.2

| Q1 2026 Earnings Presentation April 21, 2026 |

| 2 FORWARD-LOOKING STATEMENTS This presentation and statements by our management may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are statements that include, without limitation, statements regarding our acquisition of Sandy Spring Bancorp, Inc. (“Sandy Spring”), including expectations with regard to the benefits of the Sandy Spring acquisition; statements regarding our strategic expansion into North Carolina; statements regarding our business, financial and operating results, including our deposit base and funding; the impact of changes in economic conditions, anticipated changes in the interest rate environment and the related impacts on our net interest margin, changes in economic, fiscal or trade policy and the potential impacts on our business, loan demand and economic conditions in our markets and nationally; management’s beliefs regarding our liquidity, capital resources, asset quality, CRE loan portfolio and our customer relationships; statements regarding our strategy, statements that include other projections, predictions, expectations, or beliefs about future events or results or otherwise are not statements of historical fact, and statements on the slides entitled “Highlights”, “The Next Phase – Harnessing Organic Power” and “2026 Financial Outlook”. Such forward-looking statements are based on certain assumptions as of the time they are made, and are inherently subject to known and unknown risks, uncertainties, and other factors, some of which cannot be predicted or quantified, that may cause actual results, performance, or achievements to be materially different from those expressed or implied by such forward-looking statements. Forward-looking statements are often characterized by the use of qualified words (and their derivatives) such as “expect,” “believe,” “estimate,” “plan,” “project,” “anticipate,” “intend,” “will,” “may,” “view,” “opportunity,” “seek to,” “potential,” “continue,” “confidence,” or words of similar meaning or other statements concerning opinions or judgment of Atlantic Union Bankshares Corporation (the “Company,” “AUB,” “we,” “us” or “our”) and our management about future events. Although we believe that our expectations with respect to forward-looking statements are based on reasonable assumptions within the bounds of our existing knowledge of our business and operations, there can be no assurance that actual future results, performance, or achievements of, or trends affecting, us will not differ materially from any projected future results, performance, achievements or trends expressed or implied by such forward-looking statements. Actual future results, performance, achievements or trends may differ materially from historical results or those anticipated depending on a variety of factors, including, but not limited to, the effects of or changes in: • market interest rates and their related impacts on macroeconomic conditions, customer and client behavior, our funding costs and our loan and securities portfolios; • economic conditions, including inflation and recessionary conditions and their related impacts on economic growth and customer and client behavior; • U.S. and global trade policies and tensions, including changes in, or the imposition of, tariffs and/or trade barriers and the economic impacts, volatility and uncertainty resulting therefrom, and geopolitical instability; • volatility in the financial services sector, including failures or rumors of failures of other depository institutions, along with actions taken by governmental agencies to address such turmoil, and the effects on the ability of depository institutions, including us, to attract and retain depositors and to borrow or raise capital; • legislative or regulatory changes and requirements, including changes in federal state or local tax laws and changes impacting the rulemaking, supervision, examination and enforcement priorities of the federal banking agencies; • the sufficiency of liquidity and changes in our capital position; • general economic and financial market conditions in the United States generally and particularly in the markets in which we operate and which our loans are concentrated, including the effects of declines in real estate values, an increase in unemployment levels, U.S. fiscal debt, budget and tax matters, U.S. government shutdowns, and slowdowns in economic growth; • the impact of purchase accounting with respect to the Sandy Spring acquisition, or any change in the assumptions used regarding the assets acquired and liabilities assumed to determine the fair value and credit marks; • the possibility that the anticipated benefits of our acquisition activity, including our acquisitions of Sandy Spring and American National, including anticipated cost savings and strategic gains, are not realized when expected or at all, including as a result of the strength of the economy, competitive factors in the areas where we do business, or as a result of other unexpected factors or events; • potential adverse reactions or changes to business or employee relationships, including those resulting from our acquisitions of Sandy Spring and American National; • our ability to identify, recruit and retain key employees • monetary, fiscal and regulatory policies of the U.S. government, including policies of the U.S. Department of the Treasury and the Federal Reserve; • the quality or composition of our loan or investment portfolios and changes in these portfolios; • demand for loan products and financial services in our market areas; • our ability to manage our growth or implement our growth strategy; • the effectiveness of expense reduction plans; • the introduction of new lines of business or new products and services; • real estate values in our lending area; • changes in accounting principles, standards, rules, and interpretations, and the related impact on our financial statements; • an insufficient ACL or volatility in the ACL resulting from the CECL methodology, either alone or as that may be affected by changing economic conditions, credit concentrations, inflation, changing interest rates, or other factors; • concentrations of loans secured by real estate, particularly commercial real estate; • the effectiveness of our credit processes and management of our credit risk; • our ability to compete in the market for financial services and increased competition from fintech companies; • technological risks and developments, and cyber threats, attacks, or events; • emerging issues related to the development and use of artificial intelligence that could give rise to legal or regulatory action or increase the risk of a cybersecurity attack or the probability that such an attack would be successful; • operational, technological, cultural, regulatory, legal, credit, and other risks associated with the exploration, consummation and integration of potential future acquisitions, whether involving stock or cash consideration; • the potential adverse effects of unusual and infrequently occurring events, such as weather-related disasters, terrorist acts, geopolitical conflicts or public health events (such as pandemics), and of governmental and societal responses thereto; these potential adverse effects may include, without limitation, adverse effects on macroeconomic conditions, the ability of our borrowers to satisfy their obligations to us, on the value of collateral securing loans, on the demand for our loans or our other products and services, on supply chains and methods used to distribute products and services, on incidents of cyberattack and fraud, on our liquidity or capital positions, on risks posed by reliance on third-party service providers, on other aspects of our business operations and on financial markets and economic growth; • performance by our counterparties or vendors; • deposit flows; • the availability of financing and the terms thereof; • the level of prepayments on loans and mortgage-backed securities; • actual or potential claims, damages, and fines related to litigation or government actions, which may result in, among other things, additional costs, fines, penalties, restrictions on our business activities, reputational harm, or other adverse consequences; • any event or development that would cause us to conclude that there was an impairment of any asset, including intangible assets, such as goodwill; and • other factors, many of which are beyond our control. Please also refer to such other factors as discussed throughout Part I, Item 1A. “Risk Factors” and Part II, Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations” of our Annual Report on Form 10-K for the year ended December 31, 2025, and related disclosures in other filings, which have been filed with the U.S. Securities and Exchange Commission (“SEC”) and are available on the SEC’s website at www.sec.gov. All risk factors and uncertainties described herein and therein should be considered in evaluating forward-looking statements, and all forward-looking statements are expressly qualified by the cautionary statements contained or referred to herein and therein. The actual results or developments anticipated may not be realized or, even if substantially realized, they may not have the expected consequences to or effects on the Company or our businesses or operations. Readers are cautioned not to rely too heavily on forward-looking statements. Forward-looking statements speak only as of the date they are made. We do not intend or assume any obligation to update, revise or clarify any forward-looking statements that may be made from time to time by or on behalf of the Company, whether because of new information, future events or otherwise, except as required by law. |

| 3 ADDITIONAL INFORMATION Non-GAAP Financial Measures This presentation contains certain financial information determined by methods other than in accordance with generally accepted accounting principles in the United States (“GAAP”). These non-GAAP financial measures are a supplement to GAAP, which is used to prepare our financial statements, and should not be considered in isolation or as a substitute for comparable measures calculated in accordance with GAAP. In addition, our non-GAAP financial measures may not be comparable to non-GAAP financial measures of other companies. We use the non-GAAP financial measures discussed herein in our analysis of our performance. Our management believes that these non-GAAP financial measures provide additional understanding of ongoing operations, enhance comparability of results of operations with prior periods, show the effects of significant gains and charges in the periods presented without the impact of items or events that may obscure trends in our underlying performance, or show the potential effects of accumulated other comprehensive income (or AOCI) or unrealized losses on securities on our capital. This presentation also includes certain projections of non-GAAP financial measures. Due to the inherent variability and difficulty associated with making accurate forecasts and projections of information that is excluded from these projected non-GAAP measures, and the fact that some of the excluded information is not currently ascertainable or accessible, we are unable to quantify certain amounts that would be required to be included in the most directly comparable projected GAAP financial measures without unreasonable effort. Consequently, no disclosure of projected comparable GAAP measures is included, and no reconciliation of forward-looking non-GAAP financial information is included. Please see “Reconciliation of Non-GAAP Disclosures” at the end of this presentation for a reconciliation to the nearest GAAP financial measure. No Offer or Solicitation This presentation does not constitute an offer to sell or a solicitation of an offer to buy any securities. No offer of securities shall be made except by means of a prospectus meeting the requirements of the Securities Act of 1933, as amended, and no offer to sell or solicitation of an offer to buy shall be made in any jurisdiction in which such offer, solicitation or sale would be unlawful. Market and Industry Data Unless otherwise indicated, market data and certain industry forecast data used in this presentation were obtained from internal reports, where appropriate, as well as third party sources and other publicly available information. Data regarding the industries and markets in which the Company competes, its market position and market share within these industries are inherently imprecise and are subject to significant business, economic and competitive uncertainties beyond the Company's control. In addition, assumptions and estimates of the Company and its industries' future performance are necessarily subject to a high degree of uncertainty and risk due to a variety of factors. These and other factors could cause future performance to differ materially from assumptions and estimates. About Atlantic Union Bankshares Corporation Headquartered in Richmond, Virginia, Atlantic Union Bankshares Corporation (NYSE: AUB) is the holding company for Atlantic Union Bank. Atlantic Union Bank has branches and ATMs located in Virginia, Maryland, North Carolina and Washington, D.C. Certain non-bank financial services affiliates of Atlantic Union Bank include: Atlantic Union Equipment Finance, Inc., which provides equipment financing; AUB Investments, Inc., which provides investment services; and Atlantic Union Capital Markets, Inc., which provides capital market services. |

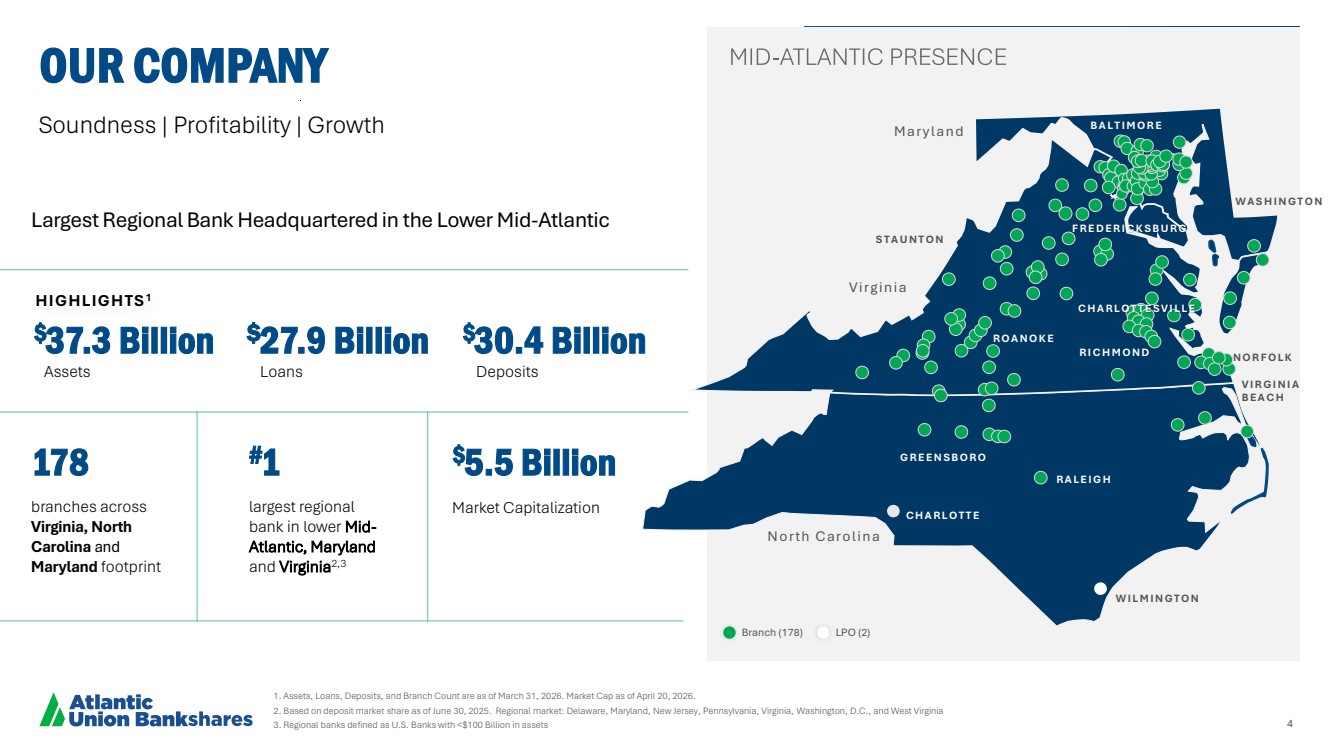

| 4 N O R F O L K V I R G I N I A B E A C H M a ry l a n d V irg in ia No rth C a ro l in a C H A R L O T T E W I L M I N G T O N B A L T I M O R E R A L E I G H G R E E N S B O R O W A S H I N G T O N R O A N O K E S T A U N T O N C H A R L O T T E S V I L L E R I C H M O N D F R E D E R I C K S B U R G HIGHLIGHTS1 branches across Virginia, North Carolina and Maryland footprint 178 largest regional bank in lower Mid-Atlantic, Maryland and Virginia2,3 #1 $37.3 Billion Assets $27.9 Billion Loans $30.4 Billion Deposits $5.5 Billion Market Capitalization Soundness | Profitability | Growth 1. Assets, Loans, Deposits, and Branch Count are as of March 31, 2026. Market Cap as of April 20, 2026. 2. Based on deposit market share as of June 30, 2025. Regional market: Delaware, Maryland, New Jersey, Pennsylvania, Virginia, Washington, D.C., and West Virginia 3. Regional banks defined as U.S. Banks with <$100 Billion in assets OUR COMPANY Branch (178) LPO (2) Largest Regional Bank Headquartered in the Lower Mid-Atlantic |

| 5 Dense, uniquely valuable presence across attractive markets FINANCIAL STRENGTH Solid balance sheet & capital levels PEER-LEADING PERFORMANCE Committed to top-tier financial performance ATTRACTIVE FINANCIAL PROFILE Solid dividend yield & payout ratio with earnings upside STRONG GROWTH POTENTIAL Organic & acquisition opportunities OUR SHAREHOLDER VALUE PROPOSITION Positioned for growth and long-term shareholder value creation as a preeminent regional bank with a leading presence in attractive markets LEADING REGIONAL PRESENCE |

| AUB Q1 2026 FINANCIAL RESULTS |

| 7 1. For non-GAAP financial measures, see reconciliation to most directly comparable GAAP measure in "Appendix - Reconciliation of Non-GAAP Disclosures” HIGHLIGHTS Q1 2026 LOANS & DEPOSITS Loan growth was approximately 2.2% annualized in Q1 2026 Non-interest bearing deposits at 23% of total deposits at March 31, 2026 Loan/Deposit ratio of 92.0% at March 31, 2026 POSITIONING FOR LONG TERM Lending pipelines remain healthy and are higher than at the start of Q1 2026 Focused on generating positive operating leverage DIFFERENTIATED CLIENT EXPERIENCE Responsive, strong and capable alternative to large national banks, while competitive with and more capable than smaller banks CAPITALIZE ON STRATEGIC OPPORTUNITIES Focused on execution after completion of Sandy Spring franchise integration Organic expansion in North Carolina planned in 2026 FINANCIAL RATIOS Q1 2026 adjusted operating return on tangible common equity of 19.6%1 Q1 2026 adjusted operating return on assets of 1.41%1 Q1 2026 adjusted operating efficiency ratio (FTE) of 49.9%1 ASSET QUALITY Q1 2026 annualized net charge-offs at 2 basis points of total average loans held for investment Allowance for Credit Loss as a percentage of loans held for investment of 1.15% 7 |

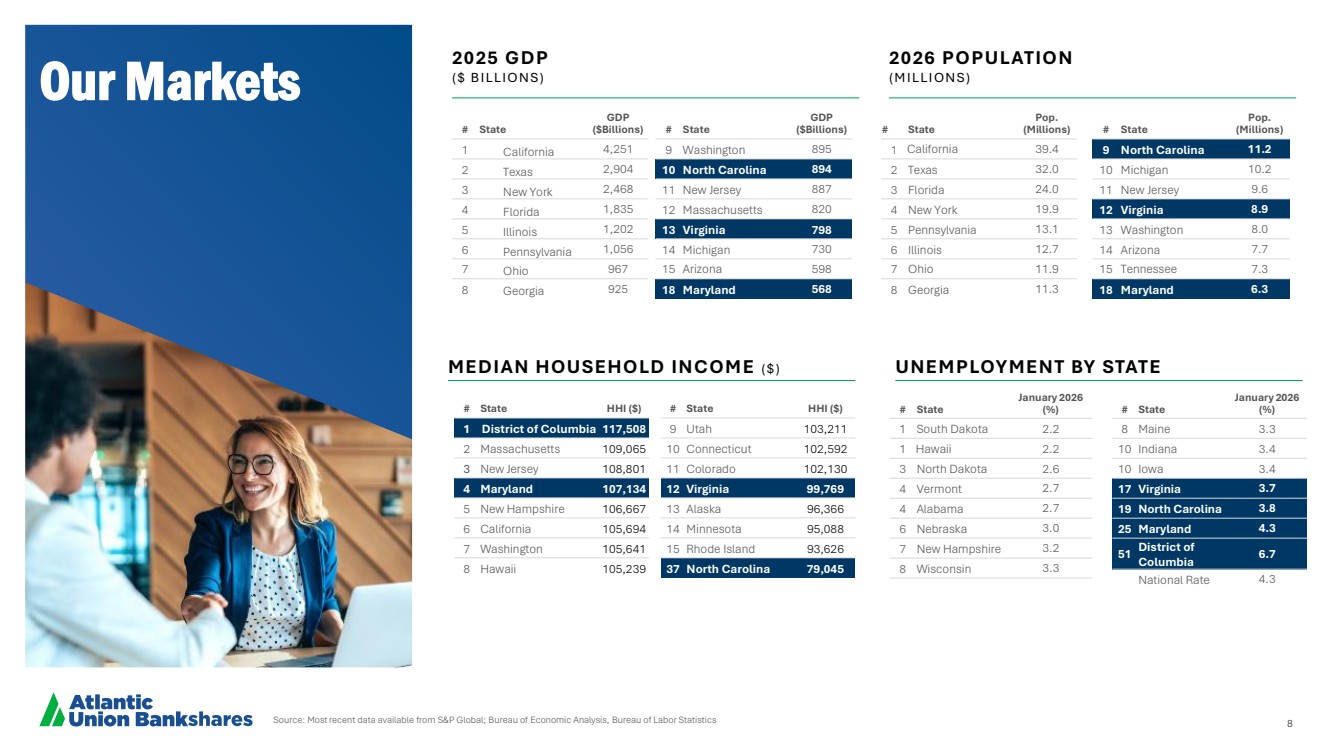

| 8 Source: Most recent data available from S&P Global; Bureau of Economic Analysis, Bureau of Labor Statistics Our Markets # State Pop. (Millions) 1 California 39.4 2 Texas 32.0 3 Florida 24.0 4 New York 19.9 5 Pennsylvania 13.1 6 Illinois 12.7 7 Ohio 11.9 8 Georgia 11.3 # State HHI ($) 1 District of Columbia 117,508 2 Massachusetts 109,065 3 New Jersey 108,801 4 Maryland 107,134 5 New Hampshire 106,667 6 California 105,694 7 Washington 105,641 8 Hawaii 105,239 # State GDP ($Billions) 1 California 4,251 2 Texas 2,904 3 New York 2,468 4 Florida 1,835 5 Illinois 1,202 6 Pennsylvania 1,056 7 Ohio 967 8 Georgia 925 # State Pop. (Millions) 9 North Carolina 11.2 10 Michigan 10.2 11 New Jersey 9.6 12 Virginia 8.9 13 Washington 8.0 14 Arizona 7.7 15 Tennessee 7.3 18 Maryland 6.3 # State HHI ($) 9 Utah 103,211 10 Connecticut 102,592 11 Colorado 102,130 12 Virginia 99,769 13 Alaska 96,366 14 Minnesota 95,088 15 Rhode Island 93,626 37 North Carolina 79,045 # State GDP ($Billions) 9 Washington 895 10 North Carolina 894 11 New Jersey 887 12 Massachusetts 820 13 Virginia 798 14 Michigan 730 15 Arizona 598 18 Maryland 568 MEDIAN HOUSEHOLD INCOME ($) 2026 POPULATION ( M I LLI O N S ) 2025 GDP ( $ B I LLI O N S ) UNEMPLOYMENT BY STATE # State January 2026 (%) 1 South Dakota 2.2 1 Hawaii 2.2 3 North Dakota 2.6 4 Vermont 2.7 4 Alabama 2.7 6 Nebraska 3.0 7 New Hampshire 3.2 8 Wisconsin 3.3 # State January 2026 (%) 8 Maine 3.3 10 Indiana 3.4 10 Iowa 3.4 17 Virginia 3.7 19 North Carolina 3.8 25 Maryland 4.3 51 District of Columbia 6.7 National Rate 4.3 |

| 9 THE NEXT PHASE Harnessing Organic Power With the franchise now established, our focus is on maximizing its potential: We Believe AUB Was Built For This Moment We have invested the capital, built the platform, and assembled the team. Now is the time to demonstrate the power of what we have built— delivering sustainable, top-tier performance and returns. Organic growth Deepening relationships, growing our company organically, and leveraging our scale efficiently. Capital generation Shifting from capital deployment to capital creation, targeting top tier returns, earnings growth, and tangible book value per share growth. Disciplined execution Delivering on the promises made to our stakeholders. |

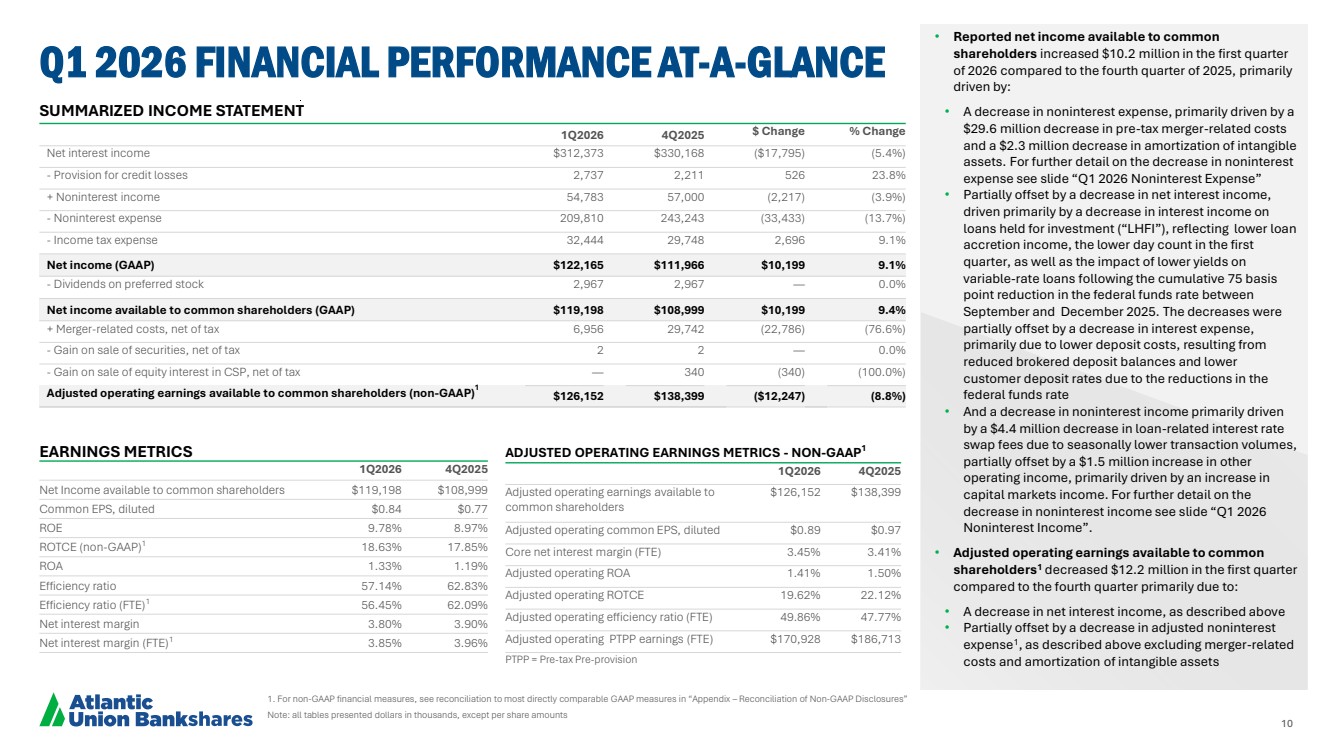

| 10 • Reported net income available to common shareholders increased $10.2 million in the first quarter of 2026 compared to the fourth quarter of 2025, primarily driven by: • A decrease in noninterest expense, primarily driven by a $29.6 million decrease in pre-tax merger-related costs and a $2.3 million decrease in amortization of intangible assets. For further detail on the decrease in noninterest expense see slide “Q1 2026 Noninterest Expense” • Partially offset by a decrease in net interest income, driven primarily by a decrease in interest income on loans held for investment (“LHFI”), reflecting lower loan accretion income, the lower day count in the first quarter, as well as the impact of lower yields on variable-rate loans following the cumulative 75 basis point reduction in the federal funds rate between September and December 2025. The decreases were partially offset by a decrease in interest expense, primarily due to lower deposit costs, resulting from reduced brokered deposit balances and lower customer deposit rates due to the reductions in the federal funds rate • And a decrease in noninterest income primarily driven by a $4.4 million decrease in loan-related interest rate swap fees due to seasonally lower transaction volumes, partially offset by a $1.5 million increase in other operating income, primarily driven by an increase in capital markets income. For further detail on the decrease in noninterest income see slide “Q1 2026 Noninterest Income”. • Adjusted operating earnings available to common shareholders1 decreased $12.2 million in the first quarter compared to the fourth quarter primarily due to: • A decrease in net interest income, as described above • Partially offset by a decrease in adjusted noninterest expense1 , as described above excluding merger-related costs and amortization of intangible assets 1. For non-GAAP financial measures, see reconciliation to most directly comparable GAAP measures in “Appendix – Reconciliation of Non-GAAP Disclosures” Note: all tables presented dollars in thousands, except per share amounts Q1 2026 FINANCIAL PERFORMANCE AT-A-GLANCE SUMMARIZED INCOME STATEMENT 1Q2026 4Q2025 $ Change % Change Net interest income $312,373 $330,168 ($17,795) (5.4%) - Provision for credit losses 2,737 2,211 526 23.8% + Noninterest income 54,783 57,000 (2,217) (3.9%) - Noninterest expense 209,810 243,243 (33,433) (13.7%) - Income tax expense 32,444 29,748 2,696 9.1% Net income (GAAP) $122,165 $111,966 $10,199 9.1% - Dividends on preferred stock 2,967 2,967 — 0.0% Net income available to common shareholders (GAAP) $119,198 $108,999 $10,199 9.4% + Merger-related costs, net of tax 6,956 29,742 (22,786) (76.6%) - Gain on sale of securities, net of tax 2 2 — 0.0% - Gain on sale of equity interest in CSP, net of tax — 340 (340) (100.0%) Adjusted operating earnings available to common shareholders (non-GAAP)1 $126,152 $138,399 ($12,247) (8.8%) EARNINGS METRICS 1Q2026 4Q2025 Net Income available to common shareholders $119,198 $108,999 Common EPS, diluted $0.84 $0.77 ROE 9.78% 8.97% ROTCE (non-GAAP)1 18.63% 17.85% ROA 1.33% 1.19% Efficiency ratio 57.14% 62.83% Efficiency ratio (FTE)1 56.45% 62.09% Net interest margin 3.80% 3.90% Net interest margin (FTE)1 3.85% 3.96% ADJUSTED OPERATING EARNINGS METRICS - NON-GAAP1 1Q2026 4Q2025 Adjusted operating earnings available to common shareholders $126,152 $138,399 Adjusted operating common EPS, diluted $0.89 $0.97 Core net interest margin (FTE) 3.45% 3.41% Adjusted operating ROA 1.41% 1.50% Adjusted operating ROTCE 19.62% 22.12% Adjusted operating efficiency ratio (FTE) 49.86% 47.77% Adjusted operating PTPP earnings (FTE) $170,928 $186,713 PTPP = Pre-tax Pre-provision |

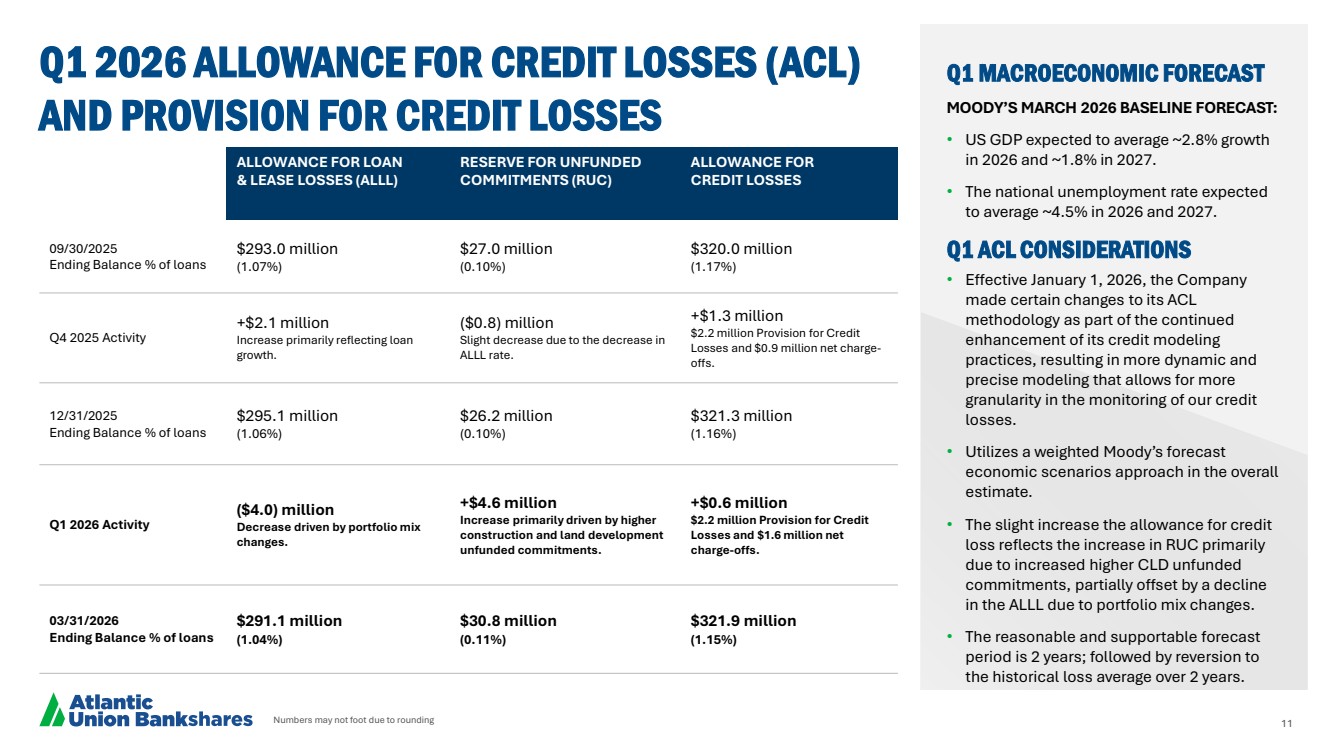

| 11 Numbers may not foot due to rounding Q1 2026 ALLOWANCE FOR CREDIT LOSSES (ACL) AND PROVISION FOR CREDIT LOSSES Q1 MACROECONOMIC FORECAST Q1 ACL CONSIDERATIONS MOODY’S MARCH 2026 BASELINE FORECAST: • US GDP expected to average ~2.8% growth in 2026 and ~1.8% in 2027. • The national unemployment rate expected to average ~4.5% in 2026 and 2027. • Effective January 1, 2026, the Company made certain changes to its ACL methodology as part of the continued enhancement of its credit modeling practices, resulting in more dynamic and precise modeling that allows for more granularity in the monitoring of our credit losses. • Utilizes a weighted Moody’s forecast economic scenarios approach in the overall estimate. • The slight increase the allowance for credit loss reflects the increase in RUC primarily due to increased higher CLD unfunded commitments, partially offset by a decline in the ALLL due to portfolio mix changes. • The reasonable and supportable forecast period is 2 years; followed by reversion to the historical loss average over 2 years. ALLOWANCE FOR LOAN & LEASE LOSSES (ALLL) RESERVE FOR UNFUNDED COMMITMENTS (RUC) ALLOWANCE FOR CREDIT LOSSES 09/30/2025 Ending Balance % of loans $293.0 million (1.07%) $27.0 million (0.10%) $320.0 million (1.17%) Q4 2025 Activity +$2.1 million Increase primarily reflecting loan growth. ($0.8) million Slight decrease due to the decrease in ALLL rate. +$1.3 million $2.2 million Provision for Credit Losses and $0.9 million net charge-offs. 12/31/2025 Ending Balance % of loans $295.1 million (1.06%) $26.2 million (0.10%) $321.3 million (1.16%) Q1 2026 Activity ($4.0) million Decrease driven by portfolio mix changes. +$4.6 million Increase primarily driven by higher construction and land development unfunded commitments. +$0.6 million $2.2 million Provision for Credit Losses and $1.6 million net charge-offs. 03/31/2026 Ending Balance % of loans $291.1 million (1.04%) $30.8 million (0.11%) $321.9 million (1.15%) |

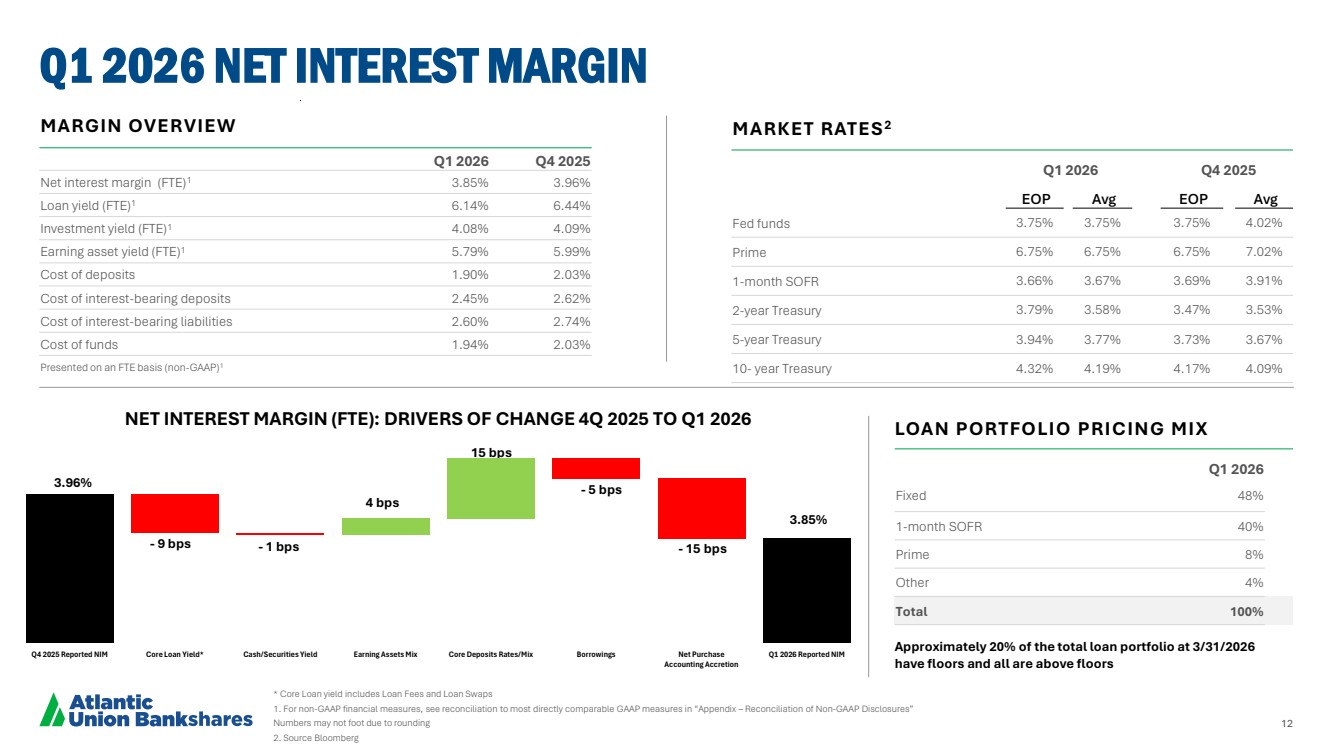

| 12 * Core Loan yield includes Loan Fees and Loan Swaps 1. For non-GAAP financial measures, see reconciliation to most directly comparable GAAP measures in “Appendix – Reconciliation of Non-GAAP Disclosures” Numbers may not foot due to rounding 2. Source Bloomberg Q1 2026 NET INTEREST MARGIN MARKET RATES2 Q1 2026 Q4 2025 EOP Avg EOP Avg Fed funds 3.75% 3.75% 3.75% 4.02% Prime 6.75% 6.75% 6.75% 7.02% 1-month SOFR 3.66% 3.67% 3.69% 3.91% 2-year Treasury 3.79% 3.58% 3.47% 3.53% 5-year Treasury 3.94% 3.77% 3.73% 3.67% 10- year Treasury 4.32% 4.19% 4.17% 4.09% MARGIN OVERVIEW Q1 2026 Q4 2025 Net interest margin (FTE)1 3.85% 3.96% Loan yield (FTE)1 6.14% 6.44% Investment yield (FTE)1 4.08% 4.09% Earning asset yield (FTE)1 5.79% 5.99% Cost of deposits 1.90% 2.03% Cost of interest-bearing deposits 2.45% 2.62% Cost of interest-bearing liabilities 2.60% 2.74% Cost of funds 1.94% 2.03% Presented on an FTE basis (non-GAAP)1 Approximately 20% of the total loan portfolio at 3/31/2026 have floors and all are above floors LOAN PORTFOLIO PRICING MIX Q1 2026 Fixed 48% 1-month SOFR 40% Prime 8% Other 4% Total 100% 3.83% - 9 bps - 1 bps 3.85% 15 bps - 5 bps 4 bps 3.96% - 15 bps Q4 2025 Reported NIM Core Loan Yield* Cash/Securities Yield Earning Assets Mix Core Deposits Rates/Mix Borrowings Net Purchase Accounting Accretion Q1 2026 Reported NIM NET INTEREST MARGIN (FTE): DRIVERS OF CHANGE 4Q 2025 TO Q1 2026 |

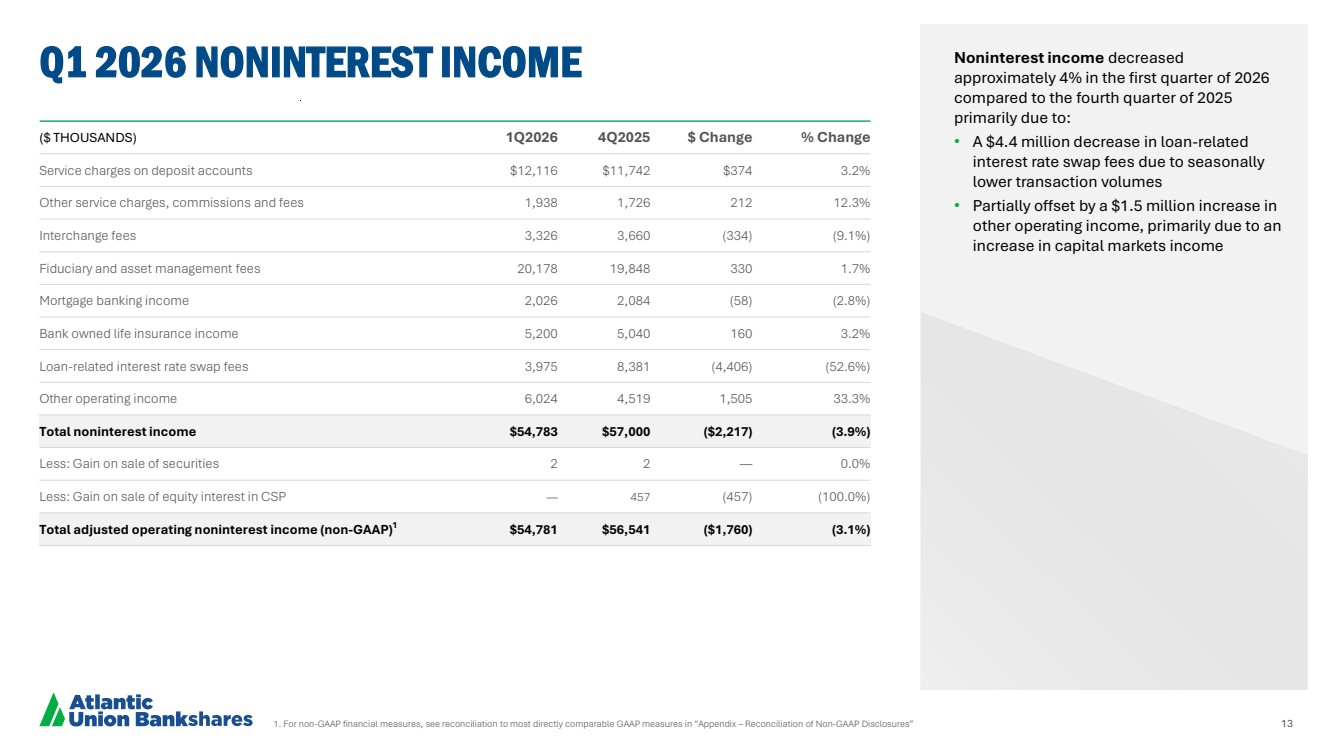

| 1. For non-GAAP financial measures, see reconciliation to most directly comparable GAAP measures in “Appendix – Reconciliation of Non-GAAP Disclosures” 13 Q1 2026 NONINTEREST INCOME Noninterest income decreased approximately 4% in the first quarter of 2026 compared to the fourth quarter of 2025 primarily due to: • A $4.4 million decrease in loan-related interest rate swap fees due to seasonally lower transaction volumes • Partially offset by a $1.5 million increase in other operating income, primarily due to an increase in capital markets income ($ THOUSANDS) 1Q2026 4Q2025 $ Change % Change Service charges on deposit accounts $12,116 $11,742 $374 3.2% Other service charges, commissions and fees 1,938 1,726 212 12.3% Interchange fees 3,326 3,660 (334) (9.1%) Fiduciary and asset management fees 20,178 19,848 330 1.7% Mortgage banking income 2,026 2,084 (58) (2.8%) Bank owned life insurance income 5,200 5,040 160 3.2% Loan-related interest rate swap fees 3,975 8,381 (4,406) (52.6%) Other operating income 6,024 4,519 1,505 33.3% Total noninterest income $54,783 $57,000 ($2,217) (3.9%) Less: Gain on sale of securities 2 2 — 0.0% Less: Gain on sale of equity interest in CSP — 457 (457) (100.0%) Total adjusted operating noninterest income (non-GAAP)1 $54,781 $56,541 ($1,760) (3.1%) |

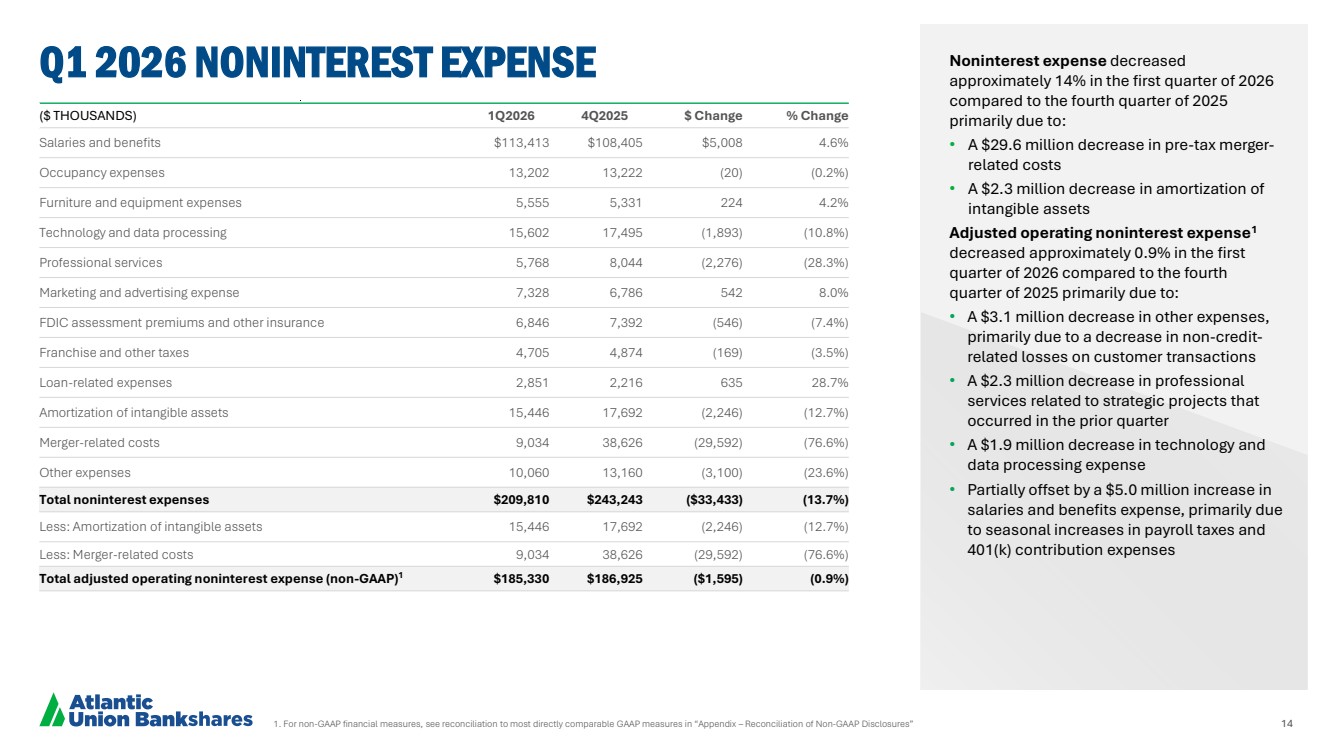

| 1. For non-GAAP financial measures, see reconciliation to most directly comparable GAAP measures in “Appendix – Reconciliation of Non-GAAP Disclosures” 14 Q1 2026 NONINTEREST EXPENSE Noninterest expense decreased approximately 14% in the first quarter of 2026 compared to the fourth quarter of 2025 primarily due to: • A $29.6 million decrease in pre-tax merger-related costs • A $2.3 million decrease in amortization of intangible assets Adjusted operating noninterest expense1 decreased approximately 0.9% in the first quarter of 2026 compared to the fourth quarter of 2025 primarily due to: • A $3.1 million decrease in other expenses, primarily due to a decrease in non-credit-related losses on customer transactions • A $2.3 million decrease in professional services related to strategic projects that occurred in the prior quarter • A $1.9 million decrease in technology and data processing expense • Partially offset by a $5.0 million increase in salaries and benefits expense, primarily due to seasonal increases in payroll taxes and 401(k) contribution expenses ($ THOUSANDS) 1Q2026 4Q2025 $ Change % Change Salaries and benefits $113,413 $108,405 $5,008 4.6% Occupancy expenses 13,202 13,222 (20) (0.2%) Furniture and equipment expenses 5,555 5,331 224 4.2% Technology and data processing 15,602 17,495 (1,893) (10.8%) Professional services 5,768 8,044 (2,276) (28.3%) Marketing and advertising expense 7,328 6,786 542 8.0% FDIC assessment premiums and other insurance 6,846 7,392 (546) (7.4%) Franchise and other taxes 4,705 4,874 (169) (3.5%) Loan-related expenses 2,851 2,216 635 28.7% Amortization of intangible assets 15,446 17,692 (2,246) (12.7%) Merger-related costs 9,034 38,626 (29,592) (76.6%) Other expenses 10,060 13,160 (3,100) (23.6%) Total noninterest expenses $209,810 $243,243 ($33,433) (13.7%) Less: Amortization of intangible assets 15,446 17,692 (2,246) (12.7%) Less: Merger-related costs 9,034 38,626 (29,592) (76.6%) Total adjusted operating noninterest expense (non-GAAP)1 $185,330 $186,925 ($1,595) (0.9%) |

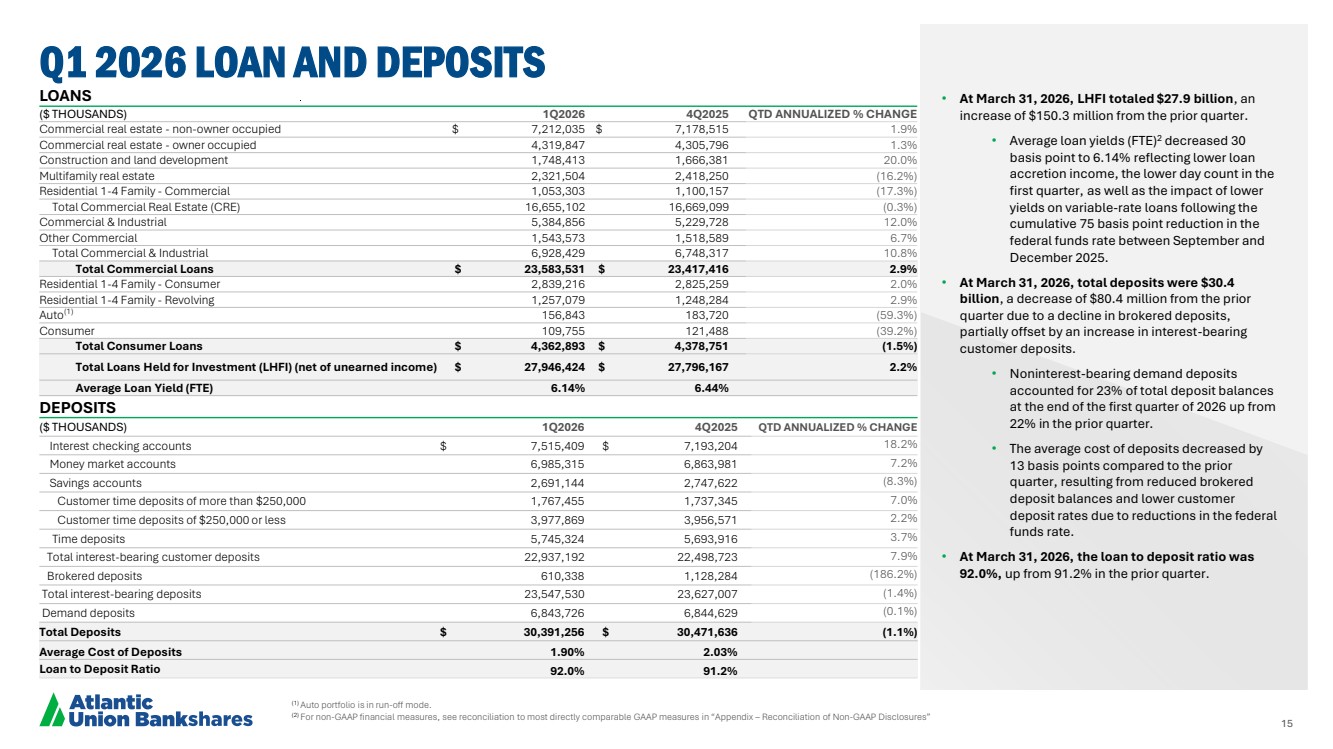

| 15 Q1 2026 LOAN AND DEPOSITS • At March 31, 2026, LHFI totaled $27.9 billion, an increase of $150.3 million from the prior quarter. • Average loan yields (FTE)2 decreased 30 basis point to 6.14% reflecting lower loan accretion income, the lower day count in the first quarter, as well as the impact of lower yields on variable-rate loans following the cumulative 75 basis point reduction in the federal funds rate between September and December 2025. • At March 31, 2026, total deposits were $30.4 billion, a decrease of $80.4 million from the prior quarter due to a decline in brokered deposits, partially offset by an increase in interest-bearing customer deposits. • Noninterest-bearing demand deposits accounted for 23% of total deposit balances at the end of the first quarter of 2026 up from 22% in the prior quarter. • The average cost of deposits decreased by 13 basis points compared to the prior quarter, resulting from reduced brokered deposit balances and lower customer deposit rates due to reductions in the federal funds rate. • At March 31, 2026, the loan to deposit ratio was 92.0%, up from 91.2% in the prior quarter. (1) Auto portfolio is in run-off mode. (2) For non-GAAP financial measures, see reconciliation to most directly comparable GAAP measures in “Appendix – Reconciliation of Non-GAAP Disclosures” LOANS ($ THOUSANDS) 1Q2026 4Q2025 QTD ANNUALIZED % CHANGE Commercial real estate - non-owner occupied $ 7,212,035 $ 7,178,515 1.9% Commercial real estate - owner occupied 4,319,847 4,305,796 1.3% Construction and land development 1,748,413 1,666,381 20.0% Multifamily real estate 2,321,504 2,418,250 (16.2%) Residential 1-4 Family - Commercial 1,053,303 1,100,157 (17.3%) Total Commercial Real Estate (CRE) 16,655,102 16,669,099 (0.3%) Commercial & Industrial 5,384,856 5,229,728 12.0% Other Commercial 1,543,573 1,518,589 6.7% Total Commercial & Industrial 6,928,429 6,748,317 10.8% Total Commercial Loans $ 23,583,531 $ 23,417,416 2.9% Residential 1-4 Family - Consumer 2,839,216 2,825,259 2.0% Residential 1-4 Family - Revolving 1,257,079 1,248,284 2.9% Auto(1) 156,843 183,720 (59.3%) Consumer 109,755 121,488 (39.2%) Total Consumer Loans $ 4,362,893 $ 4,378,751 (1.5%) Total Loans Held for Investment (LHFI) (net of unearned income) $ 27,946,424 $ 27,796,167 2.2% Average Loan Yield (FTE) 6.14% 6.44% DEPOSITS ($ THOUSANDS) 1Q2026 4Q2025 QTD ANNUALIZED % CHANGE Interest checking accounts $ 7,515,409 $ 7,193,204 18.2% Money market accounts 6,985,315 6,863,981 7.2% Savings accounts 2,691,144 2,747,622 (8.3%) Customer time deposits of more than $250,000 1,767,455 1,737,345 7.0% Customer time deposits of $250,000 or less 3,977,869 3,956,571 2.2% Time deposits 5,745,324 5,693,916 3.7% Total interest-bearing customer deposits 22,937,192 22,498,723 7.9% Brokered deposits 610,338 1,128,284 (186.2%) Total interest-bearing deposits 23,547,530 23,627,007 (1.4%) Demand deposits 6,843,726 6,844,629 (0.1%) Total Deposits $ 30,391,256 $ 30,471,636 (1.1%) Average Cost of Deposits 1.90% 2.03% Loan to Deposit Ratio 92.0% 91.2% |

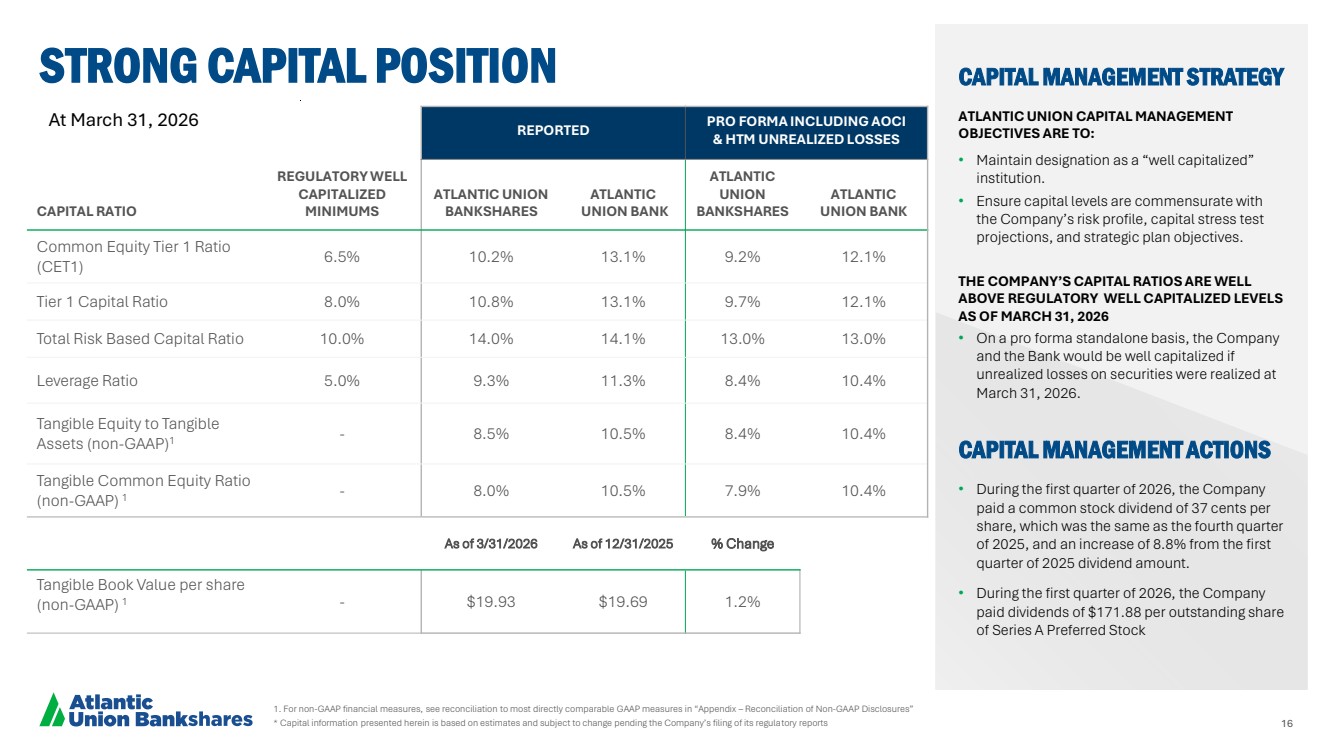

| 16 CAPITAL RATIO REGULATORY WELL CAPITALIZED MINIMUMS REPORTED PRO FORMA INCLUDING AOCI & HTM UNREALIZED LOSSES ATLANTIC UNION BANKSHARES ATLANTIC UNION BANK ATLANTIC UNION BANKSHARES ATLANTIC UNION BANK Common Equity Tier 1 Ratio (CET1) 6.5% 10.2% 13.1% 9.2% 12.1% Tier 1 Capital Ratio 8.0% 10.8% 13.1% 9.7% 12.1% Total Risk Based Capital Ratio 10.0% 14.0% 14.1% 13.0% 13.0% Leverage Ratio 5.0% 9.3% 11.3% 8.4% 10.4% Tangible Equity to Tangible Assets (non-GAAP)1 - 8.5% 10.5% 8.4% 10.4% Tangible Common Equity Ratio (non-GAAP) 1 - 8.0% 10.5% 7.9% 10.4% As of 3/31/2026 As of 12/31/2025 % Change Tangible Book Value per share (non-GAAP) 1 - $19.93 $19.69 1.2% 1. For non-GAAP financial measures, see reconciliation to most directly comparable GAAP measures in “Appendix – Reconciliation of Non-GAAP Disclosures” * Capital information presented herein is based on estimates and subject to change pending the Company’s filing of its regulatory reports STRONG CAPITAL POSITION CAPITAL MANAGEMENT STRATEGY ATLANTIC UNION CAPITAL MANAGEMENT OBJECTIVES ARE TO: • Maintain designation as a “well capitalized” institution. • Ensure capital levels are commensurate with the Company’s risk profile, capital stress test projections, and strategic plan objectives. THE COMPANY’S CAPITAL RATIOS ARE WELL ABOVE REGULATORY WELL CAPITALIZED LEVELS AS OF MARCH 31, 2026 • On a pro forma standalone basis, the Company and the Bank would be well capitalized if unrealized losses on securities were realized at March 31, 2026. CAPITAL MANAGEMENT ACTIONS • During the first quarter of 2026, the Company paid a common stock dividend of 37 cents per share, which was the same as the fourth quarter of 2025, and an increase of 8.8% from the first quarter of 2025 dividend amount. • During the first quarter of 2026, the Company paid dividends of $171.88 per outstanding share of Series A Preferred Stock At March 31, 2026 |

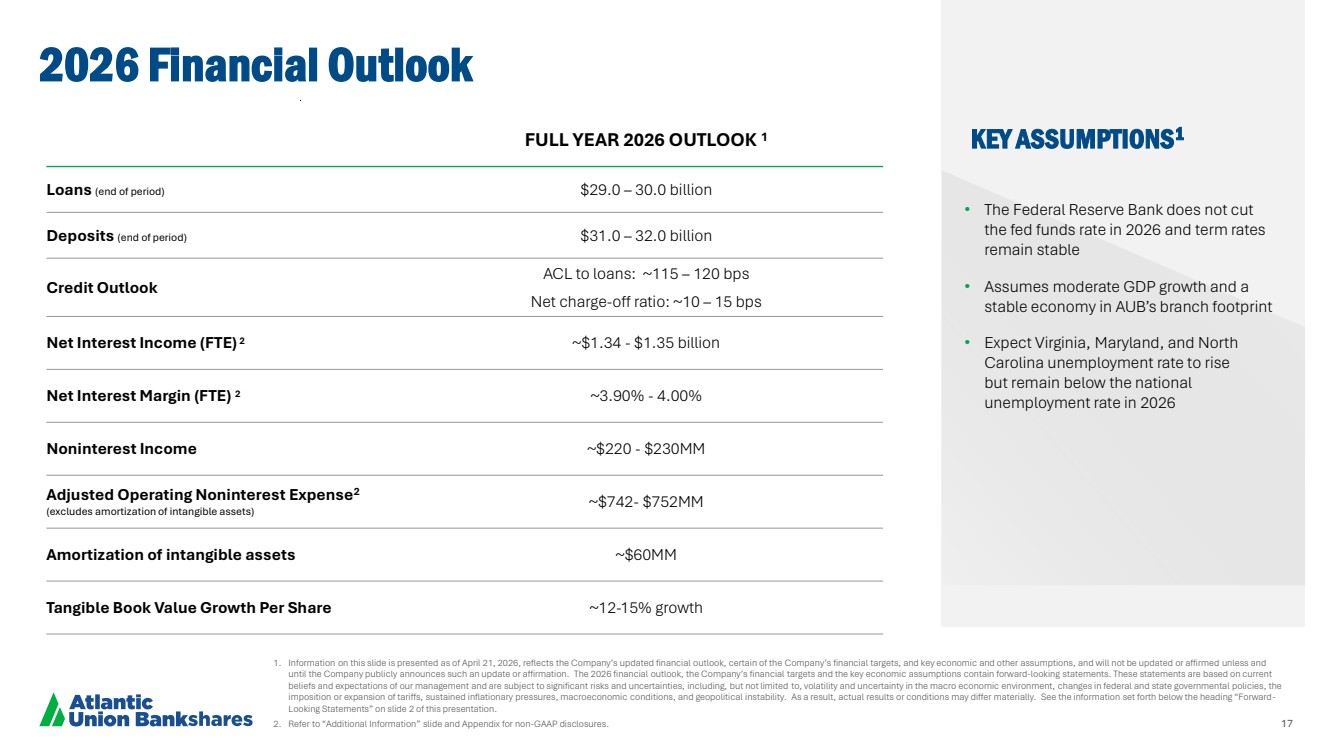

| 17 2026 Financial Outlook 1. Information on this slide is presented as of April 21, 2026, reflects the Company’s updated financial outlook, certain of the Company’s financial targets, and key economic and other assumptions, and will not be updated or affirmed unless and until the Company publicly announces such an update or affirmation. The 2026 financial outlook, the Company’s financial targets and the key economic assumptions contain forward-looking statements. These statements are based on current beliefs and expectations of our management and are subject to significant risks and uncertainties, including, but not limited to, volatility and uncertainty in the macro economic environment, changes in federal and state governmental policies, the imposition or expansion of tariffs, sustained inflationary pressures, macroeconomic conditions, and geopolitical instability. As a result, actual results or conditions may differ materially. See the information set forth below the heading “Forward-Looking Statements” on slide 2 of this presentation. 2. Refer to “Additional Information” slide and Appendix for non-GAAP disclosures. FULL YEAR 2026 OUTLOOK 1 Loans (end of period) $29.0 – 30.0 billion Deposits (end of period) $31.0 – 32.0 billion Credit Outlook ACL to loans: ~115 – 120 bps Net charge-off ratio: ~10 – 15 bps Net Interest Income (FTE) 2 ~$1.34 - $1.35 billion Net Interest Margin (FTE) 2 ~3.90% - 4.00% Noninterest Income ~$220 - $230MM Adjusted Operating Noninterest Expense2 (excludes amortization of intangible assets) ~$742- $752MM Amortization of intangible assets ~$60MM Tangible Book Value Growth Per Share ~12-15% growth • The Federal Reserve Bank does not cut the fed funds rate in 2026 and term rates remain stable • Assumes moderate GDP growth and a stable economy in AUB’s branch footprint • Expect Virginia, Maryland, and North Carolina unemployment rate to rise but remain below the national unemployment rate in 2026 KEY ASSUMPTIONS1 |

| Q1 2026 APPENDIX |

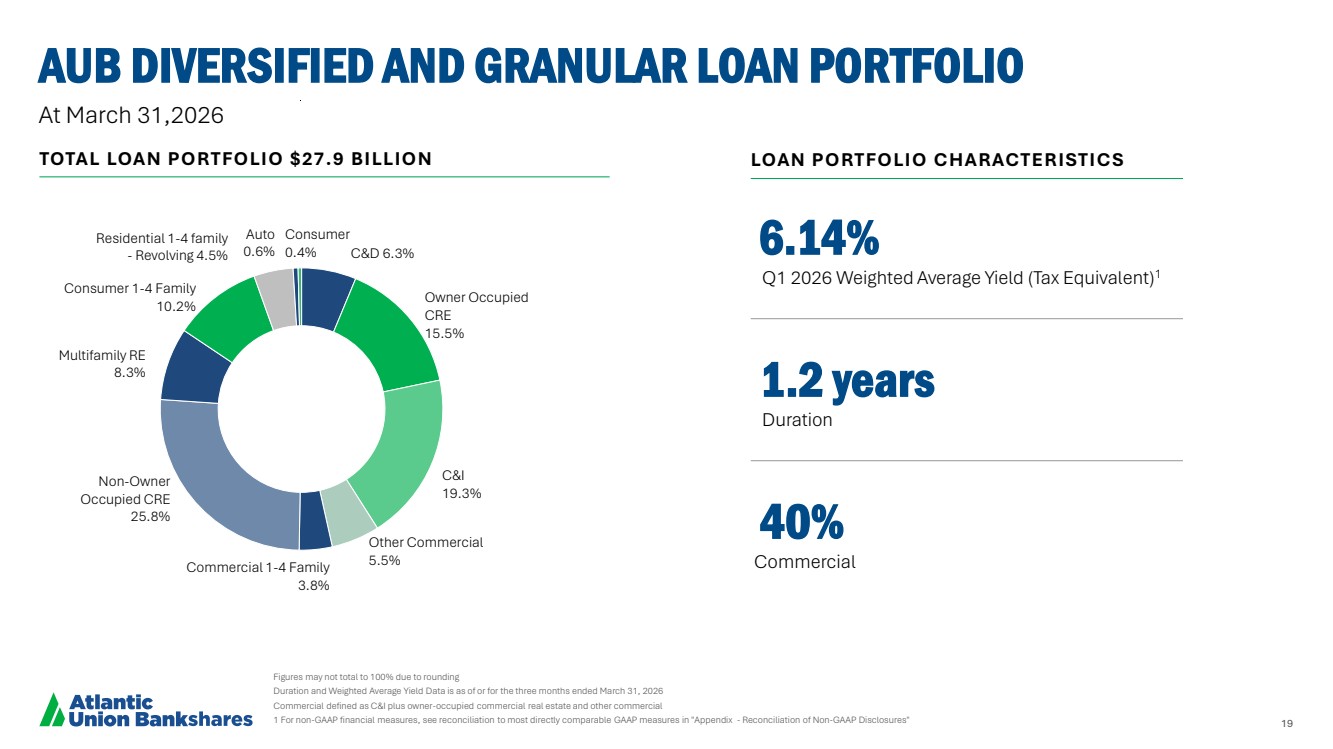

| 19 AUB DIVERSIFIED AND GRANULAR LOAN PORTFOLIO Figures may not total to 100% due to rounding Duration and Weighted Average Yield Data is as of or for the three months ended March 31, 2026 Commercial defined as C&I plus owner-occupied commercial real estate and other commercial 1 For non-GAAP financial measures, see reconciliation to most directly comparable GAAP measures in "Appendix - Reconciliation of Non-GAAP Disclosures" Duration Q2 2025 Weighted Average Yield (Tax Equivalent) C&D 6.3% Owner Occupied CRE 15.5% C&I 19.3% Other Commercial 5.5% Commercial 1-4 Family 3.8% Non-Owner Occupied CRE 25.8% Multifamily RE 8.3% Consumer 1-4 Family 10.2% Residential 1-4 family - Revolving 4.5% Auto 0.6% Consumer 0.4% TOTAL LOAN PORTFOLIO $27.9 BILLION Total Portfolio Characteristics At March 31,2026 LOAN PORTFOLIO CHARACTERISTICS 1.2 years Duration 40% Commercial 6.14% Q1 2026 Weighted Average Yield (Tax Equivalent)1 |

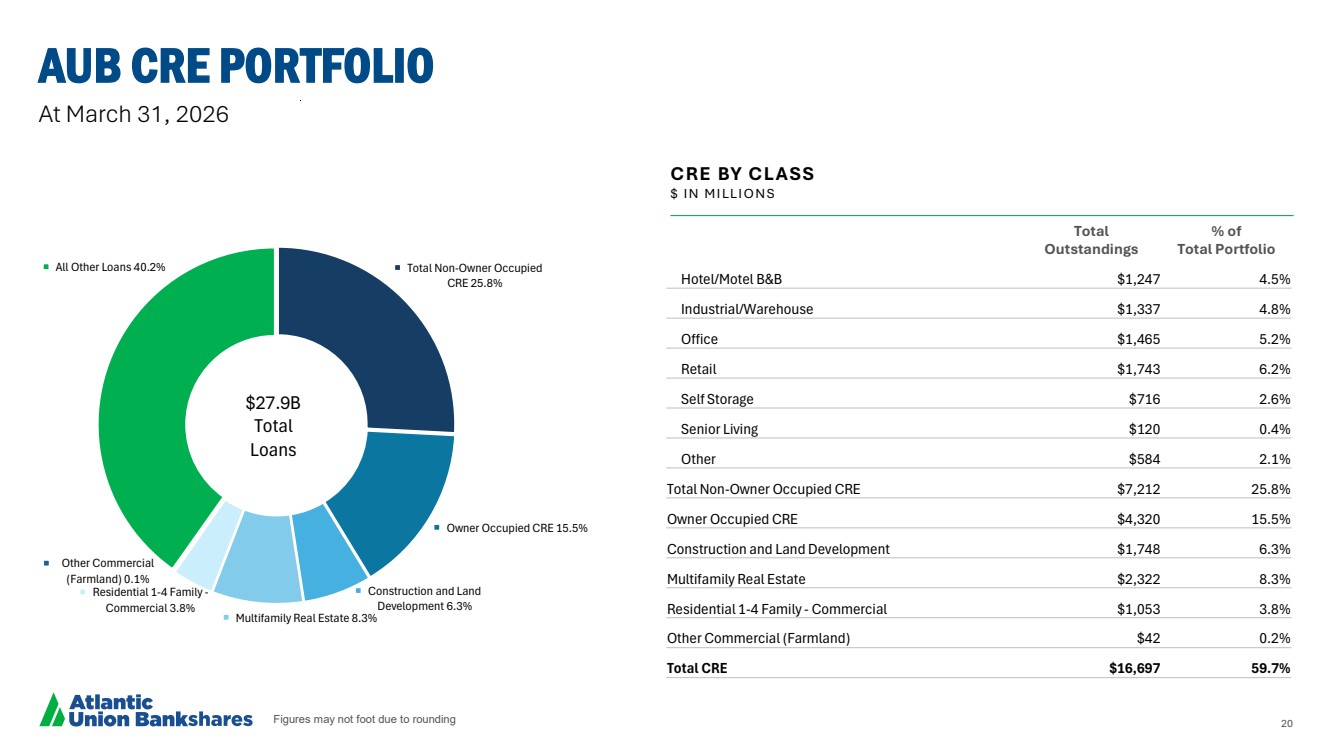

| 20 Total Non-Owner Occupied CRE 25.8% Owner Occupied CRE 15.5% Construction and Land Development 6.3% Multifamily Real Estate 8.3% Residential 1-4 Family - Commercial 3.8% Other Commercial (Farmland) 0.1% All Other Loans 40.2% Figures may not foot due to rounding AUB CRE PORTFOLIO At March 31, 2026 CRE BY CLASS $ I N M I LLI O N S Total Outstandings % of Total Portfolio Hotel/Motel B&B $1,247 4.5% Industrial/Warehouse $1,337 4.8% Office $1,465 5.2% Retail $1,743 6.2% Self Storage $716 2.6% Senior Living $120 0.4% Other $584 2.1% Total Non-Owner Occupied CRE $7,212 25.8% Owner Occupied CRE $4,320 15.5% Construction and Land Development $1,748 6.3% Multifamily Real Estate $2,322 8.3% Residential 1-4 Family - Commercial $1,053 3.8% Other Commercial (Farmland) $42 0.2% Total CRE $16,697 59.7% $27.9B Total Loans |

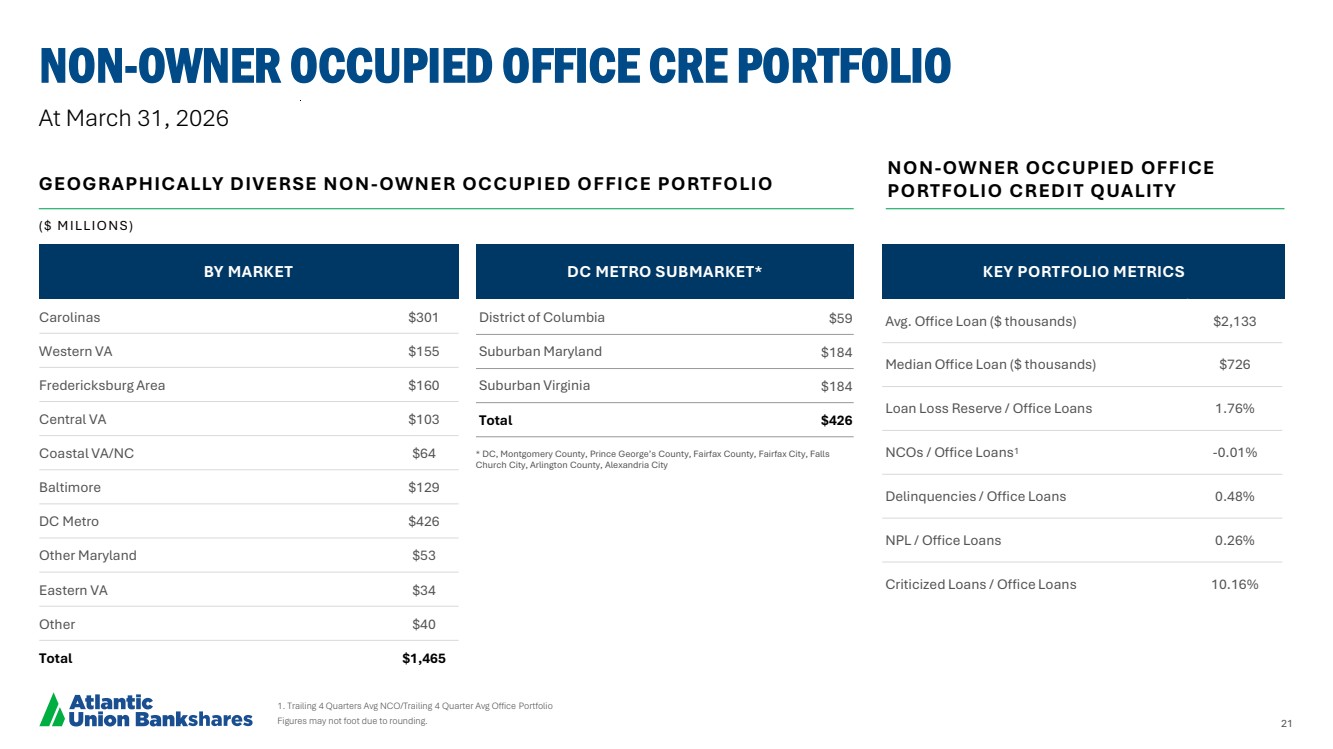

| 21 At March 31, 2026 1. Trailing 4 Quarters Avg NCO/Trailing 4 Quarter Avg Office Portfolio Figures may not foot due to rounding. NON-OWNER OCCUPIED OFFICE CRE PORTFOLIO NON-OWNER OCCUPIED OFFICE GEOGRAPHICALLY DIVERSE NON PORTFOLIO CREDIT QUALITY -OWNER OCCUPIED OFFICE PORTFOLIO * DC, Montgomery County, Prince George’s County, Fairfax County, Fairfax City, Falls Church City, Arlington County, Alexandria City ( $ M I LLI O N S ) Carolinas $301 Western VA $155 Fredericksburg Area $160 Central VA $103 Coastal VA/NC $64 Baltimore $129 DC Metro $426 Other Maryland $53 Eastern VA $34 Other $40 Total $1,465 BY MARKET DC METRO SUBMARKET* KEY PORTFOLIO METRICS Avg. Office Loan ($ thousands) $2,133 Median Office Loan ($ thousands) $726 Loan Loss Reserve / Office Loans 1.76% NCOs / Office Loans1 -0.01% Delinquencies / Office Loans 0.48% NPL / Office Loans 0.26% Criticized Loans / Office Loans 10.16% District of Columbia $59 Suburban Maryland $184 Suburban Virginia $184 Total $426 |

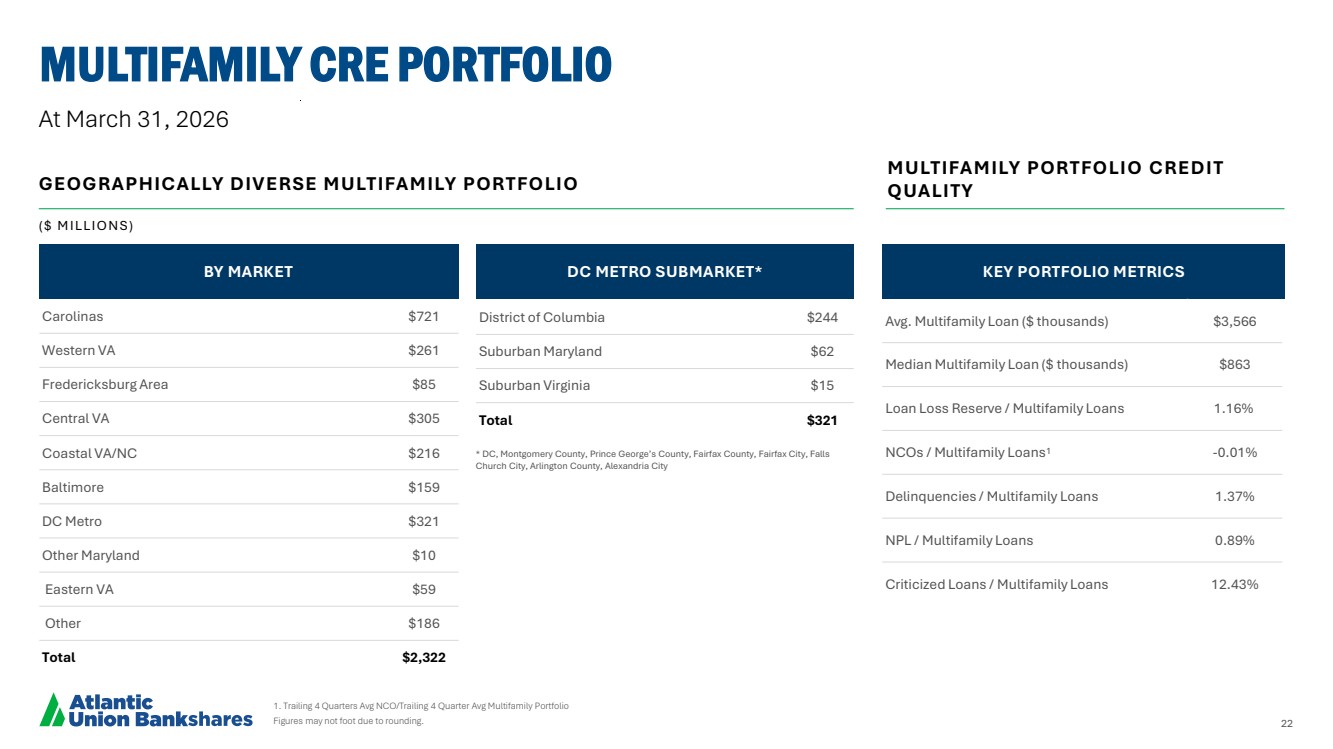

| 22 MULTIFAMILY CRE PORTFOLIO 1. Trailing 4 Quarters Avg NCO/Trailing 4 Quarter Avg Multifamily Portfolio Figures may not foot due to rounding. Carolinas $721 Western VA $261 Fredericksburg Area $85 Central VA $305 Coastal VA/NC $216 Baltimore $159 DC Metro $321 Other Maryland $10 Eastern VA $59 Other $186 Total $2,322 At March 31, 2026 * DC, Montgomery County, Prince George’s County, Fairfax County, Fairfax City, Falls Church City, Arlington County, Alexandria City BY MARKET MULTIFAMILY PORTFOLIO CREDIT GEOGRAPHICALLY DIVERSE MULTIFAMILY PORTFOLIO QUALITY DC METRO SUBMARKET* KEY PORTFOLIO METRICS ( $ M I LLI O N S ) Avg. Multifamily Loan ($ thousands) $3,566 Median Multifamily Loan ($ thousands) $863 Loan Loss Reserve / Multifamily Loans 1.16% NCOs / Multifamily Loans1 -0.01% Delinquencies / Multifamily Loans 1.37% NPL / Multifamily Loans 0.89% Criticized Loans / Multifamily Loans 12.43% District of Columbia $244 Suburban Maryland $62 Suburban Virginia $15 Total $321 |

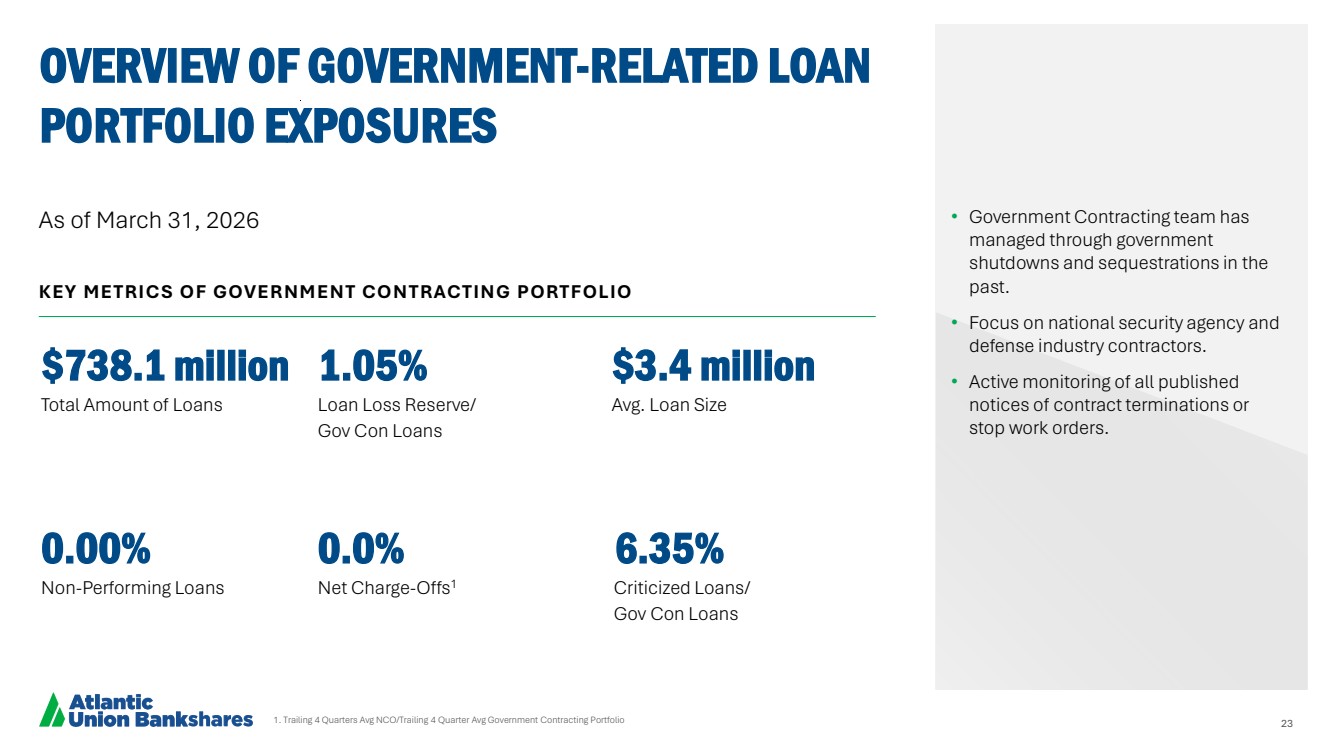

| 23 $738.1 million 1.05% $3.4 million Total Amount of Loans Loan Loss Reserve/ Gov Con Loans Avg. Loan Size 0.00% 0.0% 6.35% Non-Performing Loans Net Charge-Offs1 Criticized Loans/ Gov Con Loans 1. Trailing 4 Quarters Avg NCO/Trailing 4 Quarter Avg Government Contracting Portfolio OVERVIEW OF GOVERNMENT-RELATED LOAN PORTFOLIO EXPOSURES • Government Contracting team has managed through government shutdowns and sequestrations in the past. • Focus on national security agency and defense industry contractors. • Active monitoring of all published notices of contract terminations or stop work orders. KEY METRICS OF GOVERNMENT CONTRACTING PORTFOLIO As of March 31, 2026 |

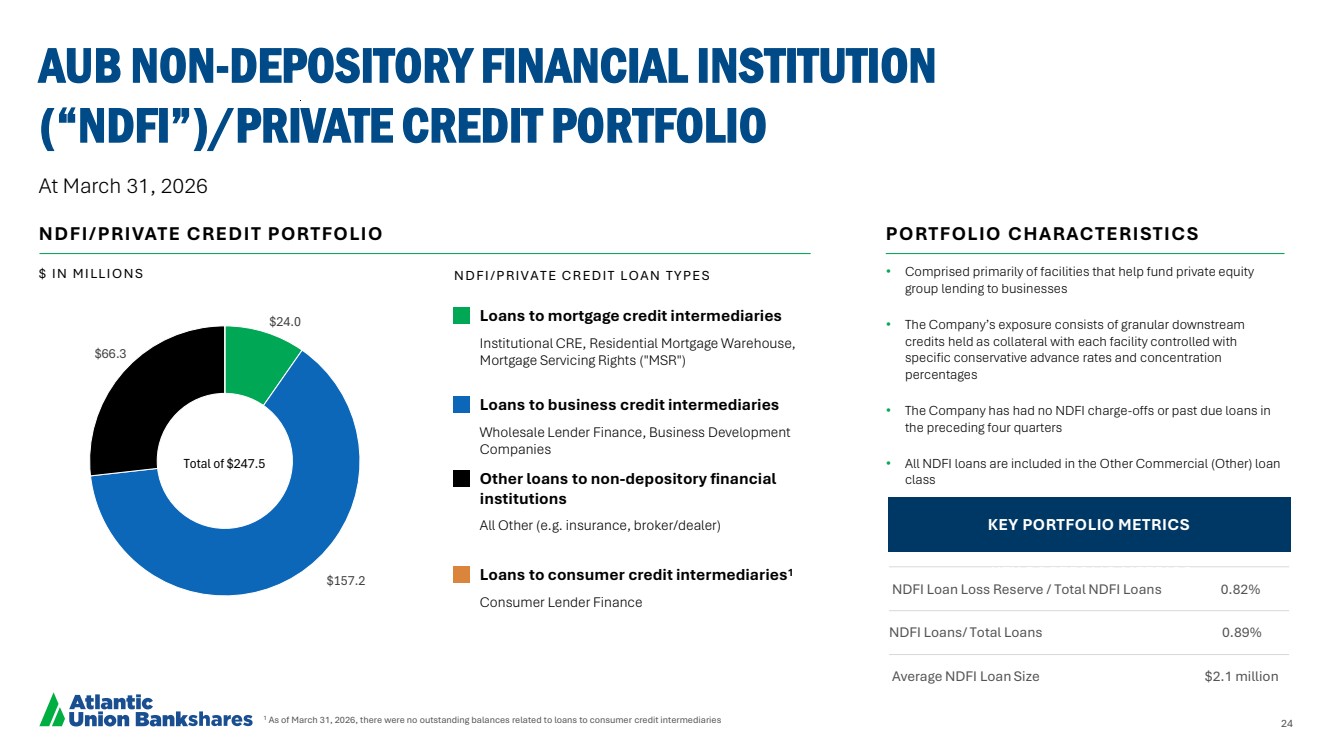

| 24 • Comprised primarily of facilities that help fund private equity group lending to businesses • The Company’s exposure consists of granular downstream credits held as collateral with each facility controlled with specific conservative advance rates and concentration percentages • The Company has had no NDFI charge-offs or past due loans in the preceding four quarters • All NDFI loans are included in the Other Commercial (Other) loan class 1 As of March 31, 2026, there were no outstanding balances related to loans to consumer credit intermediaries AUB NON-DEPOSITORY FINANCIAL INSTITUTION (“NDFI”)/PRIVATE CREDIT PORTFOLIO At March 31, 2026 $24.0 $157.2 $66.3 NDFI/PRIVATE CREDIT PORTFOLIO PORTFOLIO CHARACTERISTICS $ I N M I LLI O N S Loans to mortgage credit intermediaries Institutional CRE, Residential Mortgage Warehouse, Mortgage Servicing Rights ("MSR") Loans to business credit intermediaries Wholesale Lender Finance, Business Development Companies Other loans to non-depository financial institutions All Other (e.g. insurance, broker/dealer) Loans to consumer credit intermediaries1 Consumer Lender Finance N D F I / P R I V A T E C R E D I T LO A N T Y P E S Total of $247.5 NDFI Loan Loss Reserve / Total NDFI Loans 0.82% NDFI Loans/ Total Loans 0.89% Average NDFI Loan Size $2.1 million KEY PORTFOLIO METRICS KEY PORTFOLIO METRICS |

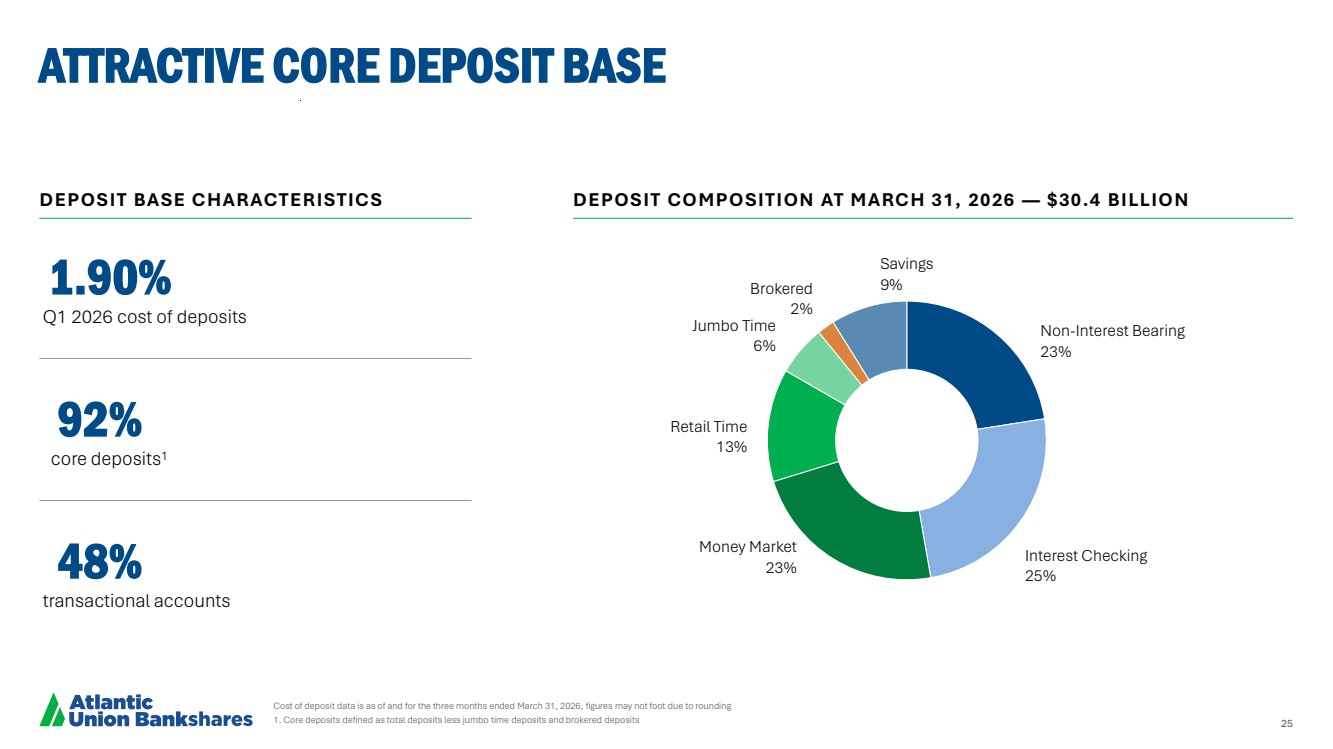

| 25 ATTRACTIVE CORE DEPOSIT BASE Cost of deposit data is as of and for the three months ended March 31, 2026, figures may not foot due to rounding 1. Core deposits defined as total deposits less jumbo time deposits and brokered deposits Non-Interest Bearing 23% Interest Checking 25% Money Market 23% Retail Time 13% Jumbo Time 6% Brokered 2% Savings 9% DEPOSIT BASE CHARACTERISTICS DEPOSIT COMPOSITION AT MARCH 31, 2026 — $30.4 BILLION 92% core deposits1 48% transactional accounts 1.90% Q1 2026 cost of deposits |

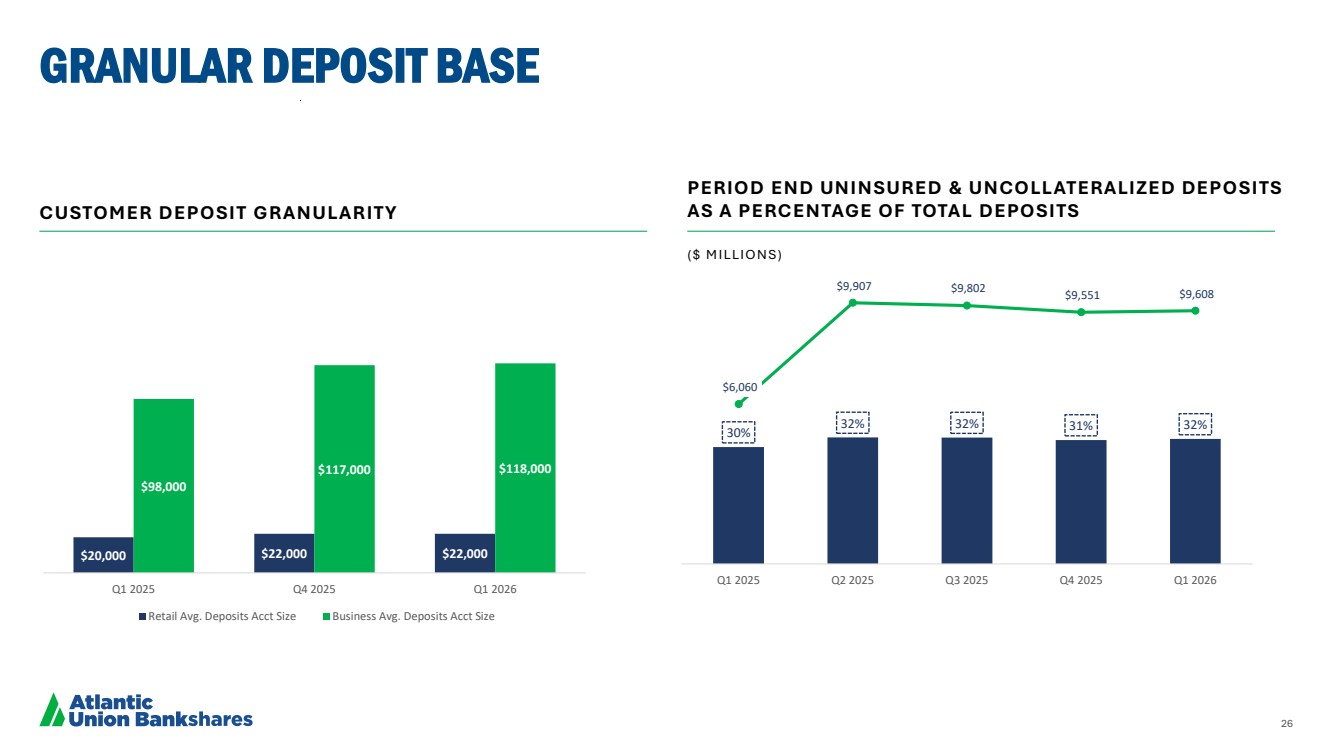

| 26 GRANULAR DEPOSIT BASE CUSTOMER DEPOSIT GRANULARITY PERIOD END UNINSURED & UNCOLLATERALIZED DEPOSITS AS A PERCENTAGE OF TOTAL DEPOSITS ( $ M I LLI O N S ) $20,000 $22,000 $22,000 $98,000 $117,000 $118,000 Q1 2025 Q4 2025 Q1 2026 Retail Avg. Deposits Acct Size Business Avg. Deposits Acct Size 30% 32% 32% 31% 32% $6,060 $9,907 $9,802 $9,551 $9,608 Q1 2025 Q2 2025 Q3 2025 Q4 2025 Q1 2026 |

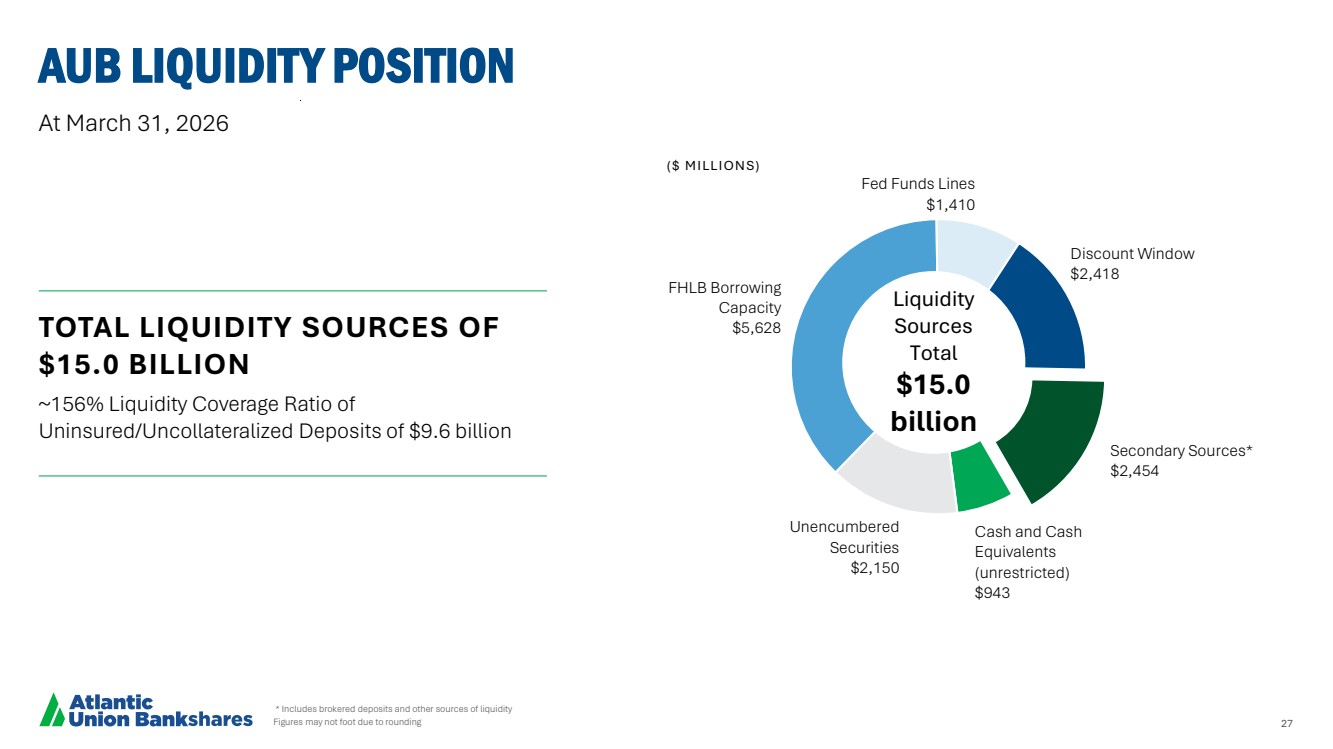

| 27 Cash and Cash Equivalents (unrestricted) $943 Unencumbered Securities $2,150 FHLB Borrowing Capacity $5,628 Fed Funds Lines $1,410 Discount Window $2,418 Secondary Sources* $2,454 AUB LIQUIDITY POSITION * Includes brokered deposits and other sources of liquidity Figures may not foot due to rounding Liquidity Sources Total $15.0 billion At March 31, 2026 TOTAL LIQUIDITY SOURCES OF $15.0 BILLION ~156% Liquidity Coverage Ratio of Uninsured/Uncollateralized Deposits of $9.6 billion ($ MILLIONS) |

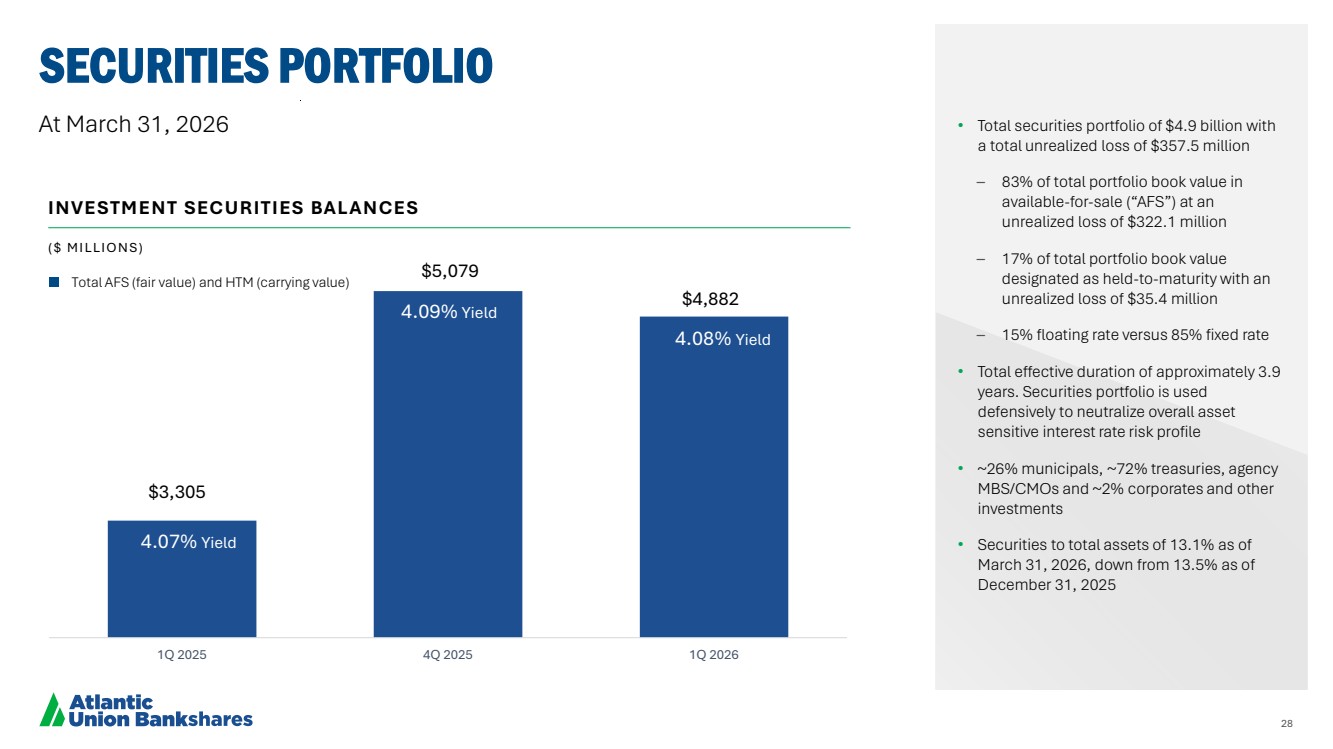

| 28 SECURITIES PORTFOLIO • Total securities portfolio of $4.9 billion with a total unrealized loss of $357.5 million – 83% of total portfolio book value in available-for-sale (“AFS”) at an unrealized loss of $322.1 million – 17% of total portfolio book value designated as held-to-maturity with an unrealized loss of $35.4 million – 15% floating rate versus 85% fixed rate • Total effective duration of approximately 3.9 years. Securities portfolio is used defensively to neutralize overall asset sensitive interest rate risk profile • ~26% municipals, ~72% treasuries, agency MBS/CMOs and ~2% corporates and other investments • Securities to total assets of 13.1% as of March 31, 2026, down from 13.5% as of December 31, 2025 $3,305 $5,079 $4,882 1Q 2025 4Q 2025 1Q 2026 4.07% Yield 4.09% Yield 4.08% Yield INVESTMENT SECURITIES BALANCES Total AFS (fair value) and HTM (carrying value) At March 31, 2026 ( $ M I LLI O N S ) |

| 29 RECONCILIATION OF NON-GAAP DISCLOSURES We have provided supplemental performance measures determined by methods other than in accordance with GAAP. These non-GAAP financial measures are a supplement to GAAP, which we use to prepare our financial statements, and should not be considered in isolation or as a substitute for comparable measures calculated in accordance with GAAP. In addition, our non-GAAP financial measures may not be comparable to non-GAAP financial measures of other companies. We use the non-GAAP financial measures discussed herein in our analysis of our performance. Management believes that these non-GAAP financial measures provide additional understanding of ongoing operations, enhance comparability of results of operations with prior periods and show the effects of significant gains and charges in the periods presented without the impact of items or events that may obscure trends in our underlying performance or show the potential effects of accumulated other comprehensive income or unrealized losses on held to maturity securities on our capital. |

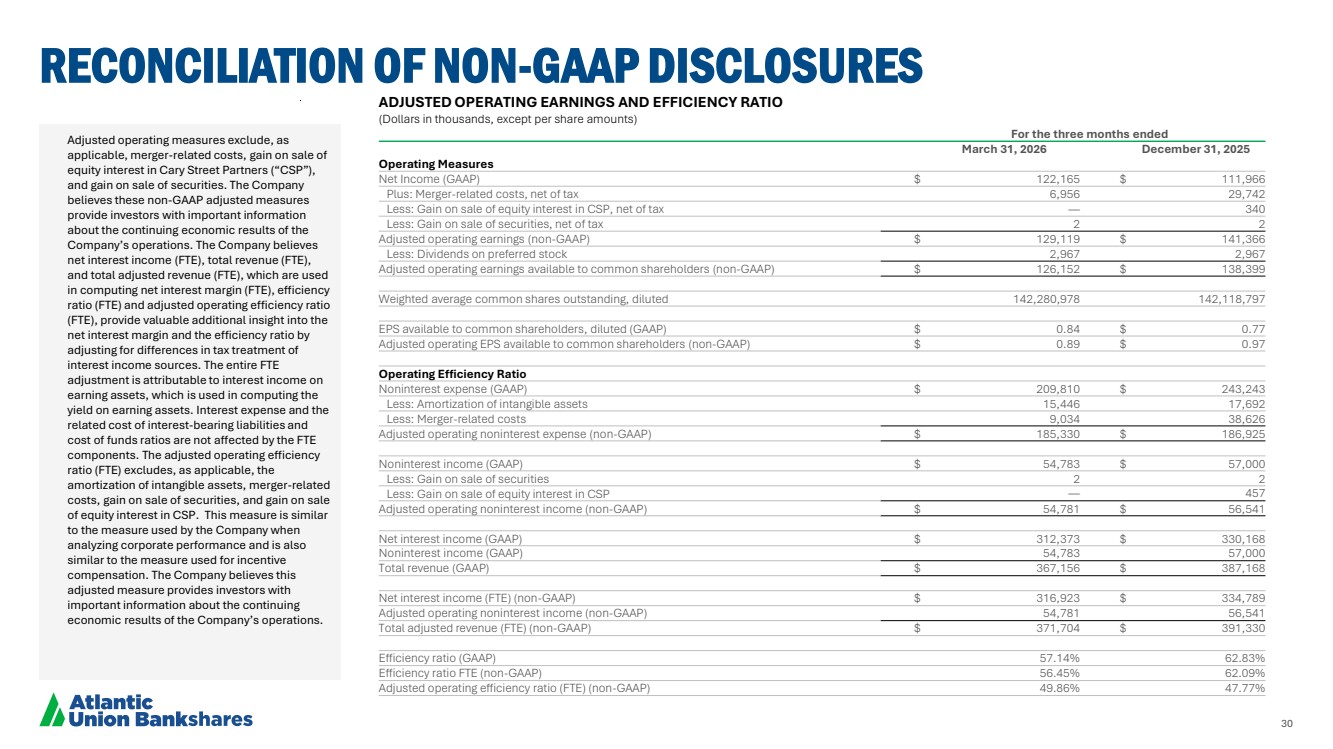

| 30 RECONCILIATION OF NON-GAAP DISCLOSURES Adjusted operating measures exclude, as applicable, merger-related costs, gain on sale of equity interest in Cary Street Partners (“CSP”), and gain on sale of securities. The Company believes these non-GAAP adjusted measures provide investors with important information about the continuing economic results of the Company’s operations. The Company believes net interest income (FTE), total revenue (FTE), and total adjusted revenue (FTE), which are used in computing net interest margin (FTE), efficiency ratio (FTE) and adjusted operating efficiency ratio (FTE), provide valuable additional insight into the net interest margin and the efficiency ratio by adjusting for differences in tax treatment of interest income sources. The entire FTE adjustment is attributable to interest income on earning assets, which is used in computing the yield on earning assets. Interest expense and the related cost of interest-bearing liabilities and cost of funds ratios are not affected by the FTE components. The adjusted operating efficiency ratio (FTE) excludes, as applicable, the amortization of intangible assets, merger-related costs, gain on sale of securities, and gain on sale of equity interest in CSP. This measure is similar to the measure used by the Company when analyzing corporate performance and is also similar to the measure used for incentive compensation. The Company believes this adjusted measure provides investors with important information about the continuing economic results of the Company’s operations. ADJUSTED OPERATING EARNINGS AND EFFICIENCY RATIO (Dollars in thousands, except per share amounts) For the three months ended March 31, 2026 December 31, 2025 Operating Measures Net Income (GAAP) $ 122,165 $ 111,966 Plus: Merger-related costs, net of tax 6,956 29,742 Less: Gain on sale of equity interest in CSP, net of tax — 340 Less: Gain on sale of securities, net of tax 2 2 Adjusted operating earnings (non-GAAP) $ 129,119 $ 141,366 Less: Dividends on preferred stock 2,967 2,967 Adjusted operating earnings available to common shareholders (non-GAAP) $ 126,152 $ 138,399 Weighted average common shares outstanding, diluted 142,280,978 142,118,797 EPS available to common shareholders, diluted (GAAP) $ 0.84 $ 0.77 Adjusted operating EPS available to common shareholders (non-GAAP) $ 0.89 $ 0.97 Operating Efficiency Ratio Noninterest expense (GAAP) $ 209,810 $ 243,243 Less: Amortization of intangible assets 15,446 17,692 Less: Merger-related costs 9,034 38,626 Adjusted operating noninterest expense (non-GAAP) $ 185,330 $ 186,925 Noninterest income (GAAP) $ 54,783 $ 57,000 Less: Gain on sale of securities 2 2 Less: Gain on sale of equity interest in CSP — 457 Adjusted operating noninterest income (non-GAAP) $ 54,781 $ 56,541 Net interest income (GAAP) $ 312,373 $ 330,168 Noninterest income (GAAP) 54,783 57,000 Total revenue (GAAP) $ 367,156 $ 387,168 Net interest income (FTE) (non-GAAP) $ 316,923 $ 334,789 Adjusted operating noninterest income (non-GAAP) 54,781 56,541 Total adjusted revenue (FTE) (non-GAAP) $ 371,704 $ 391,330 Efficiency ratio (GAAP) 57.14% 62.83% Efficiency ratio FTE (non-GAAP) 56.45% 62.09% Adjusted operating efficiency ratio (FTE) (non-GAAP) 49.86% 47.77% |

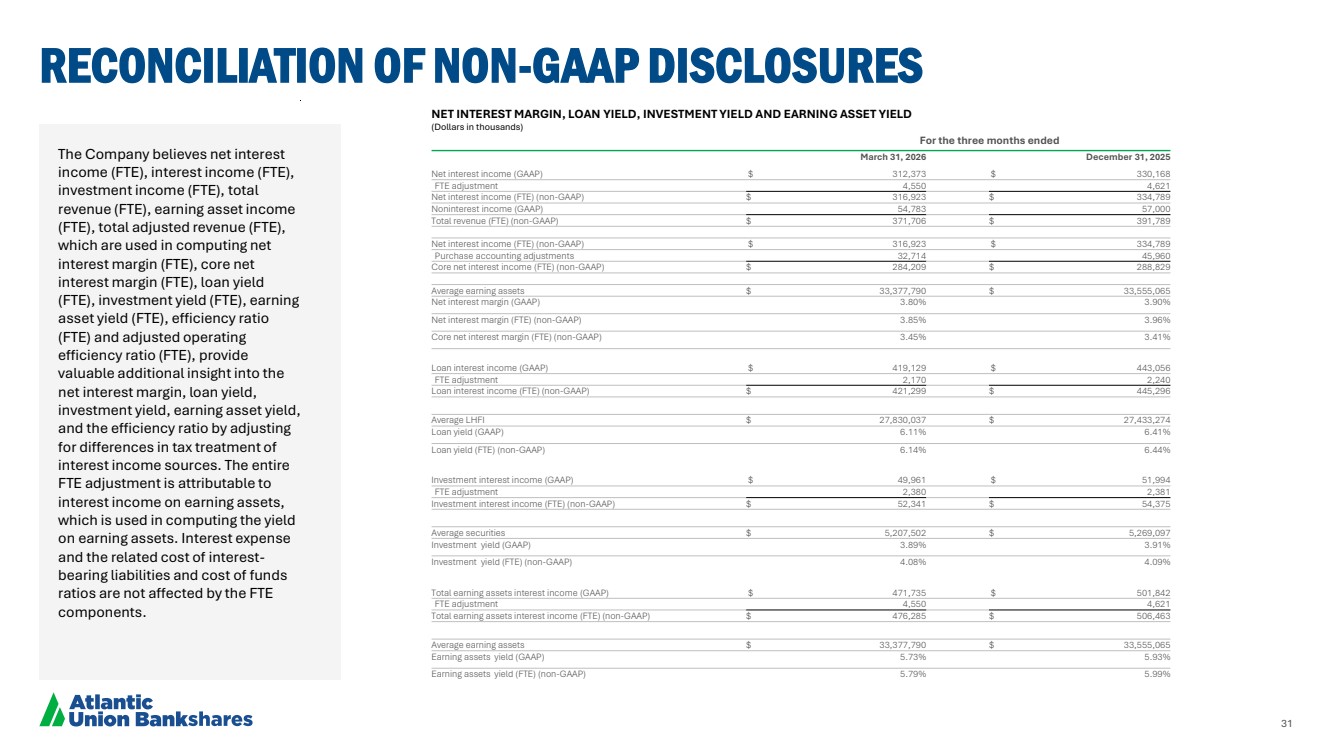

| 31 RECONCILIATION OF NON-GAAP DISCLOSURES The Company believes net interest income (FTE), interest income (FTE), investment income (FTE), total revenue (FTE), earning asset income (FTE), total adjusted revenue (FTE), which are used in computing net interest margin (FTE), core net interest margin (FTE), loan yield (FTE), investment yield (FTE), earning asset yield (FTE), efficiency ratio (FTE) and adjusted operating efficiency ratio (FTE), provide valuable additional insight into the net interest margin, loan yield, investment yield, earning asset yield, and the efficiency ratio by adjusting for differences in tax treatment of interest income sources. The entire FTE adjustment is attributable to interest income on earning assets, which is used in computing the yield on earning assets. Interest expense and the related cost of interest-bearing liabilities and cost of funds ratios are not affected by the FTE components. NET INTEREST MARGIN, LOAN YIELD, INVESTMENT YIELD AND EARNING ASSET YIELD (Dollars in thousands) For the three months ended March 31, 2026 December 31, 2025 Net interest income (GAAP) $ 312,373 $ 330,168 FTE adjustment 4,550 4,621 Net interest income (FTE) (non-GAAP) $ 316,923 $ 334,789 Noninterest income (GAAP) 54,783 57,000 Total revenue (FTE) (non-GAAP) $ 371,706 $ 391,789 Net interest income (FTE) (non-GAAP) $ 316,923 $ 334,789 Purchase accounting adjustments 32,714 45,960 Core net interest income (FTE) (non-GAAP) $ 284,209 $ 288,829 Average earning assets $ 33,377,790 $ 33,555,065 Net interest margin (GAAP) 3.80% 3.90% Net interest margin (FTE) (non-GAAP) 3.85% 3.96% Core net interest margin (FTE) (non-GAAP) 3.45% 3.41% Loan interest income (GAAP) $ 419,129 $ 443,056 FTE adjustment 2,170 2,240 Loan interest income (FTE) (non-GAAP) $ 421,299 $ 445,296 Average LHFI $ 27,830,037 $ 27,433,274 Loan yield (GAAP) 6.11% 6.41% Loan yield (FTE) (non-GAAP) 6.14% 6.44% Investment interest income (GAAP) $ 49,961 $ 51,994 FTE adjustment 2,380 2,381 Investment interest income (FTE) (non-GAAP) $ 52,341 $ 54,375 Average securities $ 5,207,502 $ 5,269,097 Investment yield (GAAP) 3.89% 3.91% Investment yield (FTE) (non-GAAP) 4.08% 4.09% Total earning assets interest income (GAAP) $ 471,735 $ 501,842 FTE adjustment 4,550 4,621 Total earning assets interest income (FTE) (non-GAAP) $ 476,285 $ 506,463 Average earning assets $ 33,377,790 $ 33,555,065 Earning assets yield (GAAP) 5.73% 5.93% Earning assets yield (FTE) (non-GAAP) 5.79% 5.99% |

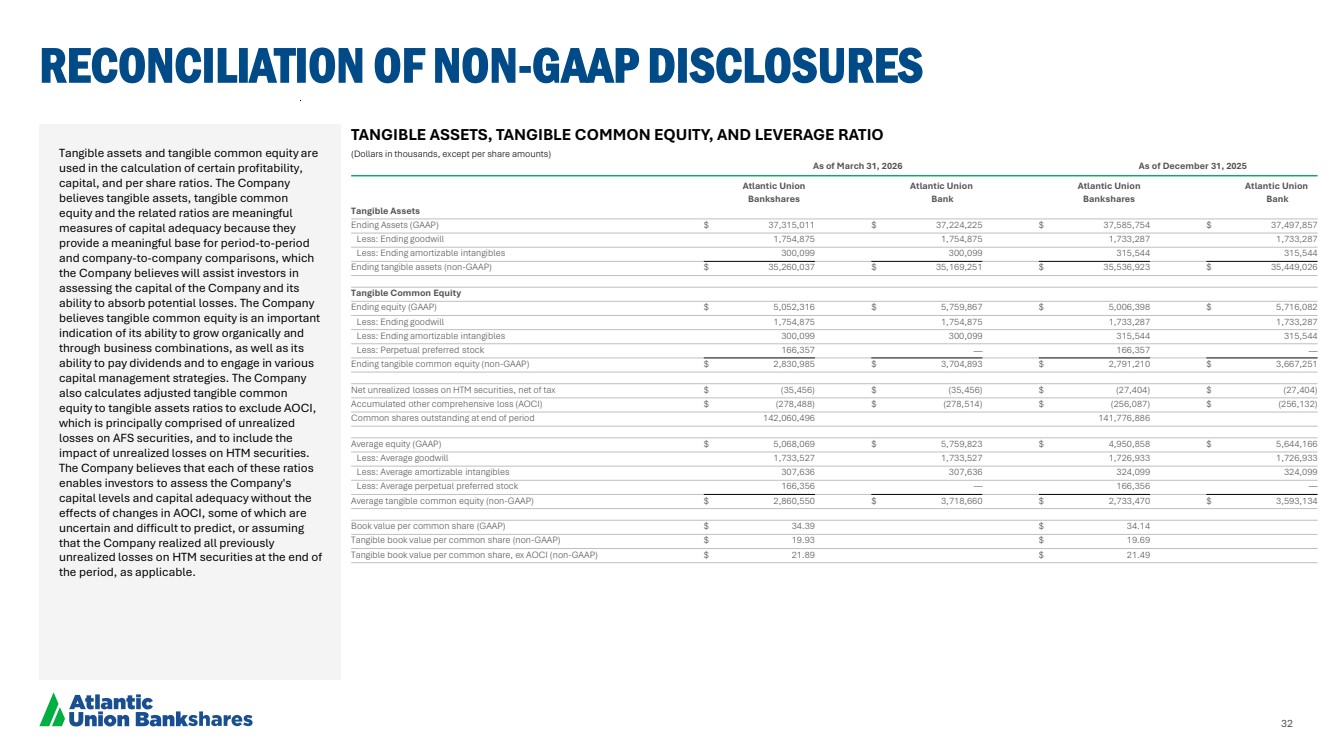

| 32 RECONCILIATION OF NON-GAAP DISCLOSURES Tangible assets and tangible common equity are used in the calculation of certain profitability, capital, and per share ratios. The Company believes tangible assets, tangible common equity and the related ratios are meaningful measures of capital adequacy because they provide a meaningful base for period-to-period and company-to-company comparisons, which the Company believes will assist investors in assessing the capital of the Company and its ability to absorb potential losses. The Company believes tangible common equity is an important indication of its ability to grow organically and through business combinations, as well as its ability to pay dividends and to engage in various capital management strategies. The Company also calculates adjusted tangible common equity to tangible assets ratios to exclude AOCI, which is principally comprised of unrealized losses on AFS securities, and to include the impact of unrealized losses on HTM securities. The Company believes that each of these ratios enables investors to assess the Company's capital levels and capital adequacy without the effects of changes in AOCI, some of which are uncertain and difficult to predict, or assuming that the Company realized all previously unrealized losses on HTM securities at the end of the period, as applicable. TANGIBLE ASSETS, TANGIBLE COMMON EQUITY, AND LEVERAGE RATIO (Dollars in thousands, except per share amounts) As of March 31, 2026 As of December 31, 2025 Atlantic Union Atlantic Union Atlantic Union Atlantic Union Bankshares Bank Bankshares Bank Tangible Assets Ending Assets (GAAP) $ 37,315,011 $ 37,224,225 $ 37,585,754 $ 37,497,857 Less: Ending goodwill 1,754,875 1,754,875 1,733,287 1,733,287 Less: Ending amortizable intangibles 300,099 300,099 315,544 315,544 Ending tangible assets (non-GAAP) $ 35,260,037 $ 35,169,251 $ 35,536,923 $ 35,449,026 Tangible Common Equity Ending equity (GAAP) $ 5,052,316 $ 5,759,867 $ 5,006,398 $ 5,716,082 Less: Ending goodwill 1,754,875 1,754,875 1,733,287 1,733,287 Less: Ending amortizable intangibles 300,099 300,099 315,544 315,544 Less: Perpetual preferred stock 166,357 — 166,357 — Ending tangible common equity (non-GAAP) $ 2,830,985 $ 3,704,893 $ 2,791,210 $ 3,667,251 Net unrealized losses on HTM securities, net of tax $ (35,456) $ (35,456) $ (27,404) $ (27,404) Accumulated other comprehensive loss (AOCI) $ (278,488) $ (278,514) $ (256,087) $ (256,132) Common shares outstanding at end of period 142,060,496 141,776,886 Average equity (GAAP) $ 5,068,069 $ 5,759,823 $ 4,950,858 $ 5,644,166 Less: Average goodwill 1,733,527 1,733,527 1,726,933 1,726,933 Less: Average amortizable intangibles 307,636 307,636 324,099 324,099 Less: Average perpetual preferred stock 166,356 — 166,356 — Average tangible common equity (non-GAAP) $ 2,860,550 $ 3,718,660 $ 2,733,470 $ 3,593,134 Book value per common share (GAAP) $ 34.39 $ 34.14 Tangible book value per common share (non-GAAP) $ 19.93 $ 19.69 Tangible book value per common share, ex AOCI (non-GAAP) $ 21.89 $ 21.49 |

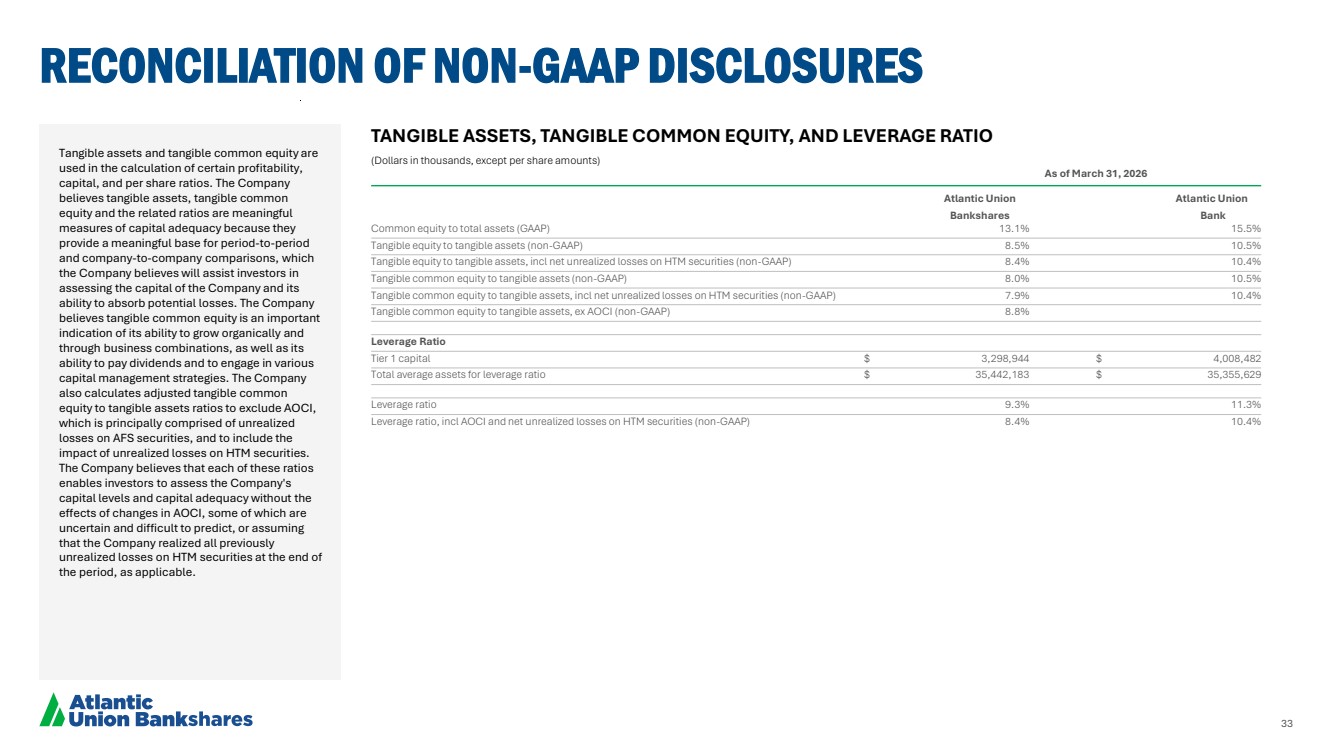

| 33 RECONCILIATION OF NON-GAAP DISCLOSURES Tangible assets and tangible common equity are used in the calculation of certain profitability, capital, and per share ratios. The Company believes tangible assets, tangible common equity and the related ratios are meaningful measures of capital adequacy because they provide a meaningful base for period-to-period and company-to-company comparisons, which the Company believes will assist investors in assessing the capital of the Company and its ability to absorb potential losses. The Company believes tangible common equity is an important indication of its ability to grow organically and through business combinations, as well as its ability to pay dividends and to engage in various capital management strategies. The Company also calculates adjusted tangible common equity to tangible assets ratios to exclude AOCI, which is principally comprised of unrealized losses on AFS securities, and to include the impact of unrealized losses on HTM securities. The Company believes that each of these ratios enables investors to assess the Company's capital levels and capital adequacy without the effects of changes in AOCI, some of which are uncertain and difficult to predict, or assuming that the Company realized all previously unrealized losses on HTM securities at the end of the period, as applicable. TANGIBLE ASSETS, TANGIBLE COMMON EQUITY, AND LEVERAGE RATIO (Dollars in thousands, except per share amounts) As of March 31, 2026 Atlantic Union Atlantic Union Bankshares Bank Common equity to total assets (GAAP) 13.1% 15.5% Tangible equity to tangible assets (non-GAAP) 8.5% 10.5% Tangible equity to tangible assets, incl net unrealized losses on HTM securities (non-GAAP) 8.4% 10.4% Tangible common equity to tangible assets (non-GAAP) 8.0% 10.5% Tangible common equity to tangible assets, incl net unrealized losses on HTM securities (non-GAAP) 7.9% 10.4% Tangible common equity to tangible assets, ex AOCI (non-GAAP) 8.8% Leverage Ratio Tier 1 capital $ 3,298,944 $ 4,008,482 Total average assets for leverage ratio $ 35,442,183 $ 35,355,629 Leverage ratio 9.3% 11.3% Leverage ratio, incl AOCI and net unrealized losses on HTM securities (non-GAAP) 8.4% 10.4% |

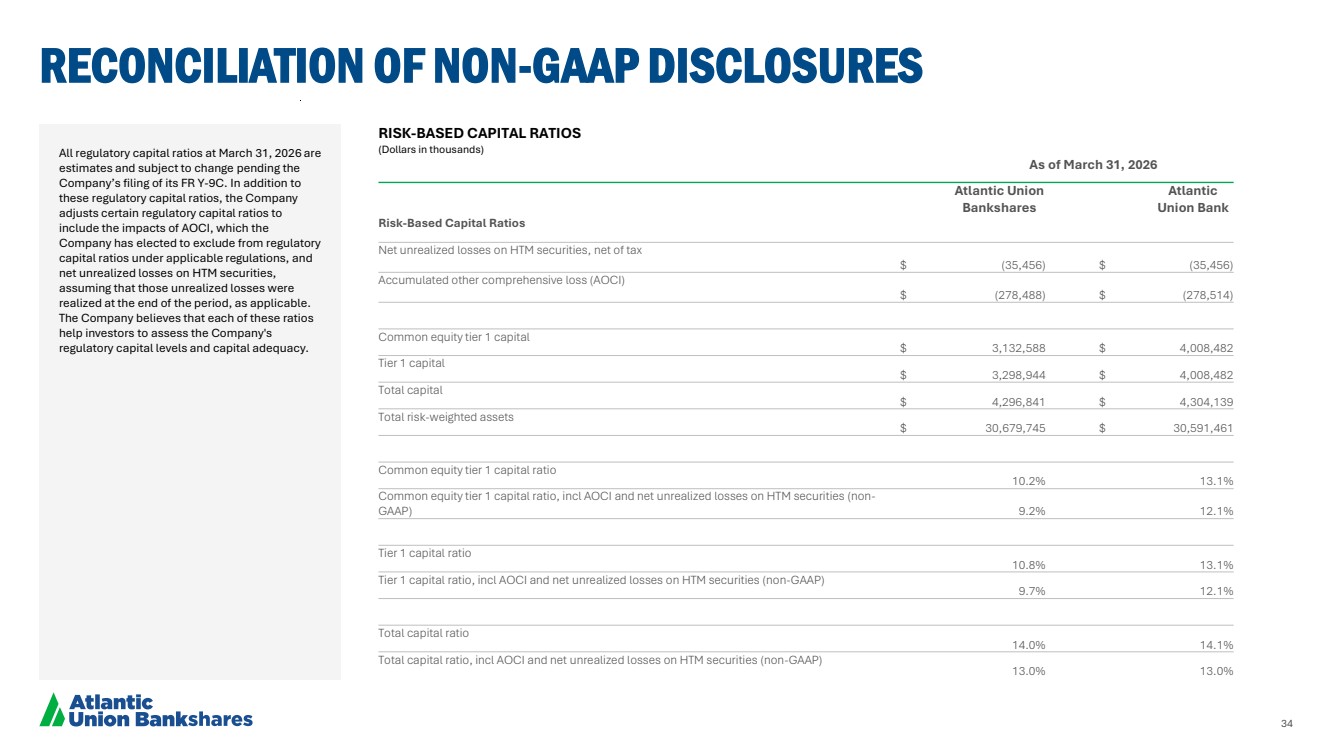

| 34 RECONCILIATION OF NON-GAAP DISCLOSURES All regulatory capital ratios at March 31, 2026 are estimates and subject to change pending the Company’s filing of its FR Y-9C. In addition to these regulatory capital ratios, the Company adjusts certain regulatory capital ratios to include the impacts of AOCI, which the Company has elected to exclude from regulatory capital ratios under applicable regulations, and net unrealized losses on HTM securities, assuming that those unrealized losses were realized at the end of the period, as applicable. The Company believes that each of these ratios help investors to assess the Company's regulatory capital levels and capital adequacy. RISK-BASED CAPITAL RATIOS (Dollars in thousands) As of March 31, 2026 Atlantic Union Bankshares Atlantic Union Bank Risk-Based Capital Ratios Net unrealized losses on HTM securities, net of tax $ (35,456) $ (35,456) Accumulated other comprehensive loss (AOCI) $ (278,488) $ (278,514) Common equity tier 1 capital $ 3,132,588 $ 4,008,482 Tier 1 capital $ 3,298,944 $ 4,008,482 Total capital $ 4,296,841 $ 4,304,139 Total risk-weighted assets $ 30,679,745 $ 30,591,461 Common equity tier 1 capital ratio 10.2% 13.1% Common equity tier 1 capital ratio, incl AOCI and net unrealized losses on HTM securities (non-GAAP) 9.2% 12.1% Tier 1 capital ratio 10.8% 13.1% Tier 1 capital ratio, incl AOCI and net unrealized losses on HTM securities (non-GAAP) 9.7% 12.1% Total capital ratio 14.0% 14.1% Total capital ratio, incl AOCI and net unrealized losses on HTM securities (non-GAAP) 13.0% 13.0% |

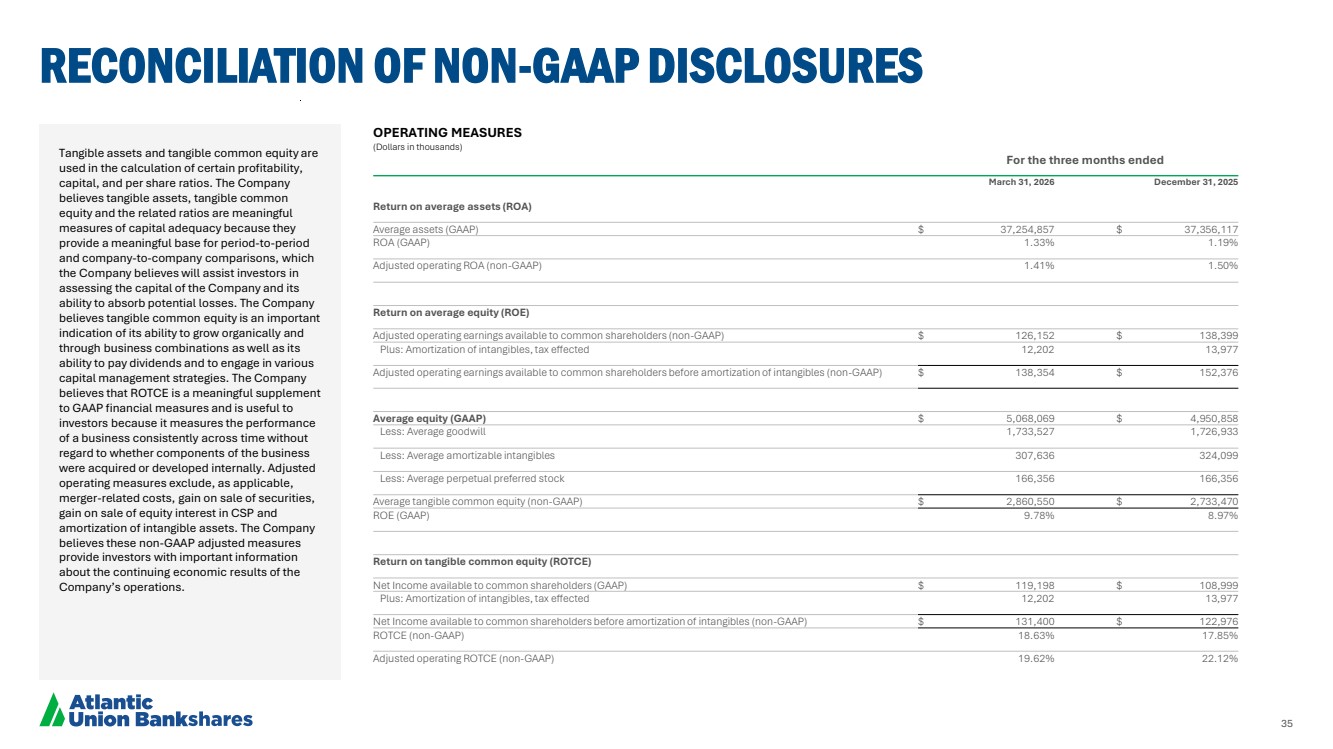

| 35 RECONCILIATION OF NON-GAAP DISCLOSURES Tangible assets and tangible common equity are used in the calculation of certain profitability, capital, and per share ratios. The Company believes tangible assets, tangible common equity and the related ratios are meaningful measures of capital adequacy because they provide a meaningful base for period-to-period and company-to-company comparisons, which the Company believes will assist investors in assessing the capital of the Company and its ability to absorb potential losses. The Company believes tangible common equity is an important indication of its ability to grow organically and through business combinations as well as its ability to pay dividends and to engage in various capital management strategies. The Company believes that ROTCE is a meaningful supplement to GAAP financial measures and is useful to investors because it measures the performance of a business consistently across time without regard to whether components of the business were acquired or developed internally. Adjusted operating measures exclude, as applicable, merger-related costs, gain on sale of securities, gain on sale of equity interest in CSP and amortization of intangible assets. The Company believes these non-GAAP adjusted measures provide investors with important information about the continuing economic results of the Company’s operations. OPERATING MEASURES (Dollars in thousands) For the three months ended March 31, 2026 December 31, 2025 Return on average assets (ROA) Average assets (GAAP) $ 37,254,857 $ 37,356,117 ROA (GAAP) 1.33% 1.19% Adjusted operating ROA (non-GAAP) 1.41% 1.50% Return on average equity (ROE) Adjusted operating earnings available to common shareholders (non-GAAP) $ 126,152 $ 138,399 Plus: Amortization of intangibles, tax effected 12,202 13,977 Adjusted operating earnings available to common shareholders before amortization of intangibles (non-GAAP) $ 138,354 $ 152,376 Average equity (GAAP) $ 5,068,069 $ 4,950,858 Less: Average goodwill 1,733,527 1,726,933 Less: Average amortizable intangibles 307,636 324,099 Less: Average perpetual preferred stock 166,356 166,356 Average tangible common equity (non-GAAP) $ 2,860,550 $ 2,733,470 ROE (GAAP) 9.78% 8.97% Return on tangible common equity (ROTCE) Net Income available to common shareholders (GAAP) $ 119,198 $ 108,999 Plus: Amortization of intangibles, tax effected 12,202 13,977 Net Income available to common shareholders before amortization of intangibles (non-GAAP) $ 131,400 $ 122,976 ROTCE (non-GAAP) 18.63% 17.85% Adjusted operating ROTCE (non-GAAP) 19.62% 22.12% |

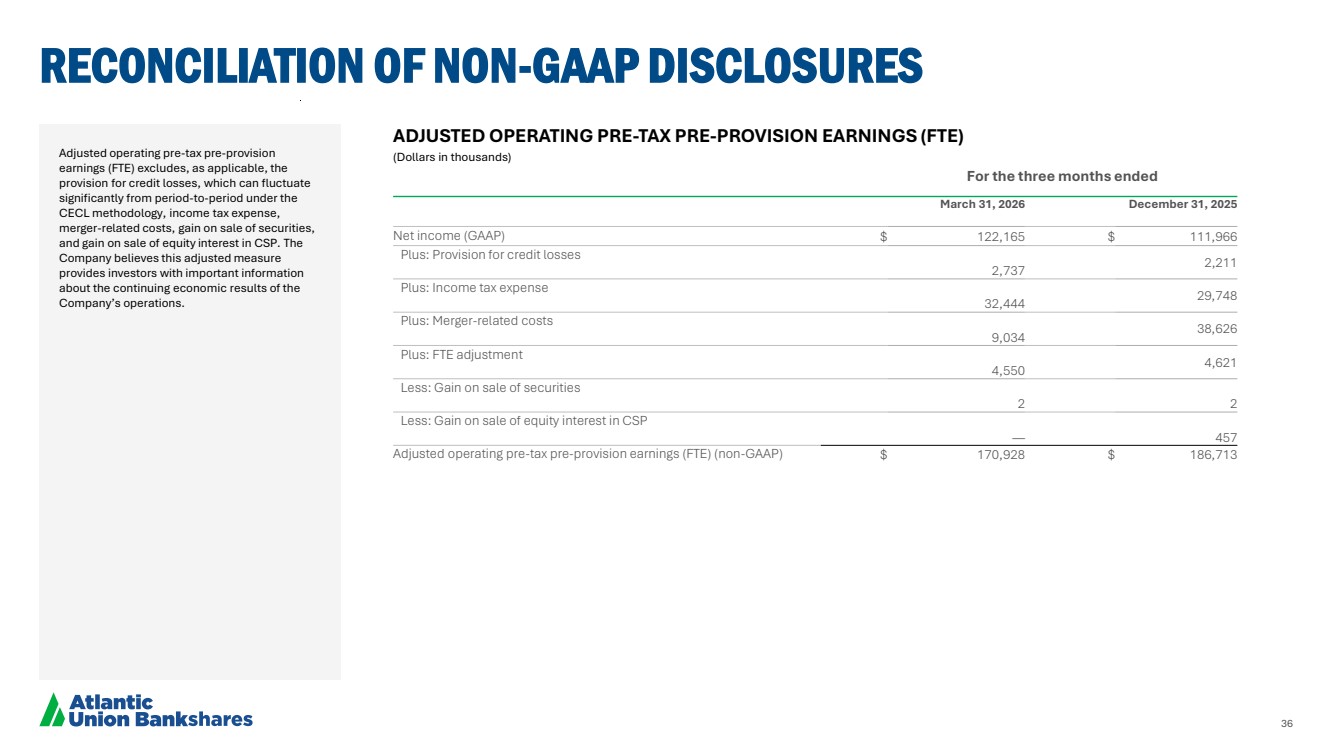

| 36 RECONCILIATION OF NON-GAAP DISCLOSURES Adjusted operating pre-tax pre-provision earnings (FTE) excludes, as applicable, the provision for credit losses, which can fluctuate significantly from period-to-period under the CECL methodology, income tax expense, merger-related costs, gain on sale of securities, and gain on sale of equity interest in CSP. The Company believes this adjusted measure provides investors with important information about the continuing economic results of the Company’s operations. ADJUSTED OPERATING PRE-TAX PRE-PROVISION EARNINGS (FTE) (Dollars in thousands) For the three months ended March 31, 2026 December 31, 2025 Net income (GAAP) $ 122,165 $ 111,966 Plus: Provision for credit losses 2,737 2,211 Plus: Income tax expense 32,444 29,748 Plus: Merger-related costs 9,034 38,626 Plus: FTE adjustment 4,550 4,621 Less: Gain on sale of securities 2 2 Less: Gain on sale of equity interest in CSP — 457 Adjusted operating pre-tax pre-provision earnings (FTE) (non-GAAP) $ 170,928 $ 186,713 |