In Q2 FY26, Cirrus Logic delivered record September quarter revenue of $561.0 million, towards the top end of our guidance range, and GAAP and non-GAAP earnings per share of $2.48 and $2.83, respectively. During the quarter, we were delighted to see multiple smartphone customers introduce their latest-generation devices featuring our audio and high-performance mixed-signal (HPMS) components. Outside of smartphones, we continued to execute on our plan to grow market share in the PC market. Progress in this space included securing our first mainstream consumer laptop design, expanding our collaboration with leading PC platform vendors, and developing new products with superior voice and audio capture capabilities. Additionally, we continue to focus on our general market business, where products tend to enjoy long lifespans and gross margins that are well above our corporate average. During the quarter, we gained design momentum with customers on all 14 variants of our latest-generation ADCs, DACs, and ultra-high-performance audio codec. We also received positive initial feedback on our family of analog front-end components targeting imaging applications and saw increased engagement on our latest timing product family. Looking forward, we are optimistic about the opportunities ahead of us as we continue to leverage our mixed-signal design and signal processing expertise to diversify our product portfolio and expand our addressable market.

Figure A: Cirrus Logic Q2 FY26

Q2 FY26

GAAP

Adj.

Non-GAAP*

Revenue

$561.0

$561.0

Gross Profit

$294.4

$0.3

$294.7

Gross Margin

52.5%

52.5%

Operating Expense

$149.6

($21.9)

$127.7

Operating Income

$144.8

$22.2

$167.0

Operating Profit

25.8%

29.8%

Interest Income

$8.7

$8.7

Other Expense

$(0.1)

$(0.1)

Income Tax Expense

$21.8

$3.9

$25.7

Net Income

$131.6

$18.4

$150.0

Diluted EPS

$2.48

$0.35

$2.83

*Complete GAAP to Non-GAAP reconciliations available on page 11

Numbers may not sum due to rounding

$ millions, except EPS

Revenue and Gross Margin

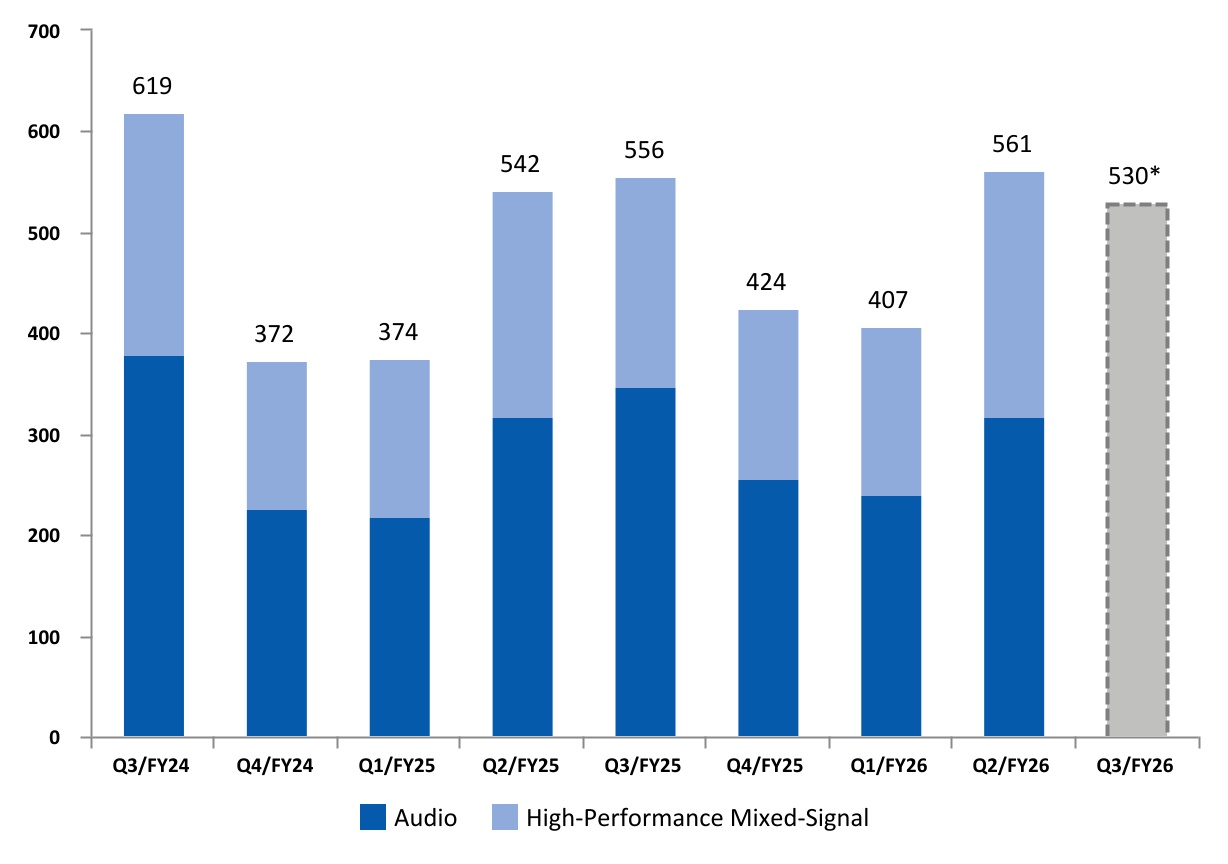

Revenue for the September quarter was $561.0 million, up thirty-eight percent quarter over quarter and up four percent year over year. The increase in revenue on a sequential basis reflects higher smartphone unit volumes. The year-over-year increase was primarily driven by higher smartphone unit volumes and sales associated with our latest-generation products. This was partially offset by pricing reductions. In the December quarter, we expect revenue to range from $500 million to $560 million, down six percent sequentially and approximately down five percent year over year at the midpoint.

In Q2 FY26, revenue derived from our audio and high-performance mixed-signal product lines represented 57 percent and 43 percent of total revenue, respectively. One customer contributed approximately 90 percent of total revenue in Q2 FY26. Our relationship with our largest customer remains

Q2 FY26 Letter to Shareholders

2

outstanding, with continued strong design activity across a wide range of products. While we understand there is intense interest in this customer, in accordance with our policy, we do not discuss specifics about this business.

GAAP gross margin in the September quarter was 52.5 percent, compared to 52.6 percent in Q1 FY26 and 52.2 percent in Q2 FY25. Non-GAAP gross margin in the September quarter was 52.5 percent, compared to 52.6 percent in Q1 FY26 and 52.2 percent in Q2 FY25. On a year-over-year basis, the increase in gross margin was largely due to a more favorable product mix. This was partially offset by higher inventory reserves. In the December quarter, we expect gross margin to range from 51 percent to 53 percent.

Operating Profit, Tax, and EPS

Operating profit for Q2 FY26 was 25.8 percent on a GAAP basis and 29.8 percent on a non-GAAP basis. GAAP operating expense was $149.6 million and included $20.2 million in stock-based compensation and $1.6 million in amortization of acquisition intangibles. On a sequential basis, GAAP operating expense increased by $8.0 million, primarily driven by higher variable compensation, product development costs that were largely due to tape outs, and facilities-related costs. This was partially offset by a reduction in employee-related expenses. On a year-over-year basis, GAAP operating expense decreased by $1.1 million largely due to lower stock-based compensation and product development costs. This was offset by

Q2 FY26 Letter to Shareholders

3

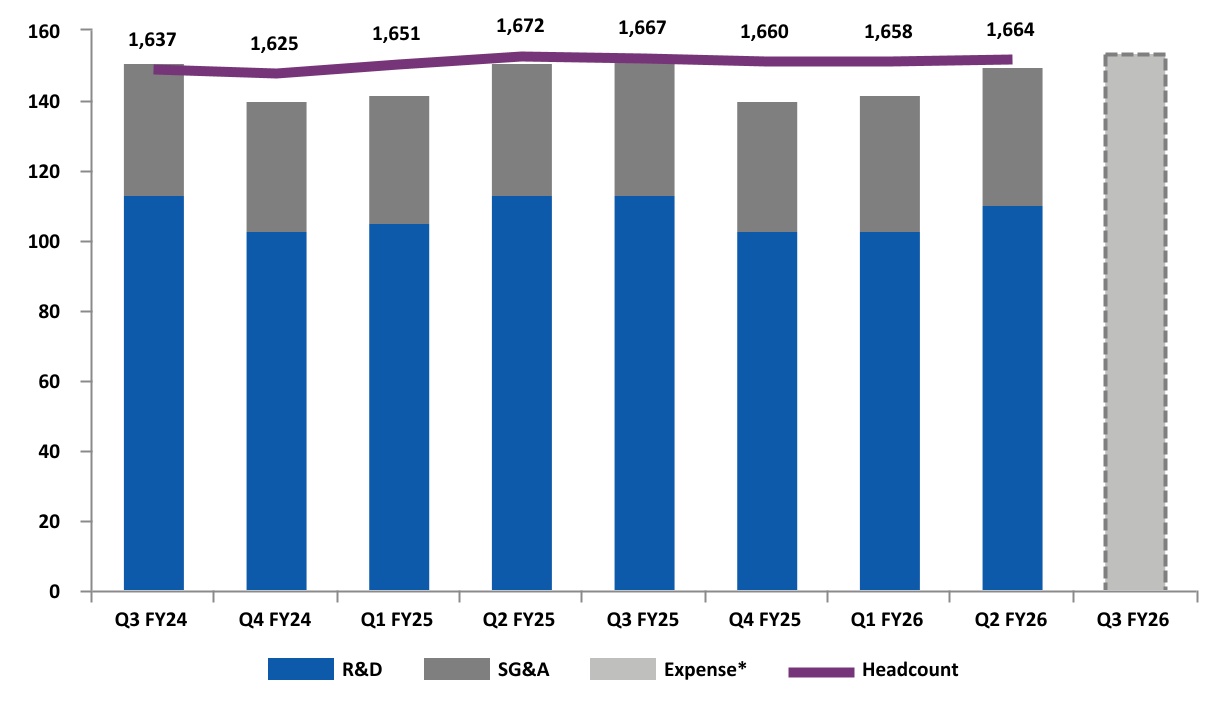

higher employee-related expenses, mostly due to annual salary increases. Non-GAAP operating expense for the quarter was $127.7 million, up $8.2 million sequentially and up $0.9 million year over year. The company’s total headcount exiting Q2 was 1,664.

Combined GAAP R&D and SG&A expenses for Q3 FY26 are expected to range from $151 million to $157 million, including approximately $21 million in stock-based compensation expense and $2 million in amortization of acquisition intangibles, resulting in a non-GAAP operating expense range between $128 million and $134 million.

Figure C: GAAP R&D and SG&A Expenses ($M)/Headcount Q3 FY24 to Q3 FY26

*Reflects midpoint of combined R&D and SG&A guidance as of November 4, 2025

For the September quarter, GAAP tax expense was $21.8 million on GAAP pre-tax income of $153.4 million, resulting in an effective tax rate of 14.2 percent. Non-GAAP tax expense for the quarter was $25.7 million on non-GAAP pre-tax income of $175.6 million, resulting in a non-GAAP effective tax rate of 14.6 percent. Both the GAAP and non-GAAP effective tax rates include the year-to-date beneficial impact of the One Big Beautiful Bill Act (the "OBBBA"), which was signed into law on July 4, 2025 and reinstated the immediate tax deductibility of U.S. R&D expenditures, among other provisions. We estimate that our FY26 non-GAAP effective tax rate will range from approximately 16 percent to 18 percent.

GAAP earnings per share for the September quarter was $2.48, compared to earnings per share of $1.14 in the prior quarter and $1.83 in Q2 FY25. Non-GAAP earnings per share for the September quarter was $2.83, versus $1.51 in Q1 FY26 and $2.25 in Q2 FY25.

Q2 FY26 Letter to Shareholders

4

Balance Sheet

Our cash and investment balance at the end of Q2 FY26 was $896.0 million, up from $847.8 million in the prior quarter and $706.6 million in Q2 FY25. . Cash flow from operations for the September quarter was $92.2 million. During the quarter, we repurchased 361,708 shares at an average price of $110.55, returning $40.0 million of cash to shareholders in the form of buybacks. At the end of Q2 FY26, the company had $414.1 million remaining in its share repurchase authorization. Over the long term, we expect strong cash flow generation, and we will continue to evaluate potential uses of this cash, including investing in the business to pursue organic growth opportunities, M&A, and returning capital to shareholders through share repurchases.

Q2 FY26 inventory was $236.4 million, down from $279.0 million in Q1 FY26. In Q3 FY26, we expect inventory to be slightly down sequentially.

Company Strategy

We remain committed to our three-pronged strategy for growing our business: first, maintaining our leadership position in smartphone audio; second, increasing HPMS content in smartphones; and third, leveraging our strength in audio and HPMS to expand into additional applications and markets with both existing and new components.

Smartphones

In smartphones, the company maintained its position as a leading supplier of audio solutions, as we experienced strong demand for our latest-generation custom boosted amplifier and first 22-nanometer smart codec. These components feature an innovative new architecture that delivers significant power and efficiency improvements while also saving valuable board space and enabling system design flexibility. As a reminder to our shareholders, while many of our products ship into consumer end devices, much of our custom silicon business offers greater returns over a significantly longer period than is typical of consumer products. For example, our latest-generation audio components superseded a codec and amplifiers that had been shipping in high-volume flagship phones for five and six years, respectively. We regard this as an important strength of our business, providing solid long-term visibility, sustained revenue contribution, and the ability to leverage our R&D resources in new areas that can drive further innovation and growth. This past quarter, a leading Android OEM also introduced its latest flagship smartphone featuring two Cirrus Logic boosted amplifiers and a haptic driver. While the majority of our general market R&D investments are focused on developing products for new markets, we continue to engage with customers on next-generation flagship smartphones and expect additional designs from various customers to come to market in the future.

Beyond audio, we continue to pursue opportunities to diversify our revenue and grow our smartphone content with HPMS solutions. Customer engagement with our camera controllers remains strong, and we were delighted to see the technology continue to be featured as an important differentiator in the new generation of devices. We believe there is an exciting path for innovation in camera controllers, and we are engaged on next-generation components that offer further feature and performance enhancements. Additionally, we continue to invest in product development for power and battery technologies, which we view as a longer-term growth driver within our HPMS product line. Today, we have a number of R&D programs underway related to battery performance, health, and longevity. Our teams are focused on

Q2 FY26 Letter to Shareholders

5

maximizing power efficiency and integrating more digital processing and control alongside analog circuits. We believe our work in this area will contribute to product diversification and broaden our footprint in the years ahead.

New Applications and Markets

Outside of smartphones, we are committed to leveraging our intellectual property and engineering capabilities to expand into new applications and markets. Our most immediate opportunity is in the PC market, where we are executing on our plan to meaningfully grow share. During the quarter, design activity across our laptop portfolio was strong, and we expect a range of consumer and commercial laptops featuring our components to come to market over the next year as the adoption of SoundWire Device Class Audio accelerates. Demand for our PC components has been driven by increased customer interest in high-quality audio and the shift toward thinner, lighter, and more power-efficient designs. After our initial success in high-end laptop programs, we are now also strategically focused on expanding into mainstream designs to target higher-volume opportunities. This enables us to capture a greater share of our serviceable addressable market and unlock additional long-term revenue opportunities. Building on our initial wins with mainstream commercial laptops earlier this year, we are delighted to have recently secured our first mainstream consumer laptop design, which is expected to ship during the next calendar year. These strategically important wins validate our capabilities and position the company well to secure more mainstream devices in the future. To enable faster time to market for OEMs, we are expanding our collaboration with leading PC platform vendors with the introduction of new audio and HPMS solutions that address a larger portion of our PC SAM in both commercial and consumer products. Further, as voice increasingly becomes a natural and preferred way to interact with AI-enabled PCs, we are developing new products to capitalize on this opportunity. These products also deliver superior voice and audio capture capabilities, including noise cleanup and voice detection. Additionally, they support ultra-low power modes, which are critical to enable features such as voice wake for AI applications while the device is in standby. We expect the first product with this technology to sample with customers during the December quarter. Overall, we are encouraged by the momentum we are building in the PC market and believe there are significant opportunities for Cirrus Logic to drive long-term revenue growth in these market segments.

While PCs represent a significant growth opportunity outside of smartphones, we also have strong interest in our general market products, which span a large number of customers across the professional audio, automotive, industrial, and imaging end markets. Applications in these areas tend to have long lifespans and gross margins that are well above our corporate average. We are targeting a growing share of these highly profitable market segments by efficiently leveraging our low-power, high-performance intellectual property to develop differentiated components for a wide range of applications and tiers. During the quarter, we gained design momentum with prosumer and automotive customers on all 14 variants of our latest-generation ADCs, DACs, and ultra-high-performance audio codec, and expect new end products utilizing these components to come to market over the next 12 months. Additionally, we are seeing increased engagement from automotive and professional audio customers on our latest timing product family, which began shipping last quarter. The company is also sampling a family of high-performance analog front-end components targeting imaging applications, and initial feedback has been positive. We are extremely pleased with our progress to date in these areas. Looking forward, we plan to further build out this portfolio of products and leverage our mixed-signal design and advanced low-power signal processing expertise to drive growth opportunities in new applications and markets.

Q2 FY26 Letter to Shareholders

6

Summary and Guidance

For the December quarter, we expect the following results:

•Revenue to range between $500 million and $560 million;

•GAAP gross margin to be between 51 percent and 53 percent; and

•Combined GAAP R&D and SG&A expenses to range between $151 million and $157 million, including approximately $21 million in stock-based compensation expense and $2 million in amortization of acquisition intangibles, resulting in a non-GAAP operating expense range between $128 million and $134 million.

In conclusion, we are proud to have delivered strong financial results for Q2 FY26 while also continuing to execute on our strategy. During the quarter, new flagship smartphones with our components came to market, we continued to build momentum with our PC business, and we had strong customer engagement across our portfolio of general market components. With an extensive intellectual property portfolio and a solid product roadmap, we believe that we are well-positioned to capitalize on the opportunities ahead of us to drive long-term shareholder value.

Sincerely,

John Forsyth

President &

Chief Executive Officer

Jeff Woolard

Chief Financial Officer

Conference Call Q&A Session

Cirrus Logic will host a live Q&A session at 5 p.m. ET today to answer questions related to its financial results and business outlook. Participants may listen to the conference call on the Cirrus Logic website.

A replay of the webcast can be accessed on the Cirrus Logic website approximately two hours following its completion or by calling (609) 800-9909 or toll-free at (800) 770-2030 (Access Code: 95424).

Use of Non-GAAP Financial Information

To supplement Cirrus Logic's financial statements presented on a GAAP basis, Cirrus has provided non-GAAP financial information, including non-GAAP net income, diluted earnings per share, operating income and profit, operating expenses, gross margin and profit, tax expense, tax expense impact on earnings per share, effective tax rate, free cash flow, and free cash flow margin. A reconciliation of the adjustments to

Q2 FY26 Letter to Shareholders

7

GAAP results is included in the tables below. We are also providing guidance on our expected non-GAAP expected effective tax rate. We are not able to provide guidance on our GAAP effective tax rate or a related reconciliation without unreasonable efforts since our future GAAP effective tax rate depends on our future stock price and related stock-based compensation information that is not currently available.

Non-GAAP financial information is not meant as a substitute for GAAP results but is included because management believes such information is useful to our investors for informational and comparative purposes. In addition, certain non-GAAP financial information is used internally by management to evaluate and manage the company. The non-GAAP financial information used by Cirrus Logic may differ from that used by other companies. These non-GAAP measures should be considered in addition to, and not as a substitute for, the results prepared in accordance with GAAP.

Safe Harbor Statement

Except for historical information contained herein, the matters set forth in this shareholder letter contain forward-looking statements, including statements about our ability to leverage our mixed-signal design and signal processing expertise to diversify our product portfolio and expand our addressable market; our ability to maintain our leadership position in smartphone audio; our ability to increase HPMS content in smartphones; our ability to leverage our strength in audio and HPMS to expand into additional applications and markets with both new and existing components; our expectation that our latest-generation custom boosted amplifier and first 22-nanometer smart codec will ship for multiple generations and provide the company an opportunity for sustained revenue contribution; our ability to deploy R&D resources on new projects that can drive further innovation and growth; our expectation that next-generation flagship smartphones will come to market in the future; our expectation that power and battery technologies will drive longer-term growth, contribute to product diversification, and broaden our footprint in the years ahead; our ability to leverage our intellectual property and engineering capabilities to expand into new applications and markets; our ability to expand into mainstream designs to capture a greater share of our serviceable addressable market and unlock additional long-term revenue opportunities; our expectation that new end products with our components will come to market in the next 12 months; our ability to drive long-term revenue growth and grow market share in the PC market; our expectation that the first product designed to capitalize on opportunities in AI-enabled PCs will sample with customers during the December quarter; our belief there is an exciting path for innovation in camera controllers; our expectation that new end products utilizing our general market components will come to market over the next 12 months; our ability to capitalize on the opportunities ahead of us to drive long-term shareholder value; our expectation that inventory will be down slightly sequentially; our non-GAAP effective tax rate for the full fiscal year 2026; and our forecasts for the third quarter of fiscal year 2026 revenue, gross margin, combined research and development and selling, general and administrative expense levels, stock-based compensation expense, and amortization of acquisition intangibles. In some cases, forward-looking statements are identified by words such as “emerge,” “expect,” “anticipate,” “foresee,” “target,” “project,” “believe,” “goals,” “opportunity,” “estimates,” “intend,” “will,” and variations of these types of words and similar expressions. In addition, any statements that refer to our plans, expectations, strategies, or other characterizations of future events or circumstances are forward-looking statements. These forward-looking statements are based on our current expectations, estimates, and assumptions and are subject to certain risks and uncertainties that could cause actual results to differ materially, and readers should not place undue reliance on such statements. These risks and uncertainties include, but are not limited to, the following: the level and timing of orders and shipments during the third quarter of fiscal year 2026, customer cancellations of orders, or the failure to place orders consistent with forecasts; changes in government trade policies, including the imposition of tariffs and export restrictions; global economic conditions and uncertainty;

Q2 FY26 Letter to Shareholders

8

and the risk factors listed in our Form 10-K for the year ended March 29, 2025 and in our other filings with the Securities and Exchange Commission, which are available at www.sec.gov. The foregoing information concerning our business outlook represents our outlook as of the date of this news release, and we expressly disclaim any obligation to update or revise any forward-looking statements, whether as a result of new developments or otherwise.

Cirrus Logic, Cirrus and the Cirrus Logic logo are registered trademarks of Cirrus Logic, Inc. All other company or product names noted herein may be trademarks of their respective holders.

Q2 FY26 Letter to Shareholders

9

Summary of Financial Data Below:

CONSOLIDATED CONDENSED STATEMENT OF OPERATIONS

(in thousands, except per share data; unaudited)

Three Months Ended

Six Months Ended

Sep. 27, 2025

Jun. 28, 2025

Sep. 28, 2024

Sep. 27, 2025

Sep. 28, 2024

Q2'26

Q1'26

Q2'25

Q2'26

Q2'25

Audio

$

318,214

$

240,043

$

316,588

$

558,257

$

535,558

High-Performance Mixed-Signal

242,746

167,229

225,269

409,975

380,325

Net sales

560,960

407,272

541,857

968,232

915,883

Cost of sales

266,586

193,242

259,267

459,828

444,368

Gross profit

294,374

214,030

282,590

508,404

471,515

Gross margin

52.5

%

52.6

%

52.2

%

52.5

%

51.5

%

Research and development

110,021

102,892

112,925

212,913

218,288

Selling, general and administrative

39,589

38,744

37,813

78,333

74,583

Total operating expenses

149,610

141,636

150,738

291,246

292,871

Income from operations

144,764

72,394

131,852

217,158

178,644

Interest income

8,695

8,622

8,134

17,317

16,336

Other income (expense)

(63)

(388)

19

(451)

1,628

Income before income taxes

153,396

80,628

140,005

234,024

196,608

Provision for income taxes

21,800

19,931

37,865

41,731

52,373

Net income

$

131,596

$

60,697

$

102,140

$

192,293

$

144,235

Basic earnings per share

$

2.57

$

1.17

$

1.92

$

3.74

$

2.70

Diluted earnings per share:

$

2.48

$

1.14

$

1.83

$

3.61

$

2.59

Weighted average number of shares:

Basic

51,175

51,727

53,275

51,451

53,354

Diluted

53,054

53,319

55,800

53,195

55,753

Prepared in accordance with Generally Accepted Accounting Principles

Q2 FY26 Letter to Shareholders

10

RECONCILIATION BETWEEN GAAP AND NON-GAAP FINANCIAL INFORMATION CONTINUED

(in thousands, except per share data; unaudited)

(not prepared in accordance with GAAP)

Non-GAAP financial information is not meant as financial information is not meant as a substitute for GAAP results, but is included because management believes such information is useful to our investors for informational and comparative purposes. In addition, certain non-GAAP financial information is used internally by management to evaluate and manage the company. As a note, the non-GAAP financial information used by Cirrus Logic may differ from that used by other companies. These non-GAAP measures should be considered in addition to, and not as a substitute for, the results prepared in accordance with GAAP.

Three Months Ended

Six Months Ended

Sep. 27, 2025

Jun. 28, 2025

Sep. 28, 2024

Sep. 27, 2025

Sep. 28, 2024

Net Income Reconciliation

Q2'26

Q1'26

Q2'25

Q2'26

Q2'25

GAAP Net Income

$

131,596

$

60,697

$

102,140

$

192,293

$

144,235

Amortization of acquisition intangibles

1,648

1,647

1,864

3,295

3,836

Stock-based compensation expense

20,597

20,809

22,447

41,406

43,832

Lease impairment

—

—

—

—

1,019

Adjustment to income taxes

(3,861)

(2,839)

(1,162)

(6,700)

(5,267)

Non-GAAP Net Income

$

149,980

$

80,314

$

125,289

$

230,294

$

187,655

Earnings Per Share Reconciliation

GAAP Diluted earnings per share

$

2.48

$

1.14

$

1.83

$

3.61

$

2.59

Effect of Amortization of acquisition intangibles

0.03

0.03

0.04

0.06

0.07

Effect of Stock-based compensation expense

0.39

0.39

0.40

0.78

0.79

Effect of Lease impairment

—

—

—

—

0.02

Effect of Adjustment to income taxes

(0.07)

(0.05)

(0.02)

(0.12)

(0.10)

Non-GAAP Diluted earnings per share

$

2.83

$

1.51

$

2.25

$

4.33

$

3.37

Operating Income Reconciliation

GAAP Operating Income

$

144,764

$

72,394

$

131,852

$

217,158

$

178,644

GAAP Operating Profit

25.8

%

17.8

%

24.3

%

22.4

%

19.5

%

Amortization of acquisition intangibles

1,648

1,647

1,864

3,295

3,836

Stock-based compensation expense - COGS

363

300

355

663

621

Stock-based compensation expense - R&D

13,019

13,072

15,844

26,091

31,607

Stock-based compensation expense - SG&A

7,215

7,437

6,248

14,652

11,604

Lease impairment

—

—

—

—

1,019

Non-GAAP Operating Income

$

167,009

$

94,850

$

156,163

$

261,859

$

227,331

Non-GAAP Operating Profit

29.8

%

23.3

%

28.8

%

27.0

%

24.8

%

Operating Expense Reconciliation

GAAP Operating Expenses

$

149,610

$

141,636

$

150,738

$

291,246

$

292,871

Amortization of acquisition intangibles

(1,648)

(1,647)

(1,864)

(3,295)

(3,836)

Stock-based compensation expense - R&D

(13,019)

(13,072)

(15,844)

(26,091)

(31,607)

Stock-based compensation expense - SG&A

(7,215)

(7,437)

(6,248)

(14,652)

(11,604)

Lease impairment

—

—

—

—

(1,019)

Non-GAAP Operating Expenses

$

127,728

$

119,480

$

126,782

$

247,208

$

244,805

Gross Margin/Profit Reconciliation

GAAP Gross Profit

$

294,374

$

214,030

$

282,590

$

508,404

$

471,515

GAAP Gross Margin

52.5

%

52.6

%

52.2

%

52.5

%

51.5

%

Stock-based compensation expense - COGS

363

300

355

663

621

Non-GAAP Gross Profit

$

294,737

$

214,330

$

282,945

$

509,067

$

472,136

Non-GAAP Gross Margin

52.5

%

52.6

%

52.2

%

52.6

%

51.5

%

Effective Tax Rate Reconciliation

GAAP Tax Expense

$

21,800

$

19,931

$

37,865

$

41,731

$

52,373

GAAP Effective Tax Rate

14.2

%

24.7

%

27.0

%

17.8

%

26.6

%

Adjustments to income taxes

3,861

2,839

1,162

6,700

5,267

Non-GAAP Tax Expense

$

25,661

$

22,770

$

39,027

$

48,431

$

57,640

Non-GAAP Effective Tax Rate

14.6

%

22.1

%

23.8

%

17.4

%

23.5

%

Tax Impact to EPS Reconciliation

GAAP Tax Expense

$

0.41

$

0.37

$

0.68

$

0.78

$

0.94

Adjustments to income taxes

0.07

0.05

0.02

0.12

0.10

Non-GAAP Tax Expense

$

0.48

$

0.42

$

0.70

$

0.90

$

1.04

Q2 FY26 Letter to Shareholders

11

CONSOLIDATED CONDENSED BALANCE SHEET

(in thousands; unaudited)

Sep. 27, 2025

Mar. 29, 2025

Sep. 28, 2024

ASSETS

Current assets

Cash and cash equivalents

$

593,476

$

539,620

$

445,759

Marketable securities

52,424

56,160

32,499

Accounts receivable, net

355,397

216,009

324,098

Inventories

236,409

299,092

271,765

Prepaid wafers

45,056

52,560

71,740

Other current assets

84,238

76,293

79,044

Total current Assets

1,367,000

1,239,734

1,224,905

Long-term marketable securities

250,146

239,036

228,302

Right-of-use lease assets

125,315

126,688

133,316

Property and equipment, net

151,154

159,900

168,265

Intangibles, net

24,451

27,461

25,700

Goodwill

435,936

435,936

435,936

Deferred tax asset

46,511

48,150

48,619

Long-term prepaid wafers

—

15,512

37,804

Other assets

29,170

34,656

53,292

Total assets

$

2,429,683

$

2,327,073

$

2,356,139

LIABILITIES AND STOCKHOLDERS' EQUITY

Current liabilities

Accounts payable

$

79,974

$

63,162

$

91,899

Accrued salaries and benefits

52,689

52,075

51,861

Lease liability

19,481

21,811

22,800

Other accrued liabilities

58,179

58,140

62,716

Total current liabilities

210,323

195,188

229,276

Non-current lease liability

120,985

121,908

129,806

Non-current income taxes

45,357

44,040

42,683

Other long-term liabilities

10,576

16,488

26,247

Total long-term liabilities

176,918

182,436

198,736

Stockholders' equity:

Capital stock

1,903,638

1,860,281

1,819,589

Accumulated earnings

139,025

90,351

107,233

Accumulated other comprehensive (loss) income

(221)

(1,183)

1,305

Total stockholders' equity

2,042,442

1,949,449

1,928,127

Total liabilities and stockholders' equity

$

2,429,683

$

2,327,073

$

2,356,139

Prepared in accordance with Generally Accepted Accounting Principles

Q2 FY26 Letter to Shareholders

12

CONSOLIDATED CONDENSED STATEMENT OF CASH FLOWS

(in thousands; unaudited)

Three Months Ended

Sep. 27,

Sep. 28,

2025

2024

Q2'26

Q2'25

Cash flows from operating activities:

Net income

$

131,596

$

102,140

Adjustments to reconcile net income to net cash provided by operating activities:

Depreciation and amortization

12,704

12,618

Stock-based compensation expense

20,597

22,447

Deferred income taxes

7,470

4,984

Loss on retirement or write-off of long-lived assets

—

12

Other non-cash charges

68

87

Net change in operating assets and liabilities:

Accounts receivable, net

(141,312)

(134,019)

Inventories

42,575

(39,199)

Prepaid wafers

16,878

25,531

Other assets

(8,485)

(341)

Accounts payable and other accrued liabilities

29,451

27,268

Income taxes payable

(19,328)

(13,297)

Net cash provided by operating activities

92,214

8,231

Cash flows from investing activities:

Maturities and sales of available-for-sale marketable securities

39,752

835

Purchases of available-for-sale marketable securities

(43,171)

(3,577)

Purchases of property, equipment and software

(3,868)

(2,670)

Investments in technology

(642)

(70)

Net cash used in investing activities

(7,929)

(5,482)

Cash flows from financing activities:

Net proceeds from the issuance of common stock

1,568

4,859

Repurchase of stock to satisfy employee tax withholding obligations

(1,261)

(3,207)

Repurchase and retirement of common stock

(39,986)

(49,993)

Net cash used in financing activities

(39,679)

(48,341)

Net increase (decrease) in cash and cash equivalents

44,606

(45,592)

Cash and cash equivalents at beginning of period

548,870

491,351

Cash and cash equivalents at end of period

$

593,476

$

445,759

Prepared in accordance with Generally Accepted Accounting Principles

Q2 FY26 Letter to Shareholders

13

RECONCILIATION BETWEEN GAAP AND NON-GAAP FINANCIAL INFORMATION

(in thousands; unaudited)

Free cash flow, a non-GAAP financial measure, is GAAP cash flow from operations (or cash provided by operating activities) less capital expenditures. Capital expenditures include purchases of property, equipment and software as well as investments in technology, as presented within our GAAP Consolidated Condensed Statement of Cash Flows. Free cash flow margin represents free cash flow divided by revenue.

Twelve Months Ended

Three Months Ended

Sep. 27,

Sep. 27,

Jun. 28,

Mar. 29,

Dec. 28,

2025

2025

2025

2025

2024

Q2'26

Q2'26

Q1'26

Q4'25

Q3'25

Net cash provided by operating activities (GAAP)

$

557,319

$

92,214

$

116,131

$

130,386

$

218,588

Capital expenditures

(23,148)

(4,510)

(2,770)

(9,181)

(6,687)

Free Cash Flow (Non-GAAP)

$

534,171

$

87,704

$

113,361

$

121,205

$

211,901

Cash Flow from Operations as a Percentage of Revenue (GAAP)

29

%

16

%

29

%

31

%

39

%

Capital Expenditures as a Percentage of Revenue (GAAP)

1

%

1

%

1

%

2

%

1

%

Free Cash Flow Margin (Non-GAAP)

27

%

16

%

28

%

29

%

38

%

Q2 FY26 Letter to Shareholders

14

RECONCILIATION BETWEEN GAAP AND NON-GAAP FINANCIAL INFORMATION