June 10, 2016

VIA EDGAR AND ELECTRONIC MAIL

Daniel F. Duchovny, Esq.

Special Counsel

Office of Mergers and Acquisitions

United States Securities and Exchange Commission

Division of Corporation Finance

100 F Street, N.E.

Washington, D.C. 20549-3628

|

|

Re:

|

Chico’s FAS, Inc. (“Chico’s” or the “Company”)

|

|

|

Soliciting Materials filed pursuant to Rule 14a-12

|

|

|

Filed on June 2, 2016 by Barington Capital Group, L.P., et al. (the “Soliciting Material”)

|

Dear Mr. Duchovny:

We acknowledge receipt of the comment letter of the Staff (the “Staff”) of the U.S. Securities and Exchange Commission (the “Commission”) dated June 9, 2016 (the “Staff Letter”) with regard to the above-referenced matter. We have reviewed the Staff Letter with our client, Barington Capital Group, L.P., and the other members of the Barington Group (collectively, “Barington”), and provide the following responses on Barington’s behalf. For ease of reference, the comments in the Staff Letter are reproduced in italicized form below.

Soliciting Materials filed pursuant to Rule 14a-12 on June 2, 2016

|

1.

|

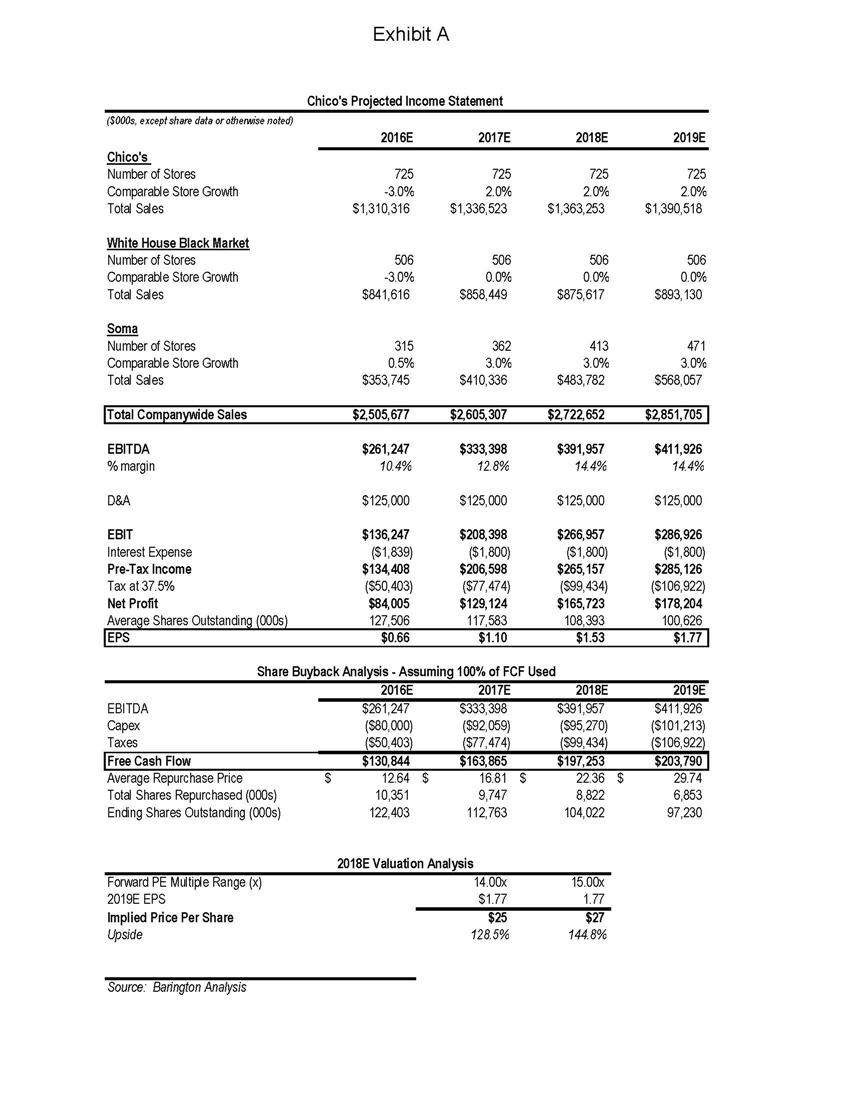

We reissue prior comment 3. Please provide us supplementally your calculations using the information previously included in the footnote to your disclosure.

|

Barington acknowledges the Staff’s comment and restates the Commission’s prior comment 3 in full below:

We note your disclosure that you believe the company’s common stock “could be worth $25 to $27 per share in three years if measures are implemented.” The inclusion of valuations in proxy materials is only appropriate and consonant with Rule 14a-9 when made in good faith and on a reasonable basis. Valuation information must therefore be accompanied by disclosure which facilitates securityholders’ understanding of the basis for and limitations of the valuation information. Please provide us support for your assertion. Also, if you choose to continue using similar language in your soliciting materials, you must include supporting disclosure of the kind described in Exchange Act Release No. 16833 (May 23, 1980). In addition, supplementally explain why your valuation is not so qualified and subject to such material limitations and qualifications as to make its inclusion unreasonable.