| |

Pre-Effective Amendment No. |

[ ] |

| |

Post-Effective Amendment No. |

[ ] |

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion Dated September 24, 2024

[Corebridge RILA] Annuity

Single Purchase Payment Deferred Registered Index-Linked Annuity

issued by

The Variable Annuity Life Insurance Company

Prospectus Dated: [•]

This prospectus describes the [Corebridge RILA] Annuity Contract and contains important information, including a description of all material features of the Contract. Please read this prospectus carefully before investing and keep it for future reference.

The Contract is a single Purchase Payment deferred registered index-linked annuity contract issued by The Variable Annuity Life Insurance Company (“VALIC”). The Contract is designed to help you accumulate funds for retirement or other long-term financial planning purposes on a tax-deferred basis.

VALIC does not allow additional Purchase Payments. The Contract is not a short-term investment and is not appropriate for investors who plan or need to take Withdrawals or Surrender the Contract during the first six Contract Years due to the application of Withdrawal Charges, or prior to the end of a Strategy Account Option Term because of the use of Interim Value to calculate the amount available for Withdrawal. These adjustments could significantly reduce the value of the Contract to less than the protection levels provided by the Strategy Account Options and could result in a loss of up to 100% of your investment under extreme circumstances. The Contract is an insurance contract and is not an index fund. The Contract is a complex investment and involves risks, including potentially significant loss of principal. You should speak with your financial representative about the Contract’s features, benefits, risks, and fees.

Under the Contract, you may allocate your Purchase Payment to one or more of the “Strategy Account Option(s)” that credit returns based on the performance of a specific Index or Indices during a defined period of time (a “Term”) and/or the “Fixed Account Option,” a fixed interest investment option. See “Appendix A: Investment Options Available Under the Contract” for additional information about each Strategy Account Option and the Fixed Account Option. The Term for a Strategy Account Option may be one, three, or six years. Positive Index returns may be limited based on the applicable interest crediting method (the “Upside Parameter”), and your investment is subject to a downside parameter that provides limited downside protection from negative Index returns (the “Buffer”). The Indices are price return indices and therefore do not reflect dividends paid on the securities comprising the Index.

The Upside Parameter limits the amount you can earn on a Strategy Account Option. Upside Parameters, except Lock Upside Parameters, including applicable rates, can change from one Term to the next subject to minimum guaranteed rates. The minimum guaranteed rates that may be established under the Contract for each of the Upside Parameters (other than Lock Upside Parameters) are: Cap Rate (no lower than [•]%), Cap Secure Rate (no lower than [•]%), Participation and Cap Rate (Participation and Cap: no lower than [•]% and [•]%), and Trigger Rate (no lower than [•]%). The Lock Thresholds for Strategy Account Options with Lock Upside Parameters are guaranteed minimum rates under the Contract and will not change from one Term to the next. The Lock Threshold percentages available are: [30], [40], [50], [75], and [100].

The Buffer provides limited protection from negative Index performance. If negative Index performance exceeds the Buffer Rate, your negative Index performance will equal the negative Index performance in excess of the Buffer Rate. In extreme circumstances, you could lose 90% of your investment in a Strategy Account Option with a Buffer Rate of 10% and 80% of your investment in a Strategy Account Option with a Buffer Rate of 20% if negative Index performance on the Term End Date is 100%. The minimum guaranteed Buffer Rate that we offer under any Strategy Account Options other than those with Lock Upside Parameter is [•]%. Buffer Rates for all Strategy Account Options other than those with Lock Upside Parameter will not change from one Term to the next. The Lock Buffer Rates can change from one Term to the next subject to the minimum guaranteed Lock Buffer Rate of [•]%. With a minimum guaranteed Lock Buffer Rate of [•]%, in extreme circumstances, you could lose [•]% of your investment in a Strategy Account Option with Lock Upside Parameter.

We reserve the right to add, replace or remove Strategy Account Options offered, change the Indices, and limit the number of offered Strategy Account Options to only one. If only one Strategy Account Option is available, you will be limited to investing in only that Strategy Account Option with terms that may not be acceptable to you. We may change the Strategy Account Options, the Upside Parameters rates, Lock Buffer Rates, and Buffer Rates subject to the stated guaranteed minimum rates. There is no guarantee that a particular Strategy Account Option or Index will be available during the entire time that you own your Contract. If you choose to Surrender the Contract, you may be subject to Interim Values, Withdrawal Charges, taxes, and tax penalties. Similarly, if you replace the Contract with another retirement vehicle, it may have different features, fees, and risks than the Contract.

The Contract is available for use in connection with qualified and non-qualified annuities, including individual retirement accounts (“IRAs”), Roth IRAs and SEP IRAs. If you are considering funding an IRA with an annuity, you should know that an annuity does not provide any additional tax deferral treatment of earnings beyond the treatment provided by the IRA itself. You should fully discuss this decision with your financial representative.

If you are a new investor in the Contract, you may cancel your Contract within 10 days of receiving it without paying fees or penalties. In some states, this cancellation period may be longer. Upon cancellation, you will generally receive a full refund of the amount you paid with your application minus any Withdrawals made. The amount of the refund may vary according to state law. Interim Value will not apply when calculating your refund of the Purchase Payment. In states where a refund of Contract Value is required, Interim Value will apply which may lower the amount of your refund. See “Appendix E: State Variations.” You should review this prospectus and consult with your financial representative for additional information about the specific cancellation terms that apply.

The Company offers several different annuity contracts to meet the diverse needs of our investors. Our contracts may provide different features, benefits, programs, and investment options offered at different fees and expenses. You should carefully consider, among other things, whether the features of the Contract and the related fees provide the most appropriate solution to help you meet your retirement savings goals. The Company’s obligations under the Contract are subject to its financial strength and claims paying ability.

These securities have not been approved or disapproved by the U.S. Securities and Exchange Commission (“SEC”) nor any state securities commission, nor has the SEC passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense. All obligations and guarantees under the Contract are subject to the creditworthiness and claims-paying ability of the Company. An investment in the Contract is not a deposit or obligation of any bank and is not insured or guaranteed by any bank, the Federal Deposit Insurance Corporation or any other government agency.

[Inquiries: If you have questions about your Contract, call your financial representative or contact us at Annuity Service Center, P.O. Box 15570, Amarillo, Texas 79105-5570. Telephone Number: (800) 445-7862 and website www.corebridgefinancial.com/annuities.]

Purchase Payments must be sent to a separate address than that listed above. Please see “Purchasing a [Corebridge RILA] Annuity” in this prospectus for the address to which you must send your Purchase Payment.

2

| 4 | ||||

| 9 | ||||

| IMPORTANT INFORMATION YOU SHOULD CONSIDER ABOUT THE CONTRACT |

13 | |||

| 17 | ||||

| 18 | ||||

| 18 | ||||

| 18 | ||||

| 19 | ||||

| 19 | ||||

| 19 | ||||

| 19 | ||||

| 20 | ||||

| 20 | ||||

| 21 | ||||

| 22 | ||||

| 23 | ||||

| 24 | ||||

| 24 | ||||

| 25 | ||||

| 26 | ||||

| 26 | ||||

| 27 | ||||

| 27 | ||||

| 27 | ||||

| 28 | ||||

| 39 | ||||

| 40 | ||||

| 40 | ||||

| 41 | ||||

| 41 | ||||

| 41 | ||||

| 41 | ||||

| 41 | ||||

| 42 | ||||

| 43 | ||||

| 44 | ||||

| 46 | ||||

| 47 | ||||

| 49 | ||||

| 49 | ||||

| 49 | ||||

| 51 | ||||

| 51 | ||||

| 52 | ||||

| 53 | ||||

| 55 | ||||

| 56 | ||||

| 56 | ||||

| 56 | ||||

| 57 | ||||

| 57 | ||||

| 58 | ||||

| 58 | ||||

| 58 | ||||

| Reduction or Elimination of Fees, Charges and Additional Amounts Credited |

58 | |||

| 58 | ||||

| 58 | ||||

| 59 | ||||

| 60 | ||||

| 62 | ||||

| 69 | ||||

| 69 | ||||

| 69 | ||||

| 70 | ||||

| 70 | ||||

| 70 |

| 70 | ||||

| 70 | ||||

| 71 | ||||

| A-1 | ||||

| B-1 | ||||

| C-1 | ||||

| APPENDIX D: OPTIONAL RETURN OF PURCHASE PAYMENT DEATH BENEFIT EXAMPLES |

D-1 | |||

| E-1 |

3

Accumulation Phase - The period during which you invest money in your Contract, from the Contract Issue Date until the Income Phase begins.

Allocation Account – A Strategy Account Option or the Fixed Account Option.

[Annuity Service Center – Annuity Service Center, P.O. Box 15570, Amarillo, Texas 79105-5570. Telephone Number: (800) 445-7862.]

Annuitant - The person on whose life we base annuity income payments after you begin the Income Phase.

Annuity Date - The date selected by you on which annuity income payments begin.

Beneficiary - The person(s) or non-natural entity(ies) you designate to receive any benefits under the Contract if you or, in the case of a non-natural Owner, the Annuitant dies. If your Contract is jointly owned, you and the joint Owner are each other’s primary Beneficiary.

Buffer – The downside parameter that provides limited protection from negative Index performance. If negative Index performance exceeds the Buffer Rate, your negative Index performance will equal the negative Index Performance in excess of the Buffer Rate. If negative Index performance does not exceed the Buffer Rate, you will not incur a loss.

Buffer Rate – A percentage used to calculate the Index Credit Rate for a Strategy Account Option when the Index Change is negative. For the purposes of this definition, “Buffer Rate” includes the “Lock Buffer Rate.”

Business Day – Each day the New York Stock Exchange (“NYSE”) is open for regular trading. Each Business Day ends when the NYSE closes each day which is typically 4:00 p.m. Eastern Time. If any transaction or event under a Contract is scheduled to occur on a day that is not a Business Day, such transaction or event will be processed using the applicable Index Value and will be deemed to occur on the next following Business Day unless otherwise specified.

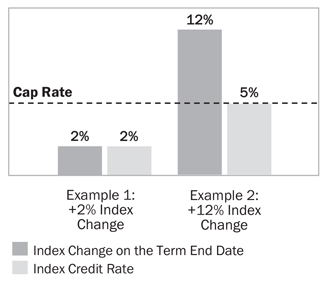

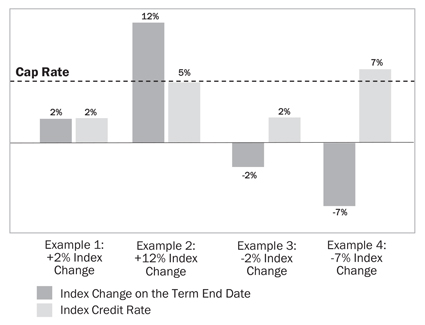

Cap – An Upside Parameter designed to limit your participation in positive Index performance on the Term End Date up to and including the Cap Rate. If you select a Strategy Account Option with a Cap, and the positive Index performance meets or exceeds the Cap Rate, you will receive an Index Credit Rate equal to the Cap Rate.

Cap Rate – A percentage used to calculate the Index Credit Rate if the Index Change is positive on the Term End Date for a Strategy Account Option with a Cap, a Dual Direction with Cap, or a Participation and Cap, as applicable.

Cap Secure – An Upside Parameter designed to limit your participation in positive Index performance up to and including the Cap Secure Rate measured each Contract Anniversary over a multi-year Term. If you select a Strategy Account Option with a Cap Secure, and Index performance on a Contract Anniversary meets or exceeds the Cap Secure Rate, the performance for the Strategy Account Option for that year will be limited to the Cap Secure Rate. While the performance for the Strategy Account Option based on the Cap Secure Rate will be calculated each Contract Anniversary, the Index Credit Rate is not applied until the Term End Date.

Cap Secure Rate – A percentage used to calculate the upside participation if the Index Change is positive measured at each Contract Anniversary over a multi-year Term for a Strategy Account Option with Cap Secure. A Cap Secure Rate is set for the entire multi-year Term and will not change throughout the Term or on any Contract Anniversary.

Cash Value – The total amount that is available for Withdrawal or Surrender. Your Cash Value is equal to the Contract Value after adjustment for any applicable fees and Withdrawal Charges. The Cash Value will never be less than the minimum required by law.

Company – The Variable Annuity Life Insurance Company (“VALIC”), the insurer that issues the Contract. The terms “we,” “us” and “our” are also used to identify the Company.

Continuation Contribution – If the optional Return of Purchase Payment Death Benefit has been elected, an amount by which the death benefit that would have been paid to the spousal Beneficiary upon the death of the original Owner exceeds the Contract Value as of the Good Order date. We will contribute this amount, if any, to the Contract Value upon spousal continuation.

Contract – The [Corebridge RILA] Annuity.

Contract Anniversary – The same date, each subsequent year, as your Contract Issue Date.

Contract Issue Date – The Business Day we issue your Contract. The Contract Issue Date will generally be no later than two (2) Business Days after we receive your Purchase Payment and Contract application in Good Order. Contract Years and Contract Anniversaries are measured from this date.

Contract Value – The total amount attributable to your Contract. The Contract Value is the sum of all amounts invested in the Strategy Account Option(s) as well as the Fixed Account Option. If you invest in the Strategy Account Options, the Interim Value of those accounts will be used when determining your Contract Value on any day that is not a Term Start Date or Term End Date.

4

Contract Year – The 12-month period beginning on the Contract Issue Date and ending on each Contract Anniversary thereafter.

Dual Direction with Cap – An Upside Parameter designed to limit your participation in positive Index performance on the Term End Date up to and including the Cap Rate, or the absolute value of any negative Index performance up to and including the Buffer Rate. The absolute value of a number is simply that number without regard to it being positive or negative. For example, the absolute value of -10 is 10. If the positive Index performance meets or exceeds the Cap Rate, you will receive an Index Credit Rate equal to the Cap Rate. If the absolute value of the negative Index performance exceeds the Buffer Rate, you will receive a negative Index Credit Rate equal to the negative Index performance in excess of the Buffer Rate.

Final Index Value – The Index Value on the Term End Date.

Fixed Account Option Minimum Withdrawal Value – The portion of the Minimum Withdrawal Value attributable to the Fixed Account Option. The Fixed Account Option Minimum Withdrawal Value is equal to the value of the Purchase Payment allocated to the Fixed Account Option multiplied by a percentage based on applicable state law increased proportionally for transfers into the Fixed Account Option and reduced proportionally for any Net Withdrawals or transfers from the Fixed Account Option; accumulated at the minimum non-forfeiture interest rate, which generally ranges from 0.15% to 3.00% depending on applicable state law.

Fixed Account Option – An investment option under the Contract in which you may invest money and earn a fixed rate of return.

Good Order – Fully and accurately completed form(s) and/or instructions as determined by us, including any necessary documentation applicable to any transaction or request received by us.

Income Phase – The period starting upon annuitization during which we make annuity income payments to you.

Index – The reference index to which a Strategy Account Option is linked. Each Index is a price return index, and its performance does not reflect any dividends or distributions paid on the securities comprising the Index.

Index Change – For all Strategy Account Options other than those with the Cap Secure Upside Parameter and Lock Upside Parameter, the percentage change in the Index Value between the Term Start Date and the Term End Date, which is determined by comparing the Index Value on the Term Start Date to the Index Value on the Term End Date.

For Strategy Account Options with Cap Secure Upside Parameter, the percentage change in the Index Value, which is measured by calculating the annual compounded percentage change in Index Value, including Contract Anniversaries during the Term.

For Strategy Account Options with Lock Upside Parameter, the percentage change in the Index Value, which is determined by comparing the Index Value on the Term Start Date and any day during the Term.

Index Credit – For all Strategy Account Options other than those with the Lock Upside Parameter, the dollar amount of gain or loss reflected in your Strategy Account Option Value on the Term End Date.

For Strategy Account Options with Lock Upside Parameter, (i) the dollar amount of gain reflected in your Strategy Account Option Value on the first day during the Term where the Index Change meets or exceeds the Lock Threshold at Market Close, or (ii) if the Index Change does not meet or exceed the Lock Threshold on any day at Market Close on or before the Term End Date, then the dollar amount of gain or loss reflected in your Strategy Account Option Value on the Term End Date.

Index Credit may be positive, negative, or zero.

Index Credit Rate – For all Strategy Account Options other than those with Cap Secure Upside Parameter and Lock Upside Parameter, a percentage gain or loss used to calculate your Strategy Account Option Value on the Term End Date.

For Strategy Account Options with Cap Secure Upside Parameter, a percentage gain or loss used to calculate your Strategy Account Option Value on the Term End Date based on the Index Change on each Contact Anniversary during the Term.

For Strategy Account Options with Lock Upside Parameter, a percentage gain or loss used to calculate your Strategy Account Option Value on any day during the Term.

The Index Credit Rate may be positive, negative, or zero.

Index Value – An Index’s closing market price at the end of the Business Day. The Index Value on any day that is not a Business Day is the value of the Index at the end of the previous Business Day. The Company relies on the Index Values reported by a third-party.

Initial Index Value – The Index Value on the Term Start Date.

5

Interim Value – The value of a Strategy Account Option on any day during the Term other than the Term Start Date or Term End Date. This value is used to determine the amount available in the Strategy Account Option for Withdrawals, Surrenders, annuitization, death benefits and to pay fees and charges during the Term. If you exercise a Performance Capture, the “captured” gain or loss will be based on an Interim Value. The Interim Value is calculated at the end of the Business Day. The Interim Value could be substantially less than the amount invested in the Strategy Account Option and could result in significant loss.

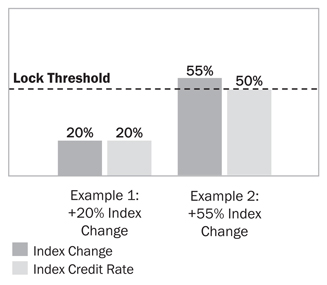

Lock – An Upside Parameter designed to limit your participation in positive Index performance if the Lock Threshold is met at Market Close on any day during the Term. If you select a Strategy Account Option with Lock Upside Parameter and the positive Index Change meets or exceeds the Lock Threshold at Market Close on any day during the Term, you will receive an Index Credit Rate equal to the Lock Threshold as of that date. When that occurs, you will no longer participate in the Index performance, and you will not receive an additional Index Credit Rate on the Term End Date for that Strategy Account Option. After we apply the Index Credit Rate as of the date the Lock Threshold is met, you will be credited with the Lock Fixed Rate until the next Contract Anniversary. If the Index Change does not meet or exceed the Lock Threshold at Market Close on any day during the Term, you will receive an Index Credit Rate equal to the Index Change on the Term End Date, subject to the Buffer.

Lock Buffer Rate – The Buffer Rate associated with a Strategy Account Option with Lock Upside Parameter.

Lock Fixed Rate – For only a Strategy Account Option with Lock Upside Parameter, the Lock Fixed Rate is a short-term fixed rate that is applied to the Strategy Account Option Value from the date the Lock Threshold is met to the next Contract Anniversary.

We may change the Lock Fixed Rate at any time at our discretion, subject to an annual guaranteed minimum interest rate of [•]%.

Lock Threshold – A percentage used as a threshold, and to calculate, the Index Credit Rate if the Index Change meets or exceeds this percentage at Market Close on any day during the Term for a Strategy Account Option with Lock Upside Parameter. If the Index Change does not meet or exceed the Lock Threshold at Market Close on any day during the Term, you will receive an Index Credit Rate equal to the Index Change on the Term End Date, subject to the Buffer.

Latest Annuity Date – The Contract Anniversary following your 95th birthday. The initial annuity income payment will be paid on the first Business Day of the month following the Latest Annuity Date.

Minimum Withdrawal Value – The minimum amount required to be paid to you on Surrender, payment of a death benefit or upon annuitization under the Contract required by applicable state law. The Minimum Withdrawal Value is equal to the Fixed Account Option Minimum Withdrawal Value.

Negative Adjustment – A proportional reduction in your Strategy Base if (i) a fee or charge is deducted from a Strategy Account Option on or before the Term End Date; or (ii) you take a Withdrawal (including, but not limited to, systematic Withdrawals under the Systematic Withdrawal Program, Withdrawals taken to satisfy the required minimum distributions under the Internal Revenue Code, or free Withdrawal amounts) from a Strategy Account Option on or before the Term End Date. A Negative Adjustment could be greater than or less than the amount withdrawn and could significantly reduce your gains (if any) on the Term End Date (because the Index Credit Rate will be applied to a smaller Strategy Base).

Net Purchase Payment – A Purchase Payment that is reduced in the same proportion as the Contract Value is reduced by a Withdrawal on the date of such Withdrawal. Note that this proportional reduction may result in the Net Purchase Payment being reduced by more than the amount withdrawn when the Contract Value is less than the Net Purchase Payment remaining. For example, assume the Contract Value is $15,000, the Net Purchase Payment is $20,000 and a Withdrawal of $6,000 is taken. The Contract Value is reduced by $6,000 which is a 40% reduction. The corresponding deduction to the Net Purchase Payment would be $8,000 (40% x $20,000). A Net Purchase Payment is an on-going calculation. It does not represent a Contract Value.

Net Withdrawals – Withdrawals after adjustment for applicable Withdrawal Charges.

Non-Qualified Contract – A contract purchased with after-tax dollars. In general, these contracts are not under any pension plan, specially sponsored program or individual retirement account (“IRA”).

Owner – The person or entity (if a non-natural Owner) with an interest or title to this Contract. The terms “you” or “your” are also used to identify the Owner.

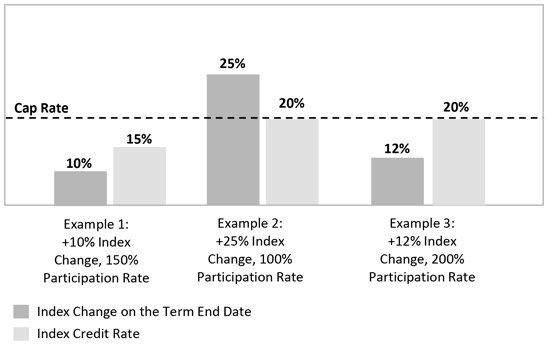

Participation and Cap – An Upside Parameter designed to limit your participation in positive Index performance on the Term End Date at a percentage equal to the Participation Rate and up to and including the Cap Rate. If you select a Strategy Account Option with a Participation and Cap, and the positive Index performance multiplied by the Participation Rate meets or exceeds the Cap Rate, you will receive an Index Credit Rate equal to the Cap Rate.

Participation Rate – A percentage used as part of the calculation of the Index Credit Rate if the Index Change is positive on the Term End Date for a Strategy Account Option with Participation and Cap. The Participation Rate is multiplied by the positive Index performance as part of the calculation of the Index Credit Rate if the Index Change is positive.

6

Performance Capture – Performance Capture is a feature offered for Strategy Account Options other than those with a Lock Upside Parameter that allows you to “capture” the Interim Value of a Strategy Account Option prior to the Term End Date. If you exercise the Performance Capture feature, your Interim Value on the Performance Capture Date will be “captured.” You will not know the Interim Value at the time Performance Capture occurs and you may be “capturing” a loss. The loss may be significant. You should speak with your financial representative before exercising Performance Capture.

The Performance Capture feature is different from the Lock Upside Parameter. Also, the Strategy Account Options for which the Performance Capture feature is available are different from the Strategy Account Options that use Lock as an Upside Parameter.

The table in “Appendix A: Investment Options Available Under the Contract” shows the Strategy Account Options that include Performance Capture as a feature versus the Strategy Account Options that include Lock as an Upside Parameter.

Once Performance Capture occurs, you will no longer participate in Index performance for the remainder of the Term, and you will not receive an Index Credit on the Term End Date for that Strategy Account Option. The “captured” value will then be credited with the Performance Capture Fixed Rate from the Performance Capture Date until the next Contract Anniversary.

You may exercise Performance Capture for one, some, or all of your applicable Strategy Account Options other than a Strategy Account Option with Lock Upside Parameter. You may decide not to exercise a Performance Capture. Performance Capture is not available for a Strategy Account Option with Lock Upside Parameter.

Performance Capture Date – If you exercise the Performance Capture for a Strategy Account Option, the date your Interim Value for that Strategy Account Option is captured.

Performance Capture Fixed Rate – For all Strategy Account Options other than those with Lock Upside Parameter, the Performance Capture Fixed Rate is a short-term fixed rate that is applied to Performance Capture amounts from the Performance Capture Date until the next Contract Anniversary.

We may change the Performance Capture Fixed Rate at any time at our discretion, subject to an annual guaranteed minimum interest rate of [•]%.

Purchase Payment – The money you give us to buy and invest in the Contract.

Qualified Contract – A contract purchased with pretax dollars. These contracts are generally purchased under an IRA.

Renewal Notice – The notification we provide to Owners at least 10 days before the Term End Date (or Contract Anniversary after a Performance Capture or a Lock Threshold is met). Among other information, your Renewal Notice will, as applicable: (i) remind you of your opportunity to decide how your Contract Value should be re-invested; (ii) remind you of the Allocation Accounts that will be available for investment; (iii) provide the current Performance Capture Fixed Rates, Lock Fixed Rates, Fixed Account Option interest rate, Upside Parameter rates and Lock Buffer Rates; and (iv) remind you to submit instructions to us before Market Close on the Term End Date (or the next Contract Anniversary after a Performance Capture or a Lock Threshold is met). If The Term End Date (or the next Contract Anniversary after a Performance Capture or a Lock Threshold is met) is not a Business Day, we must receive your instructions before Market Close on the Business Day before the Term End Date (or the next Contract Anniversary after a Performance Capture or a Lock Threshold is met). “Market Close” is the close of the New York Stock Exchange on Business Days, usually at 4:00 p.m. Eastern Time.

Return of Purchase Payment Death Benefit – The minimum death benefit provided by the optional Return of Purchase Payment Death Benefit, which may be elected, for a fee, at the time you purchase the Contract. The Return of Purchase Payment Death Benefit will equal 100% of the Purchase Payment on the Contract Issue Date. The Return of Purchase Payment Death Benefit will be proportionately reduced by Withdrawals. If the Return of Purchase Payment Death Benefit has been elected, the Return of Purchase Payment Death Benefit is only payable upon the death of the Owner during the Accumulation Phase.

Strategy Account Option – An index-linked investment option under the Contract.

Strategy Account Option Value – The value of your investment in a Strategy Account Option on any day during the Term.

Strategy Base – A value used to calculate Interim Value and Index Credits. The Strategy Base is equal to the Contract Value allocated to a Strategy Account Option on the Term Start Date and (i) reduced proportionally for Withdrawals, fees and charges, if any, deducted from the Strategy Account Option since the Term Start Date; and (ii) increased proportionally to any applicable Interim Value increase at the time of a Continuation Contribution when there is a spousal continuation upon death of Owner.

Surrender – A full Withdrawal of Cash Value and termination of the Contract.

Systematic Withdrawal Program – A program, for no additional charge, available during the Accumulation Phase where you may elect to receive periodic Withdrawals. Under the program, Withdrawals are taken proportionally from your Allocation Accounts, and you may choose to take monthly, quarterly, semi-annual or annual Withdrawals from your Contract. Under this program, if a Withdrawal is scheduled for a day that does not exist in a given calendar month, it will occur on the last day of such month.

7

Term – The duration of an Allocation Account’s investment term, expressed in years. The Term is also the period during which the performance of a Strategy Account Option is linked to the performance of an Index. The Term begins on the Term Start Date and ends on the Term End Date. The Term for a Strategy Account Option may be one, three, or six years.

Term End Date – The Contract Anniversary on the last day of the Term.

Term Start Date – The date the Purchase Payment or Contract Value is allocated to a new Term. The Term Start Date is generally the Contract Issue Date for the initial Term, and a Contract Anniversary for each subsequent Term.

Trigger – An Upside Parameter designed to limit your participation in positive Index performance on the Term End Date equal to the Trigger Rate. If you select a Strategy Account Option with a Trigger, and the Index performance on the Term End Date is greater than or equal to zero, you will receive an Index Credit Rate equal to the Trigger Rate. If Index performance exceeds the Trigger Rate, you will receive an Index Credit Rate equal to the Trigger Rate.

Trigger Rate – A percentage used to calculate the Index Credit Rate if the Index Change is greater than or equal to zero on the Term End Date for a Strategy Account Option with Trigger.

Upside Parameter – A feature of a Strategy Account Option that determines the extent to which a Strategy Account Option will participate in positive Index performance. The Upside Parameters are Cap, Cap Secure, Participation and Cap, Dual Direction with Cap, Trigger and Lock.

Withdrawal – The amount of Contract Value you withdraw from the Contract before adjustment for applicable Withdrawal Charges. A Withdrawal includes, but is not limited to, one-time Withdrawals, systematic Withdrawals under the Systematic Withdrawal Program, Withdrawals taken to satisfy required minimum distributions under the Internal Revenue Code, free withdrawal amounts, and Withdrawals under the Extended Care Waiver or the Terminal Illness Waiver.

Withdrawal Charge Period – The period during which we may apply a Withdrawal Charge to Withdrawals and Surrenders. The Withdrawal Charge Period begins on the Contract Issue Date and ends the day after the last day of the sixth Contract Year.

8

PURPOSE OF THE CONTRACT

The [Corebridge RILA] Annuity is a single purchase payment deferred registered index-linked annuity contract that is designed to help you invest on a tax-deferred basis, meet long-term financial goals, and plan for your retirement. An annuity is a contract between you (the Owner) and an insurance company (in this case, us). This Contract may be appropriate for you if you have a long investment time horizon, and the Contract’s terms and conditions are consistent with your financial goals. It is not intended for people whose liquidity needs require early or frequent withdrawals. There could be significant loss of your principal investment under a Contract. You should discuss with your financial representative whether an index-linked annuity contract is appropriate for you.

The Contract is a “single purchase payment” annuity because only one Purchase Payment is allowed under the Contract. We may agree to accept multiple payments as part of a single Purchase Payment subject to certain limitations outlined in this prospectus. After the Contract is issued, additional Purchase Payments are not allowed.

PHASES OF THE CONTRACT

The Contract has two phases: (1) the Accumulation Phase (savings) and (2) the Income Phase (income). Prior to annuitizing, your Contract is in the Accumulation Phase and the earnings (if any) are generally tax deferred. Tax deferral means you are not taxed until you take money out of your annuity. Once your Contract is annuitized, your annuity switches to the Income Phase, and we promise to pay you an income in the form of annuity income payments. Commencement of these payments is referred to as “annuitizing” your Contract.

Accumulation Phase

During the Accumulation Phase, you may allocate your Purchase Payment to one or more Allocation Accounts. The available Allocations Accounts are (i) Strategy Account Options that credit returns based on the performance of a specific Index or Indices during a Term and (ii) the Fixed Account Option. Additional information about each Strategy Account Option and the Fixed Account Option is provided in an appendix to this prospectus. See “Appendix A: Investment Options Available Under the Contract.” For all Strategy Account Options other than those with the Lock Upside Parameter, we credit positive or negative Index Credit to amounts allocated to a Strategy Account Option on the Term End Date (or, in the case of a Strategy Account Option with the Lock Upside Parameter, when the Index Change meets or exceeds the Lock Threshold at Market Close on any day during the Term) based, in part, on the performance of the applicable Index. You could lose a significant amount of money in a Strategy Account Option if the Index declines in value.

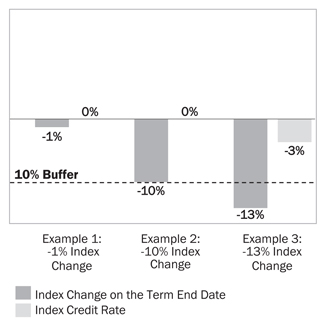

We limit the negative Index Change used in calculating the Index Credit on the Term End Date (or the annual performance on each Contract Anniversary for Strategy Account Options with Cap Secure) by applying the Buffer, which provides a limited level of protection from loss. You will incur a loss if negative Index performance is greater than the Buffer Rate on the Term End Date (and on each Contract Anniversary for Strategy Account Options with Cap Secure). For example, if the Index Change is -15% and your Buffer Rate is 10%, your Index Credit Rate would be -5% (for Strategy Account Options with Cap Secure, the annual measured performance on that Contract Anniversary would be -5% and for Strategy Account Options with Dual Direction with Cap, if the negative Index performance was within or equal to the Buffer Rate, you gain the absolute value of the negative Index performance). The minimum guaranteed Buffer Rate that we offer under any Strategy Account Option other than those with Lock Upside Parameters is [●]%. The minimum guaranteed Lock Buffer Rate that we offer under Strategy Account Options with Lock Upside Parameters is [●]%.

We limit the positive Index Change (or Index Change equal to or greater than zero in the case of the Trigger Upside Parameter) used in calculating the Index Credit on the Term End Date based on the Upside Parameters. The Upside Parameters include:

| • | Cap: Cap limits your participation in positive Index performance on the Term End Date up to and including the Cap Rate. If you select a Strategy Account Option with a Cap, and Index performance exceeds the Cap Rate, you will receive the Cap Rate. For example, if the Index Change is 15% and your Cap Rate is 10%, you will receive an Index Credit Rate of 10% on the Term End Date. The Cap Rate can change from one Term to the next. We will not establish a Cap Rate below [•]%. |

| • | Cap Secure: Cap Secure limits your participation in positive Index performance each Contract Anniversary of a multi-year Term Strategy Account Option up to and including the Cap Secure Rate. The Cap Secure Rate will remain the same for the entire multi-year Term. If you select a Strategy Account Option with a Cap Secure, and Index performance exceeds the Cap Secure Rate in any year, only the Cap Secure Rate will apply for that year . The Index Credit Rate is applied at the Term End Date based upon the values measured on each Contract Anniversary (including the Term End Date). For example, if the annual Index Change is 15% and your Cap Secure Rate is 8%, your adjusted annual Index performance is 8% on that Contract Anniversary. The adjusted annual Index performance on each Contract Anniversary within the multi-year Term would be compounded to establish the Index Credit Rate on the Term End Date. For example, if the adjusted annual Index performance is 5% on each Contract Anniversary for a six-year term, the Index Credit Rate on the Term End Date would be 34.01% ({(1+5%)6}-1=34.01%). The Cap Secure Rate can change from one Term to the next. We will not establish a Cap Secure Rate below [•]%. |

9

| • | Participation and Cap: Participation and Cap limits your participation in positive Index performance on the Term End Date at a percentage equal to the Participation Rate, up to and including the Cap Rate. If Index performance is positive on the Term End Date, first the Participation Rate is multiplied by Index Change. Then, if Index Change multiplied by the Participation Rate exceeds the Cap Rate, you will receive the Cap Rate; otherwise, you will receive Index Credit Rate equal to the Participation Rate multiplied by the Index Change. For example, if the Index Change on the Term End Date is 40% and your Participation Rate is 150% and Cap Rate is 50%, we will first multiply the Participation Rate by the Index Change (150% x 40% = 60%) and then provide you with an Index Credit Rate that is the lesser of the resulting value and the Cap Rate, which in this case would be 50%. The Participation and Cap Rates can change from one Term to the next. On the next Term Start Date, we may choose not to declare a Cap Rate for the next Term. If we do not declare a Cap Rate for a Term, it does not mean that we will not declare a Cap Rate on future Term Start Dates. We will not establish a Participation Rate below [•]% and a Cap Rate below [•]%. |

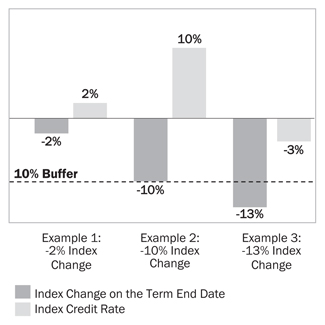

| • | Dual Direction with Cap: Dual Direction with Cap allows you to participate in positive Index performance on the Term End Date up to the Cap Rate, or the absolute value of any negative Index performance up to and including the Buffer Rate. If the positive Index performance exceeds the Cap Rate, your positive Index performance will equal the Cap Rate. For example, if the Index Change is 11% and your Cap Rate is 8%, your Index Credit Rate would be 8%. Since the Index Change was positive, the Buffer would not come into play. If the negative Index performance was within or equal to the Buffer Rate, you gain the absolute value of the negative Index performance. For example, if the Index Change is –10% and your Buffer Rate is 10%, your Index Credit Rate would be 10%. Alternatively, if the Index Change is -13% and your Buffer Rate is 10%, your Index Credit Rate would be -3%. The Cap Rate can change from one Term to the next. We will not establish a Cap Rate below [•]%. |

| • | Trigger: Trigger allows you to receive an Index Credit Rate equal to the Trigger Rate if Index performance is greater than or equal to zero on the Term End Date. If you select a Strategy Account option with a Trigger, and Index performance exceeds the Trigger Rate, you will receive the Trigger Rate. For example, if the Index Change is 2% and the Trigger Rate is 4%, your Index Credit Rate would be 4% because the Index Change was greater than zero. However, if the Index Change is 12% and the Trigger Rate is 4%, your Index Credit Rate would be 4% because the Index Change was greater than the Trigger Rate. The Trigger Rate can change from one Term to the next. We will not establish a Trigger Rate below [•]%. |

| • | Lock: Lock allows you to receive an Index Credit Rate equal to the Lock Threshold as of that date, if the Index Change meets or exceeds the Lock Threshold at Market Close on any day during the Term. For example, if the Lock Threshold is 50% and the Index Change at Market Close on any day during the Term is 50% or greater, you will receive an Index Credit Rate equal to 50%. After we apply the Index Credit Rate, you will be credited with the Lock Fixed Rate until the next Contract Anniversary. If the Index Change does not meet or exceed the Lock Threshold at Market Close on any day during the Term, but is positive on the Term End Date, you will receive an Index Credit Rate equal to the Index Change on the Term End Date. The Lock Threshold for a Strategy Account Option with a Lock Upside Parameter is a guaranteed minimum rate and will not change from one Term to the next. The available Lock Threshold percentages are: [30], [40], [50], [75], and [100]. |

Current Upside Parameter rates will be available from your financial representative and are always available online at [www.corebridgefinancial.com/rila-rates]. The rates applicable to your Purchase Payment will be stated in your Contract.

For all Strategy Account Options other than those with a Lock Upside Parameter, you will receive an Index Credit Rate reflecting a percentage gain or loss on the Term End Date.

For Strategy Account Options with a Lock Upside Parameter, if the Index Change meets or exceeds the Lock Threshold at Market Close on any day during the Term, you will receive an Index Credit Rate equal to the Lock Threshold as of that date, and thereafter will be credited with the Lock Fixed Rate until the next Contract Anniversary. At that point, the value within the Strategy Account Option will no longer be tied to Index performance. If the Index Change does not meet or exceed the Lock Threshold at Market Close on any day during the Term, you will receive an Index Credit Rate reflecting the positive or negative Index performance on the Term End Date, subject to the Buffer.

Fixed Account Option. The Fixed Account Option credits a fixed rate of interest daily that compounds over one year to the annual interest rate we declared for that Term. The initial interest rate for a Purchase Payment allocated to the Fixed Account Option is set on the Contract Issue Date and is guaranteed for a 1-year Term. A new interest rate will be declared before the Term End Date and will be guaranteed for the new Term. We determine the annual interest rates for new Terms at our discretion, subject to a guaranteed minimum interest rate that will never be less than [•]%.

10

Income Phase

When you are ready to receive guaranteed income under the Contract, you can switch to the Income Phase, at which time you will start to receive annuity income payments from us. This is also referred to as “annuitizing” your Contract. You generally decide when to annuitize your Contract, although there are restrictions on the earliest and latest times that your Contract may be annuitized. If you do not annuitize or Surrender your Contract before the Latest Annuity Date, your Contract will be automatically annuitized. Once your Contract is annuitized, you will no longer be able to Surrender, take Withdrawals of Contract Value and all other features and benefits of your Contract, including the death benefit, will terminate. You can choose from the available annuity income options, which may provide income for life, for an available time period, or a combination of both. There is no death benefit during the Income Phase. Annuity income payments may be payable after death if you select a period certain annuity income option.

The Contract offers a standard death benefit as well as an optional death benefit available for an additional charge.

CONTRACT FEATURES

Access to your Money. You may Withdraw all or a portion of your Contract Value at any time before the Annuity Date. However, Withdrawals may be subject to Withdrawal Charges, Negative Adjustments to Interim Value and taxes and tax penalties. Withdrawals will reduce the death benefit, perhaps by more than the amount withdrawn. You should consult with your financial professional about the risks associated with Withdrawals s under the Contract.

Free Withdrawal Amount. There is a free Withdrawal amount under the Contract which allows you to Withdraw a portion of your Contract Value without being subject to a Withdrawal Charge. Each Contract Year, the free Withdrawal amount will be equal to 10% of the previous Contract Anniversary Contract Value (or if withdrawn in the first Contract Year, the Purchase Payment amount) or, if higher, the amount of your required minimum related to this Contract only. The free Withdrawal amount is still subject to Interim Values and a Negative Adjustment if a Withdrawal or other transaction occurs prior to the Term End Date, forfeiture of Index Credit Rates, proportionate reductions to the optional Return of Purchase Payment Death Benefit, taxes, and potential tax penalties.

Performance Capture Feature. The Contract includes a “Performance Capture” feature for certain Strategy Account Options. If available, Performance Capture allows you to “capture” the Interim Value of a Strategy Account Option prior to the Term End Date. The Performance Capture feature may not be available on all Strategy Account Options including those with a Lock Upside Parameter. Once a Performance Capture occurs, the Strategy Account Option will earn an annual rate with daily credited interest at the Performance Capture Fixed Rate until the next Contract Anniversary. There are risks associated with the Performance Capture. Once a Performance Capture occurs, the Interim Value within the Strategy Account Option will no longer be tied to Index performance, and you will not receive an Index Credit Rate on the Term End Date. The captured Interim Value cannot be transferred to a new Allocation Account or a new Term in the same Strategy Account Option until the next Contract Anniversary. You may only exercise the Performance Capture once during a Term on the full amount allocated to an applicable Strategy Account Option, and the exercise is irrevocable. You will not know the Interim Value at the time Performance Capture occurs and you may be “capturing” a loss. The loss may be significant and could be as high as 100%. You should speak with your financial representative before exercising Performance Capture.

Death Benefit. The Contract provides a Contract Value death benefit at no additional charge. The Contract Value death benefit is equal to the greater of the Contract Value or the Minimum Withdrawal Value on the Business Day we receive all required documentation in Good Order.

Optional Return of Purchase Payment Death Benefit. For an additional fee, you may elect the Return of Purchase Payment Death Benefit which can provide greater protection for your Beneficiaries. You may only elect the Return of Purchase Payment Death Benefit at the time you purchase your Contract, and you cannot change your election thereafter at any time. The fee for the Return of Purchase Payment Death Benefit is 0.20% (annually based on remaining Net Purchase Payments). The fee will be deducted proportionally from all Allocation Account Option(s) and charged on each Contract Anniversary. The fee is pro-rated upon death or Surrender. You may pay for the optional Return of Purchase Payment Death Benefit and your Beneficiary may never receive the benefit once you begin the Income Phase. The Return of Purchase Payment Death Benefit can only be elected prior to your 76th birthday.

11

The Return of Purchase Payment Death Benefit is the greatest of:

1. Contract Value less applicable fees associated with the Return of Purchase Payment Death Benefit;

2. Minimum Withdrawal Value; or

3. Net Purchase Payments.

Withdrawals will reduce Net Purchase Payments, and therefore the Return of Purchase Payment Death Benefit, on a proportionate basis, and this reduction could be more than the amount of the Withdrawal.

Extended Care Waiver. We may waive any applicable Withdrawal Charge to partial Withdrawals or Surrenders if, beginning at least one year after the Contract Issue Date, you are receiving extended care in a Qualified Facility for 90 consecutive days or longer. The term “Qualified Facility” is defined in your Contract and means certain Assisted Living Facilities, Hospitals, or Nursing Facilities. This feature is included in the Contract for no additional charge. Withdrawals under this feature are not subject to Withdrawal Charges but may be subject to Negative Adjustments to Interim Value and taxes and tax penalties.

Terminal Illness Waiver. We may waive any applicable Withdrawal Charge to partial Withdrawals or Surrenders if, at any time on and after the Contract Issue Date, you are initially diagnosed as having a Terminal Illness by a Qualified Physician. The term “Terminal Illness” is defined in your Contract and means any disease or medical condition which a Qualified Physician expects will result in death within one year from the date of certification. This feature is included in the Contract for no additional charge. Withdrawals under this feature are not subject to Withdrawal Charges, but may be subject to Negative Adjustments to Interim Value and taxes and tax penalties.

CONTRACT ADJUSTMENTS

If you make any Withdrawals (including required minimum distributions (“RMDs”), Surrenders (including “free look” withdrawals in states that require a refund of Contract Value rather than a refund of the Purchase Payment), and free Withdrawal amounts), exercise the Performance Capture feature, pay optional death benefit fees, annuitize your Contract or a death benefit is paid from a Strategy Account Option on any date prior to the Term End Date, your Contract Value in the Strategy Account Option will be its Interim Value. You could lose a significant amount of money due to the use of the Interim Value if amounts are removed from a Strategy Account Option prior to the Term End Date. Your Interim Value may be less than the amount invested and may be less than the amount you would receive had you held the investment in the Strategy Account Option until the Term End Date. The Interim Value will generally be negatively affected by increases in the expected volatility of index prices, interest rate increases, and by poor market performance. All other factors being equal, the Interim Value would be lower the earlier a Withdrawal or Surrender is made during a Term.

12

IMPORTANT INFORMATION YOU SHOULD CONSIDER ABOUT THE CONTRACT

| FEES, EXPENSES AND ADJUSTMENTS |

LOCATION IN | |||

| Are There Charges or Adjustments for Early Withdrawals? | Yes.

Withdrawal Charges. If you take a Withdrawal from your Contract within six (6) years following the Contract Issue Date, you may be assessed a Withdrawal Charge of up to 8%, as a percentage of the Contract Value withdrawn. For example, if you make a Withdrawal during the Withdrawal Charge Period, you could pay a Withdrawal Charge of up to $8,000 on a $100,000 investment. This loss will be greater if there is a Negative Adjustment based on Interim Values of the Strategy Account Options, taxes or tax penalties.

Interim Value Adjustments. Your Contract Value in a Strategy Account Option will be adjusted to the Interim Value if all or a portion of Contract Value is removed from the Strategy Account Option during the Term. The Interim Value could be less than your investment in a Strategy Account Option even if the Index is performing positively. Under extreme conditions, you could lose up to 100% of your investment in a Strategy Account Option due to Interim Value. For example, if you allocate $100,000 to a Strategy Account Option with a 3-year Term and later withdraw the entire amount before the 3 years have elapsed, you could lose up to $100,000 of your investment. This loss will be greater (but never more than 100%) if you also have to pay a Withdrawal Charge, taxes and tax penalties. All Withdrawals taken, and fees and charges deducted, from a Strategy Account Option before the Term End Date (including fees and charges that are periodically deducted from your Contract) will reduce the Contract Value death benefit on a dollar-for-dollar basis and will trigger a Negative Adjustment which will lower your Strategy Base in the Strategy Account Option in the same proportion that the Interim Value is reduced (rather than on a dollar-for-dollar basis) and which may proportionately reduce the optional Return of Purchase Payment Death Benefit if elected. Such a reduction will reduce your Strategy Base for the remainder of the Term and the proportionate reduction may be greater than the dollar amount withdrawn, or the fee or charge deducted. The following transactions are subject to the Interim Value of Strategy Account Option:

• A fee or charge is deducted from the Strategy Account Option;

• An amount is deducted from the Strategy Account Option due to a Surrender or Withdrawal (including a systematic Withdrawal, RMDs, free Withdrawal amounts or any other Withdrawal);

• The Contract is annuitized; or

• The death benefit is paid;

You may obtain the Interim Value(s) of your Strategy Account Option(s) online at [www.corebridgefinancial.com/annuities] or by contacting your financial representative. |

Fee Table

Fees, Charges and Adjustments | ||

| Are There Transaction Charges? | No. | Not applicable | ||

13

| FEES, EXPENSES AND ADJUSTMENTS |

LOCATION IN | |||

| Are There Ongoing Fees and Expenses? | Yes.

Under the Strategy Account Options, there is an implicit ongoing fee to the extent that your participation in Index gains is limited by our use of an Upside Parameter. This means that your returns may be lower than the Index’s returns. In return for accepting a limit on Index gains, you will receive some protection from Index losses. This implicit ongoing fee is not reflected in the tables below.

The table below describes the fees and expenses that you may pay each year, depending on whether you choose the optional Return of Purchase Payment Death Benefit. Please refer to your Contract for information about the specific fees you will pay each year based on the options you have elected. |

|||

| Annual Fee |

Minimum | Maximum | ||||||

| Optional Return of Purchase Payment Death Benefit available for an additional charge(1) |

0.20 | % | 0.20 | % | ||||

| (1) As a percentage of Net Purchase Payments on each Contract Anniversary. |

| |||||||

| Because your Contract is customizable, the choices you make affect how much you will pay. To help you understand the cost of owning your Contract, the following table shows the lowest and highest cost you could pay each year, based on current charges. This estimate assumes that you do not take withdrawals from the Contract or make any other transactions, which could add Withdrawal Charges and Negative Adjustments for Interim Value that substantially increase costs. |

| Lowest Annual Cost: $0 |

Highest Annual Cost: $200.00 | |

| Assumes:

• Investment of $100,000

• 5% annual appreciation

• No Optional benefits

• No sales charges

• No transfers or withdrawals |

Assumes:

• Investment of $100,000

• 5% annual appreciation

• Optional Return of Purchase Payment Death Benefit

• No sales charges

• No transfers or withdrawals

• No adjustment for Interim Values |

| RISKS |

LOCATION IN | |||

| Is There a Risk of Loss from Poor Performance? | Yes. You could lose money by investing in the Contract. If you invest in a Strategy Account Option, under extreme circumstances, you could lose up to 90% of your investment in a Strategy Account Option with a Buffer Rate of 10% and [•]% of your investment in a Strategy Account Option with a Lock Buffer Rate of [•]% due to negative Index performance. The limits on Index loss offered under the Contract may change from one Term to the next, but we will always offer a Strategy Account Option with an Index Buffer of at least [•]%. | Principal Risks of Investing in the Contract | ||

| Is this a Short-Term Investment? | No. The Contract is not a short-term investment and is not appropriate for an investor who needs ready access to cash because the Contract is designed to provide for the accumulation of retirement savings and income on a long-term basis. As such, you should not use the Contract as a short-term investment or savings vehicle. A Withdrawal Charge may apply in certain circumstances and any Withdrawals may also be subject to federal and state income taxes and tax penalties. Withdrawals from a Strategy Account Option prior to the Term End Date may result in an adjustment for Interim Value. Your Strategy Account Option Value will be transferred on the Term End Date according to your instructions. If we do not receive transfer instructions from you within the appropriate time frame, we will automatically transfer or renew, as applicable, your Strategy Account Option and/or Fixed Account Option Value as follows:

• Any Contract Value in any expiring Strategy Account Option with a 1-year Term will remain in its current allocation for the next Term, subject to the Upside Parameter rates declared for that Term. If your Contract Value is invested in a Strategy Account Option with a 1-year Term that is no longer |

Principal Risks of Investing in the Contract | ||

14

| RISKS |

LOCATION IN | |||

| available for investment, the Contract Value in the expiring Strategy Account Option will automatically be transferred to the Fixed Account Option, subject to the renewal interest rate, and will remain there until you provide transfer instructions. The Contact Value automatically transferred to the Fixed Account Option in the absence of transfer instructions cannot be transferred to another available Strategy Account Option until the next Contract Anniversary.

• Any Contract Value in an expiring Strategy Account Option with a multi-year Term or Fixed Account Option will automatically be transferred or renewed to the Fixed Account Option, subject to the applicable renewal interest rates and will remain there until you provide transfer instructions. The Contract Value automatically renewed or transferred to the Fixed Account Option in the absence of transfer instructions cannot be transferred to a Strategy Account Option until the next Contract Anniversary. |

||||

| What Are the Risks Associated with the Investment Options? | An investment in the Contract is subject to the risk of poor investment performance and can vary depending on the performance of the Indices for the Strategy Account Options under the Contract. Each Allocation Account will have its own unique risks. You should review the Allocation Accounts before making an investment decision.

For investments in a Strategy Account Option, the Cap Rate, Cap Secure Rate, Participation Rate, Trigger Rate or Lock Threshold will limit positive Index performance (e.g., limited upside). For example:

• If the Strategy Account Option has a Cap Rate, and the Index Change is 15% and the Cap Rate is 10%, the Index Credit Rate would be 10% on the Term End Date. [Similarly, if the Participation Rate is 110% and the Cap Rate is 10% with an Index Change of 15%, the Index Credit Rate would be 10% on the Term End Date;]

• If the Strategy Account Option has a Cap Secure Rate, and the annual Index Change is 15%, and the Cap Secure Rate is 8%, the adjusted annual Index performance is 8% on that Contract Anniversary. The adjusted annual Index performance on each Contract Anniversary within the multi- year Term would be compounded to establish the Index Credit Rate on the Term End Date. For example, if the adjusted annual Index performance is 5% on each Contract Anniversary for a 6-year Term, the Index Credit Rate on the Term End Date would be 34.01% ({(1+5%)6}-1=34.01%);

• If the Strategy Account Option has a Participation and Cap Rate, and the Index Change is 10%, the Participation Rate is 100%, and the Cap Rate is [15]%, the Index Credit Rate would be [10]% on the Term End Date;

• If the Strategy Account Option has a Trigger Rate, and the Index Change is greater than or equal to zero (for example, 12%), and the Trigger Rate is 4%, the Index Credit Rate would be 4% on the Term End Date; and |

Principal Risks of Investing in the Contract | ||

|

• If the Strategy Account Option has a Lock Threshold and the Index Change meets or exceeds the Lock Threshold at Market Close on any day during the Term, you will receive an Index Credit Rate equal to the Lock Threshold as of that date. For example, if the Lock Threshold is 50% and the Index Change at Market Close on any day during the Term is 50% or greater, you will receive an Index Credit Rate equal to 50% on that date, even if the Index Change on the Term End Date is 65%.

|

||||

| This may result in you earning less than the Index return.

For investments in a Strategy Account Option, the Buffer will limit negative Index Credit Rates on the Term End Date (e.g., limited protection in the case of market decline). For example:

• If the Index Change is –25% and Buffer Rate is 10%, the Index Credit Rate would be –15% (the amount that the Index Change exceeds the Buffer Rate) on the Term End Date. |

||||

|

Each Index is a price return index, not a total return index, and therefore does not reflect dividends paid on the securities comprising the Index. This will cause the Index return to underperform in comparison to a direct investment in a total return index. |

||||

15

| RISKS |

LOCATION IN | |||

| What Are the Risks Related to the Insurance Company? | An investment in the Contract is subject to the risks related to the Company. The Company is solely responsible to the Owner for the Contract Value and the guaranteed benefits. The general obligations including the Fixed Account Option and Strategy Account Options under the Contract are supported by our general account and are subject to our claims paying ability. An Owner should look solely to our financial strength for our claims-paying ability. More information about the Company, including our financial strength ratings, may be obtained at [https://investors.corebridgefinancial.com/financials/Ratings/default.aspx]. | Principal Risks of Investing in the Contract | ||

| RESTRICTIONS |

LOCATION IN | |||

| Are There Limits on the Investment Options? | Yes.

Transfer Restrictions. Contract Value allocated to a Strategy Account Option may only be transferred on the Term End Date. Contract Value allocated to the Fixed Account Option may not be transferred until the next Contract Anniversary. If you do not want to remain invested in the Fixed Account Option until the next Contract Anniversary, or in a Strategy Account Option until the Term End Date, your only options will be to take a Withdrawal from or Surrender the Contract, or exercise the Performance Capture feature (if available) and transfer your Strategy Account Option Value on the next Contract Anniversary. If you elect one of these options, the transaction will be based on the Interim Values of the Strategy Account Options. The Interim Value could be substantially less than the amount invested in the Strategy Account Option and could result in significant loss. All Withdrawals taken (and fees and charges deducted from your Contract) will reduce your Contract Value death benefit on a dollar-for-dollar basis and will trigger a Negative Adjustment which will lower your Strategy Base in the Strategy Account Option in the same proportion that the Interim Value is reduced (rather than a dollar-for-dollar basis) which may proportionately reduce the optional Return of Purchase Payment Death Benefit if elected. Such a reduction will reduce your Strategy Base for the remainder of the Term and the proportionate reduction may be greater than the dollar amount withdrawn, and the fee or charge deducted. Withdrawals and Surrenders may be subject to Withdrawal Charges, any applicable fees, and taxes (including a 10% Federal tax penalty before age 591⁄2). |

Allocation Accounts Transfers between Allocation Accounts | ||

| Transfer requests must be provided before Market Close on the Term End Date (or Contract Anniversary after a Performance Capture or a Lock Threshold is met). If the Term End Date (or Contract Anniversary after a Performance Capture or a Lock Threshold is met) is not a Business Day, we must receive your instructions before Market Close on the Business Day before the Term End Date (or Contract Anniversary after a Performance Capture or a Lock Threshold is met). | ||||

| Performance Capture Restrictions. Manual Performance Capture is not allowed, and automatic Performance Capture settings cannot be changed, during the five (5) days prior to a Term End Date. Once a Performance Capture occurs, it cannot be revoked. | ||||

| Investment Restrictions.

• Some Strategy Account Options may only be available on the Contract Issue Date. On the Term End Date, you will only be able to invest in the Strategy Account Option(s) available at that time. |

||||

|

• When allocating Contract Value on a Term End Date among the available Allocation Accounts, you may not invest in any Strategy Account Option that has a Term that extends beyond the Latest Annuity Date. If there is no eligible Strategy Account Option, only the Fixed Account Option will be available to you for investment.

|

||||

| • The Company reserves the right to stop offering all but one Strategy Account Option. We will provide you with written notice before adding, replacing, or removing a Strategy Account Option or Index

• Availability of Strategy Account Options and Indices. We reserve the right to add, replace or remove Strategy Account Options offered, change the Indices, and limit the number of offered Strategy Account Options to only one. If only one Strategy Account Option is available, you will be limited to investing in only that Strategy Account Option with terms that may not be acceptable to you. We may change the Strategy Account Options, the Upside Parameters rates, and the Lock Buffer Rates subject to the stated guaranteed minimum rates. There is no guarantee that a particular Strategy Account Option or Index will be available during the entire time that you own your Contract. |

||||

16

| RESTRICTIONS |

LOCATION IN | |||

| Are There Any Restrictions on Contract Benefits? | Yes.

• There are restrictions and limitations relating to benefits offered under the Contract (e.g., death benefit, Performance Capture feature, Extended Care Waiver, Terminal Illness Waiver).

• Except as otherwise provided, Contract benefits may not be modified or terminated by the Company.

• Withdrawals will reduce the death benefit, perhaps by more than the amount withdrawn. |

Death Benefit – Death Benefit Options | ||

| TAXES |

LOCATION IN | |||

| What are the Contract’s Tax Implications? | • You should consult with a tax professional to determine the tax implications of an investment in and payments received under the Contract.

• If you purchase the Contract through an IRA, there is no additional tax benefit under the Contract.

• Earnings under your Contract are taxed at ordinary income tax rates when withdrawn. You may be subject to a tax penalty if you take a Withdrawal before age 591⁄2. |

Taxes | ||

| CONFLICTS OF INTEREST |

LOCATION IN | |||

| How are Investment Professionals Compensated? | Your financial representative may receive compensation for selling this Contract to you in the form of commissions, additional cash compensation, and/or non-cash compensation. We may share the revenue we earn on this Contract with your financial representative’s firm.

Revenue sharing arrangements and commissions may provide selling firms and/or their registered representatives with an incentive to favor sales of our Contracts over other annuity contracts (or other investments) with respect to which a selling firm does not receive the same level of additional compensation. You should ask your financial representative about how they are compensated. |

Payments in Connection with Distribution of the Contract | ||

| Should I Exchange My Contract? | Some financial representatives may have a financial incentive to offer you a new contract in place of the one you already own. You should exchange a contract you already own only if you determine, after comparing the features, fees, and risks of both contracts, that it is better for you to purchase the new contract rather than continue to own your existing contract. | Purchasing a [Corebridge RILA] Annuity – Exchange Offers | ||

The following tables describe the fees, expenses, and adjustments that you will pay when buying, owning, and Surrendering or making Withdrawals from an Allocation Account or from the Contract. Please refer to your contract specifications page for information about the specific fees you will pay each year based on the options you have elected.

The first table describes fees and expenses that you will pay at the time that you buy the Contract, Surrender or make Withdrawals from an Allocation Account or from the Contract, or transfer Contract Value between Allocation Accounts. Charges designed to approximate certain taxes that may be imposed on us, such as premium taxes in your state, may also apply.

| Transaction Expenses |

||||

| Sales Load Imposed on Purchases (as a percentage of purchase payments) |

None | |||

| Withdrawal Charge (as a percentage of the amount withdrawn)(1) |

8.00 | % | ||

| Transfer Fee |

None | |||

| (1) | The Withdrawal Charge is deducted upon a Withdrawal of amounts in excess of the free Withdrawal amount (generally 10% of the previous Contract Anniversary Contract Value). Important exceptions and limitations may eliminate or reduce this charge. For a complete description of charges and exceptions, see “Fees, Charges and Adjustments – Withdrawal Charges” and “Access to Your Money” in the prospectus. |

17

The next table describes the adjustments, in addition to any transaction expenses, that apply if all or a portion of the Contract Value is removed from a Strategy Account Option or from the Contract before the expiration of a specified period.

| Adjustments |

||||

| Maximum Potential Loss Due to Interim Value Adjustment (as a percentage of Contract Value withdrawn from a Strategy Account Option)(1) |

100 | % | ||

| (1) | We use the Interim Values for your Strategy Account Options if you make any Withdrawals (including required minimum distributions (“RMDs”), Surrenders (including “free look” withdrawals in states that require a refund of Contract Value rather than a refund of the Purchase Payment and free Withdrawal amounts), exercise the Performance Capture feature, pay optional death benefit fees, annuitize your Contract or a death benefit is paid from a Strategy Account Option on any date prior to the Term End Date. The maximum loss would occur if there is a total distribution for a Strategy Account Option at a time when the Index Value has declined to zero. If the Interim Value calculation applies to a transaction, the Buffer will not apply. See “Valuing Your Investment in a Strategy Account Option – Interim Values” for more information. |

The next table describes the fees and expenses that you will pay each year during the time that you own the Contract. If you choose to purchase the optional benefit, you will pay additional charges, as shown below.

| Annual Contract Expenses |

||||

| Optional Benefit Expense – Optional Return of Purchase Payment Death Benefit(1) (as a percentage of remaining Net Purchase Payments) |

0.20 | % | ||

| (1) | Charged annually based on remaining Net Purchase Payments. The fee will be deducted proportionally from the Allocation Accounts and charged on each Contract Anniversary. The fee is pro-rated upon death or Surrender. Deduction of the fee from a Strategy Account Option will trigger an Interim Value adjustment and Negative Adjustment. |

In addition to the fee described above, we may limit the amount you can earn on the Strategy Account Options. This means your returns may be lower than the Index’s returns. In return for accepting a limit on Index gains, you will receive some protection from Index losses.

PRINCIPAL RISKS OF INVESTING IN THE CONTRACT

MARKET RISK. An investment in the Contract is subject to the risk of poor investment performance of the Strategy Account Options to which you have allocated Contract Value. You can lose money by investing in this Contract, including loss of principal and/or prior earnings. While limited protection from losses is provided under your Contract through a Buffer, you bear some level of the risk of decline in your Contract Value resulting from the performance of the Indexed Crediting Rate Strategies and the risk of losses may be significant. Under extreme circumstances, you could lose up to 90% of your investment in a Strategy Account Option with a 10% Buffer Rate and up to 80% of your investment in a Strategy Account Option with a 20% Buffer Rate. The minimum guaranteed Buffer Rate that we offer under any Strategy Account Options other than those with Lock Upside Parameter is [●]%, and we will always offer at least one Strategy Account Option. If you take a withdrawal from a Strategy Account Option prior to the Term End Date, it will be based on the Interim Value and the Buffer will not apply. See “Early Withdrawal Risk” below.

This Contract is not a deposit or obligation of, or guaranteed or endorsed by, any bank. This Contract is not federally insured by the federal deposit insurance corporation, the federal reserve board, or any other agency.

EARLY WITHDRAWAL RISK. This Contract is not designed for short-term investing and may not be appropriate for an investor who needs ready access to cash. The benefits of tax deferral and long-term income protections mean that this Contract is more beneficial to investors with a long investment time horizon.

You should carefully consider the risks associated with Withdrawals under the Contract. Withdrawals may be subject to significant Withdrawal Charges. If you make a Withdrawal prior to age 591⁄2, there may be adverse tax consequences, including a 10% Federal tax penalty. A Withdrawal may reduce the value of your standard and optional benefits. For instance, a Withdrawal will reduce the value of the death benefit. A Surrender will result in the termination of your Contract. We may defer payment of Withdrawals or Surrender for up to six months when permitted by law.

If you make a Withdrawal or Surrender your Contract within six years after the Contract Issue Date, you may be assessed a Withdrawal Charge of up to 8% of the amount withdrawn in excess of the 10% annual free Withdrawal amount. In addition, Withdrawals during a Term could result in a greater reduction in your Contract Value than if you waited until the Term End Date. Withdrawals during a Term will proportionately reduce your Strategy Base, which could be significantly more than the dollar amount of your Withdrawal. The application of the Interim Value to Withdrawals taken prior to the Term End Date and proportional reductions to your Strategy Base, together with any Withdrawal Charges, could significantly reduce your Contract Value and reduce any gains on the Term End Date. The Interim Value is the amount in the Strategy Account Option that is available for transactions that occur during the Term, including Withdrawals (including RMDs), Surrenders, Withdrawals under the free look, (in states that require a refund of Contract Value rather than a refund of the Purchase Payment. See “Appendix E: State Variations”), free Withdrawal amounts, Performance Captures, optional death benefit fees, death benefit payments, and annuitization. The Interim Value could be less than your investment in a Strategy Account Option even if

18