Please wait

11238

11503

10399

10000

12543

17.1

13161

10142

10000

10252

14016

10394

10000

1.7

15093

10385

0.2

11998

14497

10581

12645

11015

13277

10945

11269

91.2

10000

10527

11434

0.3

11326

11059

6.7

1.7

10613

10981

10152

11431

12245

0.3

10452

14.9

12161

10415

12271

1.8

13382

14.9

29.1

28.2

29.1

6.7

91.2

10519

17.1

11470

10586

1.8

0.2

11506

11662

11523

11058

28.2

0000924727

false

N-1A

0000924727

imstiii1:BloombergUSAggregateBondIndexMember

2015-09-30

2015-09-30

0000924727

imstiii1:C000243216Member

2015-09-30

2015-09-30

0000924727

imstiii1:C000249814Member

2015-09-30

2015-09-30

0000924727

imstiii1:ConsumerPriceIndexSeasonallyAdjusted100BpsMember

2015-09-30

2015-09-30

0000924727

imstiii1:BloombergUSAggregateBondIndexMember

2015-10-01

2017-09-30

0000924727

imstiii1:C000243216Member

2015-10-01

2017-09-30

0000924727

imstiii1:C000249814Member

2015-10-01

2017-09-30

0000924727

imstiii1:ConsumerPriceIndexSeasonallyAdjusted100BpsMember

2015-10-01

2017-09-30

0000924727

imstiii1:BloombergUSAggregateBondIndexMember

2015-10-01

2018-09-30

0000924727

imstiii1:C000243216Member

2015-10-01

2018-09-30

0000924727

imstiii1:C000249814Member

2015-10-01

2018-09-30

0000924727

imstiii1:ConsumerPriceIndexSeasonallyAdjusted100BpsMember

2015-10-01

2018-09-30

0000924727

imstiii1:BloombergUSAggregateBondIndexMember

2015-10-01

2019-09-30

0000924727

imstiii1:C000243216Member

2015-10-01

2019-09-30

0000924727

imstiii1:C000249814Member

2015-10-01

2019-09-30

0000924727

imstiii1:ConsumerPriceIndexSeasonallyAdjusted100BpsMember

2015-10-01

2019-09-30

0000924727

imstiii1:BloombergUSAggregateBondIndexMember

2015-10-01

2021-09-30

0000924727

imstiii1:C000243216Member

2015-10-01

2021-09-30

0000924727

imstiii1:C000249814Member

2015-10-01

2021-09-30

0000924727

imstiii1:ConsumerPriceIndexSeasonallyAdjusted100BpsMember

2015-10-01

2021-09-30

0000924727

imstiii1:BloombergUSAggregateBondIndexMember

2015-10-01

2022-09-30

0000924727

imstiii1:C000243216Member

2015-10-01

2022-09-30

0000924727

imstiii1:C000249814Member

2015-10-01

2022-09-30

0000924727

imstiii1:ConsumerPriceIndexSeasonallyAdjusted100BpsMember

2015-10-01

2022-09-30

0000924727

imstiii1:BloombergUSAggregateBondIndexMember

2015-10-01

2023-09-30

0000924727

imstiii1:C000243216Member

2015-10-01

2023-09-30

0000924727

imstiii1:C000249814Member

2015-10-01

2023-09-30

0000924727

imstiii1:ConsumerPriceIndexSeasonallyAdjusted100BpsMember

2015-10-01

2023-09-30

0000924727

imstiii1:BloombergUSAggregateBondIndexMember

2015-10-01

2024-09-30

0000924727

imstiii1:C000243216Member

2015-10-01

2024-09-30

0000924727

imstiii1:C000249814Member

2015-10-01

2024-09-30

0000924727

imstiii1:ConsumerPriceIndexSeasonallyAdjusted100BpsMember

2015-10-01

2024-09-30

0000924727

2024-10-01

2025-09-30

0000924727

imstiii1:BloombergUSAggregateBondIndexMember

2015-10-01

2020-09-30

0000924727

imstiii1:C000243216Member

2015-10-01

2020-09-30

0000924727

imstiii1:C000249814Member

2015-10-01

2020-09-30

0000924727

imstiii1:ConsumerPriceIndexSeasonallyAdjusted100BpsMember

2015-10-01

2020-09-30

0000924727

imstiii1:BloombergUSAggregateBondIndexMember

2020-10-01

2025-09-30

0000924727

imstiii1:C000243216Member

2020-10-01 2025-09-30

0000924727

imstiii1:C000249814Member

2020-10-01 2025-09-30

0000924727

imstiii1:ConsumerPriceIndexSeasonallyAdjusted100BpsMember

2020-10-01

2025-09-30

0000924727

imstiii1:BloombergUSAggregateBondIndexMember

2015-10-01

2016-09-30

0000924727

imstiii1:C000243216Member

2015-10-01

2016-09-30

0000924727

imstiii1:C000249814Member

2015-10-01

2016-09-30

0000924727

imstiii1:ConsumerPriceIndexSeasonallyAdjusted100BpsMember

2015-10-01

2016-09-30

0000924727

imstiii1:BloombergUSAggregateBondIndexMember

2024-10-01

2025-09-30

0000924727

imstiii1:C000243216Member

2024-10-01

2025-09-30

0000924727

imstiii1:C000249814Member

2024-10-01 2025-09-30

0000924727

imstiii1:ConsumerPriceIndexSeasonallyAdjusted100BpsMember

2024-10-01

2025-09-30

0000924727

imstiii1:BloombergUSAggregateBondIndexMember

2015-10-01

2025-09-30

0000924727

imstiii1:C000243216Member

2015-10-01

2025-09-30

0000924727

imstiii1:C000249814Member

2015-10-01

2025-09-30

0000924727

imstiii1:ConsumerPriceIndexSeasonallyAdjusted100BpsMember

2015-10-01

2025-09-30

0000924727

imstiii1:C000243216Member

2025-09-30

0000924727

imstiii1:C000243216Member

us-gaap:AssetBackedSecuritiesMember

2025-09-30

0000924727

imstiii1:C000243216Member

imstiii1:BondsAndDebenturesMember

2025-09-30

0000924727

imstiii1:C000243216Member

us-gaap:CommercialMortgageBackedSecuritiesMember

2025-09-30

0000924727

imstiii1:C000243216Member

us-gaap:CommonStockMember

2025-09-30

0000924727

imstiii1:C000243216Member

imstiii1:CorporateBankDebtMember

2025-09-30

0000924727

imstiii1:C000243216Member

us-gaap:CorporateBondSecuritiesMember

2025-09-30

0000924727

imstiii1:C000243216Member

imstiii1:FannieMaePool1000312037Member

2025-09-30

0000924727

imstiii1:C000243216Member

imstiii1:FederalHomeLoanMortgageCorpSeriesK096ClassA225197252029Member

2025-09-30

0000924727

imstiii1:C000243216Member

imstiii1:FordCreditFloorplanMasterOwnerTrustSeries20184ClassA406011152030Member

2025-09-30

0000924727

imstiii1:C000243216Member

imstiii1:FortressCreditOpportunitiesLtdSeries20179AClassA1TR612910152033Member

2025-09-30

0000924727

imstiii1:C000243216Member

imstiii1:OtherAssetsInExcessOfLiabilitiesMember

2025-09-30

0000924727

imstiii1:C000243216Member

imstiii1:PHIGroupIncMember

2025-09-30

0000924727

imstiii1:C000243216Member

us-gaap:ResidentialMortgageBackedSecuritiesMember

2025-09-30

0000924727

imstiii1:C000243216Member

us-gaap:ShortTermInvestmentsMember

2025-09-30

0000924727

imstiii1:C000243216Member

imstiii1:USTreasuryNote36258312030Member

2025-09-30

0000924727

imstiii1:C000243216Member

imstiii1:USTreasuryNote36259302030Member

2025-09-30

0000924727

imstiii1:C000243216Member

imstiii1:USTreasuryNote38756302030Member

2025-09-30

0000924727

imstiii1:C000243216Member

imstiii1:USTreasuryNote46259302030Member

2025-09-30

0000924727

imstiii1:C000243216Member

imstiii1:USTreasuryNotesAndBondsMember

2025-09-30

0000924727

imstiii1:C000243216Member

imstiii1:VerizonMasterTrustSeries20242ClassA483012222031Member

2025-09-30

0000924727

imstiii1:C000249814Member

2025-09-30

0000924727

imstiii1:C000249814Member

us-gaap:AssetBackedSecuritiesMember

2025-09-30

0000924727

imstiii1:C000249814Member

imstiii1:BondsAndDebenturesMember

2025-09-30

0000924727

imstiii1:C000249814Member

us-gaap:CommercialMortgageBackedSecuritiesMember

2025-09-30

0000924727

imstiii1:C000249814Member

us-gaap:CommonStockMember

2025-09-30

0000924727

imstiii1:C000249814Member

imstiii1:CorporateBankDebtMember

2025-09-30

0000924727

imstiii1:C000249814Member

us-gaap:CorporateBondSecuritiesMember

2025-09-30

0000924727

imstiii1:C000249814Member

imstiii1:FannieMaePool1000312037Member

2025-09-30

0000924727

imstiii1:C000249814Member

imstiii1:FederalHomeLoanMortgageCorpSeriesK096ClassA225197252029Member

2025-09-30

0000924727

imstiii1:C000249814Member

imstiii1:FordCreditFloorplanMasterOwnerTrustSeries20184ClassA406011152030Member

2025-09-30

0000924727

imstiii1:C000249814Member

imstiii1:FortressCreditOpportunitiesLtdSeries20179AClassA1TR612910152033Member

2025-09-30

0000924727

imstiii1:C000249814Member

imstiii1:OtherAssetsInExcessOfLiabilitiesMember

2025-09-30

0000924727

imstiii1:C000249814Member

imstiii1:PHIGroupIncMember

2025-09-30

0000924727

imstiii1:C000249814Member

us-gaap:ResidentialMortgageBackedSecuritiesMember

2025-09-30

0000924727

imstiii1:C000249814Member

us-gaap:ShortTermInvestmentsMember

2025-09-30

0000924727

imstiii1:C000249814Member

imstiii1:USTreasuryNote36258312030Member

2025-09-30

0000924727

imstiii1:C000249814Member

imstiii1:USTreasuryNote36259302030Member

2025-09-30

0000924727

imstiii1:C000249814Member

imstiii1:USTreasuryNote38756302030Member

2025-09-30

0000924727

imstiii1:C000249814Member

imstiii1:USTreasuryNote46259302030Member

2025-09-30

0000924727

imstiii1:C000249814Member

imstiii1:USTreasuryNotesAndBondsMember

2025-09-30

0000924727

imstiii1:C000249814Member

imstiii1:VerizonMasterTrustSeries20242ClassA483012222031Member

2025-09-30

iso4217:USDiso4217:USDxbrli:sharesxbrli:purexbrli:sharesutr:Dimstiii1:Holding

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number

Investment Managers Series Trust III

(Exact name of registrant as specified in charter)

235 West Galena Street

Milwaukee, Wisconsin 53212

(Address of Principal Executive Offices, including Zip Code)

Diane J. Drake

Mutual Fund Administration, LLC

2220 E. Route 66, Suite 226

Glendora, California 91740

(Name and Address of Agent for Service)

COPIES TO:

Laurie Anne Dee

Morgan, Lewis & Bockius LLP

600 Anton Boulevard, Suite 1800

Costa Mesa, California 92626

Registrant's telephone number, including area code:

Date of reporting period:

Item 1. Report to Stockholders.

(a) The registrant’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Investment Act”), is as follows:

FPA New Income Fund

Institutional Class/FPNIX

ANNUAL SHAREHOLDER REPORT | September 30, 2025

This annual shareholder report contains important information about the FPA New Income Fund (“Fund”) for the period of October 1, 2024 to September 30, 2025. You can find additional information about the Fund at https://fpa.com/funds/overview/new-income. You can also request this information by contacting us at (800) 638-3060.

Fund Expenses

(Based on a hypothetical $10,000 investment)

| Fund (Class) |

Costs of a $10,000 investment |

Costs paid as a percentage

of a $10,000 investment |

FPA New Income Fund

(Institutional Class/FPNIX) |

$46 |

0.45% |

Management’s Discussion of Fund Performance

How did the Fund perform over the reporting period?

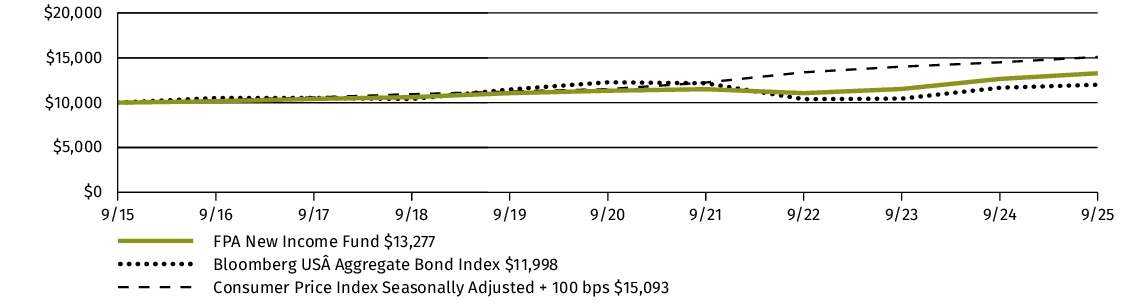

For the twelve-month period ending September 30, 2025, the FPA New Income Fund’s Institutional Class (“Fund”) net return was 5.00%, which includes reinvestment of all distributions.

What affected the Fund’s performance?

During the 12 months ending September 30, 2025, Treasury yields decreased for maturities up to two years, driven by cuts to the Fed Funds rate and expectations of further cuts. Treasury yields for maturities greater than two years increased over the 12 months ending September 30, 2025. Spreads on investment grade and high yield rated debt decreased. Due to low spreads, we largely focused on buying longer-duration, High Quality bonds (rated single-A or higher) we believe will enhance both the Fund’s long-term returns and short-term upside-versus-downside return profile. Over the past 12 months, the Fund’s duration has increased from 3.2 years to 3.3 years. We seek to opportunistically invest in Credit when we believe prices adequately compensate for the risk of permanent impairment of capital and near-term mark-to-market risk. The Fund’s exposure to investments rated BBB or lower decreased as decreasing spreads in that part of the market generally made these investments unattractive.

Fund performance can be attributed to the following:[1]

The largest contributors to performance during the 12 months ending September 30, 2025:

• Agency-guaranteed residential mortgage pools

• Corporates

• Asset-backed securities (ABS) backed by equipment

The only detractor from performance was ABS backed by credit card receivables (part of ABS Other sector). While there were individual investments that detracted from performance during the fiscal year, there were no other meaningful detractors from performance at the sector level.

[1] This information is not a recommendation for a specific security or sector and these securities/sectors may not be in the Fund at the time you receive this report. The information provided does not reflect all positions purchased, sold or recommended by FPA during the quarter. The portfolio holdings as of the most recent quarter-end may be obtained at https://fpa.com. Past performance is no guarantee, nor is it indicative, of future results.

Fund Performance

The following graph and chart compare the initial and subsequent account values at the end of each of the most recently completed 10 fiscal years of the Fund, or for the life of the Fund, if shorter. It assumes a $10,000 initial investment at the beginning of the first fiscal year in an appropriate, broad-based securities market index for the same period.

GROWTH OF $10,000

| AVERAGE ANNUAL TOTAL RETURN |

1 Year |

5 Years |

10 Years |

| FPA New Income Fund (Institutional Class/FPNIX) |

5.00% |

3.23% |

2.88% |

| Bloomberg US Aggregate Bond Index |

2.88% |

-0.45% |

1.84% |

| Consumer Price Index Seasonally Adjusted + 100 bps |

4.11% |

5.58% |

4.20% |

Keep in mind that the Fund’s past performance is not a good predictor of how the Fund will perform in the future.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Visit https://fpa.com/funds/performance/new-income for the most recent performance information.

Key Fund Statistics

The following table outlines key fund statistics that you should pay attention to.

| Fund net assets |

$10,288,577,158 |

| Total number of portfolio holdings |

358 |

| Total advisory fees paid (net) |

$33,443,026 |

| Portfolio turnover rate as of the end of the reporting period |

41% |

Graphical Representation of Holdings

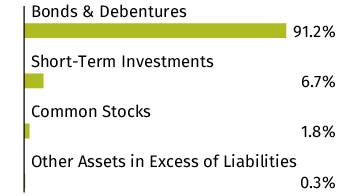

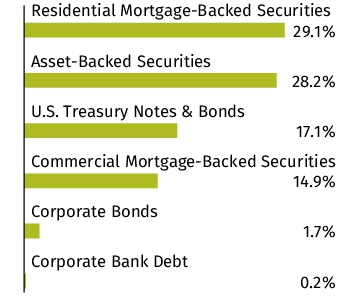

The tables below show the investment makeup of the Fund, representing percentage of the total net assets of the Fund. The Top Ten Holdings and Sector Allocation exclude short-term holdings, if any. The Top Ten Holdings table may not reflect the total exposure to an issuer. Interest rates presented in the Top Ten Holdings are as of the reporting period end. The Sector Allocation chart represents Bonds & Debentures of the Fund.

| U.S. Treasury Note, 3.875%, 6/30/2030 |

11.5% |

| U.S. Treasury Note, 3.625%, 8/31/2030 |

3.1% |

| U.S. Treasury Note, 3.625%, 9/30/2030 |

1.4% |

| PHI Group, Inc. |

1.2% |

| Fortress Credit Opportunities Ltd., Series 2017-9A, Class A1TR, 6.129%, 10/15/2033 |

1.2% |

| Fannie Mae Pool, 1.000%, 3/1/2037 |

1.1% |

| U.S. Treasury Note, 4.625%, 9/30/2030 |

1.1% |

| Verizon Master Trust, Series 2024-2, Class A, 4.830%, 12/22/2031 |

0.8% |

| Federal Home Loan Mortgage Corp., Series K096, Class A2, 2.519%, 7/25/2029 |

0.8% |

| Ford Credit Floorplan Master Owner Trust, Series 2018-4, Class A, 4.060%, 11/15/2030 |

0.8% |

Material Fund Changes

The Fund did not have any material changes that occurred since the beginning of the reporting period.

Changes in and Disagreements with Accountants

There were no changes in or disagreements with the Fund's accountants during the reporting period.

Availability of Additional Information

You can find additional information about the Fund such as the prospectus, financial information, fund holdings and proxy voting information at https://fpa.com/funds/overview/new-income. You can also request this information by contacting us at (800) 638-3060.

Householding

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports and other communication to shareholders with the same residential address, provided they have the same last name, or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call (800) 638-3060 and we will begin sending you separate copies of these materials within 30 days after receiving your request.

FPA New Income Fund - Institutional Class

FPA New Income Fund

Investor Class/FPNRX

ANNUAL SHAREHOLDER REPORT | September 30, 2025

This annual shareholder report contains important information about the FPA New Income Fund (“Fund”) for the period of October 1, 2024 to September 30, 2025. You can find additional information about the Fund at https://fpa.com/funds/overview/new-income. You can also request this information by contacting us at (800) 638-3060.

Fund Expenses

(Based on a hypothetical $10,000 investment)

| Fund (Class) |

Costs of a $10,000 investment |

Costs paid as a percentage

of a $10,000 investment |

FPA New Income Fund

(Investor Class/FPNRX) |

$56 |

0.55% |

Management’s Discussion of Fund Performance

How did the Fund perform over the reporting period?

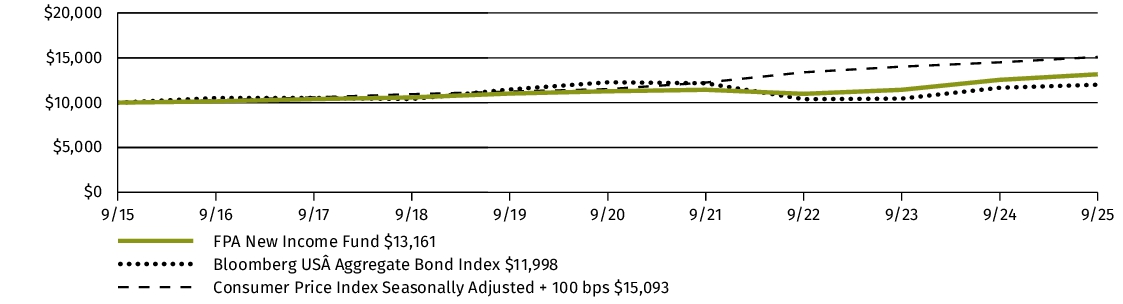

For the twelve-month period ending September 30, 2025, the FPA New Income Fund’s Investor Class (“Fund”) net return was 4.93%, which includes reinvestment of all distributions.

What affected the Fund’s performance?

During the 12 months ending September 30, 2025, Treasury yields decreased for maturities up to two years, driven by cuts to the Fed Funds rate and expectations of further cuts. Treasury yields for maturities greater than two years increased over the 12 months ending September 30, 2025. Spreads on investment grade and high yield rated debt decreased. Due to low spreads, we largely focused on buying longer-duration, High Quality bonds (rated single-A or higher) we believe will enhance both the Fund’s long-term returns and short-term upside-versus-downside return profile. Over the past 12 months, the Fund’s duration has increased from 3.2 years to 3.3 years. We seek to opportunistically invest in Credit when we believe prices adequately compensate for the risk of permanent impairment of capital and near-term mark-to-market risk. The Fund’s exposure to investments rated BBB or lower decreased as decreasing spreads in that part of the market generally made these investments unattractive.

Fund performance can be attributed to the following:[1]

The largest contributors to performance during the 12 months ending September 30, 2025:

• Agency-guaranteed residential mortgage pools

• Corporates

• Asset-backed securities (ABS) backed by equipment

The only detractor from performance was ABS backed by credit card receivables (part of ABS Other sector). While there were individual investments that detracted from performance during the fiscal year, there were no other meaningful detractors from performance at the sector level.

[1] This information is not a recommendation for a specific security or sector and these securities/sectors may not be in the Fund at the time you receive this report. The information provided does not reflect all positions purchased, sold or recommended by FPA during the quarter. The portfolio holdings as of the most recent quarter-end may be obtained at https://fpa.com. Past performance is no guarantee, nor is it indicative, of future results.

Fund Performance

The following graph and chart compare the initial and subsequent account values at the end of each of the most recently completed 10 fiscal years of the Fund, or for the life of the Fund, if shorter. It assumes a $10,000 initial investment at the beginning of the first fiscal year in an appropriate, broad-based securities market index for the same period.

GROWTH OF $10,000

| AVERAGE ANNUAL TOTAL RETURN |

1 Year |

5 Years |

10 Years |

| FPA New Income Fund (Investor Class/FPNRX)1 |

4.93% |

3.15% |

2.79% |

| Bloomberg US Aggregate Bond Index |

2.88% |

-0.45% |

1.84% |

| Consumer Price Index Seasonally Adjusted + 100 bps |

4.11% |

5.58% |

4.20% |

|

1

|

Investor Class commenced operations on April 30, 2024. The performance figures for Investor Class shares include the performance for the Institutional Class shares for the periods prior to the inception date of Investor Class shares, adjusted for the difference in Institutional Class shares and Investor Class shares expenses. Investor Class shares impose higher expenses than Institutional Class shares. Since Investor Class shares have higher expenses and are therefore more expensive than Institutional Class shares, the returns for Investor Class shares will be lower than the returns shown for Institutional Class shares.

|

Keep in mind that the Fund’s past performance is not a good predictor of how the Fund will perform in the future.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Visit https://fpa.com/funds/performance/new-income for the most recent performance information.

Key Fund Statistics

The following table outlines key fund statistics that you should pay attention to.

| Fund net assets |

$10,288,577,158 |

| Total number of portfolio holdings |

358 |

| Total advisory fees paid (net) |

$33,443,026 |

| Portfolio turnover rate as of the end of the reporting period |

41% |

Graphical Representation of Holdings

The tables below show the investment makeup of the Fund, representing percentage of the total net assets of the Fund. The Top Ten Holdings and Sector Allocation exclude short-term holdings, if any. The Top Ten Holdings table may not reflect the total exposure to an issuer. Interest rates presented in the Top Ten Holdings are as of the reporting period end. The Sector Allocation chart represents Bonds & Debentures of the Fund.

| U.S. Treasury Note, 3.875%, 6/30/2030 |

11.5% |

| U.S. Treasury Note, 3.625%, 8/31/2030 |

3.1% |

| U.S. Treasury Note, 3.625%, 9/30/2030 |

1.4% |

| PHI Group, Inc. |

1.2% |

| Fortress Credit Opportunities Ltd., Series 2017-9A, Class A1TR, 6.129%, 10/15/2033 |

1.2% |

| Fannie Mae Pool, 1.000%, 3/1/2037 |

1.1% |

| U.S. Treasury Note, 4.625%, 9/30/2030 |

1.1% |

| Verizon Master Trust, Series 2024-2, Class A, 4.830%, 12/22/2031 |

0.8% |

| Federal Home Loan Mortgage Corp., Series K096, Class A2, 2.519%, 7/25/2029 |

0.8% |

| Ford Credit Floorplan Master Owner Trust, Series 2018-4, Class A, 4.060%, 11/15/2030 |

0.8% |

Material Fund Changes

The Fund did not have any material changes that occurred since the beginning of the reporting period.

Changes in and Disagreements with Accountants

There were no changes in or disagreements with the Fund's accountants during the reporting period.

Availability of Additional Information

You can find additional information about the Fund such as the prospectus, financial information, fund holdings and proxy voting information at https://fpa.com/funds/overview/new-income. You can also request this information by contacting us at (800) 638-3060.

Householding

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports and other communication to shareholders with the same residential address, provided they have the same last name, or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call (800) 638-3060 and we will begin sending you separate copies of these materials within 30 days after receiving your request.

FPA New Income Fund - Investor Class

(b)

Not applicable.

Item

2. Code of Ethics.

The

registrant has adopted a code of ethics that applies to the registrant's principal executive officer and principal financial officer.

The registrant has not made any amendments to its code of ethics during the period covered by this report. The registrant has

not granted any waivers from any provisions of the code of ethics during the period covered by this report.

The

registrant undertakes to provide to any person without charge, upon request, a copy of its code of ethics by mail when they call

the registrant at 1-800-982-4372.

Item

3. Audit Committee Financial Expert.

The

Board of Trustees of the Registrant has determined that John Zader and Sandra Brown, who are members of the Registrant’s

Audit Committee and Board of Trustees, are “audit committee financial experts” and are “independent” as

those terms are defined in this Item.

Item

4. Principal Accountant Fees and Services.

The

registrant has engaged its principal accountant to perform audit services, audit-related services, tax services and other services

during the past two fiscal years. "Audit services" refer to performing an audit of the registrant's annual financial

statements or services that are normally provided by the accountant in connection with statutory and regulatory filings or engagements

for those fiscal years. "Audit-related services" refer to the assurance and related services by the principal accountant

that are reasonably related to the performance of the audit. "Tax services" refer to professional services rendered

by the principal accountant for tax compliance, tax advice, and tax planning. There were no "other services" provided

by the principal accountant. The following table details the aggregate fees billed or expected to be billed for each of the last

two fiscal years for audit fees, audit-related fees, tax fees and other fees by the principal accountant.

| |

FPA

New Income Fund |

FYE

9/30/2025 |

FYE

9/30/2024 |

| (a) |

Audit

Fees |

$14,500 |

$13,500 |

| (b) |

Audit-Related

Fees |

N/A |

N/A |

| (c) |

Tax

Fees |

$2,500 |

$2,500 |

| (d) |

All

Other Fees |

N/A |

N/A |

(e)(1)

The audit committee has adopted pre-approval policies and procedures that require the audit committee to pre-approve all audit

and non-audit services of the registrant, including services provided to any entity affiliated with the registrant.

(e)(2)

The percentage of fees billed by Tait, Weller, & Weller LLP applicable to non-audit services pursuant to waiver of pre-approval

requirement were as follows:

| FPA

New Income Fund |

FYE

9/30/2025 |

FYE

9/30/2024

|

| Audit-Related

Fees |

0% |

0% |

| Tax

Fees |

0% |

0% |

| All

Other Fees |

0% |

0% |

| (f) | All

of the principal accountant's hours spent on auditing the registrant's financial statements

were attributed to work performed by full-time permanent employees of the principal accountant. |

The

following table indicates the non-audit fees billed or expected to be billed by the registrant's accountant for services to the

registrant and to the registrant's investment advisor (and any other controlling entity, etc.—not sub-advisor) for the last

two years. The audit committee of the Board of Trustees has considered whether the provision of non-audit services that were rendered

to the registrant's investment advisor is compatible with maintaining the principal accountant's independence and has concluded

that the provision of such non-audit services by the accountant has not compromised the accountant's independence.

| |

FPA

New Income Fund |

FYE

9/30/2025 |

FYE

9/30/2024

|

| (g) |

Registrant

Non-Audit Related Fees |

N/A |

N/A |

| (h) |

Registrant’s

Investment Advisor |

N/A |

N/A |

Item

5. Audit Committee of Listed Registrants.

| (a) | Not

applicable to registrants who are not listed issuers (as defined in Rule 10A-3 under

the Securities Exchange Act of 1934). |

Item

6. Investments.

| (a) | Schedule

of Investments is included as part of the report to shareholders filed under Item 7 of

this Form. |

Item

7. Financial Statements and Financial Highlights for Open-End Management Investment Companies.

FPA

New Income Fund

(Investor

Class: FPNRX)

(Institutional

Class: FPNIX)

ANNUAL

FINANCIALS AND OTHER INFORMATION

SEPTEMBER

30, 2025

FPA

New Income Fund

A

series of Investment Managers Series Trust III

Table

of Contents

Please

note the Financials and Other Information only contains Items 7-11 required in Form N-CSR. All other required items will be filed

with the SEC.

| Item 7. |

Financial Statements and Financial Highlights |

|

| |

Schedule of Investments |

1 |

| |

Statement of Assets and Liabilities |

15 |

| |

Statement of Operations |

16 |

| |

Statements of Changes in Net Assets |

17 |

| |

Financial Highlights |

18 |

| |

Notes to Financial Statements |

20 |

| |

Report of Independent Registered Public Accounting

Firm |

31 |

This

report and the financial statements contained herein are provided for the general information of the shareholders of the FPA New

Income Fund (the “Fund”). This report is not authorized for distribution to prospective investors in the Fund unless

preceded or accompanied by an effective shareholder report and prospectus.

https://fpa.com

FPA

New Income Fund

SCHEDULE

OF INVESTMENTS

As

of September 30, 2025

Principal

Amount | | |

| |

Value | |

| | | | |

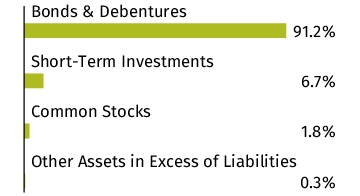

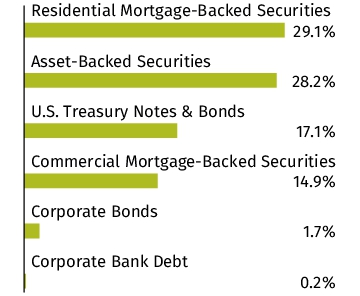

BONDS & DEBENTURES — 91.2% | |

| | |

| | | | |

ASSET-BACKED SECURITIES — 28.2% | |

| | |

| | | | |

AUTO — 6.4% | |

| | |

| | | | |

Ally Auto Receivables Trust | |

| | |

| $ | 8,996,000 | | |

Series 2023-1, Class A4, 5.270%, 11/15/2028 | |

$ | 9,163,599 | |

| | | | |

BMW Vehicle Owner Trust | |

| | |

| | 6,776,000 | | |

Series 2023-A, Class A4, 5.250%, 11/26/2029 | |

| 6,891,115 | |

| | | | |

CarMax Auto Owner Trust | |

| | |

| | 21,176,000 | | |

Series 2023-2, Class A4, 5.010%, 11/15/2028 | |

| 21,429,144 | |

| | 10,892,000 | | |

Series 2023-1, Class A4, 4.650%, 1/16/2029 | |

| 10,966,444 | |

| | 20,637,000 | | |

Series 2023-3, Class A4, 5.260%, 2/15/2029 | |

| 21,019,787 | |

| | | | |

Ford Credit Auto Owner Trust | |

| | |

| | 14,487,000 | | |

Series 2023-A, Class A4, 4.560%, 12/15/2028 | |

| 14,594,378 | |

| | 7,137,000 | | |

Series 2023-B, Class A4, 5.060%, 2/15/2029 | |

| 7,235,828 | |

| | | | |

GM Financial Consumer Automobile Receivables Trust | |

| | |

| | 15,767,000 | | |

Series 2023-1, Class A4, 4.590%, 7/17/2028 | |

| 15,839,848 | |

| | 13,758,000 | | |

Series 2023-3, Class A4, 5.340%, 12/18/2028 | |

| 13,985,930 | |

| | | | |

GM Financial Revolving Receivables Trust | |

| | |

| | 38,305,000 | | |

Series 2021-1, Class A, 1.170%, 6/12/2034(a) | |

| 37,294,951 | |

| | 49,942,000 | | |

Series 2023-1, Class A, 5.120%, 4/11/2035(a) | |

| 51,405,980 | |

| | 12,704,000 | | |

Series 2023-2, Class A, 5.770%, 8/11/2036(a) | |

| 13,317,442 | |

| | 64,237,000 | | |

Series 2024-1, Class A, 4.980%, 12/11/2036(a) | |

| 65,918,044 | |

| | | | |

Hyundai Auto Receivables Trust | |

| | |

| | 10,743,000 | | |

Series 2023-B, Class A4, 5.310%, 8/15/2029 | |

| 10,925,888 | |

| | | | |

Mercedes-Benz Auto Receivables Trust | |

| | |

| | 10,006,000 | | |

Series 2023-1, Class A4, 4.310%, 4/16/2029 | |

| 10,046,709 | |

| | 8,831,000 | | |

Series 2024-1, Class A4, 4.790%, 7/15/2031 | |

| 8,966,606 | |

| | | | |

Nissan Auto Receivables Owner Trust | |

| | |

| | 13,366,000 | | |

Series 2022-B, Class A4, 4.450%, 11/15/2029 | |

| 13,419,197 | |

| | 15,538,000 | | |

Series 2023-A, Class A4, 4.850%, 6/17/2030 | |

| 15,701,673 | |

| | | | |

Porsche Financial Auto Securitization Trust | |

| | |

| | 17,279,000 | | |

Series 2023-1A, Class A4, 4.720%, 6/23/2031(a) | |

| 17,429,763 | |

| | | | |

SFS Auto Receivables Securitization Trust | |

| | |

| | 8,951,000 | | |

Series 2023-1A, Class A4, 5.470%, 12/20/2029(a) | |

| 9,125,319 | |

| | | | |

Toyota Auto Loan Extended Note Trust | |

| | |

| | 54,519,000 | | |

Series 2022-1A, Class A, 3.820%, 4/25/2035(a) | |

| 54,395,951 | |

| | 43,813,000 | | |

Series 2023-1A, Class A, 4.930%, 6/25/2036(a) | |

| 44,828,108 | |

| | 56,286,000 | | |

Series 2024-1A, Class A, 5.160%, 11/25/2036(a) | |

| 58,278,980 | |

| | | | |

Toyota Auto Receivables Owner Trust | |

| | |

| | 16,189,000 | | |

Series 2023-A, Class A4, 4.420%, 8/15/2028 | |

| 16,280,559 | |

| | 19,879,000 | | |

Series 2023-B, Class A4, 4.660%, 9/15/2028 | |

| 20,035,493 | |

| | 25,523,000 | | |

Series 2023-C, Class A4, 5.010%, 2/15/2029 | |

| 25,881,583 | |

| | | | |

Volkswagen Auto Loan Enhanced Trust | |

| | |

| | 11,637,000 | | |

Series 2023-1, Class A4, 5.010%, 1/22/2030 | |

| 11,792,882 | |

| | | | |

World Omni Auto Receivables Trust | |

| | |

| | 14,612,000 | | |

Series 2023-A, Class A4, 4.660%, 5/15/2029 | |

| 14,723,029 | |

FPA

New Income Fund

SCHEDULE

OF INVESTMENTS - Continued

As

of September 30, 2025

Principal

Amount | | |

| |

Value | |

| | | | |

BONDS & DEBENTURES (Continued) | |

| | |

| | | | |

ASSET-BACKED SECURITIES (Continued) | |

| | |

| | | | |

AUTO (Continued) | |

| | |

| $ | 21,627,000 | | |

Series 2023-B, Class A4, 4.680%, 5/15/2029 | |

$ | 21,752,021 | |

| | 10,417,000 | | |

Series 2023-C, Class A4, 5.030%, 11/15/2029 | |

| 10,558,853 | |

| | | | |

| |

| 653,205,104 | |

| | | | |

| |

| | |

| | | | |

COLLATERALIZED LOAN OBLIGATION — 3.1% | |

| | |

| | | | |

Cerberus Loan Funding LLC | |

| | |

| | 10,299,000 | | |

Series 2023-1A, Class A, 6.718% (3-Month Term SOFR+240 basis points), 3/22/2035(a),(b) | |

| 10,308,145 | |

| | 51,840,000 | | |

Series 2023-2A, Class A1, 6.867% (3-Month Term SOFR+255 basis points), 7/15/2035(a),(b) | |

| 52,389,867 | |

| | 52,569,000 | | |

Series 2023-4A, Class A, 6.743% (3-Month Term SOFR+242.5 basis points), 10/15/2035(a),(b) | |

| 53,036,549 | |

| | | | |

Fortress Credit Opportunities Ltd. | |

| | |

| | 118,776,000 | | |

Series 2017-9A, Class A1TR, 6.129% (3-Month Term SOFR+181.161 basis points), 10/15/2033(a),(b) | |

| 119,190,528 | |

| | | | |

Golub Capital Partners Ltd. | |

| | |

| | 43,478,000 | | |

Series 2023-67A, Class A1, 6.726% (3-Month Term SOFR+250 basis points), 5/9/2036(a),(b) | |

| 43,959,041 | |

| | 41,996,000 | | |

Series 2019-46A, Class A1R, 6.135% (3-Month Term SOFR+181 basis points), 4/20/2037(a),(b) | |

| 42,093,095 | |

| | | | |

| |

| 320,977,225 | |

| | | | |

| |

| | |

| | | | |

EQUIPMENT — 10.9% | |

| | |

| | | | |

Avis Budget Rental Car Funding AESOP LLC | |

| | |

| | 4,211,000 | | |

Series 2021-2A, Class A, 1.660%, 2/20/2028(a) | |

| 4,089,847 | |

| | 13,136,000 | | |

Series 2023-1A, Class A, 5.250%, 4/20/2029(a) | |

| 13,437,449 | |

| | 38,251,000 | | |

Series 2023-4A, Class A, 5.490%, 6/20/2029(a) | |

| 39,286,986 | |

| | 48,017,000 | | |

Series 2023-6A, Class A, 5.810%, 12/20/2029(a) | |

| 50,013,240 | |

| | 34,038,000 | | |

Series 2023-8A, Class A, 6.020%, 2/20/2030(a) | |

| 35,725,111 | |

| | 14,768,000 | | |

Series 2024-1A, Class A, 5.360%, 6/20/2030(a) | |

| 15,242,954 | |

| | 57,519,000 | | |

Series 2024-3A, Class A, 5.230%, 12/20/2030(a) | |

| 59,192,032 | |

| | | | |

CNH Equipment Trust | |

| | |

| | 7,414,000 | | |

Series 2022-B, Class A4, 3.910%, 3/15/2028 | |

| 7,402,983 | |

| | 6,738,000 | | |

Series 2023-A, Class A4, 4.770%, 10/15/2030 | |

| 6,831,885 | |

| | 17,009,000 | | |

Series 2023-B, Class A4, 5.460%, 3/17/2031 | |

| 17,608,501 | |

| | | | |

Coinstar Funding LLC | |

| | |

| | 11,767,855 | | |

Series 2017-1A, Class A2, 5.216%, 4/25/2047(a) | |

| 10,961,327 | |

| | | | |

Enterprise Fleet Financing LLC | |

| | |

| | 37,963,000 | | |

Series 2023-2, Class A3, 5.500%, 4/22/2030(a) | |

| 38,644,747 | |

| | 34,823,000 | | |

Series 2023-3, Class A3, 6.410%, 6/20/2030(a) | |

| 36,150,784 | |

| | 11,576,000 | | |

Series 2024-4, Class A4, 4.700%, 6/20/2031(a) | |

| 11,738,939 | |

| | | | |

Ford Credit Floorplan Master Owner Trust | |

| | |

| | 83,977,000 | | |

Series 2018-4, Class A, 4.060%, 11/15/2030 | |

| 83,921,525 | |

FPA

New Income Fund

SCHEDULE

OF INVESTMENTS - Continued

As

of September 30, 2025

Principal

Amount | | |

| |

Value | |

| | | | |

BONDS & DEBENTURES (Continued) | |

| | |

| | | | |

ASSET-BACKED SECURITIES (Continued) | |

| | |

| | | | |

EQUIPMENT (Continued) | |

| | |

| $ | 46,054,000 | | |

Series 2024-2, Class A, 5.240%, 4/15/2031(a) | |

$ | 47,749,524 | |

| | 27,030,000 | | |

Series 2024-4, Class A, 4.400%, 9/15/2031(a) | |

| 27,271,678 | |

| | | | |

GMF Floorplan Owner Revolving Trust | |

| | |

| | 18,848,000 | | |

Series 2023-2, Class A, 5.340%, 6/15/2030(a) | |

| 19,475,490 | |

| | 46,933,000 | | |

Series 2024-2A, Class A, 5.060%, 3/15/2031(a) | |

| 48,393,151 | |

| | | | |

GreatAmerica Leasing Receivables Funding LLC | |

| | |

| | 16,501,000 | | |

Series 2023-1, Class A4, 5.060%, 3/15/2030(a) | |

| 16,752,300 | |

| | | | |

Hertz Vehicle Financing LLC | |

| | |

| | 44,631,000 | | |

Series 2021-2A, Class A, 1.680%, 12/27/2027(a) | |

| 43,484,452 | |

| | 38,642,000 | | |

Series 2022-2A, Class A, 2.330%, 6/26/2028(a) | |

| 37,505,025 | |

| | 72,333,000 | | |

Series 2022-5A, Class A, 3.890%, 9/25/2028(a) | |

| 71,821,758 | |

| | | | |

John Deere Owner Trust | |

| | |

| | 15,675,000 | | |

Series 2023-A, Class A4, 5.010%, 12/17/2029 | |

| 15,823,521 | |

| | 11,706,000 | | |

Series 2023-B, Class A4, 5.110%, 5/15/2030 | |

| 11,882,777 | |

| | 15,742,000 | | |

Series 2023-C, Class A4, 5.390%, 8/15/2030 | |

| 16,079,457 | |

| | | | |

Kubota Credit Owner Trust | |

| | |

| | 12,897,000 | | |

Series 2023-2A, Class A4, 5.230%, 6/15/2028(a) | |

| 13,145,645 | |

| | 9,456,000 | | |

Series 2023-1A, Class A4, 5.070%, 2/15/2029(a) | |

| 9,565,258 | |

| | | | |

M&T Equipment Notes | |

| | |

| | 9,785,000 | | |

Series 2023-1A, Class A4, 5.750%, 7/15/2030(a) | |

| 9,951,055 | |

| | 17,531,000 | | |

Series 2024-1A, Class A4, 4.940%, 8/18/2031(a) | |

| 17,867,097 | |

| | | | |

MMAF Equipment Finance LLC | |

| | |

| | 24,567,000 | | |

Series 2023-A, Class A4, 5.500%, 12/13/2038(a) | |

| 25,225,772 | |

| | 7,081,000 | | |

Series 2020-A, Class A5, 1.560%, 10/9/2042(a) | |

| 6,774,765 | |

| | 29,990,727 | | |

Series 2024-A, Class A4, 5.100%, 7/13/2049(a) | |

| 30,924,146 | |

| | 8,060,000 | | |

Series 2025-A, Class A4, 5.020%, 6/13/2050(a) | |

| 8,334,854 | |

| | | | |

Prop 2017-1A | |

| | |

| | 8,456,940 | | |

5.300%, 3/15/2042(c),(d) | |

| 7,864,954 | |

| | | | |

Verizon Master Trust | |

| | |

| | 76,585,000 | | |

Series 2023-6, Class A, 5.350%, 9/22/2031(a) | |

| 79,448,789 | |

| | 85,708,000 | | |

Series 2024-2, Class A, 4.830%, 12/22/2031(a) | |

| 87,675,204 | |

| | 31,930,000 | | |

Series 2024-7, Class A, 4.350%, 8/20/2032(a) | |

| 32,204,304 | |

| | | | |

Volvo Financial Equipment LLC Series 2025-2 | |

| | |

| | 4,788,000 | | |

Series 2025-2A, Class A4, 4.060%, 6/15/2033(a) | |

| 4,786,796 | |

| | | | |

| |

| 1,120,256,082 | |

| | | | |

| |

| | |

| | | | |

OTHER — 7.8% | |

| | |

| | | | |

ABPCI Direct Lending Fund LLC | |

| | |

| | 21,942,094 | | |

Series 2022-2A, Class A1, 6.414% (3-Month Term SOFR+210 basis points), 3/1/2032(a),(b) | |

| 21,920,920 | |

| | | | |

ABPCI Direct Lending Fund Ltd. | |

| | |

| | 23,371,809 | | |

Series 2020-1A, Class A, 3.199%, 12/29/2030(a) | |

| 22,966,845 | |

FPA

New Income Fund

SCHEDULE

OF INVESTMENTS - Continued

As

of September 30, 2025

Principal

Amount | | |

| |

Value | |

| | | | |

BONDS & DEBENTURES (Continued) | |

| | |

| | | | |

ASSET-BACKED SECURITIES (Continued) | |

| | |

| | | | |

OTHER (Continued) | |

| | |

| | | | |

American Tower Trust 1 | |

| | |

| $ | 77,012,000 | | |

5.490%, 3/15/2028(a) | |

$ | 78,282,929 | |

| | | | |

Brazos Securitization LLC | |

| | |

| | 7,444,560 | | |

5.014%, 9/1/2031(a) | |

| 7,560,201 | |

| | | | |

Centerpoint Energy Restoration Bond Co. II LLC | |

| | |

| | 61,032,000 | | |

4.255%, 12/15/2034 | |

| 60,610,849 | |

| | | | |

Cleco Securitization LLC | |

| | |

| | 16,043,162 | | |

4.016%, 3/1/2031 | |

| 15,906,795 | |

| | | | |

Cologix Data Centers US Issuer LLC | |

| | |

| | 58,068,000 | | |

Series 2021-1A, Class A2, 3.300%, 12/26/2051(a) | |

| 56,674,049 | |

| | | | |

Consumers 2023 Securitization Funding LLC | |

| | |

| | 22,847,000 | | |

5.210%, 9/1/2031 | |

| 23,475,292 | |

| | | | |

DTE Electric Securitization Funding II LLC | |

| | |

| | 24,356,102 | | |

5.970%, 3/1/2033 | |

| 25,634,798 | |

| | | | |

Duke Energy Carolinas Nc Storm Funding II LLC | |

| | |

| | 27,367,000 | | |

4.226%, 7/1/2037 | |

| 27,256,684 | |

| | | | |

Elm Trust | |

| | |

| | 896,870 | | |

Series 2020-3A, Class A2, 2.954%, 8/20/2029(a) | |

| 895,581 | |

| | 1,596,291 | | |

Series 2020-4A, Class A2, 2.286%, 10/20/2029(a) | |

| 1,593,407 | |

| | | | |

Golub Capital Partners Funding Ltd. | |

| | |

| | 9,271,113 | | |

Series 2020-1A, Class A2, 3.208%, 1/22/2029(a) | |

| 9,252,914 | |

| | 30,739,956 | | |

Series 2021-1A, Class A2, 2.773%, 4/20/2029(a) | |

| 30,614,813 | |

| | 51,771,693 | | |

Series 2021-2A, Class A, 2.944%, 10/19/2029(a) | |

| 50,818,472 | |

| | | | |

Kansas Gas Service Securitization I LLC | |

| | |

| | 40,864,198 | | |

5.486%, 8/1/2032 | |

| 42,515,671 | |

| | | | |

Monroe Capital Funding Ltd. | |

| | |

| | 18,822,390 | | |

Series 2021-1A, Class A2, 2.815%, 4/22/2031(a) | |

| 18,674,729 | |

| | | | |

Oklahoma Development Finance Authority | |

| | |

| | 23,653,102 | | |

4.135%, 12/1/2033 | |

| 23,421,870 | |

| | 8,426,999 | | |

4.285%, 2/1/2034 | |

| 8,376,841 | |

| | 19,954,608 | | |

3.877%, 5/1/2037 | |

| 19,284,649 | |

| | | | |

PG&E Recovery Funding LLC | |

| | |

| | 31,252,414 | | |

5.045%, 7/15/2032 | |

| 31,994,658 | |

| | 12,226,552 | | |

4.838%, 6/1/2033 | |

| 12,447,657 | |

| | | | |

PG&E Wildfire Recovery Funding LLC | |

| | |

| | 39,088,202 | | |

4.022%, 6/1/2031 | |

| 38,892,760 | |

| | | | |

SBA Tower Trust | |

| | |

| | 14,427,000 | | |

1.631%, 11/15/2026(a) | |

| 13,967,108 | |

| | 17,196,000 | | |

2.328%, 1/15/2028(a) | |

| 16,341,115 | |

| | 12,423,000 | | |

6.599%, 1/15/2028(a) | |

| 12,722,003 | |

| | | | |

SpringCastle America Funding LLC | |

| | |

| | 7,706,529 | | |

Series 2020-AA, Class A, 1.970%, 9/25/2037(a) | |

| 7,291,839 | |

FPA

New Income Fund

SCHEDULE

OF INVESTMENTS - Continued

As

of September 30, 2025

Principal

Amount | | |

| |

Value | |

| | | | |

BONDS & DEBENTURES (Continued) | |

| | |

| | | | |

ASSET-BACKED SECURITIES (Continued) | |

| | |

| | | | |

OTHER (Continued) | |

| | |

| | | | |

Texas Electric Market Stabilization Funding N LLC | |

| | |

| $ | 29,070,560 | | |

4.265%, 8/1/2036(a) | |

$ | 28,924,472 | |

| | | | |

Texas Natural Gas Securitization Finance Corp. | |

| | |

| | 7,556,544 | | |

5.102%, 4/1/2035 | |

| 7,785,485 | |

| | | | |

VCP RRL Ltd. | |

| | |

| | 19,629,727 | | |

Series 2021-1A, Class A, 2.152%, 10/20/2031(a) | |

| 19,130,033 | |

| | | | |

Virginia Power Fuel Securitization LLC | |

| | |

| | 58,246,000 | | |

4.877%, 5/1/2031 | |

| 59,598,938 | |

| | | | |

WEPCo Environmental Trust Finance LLC | |

| | |

| | 8,310,063 | | |

Series 2021-1, Class A, 1.578%, 12/15/2035 | |

| 7,454,683 | |

| | | | |

| |

| 802,289,060 | |

| | | | |

TOTAL ASSET-BACKED SECURITIES | |

| | |

| | | | |

(Cost $2,848,579,107) | |

| 2,896,727,471 | |

| | | | |

COMMERCIAL MORTGAGE-BACKED SECURITIES — 14.9% | |

| | |

| | | | |

AGENCY — 12.3% | |

| | |

| | | | |

Federal Home Loan Mortgage Corp. | |

| | |

| | 41,061,276 | | |

Series K062, Class A2, 3.413%, 12/25/2026 | |

| 40,771,145 | |

| | 16,539,000 | | |

Series K063, Class A2, 3.430%, 1/25/2027(b) | |

| 16,422,981 | |

| | 9,702,802 | | |

Series K065, Class A2, 3.243%, 4/25/2027 | |

| 9,598,103 | |

| | 7,223,000 | | |

Series K066, Class A2, 3.117%, 6/25/2027 | |

| 7,127,130 | |

| | 8,509,735 | | |

Series K068, Class A2, 3.244%, 8/25/2027 | |

| 8,399,516 | |

| | 12,338,034 | | |

Series K072, Class A2, 3.444%, 12/25/2027 | |

| 12,205,970 | |

| | 29,086,020 | | |

Series K073, Class A2, 3.350%, 1/25/2028 | |

| 28,649,474 | |

| | 16,051,256 | | |

Series K076, Class A2, 3.900%, 4/25/2028 | |

| 16,025,110 | |

| | 4,086,000 | | |

Series K077, Class A2, 3.850%, 5/25/2028(b) | |

| 4,078,115 | |

| | 30,559,000 | | |

Series K079, Class A2, 3.926%, 6/25/2028 | |

| 30,514,051 | |

| | 25,020,308 | | |

Series K080, Class A2, 3.926%, 7/25/2028(b) | |

| 24,977,856 | |

| | 62,664,000 | | |

Series K081, Class A2, 3.900%, 8/25/2028(b) | |

| 62,607,822 | |

| | 46,777,000 | | |

Series K082, Class A2, 3.920%, 9/25/2028(b) | |

| 46,760,623 | |

| | 24,028,000 | | |

Series K083, Class A2, 4.050%, 9/25/2028(b) | |

| 24,143,938 | |

| | 68,841,723 | | |

Series K084, Class A2, 3.780%, 10/25/2028(b) | |

| 68,484,923 | |

| | 27,924,000 | | |

Series K085, Class A2, 4.060%, 10/25/2028(b) | |

| 28,058,345 | |

| | 27,195,714 | | |

Series K089, Class A2, 3.563%, 1/25/2029 | |

| 26,831,683 | |

| | 4,691,000 | | |

Series K088, Class A2, 3.690%, 1/25/2029 | |

| 4,642,935 | |

| | 43,626,000 | | |

Series K090, Class A2, 3.422%, 2/25/2029 | |

| 42,959,264 | |

| | 25,293,822 | | |

Series K091, Class A2, 3.505%, 3/25/2029 | |

| 24,907,026 | |

| | 2,376,000 | | |

Series K092, Class A2, 3.298%, 4/25/2029 | |

| 2,325,806 | |

| | 4,294,004 | | |

Series K093, Class A2, 2.982%, 5/25/2029 | |

| 4,163,331 | |

| | 84,442,000 | | |

Series K095, Class A2, 2.785%, 6/25/2029 | |

| 81,129,281 | |

| | 71,380,000 | | |

Series K094, Class A2, 2.903%, 6/25/2029 | |

| 68,853,648 | |

| | 40,814,000 | | |

Series K097, Class A2, 2.508%, 7/25/2029 | |

| 38,650,270 | |

| | 91,996,000 | | |

Series K096, Class A2, 2.519%, 7/25/2029 | |

| 87,461,968 | |

FPA

New Income Fund

SCHEDULE

OF INVESTMENTS - Continued

As

of September 30, 2025

Principal

Amount | | |

| |

Value | |

| | | | |

COMMERCIAL MORTGAGE-BACKED SECURITIES (Continued) | |

| | |

| | | | |

AGENCY (Continued) | |

| | |

| $ | 19,173,000 | | |

Series K099, Class A2, 2.595%, 9/25/2029 | |

$ | 18,227,253 | |

| | 49,942,000 | | |

Series K101, Class A2, 2.524%, 10/25/2029 | |

| 47,168,846 | |

| | 33,400,000 | | |

Series K102, Class A2, 2.537%, 10/25/2029 | |

| 31,577,085 | |

| | 47,045,000 | | |

Series K103, Class A2, 2.651%, 11/25/2029 | |

| 44,591,415 | |

| | 4,756,000 | | |

Series K107, Class A2, 1.639%, 1/25/2030 | |

| 4,327,476 | |

| | 3,071,000 | | |

Series K105, Class A2, 1.872%, 1/25/2030 | |

| 2,808,064 | |

| | 11,740,000 | | |

Series K106, Class A2, 2.069%, 1/25/2030 | |

| 10,852,060 | |

| | 16,200,000 | | |

Series K104, Class A2, 2.253%, 1/25/2030 | |

| 15,137,403 | |

| | 9,186,000 | | |

Series K108, Class A2, 1.517%, 3/25/2030 | |

| 8,307,414 | |

| | 61,806,000 | | |

Series K751, Class A2, 4.412%, 3/25/2030 | |

| 62,697,138 | |

| | 17,591,000 | | |

Series K109, Class A2, 1.558%, 4/25/2030 | |

| 15,847,297 | |

| | 22,485,000 | | |

Series K151, Class A3, 3.511%, 4/25/2030 | |

| 21,845,219 | |

| | 1,742,000 | | |

Series K111, Class A2, 1.350%, 5/25/2030 | |

| 1,552,607 | |

| | 9,465,000 | | |

Series K114, Class A2, 1.366%, 6/25/2030 | |

| 8,371,884 | |

| | 3,768,000 | | |

Series K116, Class A2, 1.378%, 7/25/2030 | |

| 3,331,594 | |

| | 18,741,000 | | |

Series K752, Class A2, 4.284%, 7/25/2030 | |

| 18,820,074 | |

| | 61,809,000 | | |

Series K117, Class A2, 1.406%, 8/25/2030 | |

| 54,580,079 | |

| | 15,691,000 | | |

Series K120, Class A2, 1.500%, 10/25/2030 | |

| 13,871,680 | |

| | 75,127,967 | | |

Series K754, Class A2, 4.940%, 11/25/2030(b) | |

| 77,682,859 | |

| | | | |

| |

| 1,272,347,761 | |

| | | | |

| |

| | |

| | | | |

AGENCY STRIPPED — 0.3% | |

| | |

| | | | |

Government National Mortgage Association | |

| | |

| | 9,206,316 | | |

Series 2014-77, Class IO, 0.518%, 12/16/2047(b) | |

| 71,643 | |

| | 12,166,009 | | |

Series 2012-150, Class IO, 0.441%, 11/16/2052(b) | |

| 174,740 | |

| | 11,537,327 | | |

Series 2012-114, Class IO, 0.609%, 1/16/2053(b) | |

| 158,339 | |

| | 32,911,833 | | |

Series 2012-125, Class IO, 0.174%, 2/16/2053(b) | |

| 222,003 | |

| | 33,178,332 | | |

Series 2012-79, Class IO, 0.350%, 3/16/2053(b) | |

| 382,616 | |

| | 16,209,046 | | |

Series 2013-45, Class IO, 0.047%, 12/16/2053(b) | |

| 3,209 | |

| | 6,444,852 | | |

Series 2013-125, Class IO, 0.248%, 10/16/2054(b) | |

| 95,941 | |

| | 23,556,494 | | |

Series 2014-157, Class IO, 0.185%, 5/16/2055(b) | |

| 140,017 | |

| | 26,404,164 | | |

Series 2014-153, Class IO, 0.320%, 4/16/2056(b) | |

| 264,865 | |

| | 48,370,919 | | |

Series 2014-175, Class IO, 0.462%, 4/16/2056(b) | |

| 648,712 | |

| | 4,792,608 | | |

Series 2014-138, Class IO, 0.508%, 4/16/2056(b) | |

| 78,808 | |

| | 54,915,992 | | |

Series 2014-187, Class IO, 0.615%, 5/16/2056(b) | |

| 1,173,231 | |

| | 4,439,035 | | |

Series 2015-41, Class IO, 0.159%, 9/16/2056(b) | |

| 22,910 | |

| | 1,346,655 | | |

Series 2015-108, Class IO, 0.340%, 10/16/2056(b) | |

| 7,295 | |

| | 10,954,688 | | |

Series 2014-110, Class IO, 0.099%, 1/16/2057(b) | |

| 48,425 | |

| | 26,448,448 | | |

Series 2015-19, Class IO, 0.293%, 1/16/2057(b) | |

| 343,589 | |

| | 9,800,337 | | |

Series 2015-7, Class IO, 0.488%, 1/16/2057(b) | |

| 190,067 | |

| | 42,815,792 | | |

Series 2015-169, Class IO, 0.248%, 7/16/2057(b) | |

| 424,955 | |

| | 7,294,169 | | |

Series 2015-150, Class IO, 0.366%, 9/16/2057(b) | |

| 110,999 | |

| | 28,937,045 | | |

Series 2016-125, Class IO, 0.814%, 12/16/2057(b) | |

| 978,738 | |

FPA

New Income Fund

SCHEDULE

OF INVESTMENTS - Continued

As

of September 30, 2025

Principal

Amount | | |

| |

Value | |

| | | | |

COMMERCIAL MORTGAGE-BACKED SECURITIES (Continued) | |

| | |

| | | | |

AGENCY STRIPPED (Continued) | |

| | |

| $ | 24,255,861 | | |

Series 2016-65, Class IO, 0.459%, 1/16/2058(b) | |

$ | 515,309 | |

| | 79,774,770 | | |

Series 2016-106, Class IO, 0.969%, 9/16/2058(b) | |

| 3,333,333 | |

| | 38,578,920 | | |

Series 2020-43, Class IO, 1.262%, 11/16/2061(b) | |

| 2,755,415 | |

| | 50,646,017 | | |

Series 2020-71, Class IO, 1.094%, 1/16/2062(b) | |

| 3,219,350 | |

| | 96,462,786 | | |

Series 2020-75, Class IO, 0.870%, 2/16/2062(b) | |

| 5,290,000 | |

| | 121,402,166 | | |

Series 2020-42, Class IO, 0.939%, 3/16/2062(b) | |

| 7,387,686 | |

| | | | |

| |

| 28,042,195 | |

| | | | |

| |

| | |

| | | | |

NON-AGENCY — 2.3% | |

| | |

| | | | |

BBCMS Trust | |

| | |

| | 5,394,741 | | |

Series 2015-SRCH, Class A1, 3.312%, 8/10/2035(a) | |

| 5,301,162 | |

| | 9,736,000 | | |

Series 2025-5C36, Class A3, 5.517%, 8/15/2058 | |

| 10,147,721 | |

| | | | |

Benchmark Mortgage Trust | |

| | |

| | 17,340,000 | | |

Series 2024-V11, Class A3, 5.909%, 11/15/2057(b) | |

| 18,219,216 | |

| | | | |

BMO Mortgage Trust | |

| | |

| | 17,350,000 | | |

Series 2024-5C7, Class A3, 5.566%, 11/15/2057(b) | |

| 17,985,779 | |

| | 8,363,000 | | |

Series 2024-5C8, Class A3, 5.625%, 12/15/2057(b) | |

| 8,703,050 | |

| | | | |

BX Commercial Mortgage Trust | |

| | |

| | 27,999,133 | | |

Series 2021-VOLT, Class E, 6.265% (1-Month Term SOFR+211.448 basis points), 9/15/2036(a),(b) | |

| 27,947,334 | |

| | | | |

Progress Residential Trust | |

| | |

| | 13,308,933 | | |

Series 2024-SFR5, Class A, 3.000%, 8/9/2029(a) | |

| 12,614,138 | |

| | 13,629,642 | | |

Series 2021-SFR11, Class A, 2.283%, 1/17/2039(a) | |

| 12,876,923 | |

| | 47,883,127 | | |

Series 2021-SFR10, Class A, 2.393%, 12/17/2040(a) | |

| 45,237,459 | |

| | 16,051,066 | | |

Series 2024-SFR3, Class A, 3.000%, 6/17/2041(a) | |

| 15,250,466 | |

| | 27,192,216 | | |

Series 2024-SFR4, Class A, 3.100%, 7/17/2041(a) | |

| 25,897,930 | |

| | 21,930,985 | | |

Series 2025-SFR2, Class A, 3.305%, 4/17/2042(a) | |

| 20,851,465 | |

| | 16,479,000 | | |

Series 2025-SFR3, Class A, 3.390%, 7/17/2042(a) | |

| 15,651,789 | |

| | | | |

| |

| 236,684,432 | |

| | | | |

TOTAL COMMERCIAL MORTGAGE-BACKED SECURITIES | |

| | |

| | | | |

(Cost $1,524,324,449) | |

| 1,537,074,388 | |

| | | | |

CORPORATE BANK DEBT — 0.2% | |

| | |

| | | | |

Capstone Acquisition Holdings, Inc. Term Loan | |

| | |

| | 19,168,952 | | |

8.763% (1-Month Term SOFR+460 basis points), 11/12/2029(b),(c),(d),(e) | |

| 19,273,269 | |

| | | | |

JC Penney Corp., Inc. | |

| | |

| | 26,526,226 | | |

5.568% (3-Month USD Libor+425 basis points), 6/23/2027*,(b),(c),(d),(e),(f) | |

| 2,653 | |

| | | | |

Lealand Finance Company B.V. Senior Exit LC | |

| | |

| | 9,783,645 | | |

5.250%, 6/30/2027(c),(d),(e),(g),(h) | |

| (978,365 | ) |

| | | | |

McDermott Technology Americas, Inc. | |

| | |

| | 354,541 | | |

8.278% (1-Month Term SOFR+400 basis points), 12/31/2027(b),(c),(d),(e),(i) | |

| 280,088 | |

| | | | |

TOTAL CORPORATE BANK DEBT | |

| | |

| | | | |

(Cost $19,246,022) | |

| 18,577,645 | |

FPA

New Income Fund

SCHEDULE

OF INVESTMENTS - Continued

As

of September 30, 2025

Principal

Amount | | |

| |

Value | |

| | | | |

CORPORATE BONDS — 1.7% | |

| | |

| | | | |

COMMUNICATIONS — 0.0% | |

| | |

| | | | |

Frontier Communications Holdings LLC | |

| | |

| $ | 5,925,000 | | |

5.875%, 10/15/2027(a) | |

$ | 5,917,594 | |

| | | | |

FINANCIALS — 1.6% | |

| | |

| | | | |

Apollo Debt Solutions BDC Senior Notes | |

| | |

| | 26,023,000 | | |

8.620%, 9/28/2028(c),(d) | |

| 26,023,000 | |

| | | | |

Blue Owl Credit Income Corp. | |

| | |

| | 22,579,000 | | |

7.950%, 6/13/2028 | |

| 24,160,361 | |

| | | | |

Hlend Senior Notes | |

| | |

| | 42,500,000 | | |

8.170%, 3/15/2028(c),(d) | |

| 42,500,000 | |

| | | | |

HPS Corporate Lending Fund | |

| | |

| | 24,864,000 | | |

6.750%, 1/30/2029 | |

| 25,913,472 | |

| | | | |

Oaktree Strategic Credit Fund | |

| | |

| | 27,351,000 | | |

8.400%, 11/14/2028 | |

| 29,700,040 | |

| | | | |

OCREDIT BDC Senior Notes | |

| | |

| | 12,891,000 | | |

7.770%, 3/7/2029(c),(d) | |

| 12,891,000 | |

| | | | |

| |

| 161,187,873 | |

| | | | |

HEALTH CARE — 0.1% | |

| | |

| | | | |

Heartland Dental LLC/Heartland Dental Finance Corp. | |

| | |

| | 8,756,000 | | |

10.500% (1-Month Term SOFR+500 basis points), 4/30/2028(a),(d) | |

| 9,226,635 | |

| | | | |

TOTAL CORPORATE BONDS | |

| | |

| | | | |

(Cost $170,227,525) | |

| 176,332,102 | |

| | | | |

RESIDENTIAL MORTGAGE-BACKED SECURITIES — 29.1% | |

| | |

| | | | |

AGENCY COLLATERALIZED MORTGAGE OBLIGATION — 0.7% | |

| | |

| | | | |

Federal National Mortgage Association | |

| | |

| | 162,466 | | |

Series 2010-43, Class MK, 5.500%, 5/25/2040 | |

| 165,014 | |

| | 5,708,072 | | |

Series 3810, Class PE, 4.000%, 2/15/2041 | |

| 5,542,078 | |

| | 775,669 | | |

Series 2012-144, Class PD, 3.500%, 4/25/2042 | |

| 766,852 | |

| | 434,519 | | |

Series 2013-93, Class PJ, 3.000%, 7/25/2042 | |

| 421,082 | |

| | 56,039,951 | | |

Series 2024-70, Class EC, 3.000%, 11/25/2047 | |

| 52,218,693 | |

| | | | |

GS Mortgage-Backed Securities Trust | |

| | |

| | 15,884,735 | | |

Series 2024-95, Class AB, 2.500%, 6/20/2045(a),(b) | |

| 14,531,592 | |

| | | | |

| |

| 73,645,311 | |

| | | | |

| |

| | |

| | | | |

AGENCY POOL ADJUSTABLE RATE — 1.5% | |

| | |

| | | | |

Fannie Mae Pool | |

| | |

| | 2,726,351 | | |

1.728% (30-Day SOFR Average+211 basis points), 7/1/2051(b) | |

| 2,475,271 | |

| | 23,088,566 | | |

1.970% (30-Day SOFR Average+207.4 basis points), 8/1/2051(b) | |

| 21,125,880 | |

| | 1,849,650 | | |

1.604% (30-Day SOFR Average+209.4 basis points), 9/1/2051(b) | |

| 1,668,746 | |

| | 21,281,666 | | |

1.888% (30-Day SOFR Average+233.4 basis points), 4/1/2052(b) | |

| 19,307,236 | |

| | | | |

Freddie Mac Non Gold Pool | |

| | |

| | 8,739,399 | | |

1.662% (30-Day SOFR Average+213 basis points), 9/1/2051(b) | |

| 7,895,132 | |

| | 10,623,064 | | |

2.556% (30-Day SOFR Average+213 basis points), 3/1/2052(b) | |

| 9,831,621 | |

| | 7,493,785 | | |

2.545% (30-Day SOFR Average+214 basis points), 5/1/2052(b) | |

| 6,946,199 | |

FPA

New Income Fund

SCHEDULE

OF INVESTMENTS - Continued

As

of September 30, 2025

Principal

Amount | | |

| |

Value | |

| | | | |

RESIDENTIAL MORTGAGE-BACKED SECURITIES (Continued) | |

| | |

| | | | |

AGENCY POOL ADJUSTABLE RATE (Continued) | |

| | |

| $ | 74,031,638 | | |

2.158% (30-Day SOFR Average+217.8 basis points), 7/1/2052(b) | |

$ | 67,507,577 | |

| | 9,049,402 | | |

3.334% (30-Day SOFR Average+222.4 basis points), 11/1/2052(b) | |

| 8,659,580 | |

| | 10,916,651 | | |

2.164% (30-Day SOFR Average+217.9 basis points), 5/1/2053(b) | |

| 9,956,551 | |

| | | | |

| |

| 155,373,793 | |

| | | | |

| |

| | |

| | | | |

AGENCY POOL FIXED RATE — 20.5% | |

| | |

| | | | |

Fannie Mae Pool | |

| | |

| | 65,832,876 | | |

1.500%, 12/1/2035 | |

| 59,195,269 | |

| | 13,155,706 | | |

1.500%, 12/1/2035 | |

| 11,800,503 | |

| | 1,918,162 | | |

1.500%, 3/1/2036 | |

| 1,721,766 | |

| | 15,012,292 | | |

1.000%, 4/1/2036 | |

| 13,060,210 | |

| | 4,913,996 | | |

1.500%, 4/1/2036 | |

| 4,410,864 | |

| | 15,957,741 | | |

1.500%, 4/1/2036 | |

| 14,323,867 | |

| | 11,595,845 | | |

1.500%, 5/1/2036 | |

| 10,408,574 | |

| | 25,349,730 | | |

1.500%, 6/1/2036 | |

| 22,754,232 | |

| | 5,560,014 | | |

1.500%, 6/1/2036 | |

| 4,990,738 | |

| | 9,853,759 | | |

1.500%, 7/1/2036 | |

| 8,844,856 | |

| | 89,192,729 | | |

1.500%, 8/1/2036 | |

| 80,199,863 | |

| | 6,434,393 | | |

1.500%, 8/1/2036 | |

| 5,769,559 | |

| | 23,313,868 | | |

1.000%, 9/1/2036 | |

| 20,218,642 | |

| | 11,124,941 | | |

1.500%, 9/1/2036 | |

| 9,975,455 | |

| | 26,625,599 | | |

1.500%, 10/1/2036 | |

| 23,874,506 | |

| | 14,355,977 | | |

1.000%, 11/1/2036 | |

| 12,396,145 | |

| | 93,119,099 | | |

1.000%, 12/1/2036 | |

| 80,408,091 | |

| | 131,244,147 | | |

1.000%, 3/1/2037 | |

| 113,328,967 | |

| | 59,151,090 | | |

1.500%, 3/1/2037 | |

| 53,094,752 | |

| | 44,493,259 | | |

1.500%, 8/1/2037 | |

| 39,868,180 | |

| | 11,294,775 | | |

2.000%, 6/1/2040 | |

| 9,908,559 | |

| | 4,212,051 | | |

2.000%, 9/1/2040 | |

| 3,689,120 | |

| | 4,571,743 | | |

2.000%, 10/1/2040 | |

| 4,002,201 | |

| | 13,294,691 | | |

2.000%, 10/1/2040 | |

| 11,642,154 | |

| | 3,317,424 | | |

1.500%, 11/1/2040 | |

| 2,809,472 | |

| | 21,793,159 | | |

2.000%, 11/1/2040 | |

| 19,067,162 | |

| | 13,687,111 | | |

1.500%, 12/1/2040 | |

| 11,582,373 | |

| | 16,365,672 | | |

2.000%, 12/1/2040 | |

| 14,308,974 | |

| | 4,683,970 | | |

1.500%, 1/1/2041 | |

| 3,960,725 | |

| | 13,012,255 | | |

1.500%, 2/1/2041 | |

| 10,994,546 | |

| | 15,166,819 | | |

1.500%, 5/1/2041 | |

| 12,773,251 | |

| | 14,489,855 | | |

2.500%, 5/1/2041 | |

| 12,997,855 | |

| | 8,779,962 | | |

2.000%, 7/1/2041 | |

| 7,641,109 | |

| | 59,562,857 | | |

2.000%, 9/1/2041 | |

| 52,099,250 | |

| | 58,008,725 | | |

1.500%, 10/1/2041 | |

| 48,651,540 | |

| | 85,988,241 | | |

1.500%, 11/1/2041 | |

| 72,069,470 | |

FPA

New Income Fund

SCHEDULE

OF INVESTMENTS - Continued

As

of September 30, 2025

Principal

Amount | | |

| |

Value | |

| | | | |

RESIDENTIAL MORTGAGE-BACKED SECURITIES (Continued) | |

| | |

| | | | |

AGENCY POOL FIXED RATE (Continued) | |

| | |

| $ | 6,275,078 | | |

1.500%, 12/1/2041 | |

$ | 5,255,428 | |

| | 5,803,688 | | |

1.500%, 3/1/2042 | |

| 4,867,329 | |

| | 18,488,064 | | |

1.500%, 3/1/2042 | |

| 15,621,142 | |

| | 28,808,470 | | |

1.500%, 3/1/2042 | |

| 24,199,221 | |

| | 42,825,645 | | |

1.500%, 3/1/2042 | |

| 35,976,865 | |

| | 51,950,048 | | |

1.500%, 3/1/2042 | |

| 43,564,406 | |

| | 20,605,793 | | |

2.000%, 8/1/2042 | |

| 17,893,653 | |

| | 57,647,194 | | |

2.000%, 8/1/2042 | |

| 49,882,578 | |

| | 29,012,253 | | |

3.500%, 4/1/2044 | |

| 27,372,645 | |

| | 38,614,353 | | |

4.000%, 6/1/2045 | |

| 37,725,620 | |

| | 67,097,350 | | |

4.000%, 3/1/2046 | |

| 65,574,200 | |

| | 8,249,818 | | |

4.000%, 7/1/2046 | |

| 8,055,586 | |

| | 9,525,465 | | |

4.000%, 10/1/2046 | |

| 9,300,414 | |

| | 5,233,554 | | |

4.000%, 10/1/2046 | |

| 5,113,210 | |

| | 7,917,341 | | |

4.000%, 3/1/2048 | |

| 7,724,312 | |

| | 34,138,705 | | |

4.500%, 1/1/2050 | |

| 34,191,756 | |

| | 30,233,454 | | |

4.500%, 1/1/2050 | |

| 30,283,373 | |

| | | | |

Freddie Mac Pool | |

| | |

| | 269,639 | | |

2.500%, 8/1/2028 | |

| 264,749 | |

| | 87,831,420 | | |

1.500%, 11/1/2035 | |

| 79,167,940 | |

| | 6,470,252 | | |

1.500%, 11/1/2035 | |

| 5,803,735 | |

| | 22,986,616 | | |

1.500%, 1/1/2036 | |

| 20,646,576 | |

| | 2,956,170 | | |

1.500%, 4/1/2036 | |

| 2,653,495 | |

| | 4,884,879 | | |

1.500%, 5/1/2036 | |

| 4,384,728 | |

| | 14,638,595 | | |

1.500%, 6/1/2036 | |

| 13,107,763 | |

| | 5,795,972 | | |

1.000%, 7/1/2036 | |

| 5,020,778 | |

| | 26,444,996 | | |

1.500%, 8/1/2036 | |

| 23,712,564 | |

| | 8,737,568 | | |

1.000%, 10/1/2036 | |

| 7,592,895 | |

| | 19,602,320 | | |

1.500%, 10/1/2036 | |

| 17,576,908 | |

| | 59,207,728 | | |

1.500%, 10/1/2036 | |

| 53,145,591 | |

| | 5,796,833 | | |

1.500%, 11/1/2036 | |

| 5,212,366 | |

| | 18,009,774 | | |

2.000%, 6/1/2040 | |

| 15,800,661 | |

| | 3,947,841 | | |

2.000%, 8/1/2040 | |

| 3,459,297 | |

| | 2,813,021 | | |

4.000%, 10/1/2040 | |

| 2,750,371 | |

| | 10,375,973 | | |

1.500%, 11/1/2040 | |

| 8,794,631 | |

| | 2,546,442 | | |

4.000%, 11/1/2040 | |

| 2,490,611 | |

| | 5,878,355 | | |

2.000%, 12/1/2040 | |

| 5,139,155 | |

| | 4,055,335 | | |

4.000%, 12/1/2040 | |

| 3,962,487 | |

| | 3,885,313 | | |

1.500%, 2/1/2041 | |

| 3,287,899 | |

| | 32,775,375 | | |

1.500%, 3/1/2041 | |

| 27,657,104 | |

| | 86,649,151 | | |

1.500%, 3/1/2041 | |

| 73,210,847 | |

| | 24,556,878 | | |

1.500%, 4/1/2041 | |

| 20,706,065 | |

| | 76,011,475 | | |

1.500%, 5/1/2041 | |

| 64,053,350 | |

FPA

New Income Fund

SCHEDULE

OF INVESTMENTS - Continued

As

of September 30, 2025

Principal

Amount | | |

| |

Value | |

| | | | |

RESIDENTIAL MORTGAGE-BACKED SECURITIES (Continued) | |

| | |

| | | | |

AGENCY POOL FIXED RATE (Continued) | |

| | |

| $ | 70,664,049 | | |

1.500%, 6/1/2041 | |

$ | 59,496,840 | |

| | 10,692,058 | | |

1.500%, 7/1/2041 | |

| 8,993,580 | |

| | 6,805,508 | | |

2.000%, 8/1/2041 | |

| 5,916,132 | |

| | 11,274,571 | | |

1.500%, 10/1/2041 | |

| 9,455,989 | |

| | 4,132,720 | | |

1.500%, 11/1/2041 | |

| 3,482,124 | |

| | 16,534,923 | | |

1.500%, 11/1/2041 | |

| 13,858,683 | |

| | 63,602,337 | | |

1.500%, 12/1/2041 | |

| 53,275,804 | |

| | 30,493,669 | | |

1.500%, 12/1/2041 | |

| 25,731,610 | |

| | 5,113,995 | | |

1.500%, 1/1/2042 | |

| 4,298,856 | |

| | 35,909,359 | | |

1.500%, 1/1/2042 | |

| 30,141,706 | |

| | 36,899,467 | | |

2.000%, 5/1/2042 | |

| 32,041,379 | |

| | 25,092,859 | | |

2.000%, 8/1/2042 | |

| 21,777,126 | |

| | 18,577,515 | | |

2.000%, 8/1/2042 | |

| 16,162,047 | |

| | 42,811,843 | | |

4.500%, 12/1/2045 | |

| 42,882,696 | |

| | | | |

| |

| 2,108,561,676 | |

| | | | |

| |

| | |

| | | | |

NON-AGENCY COLLATERALIZED MORTGAGE OBLIGATION — 6.4% | |

| | |

| | | | |

Citigroup Mortgage Loan Trust | |

| | |

| | 1,634,246 | | |

Series 2014-A, Class A, 4.000%, 1/25/2035(a),(b) | |

| 1,603,161 | |

| | | | |

GS Mortgage-Backed Securities Trust | |

| | |

| | 8,456,150 | | |

Series 2021-PJ4, Class A8, 2.500%, 9/25/2051(a),(b) | |

| 7,591,488 | |

| | 33,142,284 | | |

Series 2021-PJ5, Class A8, 2.500%, 10/25/2051(a),(b) | |

| 29,726,793 | |

| | 35,999,670 | | |

Series 2021-PJ6, Class A8, 2.500%, 11/25/2051(a),(b) | |

| 32,226,527 | |

| | 28,784,395 | | |

Series 2021-PJ7, Class A8, 2.500%, 1/25/2052(a),(b) | |

| 25,713,396 | |

| | 9,785,088 | | |

Series 2021-PJ10, Class A8, 2.500%, 3/25/2052(a),(b) | |

| 8,726,031 | |

| | 6,149,418 | | |

Series 2022-PJ1, Class A8, 2.500%, 5/28/2052(a),(b) | |

| 5,462,317 | |

| | 13,460,659 | | |

Series 2022-PJ2, Class A24, 3.000%, 6/25/2052(a),(b) | |

| 12,267,043 | |

| | 10,290,122 | | |

Series 2022-PJ3, Class A22, 2.500%, 8/25/2052(a),(b) | |

| 9,158,996 | |

| | 5,318,919 | | |

Series 2022-PJ3, Class A24, 3.000%, 8/25/2052(a),(b) | |

| 4,842,142 | |

| | 33,830,234 | | |

Series 2022-PJ4, Class A22, 2.500%, 9/25/2052(a),(b) | |

| 30,050,102 | |

| | 6,319,429 | | |

Series 2022-PJ4, Class A24, 3.000%, 9/25/2052(a),(b) | |

| 5,743,434 | |

| | 77,034,793 | | |

Series 2022-PJ5, Class A22, 2.500%, 10/25/2052(a),(b) | |

| 68,223,168 | |

| | 49,683,283 | | |

Series 2022-PJ6, Class A15, 2.500%, 1/25/2053(a),(b) | |

| 44,025,390 | |

| | | | |

J.P. Morgan Mortgage Trust | |

| | |

| | 4,966,883 | | |

Series 2021-6, Class A4, 2.500%, 10/25/2051(a),(b) | |

| 4,464,831 | |

| | 10,653,789 | | |

Series 2021-7, Class A4, 2.500%, 11/25/2051(a),(b) | |

| 9,566,662 | |

| | 15,654,256 | | |

Series 2021-10, Class A4A, 2.000%, 12/25/2051(a),(b) | |

| 13,687,787 | |

| | 42,085,210 | | |

Series 2021-10, Class A4, 2.500%, 12/25/2051(a),(b) | |

| 37,624,278 | |

| | 11,400,493 | | |

Series 2021-8, Class A4, 2.500%, 12/25/2051(a),(b) | |

| 10,231,705 | |

| | 52,565,230 | | |

Series 2021-11, Class A4, 2.500%, 1/25/2052(a),(b) | |

| 47,110,368 | |

| | 58,014,547 | | |

Series 2021-13, Class A4, 2.500%, 4/25/2052(a),(b) | |

| 52,104,814 | |

| | 3,297,015 | | |

Series 2021-15, Class A4, 2.500%, 6/25/2052(a),(b) | |

| 2,941,864 | |

| | 3,070,457 | | |

Series 2022-3, Class A4A, 2.500%, 8/25/2052(a),(b) | |

| 2,730,389 | |

FPA

New Income Fund

SCHEDULE

OF INVESTMENTS - Continued

As

of September 30, 2025

Principal

Amount | | |

| |

Value | |

| | | | |

RESIDENTIAL MORTGAGE-BACKED SECURITIES (Continued) | |

| | |

| | | | |

NON-AGENCY COLLATERALIZED MORTGAGE OBLIGATION (Continued) | |

| | |

| $ | 5,537,663 | | |

Series 2022-4, Class A4, 3.000%, 10/25/2052(a),(b) | |

$ | 5,039,214 | |

| | 28,069,987 | | |

Series 2024-3, Class A4, 3.000%, 5/25/2054(a),(b) | |

| 25,511,352 | |

| | 26,760,962 | | |

Series 2025-1, Class A4, 3.692%, 1/25/2063(a),(b) | |

| 25,134,321 | |

| | | | |

OBX 2021-J3 Trust | |

| | |

| | 1,414,635 | | |

Series 2021-J3, Class A4, 2.500%, 10/25/2051(a),(b) | |

| 1,266,345 | |

| | | | |

OBX 2022-J1 Trust | |

| | |

| | 39,355,928 | | |

Series 2022-J1, Class A3, 3.000%, 2/25/2052(a),(b) | |

| 35,710,699 | |

| | | | |

Pretium Mortgage Credit Partners LLC | |

| | |

| | 7,341,807 | | |

Series 2024-RPL1, Class A1, 3.900%, 10/25/2063(a),(b) | |