Financial Condition Report 2025

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

For the month of May 2026

Commission File Number 001-10882

Aegon Ltd.

| Aegon Limited | Statutory seat | Principle place of business | Bermuda Registrar of Companies number: 202302830 | |||

| An exempted company with liability | Canon’s Court | World Trade Center Schiphol | (September 30, 2023) | |||

| limited by shares | 22 Victoria Street | Schiphol Boulevard 223 | Dutch Chamber of Commerce number: 27076669 | |||

| Hamilton HM 12 | 1118 BH Schiphol | Aegon Limited is a non-resident company under the Dutch | ||||

| www.aegon.com | Bermuda | The Netherlands | Act Non Residential Companies |

Aegon’s 2025 Financial Condition Report, dated May 20, 2026, is included as appendix and incorporated herein by reference.

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| Aegon Ltd | ||||||

| (Registrant) | ||||||

| Date May 20, 2026 | By | /s/ S. Knol | ||||

| S. Knol | ||||||

| Director Financial Reporting & Operations | ||||||

Financial Condition Report 2025

Table of contents

|

|

3 |

| ||||

|

|

4 |

| ||||

|

|

4 |

| ||||

|

|

4 |

| ||||

|

|

5 |

| ||||

|

|

5 |

| ||||

| A.1 |

|

6 |

| |||

| A.2 |

|

7 |

| |||

| A.3 |

|

8 |

| |||

| A.4 |

|

8 |

| |||

| A.5 |

|

8 |

| |||

| A.6 |

|

10 |

| |||

| A.7 |

|

11 |

| |||

| A.8 |

|

12 |

| |||

| B.1 |

|

13 |

| |||

| B.2 |

|

17 |

| |||

| B.3 |

|

19 |

| |||

| B.4 |

|

23 |

| |||

| B.5 |

|

26 |

| |||

| B.6 |

Actuarial Function - a description of how the insurance Group’s Actuarial Function is implemented |

|

27 |

| ||

| B.7 |

|

28 |

| |||

| B.8 |

|

28 |

| |||

| C.1 |

|

30 |

| |||

| C.2 |

|

37 |

| |||

| C.3 |

|

39 |

| |||

| C.4 |

|

41 |

| |||

| C.5 |

|

42 |

| |||

| C.6 |

|

43 |

| |||

| D.1 |

The valuation basis, assumptions and methods used to derive the value of each asset class |

|

45 |

| ||

| D.2 |

The valuation basis, assumptions and methods used to derive the value of technical provisions |

|

45 |

| ||

| D.3 |

|

48 |

| |||

| D.4 |

The valuation basis, assumptions and methods used to derive the value of other liabilities |

|

49 |

| ||

| D.5 |

Any other material information | 50 | ||||

| E.1 |

|

52 |

| |||

| E.2 |

|

58 |

| |||

| E.3 |

|

59 |

| |||

| F.1 |

|

62 |

| |||

| F.2 |

|

62 |

| |||

| 2 | Aegon Financial Condition Report 2025 |

Aegon Ltd. is referred to in this document as ‘Aegon’, or ‘the Company’, and is together with its member companies referred to as ‘Aegon Group’ or ‘the Group’. For such purposes ‘member companies’ means, in relation to Aegon Ltd., companies that are subsidiaries and any entities in which Aegon Ltd. or its subsidiaries hold a participation (or identified as such based on the establishment, contractually or otherwise, of strong and sustainable financial relationships among those companies).

As at December 31, 2025, Aegon is subjected to insurance group regulatory supervision by the Bermuda Monetary Authority (BMA) and has been qualified as an Internationally Active Insurance Group (IAIG) by the BMA. This document represents the Group Financial Condition Report (FCR) that is required to be published under the BMA Insurance (Group Supervision) Rules 2011.

Following the transfer of Aegon’s legal domicile to Bermuda on September 30, 2023, group supervision moved from the Dutch Central Bank (DNB) to the Bermuda Monetary Authority. Aegon’s group solvency ratio and surplus under the Bermuda Solvency framework is broadly aligned with that under the previously applied Solvency II framework during a transition period until the end of 2027. This includes translating Transamerica’s capital position into the group solvency position.

Aegon agreed to fully adopt the Bermuda solvency framework after the transition period. Aegon announced on May 16, 2025 that it will apply an aggregation approach to calculate its group solvency under the Bermuda solvency framework after the transition period. The resulting group solvency ratio is expected to be broadly similar to the current group solvency ratio and Aegon expects no material impact on its capital management framework. As announced on the Capital Markets Day held on December 10, 2025, due to the proposed redomiciliation of the legal seat to the US, Aegon needs to report under the US capital framework, which is currently expected to occur per January 2028. The lead and scope of group supervision will be reassessed by relevant regulators at the time of the redomiciliation.

Furthermore, the BMA has concluded its review of the eligibility of Aegon’s capital instruments under the Bermuda solvency framework:

| ● |

Aegon’s Solvency II-compliant instruments will continue to be eligible under the Bermuda solvency framework in the corresponding tier to Solvency II, and without any limitations; |

| ● |

The Junior Perpetual Capital Securities (JPCS), which in 2025 are still treated as Restricted Tier 1 until January 1, 2026, are eligible as Tier 2 Ancillary Capital following that date, until the end of 2029. Subject to a review in 2029, eligibility may be extended; |

| ● |

The Perpetual Cumulative Subordinated Bonds (PCSB), which in 2025 were treated as Restricted Tier 1, lost eligibility from January 1, 2026. |

The FCR for the year 2025 contains information about the Group’s business and performance, system of governance, risk profile, valuation for solvency purposes and capital management for the reporting period January 1, 2025 to December 31, 2025.

The figures in the FCR reflecting monetary amounts are presented in millions of euros and rounded to the nearest million unless stated otherwise. The rounded amounts may therefore not add up to the rounded total in all cases. All ratios and variances are calculated using the underlying amount rather than the rounded amount.

| 3 | Aegon Financial Condition Report 2025 |

|

||

Aegon has life insurance and pensions operations and is also active in savings and asset management operations, accident and health insurance and general insurance. Aegon focuses on two core markets (the United States and the United Kingdom1), three growth markets (Spain & Portugal, China, and Brazil) and one global asset manager.

Aegon operates in a fast-changing environment, in which we face new challenges but also opportunities. Aegon aims to play a key role in shaping a thriving and sustainable society by delivering on our purpose of Helping people live their best lives.

Aegon’s strategy is not just about strengthening our operational and financial performance, but also strives to have a positive impact on society at large, including by managing our direct operations and our investment activities as sustainably and responsibly as possible. For more information on Aegon’s strategy, please see pages 17 – 21 of Aegon’s 2025 Integrated Annual Report.

Full details on Aegon’s business and performance in 2025 are described in section A. Business and performance. Details of material subsequent events are set out in section F. Subsequent events.

Aegon’s Board of Directors consists of ten Non-Executive Directors and one Executive Director per December 31, 2025.

Subject to the provisions of the Bermuda Companies Act and the Company bye-laws, the Board manages and conducts the business of Aegon and is responsible for the general affairs of the Company, which includes setting the strategy of the Company. The Board may exercise all the powers of the Company except those powers that are required by the Bermuda Companies Act or the Company bye-laws to be exercised by the General Meeting.

Aegon’s risk management framework is designed and applied to identify and manage potential events and risks that may affect Aegon. This is established in the Enterprise Risk Management (ERM) framework, which aims to identify and manage individual and aggregate risks within Aegon’s risk tolerance to provide reasonable assurance regarding the achievement of Aegon’s objectives. The ERM framework applies to all businesses of Aegon for which it has operational control.

Full details on the Aegon’s system of governance are described in section B. Governance structure.

As an insurance group, Aegon accepts and manages risks for the benefit of its customers and other stakeholders. Aegon’s risk management and control systems are designed to ensure that these risks are managed effectively and efficiently in a way that is aligned with the Company’s strategy. The targeted risk profile is determined by customer needs, Aegon’s competence to manage the risk, Aegon’s preference for this risk, and whether there is sufficient capacity to take the risk. The targeted risk profile is set at Aegon Group level and developed in more detail within the subsidiaries where business is written. Aegon’s risk strategy provides direction for the targeted Aegon risk profile while supporting Aegon’s business strategy. Aegon is exposed to a range of underwriting, market, credit, liquidity and operational risks.

| 1 | On April 15, 2026, Aegon announced the sale of Aegon UK to Standard Life. This transaction further supports Aegon in its ambition to become a leading US life insurance and retirement group. |

| 4 | Aegon Financial Condition Report 2025 |

|

Composition of Group SCR |

||||||||||

| Amounts in EUR millions | 2025 | 2024 | ||||||||

| C.1.1 Market risk |

Market Risk (SF) | 252 | 274 | |||||||

| Market Risk (IM) | 1,132 | 1,190 | ||||||||

| C.1.3 Credit risk |

Counterparty default risk (SF) | 97 | 106 | |||||||

| Counterparty default risk (IM) | - | - | ||||||||

| C.1.2 Underwriting risk |

Life underwriting risk (SF) | 231 | 207 | |||||||

| Life underwriting risk (IM) | 1,433 | 1,518 | ||||||||

| Health underwriting risk (SF) | 44 | 39 | ||||||||

| Health underwriting risk (IM) | - | - | ||||||||

| Non-life underwriting risk (SF) | 35 | 34 | ||||||||

| Non-life underwriting risk (IM) | - | - | ||||||||

| C.1.5 Operational risk |

Operational risk (SF) | 22 | 20 | |||||||

| Operational risk (IM) | 253 | 320 | ||||||||

| LAC-DT | (424 | ) | (454 | ) | ||||||

| Total undiversified components | 3,076 | 3,255 | ||||||||

| Diversification | (1,325 | ) | (1,418 | ) | ||||||

| PIM SCR after diversification (AC only) | 1,751 | 1,837 | ||||||||

| Capital requirements for D&A, OFS and other | 3,273 | 3,770 | ||||||||

| Capital requirement for a.s.r. stake | 1,439 | 1,860 | ||||||||

| Group SCR | 6,464 | 7,466 | ||||||||

Full details on Aegon’s risk profile are described in section C. Risk profile.

Aegon values its Group Solvency balance sheet items on a basis that reflects their economic value.

Section D. Solvency valuation of this report provides further description of the bases, methods and assumptions used in the valuation of assets, technical provisions and other liabilities used to determine the Group’s Solvency position.

During 2025 Aegon Group and all the regulated entities within the Group continued to comply with the minimum regulatory capital requirements.

| Capital | ||||||||

| Amounts in EUR millions |

2025 | 2024 | ||||||

| Eligible Own Funds |

11,901 | 14,030 | ||||||

| SCR |

6,464 | 7,466 | ||||||

| Solvency ratio |

184% | 188% | ||||||

On a pro-forma basis taking into account this ineligibility for the PCSB, as mentioned in the Introduction, Aegon’s group solvency ratio would have been 7%-points lower compared with the group solvency ratio of 184% on December 31, 2025.

Further details of Aegon’s capital management objectives and policies, and regulatory capital on December 31, 2025, including Group sensitivities are described in section E. Capital management and section C. Risk profile.

| 5 | Aegon Financial Condition Report 2025 |

|

|

||

| Business and performance | ||

A.1.1 Name and contact details

Aegon, an exempted company limited by shares domiciled in Bermuda, is the holding company of the Aegon group of companies.

Statutory seat

Canon’s Court

22 Victoria street

Hamilton HM 12

Bermuda

Headquarters

Aegon Ltd.

Schiphol Boulevard 223

1118 BH Schiphol

The Netherlands

Telephone: +31 (0) 20 259 2500

www.aegon.com

A.1.2 Business overview

Aegon is an international financial services group which unites a diverse range of businesses that, together, help millions of people around the world live their best lives by offering a broad mix of investment, protection, and retirement solutions.

Aegon’s common shares are listed on Euronext Amsterdam and the New York Stock Exchange. Aegon’s main operating units are separate legal entities that operate under the laws of their respective countries. These legal entities are directly or indirectly held by several intermediate holding companies incorporated under Dutch law, including:

| • |

Aegon Iberia Holding B.V., the holding company for Aegon’s activities in Spain and Portugal; |

| • |

Aegon Europe Holding B.V., the holding company for Aegon’s UK activities and its employees in the Netherlands; |

| • |

Aegon International B.V., which serves as a holding company for the Aegon Group companies of non-European countries; and |

| • |

Aegon Asset Management Holding B.V., the holding company for a number of its asset management entities. |

Aegon’s financial results are impacted by a number of external factors, including demographic trends, market conditions and regulation. Furthermore, corporate actions taken by the Group, including acquisitions, disposals and other actions in order to achieve Aegon’s strategy impact Aegon’s financial results. The key significant business events or other events that have occurred over the reporting period that have had a material impact on Aegon are mentioned in section A.1.3.

A.1.3 Significant events in the reporting period

The following significant events took place during the reporting period.

Rate increase programs in Long-Term Care in Transamerica

Actuarially justified rate increases in Long-Term Care with a total value of approvals achieved since the beginning of 2023 amounts to USD 871 million, which is 124% of the USD 700 million target set at the 2023 CMD.

| 6 | Aegon Financial Condition Report 2025 |

Business and performance Name and contact details of the group supervisor

Expansion of dynamic hedge program for Variable Annuities

Transamerica expanded its dynamic hedge program for Variable Annuities to further reduce its equity market exposure. Previously, the program hedged market risks from policy riders. The expansion now includes first order equity market exposure of 25% of the Variable Annuities base contracts held by Transamerica Life Insurance Company, Transamerica’s largest insurance carrier. This reduces the economic equity market sensitivity for equity decreases of the portfolio and further solidifies the run-off of the Variable Annuities portfolio.

Reinsurance Secondary Guarantee Universal Life

Aegon decided to reinsure a block of Secondary Guarantee Universal Life (SGUL) contracts.

The transaction covers 30% of the face value of Transamerica’s SGUL business, bringing the total value addressed to 80% of the total SGUL portfolio in combination with previously executed management actions. It decreases the total capital employed by USD 0.3 billion to USD 2.7 billion, well ahead of the targeted reduction in 2025.

Share buyback

On January 13, 2025, Aegon announced the beginning of a EUR 150 million share buyback program. The share buyback program was completed on July 1, 2025, 25,200,170 common shares were repurchased for a total amount of EUR 150 million at an average price of EUR 5.9641 per share.

On July 1, 2025, Aegon announced the beginning of a EUR 200 million share buyback program. The share buyback program commenced on July 1, 2025, and was increased by EUR 200 million to EUR 400 million on August 25, 2025. The share buyback program was completed on December 16, 2025, 61,197,437 common shares were repurchased for a total amount of EUR 400 million at an average price of EUR 6.4772 per share.

Sale of its 12.5 million shares in a.s.r.

On September 3, 2025, Aegon sold 12.5 million shares of ASR Nederland N.V. through an accelerated bookbuild process to qualified institutional investors. The transaction price amounted to EUR 56 per a.s.r. share, resulting in gross proceeds of EUR 700 million and was settled on September 5, 2025. Through this transaction, Aegon’s share in a.s.r. reduced from 29.96% to 24.12% of a.s.r.’s share capital. The transaction resulted in a 13 percentage points increase in the Group solvency ratio and an IFRS book gain of approximately EUR 0.2 billion.

Capital funding

On June 8, 2025, Aegon has reset the annual interest rate on its EUR 114 million (NLG 250 million) perpetual cumulative subordinated bonds, which was originally issued in 1995, at 3.568%. As of June 8, 2005, and every ten years thereafter, Aegon has had the option to either call the bonds or reset the coupon.

Details of significant subsequent events are set out in section F. Subsequent events.

A.2 Name and contact details of the group supervisor

The Bermuda Monetary Authority is the group supervisor for Aegon.

BMA House

43 Victoria Street

Hamilton HM12

Bermuda

Telephone: +1 441 295 5278

www.bma.bm

| 7 | Aegon Financial Condition Report 2025 |

|

|

||

| Business and performance A description of the ownership details | ||

A.3 Name and contact details of the approved group auditor

EY Accountants B.V. is Aegon’s independent auditor.

EY Accountants B.V.

Antonio Vivaldistraat 150

1083 HP Amsterdam

The Netherlands

Telephone: +31 (0) 88 407 10 00

www.ey.com

A.4 A description of the ownership details including proportion of ownership interest of the insurance Group

A qualifying holding means a direct or indirect holding in Aegon Ltd., which represents 10% or more of the capital or of the voting rights or which makes it possible to exercise a significant influence over the management of Aegon Ltd. Only Vereniging Aegon’s holding qualifies based on this definition as of December 31, 2025.

Vereniging Aegon is a Dutch association located in Schiphol, the Netherlands, with a special purpose to protect the broader interests of Aegon Ltd. and its stakeholders. On December 31, 2025, Vereniging Aegon, Aegon’s largest shareholder, held a total of 270,149,311 common shares and 327,885,200 common shares B.

Under the terms of the 1983 Merger Agreement as amended in May 2013, Vereniging Aegon has the option to acquire additional common shares B. Vereniging Aegon may exercise this call option to keep or restore its total stake to 32.6% of the voting rights, irrespective of the circumstances that caused the total shareholding to be or become lower than 32.6%. Under the terms of the Voting Rights Agreement, in the absence of a ‘Special Cause’ Vereniging Aegon may cast one vote for every common share it holds and one vote only for every 40 common shares B it holds. A ‘Special Cause’ may include but is not limited to the acquisition of a 15% interest in Aegon Ltd., a tender offer for Aegon Ltd. shares a proposed business combination by any person or group of persons, whether individually or as a group, in each case other than in a transaction approved by the Board of Directors; or any other circumstance in which, in the opinion of the Vereniging Aegon, Vereniging Aegon not exercising its full voting power would seriously harm the interests of the company and the business connected with it. If Vereniging Aegon, acting at its sole discretion, determines that a Special Cause has arisen, it must notify the General Meeting of Shareholders at a shareholders meeting. In this event, Vereniging Aegon retains full voting rights on its common shares B for a period limited to six months after the announcement made in the shareholders meeting. Vereniging Aegon would, for that limited period, command 32.6% of the votes at a General Meeting of Shareholders. Accordingly, at December 31, 2025, the voting power of Vereniging Aegon under normal circumstances amounted to approximately 18.4%, based on the number of outstanding and voting shares (excluding issued common shares held in treasury by Aegon). In the event of a Special Cause, Vereniging Aegon’s voting rights will increase, to 32.6%, for up to six months. However, Vereniging Aegon may elect, after a Special Cause has occurred or commenced, to regard any related subsequent circumstance as a new Special Cause. In that case the Vereniging Aegon will make a new announcement in the general meeting of shareholders.

The principal subsidiaries of the parent company Aegon Ltd. are listed by geographical segment in section A.5. Except indicated otherwise, all are wholly owned, directly or indirectly, and are involved in insurance or reinsurance business, pensions, asset management or services related to these activities. The voting power in these subsidiaries held by Aegon is equal to the shareholdings, unless stated otherwise.

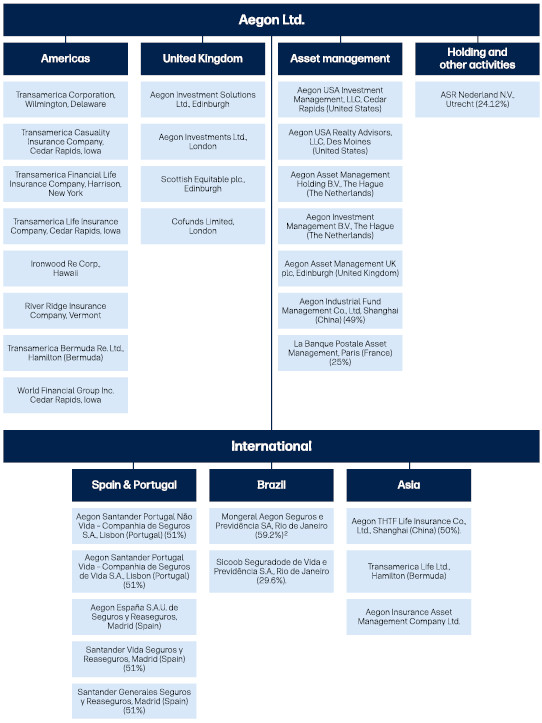

A.5 A group structure chart detailing the Group structure

Aegon’s operating segments are based on the businesses as presented in internal reports that are regularly reviewed by the CEO who is regarded as the chief operating decision maker. All reportable segments are involved in insurance or reinsurance business, asset management or services related to these activities. As per year-end 2025 the reportable segments are:

| • |

Americas: one operating segment which covers business units in the United States, including any of the units’ activities located outside of the United States; |

| • |

United Kingdom: one operating segment which covers business activities from platform business and traditional insurance in the United Kingdom; |

| 8 | Aegon Financial Condition Report 2025 |

Business and performance Insurance business written by changes in liability

| • |

International: one operating segment which covers businesses operating in Hong Kong, Singapore, China, Brazil, Bermuda, Spain and Portugal including any of these business units’ activities located outside these countries; |

| • |

Asset Management: one operating segment which covers business activities from Aegon Asset Management (AAM) Global Platforms and Strategic Partnerships; and |

| • |

Holding and other activities: one operating segment which includes financing, employee and other administrative expenses of holding companies. |

Aegon Ltd. is the ultimate owner of all entities within the group of entities. All subsidiary entities are owned 100%, directly or indirectly, by Aegon Ltd., unless indicated otherwise.

The structure of Aegon Ltd. is as follows1:

| 1 | This chart reflects the reporting structure, which is different from Aegon’s legal structure. This chart is not an exhaustive overview of Aegon’s structure. |

| 2 | Aegon has 50% voting rights in Mongeral Aegon, Seguros e Previdencia S.A., Rio de Janeiro. |

| 9 | Aegon Financial Condition Report 2025 |

|

|

||

| Business and performance Performance of investments by asset class | ||

A.6 Insurance business written by changes in liability for remaining coverage and segment by the insurance Group during the reporting period

The following table shows total insurance revenue split by component and split by reporting segment.

| Insurance revenue | ||||||||

| Amounts in EUR millions |

2025 | 2024 | ||||||

| Expected insurance claims and expenses |

7,194 | 7,870 | ||||||

| Earnings released from contractual service margin |

930 | 958 | ||||||

| Release of risk adjustment for non-financial risk |

265 | 295 | ||||||

| Allocated proportion of consideration that relates to recovery acquisition costs |

538 | 553 | ||||||

| Other |

(20 | ) | (19 | ) | ||||

| Insurance contracts not measured under the Premium Allocation Approach (PAA) |

8,906 | 9,656 | ||||||

| Insurance contracts measured under the PAA |

114 | 104 | ||||||

| Investment contracts with discretionary participation features (DPF) |

77 | 80 | ||||||

| Total Insurance revenue |

9,097 | 9,841 | ||||||

| Americas |

8,477 | 9,102 | ||||||

| United Kingdom |

422 | 543 | ||||||

| International |

1,748 | 1,674 | ||||||

| Eliminations |

(39 | ) | (45 | ) | ||||

| Segment total |

10,608 | 11,275 | ||||||

| Joint ventures and associates eliminations |

(1,511 | ) | (1,434 | ) | ||||

| Total Insurance revenue |

9,097 | 9,841 | ||||||

For further details and explanation, please refer to note 2 Material accounting policies information, note 5 Segment information and note 6 Insurance revenue of Aegon’s 2025 Integrated Annual Report.

| 10 | Aegon Financial Condition Report 2025 |

Business and performance Performance of investments by asset class

A.7 Performance of investments by asset class and details on material income and expenses incurred by the insurance Group during the reporting period

The following tables show the consolidated income statement, investment income and net result.

| Consolidated income statement | ||||||||

| Amounts in EUR millions |

2025 | 2024 | ||||||

| Insurance revenue |

9,097 | 9,841 | ||||||

| Insurance service expense |

(9,423 | ) | (9,790 | ) | ||||

| Net income / (expenses) on reinsurance held |

836 | 325 | ||||||

| Insurance service result |

511 | 376 | ||||||

| Interest revenue on financial instruments calculated using the effective interest method |

2,683 | 2,720 | ||||||

| Interest income from instruments measured at FVPL |

615 | 637 | ||||||

| Other investment income |

1,198 | 1,340 | ||||||

| Results from financial transactions |

15,632 | 11,593 | ||||||

| Impairment (losses) / reversals |

(46 | ) | (190 | ) | ||||

| Insurance finance income / (expenses) |

(20,227 | ) | (16,506 | ) | ||||

| Net reinsurance finance income/ (expenses) on reinsurance held |

564 | 611 | ||||||

| Interest expenses |

(135 | ) | (171 | ) | ||||

| Insurance net investment result |

285 | 34 | ||||||

| Interest revenue on financial instruments calculated using the effective interest method |

636 | 605 | ||||||

| Interest income from instruments measured at FVPL |

217 | 186 | ||||||

| Other investment income |

825 | 729 | ||||||

| Results from financial transactions |

10,065 | 7,634 | ||||||

| Impairment (losses) / reversals |

(22 | ) | (47 | ) | ||||

| Investment contract income / (expenses) |

(11,372 | ) | (8,781 | ) | ||||

| Interest expenses |

(18 | ) | (32 | ) | ||||

| Other net investment result |

331 | 294 | ||||||

| Interest charges |

(178 | ) | (190 | ) | ||||

| Financing net investment result |

(178 | ) | (190 | ) | ||||

| Total net investment result |

438 | 139 | ||||||

| Fees and commission income |

2,390 | 2,378 | ||||||

| Other operating expenses |

(2,928 | ) | (2,961 | ) | ||||

| Other income / (charges) |

130 | 145 | ||||||

| Other result |

(408 | ) | (438 | ) | ||||

| Results before share in profit / (loss) of joint ventures, associates and tax |

541 | 77 | ||||||

| Share and profit / (loss) of joint ventures |

303 | 238 | ||||||

| Share and profit / (loss) of associates |

200 | 345 | ||||||

| Result before tax from continuing operations |

1,045 | 660 | ||||||

| Income tax (expense) / benefit |

(65 | ) | 16 | |||||

| Net result |

980 | 676 | ||||||

| Investment income | 2025 | 2024 | ||||||||||||||||||||||||||||||

| Amounts in EUR millions | Interest income |

Dividend income |

Rental income |

Total | Interest income |

Dividend income |

Rental income |

Total | ||||||||||||||||||||||||

| Shares |

- | 1,993 | - | 1,993 | - | 2,041 | - | 2,041 | ||||||||||||||||||||||||

| Debt securities and money market instruments |

2,994 | - | - | 2,994 | 2,969 | - | - | 2,969 | ||||||||||||||||||||||||

| Loans |

420 | - | - | 420 | 428 | - | - | 428 | ||||||||||||||||||||||||

| Real estate |

- | - | 31 | 31 | - | - | 27 | 27 | ||||||||||||||||||||||||

| Other |

738 | - | - | 738 | 752 | - | - | 752 | ||||||||||||||||||||||||

| Total |

4,152 | 1,993 | 31 | 6,176 | 4,149 | 2,041 | 27 | 6,217 | ||||||||||||||||||||||||

| 11 | Aegon Financial Condition Report 2025 |

|

|

||

| Business and performance Any other material information | ||

| Results | ||||||||

| Amounts in EUR millions |

2025 | 2024 | ||||||

| Operating result geographically |

||||||||

| Americas |

1,209 | 1,062 | ||||||

| United Kingdom |

219 | 198 | ||||||

| International |

224 | 183 | ||||||

| Asset Management |

217 | 201 | ||||||

| Holding and other activities |

(224 | ) | (209 | ) | ||||

| Eliminations |

58 | 50 | ||||||

| Operating result |

1,702 | 1,485 | ||||||

| Fair value items |

80 | (208 | ) | |||||

| Realized gains / (losses) on investments |

(248 | ) | (36 | ) | ||||

| Net impairments |

(64 | ) | (236 | ) | ||||

| Non-operating items |

(231 | ) | (480 | ) | ||||

| Other income / (charges) |

(317 | ) | (245 | ) | ||||

| Result before tax |

1,154 | 760 | ||||||

| Income tax |

(174 | ) | (85 | ) | ||||

| Of which income tax from certain proportionately consolidated joint ventures and associates included income before tax | 109 | 100 | ||||||

| Net result |

980 | 676 | ||||||

For further details and explanation, please refer to note 2 Material accounting policies information, note 5 Segment information and note 6 Insurance revenue of Aegon’s 2025 Integrated Annual Report.

A.8 Any other material information

Aegon does not have any other material information regarding its business and performance to report.

| 12 | Aegon Financial Condition Report 2025 |

Governance structure

The governance structure of the Group is described in this chapter.

B.1 Parent board and senior executives

B.1.1 A description of the structure of the parent Board of Directors (Board) and senior executives, the roles, responsibilities and segregation of these responsibilities

Aegon is governed by two main corporate bodies: the Board of Directors and the General Meeting of Shareholders.

Aegon’s Board of Directors consists of ten Non-Executive Directors and one Executive Director per December 31, 2025. Subject to the provisions of the Bermuda Companies Act and the Company bye-laws, the Board manages and conducts the business of Aegon and is responsible for the general affairs of the Company, which includes setting the strategy of the Company. The Board may exercise all the powers of the Company except those powers that are required by the Bermuda Companies Act or the Company bye-laws to be exercised by the General Meeting.

The members of the Board owe a fiduciary duty to Aegon to act in good faith in their dealings with or on behalf of Aegon and exercise their powers and fulfil the duties of their office honestly. In the exercise of its duties the Board shall take into account (among other matters) the long-term consequences of decisions, sustainability, the Company’s reputation and the interests of all corporate stakeholders. For the purposes of a Director’s duty to act in the way they consider, in good faith, is in the best interests of the Company, the Director shall not be required to regard the benefit of any particular stakeholder interest or group of stakeholder interests as more important than any other.

The Board may, subject to its control, delegate all powers, authorities, and discretions relating to the day-to-day-operations and general business and affairs of Aegon to Aegon’s Chief Executive Officer (CEO). The Board oversees the execution of its responsibilities and delegated powers, authorities and discretions by the CEO and any other person or committee to which the Board has delegated any of its duties and responsibilities and is ultimately responsible for the fulfillment of the Board’s duties by them.

Pursuant to Aegon’s Board Regulations, the following matters are exclusively within the remit of the Board and cannot be delegated to the CEO:

| ● |

Reviewing and adopting (any material amendment to) the Company’s strategy and strategic plan, including the annual capital budget and allocation; |

| ● |

Reviewing the risks of the Business and the evaluation by the Board of the structure and operation of the internal risk management and control systems; |

| ● |

Reviewing and approving (any material amendment to) the (annual) business plan and the medium-term plan of the Region to the extent that it relates to the Group Budget; |

| ● |

Reviewing and approving (any material amendment to) the Group Budget; |

| ● |

Receiving, considering, and approving reports from the committees of the Board; and |

| ● |

The material matters listed in schedule 2 of Aegon Ltd. Board Regulations. |

The CEO is assisted by the Executive Committee, which provides support and expertise in safeguarding Aegon’s strategic goals. Aegon’s Executive Committee is composed of Lard Friese (CEO), Duncan Russell (CFO), Michele Bareggi, Will Fuller, Mike Holliday-Williams, Astrid Jäkel, Marco Keim, Onno van Klinken, Shawn Johnson, Deborah Waters and Holly Waters.

The Board has established an Audit Committee, Risk Committee, Compensation and Human Resource Committee and Nomination and Governance Committee from amongst its members.

General Meeting of Shareholders

A General Meeting of Shareholders (the “General Meeting”) is held annually and, if deemed necessary, the Board may convene a special General Meeting. The main function of the General Meeting is to decide on:

| ● |

(re)appointments to the Board; |

| ● |

appointment of the auditor; |

| ● |

amendments of the bye-laws; |

| ● |

adoption of the remuneration policy; |

| 13 | Aegon Financial Condition Report 2025 |

Governance structure Parent board and senior executives

| ● |

approval of resolutions of the Board entailing a significant change in the identity or character of the company or its business; |

| ● |

approval of final dividend payment; and |

| ● |

authorizing the Board to (i) limit or exclude pre-emptive rights, (ii) repurchase shares, and (iii) issue Aegon shares exceeding 10% of Aegon’s issued share capital unless the Board determines that the issuance of shares is necessary or conducive for purposes of safeguarding, conserving, or strengthening the capital position of Aegon. |

At the Annual General Meeting, the Board shall present shareholders with the annual accounts to be discussed during the meeting. The Board shall also annually present shareholders with a remuneration report that shall be put to an advisory vote, which shall not be binding on the Board or the company.

At the General Meeting, each common share carries one vote. In the absence of a Special Cause, Vereniging Aegon casts one vote for every 40 common shares B it holds.

Composition of the Board

The General Meeting appoints the members of the Board. The Board shall determine the number of Directors in its sole discretion, provided that the majority of the Board shall consist of Non-Executive Directors.

If the appointment of a member of the Board is proposed by the Board, the resolution of the General Meeting requires a simple majority of the votes cast, while otherwise, the resolution requires a two-thirds majority of the votes cast, which majority must represent at least half (1/2) of the then issued and outstanding shares.

Members of the Board will be appointed for a term of not more than four years and may be reappointed thereafter. After 12 years, a Non-Executive Director will no longer be considered independent. Aegon aims to ensure that the composition of the company’s Board is in line with Aegon’s Diversity and Inclusion Policy and is as such well-balanced in terms of professional background, geography, gender, and other relevant aspects of this policy. A profile, which is published on aegon.com as schedule 3 to the Board Regulations, has been established that outlines the required qualifications of the members of the Board. If the removal or suspension of a member of the Board is proposed by the Board, the General Meeting resolution requires a simple majority of the votes cast, while otherwise, the resolution requires a two-thirds majority of the votes cast, which majority must represent more than half (1/2) of the then issued and outstanding shares. The Board determines the remuneration and other terms of service of the Executive Director and the Non-Executive Directors, with due observance of the remuneration policy for the Board. This remuneration policy is adopted by the General Meeting ultimately at the fourth annual general meeting held after the General Meeting in which the remuneration policy was most recently adopted.

Committees

The Board also oversees the activities of its committees. These committees are composed exclusively of Non-Executive Directors and deal with specific issues related to Aegon’s financial accounts, risk management, executive remuneration, and appointments. These committees are the:

| ● |

Audit Committee; |

| ● |

Risk Committee; |

| ● |

Compensation and Human Resource Committee; and |

| ● |

Nomination and Governance Committee |

Audit Committee

Aegon has both an Audit Committee and a Risk Committee. With regard to the oversight of the operation of the risk management framework and risk control systems, including supervising the enforcement of relevant legislation and regulations, the Audit Committee operates in close coordination with the Risk Committee. Certain Board members participate in both committees and a combined meeting of the Audit and Risk Committees is scheduled on an annual basis.

The main role and responsibilities of the Audit Committee are to assist and advise the Board in fulfilling its oversight responsibilities regarding:

| ● |

The integrity and quality of the consolidated financial statements for the Group; |

| ● |

The effectiveness of the design, operation, and appropriateness of the enterprise risk management framework and internal control systems of the Group, including supervising the enforcement of the relevant legislation and regulations, supervising the operation of the code of conduct, and monitoring the internal control over financial reporting; |

| ● |

The disclosure of financial and non-financial information by the Group, including but not limited to the choice of accounting policies, application, and assessment of the effects of new rules, information about the handling of estimated items in the annual accounts, forecasts, and work of the External and Internal Auditors; |

| 14 | Aegon Financial Condition Report 2025 |

Governance structure Parent board and senior executives

| ● |

Compliance with recommendations and observations and following up on comments of Internal and External Auditors, including the review of compliance and complaints (whistleblowing) procedures and reports; |

| ● |

The role and functioning of the internal audit function; |

| ● |

The policy of the Company on tax planning; |

| ● |

Actuarial matters; |

| ● |

The funding, financing, capital structure and capital reporting of the Group, the Group Capital Plan, the Group Funding Plan, and treasury policies and procedures, including significant financial exposures; |

| ● |

Applications of information and communication technology, including risks relating to cyber security and information security; |

| ● |

Relationship with the External Auditor, including in particular its appointment, reappointment, or dismissal, qualifications, independence, remuneration, and any services for the Group; and |

| ● |

The performance of the external auditors and the effectiveness of the external audit process, including monitoring the independence and objectivity of the external auditor. |

The Audit Committee reports to the Board on its activities, identifying any matters about which it considers action or improvements are needed, and making recommendations on the steps to be taken. For more information about the functioning of the Audit Committee, please see the Audit Committee Charter on aegon.com.

Risk Committee

The Risk Committee focuses on the effectiveness of the design and operation and the appropriateness of the enterprise risk management framework and internal control systems of Aegon Ltd. This includes:

| ● |

Risk management strategy; |

| ● |

Risk tolerance; |

| ● |

Risk governance structure; |

| ● |

Risk competencies; |

| ● |

Product development and pricing; |

| ● |

Risk assessment; |

| ● |

Risk responses and internal control effectiveness; |

| ● |

Risk monitoring; and |

| ● |

Risk reporting |

Furthermore, the Risk Committee is responsible for reviewing and advising the Board with respect to the risk exposures as they relate to capital, earnings, liquidity, operations, and compliance with risk policies. The Audit Committee primarily relies on the Risk Committee for the topics mentioned above.

The Risk Committee works closely with the Audit Committee. One combined meeting was held in 2025. The meeting focused on the 2026 Group risk plan, and the 2025 Model Validation outcome and the 2026 Model Risk and Validation plan.

Compensation and Human Resource Committee

The Compensation and Human Resource Committee (formerly known as the Remuneration Committee) is designated to safeguard sound remuneration policies and practices within the company by overseeing the development and execution of these policies and practices in accordance with applicable laws and regulations. In order to ensure that the remuneration policies and practices take all types of risks properly into account, in addition to considering liquidity and capital levels, the Compensation and Human Resource Committee assesses in particular the remuneration governance processes, procedures and methodologies adopted. Furthermore, the Committee ensures that the overall remuneration policy is consistent with the longer-term strategy of the company and the longer-term interests of its shareholders, investors and other stakeholders as well as the public at large. This includes, among other things:

| ● |

Reviewing Aegon’s Global Remuneration Framework and making recommendations on the remuneration policies and advising the Board on the approval and adoption of the Global Remuneration framework; |

| ● |

Preparing a proposal for the remuneration of, and overseeing the remuneration of the Executive Directors; |

| ● |

Reviewing annually a proposal for the remuneration of the Heads of Control Functions; |

| ● |

Preparing recommendations regarding variable compensation both at the beginning and at the end of the performance year; and |

| ● |

Preparing the information provided to shareholders on remuneration policies and practices, including the Remuneration Report. |

| 15 | Aegon Financial Condition Report 2025 |

Governance structure Parent board and senior executives

Nomination and Governance Committee

The Nomination and Governance Committee focuses on the size, composition, and profile of the Board and addresses the functioning, succession, and proposed nomination of Directors and ensures that the corporate governance structure is in line with the applicable rules and regulations and advises on the responsible business strategy. This includes:

| ● |

Drawing up selection criteria and (re-)appointment procedures for nominations of Directors; |

| ● |

Preparing selection criteria and appointment procedures and proposal for the nomination of the Chief Executive Officer; |

| ● |

Updating the Board Profile and periodically assessing the size and composition of the Board and making a proposal for a composition profile of the Board; |

| ● |

Assessing the functioning of individual Directors and drawing up a plan for the succession of Directors; |

| ● |

Advising on and proposing to the Board candidates to be designated as Chairperson and Vice-Chairperson of the Board; |

| ● |

Supervising the policy of the Board on the selection criteria and appointment procedures for senior management; |

| ● |

Periodically discussing any relevant developments within the senior management and advising on any potential appointments of senior management; |

| ● |

Overseeing the corporate governance structure of the Company and compliance with any applicable corporate governance legislation and regulations; |

| ● |

Periodically assessing and advising on the responsible business strategy, including sustainability / Environmental, Social and Governance (ESG) strategy, as part of the corporate strategy; and |

| ● |

Overseeing the process of the annual self-evaluation of the Board and each of its committees. |

B.1.2 A description of remuneration policy and practices and performance-based criteria governing the parent board, senior executives and employees

Aegon’s Global Remuneration Framework (GRF) was designed in accordance with relevant rules and regulations. These included the remuneration rules of the Bermuda Monetary Authority. All remuneration policies within Aegon are derived from the GRF, such as the Directors’ Remuneration Policy and the local Remuneration Policies of our business units.

Aegon’s remuneration policies are derived from the GRF, which includes the Remuneration Policy for the Executive Director(s) and local business Remuneration Policies. These policies define specific terms and conditions for the employment of Aegon’s employee across various countries and local businesses. All steps in the remuneration process are governed by the GRF and its underlying policies. Staff from Human Resources, Risk Management and Compliance are involved in all steps of the process.

The below provides a summary of Aegon’s remuneration policies for the Directors of the Board in 2025. For further details, reference is made to the Remuneration Report on pages 68 - 79 of Aegon’s 2025 Integrated Annual Report.

The purpose of Non-Executive Director remuneration is to provide guaranteed, non-performance based, compensation for the different roles and responsibilities within the Board and its committees. The policy remains in place until the shareholders have adopted a new or revised policy in accordance with the applicable rules and regulatory requirements from the Insurance Code of Conduct of the Bermuda Monetary Authority. The Board of Directors will submit a proposal to the shareholders to adopt a remuneration policy at an Annual General Meeting at least every four years.

The remuneration of the Non-Executive Directors consists of annual Board retainers, partly paid in shares, and Committee membership retainers.

Each of these fees is a fixed amount. Where required, Aegon pays the employer social security contributions in the home country of the Non-Executive Board member. The employee social security contributions in the home country, if any, are paid by the Non-Executive Board member. The Non-Executive Board members are allowed to annually index the fees for economic developments in the Netherlands.

Executive Director remuneration in 2025

The total compensation allocated to Mr. Friese related to the 2025 performance year was EUR 3.5 million (2024: EUR 3.4 million), consisting of fixed compensation, Short-Term Incentive, pension, and benefits. The first vesting of a Long-Term Incentive grant is expected in 2028.

| 16 | Aegon Financial Condition Report 2025 |

Governance structure Fitness and proper requirements

Remuneration Executive Committee members

Members of the Executive Committee (excluding the CEO) were rewarded in 2025 based on local remuneration policies and in line with local market practice for roles with a similar scope and complexity. These policies were derived from the GRF. Their remuneration included fixed compensation, Short-Term Incentive, Long-Term Incentive, pension, and benefits. The Short-Term incentive was determined by a mix of individual and company performance indicators that are linked to Aegon’s objectives, business strategy, risk tolerance and long-term performance. Their targets, levels and performance assessment were agreed and determined by their local Remuneration Committee. The first vesting of a Long-Term Incentive grants is expected in 2028.

The Board and/or their local Remuneration Committee may decide on a potential downward adjustment of the variable compensation (based on either an ex-ante or ex-post risk assessment) or claw back.

Depending on local practices the pension arrangements may include provisions allowing for early retirement.

B.1.3 A description of pension as part of the Director remuneration policy

Pension is guaranteed remuneration which aims at the future financial security after retirement. The Executive Director is enrolled in the applicable local employee pension plan(s) and/or receives cash in lieu of pension. The annual total pension contributions equal 15% of base salary. For Mr. Friese these were paid in 2025 through the participation in Aegon’s defined contribution pension plan for employees based in the Netherlands (for their eligible earnings up to EUR 137,800) and as an additional gross allowance for the remaining part up to 15% of base salary.

B.1.4 Any material transactions with shareholder controllers, persons who exercise significant influence, the parent board or senior executives

There were no material transactions with members of the Board of Directors or Executive Committee.

B.2 Fitness and proper requirements

B.2.1 A description of the fit and proper process in assessing the parent board and senior executives

In accordance with the Bermudian Insurance Act 1978 (Insurance Act), Aegon has identified all persons who are a controller or officer as they are subject to fit and proper requirements, outlined in the Schedule, Minimum Criteria For Registration Section 1. These persons are subject to screening by the Bermuda Monetary Authority prior to their appointment in a controller or officer function as stated and defined by rule 30J of the Insurance Act. In connection with rule 5.6.A of the Insurance (Group Supervision) Rules 2011, assessment of the fit and proper condition of the controllers and officers is required on continuous basis.

Ongoing compliance with propriety requirements of the persons that effectively run the undertaking or have other key functions is a joint responsibility of the respective person as well as Aegon.

Fitness of the persons that effectively run the undertaking or have other key functions is determined at the point of selection as well as thereafter. As regards the point of selection, Aegon has drawn up a specific job profile for each function. These profiles detail the requirements in terms of the level of skills, knowledge and experience required to successfully fulfil the specific position within the company. The selection of the jobholder takes place by assessing the candidate for a position against these specific job requirements. The score on the three elements (expertise, knowledge and experience) is balanced and leads to potential recruitment in the position. Once selected, fitness of a specific person for a function is continuously assessed against this job profile. The ongoing compliance with fitness requirements is monitored as part of the regular human resource cycle within Aegon. Regular formal assessments of performance against the requirements are part of this cycle and are documented for record keeping purposes. In the human resources cycle, performance management is an important element in which targets are set and the results are monitored to assess if the jobholder continues to meet both the specific job requirements and the fitness requirements.

B.2.2 A description of the professional qualifications, skills, and expertise of the parent board and senior executives to carry out their functions

Executive Committee

The members of Aegon’s Executive Committee work alongside the CEO and help oversee operational issues and the implementation of Aegon’s strategy. Members are drawn from Aegon’s functional, business, and country units, and have both regional and global responsibilities. This ensures that Aegon is managed as an integrated international business. The Executive Committee provides vital support and expertise in pursuit of the company’s strategic objectives.

| 17 | Aegon Financial Condition Report 2025 |

|

|

||

| Governance structure Fitness and proper requirements | ||

Control functions

Furthermore, with regard to rule 4.5 of the Insurance (Group Supervision) Rules 2011, Aegon has implemented the following control functions: Risk Management, Compliance, Internal Audit, and the Actuarial Function. These functions have been in place within Aegon for many years.

Board of Directors

In accordance with Bermuda law, the Board manages and conducts the business of the Company and is responsible for the general affairs of the Company. This includes setting and evaluating the Company’s strategy, management’s policies and the effectiveness of which management implements its policies and it includes overseeing compliance with legal and regulatory requirements. In the exercise of its duties the Board shall take into account (among other matters) the long-term consequences of decisions, sustainability, Environmental, Social and Governance (ESG) priorities of the Company, the Company’s reputation, and the interest of all corporate stakeholders, including, amongst others, the shareholders, the Company’s employees, business relations, policyholders, relations with regulators, and other groups, directly or indirectly, influenced by the business of the Company, all in the broadest sense. The members of the Board of Directors can be found on Aegon’s website under the section ‘About, Governance, Board’.

The Board, as a whole, should have:

| ● |

An international composition, which does justice to the geographical spread of the Group’s activities; |

| ● |

Experience with, and understanding of, the administrative procedures and internal control systems in a large, international organization; |

| ● |

An affinity with, and knowledge of, the insurance industry, its customers, its products and services, the financial services market, and the Group’s businesses and strategy; |

| ● |

Knowledge and experience in (digital) marketing and distribution, and the application of information technology; |

| ● |

Expertise and experience in digital transformation; |

| ● |

Experience in the business world, both nationally and internationally; |

| ● |

An understanding of the main characteristics of the form of government and the social aspects of, as well as developments in, the countries in which the Group is active; |

| ● |

A financial expert, and more in general, financial, accounting and business economics’ expertise and the ability to judge issues in the areas of solvency, actuarial, currencies, investment and acquisition projects, and risk management, including the management of cybersecurity risk; |

| ● |

An understanding of employment relationships, human resources, and social developments; |

| ● |

An understanding of public policy, regulatory, compliance and legal matters, and corporate governance; |

| ● |

Insight into, and experience with, sustainability or Environmental, Social and Governance (ESG) aspects; and |

| ● |

Experience and knowledge in the area of executive remuneration. |

Risk Management

The Aegon Group Chief Risk Officer (CRO) is the function holder for risk management. The Aegon Group CRO is also member of the Executive Committee and of high-level Risk Committees. For more information about the risk management system and its functions, please refer to section B.3 Risk management Solvency self-assessment.

Compliance

The Global Head of Compliance is the function holder for compliance. For more details about the Compliance function reference is made to section B.4.1 Internal control system.

Internal Audit

The Global Head of Internal Audit is the function holder for Internal Audit. In line with the requirements, Internal Audit is objective and independent from the operational functions, reporting directly to the CEO and the Audit Committee Board of Directors. For more details about the Internal Audit function refer to section B.5 Internal Audit Function.

Actuarial Function

The Actuarial Function Holder is the Global Chief Actuary & Head of Underwriting Risk Management and is part of the second line at Aegon Group level. For more details about the Actuarial Function please refer to section B.6 Actuarial Function.

| 18 | Aegon Financial Condition Report 2025 |

Governance structure Risk management and Solvency self-assessment

The key functions stated above have the necessary resources to carry out their tasks. Resourcing of staff and other means required to execute control is documented as part of the Board Regulations and Charters agreed with the Board of Directors of Aegon Ltd. Changes to the resources require approval from the control function. The necessary operational independence of the control functions is also documented as part of the Board Regulations and Charters agreed with the Board of Directors. Issues can be brought forward to the Board of Directors for resolution.

B.3 Risk management and Solvency self-assessment

B.3.1 A description of the insurance Group’s risk management process and procedures to effectively identify, measure, manage and report on risk exposures

The Risk Management Function is defined in accordance with rule 8 of the Bermuda Insurance (Group Supervision) Rules 2011.

Risk management system

As an insurance group, Aegon manages risk for the benefit of its customers and other stakeholders. The company is exposed to a range of financial, underwriting, and operational risks. Aegon’s risk management and internal control systems are designed to ensure that these risks are managed effectively and efficiently in a way that is aligned with the company’s strategy.

For Aegon, risk management involves:

| ● |

Understanding risks that the company faces; |

| ● |

Maintaining a group-wide framework through which the risk-return trade-off associated with these risks can be assessed; |

| ● |

Maintaining risk tolerances and supporting policies to limit exposure to a particular risk or combination of risks; and |

| ● |

Monitoring risk exposures and actively maintaining oversight of the Company’s overall risk and solvency positions. |

This section describes Aegon’s risk management framework.

Enterprise Risk Management (ERM) framework

The formulation of the risk strategy starts with the principle that taking a risk should be based on serving a customer’s needs. The competence to manage the risk is assessed and Aegon’s risk preferences are formulated, considering Aegon’s risk capacity. The process results in a targeted risk profile, reflecting the risks Aegon wants to assume and the risks Aegon would like to avoid or mitigate.

Aegon’s risk appetite statement and risk tolerances are established to assist management in carrying out Aegon’s strategy within the boundaries of the resources available to Aegon. Aegon’s risk appetite statement is to:

“Fulfill our promises towards our customers and other stakeholders by delivering sustainable long-term growth through strong resilience in solvency and liquidity, implementing robust risk management practices that align with our ethical standards and regulatory requirements.”

Following from the risk appetite statement, risk tolerances are defined based on the following:

| ● |

Aegon should maintain adequate financial resources across the Group, both on Regulatory Capital and IFRS bases under adverse stress scenarios; |

| ● |

The Group should maintain sufficient resources on a market-informed basis to be able to pay policyholders and other contractual obligations under adverse stress scenarios; |

| ● |

Aegon acts as a responsible business with effective controls, which acknowledges an acceptable level of operational risk and stresses a low tolerance for (lack of) actions that could lead to material adverse risk events that result in breaking promises to or not meeting reasonable expectations of customers, legal and regulatory breaches, reputational damage, financial detriment or financial misstatement. |

The tolerances are further developed into measures, thresholds, and indicators that must be met to remain within the tolerances.

| 19 | Aegon Financial Condition Report 2025 |

|

|

||

| Governance structure Risk management and Solvency self-assessment | ||

Risk universe

Aegon’s risk universe is structured to reflect the type of risks to which the company is exposed. The identified risk categories are financial risk, underwriting risk, and operational risk. Specific risk types are identified within these risk categories. These internal or external risks may affect the company’s operations, earnings, share price, value of its investments, or the sale of products and services.

In the context of Aegon’s risk strategy, a risk appetite is set for the three identified risk categories (see table below).

| Risk category | Description | Appetite | ||

| Underwriting |

The risk of incurring losses when actual experience deviates from Aegon’s best estimate assumptions on mortality, longevity, morbidity, policyholder behavior, and property and casualty claims and expenses used to price products and establish technical provisions. | Medium to high - Underwriting risk is Aegon’s core business and meets customer needs. | ||

| Financial |

The risk of incurring financial losses due to movements in financial markets and the market value of balance sheet items. The elements of financial risk include credit risk, inflation risk, investment risk, interest rate risk, and currency risk. | Low to medium - Accepted where it meets customer needs and the risk-return profile is acceptable. | ||

| Operational |

The risk of losses resulting from inadequate or failed internal processes and controls, people and systems, or from external events, such as processing errors, legal and compliance issues, natural or man-made disasters, and cybercrime. | Low - Accepted as a necessary condition of conducting business, but mitigated as much as possible in an economically efficient manner. | ||

Risk identification and risk assessment

Aegon has identified a risk universe that captures all known material risks to which the company is exposed. To assess all risks, Aegon maintains a documented, consistent methodology for measuring risks. The risk metrics are embedded in Aegon’s key reports and are used for decision-making.

Risk response

Aegon distinguishes the following risk responses, which are particularly relevant where risks are out of tolerance:

| ● |

Risk acceptance: The risk is accepted by management; |

| ● |

Risk control: The risk is reduced by reducing the exposure, by improving processes and existing controls or by introducing new controls; |

| ● |

Risk transfer: The risk is reduced by insuring the company against the risk or by outsourcing activities to third parties; or |

| ● |

Risk avoidance: Activities that are the source of the risk are terminated. |

Risk monitoring and reporting

Risks are monitored regularly and reported internally on at least a quarterly basis. The impact of key financial, underwriting, and operational risk drivers on earnings and capital is shown in the quarterly risk dashboards for the various risk types, both separately and on an aggregate basis.

Risk exposures are compared with the measures and indicators as defined by Aegon’s risk appetite framework. Reporting also includes compliance and incident reporting. Finally, the main risks derived from Aegon’s strategy and day-to-day business are discussed, as well as forward-looking points for attention. If necessary, mitigating actions are taken and documented.

Risk control

A system of effective controls is required to mitigate the risks identified. In Aegon’s ERM framework, risk control includes risk governance, risk policies, an internal control framework, model validation, risk framework embedding, risk culture, and compliance.

Change risk management

The ERM framework, including the operational risk universe, applies to all change initiatives and special projects across Aegon. The risk function provides oversight to ensure that change initiatives adhere to the principles of the risk framework and to verify that the control framework during and after the change continues to operate in line with company requirements. For example, as Aegon moves its head office and legal seat to the United States, Risk will contribute to project oversight and provide input through regular risk reporting and risk opinions, similar to its role when Aegon moved its legal seat to Bermuda.

| 20 | Aegon Financial Condition Report 2025 |

Governance structure Risk management and Solvency self-assessment

B.3.2 A description of how the risk management and Solvency self-assessment system are implemented and integrated into

the insurance Group’s operations; including strategic planning and organizational and

decision-making process

Risk governance framework

Aegon’s risk management framework is represented across all levels of the organization, designed to encourage a coherent and integrated approach to risk management throughout the company. Similarly, Aegon offers a comprehensive range of group-wide risk policies that specify operating guidelines and limits. These policies include legal, regulatory, and internally set requirements and are designed to keep risk exposures to a manageable level. Any breach of policy limits or warning levels triggers remedial action or heightened monitoring. Further risk policies may be developed at a local level to cover situations specific to particular business units.

Aegon’s risk management governance structure has four layers:

| ● |

The Board of Directors (Board) and its Risk Committee; |

| ● |

The CEO and the Executive Committee; |

| ● |

The Group Risk & Capital Committee (GRCC) and its sub-committees; |

| ● |

The local Risk & Capital Committees. |

The Risk Committee reports to the Board on topics related to the ERM framework and the internal control system. This includes:

| ● |

Risk strategy, risk tolerance, and risk governance; |

| ● |

Product development and pricing; |

| ● |

Risk assessment; |

| ● |

Risk responses and internal control effectiveness; |

| ● |

Risk monitoring; and Risk reporting. |

The CEO and the Group’s Chief Risk Officer (CRO) are responsible for informing the Board of any risk that directly threatens the company’s solvency, liquidity, or operations. The CEO has overall responsibility for managing risk. The CEO adopts the risk strategy, risk governance, risk tolerance, and material changes in risk methodology and risk policies. The Group’s CRO has a standing invitation to attend the CEO meeting and has a direct reporting line to the Board to discuss ERM and related matters. The CRO is also a member of the Executive Committee.

The Executive Committee oversees a broad range of strategic and operational issues. While the CEO is Aegon’s statutory Executive Director, the Executive Committee provides vital support and expertise in safeguarding Aegon’s strategic goals. The Executive Committee discusses and sponsors ERM, in particular the risk strategy, risk governance, risk tolerance, and the introduction of new risk policies.

The CEO and Executive Committee are supported by the GRCC. The GRCC is Aegon’s most senior risk committee. It is responsible for managing Aegon’s balance sheet at the global level and is in charge of risk oversight, risk monitoring, and risk management-related decisions on behalf of the CEO and in line with its charter. The GRCC ensures risk-taking is within Aegon’s risk tolerances, that the capital position is adequate to support financial strength and regulatory requirements, and that capital is properly allocated. The GRCC informs the CEO about any identified breaches of overall tolerance levels and threats to the company’s solvency, liquidity, or operations.

The GRCC has three sub-committees: the ERM framework, Accounting and Actuarial Committee (ERMAAC), the Non-Financial Risk Committee (NFRC) and the Model Validation Committee (MVC).

The purpose of the ERMAAC is to assist the GRCC, CEO, and Executive Committee with the setting and maintenance of the financial risk framework across all group-level balance sheet bases, including policies, standards, guidelines, methodologies, and assumptions.

The purpose of the NFRC is to assist the GRCC, CEO and Executive Committee with non-financial risk framework setting and maintenance, including policies, standards, guidelines, and methodologies, and to act as a formal discussion and information- exchange platform on matters concerning non-financial risk management.

The MVC is responsible for approving all model validation reports across Aegon. This independent committee reports to the GRCC and the CEO to provide information on model integrity and recommendations on how to strengthen these models further.

| 21 | Aegon Financial Condition Report 2025 |

|

|

||

| Governance structure Risk management and Solvency self-assessment | ||

Aegon’s business units have a Risk, or Risk and Capital Committee, and an Audit Committee. While naming and organizational set-up can differ, the responsibilities and prerogatives of the committees are aligned with those of the company-level committees and further elaborated in their respective charters, which are tailored to local circumstances.

In addition to the four layers described above, Aegon has an established group-wide Risk function. It is the mission of the Risk function to ensure the continuity of the company by safeguarding the value of existing business, protecting Aegon’s balance sheet and reputation, and supporting the creation of sustainable value for all stakeholders.

In general, the objective of the Risk function is to support the CEO, Executive Committee, Board, and business unit boards in ensuring that the company reviews, assesses, understands, and manages its risk profile. Through oversight, the Risk function ensures the company-wide risk profile is managed in line with Aegon’s risk tolerances, and stakeholder expectations are managed under both normal business conditions and adverse conditions caused by unforeseen negative events.

The following roles are important to realize the objective of the Risk function:

| ● |

Advising on risk-related matters including risk tolerance, risk governance, risk methodology, and risk policies; |

| ● |

Supporting and facilitating the development, incorporation, maintenance, and embedding of the ERM framework and sound practices; and |

| ● |

Monitoring and challenging the implementation and effectiveness of ERM practices. |

B.3.3 A description of the relationship between the Solvency self-assessment, Solvency needs, and capital and risk management systems of the insurance Group

Aegon’s Group Solvency Self-Assessment (GSSA) process has a primary purpose of providing a holistic, inter-connected view of our business strategy, the risks to which the business is exposed and our capital levels. It assesses the financial security of the business given the risks we run.

The Aegon GSSA process includes the following elements:

| ● |

Budget/MTP: is a group-wide strategy and Budget setting process which forms the basis of the forward looking assessment of the business strategy, associated risks and the capital position. In addition to a best estimate ‘base’ scenario, the exercise also projects adverse scenarios to test the robustness of its strategic planning. The scenarios are analyzed using the risk tolerance statements and the Capital Management policy. |

| ● |

Risk Reporting Dashboard: Aegon produces a comprehensive set of risk reports to measure, monitor and manage the risks in the business. The reports show the impact of key market or financial risks and underwriting risk drivers on earnings and capital generation for the various risk types. Furthermore, it contains analyses for non-financial risk and the impact of operational risk events at the regional and aggregated levels. An important part of the risk reporting process is compliance testing. Risk exposures for various risk types and tolerance measures are compared to the indicators / target levels as defined by Aegon’s Global Risk Appetite Framework. Group Risk produces a risk dashboard on at least on a quarterly basis. However, sections of the report can be produced on a more frequent or ad hoc basis. |

| ● |

Liquidity Risk Management Plan: Risk Tolerance Statement for liquidity requires that the Group and each legal entity must have sufficient liquidity to meet cash demands after an extreme event. The Risk Tolerance Statement is further developed into a set of specific limits, policy requirements and other operating standards, methodologies and procedures that must be complied with to maintain within tolerance. |

| ● |

Aegon Recovery Plan: serves as a useful management tool for Aegon to manage through crisis situations. Among others, the recovery measures are in place to help Aegon recover from a crisis situation. It demonstrates Aegon’s ability to recover from company-specific and market-wide stresses, bringing both capital and liquidity position under pressure. It contains an up-to-date list of our contingent recovery measures which are available to improve capital and liquidity during or after a crisis. |

| ● |

Group Capital Update: it is a monthly process whereby operating units provide current quarter and year-end forecasts for their solvency position. Operating units identify the key threats and initiatives as well as market developments expected to impact their solvency position over a short term time horizon (next quarter end and year end). Next to the solvency positions of the Group and our operating units, the Cash Capital at Holding balance and the operating capital generation are forecasted. |

In addition to running our business with a GSSA mind-set, a GSSA report is produced annually and required for regulatory purposes. The GSSA report includes at least an assessment of the current and forward-looking risk profile and capital position in quantitative as well as qualitative terms, as well as a summary of how risk management is embedded within the business strategy and medium-term plan, providing a forward looking perspective to achieve our targets and remain solvent given our risk profile.

| 22 | Aegon Financial Condition Report 2025 |

Governance structure Internal controls

B.3.4 A description of the Solvency self-assessment approval process including the level of oversight and independent verification by the parent board and senior executives