Cautionary Language Regarding Forward-Looking Statements

This supplemental information package ("Supplement") contains forward-looking statements and information that are based on our management's current expectations as of the date of this Supplement. Statements that are not historical facts are hereby identified as forward-looking statements. Words such as "Outlook," "guide," "forecast," "estimate," "anticipate," "project," "plan," "intend," "believe," "expect," "likely," "predicted," "positioned," and any variations of these words and similar expressions are intended to identify such forward looking statements. Such statements include plans, projections and estimates regarding (1) demand for data and our towers, (2) cash flow growth (including from discontinued operations), (3) our Outlook for full year 2026, including Free Cash Flow from Discontinued Operations, (4) our business model, strategy and strategic position, and the value thereof, (5) revenues from tenant contracts, (6) expenses from existing ground leases, (7) growth of the U.S. market for towers ownership, (8) levels of commitments under our debt instruments, (9) the impact of Sprint Cancellations and DISH Terminations to our operating and financial results, (10) results from the Fiber Business, and (11) closing of the Fiber Strategic Transaction (as defined below).

Such forward-looking statements are subject to certain risks, uncertainties and assumptions, including, but not limited to, prevailing market conditions. Should one or more of these or other risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those expected. Crown Castle assumes no obligation to update publicly any forward-looking statements, whether as a result of new information, future events or otherwise. More information about potential risk factors which could affect our results is included in our filings with the Securities and Exchange Commission ("SEC"). Our filings with the SEC are available through the SEC website at www.sec.gov or through our investor relations website at investor.crowncastle.com. We use our investor relations website to disclose information about us that may be deemed to be material. We encourage investors, the media and others interested in us to visit our investor relations website from time to time to review up-to-date information or to sign up for e-mail alerts to be notified when new or updated information is posted on the site.

This Supplement contains certain figures, projections and calculations based in part on management's underlying assumptions. Management believes these assumptions are reasonable; however, other reasonable assumptions could provide differing outputs.

The components of forward looking financial information presented herein may not sum due to rounding. In addition, the sum of quarterly historical information presented herein may not agree to year to date historical information provided herein due to rounding. Throughout this document, percentage calculations, which are based on non-rounded dollar values, may not be able to be recalculated using the dollar values included in this document due to the rounding of those dollar values.

Definitions and reconciliations of non-GAAP financial measures, information regarding segment measures and other information are provided in the Appendix to this Supplement.

As used herein, the term "including" and any variation thereof, means "including without limitation." The use of the word "or" herein is not exclusive.

2

Crown Castle Inc.

Fourth Quarter 2025

COMPANY OVERVIEW

OUTLOOK

FINANCIAL

HIGHLIGHTS

CAPITALIZATION OVERVIEW

APPENDIX

COMPANY PROFILE

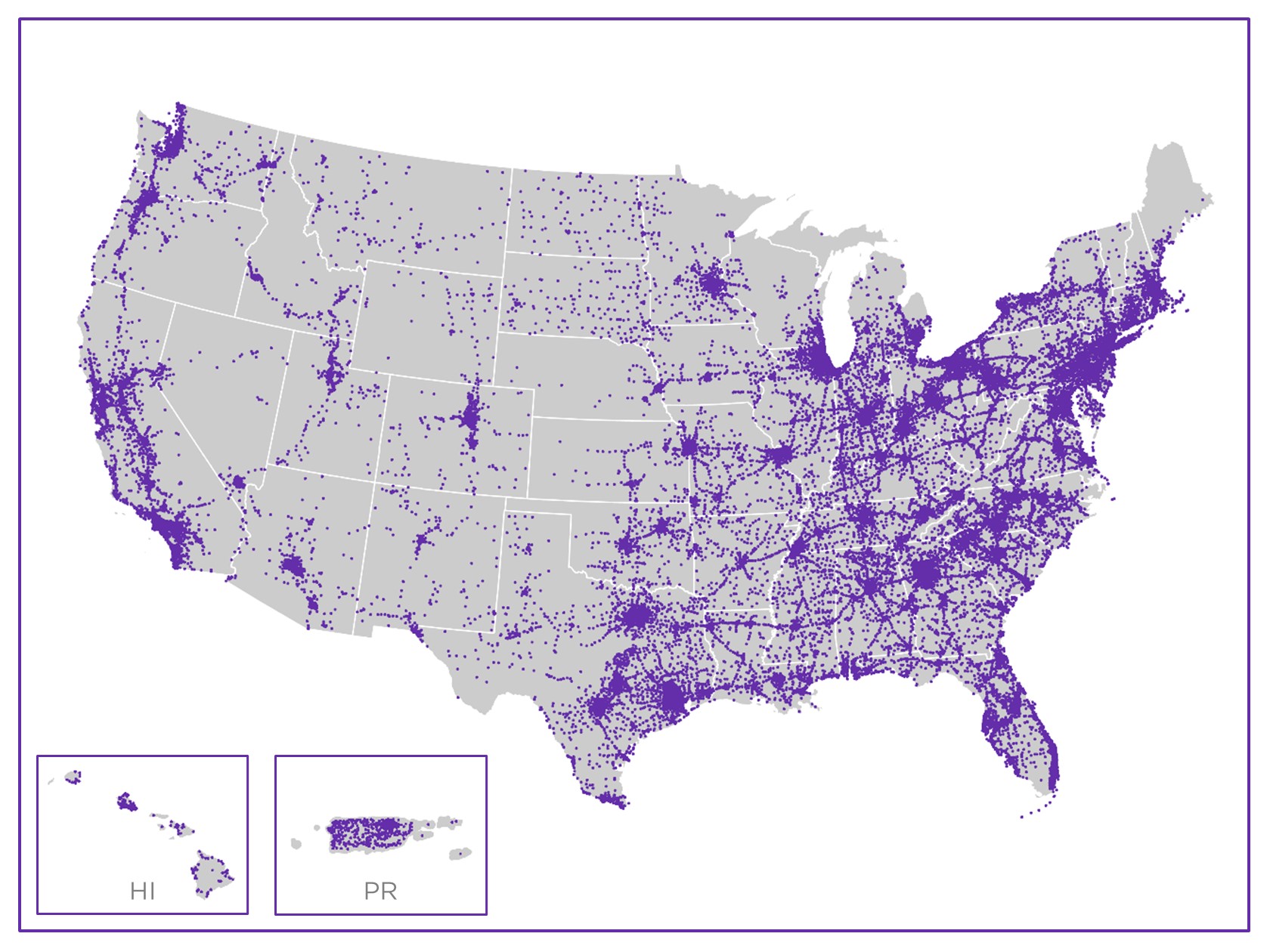

Crown Castle Inc. (to which the terms "Crown Castle," "CCI," "we," "our," "the Company" or "us" as used herein refer) owns, operates and leases shared communications infrastructure that is geographically dispersed throughout the U.S., including (1) approximately 40,000 towers and other structures, such as rooftops (collectively, "towers"), (2) approximately 105,000 small cells on air or under contract and (3) approximately 90,000 route miles of fiber primarily supporting small cells and fiber solutions. We refer to our towers, small cells and fiber assets collectively as "communications infrastructure," and to our customers on our communications infrastructure as "tenants." We provide access, including space or capacity, to our communications infrastructure via long-term contracts in various forms, including lease, license, sublease and service agreements (collectively, "tenant contracts").

Our towers have a significant presence in each of the top 100 basic trading areas, and the majority of our small cells and fiber assets are located in major metropolitan areas, including a presence in most U.S. markets. We seek to increase our site rental revenues by adding more tenants to our existing towers, which we expect to result in significant incremental cash flows due to our low incremental operating costs.

On March 13, 2025, management signed a definitive agreement ("Strategic Fiber Agreement") to sell our small cells and fiber solutions businesses, together with certain supporting assets and personnel ("Fiber Business"), with Zayo Group Holdings Inc. ("Zayo") acquiring the fiber solutions business and EQT Active Core Infrastructure fund ("EQT") acquiring the small cells business ("Strategic Fiber Transaction"). Under the Strategic Fiber Agreement, we will receive $8.5 billion in aggregate, subject to certain closing adjustments. Pending the closing of the Strategic Fiber Transaction, we will continue to operate the Fiber Business in accordance with the Strategic Fiber Agreement.

The results and net assets of the Fiber Business are presented within the financial statements as discontinued operations, with comparable prior periods recast to reflect this change. Following the classification of the Fiber Business as discontinued operations, the Company has one reportable segment that constitutes consolidated results consisting of its towers operations. Unless otherwise noted and other than net income (loss) and net income (loss) per share, all activities and amounts reported below relate to the continuing operations of the Company and exclude activities and amounts related to discontinued operations.

We operate as a Real Estate Investment Trust ("REIT") for U.S. federal income tax purposes.

STRATEGY

As a leading provider of towers in the U.S., our strategy is to create long-term stockholder value via a combination of (1) growing cash flows generated from our existing portfolio of towers, (2) returning a meaningful portion of our cash generated by operating activities to our common stockholders in the form of dividends and share repurchases and (3) investing capital efficiently to grow cash flows. Our strategy is based, in part, on our belief that the U.S. is the most attractive market in the world for towers. We measure our efforts to create "long-term stockholder value" by the combined payments of dividends to stockholders and growth in our per-share results. The key elements of our strategy are to:

•Grow cash flows from our existing towers. We are focused on maximizing the recurring site rental cash flows generated from providing our tenants with long-term access to our towers, which we believe is the core driver of value for our stockholders. Tenant additions or modifications of existing tenant equipment (collectively, "tenant additions") enable our tenants to expand coverage and capacity in order to meet increasing demand for data while generating high incremental returns for our business. We believe our towers provide an efficient and cost-effective solution for our wireless tenants' growing networks that provides an opportunity to generate cash flows and increase stockholder return.

•Return cash generated by operating activities to stockholders in the form of dividends and share repurchases. We believe that distributing a meaningful portion of our cash generated by operating activities appropriately provides stockholders with increased certainty for a portion of expected long-term stockholder value while still allowing us to retain sufficient flexibility to invest in our business and deliver growth. We believe this decision reflects the translation of the high-quality, long-term contractual cash flows of our business into stable capital returns to stockholders.

•Invest capital efficiently to grow cash flows. In addition to adding tenants to our existing towers, we seek to invest our available capital, including the net cash generated by our operating activities and external financing sources, in a manner that will increase long-term stockholder value. These investments include acquisition of land interests, making improvements and structural enhancements to our existing towers, and constructing and acquiring new towers that we expect will generate future cash flow growth and attractive long-term returns by adding tenants to those assets over time.

Our strategy to create long-term stockholder value is based on our belief that there will be considerable future demand for our towers based on the location of our assets and the rapid and continuing growth in the demand for data. We believe that such demand for our towers will continue, will result in growth of our cash flows due to tenant additions on our existing towers, and will create other growth opportunities for us, such as demand for newly constructed or acquired towers, as described above. Further, we seek to augment the long-term value creation associated with growing our recurring site rental cash flows by offering certain ancillary site development services.

3

Crown Castle Inc.

Fourth Quarter 2025

COMPANY OVERVIEW

OUTLOOK

FINANCIAL

HIGHLIGHTS

CAPITALIZATION OVERVIEW

APPENDIX

GENERAL COMPANY INFORMATION

Principal executive offices

8020 Katy Freeway, Houston, TX 77024

Common shares trading symbol

CCI

Stock exchange listing

New York Stock Exchange

Fiscal year ending date

December 31

Fitch - Long-term Issuer Default Rating

BBB+

Moody’s - Long-term Corporate Family Rating

Baa3

Standard & Poor’s - Long-term Local Issuer Credit Rating

BBB

Note: These credit ratings may not reflect the potential risks relating to the structure or trading of the Company’s securities and are provided solely for informational purposes. Credit ratings are not recommendations to buy, sell or hold any security, and may be revised or withdrawn at any time by the issuing organization in its sole discretion. The Company does not undertake any obligation to maintain the ratings or to advise of any change in the ratings. Each agency’s rating should be evaluated independently of any other agency’s rating. An explanation of the significances of the ratings can be obtained from each of the ratings agencies.

TOWER ASSET PORTFOLIO FOOTPRINT

HISTORICAL COMMON STOCK DATA

Three Months Ended

(in millions, except per share amounts)

12/31/24

3/31/25

6/30/25

9/30/25

12/31/25

High price(a)

$

112.14

$

103.85

$

105.66

$

113.18

$

99.35

Low price(a)

$

84.52

$

80.05

$

88.02

$

89.17

$

84.21

Period end closing price(b)

$

86.31

$

100.78

$

100.40

$

95.36

$

88.87

Dividends paid per common share

$

1.57

$

1.57

$

1.06

$

1.06

$

1.06

Volume weighted average price for the period(a)

$

96.68

$

90.59

$

97.91

$

98.81

$

91.00

Common shares outstanding, at period end

435

435

435

435

435

Market value of outstanding common shares, at period end(c)

$

37,514

$

43,884

$

43,721

$

41,529

$

38,702

(a)Based on the sales price, adjusted for common stock dividends, as reported by Bloomberg.

(b)Based on the period end closing price, adjusted for common stock dividends, as reported by Bloomberg.

(c)Calculated as the product of (1) common shares outstanding, at period end and (2) period end closing price, adjusted for common stock dividends, as reported by Bloomberg.

4

Crown Castle Inc.

Fourth Quarter 2025

COMPANY OVERVIEW

OUTLOOK

FINANCIAL

HIGHLIGHTS

CAPITALIZATION OVERVIEW

APPENDIX

EXECUTIVE MANAGEMENT TEAM

Name

Position

Age

Years with Company

Christian H. Hillabrant

President and Chief Executive Officer

60

<1

Sunit Patel

Executive Vice President and Chief Financial Officer

64

<1

Catherine Piche

Executive Vice President and Chief Operating Officer - Towers

55

13(a)

Christopher D. Levendos

Executive Vice President and Chief Operating Officer - Fiber

58

7

Edward B. Adams, Jr.

Executive Vice President and General Counsel

57

9

Daniel K. Schlanger

Executive Vice President and Chief Transformation Officer

52

9

BOARD OF DIRECTORS

Name

Position

Committees

Age

Years as Director

P. Robert Bartolo

Chair

Nominating and Governance, Finance, Fiber Review

54

11

Jason Genrich

Director

Finance, Fiber Review

38

2

Andrea J. Goldsmith

Director

Compensation and Human Capital

61

7

Christian H. Hillabrant

Director

60

<1

Tammy K. Jones

Director

Audit, Nominating and Governance, Finance

60

5

Kevin T. Kabat

Director

Compensation and Human Capital, Nominating and Governance

68

2

Anthony J. Melone

Director

Audit, Nominating and Governance, Fiber Review

65

10

Katherine Motlagh

Director

Audit, Compensation and Human Capital, Finance

51

<1

Kevin A. Stephens

Director

Audit, Compensation and Human Capital, Fiber Review

64

5

Matthew Thornton III

Director

Audit, Compensation and Human Capital, Nominating and Governance

67

5

RESEARCH COVERAGE

Equity Research

Bank of America

Michael Funk

(646) 855-5664

Barclays Brendan Lynch (212) 526-9428

BMO Capital Markets Ari Klein (212) 885-4103

Citigroup Michael Rollins (212) 816-1116

Goldman Sachs

Jim Schneider

(212) 357-2929

Green Street David Guarino (949) 640-8780

HSBC

Luigi Minerva

(207) 991-6928

Jefferies Jonathan Petersen (212) 284-1705

JMP Securities

Greg Miller

(212) 699-2917

JPMorgan

Richard Choe

(212) 622-6708

KeyBanc Brandon Nispel (503) 821-3871

MoffettNathanson Nick Del Deo (212) 519-0025

Morgan Stanley

Benjamin Swinburne

(212) 761-7527

New Street Research Jonathan Chaplin (212) 921-9876

Raymond James Ric Prentiss (727) 567-2567

RBC Capital Markets Jonathan Atkin (415) 633-8589

Scotiabank

Maher Yaghi

(437) 995-5548

TD Cowen

Michael Elias

(646) 562-1358

UBS Batya Levi (212) 713-8824

Wells Fargo Eric Luebchow (312) 630-2386

Wolfe Research Andrew Rosivach (646) 582-9350

Rating Agencies

Fitch

Jeff Danforth

(312) 368-5447

Moody’s

Ranjini Venkatesan

(212) 553-3828

Standard & Poor’s

Allyn Arden

(212) 438-7832

(a)Includes credit for prior service with the Company prior to Ms. Piche's reappointment as Executive Vice President and Chief Operating Officer - Towers of the Company effective October 28, 2024.

5

Crown Castle Inc.

Fourth Quarter 2025

COMPANY OVERVIEW

OUTLOOK

FINANCIAL

HIGHLIGHTS

CAPITALIZATION OVERVIEW

APPENDIX

OUTLOOK

(in millions, except per share amounts)

Full Year 2026 Outlook(a)

Site rental billings(b)

$3,800

to

$3,830

Amortization of prepaid rent

65

to

95

Straight-lined revenues

(75)

to

(45)

Other revenues

15

to

15

Site rental revenues

3,828

to

3,873

Site rental costs of operations(c)

978

to

1,023

Services and other gross margin

90

to

120

Net income (loss)(d)

640

to

920

Net income (loss) per share—diluted(d)

1.48

to

2.12

Adjusted EBITDA(b)

2,665

to

2,715

Depreciation, amortization and accretion

627

to

722

Interest expense and amortization of deferred financing costs, net(e)

832

to

877

Income (loss) from discontinued operations, net of tax(f)

(360)

to

(80)

FFO(b)

1,640

to

1,670

AFFO(b)

1,895

to

1,945

AFFO per share(b)

$4.38

to

$4.49

(a)As issued on February 4, 2026.

(b)See "Non-GAAP Measures and Other Information" for further information and reconciliation of non-GAAP financial measures to net income (loss), including on a per share basis, and for definition of site rental billings.

(c)Exclusive of depreciation, amortization and accretion.

(d)Includes contribution from discontinued operations through June 30, 2026.

(e)See our reconciliation of "Outlook for Components of Interest Expense" for a discussion of non-cash interest expense.

(f)Represents expected results from the Fiber Business, including the estimated loss on disposal, through June 30, 2026.

6

Crown Castle Inc.

Fourth Quarter 2025

COMPANY OVERVIEW

OUTLOOK

FINANCIAL

HIGHLIGHTS

CAPITALIZATION OVERVIEW

APPENDIX

OUTLOOK FOR COMPONENTS OF CHANGES IN SITE RENTAL REVENUES

(dollars in millions; totals may not sum due to rounding)

Full Year 2026 Outlook(a)

Components of changes in site rental revenues:

Prior year site rental billings excluding site rental billings to DISH(b)

$3,701

Prior year site rental billings to DISH(b)

222

Prior year site rental billings(b)

$3,923

Core leasing activity(b)

60

to

70

Escalators

95

to

105

Non-renewals(b)

(35)

to

(25)

Other billings(b)

(5)

to

(5)

Organic Contribution to Site Rental Billings as Adjusted for Impact of Sprint Cancellations and DISH Terminations(b)

115

to

145

Non-renewals associated with Sprint Cancellations(b)

(20)

to

(20)

Non-renewals associated with DISH Terminations(b)

(220)

to

(220)

Organic Contribution to Site Rental Billings(b)

(125)

to

(95)

Straight-lined revenues

(75)

to

(45)

Amortization of prepaid rent

65

to

95

Other revenues

15

to

15

Acquisitions(c)

—

Total site rental revenues

$3,828

to

$3,873

Year-over-year changes in revenues:(d)

Site rental revenues as a percentage of prior year site rental revenues

(4.9)%

Organic Contribution to Site Rental Billings as Adjusted for Impact of Sprint Cancellations and DISH Terminations as a percentage of prior year site rental billings excluding site rental billings to DISH(b)

3.5%

Organic Contribution to Site Rental Billings as Adjusted for Impact of Sprint Cancellations and DISH Terminations as a percentage of prior year site rental billings(b)

3.3%

Organic Contribution to Site Rental Billings as a percentage of prior year site rental billings(b)

(2.8)%

OUTLOOK FOR COMPONENTS OF INTEREST EXPENSE

(in millions)

Full Year 2026 Outlook(a)

Interest expense on debt obligations

$815

to

$855

Amortization of deferred financing costs and adjustments on long-term debt

25

to

35

Capitalized interest

(15)

to

(5)

Interest expense and amortization of deferred financing costs, net

$832

to

$877

(a)As issued on February 4, 2026.

(b)See our definitions of site rental billings, core leasing activity, non-renewals, other billings, Sprint Cancellations, DISH Terminations, Organic Contribution to Site Rental Billings and Organic Contribution to Site Rental Billings as Adjusted for Impact of Sprint Cancellations and DISH Terminations in "Non-GAAP Measures and Other Information."

(c)Represents the contribution from recent acquisitions. The financial impact of recent acquisitions is excluded from Organic Contribution to Site Rental Billings, including as Adjusted for Impact of Sprint Cancellations and DISH Terminations, until the one-year anniversary of such acquisitions.

(d)Calculated based on midpoint of full year 2026 Outlook, where applicable.

7

Crown Castle Inc.

Fourth Quarter 2025

COMPANY OVERVIEW

OUTLOOK

FINANCIAL

HIGHLIGHTS

CAPITALIZATION OVERVIEW

APPENDIX

SUMMARY FINANCIAL HIGHLIGHTS(a)

2024

2025

Twelve Months Ended December 31,

(in millions, except per share amounts; totals may not sum due to rounding)

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

2024

2025

Net revenues:

Site rental

Site rental billings(b)

$

966

$

967

$

995

$

1,006

$

964

$

961

$

996

$

1,002

$

3,934

$

3,923

Amortization of prepaid rent

41

39

39

40

25

23

23

28

160

98

Straight-lined revenues

57

54

28

20

19

20

(11)

(15)

160

12

Other revenues

4

4

4

4

4

4

4

4

15

16

Total site rental

1,068

1,064

1,066

1,070

1,011

1,008

1,012

1,019

4,268

4,049

Services and other

46

43

54

49

50

52

60

53

192

215

Net revenues

$

1,114

$

1,107

$

1,120

$

1,119

$

1,061

$

1,060

$

1,072

$

1,072

$

4,460

$

4,264

Select operating expenses:

Costs of operations(c)

Site rental exclusive of straight-lined expenses

$

227

$

233

$

232

$

227

$

225

$

236

$

235

$

238

$

920

$

934

Straight-lined expenses

16

16

15

15

15

15

15

14

63

58

Total site rental

243

249

247

242

240

251

250

252

983

992

Services and other

29

25

27

26

28

27

30

29

107

113

Total costs of operations

272

274

274

268

268

278

280

281

1,090

1,105

Selling, general and administrative

$

114

$

136

$

93

$

92

$

93

$

99

$

97

$

94

$

435

$

383

Net income (loss)

$

311

$

251

$

303

$

(4,768)

$

(464)

$

291

$

323

$

294

$

(3,903)

$

444

Adjusted EBITDA(b)

754

727

777

777

722

705

718

718

3,035

2,863

Depreciation, amortization and accretion

191

180

181

184

177

175

167

170

736

690

Interest expense and amortization of deferred financing costs, net

226

230

236

240

236

243

247

246

(932)

972

FFO(b)

478

436

466

483

451

429

443

442

1,863

1,764

AFFO(b)

$

484

$

449

$

525

$

523

$

479

$

444

$

490

$

489

$

1,980

$

1,904

Weighted-average common shares outstanding— diluted

435

435

436

435

436

437

437

437

434

437

Net income (loss) per share—diluted

$

0.71

$

0.58

$

0.70

$

(10.97)

$

(1.07)

$

0.67

$

0.74

$

0.67

$

(8.98)

$

1.01

AFFO per share(b)

$

1.11

$

1.03

$

1.20

$

1.20

$

1.10

$

1.02

$

1.12

$

1.12

$

4.55

$

4.36

(a)With the exception of net income (loss) and net income (loss) per share-diluted, amounts are exclusive of the Fiber Business, which is presented in discontinued operations.

(b)See "Non-GAAP Measures and Other Information" for our definition of site rental billings and for further information and reconciliation of non-GAAP financial measures to net income (loss), including on a per share basis.

(c)Exclusive of depreciation, amortization and accretion, which are shown separately.

8

Crown Castle Inc.

Fourth Quarter 2025

COMPANY OVERVIEW

OUTLOOK

FINANCIAL

HIGHLIGHTS

CAPITALIZATION OVERVIEW

APPENDIX

COMPONENTS OF CHANGES IN SITE RENTAL REVENUES(a)

2024

2025

Twelve Months Ended December 31,

(dollars in millions; totals may not sum due to rounding)

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

2024

2025

Components of changes in site rental revenues:

Prior year site rental billings(b)

$

923

$

922

$

952

$

966

$

966

$

966

$

995

$

1,006

$

3,763

$

3,934

Core leasing activity(b)

28

28

27

28

28

28

33

29

110

118

Escalators

23

23

23

24

24

24

24

25

92

96

Non-renewals(b)

(8)

(7)

(8)

(8)

(7)

(7)

(7)

(7)

(31)

(27)

Other billings(b)

—

2

—

(4)

3

—

2

—

(2)

5

Organic Contribution to Site Rental Billings as Adjusted for Impact of Sprint Cancellations(b)

43

45

43

40

49

45

52

47

170

193

Non-renewals associated with Sprint Cancellations(b)

—

—

—

—

(51)

(51)

(51)

(51)

—

(204)

Organic Contribution to Site Rental Billings(b)

43

45

43

40

(2)

(6)

1

(4)

170

(11)

Straight-lined revenues

57

54

28

20

19

20

(11)

(15)

160

12

Amortization of prepaid rent

41

39

39

40

25

23

23

28

160

98

Other revenues

4

4

4

4

4

4

4

4

15

16

Total site rental revenues

$

1,068

$

1,064

$

1,066

$

1,070

$

1,011

$

1,008

$

1,012

$

1,019

$

4,268

$

4,049

Year-over-year changes in revenues:

Site rental revenues as a percentage of prior year site rental revenues

(1.2)

%

(1.5)

%

(0.8)

%

(0.8)

%

(5.3)

%

(5.3)

%

(5.1)

%

(4.8)

%

(1.0)

%

(5.1)

%

Organic Contribution to Site Rental Billings as Adjusted for Impact of Sprint Cancellations as a percentage of prior year site rental billings(b)

4.6

%

4.8

%

4.5

%

4.1

%

5.1

%

4.7

%

5.2

%

4.7

%

4.5

%

4.9

%

Organic Contribution to Site Rental Billings as a percentage of prior year site rental billings(b)

4.6

%

4.8

%

4.5

%

4.1

%

(0.2)

%

(0.6)

%

0.1

%

(0.4)

%

4.5

%

(0.3)

%

(a)The financial impact of the Fiber Business revenues is excluded as these amounts are presented within discontinued operations.

(b)See our definitions of site rental billings, core leasing activity, non-renewals, other billings, Sprint Cancellations, Organic Contribution to Site Rental Billings and Organic Contribution to Site Rental Billings as Adjusted for Impact of Sprint Cancellations in "Non-GAAP Measures and Other Information."

9

Crown Castle Inc.

Fourth Quarter 2025

COMPANY OVERVIEW

OUTLOOK

FINANCIAL

HIGHLIGHTS

CAPITALIZATION OVERVIEW

APPENDIX

SUMMARY OF CAPITAL EXPENDITURES(a)

2024

2025

Twelve Months Ended December 31,

(dollars in millions; totals may not sum due to rounding)

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

2024

2025

Discretionary capital expenditures:

Tower improvements and other capital projects

$

26

$

20

$

21

$

18

$

15

$

17

$

20

$

18

$

84

$

72

Purchases of land interests

13

11

14

20

18

16

16

27

58

77

Total discretionary capital expenditures

39

31

35

38

33

33

36

45

142

149

Sustaining capital expenditures

8

9

6

12

7

7

6

14

34

33

Total capital expenditures

47

40

41

50

40

40

42

59

176

182

Less: Prepaid rent additions(b)

12

8

13

12

10

11

11

11

45

43

Capital expenditures less prepaid rent additions

$

35

$

32

$

28

$

38

$

30

$

29

$

31

$

48

$

131

$

139

PORTFOLIO HIGHLIGHTS(c)

(as of December 31, 2025)

Number of towers (in thousands)(d)

40

Average number of tenants per tower

2.4

Remaining contracted tenant receivables (in billions)(e)

$

27

Weighted average remaining tenant contract term (years)(e)(f)

6

Percent of towers in the Top 50 / 100 Basic Trading Areas

56% / 71%

Percent of ground leased / owned(g)

57% / 43%

Weighted average maturity of ground leases (years)(g)(h)

35

(a)See our definitions of discretionary capital expenditures and sustaining capital expenditures in "Non-GAAP Measures and Other Information." Excludes amounts related to the Fiber Business, which are presented in discontinued operations.

(b)Reflects up-front consideration from long-term tenant contracts (commonly referred to as prepaid rent) that are amortized and recognized as revenue over the associated estimated lease term in accordance with GAAP.

(c)Reflects amounts related to DISH. See the Company's Form 8-K filed January 12, 2026 for additional information.

(d)Excludes third-party land interests.

(e)Relates to continuing operations only and excludes renewal terms at tenants' option.

(f)Weighted by site rental revenues.

(g)Weighted by site rental gross margin exclusive of straight-lined revenues, amortization of prepaid rent and straight-lined expenses.

(h)Includes all renewal terms at the Company's option.

10

Crown Castle Inc.

Fourth Quarter 2025

COMPANY OVERVIEW

OUTLOOK

FINANCIAL

HIGHLIGHTS

CAPITALIZATION OVERVIEW

APPENDIX

CONSOLIDATED RETURN ON INVESTED CAPITAL(a)(b)

(as of December 31, 2025; dollars in millions)

Q4 2025 LQA

Q4 2024 LQA

Adjusted EBITDA(c)

$

2,872

$

3,108

Cash taxes (paid) refunded

(13)

(9)

Adjusted EBITDA less cash taxes paid

$

2,859

$

3,099

Historical gross investment in property and equipment(d)

$

16,979

$

16,838

Historical gross investment in site rental contracts and tenant relationships

4,590

4,589

Historical gross investment in goodwill

5,127

5,127

Consolidated Invested Capital(a)

$

26,696

$

26,554

Consolidated Return on Invested Capital(a)

10.7

%

11.7

%

CASH YIELD ON INVESTED CAPITAL(a)(b)(e)

(as of December 31, 2025; dollars in millions)

Q4 2025 LQA

Q4 2024 LQA

Adjusted Site Rental Gross Margin(c)

$

3,088

$

3,336

Less: Amortization of prepaid rent

(110)

(160)

Add (less): Straight-lined revenues

60

(80)

Add: Straight-lined expenses

43

44

Numerator

$

3,081

$

3,140

Net investment in property and equipment(f)

$

13,652

$

13,547

Investment in site rental contracts and tenant relationships

4,590

4,589

Investment in goodwill(g)

5,351

5,351

Net Invested Capital(a)

$

23,593

$

23,487

Cash Yield on Invested Capital(a)

13.1

%

13.4

%

(a)See "Non-GAAP Measures and Other Information" for further information on, and our definitions of, Consolidated Return on Invested Capital, Consolidated Invested Capital, Cash Yield on Invested Capital, and Net Invested Capital.

(b)Excludes amounts related to the Fiber Business, which are presented in discontinued operations.

(c)See "Non-GAAP Measures and Other Information" for further information and reconciliation of non-GAAP financial measures to net income (loss).

(d)Historical gross investment in property and equipment excludes the impact of construction in process.

(e)Section is equivalent to the historically reported Tower Segment Cash Yield on Invested Capital.

(f)Net investment in property and equipment excludes the impact of construction in process and non-productive assets (such as information technology assets and buildings) and is reduced by the amount of prepaid rent received from tenants.

(g)Investment in goodwill excludes the impact of certain assets and liabilities recorded in connection with acquisitions.

11

Crown Castle Inc.

Fourth Quarter 2025

COMPANY OVERVIEW

OUTLOOK

FINANCIAL

HIGHLIGHTS

CAPITALIZATION OVERVIEW

APPENDIX

TENANT OVERVIEW(a)

(as of December 31, 2025)

Percentage of Q4 2025 LQA Site Rental Revenues

Weighted Average Current Term Remaining(c)

T-Mobile

40%

7

AT&T

27%

3

Verizon

22%

6

All Others Combined

11%

8

Total / Weighted Average

100%

6

ANNUALIZED RENTAL CASH PAYMENTS AT TIME OF RENEWAL(a)(b)(d)

Years Ending December 31,

(as of December 31, 2025; in millions)

2026

2027

2028

2029

2030

T-Mobile

$

26

$

33

$

27

$

24

$

26

AT&T

16

13

775

238

107

Verizon

5

7

31

48

71

All Others Combined

48

37

28

44

59

Total

$

95

$

90

$

861

$

354

$

263

PROJECTED REVENUES FROM TENANT CONTRACTS ASSOCIATED WITH ACTIVE LICENSES(a)(b)(e)

Years Ending December 31,

(as of December 31, 2025; in millions)

2026

2027

2028

2029

2030

Components of site rental revenues:

Site rental billings(f)

$

3,817

$

3,925

$

4,044

$

4,165

$

4,291

Amortization of prepaid rent

77

65

43

27

16

Straight-lined revenues

(58)

(171)

(236)

(207)

(282)

Site rental revenues

$

3,836

$

3,819

$

3,851

$

3,985

$

4,025

(a)Excludes amounts related to the Fiber Business, which are presented in discontinued operations.

(b)Excludes amounts associated with DISH. See the Company's Form 8-K filed January 12, 2026 for additional information.

(c)Weighted by site rental revenues and excludes renewals at the tenants' option.

(d)Reflects lease renewals by year by tenant; dollar amounts represent annualized cash site rental revenues from assumed renewals or extensions as reflected in "Projected Revenues from Tenant Contracts Associated with Active Licenses" below.

(e)Based on tenant licenses in place and active as of December 31, 2025. All tenant licenses are assumed to renew for a new term no later than the respective current term end date, and as such, projected revenues do not reflect the impact of estimated annual churn. CPI-linked tenant contracts are assumed to escalate at 3% per annum.

(f)See "Non-GAAP Measures and Other Information" for our definition of site rental billings.

12

Crown Castle Inc.

Fourth Quarter 2025

COMPANY OVERVIEW

OUTLOOK

FINANCIAL

HIGHLIGHTS

CAPITALIZATION OVERVIEW

APPENDIX

PROJECTED EXPENSES FROM EXISTING GROUND LEASES(a)(b)

Years Ending December 31,

(as of December 31, 2025; in millions)

2026

2027

2028

2029

2030

Components of ground lease expenses:

Ground lease expenses exclusive of straight-lined expenses

$

690

$

703

$

721

$

740

$

761

Straight-lined expenses

47

34

24

13

2

Ground lease expenses

$

737

$

737

$

745

$

753

$

763

SUMMARY OF TOWER PORTFOLIO BY VINTAGE(c)

(as of December 31, 2025; dollars in thousands)

Acquired and Built 2006 and Prior

Acquired and Built 2007 to Present

Cash yield(d)

21

%

10

%

Number of tenants per tower

2.9

2.2

Last quarter annualized average cash site rental revenue per tower(e)

$

139

$

83

Last quarter annualized average site rental gross cash margin per tower(f)

$

119

$

58

Net invested capital per tower(g)

$

567

$

595

Number of towers

11,157

28,647

GROUND INTEREST OVERVIEW

(as of December 31, 2025; dollars in millions)

LQA Cash Site Rental Revenues(e)

Percentage of LQA Cash Site Rental Revenues(e)

LQA Site Rental Gross Cash Margin(f)

Percentage of LQA Site Rental Gross Cash Margin(f)

Number of Towers(h)

Percentage of Towers

Weighted Average Term Remaining (by years)(i)

Less than 10 years

$

433

11

%

$

236

8

%

5,360

14

%

10 to 20 years

$

575

14

%

$

362

12

%

6,106

15

%

Greater than 20 years

$

1,558

40

%

$

1,121

37

%

16,293

41

%

Total leased

$

2,566

65

%

$

1,719

57

%

27,759

70

%

35

Owned

$

1,364

35

%

$

1,280

43

%

12,045

30

%

Total / Average

$

3,930

100

%

$

2,999

100

%

39,804

100

%

(a)Based on existing ground leases as of December 31, 2025. CPI-linked contracts are assumed to escalate at 3% per annum.

(b)Excludes amounts related to the Fiber Business, which are presented in discontinued operations.

(c)All tower portfolio figures are calculated exclusively for the Company's towers and rooftops and do not give effect to other activities.

(d)Cash yield is calculated as last quarter annualized site rental gross margin, exclusive of straight-lined revenues, amortization of prepaid rent, and straight-lined expenses, divided by invested capital net of the amount of prepaid rent received from tenants.

(e)Exclusive of straight-lined revenues and amortization of prepaid rent.

(f)Exclusive of straight-lined revenues, amortization of prepaid rent and straight-lined expenses.

(g)Reflects gross total assets (including incremental capital invested by the Company since time of acquisition or construction completion), less any prepaid rent. Inclusive of invested capital related to land at the tower site.

(h)Excludes third-party land interests.

(i)Includes all renewal terms at the Company's option and weighted by site rental gross margin exclusive of straight-lined revenues, amortization of prepaid rent and straight-lined expenses.

13

Crown Castle Inc.

Fourth Quarter 2025

COMPANY OVERVIEW

OUTLOOK

FINANCIAL

HIGHLIGHTS

CAPITALIZATION OVERVIEW

APPENDIX

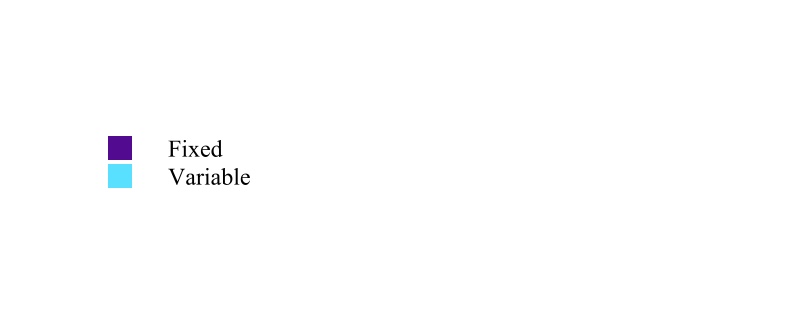

CAPITALIZATION OVERVIEW

(as of December 31, 2025; dollars in millions)

Face Value(a)

Fixed vs. Variable

Interest Rate(b)

Maturity

Cash and cash equivalents and restricted cash and cash equivalents(c)

$

274

Senior Secured Notes, Series 2009-1, Class A-2(d)

26

Fixed

9.0%

Aug. 2029

Senior Secured Tower Revenue Notes, Series 2018-2(e)

750

Fixed

4.2%

July 2048

Installment purchase liabilities and finance leases(f)

258

Fixed

Various

Various

Total secured debt

$

1,034

4.4%

2016 Revolver(g)

945

Variable

5.4%

July 2027

2016 Term Loan A(h)

1,056

Variable

5.0%

July 2027

Commercial Paper Notes(i)

1,931

Variable

4.2%

Various

4.450% Senior Notes

900

Fixed

4.5%

Feb. 2026

3.700% Senior Notes

750

Fixed

3.7%

June 2026

1.050% Senior Notes

1,000

Fixed

1.1%

July 2026

2.900% Senior Notes

750

Fixed

2.9%

Mar. 2027

4.000% Senior Notes

500

Fixed

4.0%

Mar. 2027

3.650% Senior Notes

1,000

Fixed

3.7%

Sept. 2027

5.000% Senior Notes

1,000

Fixed

5.0%

Jan. 2028

3.800% Senior Notes

1,000

Fixed

3.8%

Feb. 2028

4.800% Senior Notes

600

Fixed

4.8%

Sept. 2028

4.300% Senior Notes

600

Fixed

4.3%

Feb. 2029

5.600% Senior Notes

750

Fixed

5.6%

June 2029

4.900% Senior Notes

550

Fixed

4.9%

Sept. 2029

3.100% Senior Notes

550

Fixed

3.1%

Nov. 2029

3.300% Senior Notes

750

Fixed

3.3%

July 2030

2.250% Senior Notes

1,100

Fixed

2.3%

Jan. 2031

2.100% Senior Notes

1,000

Fixed

2.1%

Apr. 2031

2.500% Senior Notes

750

Fixed

2.5%

July 2031

5.100% Senior Notes

750

Fixed

5.1%

May 2033

5.800% Senior Notes

750

Fixed

5.8%

Mar. 2034

5.200% Senior Notes

700

Fixed

5.2%

Sept. 2034

2.900% Senior Notes

1,250

Fixed

2.9%

Apr. 2041

4.750% Senior Notes

350

Fixed

4.8%

May 2047

5.200% Senior Notes

400

Fixed

5.2%

Feb. 2049

4.000% Senior Notes

350

Fixed

4.0%

Nov. 2049

4.150% Senior Notes

500

Fixed

4.2%

July 2050

3.250% Senior Notes

900

Fixed

3.3%

Jan. 2051

Total unsecured debt

$

23,432

3.9%

Net Debt(j)

$

24,192

3.9%

Market Capitalization(k)

38,702

Firm Value(l)

$

62,894

(a)Net of required principal amortizations.

(b)Represents the weighted-average stated interest rate, as applicable, exclusive of finance leases and other obligations.

(c)As of December 31, 2025, excludes $34 million associated with discontinued operations relating to the Fiber Business.

(d)The Senior Secured Notes, 2009-1, Class A-2 principal amortizes over a period ending in August 2029.

(e)If the $750 million aggregate principal amount of 4.241% senior secured tower revenue notes ("Tower Revenue Notes, Series 2018-2") is not paid in full on or prior to July 2028, the anticipated repayment date, then the Excess Cash Flow (as defined in the indenture) of the issuers of such notes will be used to repay the principal, and additional interest (of approximately 5% per annum) will accrue on such notes. The Tower Revenue Notes, Series 2018-2 are prepayable at par if voluntarily repaid within eighteen months of the anticipated repayment date; earlier prepayment may require additional consideration.

(f)As of December 31, 2025, reflects $5 million in finance lease obligations (primarily related to vehicles), which excludes $29 million associated with discontinued operations.

(g)As of December 31, 2025, the undrawn availability under the $7.0 billion 2016 Revolver was $6.0 billion. The Company pays a commitment fee on the undrawn available amount, which as of December 31, 2025 ranged from 0.080% to 0.300%, based on the Company's senior unsecured debt rating, per annum.

(h)The 2016 Term Loan A principal amortizes over a period ending in July 2027.

(i)As of December 31, 2025, the Company had $69 million available for issuance under the $2.0 billion unsecured commercial paper program ("CP Program"). The maturities of the Commercial Paper Notes ("CP Notes"), when outstanding, may vary but may not exceed 397 days from the date of issue.

(j)See "Non-GAAP Measures and Other Information" for further information on, and our definition and calculation of, Net Debt.

(k)Market capitalization calculated based on $88.87 closing price and 435 million shares outstanding as of December 31, 2025.

(l)Represents the sum of Net Debt and market capitalization. See "Non-GAAP Measures and Other Information" for further information on, and our definition and calculation of, Net Debt.

14

Crown Castle Inc.

Fourth Quarter 2025

COMPANY OVERVIEW

OUTLOOK

FINANCIAL HIGHLIGHTS

CAPITALIZATION OVERVIEW

APPENDIX

DEBT MATURITY OVERVIEW(a)(b)

(as of December 31, 2025; in millions)

(a)Where applicable, maturities reflect the anticipated repayment date of the Tower Revenue Notes, Series 2018-2; excludes finance leases and other obligations; amounts presented at face value, net of required principal amortizations and repurchases held at the Company.

(b)The $1.9 billion outstanding in CP Notes have been excluded from this overview. Amounts available under the CP Program may be borrowed, repaid and re-borrowed from time to time. We intend to maintain available commitments under our 2016 Revolver in an amount at least equal to the amount of CP Notes outstanding at any point in time.

15

Crown Castle Inc.

First Quarter 2025

COMPANY OVERVIEW

OUTLOOK

FINANCIAL

HIGHLIGHTS

CAPITALIZATION OVERVIEW

APPENDIX

LIQUIDITY OVERVIEW(a)

(in millions)

December 31, 2025

Cash and cash equivalents, and restricted cash and cash equivalents(b)(c)

$

274

Undrawn 2016 Revolver availability(d)

6,015

Total debt and other obligations (current and non-current)(c)(e)

24,337

Total equity (deficit)

(1,635)

SUMMARY OF MAINTENANCE AND FINANCIAL COVENANTS

Debt

Borrower / Issuer

Covenant(f)

Covenant Level Requirement

As of December 31, 2025

Maintenance Financial Covenants(g)

2016 Credit Facility

CCI

Total Net Leverage Ratio

≤ 6.50x

5.9x

2016 Credit Facility

CCI

Total Senior Secured Leverage Ratio

≤ 3.50x

0.2x

2016 Credit Facility

CCI

Consolidated Interest Coverage Ratio(h)

N/A

N/A

Financial covenants requiring excess cash flows to be deposited in a cash trap reserve account and not released

Tower Revenue Notes, Series 2018-2

Crown Castle Towers LLC and its Subsidiaries

Debt Service Coverage Ratio

> 1.75x

(i)

30.4x

2009 Securitized Notes

Pinnacle Towers Acquisition Holdings LLC and its Subsidiaries

Debt Service Coverage Ratio

> 1.30x

(i)

42.8x

Financial covenants restricting ability of relevant issuer to issue additional notes under the applicable indenture

Tower Revenue Notes, Series 2018-2

Crown Castle Towers LLC and its Subsidiaries

Debt Service Coverage Ratio

≥ 2.00x

(j)

30.4x

2009 Securitized Notes

Pinnacle Towers Acquisition Holdings LLC and its Subsidiaries

Debt Service Coverage Ratio

≥ 2.34x

(j)

42.8x

(a)In addition, we have the following sources of liquidity:

i.In March 2024, we established an at-the-market stock offering program ("ATM Program") through which we may, from time to time, issue and sell shares of our common stock having an aggregate gross sales price of up to $750 million to or through sales agents. No shares of common stock have been sold under the ATM Program.

ii.In April 2019, we established a CP Program through which we may issue short term, unsecured CP Notes. Amounts available under the CP Program may be issued, repaid and re-issued from time to time, with the aggregate principal amount of CP Notes outstanding under the CP Program at any time not to exceed $2.0 billion. As of December 31, 2025, there were $1.9 billion CP Notes outstanding under our CP Program. We intend to maintain available commitments under our 2016 Revolver in an amount at least equal to the amount of CP Notes outstanding at any point in time.

(b)Inclusive of $5 million included within "Other assets, net" on our condensed consolidated balance sheet.

(c)Excludes amounts related to the Fiber Business, which are presented in discontinued operations.

(d)Availability at any point in time is subject to reaffirmation of the representations and warranties in, and there being no default under, the credit agreement governing our 2016 Revolver.

(e)See "Non-GAAP Measures and Other Information" for further information on, and reconciliation to, Net Debt.

(f)As defined in the respective debt agreement. In the indentures for the Tower Revenue Notes, Series 2018-2 and the 2009 Securitized Notes, the defined term for Debt Service Coverage Ratio is "DSCR." Total Net Leverage Ratio, Total Senior Secured Leverage Ratio and all DSCR ratios are calculated using the trailing twelve months.

(g)Failure to comply with the financial maintenance covenants would, absent a waiver, result in an event of default under the credit agreement governing our 2016 Credit Facility.

(h)Applicable solely to the extent that the senior unsecured debt rating by any two of S&P, Moody's and Fitch is lower than BBB-, Baa3 or BBB-, respectively. If applicable, the consolidated interest coverage ratio must be greater than or equal to 2.50.

(i)The Tower Revenue Notes, Series 2018-2 and 2009 Securitized Notes also include the potential for amortization events, which could result in applying current and future cash flow to the prepayment of debt with applicable prepayment consideration. An amortization event occurs when the Debt Service Coverage Ratio falls below 1.45x or 1.15x, in each case as described under the indentures for the Tower Revenue Notes, Series 2018-2 or 2009 Securitized Notes, respectively.

(j)Rating Agency Confirmation (as defined in the respective debt agreement) is required.

16

Crown Castle Inc.

First Quarter 2025

COMPANY OVERVIEW

OUTLOOK

FINANCIAL

HIGHLIGHTS

CAPITALIZATION OVERVIEW

APPENDIX

INTEREST RATE EXPOSURE(a)

(as of December 31, 2025; dollars in millions)

Fixed Rate Debt

Floating Rate Debt

Face value of principal outstanding(b)

$20,276

Face value of principal outstanding(b)

$3,932

% of total debt

84%

% of total debt

16%

Weighted average interest rate

3.8%

Weighted average interest rate(c)

4.7%

Upcoming maturities:

2026

2027

Interest rate sensitivity of 25 bps increase in interest rates:

Face value of principal outstanding(b)

$2,650

$2,250

Full year effect(d)

$9.8

Weighted average interest rate

2.95%

3.48%

COMPONENTS OF INTEREST EXPENSE

2024

2025

Twelve Months Ended December 31,

(in millions; totals may not sum due to rounding)

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

2024

2025

Interest expense on debt obligations

$

223

$

227

$

234

$

236

$

233

$

239

$

244

$

241

$

920

$

956

Amortization of deferred financing costs and adjustments on long-term debt

8

8

8

8

8

8

8

8

32

31

Capitalized interest

(5)

(5)

(6)

(4)

(5)

(4)

(5)

(3)

(20)

(15)

Interest expense and amortization of deferred financing costs, net

$

226

$

230

$

236

$

240

$

236

$

243

$

247

$

246

$

932

$

972

(a)Excludes finance leases and other obligations; assumes no default.

(b)Net of required principal amortization.

(c)In June 2021, the Company entered into an amendment to the credit agreement governing our 2016 Credit Facility that provided for, among other things, a reduction to the interest rate spread ("Spread") of up to 0.05% if the Company meets specified annual sustainability targets ("Targets") and an increase to the Spread of up to 0.05% if the Company fails to meet specified annual sustainability thresholds ("Thresholds"). In January 2026, the Company submitted the required documentation and received confirmation from its administrative agent that all Targets were met as of December 31, 2025, and, as such, the Spread reduction is maintained for 2026. The weighted average interest rate reflects the reduced Spread.

(d)Represents incremental interest expense over a 12-month period based on a hypothetical interest rate increase of 25 bps on face value of variable indebtedness outstanding as of December 31, 2025; assumes no debt maturities.

17

Crown Castle Inc.

Fourth Quarter 2025

COMPANY OVERVIEW

OUTLOOK

FINANCIAL

HIGHLIGHTS

CAPITALIZATION OVERVIEW

APPENDIX

CONDENSED CONSOLIDATED BALANCE SHEET (Unaudited)

(in millions, except par values)

December 31, 2025

December 31, 2024

ASSETS

Current assets:

Cash and cash equivalents

$

99

$

100

Restricted cash and cash equivalents

170

170

Receivables, net

172

129

Prepaid expenses

79

74

Deferred site rental receivables

167

164

Other current assets

23

24

Current assets of discontinued operations

434

429

Total current assets

1,144

1,090

Deferred site rental receivables

2,288

2,279

Property and equipment, net

6,273

6,577

Operating lease right-of-use assets

5,473

5,600

Goodwill

5,127

5,127

Other intangible assets, net

861

1,037

Other assets, net

61

58

Non-current assets of discontinued operations

10,291

10,968

Total assets

$

31,518

$

32,736

LIABILITIES AND EQUITY (DEFICIT)

Current liabilities:

Accounts payable

$

71

$

48

Accrued interest

235

244

Deferred revenues

192

141

Other accrued liabilities

168

167

Current maturities of debt and other obligations

2,783

603

Current portion of operating lease liabilities

268

264

Current liabilities of discontinued operations

762

710

Total current liabilities

4,479

2,177

Debt and other long-term obligations

21,554

23,451

Operating lease liabilities

4,961

5,062

Other long-term liabilities

607

645

Non-current liabilities of discontinued operations

1,552

1,534

Total liabilities

33,153

32,869

Commitments and contingencies

Stockholders' equity (deficit):

Common stock, 0.01 par value; 1,200 shares authorized; shares issued and outstanding: December 31, 2025—435 and December 31, 2024—435

4

4

Additional paid-in capital

18,527

18,393

Accumulated other comprehensive income (loss)

(5)

(5)

Dividends/distributions in excess of earnings

(20,161)

(18,525)

Total equity (deficit)

(1,635)

(133)

Total liabilities and equity (deficit)

$

31,518

$

32,736

18

Crown Castle Inc.

Fourth Quarter 2025

COMPANY OVERVIEW

OUTLOOK

FINANCIAL

HIGHLIGHTS

CAPITALIZATION OVERVIEW

APPENDIX

CONDENSED CONSOLIDATED STATEMENT OF OPERATIONS (Unaudited)

Three Months Ended December 31,

Twelve Months Ended December 31,

(in millions, except per share amounts)

2025

2024

2025

2024

Net revenues:

Site rental

$

1,019

$

1,070

$

4,049

$

4,268

Services and other

53

49

215

192

Net revenues

1,072

1,119

4,264

4,460

Operating expenses:

Costs of operations:(a)

Site rental

252

242

992

983

Services and other

29

26

113

107

Selling, general and administrative

94

92

383

435

Asset write-down charges

4

1

11

11

Depreciation, amortization and accretion

170

184

690

736

Restructuring charges

—

3

—

70

Total operating expenses

549

548

2,189

2,342

Operating income (loss)

523

571

2,075

2,118

Interest expense and amortization of deferred financing costs, net

(246)

(240)

(972)

(932)

Interest income

3

5

13

20

Other income (expense)

—

(23)

3

(26)

Income (loss) from continuing operations before income taxes

280

313

1,119

1,180

Benefit (provision) for income taxes

(3)

(4)

(16)

(18)

Income (loss) from continuing operations

$

277

$

309

$

1,103

$

1,162

Discontinued operations:

Income (loss) from discontinued operations before gain (loss) from disposal, net of tax

279

(5,077)

916

(5,065)

Gain (loss) from disposal of discontinued operations

(262)

—

(1,575)

—

Income (loss) from discontinued operations, net of tax

17

(5,077)

(659)

(5,065)

Net income (loss)

$

294

$

(4,768)

$

444

$

(3,903)

Net income (loss), per common share:

Income (loss) from continuing operations, basic

$

0.64

$

0.71

$

2.53

$

2.68

Income (loss) from discontinued operations, basic

$

0.03

$

(11.68)

$

(1.51)

$

(11.66)

Net income (loss)—basic

$

0.67

$

(10.97)

$

1.02

$

(8.98)

Income (loss) from continuing operations, diluted

$

0.63

$

0.71

$

2.52

$

2.68

Income (loss) from discontinued operations, diluted

$

0.04

$

(11.68)

$

(1.51)

$

(11.66)

Net income (loss)—diluted

$

0.67

$

(10.97)

$

1.01

$

(8.98)

Weighted-average common shares outstanding:

Basic

435

435

435

434

Diluted

437

435

437

434

(a)Exclusive of depreciation, amortization and accretion shown separately.

19

Crown Castle Inc.

Fourth Quarter 2025

COMPANY OVERVIEW

OUTLOOK

FINANCIAL

HIGHLIGHTS

CAPITALIZATION OVERVIEW

APPENDIX

CONDENSED CONSOLIDATED STATEMENT OF CASH FLOWS (Unaudited)

Twelve Months Ended December 31,

(in millions)

2025

2024

Cash flows from operating activities:

Net income (loss)

$

444

$

(3,903)

(Income) loss from discontinued operations before (gain) loss from disposal, net of tax

(916)

5,065

(Gain) loss from disposal of discontinued operations

1,575

—

Income (loss) from continuing operations

1,103

1,162

Adjustments to reconcile income (loss) from continuing operations to net cash provided by (used for) operating activities:

Depreciation, amortization and accretion

690

736

Amortization of deferred financing costs and other non-cash interest

32

32

Stock-based compensation expense, net

73

84

Asset write-down charges

11

11

Deferred income tax (benefit) provision

—

4

Restructuring charges, non-cash

—

10

Other non-cash adjustments, net

(4)

23

Net cash provided by (used for) operating activities from discontinued operations

1,185

1,123

Changes in assets and liabilities, excluding the effects of acquisitions:

Increase (decrease) in liabilities

(47)

(164)

Decrease (increase) in assets

14

(78)

Net cash provided by (used for) operating activities

3,057

2,943

Cash flows from investing activities:

Capital expenditures

(182)

(176)

Payments for acquisitions, net of cash acquired

—

(8)

Other investing activities, net

4

9

Net cash provided by (used for) investing activities from discontinued operations

(980)

(1,045)

Net cash provided by (used for) investing activities

(1,158)

(1,220)

Cash flows from financing activities:

Proceeds from issuance of long-term debt

—

1,244

Principal payments on debt and other long-term obligations

(118)

(99)

Purchases and redemptions of long-term debt

(1,200)

(750)

Borrowings under revolving credit facility

1,200

—

Payments under revolving credit facility

(255)

(670)

Net issuances (repayments) under commercial paper program

590

1,341

Payments for financing costs

—

(12)

Purchases of common stock

(23)

(33)

Dividends/distributions paid on common stock

(2,080)

(2,729)

Net cash provided by (used for) financing activities

(1,886)

(1,708)

Net increase (decrease) in cash and cash equivalents and restricted cash and cash equivalents

13

15

Effect of exchange rate changes on cash

—

(1)

Cash and cash equivalents and restricted cash and cash equivalents at beginning of period(a)

295

281

Cash and cash equivalents and restricted cash and cash equivalents at end of period(a)

$

308

$

295

Supplemental disclosure of cash flow information:

Interest paid

$

965

$

895

Income taxes paid (refunded)

$

15

$

10

(a)Inclusive of cash and cash equivalents and restricted cash and cash equivalents included in discontinued operations.

20

Crown Castle Inc.

Fourth Quarter 2025

COMPANY OVERVIEW

OUTLOOK

FINANCIAL

HIGHLIGHTS

CAPITALIZATION OVERVIEW

APPENDIX

NON-GAAP MEASURES AND OTHER INFORMATION

This Supplement includes presentations of Adjusted EBITDA, Adjusted Funds from Operations ("AFFO"), including per share amounts, Funds from Operations ("FFO"), including per share amounts, Organic Contribution to Site Rental Billings, (including as Adjusted for Impact of Sprint Cancellations and as Adjusted for Impact of Sprint Cancellations and DISH Terminations), Adjusted Site Rental Gross Margin, Adjusted Services and Other Gross Margin, Net Debt, Consolidated Return on Invested Capital, Cash Yield on Invested Capital, and Free Cash Flow from Discontinued Operations, which are non-GAAP financial measures. These non-GAAP financial measures are not intended as alternative measures of operating results or cash flow from operations (as determined in accordance with Generally Accepted Accounting Principles ("GAAP")).

Our non-GAAP financial measures may not be comparable to similarly titled measures of other companies, including other companies in the towers sector or other REITs.

In addition, we provide the components of certain GAAP measures, such as site rental revenues and capital expenditures.

Our non-GAAP financial measures are presented as additional information because management believes these measures are useful indicators of the financial performance of our business. Among other things, management believes that:

•Adjusted EBITDA is useful to investors or other interested parties in evaluating our financial performance. Adjusted EBITDA is a financial measure frequently used by management (1) to evaluate the economic productivity of our operations and (2) for purposes of making decisions about allocating resources to, and assessing the performance of, our operations. Management believes that Adjusted EBITDA helps investors or other interested parties meaningfully evaluate and compare the results of our operations (1) from period to period and (2) to our competitors, by removing the impact of our capital structure (primarily interest charges from our outstanding debt) and asset base (primarily depreciation, amortization and accretion) from our financial results. Management also believes Adjusted EBITDA is frequently used by investors or other interested parties in the evaluation of the towers sector and other REITs to measure financial performance without regard to items such as depreciation, amortization and accretion, which can vary depending upon accounting methods and the book value of assets. Adjusted EBITDA should be considered only as a supplement to net income (loss) computed in accordance with GAAP as a measure of our performance.

•AFFO, including per share amounts, is useful to investors or other interested parties in evaluating our financial performance. Management believes that AFFO helps investors or other interested parties meaningfully evaluate our financial performance as it includes (1) the impact of our capital structure (primarily interest expense on our outstanding debt and dividends on our preferred stock (in periods where applicable)) and (2) sustaining capital expenditures, and excludes the impact of our (1) asset base (primarily depreciation, amortization and accretion) and (2) certain non-cash items, including straight-lined revenues and expenses related to fixed escalations and rent free periods. GAAP requires rental revenues and expenses related to leases that contain specified rental increases over the life of the lease to be recognized evenly over the life of the lease. In accordance with GAAP, if payment terms call for fixed escalations or rent free periods, the (1) revenues are recognized on a straight-lined basis over the fixed, non-cancelable term of the tenant contract, and (2) expenses are recognized on a straight-lined basis over the estimated lease term including renewal options that are reasonably certain to be exercised. Management notes that Crown Castle uses AFFO only as a performance measure. AFFO should be considered only as a supplement to net income (loss) computed in accordance with GAAP as a measure of our performance and should not be considered as an alternative to cash flow from operations or as residual cash flow available for discretionary investment.

•FFO, including per share amounts, is useful to investors or other interested parties in evaluating our financial performance. Management believes that FFO may be used by investors or other interested parties as a basis to compare our financial performance with that of other REITs. FFO helps investors or other interested parties meaningfully evaluate financial performance by excluding the impact of our asset base (primarily real estate depreciation, amortization and accretion). FFO is not a key performance indicator used by Crown Castle. FFO should be considered only as a supplement to net income (loss) computed in accordance with GAAP as a measure of our performance and should not be considered as an alternative to cash flow from operations.

•Organic Contribution to Site Rental Billings (also referred to as organic growth) is useful to investors or other interested parties in understanding the components of the year-over-year changes in our site rental revenues computed in accordance with GAAP. Management uses Organic Contribution to Site Rental Billings to assess year-over-year growth rates for our rental activities, to evaluate current performance, to capture trends in rental rates, core leasing activities and tenant non-renewals in our core business, as well as to forecast future results. Separately, we are also disclosing Organic Contribution to Site Rental Billings as Adjusted for Impact of Sprint Cancellations and Organic Contribution to Site Rental Billings as Adjusted for Sprint Cancellations and DISH Terminations, which are outside of ordinary course, to provide further insight into our results of operations and underlying trends. Management believes that identifying the impact of Sprint Cancellations and DISH Terminations provides increased transparency and comparability across periods. Organic Contribution to Site Rental Billings (including as Adjusted for Impact of Sprint Cancellations and as Adjusted for Impact of Sprint Cancellations and DISH Terminations) is not meant as an alternative measure of revenue and should be considered only as a supplement in understanding and assessing the performance of our site rental revenues computed in accordance with GAAP.

21

Crown Castle Inc.

Fourth Quarter 2025

COMPANY OVERVIEW

OUTLOOK

FINANCIAL

HIGHLIGHTS

CAPITALIZATION OVERVIEW

APPENDIX

•Adjusted Site Rental Gross Margin and Adjusted Services and Other Gross Margin are useful to investors or other interested parties in evaluating our financial performance. These measures are used by our management (1) to evaluate the economic productivity of our business, (2) to identify underlying business trends that are impacting our performance, and (3) for purposes of making decisions about allocating resources to, and assessing the performance of, our business. We also believe it helps investors and other interested parties meaningfully evaluate and compare the results of our operations from period to period.

•Net Debt is useful to investors or other interested parties in evaluating our overall debt position and future debt capacity. Management uses Net Debt in assessing our leverage. Net Debt is not meant as an alternative measure of debt and should be considered only as a supplement in understanding and assessing our leverage.

•Consolidated Return on Invested Capital and Cash Yield on Invested Capital are useful to investors or other interested parties in evaluating the financial performance of our assets. Management believes that these metrics are useful in assessing our efficiency at allocating capital to generate returns over time. Consolidated Return on Invested Capital and Cash Yield on Invested Capital are not meant as alternatives to GAAP measures such as revenues, operating income, and certain asset classes (such as property and equipment, site rental contracts and tenant relationships, and goodwill) computed in accordance with GAAP. Such non-GAAP metrics should be considered only as a supplement in understanding and assessing the performance of our assets.

•Free Cash Flow from Discontinued Operations is useful to investors or other interested parties in understanding the net cash flows generated from discontinued operations for a particular period, after taking into consideration capital expenditures for that same period. Such net cash flows are available for reinvestment within discontinued operations or for other use by the Company. Management believes that Free Cash Flow from Discontinued Operations helps investors and other interested parties meaningfully evaluate the liquidity associated with discontinued operations from period to period. Free Cash Flow from Discontinued Operations does not reflect the impact of our capital structure (primarily interest charges on our outstanding debt) and should be considered only as a supplement to: a) Income (loss) from Discontinued Operations, net of tax, computed in accordance with GAAP as a measure of the performance of discontinued operations; and b) the condensed consolidated statement of cash flows prepared in accordance with GAAP as a measure of the cash flows of the Company.

Non-GAAP Financial Measures

Adjusted EBITDA. We define Adjusted EBITDA as net income (loss) plus restructuring charges (credits), asset write-down charges, goodwill impairment charges, acquisition and integration costs, depreciation, amortization and accretion, amortization of prepaid lease purchase price adjustments, interest expense and amortization of deferred financing costs, net, (gains) losses on retirement of long-term obligations, net (gain) loss on interest rate swaps, (gains) losses on foreign currency swaps, impairment of available-for-sale securities, interest income, other (income) expense, (benefit) provision for income taxes, (income) loss from discontinued operations, net of tax, cumulative effect of a change in accounting principle and stock-based compensation expense, net.

AFFO. We define AFFO as FFO before straight-lined revenues, straight-lined expenses, stock-based compensation expense, net, non-cash portion of tax provision, non-real estate related depreciation, amortization and accretion, amortization of non-cash interest expense, other (income) expense, (gains) losses on retirement of long-term obligations, net (gain) loss on interest rate swaps, (gains) losses on foreign currency swaps, impairment of available-for-sale securities, acquisition and integration costs, restructuring charges (credits), cumulative effect of a change in accounting principle and adjustments for noncontrolling interests, less sustaining capital expenditures.

AFFO per share. We define AFFO per share as AFFO divided by diluted weighted-average common shares outstanding.

FFO. We define FFO as net income (loss) plus real estate related depreciation, amortization and accretion, asset write-down charges, goodwill impairment charges, and (income) loss from discontinued operations, net of tax, less noncontrolling interest and cash paid for preferred stock dividends (in periods where applicable), and is a measure of funds from operations attributable to common stockholders.

FFO per share. We define FFO per share as FFO divided by diluted weighted-average common shares outstanding.