VERTEX PHARMACEUTICALS ACQUISITION OF CRINETICS PHARMACEUTICALS July 6, 2026 Presentation intended for the investment community ©2026 Vertex Pharmaceuticals Incorporated ©2026 Vertex Pharmaceuticals Incorporated

Forward-Looking Statements and Non-GAAP Financial Information This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 related to Vertex, Crinetics and the proposed acquisition of Crinetics by Vertex (the “Transaction”) that are subject to risks, uncertainties and other factors. While Vertex believes the forward-looking statements contained in this presentation are accurate, these forward-looking statements represent Vertex’s belief only as of the date of this presentation, and there are a number of risks and uncertainties that could cause actual events or results to differ materially from those expressed or implied by such forward-looking statements. All statements other than statements of historical fact are statements that could be deemed forward-looking statements, including all statements regarding the intent, belief or current expectation of the companies’ and members of their senior management teams. Forward-looking statements are not purely historical and may be accompanied by words such as “anticipates,” “may,” “forecasts,” “expects,” “intends,” “plans,” “potentially,” “believes,” “seeks,” “estimates,” and other words and terms of similar meaning. Such statements may relate to, but are not limited to: the benefits and impact of the Transaction, including the financial benefits and impact to Vertex; anticipated future operating performance and results of Crinetics; Vertex's ability to accelerate launches and pipeline development; the expected timing of the completion of the Transaction and other transactions contemplated by the merger agreement and expectations for the associated integration plans; the ability to complete the Transaction considering the various closing conditions; the potential clinical benefits and commercial potential of PALSONIFY, atumelnant, and Crinetics' other pipeline assets; expectations that the Transaction will contribute to Vertex's revenue growth, including the potential for more than $5 billion in annual revenue, and support Vertex's goal of sustained double digit revenue growth; expectations that the Transaction will become accretive to non-GAAP operating income in 2029; expectations for Vertex's financing of the Transaction, including support by the fully committed bridge financing; and any assumptions underlying any of the foregoing. Forward-looking statements are subject to certain risks, uncertainties, or other factors that are difficult to predict and could cause actual events or results to differ materially from those indicated in any such statements due to a number of risks and uncertainties. Those risks and uncertainties that could cause the actual results to differ from expectations contemplated by forward-looking statements include, among other things: the occurrence of any event or circumstance that could give rise to the right of Vertex or Crinetics to terminate the merger agreement, including circumstances requiring payment of a termination fee; failure to obtain applicable regulatory or Crinetics' stockholder approval in a timely manner or otherwise; the risk that the Transaction may not close in the anticipated timeframe or at all due to one or more of the other closing conditions not being satisfied or waived; the risk that there may be unexpected costs, charges or expenses resulting from the Transaction; risks related to the ability of Vertex and Crinetics to successfully integrate the businesses and the possibility that integration may be more difficult, time consuming or costly than expected; the effects of the Transaction on relationships with employees, other business partners or governmental entities; the difficulty of predicting the timing or outcome of regulatory approvals or actions, if any; the impact of competitive products and pricing; that Vertex may not realize the potential benefits of the Transaction; other business effects, including the effects of industry, economic or political conditions outside of the companies’ control; the risks related to disruption of each company's respective management's time and attention from ongoing business operations due to the Transaction;the risk that any announcements relating to the Transaction could have adverse effects on the market price of Crinetics' and or Vertex's common stock, credit ratings or operating results; and actual or contingent liabilities related to the Transaction. In addition, the product candidates being developed by Crinetics are subject to all the risks inherent in the drug development process, and there can be no assurance that the development of these product candidates will be commercially successful. Forward-looking statements in this communication should be evaluated together with the many uncertainties that affect Vertex’s and Crinetics' businesses, particularly those risks listed under the heading “Risk Factors” and the other cautionary factors discussed in the parties’ periodic reports filed with the SEC, including Vertex’s and Crinetics' annual reports on Form 10-K for the year ended December 31, 2025, and subsequent quarterly reports on Form 10-Q and current reports on Form 8-K, all of which are available on the SEC’s website at www.sec.gov. You should not place undue reliance on these statements. All forward-looking statements are based on information currently available to Vertex, and Vertex disclaims any obligation to update the information contained in this communication as new information becomes available, except as required by law. ©2026 Vertex Pharmaceuticals Incorporated 2

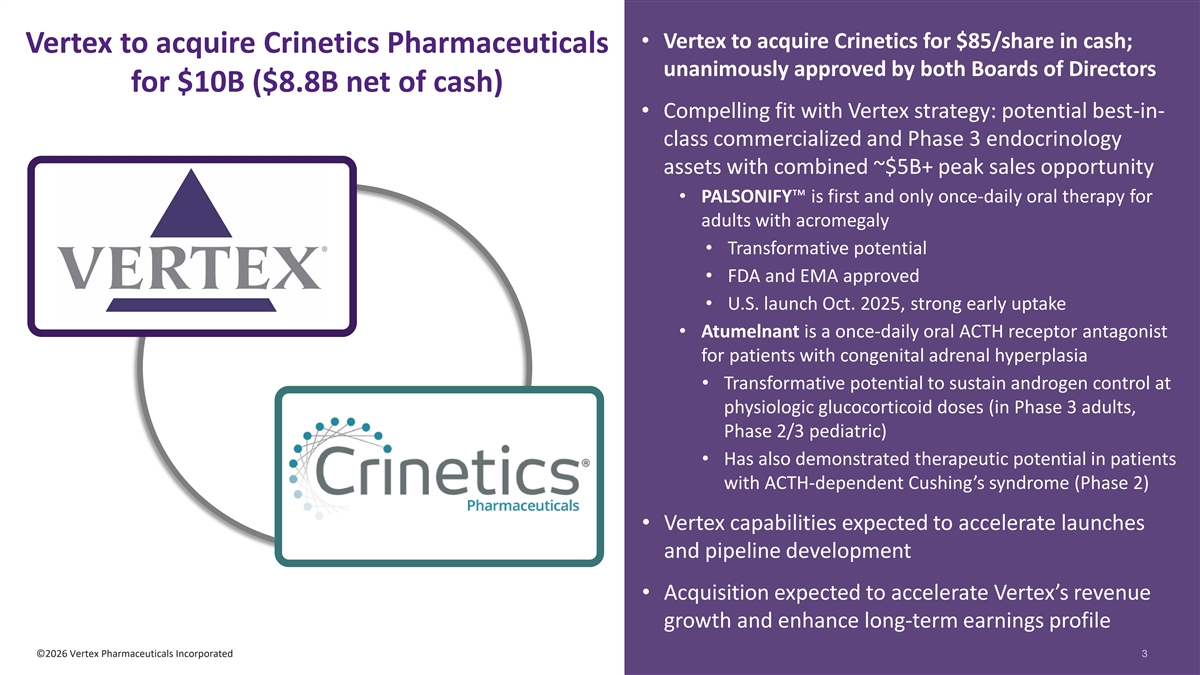

• Vertex to acquire Crinetics for $85/share in cash; Vertex to acquire Crinetics Pharmaceuticals unanimously approved by both Boards of Directors for $10B ($8.8B net of cash) • Compelling fit with Vertex strategy: potential best-in- class commercialized and Phase 3 endocrinology assets with combined ~$5B+ peak sales opportunity • PALSONIFY is first and only once-daily oral therapy for adults with acromegaly • Transformative potential • FDA and EMA approved • U.S. launch Oct. 2025, strong early uptake • Atumelnant is a once-daily oral ACTH receptor antagonist for patients with congenital adrenal hyperplasia • Transformative potential to sustain androgen control at physiologic glucocorticoid doses (in Phase 3 adults, Phase 2/3 pediatric) • Has also demonstrated therapeutic potential in patients with ACTH-dependent Cushing’s syndrome (Phase 2) • Vertex capabilities expected to accelerate launches and pipeline development • Acquisition expected to accelerate Vertex’s revenue growth and enhance long-term earnings profile ©2026 Vertex Pharmaceuticals Incorporated 33

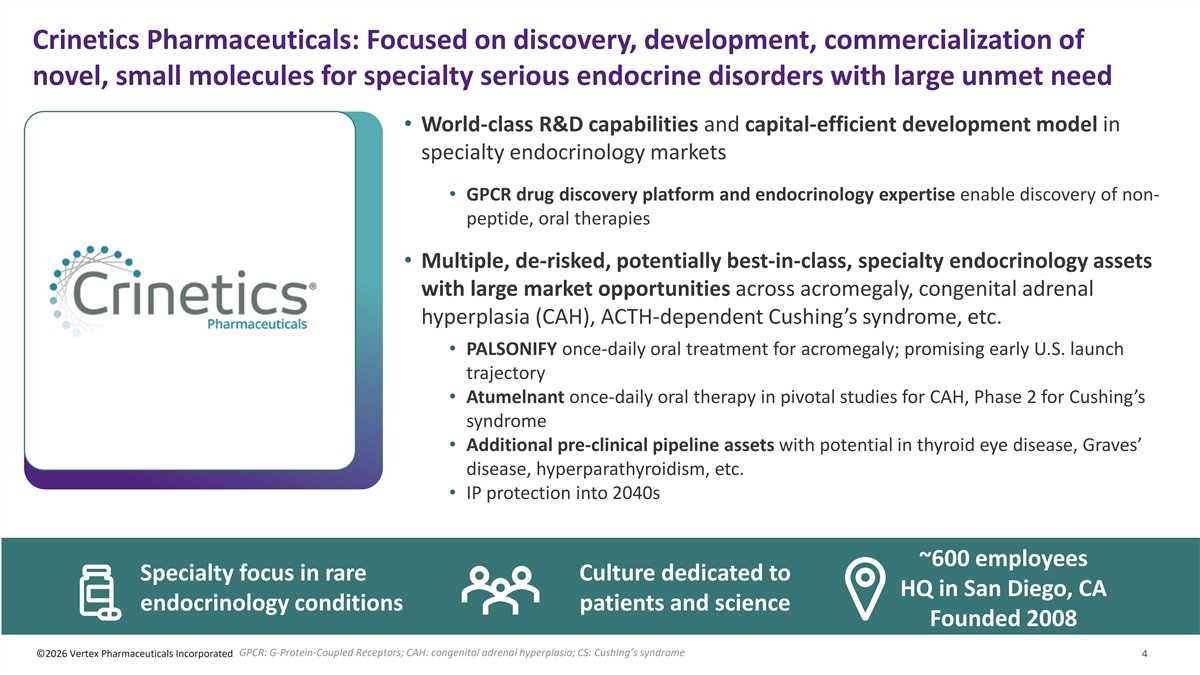

Crinetics Pharmaceuticals: Focused on discovery, development, commercialization of novel, small molecules for specialty serious endocrine disorders with large unmet need • World-class R&D capabilities and capital-efficient development model in specialty endocrinology markets • GPCR drug discovery platform and endocrinology expertise enable discovery of non- peptide, oral therapies • Multiple, de-risked, potentially best-in-class, specialty endocrinology assets with large market opportunities across acromegaly, congenital adrenal hyperplasia (CAH), ACTH-dependent Cushing’s syndrome, etc. • PALSONIFY once-daily oral treatment for acromegaly; promising early U.S. launch trajectory • Atumelnant once-daily oral therapy in pivotal studies for CAH, Phase 2 for Cushing’s syndrome • Additional pre-clinical pipeline assets with potential in thyroid eye disease, Graves’ disease, hyperparathyroidism, etc. • IP protection into 2040s ~600 employees Specialty focus in rare Culture dedicated to HQ in San Diego, CA endocrinology conditions patients and science Founded 2008 GPCR: G-Protein-Coupled Receptors; CAH: congenital adrenal hyperplasia; CS: Cushing’s syndrome ©2026 Vertex Pharmaceuticals Incorporated 4

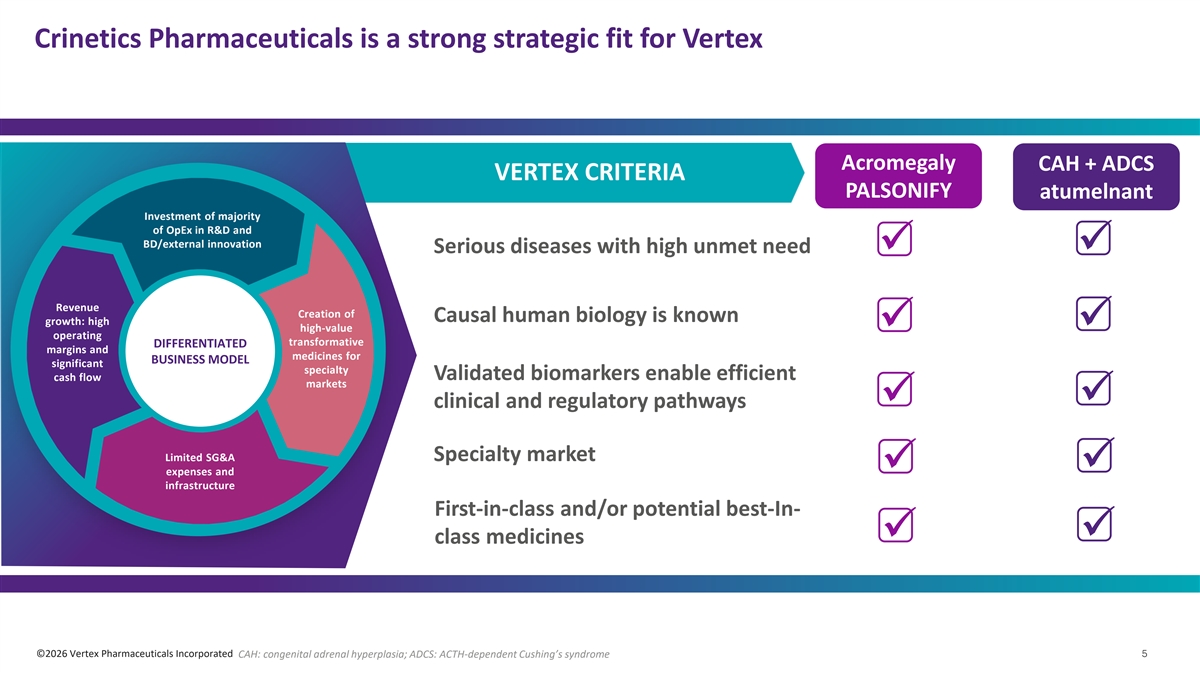

Crinetics Pharmaceuticals is a strong strategic fit for Vertex Acromegaly CAH + ADCS VERTEX CRITERIA PALSONIFY atumelnant Investment of majority of OpEx in R&D and BD/external innovation Serious diseases with high unmet need üü Revenue Creation of Causal human biology is known growth: high high-value ü ü operating transformative DIFFERENTIATED margins and medicines for BUSINESS MODEL significant specialty Validated biomarkers enable efficient cash flow markets ü ü clinical and regulatory pathways Limited SG&A Specialty market ü ü expenses and infrastructure First-in-class and/or potential best-In- üü class medicines ©2026 Vertex Pharmaceuticals Incorporated CAH: congenital adrenal hyperplasia; ADCS: ACTH-dependent Cushing’s syndrome 5

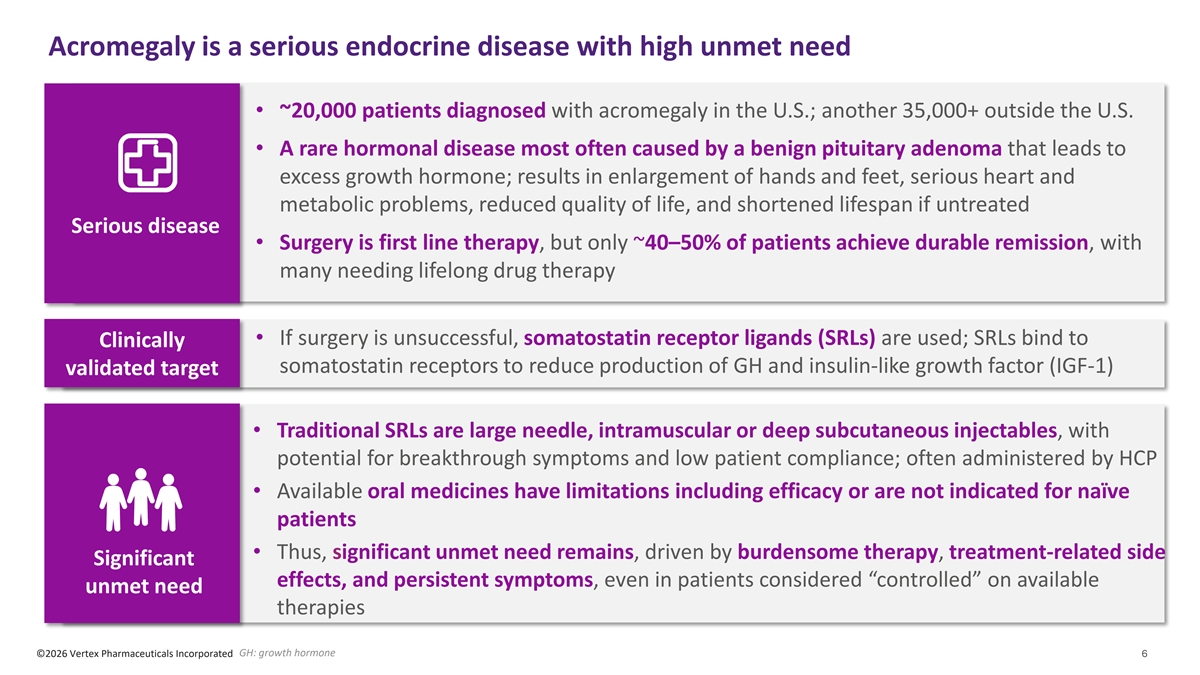

Acromegaly is a serious endocrine disease with high unmet need • ~20,000 patients diagnosed with acromegaly in the U.S.; another 35,000+ outside the U.S. • A rare hormonal disease most often caused by a benign pituitary adenoma that leads to excess growth hormone; results in enlargement of hands and feet, serious heart and metabolic problems, reduced quality of life, and shortened lifespan if untreated Serious disease • Surgery is first line therapy, but only ~40–50% of patients achieve durable remission, with many needing lifelong drug therapy • If surgery is unsuccessful, somatostatin receptor ligands (SRLs) are used; SRLs bind to Clinically somatostatin receptors to reduce production of GH and insulin-like growth factor (IGF-1) validated target • Traditional SRLs are large needle, intramuscular or deep subcutaneous injectables, with potential for breakthrough symptoms and low patient compliance; often administered by HCP • Available oral medicines have limitations including efficacy or are not indicated for naïve patients • Thus, significant unmet need remains, driven by burdensome therapy, treatment-related side Significant effects, and persistent symptoms, even in patients considered “controlled” on available unmet need therapies GH: growth hormone ©2026 Vertex Pharmaceuticals Incorporated 6

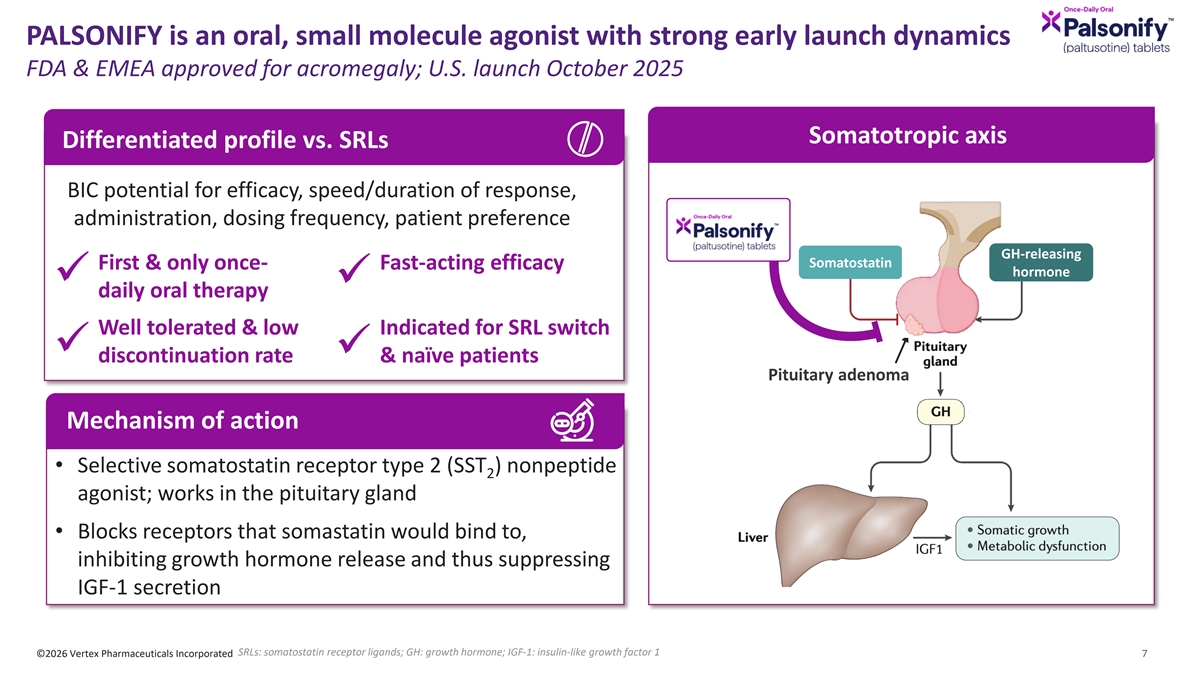

PALSONIFY is an oral, small molecule agonist with strong early launch dynamics FDA & EMEA approved for acromegaly; U.S. launch October 2025 Somatotropic axis Differentiated profile vs. SRLs BIC potential for efficacy, speed/duration of response, administration, dosing frequency, patient preference GH-releasing Somatostatin First & only once- Fast-acting efficacy hormone ü ü daily oral therapy Well tolerated & low Indicated for SRL switch ü ü discontinuation rate & naïve patients Pituitary adenoma Mechanism of action • Selective somatostatin receptor type 2 (SST ) nonpeptide 2 agonist; works in the pituitary gland • Blocks receptors that somastatin would bind to, inhibiting growth hormone release and thus suppressing IGF-1 secretion SRLs: somatostatin receptor ligands; GH: growth hormone; IGF-1: insulin-like growth factor 1 ©2026 Vertex Pharmaceuticals Incorporated 7

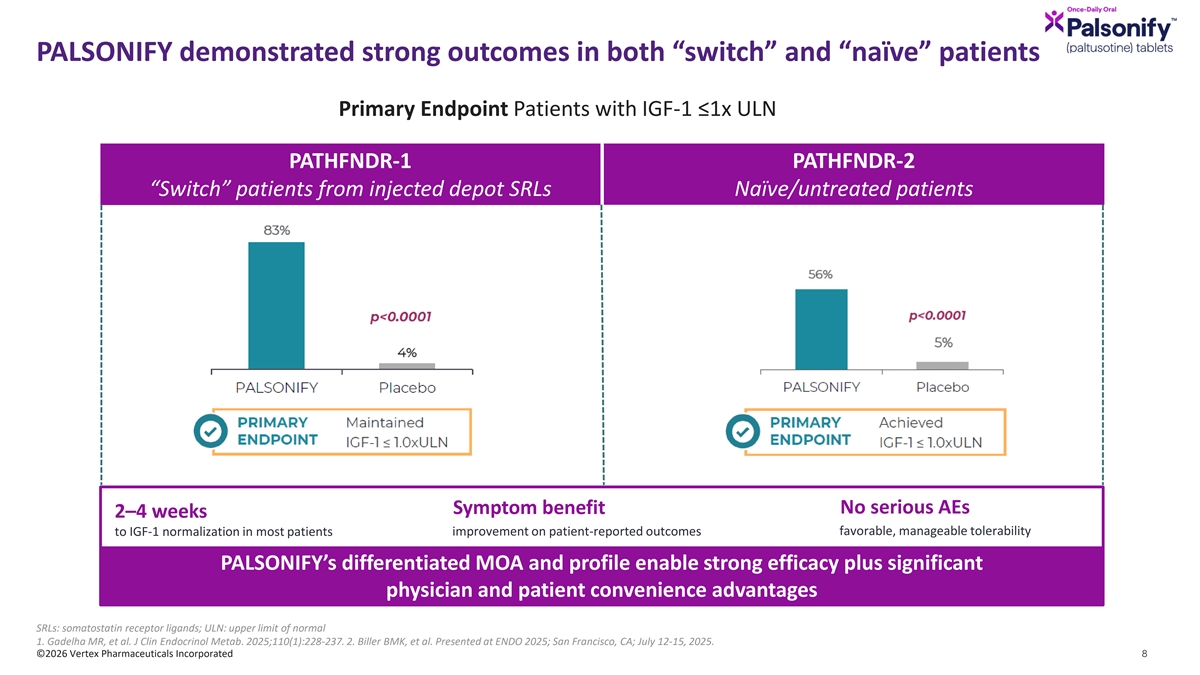

PALSONIFY demonstrated strong outcomes in both “switch” and “naïve” patients Primary Endpoint Patients with IGF-1 ≤1x ULN PATHFNDR-1 PATHFNDR-2 “Switch” patients from injected depot SRLs Naïve/untreated patients Symptom benefit No serious AEs 2–4 weeks favorable, manageable tolerability to IGF-1 normalization in most patients improvement on patient-reported outcomes PALSONIFY’s differentiated MOA and profile enable strong efficacy plus significant physician and patient convenience advantages SRLs: somatostatin receptor ligands; ULN: upper limit of normal 1. Gadelha MR, et al. J Clin Endocrinol Metab. 2025;110(1):228-237. 2. Biller BMK, et al. Presented at ENDO 2025; San Francisco, CA; July 12-15, 2025. ©2026 Vertex Pharmaceuticals Incorporated 8

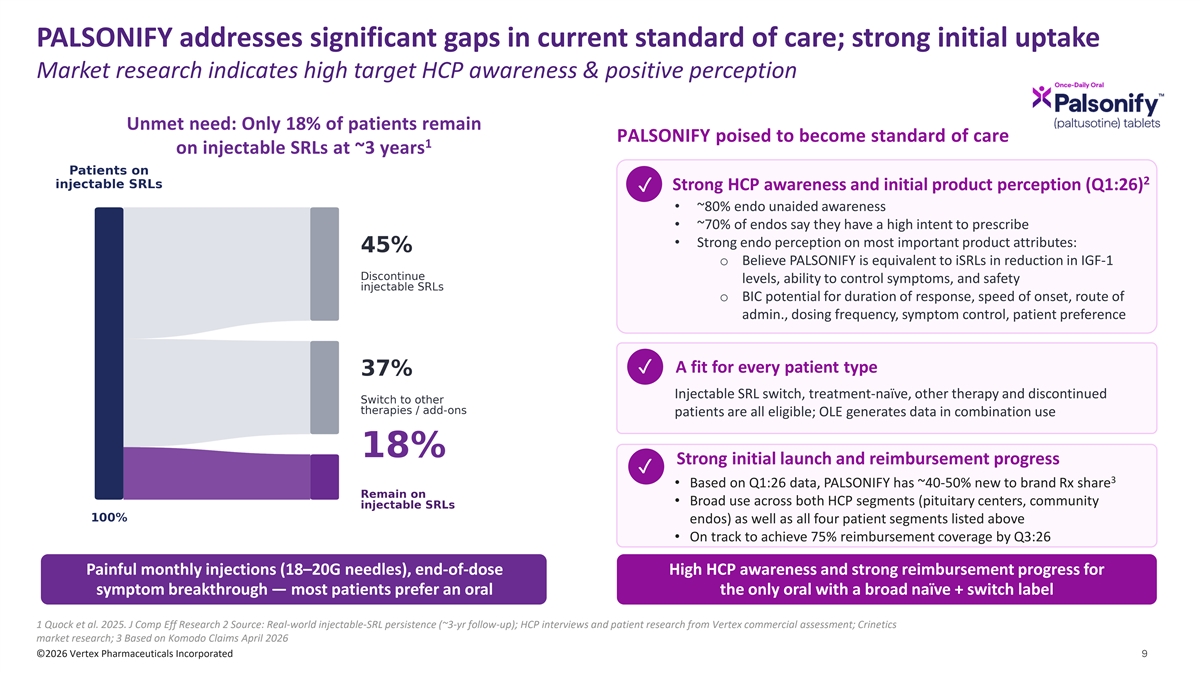

PALSONIFY addresses significant gaps in current standard of care; strong initial uptake Market research indicates high target HCP awareness & positive perception Unmet need: Only 18% of patients remain PALSONIFY poised to become standard of care 1 on injectable SRLs at ~3 years 2 Strong HCP awareness and initial product perception (Q1:26) ✓ • ~80% endo unaided awareness • ~70% of endos say they have a high intent to prescribe • Strong endo perception on most important product attributes: o Believe PALSONIFY is equivalent to iSRLs in reduction in IGF-1 levels, ability to control symptoms, and safety o BIC potential for duration of response, speed of onset, route of admin., dosing frequency, symptom control, patient preference A fit for every patient type ✓ Injectable SRL switch, treatment-naïve, other therapy and discontinued patients are all eligible; OLE generates data in combination use Strong initial launch and reimbursement progress ✓ 3 • Based on Q1:26 data, PALSONIFY has ~40-50% new to brand Rx share • Broad use across both HCP segments (pituitary centers, community endos) as well as all four patient segments listed above • On track to achieve 75% reimbursement coverage by Q3:26 Painful monthly injections (18–20G needles), end-of-dose High HCP awareness and strong reimbursement progress for symptom breakthrough — most patients prefer an oral the only oral with a broad naïve + switch label 1 Quock et al. 2025. J Comp Eff Research 2 Source: Real-world injectable-SRL persistence (~3-yr follow-up); HCP interviews and patient research from Vertex commercial assessment; Crinetics market research; 3 Based on Komodo Claims April 2026 ©2026 Vertex Pharmaceuticals Incorporated 9

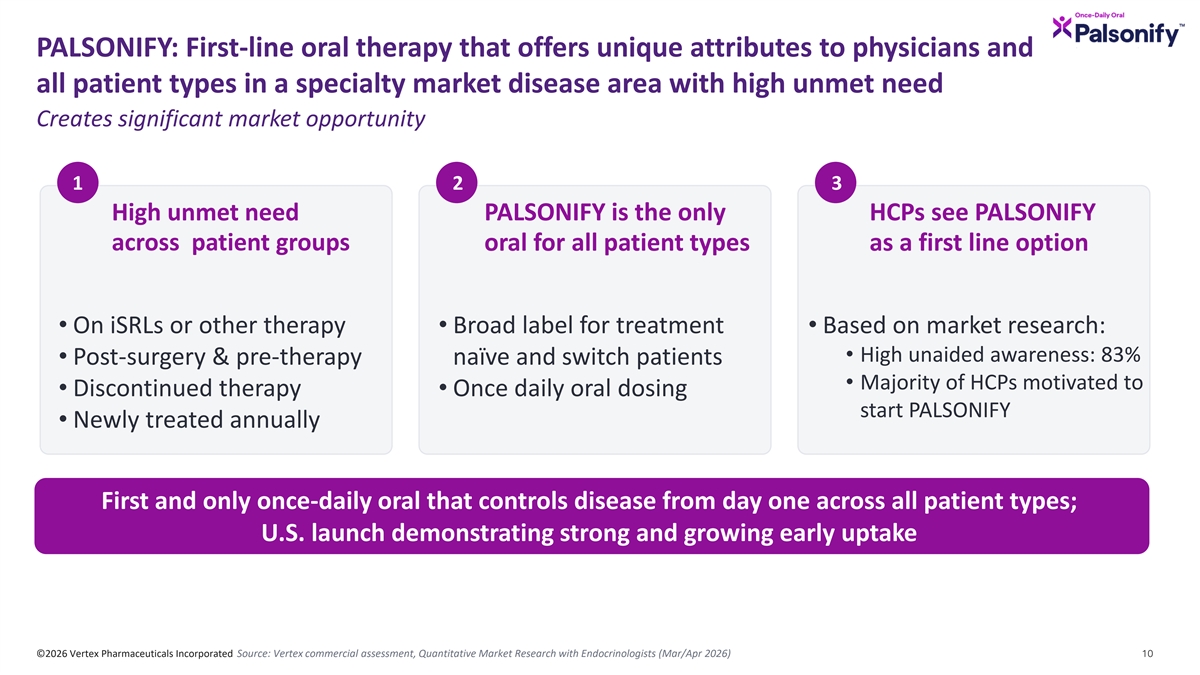

PALSONIFY: First-line oral therapy that offers unique attributes to physicians and all patient types in a specialty market disease area with high unmet need Creates significant market opportunity 1 2 3 High unmet need PALSONIFY is the only HCPs see PALSONIFY across patient groups oral for all patient types as a first line option • On iSRLs or other therapy • Broad label for treatment • Based on market research: • High unaided awareness: 83% • Post-surgery & pre-therapy naïve and switch patients • Majority of HCPs motivated to • Discontinued therapy • Once daily oral dosing start PALSONIFY • Newly treated annually First and only once-daily oral that controls disease from day one across all patient types; U.S. launch demonstrating strong and growing early uptake ©2026 Vertex Pharmaceuticals Incorporated Source: Vertex commercial assessment, Quantitative Market Research with Endocrinologists (Mar/Apr 2026) 10

CAH is a rare genetic endocrine disease with high unmet need • ~17,000 patients diagnosed with classic CAH in the U.S. (~12,000 adults/~5,000 pediatrics); another 15,000+ outside the U.S • Due to lack of adrenal enzyme activity, patients lack the ability to produce cortisol and accumulate high levels of androgens • Patients need physiologic doses of glucocorticoids (GCs) to replace cortisol but are often administered supraphysiologic doses to reduce androgen levels Serious disease • Patients suffer from significant disease morbidity: • 1) high androgen levels can lead to complications such as short stature, acne, hirsutism, early puberty, infertility, and long-term physical and emotional burden • 2) high dose GCs can lead to heart disease, obesity, diabetes, bone loss, other persistent QoL issues • Classic CAH is a group of autosomal recessive genetic diseases that result in a deficiency in the adrenal Well understood enzyme 21-hydroxylase (21-OH)* causal biology • No medicine currently approved can durably normalize androgens and allow patients to be maintained on physiologic glucocorticoid doses • Recent market entrant suppresses upstream at the pituitary gland level, provides incomplete blockade of the pathway, and doesn’t normalize A4 without supplementation of high dose glucocorticoids Significant • Atumelnant suppresses at the adrenal cortex and thus holds the promise for concurrent and sustained unmet need control of androgen A4 and low physiologic doses of glucocorticoids ©2026 Vertex Pharmaceuticals Incorporated *In ~95% of cases 11

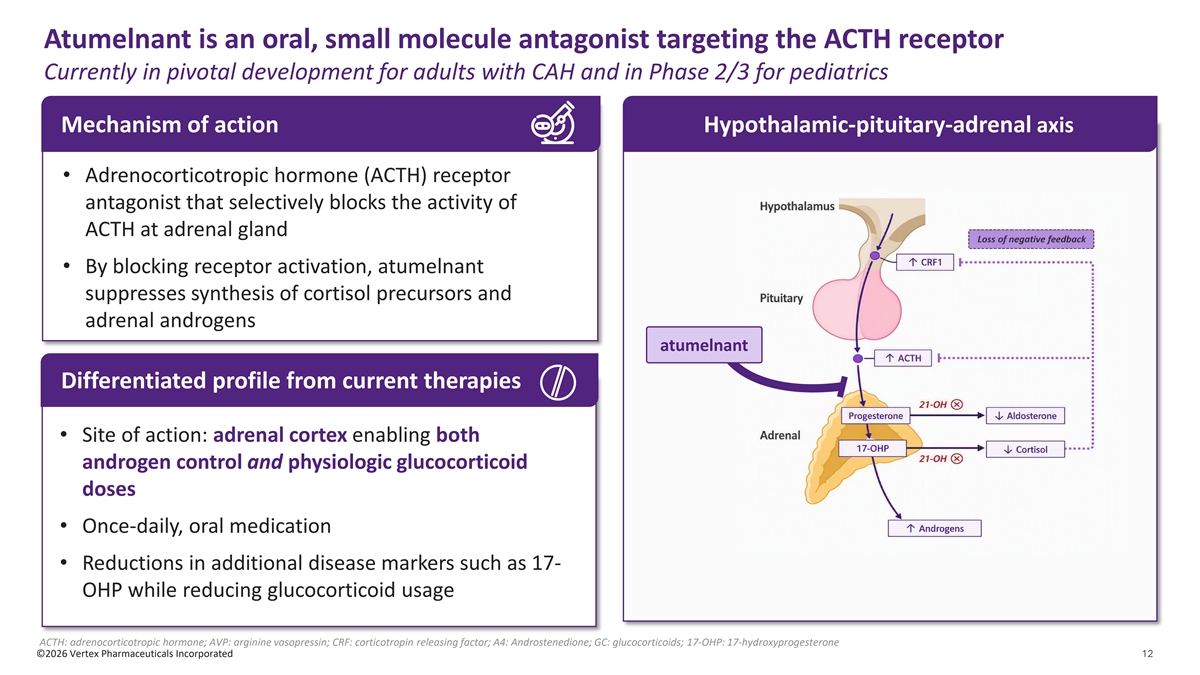

Atumelnant is an oral, small molecule antagonist targeting the ACTH receptor Currently in pivotal development for adults with CAH and in Phase 2/3 for pediatrics Mechanism of action Hypothalamic-pituitary-adrenal axis • Adrenocorticotropic hormone (ACTH) receptor antagonist that selectively blocks the activity of ACTH at adrenal gland • By blocking receptor activation, atumelnant suppresses synthesis of cortisol precursors and adrenal androgens atumelnant Differentiated profile from current therapies • Site of action: adrenal cortex enabling both androgen control and physiologic glucocorticoid doses • Once-daily, oral medication • Reductions in additional disease markers such as 17- OHP while reducing glucocorticoid usage ACTH: adrenocorticotropic hormone; AVP: arginine vasopressin; CRF: corticotropin releasing factor; A4: Androstenedione; GC: glucocorticoids; 17-OHP: 17-hydroxyprogesterone ©2026 Vertex Pharmaceuticals Incorporated 12

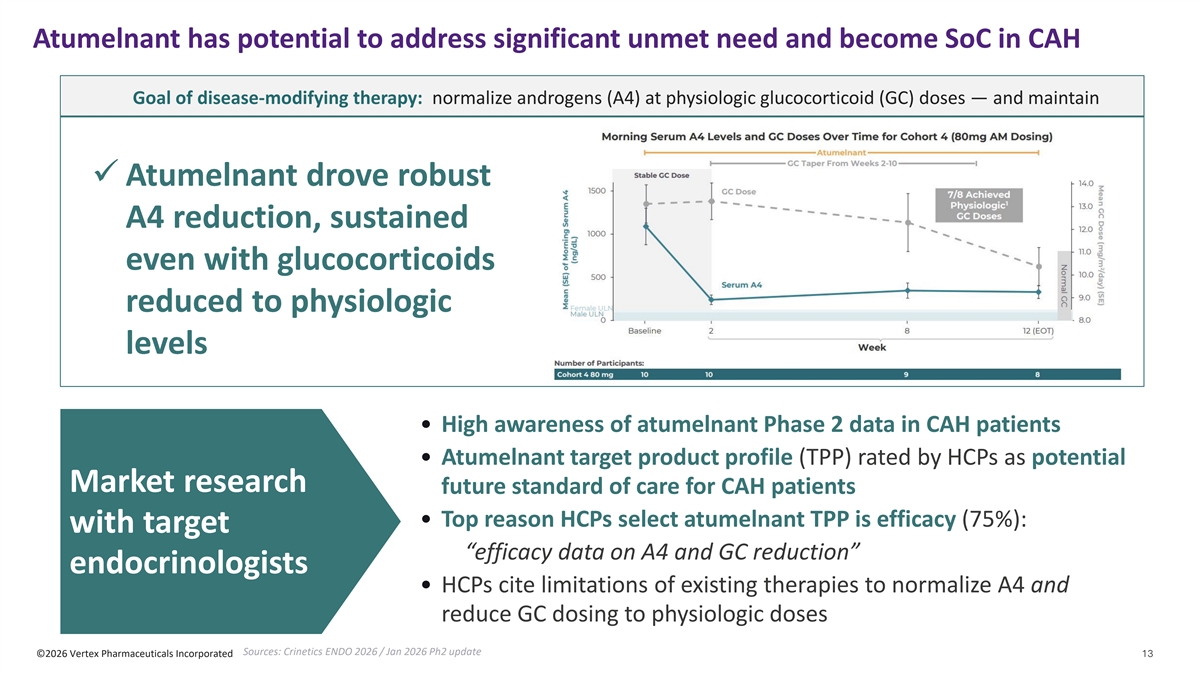

Atumelnant has potential to address significant unmet need and become SoC in CAH Goal of disease-modifying therapy: normalize androgens (A4) at physiologic glucocorticoid (GC) doses — and maintain ü Atumelnant drove robust A4 reduction, sustained even with glucocorticoids reduced to physiologic levels • High awareness of atumelnant Phase 2 data in CAH patients • Atumelnant target product profile (TPP) rated by HCPs as potential Market research future standard of care for CAH patients • Top reason HCPs select atumelnant TPP is efficacy (75%): with target “efficacy data on A4 and GC reduction” endocrinologists • HCPs cite limitations of existing therapies to normalize A4 and reduce GC dosing to physiologic doses Sources: Crinetics ENDO 2026 / Jan 2026 Ph2 update ©2026 Vertex Pharmaceuticals Incorporated 13

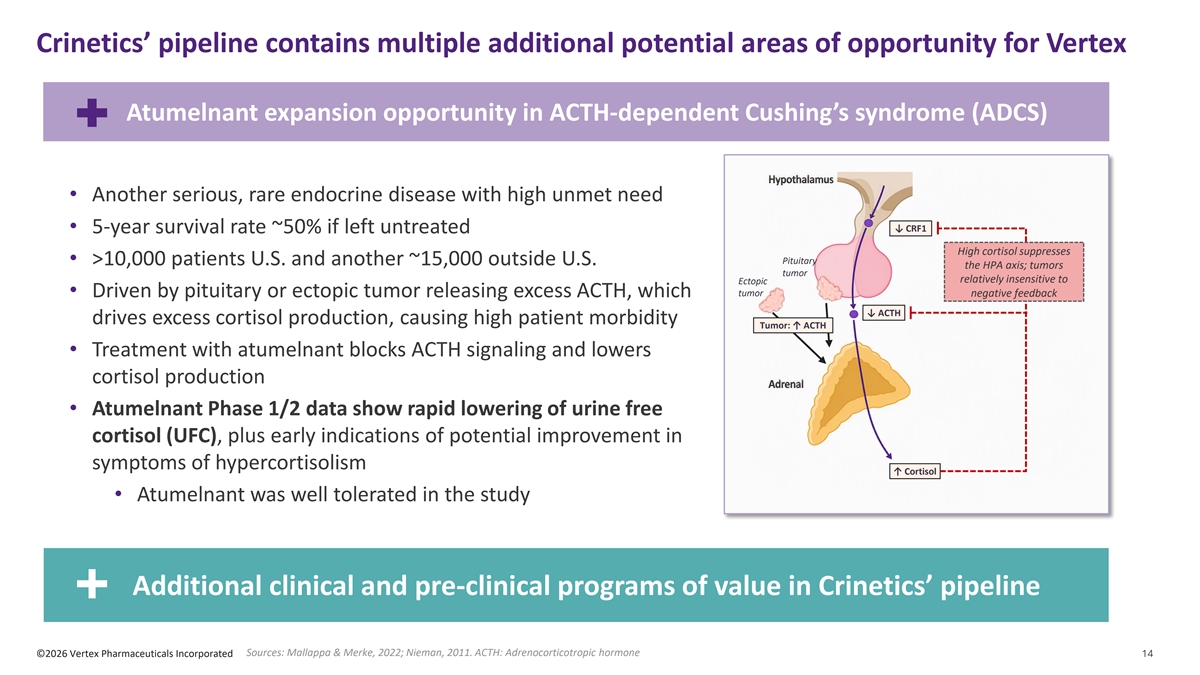

Crinetics’ pipeline contains multiple additional potential areas of opportunity for Vertex Atumelnant expansion opportunity in ACTH-dependent Cushing’s syndrome (ADCS) ADCS Pathophysiology • Another serious, rare endocrine disease with high unmet need ↓ CRF1 • 5-year survival rate ~50% if left untreated High cortisol suppresses Pituitary • >10,000 patients U.S. and another ~15,000 outside U.S. the HPA axis; tumors tumor relatively insensitive to Ectopic tumor • Driven by pituitary or ectopic tumor releasing excess ACTH, which negative feedback ↓ ACTH drives excess cortisol production, causing high patient morbidity Tumor: ↑ ACTH • Treatment with atumelnant blocks ACTH signaling and lowers cortisol production • Atumelnant Phase 1/2 data show rapid lowering of urine free cortisol (UFC), plus early indications of potential improvement in symptoms of hypercortisolism ↑ Cortisol • Atumelnant was well tolerated in the study Additional clinical and pre-clinical programs of value in Crinetics’ pipeline Sources: Mallappa & Merke, 2022; Nieman, 2011. ACTH: Adrenocorticotropic hormone ©2026 Vertex Pharmaceuticals Incorporated 14

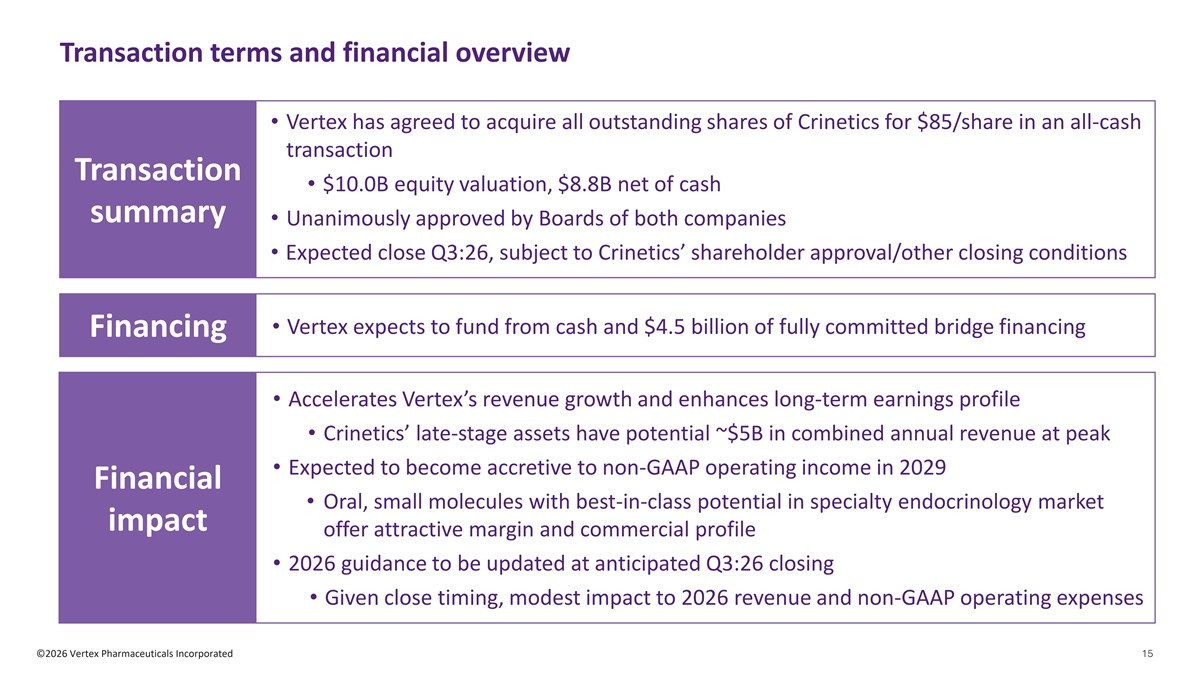

Transaction terms and financial overview • Vertex has agreed to acquire all outstanding shares of Crinetics for $85/share in an all-cash transaction Transaction • $10.0B equity valuation, $8.8B net of cash summary • Unanimously approved by Boards of both companies • Expected close Q3:26, subject to Crinetics’ shareholder approval/other closing conditions • Vertex expects to fund from cash and $4.5 billion of fully committed bridge financing Financing • Accelerates Vertex’s revenue growth and enhances long-term earnings profile • Crinetics’ late-stage assets have potential ~$5B in combined annual revenue at peak • Expected to become accretive to non-GAAP operating income in 2029 Financial • Oral, small molecules with best-in-class potential in specialty endocrinology market impact offer attractive margin and commercial profile • 2026 guidance to be updated at anticipated Q3:26 closing • Given close timing, modest impact to 2026 revenue and non-GAAP operating expenses ©2026 Vertex Pharmaceuticals Incorporated 15

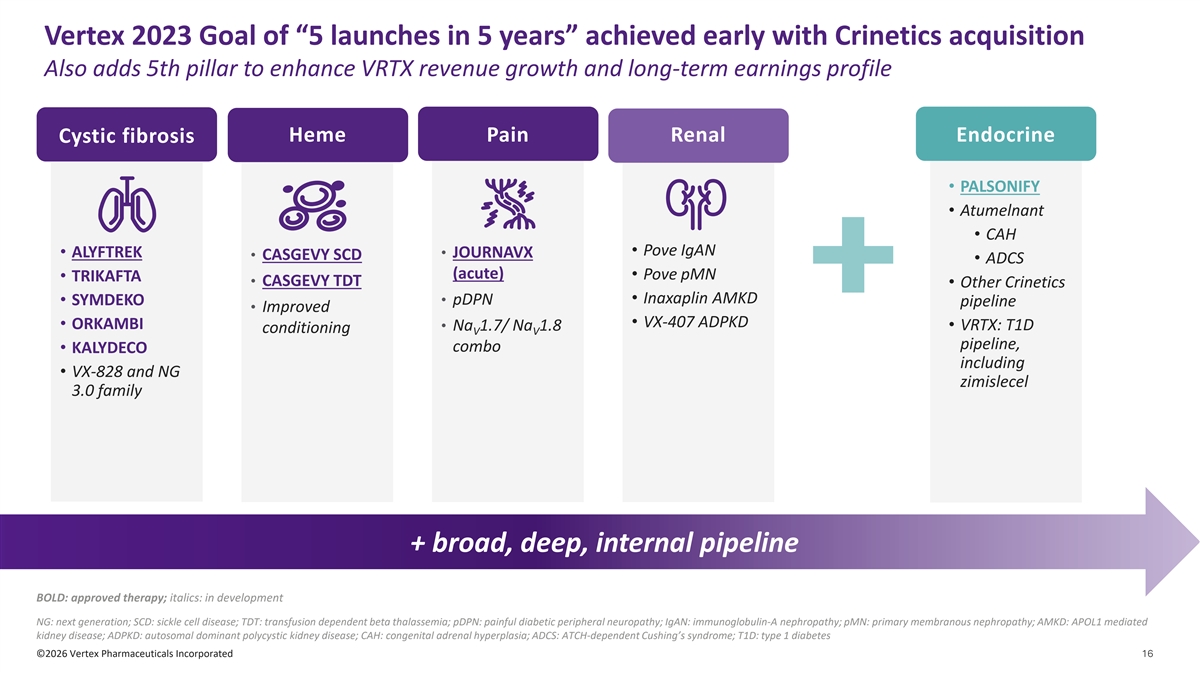

Vertex 2023 Goal of “5 launches in 5 years” achieved early with Crinetics acquisition Also adds 5th pillar to enhance VRTX revenue growth and long-term earnings profile Heme Pain Renal Endocrine Cystic fibrosis • PALSONIFY • Atumelnant • CAH • Pove IgAN • ALYFTREK • JOURNAVX • CASGEVY SCD • ADCS (acute) • Pove pMN • TRIKAFTA • CASGEVY TDT • Other Crinetics • Inaxaplin AMKD • SYMDEKO • pDPN pipeline • Improved • VX-407 ADPKD • ORKAMBI • VRTX: T1D • Na 1.7/ Na 1.8 conditioning V V pipeline, combo • KALYDECO including • VX-828 and NG zimislecel 3.0 family + broad, deep, internal pipeline BOLD: approved therapy; italics: in development NG: next generation; SCD: sickle cell disease; TDT: transfusion dependent beta thalassemia; pDPN: painful diabetic peripheral neuropathy; IgAN: immunoglobulin-A nephropathy; pMN: primary membranous nephropathy; AMKD: APOL1 mediated kidney disease; ADPKD: autosomal dominant polycystic kidney disease; CAH: congenital adrenal hyperplasia; ADCS: ATCH-dependent Cushing’s syndrome; T1D: type 1 diabetes ©2026 Vertex Pharmaceuticals Incorporated 16

• Vertex to acquire Crinetics for $85/share in cash; Vertex to acquire Crinetics Pharmaceuticals unanimously approved by both Boards of Directors for $10B ($8.8B net of cash) • Compelling fit with Vertex strategy: potential best-in- class commercialized and Phase 3 endocrinology assets with combined ~$5B+ peak sales opportunity • PALSONIFY is first and only once-daily oral therapy for adults with acromegaly • Transformative potential • FDA and EMA approved • U.S. launch Oct. 2025, strong early uptake • Atumelnant is a once-daily oral ACTH receptor antagonist for patients with congenital adrenal hyperplasia • Transformative potential to sustain androgen control at physiologic glucocorticoid doses (in Phase 3 adults, Phase 2/3 pediatric) • Has also demonstrated therapeutic potential in patients with ACTH-dependent Cushing’s syndrome (Phase 2) • Vertex capabilities expected to accelerate launches and pipeline development • Acquisition expected to accelerate Vertex’s revenue growth and enhance long-term earnings profile ©2026 Vertex Pharmaceuticals Incorporated 17 17