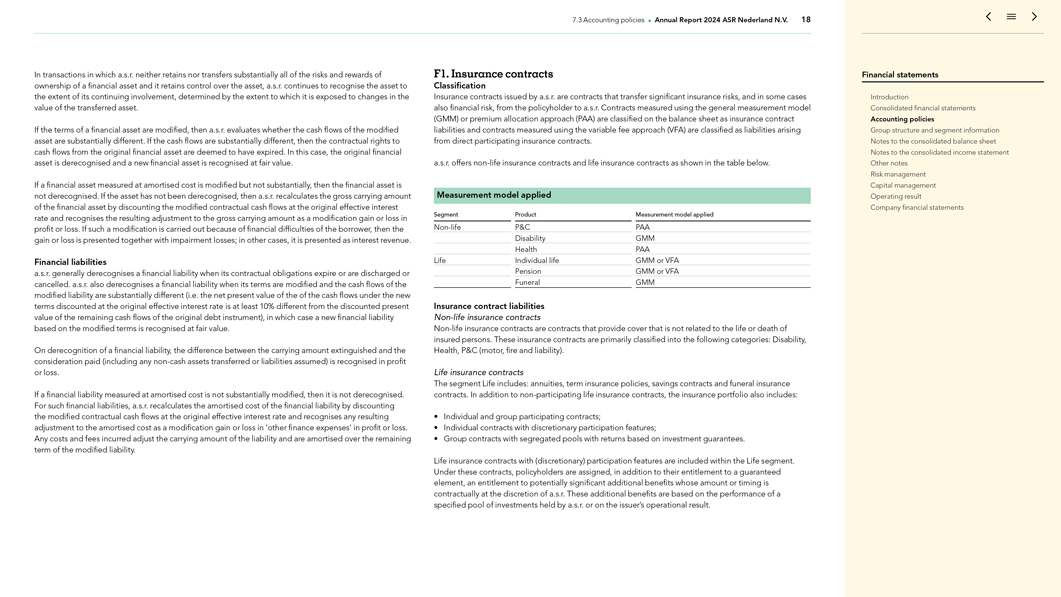

7.3 Accounting policies • Annual Report 2024 ASR Nederland N.V. 18 In transactions in which a.s.r. neither retains nor transfers substantially all of the risks and rewards of ownership of a financial asset and it retains control over the asset, a.s.r. continues to recognise the asset to the extent of its continuing involvement, determined by the extent to which it is exposed to changes in the value of the transferred asset. If the terms of a financial asset are modified, then a.s.r. evaluates whether the cash flows of the modified asset are substantially different. If the cash flows are substantially different, then the contractual rights to cash flows from the original financial asset are deemed to have expired. In this case, the original financial asset is derecognised and a new financial asset is recognised at fair value. If a financial asset measured at amortised cost is modified but not substantially, then the financial asset is not derecognised. If the asset has not been derecognised, then a.s.r. recalculates the gross carrying amount of the financial asset by discounting the modified contractual cash flows at the original effective interest rate and recognises the resulting adjustment to the gross carrying amount as a modification gain or loss in profit or loss. If such a modification is carried out because of financial difficulties of the borrower, then the gain or loss is presented together with impairment losses; in other cases, it is presented as interest revenue. Financial liabilities a.s.r. generally derecognises a financial liability when its contractual obligations expire or are discharged or cancelled. a.s.r. also derecognises a financial liability when its terms are modified and the cash flows of the modified liability are substantially different (i.e. the net present value of the of the cash flows under the new terms discounted at the original effective interest rate is at least 10% different from the discounted present value of the remaining cash flows of the original debt instrument), in which case a new financial liability based on the modified terms is recognised at fair value. On derecognition of a financial liability, the difference between the carrying amount extinguished and the consideration paid (including any non-cash assets transferred or liabilities assumed) is recognised in profit or loss. If a financial liability measured at amortised cost is not substantially modified, then it is not derecognised. For such financial liabilities, a.s.r. recalculates the amortised cost of the financial liability by discounting the modified contractual cash flows at the original effective interest rate and recognises any resulting adjustment to the amortised cost as a modification gain or loss in ‘other finance expenses’ in profit or loss. Any costs and fees incurred adjust the carrying amount of the liability and are amortised over the remaining term of the modified liability. 879241-001-Part-2 28Mar25 13:48 Page 188 F1. Insurance contracts Classification Insurance contracts issued by a.s.r. are contracts that transfer significant insurance risks, and in some cases also financial risk, from the policyholder to a.s.r. Contracts measured using the general measurement model (GMM) or premium allocation approach (PAA) are classified on the balance sheet as insurance contract liabilities and contracts measured using the variable fee approach (VFA) are classified as liabilities arising from direct participating insurance contracts. a.s.r. offers non-life insurance contracts and life insurance contracts as shown in the table below. Measurement model applied Segment Product Measurement model applied Non-life P&C PAA Disability GMM Health PAA Life Individual life GMM or VFA Pension GMM or VFA Funeral GMM Insurance contract liabilities Non-life insurance contracts Non-life insurance contracts are contracts that provide cover that is not related to the life or death of insured persons. These insurance contracts are primarily classified into the following categories: Disability, Health, P&C (motor, fire and liability). Life insurance contracts The segment Life includes: annuities, term insurance policies, savings contracts and funeral insurance contracts. In addition to non-participating life insurance contracts, the insurance portfolio also includes: • Individual and group participating contracts; • Individual contracts with discretionary participation features; • Group contracts with segregated pools with returns based on investment guarantees. Life insurance contracts with (discretionary) participation features are included within the Life segment. Under these contracts, policyholders are assigned, in addition to their entitlement to a guaranteed element, an entitlement to potentially significant additional benefits whose amount or timing is contractually at the discretion of a.s.r. These additional benefits are based on the performance of a specified pool of investments held by a.s.r. or on the issuer’s operational result. Financial statements Introduction Consolidated financial statements Accounting policies Group structure and segment information Notes to the consolidated balance sheet Notes to the consolidated income statement Other notes Risk management Capital management Operating result Company financial statements

7.3 Accounting policies • Annual Report 2024 ASR Nederland N.V. 19 Liabilities arising from direct participating insurance contracts. a.s.r. classifies an insurance contract as a direct participating contract for which at inception the following criteria are met: • the contractual terms specify that the policyholder participates in a share of a clearly identified pool of underlying items; • a.s.r. expects to pay the policyholder an amount equal to a substantial share of the fair value returns on the underlying items; and • a.s.r. expects a substantial proportion of any change in the amounts to be paid to the policy holder to vary with the change in the fair value of the underlying items. Life insurance contracts with direct participating features are included within the Life segment and mainly concern unit-linked contracts and group pension contracts, with policyholders bearing the investment risk. An investment unit is a share in an investment fund that a.s.r. acquires on behalf of the policyholders using net premiums paid by the policyholders. The cash flow upon maturity of the contract is equal to the value of the investment units of the fund in question. Contracts that meet the requirements of a direct participating contract are measured using the variable fee approach (VFA). Separating components Currently a.s.r. does not separate any components from its insurance contracts. Non-distinct investment components Non-distinct investment components are identified for products where under all circumstances a payment will be made to the policyholder. These are generally recognised for GMM as the surrender value of the funeral insurance and as the savings account related to the mortgage savings insurance. For VFA policies the non-distinct investment component is the minimum payment that will be made under all circumstances (i.e. the minimum of surrender, lapse and maturity). Level of aggregation Insurance contracts are aggregated into groups for measurement purposes. a.s.r. identifies portfolios of insurance contracts comprising contracts subject to similar risks and managed together. Each portfolio is then divided into cohorts of contracts issued within a maximum of one year and divided into two groups based on the profitability buckets for: • any contracts that are onerous on initial recognition; and • any remaining contracts in the portfolio. The profitability bucket for contracts that have no significant possibility of becoming onerous subsequently is currently not used by a.s.r. Similar risks managed together are generally based on the homogeneous risk groups similar to those used in Solvency II at inception, more or less granularity is applied where applicable. Contracts within a portfolio that would fall into different groups only because law or regulation specifically constraints a.s.r.’s practical ability to set a different price or level of benefits for policyholders with different characteristics are included in the same group. This applies to contracts issued in Europe that are required by EU regulation to be priced on a gender-neutral basis. The resulting groups represent the level at which the recognition and measurement accounting policies are applied. The groups are established on initial recognition and their composition is not subsequently reassessed. Whether a contract is onerous or not is a policy (test) which is set per business. Part of this policy will be pricing and thresholds and forward looking metrics available within a.s.r. The test is performed based on the contracts which are issued in any specific calendar year and are grouped according to the similar risks managed together criteria as described above. The test is generally performed on a set of contracts using reasonable and supportable information, considering that the outcome would be the same had the individual policy assessment been performed. Recognition a.s.r. recognises a group of insurance contracts issued from the earliest of: • the beginning of the coverage period of the group of contracts. The coverage period is the period during which a.s.r. provides services (insurance services, investment-return services or investment-related services) in respect of all premiums within the boundary of the insurance contract; • the date when the first payment from a policyholder in the group becomes due. If there is no contractual due date, then it is considered to be the date when the first payment is received from the policyholder; or • the group of onerous contracts, the date when the group becomes onerous. Insurance contracts acquired in a (portfolio) transfer or a business combination are recognised on the date of acquisition. When the contract is recognised, it is added to an existing group of contracts or, if the contract does not qualify for inclusion in an existing group, it forms a new group to which future contracts can be added. Groups of contracts are established on initial recognition and their composition is not revised once all contracts have been added to the group. Contract boundaries The measurement of a group of contracts includes all of the future cash flows within the boundary of each contract in the group. Cash flows are within the boundary of a contract if they arise from substantive rights and obligations that exist during the reporting period under which a.s.r. can compel the policyholder to pay premiums or has a substantive obligation to provide services. 879241-001-Part-2 28Mar25 13:48 Page 189 Financial statements Introduction Consolidated financial statements Accounting policies Group structure and segment information Notes to the consolidated balance sheet Notes to the consolidated income statement Other notes Risk management Capital management Operating result Company financial statements