TASEKO MINES LIMITED

Management's Discussion and Analysis

This management's discussion and analysis ("MD&A") is intended to help the reader understand Taseko Mines Limited ("Taseko", "we", "our" or the "Company"), our operations, financial performance, and current and future business environment. This MD&A is intended to supplement and complement the consolidated financial statements and notes thereto, prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board ("IFRS Accounting Standards") for the year ended December 31, 2025 (the "Financial Statements"). You are encouraged to review the Financial Statements in conjunction with your review of this MD&A and the Company's other public filings, which are available on the Canadian Securities Administrators' website at www.sedarplus.ca ("SEDAR+") and on the Electronic Data Gathering, Analysis and Retrieval ("EDGAR") system on the United States Securities and Exchange Commission's ("SEC") website at www.sec.gov.

This MD&A is prepared as of February 18, 2026. All dollar figures stated herein are expressed in thousands of Canadian dollars ("$", "Cdn$"), unless otherwise indicated. Included throughout this MD&A are references to non-GAAP performance measures which are denoted with an asterisk. An explanation of these non-GAAP measures and their calculations are provided on page 38.

Cautionary Statement on Forward-Looking Information

This discussion includes certain statements that may be deemed "forward-looking statements". All statements in this discussion, other than statements of historical facts, that address future production, reserve potential, exploration drilling, exploration activities, and events or developments that the Company expects are forward- looking statements. Although we believe the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those in the forward-looking statements. Factors that could cause actual results to differ materially from those in forward-looking statements include market prices, exploitation and exploration successes, continued availability of capital and financing, and general economic, market or business conditions. Investors are cautioned that any such statements are not guarantees of future performance and actual results or developments may differ materially from those projected in the forward-looking statements. All of the forward-looking statements made in this MD&A are qualified by these cautionary statements. We disclaim any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise, except to the extent required by applicable law. Further information concerning risks and uncertainties associated with these forward-looking statements and our business may be found in the Company's other public filings with the SEC and Canadian provincial securities regulatory authorities.

TASEKO MINES LIMITED

Management's Discussion and Analysis

Table of Contents

TASEKO MINES LIMITED

Management's Discussion and Analysis

Overview

Taseko is a copper-focused mining company that seeks to create long-term shareholder value by acquiring, developing and operating large tonnage mineral deposits in stable jurisdictions that are capable of supporting a mine for decades. The Company's principal assets are the wholly-owned Gibraltar mine ("Gibraltar"), which is located in central British Columbia ("BC") and is one of the largest copper mines in North America, and Florence Copper ("Florence" or "Florence Copper"), which is located in Arizona and has recently commenced operations. Taseko also owns the Yellowhead copper, New Prosperity copper-gold, and Aley niobium projects in British Columbia.

Highlights

| Operating data | Three months ended December 31, |

Year ended December 31, |

|||||||||||||||||

| (Gibraltar - 100% basis) | 2025 | 2024 | Change | 2025 | 2024 | Change | |||||||||||||

| Tons mined (millions) | 28.0 | 24.0 | 4.0 | 110.9 | 88.3 | 22.6 | |||||||||||||

| Tons milled (millions) | 7.2 | 8.3 | (1.1 | ) | 30.6 | 29.3 | 1.3 | ||||||||||||

| Production (million pounds Cu) | 30.7 | 28.6 | 2.1 | 98.1 | 105.6 | (7.5 | ) | ||||||||||||

| Sales (million pounds Cu) | 31.6 | 27.4 | 4.2 | 98.7 | 108.0 | (9.3 | ) | ||||||||||||

| Financial data | Three months ended December 31, |

Year ended December 31, |

|||||||||||||||||

| (Cdn$ in thousands, except per share amounts) | 2025 | 2024 | Change | 2025 | 20241 | Change | |||||||||||||

| Revenues | 243,767 | 167,799 | 75,968 | 672,904 | 608,093 | 64,811 | |||||||||||||

| Cash flows from operations | 101,234 | 73,292 | 27,942 | 219,558 | 232,615 | (13,057 | ) | ||||||||||||

| Net income (loss) | 4,454 | (21,207 | ) | 25,661 | (30,076 | ) | (13,444 | ) | (16,632 | ) | |||||||||

| Per share - Basic ("EPS") | 0.01 | (0.07 | ) | 0.08 | (0.09 | ) | (0.05 | ) | (0.04 | ) | |||||||||

| Earnings from mining operations before depletion, amortization and non-recurring items* | 124,055 | 59,405 | 64,650 | 250,664 | 243,646 | 7,018 | |||||||||||||

| Adjusted EBITDA* | 116,464 | 55,602 | 60,862 | 230,424 | 223,991 | 6,433 | |||||||||||||

| Adjusted net income* | 41,525 | 10,468 | 31,057 | 27,141 | 56,927 | (29,786 | ) | ||||||||||||

| Per share - Basic ("Adjusted EPS")* | 0.11 | 0.03 | 0.08 | 0.07 | 0.19 | (0.12 | ) | ||||||||||||

1 Amounts for the year ended December 31, 2024 reflect the impact from the March 25, 2024 acquisition of Cariboo from Dowa and Furukawa, which increased the Company's effective interest in the Gibraltar mine from 87.5% to 100%.

TASEKO MINES LIMITED

Management's Discussion and Analysis

2025 Annual Review

• Earnings from mining operations before depletion, amortization and non-recurring items* was $250.7 million, Adjusted EBITDA* was $230.4 million and cash flow from operations was $219.6 million;

• Net loss was $30.1 million ($0.09 loss per share) and Adjusted net income* was $27.1 million ($0.07 adjusted earnings per share);

• Gibraltar produced 98.1 million pounds of copper at a total operating cost (C1)* of US$2.66 per pound of copper produced. Copper head grades averaged 0.22% and recoveries averaged 73%;

• Copper production included 2.2 million pounds of copper cathode from the Gibraltar SX/EW plant which was restarted in May;

• Gibraltar sold 98.7 million pounds of copper at an average realized copper price of US$4.61 per pound contributing to revenues of $672.9 million for Taseko;

• Construction activities at Florence Copper continued throughout 2025, completing in the fourth quarter on time and largely on budget at US$275 million. During the 24-month construction period, there were approximately 1,000,000 project hours worked with no lost time injuries and no reportable incidents;

• In July, the Company filed an updated technical report for the Yellowhead project highlighting a 25 year mine life with an average annual copper production of 178 million pounds at a total cash cost (C1) of US$1.90 per pound, and a net present value of $2.0 billion (8% discount rate, US$4.25 per pound copper and US$2,400 per ounce gold). The Company also announced that it had formally commenced the Environmental Assessment process for the Yellowhead project; and

• In June, Taseko, Tŝilhqot'in Nation and the Province of BC reached an agreement concerning the New Prosperity project. Taseko received a payment of $75 million from the Province of BC upon closing of the transaction.

TASEKO MINES LIMITED

Management's Discussion and Analysis

Fourth Quarter Review

• Earnings from mining operations before depletion, amortization and non-recurring items* was $124.1 million, Adjusted EBITDA* was $116.5 million and cash flow from operations was $101.2 million;

• Net income was $4.5 million ($0.01 earnings per share) and Adjusted net income* was $41.5 million ($0.11 adjusted earnings per share);

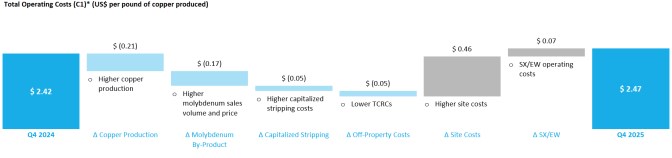

• Gibraltar produced 30.7 million pounds of copper, including 0.9 million pounds of copper cathode, at a total operating cost (C1)* of US$2.47 per pound of copper produced. Copper head grades averaged 0.26% and recoveries averaged 81%;

• Gibraltar sold 31.6 million pounds of copper at an average realized copper price of US$5.13 per pound contributing to revenues of $243.8 million for Taseko;

• In October 2025, the Company closed an equity financing (the "Offering") with a syndicate of underwriters pursuant to which the Company issued 42.7 million common shares at a price of US$4.05 per share for gross proceeds of US$172.8 million. Proceeds from the Offering were partially used to repay outstanding debt under the Company's revolving credit facility, with the remainder available for general corporate purposes; and

• The Company received the final approvals required to commence wellfield injection and recovery operations at Florence Copper in October. Commercial wellfield acidification commenced in early November, and by early December mining solutions were circulating in all the new production wells within the commercial wellfield. Production of copper cathode commenced mid-February with the startup of the electrowinning circuit, and the Florence Copper SX/EW plant is now fully operational with copper being plated.

TASEKO MINES LIMITED

Management's Discussion and Analysis

Review of Operations

Gibraltar

| Operating data (100% basis) | Q4 2025 | Q3 2025 | Q2 2025 | Q1 2025 | Q4 2024 | 2025 | 2024 | ||||||||||||||||

| Tons mined (millions) | 28.0 | 29.3 | 30.4 | 23.2 | 24.0 | 110.9 | 88.3 | ||||||||||||||||

| Tons milled (millions) | 7.2 | 7.8 | 7.7 | 7.9 | 8.3 | 30.6 | 29.3 | ||||||||||||||||

| Strip ratio | 2.2 | 1.5 | 2.3 | 4.6 | 1.9 | 2.3 | 1.6 | ||||||||||||||||

| Site operating cost per ton milled* | $ | 16.61 | $ | 14.98 | $ | 11.23 | $ | 8.73 | $ | 12.18 | $ | 12.81 | $ | 12.93 | |||||||||

| Copper concentrate | |||||||||||||||||||||||

| Head grade (%) | 0.26 | 0.22 | 0.20 | 0.19 | 0.22 | 0.22 | 0.23 | ||||||||||||||||

| Recovery (%) | 80.9 | 77.2 | 63.2 | 67.5 | 78.2 | 72.8 | 78.5 | ||||||||||||||||

| Production (million pounds Cu) | 29.8 | 26.7 | 19.4 | 20.0 | 28.6 | 95.9 | 105.6 | ||||||||||||||||

| Sales (million pounds Cu) | 30.8 | 25.4 | 19.0 | 21.8 | 27.4 | 97.0 | 108.0 | ||||||||||||||||

| Inventory (million pounds Cu) | 2.9 | 4.0 | 2.7 | 2.3 | 4.1 | 2.9 | 4.1 | ||||||||||||||||

| Copper cathode | |||||||||||||||||||||||

| Production (thousand pounds Cu) | 919 | 895 | 395 | - | - | 2,209 | - | ||||||||||||||||

| Sales (thousand pounds Cu) | 783 | 905 | - | - | - | 1,688 | - | ||||||||||||||||

| Molybdenum concentrate | |||||||||||||||||||||||

| Production (thousand pounds Mo) | 830 | 558 | 180 | 336 | 578 | 1,902 | 1,432 | ||||||||||||||||

| Sales (thousand pounds Mo) | 953 | 421 | 178 | 364 | 607 | 1,916 | 1,434 | ||||||||||||||||

| Per unit data (US$ per Cu pound produced)1 | |||||||||||||||||||||||

| Site operating cost* | $ | 2.80 | $ | 3.09 | $ | 3.15 | $ | 2.41 | $ | 2.52 | $ | 2.86 | $ | 2.61 | |||||||||

| By-product credit* | (0.59 | ) | (0.39 | ) | (0.19 | ) | (0.33 | ) | (0.42 | ) | (0.40 | ) | (0.28 | ) | |||||||||

| Site operating cost, net of by-product credit* | 2.21 | 2.70 | 2.96 | 2.08 | 2.10 | 2.46 | 2.33 | ||||||||||||||||

| Off-property cost* | 0.26 | 0.17 | 0.18 | 0.18 | 0.32 | 0.20 | 0.33 | ||||||||||||||||

| Total operating cost (C1)* | $ | 2.47 | $ | 2.87 | $ | 3.14 | $ | 2.26 | $ | 2.42 | $ | 2.66 | $ | 2.66 |

1 Copper pounds produced includes copper in concentrate and copper cathode.

TASEKO MINES LIMITED

Management's Discussion and Analysis

Operations Analysis

Annual Results

Gibraltar mining operations were focused in the Connector pit during 2025, which is the primary source of mill feed for the next few years. Mining rates increased approximately 25% year-over-year to 110.9 million tons in 2025, compared to 88.3 million tons in 2024, with the higher mining rates attributable to increased operating hours and improved productivity of the haul truck fleet.

Copper production was 98.1 million pounds in 2025, including 2.2 million pounds of copper cathode from the Gibraltar solvent extraction and electrowinning ("SX/EW") plant that was restarted in May. Mill throughput was 30.6 million tons for the year with average copper head grades of 0.22% and copper recoveries of 73%, which steadily improved throughout the year as mining advanced beyond the oxidized and supergene zones encountered in the initial phases of Connector pit. Copper production in the second half of the year was a notable improvement over the first half of the year attributable to higher grades and better quality ore.

Total site costs* were $473.2 million (including capitalized stripping of $80.9 million) in 2025, compared to $400.2 million (including capitalized stripping of $32.5 million) in 2024. The increase in total site costs is a result of higher mining rates and costs to restart and operate the Gibraltar SX/EW plant, which processes stockpiled oxide ore to produce copper cathode.

Molybdenum production increased to 1.9 million pounds in 2025 from 1.4 million pounds in 2024 primarily due to higher molybdenum grades and improved recoveries. At an average molybdenum price of US$22.16 per pound for the year, molybdenum contributed to a by-product credit of US$0.40 per pound of copper produced.

Off-property costs were US$0.20 per pound of copper produced in 2025, compared to US$0.33 per pound of copper produced in 2024, and reflect Gibraltar's favorable offtake agreements with average treatment and refining charges ("TCRC") of around $nil for the year.

Total operating costs (C1)* were US$2.66 per pound of copper produced in 2025, consistent with US$2.66 per pound of copper produced in 2024. The impacts of higher capitalized stripping, lower TCRCs, and higher molybdenum sales were offset by higher site operating costs due to higher mining rates, lower copper production, and the recommissioning and initial operation of the Gibraltar SX/EW plant.

Fourth Quarter Results

Mining continues to advance deeper into the Connector pit and benefit from improved copper grades and ore quality. A total of 28.0 million tons were mined in the fourth quarter, comparable to the previous quarter. The average strip ratio was 2.2 in the fourth quarter, and in line with the life-of-mine average.

TASEKO MINES LIMITED

Management's Discussion and Analysis

Mill throughput was 7.2 million tons in the fourth quarter and was impacted by unanticipated mill downtime due to unscheduled maintenance activities and a serious accident which resulted in a temporary site wide shutdown in November.

Copper production increased to 30.7 million pounds (including 0.9 million pounds of copper cathode) in the fourth quarter, compared to 27.6 million pounds (including 0.9 million pounds of copper cathode) in the previous quarter, driven by higher copper head grades averaging 0.26% and copper recoveries averaging 81%.

Total site costs* were $125.6 million (including capitalized stripping of $6.0 million) in the fourth quarter, comparable to the previous quarter.

Molybdenum production increased to 830 thousand pounds in the fourth quarter and reflects the higher molybdenum grades realized in Connector pit ore. At an average molybdenum price of US$22.89 per pound for the quarter, molybdenum provided a by-product credit of US$0.59 per pound of copper produced.

Off-property costs were US$0.26 per pound of copper produced and were higher than previous quarters due to the timing of shipments with higher TCRC terms.

Total operating costs (C1)* were US$2.47 per pound of copper produced for the fourth quarter, lower than the prior quarter and comparable to the prior year comparative quarter. Increased site operating costs from higher mining rates were offset by higher copper production, improved molybdenum by-product credits, higher capitalized stripping costs, and lower TCRCs.

Gibraltar Outlook

Mining activity over the last 18 months has been focused in the Connector Pit, which was the primary source of mill feed in 2025, and will continue to be the primary source of ore for the next three years (2026 through 2028). In recent months, head grades in the Connector Pit have been 5% to 10% lower than originally expected due to the impact of small higher grade zones that have not been realized through mining to date. In addition, oxide copper and metallurgically challenging supergene ore has been more abundant in the Connector Pit than previously estimated, and recoveries in 2026 are expected to average between 75% to 80% (similar to the second half of 2025). On a positive note, the additional oxide ore mined from Connector Pit has been stacked on leach pads and will be processed in the Gibraltar SX/EW plant in the coming years. Taking all of these factors into account, total copper production at Gibraltar for 2026 is expected to be in the range of 110 to 115 million pounds and is expected to continue at similar levels (± 5%) until completion of mining in the Connector pit in mid-2029.

Molybdenum production in 2026 is expected to remain at similar levels to 2025, and with molybdenum prices stabilizing above US$20.00 per pound we continue to expect strong molybdenum by-product credits.

TASEKO MINES LIMITED

Management's Discussion and Analysis

The Company has offtake agreements covering substantially all of Gibraltar's copper concentrate production for 2026, which contain low and in certain cases negative TCRC rates reflecting the continued tight copper smelting market. Based on the contract terms, the Company expects average TCRCs to be similar to 2025.

The Company has a prudent hedging program in place to protect a minimum copper price and Gibraltar cash flow during the commissioning period and ramp-up of commercial operations at Florence Copper. Currently, the Company has copper collar contracts in place with a floor of US$4.00 per pound and a ceiling of US$5.40 per pound for 54 million pounds of copper production for the first half of 2026 and a floor of US$4.75 per pound and a ceiling of between US$7.50 and US$8.50 per pound for 24 million pounds of copper production for the third quarter of 2026 (refer to "Financial Condition Review-Hedging Strategy" for details).

Florence Copper

Florence Copper is an in-situ copper recovery ("ISCR") operation, located in Arizona, USA, that will produce LME Grade A copper metal without conventional open-pit mining or major surface disturbance. Florence Copper is projected to rank among the lowest greenhouse gas ("GHG") intensity primary copper producers in North America, delivering environmentally responsible copper to North American manufacturers and consumers. The project is expected to commence commercial production in early 2026, with production ramping up to 85 million pounds per year at full capacity.

Construction activities at Florence Copper were completed on time and largely on budget in the fourth quarter of 2025. The focus of the operating team has transitioned to wellfield operations, commissioning of the SX/EW plant and the startup of commercial production.

Commercial wellfield acidification commenced in early November, and by early December mining solutions were circulating in all the new production wells within the commercial wellfield. Initial injection flowrates were above expectations resulting in faster initial acidification of the wellfield. The grade of copper recovered in solution from the recovery wells continued to increase, and the average solution grade reached the level required for SX/EW plant operations. Commissioning of the SX/EW plant area advanced in parallel with initial wellfield operations, and plant operations commenced mid-February. Production of copper cathode commenced mid-February with the startup of the electrowinning circuit. The Florence Copper SX/EW plant is now fully operational and copper is being plated. The project team is focused on the successful ramp-up of operations in 2026, and total production in 2026 is expected to be in the range of 30 to 35 million pounds of copper cathode.

Wellfield drilling also re-commenced in late 2025 and by early 2026 there were three drill rigs operating on site with a fourth drill rig being mobilized at site. Continued expansion of the commercial wellfield will be required to support higher solution flows and increased copper production as the Florence Copper commercial operation progresses through the ramp-up in 2026.

| Florence Copper capital spend (US$ in thousands) |

Three months ended December 31, 2025 |

Year ended December 31, 2025 |

|||||

| Commercial facility construction costs | 8,016 | 119,644 | |||||

| Plant and site commissioning costs | 3,636 | 3,636 | |||||

| Site and PTF operations | 12,260 | 34,662 | |||||

| Total Florence Copper capital spend | 23,912 | 157,942 |

Florence Copper commercial facility construction costs were US$8.0 million in the fourth quarter and US$119.6 million in 2025. Total construction costs for the Florence Copper commercial facility were US$274.6 million.

TASEKO MINES LIMITED

Management's Discussion and Analysis

Long-term Growth Strategy

Taseko's strategy has been to grow the Company by acquiring and developing a pipeline of projects focused on copper in North America. We continue to believe this will generate long-term returns for shareholders. Our other development projects are located in BC, Canada.

Yellowhead copper project

In July 2025, the Company published a new report titled "Technical Report Update on the Yellowhead Copper Project, British Columbia, Canada" (the "Yellowhead 2025 Technical Report"). Based on the Yellowhead 2025 Technical Report, the Yellowhead copper project is expected to produce 4.4 billion pounds of copper over a 25-year mine life at an average C1 cost, net of by-product credit, of US$1.90 per pound of copper produced. During the first 5 years of operation, the Yellowhead project is expected to produce an average of 206 million pounds of copper per year at an average C1 cost, net of by-product credit, of US$1.62 per pound of copper produced. The Yellowhead project also contains valuable precious metal by-products with 282,000 ounces of gold production and 19.4 million ounces of silver production over the life of mine.

The economic analysis in the Yellowhead 2025 Technical Report was prepared using a copper price of US$4.25 per pound, a gold price of US$2,400 per ounce, and a silver price of US$28.00 per ounce.

Project highlights based on the Yellowhead 2025 Technical Report are detailed below:

• Average annual copper production of 178 million pounds over a 25 year mine life at total cash costs (C1) of US$1.90 per pound of copper produced;

• Over the first 5 years of the mine life, copper grade is expected to average 0.32% producing an average of 206 million pounds of copper at total cash costs (C1) of US$1.62 per pound of copper produced;

• Concentrator designed to process 90,000 tonnes per day of ore with an expected copper recovery of 90%, and produce a clean copper concentrate with payable gold and silver by-products;

• Conventional open pit mining with a low strip ratio of 1.4;

• After-tax net present value of $2.0 billion (8% after-tax discount rate) and after-tax internal rate of return of 21%;

• Initial capital costs of $2.0 billion with a payback period of 3.3 years; and

• Expected to be eligible for the Canadian federal Clean Technology Manufacturing Investment Tax Credit, with 30% (approximately $540 million) of eligible initial capital costs reimbursed in year 1 of operation.

In June 2025, the Yellowhead project's Initial Project Description was filed and accepted by the British Columbia Environmental Assessment Office and Impact Assessment Agency of Canada, formally commencing the Environmental Assessment process. The Company will continue to engage with project stakeholders to ensure that the development of the Yellowhead Project is in line with environmental and social expectations. The Company opened a community office for the Yellowhead project in 2024 to support ongoing engagement with local communities including First Nations.

New Prosperity copper-gold project

In June 2025, Taseko, the Tŝilhqot'in Nation and the Province of BC reached a historic agreement concerning the New Prosperity project (the "Teẑtan Biny Agreement"). The Teẑtan Biny Agreement ends litigation among the parties while providing certainty with respect to how the significant copper-gold resource at New Prosperity may be developed in the future.

TASEKO MINES LIMITED

Management's Discussion and Analysis

Key elements of the Teẑtan Biny Agreement include:

• Taseko received a payment of $75 million from the Province of BC upon closing of the agreement;

• Taseko contributed a 22.5% equity interest in the New Prosperity mineral tenures to a trust for the future benefit of the Tŝilhqot'in Nation. The trust will transfer the property interest to the Tŝilhqot'in Nation if and when it consents to a proposal to pursue mineral development in the project area;

• Taseko retains a majority interest (77.5%) in the New Prosperity mineral tenures and can divest some or all of its interest at any time, including to other mining companies that could advance a project with the consent of the Tŝilhqot'in Nation. However, Taseko has committed not to be the proponent (operator) of mineral exploration and development activities at New Prosperity, nor the owner of a future mine development;

• Taseko has entered into a consent agreement with the Tŝilhqot'in Nation, whereby no mineral exploration or development activity can proceed in the New Prosperity project area without the free, prior and informed consent of the Tŝilhqot'in Nation;

• The Province of BC and the Tŝilhqot'in Nation have agreed to negotiate the process by which the consent of the Tŝilhqot'in Nation will be sought for any proposed mining project to proceed through an environmental assessment process; and

• The Tŝilhqot'in Nation and the Province of BC have agreed to undertake a land-use planning process for the area of the mineral tenures and a broader area of land within Tŝilhqot'in territory.

Aley niobium project

The converter pilot test is ongoing to provide additional process data to support the design of commercial process facilities. In the fourth quarter, the Company produced on-spec ferro-niobium, and the process is now scaling up to provide product samples to support marketing initiatives. The Company is also conducting a scoping study to investigate the potential for Aley niobium oxide production to supply the growing market for niobium-based batteries.

Sustainability

Taseko is a leading North American copper producer, whose approach to sustainability is wholly aligned with our commitment to efficiency and operational excellence.

Recognized as a top-tier operator, Taseko is committed to strong health and safety standards, responsible environmental practices, and creating lasting value for people and communities. Together, these commitments define the organization's sustainability framework.

Critical minerals

Copper is fundamental to renewable energy systems, electrification, modern infrastructure, and the rapid expansion of AI-driven data centres. As demand for clean energy and advanced technologies accelerates, so too will the need for copper. Taseko is well positioned to support this transition by ensuring stable, secure, and responsibly produced supply of this essential material.

TASEKO MINES LIMITED

Management's Discussion and Analysis

Operational excellence

Operational excellence underpins Taseko's sustainability performance. The Company maintains rigorous health and safety standards to protect employees and contractors, while taking a proactive approach to environmental stewardship and processive reclamation.

By integrating responsible environmental management with disciplined operations, Taseko delivers sustainable, long-term value.

Delivering 360 degrees of value

Taseko works to ensure that the benefits of responsible resource development are broadly shared. Community engagement is a cornerstone of the Company's sustainability strategy.

Taseko prioritizes meaningful, mutually beneficial partnerships with local communities and First Nations partners, fostering trust, collaboration and shared opportunity. Through employment, procurement, and community investment, Taseko's approach is about delivering lasting value at every level-for employees, communities, Indigenous partners, investors and North America as a whole.

Taseko's annual Sustainability Report is available at www.tasekomines.com/sustainability/overview.

Taseko received a rating of 'BBB' from MSCI, indicating an industry-average level of ESG risk management relative to our peers.

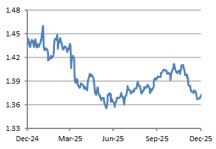

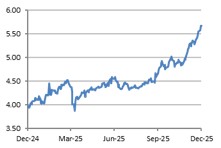

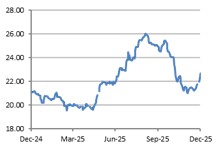

Market Review

| Copper | Molybdenum | Canadian dollar/US dollar Exchange |

|

|

|

1 Commodity prices in US dollars per pound.

2 Sources: London Metals Exchange for copper prices, Platts Metals for molybdenum prices, Bank of Canada for Canadian dollar/US dollar exchange rates.

Copper prices on the London Metal Exchange ("LME") are currently around US$5.75 per pound compared to US$5.67 per pound at December 31, 2025 and the fourth quarter average of US$5.03 per pound. Copper prices have continued to climb supported by tightening global supply amid heavy stockpiling in the US.

Longer-term demand for copper is expected to remain strong driven by strong structural demand trends in artificial intelligence, electrification, renewable energy and overall industrial activity. Tight supply conditions are expected to continue due to few available sources of new primary copper supply. These factors continue to provide structural catalysts and support for a higher copper price in the longer term as significant new mine supply lags behind growth in copper demand.

TASEKO MINES LIMITED

Management's Discussion and Analysis

Smelter TCRCs remain historically low, including spot rates at negative (premium) rates, driven by an increase in global copper smelting capacity and disruptions in the supply of copper concentrates. Tight copper concentrate supply could continue putting persistent pressure on spot TCRCs to record low rates.

Approximately 8% of the Company's revenue is made up of molybdenum sales and Connector pit ore is expected to provide higher molybdenum grades in the coming years. Molybdenum prices are currently around US$28.75 per pound compared to US$22.70 per pound at December 31, 2025 and the fourth quarter average of US$22.89 per pound. The Company's sales agreements specify molybdenum pricing based on published Platts Metals reports.

The Company's sales contracts are priced in US dollars while a majority of Gibraltar's costs are Canadian dollar denominated, and, therefore, fluctuations in the Canadian dollar/US dollar exchange rate can have a significant effect on the Company's financial results.

TASEKO MINES LIMITED

Management's Discussion and Analysis

Financial Performance

Earnings

| Year ended December 31, | ||||||||||

| (Cdn$ in thousands) | 2025 | 20241 | Change | |||||||

| Net loss | (30,076 | ) | (13,444 | ) | (16,632 | ) | ||||

| Unrealized foreign exchange (gain) loss | (32,974 | ) | 52,299 | (85,273 | ) | |||||

| Unrealized loss (gain) and fair value adjustments on derivatives | 85,678 | (10,141 | ) | 95,819 | ||||||

| Accretion on Cariboo consideration payable | 13,237 | 23,920 | (10,683 | ) | ||||||

| Accretion on Florence royalty obligation | 34,178 | 12,933 | 21,245 | |||||||

| Other operating costs | - | 18,665 | (18,665 | ) | ||||||

| Gain on Cariboo acquisition | - | (47,426 | ) | 47,426 | ||||||

| Gain on acquisition of control of Gibraltar2 | - | (14,982 | ) | 14,982 | ||||||

| Realized gain on sale of inventory3 | - | 17,122 | (17,122 | ) | ||||||

| Realized gain on processing of ore stockpiles4 | - | 9,227 | (9,227 | ) | ||||||

| Non-recurring other expenses related to Cariboo acquisition | - | 532 | (532 | ) | ||||||

| Call premium on settlement of debt | - | 9,571 | (9,571 | ) | ||||||

| Loss on settlement of debt, net of capitalized interest | - | 2,904 | (2,904 | ) | ||||||

| Tax effect of sale of non-controlling interest in New Prosperity | (9,285 | ) | - | (9,285 | ) | |||||

| Estimated tax effect of adjustments | (33,617 | ) | (4,253 | ) | (29,364 | ) | ||||

| Adjusted net income | 27,141 | 56,927 | (29,786 | ) | ||||||

1 Amounts for the year ended December 31, 2024 reflect the impact from the March 25, 2024 acquisition of Cariboo from Dowa and Furukawa, which increased the Company's effective interest in the Gibraltar mine from 87.5% to 100%.

2 Gain on acquisition of control of Gibraltar relates to Taseko's 87.5% share of copper concentrate inventories held at March 25, 2024 that was written-up to fair value as part of the acquisition of control of Gibraltar.

3 Realized gain on sale of inventory relates to copper concentrate inventories held at March 25, 2024 that was written-up to fair value as part of the acquisition of control of Gibraltar and subsequently sold. The realized portion of these gains have been added back to Adjusted net income in the period the inventories were sold.

4 Realized gain on processing of ore stockpiles relates to ore stockpile inventories held at March 25, 2024 that was written-up to fair value as part of the acquisition of control of Gibraltar and subsequently processed. The realized portion of these gains have been added back to Adjusted net income in the period the inventories were processed.

Adjusted net income decreased to $27.1 million ($0.07 adjusted earnings per share) in 2025, compared to $56.9 million ($0.19 adjusted earnings per share) in 2024, primarily driven by lower production and sales volumes, and higher unit cost of production resulting from the processing of lower grade stockpiled material that was used as the primary source of mill feed during the first half of the year, partially offset by higher prevailing commodity prices during the year. The comparative prior year amount also contained an insurance recovery of $26.3 million received from a business interruption insurance claim related to a major component repair in Concentrator #2.

Net loss was $30.1 million ($0.09 loss per share) in 2025, which included unrealized losses and fair value adjustments on derivatives of $85.7 million, accretion on Florence royalty obligation of $34.2 million and accretion on Cariboo consideration payable of $13.2 million, reflecting higher prevailing copper price trends and the impact on the valuation of the respective instruments, partially offset by an unrealized foreign exchange gain of $33.0 million due to the effect of a weaker US dollar on the Company's US dollar-denominated debt.

TASEKO MINES LIMITED

Management's Discussion and Analysis

Net loss was $13.4 million in 2024, which included an unrealized foreign exchange loss of $52.3 million due to the effect of a stronger US dollar on the Company's US dollar-denominated debt, accretion on Cariboo consideration payable of $23.9 million and accretion on Florence royalty obligation of $12.9 million, partially offset by unrealized gains and fair value adjustments on derivatives of $10.1 million reflecting lower prevailing commodity prices and the impact on the valuation of the respective instruments. Net loss for 2024 also reflects losses on the settlement of debt, and other site costs associated with the crusher relocation project and site care and maintenance costs during the June 2024 unionized labour strike at Gibraltar, and the impact of gains recognized in connection with the acquisition of Cariboo.

Revenues

| Year ended December 31, | ||||||||||

| (Cdn$ in thousands) | 2025 | 20241 | Change | |||||||

| Copper contained in concentrate | 599,138 | 575,012 | 24,126 | |||||||

| Copper cathode | 11,717 | - | 11,717 | |||||||

| Molybdenum concentrate | 52,586 | 41,712 | 10,874 | |||||||

| Silver | 5,878 | 6,437 | (559 | ) | ||||||

| Gold | 2,120 | - | 2,120 | |||||||

| Total gross revenue | 671,439 | 623,161 | 48,278 | |||||||

| Treatment and refining premiums (costs) | 1,465 | (15,068 | ) | 16,533 | ||||||

| Revenue | 672,904 | 608,093 | 64,811 | |||||||

| Sales of copper in concentrate2 (thousand pounds) | 93,125 | 100,759 | (7,634 | ) | ||||||

| Average realized copper price (US$ per pound) | 4.61 | 4.17 | 0.44 | |||||||

| Average LME copper price (US$ per pound) | 4.51 | 4.15 | 0.36 | |||||||

| Average exchange rate (CAD/USD) | 1.40 | 1.37 | 0.03 | |||||||

1 Amounts for the year ended December 31, 2024 reflect the impact from the March 25, 2024 acquisition of Cariboo from Dowa and Furukawa, which increased the Company's effective interest in the Gibraltar mine from 87.5% to 100%.

2 Sales of copper in concentrate includes a net smelter payable deduction of approximately 3.5% to derive net payable pounds of copper sold.

Revenues from the sales of copper contained in concentrate increased by $24.1 million to $599.1 million in 2025, compared to $575.0 million in 2024. The increase was driven by a positive price variance of $57.6 million, reflecting a US$0.44 per pound higher average realized copper price, and a positive foreign exchange variance of $10.7 million, due to a stronger Canadian dollar trend throughout the year, partially offset by a negative volume variance of $44.2 million, due to lower payable sales volumes from lower production.

Copper cathode revenues were $11.7 million in 2025 as the Company began shipping copper cathode produced from the Gibraltar SX/EW plant during the second half of the year, supplementing revenues from the sales of copper contained in concentrate.

Molybdenum revenues increased by $10.9 million to $52.6 million in 2025, compared to $41.7 million in 2024, primarily attributable to increased sales volumes as Gibraltar began to realize the higher expected molybdenum grades and recoveries from Connector pit ore.

Gold revenues were $2.1 million in 2025 as the Company benefited from payable gold under one of its concentrate offtake agreements for Gibraltar concentrate.

TASEKO MINES LIMITED

Management's Discussion and Analysis

The Company recorded treatment and refining premiums of $1.5 million in 2025, compared to treatment and refining costs of $15.1 million in 2024, reflecting the favorable TCRC rates realized under the Company's 2025 offtake agreements.

Cost of sales and other operating costs

| Year ended December 31, | ||||||||||

| (Cdn$ in thousands) | 2025 | 20241 | Change | |||||||

| Site operating costs | 392,220 | 367,689 | 24,531 | |||||||

| Transportation costs | 29,940 | 35,413 | (5,473 | ) | ||||||

| Changes in inventories: | ||||||||||

| Changes in finished goods | 1,773 | 23,852 | (22,079 | ) | ||||||

| Changes in sulphide ore stockpiles | 16,327 | 2 | 16,325 | |||||||

| Changes in oxide ore stockpiles | (18,020 | ) | (9,870 | ) | (8,150 | ) | ||||

| Production costs | 422,240 | 417,086 | 5,154 | |||||||

| Depletion and amortization | 102,718 | 73,852 | 28,866 | |||||||

| Cost of sales | 524,958 | 490,938 | 34,020 | |||||||

| Site operating costs per ton milled* | $ | 12.81 | $ | 12.93 | $ | (0.12 | ) | |||

| Other operating costs: | ||||||||||

| Research and development tax credits | (4,008 | ) | - | (4,008 | ) | |||||

| Crusher relocation costs | - | 16,141 | (16,141 | ) | ||||||

| Site care and maintenance costs | - | 2,524 | (2,524 | ) | ||||||

| Other operating (income) costs | (4,008 | ) | 18,665 | (22,673 | ) | |||||

| Insurance recovery | - | (26,290 | ) | 26,290 | ||||||

1 Amounts for the year ended December 31, 2024 reflect the impact from the March 25, 2024 acquisition of Cariboo from Dowa and Furukawa, which increased the Company's effective interest in the Gibraltar mine from 87.5% to 100%.

Site operating costs were $392.2 million in 2025, compared to $367.7 million in 2024. The increase in site operating costs was primarily attributable to increased mining costs needed to support the higher mining rates achieved at Gibraltar during the year, and the recommissioning and operation of the Gibraltar SX/EW plant to produce copper cathode from oxide ore stockpiles. Site operating costs in 2024 were also impacted by the June 2024 unionized labour strike at Gibraltar, which put the mine site into care and maintenance for a period, and the crusher relocation and concurrent mill maintenance projects, which reduced mill availability and related milling costs.

Transportation costs were $29.9 million in 2025 compared to $35.4 million in 2024 and generally reflecting the lower sales volume in the current year.

Cost of sales was impacted by changes in stockpile inventories. Stockpiled ore was used to supplement mined ore in the first half of the year, resulting in a drawdown of 9.9 million tons of sulphide ore stockpiles. 4.0 million tons were added back to sulphide ore stockpiles in the second half of the year as mining advanced deeper and quality ore was released from the Connector pit. The resulting net drawdown of 5.9 million tons contributed to an increase in production costs of $16.3 million in 2025.

TASEKO MINES LIMITED

Management's Discussion and Analysis

Oxide ore was added to the heap leach pads for SX/EW processing as Gibraltar mined through the oxide layer capping the Connector pit. Oxide ore stockpiles increased by 8.9 million tons in 2025, contributing to a decrease in production costs of $18.0 million.

Depletion and amortization increased by $28.9 million to $102.7 million in 2025, compared to $73.9 million in 2024, reflecting Gibraltar's transition of mining activities to the Connector pit and the associated amortization of previously deferred stripping costs.

Other expenses (income)

| Year ended December 31, | ||||||||||

| (Cdn$ in thousands) | 2025 | 2024 | Change | |||||||

| General and administrative | 14,632 | 12,942 | 1,690 | |||||||

| Share-based compensation expense | 22,549 | 9,002 | 13,547 | |||||||

| Realized loss on derivatives | 5,333 | 5,342 | (9 | ) | ||||||

| Unrealized loss (gain) on derivatives | 52,212 | (21,020 | ) | 73,232 | ||||||

| Fair value adjustment on Florence copper stream derivative | 20,323 | 10,880 | 9,443 | |||||||

| Fair value adjustment on Cariboo contingent performance payments | 13,143 | - | 13,143 | |||||||

| Project evaluation expense | 3,909 | 3,623 | 286 | |||||||

| Gain on Cariboo acquisition | - | (47,426 | ) | 47,426 | ||||||

| Gain on acquisition of control of Gibraltar1 | - | (14,982 | ) | 14,982 | ||||||

| Call premium on settlement of debt | - | 9,571 | (9,571 | ) | ||||||

| Other expenses (income), net | (81 | ) | 307 | (388 | ) | |||||

| Other expenses (income) | 132,020 | (31,761 | ) | 163,781 | ||||||

1 Gain on acquisition of control of Gibraltar relates Taseko's 87.5% share of copper concentrate inventories held at March 25, 2024 that was written-up to fair value as part of the acquisition of control of Gibraltar.

General and administrative expenses were $14.6 million in 2025, compared to $12.9 million in 2024. The increase in general and administrative expenses was attributable to increased personnel and scaling of corporate functions to support the ramp-up of Florence Copper and the Yellowhead Environmental Assessment process.

Share-based compensation relates to expenses associated with the vesting of share options and performance share units over their respective vesting periods, and fair value adjustments on deferred share units and restricted share units. Share-based compensation expenses increased by $13.5 million to $22.5 million in 2025 from $9.0 million in 2024, primarily reflecting the increase in the Company's share price and its impact on the valuation of the Company's long-term incentive awards. For more information, refer to Financial Statements-Note 23.

Realized loss on derivatives was $5.3 million in 2025, consistent with 2024, and reflects the amortization of premiums paid for copper collars and fuel call options entered into as part of the Company's hedging strategy. Unrealized loss on derivatives was $52.2 million in 2025, compared to an unrealized gain on derivatives of $21.0 million in 2024, driven by increasing prevailing copper prices, which closed the year at US$5.67 per pound, and the impact on changes in fair value of the Company's outstanding copper collar positions with a floor of US$4.00 per pound and a ceiling of US$5.40 per pound.

TASEKO MINES LIMITED

Management's Discussion and Analysis

Fair value adjustment on Florence copper stream derivative was $20.3 million in 2025. Fair value adjustment on Cariboo contingent performance payments was $13.1 million in 2025. These fair value adjustments primarily reflect increases in prevailing and forecast copper prices.

Project evaluation expense represents costs associated with the New Prosperity project and other technical expenditures undertaken by Taseko's engineering and technical teams on various project initiatives.

On March 25, 2024, the Company completed its acquisition of the remaining 50% of Cariboo Copper Corp. ("Cariboo") from Dowa Metals & Mining Co., Ltd. ("Dowa") and Furukawa Co., Ltd. ("Furukawa"), and increased its effective interest in the Gibraltar mine from 87.5% to 100%. The Company recognized a gain on acquisition of Cariboo of $47.4 million representing the difference between the estimated fair value of net assets acquired and the estimated fair value of total consideration payable. The acquisition also gave the Company full control over Gibraltar and required a deemed disposition and reacquisition of its previously held 87.5% interest in Gibraltar according to IFRS Accounting Standards. The Company recognized a gain on acquisition of control of Gibraltar of $15.0 million representing the write-up of finished copper concentrate inventory held at the date of acquisition to fair value. Further details on the Cariboo acquisition can be found in Financial Statements-Note 17.

Finance expenses and income

| Year ended December 31, | ||||||||||

| (Cdn$ in thousands) | 2025 | 2024 | Change | |||||||

| Interest expense | 71,447 | 61,886 | 9,561 | |||||||

| Amortization of deferred financing charges | 2,503 | 2,515 | (12 | ) | ||||||

| Loss on settlement of debt | - | 4,646 | (4,646 | ) | ||||||

| Finance income | (3,920 | ) | (5,175 | ) | 1,255 | |||||

| Less: Capitalized interest expense | (29,759 | ) | (23,060 | ) | (6,699 | ) | ||||

| Finance expenses, net | 40,271 | 40,812 | (541 | ) | ||||||

| Accretion on deferred revenue | 10,165 | 7,244 | 2,921 | |||||||

| Accretion on provision for environmental rehabilitation | 2,862 | 2,780 | 82 | |||||||

| Accretion on Cariboo consideration payable | 13,237 | 23,920 | (10,683 | ) | ||||||

| Accretion on Florence royalty obligation | 34,178 | 12,993 | 21,185 | |||||||

| Accretion expenses | 60,442 | 46,937 | 13,505 | |||||||

Net finance expenses were $40.3 million in 2025, comparable to $40.8 million in 2024. Interest expense increased by $9.6 million, reflecting higher principal outstanding and higher coupon rates on the Company's senior notes refinanced in April 2024, and higher borrowings against the Company's revolving credit facility during the year to support construction activities at Florence Copper, and was partially offset by increased capitalized interest of $6.7 million, reflecting increased capital spend on the commercial production facility.

Accretion on Cariboo consideration payable was $13.2 million in 2025 and reflects changes in the timing of expected cash flows arising from changes in forecast copper price assumptions applied over the remaining term of the Sojitz earn-out and the Dowa and Furukawa earn-out obligations.

Accretion on Florence royalty obligation was $34.2 million in 2025 and reflects accretion and changes in the timing of expected cash flows arising from higher prevailing copper price forecasts applied over the term of the Florence royalty obligation.

TASEKO MINES LIMITED

Management's Discussion and Analysis

Income tax

| Year ended December 31, | ||||||||||

| (Cdn$ in thousands) | 2025 | 2024 | Change | |||||||

| Current income tax expense | 1,696 | 3,482 | (1,786 | ) | ||||||

| Deferred income tax (recovery) expense | (21,101 | ) | 28,060 | (49,161 | ) | |||||

| Income tax (recovery) expense | (19,405 | ) | 31,542 | (50,947 | ) | |||||

| Effective tax rate | 39.2 % | 174.3 % | (135.1) % | |||||||

| Canadian statutory rate | 27.0 % | 27.0 % | - | |||||||

| BC mineral tax rate | 9.5 % | 9.5 % | - | |||||||

A reconciliation of the effective tax rate is presented below:

| Year ended December 31, | ||||||||||

| (Cdn$ in thousands) | 2025 | 2024 | Change | |||||||

| Income tax expense at Canadian statutory rate of 36.5% | (18,055 | ) | 6,603 | (24,658 | ) | |||||

| Permanent differences | 13,844 | 20,684 | (6,840 | ) | ||||||

| Foreign tax rate differentials | 1,482 | 629 | 853 | |||||||

| Unrecognized tax benefits | 1,097 | 6,627 | (5,530 | ) | ||||||

| Utilization of previously unrecognized capital losses | (9,238 | ) | - | (9,238 | ) | |||||

| Recognition of previously unrecognized non-capital losses | (7,569 | ) | - | (7,569 | ) | |||||

| Deferred tax adjustments related to prior periods | (966 | ) | (3,001 | ) | 2,035 | |||||

| Income tax (recovery) expense | (19,045 | ) | 31,542 | (50,947 | ) | |||||

The effective tax rate for 2025 is higher than the combined BC mineral tax rate and the federal and provincial statutory income tax rate due to certain expenses such as finance charges, derivative expenses, and general and administrative costs that are not deductible for BC mineral tax purposes.

As foreign exchange revaluations on the senior secured notes are not recognized for tax purposes until realized, and in the case of capital losses, until they are applied, the effective tax rate may be significantly higher or lower than statutory rates, as is the case for the 2025 and 2024 periods.

Capital losses were utilized against the gain recognized on the disposition of a 22.5% interest in New Prosperity. The recognition of previously unrecognized losses relate to the Company's Yellowhead copper project.

TASEKO MINES LIMITED

Management's Discussion and Analysis

Financial Condition Review

Balance sheet review

| (Cdn$ in thousands, unless otherwise indicated) | December 31, 2025 |

December 31, 2024 |

Change | |||||||

| Cash | 187,961 | 172,732 | 15,229 | |||||||

| Other current assets | 156,925 | 180,507 | (23,582 | ) | ||||||

| Property, plant and equipment | 2,045,452 | 1,770,102 | 275,350 | |||||||

| Other assets | 82,149 | 71,702 | 10,447 | |||||||

| Total assets | 2,472,487 | 2,195,043 | 277,444 | |||||||

| Current liabilities1 | 194,313 | 173,983 | 20,330 | |||||||

| Debt: | ||||||||||

| Senior secured notes | 674,114 | 706,741 | (32,627 | ) | ||||||

| Equipment-related financings | 72,882 | 90,467 | (17,585 | ) | ||||||

| Cariboo consideration payable | 132,006 | 129,421 | 2,585 | |||||||

| Florence copper stream | 91,501 | 67,813 | 23,688 | |||||||

| Florence royalty obligation | 107,599 | 84,383 | 23,216 | |||||||

| Deferred revenue | 82,617 | 77,327 | 5,290 | |||||||

| Other liabilities | 338,792 | 361,686 | (22,894 | ) | ||||||

| Total liabilities | 1,693,824 | 1,691,821 | 2,003 | |||||||

| Equity | 778,663 | 503,222 | 275,441 | |||||||

| Net debt (debt minus cash) | 559,035 | 624,476 | (65,441 | ) | ||||||

| Total common shares outstanding (million shares) | 361.1 | 304.7 | 56.4 |

1 Current liabilities exclude the current portion of long-term debt.

The Company's asset base is principally comprised of property, plant and equipment reflecting the capital-intensive nature of its large scale, open pit mining operation at Gibraltar and the commercial SX/EW facility at Florence Copper. Other current assets primarily include accounts receivable, inventories (concentrate inventories, ore stockpiles, and supplies), prepaid expenses, and marketable securities. Concentrate inventories, accounts receivable and cash balances can fluctuate due to the timing of sales and cash settlements.

Property, plant and equipment increased by $275.4 million during the year, which includes Florence Copper construction costs of $233.7 million (capital project costs of $182.8 million and site costs of $50.9 million) and Gibraltar capital expenditures of $172.4 million (capitalized stripping costs of $93.6 million and other capital expenditures of $78.8 million).

Net debt decreased by $65.4 million during the year, primarily due to the October equity financings, which was partially used to fund the construction of the Florence Copper commercial facility and to reduce outstanding debt.

Cariboo consideration payable relates to earn-out obligations arising from the acquisition of Cariboo. Cariboo consideration payable increased by $2.6 million during the year, primarily due to accretion of the liability reflecting higher copper price assumptions applied over the remaining term of the Cariboo earn-out liabilities, partially offset by $16.6 million of payments made to Sojitz during the year.

TASEKO MINES LIMITED

Management's Discussion and Analysis

Florence royalty obligation increased $23.2 million, primarily reflecting changes in the timing of expected cash flows driven by higher forecast copper prices applied over the term of the obligation. Florence copper stream increased $23.7 million, primarily due to the receipt of the final US$10.0 million instalment under the Mitsui copper stream during the period and the fair value impacts associated with higher forecast copper prices applied over the term of the stream.

Deferred revenue relates to the advance payments received from OR Royalties Inc. (formerly Osisko Gold Royalties Inc.) for the sale of future silver production from Gibraltar.

Other liabilities decreased by $22.9 million primarily due to changes in deferred tax liabilities.

At February 18, 2026, there were 364,557,150 common shares and 8,091,464 stock options outstanding. More information on these instruments and the terms of their exercise can be found in Financial Statements-Notes 21 and 23.

Liquidity, cash flow and capital resources

At December 31, 2025, the Company had cash of $188.0 million (December 31, 2024 - $172.7 million) and available liquidity of approximately $338.7 million including its undrawn US$110 million revolving credit facility (December 31, 2024 - $331.0 million).

Cash provided by operating activities was $219.6 million in 2025, compared to $232.6 million in 2024. The decrease in cash provided by operating activities primarily reflects non-recurring cash flows recorded in the comparative prior year amount, including $26.3 million in insurance proceeds received from a business interruption insurance claim related to a faulty component in Concentrator #2 and an $18.2 million payment arising from the amendment of the Gibraltar silver stream with OR Royalties Inc. (formerly Osisko Gold Royalties Inc.). This impact was partially offset by increased operating cash inflows, driven by increased revenues reflecting higher prevailing copper prices during the year.

Cash used for investing activities was $425.8 million in 2025, compared to $317.9 million in 2024. Investing activities include $149.9 million in capital expenditures at Gibraltar ($80.9 million in capitalized stripping and $69.0 million in other capital expenditures), and $269.5 million in capital expenditures at Florence Copper, which includes $50.9 million in capitalized site costs to support meeting final permitting conditions and operational readiness.

Cash provided by financing activities was $224.5 million in 2025, compared to $157.2 million in 2024. Financing activities include $258.6 million in net proceeds from share issuances, $71.8 million in net proceeds received from the Province of BC upon closing of the Teẑtan Biny Agreement, and $14.4 million (US$10.0 million) for the final instalment under the US$50 million Mitsui copper stream, offset by $73.4 million in interest payments, $40.3 million in repayments against the Company's equipment financings, and $16.6 million in payments to Sojitz related to the Cariboo earn-out obligations.

Liquidity outlook

At December 31, 2025, the Company had approximately $338.7 million (December 31, 2024 - $331.0 million) of available liquidity including $188.0 million in cash and US$110 million undrawn capacity on its corporate revolving credit facility.

In October 2025, the Company closed an equity financing (the "Offering") with a syndicate of underwriters and issued 42.7 million common shares with a value of US$4.05 per share for gross proceeds of US$172.8 million. Proceeds from the Offering were used to repay outstanding debt under the Company's revolving credit facility with the balance available for general corporate purposes, including to support further wellfield development at Florence Copper and to advance the Yellowhead project.

TASEKO MINES LIMITED

Management's Discussion and Analysis

Based on current copper prices and with copper hedges in place, the Company expects stable operating margins and cash flows from Gibraltar in 2026.

Construction of the Florence Copper commercial production facility is now complete, and the operating team has commenced wellfield operations. Wellfield drilling has also re-commenced, with three drill rigs on site and a fourth being mobilized, to continue the expansion of the commercial wellfield and support higher solution flowrates and increased copper production. Production of copper cathode commenced recently with the startup of the electrowinning circuit. The Florence Copper SX/EW plant is fully operational and copper is now being plated.

If needed, the Company could raise further additional capital through equity financings or asset sales, including royalties, sales of project interests, joint ventures, or additional credit facilities, including additional notes offerings or increasing borrowings from commercial banks or credit funds through one or more credit facilities including increases to its existing revolving credit facility. The Company evaluates these financing alternatives based on a number of factors, including the prevailing metal prices and projected operating cash flows from Gibraltar, relative valuation, liquidity requirements, covenant restrictions and other factors, in order to optimize the Company's cost of capital and maximize shareholder value.

Future changes in copper and molybdenum market prices could also impact the timing and amount of cash available for future investment in the Company's capital commitments and development projects, debt obligations and other uses of capital including potential returns to shareholders. To mitigate commodity price risks in the short term, copper price options are entered into for a substantial portion of Gibraltar's copper production and the Company has a long track history of doing so. The Company currently has copper price protection in place for 54 million pounds of production for the first half of 2026 at a LME floor price of US$4.00 per pound and a ceiling of US$5.40 per pound, and 24 million pounds of production for the third quarter of 2026 at a LME floor price of US$4.75 per pound and a ceiling between US$7.50 and US$8.50 per pound.

Hedging strategy

The Company generally fixes all or substantially all of the copper prices of its copper concentrate shipments at the time of shipment. Where the customer's offtake contract does not provide a price fixing option, the Company may look to undertake a quotational period hedge directly with a financial institution as the counterparty in order to fix the price of the shipment.

To protect against sudden and unexpected copper price volatility in the market, the Company's hedging strategy aims to secure a minimum price for a significant portion of future copper production using copper put options that are either purchased outright or substantially funded by the sale of copper call options that are out of the money. The amount and duration of the copper hedge positions is based on an assessment of business-specific risk elements combined with the copper pricing outlook. Copper price and quantity exposure are reviewed regularly to ensure that adequate revenue protection is in place.

Hedge positions are typically extended by adding incremental quarters at established floor prices (the strike price of the copper put option) to provide the necessary price protection. Considerations for the cost of the hedging program include an assessment of Gibraltar's estimated production costs, copper price trends and the Company's fixed capital requirements during the relevant period. During periods of volatility or step changes in the copper price, the Company may revisit outstanding hedging contracts and determine whether copper put (floor) or call (ceiling) levels should be adjusted in line with the market while maintaining copper price protection. The Company will revert to shorter term floor price protection utilizing put options once Florence Copper is through commissioning and ramp-up.

TASEKO MINES LIMITED

Management's Discussion and Analysis

From time to time, the Company will look at potential hedging opportunities that mitigate the risk of rising input costs, including foreign exchange and fuel prices, where such a strategy is cost effective. To protect against a potential operating margin squeeze that could arise from oil and diesel price shocks, the Company has purchased fuel call options in the past to provide a price ceiling for diesel that is used by the mining fleet and may do so in the future.

A summary of the Company's outstanding hedge positions is as follows:

| Notional amount | Strike price | Term to maturity | Original cost | |||||

| At December 31, 2025 | ||||||||

| Copper collars | 27 million lbs | Floor - US$4.00 per lb Ceiling - US$5.40 per lb |

Q1 2026 | $1.5 million | ||||

| Copper collars | 27 million lbs | Floor - US$4.00 per lb Ceiling - US$5.40 per lb |

Q2 2026 | $nil | ||||

| Acquired subsequent to December 31, 2025 | ||||||||

| Copper collars | 12 million lbs | Floor - US$4.75 per lb Ceiling - US$7.50 per lb |

Q3 2026 | $0.1 million | ||||

| Copper collars | 12 million lbs | Floor - US$4.75 per lb Ceiling - US$8.50 per lb |

Q3 2026 | $nil | ||||

Commitments and contingencies

| Payments due | ||||||||||||||||||||||

| (Cdn$ in thousands) | 2026 | 2027 | 2028 | 2029 | 2030 | Thereafter | Total | |||||||||||||||

| Debt | ||||||||||||||||||||||

| 2030 Notes | - | - | - | - | 685,300 | - | 685,300 | |||||||||||||||

| Interest | 56,537 | 56,537 | 56,537 | 56,537 | 28,269 | - | 254,417 | |||||||||||||||

| Equipment loans | ||||||||||||||||||||||

| Principal | 27,333 | 14,448 | 12,143 | 742 | 442 | - | 55,108 | |||||||||||||||

| Interest | 3,594 | 1,706 | 589 | 71 | 8 | - | 5,968 | |||||||||||||||

| Lease liabilities | ||||||||||||||||||||||

| Principal | 8,493 | 5,552 | 1,866 | 1,228 | 454 | 181 | 17,774 | |||||||||||||||

| Interest | 1,339 | 685 | 200 | 92 | 29 | 9 | 2,354 | |||||||||||||||

| Cariboo consideration payable1 | 13,800 | 25,250 | 25,250 | 15,250 | 15,250 | 47,200 | 142,000 | |||||||||||||||

| PER2 | - | - | - | - | - | 155,651 | 155,651 | |||||||||||||||

| Capital expenditures | 25,288 | - | - | - | - | - | 25,288 | |||||||||||||||

| Other expenditures: | ||||||||||||||||||||||

| Transportation-related services3 | 11,537 | 1,679 | - | - | - | - | 13,216 | |||||||||||||||

TASEKO MINES LIMITED

Management's Discussion and Analysis

1 On March 15, 2023, the Company completed the acquisition of 50% of Cariboo from Sojitz Corporation ("Sojitz"). The acquisition price payable to Sojitz is a minimum of $60 million payable over 5 years and potential contingent payments dependent upon Gibraltar copper revenue and average annual LME copper prices. As of December 31, 2025, $30 million of the $60 million minimum amount has been paid to Sojitz. The remaining minimum amounts will be paid in $10 million annual instalments over the next 3 years. There is no interest payable on these minimum amounts. The Company also estimates $47.0 million of contingent payments payable over the next 3 years, which have not been included in the table above.

On March 25, 2024, the Company completed the acquisition of the remaining 50% of Cariboo from Dowa and Furukawa. The acquisition price payable to Dowa and Furukawa is a minimum $117 million payable over 10 years. The amount and timing of these payments is dependent upon Gibraltar cash flow and average annual LME copper prices.

2 Provision for environmental rehabilitation ("PER") represents the net present value of estimated costs of legal and constructive obligations required to retire an asset, including decommissioning and other site restoration activities, primarily for Gibraltar and Florence Copper. At December 31, 2025, the Company has provided surety bonds for $124.2 million for Gibraltar's reclamation security and US$37.1 million for Florence Copper's reclamation security.

3 Transportation-related services include ocean freight and port handling services, which are both cancelable upon certain operating circumstances.

Concurrent with the execution of the Teẑtan Biny Agreement, the Company also agreed to contribute $6 million to the Tŝilhqot'in Nation to support community and land use planning initiatives, comprised of a $3 million payment at closing and three annual instalments of $1 million.

In December 2024, Gibraltar received an amendment to its M-40 permit in which the required closure bonding from the Province of BC to increase from $108.5 million to $139.9 million. Gibraltar was required to post this additional bonding over a 15-month period. In March 2025, Gibraltar posted surety bonds of $15.7 million to the Province of BC, and in July 2025 Gibraltar posted additional surety bonding of $1.0 million to the Province of BC. An additional surety bond of $15.7 million is due before March 31, 2026. The Company intends to post additional surety bonds to meet the remaining bonding requirements from insurance underwriters.

Selected Annual Information

| Year ended December 31, | ||||||||||

| (Cdn$ in thousands, except per share amounts) | 2025 | 2024 | 2023 | |||||||

| Revenues | 672,904 | 608,093 | 524,972 | |||||||

| Net (loss) income | (30,076 | ) | (13,444 | ) | 82,726 | |||||

| Per share - Basic | (0.09 | ) | (0.05 | ) | 0.29 | |||||

| Per share - Diluted | (0.09 | ) | (0.05 | ) | 0.28 | |||||

| At December 31, | ||||||||||

| (Cdn$ in thousands) | 2025 | 2024 | 2023 | |||||||

| Total assets | 2,472,487 | 2,195,043 | 1,584,139 | |||||||

| Total long-term financial liabilities1 | 867,600 | 901,928 | 670,802 | |||||||

1 Total long-term financial liabilities includes long-term debt, long-term Cariboo consideration payable and other financial liabilities.

TASEKO MINES LIMITED

Management's Discussion and Analysis

Fourth Quarter Results

| Consolidated Statements of Comprehensive (Loss) Income | Three months ended December 31, |

||||||

| (Cdn$ in thousands, except per share amounts) | 2025 | 2024 | |||||

| Revenues | 243,767 | 167,799 | |||||

| Cost of sales | |||||||

| Production costs | (119,712 | ) | (110,299 | ) | |||

| Depletion and amortization | (27,207 | ) | (24,641 | ) | |||

| Other operating costs | - | (4,132 | ) | ||||

| Earnings from mining operations | 96,848 | 28,727 | |||||

| General and administrative | (3,753 | ) | (2,754 | ) | |||

| Share-based compensation (expense) recovery | (6,600 | ) | 385 | ||||

| Project evaluation expenditures | (1,769 | ) | (191 | ) | |||

| Changes in derivatives and other fair value instruments | (38,783 | ) | 24,511 | ||||

| Other income (expenses), net | 110 | (69 | ) | ||||

| Income before financing costs and income taxes | 46,053 | 50,609 | |||||

| Finance expenses, net | (10,076 | ) | (8,645 | ) | |||

| Accretion expenses | (25,751 | ) | (11,154 | ) | |||

| Foreign exchange gain (loss) | 7,324 | (40,310 | ) | ||||

| Income (loss) before income taxes | 17,550 | (9,500 | ) | ||||

| Income tax expense | (13,096 | ) | (11,707 | ) | |||

| Net income (loss) | 4,454 | (21,207 | ) | ||||

| Other comprehensive (loss) income | |||||||

| Unrealized gain (loss) on financial assets | 594 | (792 | ) | ||||

| Foreign currency translation reserve | (11,069 | ) | 27,478 | ||||

| Total other comprehensive (loss) income | (10,475 | ) | 26,686 | ||||

| Total comprehensive (loss) income | (6,021 | ) | 5,479 | ||||

| Earnings (loss) per share | |||||||

| Basic | 0.01 | (0.07 | ) | ||||

| Diluted | 0.01 | (0.07 | ) | ||||

| Weighted-average shares outstanding (thousands) | |||||||

| Basic | 350,378 | 303,794 | |||||

| Diluted | 355,828 | 303,794 | |||||

TASEKO MINES LIMITED

Management's Discussion and Analysis

| Consolidated Statements of Cash Flows | Three months ended December 31, |

||||||

| (Cdn$ in thousands, except per share amounts) | 2025 | 2024 | |||||

| Operating activities | |||||||

| Net income (loss) | 4,454 | (21,207 | ) | ||||

| Adjustments for: | |||||||

| Depletion and amortization | 27,356 | 25,110 | |||||

| Income tax expense | 13,096 | 11,707 | |||||

| Finance expenses, net | 10,076 | 8,585 | |||||

| Accretion expenses | 25,751 | 11,214 | |||||

| Changes in derivatives and other fair value instruments | 38,783 | (24,511 | ) | ||||

| Foreign exchange (gain) loss | (9,000 | ) | 40,462 | ||||

| Share-based compensation expense (recovery) | 6,683 | (323 | ) | ||||

| Recognition of deferred revenue | (1,903 | ) | (1,645 | ) | |||

| Deferred revenue deposit | - | 18,244 | |||||

| Inventory sold or processed with write-ups to fair value | - | 1,905 | |||||

| Other operating activities | (482 | ) | 3,839 | ||||

| Net change in working capital | (13,580 | ) | (88 | ) | |||

| Cash provided by operating activities | 101,234 | 73,292 | |||||

| Investing activities | |||||||

| Gibraltar capitalized stripping costs | (5,986 | ) | (2,315 | ) | |||

| Gibraltar capital expenditures | (23,424 | ) | (26,799 | ) | |||

| Florence Copper development costs | (51,920 | ) | (84,470 | ) | |||

| Other project development costs | (2,729 | ) | (1,213 | ) | |||

| Other investing activities | 1,098 | 1,708 | |||||

| Cash used for investing activities | (82,961 | ) | (113,089 | ) | |||

| Financing activities | |||||||

| Interest paid | (33,338 | ) | (35,575 | ) | |||

| Repayments of revolving credit facility | (103,995 | ) | - | ||||

| Repayment of Gibraltar equipment financings | (8,766 | ) | (9,011 | ) | |||

| Proceeds from Gibraltar equipment financings | - | 15,673 | |||||

| Repayment of Florence Copper equipment financings | (2,460 | ) | (1,619 | ) | |||

| Proceeds from Florence Copper equipment financings | - | 14,135 | |||||

| Net proceeds from share issuances | 228,967 | 14,208 | |||||

| Proceeds from exercise of share options | 1,725 | 445 | |||||

| Cash provided by (used for) financing activities | 82,133 | (1,744 | ) | ||||

| Effect of exchange rate changes on cash | (3,216 | ) | 5,522 | ||||

| Increase (decrease) in cash | 97,190 | (36,019 | ) | ||||

| Cash, beginning of period | 90,771 | 208,751 | |||||

| Cash, end of period | 187,961 | 172,732 | |||||

TASEKO MINES LIMITED

Management's Discussion and Analysis

Earnings

| Three months ended December 31, | ||||||||||

| (Cdn$ in thousands) | 2025 | 2024 | Change | |||||||

| Net income (loss) | 4,454 | (21,207 | ) | 25,661 | ||||||

| Unrealized foreign exchange (gain) loss | (9,000 | ) | 40,462 | (49,462 | ) | |||||

| Unrealized loss (gain) and fair value adjustments on derivatives | 37,676 | (25,514 | ) | 63,190 | ||||||

| Accretion on Cariboo consideration payable | 4,048 | 4,543 | (495 | ) | ||||||

| Accretion on Florence royalty obligation | 18,415 | 3,682 | 14,733 | |||||||

| Other operating costs | - | 4,132 | (4,132 | ) | ||||||

| Realized gain on processing of ore stockpiles1 | - | 1,905 | (1,905 | ) | ||||||

| Estimated tax effect of adjustments | (14,068 | ) | 2,465 | (16,533 | ) | |||||

| Adjusted net income | 41,525 | 10,468 | 31,057 | |||||||

1 Realized gain on processing of ore stockpiles relates to ore stockpile inventories held at March 25, 2024 that was written-up to fair value as part of the acquisition of control of Gibraltar and subsequently processed. The realized portion of these gains have been added back to Adjusted net income in the period the inventories were processed.

Adjusted net income increased by $31.1 million to $41.5 million ($0.11 adjusted earnings per share) in the fourth quarter, compared to $10.5 million ($0.03 adjusted earnings per share) in the comparative prior year quarter, driven by higher revenues reflecting increased sales volumes and higher prevailing copper prices.

Net income was $4.5 million ($0.01 earnings per share) in the fourth quarter, which included unrealized losses and fair value adjustments on derivatives of $37.7 million, accretion on Florence royalty obligation of $18.4 million and accretion on Cariboo consideration payable of $4.0 million, primarily reflecting higher prevailing copper price trends in the quarter and the impact on the valuation of the respective instruments, partially offset by an unrealized foreign exchange gain of $7.3 million on the Company's US dollar-denominated debt.

Net loss was $21.2 million ($0.08 loss per share) in the comparative prior year quarter, which included an unrealized foreign exchange loss of $40.5 million due to a weaker Canadian dollar during the period and the effect on the Company's US dollar-denominated debt, accretion on Cariboo consideration payable of $4.5 million and accretion on Florence royalty obligation of $3.7 million, partially offset by unrealized gains and fair value adjustments on derivatives of $25.5 million due to the lower prevailing commodity prices during the period.

Revenues

| Three months ended December 31, | ||||||||||

| (Cdn$ in thousands) | 2025 | 2024 | Change | |||||||

| Copper contained in concentrate | 210,721 | 151,943 | 58,778 | |||||||

| Copper cathode | 6,081 | - | 6,081 | |||||||

| Molybdenum concentrate | 25,095 | 17,836 | 7,259 | |||||||

| Silver | 1,645 | 1,783 | (138 | ) | ||||||

| Gold | 619 | - | 619 | |||||||

| Total gross revenue | 244,161 | 171,562 | 72,599 | |||||||

| Treatment and refining costs | (394 | ) | (3,763 | ) | 3,369 | |||||

| Revenue | 243,767 | 167,799 | 75,968 | |||||||

TASEKO MINES LIMITED

Management's Discussion and Analysis

| Sales of copper in concentrate1 (thousand pounds) | 29,499 | 26,282 | 3,217 | |||||||

| Average realized copper price (US$ per pound) | 5.13 | 4.13 | 1.00 | |||||||

| Average LME copper price (US$ per pound) | 5.03 | 4.17 | 0.86 | |||||||

| Average exchange rate (CAD/USD) | 1.39 | 1.40 | (0.01 | ) |

1 Sales of copper in concentrate includes a net smelter payable deduction of approximately 3.5% to derive net payable pounds of copper sold.

Revenues from the sales of copper contained in concentrate increased by $58.8 million to $210.7 million in the fourth quarter, compared to $151.9 million in comparative prior year quarter. The increase was driven by a positive price variance of $41.9 million, reflecting a US$1.00 per pound higher average realized copper price, and a positive volume variance of $19.3 million, reflecting a higher payable sales volume of 3.2 million pounds, partially offset by a negative foreign exchange variance of $2.4 million due to a slightly weaker US dollar.

Copper cathode revenues were $6.1 million in the fourth quarter on sales of 0.8 million pounds of copper cathode produced from the Gibraltar SX/EW plant, supplementing revenues from the sales of copper contained in concentrate.

Molybdenum revenues increased by $7.3 million to $25.1 million in the fourth quarter, compared to $17.8 million in the comparative prior year quarter, and was primarily attributable to increased sales volumes as Gibraltar began to realize the higher expected molybdenum grades from Connector pit ore.

The Company also recorded gold revenues of $0.6 million in the fourth quarter as the Company benefited from payable gold under one of its concentrate offtake agreements for Gibraltar concentrate.

Treatment and refining costs decreased by $3.4 million to $0.4 million in the fourth quarter, compared to $3.8 million in the comparative prior year quarter, reflecting the favorable TCRC rates realized under the Company's 2025 offtake agreements.

Cost of sales

| Three months ended December 31, | ||||||||||

| (Cdn$ in thousands) | 2025 | 2024 | Change | |||||||

| Site operating costs | 119,585 | 100,495 | 19,090 | |||||||

| Transportation costs | 10,989 | 10,170 | 819 | |||||||

| Changes in inventories: | ||||||||||

| Changes in finished goods | 2,611 | (4,064 | ) | 6,675 | ||||||