ALEXANDRIA EXECUTES LARGEST LIFE SCIENCE LEASE IN COMPANY

HISTORY WITH A LONG-STANDING MULTINATIONAL PHARMACEUTICAL

TENANT FOR A 466,598 RSF BUILD-TO-SUIT RESEARCH HUB AT

THE CAMPUS POINT MEGACAMPUS™ IN SAN DIEGO

Our long-term lease with a high-credit tenant underscores the strength and uniqueness of the Alexandria brand, as underpinned by: | ||

• | Enduring tenant relationships and commitment to innovation | |

• | Expertise in design, development, and operations | |

• | Our Megacampus platform supporting tenant growth and talent recruitment and retention | |

| |

Table of Contents | |

September 30, 2025 | |

COMPANY HIGHLIGHTS | Page | Page | |||

Mission and Cluster Model ..................................................................... | |||||

EARNINGS PRESS RELEASE | |||||

Third Quarter Ended September 30, 2025 Financial and Operating Results ................................................................................ | Earnings Call Information and About the Company ....................... | ||||

2025 Guidance ......................................................................................... | Consolidated Statements of Operations .......................................... | ||||

2026 Considerations ............................................................................... | Consolidated Balance Sheets ............................................................ | ||||

Dispositions and Exchange of Partial Interests ................................... | |||||

SUPPLEMENTAL INFORMATION | |||||

Company Profile ....................................................................................... | External Growth / Investments in Real Estate | ||||

Investor Information ................................................................................. | Investments in Real Estate ................................................................ | ||||

Financial and Asset Base Highlights ..................................................... | New Class A/A+ Development and Redevelopment Properties: | ||||

High-Quality and Diverse Client Base ................................................. | Recent Deliveries ........................................................................... | ||||

Internal Operating Metrics | Current Projects .............................................................................. | ||||

Key Operating Metrics ............................................................................. | Summary of Pipeline ...................................................................... | ||||

Same Property Performance .................................................................. | Construction Spending ........................................................................ | ||||

Leasing Activity ......................................................................................... | Capitalization of Interest ..................................................................... | ||||

Contractual Lease Expirations ............................................................... | Joint Venture Financial Information ................................................... | ||||

Top 20 Tenants ......................................................................................... | Balance Sheet Management | ||||

Summary of Properties and Occupancy .............................................. | Investments .......................................................................................... | ||||

Property Listing ........................................................................................ | Balance Sheet ...................................................................................... | ||||

Key Credit Metrics ............................................................................... | |||||

Summary of Debt ................................................................................. | |||||

Definitions and Reconciliations | |||||

Definitions and Reconciliations .......................................................... | |||||

CONFERENCE CALL INFORMATION: | ||

Tuesday, October 28, 2025 2:00 p.m. Eastern Time 11:00 a.m. Pacific Time | ||

(833) 366-1125 or (412) 902-6738 | ||

Ask to join the conference call for Alexandria Real Estate Equities, Inc. | ||

CONTACT INFORMATION: | ||

Alexandria Real Estate Equities, Inc. corporateinformation@are.com | ||

JOEL S. MARCUS Executive Chairman & Founder | ||

PETER M. MOGLIA Chief Executive Officer & Chief Investment Officer | ||

MARC E. BINDA Chief Financial Officer & Treasurer | ||

PAULA SCHWARTZ Managing Director, Rx Communications Group (917) 633-7790 | ||

ALEXANDRIA: THE MOST

TRUSTED BRAND IN LIFE

SCIENCE REAL ESTATE™

WE INVENTED IT.

WE DOMINATE IT.

ALEXANDRIA’S MEGACAMPUS™ PLATFORM REPRESENTS |

77% OF OUR ANNUAL RENTAL REVENUE |

LARGEST, HIGHEST-QUALITY ASSET BASE CLUSTERED IN THE KEY CENTERS OF LIFE SCIENCE INNOVATION |

SECTOR-LEADING CLIENT BASE OF ~700 TENANTS |

HIGH-QUALITY CASH FLOWS |

PROVEN UNDERWRITING |

FORTRESS BALANCE SHEET |

LONG-TENURED, HIGHLY EXPERIENCED MANAGEMENT TEAM |

As of September 30, 2025. Refer to “Definitions and reconciliations” in the Supplemental Information for additional details.

ALEXANDRIA’S MEGACAMPUS™ PLATFORM DRIVES SUPERIOR OPERATING

RESULTS BY CLUSTERING HIGH-QUALITY COLLABORATIVE LIFE SCIENCE AND

ADVANCED TECHNOLOGIES FACILITIES IN TOP INNOVATION MARKETS

ALEXANDRIA’S MEGACAMPUS OCCUPANCY OUTPERFORMS THE MARKET(1) | ||

ALEXANDRIA’S MEGACAMPUS PLATFORM | ||||

77% of Annual Rental Revenue | ||||

91% Megacampus | 73% Market | ||||

18% Occupancy Outperformance |

As of September 30, 2025. Refer to “Definitions and reconciliations” in the Supplemental Information for additional details.

(1)Represents the occupancy of operating properties at Alexandria’s Megacampus ecosystems within the Greater Boston, San Francisco Bay Area, and San Diego markets as of September 30, 2025, compared to the average market

occupancy for these markets per the Q2 2025 U.S. Life Sciences Report published by CBRE Research.

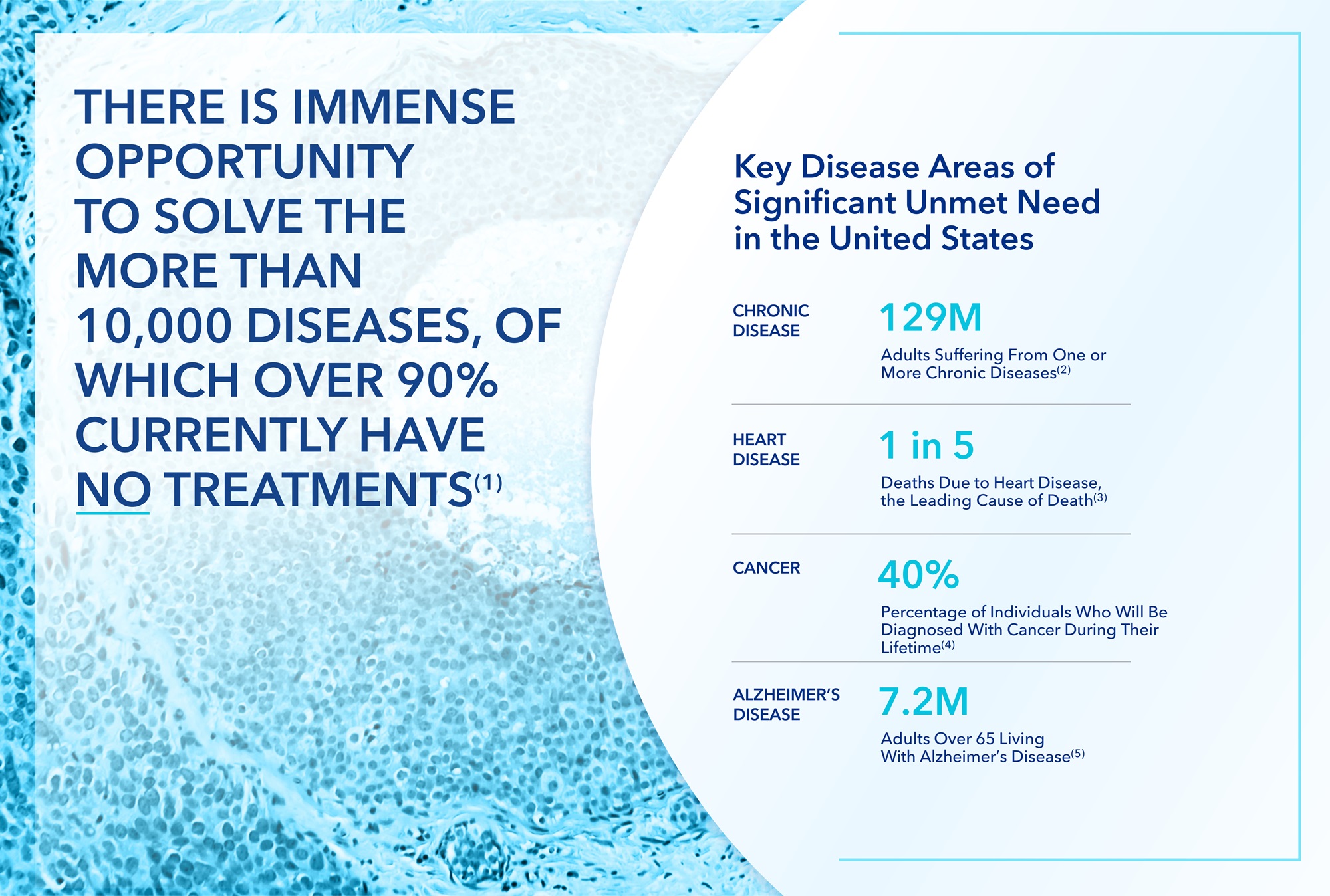

(1)Source: U.S. House Committee on Energy and Commerce, “The 21st Century Cures Discussion Document White Paper,” January 27, 2015.

(1)Source: U.S. House Committee on Energy and Commerce, “The 21st Century Cures Discussion Document White Paper,” January 27, 2015.

(2)Source: PhRMA, “Medicines in Development for Chronic Diseases: 2024 Report.”

(3)Source: Centers for Disease Control and Prevention, “Heart Disease Facts,” October 24, 2024. Represents the latest published data, which reflects the U.S. estimate for 2022.

(4)Source: National Cancer Institute, “Cancer Statistics,” updated May 7, 2025. Represents the latest published data, which reflects 2018–2021 data, not including 2020 due to COVID.

(5)Source: Alzheimer’s Association, “2025 Alzheimer’s Disease Facts and Figures.” Represents the latest published data, which reflects the U.S. estimate for 2025.

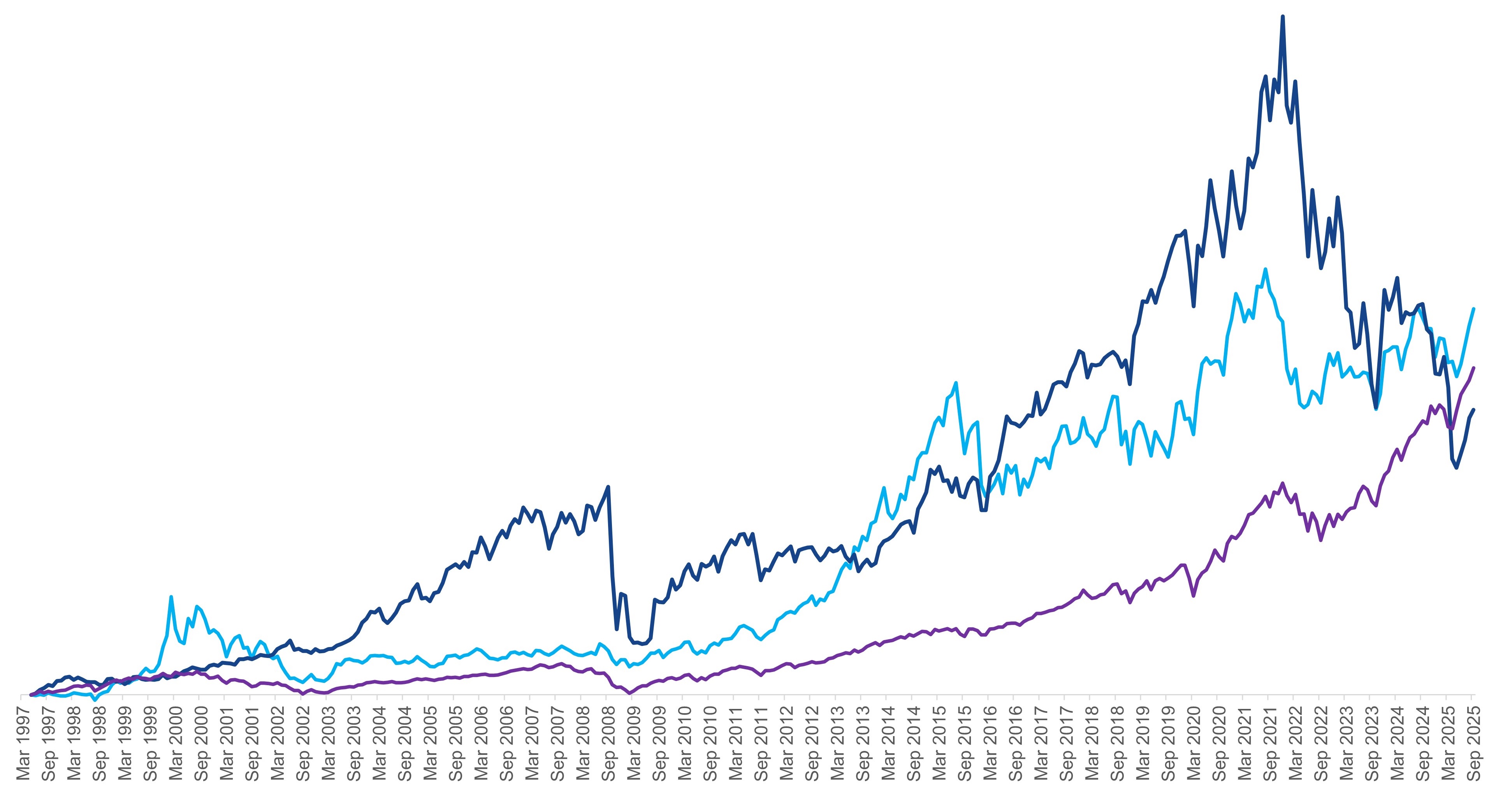

NASDAQ BIOTECHNOLOGY INDEX (NBI) TSR CONTINUES TO BROADLY TRACK THE

DIRECTIONAL PATH OF THE S&P 500 INDEX TSR

NBI TSR

1,441%

S&P 500

Index TSR

1,221%

ARE TSR

1,064%

Total Shareholder Return

From ARE’s IPO on May 27, 1997 to September 30, 2025

Source: S&P Global Market Intelligence.

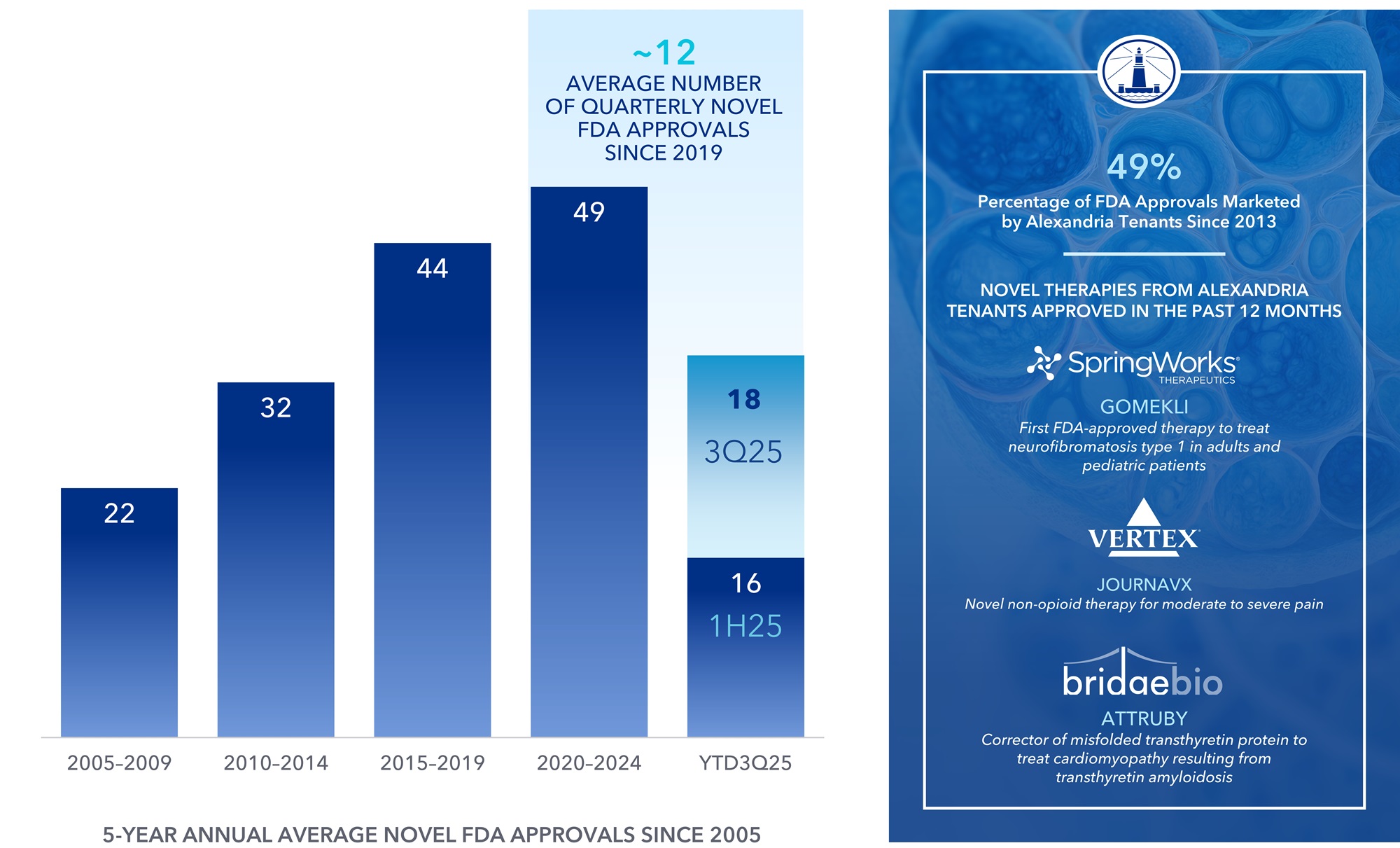

AFTER A SLOW START TO THE YEAR, NOVEL FDA APPROVALS HAVE

RESUMED A HEALTHY PACE THROUGH THE THIRD QUARTER

(1)

Source: U.S. Food and Drug Administration. Novel therapies approved by the FDA (Center for Drug Evaluation and Research) include new molecular entities and new biologics defined as products containing active moieties that have

not previously been approved by the FDA.

(1)Includes two additional approvals through October 24, 2025.

ALEXANDRIA’S LIFE SCIENCE INDUSTRY AND

CORPORATE RESPONSIBILITY LEADERSHIP

2025 RECYCLED ASSETS SOLD OR TO BE SOLD TO FUND OUR CAPITAL NEEDS AND

ENABLE ACHIEVEMENT OF 80% ANNUAL RENTAL REVENUE FROM

MEGACAMPUSES

$87M REDUCTION IN ANNUAL NET OPERATING INCOME(1) FROM 2025 DISPOSITIONS(2) |

32 TOTAL TRANSACTIONS(2) |

$1.5B TOTAL SALES(2) |

Stabilized

Properties

Land

20% to

30%

20% to

30%

40% to 60%

Non-stabilized Properties

2025 DISPOSITIONS BY REAL ESTATE CLASSIFICATION(2)

(1)Represents annual net operating income for the quarter preceding the date on which the property is sold, or near-term prospective net operating income.

(2)Represents completed and pending YTD 2025 dispositions.. Refer to “Dispositions and Exchange of Partial Interests” in the Earnings Release for additional details.

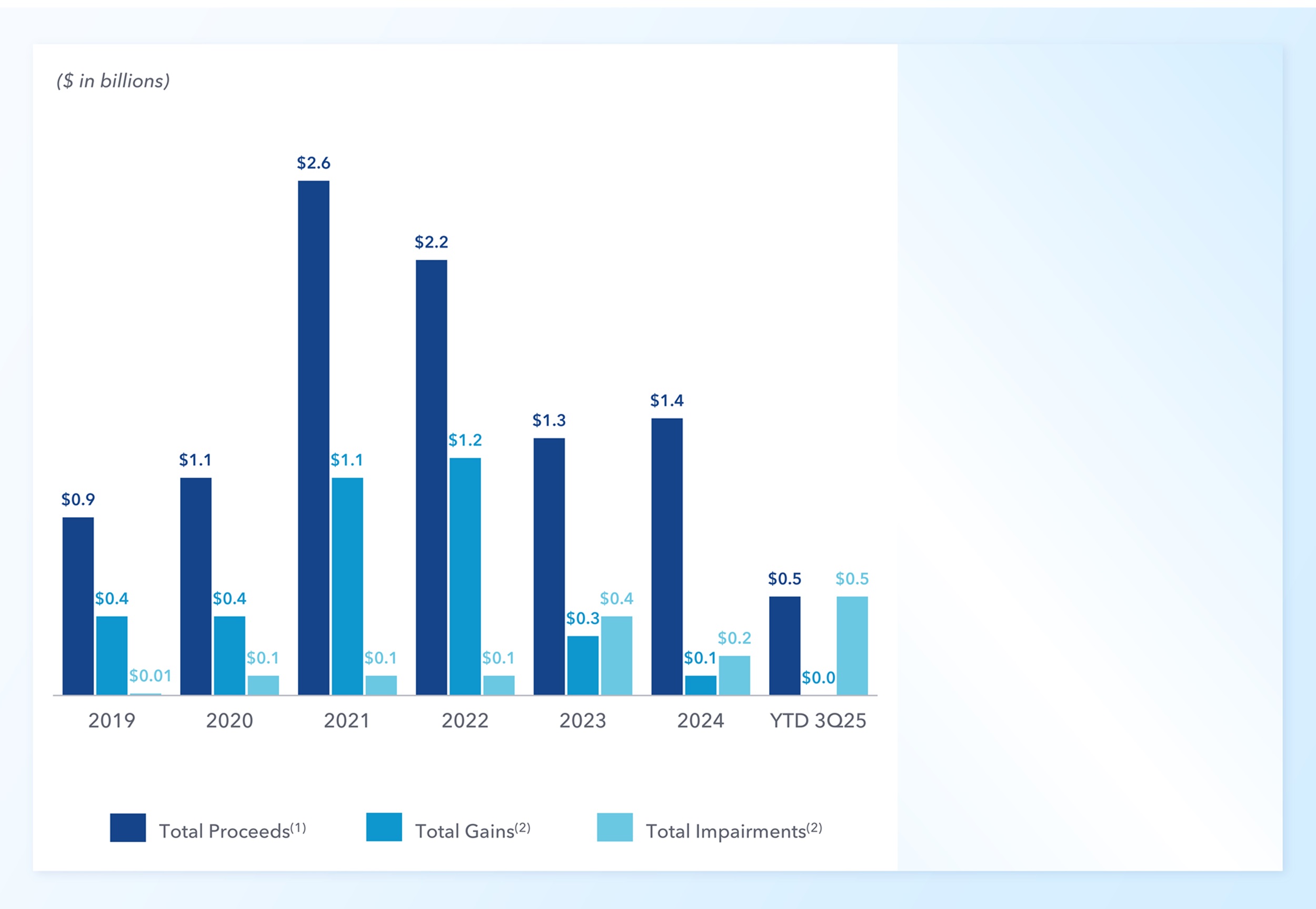

ALEXANDRIA’S LONG-STANDING TRACK RECORD OF MONETIZING EMBEDDED

ASSET VALUE: 2019–YTD 3Q25 DISPOSITIONS AND PARTIAL INTEREST SALES

2019–YTD 3Q25 AGGREGATE $10B Total Proceeds(1) |

$3.6B Total Gains on Sales of Real Estate(2) |

$1.4B Total Impairments of Real Estate(2) |

2019–YTD 3Q25 DISPOSITIONS AND PARTIAL INTEREST SALES

(1)Represents aggregate proceeds from outright sales and sales of partial interests.

(2)Total gains and impairments include any amounts related to sales of partial interests recognized in additional paid-in capital.

ALEXANDRIA’S DISCIPLINED COST-CONTROL AND EFFICIENCY INITIATIVES HAVE

DRIVEN SUBSTANTIAL REDUCTIONS IN GENERAL AND ADMINISTRATIVE EXPENSES

Alexandria’s 2025 overhead is approximately half that of other S&P 500 REITs

ALEXANDRIA

S&P 500 REITS

(excluding Alexandria)

VS

(1)

(1)

GENERAL AND ADMINISTRATIVE EXPENSES AS A PERCENTAGE OF NET OPERATING INCOME(2)

Source for S&P 500 REIT data: S&P Global Market Intelligence.

(1)Trailing twelve months ended September 30, 2025 and June 30, 2025, respectively. Refer to “2026 Considerations” in the Earnings Release for additional details.

(2)Refer to “Net operating income” under “Definitions and reconciliations” in the Supplemental Information for additional details.

Alexandria Real Estate Equities, Inc. Reports:

3Q25 and YTD 3Q25 Net Loss per Share – Diluted of $(1.38) and $(2.09), respectively; and

3Q25 and YTD 3Q25 FFO per Share – Diluted, as Adjusted, of $2.22 and $6.85, respectively

PASADENA, Calif. – October 27, 2025 – Alexandria Real Estate Equities, Inc. (NYSE: ARE)

announced financial and operating results for the third quarter ended September 30, 2025.

Key highlights | ||||||||

YTD | ||||||||

Operating results | 3Q25 | 3Q24 | 3Q25 | 3Q24 | ||||

Net (loss) income attributable to Alexandria’s common stockholders – diluted: | ||||||||

In millions | $(234.9) | $164.7 | $(356.1) | $374.5 | ||||

Per share | $(1.38) | $0.96 | $(2.09) | $2.18 | ||||

Funds from operations attributable to Alexandria’s common stockholders – diluted, as adjusted: | ||||||||

In millions | $377.8 | $407.9 | $1,166.3 | $1,217.3 | ||||

Per share | $2.22 | $2.37 | $6.85 | $7.08 | ||||

A sector-leading REIT with a high-quality, diverse tenant base, strong margins, and long lease

terms

(As of September 30, 2025, unless stated otherwise) | |||

Occupancy of operating properties in North America | 90.6% | ||

Percentage of annual rental revenue in effect from Megacampus™ platform | 77% | ||

Percentage of annual rental revenue in effect from investment-grade or publicly traded large cap tenants | 53% | ||

Operating margin | 68% | ||

Adjusted EBITDA margin | 71% | ||

Percentage of leases containing annual rent escalations | 97% | ||

Weighted-average remaining lease term: | |||

Top 20 tenants | 9.4 | years | |

All tenants | 7.5 | years | |

Strong 3Q25 tenant collections: | |||

3Q25 tenant rents and receivables collected as of October 27, 2025 | 99.9% |

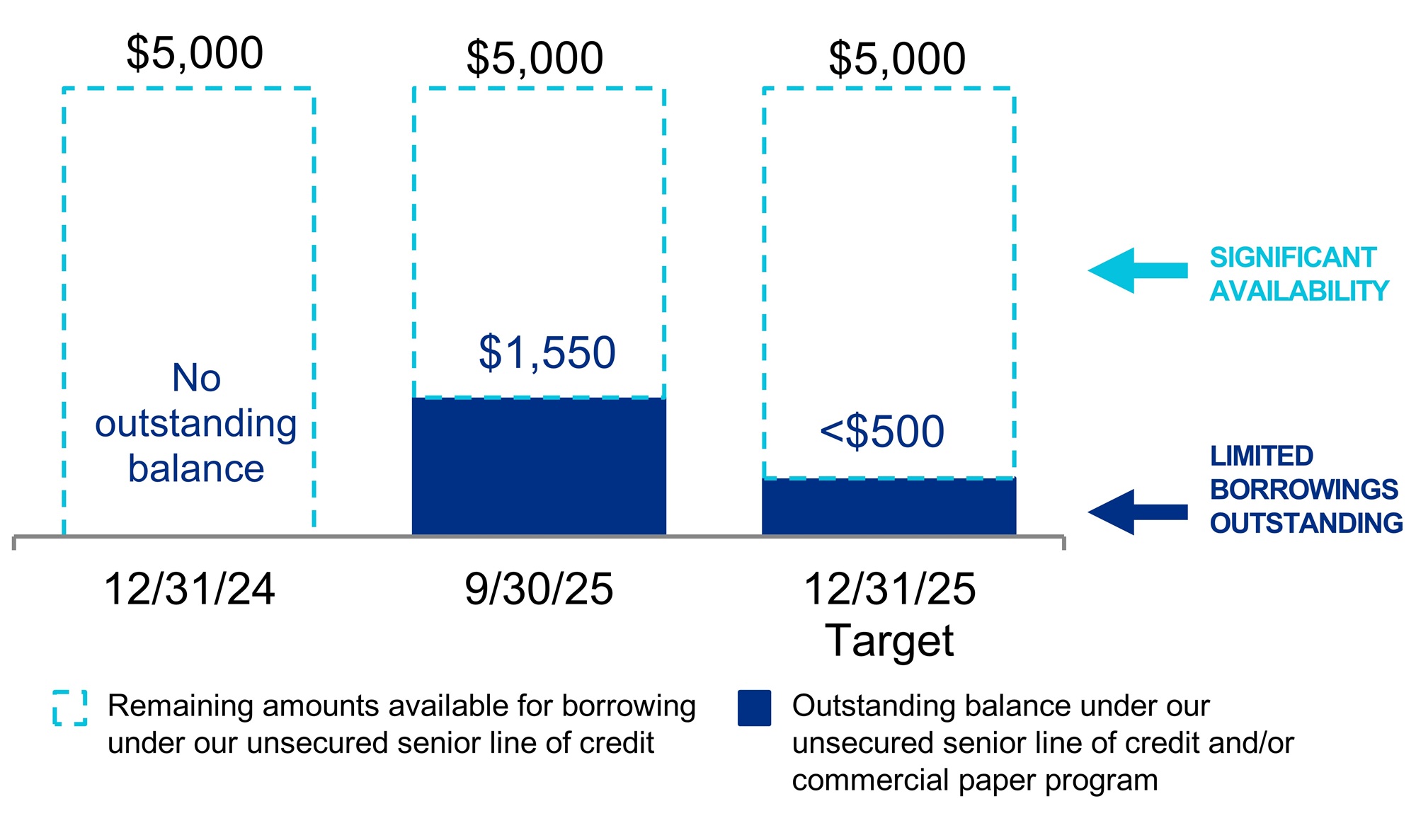

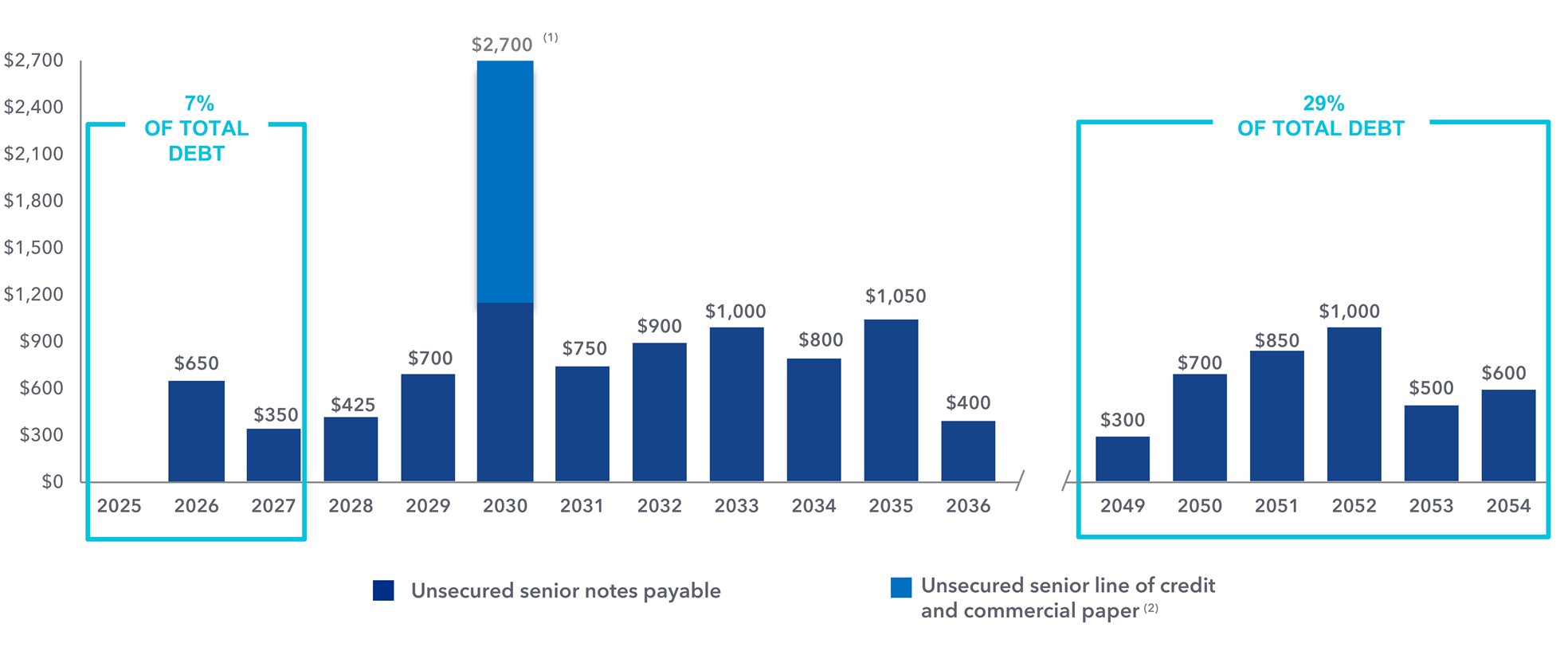

Strong and flexible balance sheet with significant liquidity; top 15% credit rating ranking among all

publicly traded U.S. REITs

•$27.8 billion in total market capitalization.

•$14.2 billion in total equity capitalization.

•Net debt and preferred stock to Adjusted EBITDA of 6.1x and fixed-charge coverage ratio of

3.9x for 3Q25 annualized, with 4Q25 annualized targets of 5.5x to 6.0x and 3.6x to 4.1x,

respectively.

•Significant liquidity of $4.2 billion, or 4.2x our debt maturities through 2027.

•Only 7% of our total debt matures through 2027.

•11.6 years weighted-average remaining term of debt, longest among S&P 500 REITs.

•Since 2021, our quarter-end fixed-rate debt has averaged 96.7%.

•Total debt and preferred stock to gross assets of 31%.

•$166.9 million of capital contribution commitments from existing real estate joint venture

partners to fund construction from 4Q25 through 2027 and beyond.

Solid leasing volume and rental rate increases

•Leasing volume of 1.2 million RSF during 3Q25.

•Includes the largest life science lease in company history with a long-standing multinational

pharmaceutical tenant for a 16-year build-to-suit lease expansion aggregating

466,598 RSF, located on the Campus Point by Alexandria Megacampus in our University

Town Center submarket.

•Leasing of previously vacant space aggregating 256,633 RSF, up 40%, over the quarterly

average over the last five quarters.

•Rental rate increases on lease renewals and re-leasing of space of 15.2% and 6.1% (cash

basis) for 3Q25 and 13.6% and 6.8% (cash basis) for YTD 3Q25.

•82% of our leasing activity during the last twelve months was generated from our existing

tenant base.

3Q25 | YTD 3Q25 | ||||

Lease renewals and re-leasing of space: | |||||

Rental rate increase | 15.2% | 13.6% | |||

Rental rate increase (cash basis) | 6.1% | 6.8% | |||

RSF | 354,367 | 1,722,184 | |||

Leasing of previously vacant space – RSF | 256,633 | 550,986 | |||

Leasing of development and redevelopment space – RSF | 560,344 | 698,542 | |||

Total leasing activity – RSF | 1,171,344 | 2,971,712 |

Dividend strategy to share net cash flows from operating activities with stockholders while

retaining a significant portion for reinvestment

•Common stock dividend declared of $1.32 per share for 3Q25, aggregating $5.28 per

common share for the twelve months ended September 30, 2025, up 14 cents, or 2.7%, over

the twelve months ended September 30, 2024.

•Dividend yield of 6.3% as of September 30, 2025 and dividend payout ratio of 60% for the

three months ended September 30, 2025.

•Significant net cash flows provided by operating activities after dividends retained for

reinvestment aggregating $2.3 billion for the years ended December 31, 2021 through 2024

and the midpoint of our 2025 guidance range.

•In addition, as described in the “2026 Considerations” section of guidance, in light of market

and life science industry conditions and our continued focus on capital efficiency, our Board of

Directors expects to carefully evaluate our 2026 dividend strategy.

Ongoing execution of Alexandria’s 2025 capital recycling strategy

We expect to fund a significant portion of our capital requirements for the year ending

December 31, 2025 through dispositions of non-core assets, land, partial interest sales, and

sales to owner/users. We expect dispositions of land to represent 20%–30% of our total

dispositions and sales of partial interests for 2025.

(dollars in millions) | Sales Price | ||

Total dispositions completed as of October 27, 2025 | $508 | ||

Our share of pending transactions subject to non-refundable deposits, signed letters of intent, and/or purchase and sale agreement negotiations | 1,032 | ||

Our share of completed and pending 2025 dispositions and sales of partial interests | $1,540 | (1) |

(1)Excludes an exchange of partial interests of Pacific Technology Park and 199 East Blaine Street with nominal

net cash proceeds. Refer to “Dispositions and exchange of partial interests” in the Earnings Press Release for

additional details.

| |

Third Quarter Ended September 30, 2025 Financial and Operating Results (continued) | |

September 30, 2025 | |

Leasing progress on temporary vacancy

Operating occupancy as of June 30, 2025 | 90.8% | ||

Assets with vacancy designated as held for sale during 3Q25 now excluded from operating occupancy and expected to be sold primarily in 4Q25 | 0.9 | ||

Reduction in occupancy, primarily from 3Q25 lease expirations | (1.1) | (1) | |

Operating occupancy as of September 30, 2025 | 90.6 | ||

Key vacant space leased with future delivery | 1.6 | (2) | |

Operating occupancy as of September 30, 2025, including leased but not yet delivered space | 92.2% | ||

(1)Comprises the following: (i) 0.3% related to lease expirations that became vacant in 3Q25 and have been re-

leased with a future delivery upon completion of construction (and is included in item 2 below); (ii) 0.2%

vacancy at one asset in our Greater Stanford submarket, which was recently acquired with the intent to

redevelop office to laboratory space but for which we are now evaluating options to reposition for advanced

technologies use; and (iii) 0.6% of other occupancy declines, primarily from space that became vacant during

3Q25 which we are currently marketing. These lease expirations resulting in the 1.1% decline in occupancy

previously generated annual rental revenue aggregating approximately $29.0 million and had a weighted-

average lease expiration date at the end of July 2025.

(2)Represents temporary vacancies as of September 30, 2025 aggregating 617,458 RSF, primarily in the Greater

Boston, San Francisco Bay Area, San Diego, and Seattle markets, that are leased and expected to be

occupied upon completion of building and/or tenant improvements. The weighted-average expected delivery

date is approximately May 1, 2026 and the expected annual rental revenue is approximately $46 million.

Key operating metrics

Operating metrics | 3Q25 | YTD 3Q25 | |||

(dollars in millions) | |||||

Net operating income (cash basis) – annualized | $1,928 | (1) | $1,975 | ||

(Decline)/Increase compared to 3Q24 and YTD 3Q24, annualized | (5.8)% | (2) | 1.3% | (2) | |

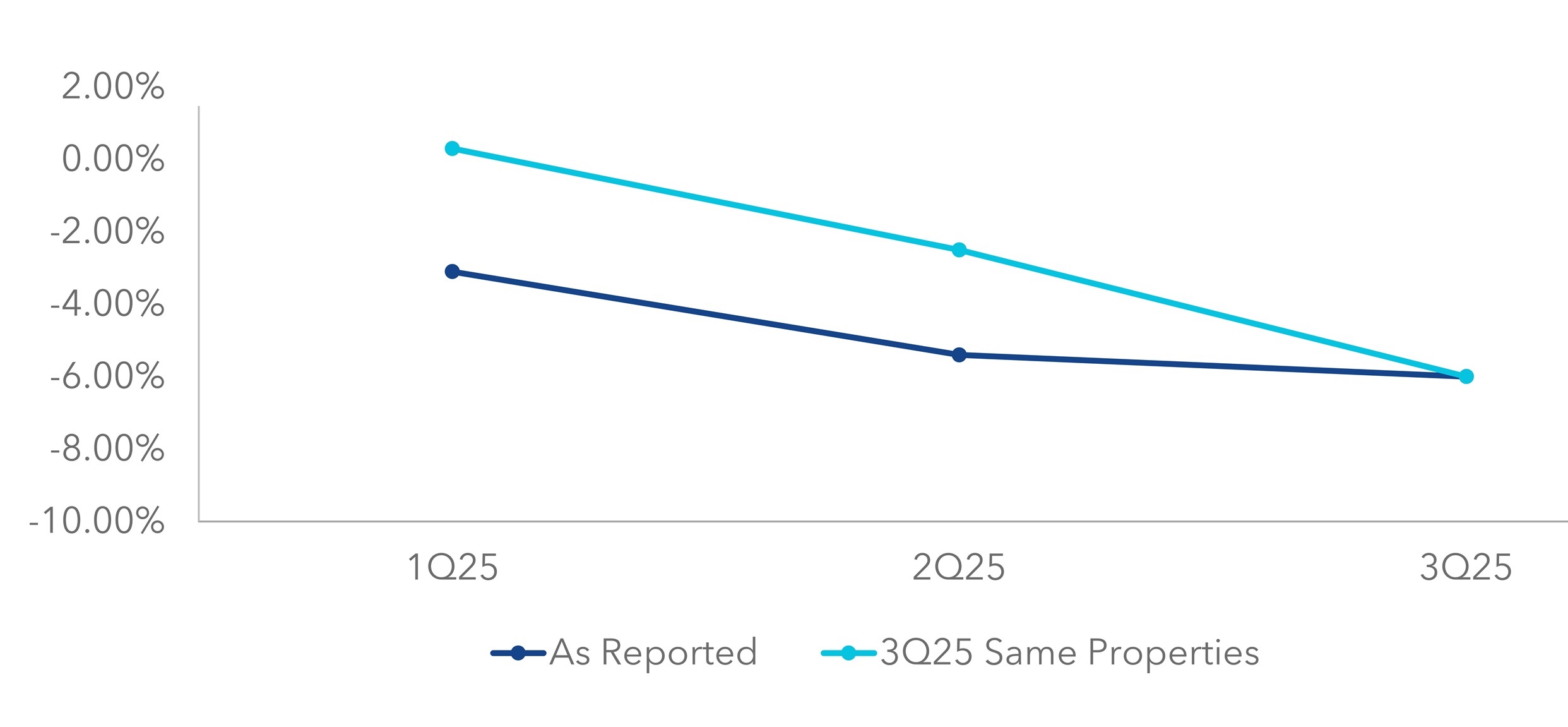

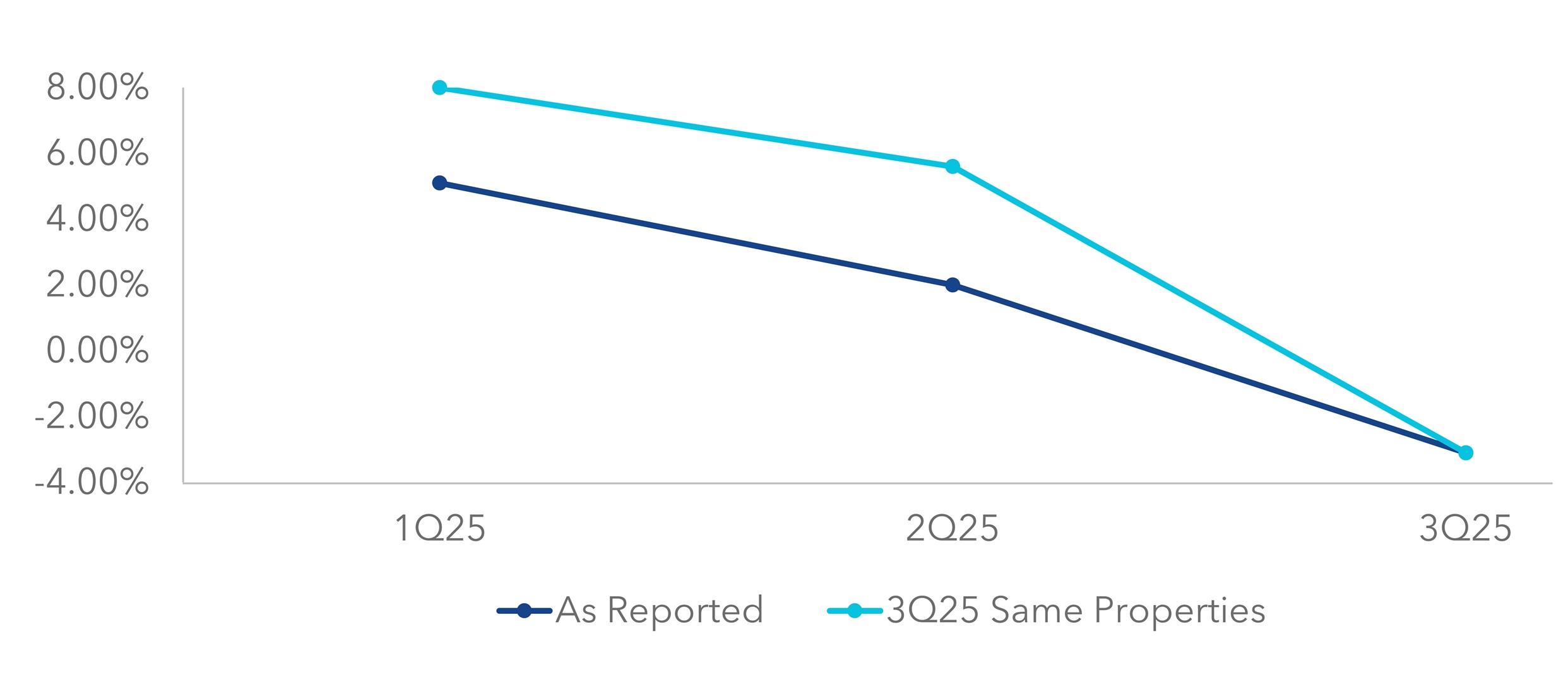

Same property performance: | |||||

Net operating income changes | (6.0)% | (3.1)% | |||

Net operating income changes (cash basis) | (3.1)% | 3.0% | |||

Occupancy – current-period average | 91.4% | 92.6% | |||

Occupancy – same-period prior-year average | 94.8% | 94.6% |

(1)Quarter annualized.

(2)Decrease in net operating income (cash basis) includes the impact of operating properties disposed of after

January 1, 2024. Excluding these dispositions, net operating income (cash basis) – annualized for the three

months ended September 30, 2025 would have decreased by 1.2%, and for the nine months ended

September 30, 2025 would have increased by 7.3%, compared to the corresponding periods in 2024.

•General and administrative expenses of $89.0 million for YTD 3Q25, representing cost

reductions of $46.6 million or 34%, compared to YTD 3Q24, primarily the result of cost-

control and efficiency initiatives related to reducing personnel-related costs and streamlining

business processes. Given that some of these cost savings are expected to be temporary in

nature, we anticipate approximately half of the cost reduction expected to be achieved in

2025 will continue in 2026.

•As a percentage of net operating income, our general and administrative expenses for the

trailing twelve months ended September 30, 2025 were 5.7% — the lowest level in the past

ten years and approximately half the average of other S&P 500 REITs.

Alexandria’s development and redevelopment pipeline delivered incremental annual net operating

income of $16 million commencing during 3Q25, with an additional $111 million of incremental

annual net operating income anticipated to deliver by 4Q26 primarily from projects that are 80%

leased/negotiating

•During 3Q25, we placed into service development projects aggregating 185,517 RSF that are

89% occupied across multiple submarkets and delivered incremental annual net operating

income of $16 million.

•A significant 3Q25 delivery consisted of 122,302 RSF at 10935, 10945, and 10955

Alexandria Way on the One Alexandria Square Megacampus in our Torrey Pines

submarket.

•Annual net operating income (cash basis) from recently delivered projects is expected to

increase by $50 million upon the burn-off of initial free rent, which has a weighted-average

remaining period of approximately three months.

•During 1Q25–4Q26, we expect to deliver annual net operating income representing nearly

8% growth in total net operating income from 2024 from projects that are 85% leased.

•76% of the RSF in our total development and redevelopment pipeline is within our

Megacampus ecosystems.

Development and Redevelopment Projects | Incremental Annual Net Operating Income | RSF | Occupied/ Leased/ Negotiating Percentage | |||||

(dollars in millions) | ||||||||

Placed into service: | ||||||||

1H25 | $52 | 527,268 | 96% | |||||

3Q25 | 16 | 185,517 | 89 | |||||

Placed into service in YTD 3Q25 | $68 | (1) | 712,785 | 94% | ||||

Expected to be placed into service: | ||||||||

4Q25 through 4Q26 | $111 | (2) | 969,524 | (3) | 80% | (4) | ||

(1)Excludes future incremental annual net operating income from recently delivered spaces aggregating 42,449

RSF that were vacant and/or unleased at delivery.

(2)Includes expected partial deliveries through 4Q26 from projects expected to stabilize in 2027 and beyond,

including speculative future leasing that is not yet fully committed. Refer to the initial and stabilized occupancy

years under “New Class A/A+ development and redevelopment properties: current projects” in the

Supplemental Information for additional details.

(3)Represents the RSF related to projects expected to stabilize by 4Q26. Does not include RSF for partial

deliveries through 4Q26 from projects expected to stabilize in 2027 and beyond.

(4)Represents the current leased/negotiating percentage of development and redevelopment projects that are

expected to stabilize during 4Q25 through 4Q26.

| |

Third Quarter Ended September 30, 2025 Financial and Operating Results (continued) | |

September 30, 2025 | |

Strong and flexible balance sheet

Key capital events

•In August 2025, we repaid a secured construction loan aggregating $154.6 million with an

interest rate of 7.18%, which was secured by our development project at 99 Coolidge Avenue

in our Cambridge/Inner Suburbs submarket. The project is currently 81% leased/negotiating

and is expected to be delivered in 4Q26. In connection with the repayment, we recognized a

loss on early extinguishment of debt of $107 thousand for the write-off of unamortized

deferred financing costs in 3Q25.

Investments

•As of September 30, 2025:

•Our non-real estate investments aggregated $1.5 billion.

•Unrealized gains presented in our consolidated balance sheet were $28.3 million,

comprising gross unrealized gains and losses aggregating $180.4 million and

$152.1 million, respectively.

•Investment income of $28.2 million for 3Q25 presented in our consolidated statement of

operations consisted of $34.8 million of realized gains, $18.5 million of unrealized gains, and

$25.1 million of impairment charges.

Other key highlights

Key items included in net income attributable to Alexandria’s common stockholders: | |||||||||||||||

YTD | |||||||||||||||

3Q25 | 3Q24 | 3Q25 | 3Q24 | 3Q25 | 3Q24 | 3Q25 | 3Q24 | ||||||||

(in millions, except per share amounts) | Amount | Per Share – Diluted | Amount | Per Share – Diluted | |||||||||||

Unrealized gains (losses) on non-real estate investments | $18.5 | $2.6 | $0.11 | $0.02 | $(71.6) | $(32.5) | $(0.42) | $(0.19) | |||||||

Gain on sales of real estate | 9.4 | 27.1 | 0.06 | 0.16 | 22.5 | 27.5 | 0.13 | 0.16 | |||||||

Impairment of non-real estate investments | (25.1) | (10.3) | (0.15) | (0.06) | (75.5) | (37.8) | (0.45) | (0.22) | |||||||

Impairment of real estate(1) | (323.9) | (5.7) | (1.90) | (0.03) | (485.6) | (36.5) | (2.85) | (0.22) | |||||||

Loss on early extinguishment of debt | (0.1) | — | — | — | (0.1) | — | — | — | |||||||

Increase in provision for expected credit losses on financial instruments | — | — | — | — | (0.3) | — | — | — | |||||||

Total | $(321.2) | $13.7 | $(1.88) | $0.09 | $(610.6) | $(79.3) | $(3.59) | $(0.47) | |||||||

(1)Refer to “Funds from operations and funds from operations per share” in the Earnings Press Release for additional details. | |||||||||||||||

Subsequent event

•In October 2025, we completed dispositions aggregating $167.4 million across three

submarkets and recognized a gain on sales of real estate of $4.4 million. Refer to

“Dispositions and exchange of partial interests” in the Earnings Press Release for additional

details.

2025 Guidance | |

September 30, 2025 | |

(Dollars in millions, except per share amounts) | |

Guidance for 2025 has been updated to reflect our current view of existing market conditions and assumptions for the year ending December 31, 2025. There can be no assurance that actual amounts will

not be materially higher or lower than these expectations. Our guidance for 2025 is subject to a number of variables and uncertainties, including actions and changes in policy by the current U.S. administration

related to the regulatory environment, life science funding, the U.S. Food and Drug Administration and National Institutes of Health, trade, and other areas. For additional discussion relating to risks and uncertainties

that could cause actual results to differ materially from those anticipated, refer to our discussion of “forward-looking statements” on page 8 of the Earnings Press Release as well as our SEC filings, including our

most recent annual report on Form 10-K and any subsequent quarterly reports on Form 10-Q.

Key changes to our 2025 guidance include the following:

1)The midpoint of our guidance range for 2025 net (loss) income per share was reduced by $3.44 from $0.50 to $(2.94). In addition to the items discussed in item 2 below, the update to our guidance range

for 2025 net (loss) income per share includes the following:

•Potential additional impairments of real estate (including impairments on stabilized and non-stabilized properties and land) that may be recognized in 4Q25 ranging from $0 to $685 million, related to

assets that could potentially be sold in 4Q25 or 2026, and if such assets meet the held for sale criteria in 4Q25, considering market factors, buyer ability to perform, our desire to proceed with a sale at

a particular price, and other factors.

•Potential additional gain on sales of real estate that may be recognized in 4Q25 ranging from $0 to $240 million related to assets that may be sold in 4Q25.

•These potential impairments and gains on sales of real estate will not impact our funds from operations per share pursuant to the Nareit definition of funds from operations.

2)The midpoint of our guidance range for 2025 funds from operations per share – diluted, as adjusted, was reduced by 25 cents, from $9.26 to $9.01. The primary drivers of the change include the following:

•A 1.0% reduction in projected 2025 same property net operating income and a 0.9% reduction in our projected operating occupancy percentage in North America as of December 31, 2025 (at the

midpoints of our guidance ranges), primarily due to slower than anticipated re-leasing of expiring spaces and lease-up of vacancy in our operating portfolio, reflecting reduced demand across the life

science industry.

•A reduction in projected 2025 realized gains on non-real estate investments. The midpoint of our revised guidance range for 2025 realized gains on non-real estate investments assumes

approximately $15 million in 4Q25, compared to the quarterly average realized gains of approximately $32 million per quarter for the nine months ended September 30, 2025.

3)Our guidance range for net debt and preferred stock Adjusted EBITDA – 4Q25 annualized increased from less than or equal to 5.2x to a range of 5.5x to 6.0x. The primary drivers of the change include the

following:

•A $450 million reduction in the midpoint of our guidance range for 2025 dispositions and sales of partial interests. This includes expected delays in the closing of certain dispositions that are now

anticipated to be completed in 1H26.

•A reduction in projected Adjusted EBITDA in 4Q25 related to the changes in same property performance (net operating income) and realized gains on non-real estate investments as described above.

Refer to “Key assumptions” and “Key sources and uses of capital” on the following page.

Projected 2025 Earnings per Share and Funds From Operations per Share Attributable to Alexandria’s Common Stockholders – Diluted | ||||||||||

As of 10/27/25 | As of 7/21/25 | Key Changes to Midpoint | ||||||||

Net (loss) income per share(1) | $(5.68) to $(0.20) | $0.40 to $0.60 | (2) | |||||||

Depreciation and amortization of real estate assets | 7.05 | 7.05 | ||||||||

Gain on sales of real estate | (0.14) to (1.54) | (0.08) | (2) | |||||||

Impairment of real estate – rental properties and land(3) | 6.69 to 2.67 | 0.77 | (2) | |||||||

Allocation to unvested restricted stock awards | (0.03) | (0.03) | ||||||||

Funds from operations per share(4) | $7.89 to $7.95 | $8.11 to $8.31 | ||||||||

Unrealized losses on non-real estate investments | 0.42 | 0.53 | ||||||||

Impairment of non-real estate investments(3) | 0.45 | 0.30 | ||||||||

Impairment of real estate | 0.23 | 0.23 | ||||||||

Allocation to unvested restricted stock awards | (0.01) | (0.01) | ||||||||

Funds from operations per share, as adjusted(4) | $8.98 to $9.04 | $9.16 to $9.36 | ||||||||

Midpoint | $9.01 | $9.26 | Reduction of 25 cents(2) | |||||||

Key Credit Metrics Targets | As of 10/27/25 | As of 7/21/25 | Key Changes | |||

Net debt and preferred stock to Adjusted EBITDA – 4Q25 annualized | 5.5x to 6.0x | Less than or equal to 5.2x | 0.6x increase(2) | |||

Fixed-charge coverage ratio – 4Q25 annualized | 3.6x to 4.1x | 4.0x to 4.5x | 0.4x reduction | |||

(1)Excludes unrealized gains or losses on non-real estate investments after September 30, 2025 that are required to be recognized in earnings and are excluded from funds from operations per share, as adjusted.

(2)Refer to the discussion regarding key changes to our 2025 guidance above for additional details.

(3)Refer to “Funds from operations and funds from operations per share” in the Earnings Press Release for additional details.

(4)Refer to “Funds from operations and funds from operations, as adjusted, attributable to Alexandria’s common stockholders” under “Definitions and reconciliations” in the Supplemental Information for additional details.

2025 Guidance (continued) | |

September 30, 2025 | |

(Dollars in millions) | |

As of 10/27/25 | As of 7/21/25 | Key Changes to Midpoint | |||||||||

Key Assumptions | Low | High | Low | High | |||||||

Operating occupancy percentage in North America as of December 31, 2025 | 90.0% | 91.6% | (1) | 90.9% | 92.5% | 90 bps reduction | |||||

Lease renewals and re-leasing of space: | |||||||||||

Rental rate changes | 7.0% | 15.0% | 9.0% | 17.0% | 200 bps reduction(2) | ||||||

Rental rate changes (cash basis) | 0.5% | 8.5% | 0.5% | 8.5% | No change | ||||||

Same property performance: | |||||||||||

Net operating income changes | (4.7)% | (2.7)% | (3.7)% | (1.7)% | 100 bps reduction | ||||||

Net operating income changes (cash basis) | (1.2)% | 0.8% | (1.2)% | 0.8% | No change | ||||||

Straight-line rent revenue | $75 | $95 | $96 | $116 | $21 million reduction | ||||||

General and administrative expenses | $112 | $127 | $112 | $127 | No Change | ||||||

Capitalization of interest | $320 | $350 | $320 | $350 | |||||||

Interest expense | $195 | $225 | $185 | $215 | $10 million increase(3) | ||||||

Realized gains on non-real estate investments(4) | $100 | $120 | $100 | $130 | $5 million reduction | ||||||

(1)Our guidance assumes an approximate 1% benefit related to a range of assets with vacancy that could potentially qualify for classification as held for sale in 4Q25 that have not yet reached the criteria for held for sale designation as of

3Q25.

(2)In October 2025, we executed a one-year lease extension aggregating 247,743 RSF with an investment-grade rated government institution tenant at a recently acquired office property in our Canada market. At acquisition, this building was

originally targeted for a future change in use, but we instead renewed the existing tenant through the beginning of 2027, with no incremental capital investment. We continue to evaluate options to convert this space, subject to market

conditions. The impact from this renewal on our 2025 rental rate changes is anticipated to result in a reduction of approximately 2.0%.

(3)The increase in the midpoint of our guidance range for 2025 interest expense is primarily due to the $450 million reduction to the midpoint of our guidance range for 2025 dispositions and sales of partial interests, which includes expected

delays in the closing of certain dispositions that are now anticipated to be completed in 1H26.

(4)Represents realized gains and losses included in funds from operations per share – diluted, as adjusted, and excludes significant impairments realized on non-real estate investments, if any. The midpoint of our revised guidance range for

2025 realized gains on non-real estate investments assumes approximately $15 million in 4Q25, compared to the quarterly average realized gains of approximately $32 million per quarter for the nine months ended September 30, 2025.

Refer to “Investments” in the Supplemental Information for additional details.

As of 10/27/25 | As of 7/21/25 Midpoint | Key Changes to Midpoint | ||||||||||||

Key Sources and Uses of Capital | Range | Midpoint | Certain Completed Items | |||||||||||

Sources of capital: | ||||||||||||||

Increase in debt | $60 | $260 | $160 | See below | $(290) | $450 million increase | ||||||||

Net cash provided by operating activities after dividends | 425 | 525 | 475 | 475 | ||||||||||

Dispositions and sales of partial interests (refer to page 7) | 1,100 | 1,900 | 1,500 | (1) | 1,950 | $450 million decrease | ||||||||

Total sources of capital | $1,585 | $2,685 | $2,135 | $2,135 | ||||||||||

Uses of capital: | ||||||||||||||

Construction | $1,450 | $2,050 | $1,750 | $1,750 | ||||||||||

Acquisitions and other opportunistic uses of capital | — | 500 | 250 | $208 | (2) | 250 | ||||||||

Ground lease prepayment | 135 | 135 | 135 | $135 | 135 | |||||||||

Total uses of capital | $1,585 | $2,685 | $2,135 | $2,135 | ||||||||||

Increase in debt (included above): | ||||||||||||||

Issuance of unsecured senior notes payable | $550 | $550 | $550 | $550 | $550 | |||||||||

Repayment of unsecured note payable | (600) | (600) | (600) | $(600) | (600) | |||||||||

Repayment of secured note payable | (154) | (154) | (154) | $(154) | (3) | (154) | ||||||||

Unsecured senior line of credit, commercial paper, and other | 264 | 464 | 364 | (86) | ||||||||||

Increase in debt | $60 | $260 | $160 | $(290) | $450 million increase | |||||||||

(1)As of October 27, 2025, completed dispositions aggregated $508.3 million and our share of pending transactions subject to non-refundable deposits, signed letters of intent, or purchase and sale agreement negotiations aggregated

$1.0 billion. We expect to achieve a weighted-average capitalization rate on our projected 2025 dispositions and sales of partial interests (excluding land and including stabilized and non-stabilized operating properties) in the 7.5%–8.5%

range. We expect dispositions of land to represent 20%–30% of our total dispositions and sales of partial interest sales for the year ending December 31, 2025. Refer to “Dispositions and exchange of partial interests” in the Earnings Press

Release for additional details.

(2)Under our common stock repurchase program authorized in December 2024, we may repurchase up to $500 million of our common stock through December 31, 2025. During 3Q25, we did not repurchase any shares of common stock. As

of October 27, 2025, the approximate value of shares authorized and remaining under this program was $241.8 million. Subject to market conditions, we may consider repurchasing additional shares of our common stock.

(3)In August 2025, we repaid a secured construction loan held by our development project at 99 Coolidge Avenue in our Cambridge/Inner Suburbs submarket. Refer to “Key capital events” in the Earnings Press Release for additional details.

2026 Considerations | |

September 30, 2025 | |

Summary of Key Items That May Impact 2026 Results

We expect to introduce 2026 guidance on December 3, 2025 at our Investor Day. The following is an initial summary of key items that are expected to impact 2026 results:

•Core operations – Slower demand across the life science sector and increased supply for life science real estate could negatively impact future occupancy. Additional considerations

include the following:

•Same property net operating income decrease for 3Q25 compared to 3Q24 of 6.0% reflects a decline relative to the first half of 2025. Refer to “Same property performance” in the

Supplemental Information for additional details.

•Operating occupancy has decreased four consecutive quarters from 94.7% as of September 30, 2024 to 90.6% as of September 30, 2025.

•Before the benefit of excluding assets designated as held for sale which contained vacancy, 3Q25 occupancy declined 1.1% compared to 2Q25, primarily related to 3Q25 lease

expirations. These lease expirations resulting in the 1.1% decline in occupancy previously generated annual rental revenue aggregating approximately $29.0 million and had a

weighted-average lease expiration date at the end of July 2025. We are currently marketing these spaces.

•Our guidance for operating occupancy percentage in North America as of December 31, 2025 assumes an approximate 1% benefit related to a range of assets with vacancy that

could potentially qualify for designation as held for sale by December 31, 2025, but that have not yet qualified as of September 30, 2025. After considering this potential adjustment,

the midpoint of our guidance range for occupancy as of December 31, 2025 implies an 80 bps decline in operating occupancy percentage during 4Q25.

•There are key lease expirations primarily located in the Greater Boston, San Francisco Bay Area, and San Diego markets aggregating 1.2 million RSF with a weighted-average lease

expiration date of March 19, 2026 and annual rental revenue aggregating $81 million, which are expected to become vacant upon lease expiration. We expect downtime on these

spaces ranging from 6 to 24 months on a weighted-average basis. Refer to “Contractual lease expirations” in the Supplemental Information for additional details.

•Capitalized interest – There is approximately $4.2 billion of average real estate basis capitalized during YTD 3Q25 related to future pipeline projects undergoing critical pre-construction

activities, including various phases of entitlement, design, site work, and other activities necessary to begin aboveground vertical construction. We expect these projects to reach

anticipated pre-construction milestones on April 14, 2026, on a weighted-average real estate investment basis. We will evaluate, on an asset-by-asset basis, whether to (i) proceed with

additional pre-construction and/or construction activities based on leasing demand and/or market conditions, (ii) pause future investments, or (iii) consider the potential dispositions of

these real estate assets. If we cease activities necessary to prepare a project for its intended use, costs related to such project, including interest, payroll, property taxes, insurance, and

other costs directly related and essential to the construction of Class A/A+ properties, will be expensed as incurred. Refer to “Capitalization of interest” in the Supplemental Information for

additional details.

•Realized gains on non-real estate investments – The midpoint of our revised guidance range for 2025 realized gains on non-real estate investments assumes approximately $15 million in

4Q25, compared to the quarterly average realized gains of approximately $32 million per quarter for the nine months ended September 30, 2025. Refer to “Investments” in the

Supplemental Information for additional details.

•General and administrative expenses – Over the past several years, we have implemented comprehensive measures to reduce our expenditures across our organization, including our

general and administrative expenses. These initiatives are expected to generate a reduction in general and administrative expenses of approximately $49 million, or 29%, during the year

ending December 31, 2025 (at the midpoint of our 2025 guidance range) compared to the year ended December 31, 2024. Given that some of these costs savings are expected to be

temporary in nature, we anticipate approximately half of the cost reductions expected to be achieved in 2025 will continue in 2026.

•Dispositions and equity-type capital

•As of October 27, 2025, our share of pending dispositions subject to non-refundable deposits, signed letters of intent, and/or purchase and sale agreement negotiations aggregated

$1.0 billion. We expect these dispositions to close in late 4Q25; therefore, the corresponding reduction in EBITDA is expected to impact 1Q26. Refer to “Dispositions and exchange of

partial interests” in the Earnings Press Release for additional details.

•We expect construction spending in 2026 to be similar or slightly higher than the $1.75 billion midpoint of our guidance range for 2025 construction in order to complete our active

construction projects and significant revenue- and non-revenue-enhancing capital expenditures necessary to lease vacant space. Given the factors previously described that could

negatively impact EBITDA, we may require significant equity-type capital to manage our leverage profile.

•We expect a significant source of funding to come from the sale of non-core assets in 2026. We anticipate an end to our large-scale non-core asset sales program in 2026 or early

2027. As of September 30, 2025, 77% of our annual rental revenue is from our Megacampus™ platform, and we expect this percentage to continue to grow over time.

•Dividends and net cash provided by operating activities after dividends

•From 2013 to 2025, dividends per share and funds from operations per share, as adjusted have been highly correlated, with cumulative increases of 102% and 105%, respectively.

•The factors previously described could lead to a reduction in funds from operations per share, as adjusted and net cash provided by operating activities. At the current dividend rate,

the amount of net cash provided by operating activities after payment of dividends available to recycle and address our 2026 capital needs could be reduced. As a result, we expect

our Board of Directors to carefully evaluate our 2026 dividend strategy.

Dispositions and Exchange of Partial Interests | |

September 30, 2025 | |

(Dollars in thousands) | |

Interest Sold/ Acquired | Square Footage | Gain on Sales of Real Estate | ||||||||||||||

Property | Submarket/Market | Date of Transaction | Operating | Future Development | Price | |||||||||||

Dispositions | ||||||||||||||||

Completed in 1H25 | $260,639 | $13,165 | ||||||||||||||

Completed in 3Q25: | ||||||||||||||||

5505 Morehouse Drive(1) | Sorrento Mesa/San Diego | 8/26/25 | 100% | 79,945 | — | 45,000 | — | |||||||||

Other | Various | 35,232 | 76 | |||||||||||||

Total dispositions completed in 3Q25 | 80,232 | (2) | 76 | (3) | ||||||||||||

Completed in October 2025: | ||||||||||||||||

550 Arsenal Street(4) | Cambridge/Inner Suburbs/Greater Boston | 10/15/25 | 100% | 249,275 | 281,592 | 99,250 | — | |||||||||

Other | Various | 68,129 | 4,362 | |||||||||||||

167,379 | (2) | 4,362 | ||||||||||||||

Total dispositions as of October 27, 2025 | 508,250 | $17,603 | ||||||||||||||

Our share of pending dispositions subject to non-refundable deposits, signed letters of intent, and/or purchase and sale agreement negotiations | 1,032,495 | |||||||||||||||

Completed and pending YTD 2025 dispositions, excluding exchange of partial interests (see below) | $1,540,745 | |||||||||||||||

2025 guidance range for dispositions and sales of partial interests | $1,100,000 – $1,900,000 | |||||||||||||||

2025 guidance midpoint for dispositions and sales of partial interests | $1,500,000 | |||||||||||||||

Exchange of partial interests(5) | ||||||||||||||||

Disposition of Pacific Technology Park | Sorrento Mesa/San Diego | 9/9/25 | 50% | 544,352 | — | $96,000 | $9,290 | |||||||||

Acquisition of 199 East Blaine Street | Lake Union/Seattle | 9/9/25 | 70% | 115,084 | — | (94,430) | ||||||||||

Difference in sales price received in cash | $1,570 | |||||||||||||||

Refer to “Definitions and reconciliations” in the Supplemental Information for additional details.

(1)Represents a laboratory property with significant near-term lease expirations.

(2)Dispositions completed during the three months ended September 30, 2025 had annual net operating income of $4.3 million (based on 2Q25 annualized) with a weighted-average disposition date of September 2, 2025. Additionally,

October 2025 dispositions had annual net operating income of $13.0 million (based on 3Q25 annualized) with a weighted-average disposition date of October 13, 2025.

(3)Excludes a gain on sale of interest related to an unconsolidated real estate joint venture of $458 thousand, which is classified as equity in earnings of unconsolidated real estate joint ventures in our consolidated statement of operations.

(4)Represents a retail shopping center with future development opportunity. We originally acquired the property in 2021 with the intent to demolish the retail center and develop it into laboratory space. However, due to the project’s financial

outlook and the substantial capital that development would have required, we decided to recycle the capital generated by the disposition into our development and redevelopment pipeline. The capitalization rates of the disposition were

6.1% and 5.4% (cash basis) based upon net operating income and net operating income (cash basis), respectively, for 3Q25 annualized.

(5)In September 2025, we completed an exchange of partial interests in two consolidated joint ventures, Pacific Technology Park and 199 East Blaine Street, with one joint venture partner, resulting in a sales price received by cash of $1.6

million:

•We sold our 50% controlling interest in Pacific Technology Park, a non-Megacampus comprising five non-laboratory properties that were 93% occupied, at capitalization rates of 4.9% and 5.0% (cash basis). The disposition had

consolidated annual net operating income of $9.4 million based on 2Q25 annualized (at 100%). As of September 30, 2025, we no longer have any ownership interest in Pacific Technology Park, and the consolidated net operating

income is no longer included in our statement of operations following the sale.

•We acquired our partner’s 70% noncontrolling interest at 199 East Blaine Street, a fully occupied laboratory building located in our Alexandria Center® for Life Science – Eastlake Megacampus, with a weighted-average remaining lease

term of 1.3 years. The purchase price exceeded the book value of the noncontrolling interest by $66.3 million, which was recognized in additional paid-in capital. As of September 30, 2025, we own 100% of 199 East Blaine Street.

| |

Earnings Call Information and About the Company | |

September 30, 2025 | |

We will host a conference call on Tuesday, October 28, 2025, at 2:00 p.m. Eastern Time (“ET”)/11:00 a.m. Pacific Time (“PT”), which is open to the general public, to discuss our financial and operating

results for the third quarter ended September 30, 2025. To participate in this conference call, dial (833) 366-1125 or (412) 902-6738 shortly before 2:00 p.m. ET/11:00 a.m. PT and ask the operator to join the call for

Alexandria Real Estate Equities, Inc. The audio webcast can be accessed at www.are.com in the “For Investors” section. A replay of the call will be available for a limited time from 4:00 p.m. ET/1:00 p.m. PT on

Tuesday, October 28, 2025. The replay number is (877) 344-7529 or (412) 317-0088, and the access code is 6086829.

Additionally, a copy of this Earnings Press Release and Supplemental Information for the third quarter ended September 30, 2025 is available in the “For Investors” section of our website at www.are.com

or by following this link: https://www.are.com/fs/2025q3.pdf.

For any questions, please contact corporateinformation@are.com; Joel S. Marcus, executive chairman and founder; Peter M. Moglia, chief executive officer and chief investment officer; Marc E. Binda,

chief financial officer and treasurer; or Paula Schwartz, managing director of Rx Communications Group, at (917) 633-7790.

About the Company

Alexandria Real Estate Equities, Inc. (NYSE: ARE), an S&P 500® company, is a best-in-class, mission-driven life science REIT making a positive and lasting impact on the world. With our founding in 1994,

Alexandria pioneered the life science real estate niche. Alexandria is the preeminent and longest-tenured owner, operator, and developer of collaborative Megacampus™ ecosystems in AAA life science innovation

cluster locations, including Greater Boston, the San Francisco Bay Area, San Diego, Seattle, Maryland, Research Triangle, and New York City. As of September 30, 2025, Alexandria has a total market capitalization

of $27.8 billion and an asset base in North America that includes 39.1 million RSF of operating properties and 4.2 million RSF of Class A/A+ properties undergoing construction and one 100% pre-leased committed

near-term project expected to commence construction in the next year. Alexandria has a long-standing and proven track record of developing Class A/A+ properties clustered in highly dynamic and collaborative

Megacampus environments that enhance our tenants’ ability to successfully recruit and retain world-class talent and inspire productivity, efficiency, creativity, and success. Alexandria also provides strategic capital to

transformative life science companies through our venture capital platform. We believe our unique business model and diligent underwriting ensure a high-quality and diverse tenant base that results in higher

occupancy levels, longer lease terms, higher rental income, higher returns, and greater long-term asset value. For more information on Alexandria, please visit www.are.com.

Forward-Looking Statements

This document includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

Such forward-looking statements include, without limitation, statements regarding our projected 2025 earnings per share, projected 2025 funds from operations per share, projected 2025 funds from operations per

share, as adjusted, projected net operating income, and our projected sources and uses of capital. You can identify the forward-looking statements by their use of forward-looking words, such as “forecast,”

“guidance,” “goals,” “projects,” “estimates,” “anticipates,” “believes,” “expects,” “intends,” “may,” “plans,” “seeks,” “should,” “targets,” or “will,” or the negative of those words or similar words. These forward-looking

statements are based on our current expectations, beliefs, projections, future plans and strategies, anticipated events or trends, and similar expressions concerning matters that are not historical facts, as well as a

number of assumptions concerning future events. There can be no assurance that actual results will not be materially higher or lower than these expectations. These statements are subject to risks, uncertainties,

assumptions, and other important factors that could cause actual results to differ materially from the results discussed in the forward-looking statements. Factors that might cause such a difference include, without

limitation, our failure to obtain capital (debt, construction financing, and/or equity) or refinance debt maturities, lower than expected yields, increased interest rates and operating costs, adverse economic or real

estate developments in our markets, our failure to successfully place into service and lease any properties undergoing development or redevelopment and our existing space held for future development or

redevelopment (including new properties acquired for that purpose), our failure to successfully operate or lease acquired properties, decreased rental rates, increased vacancy rates or failure to renew or replace

expiring leases, defaults on or non-renewal of leases by tenants, adverse general and local economic conditions, an unfavorable capital market environment, decreased leasing activity or lease renewals, failure to

obtain LEED and other healthy building certifications and efficiencies, and other risks and uncertainties detailed in our filings with the Securities and Exchange Commission (“SEC”). Accordingly, you are cautioned

not to place undue reliance on such forward-looking statements. All forward-looking statements are made as of the date of this Earnings Press Release and Supplemental Information, and unless otherwise stated,

we assume no obligation to update this information and expressly disclaim any obligation to update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. For

more discussion relating to risks and uncertainties that could cause actual results to differ materially from those anticipated in our forward-looking statements, and risks to our business in general, please refer to our

SEC filings, including our most recent annual report on Form 10-K and any subsequent quarterly reports on Form 10-Q.

This document is not an offer to sell or a solicitation to buy securities of Alexandria Real Estate Equities, Inc. Any offers to sell or solicitations to buy our securities shall be made only by means of a

prospectus approved for that purpose. Unless otherwise indicated, the “Company,” “Alexandria,” “ARE,” “we,” “us,” and “our” refer to Alexandria Real Estate Equities, Inc. and our consolidated subsidiaries.

Alexandria®, Lighthouse Design® logo, Building the Future of Life-Changing Innovation®, That’s What’s in Our DNA®, Megacampus™, At the Vanguard and Heart of the Life Science Ecosystem™, Alexandria

Center®, Alexandria Technology Square®, Alexandria Technology Center®, and Alexandria Innovation Center® are copyrights and trademarks of Alexandria Real Estate Equities, Inc. All other company names,

trademarks, and logos referenced herein are the property of their respective owners.

Consolidated Statements of Operations | |

September 30, 2025 | |

(Dollars in thousands, except per share amounts) | |

Three Months Ended | Nine Months Ended | |||||||||||||

9/30/25 | 6/30/25 | 3/31/25 | 12/31/24 | 9/30/24 | 9/30/25 | 9/30/24 | ||||||||

Revenues: | ||||||||||||||

Income from rentals | $735,849 | $737,279 | $743,175 | $763,249 | $775,744 | $2,216,303 | $2,286,457 | |||||||

Other income | 16,095 | 24,761 | 14,983 | 25,696 | 15,863 | 55,839 | 40,992 | |||||||

Total revenues | 751,944 | 762,040 | 758,158 | 788,945 | 791,607 | 2,272,142 | 2,327,449 | |||||||

Expenses: | ||||||||||||||

Rental operations | 239,234 | 224,433 | 226,395 | 240,432 | 233,265 | 690,062 | 668,833 | |||||||

General and administrative | 29,224 | 29,128 | 30,675 | 32,730 | 43,945 | 89,027 | 135,629 | |||||||

Interest | 54,852 | 55,296 | 50,876 | 55,659 | 43,550 | 161,024 | 130,179 | |||||||

Depreciation and amortization | 340,230 | 346,123 | 342,062 | 330,108 | 293,998 | 1,028,415 | 872,272 | |||||||

Impairment of real estate | 323,870 | (1) | 129,606 | 32,154 | 186,564 | 5,741 | 485,630 | 36,504 | ||||||

Loss on early extinguishment of debt | 107 | — | — | — | — | 107 | — | |||||||

Total expenses | 987,517 | 784,586 | 682,162 | 845,493 | 620,499 | 2,454,265 | 1,843,417 | |||||||

Equity in earnings (losses) of unconsolidated real estate joint ventures | 201 | (9,021) | (507) | 6,635 | 139 | (9,327) | 424 | |||||||

Investment income (loss) | 28,161 | (30,622) | (49,992) | (67,988) | 15,242 | (52,453) | 14,866 | |||||||

Gain on sales of real estate | 9,366 | — | 13,165 | 101,806 | 27,114 | 22,531 | 27,506 | |||||||

Net (loss) income | (197,845) | (62,189) | 38,662 | (16,095) | 213,603 | (221,372) | 526,828 | |||||||

Net income attributable to noncontrolling interests | (34,909) | (44,813) | (47,601) | (46,150) | (45,656) | (127,323) | (141,634) | |||||||

Net (loss) income attributable to Alexandria Real Estate Equities, Inc.’s stockholders | (232,754) | (107,002) | (8,939) | (62,245) | 167,947 | (348,695) | 385,194 | |||||||

Net income attributable to unvested restricted stock awards | (2,183) | (2,609) | (2,660) | (2,677) | (3,273) | (7,452) | (10,717) | |||||||

Net (loss) income attributable to Alexandria Real Estate Equities, Inc.’s common stockholders | $(234,937) | $(109,611) | $(11,599) | $(64,922) | $164,674 | $(356,147) | $374,477 | |||||||

Net (loss) income per share attributable to Alexandria Real Estate Equities, Inc.’s common stockholders: | ||||||||||||||

Basic | $(1.38) | $(0.64) | $(0.07) | $(0.38) | $0.96 | $(2.09) | $2.18 | |||||||

Diluted | $(1.38) | $(0.64) | $(0.07) | $(0.38) | $0.96 | $(2.09) | $2.18 | |||||||

Weighted-average shares of common stock outstanding: | ||||||||||||||

Basic | 170,181 | 170,135 | 170,522 | 172,262 | 172,058 | 170,278 | 172,007 | |||||||

Diluted | 170,181 | 170,135 | 170,522 | 172,262 | 172,058 | 170,278 | 172,007 | |||||||

Dividends declared per share of common stock | $1.32 | $1.32 | $1.32 | $1.32 | $1.30 | $3.96 | $3.87 | |||||||

(1) Refer to footnote 2 in “Funds from operations and funds from operations per share” in the Earnings Press Release for additional details.

Consolidated Balance Sheets | |

September 30, 2025 | |

(In thousands) | |

9/30/25 | 6/30/25 | 3/31/25 | 12/31/24 | 9/30/24 | ||||||

Assets | ||||||||||

Investments in real estate | $31,743,917 | $32,160,600 | $32,121,712 | $32,110,039 | $32,951,777 | |||||

Investments in unconsolidated real estate joint ventures | 39,601 | 40,234 | 50,086 | 39,873 | 40,170 | |||||

Cash and cash equivalents | 579,474 | 520,545 | 476,430 | 552,146 | 562,606 | |||||

Restricted cash | 4,705 | 7,403 | 7,324 | 7,701 | 17,031 | |||||

Tenant receivables | 6,409 | 6,267 | 6,875 | 6,409 | 6,980 | |||||

Deferred rent | 1,257,378 | 1,232,719 | 1,210,584 | 1,187,031 | 1,216,176 | |||||

Deferred leasing costs | 505,241 | 491,074 | 489,287 | 485,959 | 516,872 | |||||

Investments | 1,537,638 | 1,476,696 | 1,479,688 | 1,476,985 | 1,519,327 | |||||

Other assets | 1,700,785 | 1,688,091 | 1,758,442 | 1,661,306 | 1,657,189 | |||||

Total assets | $37,375,148 | $37,623,629 | $37,600,428 | $37,527,449 | $38,488,128 | |||||

Liabilities, Noncontrolling Interests, and Equity | ||||||||||

Secured notes payable | $— | $153,500 | $150,807 | $149,909 | $145,000 | |||||

Unsecured senior notes payable | 12,044,999 | 12,042,607 | 12,640,144 | 12,094,465 | 12,092,012 | |||||

Unsecured senior line of credit and commercial paper | 1,548,542 | 1,097,993 | 299,883 | — | 454,589 | |||||

Accounts payable, accrued expenses, and other liabilities | 2,432,726 | 2,360,840 | 2,281,414 | 2,654,351 | 2,865,886 | |||||

Dividends payable | 230,603 | 229,686 | 228,622 | 230,263 | 227,191 | |||||

Total liabilities | 16,256,870 | 15,884,626 | 15,600,870 | 15,128,988 | 15,784,678 | |||||

Commitments and contingencies | ||||||||||

Redeemable noncontrolling interests | 58,662 | 9,612 | 9,612 | 19,972 | 16,510 | |||||

Alexandria Real Estate Equities, Inc.’s stockholders’ equity: | ||||||||||

Common stock | 1,703 | 1,701 | 1,701 | 1,722 | 1,722 | |||||

Additional paid-in capital | 16,669,802 | 17,200,949 | 17,509,148 | 17,933,572 | 18,238,438 | |||||

Accumulated other comprehensive loss | (32,203) | (27,415) | (46,202) | (46,252) | (22,529) | |||||

Alexandria Real Estate Equities, Inc.’s stockholders’ equity | 16,639,302 | 17,175,235 | 17,464,647 | 17,889,042 | 18,217,631 | |||||

Noncontrolling interests | 4,420,314 | 4,554,156 | 4,525,299 | 4,489,447 | 4,469,309 | |||||

Total equity | 21,059,616 | 21,729,391 | 21,989,946 | 22,378,489 | 22,686,940 | |||||

Total liabilities, noncontrolling interests, and equity | $37,375,148 | $37,623,629 | $37,600,428 | $37,527,449 | $38,488,128 |

Funds From Operations and Funds From Operations per Share | |

September 30, 2025 | |

(In thousands) | |

The following table presents a reconciliation of net income (loss) attributable to Alexandria’s common stockholders, the most directly comparable financial measure presented in

accordance with U.S. generally accepted accounting principles (“GAAP”), including our share of amounts from consolidated and unconsolidated real estate joint ventures, to funds from operations

attributable to Alexandria’s common stockholders – diluted, and funds from operations attributable to Alexandria’s common stockholders – diluted, as adjusted, for the periods below:

Three Months Ended | Nine Months Ended | |||||||||||||

9/30/25 | 6/30/25 | 3/31/25 | 12/31/24 | 9/30/24 | 9/30/25 | 9/30/24 | ||||||||

Net (loss) income attributable to Alexandria’s common stockholders – basic and diluted | $(234,937) | $(109,611) | $(11,599) | $(64,922) | $164,674 | $(356,147) | $374,477 | |||||||

Depreciation and amortization of real estate assets | 338,182 | 343,729 | 339,381 | 327,198 | 291,258 | 1,021,292 | 864,326 | |||||||

Noncontrolling share of depreciation and amortization from consolidated real estate JVs | (45,327) | (36,047) | (33,411) | (34,986) | (32,457) | (114,785) | (94,725) | |||||||

Our share of depreciation and amortization from unconsolidated real estate JVs | 852 | 942 | 1,054 | 1,061 | 1,075 | 2,848 | 3,177 | |||||||

Gain on sales of real estate | (9,824) | (1) | — | (13,165) | (100,109) | (27,114) | (22,989) | (27,506) | ||||||

Impairment of real estate – rental properties and land | 323,870 | (2) | 131,090 | — | 184,532 | 5,741 | 454,960 | 7,923 | ||||||

Allocation to unvested restricted stock awards | (1,648) | (1,222) | (686) | (1,182) | (2,908) | (3,590) | (7,657) | |||||||

Funds from operations attributable to Alexandria’s common stockholders – diluted(3) | 371,168 | 328,881 | 281,574 | 311,592 | 400,269 | 981,589 | 1,120,015 | |||||||

Unrealized (gains) losses on non-real estate investments | (18,515) | 21,938 | 68,145 | 79,776 | (2,610) | 71,568 | 32,470 | |||||||

Impairment of non-real estate investments | 25,139 | (4) | 39,216 | 11,180 | 20,266 | 10,338 | 75,535 | 37,824 | ||||||

Impairment of real estate | — | 7,189 | 32,154 | 2,032 | — | 39,343 | 28,581 | |||||||

Loss on early extinguishment of debt | 107 | — | — | — | — | 107 | — | |||||||

Increase (decrease) in provision for expected credit losses on financial instruments | — | — | 285 | (434) | — | 285 | — | |||||||

Allocation to unvested restricted stock awards | (74) | (794) | (1,329) | (1,407) | (125) | (2,156) | (1,640) | |||||||

Funds from operations attributable to Alexandria’s common stockholders – diluted, as adjusted | $377,825 | $396,430 | $392,009 | $411,825 | $407,872 | $1,166,271 | $1,217,250 | |||||||

Refer to “Definitions and reconciliations” in the Supplemental Information for additional details.

(1)Includes our share of a gain on sale of real estate asset by an unconsolidated real estate joint venture of $458 thousand, which is classified as equity in earnings of unconsolidated real estate joint ventures in our consolidated

statements of operations.

(2)Primarily represents impairment charges to reduce the carrying amount of our investments in real estate assets to their respective estimated fair values less costs to sell upon their classification as held for sale in 3Q25, including (i)

$206.2 million related to our only property located in Long Island City, in our New York City market, which was a full building conversion to laboratory/office space and is currently 52% occupied, (ii) $43.4 million related to a retail

shopping center at 550 Arsenal Street that was originally intended to be a life science development in our Cambridge/Inner Suburbs submarket that was sold in October 2025, (iii) $31.8 million related to a vacant property that would

require significant re-leasing capital in our Research Triangle submarket, and (iv) $27.8 million related to land parcels in our Sorrento Mesa submarket.

(3)Calculated in accordance with standards established by the Nareit Board of Governors.

(4)Primarily related to four non-real estate investments in privately held entities that do not report NAV.

Funds From Operations and Funds From Operations per Share (continued) | |

September 30, 2025 | |

(In thousands, except per share amounts) | |

The following table presents a reconciliation of net income (loss) per share attributable to Alexandria’s common stockholders, the most directly comparable financial measure presented in

accordance with GAAP, including our share of amounts from consolidated and unconsolidated real estate joint ventures, to funds from operations per share attributable to Alexandria’s common

stockholders – diluted, and funds from operations per share attributable to Alexandria’s common stockholders – diluted, as adjusted, for the periods below. Per share amounts may not add due to

rounding.

Three Months Ended | Nine Months Ended | |||||||||||||

9/30/25 | 6/30/25 | 3/31/25 | 12/31/24 | 9/30/24 | 9/30/25 | 9/30/24 | ||||||||

Net (loss) income per share attributable to Alexandria’s common stockholders – diluted | $(1.38) | $(0.64) | $(0.07) | $(0.38) | $0.96 | $(2.09) | $2.18 | |||||||

Depreciation and amortization of real estate assets | 1.73 | 1.81 | 1.80 | 1.70 | 1.51 | 5.34 | 4.49 | |||||||

Gain on sales of real estate | (0.06) | — | (0.08) | (0.58) | (0.16) | (0.14) | (0.16) | |||||||

Impairment of real estate – rental properties and land | 1.90 | 0.77 | — | 1.07 | 0.03 | 2.67 | 0.05 | |||||||

Allocation to unvested restricted stock awards | (0.01) | (0.01) | — | — | (0.01) | (0.02) | (0.05) | |||||||

Funds from operations per share attributable to Alexandria’s common stockholders – diluted | 2.18 | 1.93 | 1.65 | 1.81 | 2.33 | 5.76 | 6.51 | |||||||

Unrealized (gains) losses on non-real estate investments | (0.11) | 0.13 | 0.40 | 0.46 | (0.02) | 0.42 | 0.19 | |||||||

Impairment of non-real estate investments | 0.15 | 0.23 | 0.07 | 0.12 | 0.06 | 0.45 | 0.22 | |||||||

Impairment of real estate | — | 0.04 | 0.19 | 0.01 | — | 0.23 | 0.17 | |||||||

Allocation to unvested restricted stock awards | — | — | (0.01) | (0.01) | — | (0.01) | (0.01) | |||||||

Funds from operations per share attributable to Alexandria’s common stockholders – diluted, as adjusted | $2.22 | $2.33 | $2.30 | $2.39 | $2.37 | $6.85 | $7.08 | |||||||

Weighted-average shares of common stock outstanding – diluted | ||||||||||||||

Earnings per share – diluted | 170,181 | 170,135 | 170,522 | 172,262 | 172,058 | 170,278 | 172,007 | |||||||

Funds from operations – diluted, per share | 170,305 | 170,192 | 170,599 | 172,262 | 172,058 | 170,351 | 172,007 | |||||||

Funds from operations – diluted, as adjusted, per share | 170,305 | 170,192 | 170,599 | 172,262 | 172,058 | 170,351 | 172,007 | |||||||

Refer to “Definitions and reconciliations” in the Supplemental Information for additional details.

SUPPLEMENTAL

INFORMATION

| |

Company Profile | |

September 30, 2025 | |

Alexandria Real Estate Equities, Inc. (NYSE: ARE), an S&P 500® company, is a

best-in-class, mission-driven life science REIT making a positive and lasting impact on the

world. With our founding in 1994, Alexandria pioneered the life science real estate niche.

Alexandria is the preeminent and longest-tenured owner, operator, and developer of

collaborative Megacampus™ ecosystems in AAA life science innovation cluster locations,

including Greater Boston, the San Francisco Bay Area, San Diego, Seattle, Maryland,

Research Triangle, and New York City.

As of September 30, 2025, Alexandria has a total market capitalization of

$27.8 billion and an asset base in North America that includes 39.1 million RSF of

operating properties and 4.2 million RSF of Class A/A+ properties undergoing construction

and one 100% pre-leased committed near-term project expected to commence

construction in the next year.

Alexandria has a long-standing and proven track record of developing Class A/A+

properties clustered in highly dynamic and collaborative Megacampus environments that

enhance our tenants’ ability to successfully recruit and retain world-class talent and inspire

productivity, efficiency, creativity, and success.

Alexandria also provides strategic capital to transformative life science

companies through our venture capital platform. We believe our unique business model

and diligent underwriting ensure a high-quality and diverse tenant base that results in

higher occupancy levels, longer lease terms, higher rental income, higher returns, and

greater long-term asset value. For more information on Alexandria, please visit

www.are.com.

Tenant base

Alexandria is known for our high-quality and diverse tenant base, with 53% of our

annual rental revenue being generated from tenants that are investment-grade rated or

publicly traded large cap companies. The quality, diversity, breadth, and depth of our

significant relationships with our tenants provide Alexandria with high-quality and stable

cash flows. Alexandria’s underwriting team and long-term industry relationships positively

distinguish us from all other publicly traded REITs and real estate companies.

Executive and senior management team

Alexandria’s executive and senior management team has unique experience and

expertise in creating, owning, and operating highly dynamic and collaborative

Megacampus real estate in key life science cluster locations to catalyze innovation. From

design to development to the management of our high-quality, sustainable real estate, as

well as our ongoing cultivation of collaborative environments with unique amenities and

events, the Alexandria team has a best-in-class reputation of excellence in life science real

estate. Alexandria’s highly experienced management team includes regional market

directors with leading reputations and long-standing relationships within the life science

communities in their respective innovation clusters. We believe that our experience,

expertise, reputation, and key relationships in the real estate and life science industries

provide Alexandria significant competitive advantages in attracting new business

opportunities.

Alexandria’s executive and senior management team consists of

61 individuals averaging 24 years of real estate experience,

including 13 years with Alexandria. Our executive management

team alone averages 19 years with Alexandria.

EXECUTIVE MANAGEMENT TEAM | ||

Joel S. Marcus | Peter M. Moglia | |

Executive Chairman & Founder | Chief Executive Officer & Chief Investment Officer | |

Daniel J. Ryan | Hunter L. Kass | |

Co-President & Regional Market Director – San Diego | Co-President & Regional Market Director – Greater Boston | |

Marc E. Binda | Lawrence J. Diamond | |

Chief Financial Officer & Treasurer | Co-Chief Operating Officer & Regional Market Director – Maryland | |

Joseph Hakman | Hart Cole | |

Co-Chief Operating Officer & Chief Strategic Transactions Officer | Executive Vice President – Capital Markets/Strategic Operations & Co-Regional Market Director – Seattle | |

Jackie B. Clem | Gary D. Dean | |

General Counsel & Secretary | Executive Vice President – Real Estate Legal Affairs | |

Andres R. Gavinet | Onn C. Lee | |

Chief Accounting Officer | Executive Vice President – Accounting | |

Kristina A. Fukuzaki-Carlson | Madeleine T. Alsbrook | |

Executive Vice President – Business Operations | Executive Vice President – Talent Management | |

| |

Investor Information | |

September 30, 2025 | |

Corporate Headquarters | New York Stock Exchange Trading Symbol | Information Requests | |||

26 North Euclid Avenue | Common stock: ARE | Phone: | (626) 578-0777 | ||

Pasadena, California 91101 | Email: | corporateinformation@are.com | |||

www.are.com | Website: | investor.are.com | |||

Equity Research Coverage |

Alexandria is currently covered by the following research analysts. This list may be incomplete and is subject to change as firms initiate or discontinue coverage of our company. Please note that any opinions, estimates, or forecasts regarding our historical or predicted performance made by these analysts are theirs alone and do not represent opinions, estimates, or forecasts of Alexandria or our management. Alexandria does not by our reference or distribution of the information below imply our endorsement of or concurrence with any opinions, estimates, or forecasts of these analysts. Interested persons may obtain copies of analysts’ reports on their own as we do not distribute these reports. Several of these firms may, from time to time, own our stock and/or hold other long or short positions in our stock and may provide compensated services to us. |

BMO | Cantor Fitzgerald | Deutsche Bank AG | Jefferies | |||

John Kim / Juan Sanabria | Richard Anderson | Tayo Okusanya / Samuel Ohiomah | Joe Dickstein / Katie Elders | |||

(212) 885-4115 / (312) 845-4074 | (929) 441-6927 | (212) 250-9284 / (212) 250-0057 | (212) 778-8771 / (917) 421-1968 | |||

BNP Paribas Exane | CFRA | Evercore ISI | Mizuho Securities USA LLC | |||

Nate Crossett / Monir Koummal | Nathan Schmidt | Steve Sakwa / James Kammert | Vikram Malhotra | |||

(646) 342-1588 / (646) 342-1554 | (646) 517-1144 | (212) 446-9462 / (312) 705-4233 | (212) 282-3827 | |||

BofA Securities | Citigroup Global Markets Inc. | Green Street | RBC Capital Markets | |||

Farrell Granath / Jeff Spector | Nicholas Joseph / Seth Bergey | Dylan Burzinski | Michael Carroll | |||

(646) 855-1351 / (646) 855-1363 | (212) 816-1909 / (212) 816-2066 | (949) 640-8780 | (440) 715-2649 | |||

BTIG, LLC | Citizens | J.P. Morgan Securities LLC | Robert W. Baird & Co. Incorporated | |||

Tom Catherwood / Michael Tompkins | Aaron Hecht / Linda Fu | Anthony Paolone / Ray Zhong | Wesley Golladay / Nicholas Thillman | |||

(212) 738-6140 / (212) 527-3566 | (415) 835-3963 / (415) 869-4411 | (212) 622-6682 / (212) 622-5411 | (216) 737-7510 / (414) 298-5053 | |||

Fixed Income Research Coverage | Rating Agencies | |||||

Barclays Capital Inc. | J.P. Morgan Securities LLC | Moody’s Ratings | S&P Global Ratings | |||

Srinjoy Banerjee / Ishaan Pandya | Mark Streeter / Tyler Schachner | (212) 553-0376 | Michael Souers | |||

(212) 526-3521 / (212) 526-2970 | (212) 834-5086 / (212) 834-2238 | (212) 438-2508 | ||||

CreditSights | Mizuho Securities USA LLC | |||||

Nicholas Moglia | Thierry Perrein | |||||

(212) 340-3886 | (212) 205-7665 | |||||

Financial and Asset Base Highlights | |

September 30, 2025 | |

(Dollars in thousands, except per share amounts) | |

Three Months Ended (unless stated otherwise) | ||||||||||

9/30/25 | 6/30/25 | 3/31/25 | 12/31/24 | 9/30/24 | ||||||

Selected financial data from consolidated financial statements and related information | ||||||||||

Rental revenues | $541,070 | (1) | $553,377 | $552,112 | $566,535 | $579,569 | ||||

Tenant recoveries | $194,779 | $183,902 | $191,063 | $196,714 | $196,175 | |||||

General and administrative expenses | $29,224 | $29,128 | $30,675 | $32,730 | $43,945 | |||||

General and administrative expenses as a percentage of net operating income – trailing 12 months | 5.7% | 6.3% | 6.9% | 7.6% | 8.9% | |||||

Operating margin | 68% | 71% | 70% | 70% | 71% | |||||

Adjusted EBITDA margin | 71% | 71% | 71% | 72% | 70% | |||||

Adjusted EBITDA – quarter annualized | $2,130,008 | $2,174,160 | $2,165,632 | $2,273,480 | $2,219,632 | |||||