☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended June 30, 2024

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ______ to ______

Commission file number 1-11840

THE ALLSTATE CORPORATION

(Exact name of registrant as specified in its charter)

Delaware

36-3871531

(State or other jurisdiction of incorporation or organization)

(I.R.S. Employer Identification No.)

3100 Sanders Road,Northbrook, Illinois60062

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (847) 402-2800

Securities registered pursuant to Section 12(b) of the Act:

Title of each class

Trading Symbols

Name of each exchange on which registered

Common Stock, par value $.01 per share

ALL

New York Stock Exchange

Chicago Stock Exchange

5.100% Fixed-to-Floating Rate Subordinated Debentures due 2053

ALL.PR.B

New York Stock Exchange

Depositary Shares represent 1/1,000th of a share of 5.100% Noncumulative Preferred Stock, Series H

ALL PR H

New York Stock Exchange

Depositary Shares represent 1/1,000th of a share of 4.750% Noncumulative Preferred Stock, Series I

ALL PR I

New York Stock Exchange

Depositary Shares represent 1/1,000th of a share of 7.375% Noncumulative Preferred Stock, Series J

ALL PR J

New York Stock Exchange

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes☒No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes☒No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer

☒

Accelerated filer

☐

Non-accelerated filer

☐

Smaller reporting company

☐

Emerging growth company

☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of July 12, 2024, the registrant had 264,040,589 common shares, $.01 par value, outstanding.

The Allstate Corporation

Index to Quarterly Report on Form 10-Q

June 30, 2024

Part I Financial Information

Page

Item 1. Financial Statements (unaudited) as of June 30, 2024 and December 31, 2023 and for the Three Month and Six Month Periods Ended June 30, 2024 and 2023

Unamortized pension and other postretirement prior service credit

—

(5)

(1)

(9)

Discount rate for reserve for future policy benefits

(1)

8

24

(1)

Other comprehensive (loss) income, after-tax

(143)

(241)

(326)

478

Comprehensive income (loss)

204

(1,616)

1,219

(1,218)

Less: Comprehensive income (loss) attributable to noncontrolling interest

16

(24)

(3)

(20)

Comprehensive income (loss) attributable to Allstate

$

188

$

(1,592)

$

1,222

$

(1,198)

See notes to condensed consolidated financial statements.

2www.allstate.com

Condensed Consolidated Financial Statements

The Allstate Corporation and Subsidiaries

Condensed Consolidated Statements of Financial Position (unaudited)

($ in millions, except par value data)

June 30, 2024

December 31, 2023

Assets

Investments

Fixed income securities, at fair value (amortized cost, net $53,788 and $49,649)

$

52,576

$

48,865

Equity securities, at fair value (cost $2,003 and $2,244)

2,216

2,411

Mortgage loans, net

815

822

Limited partnership interests

8,730

8,380

Short-term, at fair value (amortized cost $5,290 and $5,145)

5,288

5,144

Other investments, net

979

1,055

Total investments

70,604

66,677

Cash

599

722

Premium installment receivables, net

10,762

10,044

Deferred policy acquisition costs

6,112

5,940

Reinsurance and indemnification recoverables, net

8,730

8,809

Accrued investment income

609

539

Deferred income taxes

212

219

Property and equipment, net

777

859

Goodwill

3,502

3,502

Other assets, net

6,461

6,051

Total assets

108,368

103,362

Liabilities

Reserve for property and casualty insurance claims and claims expense

41,553

39,858

Reserve for future policy benefits

1,344

1,347

Contractholder funds

891

888

Unearned premiums

25,929

24,709

Claim payments outstanding

1,575

1,353

Other liabilities and accrued expenses

10,421

9,635

Debt

8,082

7,942

Total liabilities

89,795

85,732

Commitments and Contingent Liabilities (Note 14)

Equity

Preferred stock and additional capital paid-in, $1 par value, 25 million shares authorized, 82.0 thousand shares issued and outstanding, $2,050 aggregate liquidation preference

2,001

2,001

Common stock, $.01 par value, 2.0 billion shares authorized and 900 million issued, 264 million and 262 million shares outstanding

9

9

Additional capital paid-in

3,927

3,854

Retained income

50,718

49,716

Treasury stock, at cost (636 million and 638 million shares)

Unamortized pension and other postretirement prior service credit

12

13

Discount rate for reserve for future policy benefits

13

(11)

Total accumulated other comprehensive loss

(1,026)

(700)

Total Allstate shareholders’ equity

18,593

17,770

Noncontrolling interest

(20)

(140)

Total equity

18,573

17,630

Total liabilities and equity

$

108,368

$

103,362

See notes to condensed consolidated financial statements.

Second Quarter 2024 Form 10-Q 3

Condensed Consolidated Financial Statements

The Allstate Corporation and Subsidiaries

Condensed Consolidated Statements of Shareholders’ Equity (unaudited)

($ in millions, except per share data)

Three months ended June 30,

Six months ended June 30,

2024

2023

2024

2023

Preferred stock par value

$

—

$

—

$

—

$

—

Preferred stock additional capital paid-in

Balance, beginning of period

2,001

1,970

2,001

1,970

Preferred stock issuance, net of issuance costs

—

587

—

587

Preferred stock redemption

—

(556)

—

(556)

Balance, end of period

2,001

2,001

2,001

2,001

Common stock par value

9

9

9

9

Common stock additional capital paid-in

Balance, beginning of period

3,894

3,780

3,854

3,788

Equity incentive plans activity, net

33

6

73

(2)

Balance, end of period

3,927

3,786

3,927

3,786

Retained income

Balance, beginning of period

50,662

50,388

49,716

50,970

Net income (loss)

331

(1,352)

1,549

(1,672)

Dividends on common stock (declared per share of $0.92, $0.89, $1.84, and $1.78 )

(245)

(233)

(488)

(469)

Dividends on preferred stock

(30)

(37)

(59)

(63)

Balance, end of period

50,718

48,766

50,718

48,766

Treasury stock

Balance, beginning of period

(37,044)

(36,980)

(37,110)

(36,857)

Shares acquired

—

(154)

—

(307)

Shares reissued under equity incentive plans, net

8

3

74

33

Balance, end of period

(37,036)

(37,131)

(37,036)

(37,131)

Accumulated other comprehensive income (loss)

Balance, beginning of period

(883)

(1,673)

(700)

(2,392)

Change in unrealized net capital gains and losses

(119)

(272)

(334)

410

Change in unrealized foreign currency translation adjustments

(23)

28

(15)

78

Change in unamortized pension and other postretirement prior service credit

—

(5)

(1)

(9)

Change in discount rate for reserve for future policy benefits

(1)

8

24

(1)

Balance, end of period

(1,026)

(1,914)

(1,026)

(1,914)

Total Allstate shareholders’ equity

18,593

15,517

18,593

15,517

Noncontrolling interest

Balance, beginning of period

(159)

(121)

(140)

(125)

Change in unrealized net capital gains and losses

—

(1)

1

4

Noncontrolling income (loss)

16

(23)

(4)

(24)

Capital transaction for noncontrolling interest

123

—

123

—

Balance, end of period

(20)

(145)

(20)

(145)

Total equity

$

18,573

$

15,372

$

18,573

$

15,372

See notes to condensed consolidated financial statements.

4www.allstate.com

Condensed Consolidated Financial Statements

The Allstate Corporation and Subsidiaries

Condensed Consolidated Statements of Cash Flows (unaudited)

($ in millions)

Six months ended June 30,

2024

2023

Cash flows from operating activities

Net income (loss)

$

1,545

$

(1,696)

Adjustments to reconcile net income (loss) to net cash provided by operating activities

Depreciation, amortization and other non-cash items

264

363

Net (gains) losses on investments and derivatives

267

137

Pension and other postretirement remeasurement (gains) losses

(11)

(93)

Changes in:

Policy benefits and other insurance reserves

1,750

2,917

Unearned premiums

1,262

1,032

Deferred policy acquisition costs

(175)

(162)

Premium installment receivables, net

(745)

(532)

Reinsurance recoverables, net

76

468

Income taxes

91

(538)

Other operating assets and liabilities

(299)

(126)

Net cash provided by operating activities

4,025

1,770

Cash flows from investing activities

Proceeds from sales

Fixed income securities

15,463

12,454

Equity securities

1,510

4,183

Limited partnership interests

248

516

Other investments

120

81

Investment collections

Fixed income securities

1,002

992

Mortgage loans

10

36

Other investments

19

53

Investment purchases

Fixed income securities

(20,376)

(15,875)

Equity securities

(1,257)

(1,717)

Limited partnership interests

(560)

(424)

Mortgage loans

(1)

(100)

Other investments

(59)

(140)

Change in short-term and other investments, net

64

(986)

Purchases of property and equipment, net

(97)

(141)

Proceeds from sale of property and equipment

18

19

Net cash used in investing activities

(3,896)

(1,049)

Cash flows from financing activities

Proceeds from issuance of debt

495

743

Redemption and repayment of debt

(350)

(750)

Proceeds from issuance of preferred stock

—

587

Redemption of preferred stock

—

(575)

Contractholder fund deposits

67

66

Contractholder fund withdrawals

(16)

(16)

Dividends paid on common stock

(476)

(459)

Dividends paid on preferred stock

(59)

(53)

Treasury stock purchases

—

(307)

Shares reissued under equity incentive plans, net

93

10

Other

(6)

(4)

Net cash used in financing activities

(252)

(758)

Net decrease in cash

(123)

(37)

Cash at beginning of period

722

736

Cash at end of period

$

599

$

699

See notes to condensed consolidated financial statements.

Second Quarter 2024 Form 10-Q 5

Notes to Condensed Consolidated Financial Statements

The Allstate Corporation and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Note 1

General

Basis of presentation

The accompanying condensed consolidated financial statements include the accounts of The Allstate Corporation (the “Corporation”) and its wholly owned subsidiaries, primarily Allstate Insurance Company (“AIC”), a property and casualty insurance company (collectively referred to as the “Company” or “Allstate”) and variable interest entities (“VIEs”) in which the Company is considered a primary beneficiary. These condensed consolidated financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America (“GAAP”).

The condensed consolidated financial statements and notes as of June 30, 2024 and for the three and six month periods ended June 30, 2024 and 2023 are unaudited. The condensed consolidated financial statements reflect all adjustments (consisting only of normal recurring accruals) which are, in the opinion of management, necessary for the fair presentation of the financial position, results of operations and cash flows for the interim periods. Certain amounts have been reclassified to conform to current year presentation.

These condensed consolidated financial statements and notes should be read in conjunction with the consolidated financial statements and notes thereto included in the Company’s annual report on Form 10-K for the year ended December 31, 2023. The results of operations for the interim periods should not be considered indicative of results to be expected for the full year. All significant intercompany accounts and transactions have been eliminated.

Pending accounting standards

Accounting for joint ventures In August 2023, the Financial Accounting Standards Board (“FASB”) issued guidance requiring a joint venture to initially measure assets contributed and liabilities assumed at fair value as of the formation date. The new guidance will be applied prospectively for joint ventures with a formation date on or after January 1, 2025. The impact of the adoption is not expected to be material to the Company’s results of operations or financial position.

Segment reporting In November 2023, the FASB issued guidance expanding segment disclosures by requiring disclosure of significant segment expenses that are regularly provided to the chief operating decision maker and included within each reported measure of segment profit or loss, an amount and description of its composition for other segment items, and interim disclosures of reportable segments’ profit or loss and assets. The guidance is effective for annual periods beginning after December 15, 2023 and interim periods beginning after December 15, 2024 and is to be applied retrospectively, with early adoption permitted. The Company is currently evaluating the impact of adopting the guidance to its disclosures.

Income tax disclosures In December 2023, the FASB issued guidance enhancing various aspects of income tax disclosures. The guidance requires a tabular reconciliation between statutory and effective income tax expense (benefit) with both amounts and percentages for a list of required categories. For certain required categories where an individual category is at least five percent of the statutory tax amount, the required category must be further broken out by nature and, for foreign tax effects, jurisdiction. Additionally, entities must disclose income taxes paid, net of refunds received, broken out between federal, state and foreign, and amounts paid, net of refunds received, to an individual jurisdiction when five percent or more of the total income taxes paid, net of refunds received.

All requirements in the guidance are annual in nature, and the guidance is effective for annual reporting periods beginning after December 15, 2024, with early adoption permitted. The guidance only affects disclosures and will have no impact on the Company’s consolidated financial statements. The Company is currently evaluating the impact of adopting the guidance to its disclosures.

Climate disclosures In March 2024, the Securities and Exchange Commission (“SEC”) adopted a final rule requiring registrants to disclose certain climate-related information in their registration statements and annual reports. The rule requires the disclosure of qualitative and quantitative information, with certain information, such as financial statement effects of severe weather events, included in the notes to the audited financial statements. Other disclosure requirements include material climate-related risks, processes to manage and govern those risks, disclosure of targets if the targets materially affect or are reasonably likely to materially affect the Company, and, if material, disclosure of certain greenhouse gas emissions. On April 4, 2024, the SEC issued a voluntary stay of the final rule, pending the outcome of pending litigation.

The requirements will be applied prospectively and have phased-in effective dates. For the Company, the Form 10-K for the year ended December 31, 2025, will be the first annual report with new climate-related disclosures. The Company is currently evaluating the impact of adopting the final rule.

6www.allstate.com

Notes to Condensed Consolidated Financial Statements

Note 2

Earnings per Common Share

Basic earnings per common share is computed using the weighted average number of common shares outstanding, including vested unissued participating restricted stock units. Diluted earnings per common share is computed using the weighted average number of common and dilutive potential common shares outstanding.

For the Company, dilutive potential common shares consist of outstanding stock options, unvested

non-participating restricted stock units and contingently issuable performance stock awards. The effect of dilutive potential common shares does not include the effect of options with an anti-dilutive effect on earnings per common share because their exercise prices exceed the average market price of Allstate common shares during the period or for which the unrecognized compensation cost would have an anti-dilutive effect.

Computation of basic and diluted earnings per common share

(In millions, except per share data)

Three months ended June 30,

Six months ended June 30,

2024

2023

2024

2023

Numerator:

Net income (loss)

$

347

$

(1,375)

$

1,545

$

(1,696)

Less: Net income (loss) attributable to noncontrolling interest

16

(23)

(4)

(24)

Net income (loss) attributable to Allstate

331

(1,352)

1,549

(1,672)

Less: Preferred stock dividends

30

37

59

63

Net income (loss) applicable to common shareholders

$

301

$

(1,389)

$

1,490

$

(1,735)

Denominator:

Weighted average common shares outstanding

264.1

262.6

263.8

263.1

Effect of dilutive potential common shares (1):

Stock options

2.5

—

2.5

—

Restricted stock units (non-participating) and performance stock awards

0.5

—

0.5

—

Weighted average common and dilutive potential common shares outstanding

267.1

262.6

266.8

263.1

Earnings per common share - Basic

$

1.14

$

(5.29)

$

5.65

$

(6.59)

Earnings per common share - Diluted (1)

$

1.13

$

(5.29)

$

5.58

$

(6.59)

Anti-dilutive options excluded from diluted earnings per common share

0.6

3.2

0.5

2.9

Weighted average dilutive potential common shares excluded due to net loss applicable to common shareholders (1)

—

1.7

—

2.1

(1)As a result of the net loss reported for the three and six month periods ended June 30, 2023, weighted average shares for basic earnings per share is also used for calculating diluted earnings per share because all dilutive potential common shares are anti-dilutive and are therefore excluded from the calculation.

Note 3

Reportable Segments

Measuring segment profit or loss

The measure of segment profit or loss used in evaluating performance is underwriting income for the Allstate Protection and Run-off Property-Liability segments and adjusted net income for the Protection Services, Allstate Health and Benefits and Corporate and Other segments.

Allstate Protection and Run-off Property Liability segments comprise Property-Liability. The Company does not allocate investment income, net gains and losses on investments and derivatives, or assets to the Allstate Protection and Run-off Property Liability segments. Management reviews assets at the Property-Liability, Protection Services, Allstate Health and Benefits, and Corporate and Other levels for decision-making purposes.

Underwriting income is calculated as premiums earned and other revenue, less claims and claims expenses (“losses”), amortization of deferred policy

acquisition costs (“DAC”), operating costs and expenses, amortization or impairment of purchased intangibles and restructuring and related charges as determined using GAAP.

Adjusted net income is net income (loss) applicable to common shareholders, excluding:

•

Net gains and losses on investments and derivatives

•

Pension and other postretirement remeasurement gains and losses

•

Amortization or impairment of purchased intangibles

•

Gain or loss on disposition

•

Adjustments for other significant non-recurring, infrequent or unusual items, when (a) the nature of the charge or gain is such that it is reasonably unlikely to recur within two years, or (b) there has been no similar charge or gain within the prior two years

•

Income tax expense or benefit on reconciling items

Second Quarter 2024 Form 10-Q 7

Notes to Condensed Consolidated Financial Statements

A reconciliation of these measures to net income (loss) applicable to common shareholders is provided below.

Reportable segments financial performance

Three months ended June 30,

Six months ended June 30,

($ in millions)

2024

2023

2024

2023

Underwriting income (loss) by segment

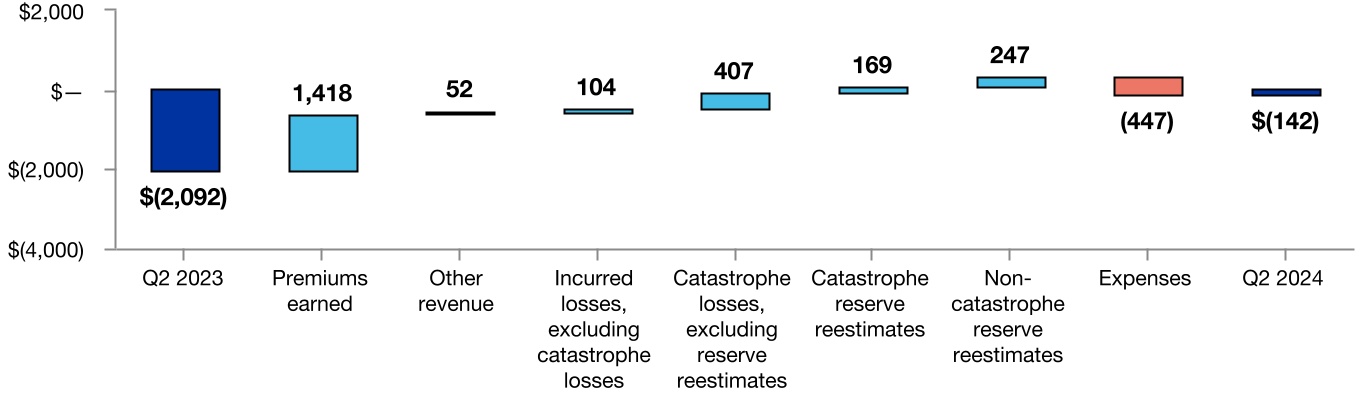

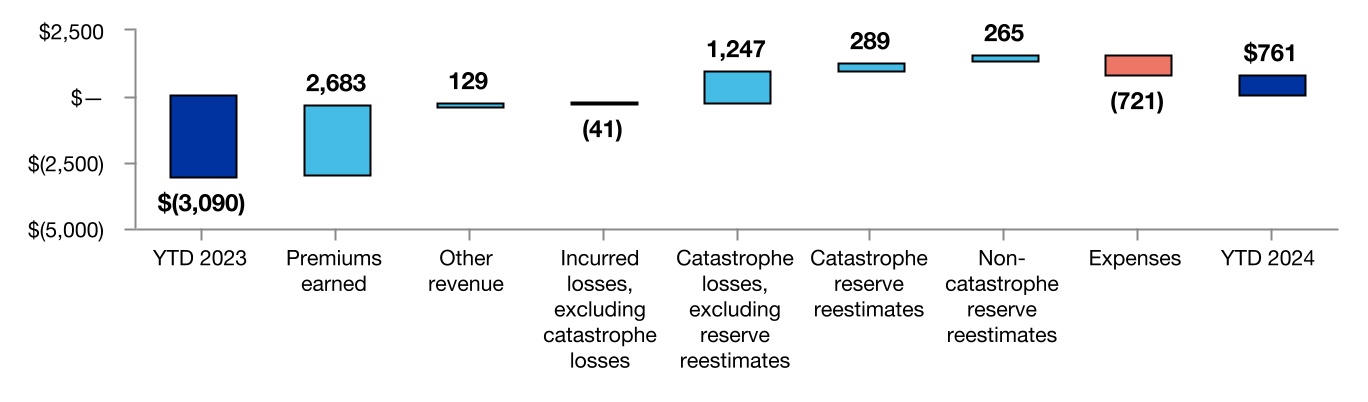

Allstate Protection

$

(142)

$

(2,092)

$

761

$

(3,090)

Run-off Property-Liability

(3)

(2)

(8)

(5)

Total Property-Liability

(145)

(2,094)

753

(3,095)

Adjusted net income (loss) by segment, after-tax

Protection Services

55

41

109

75

Allstate Health and Benefits

58

57

114

113

Corporate and Other

(104)

(111)

(210)

(200)

Reconciling items

Allstate Protection and Run-off Property-Liability net investment income

643

544

1,345

1,053

Net gains (losses) on investments and derivatives

(103)

(151)

(267)

(137)

Pension and other postretirement remeasurement gains (losses)

9

40

11

93

Amortization of purchased intangibles (1)

(19)

(24)

(37)

(48)

Gain (loss) on disposition

1

(8)

5

1

Non-recurring costs(2)

—

(90)

—

(90)

Income tax (expense) benefit on Property-Liability and reconciling items (3)

(78)

384

(337)

476

Total reconciling items

453

695

720

1,348

Less: Net income (loss) attributable to noncontrolling interest (4)

16

(23)

(4)

(24)

Net income (loss) applicable to common shareholders

$

301

$

(1,389)

$

1,490

$

(1,735)

(1)Excludes amortization of purchased intangibles in Property-Liability, which is already included above in underwriting income.

(2)Relates to settlement costs for non-recurring litigation that is outside of the ordinary course of business.

(3)The tax computation of the reporting segments and income tax benefit (expense) on reconciling items to net income (loss) are computed discretely based on the tax law of the jurisdictions applicable to the reporting entities.

(4)Reflects net income (loss) attributable to noncontrolling interest in Property-Liability.

8www.allstate.com

Notes to Condensed Consolidated Financial Statements

Reportable segments revenue information

($ in millions)

Three months ended June 30,

Six months ended June 30,

2024

2023

2024

2023

Property-Liability

Insurance premiums

Auto

$

9,079

$

8,121

$

17,857

$

16,029

Homeowners

3,255

2,883

6,409

5,693

Other personal lines

701

587

1,360

1,149

Commercial lines

158

202

327

434

Other business lines

146

128

286

251

Allstate Protection

13,339

11,921

26,239

23,556

Run-off Property-Liability

—

—

—

—

Total Property-Liability insurance premiums

13,339

11,921

26,239

23,556

Other revenue

441

389

871

742

Net investment income

643

544

1,345

1,053

Net gains (losses) on investments and derivatives

(103)

(135)

(265)

(123)

Total Property-Liability

14,320

12,719

28,190

25,228

Protection Services

Protection plans

453

373

892

734

Roadside assistance

34

48

81

97

Protection and insurance products

126

128

252

256

Intersegment premiums and service fees (1)

39

35

74

68

Other revenue

98

84

183

168

Net investment income

23

18

44

34

Net gains (losses) on investments and derivatives

(1)

(4)

(6)

(5)

Total Protection Services

772

682

1,520

1,352

Allstate Health and Benefits

Employer voluntary benefits

246

245

494

500

Group health

120

110

238

217

Individual health

108

98

220

199

Other revenue

121

101

255

202

Net investment income

25

21

48

40

Net gains (losses) on investments and derivatives

—

1

2

3

Total Allstate Health and Benefits

620

576

1,257

1,161

Corporate and Other

Other revenue

19

23

39

46

Net investment income

21

27

39

58

Net gains (losses) on investments and derivatives

1

(13)

2

(12)

Total Corporate and Other

41

37

80

92

Intersegment eliminations (1)

(39)

(35)

(74)

(68)

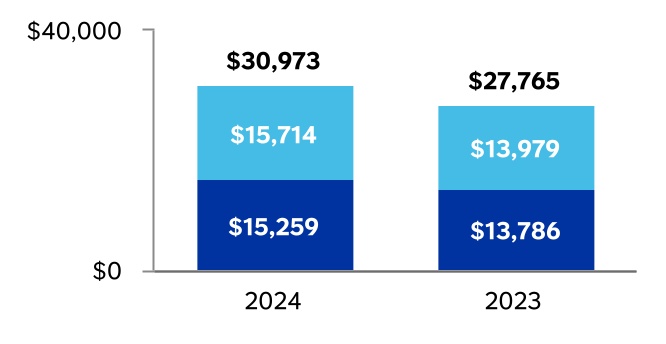

Consolidated revenues

$

15,714

$

13,979

$

30,973

$

27,765

(1)Intersegment insurance premiums and service fees are primarily related to Arity and Allstate Roadside and are eliminated in the condensed consolidated financial statements.

Second Quarter 2024 Form 10-Q 9

Notes to Condensed Consolidated Financial Statements

Note 4

Investments

Portfolio composition

($ in millions)

June 30, 2024

December 31, 2023

Fixed income securities, at fair value

$

52,576

$

48,865

Equity securities, at fair value

2,216

2,411

Mortgage loans, net

815

822

Limited partnership interests

8,730

8,380

Short-term investments, at fair value

5,288

5,144

Other investments, net

979

1,055

Total

$

70,604

$

66,677

Amortized cost, gross unrealized gains (losses) and fair value for fixed income securities

($ in millions)

Amortized cost, net

Gross unrealized

Fair

value

Gains

Losses

June 30, 2024

U.S. government and agencies

$

10,724

$

34

$

(194)

$

10,564

Municipal

6,661

46

(169)

6,538

Corporate

33,443

191

(1,120)

32,514

Foreign government

1,299

5

(15)

1,289

ABS

1,661

16

(6)

1,671

Total fixed income securities

$

53,788

$

292

$

(1,504)

$

52,576

December 31, 2023

U.S. government and agencies

$

8,624

$

114

$

(119)

$

8,619

Municipal

6,049

109

(152)

6,006

Corporate

31,951

397

(1,143)

31,205

Foreign government

1,286

17

(13)

1,290

ABS

1,739

13

(7)

1,745

Total fixed income securities

$

49,649

$

650

$

(1,434)

$

48,865

Scheduled maturities for fixed income securities

($ in millions)

June 30, 2024

December 31, 2023

Amortized cost, net

Fair

value

Amortized cost, net

Fair

value

Due in one year or less

$

2,692

$

2,655

$

3,422

$

3,374

Due after one year through five years

23,799

23,172

23,218

22,614

Due after five years through ten years

16,675

16,305

12,553

12,273

Due after ten years

8,961

8,773

8,717

8,859

52,127

50,905

47,910

47,120

ABS

1,661

1,671

1,739

1,745

Total

$

53,788

$

52,576

$

49,649

$

48,865

Actual maturities may differ from those scheduled as a result of calls and make-whole payments by the issuers. ABS is shown separately because of potential prepayment of principal prior to contractual maturity dates.

Net investment income

($ in millions)

Three months ended June 30,

Six months ended June 30,

2024

2023

2024

2023

Fixed income securities

$

571

$

422

$

1,097

$

812

Equity securities

18

21

33

32

Mortgage loans

9

8

18

16

Limited partnership interests

103

122

302

256

Short-term investments

62

69

129

135

Other investments

25

39

46

80

Investment income, before expense

788

681

1,625

1,331

Investment expense

(76)

(71)

(149)

(146)

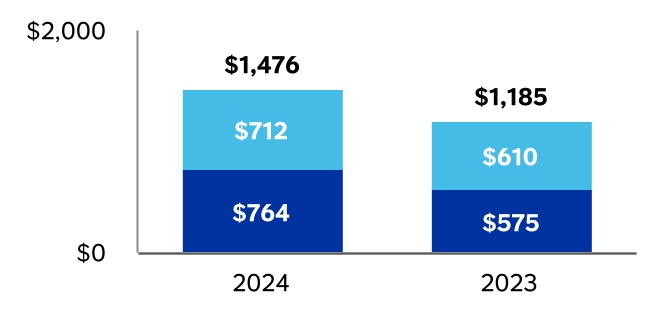

Net investment income

$

712

$

610

$

1,476

$

1,185

10www.allstate.com

Notes to Condensed Consolidated Financial Statements

Net gains (losses) on investments and derivatives by asset type

($ in millions)

Three months ended June 30,

Six months ended June 30,

2024

2023

2024

2023

Fixed income securities

$

(96)

$

(132)

$

(197)

$

(268)

Equity securities

14

21

76

188

Mortgage loans

1

(3)

1

(3)

Limited partnership interests

(13)

(15)

(5)

7

Derivatives

(15)

(7)

(23)

(59)

Other investments

6

(15)

4

(2)

Other (1)

—

—

(123)

—

Net gains (losses) on investments and derivatives

$

(103)

$

(151)

$

(267)

$

(137)

(1)Related to the loss for the carrying value of the surplus notes issued by Adirondack Insurance Exchange and New Jersey Skylands Insurance Association (together “Reciprocal Exchanges”). See Note 7 for further detail.

Net gains (losses) on investments and derivatives by transaction type

($ in millions)

Three months ended June 30,

Six months ended June 30,

2024

2023

2024

2023

Sales

$

(90)

$

(130)

$

(201)

$

(250)

Credit losses

(16)

(37)

(131)

(49)

Valuation change of equity investments (1)

18

23

88

221

Valuation change and settlements of derivatives

(15)

(7)

(23)

(59)

Net gains (losses) on investments and derivatives

$

(103)

$

(151)

$

(267)

$

(137)

(1)Includes valuation change of equity securities and certain limited partnership interests where the underlying assets are predominately public equity securities.

Gross realized gains (losses) on sales of fixed income securities

($ in millions)

Three months ended June 30,

Six months ended June 30,

2024

2023

2024

2023

Gross realized gains

$

33

$

28

$

74

$

74

Gross realized losses

(124)

(153)

(270)

(326)

Net appreciation (decline) recognized in net income for assets that are still held

($ in millions)

Three months ended June 30,

Six months ended June 30,

2024

2023

2024

2023

Equity securities

$

18

$

19

$

78

$

66

Limited partnership interests carried at fair value

17

32

47

48

Total

$

35

$

51

$

125

$

114

Second Quarter 2024 Form 10-Q 11

Notes to Condensed Consolidated Financial Statements

Credit losses recognized in net income

($ in millions)

Three months ended June 30,

Six months ended June 30,

2024

2023

2024

2023

Assets

Fixed income securities:

Corporate

$

(5)

$

(7)

$

(1)

$

(16)

Total fixed income securities

(5)

(7)

(1)

(16)

Mortgage loans

1

(3)

1

(3)

Limited partnership interests

(16)

(16)

(16)

(16)

Other investments

Bank loans

2

(11)

5

(14)

Real estate

2

—

2

—

Other assets

—

—

(123)

—

Total credit losses by asset type

$

(16)

$

(37)

$

(132)

$

(49)

Liabilities

Commitments to fund commercial mortgage loans and bank loans

—

—

1

—

Total

$

(16)

$

(37)

$

(131)

$

(49)

Unrealized net capital gains and losses included in accumulated other comprehensive income (“AOCI”)

($ in millions)

Fair

value

Gross unrealized

Unrealized net

gains (losses)

June 30, 2024

Gains

Losses

Fixed income securities

$

52,576

$

292

$

(1,504)

$

(1,212)

Short-term investments

5,288

—

(2)

(2)

Derivative instruments

—

—

(2)

(2)

Limited partnership interests

—

Unrealized net capital gains and losses, pre-tax

(1,216)

Reclassification of noncontrolling interest

12

Deferred income taxes

266

Unrealized net capital gains and losses, after-tax

$

(938)

December 31, 2023

Fixed income securities

$

48,865

$

650

$

(1,434)

$

(784)

Short-term investments

5,144

—

(1)

(1)

Derivative instruments

—

—

(2)

(2)

Limited partnership interests (1)

(4)

Unrealized net capital gains and losses, pre-tax

(791)

Reclassification of noncontrolling interest

13

Deferred income taxes

174

Unrealized net capital gains and losses, after-tax

$

(604)

(1)Unrealized net capital gains and losses for limited partnership interests represent the Company’s share of the equity method of accounting (“EMA”) limited partnerships’ OCI. Fair value and gross unrealized gains and losses are not applicable.

Change in unrealized net capital gains (losses)

($ in millions)

Six months ended June 30, 2024

Fixed income securities

$

(428)

Short-term investments

(1)

Derivative instruments

—

Limited partnership interests

4

Total

(425)

Reclassification of noncontrolling interest

(1)

Deferred income taxes

92

Change in unrealized net capital gains and losses, after-tax

$

(334)

12www.allstate.com

Notes to Condensed Consolidated Financial Statements

Carrying value for limited partnership interests

($ in millions)

June 30, 2024

December 31, 2023

Private equity

$

7,426

$

7,154

Real estate

1,142

1,085

Other (1)

162

141

Total

$

8,730

$

8,380

(1)Other consists of certain limited partnership interests where the underlying assets are predominately public equity and debt securities.

Short-term investments Short-term investments, including money market funds, commercial paper, U.S. Treasury bills and other short-term investments, are carried at fair value. As of June 30, 2024 and December 31, 2023, the fair value of short-term investments totaled $5.29 billion and $5.14 billion, respectively.

Other investments Other investments primarily consist of bank loans, real estate, policy loans and derivatives. Bank loans are primarily senior secured corporate loans and are carried at amortized cost, net. Real estate is carried at cost less accumulated depreciation. Policy loans are carried at unpaid principal balances.

Other investments by asset type

($ in millions)

June 30, 2024

December 31, 2023

Bank loans, net

$

149

$

224

Real estate

708

709

Policy loans

120

119

Other

2

3

Total

$

979

$

1,055

Portfolio monitoring and credit losses

Fixed income securitiesThe Company has a comprehensive portfolio monitoring process to identify and evaluate each fixed income security that may require a credit loss allowance.

For each fixed income security in an unrealized loss position, the Company assesses whether management with the appropriate authority has made the decision to sell or whether it is more likely than not the Company will be required to sell the security before recovery of the amortized cost basis for reasons such as liquidity, contractual or regulatory purposes. If a security meets either of these criteria, any existing credit loss allowance would be written-off against the amortized cost basis of the asset along with any remaining unrealized losses, with incremental losses recorded in earnings.

If the Company has not made the decision to sell the fixed income security and it is not more likely than not the Company will be required to sell the fixed income security before recovery of its amortized cost basis, the Company evaluates whether it expects to receive cash flows sufficient to recover the entire amortized cost basis of the security. The Company calculates the estimated recovery value based on the best estimate of future cash flows considering past events, current conditions and reasonable and supportable forecasts. The estimated future cash flows are discounted at the security’s current effective rate and is compared to the amortized cost of the security.

The determination of cash flow estimates is inherently subjective, and methodologies may vary depending on facts and circumstances specific to the security. All reasonably available information relevant to the collectability of the security is considered when developing the estimate of cash flows expected to be collected. That information generally includes, but is

not limited to, the remaining payment terms of the security, prepayment speeds, the financial condition and future earnings potential of the issue or issuer, expected defaults, expected recoveries, the value of underlying collateral, origination vintage year, geographic concentration of underlying collateral, available reserves or escrows, current subordination levels, third-party guarantees and other credit enhancements. Other information, such as industry analyst reports and forecasts, credit ratings, financial condition of the bond insurer for insured fixed income securities, and other market data relevant to the realizability of contractual cash flows, may also be considered. The estimated fair value of collateral will be used to estimate recovery value if the Company determines that the security is dependent on the liquidation of collateral for ultimate settlement.

If the Company does not expect to receive cash flows sufficient to recover the entire amortized cost basis of the fixed income security, a credit loss allowance is recorded in earnings for the shortfall in expected cash flows; however, the amortized cost, net of the credit loss allowance, may not be lower than the fair value of the security. The portion of the unrealized loss related to factors other than credit remains classified in AOCI. If the Company determines that the fixed income security does not have sufficient cash flow or other information to estimate a recovery value for the security, the Company may conclude that the entire decline in fair value is deemed to be credit related and the loss is recorded in earnings.

When a security is sold or otherwise disposed or when the security is deemed uncollectible and written off, the Company removes amounts previously recognized in the credit loss allowance. Recoveries after write-offs are recognized when received. Accrued interest excluded from the amortized cost of fixed income securities totaled $570 million and $495 million

Second Quarter 2024 Form 10-Q 13

Notes to Condensed Consolidated Financial Statements

as of June 30, 2024 and December 31, 2023, respectively, and is reported within the accrued investment income line of the Condensed Consolidated Statements of Financial Position. The Company monitors accrued interest and writes off amounts when they are not expected to be received.

The Company’s portfolio monitoring process includes a quarterly review of all securities to identify instances where the fair value of a security compared to its amortized cost is below internally established thresholds. The process also includes the monitoring of other credit loss indicators such as ratings, ratings downgrades and payment defaults. The securities identified, in addition to other securities for which the Company may have a concern, are evaluated for potential credit losses using all reasonably available

information relevant to the collectability or recovery of the security. Inherent in the Company’s evaluation of credit losses for these securities are assumptions and estimates about the financial condition and future earnings potential of the issue or issuer. Some of the factors that may be considered in evaluating whether a decline in fair value requires a credit loss allowance are: 1) the financial condition, near-term and long-term prospects of the issue or issuer, including relevant industry specific market conditions and trends, geographic location and implications of rating agency actions and offering prices; 2) the specific reasons that a security is in an unrealized loss position, including overall market conditions which could affect liquidity; and 3) the extent to which the fair value has been less than amortized cost.

Rollforward of credit loss allowance for fixed income securities

Three months ended June 30,

Six months ended June 30,

($ in millions)

2024

2023

2024

2023

Beginning balance

$

(17)

$

(22)

$

(36)

$

(13)

Credit losses on securities for which credit losses not previously reported

(4)

(4)

(7)

(4)

Net (increases) decreases related to credit losses previously reported

(1)

(3)

3

(12)

(Increase) decrease of allowance related to sales and other

—

—

3

—

Write-offs

3

—

18

—

Ending balance

$

(19)

$

(29)

$

(19)

$

(29)

Components of credit loss allowance as of June 30

Corporate bonds

$

(18)

$

(27)

ABS

(1)

(2)

Total

$

(19)

$

(29)

14www.allstate.com

Notes to Condensed Consolidated Financial Statements

Gross unrealized losses and fair value by type and length of time held in a continuous unrealized loss position (1)

($ in millions)

Less than 12 months

12 months or more

Total

unrealized

losses

Number

of

issues

Fair

value

Unrealized

losses

Number

of

issues

Fair

value

Unrealized

losses

June 30, 2024

Fixed income securities

U.S. government and agencies

106

$

3,935

$

(64)

135

$

3,297

$

(130)

$

(194)

Municipal

629

2,063

(19)

1,525

2,060

(150)

(169)

Corporate

712

7,939

(119)

1,883

14,087

(1,001)

(1,120)

Foreign government

36

257

(2)

76

286

(13)

(15)

ABS

72

345

(2)

98

92

(4)

(6)

Total fixed income securities

1,555

$

14,539

$

(206)

3,717

$

19,822

$

(1,298)

$

(1,504)

Investment grade fixed income securities

1,462

$

14,107

$

(196)

3,404

$

17,754

$

(1,148)

$

(1,344)

Below investment grade fixed income securities

93

432

(10)

313

2,068

(150)

(160)

Total fixed income securities

1,555

$

14,539

$

(206)

3,717

$

19,822

$

(1,298)

$

(1,504)

December 31, 2023

Fixed income securities

U.S. government and agencies

63

$

2,554

$

(38)

117

$

2,513

$

(81)

$

(119)

Municipal

271

400

(4)

1,784

2,245

(148)

(152)

Corporate

251

2,225

(48)

2,106

17,319

(1,095)

(1,143)

Foreign government

7

31

—

75

356

(13)

(13)

ABS

19

64

(1)

150

584

(6)

(7)

Total fixed income securities

611

$

5,274

$

(91)

4,232

$

23,017

$

(1,343)

$

(1,434)

Investment grade fixed income securities

568

$

5,061

$

(83)

3,864

$

20,429

$

(1,151)

$

(1,234)

Below investment grade fixed income securities

43

213

(8)

368

2,588

(192)

(200)

Total fixed income securities

611

$

5,274

$

(91)

4,232

$

23,017

$

(1,343)

$

(1,434)

(1)Includes fixed income securities with fair values of $24 million and $32 million and unrealized losses of $6 million and $3 million with credit loss allowances of $4 million and $8 million as of June 30, 2024 and December 31, 2023, respectively.

Gross unrealized losses by unrealized loss position and credit quality as of June 30, 2024

($ in millions)

Investment

grade

Below investment grade

Total

Fixed income securities with unrealized loss position less than 20% of amortized cost, net (1)

$

(1,266)

$

(134)

$

(1,400)

Fixed income securities with unrealized loss position greater than or equal to 20% of amortized cost, net (2)

(78)

(26)

(104)

Total unrealized losses

$

(1,344)

$

(160)

$

(1,504)

(1)Related to securities with an unrealized loss position less than 20% of amortized cost, net, the degree of which suggests that these securities do not pose a high risk of having credit losses.

(2)Evaluated based on factors such as discounted cash flows and the financial condition and near-term and long-term prospects of the issue or issuer and were determined to have adequate resources to fulfill contractual obligations.

Investment grade is defined as a security having a National Association of Insurance Commissioners (“NAIC”) designation of 1 or 2, which is comparable to a rating of Aaa, Aa, A or Baa from Moody’s or AAA, AA, A or BBB from S&P Global Ratings (“S&P”), or a comparable internal rating if an externally provided rating is not available. Market prices for certain securities may have credit spreads which imply higher or lower credit quality than the current third-party rating. Unrealized losses on investment grade securities are principally related to an increase in market yields which may include increased risk-free interest rates or wider credit spreads since the time of initial purchase. The unrealized losses are expected to reverse as the securities approach maturity.

ABS in an unrealized loss position were evaluated based on actual and projected collateral losses relative to the securities’ positions in the respective securitization trusts, security specific expectations of cash flows, and credit ratings. This evaluation also takes into consideration credit enhancement, measured in terms of (i) subordination from other classes of securities in the trust that are contractually obligated to absorb losses before the class of security the Company owns, and (ii) the expected impact of other structural features embedded in the securitization trust beneficial to the class of securities the Company owns, such as overcollateralization and excess spread. Municipal bonds in an unrealized loss position were evaluated based on the underlying credit

Second Quarter 2024 Form 10-Q 15

Notes to Condensed Consolidated Financial Statements

quality of the primary obligor, obligation type and quality of the underlying assets.

As of June 30, 2024, the Company has not made the decision to sell and it is not more likely than not the Company will be required to sell fixed income securities with unrealized losses before recovery of the amortized cost basis.

Loans The Company establishes a credit loss allowance for mortgage loans and bank loans when they are originated or purchased, and for unfunded commitments unless they are unconditionally cancellable by the Company. The Company uses a probability of default and loss given default model for mortgage loans and bank loans to estimate current expected credit losses that considers all relevant information available including past events, current conditions, and reasonable and supportable forecasts over the life of an asset. The Company also considers such factors as historical losses, expected prepayments and various economic factors. For mortgage loans, the Company considers origination vintage year and property level information such as debt service coverage, property type, property location and collateral value. For bank loans, the Company considers the credit rating of the borrower, credit spreads and type of loan. After the reasonable and supportable forecast period, the Company’s model reverts to historical loss trends.

Loans are evaluated on a pooled basis when they share similar risk characteristics. The Company monitors loans through a quarterly credit monitoring process to determine when they no longer share similar risk characteristics and are to be evaluated individually when estimating credit losses.

Loans are written off against their corresponding allowances when there is no reasonable expectation of recovery. If a loan recovers after a write-off, the estimate of expected credit losses includes the expected recovery.

Accrual of income is suspended for loans that are in default or when full and timely collection of principal

and interest payments is not probable. Accrued income receivable is monitored for recoverability and when not expected to be collected is written off through net investment income. Cash receipts on loans on non-accrual status are generally recorded as a reduction of amortized cost.

Accrued interest is excluded from the amortized cost of loans and is reported within the accrued investment income line of the Condensed Consolidated Statements of Financial Position. Accrued interest as of June 30, 2024 and December 31, 2023 was not significant for bank loans or mortgage loans.

Mortgage loans When it is determined a mortgage loan shall be evaluated individually, the Company uses various methods to estimate credit losses on individual loans such as using collateral value less estimated costs to sell where applicable, including when foreclosure is probable or when repayment is expected to be provided substantially through the operation or sale of the collateral and the borrower is experiencing financial difficulty. When collateral value is used, the mortgage loans may not have a credit loss allowance when the fair value of the collateral exceeds the loan’s amortized cost. An alternative approach may be utilized to estimate credit losses using the present value of the loan’s expected future repayment cash flows discounted at the loan’s current effective interest rate. Individual loan credit loss allowances are adjusted for subsequent changes in the fair value of the collateral less costs to sell, when applicable, or present value of the loan’s expected future repayment cash flows.

Debt service coverage ratio is considered a key credit quality indicator when mortgage loan credit loss allowances are estimated. Debt service coverage ratio represents the amount of estimated cash flow from the property available to the borrower to meet principal and interest payment obligations. Debt service coverage ratio estimates are updated annually or more frequently if conditions are warranted based on the Company’s credit monitoring process.

Mortgage loans amortized cost by debt service coverage ratio distribution and year of origination

June 30, 2024

December 31, 2023

($ in millions)

2019 and prior

2020

2021

2022

2023

Current

Total

Total

Below 1.0

$

—

$

—

$

—

$

13

$

—

$

—

$

13

$

13

1.0 - 1.25

39

—

—

—

2

—

41

41

1.26 - 1.50

74

10

—

30

66

—

180

133

Above 1.50

230

42

183

60

76

—

591

646

Amortized cost before allowance

$

343

$

52

$

183

$

103

$

144

$

—

$

825

$

833

Allowance

(10)

(11)

Amortized cost, net

$

815

$

822

16www.allstate.com

Notes to Condensed Consolidated Financial Statements

Mortgage loans with a debt service coverage ratio below 1.0 that are not considered impaired primarily relate to instances where the borrower has the financial capacity to fund the revenue shortfalls from the properties for the foreseeable term, the decrease in cash flows from the properties is considered

temporary, or there are other risk mitigating circumstances such as additional collateral, escrow balances or borrower guarantees. Payments on all mortgage loans were current as of June 30, 2024 and December 31, 2023.

Rollforward of credit loss allowance for mortgage loans

Three months ended June 30,

Six months ended June 30,

($ in millions)

2024

2023

2024

2023

Beginning balance

$

(11)

$

(7)

$

(11)

$

(7)

Net (increases) decreases related to credit losses

1

(3)

1

(3)

Write-offs

—

—

—

—

Ending balance

$

(10)

$

(10)

$

(10)

$

(10)

Bank loans When it is determined a bank loan shall be evaluated individually, the Company uses various methods to estimate credit losses on individual loans such as the present value of the loan’s expected future repayment cash flows discounted at the loan’s current effective interest rate.

Credit ratings of the borrower are considered a key credit quality indicator when bank loan credit loss allowances are estimated. The ratings are either received from the Securities Valuation Office of the NAIC based on availability of applicable ratings from rating agencies on the NAIC credit rating provider list or a comparable internal rating. The year of origination is determined to be the year in which the asset is acquired.

Bank loans amortized cost by credit rating and year of origination

June 30, 2024

December 31, 2023

($ in millions)

2019 and prior

2020

2021

2022

2023

Current

Total

Total

NAIC 2 / BBB

$

—

$

1

$

—

$

—

$

1

$

1

$

3

$

9

NAIC 3 / BB

—

—

1

—

5

12

18

38

NAIC 4 / B

24

1

8

3

49

39

124

153

NAIC 5-6 / CCC and below

8

—

2

—

2

3

15

46

Amortized cost before allowance

$

32

$

2

$

11

$

3

$

57

$

55

$

160

$

246

Allowance

(11)

(22)

Amortized cost, net

$

149

$

224

Rollforward of credit loss allowance for bank loans

($ in millions)

Three months ended June 30,

Six months ended June 30,

2024

2023

2024

2023

Beginning balance

$

(13)

$

(52)

$

(22)

$

(57)

Net (increases) decreases related to credit losses

2

(11)

5

(14)

Reduction of allowance related to sales

—

1

—

6

Write-offs

—

—

6

3

Ending balance

$

(11)

$

(62)

$

(11)

$

(62)

Note 5

Fair Value of Assets and Liabilities

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The hierarchy for inputs used in determining fair value maximizes the use of observable inputs and minimizes the use of unobservable inputs by requiring that observable inputs be used when available. Assets and liabilities recorded on the Condensed Consolidated Statements of Financial Position at fair value are categorized in the

fair value hierarchy based on the observability of inputs to the valuation techniques as follows:

Level 1: Assets and liabilities whose values are based on unadjusted quoted prices for identical assets or liabilities in an active market that the Company can access.

Level 2: Assets and liabilities whose values are based on the following:

(a)Quoted prices for similar assets or liabilities in active markets;

Second Quarter 2024 Form 10-Q 17

Notes to Condensed Consolidated Financial Statements

(b)Quoted prices for identical or similar assets or liabilities in markets that are not active; or

(c)Valuation models whose inputs are observable, directly or indirectly, for substantially the full term of the asset or liability.

Level 3: Assets and liabilities whose values are based on prices or valuation techniques that require inputs that are both unobservable and significant to the overall fair value measurement. Unobservable inputs reflect the Company’s estimates of the assumptions that market participants would use in valuing the assets and liabilities.

The availability of observable inputs varies by instrument. In situations where fair value is based on internally developed pricing models or inputs that are unobservable in the market, the determination of fair value requires more judgment. The degree of judgment exercised by the Company in determining fair value is typically greatest for instruments categorized in Level 3. In many instances, valuation inputs used to measure fair value fall into different levels of the fair value hierarchy. The category level in the fair value hierarchy is determined based on the lowest level input that is significant to the fair value measurement in its entirety. The Company uses prices and inputs that are current as of the measurement date, including during periods of market disruption. In periods of market disruption, the ability to observe prices and inputs may be reduced for many instruments.

The Company is responsible for the determination of fair value and the supporting assumptions and methodologies. The Company gains assurance that assets and liabilities are appropriately valued through the execution of various processes and controls designed to ensure the overall reasonableness and consistent application of valuation methodologies, including inputs and assumptions, and compliance with accounting standards. For fair values received from third parties or internally estimated, the Company’s processes and controls are designed to ensure that the valuation methodologies are appropriate and consistently applied, the inputs and assumptions are reasonable and consistent with the objective of determining fair value, and the fair values are accurately recorded. For example, on a continuing basis, the Company assesses the reasonableness of individual fair values that have stale security prices or that exceed certain thresholds as compared to previous fair values received from valuation service providers or brokers or derived from internal models. The Company performs procedures to understand and assess the methodologies, processes and controls of valuation service providers.

In addition, the Company may validate the reasonableness of fair values by comparing information obtained from valuation service providers or brokers to other third-party valuation sources for selected securities. The Company performs ongoing price validation procedures such as back-testing of actual sales, which corroborate the various inputs used in internal models to market observable data. When fair

value determinations are expected to be more variable, the Company validates them through reviews by members of management who have relevant expertise and who are independent of those charged with executing investment transactions.

The Company has two types of situations where investments are classified as Level 3 in the fair value hierarchy:

(1)Specific inputs significant to the fair value estimation models are not market observable. This primarily occurs in the Company’s use of broker quotes to value certain securities where the inputs have not been corroborated to be market observable, and the use of valuation models that use significant non-market observable inputs.

(2)Quotes continue to be received from independent third-party valuation service providers and all significant inputs are market observable; however, there has been a significant decrease in the volume and level of activity for the asset when compared to normal market activity such that the degree of market observability has declined to a point where categorization as a Level 3 measurement is considered appropriate. The indicators considered in determining whether a significant decrease in the volume and level of activity for a specific asset has occurred include the level of new issuances in the primary market, trading volume in the secondary market, the level of credit spreads over historical levels, applicable bid-ask spreads, and price consensus among market participants and other pricing sources.

Certain assets are not carried at fair value on a recurring basis, including mortgage loans, bank loans, real estate and policy loans and are only included in the fair value hierarchy disclosure when the individual investment is reported at fair value.

In determining fair value, the Company principally uses the market approach which generally utilizes market transaction data for the same or similar instruments. To a lesser extent, the Company uses the income approach which involves determining fair values from discounted cash flow methodologies. For the majority of Level 2 and Level 3 valuations, a combination of the market and income approaches is used.

Summary of significant inputs and valuation techniques for Level 2 and Level 3 assets and liabilities measured at fair value on a recurring basis

Level 2 measurements

•Fixed income securities:

U.S. government and agencies, municipal, corporate - public and foreign government: The primary inputs to the valuation include quoted prices for identical or similar assets in markets that are not active, contractual cash flows, benchmark yields and credit spreads.

Corporate - privately placed:Privately placed are valued using a discounted cash flow model that is widely accepted in the financial services industry

18www.allstate.com

Notes to Condensed Consolidated Financial Statements

and uses market observable inputs and inputs derived principally from, or corroborated by, observable market data. The primary inputs to the discounted cash flow model include an interest rate yield curve, as well as published credit spreads for similar assets in markets that are not active that incorporate the credit quality and industry sector of the issuer.

Corporate - privately placed also includes redeemable preferred stock that are valued using quoted prices for identical or similar assets in markets that are not active, contractual cash flows, benchmark yields, underlying stock prices and credit spreads.

ABS:The primary inputs to the valuation include quoted prices for identical or similar assets in markets that are not active, contractual cash flows, benchmark yields, collateral performance and credit spreads. Certain ABS are valued based on non-binding broker quotes whose inputs have been corroborated to be market observable. Residential mortgage-backed securities, included in ABS, use prepayment speeds as a primary input for valuation.

•Equity securities: The primary inputs to the valuation include quoted prices or quoted net asset values for identical or similar assets in markets that are not active.

•Short-term: The primary inputs to the valuation include quoted prices for identical or similar assets in markets that are not active, contractual cash flows, benchmark yields and credit spreads.

•Other investments: Free-standing exchange listed derivatives that are not actively traded are valued based on quoted prices for identical instruments in markets that are not active.

Over-the-counter (“OTC”) derivatives, including interest rate swaps, foreign currency swaps, total return swaps, foreign exchange forward contracts, certain options and certain credit default swaps, are valued using models that rely on inputs such as interest rate yield curves, implied volatilities, index price levels, currency rates, and credit spreads that are observable for substantially the full term of the contract. The valuation techniques underlying the models are widely accepted in the financial services industry and do not involve significant judgment.

Level 3 measurements

•Fixed income securities:

Municipal:Comprise municipal bonds that are not rated by third-party credit rating agencies. The primary inputs to the valuation of these municipal bonds include quoted prices for identical or similar assets that are not market observable, contractual cash flows, benchmark yields and credit spreads. Also included are municipal bonds valued based on non-binding broker quotes where the inputs have not been corroborated to be market observable

and municipal bonds in default valued based on the present value of expected cash flows.

Corporate - public and privately placed and ABS: Primarily valued based on non-binding broker quotes where the inputs have not been corroborated to be market observable. Other inputs for corporate fixed income securities include an interest rate yield curve, as well as published credit spreads for similar assets that incorporate the credit quality and industry sector of the issuer.

•Equity securities: The primary inputs to the valuation include quoted prices or quoted net asset values for identical or similar assets that are not market observable.

•Short-term: For certain short-term investments, amortized cost is used as the best estimate of fair value.

•Other investments: Certain options (including swaptions) are valued using models that are widely accepted in the financial services industry. These are categorized as Level 3 as a result of the significance of non-market observable inputs such as volatility. Other primary inputs include interest rate yield curves and quoted prices for identical or similar assets in markets that exhibit less liquidity relative to those markets supporting Level 2 fair value measurements.

•Other assets: Includes the contingent consideration provision in the sale agreement for Allstate Life Insurance Company (“ALIC”) which meets the definition of a derivative. This derivative is valued internally using a model that includes stochastically determined cash flows and inputs that include spot and forward interest rates, volatility, corporate credit spreads and a liquidity discount. This derivative is categorized as Level 3 due to the significance of non-market observable inputs.

Assets measured at fair value on a non-recurring basis

Comprise long-lived assets to be disposed of by sale, including real estate, that are written down to fair value less costs to sell and bank loans written down to fair value in connection with recognizing credit losses.

Investments excluded from the fair value hierarchy

Investments reported at net asset value (“NAV”)

Limited partnerships carried at fair value, which do not have readily determinable fair values, use NAV provided by the investees and are excluded from the fair value hierarchy. These investments are generally not redeemable by the investees and generally cannot be sold without approval of the general partner. The Company receives distributions of income and proceeds from the liquidation of the underlying assets of the investees, which usually takes place in years 4-9 of the typical contractual life of 10-12 years. As of June 30, 2024, the Company has commitments to invest $171 million in these limited partnership interests.

Second Quarter 2024 Form 10-Q 19

Notes to Condensed Consolidated Financial Statements

Assets and liabilities measured at fair value

June 30, 2024

($ in millions)

Quoted prices in active markets for identical assets (Level 1)

Significant other observable inputs (Level 2)

Significant unobservable inputs (Level 3)

Counterparty and cash collateral netting

Total

Assets

Fixed income securities:

U.S. government and agencies

$

10,551

$

13

$

—

$

10,564

Municipal

—

6,531

7

6,538

Corporate - public

—

23,470

30

23,500

Corporate - privately placed

—

8,964

50

9,014

Foreign government

—

1,289

—

1,289

ABS

—

1,600

71

1,671

Total fixed income securities

10,551

41,867

158

52,576

Equity securities (1)

1,451

222

393

2,066

Short-term investments

1,596

3,691

1

5,288

Other investments

—

7

2

$

(7)

2

Other assets

2

—

121

123

Total recurring basis assets

13,600

45,787

675

(7)

60,055

Non-recurring basis

—

—

11

11

Total assets at fair value

$

13,600

$

45,787

$

686

$

(7)

$

60,066

% of total assets at fair value

22.7

%

76.2

%

1.1

%

—

%

100.0

%

Investments reported at NAV

1,138

Total

$

61,204

Liabilities

Other liabilities

$

(3)

$

(2)

$

—

$

—

$

(5)

Total recurring basis liabilities

(3)

(2)

—

—

(5)

Total liabilities at fair value

$

(3)

$

(2)

$

—

$

—

$

(5)

% of total liabilities at fair value

60.0

%

40.0

%

—

%

—

%

100.0

%

(1)Excludes $150 million of preferred stock measured at cost.

20www.allstate.com

Notes to Condensed Consolidated Financial Statements

Assets and liabilities measured at fair value

December 31, 2023

($ in millions)

Quoted prices in active markets for identical assets (Level 1)

Significant other observable inputs (Level 2)

Significant unobservable inputs (Level 3)

Counterparty and cash collateral netting

Total

Assets

Fixed income securities:

U.S. government and agencies

$

8,606

$

13

$

—

$

8,619

Municipal

—

5,995

11

6,006

Corporate - public

—

23,272

26

23,298

Corporate - privately placed

—

7,849

58

7,907

Foreign government

—

1,290

—

1,290

ABS

—

1,687

58

1,745

Total fixed income securities

8,606

40,106

153

48,865

Equity securities (1)

1,656

203

402

2,261

Short-term investments

1,676

3,467

1

5,144

Other investments

—

3

2

$

(2)

3

Other assets

3

—

118

121

Total recurring basis assets

11,941

43,779

676

(2)

56,394

Non-recurring basis

—

—

15

15

Total assets at fair value

$

11,941

$

43,779

$

691

$