THE MEXICO EQUITY AND INCOME FUND, INC.

Annual

Report

July 31, 2025

| |

| Revolution Monument, Mexico City. Source: CANVA. |

UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-06111

The

(Exact name of registrant as specified in charter)

615 East Michigan Street

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

Mr. Mauro Castañeda

c/o U.S. Bancorp Fund Services, LLC

615 East Michigan Street

Milwaukee,

WI 53202

(Name and address of agent for service)

(877) 785-0376

Registrant’s telephone number, including area code

Date of fiscal year end: July 31

Date

of reporting period:

Updated June 27, 2024

Item 1. Reports to Stockholders.

THE MEXICO EQUITY AND INCOME FUND, INC.

Annual

Report

July 31, 2025

| |

| Revolution Monument, Mexico City. Source: CANVA. |

THE MEXICO EQUITY AND INCOME FUND, INC.

Annual

Report

Table of Contents

The

Mexico Equity and Income Fund, Inc. (“The Fund”)

Annual Report, ending July 31, 2025

Dear Stakeholder,

Global Context

The global economy in 2025 has been characterized by moderate growth and persistent uncertainty. Global Gross Domestic Product (“GDP”) expectations remain near 3%, with the U.S. showing resilience despite slower momentum, Europe struggling with weak industrial activity, and China facing continued stress from its real estate sector and high debt levels. Inflation trends have diverged across regions: the U.S. saw progress toward its 2% target, allowing the Federal Reserve to begin modest rate cuts, while the European Central Bank remained cautious. Commodity prices, particularly oil and industrial metals, remained volatile due to supply constraints and geopolitical instability. Ongoing conflicts in Ukraine and the Middle East, as well as U.S.–China trade frictions, added further risks to global trade flows. Source: INEGI; Bureau of Economic Analysis.

Nevertheless, capital flows into emerging markets were robust, supported by strong currencies and attractive carry trades, with Mexico, Brazil, and India among the main beneficiaries.

Mexico Macro Domestic

Mexico’s economy displayed a modest recovery in the first half of 2025. GDP expanded by 0.6% in Q1 and 1.2% in Q2, though full-year growth expectations remain subdued, with institutions warning of possible stagnation. Services, which account for roughly two-thirds of GDP, grew by 1.8% year-over-year in Q2, supported by commerce, transportation, and tourism. The industrial sector contracted slightly (-0.2% y/y), though manufacturing (+2%) and construction (+5–6%) offered bright spots. The primary sector moderated from earlier strength but remained in positive territory. Source: INEGI.

Inflation pressures persisted. Headline CPI eased to 3.5% in July from 4.5% in June, while core inflation remained sticky around 4.2%. Despite this, the Bank of Mexico cut rates five times in 2025, bringing the benchmark rate to 7.75% by August, a clear signal that supporting growth is now a priority. Source: INEGI; Banxico.

External balances remained resilient. Mexico recorded a current account surplus of 205 billion pesos (~0.3% of GDP) in Q2, backed by robust foreign direct investment inflows of US$21.4 billion in Q1. However, remittances weakened by 5.6% YoY in 1H 2025, reflecting U.S. immigration and labor market uncertainty. Source: Banxico.

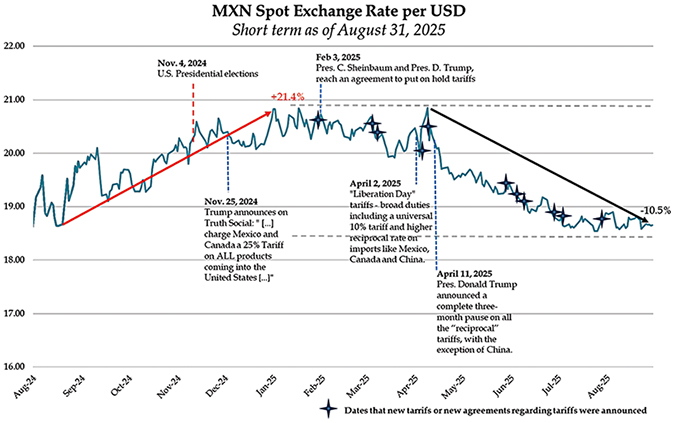

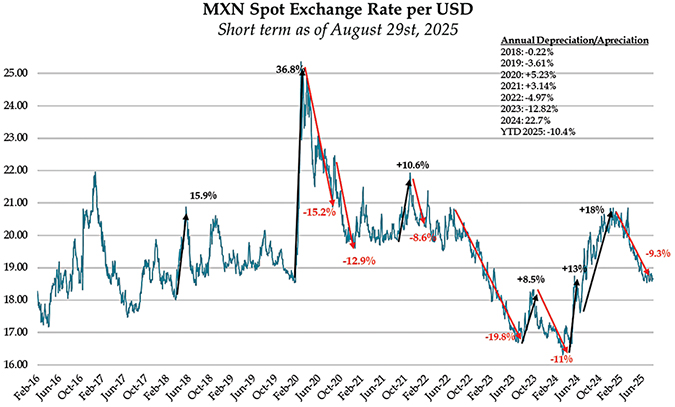

Year-to-date, the peso has strengthened approx. 10.5% against the dollar, one of the most significant gains among emerging-market currencies. In USD terms, the USD/MXN rate has dropped from 20.63 in early January to around 18.70–18.66 by August 29. Among the factors that explain the appreciation of the Mexican peso are: (i) inflows driven by a strong carry trade due to the high interest rate differential in favor of Mexico; (ii) periods of optimism, especially between March and June, stemming from exemptions to tariffs on steel and aluminum, and the postponement of tariffs on automotive exports under the USMCA, lifting the peso ~1–2% on each news wave. Source: Bloomberg.

Please see the August 2025 Economic Report at the Fund’s webpage: mxefund.com

1

THE MEXICO EQUITY AND INCOME FUND, INC. (Unaudited)

Source: Bloomberg, as of July 31, 2025.

Source: Bloomberg, as of August 29, 2025.

2

THE MEXICO EQUITY AND INCOME FUND, INC. (Unaudited)

The S&P/BMV IPyC

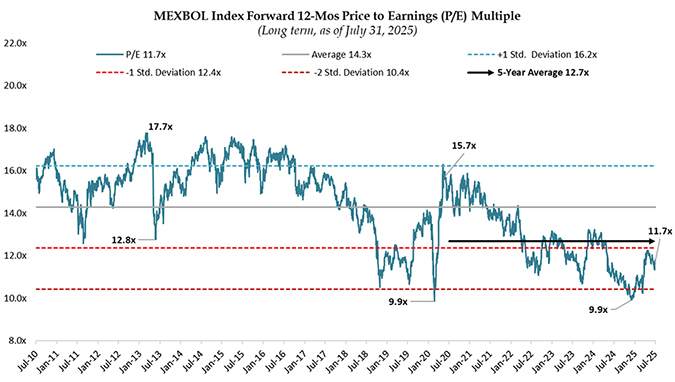

The S&P/BMV IPyC delivered a 19% return in local currency during 1H 2025 and reached 21.7% by late August, outperforming most global peers. Defensive sectors such as consumer staples and telecommunications insulated the index from tariff shocks, while government negotiations to delay U.S. trade measures helped sustain investor confidence. The Equity market valuations have historically been low. The 11.7x valuation graph below suggests an attractive entry point for long-term investors. Source: Bloomberg.

Source: Bloomberg, as of July 31, 2025.

3

THE MEXICO EQUITY AND INCOME FUND, INC. (Unaudited)

Benchmark indices outperformed, resulting in negative excess return, driven mainly by materials, industrials, and financials underweights. Conversely, staples and communication services contributed positively. For Sectorial contributors and detractor -return attribution analysis & Sectorial deviation, please call the MXE’s Portfolio Adviser, PAM.

Source: U.S. Bancorp Fund Services, Bloomberg.

| ** | On January 31, 2020, the Fund completed the Tender offer to purchase up to 67% of the outstanding shares at 98% of the Fund’s net asset value (“NAV”) |

| * | On October 12, 2021, the fund announced the results of its Opportunistic Rights Offering 146% of outstanding shares at a subscription price of US $8.90 per common stock. |

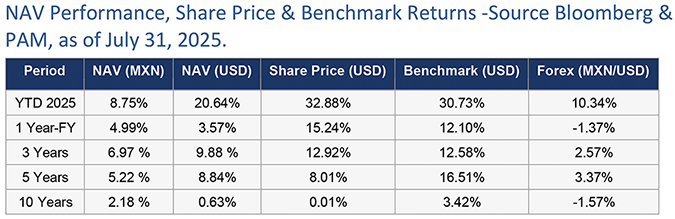

Performance data represents past performance; past performance does not guarantee future results.

The investment return and principal value of an investment will fluctuate so that the investor’s shares, when sold, may be worth more or less than their original cost. Performance data to the most recent month end may be obtained by calling U.S. Bancorp Fund Services, LLC, (414)765-4255, or by consulting the Fund’s web page: www.mxefund.com. The Fund s shares have traded in the market above (at a premium), at, and below (at a discount) the net asset value per share (NAV) since the commencement of the Fund s operations. Generally, shares of closed-end investment companies, including those of the Fund, trade at a discount from NAV.

The Fund navigated a challenging fiscal year ending July 31, 2025. April 2025 represented a turning point as tariff announcements disrupted markets. The Fund adopted a more defensive stance, temporarily reducing equity exposure to preserve capital. While this decision weighed on relative performance as markets rebounded later in April, it reflected prudent risk management.

In May and June, optimism returned as the stock market reached new highs and the peso appreciated further. The Fund participated in these gains, although relative performance lagged concentrated benchmarks. Active portfolio construction favored consumption, telecommunications, and selective industrials.

4

THE MEXICO EQUITY AND INCOME FUND, INC. (Unaudited)

Looking forward, we remain confident in the resilience of Mexico’s structural advantages, including its trade integration, competitive positioning, and investor inflows. Our disciplined investment approach prioritizes quality and value across cycles, aiming to deliver consistent long-term returns.

We thank you for your continued trust and support.

Sincerely,

|

|

| Eugenia Pichardo Principal & CEO |

David Estevez Analyst, Portfolio Manager, and Fund Secretary |

5

THE MEXICO EQUITY AND INCOME FUND, INC. (Unaudited)

DISCLAIMER

The Mexico Equity and Income Fund, Inc. (the “Fund”), achieves its investment objective through investments in securities, primarily equity, listed on the Mexican Stock Exchange. It serves as a vehicle for those who seek to invest in Mexican companies through a managed non-diversified portfolio as part of their overall investment program.

Fund holdings and sector allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Please see the Schedule of Investments in this report for a complete list of fund holdings. The information and views provided herein represent the opinion of Pichardo Asset Management, not the Fund’s Board of Directors, and it does not intend to be a forecast of future events, a guarantee of future results, or investment advice. This report contains certain forward-looking statements about factors that may affect the Fund’s future performance.

Our management, with a firm belief in the reasonableness of these forward-looking statements, acknowledges their inherent uncertainty and difficulty in prediction. This belief is a testament to our commitment to providing you with the most informed investment decisions.

Investors, in their pursuit of sound investment decisions, must diligently consider the Fund’s investment objectives, risks, charges, expenses, and restrictions. The prospectus, a comprehensive source of this and other important information about the investment company is available for your perusal. We strongly advise you to read it carefully before making any investment.

All investments involve risk. Principal loss is possible. Investing in equities in Emerging markets involves additional risks such as currency fluctuations, currency devaluations, price volatility, social and economic instability, differing securities regulations and accounting standards, limited publicly available information, changes in taxation, periods of illiquidity, and other factors. These risks are more significant in emerging markets. Stocks of small- and medium-capitalization companies involve greater volatility and less liquidity than stocks of larger-capitalization companies.

Investing in Foreign Securities

Investment in Mexican securities involves special considerations and risks that are not generally associated with investments in U.S. securities, including (1) relatively higher price volatility, lower liquidity, and the small market capitalization of Mexican securities markets; (2) currency fluctuations and the cost of converting Mexican pesos into U.S. dollars; (3) restrictions on foreign investment; (4) political, economic and social risks and uncertainties (5) higher rates of inflation and interest rates than in the United States. In addition, Mexican equity investments are in Mexican pesos. As a result, the Portfolio Securities must increase in market value at a rate over the rate of any decline in the peso’s value against the U.S. dollar to avoid a reduction in their equivalent U.S. dollar value.

The Fund may have a higher turnover rate, which may result in higher transaction costs and tax liability, which may affect returns.

6

THE MEXICO EQUITY AND INCOME FUND, INC. (Unaudited)

Definitions

| • | The stock’s net asset value (NAV) is the value of a fund’s assets minus its liabilities. The term “net asset value” is commonly used concerning closed-end funds to determine the value of the assets held. |

| • | The market price of the ordinary share of a closed-end fund is determined in the open market by buyers and sellers and is the price at which investors may purchase or sell the common shares of a closed-end fund, which fluctuates throughout the day. The standard share market price may differ from the Fund’s Net Asset Value; shares of a closed-end fund may trade at a premium to (higher than) or a discount to (lower than) NAV. The difference between the market price and NAV is a discount. |

| • | A basis point (bps) is one-hundredth of a percentage point (0.01%). |

| • | Premium/Discount: An investment trust’s share price can differ from its net asset value (NAV). If the current share price is above the NAV, the trust is said to be trading at a premium, i.e., it costs more to buy the shares than the underlying investments are worth. When the share price is below the NAV, this is known as trading at a discount. |

| • | MEXBOL, or the IPC (Indice de Precios y Cotizaciones), is a capitalization-weighted index of the Mexican stock exchange’s leading stocks. |

| • | MSCI-Mexico Net Total Return Index: The Morgan Stanley Capital International Index Mexico is a free float capitalization-weighted index that tracks the Mexican Stock Market. One cannot invest directly in an index. |

| • | Credit Ratings: A credit rating is an independent assessment of the ability of a corporation or a government to repay a debt, either in general terms or regarding a specific financial obligation. Credit ratings are issued to companies and governments by several companies including S&P Global, Moody’s, and Fitch Ratings. Credit ratings are used by investors who want to know the risk of buying bonds or other debt instruments issued by these entities. |

| • | BANXICO: Banco de Mexico is the Central Bank of Mexico. By constitutional mandate, it is autonomous in both its operations and management. Its primary function is to provide domestic currency to the Mexican economy, and its main priority is to ensure the stability of the domestic currency’s purchasing power. |

| • | Reference Rate: is an interest rate benchmark used to set other interest rates. Various types of transactions use different reference rate benchmarks, but the most common include the Fed Funds Rate, LIBOR, the prime rate, and the rate on benchmark U.S., among others. |

| • | INEGI: The National Institute of Statistics and Geography. |

| • | CONSAR: Comisión Nacional de Sistemas de Ahorro para el Retiro, the Borrower’s National Retirements Savings System Commission. |

| • | CNBV: The National Banking and Securities Commission (CNBV) |

| • | Gross Domestic Product (GDP): is the standard measure of the value added created by producing goods and services in a country during a specific period. As such, it also measures the income earned from that production or the total amount spent on final goods and services (less imports). |

7

THE MEXICO EQUITY AND INCOME FUND, INC. (Unaudited)

| • | The debt-to-GDP ratio is a metric that compares a country’s public debt to its gross domestic product (GDP). It reliably indicates a country’s ability to pay back its debts by comparing what the country owes with what it produces. The debt-to-GDP ratio is often expressed as a percentage and it can also be interpreted as the number of years necessary to pay back debt if GDP is dedicated entirely to debt repayment. |

| • | Remittances are money sent from one party to another. Nowadays, the term is most often used to describe a sum of money sent by someone working abroad to their family back home. |

| • | Foreign Direct Investment (FDI) is an investment made by a company or individual in one country in business interests in another country. This investment can be in the form of either establishing business operations or acquiring business assets in another country, such as ownership or a controlling interest in a foreign company. |

| • | Gross Fixed Investment Indicator (IIFB): Describes the net capital accumulation during an accounting period for a country. The term refers to additions of capital stock, such as equipment, tools, transportation assets, and electricity. |

| • | An import is a good or service bought in one country that was produced in another. Imports and exports are the components of international trade. |

| • | Exports: Exports are goods and services produced in one country and sold to buyers in another. Together with imports, exports make up international trade. |

| • | Forward PE Ratio: The regular P/E ratio is the current stock price over its earnings per share. The forward P/E ratio is the current stock price over its “predicted” earnings per share. If the forward P/E ratio is higher than the current P/E ratio, it indicates decreased expected earnings. |

| • | EV/EBITDA: This is a popular valuation multiple used in the finance industry to measure a company’s value. It is the most widely used valuation multiple based on enterprise value. |

| • | Attribution analysis: is a sophisticated method for evaluating the performance of a portfolio or fund manager. The method focuses on three factors: the manager’s investment style, their specific stock picks, and the market timing of those decisions. It attempts to provide a quantitative analysis of a fund manager’s investment selections and philosophy that lead to that fund’sFund’s performance. |

| • | Treasury Bond (T-Bond): A marketable, fixed-interest U.S. government debt securities with more than 10 years of maturity. Treasury bonds make interest payments semiannually, and the income received is only taxed at the federal level. |

| • | M-Bond: Mexico Federal Government fixed-rate development bonds that are issued and placed at terms of over one year, pay interest every six months, and their interest rate is determined at the issue date and remains fixed all along the bond’s life. |

| • | Consumer Price Index (INPC): This is a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item in the predetermined basket of goods and averaging them. |

8

THE MEXICO EQUITY AND INCOME FUND, INC. (Unaudited)

| • | Basis points (bps): Refers to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001. |

| • | Foreign Direct Investment (FDI): Is an investment made by a company or individual in one country in business interests in another country, in the form of either establishing business operations or acquiring business assets in the other country, such as ownership or controlling interest in a foreign company. |

9

THE MEXICO EQUITY AND INCOME FUND, INC. (Unaudited)

RELEVANT ECONOMIC INFORMATION for the years ended December 31

| Real_Activity (billion US$) | 2024 | 2023 | 2022 | 2021 | 2020 |

| Real GDP Growth (y-o-y) | 1.50% |

3.20% |

3.10% |

4.80% |

-8.30% |

| Industrial Production (y-o-y) | 0.20% | 1.20% | 3.10% | 6.71% | -3.15% |

| Trade Balance (US billions) | -$8.21 | -$5.46 | -$26.42 | -$11.49 | $34.48 |

| Exports (US billions) | $617.10 | $593.01 | $578.19 | $494.23 | $417.67 |

| Export growth (y-o-y) | 4.06% | 2.56% | 16.90% | 18.52% | -9.34% |

| Imports (US billions) | $625.31 | $598.48 | $604.61 | $505.72 | $383.19 |

| Import growth (y-o-y) | 4.48% | -1.02% | 19.60% | 32.05% | -15.84% |

| Financial Variables and Prices | |||||

| 28-Day CETES (T-bills)/Average | 10.71% | 11.10% | 7.66% | 4.45% | 5.30% |

| Exchange rate (Pesos/US$)Average | 18.33 | 17.73 | 20.11 | 20.29 | 21.47 |

| Inflation IPC, 12 month trailing | 4.21% | 4.66% | 7.82% | 7.36% | 3.15% |

| Mexbol Index | |||||

| USD Return | -27.77% | 40.87% | -1.09% | 20.94% | -2.35% |

| Market Cap- (US billions) | $297.23 | $438.75 | $326.47 | $326.47 | $282.91 |

| EV/EBITDA | 5.28x | 5.34x | 5.65x | 7.29x | 8.42x |

Sources: Banamex, Banco de Mexico, Bloomberg, MSCI.

10

THE MEXICO EQUITY AND INCOME FUND, INC.

Performance at a glance (unaudited)

Average annual total returns for common stock for the periods ended 7/31/2025

| Net asset value returns(1) | 1 year | 5 years | 10 years |

| The Mexico Equity and Income Fund, Inc. | 3.57% | 8.84% | 0.63% |

| Market price returns | |||

| The Mexico Equity and Income Fund, Inc. | 15.24% | 8.01% | 0.01% |

| Index returns | |||

| MSCI Mexico Index | 12.10% | 16.52% | 3.42% |

| Share price as of 7/31/2025 | |||

| Net asset value | |||

| Market price |

| (1) | The returns shown are based on net asset value calculated for shareholder transactions, which do not reflect adjustments made to the net asset value for financial reporting purposes in accordance with accounting principles generally accepted in the United States of America. |

Past performance does not predict future performance. The return and value of an investment will fluctuate so that an investor’s share, when sold, may be worth more or less than their original cost. The Fund’s common stock net asset value (“NAV”) return assumes, for illustration only, that dividends and other distributions, if any, were reinvested at the NAV on the ex-dividend date. The Fund’s common stock market price returns assume that all dividends and other distributions, if any, were reinvested at the lower of the NAV or the closing market price on the ex-dividend date. NAV and market price returns for the period of less than one year have not been annualized. Returns do not reflect the deduction of taxes that a shareholder could pay on Fund dividends and other distributions, if any, or the sale of Fund shares.

The MSCI Mexico Index is designed to measure the performance of the large and mid cap segments of the Mexican market. With 24 constituents, the MSCI Mexico Index covers approximately 85% of the free float-adjusted market capitalization in Mexico.

11

THE MEXICO EQUITY AND INCOME FUND, INC.

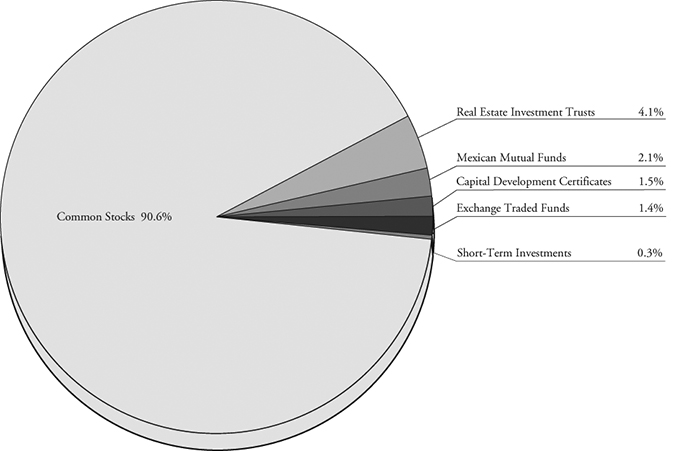

Allocation of Portfolio Assets (Calculated as a percentage of Total Investments) |

July 31, 2025 (Unaudited) |

12

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2025

Schedule of Investments

| COMMON STOCKS – 91.0% | Shares | Value | ||||||

| Airports – 9.3% | ||||||||

| Grupo Aeroportuario del Centro Norte, S.A.B. de C.V. | 96,258 | $ | 1,276,790 | |||||

| Grupo Aeroportuario del Pacifico, S.A.B. de C.V. – Series B | 64,700 | 1,486,368 | ||||||

| Grupo Aeroportuario del Sureste, S.A.B. de C.V. – Series B | 86,274 | 2,615,156 | ||||||

| 5,378,314 | ||||||||

| Auto Parts & Equipment – 4.0% | ||||||||

| Nemak, S.A.B. de C.V. (a)(b) | 12,856,484 | 2,344,357 | ||||||

| Beverages – 17.1% | ||||||||

| Arca Continental, S.A.B. de C.V. | 273,920 | 2,854,925 | ||||||

| Coca-Cola FEMSA, S.A.B. de C.V. | 238,400 | 1,976,704 | ||||||

| Fomento Economico Mexicano, S.A.B. de C.V. – Series UBD | 567,925 | 5,127,130 | ||||||

| 9,958,759 | ||||||||

| Building Materials – 7.7% | ||||||||

| Cemex, S.A.B. de C.V. | 2,261,861 | 1,974,707 | ||||||

| Grupo Cementos de Chihuahua, S.A.B. de C.V. | 269,036 | 2,513,950 | ||||||

| 4,488,657 | ||||||||

| Communication Services – 8.8% | ||||||||

| America Movil, S.A.B. de C.V. (a) | 5,680,255 | 5,127,736 | ||||||

| Construction and Infrastructure – 1.9% | ||||||||

| Promotora y Operadora de Infraestructura, S.A.B. de C.V. | 94,013 | 1,108,073 | ||||||

| Financial Groups – 4.9% | ||||||||

| Grupo Financiero Banorte, S.A.B. de C.V. – Series O | 317,354 | 2,828,177 | ||||||

| Food – 6.9% | ||||||||

| Alfa, S.A.B. de C.V. – Series A | 2,533,811 | 1,856,203 | ||||||

| Grupo Bimbo, S.A.B. de C.V. – Series A | 735,118 | 2,133,070 | ||||||

| 3,989,273 | ||||||||

| GICS~Chemicals – 1.2% | ||||||||

| Alpek, S.A.B. de C.V. | 1,447,133 | 694,225 | ||||||

| GICS~Media – 0.6% | ||||||||

| Megacable Holdings, S.A.B. de C.V. – Series A | 122,548 | 340,588 | ||||||

The accompanying notes are an integral part of these financial statements.

13

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2025

Schedule of Investments (continued)

| COMMON STOCKS (continued) | Shares | Value | ||||||

| Hotels, Restaurants, and Recreation – 0.5% | ||||||||

| Grupe, S.A.B. de C.V. (a)(c) | 200,591 | $ | 308,356 | |||||

| Mining – 7.7% | ||||||||

| Grupo Mexico, S.A.B. de C.V. – Series B | 713,274 | 4,464,910 | ||||||

| Railroads – 1.8% | ||||||||

| Grupo Traxion S.A.B. de C.V. (a)(b) | 1,180,634 | 1,037,005 | ||||||

| Real Estate Services – 2.7% | ||||||||

| Corporacion Inmobiliaria Vesta, S.A.B. de C.V. | 565,524 | 1,591,201 | ||||||

| Retail – 15.9% | ||||||||

| El Puerto de Liverpool, S.A.B. de C.V. – Series C1 | 305,674 | 1,502,040 | ||||||

| Grupo Comercial Chedraui, S.A. de C.V. | 165,296 | 1,338,928 | ||||||

| Wal-Mart de Mexico, S.A.B. de C.V. | 2,162,780 | 6,375,415 | ||||||

| 9,216,383 | ||||||||

| TOTAL COMMON STOCKS (Cost $46,404,022) | 52,876,014 | |||||||

| REAL ESTATE INVESTMENT TRUSTS – COMMON – 4.1% | ||||||||

| REITS – 4.1% | ||||||||

| Prologis Property Mexico, S.A. de C.V. | 640,033 | 2,405,764 | ||||||

| TOTAL REAL ESTATE INVESTMENT TRUSTS – COMMON | ||||||||

| (Cost $2,211,752) | 2,405,764 | |||||||

| MEXICAN MUTUAL FUNDS – 2.1% | ||||||||

| GBM Fondo de Corto Plazo SAB de CV SIID – Series BX (a) | 19,568,409 | 1,210,636 | ||||||

| TOTAL MEXICAN MUTUAL FUNDS (Cost $1,224,907) | 1,210,636 | |||||||

| CAPITAL DEVELOPMENT CERTIFICATES – 1.5% | ||||||||

| Atlas Discovery Trust II (a)(c) | 300,000 | 897,015 | ||||||

| TOTAL CAPITAL DEVELOPMENT CERTIFICATES (Cost $2,147) | 897,015 | |||||||

The accompanying notes are an integral part of these financial statements.

14

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2025

Schedule of Investments (concluded)

| EXCHANGE TRADED FUNDS – 1.4% | Shares | Value | ||||||

| iShares USD Treasury Bond 0-1yr UCITS ETF (a) | 1,800 | $ | 834,116 | |||||

| TOTAL EXCHANGE TRADED FUNDS (Cost $741,060) | 834,116 | |||||||

| SHORT-TERM INVESTMENTS | ||||||||

| MONEY MARKET FUNDS – 0.3% | ||||||||

| Morgan Stanley Institutional Liquidity Funds – Government Portfolio – | ||||||||

| Institutional Class, 4.22% (d) | 150,315 | 150,315 | ||||||

| TOTAL MONEY MARKET FUNDS (Cost $150,315) | 150,315 | |||||||

| TOTAL INVESTMENTS – 100.4% (Cost $50,734,203) | 58,373,860 | |||||||

| Liabilities in Excess of Other Assets – (0.4)% | (234,831 | ) | ||||||

| TOTAL NET ASSETS – 100.0% | $ | 58,139,029 | ||||||

Percentages are stated as a percent of net assets.

REIT – Real Estate Investment Trust

| (a) | Non-income producing security. |

| (b) | Security is exempt from registration pursuant to Rule 144A under the Securities Act of 1933, as amended. These securities may only be resold in transactions exempt from registration to qualified institutional investors. As of July 31, 2025, the value of these securities total $3,381,362 or 5.8% of the Fund’s net assets. |

| (c) | Fair value determined using significant unobservable inputs in accordance with procedures established by and under the supervision of the Fund’s Board of Directors. These securities represented $1,205,371 or 2.1% of net assets as of July 31, 2025. |

| (d) | The rate shown represents the 7-day annualized effective yield as of July 31, 2025. |

The accompanying notes are an integral part of these financial statements.

15

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2025

Statement of Assets & Liabilities

| ASSETS: | ||||

| Investments, at value (cost $50,734,203) | $ | 58,373,860 | ||

| Interest receivable | 653 | |||

| Foreign currency (cost $162) | 159 | |||

| Other Assets | 8,337 | |||

| Total Assets | 58,383,009 | |||

| LIABILITIES: | ||||

| Payables: | ||||

| Directors | 58,533 | |||

| Advisory | 36,091 | |||

| NYSE | 39,070 | |||

| Audit | 33,441 | |||

| Administration | 23,825 | |||

| Printing and mailing | 22,995 | |||

| Fund accounting | 13,525 | |||

| Legal | 7,247 | |||

| Custody | 5,093 | |||

| CCO | 4,160 | |||

| Total Liabilities | 243,980 | |||

| Net Assets | 58,139,029 | |||

| Net Asset Value Per Common Share ($58,139,029 / ) | $ | |||

| NET ASSETS CONSIST OF: | ||||

| Common stock, $0.001 par value; shares outstanding ( shares authorized) | 4,400 | |||

| Paid-in capital | 53,757,904 | |||

| Total distributable earnings | 4,376,725 | |||

| Net Assets | $ | 58,139,029 | ||

The accompanying notes are an integral part of these financial statements.

16

THE MEXICO EQUITY AND INCOME FUND, INC.

For the Year Ended July 31, 2025 | |

| Statement of Operations |

| INVESTMENT INCOME | ||||

| Dividends(1) | $ | 1,821,379 | ||

| Interest | 121,630 | |||

| Total Investment Income | 1,943,009 | |||

| EXPENSES AND FEES | ||||

| Advisory (Note B) | 491,839 | |||

| Directors (Note B) | 182,813 | |||

| Administration (Note B) | 94,432 | |||

| CCO (Note B) | 65,211 | |||

| Fund accounting (Note B) | 49,961 | |||

| NYSE | 56,562 | |||

| Custodian (Note B) | 35,821 | |||

| Audit | 33,446 | |||

| Printing and mailing | 40,214 | |||

| Legal | 33,283 | |||

| Insurance | 30,710 | |||

| Transfer agent (Note B) | 26,178 | |||

| Total Expenses | 1,140,470 | |||

| NET INVESTMENT INCOME | 802,539 | |||

| NET REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS | ||||

| Net realized loss from investments and foreign currency transactions | (3,829,395 | ) | ||

| Net change in unrealized appreciation (depreciation) on investments and foreign currency transactions | 4,914,832 | |||

| Net gain from investments and foreign currency transactions | 1,085,437 | |||

| Net increase in net assets resulting from operations | $ | 1,887,976 | ||

| (1) | Net of $184,951 in dividend withholding tax. |

The accompanying notes are an integral part of these financial statements.

17

THE MEXICO EQUITY AND INCOME FUND, INC.

Statements of Changes in Net Assets

| For the | For the | |||||||

| Year Ended | Year Ended | |||||||

| July 31, 2025 | July 31, 2024 | |||||||

| INCREASE (DECREASE) IN NET ASSETS | ||||||||

| Operations: | ||||||||

| Net investment income | $ | 802,539 | $ | 2,096,497 | ||||

| Net realized gain (loss) on investments and foreign currency transactions | (3,829,395 | ) | 5,642,653 | |||||

| Net change in unrealized appreciation (depreciation) in value | ||||||||

| of investments and foreign currency transactions | 4,914,832 | (14,406,705 | ) | |||||

| Net increase (decrease) in net assets resulting from operations | 1,887,976 | (6,667,555 | ) | |||||

| Distributions to Common Shareholders from: | ||||||||

| Net dividends and distributions | (1,311,836 | ) | (1,325,465 | ) | ||||

| Decrease in net assets resulting from distributions | (1,311,836 | ) | (1,325,465 | ) | ||||

| Total increase (decrease) in net assets | 576,140 | (7,993,020 | ) | |||||

| Net Assets: | ||||||||

| Beginning of year | 57,562,889 | 65,555,909 | ||||||

| End of year | $ | 58,139,029 | $ | 57,562,889 | ||||

The accompanying notes are an integral part of these financial statements.

18

THE MEXICO EQUITY AND INCOME FUND, INC.

Financial Highlights

For a Common Share Outstanding Throughout Each Year

| For the Years Ended July 31, | ||||||||||||||||||||

| 2025 | 2024 | 2023 | 2022 | 2021 | ||||||||||||||||

| Per Share Operating Performance | ||||||||||||||||||||

| Net asset value, beginning of year | $ | $ | $ | $ | $ | |||||||||||||||

| Net investment income (loss) | 0.18 | 0.48 | 0.43 | 0.43 | (0.18 | ) | ||||||||||||||

| Net realized and unrealized gains (losses) on | ||||||||||||||||||||

| investments and foreign currency transactions | 0.25 | (2.00 | ) | 4.05 | (1.50 | ) | 5.57 | |||||||||||||

| Net increase (decrease) from investment operations | 0.43 | (1.52 | ) | 4.48 | (1.07 | ) | 5.39 | |||||||||||||

| Less: Distributions | ||||||||||||||||||||

| Dividends from net investment income | (0.30 | ) | (0.30 | ) | — | — | — | |||||||||||||

| Distributions from net realized gains | — | — | — | — | — | |||||||||||||||

| Total dividends and distributions | (0.30 | ) | (0.30 | ) | — | — | — | |||||||||||||

| Capital Share Transactions | ||||||||||||||||||||

| Anti-dilutive effect of Tender Offer | — | — | — | — | — | |||||||||||||||

| Dilutive effect of Common Share Rights Offering | — | — | — | (2.94 | ) | — | ||||||||||||||

| Total capital share transactions | — | — | — | (2.94 | ) | — | ||||||||||||||

| Net Asset Value, end of year | $ | $ | $ | $ | $ | |||||||||||||||

| Per share market value, end of year | $ | $ | $ | $ | $ | |||||||||||||||

| Total Investment Return Based on | ||||||||||||||||||||

| Market Value, end of year(1) | 15.24 | % | (7.98 | )% | 35.79 | % | (36.30 | )% | 60.23 | % | ||||||||||

| Ratios/Supplemental Data | ||||||||||||||||||||

| Net assets, end of year (000’s) | $58,129 | $57,563 | $65,556 | $45,870 | $25,770 | |||||||||||||||

| Ratios of expenses to average net assets: | 2.13 | % | 1.91 | % | 2.13 | % | 2.32 | % | 3.89 | % | ||||||||||

| Ratios of net investment income (loss) | ||||||||||||||||||||

| to average net assets: | 1.50 | % | 3.33 | % | 3.43 | % | 1.12 | % | (1.56 | )% | ||||||||||

| Portfolio turnover rate | 156.07 | % | 166.37 | % | 159.02 | % | 153.01 | % | 217.50 | % | ||||||||||

| (1) | Total investment return is calculated assuming a purchase of common stock at the current market price on the first day and a sale at the current market price on the last day of each period reported. Dividends and distributions, if any, are assumed for purposes of this calculation to be reinvested at the closing market price on the dividend ex-date. Total investment does not reflect brokerage commissions. |

The accompanying notes are an integral part of these financial statements.

19

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2025

Notes to Financial Statements

NOTE A: ORGANIZATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The Mexico Equity and Income Fund, Inc. (the “Fund”) was incorporated in Maryland on May 24, 1990, and commenced operations on August 21, 1990. The Fund is registered under the Investment Company Act of 1940, as amended, as a closed-end, non-diversified management investment company.

The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (FASB) Accounting Standard Codification Topic 946 “Financial Services—Investment Companies”.

The preparation of financial statements in accordance with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from those estimates.

Significant accounting policies are as follows:

Portfolio Valuation. Investments are stated at value in the accompanying financial statements. Listed equity securities are valued at the closing price on the exchange or market on which the security is primarily traded (the “Primary Market”) at the valuation time. If the security did not trade on the Primary Market, it shall be valued at the closing price on another comparable exchange where it trades at the valuation time. If there are no such closing prices, the security shall be valued at the mean between the most recent highest bid and lowest ask prices at the valuation time. Investments in short-term debt securities having a maturity of 60 days or less are valued at amortized cost if their term to maturity from the date of purchase was less than 60 days, or by amortizing their value on the 61st day prior to maturity if their term to maturity from the date of purchase when acquired by the Fund was more than 60 days. Other assets and securities for which no quotations are readily available will be valued in good faith at fair value using methods determined by the Board of Directors. These methods include, but are not limited to, the fundamental analytical data relating to the investment; the nature and duration of restrictions in the market in which they are traded (including the time needed to dispose of the security, methods of soliciting offers and mechanics of transfer); the evaluation of the forces which influence the market in which these securities may be purchased or sold, including the economic outlook and the condition of the industry in which the issuer participates and sum of the parts methodology. The Fund has a Valuation Committee comprised of independent directors which oversees the valuation of portfolio securities. Any securities or other assets for which market quotations are not readily available are valued at their fair value pursuant to policies and procedures adopted pursuant to Rule 2a-5 under the 1940 Act.

Investment Transactions and Investment Income. The cost of investments sold is determined by use of the specific identification method for both financial reporting and income tax purposes. Interest income, including the accretion of discount and amortization of premium on investments, is recorded on an accrual basis; dividend income is recorded on the ex-dividend date or, using reasonable diligence, when known to the Fund. The collectibility of income receivable from foreign securities is evaluated periodically, and any

20

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2025

Notes to Financial Statements (continued)

resulting allowances for uncollectible amounts are reflected currently in the determination of investment income. There was no allowance for uncollectible amounts at July 31, 2025.

Tax Status. No provision is made for U.S. Federal income or excise taxes as it is the Fund’s intention to continue to qualify as a regulated investment company and to make the requisite distributions to its shareholders that will be sufficient to relieve it from all or substantially all U.S. Federal income and excise taxes.

The Fund is subject to the following withholding taxes on income from Mexican sources:

Interest income on debt issued by the Mexican federal government is generally not subject to withholding. Withholding tax on interest from other debt obligations such as publicly traded bonds and loans by banks or insurance companies is at a rate of 4.9% under the tax treaty between Mexico and the United States.

Gains realized from the sale or disposition of debt securities may be subject to a 4.9% withholding tax. Gains realized by the Fund from the sale or disposition of equity securities that are listed and traded on the Mexican Stock Exchange (“MSE”) are exempt from Mexican withholding tax if sold through the stock exchange. Gains realized on transactions outside of the MSE may be subject to withholding at a rate of 25% (20% rate prior to January 1, 2002) of the value of the shares sold or, upon the election of the Fund, at 35% (40% rate prior to January 1, 2002) of the gain. If the Fund has owned less than 25% of the outstanding stock of the issuer of the equity securities within the 12 month period preceding the disposition, then such disposition will not be subject to capital gains taxes as provided for in the treaty to avoid double taxation between Mexico and the United States.

Investment Objectives

The Fund’s investment objective is to seek high total return through capital appreciation and current income. There can be no assurance that the Fund’s objective will be achieved.

Investment Strategies

The Fund pursues its objective primarily by investing, under normal circumstances, at least 80% of the Fund’s assets in equity and convertible securities issued by Mexican companies and debt securities of Mexican issuers.

The Fund invests in equity securities, convertible securities and debt securities and may also invest in other securities such as capital development certificates, real estate investment trusts, mutual funds, exchange traded funds, preferred stocks, rights and warrants. The Fund may, without limitation, hold cash or invest in assets in money market instruments, including U.S. and non-U.S. government securities, high grade commercial paper and certificates of deposit and bankers’ acceptances issued by U.S. and non-U.S. banks.

The Adviser may invest the Fund’s cash balances in any investments it deems appropriate, subject to the restrictions set forth in below under “Fundamental Investment Restrictions” and as permitted under the

21

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2025

Notes to Financial Statements (continued)

1940 Act. Any income earned from such investments will ordinarily be reinvested by the Fund in accordance with its investment program. Many of the considerations entering into the Adviser’s recommendations and decisions are subjective.

The Fund may, in limited circumstances, hedge against a decline in the value of the Mexican peso.

The short-term instruments in which the Fund may invest include (a) obligations of the United States Government and the Mexican Government, including the agencies or instrumentalities of each (including repurchase agreements with respect to these securities); (b) bank obligations (including certificates of deposit, time deposits and bankers’ acceptances of United States and Mexican banks denominated in U.S. dollars or pesos); (c) obligations of United States and Mexican companies that are rated no lower than A-2 by S&P or P-2 by Moody’s or the equivalent from another rating service or, if unrated, deemed to be of equivalent quality by the Adviser; and (d) shares of money market funds that are authorized to invest in (a) through (c).

Among the obligations of agencies and instrumentalities of the United States Government in which the Fund may invest are securities that are supported by the “full faith and credit” of the United States Government (such as securities of the Government National Mortgage Association), by the right of the issuer to borrow from the United States Treasury (such as those of the Export-Import Bank of the United States), by the discretionary authority of the United States Government to purchase the agency’s obligations (such as those of the Federal National Mortgage Association) or by the credit of the United States Government instrumentality itself (such as those of the Student Loan Marketing Association).

The Fund may, from time to time, take temporary defensive positions that are inconsistent with the Fund’s principal investment strategies in attempting to respond to adverse market, economic, political or other conditions. During such times, the Fund may temporarily invest up to 100% of its assets in cash or cash equivalents, including money market instruments, prime commercial paper, repurchase agreements, Treasury bills and other short-term obligations of the U.S. Government, its agencies or instrumentalities. In these and in other cases, the Fund may not achieve its investment objective.

Portfolio Investments

Common Stocks

The Fund will invest in common stocks. Common stocks represent an ownership interest in an issuer. While offering greater potential for long-term growth, common stocks are more volatile and riskier than some other forms of investment in short-term periods. Common stock prices fluctuate for many reasons, including adverse exogenous macro and systemic events, abrupt change in companies’ revenues due to commodity cycle or epidemic diseases, capital allocation, a period of disappointing financial reporting economics, fiscal, and monetary policies in the U.S.A, and Mexico.

Capital Development Certificates

Capital development certificates are hybrid instruments that may include debt and equity. Capital development certificates grant their holders the right to variable income arising from various projects and/or companies.

22

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2025

Notes to Financial Statements (continued)

Convertible Securities

Initially, the Fund’s management anticipated that the Fund would acquire convertible debt securities in privately negotiated transactions. However, because of the extremely limited number of convertible debt securities issued by Mexican companies, the Fund has not acquired convertible debt securities of Mexican companies for the last 25 years. However, the Fund may acquire convertible debt securities in Mexican companies in the future if and when they become available. A convertible debt security is a bond, debenture or note that may be converted into or exchanged for, or may otherwise entitle the holder to purchase, a prescribed amount of common stock or other equity security of the same or a different Mexican company within a particular period of time at a specified price or formula. A convertible debt security entitles the holder to receive interest paid or accrued on debt until the convertible security matures or is redeemed, converted or exchanged. Before conversion, convertible debt securities have characteristics similar to nonconvertible debt securities in that they ordinarily provide for a fixed stream of income with generally higher yields than those of stocks of the same or similar issuers. Convertible debt securities rank senior to stock in a corporation’s capital structure and, therefore, generally entail less risk than the corporation’s stock. Given the volatility of the Mexican securities market and the pricing of securities in Mexico, a significant portion of the value of a Mexican convertible debt security may be derived from the conversion feature rather than the fixed income feature.

The Fund defines debt securities (other than convertible debt securities) to mean bonds, notes, bills and debentures. The Fund’s investments in debt securities of Mexican issuers include debt securities issued by private Mexican companies and by the Mexican Government and its agencies and instrumentalities. These debt securities may be denominated either in pesos or in U.S. dollars.

Corporate Bonds, Government Debt Securities and Other Debt Securities

The Fund may invest in corporate bonds, debentures and other debt securities or in investment companies which hold such instruments. Bonds and other debt securities generally are issued by corporations and other issuers to borrow money from investors. The issuer pays the investor a fixed rate of interest and normally must repay the amount borrowed on or before maturity. Certain debt securities are “perpetual” in that they have no maturity date.

The Fund will invest in government debt securities. These securities may be U.S. dollar-denominated or non-U.S. dollar-denominated and include: (a) debt obligations issued or guaranteed by foreign national, provincial, state, municipal or other governments with taxing authority or by their agencies or instrumentalities; and (b) debt obligations of supranational entities. Government debt securities include: debt securities issued or guaranteed by governments, government agencies or instrumentalities and political subdivisions; debt securities issued by government owned, controlled or sponsored entities; interests in entities organized and operated for the purpose of restructuring the investment characteristics issued by the above noted issuers; or debt securities issued by supranational entities such as the World Bank or the European Union.

23

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2025

Notes to Financial Statements (continued)

Exchange Traded Funds

The Fund may invest in Exchange Traded Funds (“ETFs”), which are investment companies that aim to track or replicate a desired index, such as a sector, market or global segment. ETFs are passively managed and their shares are traded on a national exchange. ETFs do not sell individual shares directly to investors and only issue their shares in large blocks known as “creation units.” The investor purchasing a creation unit may sell the individual shares on a secondary market. Therefore, the liquidity of ETFs depends on the adequacy of the secondary market. There can be no assurance that an ETF’s investment objective will be achieved, as ETFs based on an index may not replicate and maintain exactly the composition and relative weightings of securities in the index. ETFs are subject to the risks of investing in the underlying securities. The Fund, as a holder of the securities of the ETF, will bear its pro rata portion of the ETF’s expenses, including advisory fees. These expenses are in addition to the direct expenses of the Fund’s own operations.

Real Estate Investment Trusts

The Fund may invest in securities of Real Estate Investment Trusts (“REITs”). REITs are trusts that specialize in acquiring, holding and managing residential, commercial or industrial real estate. A REIT is not taxed at the entity level on income distributed to its shareholders or unitholders if it distributes to shareholders or unitholders at least 90% of its taxable income for each taxable year and complies with regulatory requirements relating to its organization, ownership, assets and income.

Other Securities

Although it has no current intention do so to any material extent, the Fund may determine to invest the Fund’s assets in some or all of the following securities.

Forward Currency Contracts

The Fund may, in limited circumstances, hedge against a decline in the value of the Mexican peso. On March 19, 1995, Banco de Mexico approved the establishment of over-the-counter forward and option contracts in Mexico on the new peso between banks and their clients. Also, Banco de Mexico authorized the issuance and trading of futures contracts in respect of the new peso on the Chicago Mercantile Exchange (“CME”). Trading of new peso futures contracts began on the CME on April 25, 1995.

The Fund will conduct any forward currency exchange transactions, which are considered derivative transactions, only for hedging and not speculation. The risk of future currency devaluations and fluctuations should be carefully considered by investors in determining whether to purchase shares of the Fund. Although the Fund will value its assets daily in terms of U.S. dollars, it does not intend physically to convert its holdings of pesos into U.S. dollars on a daily basis. The Fund will do so from time to time, and investors should be aware of the costs of currency conversion. Although foreign exchange dealers do not charge a fee for conversion, they do realize a profit based on the difference (the “spread”) between the prices at which they are buying and selling various currencies. Thus, a dealer may offer to sell a foreign currency to the Fund at one rate, while offering a lesser rate of exchange should the Fund desire to resell that currency to the dealer.

24

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2025

Notes to Financial Statements (continued)

A forward currency contract involves an obligation to purchase or sell a specific currency at a future date, which may be any fixed number of days from the date of the contract agreed upon by the parties, at a price set at the time of the contract. The Fund’s dealings in forward currency contracts will be limited to hedging involving either specific transactions or portfolio positions. Transaction hedging is the purchase or sale of forward currency contracts with respect to specific receivables or payables of the Fund generally arising in connection with the purchase or sale of its portfolio securities or in anticipation of receipt of dividend or interest payments. Position hedging is the purchase or sale of forward currency contracts with respect to portfolio security positions denominated or quoted in the currency.

The Fund may not position hedge with respect to a particular currency to an extent greater than the aggregate market value (at the time of making such purchase or sale) of the securities held in its portfolio denominated or quoted in or currently convertible into that particular currency. If the Fund enters into a position hedging transaction, the custodian of the Fund’s assets being hedged will place cash or readily marketable securities in a segregated account of the Fund in an amount equal to the value of the Fund’s total assets committed to the consummation of the forward contract. If the value of the securities placed in the segregated account declines, additional cash or securities will be placed in the account so that the value of the account will equal the amount of the Fund’s commitment with respect to the contract.

The Fund may enter into forward currency contracts in several circumstances. When the Fund enters into a contract for the purchase or sale of securities denominated in a foreign currency, or when the Fund anticipates the receipt in a foreign currency of interest or dividend payments, the Fund may desire to “lock-in” the U.S. dollar price of the security or the U.S. dollar equivalent of such interest or dividend payment, as the case may be. By entering into a forward contract for a fixed amount of U.S. dollars for the purchase or sale of the amount of foreign currency involved in the underlying transactions, the Fund will be able to protect itself against a possible loss resulting from an adverse change in the relationship between the U.S. dollar and the subject foreign currency during the period between the date on which the security is purchased or sold, or on which the dividend payment is declared, and the date on which such dividend or interest payment is to be received.

At or before the maturity of a forward currency contract, the Fund may either sell a portfolio security and make delivery of the currency, or retain the security and offset its contractual obligation to deliver the currency by purchasing a second contract pursuant to which the Fund will obtain, on the same maturity date, the same amount of the currency that it is obligated to deliver. If the Fund retains the portfolio security and engages in an offsetting transaction, the Fund, at the time of execution of the offsetting transaction, will incur a gain or a loss to the extent that movement has occurred in forward contract prices. The use of forward currency contracts does not eliminate fluctuation in the underlying prices of the securities, but it does establish a rate of exchange that can be achieved in the future. In addition, although forward currency contracts limit the risk of loss due to a decline in the value of the hedged currency, at the same time they limit any potential

25

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2025

Notes to Financial Statements (continued)

gain that might result should the value of the currency increase. If a devaluation is generally anticipated, the Fund may not be able to contract to sell the currency at a price above the devaluation level it anticipates.

The cost to the Fund of engaging in currency transactions either on a spot or forward basis will vary with factors such as the currency involved, the length of the contract period and the market conditions then prevailing. Because transactions in currency exchange are usually conducted on a principal basis, no fees or commissions are involved, although the price charged in the transaction includes a dealer’s markup.

Certain provisions of the Code may limit the extent to which the Fund may enter into the foreign currency transactions described above. These transactions may also affect the character and timing of income, and the amount of gain or loss recognized by the Fund and its stockholders for U.S. federal income tax purposes.

Investment Companies

The Fund may invest in the securities of other investment companies (“underlying funds”), including those that invest a substantial portion of their assets in Mexican securities, to the extent permitted by, and subject to the conditions imposed by, the 1940 Act and the rules and regulations thereof. By investing in an investment company, the Fund bears a ratable share of the investment company’s expenses, as well as continuing to bear the Fund’s advisory and administrative fees with respect to the amount of the investment. Investment companies are subject to the risks of investing in the underlying securities. Under the 1940 Act, banks organized outside of the United States are deemed to be investment companies, although the SEC has adopted a rule which would permit the Fund to invest in the securities of foreign commercial banks, under certain circumstances, without regard to the percentage limitations of the 1940 Act.

The Fund may be subject to the risks of the securities and other instruments described herein through its own direct investments and indirectly through investments in the underlying funds, as those recently included in the “Bolsa”, named FIBRA E, (similar to a REIT in the U.S.) which corresponds to a Mexican mechanism to finance infrastructure, energy and long term projects, as well as private equity, regulated by the Comisión Nacional Bancaria y de Valores (corresponding SEC in the U.S.).

Illiquid Securities

Illiquid securities are securities that are not readily marketable. Illiquid securities include securities that have a low daily turnover or that trade on odd lots or trading-block among small and medium portfolio managers referred to as specialists but do not provide liquidity to trade at reasonable fair value. Illiquid securities usually present a high spread between the bid and ask quotes. If the Fund sells an illiquid security during a period with adverse market conditions, the Fund might obtain a less favorable price. Illiquid securities also include securities that have legal or contractual restrictions on resale, and repurchase agreements maturing in more than seven days. The Fund may invest up to 15% of the value of its total assets in illiquid securities. Restricted securities for which no market exists and other illiquid investments are valued at fair value as determined in accordance to policies and procedures adopted pursuant to Rule 2a-5 under the 1940 Act and periodically reviewed by the Board of Directors. At January 31, 2025 the Fund held 2.1% of its total net assets in illiquid positions.

26

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2025

Notes to Financial Statements (continued)

Rule 144A Securities

The Fund may invest in restricted securities that are eligible for resale pursuant to Rule 144A under the Securities Act of 1933, as amended, (the “1933 Act”). Generally, Rule 144A establishes a safe harbor from the registration requirements of the 1933 Act for resale by large institutional investors of securities that are not publicly traded. The Adviser determines the liquidity of the Rule 144A securities according to the Fund’s pricing policy and guidelines adopted by the Board of Directors. The Board of Directors monitors the application of those guidelines and procedures. Securities eligible for resale pursuant to Rule 144A, which are determined to be liquid, are not subject to the Fund’s 15% limit on investments in illiquid securities.

Preferred Stocks

The Fund may invest in preferred stocks. Preferred stock, like common stock, represents an equity ownership in an issuer. Generally, preferred stock has a priority of claim over common stock in dividend payments and upon liquidation of the issuer. Unlike common stock, preferred stock does not usually have voting rights. Preferred stock in some instances is convertible into common stock. Although they are equity securities, preferred stocks have characteristics of both debt and common stock. Like debt, their promised income is contractually fixed. Like common stock, they do not have rights to precipitate bankruptcy proceedings or collection activities in the event of missed payments. Other equity characteristics are their subordinated position in an issuer’s capital structure and that their quality and value are heavily dependent on the profitability of the issuer rather than on any legal claims to specific assets or cash flows.

Distributions on preferred stock must be declared by the board of directors and may be subject to deferral, and thus they may not be automatically payable. Income payments on preferred stocks may be cumulative, causing dividends and distributions to accrue even if not declared by the company’s board or otherwise made payable, or they may be non-cumulative, so that skipped dividends and distributions do not continue to accrue. There is no assurance that dividends on preferred stocks in which the Fund invests will be declared or otherwise made payable. The Fund may invest in non-cumulative preferred stock, although the Adviser may consider, among other factors, their non-cumulative nature in making any decision to purchase or sell such securities.

Shares of preferred stock have a liquidation value that generally equals the original purchase price at the date of issuance. The market values of preferred stock may be affected by favorable and unfavorable changes impacting the issuers’ industries or sectors, including companies in the utilities and financial services sectors, which are prominent issuers of preferred stock. They may also be affected by actual and anticipated changes or ambiguities in the tax status of the security and by actual and anticipated changes or ambiguities in tax laws, such as changes in corporate and individual income tax rates, and in the dividends received deduction for corporate taxpayers or the lower rates applicable to certain dividends.

Because the claim on an issuer’s earnings represented by preferred stock may become onerous when interest rates fall below the rate payable on the stock or for other reasons, the issuer may redeem preferred stock, generally

27

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2025

Notes to Financial Statements (continued)

after an initial period of call protection in which the stock is not redeemable. Thus, in declining interest rate environments in particular, the Fund’s holdings of higher dividend -paying preferred stocks may be reduced and the Fund may be unable to acquire securities paying comparable rates with the redemption proceeds.

Warrants

The Fund may invest in equity and index warrants of domestic and international issuers. Equity warrants are securities that give the holder the right, but not the obligation, to subscribe for equity issues of the issuing company or a related company at a fixed price either on a certain date or during a set period. Changes in the value of a warrant do not necessarily correspond to changes in the value of its underlying security. The price of a warrant may be more volatile than the price of its underlying security, and a warrant may offer greater potential for capital appreciation as well as capital loss. Warrants do not entitle a holder to dividends or voting rights with respect to the underlying security and do not represent any rights in the assets of the issuing company. A warrant ceases to have value if it is not exercised prior to its expiration date. These factors can make warrants more speculative than other types of investments. The sale of a warrant results in a long or short-term capital gain or loss depending on the period for which the warrant is held.

RISK FACTORS

An investment in the Fund is not guaranteed to achieve its investment objective; is not a deposit with a bank; is not insured, endorsed or guaranteed by the Federal Deposit Insurance Corporation or any other government agency; and is subject to investment risks. The value of the Fund’s investments will increase or decrease based on changes in the prices of the investments it holds. You could lose money by investing in the Fund. By itself, the Fund does not constitute a balanced investment program. You should consider carefully the following principal and non-principal risks before investing in the Fund. There may be additional risks that the Fund does not currently foresee or consider material. You may wish to consult with your legal or tax advisors, before deciding whether to invest in the Fund. This section describes the risk factors associated with investment in the Fund specifically, as well as those factors generally associated with investment in an investment company with investment objectives, investment policies, capital structure or trading markets similar to the Fund’s. Each risk summarized below is a risk of investing in the Fund and different risks may be more significant at different times depending upon market conditions or other factors.

The Fund may invest in securities of other investment companies (“underlying funds”). The Fund may be subject to the risks of the securities and other instruments described below through its own direct investments and indirectly through investments in the underlying funds.

Principal Risks

Investments in Foreign Securities Risks.

The Fund invests in the universe of Mexican securities market. Investing in Mexican securities presents political, regulatory and economic risks in some ways similar to those that face a re-emerging country and a developing county; and different in kind and degree from the risks presented by investing in the U.S. financial markets or any other fairly comparable emerging country in the Latin American region, pertaining

28

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2025

Notes to Financial Statements (continued)

to the emerging market risk. Some of these risks may include devaluation and/or appreciation of the exchange rate of the Mexican Peso, greater market price volatility, substantially less liquidity, controls on foreign investment, and limitations on repatriation of invested capital. Unlike U.S. issuers which are required to comply GAAP accounting policy standards, Mexican issuers comply with mandatory regulation to IFR’s accounting standards and policies. Additional risks of investing in foreign securities are detailed below.

Market Illiquidity, Volatility. Although one of the largest in Latin America by market capitalization, the Bolsa Mexicana de Valores, S.A. de C.V. (the “Mexican Stock Exchange” or “Bolsa”) is substantially smaller, less liquid and more volatile than the major securities markets in the United States. In addition, trading on the Mexican Stock Exchange is concentrated. Thus, the performance of the Mexican Stock Exchange, as further described below, may be highly dependent on the performance of a few issuers. Additionally, prices of equity securities traded on the Mexican Stock Exchange are generally more volatile than prices of equity securities traded on the New York Stock Exchange. The combination of price volatility and the relatively limited liquidity of the Mexican Stock Exchange may have an adverse impact on the investment performance of the Fund.

Market Corrections. Although less so in recent times, the Mexican securities market has been subject to periodic severe market corrections. A recent correction in the Bolsa’s Index occurred at the cancellation of the latest state of the ongoing art construction of a new airport by the new administration in Mexico starting in 2017. Due to the high concentration of investors, issuers and intermediaries in the Mexican securities market and the generally high volatility of the Mexican economy, the Mexican securities market may be subject to severe market corrections than more broadly based markets. As is the case with investing in any securities market, there can be no assurance that market corrections will not occur again.

The Mexican Economy. In the past, the Mexican economy has experienced peso devaluations, significant rises in inflation and domestic interest rates and other economic instability and there can be no assurance that it will not experience such instability in the future.

Common Stock Risk. The Fund invests in common stocks. Common stocks represent an ownership interest in a company. The Fund may also invest in securities that can be exercised for or converted into common stocks (such as convertible preferred stock). Common stocks and similar equity securities are more volatile and riskier than some other forms of investments. Therefore, the value of your investment in the Fund may sometimes decrease instead of increase. Common stock prices fluctuate for many reasons, including adverse events such as unfavorable earnings reports, changes in investors’ perceptions of the financial condition of an issuer, the general condition of the relevant stock market or when political or economic events affecting the issuers occur. In addition, common stock prices may be sensitive to rising interest rates, as the costs of capital rise and borrowing costs increase for issuers. Because convertible securities can be converted into equity securities, their values will normally increase or decrease as the values of the underlying equity securities increase or decrease. The common stocks in which the Fund invests are structurally subordinated to preferred

29

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2025

Notes to Financial Statements (continued)

securities, bonds and other debt instruments in a company’s capital structure in terms of priority to corporate income and assets and, therefore, will be subject to greater risk than the preferred securities or debt instruments of such issuers.

Convertible Securities Risk. The Fund may acquire convertible debt securities in Mexican companies. A convertible debt security is a bond, debenture or note that may be converted into or exchanged for, or may otherwise entitle the holder to purchase, a prescribed amount of common stock or other equity security of the same or a different Mexican company within a particular period of time at a specified price or formula. A convertible debt security entitles the holder to receive interest paid or accrued on debt until the convertible security matures or is redeemed, converted or exchanged. Before conversion, convertible debt securities have characteristics similar to nonconvertible debt securities in that they ordinarily provide for a fixed stream of income with generally higher yields than those of stocks of the same or similar issuers. Convertible debt securities rank senior to stock in a corporation’s capital structure and, therefore, generally entail less risk than the corporation’s stock. Given the volatility of the Mexican securities market and the pricing of securities in Mexico, a significant portion of the value of a Mexican convertible debt security may be derived from the conversion feature rather than the fixed income feature.

The value of a convertible security, including, for example, a warrant, is a function of its investment value (determined by its yield in comparison with the yields of other securities of comparable maturity and quality that do not have a conversion privilege) and its conversion value (the security’s worth, at market value, if converted into the underlying common stock). The investment value of a convertible security is influenced by changes in interest rates, with investment value declining as interest rates increase and increasing as interest rates decline. The credit standing of the issuer and other factors may also have an effect on the convertible security’s investment value. The conversion value of a convertible security is determined by the market price of the underlying common stock. If the conversion value is low relative to the investment value, the price of the convertible security is governed principally by its investment value. Generally, the conversion value decreases as the convertible security approaches maturity. To the extent the market price of the underlying common stock approaches or exceeds the conversion price, the price of the convertible security will be increasingly influenced by its conversion value. A convertible security generally will sell at a premium over its conversion value by the extent to which investors place value on the right to acquire the underlying common stock while holding a fixed income security. A convertible security may be subject to redemption at the option of the issuer at a price established in the convertible security’s governing instrument. If a convertible security held by the Fund is called for redemption, the Fund will be required to permit the issuer to redeem the security, convert it into the underlying common stock or sell it to a third party. Any of these actions could have an adverse effect on the Fund’s ability to achieve its investment objective.

Small and Medium Capitalization Company Risk. The Fund may invest in securities without regard to market capitalization. Compared to investment companies that focus only on large capitalization companies, the Fund’s share price may be more volatile because it also invests in small and medium capitalization

30

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2025

Notes to Financial Statements (continued)

companies. Compared to large companies, small and medium capitalization companies are more likely to have (i) more limited product lines or markets and less mature businesses, (ii) fewer capital resources, (iii) more limited management depth and (iv) shorter operating histories. Further, compared to large capitalization companies, the securities of small and medium capitalization companies are more likely to experience sharper swings in market values, be harder to sell at times and at prices that the Adviser believes appropriate.

Market Risk. Overall market risk may affect the value of individual instruments in which the Fund invests. The Fund is subject to the risk that the securities markets will move down, sometimes rapidly and unpredictably, based on overall economic conditions and other factors, which may negatively affect the Fund’s performance. Factors such as domestic and foreign (non-U.S.) economic growth and market conditions, real or perceived adverse economic or political conditions, inflation, changes in interest rate levels, lack of liquidity in the markets, volatility in the securities markets, adverse investor sentiment affect the securities markets and political vents affect the securities markets. Securities markets also may experience long periods of decline in value. When the value of the Fund’s investments goes down, your investment in the Fund decreases in value and you could lose money.

Local, state, regional, national or global factors or events could have a significant impact on the Fund and its investments and could result in decreases to the Fund’s net asset value. Political, geopolitical, economic, social, natural and other factors or events, including war, military conflicts, terrorism, trade disputes, tariff arrangements, sanctions, cybersecurity attacks, government shutdowns, market closures, recessions, natural and environmental disasters, epidemics, pandemics and other public health crises and related events and governments’ reactions to such events have led, and in the future may lead, to economic uncertainty, decreased economic activity, increased market volatility and other disruptive effects on U.S. and global economies and markets. The extent and duration of such factors and events and resulting market disruptions cannot be predicted. Such events may have significant adverse direct or indirect effects on the Fund and its investments. For example, a widespread health crisis such as a global pandemic could cause substantial market volatility, exchange trading suspensions and closures, impact the ability to complete redemptions, and affect Fund performance. A health crisis may exacerbate other pre-existing political, social and economic risks. In addition, the increasing interconnectedness of markets around the world may result in many markets being affected by events or conditions in a single country or region or events affecting a single or small number of issuers.

Market Discount from Net Asset Value Risk. Shares of closed-end investment companies frequently trade at a discount from their net asset value (“NAV”). Because the market price of the Shares is determined by factors such as relative supply of and demand for the Shares in the market, general market and economic conditions, and other factors beyond the control of the Fund, the Fund cannot predict whether the Shares will trade at, below or above net asset value.

31

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2025

Notes to Financial Statements (continued)

Management Risk. The Fund is subject to management risk because it is an actively managed portfolio. The Fund’s successful pursuit of its investment objective depends upon the Adviser’s ability to find and exploit market inefficiencies with respect to undervalued securities. Such situations occur infrequently and may be difficult to predict, and may not result in a favorable pricing opportunity for the Fund. The Adviser’s sector allocation and stock selection decisions might produce losses or cause the Fund to underperform its benchmark or underperform when compared to other funds with similar investment goals. If one or more key individuals leave the employment of the Adviser, the Adviser may not be able to hire qualified replacements, or may require an extended time to do so. This could prevent the Fund from achieving its investment objective.

Real Estate Investment Trust (“REIT”) Risk. Investments in REITs will subject the Fund to various risks. The first, real estate industry risk, is the risk that REIT share prices will decline because of adverse developments affecting the real estate industry and real property values. In general, real estate values can be affected by a variety of factors, including supply and demand for properties, the economic health of the country or of different regions, and the strength of specific industries that rent properties. REITs often invest in highly leveraged properties. The second risk is the risk that returns from REITs, which typically are small or medium capitalization stocks, will trail returns from the overall stock market. The third, interest rate risk, is the risk that changes in interest rates may hurt real estate values or make REIT shares less attractive than other income producing investments. REITs are also subject to heavy cash flow dependency, defaults by borrowers and self-liquidation.