false2025FYGENESIS ENERGY LP0001022321122,424,32139,997P1YP1YP1YP1YP1YP1YP1YP1YP1YP1YP1YP1Yhttp://fasb.org/us-gaap/2025#AccruedLiabilitiesCurrenthttp://fasb.org/us-gaap/2025#AccruedLiabilitiesCurrenthttp://fasb.org/us-gaap/2025#OtherLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2025#OtherLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2025#AssetImpairmentChargesP1Y6.5iso4217:USDxbrli:sharesxbrli:pureiso4217:USDxbrli:sharesgel:segmentgel:extensiongel:metricgel:buyergel:quartersgel:directorutr:bbliso4217:USDutr:bblutr:MMBTUiso4217:USDutr:MMBTU00010223212025-01-012025-12-3100010223212025-06-300001022321us-gaap:CommonClassAMember2026-02-180001022321us-gaap:CommonClassBMember2026-02-180001022321gel:AlkaliBusinessMember2025-02-280001022321gel:AlkaliBusinessMember2025-02-282025-02-280001022321gel:FivePointEightSevenFivePercentageSeniorSecuredNoteMemberus-gaap:SeniorNotesMember2025-02-280001022321us-gaap:ConvertiblePreferredStockMember2025-03-062025-03-060001022321gel:EightPercentageSeniorUnsecuredNotesMemberus-gaap:SeniorNotesMember2025-04-032025-04-030001022321gel:PoseidonOilPipelineCompanyMembergel:OffshorePipelineTransportationMember2025-12-310001022321gel:OdysseyPipelineLLCMembergel:OffshorePipelineTransportationMember2025-12-310001022321gel:NeptunePipelineCompanyLLCMembergel:OffshorePipelineTransportationMember2025-12-3100010223212025-10-012025-12-3100010223212025-12-3100010223212024-12-310001022321us-gaap:ConvertiblePreferredStockMember2025-12-310001022321us-gaap:ConvertiblePreferredStockMember2024-12-310001022321gel:OffshorePipelineTransportationRevenueMembergel:OffshorePipelineTransportationSegmentMember2025-01-012025-12-310001022321gel:OffshorePipelineTransportationRevenueMembergel:OffshorePipelineTransportationSegmentMember2024-01-012024-12-310001022321gel:OffshorePipelineTransportationRevenueMembergel:OffshorePipelineTransportationSegmentMember2023-01-012023-12-310001022321gel:MarineTransportationRevenueMembergel:MarineTransportationSegmentMember2025-01-012025-12-310001022321gel:MarineTransportationRevenueMembergel:MarineTransportationSegmentMember2024-01-012024-12-310001022321gel:MarineTransportationRevenueMembergel:MarineTransportationSegmentMember2023-01-012023-12-310001022321gel:OnshoreFacilitiesAndTransportationRevenueMembergel:OnshoreTransportationAndServicesSegmentMember2025-01-012025-12-310001022321gel:OnshoreFacilitiesAndTransportationRevenueMembergel:OnshoreTransportationAndServicesSegmentMember2024-01-012024-12-310001022321gel:OnshoreFacilitiesAndTransportationRevenueMembergel:OnshoreTransportationAndServicesSegmentMember2023-01-012023-12-3100010223212024-01-012024-12-3100010223212023-01-012023-12-310001022321gel:OffshorePipelineTransportationRevenueMember2025-01-012025-12-310001022321gel:OffshorePipelineTransportationRevenueMember2024-01-012024-12-310001022321gel:OffshorePipelineTransportationRevenueMember2023-01-012023-12-310001022321gel:MarineTransportationRevenueMember2025-01-012025-12-310001022321gel:MarineTransportationRevenueMember2024-01-012024-12-310001022321gel:MarineTransportationRevenueMember2023-01-012023-12-310001022321gel:OnshoreFacilitiesAndTransportationProductMember2025-01-012025-12-310001022321gel:OnshoreFacilitiesAndTransportationProductMember2024-01-012024-12-310001022321gel:OnshoreFacilitiesAndTransportationProductMember2023-01-012023-12-310001022321gel:OnshoreTransportationAndServicesMember2025-01-012025-12-310001022321gel:OnshoreTransportationAndServicesMember2024-01-012024-12-310001022321gel:OnshoreTransportationAndServicesMember2023-01-012023-12-310001022321gel:PartnersCapitalDeficitMember2022-12-310001022321us-gaap:NoncontrollingInterestMember2022-12-310001022321us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-3100010223212022-12-310001022321gel:PartnersCapitalDeficitMember2023-01-012023-12-310001022321us-gaap:NoncontrollingInterestMember2023-01-012023-12-310001022321us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-01-012023-12-310001022321gel:PartnersCapitalDeficitMember2023-12-310001022321us-gaap:NoncontrollingInterestMember2023-12-310001022321us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-12-3100010223212023-12-310001022321gel:PartnersCapitalDeficitMember2024-01-012024-12-310001022321us-gaap:NoncontrollingInterestMember2024-01-012024-12-310001022321us-gaap:AccumulatedOtherComprehensiveIncomeMember2024-01-012024-12-310001022321gel:PartnersCapitalDeficitMember2024-12-310001022321us-gaap:NoncontrollingInterestMember2024-12-310001022321us-gaap:AccumulatedOtherComprehensiveIncomeMember2024-12-310001022321gel:PartnersCapitalDeficitMember2025-01-012025-12-310001022321us-gaap:NoncontrollingInterestMember2025-01-012025-12-310001022321us-gaap:AccumulatedOtherComprehensiveIncomeMember2025-01-012025-12-310001022321gel:PartnersCapitalDeficitMember2025-12-310001022321us-gaap:NoncontrollingInterestMember2025-12-310001022321us-gaap:AccumulatedOtherComprehensiveIncomeMember2025-12-310001022321gel:GenesisEnergyLLCMember2025-01-012025-12-310001022321gel:NeptunePipelineCompanyLLCMembergel:PalomaPipelineCompanyMember2025-12-310001022321srt:MinimumMemberus-gaap:PipelinesMember2025-12-310001022321srt:MaximumMemberus-gaap:PipelinesMember2025-12-310001022321srt:MinimumMembergel:MarineVesselsMember2025-12-310001022321srt:MaximumMembergel:MarineVesselsMember2025-12-310001022321srt:MinimumMemberus-gaap:MachineryAndEquipmentMember2025-12-310001022321srt:MaximumMemberus-gaap:MachineryAndEquipmentMember2025-12-310001022321srt:MinimumMemberus-gaap:TransportationEquipmentMember2025-12-310001022321srt:MaximumMemberus-gaap:TransportationEquipmentMember2025-12-310001022321srt:MinimumMemberus-gaap:BuildingAndBuildingImprovementsMember2025-12-310001022321srt:MaximumMemberus-gaap:BuildingAndBuildingImprovementsMember2025-12-310001022321gel:FeebasedRevenuesMembergel:OffshorePipelineTransportationSegmentMember2025-01-012025-12-310001022321gel:FeebasedRevenuesMembergel:MarineTransportationSegmentMember2025-01-012025-12-310001022321gel:FeebasedRevenuesMembergel:OnshoreTransportationAndServicesSegmentMember2025-01-012025-12-310001022321gel:FeebasedRevenuesMember2025-01-012025-12-310001022321gel:ProductSalesMembergel:OffshorePipelineTransportationSegmentMember2025-01-012025-12-310001022321gel:ProductSalesMembergel:MarineTransportationSegmentMember2025-01-012025-12-310001022321gel:ProductSalesMembergel:OnshoreTransportationAndServicesSegmentMember2025-01-012025-12-310001022321gel:ProductSalesMember2025-01-012025-12-310001022321gel:RefineryServicesMembergel:OffshorePipelineTransportationSegmentMember2025-01-012025-12-310001022321gel:RefineryServicesMembergel:MarineTransportationSegmentMember2025-01-012025-12-310001022321gel:RefineryServicesMembergel:OnshoreTransportationAndServicesSegmentMember2025-01-012025-12-310001022321gel:RefineryServicesMember2025-01-012025-12-310001022321gel:OffshorePipelineTransportationSegmentMember2025-01-012025-12-310001022321gel:MarineTransportationSegmentMember2025-01-012025-12-310001022321gel:OnshoreTransportationAndServicesSegmentMember2025-01-012025-12-310001022321gel:FeebasedRevenuesMembergel:OffshorePipelineTransportationSegmentMember2024-01-012024-12-310001022321gel:FeebasedRevenuesMembergel:MarineTransportationSegmentMember2024-01-012024-12-310001022321gel:FeebasedRevenuesMembergel:OnshoreTransportationAndServicesSegmentMember2024-01-012024-12-310001022321gel:FeebasedRevenuesMember2024-01-012024-12-310001022321gel:ProductSalesMembergel:OffshorePipelineTransportationSegmentMember2024-01-012024-12-310001022321gel:ProductSalesMembergel:MarineTransportationSegmentMember2024-01-012024-12-310001022321gel:ProductSalesMembergel:OnshoreTransportationAndServicesSegmentMember2024-01-012024-12-310001022321gel:ProductSalesMember2024-01-012024-12-310001022321gel:RefineryServicesMembergel:OffshorePipelineTransportationSegmentMember2024-01-012024-12-310001022321gel:RefineryServicesMembergel:MarineTransportationSegmentMember2024-01-012024-12-310001022321gel:RefineryServicesMembergel:OnshoreTransportationAndServicesSegmentMember2024-01-012024-12-310001022321gel:RefineryServicesMember2024-01-012024-12-310001022321gel:OffshorePipelineTransportationSegmentMember2024-01-012024-12-310001022321gel:MarineTransportationSegmentMember2024-01-012024-12-310001022321gel:OnshoreTransportationAndServicesSegmentMember2024-01-012024-12-310001022321gel:FeebasedRevenuesMembergel:OffshorePipelineTransportationSegmentMember2023-01-012023-12-310001022321gel:FeebasedRevenuesMembergel:MarineTransportationSegmentMember2023-01-012023-12-310001022321gel:FeebasedRevenuesMembergel:OnshoreTransportationAndServicesSegmentMember2023-01-012023-12-310001022321gel:FeebasedRevenuesMember2023-01-012023-12-310001022321gel:ProductSalesMembergel:OffshorePipelineTransportationSegmentMember2023-01-012023-12-310001022321gel:ProductSalesMembergel:MarineTransportationSegmentMember2023-01-012023-12-310001022321gel:ProductSalesMembergel:OnshoreTransportationAndServicesSegmentMember2023-01-012023-12-310001022321gel:ProductSalesMember2023-01-012023-12-310001022321gel:RefineryServicesMembergel:OffshorePipelineTransportationSegmentMember2023-01-012023-12-310001022321gel:RefineryServicesMembergel:MarineTransportationSegmentMember2023-01-012023-12-310001022321gel:RefineryServicesMembergel:OnshoreTransportationAndServicesSegmentMember2023-01-012023-12-310001022321gel:RefineryServicesMember2023-01-012023-12-310001022321gel:OffshorePipelineTransportationSegmentMember2023-01-012023-12-310001022321gel:MarineTransportationSegmentMember2023-01-012023-12-310001022321gel:OnshoreTransportationAndServicesSegmentMember2023-01-012023-12-310001022321gel:OffshorePipelineTransportationMember2025-01-012025-12-310001022321gel:OnshoreFacilitiesandTransportationMember2025-01-012025-12-310001022321gel:OffshorePipelineTransportationMember2026-01-012025-12-310001022321gel:OnshoreFacilitiesandTransportationMember2026-01-012025-12-310001022321gel:OffshorePipelineTransportationMember2027-01-012025-12-310001022321gel:OnshoreFacilitiesandTransportationMember2027-01-012025-12-310001022321gel:OffshorePipelineTransportationMember2028-01-012025-12-310001022321gel:OnshoreFacilitiesandTransportationMember2028-01-012025-12-310001022321gel:OffshorePipelineTransportationMember2029-01-012025-12-310001022321gel:OnshoreFacilitiesandTransportationMember2029-01-012025-12-310001022321gel:OffshorePipelineTransportationMember2030-01-012025-12-310001022321gel:OnshoreFacilitiesandTransportationMember2030-01-012025-12-310001022321gel:OffshorePipelineTransportationMember2025-12-310001022321gel:OnshoreFacilitiesandTransportationMember2025-12-310001022321us-gaap:DisposalGroupHeldforsaleNotDiscontinuedOperationsMember2025-01-012025-12-310001022321us-gaap:DisposalGroupHeldforsaleNotDiscontinuedOperationsMember2024-01-012024-12-310001022321us-gaap:DisposalGroupHeldforsaleNotDiscontinuedOperationsMember2023-01-012023-12-310001022321us-gaap:DiscontinuedOperationsDisposedOfBySaleMember2025-01-012025-12-310001022321us-gaap:DiscontinuedOperationsDisposedOfBySaleMember2024-01-012024-12-310001022321us-gaap:DiscontinuedOperationsDisposedOfBySaleMember2023-01-012023-12-310001022321us-gaap:TransportationEquipmentMember2025-12-310001022321us-gaap:TransportationEquipmentMember2024-12-310001022321gel:OfficeSpaceandEquipmentMember2025-12-310001022321gel:OfficeSpaceandEquipmentMember2024-12-310001022321gel:FacilitiesandEquipmentMember2025-12-310001022321gel:FacilitiesandEquipmentMember2024-12-310001022321gel:MarineTransportationMember2025-01-012025-12-310001022321gel:MarineTransportationMember2024-01-012024-12-310001022321gel:MarineTransportationMember2023-01-012023-12-310001022321gel:MarineTransportationMember2025-12-310001022321us-gaap:PipelinesMember2025-12-310001022321us-gaap:PipelinesMember2024-12-310001022321us-gaap:MachineryAndEquipmentMember2025-12-310001022321us-gaap:MachineryAndEquipmentMember2024-12-310001022321us-gaap:MaritimeEquipmentMember2025-12-310001022321us-gaap:MaritimeEquipmentMember2024-12-310001022321us-gaap:LandBuildingsAndImprovementsMember2025-12-310001022321us-gaap:LandBuildingsAndImprovementsMember2024-12-310001022321us-gaap:FurnitureAndFixturesMember2025-12-310001022321us-gaap:FurnitureAndFixturesMember2024-12-310001022321us-gaap:ConstructionInProgressMember2025-12-310001022321us-gaap:ConstructionInProgressMember2024-12-310001022321us-gaap:PropertyPlantAndEquipmentOtherTypesMember2025-12-310001022321us-gaap:PropertyPlantAndEquipmentOtherTypesMember2024-12-310001022321us-gaap:AccruedLiabilitiesMember2025-12-310001022321us-gaap:AccruedLiabilitiesMember2024-12-310001022321us-gaap:ContractualRightsMembergel:OffshorePipelineTransportationMember2025-12-310001022321us-gaap:ContractualRightsMembergel:OffshorePipelineTransportationMember2024-12-310001022321us-gaap:OtherIntangibleAssetsMember2025-12-310001022321us-gaap:OtherIntangibleAssetsMember2024-12-310001022321us-gaap:ContractualRightsMember2025-12-310001022321gel:SodiumMineralsAndSulfurServicesSegmentMember2024-12-310001022321gel:SodiumMineralsAndSulfurServicesSegmentMember2025-12-310001022321us-gaap:RevolvingCreditFacilityMembergel:SeniorSecuredCreditFacilityMemberus-gaap:LineOfCreditMember2025-12-310001022321us-gaap:RevolvingCreditFacilityMembergel:SeniorSecuredCreditFacilityMemberus-gaap:LineOfCreditMember2024-12-310001022321gel:EightPercentageSeniorUnsecuredNotesMemberus-gaap:SeniorNotesMember2025-12-310001022321gel:EightPercentageSeniorUnsecuredNotesMemberus-gaap:SeniorNotesMember2024-12-310001022321gel:SevenPointSevenFivePercentageSeniorUnsecuredNoteMemberus-gaap:SeniorNotesMember2025-12-310001022321gel:SevenPointSevenFivePercentageSeniorUnsecuredNoteMemberus-gaap:SeniorNotesMember2024-12-310001022321gel:A8.250SeniorUnsecuredNotesDue2029Memberus-gaap:SeniorNotesMember2025-12-310001022321gel:A8.250SeniorUnsecuredNotesDue2029Memberus-gaap:SeniorNotesMember2024-12-310001022321gel:A8.875SeniorUnsecuredNotesDue2030Memberus-gaap:SeniorNotesMember2025-12-310001022321gel:A8.875SeniorUnsecuredNotesDue2030Memberus-gaap:SeniorNotesMember2024-12-310001022321gel:A7.875SeniorUnsecuredNotesDue2032Memberus-gaap:SeniorNotesMember2025-12-310001022321gel:A7.875SeniorUnsecuredNotesDue2032Memberus-gaap:SeniorNotesMember2024-12-310001022321gel:A8.000SeniorUnsecuredNotesDue2033Memberus-gaap:SeniorNotesMember2025-12-310001022321gel:A8.000SeniorUnsecuredNotesDue2033Memberus-gaap:SeniorNotesMember2024-12-310001022321us-gaap:RevolvingCreditFacilityMembergel:SeniorSecuredCreditFacilityRevolvingMemberus-gaap:LineOfCreditMember2025-12-310001022321us-gaap:RevolvingCreditFacilityMembergel:SeniorSecuredCreditFacilityRevolvingMemberus-gaap:LineOfCreditMember2024-12-310001022321us-gaap:RevolvingCreditFacilityMembergel:SeniorSecuredCreditFacilityRevolvingMemberus-gaap:LineOfCreditMember2024-07-190001022321gel:SeniorSecuredCreditFacilityMemberus-gaap:LineOfCreditMember2024-07-192024-07-190001022321gel:SevenPointSevenFivePercentageSeniorUnsecuredNoteMemberus-gaap:SeniorNotesMember2024-07-190001022321us-gaap:RevolvingCreditFacilityMembergel:SeniorSecuredCreditFacilityRevolvingMemberus-gaap:LineOfCreditMember2025-02-270001022321gel:SeniorSecuredCreditFacilityMemberus-gaap:LineOfCreditMember2025-02-270001022321us-gaap:RevolvingCreditFacilityMembergel:FederalFundsEffectiveRateMembergel:SeniorSecuredCreditFacilityRevolvingMemberus-gaap:LineOfCreditMember2025-01-012025-12-310001022321us-gaap:RevolvingCreditFacilityMembergel:LiborRateMembergel:SeniorSecuredCreditFacilityRevolvingMembersrt:MaximumMemberus-gaap:LineOfCreditMember2025-01-012025-12-310001022321gel:TermSOFRAdjustmentMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMembergel:SeniorSecuredCreditFacilityRevolvingMembersrt:MaximumMemberus-gaap:LineOfCreditMember2025-01-012025-12-310001022321us-gaap:RevolvingCreditFacilityMembergel:AlternateBaseRateMembergel:SeniorSecuredCreditFacilityRevolvingMembersrt:MinimumMemberus-gaap:LineOfCreditMember2025-01-012025-12-310001022321us-gaap:RevolvingCreditFacilityMembergel:AlternateBaseRateMembergel:SeniorSecuredCreditFacilityRevolvingMembersrt:MaximumMemberus-gaap:LineOfCreditMember2025-01-012025-12-310001022321us-gaap:RevolvingCreditFacilityMembergel:EurodollarRateMembergel:SeniorSecuredCreditFacilityRevolvingMembersrt:MinimumMemberus-gaap:LineOfCreditMember2025-01-012025-12-310001022321us-gaap:RevolvingCreditFacilityMembergel:EurodollarRateMembergel:SeniorSecuredCreditFacilityRevolvingMembersrt:MaximumMemberus-gaap:LineOfCreditMember2025-01-012025-12-310001022321us-gaap:RevolvingCreditFacilityMembergel:AlternateBaseRateMembergel:SeniorSecuredCreditFacilityRevolvingMemberus-gaap:LineOfCreditMember2025-12-312025-12-310001022321us-gaap:RevolvingCreditFacilityMemberus-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMembergel:SeniorSecuredCreditFacilityRevolvingMemberus-gaap:LineOfCreditMember2025-12-312025-12-310001022321us-gaap:RevolvingCreditFacilityMembergel:SeniorSecuredCreditFacilityMembersrt:MinimumMemberus-gaap:LineOfCreditMember2025-01-012025-12-310001022321us-gaap:RevolvingCreditFacilityMembergel:SeniorSecuredCreditFacilityMembersrt:MaximumMemberus-gaap:LineOfCreditMember2025-01-012025-12-310001022321us-gaap:RevolvingCreditFacilityMembergel:SeniorSecuredCreditFacilityMemberus-gaap:LineOfCreditMember2025-12-312025-12-310001022321us-gaap:RevolvingCreditFacilityMembergel:SeniorSecuredCreditFacilityRevolvingMembersrt:MinimumMemberus-gaap:LineOfCreditMember2025-01-012025-12-310001022321us-gaap:RevolvingCreditFacilityMembergel:SeniorSecuredCreditFacilityRevolvingMembersrt:MaximumMemberus-gaap:LineOfCreditMember2025-01-012025-12-310001022321us-gaap:RevolvingCreditFacilityMembergel:SeniorSecuredCreditFacilityRevolvingMemberus-gaap:LineOfCreditMember2025-12-312025-12-310001022321us-gaap:RevolvingCreditFacilityMembergel:SeniorSecuredCreditFacilityRevolvingMemberus-gaap:LineOfCreditMemberus-gaap:PublicUtilitiesInventoryPetroleumProductsMember2025-12-310001022321us-gaap:BridgeLoanMembergel:SeniorSecuredCreditFacilityRevolvingMemberus-gaap:LineOfCreditMemberus-gaap:PublicUtilitiesInventoryPetroleumProductsMember2025-12-310001022321us-gaap:RevolvingCreditFacilityMembergel:SeniorSecuredCreditFacilityRevolvingMembersrt:MaximumMemberus-gaap:LineOfCreditMember2025-12-310001022321gel:SevenPointSevenFivePercentageSeniorUnsecuredNoteMemberus-gaap:SeniorNotesMember2020-01-160001022321gel:SevenPointSevenFivePercentageSeniorUnsecuredNoteMemberus-gaap:SeniorNotesMember2020-01-162020-01-160001022321gel:SixPointSevenFivePercentageSeniorUnsecuredNotesMemberus-gaap:SeniorNotesMember2020-01-160001022321gel:EightPercentageSeniorUnsecuredNotesMemberus-gaap:SeniorNotesMember2020-12-170001022321gel:EightPercentageSeniorUnsecuredNotesMemberus-gaap:SeniorNotesMember2021-04-220001022321gel:EightPercentageSeniorUnsecuredNotesMemberus-gaap:SeniorNotesMember2024-12-202024-12-200001022321gel:A2029NotesMemberus-gaap:SeniorNotesMember2024-12-190001022321gel:A2030NotesMemberus-gaap:SeniorNotesMember2023-01-250001022321gel:A2030NotesMemberus-gaap:SeniorNotesMember2023-01-252023-01-250001022321us-gaap:SeniorNotesMembergel:FivePointSixTwoFivePercentageSeniorUnsecuredNotesMember2023-01-252023-01-250001022321gel:FivePointSixTwoFivePercentageSeniorUnsecuredNotesMemberus-gaap:SeniorNotesMember2023-01-250001022321us-gaap:SeniorNotesMembergel:FivePointSixTwoFivePercentageSeniorUnsecuredNotesMember2023-01-250001022321gel:A2029NotesMemberus-gaap:SeniorNotesMember2023-12-070001022321gel:A2029NotesMemberus-gaap:SeniorNotesMember2023-12-072023-12-070001022321us-gaap:SeniorNotesMembergel:SixPointfivepercentageSeniorUnsecuredNotesDue2025Member2023-12-072023-12-070001022321us-gaap:SeniorNotesMembergel:SixPointfivepercentageSeniorUnsecuredNotesDue2025Member2023-12-070001022321us-gaap:SeniorNotesMembergel:A2032NotesMember2024-05-090001022321gel:FivePointEightSevenFivePercentageSeniorSecuredNoteMemberus-gaap:SeniorNotesMember2024-05-092024-05-090001022321gel:SixpointtwofivepercentageseniorunsecurednotesMemberus-gaap:SeniorNotesMember2017-12-110001022321gel:SixpointtwofivepercentageseniorunsecurednotesMemberus-gaap:SeniorNotesMember2024-05-092024-05-090001022321gel:SixpointtwofivepercentageseniorunsecurednotesMemberus-gaap:SeniorNotesMember2024-01-012024-12-310001022321gel:A2029NotesMemberus-gaap:SeniorNotesMember2024-12-192024-12-190001022321us-gaap:SeniorNotesMembergel:SixPointfivepercentageSeniorUnsecuredNotesDue2025Member2024-12-192024-12-190001022321us-gaap:SeniorNotesMembergel:FivePointSixTwoFivePercentageSeniorUnsecuredNotesMember2024-12-192024-12-190001022321us-gaap:SeniorNotesMember2025-01-012025-12-310001022321gel:FivePointSixTwoFivePercentageSeniorUnsecuredNotesMemberus-gaap:SeniorNotesMember2025-01-012025-12-310001022321gel:SixpointtwofivepercentageseniorunsecurednotesMemberus-gaap:SeniorNotesMember2025-01-012025-12-310001022321gel:SixPointfivepercentageSeniorUnsecuredNotesDue2025Memberus-gaap:SeniorNotesMember2025-01-012025-12-310001022321gel:EightPercentageSeniorUnsecuredNotesMemberus-gaap:SeniorNotesMember2025-01-012025-12-310001022321us-gaap:SeniorNotesMember2025-12-310001022321gel:GenesisEnergyLLCMembersrt:GuarantorSubsidiariesMembergel:GenesisFinanceCorporationMemberus-gaap:SeniorNotesMember2025-01-012025-12-310001022321gel:SeniorSecuredCreditFacilityMemberus-gaap:LineOfCreditMember2025-12-310001022321gel:DebtCovenantPeriodTwoMembergel:SeniorSecuredCreditFacilityMemberus-gaap:LineOfCreditMember2025-12-310001022321gel:DebtCovenantPeriodOneMembergel:SeniorSecuredCreditFacilityMemberus-gaap:LineOfCreditMember2025-12-310001022321gel:DebtCovenantPeriodThreeMembergel:SeniorSecuredCreditFacilityMemberus-gaap:LineOfCreditMember2025-12-310001022321us-gaap:LimitedPartnerMemberus-gaap:CommonClassAMember2025-12-310001022321us-gaap:LimitedPartnerMemberus-gaap:CommonClassBMember2025-12-310001022321us-gaap:LimitedPartnerMemberus-gaap:PreferredClassAMember2025-12-310001022321gel:A2023RepurchaseProgramMemberus-gaap:CommonClassAMember2023-08-080001022321gel:A2023RepurchaseProgramMemberus-gaap:CommonClassAMember2023-01-012023-12-310001022321gel:CommonUnitholdersMember2023-05-152023-05-150001022321gel:CommonUnitholdersMember2023-05-150001022321gel:CommonUnitholdersMember2023-08-142023-08-140001022321gel:CommonUnitholdersMember2023-08-140001022321gel:CommonUnitholdersMember2023-11-142023-11-140001022321gel:CommonUnitholdersMember2023-11-140001022321gel:CommonUnitholdersMember2024-02-142024-02-140001022321gel:CommonUnitholdersMember2024-02-140001022321gel:CommonUnitholdersMember2024-05-152024-05-150001022321gel:CommonUnitholdersMember2024-05-150001022321gel:CommonUnitholdersMember2024-08-142024-08-140001022321gel:CommonUnitholdersMember2024-08-140001022321gel:CommonUnitholdersMember2024-11-142024-11-140001022321gel:CommonUnitholdersMember2024-11-140001022321gel:CommonUnitholdersMember2025-02-142025-02-140001022321gel:CommonUnitholdersMember2025-02-140001022321gel:CommonUnitholdersMember2025-05-152025-05-150001022321gel:CommonUnitholdersMember2025-05-150001022321gel:CommonUnitholdersMember2025-08-142025-08-140001022321gel:CommonUnitholdersMember2025-08-140001022321gel:CommonUnitholdersMember2025-11-142025-11-140001022321gel:CommonUnitholdersMember2025-11-140001022321gel:CommonUnitholdersMemberus-gaap:SubsequentEventMember2026-02-142026-02-140001022321gel:CommonUnitholdersMemberus-gaap:SubsequentEventMember2026-02-140001022321us-gaap:ConvertiblePreferredStockMemberus-gaap:PrivatePlacementMember2017-09-012017-09-010001022321us-gaap:ConvertiblePreferredStockMemberus-gaap:PrivatePlacementMember2017-09-010001022321us-gaap:ConvertiblePreferredStockMember2017-09-010001022321us-gaap:ConvertiblePreferredStockMember2017-09-012017-09-010001022321srt:MinimumMemberus-gaap:ConvertiblePreferredStockMember2017-09-012017-09-010001022321srt:MaximumMemberus-gaap:ConvertiblePreferredStockMember2017-09-012017-09-010001022321us-gaap:ConvertiblePreferredStockMembergel:InArrearsAtAnnualRateMember2017-09-012017-09-010001022321us-gaap:ConvertiblePreferredStockMembergel:QuarterlyRateMember2017-09-012017-09-010001022321us-gaap:ConvertiblePreferredStockMember2022-09-290001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2025-12-310001022321us-gaap:ConvertiblePreferredStockMember2019-09-012019-09-010001022321us-gaap:ConvertiblePreferredStockMember2019-09-010001022321us-gaap:ConvertiblePreferredStockMember2019-03-012019-03-010001022321us-gaap:ConvertiblePreferredStockMember2019-03-010001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2023-05-150001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2023-05-152023-05-150001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2023-08-140001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2023-08-142023-08-140001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2023-11-140001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2023-11-142023-11-140001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2024-02-140001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2024-02-142024-02-140001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2024-05-150001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2024-05-152024-05-150001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2024-08-140001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2024-08-142024-08-140001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2024-11-140001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2024-11-142024-11-140001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2025-02-140001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2025-02-142025-02-140001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2025-05-150001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2025-05-152025-05-150001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2025-08-140001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2025-08-142025-08-140001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2025-11-140001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2025-11-142025-11-140001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMemberus-gaap:SubsequentEventMember2026-02-140001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMemberus-gaap:SubsequentEventMember2026-02-142026-02-140001022321us-gaap:ConvertiblePreferredStockMember2023-10-032023-10-030001022321us-gaap:ConvertiblePreferredStockMember2023-07-032023-07-030001022321us-gaap:ConvertiblePreferredStockMember2023-04-032023-04-030001022321us-gaap:ConvertiblePreferredStockMember2023-04-030001022321us-gaap:ConvertiblePreferredStockMember2025-03-060001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2025-03-062025-03-060001022321us-gaap:ConvertiblePreferredStockMembergel:PreferredUnitholdersMember2025-03-060001022321us-gaap:ConvertiblePreferredStockMember2025-01-012025-12-310001022321us-gaap:ConvertiblePreferredStockMember2024-01-012024-12-310001022321us-gaap:ConvertiblePreferredStockMember2023-01-012023-12-310001022321gel:CameronHighwayOilPipelineMembersrt:AffiliatedEntityMember2021-11-162021-11-160001022321gel:CameronHighwayOilPipelineMembersrt:AffiliatedEntityMember2021-11-172021-11-170001022321gel:CameronHighwayOilPipelineMembersrt:AffiliatedEntityMember2021-11-172021-12-310001022321gel:GenesisEnergyLLCMembersrt:AffiliatedEntityMembergel:IndependenceHubLLCMember2025-12-310001022321gel:GenesisAlkaliHoldingsCompanyLLCMembersrt:SubsidiariesMember2019-09-232019-09-230001022321us-gaap:OperatingSegmentsMembergel:OffshorePipelineTransportationSegmentMember2025-01-012025-12-310001022321us-gaap:OperatingSegmentsMembergel:MarineTransportationSegmentMember2025-01-012025-12-310001022321us-gaap:OperatingSegmentsMembergel:OnshoreFacilitiesAndTransportationSegmentMember2025-01-012025-12-310001022321us-gaap:OperatingSegmentsMember2025-01-012025-12-310001022321us-gaap:IntersegmentEliminationMembergel:OffshorePipelineTransportationSegmentMember2025-01-012025-12-310001022321us-gaap:IntersegmentEliminationMembergel:MarineTransportationSegmentMember2025-01-012025-12-310001022321us-gaap:IntersegmentEliminationMembergel:OnshoreFacilitiesAndTransportationSegmentMember2025-01-012025-12-310001022321us-gaap:IntersegmentEliminationMember2025-01-012025-12-310001022321gel:OnshoreFacilitiesAndTransportationSegmentMember2025-01-012025-12-310001022321gel:OnshoreFacilitiesAndTransportationSegmentMember2024-01-012024-12-310001022321us-gaap:OperatingSegmentsMember2024-01-012024-12-310001022321us-gaap:OperatingSegmentsMembergel:OffshorePipelineTransportationSegmentMember2024-01-012024-12-310001022321us-gaap:OperatingSegmentsMembergel:MarineTransportationSegmentMember2024-01-012024-12-310001022321us-gaap:OperatingSegmentsMembergel:OnshoreFacilitiesAndTransportationSegmentMember2024-01-012024-12-310001022321us-gaap:OperatingSegmentsMembergel:OffshorePipelineTransportationSegmentMember2023-01-012023-12-310001022321us-gaap:OperatingSegmentsMembergel:MarineTransportationSegmentMember2023-01-012023-12-310001022321us-gaap:OperatingSegmentsMembergel:OnshoreFacilitiesAndTransportationSegmentMember2023-01-012023-12-310001022321us-gaap:OperatingSegmentsMember2023-01-012023-12-310001022321us-gaap:IntersegmentEliminationMembergel:OffshorePipelineTransportationSegmentMember2023-01-012023-12-310001022321us-gaap:IntersegmentEliminationMembergel:MarineTransportationSegmentMember2023-01-012023-12-310001022321us-gaap:IntersegmentEliminationMembergel:OnshoreFacilitiesAndTransportationSegmentMember2023-01-012023-12-310001022321us-gaap:IntersegmentEliminationMember2023-01-012023-12-310001022321gel:OnshoreFacilitiesAndTransportationSegmentMember2023-01-012023-12-310001022321us-gaap:OperatingSegmentsMembergel:OffshorePipelineTransportationSegmentMember2025-12-310001022321us-gaap:OperatingSegmentsMembergel:OffshorePipelineTransportationSegmentMember2024-12-310001022321us-gaap:OperatingSegmentsMembergel:MarineTransportationSegmentMember2025-12-310001022321us-gaap:OperatingSegmentsMembergel:MarineTransportationSegmentMember2024-12-310001022321us-gaap:OperatingSegmentsMembergel:OnshoreFacilitiesAndTransportationSegmentMember2025-12-310001022321us-gaap:OperatingSegmentsMembergel:OnshoreFacilitiesAndTransportationSegmentMember2024-12-310001022321us-gaap:OperatingSegmentsMember2025-12-310001022321us-gaap:OperatingSegmentsMember2024-12-310001022321us-gaap:CorporateNonSegmentMember2025-12-310001022321us-gaap:CorporateNonSegmentMember2024-12-310001022321us-gaap:MaterialReconcilingItemsMember2025-01-012025-12-310001022321us-gaap:MaterialReconcilingItemsMember2024-01-012024-12-310001022321gel:PoseidonOilPipelineCompanyMemberus-gaap:EquityMethodInvesteeMember2025-01-012025-12-310001022321gel:PoseidonOilPipelineCompanyMemberus-gaap:EquityMethodInvesteeMember2024-01-012024-12-310001022321gel:PoseidonOilPipelineCompanyMemberus-gaap:EquityMethodInvesteeMember2023-01-012023-12-310001022321srt:ChiefExecutiveOfficerMember2025-01-012025-12-310001022321srt:ChiefExecutiveOfficerMember2024-01-012024-12-310001022321srt:ChiefExecutiveOfficerMember2023-01-012023-12-310001022321gel:PoseidonOilPipelineCompanyMember2025-12-310001022321gel:FeesMemberus-gaap:EquityMethodInvesteeMember2025-01-012025-12-310001022321gel:FeesMemberus-gaap:EquityMethodInvesteeMember2024-01-012024-12-310001022321gel:FeesMemberus-gaap:EquityMethodInvesteeMember2023-01-012023-12-310001022321us-gaap:EquityMethodInvesteeMember2025-12-310001022321us-gaap:EquityMethodInvesteeMember2024-12-310001022321gel:TwoThousandAndTenLongTermIncentivePlanMemberus-gaap:PhantomShareUnitsPSUsMember2025-01-012025-12-310001022321gel:TwoThousandAndTenLongTermIncentivePlanMemberus-gaap:PhantomShareUnitsPSUsMember2024-01-012024-12-310001022321gel:TwoThousandAndTenLongTermIncentivePlanMemberus-gaap:PhantomShareUnitsPSUsMember2023-01-012023-12-310001022321gel:ServiceBasedPhantomShareUnitsPSUsMember2022-12-310001022321gel:ServiceBasedPhantomShareUnitsPSUsMember2023-01-012023-12-310001022321gel:ServiceBasedPhantomShareUnitsPSUsMember2023-12-310001022321gel:ServiceBasedPhantomShareUnitsPSUsMember2024-01-012024-12-310001022321gel:ServiceBasedPhantomShareUnitsPSUsMember2024-12-310001022321gel:ServiceBasedPhantomShareUnitsPSUsMember2025-01-012025-12-310001022321gel:ServiceBasedPhantomShareUnitsPSUsMember2025-12-310001022321gel:TwoThousandAndTenLongTermIncentivePlanMemberus-gaap:PhantomShareUnitsPSUsMember2025-12-310001022321gel:TwoThousandAndTenLongTermIncentivePlanMemberus-gaap:PhantomShareUnitsPSUsMember2024-12-310001022321gel:ShellMemberus-gaap:CustomerConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerMember2024-01-012024-12-310001022321gel:ShellMemberus-gaap:CustomerConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerMember2023-01-012023-12-310001022321us-gaap:FutureMemberus-gaap:DesignatedAsHedgingInstrumentMembersrt:CrudeOilMemberus-gaap:ShortMember2025-01-012025-12-310001022321us-gaap:FutureMemberus-gaap:DesignatedAsHedgingInstrumentMembersrt:CrudeOilMemberus-gaap:LongMember2025-01-012025-12-310001022321us-gaap:SwapMemberus-gaap:NondesignatedMembersrt:NaturalGasReservesMemberus-gaap:ShortMember2025-01-012025-12-310001022321us-gaap:SwapMemberus-gaap:NondesignatedMembersrt:NaturalGasReservesMemberus-gaap:LongMember2025-01-012025-12-310001022321us-gaap:OptionMemberus-gaap:NondesignatedMembersrt:CrudeOilMemberus-gaap:ShortMember2025-01-012025-12-310001022321us-gaap:OptionMemberus-gaap:NondesignatedMembersrt:CrudeOilMemberus-gaap:LongMember2025-01-012025-12-310001022321us-gaap:CommodityContractMemberus-gaap:NondesignatedMember2025-12-310001022321us-gaap:CommodityContractMemberus-gaap:NondesignatedMember2024-12-310001022321us-gaap:CommodityContractMemberus-gaap:DesignatedAsHedgingInstrumentMember2025-12-310001022321us-gaap:CommodityContractMemberus-gaap:DesignatedAsHedgingInstrumentMember2024-12-310001022321us-gaap:CommodityContractMemberus-gaap:OtherCurrentAssetsMemberus-gaap:NondesignatedMember2025-12-310001022321us-gaap:CommodityContractMemberus-gaap:OtherCurrentAssetsMemberus-gaap:NondesignatedMember2024-12-310001022321us-gaap:CommodityContractMemberus-gaap:OtherCurrentAssetsMemberus-gaap:DesignatedAsHedgingInstrumentMember2025-12-310001022321us-gaap:CommodityContractMemberus-gaap:OtherCurrentAssetsMemberus-gaap:DesignatedAsHedgingInstrumentMember2024-12-310001022321gel:OnshoreFacilitiesandTransportationProductCostsMemberus-gaap:CommodityContractMemberus-gaap:DesignatedAsHedgingInstrumentMember2025-01-012025-12-310001022321gel:OnshoreFacilitiesandTransportationProductCostsMemberus-gaap:CommodityContractMemberus-gaap:DesignatedAsHedgingInstrumentMember2024-01-012024-12-310001022321gel:OnshoreFacilitiesandTransportationProductCostsMemberus-gaap:CommodityContractMemberus-gaap:DesignatedAsHedgingInstrumentMember2023-01-012023-12-310001022321gel:OnshoreFacilitiesandTransportationProductCostsSodiumMineralsandSulfurServicesOperatingcostsMemberus-gaap:CommodityContractMemberus-gaap:NondesignatedMember2025-01-012025-12-310001022321gel:OnshoreFacilitiesandTransportationProductCostsSodiumMineralsandSulfurServicesOperatingcostsMemberus-gaap:CommodityContractMemberus-gaap:NondesignatedMember2024-01-012024-12-310001022321gel:OnshoreFacilitiesandTransportationProductCostsSodiumMineralsandSulfurServicesOperatingcostsMemberus-gaap:CommodityContractMemberus-gaap:NondesignatedMember2023-01-012023-12-310001022321us-gaap:CommodityContractMember2025-01-012025-12-310001022321us-gaap:CommodityContractMember2024-01-012024-12-310001022321us-gaap:CommodityContractMember2023-01-012023-12-310001022321us-gaap:CommodityContractMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2025-12-310001022321us-gaap:CommodityContractMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2025-12-310001022321us-gaap:CommodityContractMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2025-12-310001022321us-gaap:CommodityContractMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2024-12-310001022321us-gaap:CommodityContractMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2024-12-310001022321us-gaap:CommodityContractMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2024-12-310001022321gel:SeniorUnsecuredNotesMember2025-12-310001022321gel:SeniorUnsecuredNotesMember2024-12-310001022321country:US2025-12-310001022321country:US2024-12-310001022321us-gaap:StateAndLocalJurisdictionMember2025-12-310001022321us-gaap:StateAndLocalJurisdictionMember2024-12-310001022321us-gaap:SubsequentEventMember2026-02-030001022321us-gaap:SubsequentEventMember2026-02-032026-02-03

☒ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2025

OR

☐TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission file number 1-12295

GENESIS ENERGY, L.P.

(Exact name of registrant as specified in its charter)

Delaware

76-0513049

(State or other jurisdiction of incorporation or organization)

(I.R.S. Employer Identification No.)

811 Louisiana, Suite 1200,

Houston

,

TX

77002

(Address of principal executive offices)

(Zip code)

Registrant’s telephone number, including area code:

(713)

860-2500

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class

Trading Symbol(s)

Name of Each Exchange on Which Registered

Common Units

GEL

NYSE

Securities registered pursuant to Section 12(g) of the Act:

NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yesx No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes oNox

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yesx No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T(§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yesx No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer

x

Accelerated filer

☐

Non-accelerated filer

☐

Smaller reporting company

☐

Emerging growth company

☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2) of the Act). Yes ☐ No x

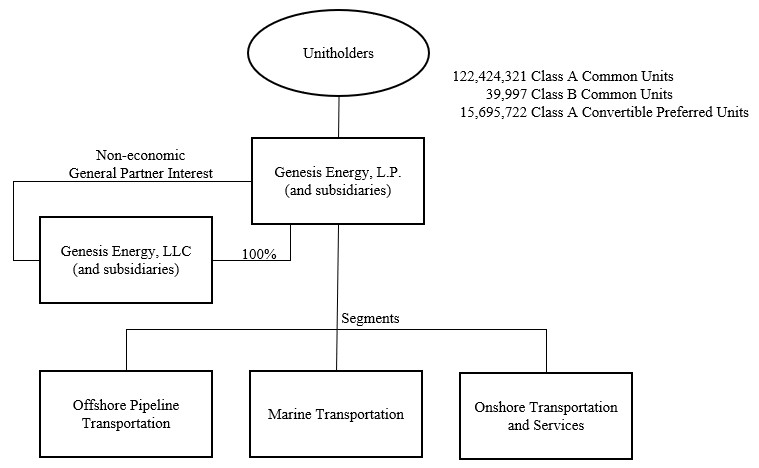

The aggregate market value of the Class A common units held by non-affiliates of the Registrant on June 30, 2025 (the last business day of Registrant’s most recently completed second fiscal quarter) was approximately $1,855.0 million based on $17.23 per unit, the closing price of the common units as reported on the NYSE. For purposes of this computation, all executive officers and directors are deemed to be affiliates. Such a determination should not be deemed an admission that such executive officers and directors are affiliates. On February 18, 2026, the Registrant had 122,424,321 Class A Common Units and 39,997 Class B Common Units outstanding.

Unless the context otherwise requires, references in this annual report to “Genesis Energy, L.P.,” “Genesis,” “we,” “our,” “us,” “the Company” or like terms refer to Genesis Energy, L.P. and its operating subsidiaries. Unless the context otherwise requires, references made in this annual report to the“Alkali Business” as defined below in Item 1. “Business” relate specifically to the period of our ownership of such business prior to the date of sale, February 28, 2025. As generally used within the energy industry and in this annual report, the identified terms have the following meanings:

Bbl or Barrel: One stock tank barrel, or 42 U.S. gallons liquid volume, used in reference to crude oil or other liquid hydrocarbons.

Bbls/day: Barrels per day.

DST: Dry short tons (2,000 pounds), a unit of weight measurement.

FERC: Federal Energy Regulatory Commission.

MBbls: Thousand Bbls.

MBbls/day: Thousand Bbls per day.

Mcf: Thousand cubic feet of gas.

MMBtu: One million British thermal units, an energy measurement.

MMcf: Thousand Mcf.

MMcf/day: Thousand Mcf per day.

NaHS: (commonly pronounced as “nash”) Sodium hydrosulfide.

NaOH or Caustic Soda: Sodium hydroxide.

Natural gas liquid(s) or NGL(s): The combination of ethane, propane, normal butane, isobutane and natural gasolines that, when removed from natural gas, become liquid under various levels of higher pressure and lower temperature.

Sour gas: Natural gas containing more than four parts per million of hydrogen sulfide.

Wellhead: The point at which the hydrocarbons and water exit the ground.

FORWARD-LOOKING INFORMATION

The statements in this Annual Report on Form 10-K that are not historical information may be “forward looking statements” as defined under federal law. All statements, other than historical facts, included in this document that address activities, events or developments that we expect or anticipate will or may occur in the future, including things such as plans for growth of the business, future capital expenditures, competitive strengths, goals, references to future goals or intentions, estimated or projected future financial performance, and other such references are forward-looking statements, and historical performance is not necessarily indicative of future performance. These forward-looking statements are identified as any statement that does not relate strictly to historical or current facts. They use words such as “anticipate,” “believe,” “continue,” “estimate,” “expect,” “forecast,” “goal,” “intend,” “may,” “could,” “plan,” “position,” “projection,” “strategy,” “should” or “will,” or the negative of those terms or other variations of them or by comparable terminology. In particular, statements, expressed or implied, concerning future actions, conditions or events (including production rates and other conditions and events), future operating results, the ability to generate sales, income or cash flow, the timing and anticipated benefits of our development projects and the expected performance of our offshore assets and other projects and business segments, the ability to simplify our capital structure and lower our cost of capital, and the availability of borrowing capacity to fund our growth capital expenditures are forward-looking statements. Forward-looking statements are not guarantees of performance. They involve risks, uncertainties and assumptions. Future actions, conditions or events and future results of operations may differ materially from those expressed in these forward-looking statements. Many of the factors that will determine these results are beyond our ability or the ability of our affiliates to control or predict. Specific factors that could cause actual results to differ from those in the forward-looking statements include, among others:

•demand for, the supply of, our assumptions about, changes in forecast data for, and price trends related to crude oil, liquid petroleum, natural gas, NaHS, and caustic soda, all of which may be affected by economic activity, capital expenditures and operational and technical issues experienced by energy producers, weather, alternative energy sources, international conflicts and international events (including the war in Ukraine, the Israel and Hamas war and broader geopolitical tensions in South America, the Caribbean, the Middle East and Europe), global pandemics, inflation, the actions of OPEC and other oil exporting nations, conservation and technological advances;

•our ability to successfully execute our business and financial strategies;

•our ability to continue to realize cost savings from our cost saving measures;

•throughput levels and rates;

•changes in, or challenges to, our tariff rates;

•our ability to successfully identify and close strategic acquisitions on acceptable terms (including obtaining third-party consents and waivers of preferential rights), develop or construct infrastructure assets, make cost saving changes in operations and integrate acquired assets or businesses into our existing operations;

•service interruptions in our pipeline transportation systems, or processing operations, including due to adverse weather events;

•shutdowns or cutbacks at refineries, petrochemical plants, utilities, individual plants or other businesses for which we transport crude oil, petroleum, natural gas or other products or to whom we sell petroleum or other products;

•risks inherent in marine transportation and vessel operation, including accidents and discharge of pollutants;

•changes in laws and regulations to which we are subject, including tax withholding issues, regulations regarding qualifying income, accounting pronouncements, and safety, environmental and employment laws and regulations;

•the effects of production declines resulting from a suspension of drilling in the Gulf of America or otherwise;

•the effects of future laws and regulations, including increased tariffs and proposed tariffs, taxes, duties and similar matters affecting international trade;

•planned capital expenditures and availability of capital resources to fund capital expenditures, and our ability to access the credit and capital markets to obtain financing on terms we deem acceptable;

•our inability to borrow or otherwise access funds needed for operations, expansions or capital expenditures as a result of our credit agreement and the indentures governing our notes, which contain various affirmative and negative covenants;

•loss of key personnel;

•cash from operations that we generate could decrease or fail to meet expectations, either of which could reduce our ability to pay quarterly cash distributions (common and preferred) at the current level or to increase quarterly cash distributions in the future;

•an increase in the competition that our operations encounter;

•cost and availability of insurance;

•hazards and operating risks that may not be covered fully by insurance;

•our financial and commodity hedging arrangements, which may reduce our earnings, profitability and cash flow;

•changes in global economic conditions, including capital and credit markets conditions, inflation and interest rates, including the result of any economic recession or depression that has occurred or may occur in the future;

•the impact of natural disasters, international military conflicts (such as the war in Ukraine, the Israel and Hamas war and broader geopolitical tensions in South America, the Caribbean, the Middle East and Europe), global pandemics, epidemics, accidents or terrorism, and actions taken by governmental authorities and other third parties in response thereto, on our business financial condition and results of operations;

•reduction in demand for our services resulting in impairments of our assets;

•changes in the financial condition of customers or counterparties;

•adverse rulings, judgments, or settlements in litigation or other legal or tax matters;

•the treatment of us as a corporation for federal income tax purposes or if we become subject to entity-level taxation for state tax purposes;

•the potential that our internal controls may not be adequate, weaknesses may be discovered or remediation of any identified weaknesses may not be successful and the impact these could have on our unit price; and

•a cyberattack involving our information systems and related infrastructure, or that of our business associates.

You should not put undue reliance on any forward-looking statements. When considering forward-looking statements, please review the risk factors described under “Risk Factors” discussed in Item 1A. These risks may also be specifically described in our Quarterly Reports on Form 10-Q, Current Reports on Form 8-K (or any amendments to those reports) and other documents that we may file from time to time with the SEC. New factors that could cause actual results to differ materially from those described in forward-looking statements emerge from time to time, and it is not possible for us to predict all such factors, or the extent to which any such factor or combination of factors may cause actual results to differ from those contained in any forward-looking statement. Except as required by applicable securities laws, we do not intend to update these forward-looking statements and information.

We are a growth-oriented master limited partnership (“MLP”) formed in Delaware in 1996 focused on the midstream segment of the crude oil and natural gas industry. Our common units are traded on the New York Stock Exchange (“NYSE”), under the ticker symbol “GEL.” We provide an integrated suite of services (including transportation, storage, sulfur removal, blending, terminaling and processing) to crude oil and natural gas producers, refiners, and industrial and commercial enterprises. Our operations are primarily located in the Gulf of America and in the Gulf Coast region of the United States. We have a diverse portfolio of assets, including pipelines, offshore hub and junction platforms, refinery-related plants, storage tanks, terminals, railcars, rail unloading facilities, barges and other vessels, and trucks. Prior to February 28, 2025, our business also included the trona and trona-based exploring, mining, processing, producing, marketing, logistics and selling business based in Wyoming (the “Alkali Business”).

In the first quarter of 2025, we sold the Alkali Business and, as a result, re-organized our operating segments to represent how our chief operating decision maker, who is our Chief Executive Officer (our “CODM”), evaluates the performance of operations, develops strategy and allocates resources, including capital. Our sulfur services business, formerly reported under our soda and sulfur services reporting segment along with our Alkali Business, is now reported under our onshore transportation and services reporting segment along with those businesses that were included within our previously reported onshore facilities and transportation segment. As a result of this change, we now manage our businesses through the following three divisions that constitute our reportable segments:

•Offshore pipeline transportation, which includes the transportation and processing of crude oil and natural gas in the Gulf of America;

•Marine transportation, which provides waterborne transportation of petroleum products (primarily fuel oil, asphalt and other heavy refined products) and crude oil throughout North America; and

•Onshore transportation and services, which includes terminaling, blending, storing, and marketing crude oil, and transporting crude oil and refined products, as well as the processing of high sulfur (or “sour”) gas streams for refineries to remove the sulfur, and selling the related by-product, NaHS.

For additional information regarding our reportable segments, see discussion below entitled “Description of Segments and Related Assets.”

We conduct our operations and own our operating assets through our subsidiaries and joint ventures. Our general partner, Genesis Energy, LLC, a wholly-owned subsidiary that owns a non-economic general partner interest in us, has sole responsibility for conducting our business and managing our operations. Our outstanding common units (including our Class B Common Units), and our outstanding Class A convertible preferred units (our “Class A Convertible Preferred Units”), representing limited partner interests, constitute all of the economic equity interests in us.

The following chart depicts our organizational structure at December 31, 2025.

Our Objectives and Strategies

Our primary objectives and strategies are to generate and grow stable free cash flows from operations and continue to deleverage our balance sheet, while never wavering from our commitment to safe and responsible operations. We believe the following have been and are critical to meet our objectives:

•The completion of our major growth capital spending program during 2025, which included the construction and connection of our SYNC Pipeline (as defined and discussed further below under “Recent Developments”) and the expansion of our existing Cameron Highway oil pipeline system (“CHOPS Pipeline”) (as discussed further below under “Recent Developments”).

•An increase in volumes from long-term contracted offshore commercial opportunities in the Gulf of America, including volumes from the Shenandoah development, which saw first production in the third quarter of 2025 and ties into our SYNC Pipeline and further downstream to our CHOPS Pipeline, and volumes from the Salamanca Floating Production System (“FPS”), which also saw first production in the third quarter of 2025 and ties into our existing Southeast Keathley Canyon pipeline system (“SEKCO Pipeline”) for further transportation downstream to our Poseidon oil pipeline system (“Poseidon Pipeline”).

•New and incremental volumes from continued in-field and sub-sea tieback opportunities as a result of the continued investment by the offshore producing community. These opportunities require minimal to no additional investment from us as a result of the current production handling capacity on our offshore pipeline transportation assets in the Gulf of America.

•The creation of financial flexibility from the combination of a significant amount of available borrowing capacity under our senior secured credit facility, subject to compliance with covenants, and our increasing cash flows from operations as discussed above, which will allow us to maximize our cash flow and focus on returning value to our capital structure with an emphasis on reducing debt in absolute terms, opportunistically redeeming our Class A Convertible Preferred Units and thoughtfully evaluating increases in our quarterly distributions to common unitholders.

Our primary business strategy is to provide an integrated suite of services to crude oil and natural gas producers and refiners and provide NaHS and caustic soda to industrial and commercial enterprises. Successfully executing this strategy should enable us to generate and grow stable cash flows from operations. We intend to execute this strategy by:

•Identifying and exploiting incremental profit opportunities, including cost synergies, across an increasingly integrated footprint;

•Economically expanding our pipeline and terminal operations by utilizing capacity currently available on our existing assets that requires minimal to no additional investment;

•Optimizing our existing assets and creating synergies through additional commercial and operating advancement;

•Leveraging customer relationships across business segments;

•Attracting new customers and expanding our scope of services offered to existing customers;

•Expanding the geographic reach of our businesses;

•Evaluating internal and third party growth opportunities (including asset and business acquisitions) that leverage our core competencies and strengths and further integrate our businesses; and

•Focusing on health, safety and environmental stewardship, and advancement of our sustainability program.

Financial Strategy

We believe that preserving financial flexibility is an important factor in our overall strategy and success. Over the long-term, we intend to:

•Increase the relative contribution of recurring and throughput-based revenues, emphasizing longer-term contractual arrangements;

•Maintain a sound, disciplined capital structure, including our current and forward path to deleveraging;

•Preserve a significant amount of available borrowing capacity under our senior secured credit facility;

•Reduce our overall cost of capital through a combination of reducing debt in absolute terms and opportunistically redeeming our high-cost Class A Convertible Preferred Units;

•Create strategic arrangements and share capital costs and risks through joint ventures and strategic alliances;

•Prudently manage our limited direct commodity price risks; and

•Pursue divestitures that support our deleveraging objective.

Competitive Strengths

We believe we are well positioned to execute our strategies and ultimately achieve our objectives due primarily to the following competitive strengths:

•Certain of our businesses are among the leaders in each of their respective markets, have long commercial lives, and have significant barriers to entry. We operate, among others, diversified businesses, each of which is one of the leaders in its market, has a long commercial life, and has significant barriers to entry. We operate one of the largest pipeline networks (based on throughput capacity) in the Deepwater area of the Gulf of America, an area that produced approximately 14% of the oil produced in the U.S. during 2025. We are one of the largest producers and marketers (based on tons produced) of NaHS in North and South America. We are one of the leading providers of crude oil and petroleum product transportation, storage and other handling services for two large, complex refineries in Baton Rouge, Louisiana and Baytown, Texas, both of which have been operational for over 100 years.

•Our businesses encompass a balanced, diversified portfolio of customers, operations and assets. We operate three business segments composed of a diversified suite of assets that enable us to provide a number of services primarily to crude oil and natural gas producers and refiners, and provide NaHS and caustic soda to industrial and commercial enterprises. Our businesses complement each other by allowing us to offer an integrated suite of services to common customers across our segments.

•We are financially flexible and have significant liquidity. As of December 31, 2025, we had $788.6 million of availability under our $800.0 million senior secured credit facility, subject to compliance with our covenants, including up to $171.9 million available under the $200.0 million petroleum products inventory loan sublimit and $45.0 million available for letters of credit. Our inventory borrowing base was $28.1 million at December 31, 2025.

•Our businesses provide relatively consistent consolidated financial performance. Our historically consistent financial performance, combined with our goal of a conservative capital structure over the long term, has allowed us to generate relatively stable cash flows from operations.

•We have limited direct commodity price risk exposure in our crude oil marketing business and limited cost exposure in our NaHS business. The volumes of crude oil, refined products or intermediate feedstocks we purchase are either subject to back-to-back sales contracts or are hedged with exchange-traded derivatives to limit our direct exposure to movements in the price of the commodity; however, we cannot completely eliminate commodity price exposure. We have a risk management policy that requires us to monitor the effectiveness of the hedges as well as other limitations on the maximum levels of inventory we may hold that is not hedged. In addition, our service contracts with refiners allow us to adjust the rates we charge for processing to maintain a balance between NaHS supply and demand.

•Our offshore Gulf of America crude oil and natural gas pipeline transportation and handling operations are located in a significant producing region with large-reservoir, long-lived crude oil and natural gas properties. We provide a suite of services, primarily to integrated and large independent energy companies who make intensive capital investments to develop numerous large-reservoir, long-lived crude oil and natural gas properties in one of the largest producing regions in the U.S., the deepwater Gulf of America.

•Our expertise and reputation for high performance standards and quality enable us to provide refiners with economic and proven services. Our extensive understanding of the sulfur removal process and crude oil refining can provide us with an advantage when evaluating new opportunities and/or markets.

•Some of our pipeline transportation and related assets are strategically located. Our pipelines are critical to the ongoing operations of our refiner and producer customers. In addition, a majority of our terminals are located in areas that can be accessed by pipeline, truck, rail or barge.

•Some of our onshore transportation and services assets are operationally flexible. Our portfolio of trucks, barges, pipelines, rail unloading facilities, tanks and terminals affords us flexibility within our existing regional footprint and provides us the capability to enter new markets and expand our customer relationships.

•Our marine transportation assets provide waterborne transportation throughout North America. We own and operate a fleet of barges and boats used to provide transportation services to both inland and offshore customers within a large North American geographic footprint. All of our vessels operate under the U.S. flag and are qualified for U.S. coastwise trade under the Jones Act.

•We have an experienced, knowledgeable and motivated executive management team with a proven track record. Our executive management team has a significant level of experience in the midstream sector. Certain of our executive management team members have worked in leadership roles at a number of large, successful public companies, including other publicly-traded partnerships. Through their equity interest in us and compensation package (including long term incentive awards based on available cash before reserves, leverage, sustainability and safety metrics), our executive management team is incentivized to create value.

Recent Developments

The following is a brief listing of developments since December 31, 2024. Additional information regarding most of these items may be found elsewhere in this report.

Sale of the Alkali Business and Related Transactions

On February 28, 2025, we completed the sale of the Alkali Business to an indirect affiliate of WE Soda Ltd for a gross purchase price of $1.425 billion. The sale generated proceeds of approximately $1.0 billion, which reflects the net proceeds after the assumption of $413.4 million of our then outstanding 5.875% senior secured notes due 2042 (the “Alkali senior secured notes”) by an indirect affiliate of WE Soda Ltd, and other purchase price adjustments. We used the proceeds to pay down the outstanding balance on our senior secured credit facility on February 28, 2025, purchase 7,416,196 Class A Convertible Preferred Units on March 6, 2025 at a purchase price of $35.40, and redeem the remaining $406.2 million of principal outstanding on the 8.000% senior unsecured notes due January 15, 2027 (the “2027 Notes”) on April 3, 2025.

On February 27, 2025, in connection with the sale of the Alkali Business discussed above, we entered into the Second Amendment to the Seventh Amended and Restated Credit Agreement. This amendment primarily provides for: (i) a reduction from $900 million to $800 million of total borrowing capacity under our senior secured credit facility; (ii) unlimited cash netting against our outstanding debt for purposes of our leverage ratio calculation if our credit facility is undrawn at the end of a reporting period, otherwise a maximum netting of $25 million is allowed; and (iii) an increased permitted investment basket under certain circumstances that will allow us to opportunistically purchase existing private or public securities across our capital structure. Our senior secured credit facility matures on September 1, 2028, subject to extension at our request for one additional year on up to two occasions and subject to certain conditions, provided that if more than $150 million of our 7.750%

senior unsecured notes due February 1, 2028 (the “2028 Notes”) remain outstanding as of November 2, 2027, the senior secured credit facility matures on such date.

Offshore Growth Capital Projects Completion

We previously entered into definitive agreements to provide transportation services for 100% of the crude oil production associated with two separate standalone deepwater developments (Shenandoah and Salamanca). In conjunction with these agreements, we committed to two offshore growth capital projects, which included expanding the current capacity of our 64% owned CHOPS Pipeline (the “CHOPS expansion”) and constructing a new 100% owned, approximately 105-mile, 20” diameter crude oil pipeline (the “SYNC Pipeline”) to connect the Shenandoah deepwater development to our existing asset footprint in the Gulf of America.

The CHOPS expansion included a complete overhaul of the Garden Banks 72 platform (“GB-72”) topside facilities, reconnection of the CHOPS Pipeline to the GB-72 platform, and the addition of pumps at both the High Island A5 (“HI-A5”) and GB-72 platforms to upgrade processing capabilities and increase throughput on the CHOPS Pipeline.

During 2025, we successfully finished the CHOPS expansion and SYNC Pipeline, which completed our major growth capital spending program. During the third quarter of 2025, we saw first production from the Shenandoah and Salamanca deepwater developments, and during the fourth quarter of 2025, Shenandoah throughput was well above the minimum volume commitments (“MVCs”) and volumes from Salamanca continued to ramp toward targeted production levels.

Market Update

Over the past several years, we have seen a heightened level of volatility in global markets and commodity prices driven by various events or circumstances outside of our control including, but not limited to, global pandemics, international military conflicts, geopolitical events and significant changes in economic policies. This volatility could negatively impact future prices for crude oil, natural gas, petroleum products and industrial products.

Management’s estimates are based on numerous assumptions about future operations and market conditions, which we believe to be reasonable, but are inherently uncertain. The uncertainties underlying our assumptions could cause our estimates to differ significantly from actual results, including with respect to the duration and severity of the lasting impacts of international conflicts and the result of any economic recession or depression that has occurred or may occur in the future as a result of or as it relates to changes in governmental policies (including with respect to tariffs or proposed tariffs, taxes, duties and similar matters affecting international trade) aimed at addressing inflation or other conditions or events, which could cause fluctuations in global economic conditions, including capital and credit markets. We will continue to monitor the current market environment and to the extent conditions deteriorate, we may identify triggering events that may require future evaluations of the recoverability of the carrying value of our long-lived assets, intangible assets and goodwill, which could result in impairment charges that could be material to our results of operations.

Although the ultimate impacts of these international conflicts, changes in governmental policies (including with respect to tariffs or proposed tariffs, taxes, duties and similar matters) and fluctuations in global economic conditions, including capital and credit markets, are still unknown at this time, we believe the fundamentals of our core businesses continue to remain strong and, considering the current industry environment and capital market behavior, we have continued our focus on deleveraging our balance sheet as further explained in “Liquidity and Capital Resources.”

Description of Segments and Related Assets

We conduct our businesses through three operating segments: offshore pipeline transportation, marine transportation and onshore transportation and services. These segments are strategic business units that provide a variety of midstream energy-related services. Financial information with respect to each of our operating segments can be found in Note 14 to our Consolidated Financial Statements in Item 8. Below is a more detailed description of our operating segments and their related assets.

We conduct our offshore crude oil and natural gas pipeline transportation and handling operations in the Gulf of America through our offshore pipeline transportation segment, which focuses on providing a suite of services to integrated and large independent energy companies who make intensive capital investments (often in excess of a billion dollars) to develop large-reservoir, long-lived crude oil and natural gas properties located primarily in offshore Texas, Louisiana and Mississippi. The Gulf of America is one of the most active drilling and development regions in the U.S. representing approximately 14% of the crude oil production in the U.S. during 2025. Because the related pipelines and other infrastructure needed to develop the large-reservoir properties are capital intensive, we believe they are generally much less sensitive to short-term commodity price volatility, particularly once a project has been sanctioned or brought on-line.

We own interests in various offshore crude oil and natural gas pipeline systems, platforms and related infrastructure. Our interests in offshore crude oil pipeline systems that are currently operating (a number of which pipeline systems are substantial and/or strategically located) include approximately 1,536 miles of pipe with an aggregate design capacity of approximately 2,094 MMbls/day. For example, we own a 64% interest in the CHOPS Pipeline and a 64% interest in the Poseidon Pipeline, which are two of the largest crude oil pipelines (in terms of both length and design capacity) located in the Gulf of America. We also own 100% of the SEKCO Pipeline, which is a deepwater pipeline currently servicing the Lucius, Buckskin and Hadrian North fields as well as the Leon and Castille fields (through the Salamanca FPS), in the southern Keathley Canyon area of the Gulf of America and 100% of the SYNC Pipeline, which is a deepwater pipeline currently servicing the Shenandoah production field in the Walker Ridge area of the Gulf of America.

Our interests in operating offshore natural gas pipeline systems and related infrastructure include approximately 759 miles of pipe with an aggregate design capacity of approximately 2,200 MMcf/day. We also own an interest in two offshore hub platforms with an aggregate processing capacity of approximately 495 MMcf/day of natural gas and 123 MBbls/day of crude oil. Additionally, we own an interest in a number of junction and service platforms in the Gulf of America, which are used to (i) interconnect the offshore pipeline network; (ii) provide an efficient means to perform pipeline maintenance; and (iii) increase or direct the flow on our pipelines via pumps and measurement equipment.

We generate cash flows from our offshore pipelines from fees charged to customers or substantially similar arrangements that otherwise limit our direct exposure to changes in commodity prices.

We believe our offshore pipeline transportation segment is well positioned to participate in both the energy transition and lower carbon world as barrels produced from the Gulf of America are some of the least emission intensive barrels, from reservoir to refinery, of any barrel refined by Gulf Coast refineries (including shipping).

The table below reflects our interests in our operating offshore crude oil pipelines:

Offshore crude oil pipelines

Operator

System Miles

Design Capacity (Bbls/day)(1)

Interest Owned

Throughput (Bbls/day) 100% basis(1)

Throughput (Bbls/day) net to ownership interest

Main Lines

CHOPS Pipeline

Genesis

380

550,000

64

%

357,207

228,612

Poseidon Pipeline

Genesis

367

350,000

64

%

256,777

164,337

Odyssey Pipeline

Shell Pipeline

120

200,000

29

%

66,906

19,403

Eugene Island Pipeline System

Genesis/Shell Pipeline

184

39,000

29

%

1,629

1,629

Total

1,051

1,139,000

682,519

413,981

Lateral Lines(2)

SEKCO Pipeline

Genesis

149

115,000

100

%

SYNC Pipeline

Genesis

105

240,000

100

%

Shenzi Crude Oil Pipeline

Genesis

83

230,000

100

%

Allegheny Crude Oil Pipeline

Genesis

40

140,000

100

%

Marco Polo Crude Oil Pipeline

Genesis

37

120,000

100

%

Constitution Crude Oil Pipeline

Genesis

67

80,000

100

%

Tarantula

Genesis

4

30,000

100

%

(1)Capacity figures presented represent 100% of the design capacity as of December 31, 2025 and throughput figures represent 100% of the volumes in the period; except for Eugene Island, which represents our net capacity and volumes in the undivided interest (29%) in that system. Ultimate capacities can vary primarily as a result of crude oil quality, pressure requirements, installed pumps, related facilities, utilization of drag reducing agents and the viscosity of the crude oil actually moved.

(2)Represents 100% owned lateral crude oil pipelines which ultimately flow into our other offshore crude oil pipelines (including the CHOPS Pipeline and Poseidon Pipeline) and thus are excluded from main lines above.

•CHOPS Pipeline. CHOPS Pipeline is comprised of 24- to 30-inch diameter pipelines designed to deliver crude oil from fields in the Gulf of America to refining markets along the Texas Gulf Coast via interconnections with refineries and terminals located in Port Arthur and Texas City, Texas. Cameron Highway Oil Pipeline Company, LLC (“CHOPS”) also owns three strategically located multi-purpose offshore platforms. A financial party owns the remaining 36% interest in CHOPS.

•Poseidon Pipeline. The Poseidon Pipeline is comprised of 16- to 24-inch diameter pipelines to deliver crude oil from developments in the central and western offshore Gulf of America to other pipelines and terminals located in onshore and offshore Louisiana. An affiliate of Shell owns the remaining 36% interest in Poseidon Oil Pipeline Company, LLC (“Poseidon”).

•Odyssey Pipeline. The Odyssey pipeline is comprised of 12- to 20-inch diameter pipelines to deliver crude oil from developments in the eastern Gulf of America to other pipelines and terminals onshore in Louisiana. An affiliate of Shell owns the remaining 71% interest in Odyssey Pipeline, LLC (“Odyssey”).

•Eugene Island. The Eugene Island system is comprised of a network of crude oil pipelines, the main pipeline of which is 20 inches in diameter, to deliver crude oil from developments in the central Gulf of America to other pipelines and onshore terminals in Louisiana. Other owners in Eugene Island include affiliates of Exxon Mobil and Shell Oil Company.

•SEKCO Pipeline. The SEKCO Pipeline is a deepwater pipeline that connects the Lucius platform, which supports the Lucius, Hadrian, and Buckskin production fields, and the Salamanca FPS, which supports the Leon and Castille production fields, located in the southern Keathley Canyon area of the Gulf of America, to our CHOPS Pipeline and Poseidon Pipeline.

•SYNC Pipeline. The SYNC pipeline is a newly constructed 20-inch diameter crude oil pipeline that connects the Shenandoah FPS, supporting the Shenandoah production field located in the Walker Ridge area of the Gulf of America, to our CHOPS Pipeline and Poseidon Pipeline.

•Shenzi Pipeline. The Shenzi Pipeline connects the Shenzi platform, supporting the Shenzi production field, and the King’s Quay FPS, which supports the Khaleesi, Mormont and Samurai production fields, located in the Green Canyon area of the Gulf of America, to our CHOPS Pipeline and Poseidon Pipeline.

•Allegheny Pipeline. The Allegheny Pipeline connects the Allegheny platform, which supports the Allegheny and Pegasus production fields, and the South Timbalier 316 platform, which supports the South Timbalier 316 production field, in the Green Canyon area of the Gulf of America, to our CHOPS Pipeline and Poseidon Pipeline.

•Marco Polo Pipeline. The Marco Polo Pipeline connects the Marco Polo platform, which supports the Shenzi K, K2 and Warrior production fields, to an interconnect with the Allegheny Crude Oil Pipeline in Green Canyon Block 164.

•Constitution Pipeline. The Constitution Pipeline connects the Constitution platform, which supports the Constitution, Constellation and Caesar Tonga production fields located in the Green Canyon area of the Gulf of America, to our CHOPS Pipeline and Poseidon Pipeline.

None of our offshore crude oil pipelines are rate regulated with the exception of Eugene Island, which is regulated by the FERC.