|

|

Credicorp Ltd.

April 30, 2026

|

This report does not constitute a rating action.

|

|

|||||||||||||

| Primary Contact | ||||||||||||||

|

Ratings Score Snapshot

|

Camilo Andres Perez

Mexico City

|

|||||||||||||

|

52-55-5081-4446

|

||||||||||||||

|

SACP: bbb

|

Support: 0

|

Additional factors: -1

|

camilo.perez

|

|||||||||||

| Anchor |

bbb- |

Holding company ICR

|

@spglobal.com

|

|||||||||||

|

Business position

|

Strong |

1 |

ALAC support

|

0 |

||||||||||

|

Capital and earnings

|

Adequate | 0 |

GRE support

|

0 |

|

Secondary Contact

|

||||||||

|

Risk

position

|

Adequate | 0 |

Group support

|

0 |

BBB-/Stable/--

|

Jesus Sotomayor

|

||||||||

|

Funding

|

Adequate | 0 |

Sovereign support

|

0 |

|

Mexico City | ||||||||

|

Liquidity

|

Adequate |

|

520445513524919

|

|||||||||||

|

CRA adjustment

|

0 |

|

jesus.sotomayor

|

|||||||||||

| @spglobal.com | ||||||||||||||

ALAC--Additional loss-absorbing capacity. CRA--Comparable ratings analysis. GRE--Government-related entity. ICR--Issuer credit rating. SACP--Stand-alone credit profile.

Credit Highlights

Overview

| Key strengths | Key risks | |

|

High‑quality and diverse asset base with dominant positions in most business segments.

|

Complex political landscape could dent short‑ to medium‑term economic growth in Peru, limiting better business conditions. | |

| Sound profitability at most of its operating subsidiaries helps keep adequate capitalization while consistently upstreaming dividends. |

|

Credicorp Ltd. has investments in multiple large assets in the financial industry in Peru and some presence in other Latin American countries. The rating on the Bermuda-based

nonoperating holding company (NOHC) incorporates the Credicorp group's leading position in Peru's financial industry, along with its business diversification by product, steady earnings despite regional economic challenges, adequate

capitalization, stable funding base, and ample liquidity coverage.

Our rating on Peru influences the creditworthiness of companies operating in the domestic financial sector, including Credicorp. Our foreign currency

sovereign credit rating on Peru (BBB-/Stable/A-3) limits the group credit profile (GCP) on Credicorp because we consider it unlikely that the group, like other domestic financial companies, would remain unaffected in a sovereign default

scenario, given its large asset exposure to the country.

Credicorp's assets have grown 5% annually since 2024, accompanied by moderate internal growth at its main subsidiaries. The company also acquired the

remaining 50% of the joint venture with Empresas Banmédica in 2025, which strengthened the group's presence in the health care and medical services sector in Peru.

In December 2025, Credicorp announced an agreement to acquire Helm Bank (not rated) in the U.S., subject to regulatory approvals. The aim of the transaction is to strengthen cross-border

capabilities by serving international clients, particularly those whose financial activities span Latin America and the U.S. Helm Bank has over $1 billion in assets with a large presence in Florida. We don't expect significant changes in

Credicorp's credit profile if the transaction closes because Helm Bank's assets, loans, and equity represent less than 1.5% of the group's total volumes.

Our rating on Credicorp is at the same level as the 'bbb-' GCP because we believe the holding company will not carry any financial debt in 2026-2027. We

base this view on the fact that its current capital and liquidity support adequately its short- to medium-term strategies. During 2025, Credicorp repaid its only debt issuance (totaling $500 million) using unencumbered liquid assets it had. The

main purpose of the issuance, which it made in 2020, was to enhance the group's cash cushion for potential contingencies during the past adverse years.

As of December 2025, the NOHC's liabilities reported relate only to taxes and dividends, and its cash comfortably covers its small amount of operating expenses. Thus, at this point, we don't expect

the holding to rely on dividends, which mainly come from highly regulated subsidiaries. We expect double leverage to remain at conservative levels (around 100%), as seen in recent years.

Outlook

The stable rating outlook on Credicorp for the next 12-24 months reflects that on Peru, which will continue influencing the group's credit fundamentals. We don't expect the holding company to raise

debt in 2026, and anticipate it will keep stable double leverage below 120% and comfortable liquidity to support its operations.

The stable outlook also indicates the resilience of the group's largest subsidiary, Banco de Credito del Peru, which

we don't expect to downgrade unless its stand-alone credit profile falls below 'bbb-', which is unlikely.

Downside scenario

A downgrade of Peru could trigger a similar action on Credicorp. We could also lower the rating on Credicorp if it issues new debt and starts relying on dividends from its regulated subsidiaries to

meet its financial obligations.

Upside scenario

We could upgrade Credicorp if we were to take a similar action on the sovereign while the group's intrinsic credit fundamentals and holding company's debt strategy remain unchanged.

Key Metrics

Credicorp Ltd.‑‑Key ratios and forecasts

|

‑‑Fiscal year ended Dec. 31‑-

|

|||||

|

(%)

|

2023a

|

2024a

|

2025a

|

2026f

|

2027f

|

|

Growth in customer loans

|

‑2.5

|

0.5

|

2.9

|

7.5‑9.5

|

9.0‑12.0

|

|

Net interest income/average earning assets (NIM)

|

6.6

|

6.9

|

7.0

|

7.0‑7.3

|

6.9‑7.4

|

|

Cost‑to‑income ratio

|

46.9

|

47.7

|

47.1

|

45.0‑47.0

|

44.0‑46.0

|

|

Return on average common equity

|

15.8

|

16.5

|

19.0

|

17.5‑19.5

|

17.0‑21.0

|

|

New loan loss provisions/average customer loans

|

2.5

|

2.4

|

1.6

|

1.7‑1.9

|

1.6‑2.0

|

|

Gross nonperforming assets/customer loans

|

4.3

|

3.8

|

3.3

|

3.2‑3.4

|

3.0‑3.5

|

|

Net charge‑offs/average customer loans

|

2.0

|

2.4

|

1.7

|

1.5‑1.7

|

1.3‑1.9

|

|

Risk‑adjusted capital ratio

|

9.5

|

9.7

|

9.8

|

9.6‑9.9

|

9.4‑9.9

|

All figures include S&P Global Ratings' adjustments. a‑‑Actual. e‑‑Estimate. f‑‑Forecast. NIM‑‑Net interest margin.

Anchor: 'bbb-' For Financial Institutions Operating In Peru

Our bank criteria use our Banking Industry Country Risk Assessment's economic risk and industry risk scores to determine a bank's anchor, the starting point in assigning an issuer credit rating.

Our anchor for a financial entity operating in Peru (where Credicorp mostly operates) is 'bbb-'. (See "Banking Industry Country Risk Assessment: Peru,"

Jan. 20, 2026.)

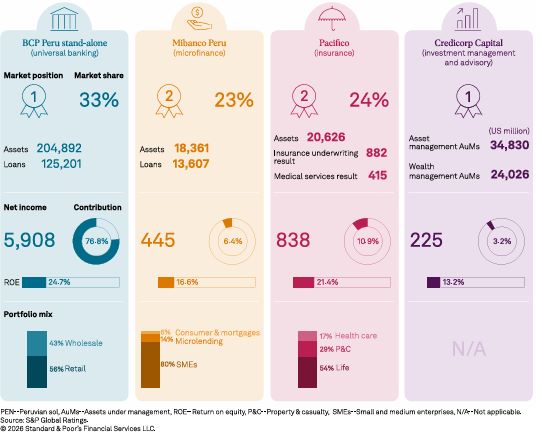

Business Position: Largest Financial Group In Peru With Ample Business Stability

Credicorp's solid business position reflects its leadership in Peru's financial sector, primarily through its largest subsidiary, Banco de Credito del Peru (BCP;

BBB-/Stable/A-3), which owns MiBanco Banco de la Microempresa S.A. (BBB-/Stable/A-3). BCP, which has diversified operations across all retail and wholesale segments, is the leading bank in

Peru, with a lending market share of about 37%, including its microlender subsidiary, MiBanco. These factors support the stability of the bank's business and dividend flows to Credicorp.

The group also has smaller banking operations, including ASB Bank Corp. (BB+/Stable/B) based in Panama and Banco de Credito de Bolivia (not

rated) based in Bolivia. It also has activities in the Peruvian insurance and pension fund industries through Pacifico Seguros and Prima AFP, respectively (both not rated). Pacifico Seguros is one of the leaders in Peru's life, health, and

property/casualty insurance segments. AFP Prima is the second-largest player in the pension industry, with a 29% share in assets under management. In addition, Credicorp has investment management and advisory operations in Colombia, Chile, and

Peru through Credicorp Capital (not rated). Credicorp also has a corporate venture capital arm (Krealo) that focuses on external innovation to complement the businesses of the group and support its growth.

BCP has made up 75%-80% of Credicorp's earnings and dividends in recent years, while insurance and pension fund business have made up 10%-15%. Banking operations in other jurisdictions and Credicorp Capital made up

the rest.

The steady investments in digital initiatives over the past years continue to pay off, benefiting Credicorp's competitiveness in the Peruvian financial industry. In particular,

Yape, the most used digital financial services app in Peru, with about 16 million active users, has been increasing its functionalities and supplementing banking and insurance products, increasing the group's client base and benefiting income

and profitability through its payment and lending operations. We expect investments in digitalization to continue, supporting the group's adaptability and competitive position amid continued disruptions in the financial industry.

Capital And Earnings: Adequate Capitalization To Support Business Strategy

We consider Credicorp's capitalization metrics commensurate with its business strategy. We expect its risk-adjusted capital ratio (calculated according to our methodology) to remain stable at

9.7%-9.8% in 2026-2027 thanks to its main operating subsidiaries' high and stable capacity to build earnings.

Our base case considers the following:

| • |

Annual GDP growth in Peru close to 3.0%

|

| • |

Annual inflation stabilizing at 2.0%

|

| • |

Stable policy rate at 4.25%

|

| • |

Annual loan growth of 9%-11%

|

| • |

Return on average equity at 17%-19%

|

| • |

Dividend distributions from Credicorp to its shareholders of 50%-80% of results but with flexibility to reduce them if needed

|

Credicorp has good regulatory capital metrics, with total regulatory capital at 1.3x the minimum requirement.

Credicorp's profitability continues to reach new highs, with return on average equity at 19.0% and return on average assets at 2.6% in 2025, compared to the 16.3% and 2.1% averages in 2022-2024.

Overall, improving operating conditions in Peru --including internal demand recovery, better employment dynamics, very low inflation, and relatively stable interest rates--, along with continued pension fund withdrawals, supported higher

earnings across the financial group's key operating units last year.

In particular, BCP (including MiBanco)'s ROE reached 24.8% in 2025, from 21.3% in 2024, mainly thanks to a marked decrease of the cost of risk due to dissipating credit risks amid borrowers'

improved payment capacity and the banks' more conversative underwriting and collection practices.

In addition, lending growth rebound, lower funding costs due to falling interest rates, and BCP's strong competitiveness in the transactional deposits segment helped keep net interest margins strong

last year. Stable cost efficiencies despite continued investments in technology and marketing also have contributed to sound bottom-line results.

We expect Credicorp's profitability to remain stable in 2026, with return on average equity at 17.5%-19.5%. Lending growth will continue and funding costs will remain low amid relatively stable

interest rates, while decreasing credit risks will anchor the cost of risk. Yape's improving performance and sound insurance results will also be key to keep solid earnings.

Risk Position: Diversified Business Mix And Improving Asset Quality

Credicorp has ample business diversification, conservative growth strategies, and manageable risks at its operating subsidiaries, in our view. The group's risk position mainly reflects our

assessment of its largest subsidiary, BCP, which has banking operations that focus on lending, with no relevant concentrations among economic sectors or customers.

As in the overall Peruvian banking industry, BCP's asset quality has been consistently improving since the second half of 2024 thanks to more stable local economic conditions, higher liquidity amid

the seventh and eight pension fund withdrawals, and banks' conservative underwriting of new loans. Thus, Credicorp's nonperforming assets (NPA) ratio decreased to 3.3% as of December 2025 (in line with the industry average) from 4.3% in

December 2023. In 2023 and part of 2024, volatile political conditions and adverse climate events eroded asset quality, especially that of microcredits, loans to small and midsize enterprises, and consumer credits to middle- and low-income

borrowers.

Our base-case scenario assumes adequate macroeconomic fundamentals, along with the group's conservative growth strategies, will help keep asset quality manageable in 2026, with NPAs stable at about 3.3%. Although

risks to the economy around political uncertainties and climate events in Peru seem to be manageable so far, we will continue monitoring these factors. Credicorp's good credit loss provisions coverage, capitalization, and liquidity would help

manage unexpected pressures on asset quality.

Funding And Liquidity: Stable Funding Base And Healthy Liquidity

We think the group has adequate funding structure and liquidity, in line with our assesment on BCP. According to our calculations, Credicorp's stable funding ratio has been 110%-120% in recent

years. Its broad liquid assets represented 32% of total assets, 49% of customer deposits, and 4.0x its short-term wholesale funding as of December 2025, indicating ample capacity to cover needs in 2026.

Customer deposits make up roughly 80% of Credicorp's consolidated funding base, and half are retail deposits, which we deem more stable, particularly during times of market distress. The funding

base also includes interbank credit lines, market debt, and central bank repurchase agreements.

Support: No Uplift To The Group Credit Profile

Credicorp is 12.3% owned by the Romero family (based on common shares), and the rest is held by private and institutional investors. Because of this, we base our rating on Credicorp on its own

credit quality, excluding parental support.

Despite the relevance of banking operations, our rating on Credicorp doesn't include potential extraordinary government support. Although we believe BCP would receive support, given its high

systemic importance in Peru, we don't expect such support would be extended to the holding company.

Environmental, Social, And Governance

Environmental, social, and governance (ESG) factors have no material influence on our credit rating analysis of Credicorp, as with industry and domestic peers. Peru is somewhat exposed to natural

disasters such as earthquakes, volcanic activity, landslides, and the El Niño climate pattern. However, Credicorp, like other domestic financial entities, has been able to keep credit and operating losses moderate during such conditions. The

group has solid loan diversification with low exposure to the agriculture sector, which is vulnerable to these conditions.

The Peruvian economy depends to some extent on the commodity metals sector, which domestic banks generally don't directly finance. Still, banks are indirectly exposed to those

sectors through the supply chain (suppliers, subcontractors, and employees who are also retail clients).

Credicorp operates in sectors that provide services and products supporting Peru and Colombia's social development. It provides financing to micro, small, and midsize companies, which make up 27% of

total loans. Also, insurance and pension operations in Peru play an important role in the society's welfare and economic stability. Yape contributes to increased financial inclusion in Peru.

Credicorp has a satisfactory oversight framework and corporate governance practices that comply with local regulations. The board of directors is well balanced to represent shareholders' interests adequately.

Key Statistics

|

Credicorp Ltd. Key Figures

|

||||||

|

Mil. PEN

|

2025

|

2024

|

2023

|

2022

|

2021

|

|

|

Adjusted assets

|

262,598

|

252,800

|

236,217

|

233,854

|

242,112

|

|

|

Customer loans (gross)

|

149,985

|

145,732

|

144,976

|

148,626

|

147,597

|

|

|

Adjusted common equity

|

28,915

|

28,451

|

27,629

|

25,775

|

21,967

|

|

|

Operating revenues

|

23,342

|

21,718

|

19,805

|

17,288

|

14,285

|

|

|

Noninterest expenses

|

10,988

|

10,374

|

9,334

|

8,621

|

7,740

|

|

|

Core earnings

|

7,083

|

5,623

|

4,960

|

4,745

|

3,672

|

|

|

PEN--Peruvian nuevo sol.

|

||||||

|

Credicorp Ltd. Business Position

|

||||||

|

(%)

|

2025

|

2024

|

2023

|

2022

|

2021

|

|

|

Total revenues from business line (currency in millions)

|

23,342

|

21,718

|

19,805

|

17,288

|

14,285

|

|

|

Commercial & retail banking/total revenues from business line

|

81.0

|

83.8

|

81.2

|

81.2

|

84.4

|

|

|

Insurance activities/total revenues from business line

|

6.0

|

5.5

|

5.7

|

5.7

|

5.9

|

|

|

Investment banking/total revenues from business line

|

8.6

|

8.7

|

4.7

|

4.7

|

6.0

|

|

|

Return on average common equity

|

19.0

|

16.5

|

15.8

|

16.8

|

13.9

|

|

|

Credicorp Ltd. Capital And Earnings

|

||||||

|

(%)

|

2025

|

2024

|

2023

|

2022

|

2021

|

|

|

Adjusted common equity/total adjusted capital

|

100.0

|

100.0

|

100.0

|

100.0

|

100.0

|

|

|

Net interest income/operating revenues

|

63.1

|

65.1

|

67.9

|

66.6

|

65.5

|

|

|

Fee income/operating revenues

|

18.0

|

18.7

|

19.3

|

21.1

|

24.5

|

|

|

Market-sensitive income/operating revenues

|

8.6

|

8.7

|

6.9

|

6.7

|

7.9

|

|

|

Cost to income ratio

|

47.1

|

47.7

|

46.9

|

49.9

|

54.2

|

|

|

Preprovision operating income/average assets

|

4.7

|

4.6

|

4.4

|

3.6

|

2.7

|

|

|

Core earnings/average managed assets

|

2.7

|

2.3

|

2.1

|

2.0

|

1.5

|

|

|

N.M.--Not meaningful.

|

|

Credicorp Ltd. Risk Position

|

||||||

|

(%)

|

2025

|

2024

|

2023

|

2022

|

2021

|

|

|

Growth in customer loans

|

2.9

|

0.5

|

(2.5)

|

0.7

|

7.2

|

|

|

Total managed assets/adjusted common equity (x)

|

9.3

|

9.0

|

8.6

|

9.2

|

11.2

|

|

|

New loan loss provisions/average customer loans

|

1.6

|

2.4

|

2.5

|

1.2

|

0.9

|

|

|

Net charge-offs/average customer loans

|

1.7

|

2.4

|

2.0

|

1.5

|

1.8

|

|

|

Gross nonperforming assets/customer loans + other real estate owned

|

3.3

|

3.8

|

4.3

|

4.1

|

3.9

|

|

|

Loan loss reserves/gross nonperforming assets

|

156.2

|

142.9

|

132.6

|

128.8

|

148.8

|

|

|

Credicorp Ltd. Risk Position

|

|

Credicorp Ltd. Funding And Liquidity

|

||||||

|

(%)

|

2025

|

2024

|

2023

|

2022

|

2021

|

|

|

Core deposits/funding base

|

83.4

|

80.98

|

79.5

|

78.5

|

76.0

|

|

|

Customer loans (net)/customer deposits

|

83.5

|

85.1

|

92.6

|

95.8

|

92.5

|

|

|

Long-term funding ratio

|

91.3

|

87.1

|

85.3

|

86.1

|

89.5

|

|

|

Stable funding ratio

|

122.2

|

121.8

|

113.4

|

110.8

|

110.5

|

|

|

Short-term wholesale funding/funding base

|

10.2

|

15.0

|

17.1

|

15.8

|

11.8

|

|

|

Broad liquid assets/short-term wholesale funding (x)

|

4.0

|

2.9

|

2.3

|

2.3

|

2.6

|

|

|

Broad liquid assets/total assets

|

31.5

|

34.1

|

30.8

|

28.4

|

25.2

|

|

|

Broad liquid assets/customer deposits

|

49.4

|

54.0

|

49.8

|

45.7

|

41.0

|

|

|

Net broad liquid assets/short-term customer deposits

|

46.5

|

44.4

|

35.3

|

31.9

|

31.8

|

|

|

Short-term wholesale funding/total wholesale funding

|

61.5

|

78.8

|

83.5

|

73.8

|

49.3

|

|

|

Rating Component Scores

|

|

Issuer Credit Rating

|

BBB-/Stable/--

|

|

SACP

|

bbb

|

|

Anchor

|

bbb-

|

|

Business position

|

Strong (1)

|

|

Capital and earnings

|

Adequate (0)

|

|

Risk position

|

Adequate (0)

|

|

Funding and liquidity

|

Adequate and Adequate (0)

|

|

Comparable ratings analysis

|

0

|

|

Support

|

0

|

|

ALAC support

|

0

|

|

GRE support

|

0

|

|

Group support

|

0

|

|

Sovereign support

|

0

|

|

Additional factors

|

-1

|

|

SACP--Stand-alone credit profile. ALAC--Additional loss-absorbing capacity. GRE--Government-related entity.

|

|

Related Criteria

| • |

General Criteria: Hybrid Capital: Methodology And Assumptions, Oct. 13, 2025

|

| • |

Criteria | Financial Institutions | General: Risk-Adjusted Capital Framework Methodology, April 30, 2024

|

| • |

Criteria | Financial Institutions | Banks: Banking Industry Country Risk Assessment Methodology And Assumptions, Dec. 9, 2021

|

| • |

Criteria | Financial Institutions | General: Financial Institutions Rating Methodology, Dec. 9, 2021

|

| • |

General Criteria: Environmental, Social, And Governance Principles In Credit Ratings, Oct. 10, 2021

|

| • |

General Criteria: Group Rating Methodology, July 1, 2019

|

| • |

General Criteria: Ratings Above The Sovereign--Corporate And Government Ratings: Methodology And Assumptions, Nov. 19, 2013

|

| • |

General Criteria: Principles Of Credit Ratings, Feb. 16, 2011

|

Related Research

| • |

Banco de Credito del Peru, March 30, 2026

|

| • |

Banking Industry Country Risk Assessment: Peru, Jan. 20, 2026

|

| • |

Peru 'BBB-/A-3' Foreign Currency Ratings Affirmed; Outlook Remains Stable, Dec. 11, 2025

|

| • |

Mibanco - Banco de la Microempresa S.A., Nov. 24, 2025

|

|

Ratings Detail (as of April 30, 2026)*

|

|

| Credicorp Ltd. | |

|

Issuer Credit Rating

|

BBB-/Stable/--

|

|

Issuer Credit Ratings History

|

|

|

26-Apr-2024

|

BBB-/Stable/--

|

|

15-Oct-2021

|

BBB/Negative/--

|

|

08-Jun-2020

|

BBB/Stable/--

|

|

Sovereign Rating

|

|

|

Bermuda

|

A+/Stable/A-1

|

|

Related Entities

|

|

| ASB Bank Corp. | |

|

Issuer Credit Rating

|

BB+/Stable/B

|

|

Banco de Credito del Peru

|

|

|

Issuer Credit Rating

|

BBB-/Stable/A-3

|

|

Senior Unsecured

|

BBB-

|

|

Subordinated

|

BB+

|

|

Banco de Credito del Peru, Panama Branch

|

|

|

Subordinated

|

BB+

|

|

MiBanco Banco de La Microempresa S.A.

|

|

|

Issuer Credit Rating

|

BBB-/Stable/A-3

|

|

*Unless otherwise noted, all ratings in this report are global scale ratings. S&P Global Ratings’ credit ratings on the global scale are comparable across

countries. S&P Global Ratings’ credit ratings on a national scale are relative to obligors or obligations within that specific country. Issue and debt ratings could include debt guaranteed by another entity, and rated debt that an

entity guarantees.

|

|

Copyright © 2026 by Standard & Poor’s Financial Services LLC. All rights reserved.

No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part thereof (Content) may be modified, reverse

engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of Standard & Poor’s Financial Services LLC or its affiliates (collectively, S&P). The

Content shall not be used for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees or agents (collectively S&P Parties) do not guarantee the accuracy,

completeness, timeliness or availability of the Content. S&P Parties are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for the

security or maintenance of any data input by the user. The Content is provided on an “as is” basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS

FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT’S FUNCTIONING WILL BE UNINTERRUPTED OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In

no event shall S&P Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including,

without limitation, lost income or lost profits and opportunity costs or losses caused by negligence) in connection with any use of the Content even if advised of the possibility of such damages.

Some of the Content may have been created with the assistance of an artificial intelligence (AI) tool. Published Content created or processed using AI is composed, reviewed, edited, and approved by S&P personnel.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and not statements of fact. S&P’s opinions, analyses and rating

acknowledgment decisions (described below) are not recommendations to purchase, hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation to update the

Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors and/or clients when making investment and

other business decisions. S&P does not act as a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be reliable, S&P does not perform an audit and

undertakes no duty of due diligence or independent verification of any information it receives. Rating-related publications may be published for a variety of reasons that are not necessarily dependent on action by rating committees, including,

but not limited to, the publication of a periodic update on a credit rating and related analyses.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain regulatory purposes, S&P reserves the right to assign,

withdraw or suspend such acknowledgment at any time and in its sole discretion. S&P Parties disclaim any duty whatsoever arising out of the assignment, withdrawal or suspension of an acknowledgment as well as any liability for any damage

alleged to have been suffered on account thereof.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain business

units of S&P may have information that is not available to other S&P business units. S&P has established policies and procedures to maintain the confidentiality of certain non-public information received in connection with each

analytical process.

S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P reserves the right to disseminate its opinions and analyses.

S&P's public ratings and analyses are made available on its Web sites, www.spglobal.com/ratings (free of charge), and www.ratingsdirect.com (subscription), and may be distributed through other means, including via S&P publications and

third-party redistributors.

Additional information about our ratings fees is available at www.spglobal.com/usratingsfees.

STANDARD & POOR’S, S&P and RATINGSDIRECT are registered trademarks of Standard & Poor’s Financial Services LLC.

|

www.spglobal.com/ratingsdirect

|

April 30, 2026

|

10 |