QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934.

For the quarterly period ended March 31, 2026

or

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934.

For the transition period from to

Commission File Number: 001-34139

Federal Home Loan Mortgage Corporation

(Exact name of registrant as specified in its charter)

Federally chartered

52-0904874

8200 Jones Branch Drive

22102-3110

(703)

903-2003

corporation

McLean,

Virginia

(State or other jurisdiction of incorporation or organization)

(I.R.S. Employer

Identification No.)

(Address of principal executive offices)

(Zip Code)

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class

Trading Symbol(s)

Name of each exchange on which registered

None

N/A

N/A

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒Yes☐No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).☒Yes☐No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer

☒

Accelerated filer

☐

Non-accelerated filer

☐

Smaller reporting company

☐

Emerging growth company

☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes☐ No☒

As of April 7, 2026, there were 650,059,553 shares of the registrant's common stock outstanding.

Table of Contents

Table of Contents

Page

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Management's Discussion and Analysis of Financial Condition and Results of Operations

This Quarterly Report on Form 10-Q includes forward-looking statements that are based on current expectations and that are subject to significant risks and uncertainties. These forward-looking statements are made as of the date of this Form 10-Q. We undertake no obligation to update any forward-looking statement to reflect events or circumstances after the date of this Form 10-Q. Actual results might differ significantly from those described in or implied by such statements due to various factors and uncertainties, including those described in the MD&A - Forward-Looking Statements section of this Form 10-Q and the Introduction and Risk Factors sections of our Annual Report on Form 10-K for the year ended December 31, 2025, or 2025 Annual Report.

Throughout this Form 10-Q, we use certain acronyms and terms that are defined in the Glossary of our 2025 Annual Report.

You should read the following MD&A in conjunction with our 2025 Annual Report and our condensed consolidated financial statements and accompanying notes for the three months ended March 31, 2026 included in Financial Statements.

INTRODUCTION

Freddie Mac is a GSE chartered by Congress in 1970, with a mission to provide liquidity, stability, and affordability to the U.S. housing market. We do this primarily by purchasing single-family and multifamily residential mortgage loans originated by lenders. In most instances, we package these loans into guaranteed mortgage-related securities, which are sold in the global capital markets, and transfer interest-rate and liquidity risks to third-party investors. In addition, we transfer a portion of our mortgage credit risk exposure to third-party investors through our credit risk transfer programs, which include securities- and insurance-based offerings. We also invest in mortgage loans, mortgage-related securities, and other types of assets. We do not originate mortgage loans or lend money directly to mortgage borrowers.

We support the U.S. housing market and the overall economy by enabling America's families to access mortgage loan funding with better terms and by providing consistent liquidity to the single-family and multifamily mortgage markets. We have helped many distressed borrowers keep their homes or avoid foreclosure and have helped many distressed renters avoid eviction.

Since September 2008, we have been operating in conservatorship, with FHFA as our Conservator. The conservatorship and related matters significantly affect our management, business activities, financial condition, and results of operations. Our future is uncertain, and the conservatorship has no specified termination date. We do not know what changes may occur to our business model during or following conservatorship, including whether we will continue to exist. In connection with our entry into conservatorship, we entered into the Purchase Agreement with Treasury under which we issued Treasury both senior preferred stock and a warrant to purchase common stock. The Purchase Agreement with Treasury is critical to keeping us solvent and avoiding the appointment of a receiver by FHFA under statutory mandatory receivership provisions. We believe the support provided by Treasury pursuant to the Purchase Agreement currently enables us to have adequate liquidity to conduct normal business activities. For additional information on the conservatorship and related matters and the Purchase Agreement, see our 2025 Annual Report.

Freddie Mac 1Q 2026 Form 10-Q

1

Management's Discussion and Analysis

Introduction

Business Results

Consolidated Financial Results

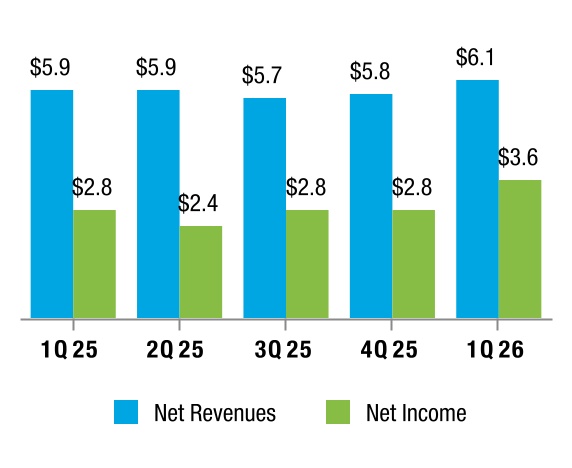

Net Revenues and Net Income

(In billions)

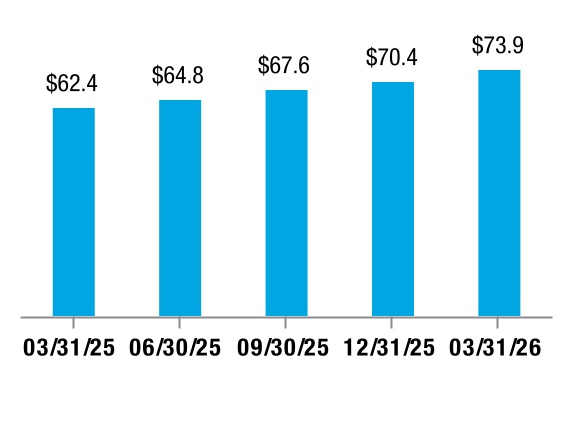

Net Worth

(In billions)

Key Drivers:

nNet income was $3.6 billion, up 27% from 1Q 2025, primarily driven by higher net revenues and a credit reserve release in 1Q 2026 compared to a credit reserve build in 1Q 2025.

nNet revenues were $6.1 billion, an increase of 5% year-over-year, primarily driven by higher net interest income, partially offset by lower non-interest income.

nNet worth was $73.9 billion as of March 31, 2026, up from $62.4 billion as of March 31, 2025. The quarterly increases in net worth have been, or will be, added to the aggregate liquidation preference of the senior preferred stock. The liquidation preference of the senior preferred stock was $143.0 billion on March 31, 2026, and will increase to $146.6 billion on June 30, 2026 based on the increase in net worth in 1Q 2026.

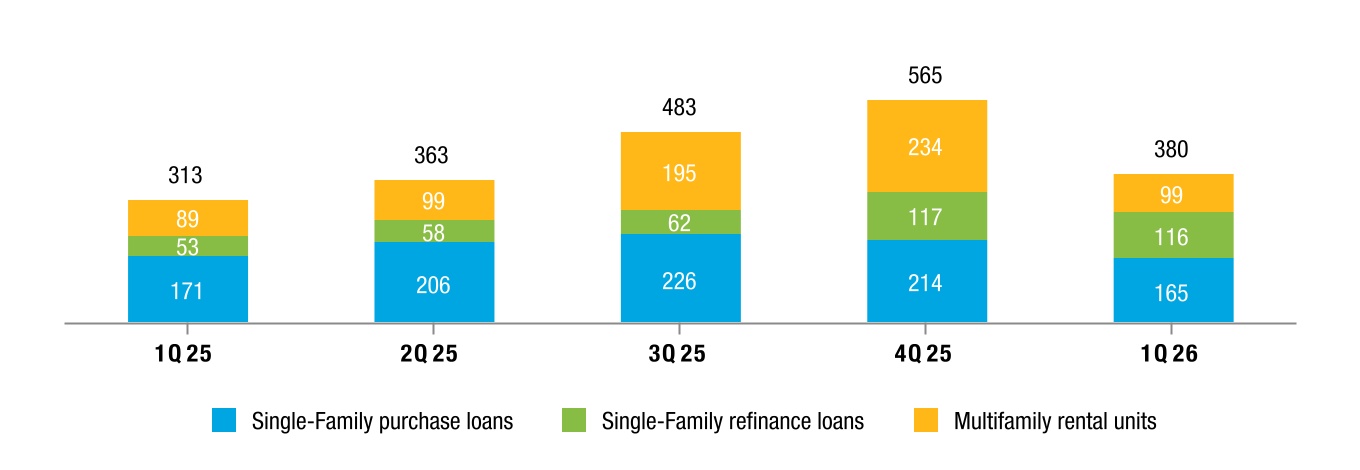

Market Liquidity

Market Liquidity

(In thousands)

We support the U.S. housing market by executing our mission to provide liquidity and help maintain credit availability for new and refinanced single-family mortgages as well as for rental housing. We provided $116 billion in liquidity to the mortgage market in 1Q 2026, which enabled the financing of 380,000 home purchases, refinancings, and rental units.

Freddie Mac 1Q 2026 Form 10-Q

2

Management's Discussion and Analysis

Introduction

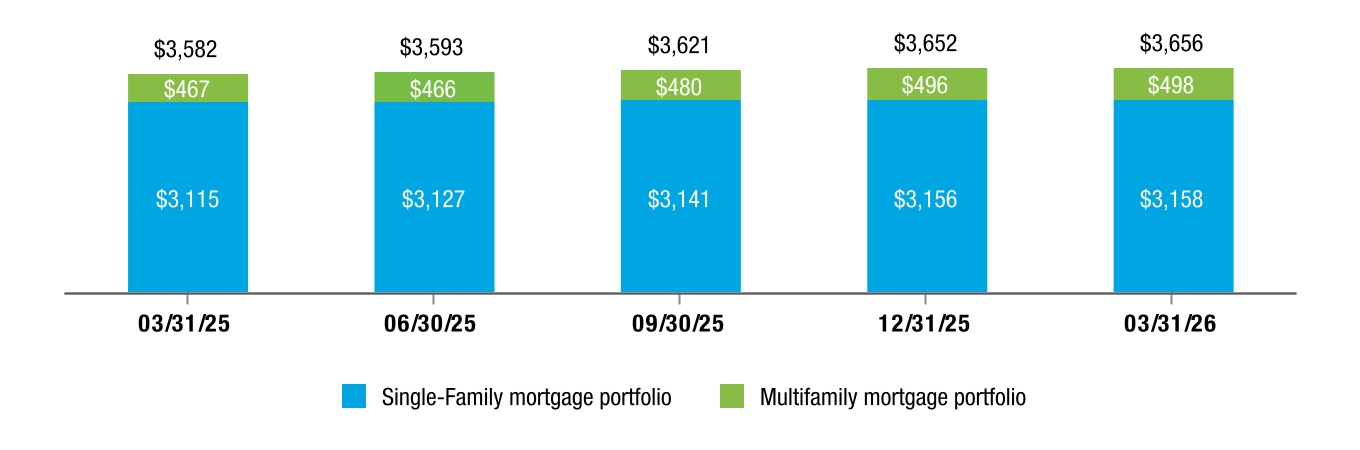

Mortgage Portfolio Balances

Mortgage Portfolio

(UPB in billions)

Key Drivers:

nOur mortgage portfolio increased 2% year-over-year to $3.7 trillion at March 31, 2026, continuing to grow at a moderate pace.

lOur Single-Family mortgage portfolio was $3.2 trillion at March 31, 2026, up 1% year-over-year.

lOur Multifamily mortgage portfolio was $498 billion at March 31, 2026, up 7% year-over-year.

Freddie Mac 1Q 2026 Form 10-Q

3

Management's Discussion and Analysis

Consolidated Results of Operations

CONSOLIDATED RESULTS OF OPERATIONS

The discussion of our consolidated results of operations should be read in conjunction with our condensed consolidated financial statements and accompanying notes.

The table below compares our summarized consolidated results of operations.

Table 1 - Summary of Consolidated Statements of Income and Comprehensive Income

Change

(Dollars in millions)

1Q 2026

1Q 2025

$

%

Net interest income

$5,619

$5,102

$517

10

%

Non-interest income

514

750

(236)

(31)

Net revenues

6,133

5,852

281

5

(Provision) benefit for credit losses

320

(280)

600

NM

Non-interest expense

(2,022)

(2,088)

66

3

Income before income tax expense

4,431

3,484

947

27

Income tax expense

(873)

(690)

(183)

(27)

Net income

3,558

2,794

764

27

Other comprehensive income (loss), net of taxes and reclassification adjustments

(20)

34

(54)

NM

Comprehensive income

$3,538

$2,828

$710

25

%

Net Revenues

Net Interest Income

The table below presents the components of net interest income.

Table 2 - Components of Net Interest Income

Change

(Dollars in millions)

1Q 2026

1Q 2025

$

%

Guarantee net interest income:

Contractual net interest income

$4,142

$3,981

$161

4

%

Deferred fee income

219

190

29

15

Total guarantee net interest income

4,361

4,171

190

5

Investments net interest income

1,357

1,297

60

5

Impact on net interest income from hedge accounting

(99)

(366)

267

73

Net interest income

$5,619

$5,102

$517

10

%

Key Drivers:

nGuarantee net interest income

l1Q 2026 vs. 1Q 2025 - Increased primarily due to an increase in the balance of fully guaranteed securitizations in the Multifamily mortgage portfolio due to the change in our Multifamily business strategy and continued mortgage portfolio growth in Single-Family.

nInvestments net interest income

l1Q 2026 vs. 1Q 2025 - Increased primarily due to growth in the mortgage-related investments portfolio.

nImpact on net interest income from hedge accounting

l1Q 2026 vs. 1Q 2025 - Decreased due to lower expense related to debt in hedge accounting relationships.

Freddie Mac 1Q 2026 Form 10-Q

4

Management's Discussion and Analysis

Consolidated Results of Operations

Net Interest Yield Analysis

The table below presents a yield analysis of interest-earning assets and interest-bearing liabilities.

Table 3 - Analysis of Net Interest Yield

1Q 2026

1Q 2025

(Dollars in millions)

Average

Balance

Interest

Income

(Expense)

Average

Rate

Average

Balance

Interest

Income

(Expense)

Average

Rate

Interest-earning assets:

Cash and cash equivalents

$8,363

$52

2.51

%

$9,355

$79

3.38

%

Securities purchased under agreements to resell

84,924

798

3.76

111,687

1,240

4.44

Investment securities

76,752

833

4.34

55,955

620

4.43

Mortgage loans held by consolidated trusts(1)

3,216,438

30,966

3.85

3,129,811

28,591

3.65

Mortgage loans held by Freddie Mac(1)

86,808

966

4.45

70,429

804

4.57

Other assets

3,100

35

4.48

2,055

31

5.98

Total interest-earning assets

3,476,385

33,650

3.87

3,379,292

31,365

3.71

Interest-bearing liabilities:

Debt issued by consolidated trusts

3,189,597

(26,001)

(3.26)

3,125,203

(24,059)

(3.08)

Short-term debt

30,089

(275)

(3.66)

14,822

(161)

(4.36)

Long-term debt

169,973

(1,702)

(4.00)

170,573

(2,000)

(4.69)

Securities sold under agreements to repurchase

5,949

(53)

(3.57)

3,999

(43)

(4.25)

Total interest-bearing liabilities

3,395,608

(28,031)

(3.30)

3,314,597

(26,263)

(3.17)

Net interest income/yield

$5,619

0.65

%

$5,102

0.60

%

(1)Loan fees included in interest income were $0.4 billion and $0.3 billion for mortgage loans held by consolidated trusts in 1Q 2026 and 1Q 2025, respectively. Loan fees for mortgage loans held by Freddie Mac were not material in 1Q 2026 or 1Q 2025 .

Non-Interest Income

The table below presents the components of non-interest income.

Table 4 - Components of Non-Interest Income

Change

(Dollars in millions)

1Q 2026

1Q 2025

$

%

Guarantee income

$320

$440

($120)

(27)

%

Investment gains (losses), net

42

192

(150)

(78)

Other income

152

118

34

29

Non-interest income

$514

$750

($236)

(31)

%

Key Drivers:

nGuarantee income

l1Q 2026 vs. 1Q 2025- Decreased primarily due to fair value losses as a result of increases in medium-term interest rates during 1Q 2026, coupled with lower revenues from a declining off-balance sheet financial guarantee portfolio.

nInvestment gains (losses), net

l1Q 2026 vs. 1Q 2025- Decreased primarily due to a lower volume of loan sale activities as we shifted the Multifamily business model to primarily issue fully guaranteed securities, as well as losses from debt extinguishments in 1Q 2026.

Freddie Mac 1Q 2026 Form 10-Q

5

Management's Discussion and Analysis

Consolidated Results of Operations

(Provision) Benefit for Credit Losses

The table below presents the components of provision for credit losses.

Table 5 - (Provision) Benefit for Credit Losses

Change

(Dollars in millions)

1Q 2026

1Q 2025

$

%

Single-Family

$311

($228)

$539

NM

Multifamily

9

(52)

61

NM

(Provision) benefit for credit losses

$320

($280)

$600

NM

Key Drivers:

n1Q 2026 vs. 1Q 2025 - The benefit for credit losses for 1Q 2026 was driven by a credit reserve release in Single-Family primarily attributable to changes in our views of forecasted house price growth rates. The provision for credit losses for 1Q 2025 was primarily driven by a credit reserve build in Single-Family attributable to new acquisitions.

Non-Interest Expense

The table below presents the components of non-interest expense.

Table 6 - Components of Non-Interest Expense

Change

(Dollars in millions)

1Q 2026

1Q 2025

$

%

Salaries and employee benefits

($376)

($423)

$47

11

%

Professional services, technology, and occupancy

(250)

(253)

3

1

Credit enhancement expense

(441)

(540)

99

18

Legislative and regulatory assessments:

Legislated guarantee fees expense

(757)

(744)

(13)

(2)

Affordable housing funds allocation

(48)

(37)

(11)

(30)

Regulatory assessment

(27)

(36)

9

25

Total legislative and regulatory assessments

(832)

(817)

(15)

(2)

Other expense

(123)

(55)

(68)

(124)

Non-interest expense

($2,022)

($2,088)

$66

3

%

Key Drivers:

nSalaries and employee benefits

l1Q 2026 vs. 1Q 2025 - Decreased primarily due to lower employee headcount.

nCredit enhancement expense

l1Q 2026 vs. 1Q 2025 - Decreased primarily due to a lower UPB of Single-Family CRT transactions outstanding, retention of higher levels of initial losses on recent CRT transactions, and lower losses on STACR Trust note repurchases.

Freddie Mac 1Q 2026 Form 10-Q

6

Management's Discussion and Analysis

Consolidated Balance Sheets Analysis

CONSOLIDATED BALANCE SHEETS ANALYSIS

The table below compares our summarized condensed consolidated balance sheets.

As of March 31, 2026 compared to December 31, 2025:

nInvestment securities decreased primarily due to net sales of U.S. Treasury securities.

nMortgage loans held-for-investment and debt issued by consolidated trusts increased primarily due togrowth in our mortgage portfolio.

nShort-term debt decreased primarily due to lower funding needs.

Freddie Mac 1Q 2026 Form 10-Q

7

Management's Discussion and Analysis

Our Portfolios

OUR PORTFOLIOS

Mortgage Portfolio

The table below presents the UPB of our mortgage portfolio by segment.

Table 8 - Mortgage Portfolio

March 31, 2026

December 31, 2025

(In millions)

Single-Family

Multifamily

Total

Single-Family

Multifamily

Total

Mortgage loans held-for-investment:

By consolidated trusts

$3,065,699

$137,404

$3,203,103

$3,063,232

$115,354

$3,178,586

By Freddie Mac

54,261

26,864

81,125

54,713

37,770

92,483

Total mortgage loans held-for-investment

3,119,960

164,268

3,284,228

3,117,945

153,124

3,271,069

Mortgage loans held-for-sale

1,449

2

1,451

1,108

136

1,244

Total mortgage loans

3,121,409

164,270

3,285,679

3,119,053

153,260

3,272,313

Mortgage-related guarantees:

Mortgage loans held by nonconsolidated trusts

29,528

324,122

353,650

30,025

332,572

362,597

Other mortgage-related guarantees

7,044

9,940

16,984

7,212

10,003

17,215

Total mortgage-related guarantees

36,572

334,062

370,634

37,237

342,575

379,812

Total mortgage portfolio

$3,157,981

$498,332

$3,656,313

$3,156,290

$495,835

$3,652,125

Guaranteed mortgage-related securities:

Issued by consolidated trusts

$3,092,678

$137,421

$3,230,099

$3,084,668

$115,610

$3,200,278

Issued by non-consolidated trusts

24,180

292,245

316,425

24,604

299,507

324,111

Total guaranteed mortgage-related securities

$3,116,858

$429,666

$3,546,524

$3,109,272

$415,117

$3,524,389

Investments Portfolio

Our investments portfolio consists of our mortgage-related investments portfolio and other investments portfolio.

Mortgage-Related Investments Portfolio

The Purchase Agreement limits the size of our mortgage-related investments portfolio to a maximum amount of $225 billion. We primarily use our mortgage-related investments portfolio to provide liquidity to the mortgage market by purchasing loans for our securitization pipeline and by purchasing delinquent and modified loans from securitization trusts. We also invest in agency mortgage-related securities.

The calculation of mortgage assets subject to the Purchase Agreement cap includes the UPB of mortgage assets and 10% of the notional value of interest-only securities. We are permitted to increase our agency MBS investments, provided that our total mortgage assets do not exceed the $225 billion cap under the terms of our senior preferred stock purchase agreement with Treasury, with CMO securities capped at $5 billion as part of agency MBS investments. We are also subject to additional limitations on the size and composition of our mortgage-related investments portfolio pursuant to FHFA guidance. For additional information on the restrictions on our mortgage-related investments portfolio, see the MD&A - Conservatorship and Related Matters section in our 2025 Annual Report.

Freddie Mac 1Q 2026 Form 10-Q

8

Management's Discussion and Analysis

Our Portfolios

The table below presents the details of our mortgage-related investments portfolio.

Table 9 - Mortgage-Related Investments Portfolio

March 31, 2026

December 31, 2025

(In millions)

Single-Family

Multifamily

Total

Single-Family

Multifamily

Total

Unsecuritized mortgage loans(1)

$55,710

$26,866

$82,576

$55,821

$37,906

$93,727

Mortgage-related securities:

Investment securities

5,241

3,207

8,448

4,438

3,891

8,329

Debt issued by consolidated trusts

47,109

1,628

48,737

35,758

1,413

37,171

Total mortgage-related securities

52,350

4,835

57,185

40,196

5,304

45,500

Mortgage-related investments portfolio

$108,060

$31,701

$139,761

$96,017

$43,210

$139,227

10% of notional amount of interest-only securities

$21,691

$21,995

Mortgage-related investments portfolio for purposes of Purchase Agreement cap

161,452

161,222

(1)Includes $37.9 billion and $35.9 billion of single-family loans that we have purchased from securitization trusts as of March 31, 2026 and December 31, 2025, respectively.

Other Investments Portfolio

The table below presents the details of the carrying value of our other investments portfolio.

Table 10 - Other Investments Portfolio

March 31, 2026

December 31, 2025

(In millions)

Liquidity and Contingency Operating Portfolio

Custodial Account

Other

Total Other Investments Portfolio

Liquidity and Contingency Operating Portfolio

Custodial Account

Other

Total Other Investments Portfolio

Cash and cash equivalents

$3,169

$1,202

$98

$4,469

$4,092

$1,136

$99

$5,327

Securities purchased under

agreements to resell

54,678

22,262

2,188

79,128

57,181

19,107

2,090

78,378

Non-mortgage related securities(1)

55,817

—

5,983

61,800

65,088

—

6,076

71,164

Other assets(2)

—

—

8,501

8,501

—

—

7,776

7,776

Other investments portfolio

$113,664

$23,464

$16,770

$153,898

$126,361

$20,243

$16,041

$162,645

(1)Primarily consists of U.S. Treasury securities.

(2)Primarily includes LIHTC investments and advances to lenders.

Freddie Mac 1Q 2026 Form 10-Q

9

Management's Discussion and Analysis

Our Business Segments

OUR BUSINESS SEGMENTS

As shown in the table below, we have two reportable segments, which are based on the way we manage our business.

Segment

Description

Single-Family

Reflects results from our purchase, securitization, and guarantee of single-family loans, our investments in single-family loans and mortgage-related securities, the management of Single-Family mortgage credit risk and market risk, and any results of our treasury function that are not allocated to each segment.

Multifamily

Reflects results from our purchase, securitization, and guarantee of multifamily loans, our investments in multifamily loans and mortgage-related securities, and the management of Multifamily mortgage credit risk and market risk.

Segment Net Revenues and Net Income

The charts below show our net revenues and net income by segment.

Segment Net Revenues

(In billions)

Segment Net Income

(In billions)

Freddie Mac 1Q 2026 Form 10-Q

10

Management's Discussion and Analysis

Our Business Segments | Single-Family

Single-Family

Housing and Mortgage Market Metrics

The table below presents certain single-family housing and mortgage market indicators that can significantly affect our business and financial results. Certain market and macroeconomic prior period data have been updated to reflect revised historical data.

Table 11 - Single-Family Housing and Mortgage Market Metrics(1)

(Mortgage amounts in billions, units in thousands)

1Q 2026

4Q 2025

3Q 2025

2Q 2025

1Q 2025

Home sales (in units):

Total home sales (annualized seasonally adjusted amount)

4,630

4,866

4,735

4,678

4,742

Sales of existing homes

4,043

4,157

4,047

4,013

4,087

Sales of new homes(2)

587

709

688

665

655

Mortgage originations (estimated)

$533

$581

$502

$506

$371

Mortgage debt outstanding(3)

N/A

14,770

14,666

14,541

14,417

Quarterly house price growth rate (seasonally adjusted rate)

0.1

%

0.4

%

0.3

%

(0.1)

%

0.3

%

30-year PMMS rate at period end

6.38

%

6.15

%

6.30

%

6.77

%

6.65

%

(1) Sources: Home sales - National Association of Realtors and U.S Census Bureau; Mortgage originations - Fannie Mae; Mortgage debt outstanding - Federal Reserve Financial Accounts of the United States of America; House price growth rate and 30-year PMMS rate - Freddie Mac.

(2) For 1Q 2026, the sales of new homes amount is based on annualized seasonally adjusted data through January 31, 2026 (the latest available information).

(3) For 1Q 2026, the mortgage debt outstanding balance is not yet available.

Business Results

The table and related discussion below present selected business results of our Single-Family segment.

Table 12 - Single-Family Segment Business Results

Change

(UPB in millions, loan count in thousands)

1Q 2026

1Q 2025

Amount

%

New business activity:

UPB:

Total UPB

$102,513

$77,646

$24,867

32

%

Home purchase

59,964

61,921

(1,957)

(3)

Refinance

42,549

15,725

26,824

171

Number of loans:

Total number of loans

281

224

57

25

Home purchase

165

171

(6)

(4)

Refinance

116

53

63

119

Average estimated guarantee fee rate (bps)(1)

54

54

Mortgage portfolio at period end:

UPB

$3,157,981

$3,115,180

$42,801

1

Average estimated guarantee fee rate (bps)(1)(2)

50

49

(1) Estimated guarantee fee rate calculations exclude the legislated guarantee fees and include deferred fees recognized over the estimated life of the related loans based on month-end market rates for the month of acquisition.

(2) Estimated guarantee fee rate calculations for the Single-Family mortgage portfolio exclude certain loans, the majority of which are held by VIEs that we do not consolidate. The UPB of these excluded loans was $38 billion and $40 billion as of March 31, 2026 and March 31, 2025, respectively.

nOur loan purchase and guarantee activity increased in 1Q 2026 compared to 1Q 2025 primarily driven by an increase in refinance activity due to lower mortgage interest rates.

nOur Single-Family mortgage portfolio was $3.2 trillion at March 31, 2026, up 1% year-over-year. The mortgage portfolio continued to grow at a moderate pace.

Freddie Mac 1Q 2026 Form 10-Q

11

Management's Discussion and Analysis

Our Business Segments | Single-Family

Financial Results

The table below presents the results of operations for our Single-Family segment. See Note 11 for additional information about segment financial results.

Other comprehensive income (loss), net of taxes and reclassification adjustments

(13)

8

(21)

NM

Comprehensive income

$2,963

$2,269

$694

31

%

Key Drivers:

n 1Q 2026 vs. 1Q 2025

lNet income of $3.0 billion, up 32% year-over-year.

–Net revenues were $5.2 billion, up 5% year-over-year.

◦Net interest income was $5.1 billion, up 8% year-over-year, primarily driven by continued mortgage portfolio growth and growth in the mortgage-related investments portfolio.

–The benefit for credit losses was $0.3 billion for 1Q 2026, driven by a credit reserve release primarily attributable to changes in our views of forecasted house price growth rates. The provision for credit losses of $0.2 billion for 1Q 2025 was primarily driven by a credit reserve build attributable to new acquisitions.

–Non-interest expense was $1.8 billion for 1Q 2026, down 5% year-over-year, primarily driven by a decrease in salaries and employee benefits and lower credit enhancement expense.

Freddie Mac 1Q 2026 Form 10-Q

12

Management's Discussion and Analysis

Our Business Segments |Multifamily

Multifamily

Housing and Mortgage Market Metrics

The table below presents certain multifamily housing and mortgage market indicators that can significantly affect our business and financial results. For example, vacancy rates provide insight into the balance between supply and demand. Meanwhile, effective rent growth, which accounts for concessions and discounts offered by landlords, represents the actual change in average rental income over time. Certain market and macroeconomic prior period data have been updated to reflect revised historical data.

Table 14 - Multifamily Housing and Mortgage Market Metrics(1)

(UPB in billions)

1Q 2026

4Q 2025

3Q 2025

2Q 2025

1Q 2025

Apartment vacancy rates

6.8

%

6.7

%

6.6

%

6.6

%

6.5

%

Quarterly change in effective rents

0.6

%

(0.8)

%

(0.1)

%

0.8

%

0.2

%

Mortgage debt outstanding(2)

N/A

$2,447

$2,393

$2,352

$2,330

Quarterly property price growth rate

0.3

%

0.4

%

(0.1)

%

(0.6)

%

0.1

%

(1) Sources: Apartment vacancy rates and change in effective rents - Moody's Analytics; Mortgage debt outstanding - Federal Reserve Financial Accounts of the United States of America; Property price growth rate - Real Capital Analytics Commercial Property Price Index (RCA CPPI).

(2) The 1Q 2026 U.S. multifamily mortgage debt outstanding balance is not yet available.

Business Results

The table and related discussion below present selected business results of our Multifamily segment.

Table 15 - Multifamily Segment Business Results

Change

(UPB in millions, units in thousands)

1Q 2026

1Q 2025

Amount

%

New business activity:

UPB(1)

$12,847

$10,276

$2,571

25

%

Total units financed(2)

99

89

10

11

Mission-driven affordable housing percentage

66

%

65

%

Outstanding index lock agreements and commitments(3)

$22,788

$16,179

$6,609

41

New securitization activity(4):

Total UPB

$23,433

$16,113

$7,320

45

Senior subordinate securitizations

666

7,273

(6,607)

(91)

Fully guaranteed securitizations

22,767

8,840

13,927

158

Mortgage portfolio at period end:

UPB

$498,332

$466,500

$31,832

7

Fixed-rate percentage

85

%

83

%

Average guarantee fees rate charged (bps)(5)

58

52

(1) Excludes new LIHTC investments of $0.2 billion for 1Q 2026. New LIHTC investments in 1Q 2025 were not material.

(2) Includes rental units financed by supplemental loans.

(3) At period end.

(4) Excludes resecuritizations.

(5) Based on guarantee exposure of $440 billion and $407 billion for 1Q 2026 and 1Q 2025, respectively, which includes guaranteed mortgage related securities that are consolidated on our condensed consolidated balance sheet where income from guarantees is recognized in net interest income.

nOur new business activity was $12.8 billion in 1Q 2026, up 25% year-over-year, primarily driven by a larger new business activity pipeline entering 1Q 2026 due to a larger multifamily mortgage originations market. Approximately 66% of our 1Q 2026 new business activity, based on UPB, was mission-driven, affordable housing, exceeding FHFA's annual minimum requirement of 50%.

nTotal securitization issuance UPB was $23.4 billion in 1Q 2026, up 45% year-over-year, driven by a larger average securitization pipeline. The larger percentage of fully guaranteed securitizations was due to the Multifamily business

Freddie Mac 1Q 2026 Form 10-Q

13

Management's Discussion and Analysis

Our Business Segments |Multifamily

strategy change.

nOur Multifamily mortgage portfolio was $498 billion as of March 31, 2026, up 7% year-over-year, primarily driven by our new business activity.

nThe average guarantee fee rate on our guarantee exposures increased year-over-year, primarily due to continued growth of fully guaranteed securitization issuances for which we charge higher guarantee fee rates.

Financial Results

The table below presents the results of operations for our Multifamily segment. See Note 11 for additional information about segment financial results.

Table 16 - Multifamily Segment Financial Results

Change

(Dollars in millions)

1Q 2026

1Q 2025

$

%

Net interest income

$499

$349

$150

43

%

Non-interest income

459

585

(126)

(22)

Net revenues

958

934

24

3

(Provision) benefit for credit losses

9

(52)

61

NM

Non-interest expense

(242)

(217)

(25)

(12)

Income before income tax expense

725

665

60

9

Income tax expense

(143)

(132)

(11)

(8)

Net income

582

533

49

9

Other comprehensive income (loss), net of taxes and reclassification adjustments

(7)

26

(33)

NM

Comprehensive income

$575

$559

$16

3

%

Key Drivers:

n1Q 2026 vs. 1Q 2025

lNet income of $0.6 billion, up 9% year-over-year.

–Net revenues were $1.0 billion, up 3% year-over-year.

◦Net interest income was $0.5 billion, up 43% year-over-year, primarily driven by an increase in the balance of fully guaranteed securitizations in the Multifamily mortgage portfolio due to the change in Multifamily business strategy.

◦Non-interest income was $0.5 billion, down 22% year-over-year, primarily driven by a lower volume of loan sale activities, as we shifted the Multifamily business model to primarily issue fully guaranteed securitizations.

Freddie Mac 1Q 2026 Form 10-Q

14

Management's Discussion and Analysis

Risk Management

RISK MANAGEMENT

To achieve our mission, we take risks as an integral part of our business activities. We are exposed to the following key types of risk: credit risk, market risk, liquidity risk, operational risk, compliance risk, legal risk, strategic risk, and reputation risk.

Credit Risk

Allowance for Credit Losses

The tables below present a summary of the changes in our allowance for credit losses and key allowance for credit losses ratios.

Table 17 - Allowance for Credit Losses Activity

1Q 2026

1Q 2025

(Dollars in millions)

Single-Family

Multifamily

Total

Single-Family

Multifamily

Total

Allowance for credit losses:

Beginning balance

$7,549

$956

$8,505

$6,691

$548

$7,239

Provision (benefit) for credit losses

(311)

(9)

(320)

228

52

280

Charge-offs

(178)

(64)

(242)

(191)

(1)

(192)

Recoveries collected

60

1

61

27

1

28

Net charge-offs

(118)

(63)

(181)

(164)

—

(164)

Other(1)

108

1

109

96

—

96

Ending balance

$7,228

$885

$8,113

$6,851

$600

$7,451

Average loans outstanding during the period(2)

$3,148,567

$151,752

$3,300,319

$3,101,599

$86,445

$3,188,044

Net charge-offs to average loans outstanding

—

%

0.04

%

0.01

%

0.01

%

—

%

0.01

%

(1)Primarily includes capitalization of past due interest related to non-accrual loans that received payment deferral plans and loan modifications.

(2)Based on amortized cost basis of mortgage loans held-for-investment for which we have not elected the fair value option.

Table 18 - Allowance for Credit Losses Ratios

March 31, 2026

December 31, 2025

(Dollars in millions)

Single-Family

Multifamily

Total

Single-Family

Multifamily

Total

Allowance for credit losses ratios:

Allowance for credit losses(1) to total loans outstanding

0.22

%

0.42

%

0.23

%

0.23

%

0.46

%

0.24

%

Non-accrual loans to total loans outstanding

0.56

0.03

0.54

0.55

0.16

0.54

Allowance for credit losses to non-accrual loans

39.46

1,321.79

43.11

41.84

295.59

45.10

Balances:

Allowance for credit losses on mortgage loans held-for-investment

$6,977

$666

$7,643

$7,297

$671

$7,968

Total loans outstanding(2)

3,146,251

156,792

3,303,043

3,145,436

145,593

3,291,029

Non-accrual loans(2)

17,681

50

17,731

17,442

227

17,669

(1)Represents allowance for credit losses on mortgage loans held-for-investment.

(2)Based on amortized cost basis of mortgage loans held-for-investment for which we have not elected the fair value option.

nMarch 31, 2026 vs. December 31, 2025 - The balance of non-accrual loans increased by $62 million due to a $239 million increase in the balance of non-accrual loans in Single-Family, partially offset by a $177 million decrease in the balance of non-accrual loans in Multifamily. The decrease in Multifamily was primarily due to loan dispositions and borrower re-performance.

Freddie Mac 1Q 2026 Form 10-Q

15

Management's Discussion and Analysis

Risk Management

Single-Family Mortgage Credit Risk

Credit Quality of New Business Activity

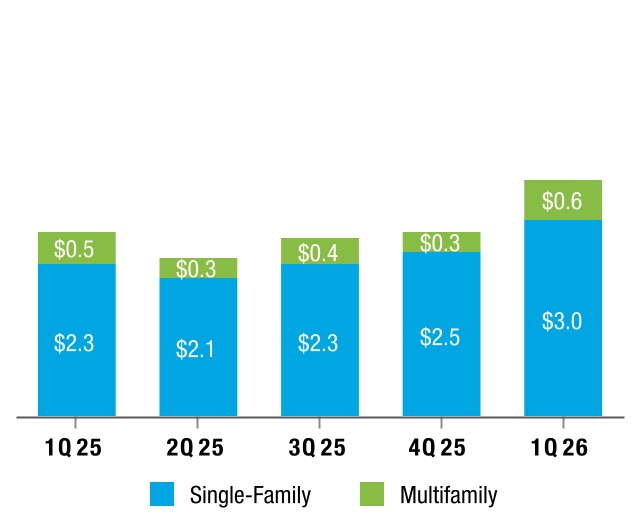

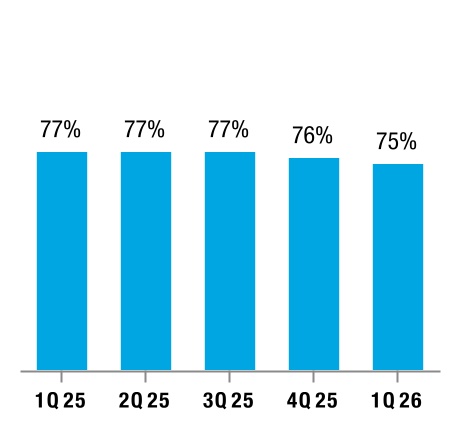

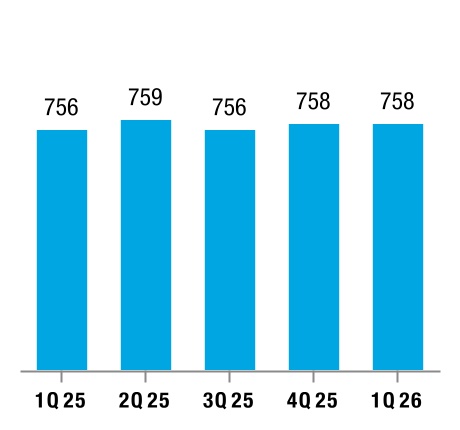

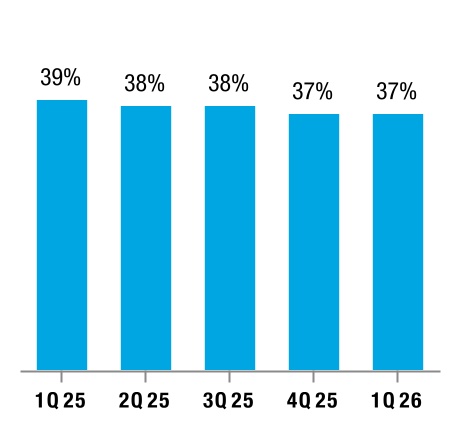

Loan Purchase Credit Characteristics

We monitor and evaluate market conditions that could affect the credit quality of our single-family loan purchases. See MD&A - Our Business Segments - Single-Family - Housing and Mortgage Market Metrics for additional information on market conditions. Additionally, when managing our new acquisitions, we consider our risk limits and guidance from FHFA and capital requirements under the ERCF. This may affect the volume and characteristics of our loan acquisitions. See MD&A - Regulation and Supervision - Federal Housing Finance Agency in our 2025 Annual Report for additional information on guidance from FHFA.

The charts below show the credit profile of the single-family loans we purchased.

Weighted Average Original LTV Ratio

Weighted Average Original Credit Score

Weighted Average Original DTI Ratio

Freddie Mac 1Q 2026 Form 10-Q

16

Management's Discussion and Analysis

Risk Management

The table below contains additional information about the single-family loans we purchased.

Table 19 - Single-Family New Business Activity

1Q 2026

1Q 2025

(Dollars in millions, except average loan UPB)

Amount

% of Total

Amount

% of Total

20- and 30-year, amortizing fixed-rate

$91,587

90

%

$72,772

93

%

15-year or less, amortizing fixed-rate

7,521

7

4,434

6

Adjustable-rate

3,405

3

440

1

Total

$102,513

100

%

$77,646

100

%

Average loan UPB (in thousands)

$365

$347

Percentage of purchases

DTI ratio > 45%

24

%

30

%

Original LTV ratio > 90%

19

23

Transaction type:

Guarantor swap

63

71

Cash window

37

29

Property type:

Detached single-family houses and townhouses

93

92

Condominium or co-op

7

8

Occupancy type:

Primary residence

94

93

Second home

2

2

Investment property

4

5

Loan purpose:

Purchase

58

79

Cash-out refinance

10

11

Other refinance

32

10

Credit Enhancements

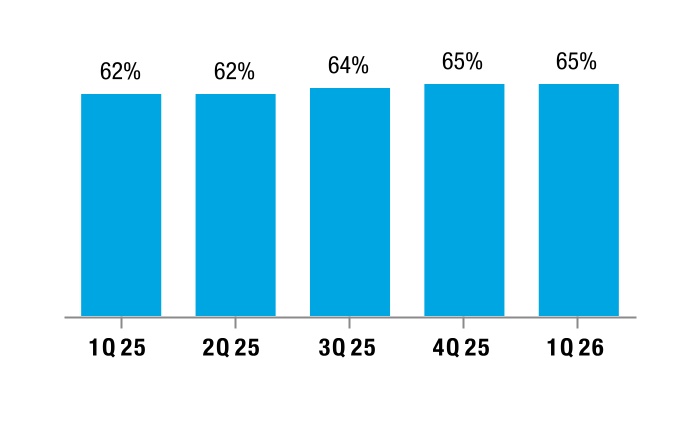

We engage in various credit enhancement arrangements to reduce our credit risk exposure on our single-family loans.

The table below provides the UPB of the mortgage loans acquired during the periods presented that were covered by primary mortgage insurance, the UPB of the mortgage loans covered by CRT transactions we entered into during the periods presented, and maximum coverage related to these newly acquired credit enhancements. In recent periods, we have changed our business strategy and revised our CRT transactions by retaining higher levels of initial losses. As a result, the benefits provided by these revised CRT transactions may be lower than those provided by the earlier CRT transactions even if the maximum coverage provided by the more recent CRT transactions is similar to that provided by the earlier CRT transactions.

(1) The primary mortgage insurance and CRT transactions presented in this table are not mutually exclusive as a single loan may be covered by both primary mortgage insurance and CRT transactions.

(2) The credit risk positions to which the maximum coverage applies may vary on a transaction-by-transaction basis.

(1) The credit risk positions to which the maximum coverage applies may vary on a transaction-by-transaction basis.

(2) Amounts exclude certain loans for which we do not control servicing, as the coverage information for these loans is not readily available to us.

(3) Other reconciling items primarily include timing differences in reporting cycles between the UPB of certain CRT transactions and the UPB of the underlying loans.

Freddie Mac 1Q 2026 Form 10-Q

18

Management's Discussion and Analysis

Risk Management

Credit Enhancement Coverage Characteristics

The table below provides the serious delinquency rates for the credit-enhanced and non-credit-enhanced loans in our Single-Family mortgage portfolio. The credit-enhanced categories are not mutually exclusive as a single loan may be covered by both primary mortgage insurance and other credit enhancements.

Table 22 - Serious Delinquency Rates for Credit-Enhanced and Non-Credit-Enhanced Loans in Our Single-Family Mortgage Portfolio

March 31, 2026

December 31, 2025

(% of portfolio based on UPB)(1)

% of Portfolio(2)

SDQ Rate

% of Portfolio(2)

SDQ Rate

Credit-enhanced:

Primary mortgage insurance

22

%

1.23

%

22

%

1.19

%

CRT and other

53

0.70

52

0.68

Non-credit-enhanced

38

0.41

39

0.40

Total

N/A

0.60

N/A

0.59

(1)Excludes loans underlying certain securitization products for which loan-level data is not available.

(2)Percentages do not total to 100% as a single loan may be included in multiple line items.

Credit Enhancement Recoveries

Our expected recovery receivable from freestanding credit enhancements was $0.1 billion as of both March 31, 2026 and December 31, 2025.

Monitoring Loan Performance and Characteristics

We review loan performance, including delinquency statistics and related loan characteristics, in conjunction with housing market and economic conditions, to assess credit risk when estimating our allowance for credit losses.

Loan Credit Characteristics

The table below contains selected credit characteristics of the loans in our Single-Family mortgage portfolio.

Single-Family mortgage portfolio year of origination:

2026

$64,135

759

759

75

%

76

%

0.00

%

33

%

2025

352,457

756

752

77

76

0.11

48

2024

272,367

753

749

78

74

0.69

72

2023

199,315

750

741

79

71

1.19

76

2022

356,008

746

740

76

63

1.03

69

2021 and prior

1,913,699

751

757

72

42

0.55

61

Total

$3,157,981

751

753

74

53

0.60

62

Loan count(in thousands)

13,922

Average loan UPB (in thousands)

$227

Freddie Mac 1Q 2026 Form 10-Q

19

Management's Discussion and Analysis

Risk Management

December 31, 2025

(Dollars in millions, except average loan UPB)

Amount

Original Credit Score

Current Credit Score

Original LTV Ratio

Current LTV Ratio

SDQ Rate

% of UPB with Credit Enhancement

Single-Family mortgage portfolio year of origination:

2025

$333,409

757

753

77

%

76

%

0.06

%

38

%

2024

291,738

753

752

78

74

0.56

68

2023

211,793

750

743

79

71

1.06

76

2022

364,361

746

741

76

63

1.01

69

2021

841,701

752

755

71

49

0.44

64

2020 and prior

1,113,288

750

761

73

37

0.60

58

Total

$3,156,290

751

754

74

53

0.59

61

Loan count(in thousands)

13,933

Average loan UPB (in thousands)

$227

(1)Excludes certain credit quality characteristics and serious delinquency rate information on loans underlying certain securitization products for which data was not available.

The table below presents the combination of credit score and CLTV ratio attributes of loans in our Single-Family mortgage portfolio.

(1) Excludes loans underlying certain securitization products for which current credit score is not available.

Geographic Concentrations

We purchase mortgage loans from across the U.S. but do not purchase an equal number of loans from each geographic area, leading to concentrations of credit risk in certain geographic areas. Local economic and other conditions can affect the borrower's ability to repay and the value of the underlying collateral. Property insurance markets in certain geographic areas, including areas with high risk of natural disaster events, have observed increases in property insurance premiums and reduction in the availability of coverage in recent years. In addition, certain states and municipalities have passed or may pass laws that limit our ability to foreclose or evict and make it more difficult and costly to manage our risk.

See Note 12 for additional information about the geographic distribution of our Single-Family mortgage portfolio.

Freddie Mac 1Q 2026 Form 10-Q

20

Management's Discussion and Analysis

Risk Management

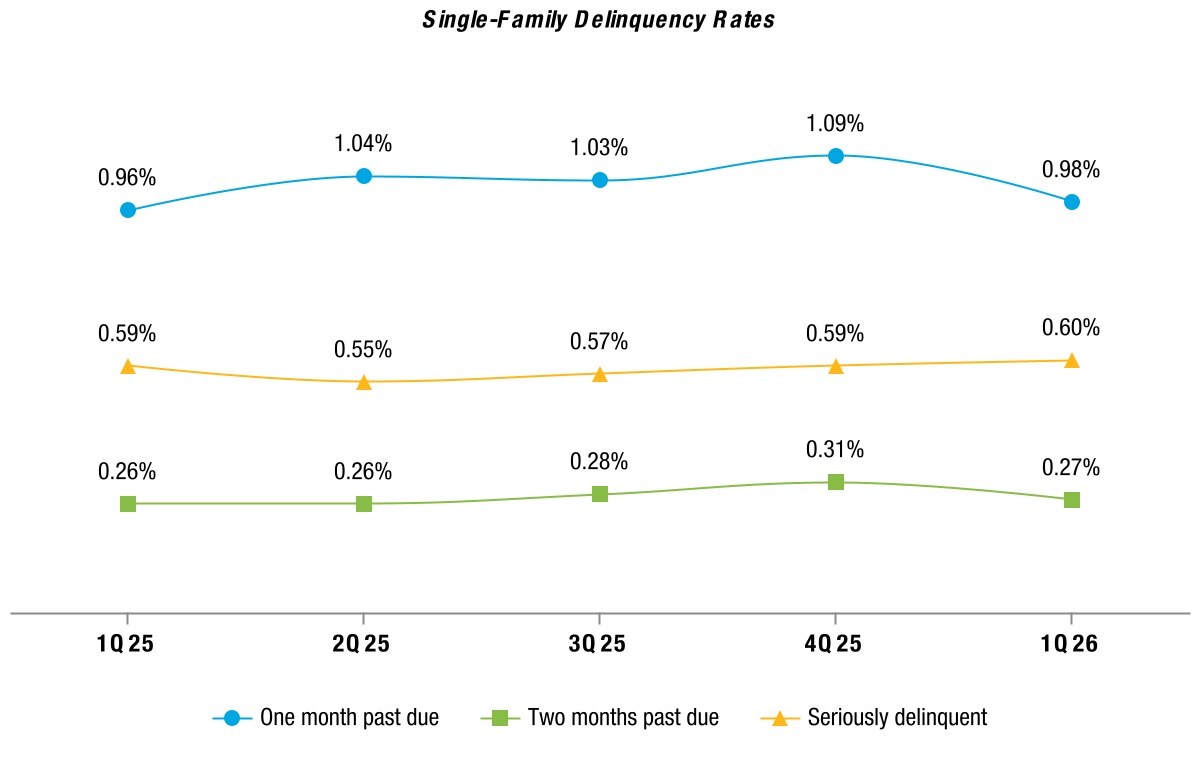

Delinquency Rates

We report Single-Family delinquency rates based on the number of loans in our Single-Family mortgage portfolio that are past due as reported to us by our servicers as a percentage of the total number of loans in our Single-Family mortgage portfolio.

The chart below presents the delinquency rates of mortgage loans in our Single-Family mortgage portfolio.

The percentage of loans that were one month past due and the percentage of loans that were two months past due both increased as of March 31, 2026 compared to March 31, 2025. The percentage of loans one month past due can be volatile due to seasonality, whether the last day of the period falls on a weekend, and other factors that may not be indicative of default. As a result, the percentage of loans two months past due tends to be a better early performance indicator than the percentage of loans one month past due.

Our Single-Family serious delinquency rate increased to 0.60% as of March 31, 2026, compared to 0.59% as of March 31, 2025. See Note 3 for additional information on the payment status of our single-family mortgage loans.

Loss Mitigation Activities

We offer a variety of borrower assistance programs.For purposes of the disclosure below related to loss mitigation activities, we generally exclude loans for which we do not control servicing. See Note 3 for additional information on our loss mitigation activities. For information on our refinance programs, see the MD&A - Risk Management -Credit Risk - Single-Family Mortgage Credit Risk section in our 2025 Annual Report.

Loan Workout Activities

We continue to help families retain their homes or otherwise avoid foreclosure through loan workouts. The table below provides details about the single-family loan workout activities that were completed during the periods presented.

(1) The forbearance data is limited to loans in forbearance that are past due based on the loans' original contractual terms and excludes loans included in certain legacy transactions, as the forbearance data for such loans is either not reported to us by the servicers or is otherwise not readily available to us. Other includes repayment plans and foreclosure alternatives.

Completed loan workout activity includes forbearance plans where borrowers fully reinstated the loan to current status during or at the end of the forbearance period, finalized payment deferral plans, settled loan modifications, successfully completed repayment plans, short sales, and deeds in lieu of foreclosure. Completed loan workout activity excludes active loss mitigation activity that was ongoing and had not been completed as of the end of the period, such as forbearance plans and repayment plans that had been initiated but not completed and trial period modifications. As of March 31, 2026, there were approximately 16,000 loans in active forbearance plans, approximately 16,000 loans on trial period modifications, and approximately 4,000 loans in active repayment plans.

Multifamily Mortgage Credit Risk

Credit Quality of New Business Activity

Our underwriting standards focus on the LTV ratio and DSCR, which estimates the value of the collateral and a borrower's ability to repay the loan using the secured property's cash flows, after expenses. The charts below provide the weighted average original LTV ratio and original DSCR for our new business activity.

Weighted Average Original LTV Ratio

Weighted Average Original DSCR(1)

(1) Assumes monthly payments that reflect amortization of principal.

Credit Enhancements

In connection with the acquisition, guarantee, and/or securitization of a loan or group of loans, we may obtain various forms of credit protection that reduce our credit risk exposure to the underlying mortgage borrower and our required capital. We evaluate and update our risk transfer strategy as needed depending on our business strategy, market conditions, and regulatory requirements.

Multifamily Mortgage Portfolio CRT Issuance

The table below provides the UPB of the multifamily mortgage loans covered by CRT transactions issued during the periods presented as well as the maximum coverage provided by those transactions upon issuance. In recent periods, we have primarily obtained credit enhancement coverage through MCIP and MSCR notes transactions due to our business strategy change. We typically retain higher levels of initial losses in these transactions compared to senior subordinate securitization transactions. As a result, the benefits provided by MCIP and MSCR notes may be lower than those provided by senior subordinate securitization transactions.

While subordination continues to be the primary form of credit enhancement coverage on our mortgage portfolio, our use of MCIP and MSCR notes transactions has grown in recent periods as a result of our business strategy change.

The table below presents the UPB and delinquency rates for both credit-enhanced and non-credit-enhanced loans underlying our Multifamily mortgage portfolio.

(1) As of March 31, 2026 and December 31, 2025, our maximum coverage outstanding provided by subordination in nonconsolidated VIEs was $31.9 billion and $33.2 billion, respectively.

The Multifamily delinquency rate was 0.43% at March 31, 2026. As of March 31, 2026, 94% of the delinquent loans in the Multifamily mortgage portfolio have credit enhancement coverage.

Credit Enhancement Recoveries

Our expected recovery receivable from freestanding credit enhancements was $0.1 billion as of both March 31, 2026 and December 31, 2025.

Seller Provided Indemnifications

Sellers are required to make certain representations and warranties regarding the loans they sell to us. In the event of a breach, sellers are obligated to either repurchase the affected loans or indemnify us for any losses incurred. Instead of demanding immediate repurchase, we may enter into forbearance and indemnification agreements with sellers. These agreements, among other provisions, delay the repurchase obligation for a specified period and fully transfer the risk of loss associated with the loan from us to the seller. Typically, as part of such agreements, we require sellers to provide cash or other collateral to secure potential future indemnification losses, although we remain subject to counterparty risk. While there has been an increase in the volume of seller repurchase and indemnification activities attributable to breaches of seller representation and warranties, these activities have remained limited. However, the volume of these activities may increase in the future.

Market Risk

Overview

Our business segments have embedded exposure to market risk, which is the economic risk associated with adverse changes in interest rates, volatility, and spreads. Market risk can adversely affect future cash flows, or economic value, as well as earnings and net worth. The primary sources of interest-rate risk are from our investments in mortgage-related assets, non-mortgage assets (including U.S. Treasury securities), the debt we issue to fund these assets, and our Single-Family guarantees.

Freddie Mac 1Q 2026 Form 10-Q

23

Management's Discussion and Analysis

Risk Management

Interest-Rate Risk

The tables below provide our duration gap, estimated point-in-time, and minimum and maximum PVS-L and PVS-YC results, and an average of the daily values and standard deviation. The table below also provides PVS-L estimated present value (gains) losses assuming an immediate 100 bps shift in the yield curve. The interest-rate sensitivity of a mortgage portfolio varies across a wide range of interest rates.

Table 28 - Duration Gap and PVS-YC and PVS-L Results Assuming Shifts of the Yield Curve

March 31, 2026

December 31, 2025

Duration Gap

PVS-YC(1)

PVS-L(1)

Duration Gap

PVS-YC(1)

PVS-L(1)

(Dollars in millions,duration gap in months)

25 bps

50 bps

100 bps

25 bps

50 bps

100 bps

Interest-rate risk related to:

Financial instruments primarily funded by debt

0.4

$2

$12

($29)

0.4

$5

$26

$18

All other financial instruments(2)

47.4

75

1,617

3,417

29.5

82

1,009

2,137

All financial instruments

11.6

77

1,629

3,388

7.3

76

1,035

2,154

PVS

77

1,629

3,388

76

1,035

2,154

(1)Positive amounts indicate the associated shift in the yield curve results in estimated present value losses. Negative amounts indicate the associated shift in the yield curve results in estimated present value gains.

(2)The UPB was $79.2 billion as of March 31, 2026 and $75.7 billion as of December 31, 2025.

Table 29 - Duration Gap and PVS Results

1Q 2026

1Q 2025

(Dollars in millions,duration gap in months)

Duration

Gap

PVS-YC

25 bps

PVS-L

50 bps

Duration Gap

PVS-YC 25 bps

PVS-L 50 bps

Average

9.3

$65

$1,324

0.8

$9

$86

Minimum

7.8

32

1,053

—

1

—

Maximum

12.0

88

1,666

2.0

24

228

Standard deviation

1.3

16

171

0.6

7

81

Derivatives enable us to reduce our economic interest-rate risk exposure as we continue to align our derivatives portfolio with the changing duration of our economically hedged assets and liabilities. The table below shows that the PVS-L risk levels, assuming a 50 bps shift in the yield curve for the periods presented, would have been higher if we had not used derivatives.

Table 30 - PVS-L Results Before Derivatives and After Derivatives

(In millions)

March 31, 2026

December 31, 2025

PVS-L (50 bps):

Before derivatives

$3,440

$3,364

After derivatives

1,629

1,035

Effect of derivatives

(1,811)

(2,329)

When managing interest-rate risk related to financial instruments not funded primarily by debt, we also consider the sensitivity of coupon income (interest income based on the stated or reinvestment rates) attributable to these instruments, which we believe is an appropriate measure as we are targeting duration to reduce our income volatility. We estimate the impact of a parallel 100 basis point increase and decrease in interest rates on coupon income attributable to these instruments over the next 12 months relative to the baseline scenario, assuming the total balance of these instruments stays constant. Unlike our economic risk measures (such as PVS and duration gap), which estimate changes to portfolio value, this analysis reflects only the coupon income sensitivity of our reported results to interest rate changes over a specific timeframe.

At March 31, 2026 and 2025, we estimate that a parallel 100 basis point increase in interest rates would result in an increase of $263 million and $489 million, respectively, and a parallel 100 basis point decrease would result in a decrease of $343 million and $492 million, respectively, in coupon income for financial instruments not primarily funded by debt, relative to the baseline.

Freddie Mac 1Q 2026 Form 10-Q

24

Management's Discussion and Analysis

Liquidity and Capital Resources

LIQUIDITY AND CAPITAL RESOURCES

Our business activities require that we maintain adequate liquidity to meet our financial obligations as they come due and meet the needs of customers in a timely and cost-efficient manner. We also must maintain adequate capital resources to avoid being placed into receivership by FHFA.

Liquidity

Primary Sources of Liquidity

Our primary sources of liquidity include both our other investments portfolio and our mortgage-related investments portfolio. See MD&A - Our Portfolios for additional information about our other investments portfolio and mortgage-related investments portfolio.

Our other investments portfolio is important to our cash flow, collateral management, asset and liability management, and ability to provide liquidity and stability to the mortgage market. Our liquidity and contingency operating portfolio primarily includes securities purchased under agreements to resell and non-mortgage-related securities. Our non-mortgage-related securities consist of U.S. Treasury securities and other investments that we could sell to provide us with an additional source of liquidity to fund our business operations. We also maintain non-interest-bearing deposits at the Federal Reserve Bank of New York and interest-bearing deposits at commercial banks. Our interest-bearing deposits at commercial banks totaled $4.0 billion as of March 31, 2026 and $4.8 billion as of December 31, 2025.

The primary source of liquidity from our mortgage-related investments portfolio is our holdings of agency securities. In addition, we hold certain single-family loans and multifamily loans that could be securitized and would then be available for sale or for use as collateral for repurchase agreements.

Primary Sources of Funding

We fund our business using short-term and long-term debt, securities sold under agreements to repurchase, and debt issued by consolidated trusts. Competition for funding can vary with economic, financial market, and regulatory environments. The amount, type, and term of our funding sources is based on a variety of factors and is designed to meet our ongoing cash needs and to comply with our Liquidity Management Framework.

Short-term and Long-term Debt

We issue debt to fund our operations. These instruments are unsecured general corporate obligations and consist of both short-term debt, which are instruments with original maturities of one year or less, and long-term debt, which are instruments with original maturities of more than one year.

As of March 31, 2026, our aggregate indebtedness pursuant to the Purchase Agreement was $198.0 billion, which was below the current $270.0 billion debt cap limit. Our aggregate indebtedness calculation primarily includes the par value of short- and long-term debt.

The table below summarizes the par value and the average rate of short-term and long-term debt securities we issued or paid off, including regularly scheduled principal payments, payments resulting from calls, and payments for repurchases. We call, exchange, or repurchase our outstanding debt securities from time to time for a variety of reasons, including managing our funding composition and supporting the liquidity of our debt securities.

Freddie Mac 1Q 2026 Form 10-Q

25

Management's Discussion and Analysis

Liquidity and Capital Resources

Table 31 - Short-term and Long-term Debt Activity

1Q 2026

1Q 2025

(Dollars in millions)

Par Value

Average Rate(1)

Par Value

Average Rate(1)

Short-term Debt:

Beginning balance

$37,867

3.82

%

$14,716

4.59

%

Issuances

31,365

3.64

38,793

4.31

Repayments

(1,480)

3.86

—

—

Maturities

(43,194)

3.78

(39,052)

4.42

Total short-term debt

24,558

3.66

14,457

4.29

Long-term Debt:

Beginning balance

172,693

4.15

172,942

3.65

Issuances

34,244

3.99

22,195

4.88

Repayments

(22,750)

4.41

(18,106)

5.10

Maturities

(10,721)

5.07

(6,824)

2.16

Total long-term debt

173,466

4.03

170,207

3.72

Total short-term and long-term debt, net

$198,024

3.98

%

$184,664

3.76

%

(1)Average rate is weighted based on par value.

Our callable debt provides us with the option to repay the outstanding principal balance of the debt prior to its contractual maturity date. As of March 31, 2026, $80.5 billion of the outstanding $98.7 billion of callable debt may be called within one year, not including callable debt due to contractually mature within one year.

Maturity and Redemption Dates

The table below presents the par value of total short-term and long-term debt by contractual maturity date and earliest redemption date. The earliest redemption date refers to the earliest call date for callable debt, and the contractual maturity date for all other short-term and long-term debt.

Table 32 - Maturity and Redemption Dates

As of March 31, 2026

As of December 31, 2025

(In millions)

Contractual Maturity Date

Earliest Redemption Date

Contractual Maturity Date

Earliest Redemption Date

Short-term debt

$24,558

$24,558

$37,867

$37,867

Long-term debt:

1 year or less

44,246

124,760

45,515

120,398

1 year through 2 years

40,497

31,258

43,860

34,849

2 years through 3 years

24,880

5,660

22,474

5,615

3 years through 4 years

9,814

2,070

9,806

2,055

4 years through 5 years

40,002

2,978

33,871

—

Thereafter

13,539

6,252

16,622

9,231

STACR and SCR debt(1)

488

488

546

546

Total short-term and long-term debt

$198,024

$198,024

$210,561

$210,561

(1)STACR debt notes and SCR debt notes are subject to prepayment risk as their payments are based upon the performance of a reference pool of mortgage assets that may be prepaid by the related mortgage borrowers at any time generally without penalty and are, therefore, included as a separate category in the table.

Debt Issued by Consolidated Trusts

Debt issued by consolidated trusts relates to securitization transactions that we consolidate for accounting purposes. We primarily issue this type of debt by securitizing mortgage loans to finance our guarantee activities. When we consolidate securitization trusts, we recognize on our condensed consolidated balance sheets the assets held by the trusts, the majority of which are mortgage loans, and the debt issued by the trusts.

Freddie Mac 1Q 2026 Form 10-Q

26

Management's Discussion and Analysis

Liquidity and Capital Resources

The table below shows the issuance and extinguishment activity for the debt issued by consolidated trusts.

Table 33 - Debt Issued by Consolidated Trusts

(In millions)

1Q 2026

1Q 2025

Beginning balance

$3,163,684

$3,085,981

Issuances

165,358

120,942

Repayments and extinguishments

(147,061)

(97,496)

Ending balance

3,181,981

3,109,427

Unamortized premiums and discounts

33,014

35,821

Debt issued by consolidated trusts

$3,214,995

$3,145,248

Off-Balance Sheet Arrangements

We enter into certain business arrangements that are not recorded on our condensed consolidated balance sheets or that may be recorded in amounts that differ from the full contractual or notional amount of the transaction that affect our short- and long-term liquidity needs. These off-balance sheet arrangements primarily consist of guarantees and commitments. Certain of these arrangements present credit risk exposure. SeeNote 2 and Note 4 for additional information on these transactions. SeeMD&A - Risk Management - Credit Riskfor additional information on our credit risk exposure on off-balance sheet arrangements.

Cash Flows

Cash and cash equivalents (including restricted cash and cash equivalents) decreased slightly from $4.8 billion as of March 31, 2025 to $4.5 billion as of March 31, 2026.

Capital Resources

The table below presents activity related to our net worth.

Table 34 - Net Worth Activity

(In millions)

1Q 2026

1Q 2025

Beginning balance

$70,384

$59,575

Comprehensive income

3,538

2,828

Capital draw from Treasury

—

—

Senior preferred stock dividends declared

—

—

Total equity / net worth

$73,922

$62,403

Remaining Treasury funding commitment

$140,162

$140,162

Aggregate draws under Purchase Agreement

71,648

71,648

Aggregate cash dividends paid to Treasury

119,680

119,680

Liquidation preference of the senior preferred stock

143,032

132,223

Freddie Mac 1Q 2026 Form 10-Q

27

Management's Discussion and Analysis

Liquidity and Capital Resources

ERCF

For a description of our capital requirements under the ERCF, including the amended provisions, see the MD&A - Regulation and Supervision section in our 2025 Annual Report.

Capital Metrics

The table below presents the components of our regulatory capital.

Table 35 - Regulatory Capital Components

(In millions)

March 31, 2026

December 31, 2025

Total equity

$73,922

$70,384

Less:

Senior preferred stock

72,648

72,648

Preferred stock

14,109

14,109

Common equity

(12,835)

(16,373)

Less: Deferred tax assets arising from temporary differences that exceed 10% of CET1 capital and other regulatory adjustments

4,886

5,169

Common equity Tier 1 capital

(17,721)

(21,542)

Add: Preferred stock

14,109

14,109

Tier 1 capital

(3,612)

(7,433)

Tier 2 capital adjustments

—

—

Adjusted total capital

($3,612)

($7,433)

The table below presents the components of our statutory capital.

Table 36 - Statutory Capital Components

(In millions)

March 31, 2026

December 31, 2025

Total equity

$73,922

$70,384

Less:

Senior preferred stock

72,648

72,648

AOCI, net of taxes

31

51

Core capital

1,243

(2,315)

General allowance for foreclosure losses(1)

8,113

8,505

Total capital

$9,356

$6,190

(1)Represents our allowance for credit losses.

Freddie Mac 1Q 2026 Form 10-Q

28

Management's Discussion and Analysis

Liquidity and Capital Resources

The table below presents our capital metrics under the ERCF.

Table 37 - Capital Metrics Under ERCF

(In billions)

March 31, 2026

December 31, 2025

Adjusted total assets

$3,903

$3,905

Risk-weighted assets (standardized approach):

Credit risk

1,112

1,091

Market risk

74

67

Operational risk

73

73

Total risk-weighted assets

$1,259

$1,231

(In billions)

March 31, 2026

December 31, 2025

Stress capital buffer

$29

$29

Stability capital buffer

31

30

Countercyclical capital buffer amount

—

—

PCCBA

$60

$59

PLBA

$15

$15

March 31, 2026

(Dollars in billions)

Minimum Capital Requirement

Applicable Buffer

Capital

Requirement

(Including Buffer(1))

Available Capital (Deficit)

Capital Shortfall

Risk-based capital amounts:

Total capital

$101

N/A

$101

$9

($92)

CET1 capital

57

$60

117

(18)

(135)

Tier 1 capital

76

60

136

(4)

(140)

Adjusted total capital

101

60

161

(4)

(165)

Risk-based capital ratios(2):

Total capital

8.0

%

N/A

8.0

%

0.7

%

(7.3)

%

CET1 capital

4.5

4.8

%

9.3

(1.4)

(10.7)

Tier 1 capital

6.0

4.8

10.8

(0.3)

(11.1)

Adjusted total capital

8.0

4.8

12.8

(0.3)

(13.1)

Leverage capital amounts:

Core capital

$98

N/A

$98

$1

($97)

Tier 1 capital

98

$15

113

(4)

(117)

Leverage capital ratios(3):

Core capital

2.5

%

N/A

2.5

%

—

%

(2.5)

%

Tier 1 capital

2.5

0.4

%

2.9

(0.1)

(3.0)

Freddie Mac 1Q 2026 Form 10-Q

29

Management's Discussion and Analysis

Liquidity and Capital Resources

December 31, 2025

(Dollars in billions)

Minimum Capital Requirement

Applicable Buffer

Capital

Requirement

(Including Buffer(1))

Available Capital (Deficit)

Capital Shortfall

Risk-based capital amounts:

Total capital

$99

N/A

$99

$6

($93)

CET1 capital

55

$59

114

(22)

(136)

Tier 1 capital

74

59

133

(7)

(140)

Adjusted total capital

99

59

158

(7)

(165)

Risk-based capital ratios(2):

Total capital

8.0

%

N/A

8.0

%

0.5

%

(7.5)

%

CET1 capital

4.5

4.8

%

9.3

(1.8)

(11.1)

Tier 1 capital

6.0

4.8

10.8

(0.6)

(11.4)

Adjusted total capital

8.0

4.8

12.8

(0.6)

(13.4)

Leverage capital amounts:

Core capital

$98

N/A

$98

($2)

($100)

Tier 1 capital

98

$15

113

(7)

(120)

Leverage capital ratios(3):

Core capital

2.5

%

N/A

2.5

%

(0.1)

%

(2.6)

%

Tier 1 capital

2.5

0.4

%

2.9

(0.2)

(3.1)

(1)PCCBA for risk-based capital and PLBA for leverage capital.

(2)As a percentage of RWA.

(3)As a percentage of ATA.

At March 31, 2026, our maximum payout ratio under the ERCF was 0.0%.

See Note 15 for additional information on our capital amounts and ratios under the ERCF.

Freddie Mac 1Q 2026 Form 10-Q

30

Management's Discussion and Analysis

Critical Accounting Estimates

CRITICAL ACCOUNTING ESTIMATES

Our critical accounting estimates and policies relate to the Single-Family allowance for credit losses. For additional information about our critical accounting estimates and significant accounting policies, see Note 1 and MD&A - Critical Accounting Estimates in our 2025 Annual Report.

Single-Family Allowance for Credit Losses

The Single-Family allowance for credit losses represents our estimate of expected credit losses over the contractual term of the mortgage loans. The Single-Family allowance for credit losses pertains to all single-family loans classified as held-for-investment on our condensed consolidated balance sheets.

Determining the appropriateness of the Single-Family allowance for credit losses is a complex process that is subject to numerous estimates and assumptions requiring significant management judgment about matters that involve a high degree of subjectivity. This process involves the use of models that require us to make judgments about matters that are difficult to predict.

Changes in forecasted house price growth rates can have a significant effect on our allowance for credit losses estimates. The table below shows our nationwide forecasted house price growth rates that were used in determining our allowance for credit losses. See Note 5 for additional information regarding our current period provision for credit losses.

Table 38 - Forecasted House Price Growth Rates

March 31, 2026

December 31, 2025

12-Month Forward

2.3

%

0.5

%

13- to 24-Month Forward

2.4

1.4

Freddie Mac 1Q 2026 Form 10-Q

31

Management's Discussion and Analysis

Regulation and Supervision

REGULATION AND SUPERVISION