QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Quarterly Period Ended June 30, 2024

OR

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Transition Period from to

Commission file number 1-13045

IRON MOUNTAIN INCORPORATED

(Exact Name of Registrant as Specified in Its Charter)

Delaware

23-2588479

(State or other Jurisdiction of Incorporation or Organization)

(I.R.S. Employer Identification No.)

85 New Hampshire Avenue, Suite 150, Portsmouth, New Hampshire03801

(Address of Principal Executive Offices, Including Zip Code)

(617) 535-4766

(Registrant's Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Exchange Act:

Title of each class

Trading Symbol(s)

Name of each exchange on which registered

Common Stock, $.01 par value

IRM

NYSE

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer

☒

Accelerated filer

☐

Non-accelerated filer

☐

Smaller reporting company

☐

Emerging growth company

☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of July 26, 2024, the registrant had 293,335,826 outstanding shares of common stock, $.01 par value.

(IN THOUSANDS, EXCEPT SHARE AND PER SHARE DATA) (UNAUDITED)

JUNE 30, 2024

DECEMBER 31, 2023

ASSETS

Current Assets:

Cash and cash equivalents

$

144,256

$

222,789

Accounts receivable (less allowances of $78,513 and $74,762 as of June 30, 2024 and December 31, 2023, respectively)

1,273,900

1,259,826

Prepaid expenses and other

295,583

252,930

Total Current Assets

1,713,739

1,735,545

Property, Plant and Equipment:

Property, plant and equipment

10,976,919

10,373,989

Less—Accumulated depreciation

(4,183,895)

(4,059,120)

Property, Plant and Equipment, Net

6,793,024

6,314,869

Other Assets, Net:

Goodwill

5,099,772

5,017,912

Customer and supplier relationships and other intangible assets

1,284,339

1,279,800

Operating lease right-of-use assets

2,593,461

2,696,024

Other

482,599

429,652

Total Other Assets, Net

9,460,171

9,423,388

Total Assets

$

17,966,934

$

17,473,802

LIABILITIES AND EQUITY

Current Liabilities:

Current portion of long-term debt

$

125,409

$

120,670

Accounts payable

527,968

539,594

Accrued expenses and other current liabilities (includes current portion of operating lease liabilities)

1,174,979

1,250,259

Deferred revenue

329,718

325,665

Total Current Liabilities

2,158,074

2,236,188

Long-term Debt, net of current portion

12,814,166

11,812,500

Long-term Operating Lease Liabilities, net of current portion

2,453,935

2,562,394

Other Long-term Liabilities

257,497

237,590

Deferred Income Taxes

231,150

235,410

Commitments and Contingencies

Redeemable Noncontrolling Interests

184,861

177,947

(Deficit) Equity:

Iron Mountain Incorporated Stockholders' (Deficit) Equity:

Preferred stock (par value $0.01; authorized 10,000,000 shares; none issued and outstanding)

—

—

Common stock (par value $0.01; authorized 400,000,000 shares; issued and outstanding 293,298,465 and 292,142,739 shares as of June 30, 2024 and December 31, 2023, respectively)

2,933

2,921

Additional paid-in capital

4,555,883

4,533,691

(Distributions in excess of earnings) Earnings in excess of distributions

(4,230,599)

(3,953,808)

Accumulated other comprehensive items, net

(461,091)

(371,156)

Total Iron Mountain Incorporated Stockholders' (Deficit) Equity

(132,874)

211,648

Noncontrolling Interests

125

125

Total (Deficit) Equity

(132,749)

211,773

Total Liabilities and (Deficit) Equity

$

17,966,934

$

17,473,802

The accompanying notes are an integral part of these condensed consolidated financial statements.

Adjustments to reconcile net income (loss) to cash flows from operating activities:

Depreciation

302,562

254,395

Amortization (includes amortization of deferred financing costs and discounts of $12,243 and $8,095 for the six months ended June 30, 2024 and 2023, respectively)

143,737

131,161

Revenue reduction associated with amortization of customer inducements and above- and below-market leases

2,798

3,491

Stock-based compensation expense

43,928

34,882

(Benefit) provision for deferred income taxes

(442)

2,799

Loss (gain) on disposal/write-down of property, plant and equipment, net

3,179

(14,566)

Loss associated with the Clutter Acquisition

—

38,000

Foreign currency transactions and other, net

12,655

69,183

(Increase) decrease in assets

(86,117)

(31,071)

(Decrease) increase in liabilities

(21,731)

(108,858)

Cash Flows from Operating Activities

512,215

446,094

Cash Flows from Investing Activities:

Capital expenditures

(777,901)

(600,758)

Cash paid for acquisitions, net of cash acquired

(123,323)

(21,465)

Customer inducements

(3,457)

(2,630)

Contract costs

(50,800)

(39,989)

Investments in joint ventures and other investments, net

(10,190)

(15,830)

Proceeds from sales of property and equipment and other, net

5,923

35,390

Cash Flows from Investing Activities

(959,748)

(645,282)

Cash Flows from Financing Activities:

Repayment of revolving credit facility, term loan facilities and other debt

(4,896,450)

(10,087,033)

Proceeds from revolving credit facility, term loan facilities and other debt

5,843,362

9,683,880

Net proceeds from sale of senior note

—

990,000

Debt financing and equity contribution from noncontrolling interests

—

9,900

Equity distribution to noncontrolling interests

(1,209)

(2,032)

Parent cash dividends

(388,709)

(367,060)

Payment of deferred purchase obligation

(158,677)

—

Net (payments) proceeds associated with employee stock-based awards

(22,146)

(15,782)

Other, net

(6,880)

(2,046)

Cash Flows from Financing Activities

369,291

209,827

Effect of Exchange Rates on Cash and Cash Equivalents

(291)

(2,943)

(Decrease) increase in Cash and Cash Equivalents

(78,533)

7,696

Cash and Cash Equivalents, Beginning of Period

222,789

141,797

Cash and Cash Equivalents, End of Period

$

144,256

$

149,493

Supplemental Information:

Cash Paid for Interest

$

382,823

$

270,146

Cash Paid for Income Taxes, Net

$

43,099

$

46,502

Non-Cash Investing and Financing Activities:

Financing Leases and Other

$

67,996

$

61,085

Accrued Capital Expenditures

$

213,636

$

192,197

Deferred Purchase Obligations and Other Deferred Payments

$

133,813

$

9,290

Dividends Payable

$

200,318

$

192,597

The accompanying notes are an integral part of these condensed consolidated financial statements.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(In thousands, except share and per share data) (Unaudited)

1. GENERAL

The unaudited condensed consolidated financial statements of Iron Mountain Incorporated, a Delaware corporation, and its subsidiaries ("we" or "us"), have been prepared pursuant to the rules and regulations of the United States Securities and Exchange Commission (the "SEC"). Certain information and footnote disclosures normally included in the annual financial statements prepared in accordance with accounting principles generally accepted in the United States of America have been omitted pursuant to those rules and regulations, but we believe that the disclosures included herein are adequate to make the information presented not misleading. The interim condensed consolidated financial statements are presented herein and, in the opinion of management, reflect all adjustments of a normal recurring nature necessary for a fair presentation. Interim results are not necessarily indicative of results for a full year.

The Condensed Consolidated Financial Statements and Notes thereto, which are included herein, should be read in conjunction with the Consolidated Financial Statements and Notes thereto for the year ended December 31, 2023 included in our Annual Report on Form 10-K filed with the SEC on February 22, 2024 (our "Annual Report").

In September 2022, we announced a global program designed to accelerate the growth of our business ("Project Matterhorn"). See Note 11.

We have been organized and have operated as a real estate investment trust for United States federal income tax purposes beginning with our taxable year ended December 31, 2014.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

A. CASH AND CASH EQUIVALENTS

Cash and cash equivalents include cash on hand and cash invested in highly liquid short-term securities, which have remaining maturities at the date of purchase of less than 90 days. Cash and cash equivalents are carried at cost, which approximates fair value.

B. ACCOUNTS RECEIVABLE

We maintain an allowance for doubtful accounts and a credit memo reserve for estimated losses resulting from the potential inability of our customers to make required payments and potential disputes regarding billing and service issues.The rollforward of the allowance for doubtful accounts and credit memo reserves for the six months ended June 30, 2024 is as follows:

Balance as of December 31, 2023

$

74,762

Credit memos charged to revenue

44,137

Allowance for bad debts charged to expense

24,233

Deductions and other(1)

(64,619)

Balance as of June 30, 2024

$

78,513

(1)Primarily consists of the issuance of credit memos, the write-off of accounts receivable and the impact associated with currency translation adjustments.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

(In thousands, except share and per share data) (Unaudited)

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

C. LEASES

We lease facilities for certain warehouses, data centers and office space. We also have land leases, including those on which certain facilities are located.

Operating and financing lease right-of-use assets and lease liabilities as of June 30, 2024 and December 31, 2023 are as follows:

DESCRIPTION

JUNE 30, 2024

DECEMBER 31, 2023

Assets:

Operating lease right-of-use assets

$

2,593,461

$

2,696,024

Financing lease right-of-use assets, net of accumulated depreciation(1)

340,842

304,600

Liabilities:

Current

Operating lease liabilities

$

302,234

$

291,795

Financing lease liabilities(1)

42,260

39,089

Long-term

Operating lease liabilities

$

2,453,935

$

2,562,394

Financing lease liabilities(1)

336,653

310,776

(1)Financing lease right-of-use assets, current financing lease liabilities and long-term financing lease liabilities are included within Property, plant and equipment, net, Current portion of long-term debt and Long-term debt, net of current portion, respectively, within our Condensed Consolidated Balance Sheets.

The components of the lease expense for the three and six months ended June 30, 2024 and 2023 are as follows:

THREE MONTHS ENDED JUNE 30,

SIX MONTHS ENDED JUNE 30,

DESCRIPTION

2024

2023

2024

2023

Operating lease cost(1)

$

172,735

$

161,241

$

344,481

$

317,114

Financing lease cost:

Depreciation of financing lease right-of-use assets

$

12,078

$

10,202

$

23,022

$

20,210

Interest expense for financing lease liabilities

5,217

4,416

10,438

8,757

(1)Operating lease cost, the majority of which is included in Cost of sales, includes variable lease costs of $39,594 and $77,688 for the three and six months ended June 30, 2024, respectively, and $34,418 and $65,998 for the three and six months ended June 30, 2023, respectively.

Other information:Supplemental cash flow information relating to our leases for the six months ended June 30, 2024 and 2023 is as follows:

SIX MONTHS ENDED JUNE 30,

CASH PAID FOR AMOUNTS INCLUDED IN MEASUREMENT OF LEASE LIABILITIES:

2024

2023

Operating cash flows used in operating leases

$

235,030

$

220,764

Operating cash flows used in financing leases (interest)

10,438

8,757

Financing cash flows used in financing leases

21,536

22,010

NON-CASH ITEMS:

Operating lease modifications and reassessments

$

573

$

44,779

New operating leases (including acquisitions and sale-leaseback transactions)

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

(In thousands, except share and per share data) (Unaudited)

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

D. GOODWILL

Our reporting units as of December 31, 2023 are described in detail in Note 2.l. to Notes to Consolidated Financial Statements included in our Annual Report.

The changes in the carrying value of goodwill attributable to each reportable segment and Corporate and Other (as defined in Note 9) for the six months ended June 30, 2024 are as follows:

GLOBAL RIM BUSINESS

GLOBAL DATA CENTER BUSINESS

CORPORATE AND OTHER

TOTAL CONSOLIDATED

Goodwill balance, net of accumulated amortization, as of December 31, 2023

$

3,911,945

$

478,930

$

627,037

$

5,017,912

Tax deductible goodwill acquired during the period

—

—

131,790

131,790

Fair value and other adjustments

963

(186)

(186)

591

Currency effects

(45,888)

(3,928)

(705)

(50,521)

Goodwill balance, net of accumulated amortization, as of June 30, 2024

$

3,867,020

$

474,816

$

757,936

$

5,099,772

Accumulated goodwill impairment balance as of June 30, 2024

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

(In thousands, except share and per share data) (Unaudited)

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

E. FAIR VALUE MEASUREMENTS

The assets and liabilities carried at fair value measured on a recurring basis as of June 30, 2024 and December 31, 2023 are as follows:

FAIR VALUE MEASUREMENTS AT JUNE 30, 2024 USING

DESCRIPTION

TOTAL CARRYING

VALUE AT

JUNE 30, 2024

QUOTED PRICES IN ACTIVE MARKETS (LEVEL 1)

SIGNIFICANT OTHER OBSERVABLE INPUTS (LEVEL 2)

SIGNIFICANT

UNOBSERVABLE

INPUTS (LEVEL 3)(2)

Money Market Funds

$

10,218

$

—

$

10,218

$

—

Time Deposits

20,762

—

20,762

—

Trading Securities

8,841

7,166

1,675

—

Derivative Assets

25,607

—

25,607

—

Derivative Liabilities

2,670

—

2,670

—

Deferred Purchase Obligations(1)

114,703

—

—

114,703

FAIR VALUE MEASUREMENTS AT DECEMBER 31, 2023 USING

DESCRIPTION

TOTAL CARRYING

VALUE AT

DECEMBER 31, 2023

QUOTED PRICES IN ACTIVE MARKETS (LEVEL 1)

SIGNIFICANT OTHER OBSERVABLE INPUTS (LEVEL 2)

SIGNIFICANT

UNOBSERVABLE

INPUTS (LEVEL 3)(2)

Money Market Funds

$

66,008

$

—

$

66,008

$

—

Time Deposits

15,913

—

15,913

—

Trading Securities

9,952

6,149

3,803

—

Derivative Assets

6,359

—

6,359

—

Derivative Liabilities

5,769

—

5,769

—

Deferred Purchase Obligations(1)

208,265

—

—

208,265

(1)Primarily relates to the fair values of the deferred purchase obligations associated with the ITRenew Transaction (as defined in Note 3 to Notes to Consolidated Financial Statements included in our Annual Report) and the Regency Transaction (as defined in Note 3).

(2)The following is a rollforward of the Level 3 liabilities presented above for December 31, 2023 through June 30, 2024:

Balance as of December 31, 2023

$

208,265

Additions

63,700

Payments

(158,677)

Other changes, including accretion

1,415

Balance as of June 30, 2024

$

114,703

The level 3 valuations of the deferred purchase obligations were determined utilizing Monte-Carlo models and take into account our forecasted projections as they relate to the underlying performance of the respective businesses. The Monte-Carlo simulation model applied in assessing the fair value of the deferred purchase obligation associated with the ITRenew Transaction incorporates assumptions as to expected gross profits over the achievement period, including adjustments for the volatility of timing and amount of the associated revenue and costs, as well as discount rates that account for the risk of the arrangement and overall market risks. The Monte-Carlo simulation model applied in assessing the fair value of the deferred purchase obligation associated with the Regency Transaction incorporates assumptions as to expected revenue over the achievement period, including adjustments for volatility and timing, as well as discount rates that account for the risk of the arrangement and overall market risks. Any material change to these assumptions may result in a significantly higher or lower fair value of the related deferred purchase obligation.

There were no material items that were measured at fair value on a non-recurring basis at June 30, 2024 and December 31, 2023 other than (i) those disclosed in Note 2.p. to Notes to Consolidated Financial Statements included in our Annual Report and (ii) assets acquired and liabilities assumed through our acquisitions that occurred during the six months ended June 30, 2024 (see Note 3), both of which are based on Level 3 inputs.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

(In thousands, except share and per share data) (Unaudited)

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

F. ACCUMULATED OTHER COMPREHENSIVE ITEMS, NET

The changes in Accumulated other comprehensive items, net for the three and six months ended June 30, 2024 and 2023 are as follows:

THREE MONTHS ENDED JUNE 30, 2024

THREE MONTHS ENDED JUNE 30, 2023

FOREIGN CURRENCY TRANSLATION AND OTHER ADJUSTMENTS

DERIVATIVE FINANCIAL INSTRUMENTS

TOTAL

FOREIGN CURRENCY TRANSLATION AND OTHER ADJUSTMENTS

DERIVATIVE FINANCIAL INSTRUMENTS

TOTAL

Beginning of Period

$

(440,129)

$

11,332

$

(428,797)

$

(414,832)

$

9,064

$

(405,768)

Other comprehensive (loss) income:

Foreign currency translation and other adjustments

(31,806)

—

(31,806)

18,155

—

18,155

Change in fair value of derivative instruments

—

(488)

(488)

—

7,896

7,896

Reclassifications from accumulated other comprehensive items, net

—

—

—

—

(2,527)

(2,527)

Total other comprehensive (loss) income

(31,806)

(488)

(32,294)

18,155

5,369

23,524

End of Period

$

(471,935)

$

10,844

$

(461,091)

$

(396,677)

$

14,433

$

(382,244)

SIX MONTHS ENDED JUNE 30, 2024

SIX MONTHS ENDED JUNE 30, 2023

FOREIGN CURRENCY TRANSLATION AND OTHER ADJUSTMENTS

DERIVATIVE FINANCIAL INSTRUMENTS

TOTAL

FOREIGN CURRENCY TRANSLATION AND OTHER ADJUSTMENTS

DERIVATIVE FINANCIAL INSTRUMENTS

TOTAL

Beginning of Period

$

(373,628)

$

2,472

$

(371,156)

$

(454,509)

$

12,506

$

(442,003)

Other comprehensive (loss) income:

Foreign currency translation and other adjustments

(98,307)

—

(98,307)

57,832

—

57,832

Change in fair value of derivative instruments

—

10,900

10,900

—

4,454

4,454

Reclassifications from accumulated other comprehensive items, net

—

(2,528)

(2,528)

—

(2,527)

(2,527)

Total other comprehensive (loss) income

(98,307)

8,372

(89,935)

57,832

1,927

59,759

End of Period

$

(471,935)

$

10,844

$

(461,091)

$

(396,677)

$

14,433

$

(382,244)

G. REVENUES

The costs associated with the initial movement of customer records into physical storage and certain commissions are considered costs to fulfill or obtain customer contracts (collectively, "Contract Costs").Contract Costs as of June 30, 2024 and December 31, 2023 are as follows:

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

(In thousands, except share and per share data) (Unaudited)

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Deferred revenue liabilities are reflected in our Condensed Consolidated Balance Sheets as follows:

DESCRIPTION

LOCATION IN BALANCE SHEET

JUNE 30, 2024

DECEMBER 31, 2023

Deferred revenue - Current

Deferred revenue

$

329,718

$

325,665

Deferred revenue - Long-term

Other Long-term Liabilities

95,605

100,770

DATA CENTER LESSOR CONSIDERATIONS

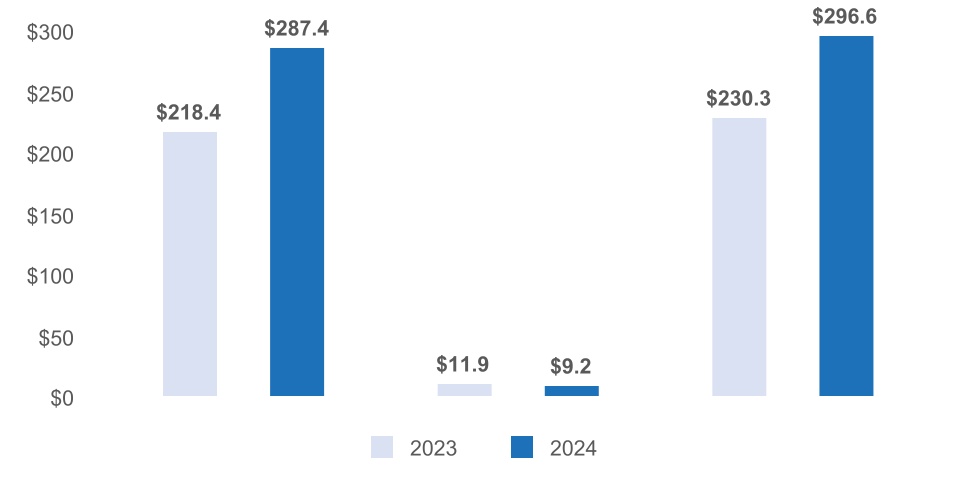

Our Global Data Center Business features storage rental provided to customers at contractually specified rates over a fixed contractual period, which are accounted for in accordance with Accounting Standards Codification 842, Leases.Storage rental revenue associated with our Global Data Center Business for the three and six months ended June 30, 2024 and 2023 is as follows:

THREE MONTHS ENDED JUNE 30,

SIX MONTHS ENDED JUNE 30,

2024

2023

2024

2023

Storage rental revenue

$

147,397

$

110,990

$

287,425

$

218,425

H. STOCK-BASED COMPENSATION

Our stock-based compensation expense includes the cost of stock options, restricted stock units ("RSUs") and performance units ("PUs") (together, the "Employee Stock-Based Awards").

STOCK-BASED COMPENSATION EXPENSE

Stock-based compensation expense for the Employee Stock-Based Awards for the three and six months ended June 30, 2024 and 2023 is as follows:

THREE MONTHS ENDED JUNE 30,

SIX MONTHS ENDED JUNE 30,

2024

2023

2024

2023

Stock-based compensation expense

$

29,889

$

22,373

$

43,928

$

34,882

During the six months ended June 30, 2024, we granted approximately 83,100 stock options, 644,200 RSUs and 450,700 PUs under the 2014 Plan (as defined in Note 2.t to Notes to Consolidated Financial Statements included in our Annual Report).

As of June 30, 2024, unrecognized compensation cost related to the unvested portion of our Employee Stock-Based Awards, inclusive of our estimated achievement of the performance metrics, is $111,128.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

(In thousands, except share and per share data) (Unaudited)

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

I. ACQUISITION AND INTEGRATION COSTS

Acquisition and integration costs represent operating expenditures directly associated with the closing and integration activities of our business acquisitions that have closed, or are highly probable of closing, and include (i) advisory, legal and professional fees to complete business acquisitions and (ii) costs to integrate acquired businesses into our existing operations, including move, severance and system integration costs (collectively, "Acquisition and Integration Costs").

Acquisition and Integration Costs for the three and six months ended June 30, 2024 and 2023 are as follows:

THREE MONTHS ENDED JUNE 30,

SIX MONTHS ENDED JUNE 30,

2024

2023

2024

2023

Acquisition and Integration Costs

$

9,502

$

1,511

$

17,311

$

3,106

J. LOSS (GAIN) ON DISPOSAL/WRITE-DOWN OF PROPERTY, PLANT AND EQUIPMENT, NET

Loss (gain) on disposal/write-down of property, plant and equipment, net for the three and six months ended June 30, 2024 and 2023 is as follows:

THREE MONTHS ENDED JUNE 30,

SIX MONTHS ENDED JUNE 30,

2024

2023

2024

2023(1)

Loss (gain) on disposal/write-down of property, plant and equipment, net

$

2,790

$

(1,505)

$

3,179

$

(14,566)

(1) The gains for the six months ended June 30, 2023 primarily consist of a gain of approximately $18,500 associated with a sale-leaseback transaction of a facility in Singapore during the first quarter 2023. The gains recognized during 2023 are the result of our program to monetize a small portion of our industrial assets through sale and sale-leaseback transactions. The terms for these leases are consistent with the terms of our lease portfolio, which are disclosed in detail in Note 2.j. to Notes to Consolidated Financial Statements included in our Annual Report.

K. OTHER EXPENSE (INCOME), NET

Other expense (income), net for the three and six months ended June 30, 2024 and 2023 consists of the following:

(1)The losses for the three and six months ended June 30, 2023 primarily consist of the impact of changes in the exchange rate of the British pound sterling against the United States dollar on our intercompany balances with and between certain of our subsidiaries.

(2)Other, net for the six months ended June 30, 2023 consists primarily of a loss of approximately $38,000 associated with the remeasurement to fair value of our previously held equity interest in the Clutter JV (as defined and discussed in Note 10) as well as losses on our equity method investments and the change in value of the Deferred Purchase Obligation (as defined in Note 3 to Notes to Consolidated Financial Statements included in our Annual Report).

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

(In thousands, except share and per share data) (Unaudited)

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

L. INCOME TAXES

We provide for income taxes during interim periods based on our estimate of the effective tax rate for the year.Our effective tax rates for the three and six months ended June 30, 2024 and 2023 are as follows:

THREE MONTHS ENDED JUNE 30,

SIX MONTHS ENDED JUNE 30,

2024(1)

2023(2)

2024

2023(2)

Effective Tax Rate

27.8

%

78.8

%

21.1

%

24.0

%

(1)The primary reconciling items between the federal statutory tax rate of 21.0% and our overall effective tax rate for the three months ended June 30, 2024 were the lack of tax benefits recognized for the year to date ordinary losses of certain entities, the benefits derived from the dividends paid deduction and the differences in the tax rates to which our foreign earnings are subject.

(2)The primary reconciling items between the federal statutory tax rate of 21.0% and our overall effective tax rate for the three and six months ended June 30, 2023 were (i) the loss of approximately $38,000 recorded in Other, net a component of Other expense (income), net during the second quarter of 2023 to reflect the remeasurement of our previously held equity interest in the Clutter JV to fair value, for which there was no tax impact, (ii) the benefits derived from the dividends paid deduction and (iii) the differences in the tax rates to which our foreign earnings are subject.

M. INCOME (LOSS) PER SHARE—BASIC AND DILUTED

The calculations of basic and diluted income (loss) per share for the three and six months ended June 30, 2024 and 2023 are as follows:

THREE MONTHS ENDED JUNE 30,

SIX MONTHS ENDED JUNE 30,

2024

2023

2024

2023

Net Income (Loss)

$

34,621

$

1,143

$

111,646

$

66,678

Less: Net (Loss) Income Attributable to Noncontrolling Interests

(1,162)

1,029

1,802

1,969

Net Income (Loss) Attributable to Iron Mountain Incorporated (utilized in numerator of Earnings Per Share calculation)

$

35,783

$

114

$

109,844

$

64,709

Weighted-average shares—basic

293,340,000

291,825,000

293,043,000

291,633,000

Effect of dilutive potential stock options

2,068,000

1,322,000

1,977,000

1,269,000

Effect of dilutive potential RSUs and PUs

430,000

380,000

509,000

386,000

Weighted-average shares—diluted

295,838,000

293,527,000

295,529,000

293,288,000

Net Income (Loss) Per Share Attributable to Iron Mountain Incorporated:

Basic

$

0.12

$

0.00

$

0.37

$

0.22

Diluted

$

0.12

$

0.00

$

0.37

$

0.22

Antidilutive stock options, RSUs and PUs excluded from the calculation

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

(In thousands, except share and per share data) (Unaudited)

3. ACQUISITIONS

REGENCY TECHNOLOGIES

On January 3, 2024, in order to expand our asset lifecycle management ("ALM") business, we acquired 100% of RSR Partners, LLC (doing business as Regency Technologies), an information technology asset disposition services provider with operations throughout the United States, for an initial purchase price of approximately $200,000, subject to certain working capital adjustments at, and subsequent to, the closing, with $125,000 paid at closing, funded by borrowings under the Revolving Credit Facility (as defined in Note 6), and the remaining $75,000 (the “January 2025 Payment”) to be paid in January 2025 (the "Regency Transaction"). The present value of the January 2025 Payment is included as a component of Accrued expenses and other current liabilities in our Condensed Consolidated Balance Sheet at June 30, 2024. The agreement for the Regency Transaction also includes a performance-based contingent consideration with a potential earnout range from zero to $200,000 based upon achievement of certain three-year cumulative revenue targets, which would be payable in 2027, if earned (the “Regency Deferred Purchase Obligation”). The preliminary fair value estimate of the Regency Deferred Purchase Obligation as of the acquisition date was approximately $78,400. See Note 2.e. for details on the methodology used to establish the fair value. The fair value of the Regency Deferred Purchase Obligation is included as a component of Other long-term liabilities in our Condensed Consolidated Balance Sheet at June 30, 2024. Subsequent increases or decreases in the fair value estimate of the Regency Deferred Purchase Obligation, as well as the accretion of the discount to present value, is included as a component of Other expense (income), net in our Condensed Consolidated Statements of Operations until the deferred purchase obligation is settled or paid. Subsequent to the acquisition, the results of Regency Technologies are included as a component of Corporate and Other.

WEB WERKS

On July 1, 2024, we entered into an agreement with the minority shareholders of Web Werks India Private Limited to acquire the remaining interest in the Web Werks JV (as defined in Note 5 to Notes to Consolidated Financial Statements included in our Annual Report). Pursuant to the agreement, we will acquire the remaining approximately 36.61% interest in the Web Werks JV in two separate transactions. On July 5, 2024, we completed the acquisition of an approximately 8.55% interest in the Web Werks JV (“Tranche I”) for approximately 3,000,000 Indian rupees (or approximately $35,000, based upon the exchange rate between the United States dollar and Indian rupee on the closing date of Tranche I). During the third quarter of 2024, we will recognize a charge of approximately $17,000, which will be recorded to Other expense (income), net, representing the difference between the purchase price of Tranche I and the related liability we have recorded on our Condensed Consolidated Balance Sheet at June 30, 2024. Subsequent to the Tranche I payment, our ownership interest in the Web Werks JV is approximately 71.94%. In March 2025, we will be required to make an additional payment of approximately 9,600,000 Indian rupees (or approximately $115,000, based upon the exchange rate between the United States dollar and Indian rupee as of June 30, 2024) (“Tranche II”) to acquire the remaining approximately 28.06% interest in the Web Werks JV. As part of the Tranche II payment in March 2025, we may also make an incremental payment of approximately 1,000,000 Indian rupees (or approximately $12,000, based upon the exchange rate between the United States dollar and Indian rupee as of June 30, 2024) if certain infrastructure goals are achieved before December 31, 2024. Any difference between the fair value of the approximately 28.06% interest and the total consideration paid will be recorded to Other expense (income), net.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

(In thousands, except share and per share data) (Unaudited)

3. ACQUISITIONS (CONTINUED)

PRELIMINARY PURCHASE PRICE ALLOCATION

A summary of the cumulative consideration paid and the preliminary allocation of the purchase price paid for our acquisition closed during the six months ended June 30, 2024 is as follows:

SIX MONTHS ENDED JUNE 30, 2024

Cash Paid (gross of cash acquired)

$

125,844

Deferred Purchase Obligations, Purchase Price Holdbacks and Other(1)

133,813

Total Consideration

259,657

Fair Value of Identifiable Assets Acquired(2)

156,108

Fair Value of Identifiable Liabilities Acquired

(28,241)

Goodwill Initially Recorded(3)

$

131,790

(1)Consists of the acquisition-date fair values of the Regency Deferred Purchase Obligation and the January 2025 Payment.

(2)Assets acquired include a supplier relationship intangible asset, which has a fair value of $107,500 and a weighted average life of approximately 20 years.

(3)Goodwill is primarily attributable to the assembled workforce, expanded market opportunities and costs and other operating synergies anticipated upon the integration of the operations of us and the acquired businesses.

The preliminary purchase price allocations that are not finalized as of June 30, 2024 relate to the final assessment of the fair value of the assets acquired and the fair value of the deferred purchase obligation, which may differ materially from these preliminary estimates associated with the acquisition closed during the six months ended June 30, 2024. Any adjustments to our estimates of purchase price allocations will be made in the periods in which the adjustments are determined, and the cumulative effect of such adjustments will be calculated as if the adjustments had been completed as of the acquisition dates. Purchase price allocation adjustments recorded during the six months ended June 30, 2024were not material to our balance sheet or results from operations.

4. INVESTMENTS

JOINT VENTURE SUMMARY

Our joint venture with AGC Equity Partners (the "Frankfurt JV") is accounted for as an equity method investment and is presented as a component of Other within Other assets, net in our Condensed Consolidated Balance Sheets. The carrying value and equity interest in the Frankfurt JV at June 30, 2024 and December 31, 2023 is as follows:

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

(In thousands, except share and per share data) (Unaudited)

5. DERIVATIVE INSTRUMENTS AND HEDGING ACTIVITIES

Derivative instruments we are party to include: (i) interest rate swap agreements (which are designated as cash flow hedges) and (ii) cross-currency swap agreements (which are designated as net investment hedges).

INTEREST RATE SWAP AGREEMENTS DESIGNATED AS CASH FLOW HEDGES

We utilize interest rate swap agreements designated as cash flow hedges to limit our exposure to changes in interest rates on a portion of our floating rate indebtedness. Certain of our interest rate swap agreements have notional amounts that will increase with the underlying hedged transaction. Under our interest rate swap agreements, we receive variable rate interest payments associated with the notional amount of each interest rate swap, based upon the one-month Secured Overnight Financing Rate ("SOFR"), in exchange for the payment of fixed interest rates as specified in the interest rate swap agreements. Our interest rate swap agreements are marked to market at the end of each reporting period, representing the fair values of the interest rate swap agreements, and any changes in fair value are recognized as a component of Accumulated other comprehensive items, net. Unrealized gains are recognized as assets, while unrealized losses are recognized as liabilities.

As of June 30, 2024 and December 31, 2023, we have approximately $1,251,000 and $520,000, respectively, in notional value outstanding on our interest rate swap agreements, with maturity dates ranging from October 2025 through May 2027.

CROSS-CURRENCY SWAP AGREEMENTS DESIGNATED AS A HEDGE OF NET INVESTMENT

We utilize cross-currency swaps to hedge the variability of exchange rate impacts between the United States dollar and the Euro. As of both June 30, 2024 and December 31, 2023, we have approximately $509,200 in notional value outstanding on cross-currency interest rate swaps, with maturity dates ranging from August 2024 through February 2026.

We have designated these cross-currency swap agreements as hedges of net investments in certain of our Euro denominated subsidiaries and they require an exchange of the notional amounts at maturity. These cross-currency swap agreements are marked to market at the end of each reporting period, representing the fair values of the cross-currency swap agreements, and any changes in fair value are recognized as a component of Accumulated other comprehensive items, net. Unrealized gains are recognized as assets while unrealized losses are recognized as liabilities. The excluded component of our cross-currency swap agreements is recorded in Accumulated other comprehensive items, net and amortized to interest expense on a straight-line basis.

The fair values of derivative instruments recognized in our Condensed Consolidated Balance Sheets at June 30, 2024 and December 31, 2023, by derivative instrument, are as follows:

JUNE 30, 2024

DECEMBER 31, 2023

DERIVATIVE INSTRUMENTS(1)

Assets

Liabilities

Assets

Liabilities

Cash Flow Hedges(2)

Interest rate swap agreements

$

11,898

$

(2,670)

$

1,601

$

(3,273)

Net Investment Hedges(3)

Cross-currency swap agreements

13,709

—

4,758

(2,496)

(1)Our derivative assets are included as a component of (i) Prepaid expenses and other or (ii) Other within Other assets, net and our derivative liabilities are included as a component of (i) Accrued expenses and other current liabilities or (ii) Other long-term liabilities in our Condensed Consolidated Balance Sheets. As of June 30, 2024, $2,074 is included within Prepaid expenses and other, $23,533 is included within Other assets and $2,670 is included within Other long-term liabilities. As of December 31, 2023, $6,359 is included within Other assets, $2,496 is included within Accrued expenses and other current liabilities and $3,273 is included within Other long-term liabilities.

(2)As of June 30, 2024, cumulative net gains recorded within Accumulated other comprehensive items, net associated with our interest rate swap agreements are $10,844.

(3)As of June 30, 2024, cumulative net gains recorded within Accumulated other comprehensive items, net associated with our cross-currency swap agreements are $52,259, which include $38,550 related to the excluded component of our cross-currency swap agreements.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

(In thousands, except share and per share data) (Unaudited)

5. DERIVATIVE INSTRUMENTS AND HEDGING ACTIVITIES (CONTINUED)

Unrealized (losses) gains recognized in Accumulated other comprehensive items, net during the three and six months ended June 30, 2024 and 2023, by derivative instrument, are as follows:

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

(In thousands, except share and per share data) (Unaudited)

6. DEBT

Long-term debt is as follows:

JUNE 30, 2024

DECEMBER 31, 2023

DEBT

(INCLUSIVE OF

DISCOUNT)

UNAMORTIZED

DEFERRED

FINANCING

COSTS

CARRYING

AMOUNT

FAIR

VALUE

DEBT

(INCLUSIVE OF

DISCOUNT)

UNAMORTIZED

DEFERRED

FINANCING

COSTS

CARRYING

AMOUNT

FAIR

VALUE

Revolving Credit Facility(1)

$

745,000

$

(4,065)

$

740,935

$

745,000

$

—

$

(4,621)

$

(4,621)

$

—

Term Loan A(1)

221,875

—

221,875

221,875

228,125

—

228,125

228,125

Term Loan B due 2026(1)

655,911

(1,874)

654,037

656,250

659,298

(2,498)

656,800

659,750

Term Loan B due 2031(1)

1,185,635

(12,369)

1,173,266

1,194,000

1,191,000

(13,026)

1,177,974

1,200,000

Virginia 3 Term Loans(2)

221,615

(3,771)

217,844

221,615

101,218

(4,641)

96,577

101,218

Virginia 4/5 Term Loans(2)

61,513

(4,286)

57,227

61,513

16,338

(5,892)

10,446

16,338

Virginia 6 Term Loans(3)

53,825

(5,585)

48,240

53,825

—

—

—

—

Australian Dollar Term Loan(2)

191,334

(365)

190,969

192,498

197,743

(482)

197,261

199,195

UK Bilateral Revolving Credit Facility(2)

177,043

—

177,043

177,043

178,239

—

178,239

178,239

GBP Notes(2)

505,836

(1,274)

504,562

492,780

509,254

(1,763)

507,491

489,108

47/8% Notes due 2027(2)

1,000,000

(4,621)

995,379

962,500

1,000,000

(5,332)

994,668

967,500

51/4% Notes due 2028(2

825,000

(4,428)

820,572

796,125

825,000

(5,019)

819,981

800,250

5% Notes due 2028(2)

500,000

(2,954)

497,046

477,500

500,000

(3,316)

496,684

478,750

7% Notes due 2029(2)

1,000,000

(9,750)

990,250

1,012,500

1,000,000

(10,813)

989,187

1,027,500

47/8% Notes due 2029(2)

1,000,000

(7,595)

992,405

937,500

1,000,000

(8,318)

991,682

945,000

51/4% Notes due 2030(2)

1,300,000

(9,151)

1,290,849

1,228,500

1,300,000

(9,903)

1,290,097

1,241,500

41/2% Notes(2)

1,100,000

(8,296)

1,091,704

990,000

1,100,000

(8,917)

1,091,083

995,500

5% Notes due 2032(2)

750,000

(10,553)

739,447

682,500

750,000

(11,206)

738,794

684,375

55/8% Notes(2)

600,000

(4,695)

595,305

565,500

600,000

(4,985)

595,015

567,000

Real Estate Mortgages, Financing Lease Liabilities and Other

568,267

(638)

567,629

568,267

519,907

(403)

519,504

519,907

Accounts Receivable Securitization Program(3)

373,800

(809)

372,991

373,800

358,500

(317)

358,183

358,183

Total Long-term Debt

13,036,654

(97,079)

12,939,575

12,034,622

(101,452)

11,933,170

Less Current Portion

(125,409)

—

(125,409)

(120,670)

—

(120,670)

Long-term Debt, Net of Current Portion

$

12,911,245

$

(97,079)

$

12,814,166

$

11,913,952

$

(101,452)

$

11,812,500

(1)Collectively, the “Credit Agreement”. The Credit Agreement consists of a revolving credit facility (the “Revolving Credit Facility”), a term loan A facility (the “Term Loan A”) and two term loan B facilities (the "Term Loan B due 2026" and the "Term Loan B due 2031"). The remaining amount available for borrowing under the Revolving Credit Facility as of June 30, 2024 was $1,496,102 (which represents the maximum availability as of such date). The weighted average interest rate in effect under the Revolving Credit Facility was 7.2% as of June 30, 2024. Due to the discontinuance of the Canadian Dollar Offered Rate reference rate on June 28, 2024, the Credit Agreement was amended on June 7, 2024 to update the interest rate benchmark available for Canadian currency borrowings under our Revolving Credit Facility to the Canadian Overnight Repo Rate Average, effective July 1, 2024. All other material terms of the Revolving Credit Facility remain the same as disclosed in Note 7 to Notes to Consolidated Financial Statements included in our Annual Report.

(2)Each as defined in Note 7 to Notes to Consolidated Financial Statements included in our Annual Report.

(3)The fair value (Level 2 of fair value hierarchy described at Note 2.e.) of this debt instrument approximates the carrying value as borrowings under this debt instrument are based on a current variable market interest rate.

See Note 7 to Notes to Consolidated Financial Statements included in our Annual Report for additional information regarding our long-term debt, including the direct obligors of each of our debt instruments as well as information regarding the fair value of our debt instruments (including the levels of the fair value hierarchy used to determine the fair value of our debt instruments, which are consistent with the levels of the fair value hierarchy used to determine the fair value of our debt as of June 30, 2024).

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

(In thousands, except share and per share data) (Unaudited)

6. DEBT (CONTINUED)

CREDIT AGREEMENT

On July 2, 2024, we amended the Credit Agreement, which resulted in (i) an increase in the principal amount of the Term Loan B due 2031 from $1,194,000 to approximately $1,806,700, (ii) a decrease in the interest rate of the Term Loan B due 2031 from SOFR plus 2.25% to SOFR plus 2.00% and (iii) a decrease in the principal amount of our Term Loan B due 2026 from approximately $656,300 to approximately $53,400. We paid original issue discount fees of approximately $4,300 in connection with this amendment. Quarterly principal payments of approximately $4,500 on the Term Loan B due 2031 will commence in September 2024. All other material terms remain the same as disclosed in Note 7 to Notes to Consolidated Financial Statements included in our Annual Report.

VIRGINIA CREDIT AGREEMENTS

As our Global Data Center business continues to expand, we have entered into credit agreements in order to partially finance the construction of various data centers. During the quarter ended June 30, 2024, we entered into two new agreements. These agreements primarily consist of the following term loan facilities:

AGREEMENT

MAXIMUM BORROWING AMOUNT

OUTSTANDING BORROWINGS AS OF JUNE 30, 2024

DIRECT OBLIGOR

CONTRACTUAL INTEREST RATE

UNUSED COMMITMENT FEE

MATURITY DATE(1)

Virginia 6 Term Loans(2)

$

210,000

$

53,825

Iron Mountain Data Centers Virginia 6, LLC

SOFR plus 2.75%

0.75%

May 3, 2027

Virginia 7 Term Loans(3)

300,000

—

Iron Mountain Data Centers Virginia 7, LLC

SOFR plus 2.50%

0.75%

April 12, 2027

(1)All obligations will become due on the specified maturity dates. Each agreement includes twoone-year options that allow us to extend the initial maturity date, subject to the conditions specified in the agreements.

(2)On May 3, 2024, Iron Mountain Data Centers Virginia 6, LLC, a wholly-owned subsidiary of Iron Mountain Data Centers Virginia 6/7 JV, LLC, entered into a credit agreement (the "Virginia 6 Credit Agreement"). The Virginia 6 Credit Agreement consists of a term loan facility (the "Virginia 6 Term Loans") and a letter of credit facility. The Virginia 6 Credit Agreement is secured by the equity interests and assets of Iron Mountain Data Centers Virginia 6, LLC. As of June 30, 2024, the interest rate in effect under the Virginia 6 Credit Agreement was 5.3%.

(3)On April 12, 2024, Iron Mountain Data Centers Virginia 7, LLC, a wholly-owned subsidiary of Iron Mountain Data Centers Virginia 6/7 JV, LLC, entered into a credit agreement (the "Virginia 7 Credit Agreement"). The Virginia 7 Credit Agreement consists of a term loan facility and a letter of credit facility. The Virginia 7 Credit Agreement is secured by the equity interests and assets of Iron Mountain Data Centers Virginia 7, LLC.

ACCOUNTS RECEIVABLE SECURITIZATION PROGRAM

On June 14, 2024, we amended the Accounts Receivable Securitization Program (as defined in Note 7 to Notes to Consolidated Financial Statements included in our Annual Report) to (i) increase the maximum borrowing capacity from $360,000 to $400,000, with an option to increase the borrowing capacity to $450,000, and (ii) extend the maturity date from July 1, 2025 to July 1, 2027, at which point all obligations become due. All other material terms of the Accounts Receivable Securitization Program remain the same as disclosed in Note 7 to Notes to Consolidated Financial Statements included in our Annual Report.

MAXIMUM AMOUNT

$400,000

OUTSTANDING BORROWING

$373,800

INTEREST RATE

6.4%

As of June 30, 2024

LETTERS OF CREDIT

As of June 30, 2024, we had outstanding letters of credit totaling $58,880, of which $8,898 reduce our borrowing capacity under the Revolving Credit Facility. The letters of credit expire at various dates between July 2024 and May 2027.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

(In thousands, except share and per share data) (Unaudited)

6. DEBT (CONTINUED)

DEBT COVENANTS

The Credit Agreement, our bond indentures and other agreements governing our indebtedness contain certain restrictive financial and operating covenants, including covenants that restrict our ability to complete acquisitions, pay cash dividends, incur indebtedness, make investments, sell assets and take other specified corporate actions. The covenants do not contain a rating trigger. Therefore, a change in our debt rating would not trigger a default under the Credit Agreement, our bond indentures or other agreements governing our indebtedness. The Credit Agreement requires that we satisfy a net total lease adjusted leverage ratio and a fixed charge coverage ratio on a quarterly basis, and our bond indentures require that, among other things, we satisfy a leverage ratio (not lease adjusted) or a fixed charge coverage ratio (not lease adjusted) as a condition to taking actions such as paying dividends and incurring indebtedness.

The Credit Agreement uses earnings before interest, taxes, depreciation and amortization and rent expense ("EBITDAR") based calculations and the bond indentures use earnings before interest, taxes, depreciation and amortization ("EBITDA") based calculations as the primary measures of financial performance for purposes of calculating leverage and fixed charge coverage ratios. The EBITDAR- and EBITDA-based leverage calculations include our consolidated subsidiaries, other than those we have designated as "Unrestricted Subsidiaries" as defined in the Credit Agreement and bond indentures. Generally, the Credit Agreement and the bond indentures use a trailing four fiscal quarter basis for purposes of the relevant calculations and require certain adjustments and exclusions for purposes of those calculations, which make the calculation of financial performance for purposes of those calculations under the Credit Agreement and bond indentures not directly comparable to Adjusted EBITDA as presented herein. We are in compliance with our leverage and fixed charge coverage ratios under the Credit Agreement, our bond indentures and other agreements governing our indebtedness as of June 30, 2024. Noncompliance with these leverage and fixed charge coverage ratios would have a material adverse effect on our financial condition and liquidity.

7. COMMITMENTS AND CONTINGENCIES

We are involved in litigation from time to time in the ordinary course of business, including litigation arising from damage to customer assets in our facilities caused by fires and other natural disasters. While the outcome of litigation is inherently uncertain, we do not believe any current litigation will have a material adverse effect on our consolidated financial condition, results of operations or cash flows.

We have estimated a reasonably possible range for all loss contingencies and believe it is reasonably possible that we could incur aggregate losses in addition to amounts currently accrued for all matters up to an additional $15,000 over the next several years, of which certain amounts would be covered by insurance or indemnity arrangement.

8. STOCKHOLDERS' EQUITY MATTERS

In fiscal year 2023 and the six months ended June 30, 2024, our board of directors declared the following dividends:

DECLARATION DATE

DIVIDEND PER SHARE

RECORD DATE

TOTAL AMOUNT

PAYMENT DATE

February 23, 2023

$

0.6185

March 15, 2023

$

180,339

April 5, 2023

May 4, 2023

0.6185

June 15, 2023

180,493

July 6, 2023

August 3, 2023

0.6500

September 15, 2023

189,730

October 5, 2023

November 2, 2023

0.6500

December 15, 2023

189,886

January 4, 2024

February 22, 2024

0.6500

March 15, 2024

190,506

April 4, 2024

May 2, 2024

0.6500

June 17, 2024

190,643

July 5, 2024

On August 1, 2024, we declared a dividend to our stockholders of record as of September 16, 2024 of $0.715 per share, payable on October 3, 2024.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

(In thousands, except share and per share data) (Unaudited)

9. SEGMENT INFORMATION

Our reportable segments as of December 31, 2023 are described in Note 11 to Notes to Consolidated Financial Statements included in our Annual Report and are as follows:

•Global RIM Business

•Global Data Center Business

The remaining activities of our business consist primarily of our Fine Arts and ALM businesses and other corporate items ("Corporate and Other").

The operations associated with acquisitions completed during the first six months of 2024 have been incorporated into our existing reportable segments.

An analysis of our business segment information and reconciliation to the accompanying Condensed Consolidated Financial Statements for the three and six months ended June 30, 2024 and 2023 is as follows:

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

(In thousands, except share and per share data) (Unaudited)

9. SEGMENT INFORMATION (CONTINUED)

Adjusted EBITDA for each segment is defined as net income (loss) before interest expense, net, provision (benefit) for income taxes, depreciation and amortization (inclusive of our share of Adjusted EBITDA from our unconsolidated joint ventures), and excluding certain items we do not believe to be indicative of our core operating results, specifically:

EXCLUDED

•Acquisition and Integration Costs

•Restructuring and other transformation

•Loss (gain) on disposal/write-down of property, plant and equipment, net (including real estate)

•Other expense (income), net

•Stock-based compensation expense

Internally, we use Adjusted EBITDA as the basis for evaluating the performance of, and allocating resources to, our operating segments.

A reconciliation of Net Income (Loss) to Adjusted EBITDA on a consolidated basis for the three and six months ended June 30, 2024 and 2023 is as follows:

THREE MONTHS ENDED JUNE 30,

SIX MONTHS ENDED JUNE 30,

2024

2023

2024

2023

Net Income (Loss)

$

34,621

$

1,143

$

111,646

$

66,678

Add/(Deduct):

Interest expense, net

176,521

144,178

341,040

281,347

Provision (benefit) for income taxes

13,319

4,255

29,928

21,013

Depreciation and amortization

224,501

195,367

434,056

377,461

Acquisition and Integration Costs

9,502

1,511

17,311

3,106

Restructuring and other transformation

46,513

45,588

87,280

82,501

Loss (gain) on disposal/write-down of property, plant and equipment, net (including real estate)

2,790

(1,505)

3,179

(14,566)

Other expense (income), net, excluding our share of losses (gains) from our unconsolidated joint ventures

4,532

58,694

(8,578)

76,185

Stock-based compensation expense

29,889

22,373

43,928

34,882

Our share of Adjusted EBITDA reconciling items from our unconsolidated joint ventures

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

(In thousands, except share and per share data) (Unaudited)

9. SEGMENT INFORMATION (CONTINUED)

Information as to our revenues by product and service lines by segment for the three and six months ended June 30, 2024 and 2023 is as follows:

THREE MONTHS ENDED JUNE 30,

SIX MONTHS ENDED JUNE 30,

2024

2023

2024

2023

Global RIM Business

Records Management(1)

$

974,480

$

898,634

$

1,911,132

$

1,766,622

Data Management(1)

131,073

130,251

263,123

259,845

Information Destruction(1)(2)

145,024

130,982

286,479

259,926

Data Center(1)

—

—

—

—

Global Data Center Business

Records Management(1)

$

—

$

—

$

—

$

—

Data Management(1)

—

—

—

—

Information Destruction(1)

—

—

—

—

Data Center(1)

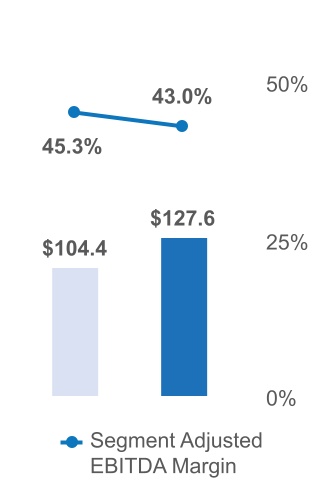

152,702

118,033

296,639

230,338

Corporate and Other

Records Management(1)

$

40,996

$

37,409

$

80,068

$

71,757

Data Management(1)

—

—

—

—

Information Destruction(1)(3)

90,134

42,627

173,831

83,797

Data Center(1)

—

—

—

—

Total Consolidated

Records Management(1)

$

1,015,476

$

936,043

$

1,991,200

$

1,838,379

Data Management(1)

131,073

130,251

263,123

259,845

Information Destruction(1)(2)(3)

235,158

173,609

460,310

343,723

Data Center(1)

152,702

118,033

296,639

230,338

(1)Each of these offerings has a component of revenue that is storage rental related and a component that is service related, except for information destruction, which does not have a storage rental component.

(2)Information destruction revenue for our Global RIM Business includes secure shredding services.

(3)Information destruction revenue for Corporate and Other includes product revenue from our ALM business.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

(In thousands, except share and per share data) (Unaudited)

10. RELATED PARTIES

In October 2020, in connection with the formation of the Frankfurt JV, we entered into agreements whereby we earn various fees, including (i) special project revenue and (ii) property management and construction and development fees for services we are providing to the Frankfurt JV (the "Frankfurt JV Agreements").

In February 2022, we entered into a storage and service agreement with the joint venture formed by Clutter, Inc. and us (the "Clutter JV") to provide certain storage and related services to the Clutter JV (the "Clutter Agreement"). On June 29, 2023, we completed the Clutter Acquisition (as defined in Note 3 to Notes to Consolidated Financial Statements included in our Annual Report) and terminated the Clutter Agreement.

Revenue recognized in the accompanying Condensed Consolidated Statements of Operations under these agreements for the three and six months ended June 30, 2024 and 2023 is as follows (approximately):

THREE MONTHS ENDED JUNE 30,

SIX MONTHS ENDED JUNE 30,

2024

2023

2024

2023

Frankfurt JV Agreements(1)

$

2,100

$

800

$

2,500

$

1,700

Clutter Agreement(2)

—

7,000

—

13,000

(1)Revenue associated with the Frankfurt JV Agreements is presented as a component of our Global Data Center Business segment.

(2)Revenue associated with the Clutter Agreement is presented as a component of our Global RIM Business segment.

11. RESTRUCTURING AND OTHER TRANSFORMATION

PROJECT MATTERHORN

In September 2022, we announced Project Matterhorn. Project Matterhorn investments focus on transforming our operating model to a global operating model. Project Matterhorn focuses on the formation of a solution-based sales approach that is designed to allow us to optimize our shared services and best practices to better serve our customers' needs. We are investing to accelerate growth and to capture a greater share of the large, global addressable markets in which we operate. We expect to incur approximately $150,000 in costs annually related to Project Matterhorn from 2023 through 2025. Costs are comprised of (1) restructuring costs, which include (i) site consolidation and other related exit costs, (ii) employee severance costs and (iii) certain professional fees associated with these activities, and (2) other transformation costs, which include professional fees such as project management costs and costs for third party consultants who are assisting in the enablement of our growth initiatives.

Restructuring and other transformation related to Project Matterhorn included in the accompanying Condensed Consolidated Statement of Operations for the three and six months ended June 30, 2024 and 2023, and from the inception of Project Matterhorn through June 30, 2024, is as follows:

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

(In thousands, except share and per share data) (Unaudited)

11. RESTRUCTURING AND OTHER TRANSFORMATION (CONTINUED)

Restructuring costs for Project Matterhorn, included as a component of Restructuring and other transformation in the accompanying Condensed Consolidated Statement of Operations, by segment for the three and six months ended June 30, 2024 and 2023, and from the inception of Project Matterhorn through June 30, 2024, is as follows:

THREE MONTHS ENDED JUNE 30,

SIX MONTHS ENDED JUNE 30,

FROM THE INCEPTION

OF PROJECT

MATTERHORN THROUGH

JUNE 30, 2024

2024

2023

2024

2023

Global RIM Business

$

12,643

$

15,000

$

22,784

$

24,525

$

82,589

Global Data Center Business

2,572

—

2,576

78

3,096

Corporate and Other

1,121

1,127

1,702

3,481

11,988

Total restructuring costs

$

16,336

$

16,127

$

27,062

$

28,084

$

97,673

Other transformation costs for Project Matterhorn, included as a component of Restructuring and other transformation in the accompanying Condensed Consolidated Statement of Operations, by segment, for the three and six months ended June 30, 2024 and 2023, and from the inception of Project Matterhorn through June 30, 2024, is as follows:

THREE MONTHS ENDED JUNE 30,

SIX MONTHS ENDED JUNE 30,

FROM THE INCEPTION

OF PROJECT

MATTERHORN THROUGH

JUNE 30, 2024

2024

2023

2024

2023

Global RIM Business

$

10,374

$

4,958

$

19,344

$

8,443

$

51,614

Global Data Center Business

1,272

498

2,663

1,368

7,685

Corporate and Other

18,531

24,005

38,211

44,606

147,456

Total other transformation costs

$

30,177

$

29,461

$

60,218

$

54,417

$

206,755

The rollforward of the accrued restructuring costs and accrued other transformation costs, which are included as components of Accrued expenses and other current liabilities in our Condensed Consolidated Balance Sheets, for December 31, 2023 through June 30, 2024, is as follows:

ITEM 2. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion and analysis of our financial condition and results of operations for the three and six months ended June 30, 2024 should be read in conjunction with our Condensed Consolidated Financial Statements and Notes thereto for the three and six months ended June 30, 2024, included herein, and our Consolidated Financial Statements and Notes thereto for the year ended December 31, 2023, included in our Annual Report on Form 10-K filed with the United States Securities and Exchange Commission ("SEC") on February 22, 2024 (our "Annual Report").

FORWARD-LOOKING STATEMENTS

We have made statements in this Quarterly Report that constitute "forward-looking statements" as that term is defined in the Private Securities Litigation Reform Act of 1995 and other securities laws. These forward-looking statements concern our current expectations regarding our future results from operations, economic performance, financial condition, goals, strategies, investment objectives, plans and achievements. These forward-looking statements are subject to various known and unknown risks, uncertainties and other factors, and you should not rely upon them except as statements of our present intentions and of our present expectations, which may or may not occur. When we use words such as "believes", "expects", "anticipates", "estimates", "plans", "intends", "pursue", "will" or similar expressions, we are making forward-looking statements. Although we believe that our forward-looking statements are based on reasonable assumptions, our expected results may not be achieved, and actual results may differ materially from our expectations. In addition, important factors that could cause actual results to differ from expectations include, among others:

•our ability or inability to execute our strategic growth plan, including our ability to invest according to plan, grow our businesses (including through joint ventures or other co-investment vehicles), incorporate alternative technologies (including artificial intelligence) into our offerings, achieve satisfactory returns on new product offerings, continue our revenue management, expand and manage our global operations, complete acquisitions on satisfactory terms, integrate acquired companies efficiently and transition to more sustainable sources of energy;

•changes in customer preferences and demand for our storage and information management services, including as a result of the shift from paper and tape storage to alternative technologies that require less physical space;

•the costs of complying with and our ability to comply with laws, regulations and customer requirements, including those relating to data privacy and cybersecurity issues, as well as fire and safety and environmental standards;

•the impact of attacks on our internal information technology ("IT") systems, including the impact of such incidents on our reputation and ability to compete and any litigation or disputes that may arise in connection with such incidents;

•our ability to fund capital expenditures;

•the impact of our distribution requirements on our ability to execute our business plan;

•our ability to remain qualified for taxation as a real estate investment trust for United States federal income tax purposes ("REIT");

•changes in the political and economic environments in the countries in which we operate and changes in the global political climate;

•our ability to raise debt or equity capital and changes in the cost of our debt;

•our ability to comply with our existing debt obligations and restrictions in our debt instruments;

•the impact of service interruptions or equipment damage and the cost of power on our data center operations;

•the cost or potential liabilities associated with real estate necessary for our business;

•unexpected events, including those resulting from climate change or geopolitical events, could disrupt our operations and adversely affect our reputation and results of operations;

•failures to implement and manage new IT systems;

•other trends in competitive or economic conditions affecting our financial condition or results of operations not presently contemplated; and

•the other risks described in our periodic reports filed with the SEC, including under the caption "Risk Factors" in Part I, Item 1A of our Annual Report.

Except as required by law, we undertake no obligation to update any forward-looking statements appearing in this report.

The following discussions set forth, for the periods indicated, management's discussion and analysis of financial condition and results of operations. Significant trends and changes are discussed for the three and six months ended June 30, 2024 within each section. Trends and changes that are consistent for both the three and six month periods are not repeated and are discussed on a year to date basis only.

PROJECT MATTERHORN

In September 2022, we announced a global program designed to accelerate the growth of our business ("Project Matterhorn"). Project Matterhorn investments focus on transforming our operating model to a global operating model. Project Matterhorn focuses on the formation of a solution-based sales approach that is designed to allow us to optimize our shared services and best practices to better serve our customers' needs. We are investing to accelerate growth and to capture a greater share of the large, global addressable markets in which we operate. We expect to incur approximately $150.0 million in costs annually related to Project Matterhorn from 2023 through 2025. Costs are comprised of (1) restructuring costs, which include (i) site consolidation and other related exit costs, (ii) employee severance costs and (iii) certain professional fees associated with these activities, and (2) other transformation costs, which include professional fees such as project management costs and costs for third party consultants who are assisting in the enablement of our growth initiatives.

See Note 11 to Notes to Condensed Consolidated Financial Statements included in this Quarterly Report for more information on Restructuring and other transformation costs.

GENERAL

RESULTS OF OPERATIONS - KEY TRENDS

•Our organic storage rental revenue growth is primarily driven by revenue management in our Global RIM Business segment, where we expect volume to be relatively stable in the near term, as well as by growth in our Global Data Center Business segment, primarily driven by lease commencements.

•Our organic service revenue growth is primarily due to increases in our service activity. We expect organic service revenue growth in 2024 to benefit from our new and existing digital offerings and asset lifecycle management ("ALM") business, as well as our traditional services.

•We expect continued total revenue and Adjusted EBITDA growth in 2024 as a result of our focus on new product and service offerings, innovation, customer solutions and market expansion in line with our Project Matterhorn objectives.

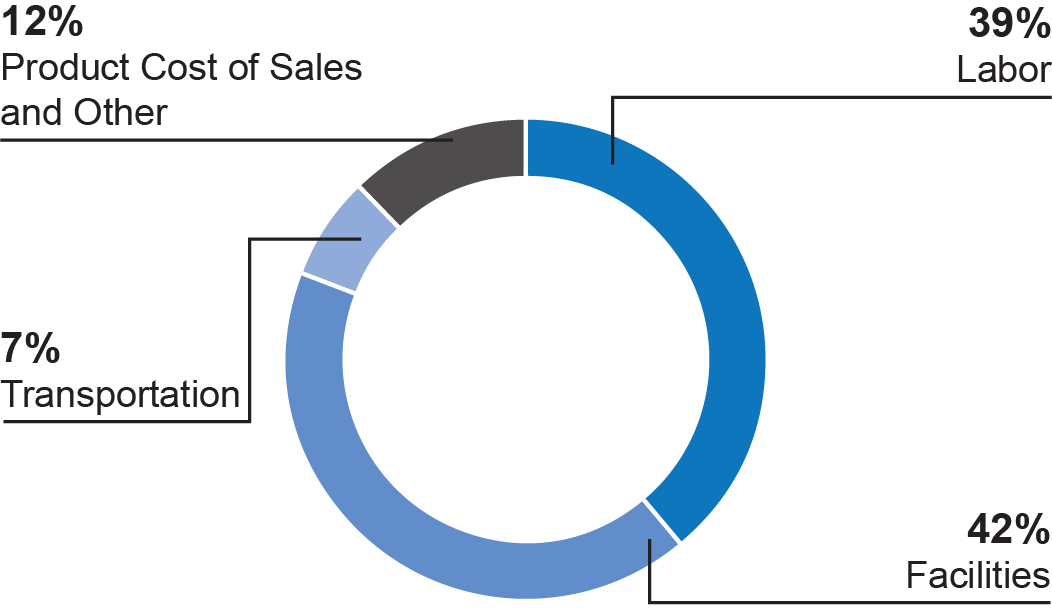

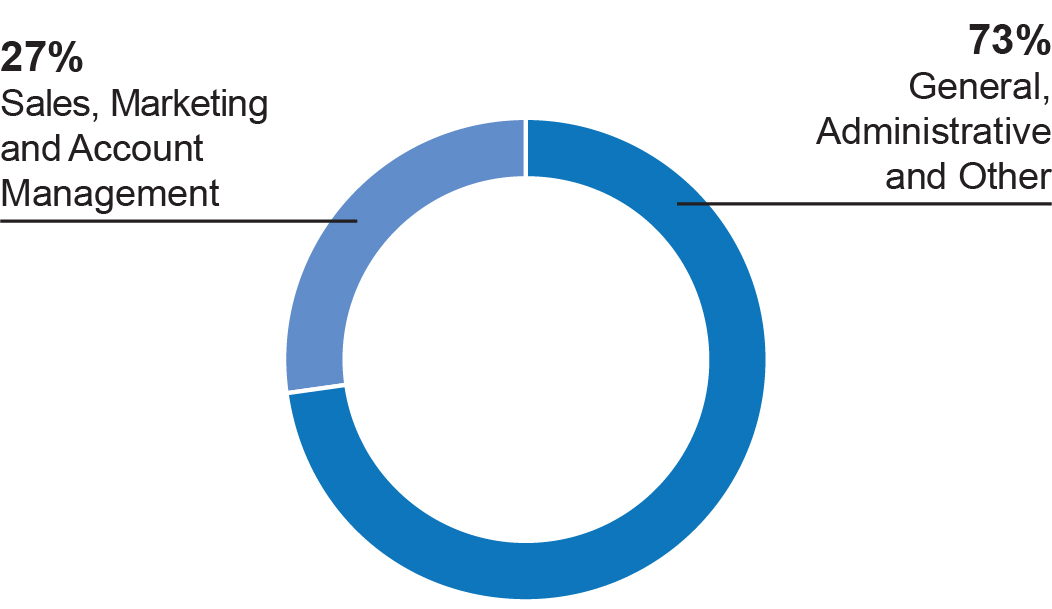

Cost of sales (excluding depreciation and amortization) and Selling, general and administrative expenses for the six months ended June 30, 2024 consists of the following:

We define Adjusted EBITDA as net income (loss) before interest expense, net, provision (benefit) for income taxes, depreciation and amortization (inclusive of our share of Adjusted EBITDA from our unconsolidated joint ventures), and excluding certain items we do not believe to be indicative of our core operating results, specifically:

EXCLUDED

•Acquisition and Integration Costs (as defined below)

•Restructuring and other transformation

•Loss (gain) on disposal/write-down of property, plant and equipment, net (including real estate)

•Other expense (income), net

•Stock-based compensation expense

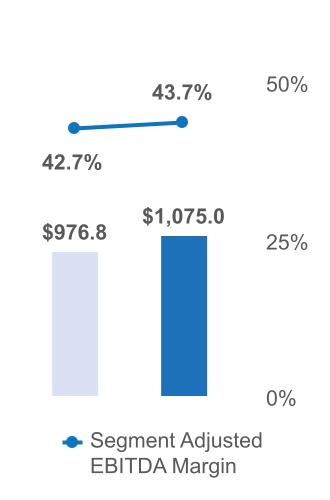

Adjusted EBITDA Margin is calculated by dividing Adjusted EBITDA by total revenues. We also show Adjusted EBITDA and Adjusted EBITDA Margin for each of our reportable segments under "Results of Operations – Segment Analysis" below.

Adjusted EBITDA excludes both interest expense, net and the provision (benefit) for income taxes. These expenses are associated with our capitalization and tax structures, which we do not consider when evaluating the operating profitability of our core operations. Adjusted EBITDA does not include depreciation and amortization expenses, in order to eliminate the impact of capital investments, which we evaluate by comparing capital expenditures to incremental revenue generated and as a percentage of total revenues. Adjusted EBITDA and Adjusted EBITDA Margin should be considered in addition to, but not as a substitute for, other measures of financial performance reported in accordance with accounting principles generally accepted in the United States of America ("GAAP"), such as operating income, net income (loss) or cash flows from operating activities.

RECONCILIATION OF NET INCOME (LOSS) TO ADJUSTED EBITDA (IN THOUSANDS):

THREE MONTHS ENDED JUNE 30,

SIX MONTHS ENDED JUNE 30,

2024

2023

2024

2023

Net Income (Loss)

$

34,621

$

1,143

$

111,646

$

66,678

Add/(Deduct):

Interest expense, net

176,521

144,178

341,040

281,347

Provision (benefit) for income taxes

13,319

4,255

29,928

21,013

Depreciation and amortization

224,501

195,367

434,056

377,461

Acquisition and Integration Costs(1)

9,502

1,511