SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13A-16 OR 15D-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

For the month of February 2026

Commission File Number: 001-12102

YPF Sociedad Anónima

(Exact name of registrant as specified in its charter)

Macacha Güemes 515

C1106BKK Buenos Aires, Argentina

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F ☒ Form 40-F ☐

YPF Sociedad Anónima

TABLE OF CONTENT

| ITEM 1 | Translation of letter to the Argentine Securities Commission (Comisión Nacional de Valores) dated February 26, 2026. |

MAIN HIGHLIGHTS OF FY2025 & 4Q25

| KPI |

4Q25 | 3Q25 | Q/Q ∆ | 4Q24 | Y/Y∆ | 2025 | 2024 | ∆ | ||||||||||||||||||||||||||

| Financial |

Revenues | 4,556 | 4,643 | -2 | % | 4,751 | -4 | % | 18,448 | 19,293 | -4 | % | ||||||||||||||||||||||

| Adjusted EBITDA | 1,283 | 1,357 | -5 | % | 839 | 53 | % | 5,009 | 4,654 | 8 | % | |||||||||||||||||||||||

| Net Result | (649 | ) | (198 | ) | 228 | % | (284 | ) | 129 | % | (799 | ) | 2,393 | N/A | ||||||||||||||||||||

| CAPEX | 1,086 | 1,017 | 7 | % | 1,320 | -18 | % | 4,477 | 5,041 | -11 | % | |||||||||||||||||||||||

| FCF | 265 | (759 | ) | N/A | 64 | 314 | % | (1,816 | ) | (760 | ) | 139 | % | |||||||||||||||||||||

| Net Debt | 9,386 | 9,595 | -2 | % | 7,434 | 26 | % | 9,386 | 7,434 | 26 | % | |||||||||||||||||||||||

| Net Leverage Ratio (x) | 1.9 | 2.1 | -11 | % | 1.6 | 17 | % | 1.9 | 1.6 | 17 | % | |||||||||||||||||||||||

| Upstream |

Hydrocarbon Production (Kboe/d) | 488.0 | 523.1 | -7 | % | 520.6 | -6 | % | 527.0 | 536.1 | -2 | % | ||||||||||||||||||||||

| Crude Oil (Kbbl/d) |

264.4 | 239.8 | 10 | % | 269.8 | -2 | % | 255.4 | 257.5 | -1 | % | |||||||||||||||||||||||

| Natural Gas (Mm3/d) |

29.6 | 38.4 | -23 | % | 34.3 | -14 | % | 36.2 | 37.4 | -3 | % | |||||||||||||||||||||||

| NGL (Kbbl/d) |

37.7 | 41.9 | -10 | % | 35.2 | 7 | % | 43.7 | 43.1 | 1 | % | |||||||||||||||||||||||

| Crude Oil Price (US$/bbl) | 53.0 | 60.0 | -12 | % | 65.7 | -19 | % | 60.1 | 68.2 | -12 | % | |||||||||||||||||||||||

| Natural Gas Price (US$/MBTU) | 2.8 | 4.3 | -36 | % | 3.1 | -11 | % | 3.6 | 3.7 | -3 | % | |||||||||||||||||||||||

| Crude Oil Exports (Kbbl/d) | 39.3 | 38.3 | 2 | % | 40.8 | -4 | % | 39.4 | 34.9 | 13 | % | |||||||||||||||||||||||

| Shale Oil Production (Kbbl/d) | 196.0 | 170.0 | 15 | % | 138.1 | 42 | % | 164.8 | 122.4 | 35 | % | |||||||||||||||||||||||

| Total Lifting Cost (US$/boe) | 9.6 | 8.8 | 9 | % | 17.3 | -44 | % | 11.6 | 15.6 | -26 | % | |||||||||||||||||||||||

| Lifting cost shale oil hub (US$/boe) | 4.2 | 4.3 | -2 | % | 4.2 | -2 | % | 4.4 | 4.2 | 4 | % | |||||||||||||||||||||||

| Midstream & Dw |

Crude Processed (Kbbl/d) | 334.9 | 326.2 | 3 | % | 304.1 | 10 | % | 320.2 | 300.7 | 6 | % | ||||||||||||||||||||||

| Refineries’ Utilization Rate (%) |

99 | % | 97 | % | 3 | % | 90 | % | 10 | % | 95 | % | 89 | % | 6 | % | ||||||||||||||||||

| Local Fuels Volume Sold (Km3) | 3,774 | 3,655 | 3 | % | 3,577 | 5 | % | 14,366 | 13,947 | 3 | % | |||||||||||||||||||||||

| Local Fuels Net Price (US$/m3) | 638 | 608 | 5 | % | 685 | -7 | % | 645 | 701 | -8 | % | |||||||||||||||||||||||

| Imported Fuels (Km3) | 36 | 50 | -27 | % | 44 | -18 | % | 258 | 309 | -16 | % | |||||||||||||||||||||||

| R&M Adj. EBITDA (US$/bbl) | 18.6 | 6.1 | 207 | % | 11.5 | 62 | % | 12.9 | 13.9 | -7 | % | |||||||||||||||||||||||

In US$ million, unless noted otherwise. EBITDA = Operating income + Depreciation of PP&E + Depreciation of the right of use assets + Amortization of intangible assets + Unproductive exploratory drillings + (Reversal) / Deterioration of PP&E. Adjusted EBITDA = EBITDA that excludes IFRS 16 effects +/- one-off items. Net Leverage Ratio = Net Debt / LTM Adj. EBITDA. FCF = Cash flow from Operations less CAPEX (Investing activities), M&A (Investing activities), and interest and leasing payments (Financing activities). Fuels = diesel + gasoline. R&M is refining and marketing business, it excludes petrochemicals and agro products.

Adj. EBITDA totaled US$5.0 billion (+8% y/y), despite Brent contraction, mainly driven by higher shale oil production (+35% y/y), lower lifting costs (-26% y/y), as a combined strategy of exiting mature fields and expanding shale, in addition to record processing level at our refineries and strong crack spreads. In 4Q25, Adj. EBITDA recorded US$1.3 billion (-5% q/q), mostly reflecting lower seasonal gas sales, in addition to higher costs in real terms, partially offset by higher local fuel prices and record processing levels of refineries.

CAPEX reached US$4.5 billion in 2025 (-11% y/y), around 10% below our original estimates, mostly driven by further operational improvements and lower costs in dollar terms where 72% was allocated to unconventional. 4Q25 capex followed this trend, reaching US$1.1 billion (+7% q/q and 73% unconventional).

Shale oil production averaged 165 kbbl/d in 2025 (+35% y/y, in line with target), fully offsetting conventional divestment. Moreover, in 4Q25 we reached 196 kbbl/d (+42% y/y and +15% q/q). In Dec-25 we signed a long-term shale oil export contract with ENAP for approximately 32 kbbl/d until Jun-33.

Vaca Muerta shale P1 reserves strongly grew to 1,128 MBOE in 2025 (+32% y/y and 88% of total P1 reserves) with a solid reserve replacement ratio of 3.2x and average life of 9.0 years: 54% oil, 40% gas and 6% NGL.

Processing levels at our refineries reached record-high of 335 kbbl/d in 4Q25, 99% of utilization rate, generating surplus of gasoline and diesel to substitute imports of other local players or export markets.

M&A activity: in Dec-25 we sold 50% of Profertil stake at US$635 million (2/3 collected as of Jan-26). Also, we acquired 4.9% of Bandurria Sur and 15% of Bajo del Toro blocks at US$163 million, subject to closing.

Progress on our main projects:

| • | Andes Phase I: 45 blocks out of the 48 involved have been completed. |

| • | Andes Phase II: 3 blocks out of 16 involved completed so far, highlighting the sale of Manantiales Behr block for US$410 million and earn-out of US$40 million signed in Feb26, subject to closing. |

| • | Argentina LNG: in Feb-26 YPF, ENI and XRG (ADNOC’s international energy investment arm) signed a binding Joint Development Agreement for a 12 MTPA project of 2 own FLNGs, enabling the beginning of FEED and related activities. Moreover, in Jan-26, YPF swapped assets with Pluspetrol to fully own 3 key wet gas blocks for the project (Meseta Buena Esperanza, Aguada Villanueva and Las Tacanas) in exchange of 20% of La Escalonada and Rincón La Ceniza blocks. |

On the financial front, in January 2026 we re-tapped 2034 international bond for US$550 million, at a yield of 8.1%, the lowest rate secured by the Company in the international capital markets in the last 9 years.

Page 2/15

Buenos Aires, 02/26/2026 – YPF (BYMA: YPFD | NYSE: YPF1). Information based on financial statements (FS) prepared according to IFRS in force in Argentina. The sum of the parts of certain figures is subject to rounding. The Company’s functional currency is US$.

1. ANALYSIS OF CONSOLIDATED RESULTS OF FY2025 & 4Q25

| Consolidated Revenues Breakdown Unaudited Figures, in US$ million |

4Q25 | 3Q25 | 4Q24 | Q/Q ∆ | Y/Y ∆ | 2025 | 2024 | Y/Y ∆ | ||||||||||||||||||||||||

| Diesel |

1,525 | 1,467 | 1,581 | 4.0 | % | -3.5 | % | 6,039 | 6,454 | -6.4 | % | |||||||||||||||||||||

| Gasoline |

1,055 | 929 | 1,022 | 13.5 | % | 3.1 | % | 3,944 | 4,013 | -1.7 | % | |||||||||||||||||||||

| Natural gas as producers (third parties) |

249 | 523 | 258 | -52.3 | % | -3.4 | % | 1,525 | 1,469 | 3.8 | % | |||||||||||||||||||||

| Other |

1,072 | 1,067 | 1,117 | 0.5 | % | -4.0 | % | 4,153 | 4,435 | -6.4 | % | |||||||||||||||||||||

| Total Domestic Market |

3,902 | 3,986 | 3,979 | -2.1 | % | -1.9 | % | 15,662 | 16,371 | -4.3 | % | |||||||||||||||||||||

| Jet fuel |

108 | 87 | 105 | 24.2 | % | 3.4 | % | 362 | 503 | -28.1 | % | |||||||||||||||||||||

| Grain and flours |

80 | 139 | 131 | -42.1 | % | -38.7 | % | 524 | 387 | 35.6 | % | |||||||||||||||||||||

| Crude oil |

216 | 238 | 262 | -9.1 | % | -17.5 | % | 948 | 962 | -1.5 | % | |||||||||||||||||||||

| Petchem & Other |

250 | 193 | 274 | 29.3 | % | -9.0 | % | 952 | 1,070 | -11.0 | % | |||||||||||||||||||||

| Total Export Market |

654 | 657 | 772 | -0.4 | % | -15.3 | % | 2,786 | 2,922 | -4.6 | % | |||||||||||||||||||||

| Total Revenues |

4,556 | 4,643 | 4,751 | -1.9 | % | -4.1 | % | 18,448 | 19,293 | -4.4 | % | |||||||||||||||||||||

Net Revenues totaled US$18.4 billion in 2025 (-4% y/y), mainly driven by a decline in Brent price of 15%, which adversely affected the pricing of fuels, crude oil, petrochemicals and other refined products, partially offset by record high processing levels that enabled higher local fuels dispatched coupled with increased sales of non-oil agro products.

In 4Q25, net revenues declined by 2% q/q, primarily driven by reduced seasonal natural gas sales and a drop in oil prices. However, these factors were partially offset by an improvement in local fuel prices—which regained alignment with import parity references—as well as increased dispatch volumes of gasoline, diesel, jet fuel, and petrochemicals in the domestic market, alongside higher oil exports.

| Unaudited Figures, in US$ million |

4Q25 | 3Q25 | 4Q24 | Q/Q ∆ | Y/Y ∆ | 2025 | 2024 | Y/Y ∆ | ||||||||||||||||||||||||

| Lifting cost |

(433 | ) | (426 | ) | (828 | ) | 1.7 | % | -47.7 | % | (2,228 | ) | (3,066 | ) | -27.3 | % | ||||||||||||||||

| Other Upstream |

(164 | ) | (184 | ) | (200 | ) | -10.7 | % | -18.0 | % | (653 | ) | (673 | ) | -2.9 | % | ||||||||||||||||

| OPEX Downstream |

(553 | ) | (518 | ) | (558 | ) | 6.9 | % | -0.8 | % | (2,128 | ) | (2,104 | ) | 1.2 | % | ||||||||||||||||

| Others Midstream & Downstream |

(143 | ) | (82 | ) | (146 | ) | 73.8 | % | -1.7 | % | (357 | ) | (338 | ) | 5.6 | % | ||||||||||||||||

| LNG & IG, New Energies, Corp. & Other |

(236 | ) | (146 | ) | (305 | ) | 61.7 | % | -22.4 | % | (793 | ) | (1,039 | ) | -23.7 | % | ||||||||||||||||

| Total OPEX |

(1,530 | ) | (1,356 | ) | (2,036 | ) | 12.8 | % | -24.9 | % | (6,159 | ) | (7,220 | ) | -14.7 | % | ||||||||||||||||

| Depreciation & Amortization |

(774 | ) | (836 | ) | (795 | ) | -7.4 | % | -2.6 | % | (3,204 | ) | (2,759 | ) | 16.1 | % | ||||||||||||||||

| Royalties |

(207 | ) | (238 | ) | (261 | ) | -13.1 | % | -20.6 | % | (953 | ) | (1,095 | ) | -12.9 | % | ||||||||||||||||

| Other costs |

(309 | ) | (284 | ) | (392 | ) | 8.9 | % | -21.3 | % | (1,224 | ) | (1,385 | ) | -11.7 | % | ||||||||||||||||

| Total Other Costs |

(1,290 | ) | (1,358 | ) | (1,448 | ) | -5.0 | % | -10.9 | % | (5,381 | ) | (5,239 | ) | 2.7 | % | ||||||||||||||||

| Fuels imports (including jet fuel) |

(25 | ) | (35 | ) | (28 | ) | -29.7 | % | -10.1 | % | (172 | ) | (225 | ) | -23.4 | % | ||||||||||||||||

| Crude oil purchases to third parties |

(545 | ) | (688 | ) | (440 | ) | -20.8 | % | 23.9 | % | (2,161 | ) | (1,755 | ) | 23.1 | % | ||||||||||||||||

| Biofuel purchases |

(231 | ) | (208 | ) | (212 | ) | 11.3 | % | 9.2 | % | (909 | ) | (910 | ) | -0.1 | % | ||||||||||||||||

| Agro products purchases |

(156 | ) | (226 | ) | (133 | ) | -31.0 | % | 16.9 | % | (723 | ) | (602 | ) | 20.2 | % | ||||||||||||||||

| Other purchases |

(177 | ) | (221 | ) | (206 | ) | -19.9 | % | -14.1 | % | (783 | ) | (1,038 | ) | -24.6 | % | ||||||||||||||||

| Stock variations |

(85 | ) | 54 | (157 | ) | N/A | -45.9 | % | (94 | ) | (127 | ) | -26.0 | % | ||||||||||||||||||

| Total Purchases & Stock Variations |

(1,219 | ) | (1,324 | ) | (1,176 | ) | -7.9 | % | 3.7 | % | (4,842 | ) | (4,657 | ) | 4.0 | % | ||||||||||||||||

| Other operating results, net |

67 | (48 | ) | (559 | ) | N/A | N/A | (330 | ) | (609 | ) | -45.8 | % | |||||||||||||||||||

| Reversal / (Impairment) of PP&E |

— | (5 | ) | (61 | ) | N/A | N/A | 4 | (87 | ) | N/A | |||||||||||||||||||||

| Operating Costs + Purchases + Impairment of Assets |

(3,972 | ) | (4,091 | ) | (5,280 | ) | -2.9 | % | -24.8 | % | (16,708 | ) | (17,812 | ) | -6.2 | % | ||||||||||||||||

Stock variations include price effects by (US$ 77) million in 4Q25, (US$4) million for 3Q25, (US$47) million for 4Q24, (US$173) million for 2025 and (US$111) million for 2024

OPEX totaled US$6.2 billion in 2025 (-15% y/y), primarily due to a substantial reduction in lifting costs driven by the divestment from mature fields and lower charge for doubtful gas sales receivables. In 4Q25, OPEX increased 13% q/q, mainly explained by Downstream’s extraordinary environmental provision and higher transportation costs, partially offset by saving associates to the reduced exposure to mature fields.

Other Costs reached US$5.4 billion in 2025 (+3% y/y), mainly driven by higher depreciation and amortization from increased shale activity, partially offset by decreased royalties (lower oil and gas prices) and reduced unproductive exploration drillings. In 4Q25, Other Costs dropped 5%, mostly due to lower depreciation and amortization from reassessment of well abandonment, and diminished royalties (seasonal decline in gas prices and lower oil prices), partially offset by higher one-off mature fields costs.

Purchases & Stock Variations recorded US$4.8 billion in 2025 (+4% y/y), mainly driven by higher crude oil purchases to third parties (reduced exposure to mature fields and higher processing levels) and increased agro product purchases, boosted by export duty cuts, higher grain output, and fertilizer restocking. These effects were partially counterbalanced by lower crude oil and fuel import prices, in line with the downward trend in international prices, and lower jet fuel purchases, following the shutdown of YPF Chile’s aviation business.

| 1 | 1 ADR = 1 share. Total issued capital stock amounted to 393,312,793 shares as of Dec-2025 (51% Argentina Government; 25% NYSE and 24% ByMA). |

Page 3/15

In 4Q25 Purchases & Stock Variations dropped 8% q/q, mostly due to lower oil unit costs and ramp-up in shale production, as well as lower seasonality in agricultural products. These effects were partially offset by stock variations, totaling (-US$85) million in 4Q25 vs. US$54 million in 3Q25, mainly explained by lower international reference prices, reducing inventory value, combined with stock consumption of agricultural products.

Other operating net results totaled (-US$330 million) in 2025 (vs. -US$609 million in 2024), mainly explained by the positive result from the divestment of 50% stake in Profertil, partially offset by the negative result from the sale of Manantiales Beher field and mature fields exit costs. In 4Q25, other operating net results reached a gain of US$67 million (vs. a loss of US$48 million in 3Q25), also mostly driven by the divestment of Profertil, partially offset by mature field costs.

| Consolidated Net Income Breakdown Unaudited Figures, in US$ million |

4Q25 | 3Q25 | 4Q24 | Q/Q ∆ | Y/Y ∆ | 2025 | 2024 | Y/Y ∆ | ||||||||||||||||||||||||

| Operating income / (loss) |

584 | 552 | (530 | ) | 5.8 | % | N/A | 1,740 | 1,480 | 17.6 | % | |||||||||||||||||||||

| Result from equity interests in associates and joint ventures |

15 | 32 | 133 | -53.1 | % | -88.7 | % | 122 | 396 | -69.2 | % | |||||||||||||||||||||

| Financial results, net |

(206 | ) | (245 | ) | (103 | ) | -15.9 | % | 100.1 | % | (952 | ) | (856 | ) | 11.3 | % | ||||||||||||||||

| Net result before tax |

393 | 339 | (500 | ) | 15.9 | % | N/A | 910 | 1,020 | -10.8 | % | |||||||||||||||||||||

| Income tax |

(1,042 | ) | (537 | ) | 216 | 94.0 | % | N/A | (1,709 | ) | 1,373 | N/A | ||||||||||||||||||||

| Net result |

(649 | ) | (198 | ) | (284 | ) | 228.0 | % | 128.5 | % | (799 | ) | 2,393 | N/A | ||||||||||||||||||

| Net Income before impairment of assets |

(649 | ) | (195 | ) | (244 | ) | 233.5 | % | 165.6 | % | (802 | ) | 2,450 | N/A | ||||||||||||||||||

Financial net results recorded (-US$952) million in 2025 (vs.-US$856 million in 2024), mainly explained by a contraction in the mark-to-market valuation of sovereign bonds included in YPF’s liquidity against last year, partially offset by lower abandonment provision following the mature field divestments. In 4Q25, financial net results showed a sequential improvement, recording a loss of US$206 million, mainly due to the recovery in sovereign bond prices.

The income tax recorded (-US$1.7) billion in 2025, mainly driven by YPF’s adherence to the Tax Normalization Plan established by ARCA Resolution No. 5.684/2025. Under this regime, the company entered roughly a US$1 billion payment plan structured in 120 monthly peso-denominated installments to settle obligations derived from revalued income tax loss carryforwards. In this sense, the company solved a considerable fiscal contingency. In 4Q25, income tax posted (-US$1.0) billion, reflecting the impact of this adherence and a decrease in the company’s tax assets value, increasing future tax payable.

Consequently, net result totaled a loss of US$799 million in 2025, compared to a gain of US$2,393 million in 2024. In 4Q25, net result was a loss of US$649 million, compared to a loss of US$198 million in 3Q25.

2. ADJ. EBITDA & CAPEX

2.1 ADJ. EBITDA RECONCILIATION

| Reconciliation of Adjusted EBITDA Unaudited Figures, in US$ million |

4Q25 | 3Q25 | 4Q24 | Q/Q ∆ | Y/Y ∆ | 2025 | 2024 | Y/Y ∆ | ||||||||||||||||||||||||

| Net result |

(649 | ) | (198 | ) | (284 | ) | 228.0 | % | 128.5 | % | (799 | ) | 2,393 | N/A | ||||||||||||||||||

| Financial results, net |

206 | 245 | 103 | -15.9 | % | 100.1 | % | 952 | 856 | 11.3 | % | |||||||||||||||||||||

| Result from equity interests in associates and joint ventures |

(15 | ) | (32 | ) | (133 | ) | -53.1 | % | -88.7 | % | (122 | ) | (396 | ) | -69.2 | % | ||||||||||||||||

| Income tax |

1,042 | 537 | (216 | ) | 94.0 | % | N/A | 1,709 | (1,373 | ) | N/A | |||||||||||||||||||||

| Unproductive exploratory drillings |

31 | — | 77 | N/A | -59.7 | % | 32 | 133 | -75.9 | % | ||||||||||||||||||||||

| Depreciation & amortization |

774 | 836 | 795 | -7.4 | % | -2.6 | % | 3,204 | 2,759 | 16.1 | % | |||||||||||||||||||||

| Reversal / (Impairment) of PP&E |

— | 5 | 61 | N/A | N/A | (4 | ) | 87 | N/A | |||||||||||||||||||||||

| EBITDA |

1,389 | 1,393 | 403 | -0.3 | % | 244.7 | % | 4,972 | 4,459 | 11.5 | % | |||||||||||||||||||||

| Leasing |

(86 | ) | (88 | ) | (85 | ) | -2.5 | % | 1.8 | % | (341 | ) | (326 | ) | 4.7 | % | ||||||||||||||||

| Provision for operating optimizations |

(3 | ) | 60 | 266 | N/A | N/A | 87 | 266 | -67.3 | % | ||||||||||||||||||||||

| Result from sale of assets |

(3 | ) | (34 | ) | (6 | ) | -91.2 | % | -49.5 | % | (219 | ) | (6 | ) | 3585.5 | % | ||||||||||||||||

| Result from changes in fair value of assets held for sale |

178 | (4 | ) | 260 | -4550.0 | % | -31.7 | % | 418 | 260 | 60.5 | % | ||||||||||||||||||||

| Provision for severance indemnities |

17 | 2 | — | N/A | N/A | 45 | — | N/A | ||||||||||||||||||||||||

| Provision for obsolescence of materials and equipment |

7 | (19 | ) | — | N/A | N/A | 247 | — | N/A | |||||||||||||||||||||||

| Result from revaluation of companies |

— | — | — | N/A | N/A | (45 | ) | — | N/A | |||||||||||||||||||||||

| Result from sale of companies |

(335 | ) | — | — | N/A | N/A | (335 | ) | — | N/A | ||||||||||||||||||||||

| Miscellaneous – Mature Fields & Others |

119 | 48 | — | 149.9 | % | N/A | 180 | — | N/A | |||||||||||||||||||||||

| Adjusted EBITDA |

1,283 | 1,357 | 839 | -5.5 | % | 53.0 | % | 5,009 | 4,654 | 7.6 | % | |||||||||||||||||||||

Page 4/15

2.2 ADJ. EBITDA & CAPEX BY SEGMENT

| By Segment |

4Q25 | 3Q25 | Q/Q ∆ | 4Q24 | Y/Y ∆ | 2025 | 2024 | ∆ | ||||||||||||||||||||||||||

| Adj. EBITDA |

Upstream | 725 | 1,042 | -30 | % | 597 | 21 | % | 3,304 | 3,028 | 9 | % | ||||||||||||||||||||||

| Midstream & Downstream | 694 | 359 | 93 | % | 377 | 84 | % | 2,015 | 1,837 | 10 | % | |||||||||||||||||||||||

| LNG & IG | 2 | (4 | ) | N/A | (3 | ) | N/A | (7 | ) | (47 | ) | -85 | % | |||||||||||||||||||||

| New Energies | 23 | 52 | -56 | % | 34 | -32 | % | 139 | 156 | -11 | % | |||||||||||||||||||||||

| Corp | (81 | ) | (62 | ) | 31 | % | (119 | ) | -32 | % | (240 | ) | (243 | ) | -1 | % | ||||||||||||||||||

| Eliminations & Others | (80 | ) | (30 | ) | 164 | % | (48 | ) | 67 | % | (202 | ) | (76 | ) | 165 | % | ||||||||||||||||||

| Total Adj. EBITDA | 1,283 | 1,357 | -5 | % | 839 | 53 | % | 5,009 | 4,654 | 8 | % | |||||||||||||||||||||||

| CAPEX |

Upstream | 774 | 751 | 3 | % | 883 | -12 | % | 3,368 | 3,664 | -8 | % | ||||||||||||||||||||||

| Midstream & Downstream | 256 | 218 | 17 | % | 350 | -27 | % | 924 | 1,187 | -22 | % | |||||||||||||||||||||||

| LNG & IG | 16 | 9 | 78 | % | 18 | -10 | % | 42 | 26 | 62 | % | |||||||||||||||||||||||

| New Energies | 12 | 7 | 60 | % | 15 | -20 | % | 38 | 40 | -5 | % | |||||||||||||||||||||||

| Corp | 28 | 31 | -9 | % | 54 | -47 | % | 105 | 124 | -15 | % | |||||||||||||||||||||||

| Total CAPEX | 1,086 | 1,017 | 7 | % | 1,320 | -18 | % | 4,477 | 5,041 | -11 | % | |||||||||||||||||||||||

| Note: | Midstream & Dw Adjusted EBITDA excludes inventories price effect of oil products, which are included in Eliminations & Other. |

3. ANALYSIS OF RESULTS BY SEGMENT

3.1 UPSTREAM

| Upstream Financials Unaudited Figures, in US$ million |

4Q25 | 3Q25 | 4Q24 | Q/Q ∆ | Y/Y ∆ | 2025 | 2024 | Y/Y ∆ | ||||||||||||||||||||||||

| Crude oil |

1,302 | 1,323 | 1,591 | -1.6 | % | -18.2 | % | 5,595 | 6,317 | -11.4 | % | |||||||||||||||||||||

| Natural gas |

317 | 611 | 345 | -48.1 | % | -8.1 | % | 1,863 | 1,825 | 2.1 | % | |||||||||||||||||||||

| Other |

27 | 33 | 33 | -15.8 | % | -17.2 | % | 117 | 133 | -12.0 | % | |||||||||||||||||||||

| Revenues |

1,646 | 1,967 | 1,969 | -16.3 | % | -16.4 | % | 7,575 | 8,275 | -8.5 | % | |||||||||||||||||||||

| Depreciation & amortization |

(544 | ) | (615 | ) | (566 | ) | -11.5 | % | -3.9 | % | (2,349 | ) | (1,963 | ) | 19.7 | % | ||||||||||||||||

| Lifting cost |

(433 | ) | (426 | ) | (828 | ) | 1.7 | % | -47.7 | % | (2,228 | ) | (3,066 | ) | -27.3 | % | ||||||||||||||||

| Royalties |

(206 | ) | (237 | ) | (258 | ) | -13.3 | % | -20.2 | % | (946 | ) | (1,083 | ) | -12.7 | % | ||||||||||||||||

| Other costs |

(526 | ) | (274 | ) | (839 | ) | 91.7 | % | -37.4 | % | (1,642 | ) | (1,570 | ) | 4.6 | % | ||||||||||||||||

| Operating income before impairment of assets |

(62 | ) | 415 | (522 | ) | N/A | -88.1 | % | 410 | 594 | -31.0 | % | ||||||||||||||||||||

| Reversal / (Impairment) of PP&E |

— | — | (58 | ) | N/A | N/A | — | (79 | ) | N/A | ||||||||||||||||||||||

| Operating income / (loss) |

(62 | ) | 415 | (580 | ) | N/A | -89.3 | % | 410 | 515 | -20.4 | % | ||||||||||||||||||||

| Depreciation & amortization |

544 | 615 | 566 | -11.5 | % | -3.9 | % | 2,349 | 1,963 | 19.7 | % | |||||||||||||||||||||

| Unproductive exploratory drillings |

31 | — | 77 | N/A | -59.7 | % | 32 | 133 | -75.9 | % | ||||||||||||||||||||||

| Reversal / (Impairment) of PP&E |

— | — | 58 | N/A | N/A | — | 79 | N/A | ||||||||||||||||||||||||

| EBITDA |

513 | 1,030 | 121 | -50.2 | % | 324.2 | % | 2,791 | 2,690 | 3.8 | % | |||||||||||||||||||||

| Leasing |

(42 | ) | (42 | ) | (44 | ) | 0.0 | % | -6.3 | % | (183 | ) | (183 | ) | 0.2 | % | ||||||||||||||||

| Provision for operating optimizations |

(3 | ) | 60 | 266 | N/A | N/A | 87 | 266 | -67.3 | % | ||||||||||||||||||||||

| Result from sale of assets |

(3 | ) | (34 | ) | (6 | ) | -91.2 | % | -49.5 | % | (219 | ) | (6 | ) | 3585.5 | % | ||||||||||||||||

| Result from changes in fair value of assets held for sale |

178 | (4 | ) | 260 | N/A | -31.7 | % | 418 | 260 | 60.5 | % | |||||||||||||||||||||

| Provision for severance indemnities |

17 | 2 | — | 750.0 | % | N/A | 45 | — | N/A | |||||||||||||||||||||||

| Provision for obsolescence of materials and equipment |

7 | (19 | ) | — | N/A | N/A | 247 | — | N/A | |||||||||||||||||||||||

| Miscellaneous – Mature Fields |

57 | 48 | — | 19.2 | % | N/A | 118 | — | N/A | |||||||||||||||||||||||

| Adjusted EBITDA |

725 | 1042 | 597 | -30.4 | % | 21.4 | % | 3,304 | 3,028 | 9.1 | % | |||||||||||||||||||||

| CAPEX |

774 | 751 | 883 | 3.0 | % | -12.4 | % | 3,368 | 3,664 | -8.1 | % | |||||||||||||||||||||

| Unit Cash Costs Unaudited Figures, in US$/boe |

4Q25 | 3Q25 | 4Q24 | Q/Q ∆ | Y/Y ∆ | 2025 | 2024 | Y/Y ∆ | ||||||||||||||||||||||||

| Lifting Cost |

9.6 | 8.8 | 17.3 | 9.0 | % | -44.2 | % | 11.6 | 15.6 | -25.9 | % | |||||||||||||||||||||

| Royalties and other taxes |

5.8 | 6.0 | 6.7 | -2.3 | % | -13.1 | % | 6.1 | 6.9 | -10.6 | % | |||||||||||||||||||||

| Other Costs |

3.9 | 4.0 | 4.3 | -2.9 | % | -10.9 | % | 3.7 | 3.6 | 2.0 | % | |||||||||||||||||||||

| Total Cash Costs (US$/boe) |

19.3 | 18.8 | 28.3 | 2.9 | % | -31.6 | % | 21.4 | 26.1 | -18.0 | % | |||||||||||||||||||||

Revenues totaled US$7.6 billion in 2025 (-8% y/y), mostly on the back of 12% reduction in oil prices, while total production declined 1.7% as the divestment of conventional fields was almost fully offset by shale expansion. To a minor extent, gas sales volume grew by 5% (which includes certain NGL production), with 3% lower price. In 4Q25 revenues dropped by 16% q/q, mainly due to off-peak seasonal gas sales, whereas lower oil prices were neutralized by shale expansion.

Lifting cost reached US$11.6/BOE in 2025 (-26% y/y), primarily driven by exit from mature fields, coupled with shale oil expansion: unconventional lifting cost averaged US$4.6/BOE (-13% y/y) and conventional lifting cost totaled US$26.0/BOE (-8% y/y). In 4Q25 lifting cost was US$9.6/BOE (+9% q/q), mainly related to additional services in unconventional blocks, beyond core-hub: unconventional was US$4.8/BOE and conventional was US$23.1/BOE.

Page 5/15

Zooming into the lifting cost in our shale oil hub2 (at 100% stake), it remained broadly stable at a very competitive level of US$4.4/BOE in 2025 and US$4.2/BOE in 4Q25, underscoring our strong operational efficiency and strong productivity achieved across our Vaca Muerta shale oil activities.

Royalties and other taxes averaged US$6.1/BOE (-11% y/y) in 2025, primarily due to oil price contraction. In 4Q25, these costs stood at US$5.8/BOE (-2% q/q), mainly driven by lower seasonal gas prices and, to a lesser extent, lower oil prices.

Other costs amounted to US$1.6 billion in 2025 (+5% y/y), mostly due to higher one-off costs related to mature fields, partially offset by lower costs from unproductive exploratory drillings. In 4Q25, other costs recorded US$526 million (vs. US$274 million in 3Q25), impacted by higher one-off costs related to mature fields and unproductive exploratory drillings.

Adj. EBITDA totaled US$3.3 billion (+9% y/y) in 2025, mainly supported by a substantial saving in lifting costs (exiting mature fields and expanding shale), partially offset by contraction in oil prices. In 4Q25, Adj. EBITDA was US$725 million (-30% q/q), primarily reflecting lower seasonal gas sales, while the decline in oil prices was fully compensated by shale ramp-up.

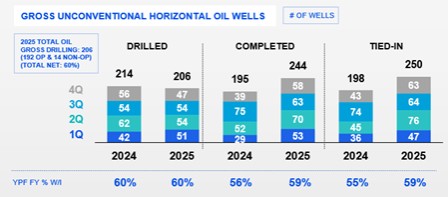

CAPEX amounted to US$3.4 billion in 2025, 8% lower than the US$3.7 billion in 2024, explained by divestment of conventional assets. It is worth noting that in the breakdown of the capex, US$3.2 billion was allocated to unconventional assets in both years, but in 2025, shale oil wells completed increased by 25% on a gross basis, showing higher efficiency and productivity in our unconventional operations. In 4Q25, capex stood at US$774 million, slightly higher than 3Q25.

Unconventional horizontal oil wells recorded solid metrics, particularly in completion and tied-in activity:

In terms of efficiencies within our unconventional operations, during 4Q25 we continued beating our own records in drilling and fracking performance. In this sense, we averaged 341 meters per day of drilling in our shale oil hub blocks (+2% q/q), and 287 stages per set per month on unconventional fracking (+3% q/q).

| 2 | 5 shale oil blocks operated by YPF: La Angostura Sur I and II (YPF owns 100%), Loma Campana (50%), La Amarga Chica (50%), Bandurria Sur (40%, in process of acquiring additional 4.9% of Equinor) and Aguada del Chañar (51%). La Angostura Sur is south-hub block and the rest core-hub blocks. |

Page 6/15

| Upstream Operating data Unaudited Figures |

4Q25 | 3Q25 | 4Q24 | Q/Q ∆ | Y/Y ∆ | 2025 | 2024 | Y/Y ∆ | ||||||||||||||||||||||||

| Net Production Breakdown |

||||||||||||||||||||||||||||||||

| Crude Production (Kbbld) |

264.4 | 239.8 | 269.8 | 10.2 | % | -2.0 | % | 255.4 | 257.5 | -0.8 | % | |||||||||||||||||||||

| Conventional |

67.6 | 69.0 | 129.6 | -1.9 | % | -47.8 | % | 89.7 | 132.8 | -32.5 | % | |||||||||||||||||||||

| Shale |

196.0 | 170.0 | 138.1 | 15.3 | % | 41.9 | % | 164.8 | 122.4 | 34.6 | % | |||||||||||||||||||||

| Tight |

0.7 | 0.9 | 2.1 | -17.4 | % | -65.2 | % | 1.0 | 2.3 | -57.3 | % | |||||||||||||||||||||

| NGL Production (Kbbld) |

37.7 | 41.9 | 35.2 | -9.9 | % | 7.2 | % | 43.7 | 43.1 | 1.4 | % | |||||||||||||||||||||

| Conventional |

6.9 | 11.3 | 9.0 | -38.3 | % | -22.9 | % | 10.9 | 10.5 | 3.3 | % | |||||||||||||||||||||

| Shale |

30.6 | 30.4 | 25.4 | 0.6 | % | 20.2 | % | 32.5 | 31.6 | 2.7 | % | |||||||||||||||||||||

| Tight |

0.2 | 0.3 | 0.8 | -17.1 | % | -71.4 | % | 0.4 | 1.0 | -61.3 | % | |||||||||||||||||||||

| Gas Production (Mm3d) |

29.6 | 38.4 | 34.3 | -23.0 | % | -13.8 | % | 36.2 | 37.4 | -3.2 | % | |||||||||||||||||||||

| Conventional |

7.3 | 8.7 | 11.2 | -16.6 | % | -35.0 | % | 9.6 | 12.3 | -21.9 | % | |||||||||||||||||||||

| Shale |

19.5 | 26.3 | 19.3 | -25.9 | % | 1.1 | % | 23.3 | 20.4 | 13.7 | % | |||||||||||||||||||||

| Tight |

2.8 | 3.4 | 3.8 | -17.0 | % | -26.5 | % | 3.4 | 4.7 | -28.3 | % | |||||||||||||||||||||

| Total Production (Kboed) |

488.0 | 523.1 | 520.6 | -6.7 | % | -6.2 | % | 527.0 | 536.1 | -1.7 | % | |||||||||||||||||||||

| Conventional |

120.4 | 135.2 | 209.1 | -10.9 | % | -42.4 | % | 161.1 | 220.8 | -27.0 | % | |||||||||||||||||||||

| Shale |

349.2 | 365.6 | 284.8 | -4.5 | % | 22.6 | % | 343.5 | 282.6 | 21.6 | % | |||||||||||||||||||||

| Tight |

18.4 | 22.2 | 26.7 | -17.1 | % | -30.8 | % | 22.5 | 32.7 | -31.4 | % | |||||||||||||||||||||

| Average realization prices |

||||||||||||||||||||||||||||||||

| Crude Oil (USD/bbl) |

53.0 | 60.0 | 65.7 | -11.6 | % | -19.2 | % | 60.1 | 68.2 | -11.9 | % | |||||||||||||||||||||

| Natural Gas (USD/MMBTU) |

2.8 | 4.3 | 3.1 | -35.7 | % | -10.9 | % | 3.6 | 3.7 | -2.9 | % | |||||||||||||||||||||

Focusing on shale oil production, in 4Q25 we produced 196 kbbl/d, increasing by 42% y/y. It is worth highlighting that La Angostura Sur grew by nearly 8 times y/y, producing 41 kbbl/d in 4Q25, and our core-hub blocks expanded by 13% y/y. As a result, the Company comfortably reached its 2025 shale oil production target of 165 kbbl/d. Moreover, in Dec25, we produced 204 kbbl/d, exceeding by far the exit rate target of 190 thousand barrels per day set at the beginning of the year.

Crude oil production in 2025 averaged 255 kbbl/d (-1% y/y), as the divestment of conventional mature fields was fully counterbalanced by a strong shale oil ramp-up.

Natural gas production contracted by -3% y/y in 2025, mainly driven by lower output from mature fields, while in 4Q25, it declined by 23% q/q, primarily due to the off-peak seasonal demand.

NGLs production slightly grew +1% y/y in 2025 to 43.7 kbbl/d. In 4Q25 it dropped by 10% q/q, mostly on the back of lower seasonal associated natural gas production.

P1 RESERVES

| 2025 |

Crude oil and condensate (millions of barrels) |

Natural gas liquids (millions of barrels) |

Natural gas (billion of cubic feet) |

Total (millions of barrels of oil equivalent) |

||||||||||||

| Proved developed and undeveloped reserves: |

||||||||||||||||

| Beginning of year |

548 | 69 | 2,688 | 1,096 | ||||||||||||

| Revisions of previous estimates |

(38 | ) | 6 | (148 | ) | (58 | ) | |||||||||

| Extensions, discoveries and improved recovery |

291 | 16 | 899 | 467 | ||||||||||||

| Purchases and sales |

(30 | ) | (1 | ) | 14 | (29 | ) | |||||||||

| Production for the year |

(93 | ) | (16 | ) | (467 | ) | (192 | ) | ||||||||

| End of year |

678 | 74 | 2,986 | 1,284 | ||||||||||||

| Proved developed reserves: |

||||||||||||||||

| Beginning of year |

284 | 44 | 1,627 | 618 | ||||||||||||

| End of year |

315 | 42 | 1,597 | 642 | ||||||||||||

| Proved undeveloped reserves: |

||||||||||||||||

| Beginning of year |

264 | 25 | 1,061 | 478 | ||||||||||||

| End of year |

363 | 32 | 1,389 | 642 | ||||||||||||

| 1 | barrel of oil equivalent = 5,615 cubic feet of gas = 1 barrel of oil, condensate or natural gas liquids |

Proved reserves (P1) closed in 2025 at 1,284 Mboe (+17% y/y), mainly driven by a solid growth of 32% in shale reserves, partially offset by a decline in conventional fields.

The addition of proved (developed and undeveloped) hydrocarbon reserves amounted to 380 million barrels of oil equivalent (from table in Mboe: 467 – 58 – 29) on the back of the progressive developments of our unconventional operations. This result was achieved through the incorporation of 244 million barrels of liquids and 136 MBOE corresponding to gas reserves. It is worth mentioning the additions from Neuquina Basin: La

Page 7/15

Angostura Sur I, La Angostura Sur II, Bandurria Sur and La Amarga Chica blocks for crude oil and La Calera block for natural gas.

Considering that reserves incorporated in 2025 exceeded the total production in the year (192 MBOE), the reserve replacement ratio (“RRR”) reached 2.0x with 6.7 years of reserve life.

Excluding the conventional fields under the divestment program Andes Phase 1 and 2, RRR would have improved to 2.7x, reserves life to 8.0 years and total P1 reserves growing by 26% y/y.

Focusing on shale reserves, it scaled up to 88% of the total P1 reserves, averaging 9.0 years of reserve life, RRR of 3.2x and growing by 32% y/y.

3.2 MIDSTREAM & DOWNSTREAM

| Midstream & Downstream Financials Unaudited Figures, in US$ million |

4Q25 | 3Q25 | 4Q24 | Q/Q ∆ | Y/Y ∆ | 2025 | 2024 | Y/Y ∆ | ||||||||||||||||||||||||

| Diesel (third parties) |

1,525 | 1,467 | 1,581 | 4.0 | % | -3.5 | % | 6,039 | 6,454 | -6.4 | % | |||||||||||||||||||||

| Gasoline (third parties) |

1,055 | 929 | 1,022 | 13.5 | % | 3.1 | % | 3,944 | 4,013 | -1.7 | % | |||||||||||||||||||||

| Other domestic market |

716 | 715 | 706 | 0.1 | % | 1.4 | % | 2,706 | 2,790 | -3.0 | % | |||||||||||||||||||||

| Export market |

630 | 619 | 739 | 1.8 | % | -14.7 | % | 2,649 | 2,766 | -4.2 | % | |||||||||||||||||||||

| Revenues |

3,926 | 3,730 | 4,047 | 5.3 | % | -3.0 | % | 15,338 | 16,023 | -4.3 | % | |||||||||||||||||||||

| Depreciation & amortization |

(196 | ) | (185 | ) | (191 | ) | 6.2 | % | 2.8 | % | (708 | ) | (660 | ) | 7.3 | % | ||||||||||||||||

| OPEX Downstream |

(553 | ) | (518 | ) | (558 | ) | 6.9 | % | -0.8 | % | (2,128 | ) | (2,104 | ) | 1.2 | % | ||||||||||||||||

| Fuels imports (including jet fuel - third parties) |

(25 | ) | (35 | ) | (28 | ) | -29.7 | % | -10.1 | % | (172 | ) | (225 | ) | -23.4 | % | ||||||||||||||||

| Crude oil purchases (intersegment + third parties) |

(1,841 | ) | (2,012 | ) | (2,031 | ) | -8.5 | % | -9.4 | % | (7,749 | ) | (8,072 | ) | -4.0 | % | ||||||||||||||||

| Biofuel purchases (third parties) |

(231 | ) | (208 | ) | (212 | ) | 11.3 | % | 9.2 | % | (909 | ) | (910 | ) | -0.1 | % | ||||||||||||||||

| Agro products purchases (third parties) |

(156 | ) | (226 | ) | (133 | ) | -31.0 | % | 16.9 | % | (723 | ) | (602 | ) | 20.2 | % | ||||||||||||||||

| Stock variations |

(137 | ) | 35 | (150 | ) | N/A | -8.5 | % | (112 | ) | (25 | ) | 354.9 | % | ||||||||||||||||||

| Other |

(470 | ) | (418 | ) | (560 | ) | 12.3 | % | -16.1 | % | (1,669 | ) | (2,066 | ) | -19.2 | % | ||||||||||||||||

| Operating income / (loss) before impairment of assets |

317 | 163 | 185 | 94.5 | % | 71.1 | % | 1,167 | 1,359 | -14.1 | % | |||||||||||||||||||||

| Reversal / (Impairment) of PP&E |

— | — | (3 | ) | N/A | N/A | — | (3 | ) | N/A | ||||||||||||||||||||||

| Operating income / (loss) |

317 | 163 | 182 | 94.5 | % | 74.0 | % | 1,167 | 1,356 | -13.9 | % | |||||||||||||||||||||

| Depreciation & amortization |

196 | 185 | 191 | 6.2 | % | 2.8 | % | 708 | 660 | 7.3 | % | |||||||||||||||||||||

| Reversal / (Impairment) of PP&E |

— | — | 3 | N/A | N/A | — | 3 | N/A | ||||||||||||||||||||||||

| EBITDA |

513 | 348 | 376 | 47.5 | % | 36.4 | % | 1,875 | 2,019 | -7.1 | % | |||||||||||||||||||||

| Leasing |

(44 | ) | (46 | ) | (40 | ) | -4.2 | % | 8.9 | % | (154 | ) | (143 | ) | 7.8 | % | ||||||||||||||||

| Result from revaluation of companies |

— | — | — | N/A | N/A | (44 | ) | — | N/A | |||||||||||||||||||||||

| Miscellaneous – Others |

62 | (1 | ) | — | N/A | N/A | 61 | — | N/A | |||||||||||||||||||||||

| Adjusted EBITDA |

531 | 301 | 336 | 76.4 | % | 58.1 | % | 1,738 | 1,876 | -7.3 | % | |||||||||||||||||||||

| Inventories price effect of oil products |

(163 | ) | (58 | ) | (41 | ) | 179.8 | % | 300.6 | % | (277 | ) | 40 | N/A | ||||||||||||||||||

| Adjusted EBITDA excl. inventories price effect of oil products |

694 | 359 | 377 | 93.2 | % | 84.3 | % | 2,015 | 1,837 | 9.7 | % | |||||||||||||||||||||

| CAPEX |

256 | 218 | 350 | 17.3 | % | -27.0 | % | 924 | 1,187 | -22.2 | % | |||||||||||||||||||||

Stock variations include price effects by (US$40) million in 4Q24, (US$164) million for 4Q25, (US$48) million for 3Q25, (US$263) million for 2025 and US$45 million for 2024.

Revenues totaled US$15.3 billion in 2025 (-4% y/y), mostly explained by a decline in export and local prices, consistent with the downward trend in international oil prices, and reduced jet fuel exports (following the exit from YPF Chile’s aviation business). These effects were partially mitigated by higher demand of grain and flour exports, and increased volumes dispatched of gasoline, diesel, jet fuel, other refined products and higher crude oil export volumes. In 4Q25, revenues increased by 5% quarter-on-quarter, driven by higher domestic fuel prices—which closed the period fully in line with international benchmarks—and greater demand for gasoline and diesel, also boosted by gasoline seasonality. However, this growth was partially offset by a 7% reduction in Brent prices, adversely affecting both local and export prices of other refined and petrochemical products.

OPEX Downstream posted a modest increase in 2025 (+1% y/y), on the back of higher refining and marketing activity levels, partially offset by new efficiency gains (particularly from optimized overland transportation contracts). In 4Q25, costs rose 7% q/q, mainly reflecting higher transportation costs, on the back of increased operational activity, and higher peso-denominated costs in dollar terms.

Fuel imports dropped 23% y/y in 2025, mostly due to lower imported fuel volumes, driven by higher processing levels, and decline in international prices. Thus, total fuel imported volumes represented only 2% of our local fuel sales in 2025, remaining broadly in line with 2024. In 4Q25, fuel imports fell 30% q/q mainly explained by lower imported diesel volume.

Page 8/15

Crude oil purchases (intersegment + third parties) fell 4% y/y in 2025, driven by a decline in oil prices, partially offset by higher volumes (reduced exposure to mature fields and increased processing levels). In 4Q25, purchases declined 9% q/q, following a similar trend: contraction in oil price partially offset by higher crude oil processing levels. Biofuel purchases remained stable in 2025, as a 1% decline in biodiesel was balanced by a 1% increase in bioethanol purchases, supporting gasoline sales. Agro product purchases rose 20% y/y in 2025, led by higher volumes and prices of both, grain and flours and fertilizers. Contrary, in 4Q25 agro product purchases fell 31% q/q, driven by lower seasonal period.

Stock variations amounted to (-US$112 million) in 2025 vs. (-US$25 million) in 2024, mainly explained by the impact of lower reference prices on our inventory valuation. In 4Q25, it was (-US$137 million) vs. US$35 million in 3Q25, reflecting both, the decline in oil prices and an inventory drawdown (in line with higher sales), while 3Q25 was impacted by better prices and higher oil purchases to restock inventories.

Other was (-US$1.7 billion) in 2025 (-19% y/y), due to lower operating costs related to the discontinuation of aviation business in YPF Chile, reduced lubricant purchases and lower taxes (mainly due to removal of Impuesto PAIS). In 4Q25, it rose 12% q/q, reflecting the result related to the acquisition of 50% of Refinor and higher environmental provision.

Adj. EBITDA, excluding inventories price effect of oil products, reached US$2,015 million in 2025 (+10% y/y), mostly explained by record high processing levels and higher crack spreads, as local fuel prices stood almost fully aligned with international parities. In 4Q25 Adj. EBITDA surged 93% q/q, led by higher processing levels and local fuels prices recovery. These effects were partially offset by the extraordinary environmental provision mentioned above and increased transportation costs.

Adj. EBITDA of the Refining & Marketing business, in unit terms, reached US$12.9/bbl in 2025, compared to US$13.9/bbl reported in 2024, mostly explained by lower local fuel prices, partially offset by higher processing levels and efficiencies gained. Notably, in 4Q25, R&M Adjusted EBITDA jumped to US$18.6/bbl (tripling q/q), on the back of record processing levels and local fuel price recovery, coupled with higher diesel crack spreads and lower costs in real terms.

CAPEX stood at US$924 million in 2025 (-22% y/y, primarily due to completion of VMOC oil pipeline) and the composition is as follows: 59% refining, 19% midstream oil and gas, 16% logistics and 6% others.

In our refineries, during 2025 CAPEX was allocated on the following main projects:

| • | New fuel specifications project, to comply with the Resolution No. 492/2023 of the Secretary of Energy. We continued moving forward with the construction of a new diesel oil hydrotreatment unit at Luján de Cuyo refinery, which is expected to be operational in 1H26. |

| • | Revamping of topping units, we completed the revamping works in Plaza Huincul refinery in 2Q25, raising shale oil processing to ~80% of the total crude oil processed in that refinery. In parallel, we continued with the revamping of topping units at Luján de Cuyo refinery, expected to be completed in 2Q26, enabling 100% shale oil processing. |

In our midstream oil business unit, we continued moving forward in our main projects:

| • | VMOS (Allen – Punta Colorada, ~440 km oil export dedicated pipeline): ~50% progress in completion, with first oil expected by January 2027 (~180 kbbl/d). Capacity will reach ~550 kbbl/d in 2027, potentially expandable to +700 kbbl/d, if necessary. As of December 2025, initial shippers’ commitment reached 490 kbbl/d (YPF’s initial shipping is 120 kbbl/d, holding the largest stake with ~25%). |

In our midstream gas business unit, we also continued making progress on our main projects:

| • | Fully Revamping of the natural gas treatment plant at Loma La Lata, increasing its current capacity, while improving the treatment of associated gas, expected to be operational in 1Q26. |

| • | South Hub gathering project to expand gas processing capacity at Sierra Barrosa treatment plants. First phase was completed in 2024, and second phase was launched in 1Q25, expected to be in place in 2027. |

Page 9/15

| • | North Hub gathering project, consists of constructing a new gas pipeline connecting Narambuena and Bajo del Toro blocks with El Portón Industrial Complex, expected to be operational in 3Q26. |

| Midstream & Downstream Operating data Unaudited Figures |

4Q25 | 3Q25 | 4Q24 | Q/Q ∆ | Y/Y ∆ | 2025 | 2024 | Y/Y ∆ | ||||||||||||||||||||||||

| Crude processed (Kbbld) |

334.9 | 326.2 | 304.1 | 2.7 | % | 10.1 | % | 320.2 | 300.7 | 6.5 | % | |||||||||||||||||||||

| Refinery utilization (%) |

99.1 | % | 96.5 | % | 90.0 | % | 257bps | 912bps | 94.7 | % | 89.0 | % | 576bps | |||||||||||||||||||

| Nominal capacity at 337.94 Kbbl/d since 1Q24. |

|

|||||||||||||||||||||||||||||||

| Sales volume to third parties (YPF stand alone) |

||||||||||||||||||||||||||||||||

| Sales of refined products (Km3) |

5,475 | 4,930 | 4,891 | 11.1 | % | 11.9 | % | 19,923 | 18,988 | 4.9 | % | |||||||||||||||||||||

| Total domestic market |

4,877 | 4,513 | 4,330 | 8.1 | % | 12.6 | % | 17,930 | 16,930 | 5.9 | % | |||||||||||||||||||||

| of which Gasoline |

1,618 | 1,501 | 1,500 | 7.8 | % | 7.8 | % | 6,012 | 5,782 | 4.0 | % | |||||||||||||||||||||

| of which Diesel |

2,156 | 2,154 | 2,077 | 0.1 | % | 3.8 | % | 8,354 | 8,165 | 2.3 | % | |||||||||||||||||||||

| Total export market |

598 | 417 | 561 | 43.5 | % | 6.6 | % | 1,993 | 2,058 | -3.2 | % | |||||||||||||||||||||

| Sales of petrochemical products (Ktn) |

163 | 131 | 145 | 24.5 | % | 12.1 | % | 548 | 616 | -11.1 | % | |||||||||||||||||||||

| Domestic market |

51 | 65 | 64 | -22.3 | % | -21.2 | % | 227 | 295 | -23.0 | % | |||||||||||||||||||||

| Export market |

112 | 65 | 81 | 71.2 | % | 38.7 | % | 321 | 321 | -0.1 | % | |||||||||||||||||||||

| Sales of fertilizers, grain and flours (Ktn) |

465 | 535 | 483 | -13.1 | % | -3.7 | % | 1,954 | 1,696 | 15.2 | % | |||||||||||||||||||||

| Domestic market |

262 | 196 | 203 | 33.4 | % | 28.8 | % | 665 | 868 | -23.4 | % | |||||||||||||||||||||

| Export market |

203 | 339 | 279 | -40.1 | % | -27.4 | % | 1,289 | 829 | 55.6 | % | |||||||||||||||||||||

| Net average prices |

||||||||||||||||||||||||||||||||

| Gasoline (USD/m3) (domestic market) |

603 | 567 | 637 | 6.3 | % | -5.3 | % | 601 | 638 | -5.8 | % | |||||||||||||||||||||

| Diesel (USD/m3) (domestic market) |

663 | 637 | 720 | 4.1 | % | -7.9 | % | 677 | 746 | -9.2 | % | |||||||||||||||||||||

| Net Average domestic prices for gasoline and diesel are net of taxes, commissions, commercial bonuses and freights. |

|

|||||||||||||||||||||||||||||||

Crude oil processed averaged 320 Kbbl/d in 2025 (+6% y/y), recording a refinery utilization of 95%, This expansion was mainly driven by La Plata refinery (+10% y/y), which operated with full crude oil availability compared to the previous year without any external events that restricted processing levels, thereby achieving full utilization of its units. Moreover, during the first half of 2025, product mix was optimized as bottlenecks in product dispatch were eliminated, minimizing imports levels. Importantly, in 4Q25, crude processed set a new record, averaging 335 Kbbl/d (+3% q/q), the highest level of the last 15 years, with a refinery utilization of 99%.

Domestic fuel sale volumes reached 14.4 million m3, growing 3% y/y in 2025 (gasoline +4% and diesel +2%), mostly driven by higher local fuel demand across all commercial segments. In 4Q25, the +3% q/q variation was led by higher seasonal fuel demand, primarily gasoline. In this context, during the year, YPF maintained the historical leading position in the market, posting a fuel sales market share of 56%.

Petrochemicals volumes declined by 11% y/y in 2025, primarily due to lower local demand of methanol.

Fertilizers, grain and flours sales volumes increased 15% y/y in 2025, driven by a substantial growth of grain and flour exports, as price dynamics between domestic and international grain markets gradually normalized throughout the year, boosting sales in the export market.

Net average fuels prices in the domestic market measured in dollar terms fell 8% y/y in 2025, remaining broadly aligned with international parities, with an average annual discount of 3% (vs. a 2% discount in 2024).

Page 10/15

3.3 LNG & INTEGRATED GAS

| LNG & Integrated Gas Unaudited Figures, in US$ million |

4Q25 | 3Q25 | 4Q24 | Q/Q ∆ | Y/Y ∆ | 2025 | 2024 | Y/Y ∆ | ||||||||||||||||||||||||

| Natural gas (intersegment + third parties) |

315 | 634 | 341 | -50.3 | % | -7.6 | % | 1,871 | 1,851 | 1.1 | % | |||||||||||||||||||||

| Other |

23 | 28 | 21 | -18.3 | % | 9.5 | % | 94 | 76 | 23.8 | % | |||||||||||||||||||||

| Revenues |

338 | 662 | 362 | -48.9 | % | -6.6 | % | 1,965 | 1,927 | 2.0 | % | |||||||||||||||||||||

| Depreciation & amortization |

1 | (2 | ) | (1 | ) | N/A | N/A | (2 | ) | (2 | ) | -0.1 | % | |||||||||||||||||||

| Natural gas purchases (intersegment + third parties) |

(314 | ) | (624 | ) | (344 | ) | -49.7 | % | -8.8 | % | (1,875 | ) | (1,838 | ) | 2.0 | % | ||||||||||||||||

| Operating cost & Other |

(22 | ) | (42 | ) | (20 | ) | -46.3 | % | 13.6 | % | (96 | ) | (136 | ) | -29.2 | % | ||||||||||||||||

| Operating income before impairment of assets |

3 | (6 | ) | (3 | ) | N/A | N/A | (8 | ) | (49 | ) | -83.6 | % | |||||||||||||||||||

| Reversal / (Impairment) of PP&E |

— | — | — | N/A | N/A | — | — | N/A | ||||||||||||||||||||||||

| Operating income |

3 | (6 | ) | (3 | ) | N/A | N/A | (8 | ) | (49 | ) | -83.6 | % | |||||||||||||||||||

| Depreciation & amortization |

(1 | ) | 2 | 1 | N/A | N/A | 2 | 2 | -0.1 | % | ||||||||||||||||||||||

| EBITDA |

2 | (4 | ) | (2 | ) | N/A | N/A | (6 | ) | (47 | ) | -87.2 | % | |||||||||||||||||||

| Leasing |

— | (0 | ) | — | N/A | N/A | (1 | ) | — | N/A | ||||||||||||||||||||||

| Adjusted EBITDA |

2 | (4 | ) | (2 | ) | N/A | N/A | (7 | ) | (47 | ) | -84.5 | % | |||||||||||||||||||

| CAPEX |

16 | 9 | 18 | 77.8 | % | -9.5 | % | 42 | 26 | 61.5 | % | |||||||||||||||||||||

Adj. EBITDA totaled negative US$7 million in 2025, compared to negative US$47 million in 2024, mainly due to the considerably lower charge for doubtful sales receivables (in 2024 we recognized US$51 million extraordinary charge, mostly owed by CAMMESA). In 4Q25 natural gas sales dropped sequentially due to lower seasonal demand, in line with the decrease in natural gas purchases. However, operating costs dropped sequentially, primarily due to lower transportation expenses and provision for doubtful receivables.

CAPEX amounted to US$42 million in 2025 (+62% y/y), mostly allocated to the Argentina LNG Project for the FEED engineering work and initial feasibility studies that continued advancing throughout the year.

3.4 NEW ENERGIES

| New Energies Unaudited Figures, in US$ million |

4Q25 | 3Q25 | 4Q24 | Q/Q ∆ | Y/Y ∆ | 2025 | 2024 | Y/Y ∆ | ||||||||||||||||||||||||

| Natural gas retail (third parties) |

141 | 201 | 169 | -30.1 | % | -17.0 | % | 676 | 760 | -11.0 | % | |||||||||||||||||||||

| Other |

47 | 33 | 38 | 44.3 | % | 25.7 | % | 167 | 144 | 15.8 | % | |||||||||||||||||||||

| Revenues |

188 | 234 | 207 | -19.7 | % | -9.2 | % | 843 | 904 | -6.7 | % | |||||||||||||||||||||

| Depreciation & amortization |

(12 | ) | (9 | ) | (11 | ) | 33.3 | % | 8.9 | % | (46 | ) | (45 | ) | 2.1 | % | ||||||||||||||||

| Natural gas purchases (intersegment + third parties) |

(76 | ) | (106 | ) | (77 | ) | -28.5 | % | -1.3 | % | (341 | ) | (397 | ) | -14.1 | % | ||||||||||||||||

| Operating cost & Other |

246 | (76 | ) | (96 | ) | N/A | N/A | (28 | ) | (351 | ) | -92.0 | % | |||||||||||||||||||

| Operating income before impairment of assets |

346 | 43 | 23 | 704.7 | % | 1404.3 | % | 428 | 111 | 285.6 | % | |||||||||||||||||||||

| Reversal / (Impairment) of PP&E |

— | (5 | ) | — | N/A | N/A | 4 | (5 | ) | N/A | ||||||||||||||||||||||

| Operating income |

346 | 38 | 23.00 | 810.5 | % | 1404.3 | % | 432 | 106 | 307.5 | % | |||||||||||||||||||||

| Depreciation & amortization |

12 | 9 | 11 | 33.3 | % | 8.9 | % | 46 | 45 | 2.1 | % | |||||||||||||||||||||

| Reversal / (Impairment) of PP&E |

— | 5 | — | N/A | N/A | (4 | ) | 5 | N/A | |||||||||||||||||||||||

| EBITDA |

358 | 52 | 34 | 588.4 | % | 952.3 | % | 474 | 156 | 203.8 | % | |||||||||||||||||||||

| Leasing |

— | — | — | N/A | N/A | — | — | N/A | ||||||||||||||||||||||||

| Result from sale of companies |

(335 | ) | — | — | N/A | N/A | (335 | ) | — | N/A | ||||||||||||||||||||||

| Adjusted EBITDA |

23 | 52 | 34 | -55.8 | % | -32.4 | % | 139 | 156 | -10.9 | % | |||||||||||||||||||||

| CAPEX |

12 | 7 | 15 | 60.0 | % | -19.6 | % | 38 | 40 | -4.5 | % | |||||||||||||||||||||

Adj. EBITDA totaled US$139 million in 2025 (-11% y/y), almost entirely attributable to Metrogas subsidiary (Adj EBITDA 2025: US$135 million), as a result of lower prices in dollar terms and, to a lesser extent, reduced gas demand. In 4Q25, Adj. EBITDA decreased by 56% q/q, mainly due to lower seasonal natural gas sales. The Adj. EBITDA excludes US$335 million for the result from the sale of 50% of Profertil affiliate, which is included in the Operating cost & Other line.

4. LIQUIDITY AND SOURCES OF CAPITAL

4.1 CASH FLOW SUMMARY

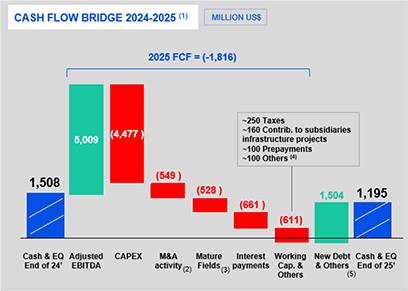

The free cash flow for 2025 was negative at US$1.8 billion, despite Adjusted EBITDA (US$5.0 billion) nearly offset CAPEX deployment (US$4.5 billion) and regular interest payments (US$661 million). This outcome is primarily attributable to extraordinary M&A activities (-US$549 million), resulting from the acquisition of three tier-one shale assets, net of partial proceeds from the divestment of 50% of Profertil and 49% of Aguada del Chañar block. Additionally, results were impacted by one-off items associated with mature fields (-US$528 million), contributions to infrastructure projects (notably VMOS, OldelVal and SESA), and prepaid dollarized costs for 2026 pursuant to our proactive hedging strategy, as well as various tax payments (including income tax at Metrogas and AESA and the new Income Tax Normalization Plan for YPF SA), among other factors.

Page 11/15

In 4Q25 free cash flow shifted into positive ground at US$265 million, as Adj. EBITDA (US$1.3 billion) exceeded CAPEX deployment (US$1.1 billion) and interest payments (US$123 million), in addition to the partial collection from divestment of Profertil (US$200 million).

In terms of liquidity, our cash and short-term investments totaled US$1,195 million by the end of Dec-2025.

Notes: [1] Approximation of cash flow evolution, highlighting key figures. Cash & equivalents include Argentine sovereign bonds and Treasury notes. [2] Includes (in MUS$): acquisition of 45% of La Escalonada & Rincón la Ceniza (-531), as well as the acquisition of 54.45% of Sierra Chata, net of divestment of 49% of Aguada del Chañar (-211), partial collection of sale of 50% of Profertil (+200), among others (-7). [3] Includes (in MUS$): operating optimizations (-318), Santa Cruz agreement (-142), severance indemnities (-58), additions of assets held for sale (-46), collections for sale of assets (+61), among others (-25). [4] Others consider leasing payments, dividend collections from affiliates, among others. [5] Others include mainly FX differences and net collection for sale of financial assets.

4.2 NET DEBT

| Net debt breakdown Unaudited Figures, in US$ million |

4Q25 | 3Q25 | 4Q24 | Q/Q ∆ | ||||||||||||

| Short-term debt |

2,355 | 2,653 | 1,907 | -11.2 | % | |||||||||||

| Long-term debt |

8,226 | 7,958 | 7,035 | 3.4 | % | |||||||||||

| Total debt |

10,581 | 10,611 | 8,942 | -0.3 | % | |||||||||||

| Avg. Interest rate for US$-debt |

6.8 | % | 6.7 | % | 6.5 | % | ||||||||||

| % of debt in USD |

99.2 | % | 98.7 | % | 99.4 | % | ||||||||||

| Cash + short term investments |

1,195 | 1,016 | 1,508 | 17.6 | % | |||||||||||

| % of liquidity dollarized |

68.4 | % | 70.5 | % | 69.5 | % | ||||||||||

| Net debt |

9,386 | 9,595 | 7,434 | -2.2 | % | |||||||||||

| Average interest rates for US$ debt refer to YPF on a stand-alone basis. |

|

|||||||||||||||

As of December 31, 2025, YPF’s consolidated net debt totaled US$9,386 million, slightly decreasing by 2% q/q but increasing by 26% y/y, mostly due to the negative free cash flow, explained above. The positive FCF of 4Q2025 combined with the increased EBITDA allowed the company to close in 2025 with a net leverage ratio of 1.9x, below the net leverage ratio of 2.1x reported in 3Q2025.

In terms of financing, in the international market, in 4Q25 we re-tapped the 2031 unsecured bond for US$500 million at an 8.25% yield. Proceeds were used to repay bridge loan for the acquisition of Total Austral’s shale assets and to finance YPF’s investment plan. Moreover, in 4Q2025 we obtained a US$700 million export-backed cross-border syndicated loan with 3-year tenor, from which only $50 million was disbursed as of February 2026, leaving a substantial undrawn commitment of $650 million, available before April 2026. Also, we fully redeemed 2026 secured bond Class XVI for US$60 million, originally due in February 2026.

Page 12/15

In the local capital market, in 4Q25 we issued two US$-MEP bonds: (1) Class XLI for US$99 million with a 1.25- year tenor at 6% rate; and (2) Class XLII for US$195 million with a 3.25-year tenor at 7% rate.

After 4Q25, in January 2026, we re-tapped 2034 international unsecured bond for US$550 million at an 8.1% yield, the lowest rate secured by the company in the international capital markets in the last 9 years. Proceeds were mostly used to prepay a US$324 million A/B Loan with CAF, executed in 2023, acquire Equinor’s assets (4.9% of Bandurria Sur and 15% of Bajo del Toro and Bajo del Toro Norte) for US$163 million, and other general corporate purposes.

In the local market, in February 2026, we re-tapped a US$-MEP bond for US$161 million, with a 3-year tenor at a 6.5% yield. The proceeds will be primarily used to redeem US$-MEP bond Class XXIX for US$131 million, net of repurchased amount, originally due in May 2026.

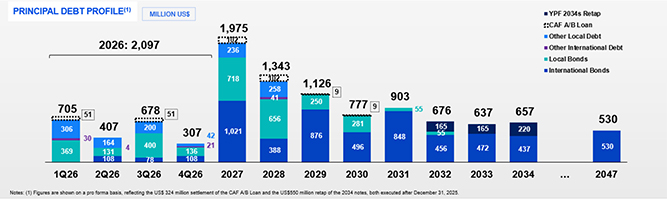

Regarding our maturity profile, the Company faces in the 12 months of 2026 US$2.1 billion3, mainly composed of: US$1.0 billion of local bonds, US$294 million of international bonds amortizations, US$215 million of short-term trade facilities (both local and international banks) and the remaining in other local debts. Thanks to a robust financial position, supported by diversified funding sources and nearly fully available bank credit lines, YPF is exceptionally well-prepared to meet its debt obligations over the next twelve months.

The following chart shows our consolidated principal debt maturity profile as of December 31, 2025:

| 3 | Considering prepayment of US$324 million of CAF A/B Loan & retap of US$550 million of 2034 Notes, executed after 2025. |

Page 13/15

5. TABLES

5.1 CONSOLIDATED BALANCE SHEET

| Consolidated Balance Sheet Unaudited Figures |

31-Dec-25 | 31-Dec-24 | ||||||

| Non-current Assets |

||||||||

| Intangible assets |

1,068 | 491 | ||||||

| Properties, plant and equipment |

19,085 | 18,736 | ||||||

| Right-of-use assets |

537 | 743 | ||||||

| Investments in associates and joint ventures |

1,610 | 1,960 | ||||||

| Deferred income tax assets, net |

9 | 330 | ||||||

| Other receivables |

648 | 337 | ||||||

| Trade receivables |

5 | 1 | ||||||

| Total Non-current Assets |

22,962 | 22,598 | ||||||

| Current Assets |

||||||||

| Assets held for disposal |

1,019 | 1,537 | ||||||

| Inventories |

1,447 | 1,546 | ||||||

| Contract assets |

3 | 30 | ||||||

| Other receivables |

1,159 | 552 | ||||||

| Trade receivables |

1,654 | 1,620 | ||||||

| Investment in financial assets |

262 | 390 | ||||||

| Cash and cash equivalents |

933 | 1,118 | ||||||

| Total Current Assets |

6,477 | 6,793 | ||||||

| Total Assets |

29,439 | 29,391 | ||||||

| Total Shareholders´ Equity |

11,044 | 11,870 | ||||||

| Non-current Liabilities |

||||||||

| Provisions |

610 | 1,084 | ||||||

| Deferred income tax liabilities, net |

373 | 90 | ||||||

| Contract liabilities |

180 | 114 | ||||||

| Income tax liability |

830 | 2 | ||||||

| Other taxes payable |

18 | 0 | ||||||

| Salaries and social security |

63 | 34 | ||||||

| Lease liabilities |

273 | 406 | ||||||

| Loans |

8,226 | 7,035 | ||||||

| Other liabilities |

373 | 74 | ||||||

| Accounts payable |

6 | 6 | ||||||

| Total non-current Liabilities |

10,952 | 8,845 | ||||||

| Current Liabilities |

||||||||

| Liabilities directly associated with assets held for sale |

1,181 | 2,136 | ||||||

| Provisions |

229 | 116 | ||||||

| Contract liabilities |

117 | 73 | ||||||

| Income tax liability |

73 | 126 | ||||||

| Taxes payable |

217 | 247 | ||||||

| Salaries and social security |

336 | 412 | ||||||

| Lease liabilities |

298 | 370 | ||||||

| Loans |

2,355 | 1,907 | ||||||

| Other liabilities |

399 | 410 | ||||||

| Accounts payable |

2,238 | 2,879 | ||||||

| Total Current Liabilities |

7,443 | 8,676 | ||||||

| Total Liabilities |

18,395 | 17,521 | ||||||

| Total Liabilities and Shareholders’ Equity |

29,439 | 29,391 | ||||||

Note: Information reported in accordance with International Financial Reporting Standards (IFRS).

Page 14/15

5.2 CONSOLIDATED INCOME STATEMENT

| Income Statement Unaudited Figures, in US$ million |

4Q25 | 3Q25 | 4Q24 | Q/Q ∆ |

Y/Y ∆ |

2025 | 2024 | Y/Y ∆ | ||||||||||||||||||

| Revenues |

4,556 | 4,643 | 4,751 | -1.9% | -4.1% | 18,448 | 19,293 | -4.4% | ||||||||||||||||||

| Costs |

(3,232 | ) | (3,319 | ) | (3,756 | ) | -2.6% | -14.0% | (13,348 | ) | (13,910 | ) | -4.0% | |||||||||||||

| Gross profit |

1,324 | 1,324 | 995 | 0.0% | 33.1% | 5,100 | 5,383 | -5.3% | ||||||||||||||||||

| Selling expenses |

(530 | ) | (495 | ) | (536 | ) | 7.1% | -1.1% | (2,088 | ) | (2,132 | ) | -2.1% | |||||||||||||

| Administrative expenses |

(229 | ) | (207 | ) | (261 | ) | 10.6% | -12.3% | (830 | ) | (836 | ) | -0.7% | |||||||||||||

| Exploration expenses |

(48 | ) | (17 | ) | (108 | ) | 182.4% | -55.6% | (116 | ) | (239 | ) | -51.5% | |||||||||||||

| Reversal / (Impairment) of PP&E and inventories write-down |

— | (5 | ) | (61 | ) | N/A | N/A | 4 | (87 | ) | N/A | |||||||||||||||

| Other net operating results |

67 | (48 | ) | (559 | ) | N/A | N/A | (330 | ) | (609 | ) | -45.8% | ||||||||||||||

| Operating income |

584 | 552 | (530 | ) | 5.8% | N/A | 1,740 | 1,480 | 17.6% | |||||||||||||||||

| Income from equity interests in associates and joint ventures |

15 | 32 | 133 | -53.1% | -88.7% | 122 | 396 | -69.2% | ||||||||||||||||||

| Financial Income |

33 | 28 | 47 | 17.9% | -29.8% | 105 | 134 | -21.6% | ||||||||||||||||||

| Financial Cost |

(266 | ) | (257 | ) | (258 | ) | 3.5% | 3.1% | (1,087 | ) | (1,169 | ) | -7.0% | |||||||||||||

| Other financial results |

27 | (16 | ) | 108 | N/A | -75.0% | 30 | 179 | -83.3% | |||||||||||||||||

| Net financial results |

(206 | ) | (245 | ) | (103 | ) | -15.9% | 100.1% | (952 | ) | (856 | ) | 11.3% | |||||||||||||

| Net profit before income tax |

393 | 339 | (500 | ) | 15.9% | N/A | 910 | 1,020 | -10.8% | |||||||||||||||||

| Income tax |

(1,042 | ) | (537 | ) | 216 | 94.0% | N/A | (1,709 | ) | 1,373 | N/A | |||||||||||||||

| Net (loss) / profit for the period |

(649 | ) | (198 | ) | (284 | ) | 228.0% | 128.5% | (799 | ) | 2,393 | N/A | ||||||||||||||

| Net (loss) / profit for the period attributable to: |

||||||||||||||||||||||||||

| Shareholders of the parent company |

(654 | ) | (206 | ) | (290 | ) | 217.5% | 125.5% | (826 | ) | 2,348 | N/A | ||||||||||||||

| Non-controlling interest |

5 | 8 | 6 | -37.5% | -16.7% | 27 | 45 | -40.0% | ||||||||||||||||||

| Earnings per share attributable to shareholders of the parent company (basic and diluted) |

(1.67 | ) | (0.53 | ) | (0.74 | ) | 215.1% | 125.7% | (2.11 | ) | 5.99 | N/A | ||||||||||||||

Note: Information reported in accordance with International Financial Reporting Standards (IFRS).

5.3 SUMMARY OF CONSOLIDATED CASHFLOW STATEMENT

| Summary Consolidated Cash Flow Unaudited Figures, in US$ million |

4Q25 | 3Q25 | 4Q24 | Q/Q ∆ |

Y/Y ∆ |

2025 | 2024 | Y/Y ∆ | ||||||||||||||||||

| Cash BoP |

799 | 774 | 877 | 3.2% | -8.9% | 1,118 | 1,123 | -0.4% | ||||||||||||||||||

| Net cash flow from operating activities |

1,738 | 1,225 | 1,663 | 41.9% | 4.5% | 4,959 | 5,869 | -15.5% | ||||||||||||||||||

| Net cash flow from investing activities |

(1,224 | ) | (1,662 | ) | (1,400 | ) | -26.4% | -12.6% | (5,527 | ) | (5,511 | ) | 0.3% | |||||||||||||

| Net cash flow from financing activities |

(354 | ) | 497 | (1 | ) | N/A |

35300.0% |

517 | (293 | ) | N/A | |||||||||||||||

| FX adjustments & other |

(26 | ) | (35 | ) | (21 | ) | -25.7% | 24.0% | (134 | ) | (70 | ) | 92.5% | |||||||||||||

| Cash EoP |

933 | 799 | 1,118 | 16.8% | -16.5% | 933 | 1,118 | -16.5% | ||||||||||||||||||

| Investment in financial assets |

262 | 217 | 390 | 20.7% | -32.8% | 262 | 390 | -32.8% | ||||||||||||||||||

| Cash + short-term investments EoP |

1,195 | 1,016 | 1,508 | 17.6% | -20.8% | 1,195 | 1,508 | -20.8% | ||||||||||||||||||

| FCF |

265 | (759 | ) | 64 | N/A | 314.1% | (1,816 | ) | (760 | ) | 138.9% | |||||||||||||||

FCF = Cash flow from Operations less capex (Investing activities), M&A (Investing activities), and interest and leasing payments (Financing activities).

6. ABOUT YPF

YPF is the largest energy company in Argentina, fully integrated in the oil and gas value chain. Our main businesses are: (i) in the upstream, we produce ~30% of the country’s oil and gas, and we are the largest shale producer in Vaca Muerta, in process of divestment of conventional mature fields; (ii) in the downstream, we operate 4 refineries (+50% of Argentina’s refining capacity) and lead the local diesel and gasoline sales (market share >55%); and (iii) in gas and power, Metrogas, our subsidiary, distributes ~25% of the country’s natural gas, while YPF Luz, our affiliate, is the third largest power generation company in Argentina. The Government is the controlling shareholder with a 51% stake, and YPF is listed in the NYSE and ByMA.

7. DISCLAIMER

Additional information about YPF S.A., a sociedad anónima organized under the laws of Argentina (the “Company” or “YPF”) can be found in the “Investors” section on the website at www.ypf.com.

This document does not constitute an offer to sell or the solicitation of any offer to buy any securities of the Company, in any jurisdiction. Securities may not be offered or sold in the United States absent registration with the U.S. Securities Exchange Commission (“SEC”), the Comisión Nacional de Valores (Argentine National Securities and Exchange Commission, or “CNV”) or an exemption from such registrations.

No reliance may be placed for any purpose whatsoever on the information contained in this document or on its completeness. Certain information contained in this document may have been obtained from published sources, which may not have been independently verified or audited. No representation or warranty, express or implied, is given or will be given by or on behalf of the Company, or any of its affiliates (within the meaning of Rule 405 under the Act, “Affiliates”), members, directors, officers or employees or any other person (the “Related Parties”) as to the accuracy, completeness or fairness of the information or opinions contained in this document or any other material discussed verbally, and any reliance you place on them will be at your sole risk. Any opinions presented herein are based on general information gathered at the time of writing and are subject to change without notice. In addition, no responsibility, obligation or liability (whether direct or indirect, in contract, tort or otherwise) is or will be accepted by the Company or any of its Related Parties in relation to such information or opinions or any other matter in connection with this document or its contents or otherwise arising in connection therewith.

This document may also include certain non-IFRS (International Financial Reporting Standards) financial measures which have not been subject to a financial audit for any period. The information and opinions contained in this document are provided as at the date of this document and are subject to verification, completion and change without notice.

This document includes “forward-looking statements” concerning the future. The words such as “believes,” “thinks,” “forecasts,” “expects,” “anticipates,” “intends,” “should,” “seeks,” “estimates,” “future” or similar expressions are included with the intention of identifying statements about the future. For the avoidance of doubt, any projection, guidance or similar estimation about the future or future results, performance or achievements is a forward-looking statement. Although the assumptions and estimates on which forward-looking statements are based are believed by our management to be reasonable and based on the best currently available information, such forward-looking statements are based on assumptions that are inherently subject to significant uncertainties and contingencies, many of which are beyond our control.

Forward-looking statements speak only as of the date on which they were made, and we undertake no obligation to release publicly any updates or revisions to any forward-looking statements contained herein because of new information, future events or other factors. In light of these limitations, undue reliance should not be placed on forward-looking statements contained in this document. Further information concerning risks and uncertainties associated with these forward-looking statements and YPF’s business can be found in YPF’s public disclosures filed on EDGAR (www.sec.gov) or at the web page of the Argentine National Securities and Exchange Commission (www.argentina.gob.ar/cnv).

You should not take any statement regarding past trends or activities as a representation that the trends or activities will continue in the future. Accordingly, you should not put undue reliance on these statements. This document is not intended to constitute and should not be construed as investment advice. The information contained herein has been prepared to assist interested parties in making their own evaluations of YPF.

Page 15/15

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| YPF Sociedad Anónima | ||||||

| Date: February 26, 2026 | By: | /s/ Margarita Chun | ||||

| Name: | Margarita Chun | |||||

| Title: | Market Relations Officer | |||||