.2

1First BanCorp Financial Results First Quarter 2026 April 22, 2026

Forward Looking Statements This presentation contains “forward -looking statements” concerning the Corporation’s future economic, operational and financial performance. The words or phrases “expect,” “anticipate,” “intend,” “should,” “would,” “will,” “plans,” “forecast,” “believe” and similar expressions are meant to identify “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are subject to the safe harbor created by such sections. The Corporation cautions readers not to place undue reliance on any such forward -looking statements, which speak only as of the date hereof, and advises readers that any such forward-looking statements are not guarantees of future performance and involve certain risks, uncertainties, estimates and assumptions by us that are difficult to predict. Various factors, some of which are beyond our control, including, but not limited to, the uncertainties more fully discussed in Part I, Item 1A, “Risk Factors” of the Corporation’s Annual Report on Form 10-K for the year ended December 31, 2025, and the following, could cause actual results to differ materially from those expressed in, or implied by, such forward-looking statements: the effect of the current global interest rate environment (including the potential for ongoing reductions in interest rates) and inflation levels on the level, composition and performance of the Corporation’s assets and liabilities, and corresponding effects on the Corporation’s net interest income, net interest margin, loan originations, deposit attrition, overall results of operations, and liquidity position; the effects of changes in the interest rate environment, including any adverse change in the Corporation’s ability to attract and retain clients and gain acceptance from current and prospective customers for new products and services,

including those related to the offering of digital banking and financial services; volatility in the financial services industry, which could result in, among other things, bank deposit runoffs, liquidity constraints, and increased regulatory requirements and costs; uncertainty as to the ability of FirstBank to retain its core deposits and generate sufficient cash flow through its wholesale funding sources, which may require us to sell investment securities at a loss; the impacts of natural or man-made disasters, widespread health emergencies, geopolitical conflicts (including sanctions, war or armed conflict such as the ongoing conflict in Ukraine, ongoing conflicts in the Middle East, such as the war in Iran); adverse changes in general political and economic conditions in Puerto Rico, the U.S., and the U.S. and British Virgin Islands, including in the interest rate environment, unemployment rates, market liquidity, housing absorption rates, real estate markets and U.S. capital markets; general competitive factors and other market risks as well as the implementation of existent or planned strategic growth opportunities, including risks, uncertainties, and other factors or events related to any business acquisitions, dispositions , strategic partnerships, strategic operational investments including system conversions, and any anticipated efficiencies or other expected results related thereto; the impact of litigation or the threat of litigation, including any settlements or judgments against the Corporation, and the potential resulting liabilities, costs, negative publicity or other reputational harm; the effects of asserted and unasserted claims and the extent of available insurance coverage; uncertainty as to the implementation of the debt restructuring plan of Puerto Rico and the Fiscal Plan for Puerto Rico as certified on June 6, 2025 by the Financial Oversight and Management Board for Puerto Rico, or any revisions to it, on our clients and

loan portfolios, and any potential impact from future economic or political developments and tax regulations in Puerto Rico; the impact of government financial assistance for hurricane recovery and other disaster relief on economic activity in Puerto Rico; the timing of sales of properties from our other real estate owned (“OREO”) portfolio; the impacts of applicable legislative, tax or regulatory changes on the Corporation’s financial condition or performance; and the effect of continued changes in the fiscal, monetary, and trade policies and regulations of the U.S. federal government, the Puerto Rico government and other governments. The Corporation does not undertake and specifically disclaims any obligation to update any “forward-looking statements” to reflect occurrences or unanticipated events or circumstances after the date of such statements, except as required by the federal securities laws. Non-GAAP Financial Measures In addition to the Corporation’s financial information presented in accordance with GAAP, management uses certain “non-GAAP” financial measures” within the meaning of Regulation G promulgated by the SEC, to clarify and enhance understanding of past performance and prospects for the future. Please refer to pages 14-16 for a reconciliation of GAAP to non-GAAP measures and calculations. 2

Agenda 1 1Q 2026 – Quarter Highlights Aurelio Alemán, President and Chief Executive Officer 2 1Q 2026 – Results of Operations Orlando Berges, Executive Vice President and Chief Financial Officer 3 1Q 2026 – Questions and Answers 3

First Quarter 2026 – Performance Highlights Profitability Net income of $88.8 million ($0.57 per diluted share), compared to $87.1 million ($0.55 per diluted share) in 4Q 2025 Net interest income decreased to $221.0 million but the margin grew by 7 basis points reaching 4.75% On a non-GAAP basis, record adjusted pre-tax, pre-provision income of $131.4 million, up 1.7% when compared to 4Q 2025 Consistent expense management discipline resulted in an efficiency ratio of 49.1% vs. 49.3% in 4Q 2025 Balance Sheet Total loans decreased slightly to $13.1 billion mainly driven by expected reductions in consumer loan balances in Puerto Rico Core deposits, other than brokered and fully collateralized government deposits, increased by $158.5 million (1.2% vs. prior quarter) Fully collateralized government deposits decreased by $146.3 million to $2.9 billion Asset Quality Non -performing assets (“NPA”) ratio decreased to 0.57% and annualized net charge-offs to average loans increased by 2 bps to 0.65% Allowance for credit losses (“ACL”) coverage ratio on loans and leases decreased by 3 bps to 1.87% Liquidity and Capital Loans in early delinquency (30-89 days past due) decreased by 24% to $110.5 million compared to $145.0 million in 4Q 2025 Total available liquidity sources of approximately $6.5 billion or 1.3x of uninsured deposits (excluding fully collateralized govt. deposits) Repurchased $50.0 million in common stock and declared $31.5 million in common stock dividends; CET1 remains strong and above well-capitalized levels at 16.9% On a non-GAAP basis, tangible book value per share grew by 1.3% to $12.45 and tangible common equity ratio reached 10.11% 4

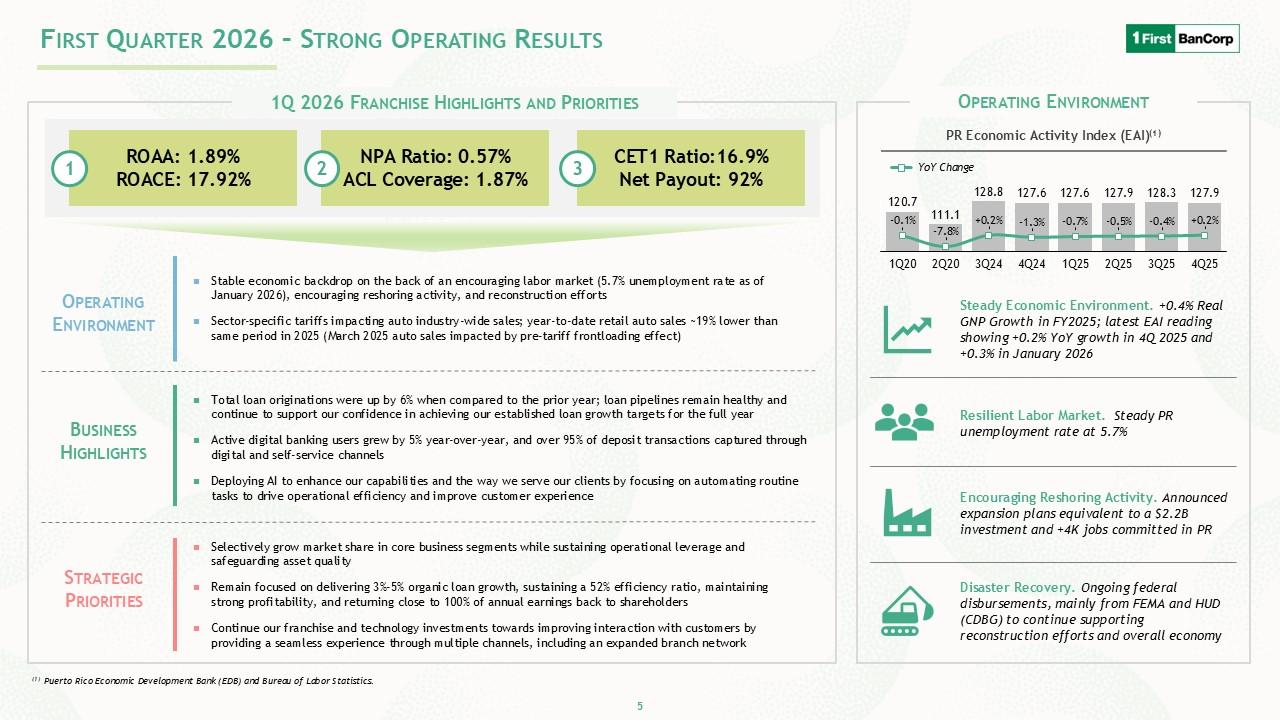

First Quarter 2026 – Strong Operating Results 1Q 2026 Franchise Highlights and Priorities 1 ROAA: 1.89% ROACE: 17.92% 2 NPA Ratio: 0.57% ACL Coverage: 1.87% 3 CET1 Ratio:16.9% Net Payout: 92% Operating Environment Stable economic backdrop on the back of an encouraging labor market (5.7% unemployment rate as of January 2026), encouraging reshoring activity, and reconstruction efforts Sector-specific tariffs impacting auto industry-wide sales; year-to-date retail auto sales ~19% lower than same period in 2025 (March 2025 auto sales impacted by pre-tariff frontloading effect) Business Highlights Linked-quarter loan originations declined by 10% but increased by 6% when compared to the first quarter of 2025; core customer deposits grew by 4.9% on a linked-quarter annualized basis Active digital banking users grew by 5% year -over-year, and over 95% of deposit transactions captured through digital and self-service channels Deploying AI to enhance our capabilities and the way we serve our clients by focusing on automating routine tasks to drive operational efficiency and improve customer experience Strategic Priorities Selectively grow market share in core business segments while sustaining operational leverage and safeguarding asset quality Remain focused on delivering 3%-5% organic loan growth, sustaining a 52% efficiency ratio, maintaining strong profitability, and returning close to 100% of annual earnings back to shareholders Continue our franchise and technology investments towards improving interaction with customers by providing a seamless experi ence through multiple channels, including an expanded branch network Operating Environment PR Economic Activity Index (EAI)(1) 120.7 111.1 128.8 127.6 127.6 127.9 128.3 127.9 -0.1% -7.8% 0.2% -1.3% -0.7% -0.5% -0.4% 0.2% 1Q20 2Q20 3Q24 4Q24 1Q25 2Q25 3Q25 4Q25 Steady Economic Environment.

+0.4% Real GNP Growth in FY2025; latest EAI reading showing +0.2% YoY growth in 4Q 2025 and +0.3% in January 2026 Resilient Labor Market. Steady PR unemployment rate at 5.7% Encouraging Reshoring Activity. Announced expansion plans equivalent to a $2.2B investment and +4K jobs committed in PR Disaster Recovery. Ongoing federal disbursements, mainly from FEMA and HUD (CDBG) to continue supporting reconstruction efforts and overall economy (1) Puerto Rico Economic Development Bank (EDB) and Bureau of Labor Statistics. 5

Results of Operations

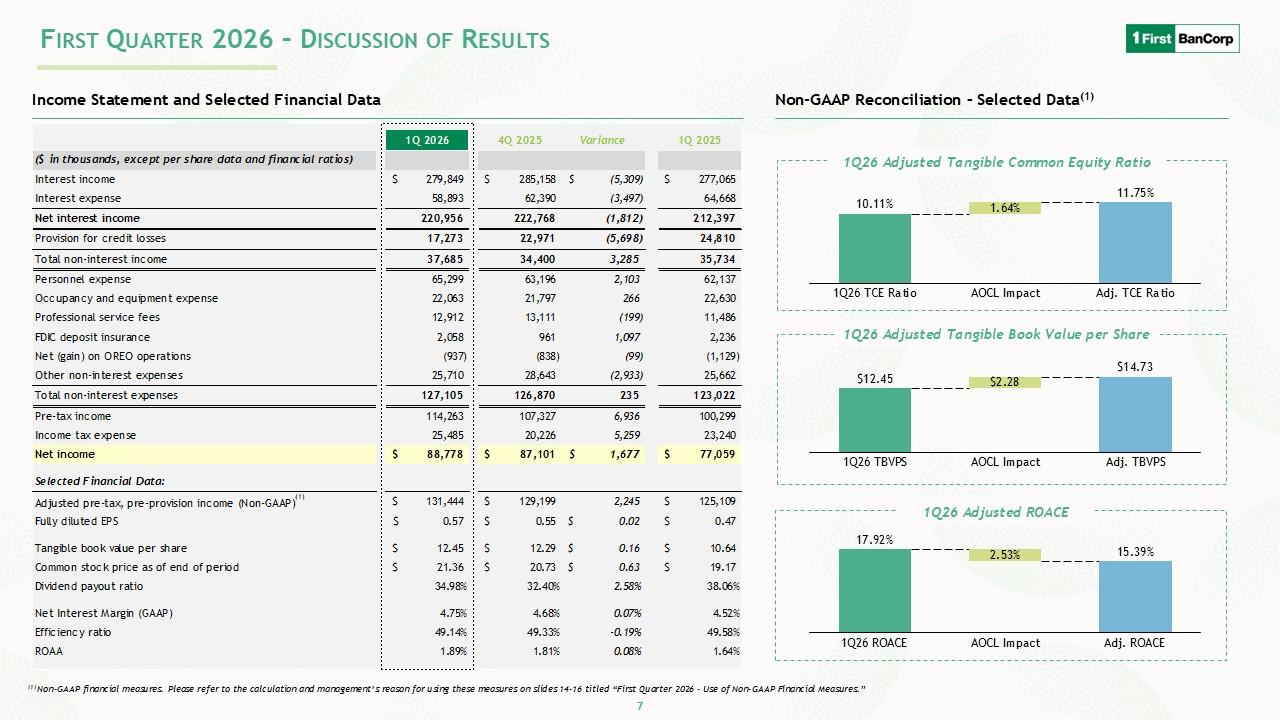

Income Statement and Selected Financial Data I 10 2026 I vl 40n (0 F ($ in thousands, except per share data and financial ratios) Interest income S 279,849 S 285,158 $ (5,309) S 277,065 Interest expense 58,893 62,390 (3,497) 64,668 Net interest income 220,956 222,768 (1,812) 212,397 Provision for credit losses 17,273 22,971 (5,698) 24,8 10 Total non-interest income 37,685 34,400 3,285 35,734 Personnel expense 65,299 63,196 2,103 62,137 Occupancy and equipment expense 22,063 21,797 266 22,630 Professional service fees 12,912 13,111 (199) 11,486 FDIC deposit insurance 2,058 961 1,097 2,236 Net (gain) on OREO operations (937) (838) (99) (1,129) Other non-interest expenses 25,710 28,643 _2,933) 25,662 Total non-interest expenses 127,1 05 126,870 23 5 123,022 Pre-tax income 114,263 107,327 6,936 100,299 Income tax expense 25,485 20,226 5,259 23,240 Net i ncome $ 88,778 $ 87,101 $ 1,677 $ 77,059 Selected Financial Data: Adjusted pre-tax, pre-provision income (Non-GAAP) S 131,444 S 129,199 2,245 S 125,109 Fully diluted EPS S 0.57 S 0.55 0.02 S 0.47 Tangible bookvaue per share S 12.45 S 12.29 0.16 S 10.64 Common stock price as of end of period S 21.36 S 20.73 0.63 S 19.17 Dividend payout ratio 34.98% 32.40% 2.58% 38.06% Net interest Margin (GAAP) 4.75% 4.68% 0.07% 4.52% Efficiency ratio 49.14% 49.33% 0. 19% 49.58% ROAA 1.89% 1.81% 0.08% 1.64% Non-GAAP Reconciliation – Selected Data(1) 1Q26 Adjusted Tangible Common Equity Ratio 10.11% 1.64% 11.75% 1Q26 TCE Ratio AOCL Impact Adj. TCE Ratio 1Q26 Adjusted Tangible Book Value per Share $12.45 $2.28 $14.73 1Q26 TBVPS AOCL Impact Adj. TBVPS 1Q26 Adjusted ROACE 17.92% 2.53% 15.39% 1Q26 ROACE AOCL Impact Adj. ROACE (1) Non-GAAP financial measures. Please refer to the calculation and management’s reason for using these measures on slides 14-16

titled “First Quarter 2026 - Use of Non-GAAP Financial Measures.” 7

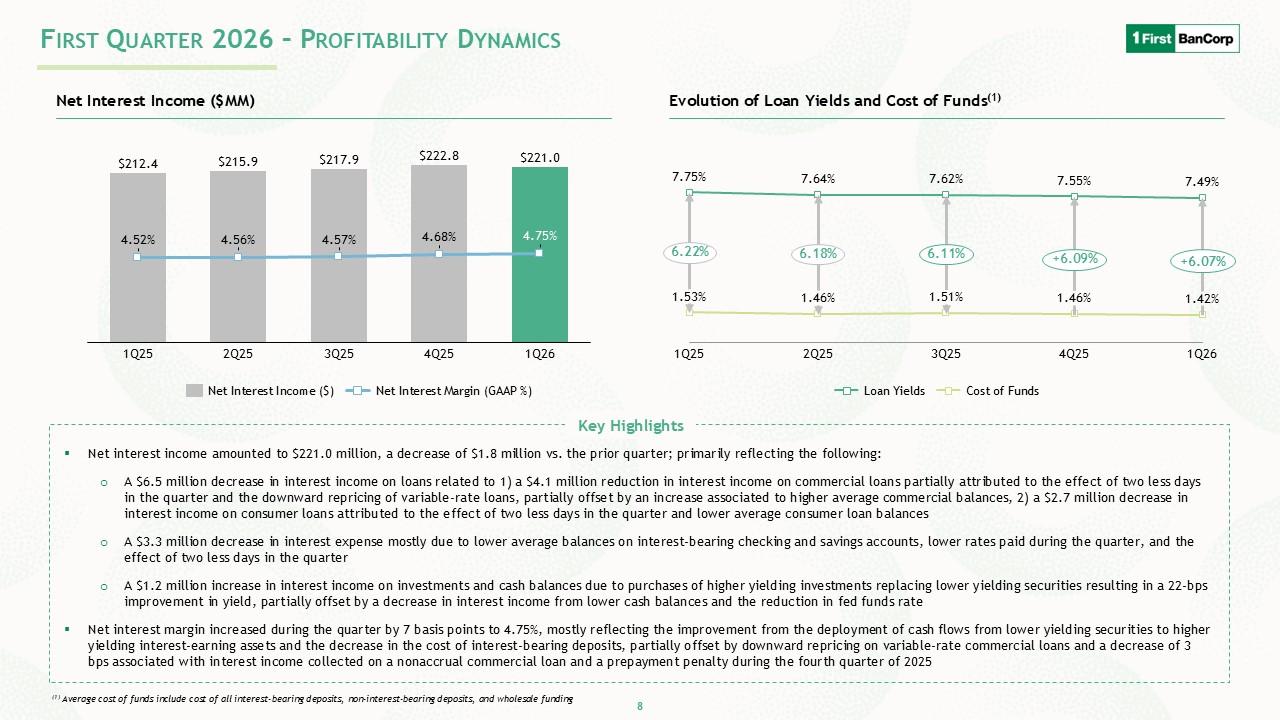

First Quarter 2026 – Profitability Dynamics Net Interest Income ($MM) $212.4 $215.9 $217.9 $222.8 $221.0 4.52% 4.56% 4.57% 4.68% 4.75% 1Q25 2Q25 3Q25 4Q25 1Q26 Net Interest Income ($) Net Interest Margin (GAAP %) Evolution of Loan Yields and Cost of Funds(1) 7.75% 7.64% 7.62% 7.55% 7.49% 6.22% 6.18% 6.11% 6.09% 6.07% 1.53% 1.46% 1.51% 1.46% 1.42% 1Q25 2Q25 3Q25 4Q25 1Q26 Loan Yields Cost of Funds Key Highlights Net interest income amounted to $221.0 million, a decrease of $1.8 million vs. the prior quarter; primarily reflecting the following: A $6.5 million decrease in interest income on loans related to 1) a $4.1 million reduction in interest income on commercial loans partially attributed to the effect of two less days in the quarter and the downward repricing of variable-rate loans, partially offset by an increase associated to higher average commercial balances, 2) a $2.7 million decrease in interest income on consumer loans attributed to the effect of two less days in the quarter and lower average consumer loan balances A $3.3 million decrease in interest expense mostly due to lower average balances on interest-bearing checking and savings accounts, lower rates paid during the quarter, and the effect of two less days in the quarter A $1.2 million increase in interest income on investments and cash balances due to purchases of higher yielding investments replacing lower yielding securities resulting in a 22-bps improvement in yield, partially offset by a decrease in interest income from lower cash balances and the reduction in fed funds rate Net interest margin increased during the quarter by 7 basis points to 4.75%, mostly reflecting the improvement from the deployment of cash flows from lower yielding securities to higher yielding interest -earning assets and the decrease in the cost of interest-bearing deposits, partially offset by downward repricing on variable-rate

commercial loans and a decrease of 3 bps associated with interest income collected on a nonaccrual commercial loan and a prepayment penalty during the fourth quarter of 2025 (1) Average cost of funds include cost of all interest-bearing deposits, non-interest-bearing deposits, and wholesale funding 8

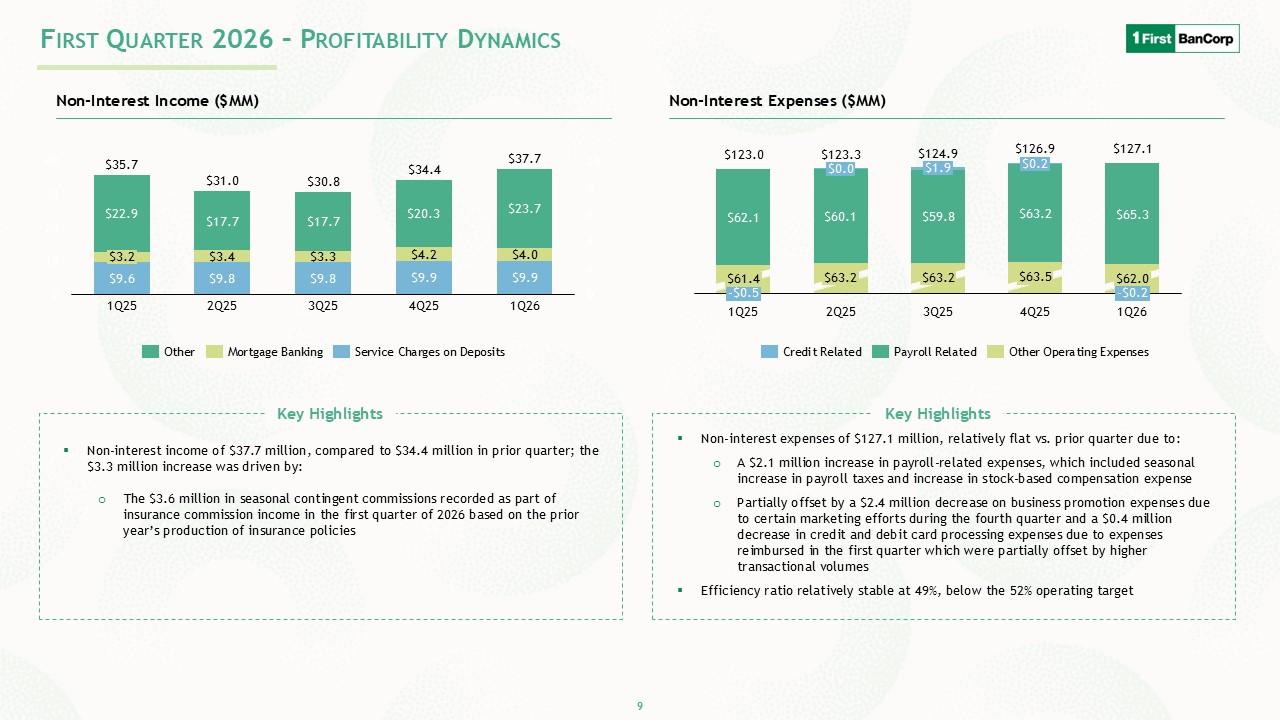

First Quarter 2026 – Profitability Dynamics Non-Interest Income ($MM) $35.7 $31.0 $30.8 $34.4 $37.7 $22.9 $17.7 $17.7 $20.3 $23.7 $3.2 $3.4 $3.3 $4.2 $4.0 $9.6 $9.8 $9.8 $9.9 $9.9 1Q25 2Q25 3Q25 4Q25 1Q26 Other Mortgage Banking Service Charges on Deposits Key Highlights Non-interest income of $37.7 million, compared to $34.4 million in prior quarter; the $3.3 million increase was driven by: The $3.6 million in seasonal contingent commissions recorded as part of insurance commission income in the first quarter of 2026 based on the prior year’s production of insurance policies Non-Interest Expenses ($MM) $123.0 $123.3 $124.9 $126.9 $127.1 -$0.5 $0.0 $1.9 $0.2 -$0.2 $62.1 $60.1 $59.8 $63.2 $65.3 $61.4 $63.2 $63.2 $63.5 $62.0 1Q25 2Q25 3Q25 4Q25 1Q26 Credit Related Payroll Related Other Operating Expenses Key Highlights Non-interest expenses of $127.1 million, relatively flat vs. prior quarter due to: A $2.1 million increase in payroll-related expenses, which included seasonal increase in payroll taxes and increase in stock-based compensation expense Partially offset by a $2.4 million decrease on business promotion expenses due to certain marketing efforts during the fourth quarter and a $0.4 million decrease in credit and debit card processing expenses due to expenses reimbursed in the first quarter which were partially offset by higher transactional volumes Efficiency ratio relatively stable at 49%, below the 52% operating target 9

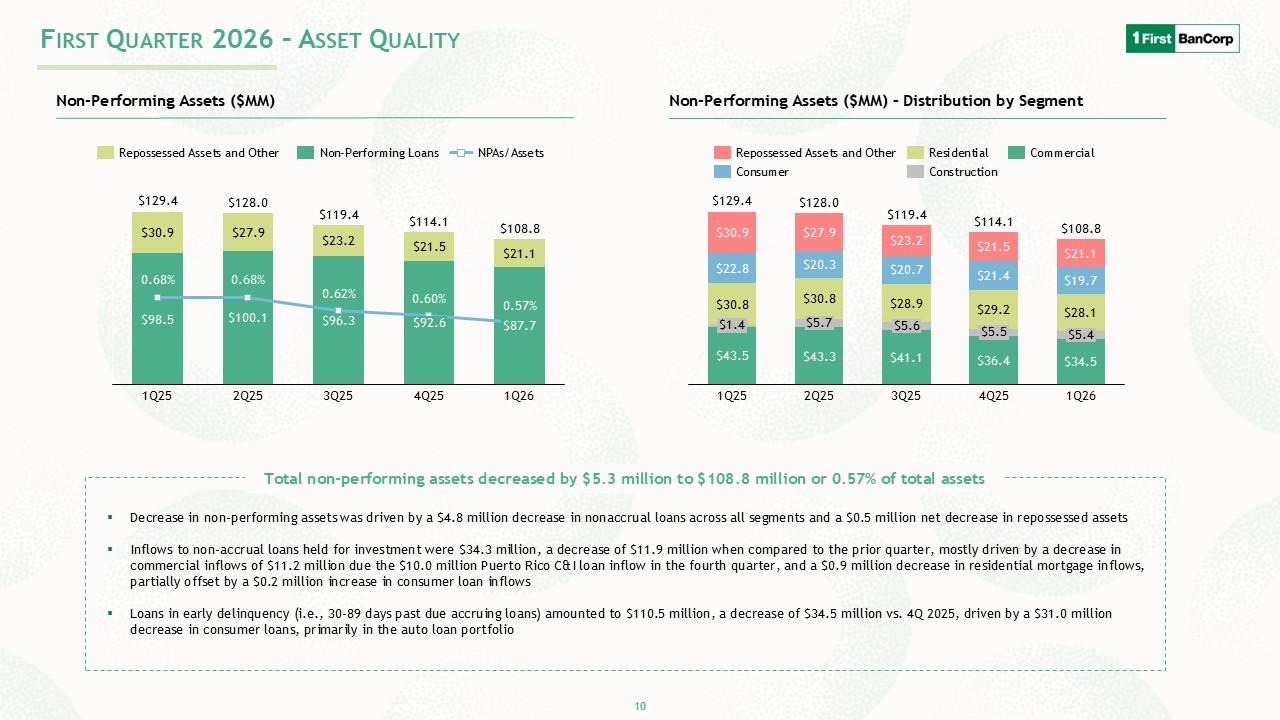

First Quarter 2026 – Asset Quality Repossessed Assets and Other Non-Performing Loans NPAs/Assets Non-Performing Assets ($MM) $129.4 $128.0 $119.4 $114.1 $108.8 $30.9 $27.9 $23.2 $21.5 $21.1 0.68% 0.68% 0.62% 0.60% 0.57% $98.5 $100.1 $69.3 $92.6 $87.7 1Q25 2Q25 3Q25 4Q25 1Q26 Repossessed Assets and Other Consumer Residential Construction Commercial $129.4 $128.0 $119.4 $114.1 $108.8 $30.9 $27.9 $23.2 $21.5 21.1. $22.8 $20.3 $20.7 $21.4 $19.7 $30.8 $30.8 $28.9 $29.2 $285.1 $1.4 $5.7 $5.6 $5.5 $5.4 $43.5 $43.3 $41.1 $36.4 $34.5 1Q25 2Q25 3Q25 4Q25 1Q26 Non-Performing Assets ($MM) – Distribution by Segment Total non-performing assets decreased by $5.3 million to $108.8 million or 0.57% of total assets Decrease in non-performing assets was driven by a $4.8 million decrease in nonaccrual loans across all segments and a $0.5 million net decrease in repossessed assets Inflows to non-accrual loans held for investment were $34.3 million, a decrease of $11.9 million when compared to the prior quarter, mostly driven by a decrease in commercial inflows of $11.2 million due the $10.0 million Puerto Rico C&I loan inflow in the fourth quarter, and a $0.9 million decrease in residential mortgage inflows, partially offset by a $0.2 million increase in consumer loan inflows Loans in early delinquency (i.e., 30-89 days past due accruing loans) amounted to $110.5 million, a decrease of $34.5 million vs. 4Q 2025, driven by a $31.0 million decrease in consumer loans, primarily in the auto loan portfolio 10

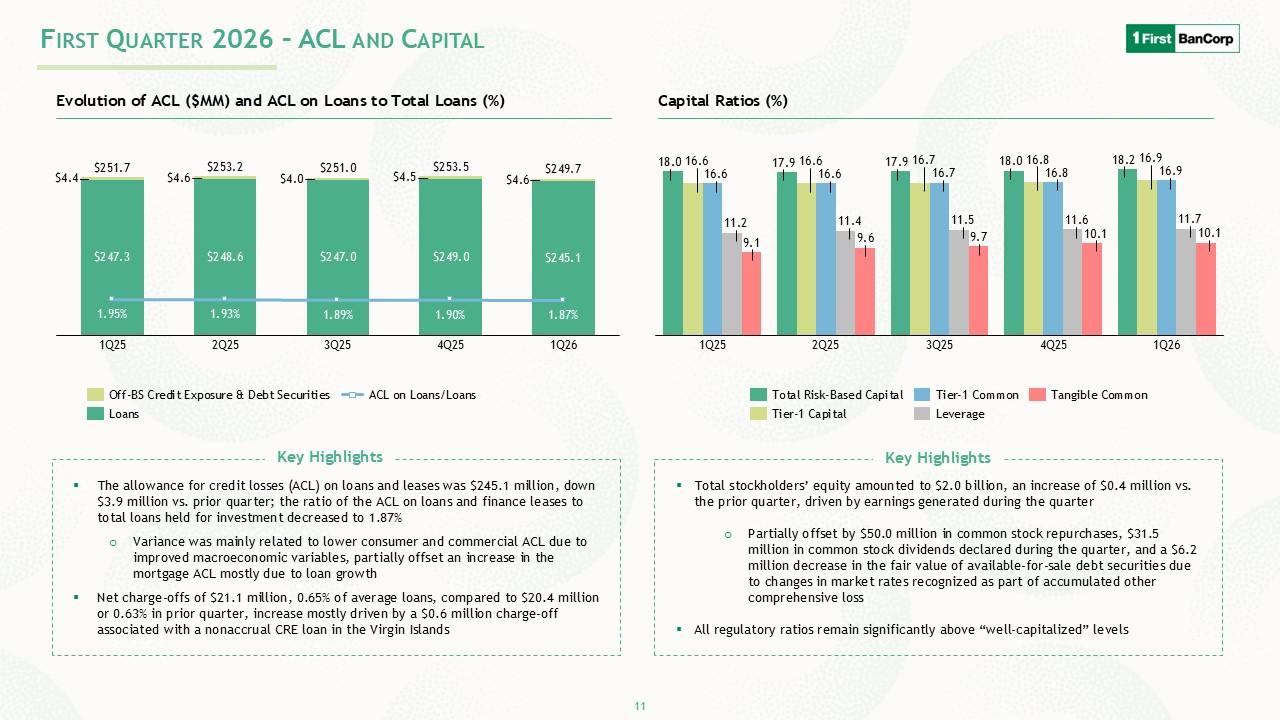

First Quarter 2026 – ACL and Capital Evolution of ACL ($MM) and ACL on Loans to Total Loans (%) $251.7 $253.2 $251.0 $253.5 $249.7 $4.4 $4.6 $4.0 $4.5 $4.6 $247.3 $248.6 $247.0 $249.0 $245.1 1.95% 1.93% 18.90% 1.90% 1.87% 1Q25 2Q25 3Q25 4Q25 1Q26 Off-BS Credit Exposure & Debt Securities Loans ACL on Loans/Loans Key Highlights The allowance for credit losses (ACL) on loans and leases was $245.1 million, down $3.9 million vs. prior quarter; the ratio of the ACL on loans and finance leases to total loans held for investment decreased to 1.87% Variance was mainly related to lower consumer and commercial ACL due to improved macroeconomic variables, partially offset an increase in the mortgage ACL mostly due to loan growth Net charge-offs of $21.1 million, 0.65% of average loans, compared to $20.4 million or 0.63% in prior quarter, increase mostly driven by a $0.6 million charge-off associated with a nonaccrual CRE loan in the Virgin Islands Capital Ratios (%) $18.0 $16.6 $16.6 $11.2 $9.1 $17.9 $16.6 $16.6 $11.4 $9.6 $17.9 $16.7 $16.7 $11.5 $9.7 $18.0 $16.8 $16.8 $11.6 $10.1 $18.2 $16.9 $16.9 $11.7 $10.1 1Q25 2Q25 3Q25 4Q25 1Q26 Total Risk-Based Capital Tier-1 Capital Tier-1 Common Leverage Tangible Common Key Highlights Total stockholders’ equity amounted to $2.0 billion, an increase of $0.4 million vs. the prior quarter, driven by earnings generated during the quarter Partially offset by $50.0 million in common stock repurchases, $31.5 million in common stock dividends declared during the quarter, and a $6.2 million decrease in the fair value of available-for-sale debt securities due to changes in market rates recognized as part of accumulated other comprehensive loss All regulatory ratios remain significantly above “well-capitalized” levels 11

1Q 2026 Financial Results Appendix and Non-GAAP Financial Measures

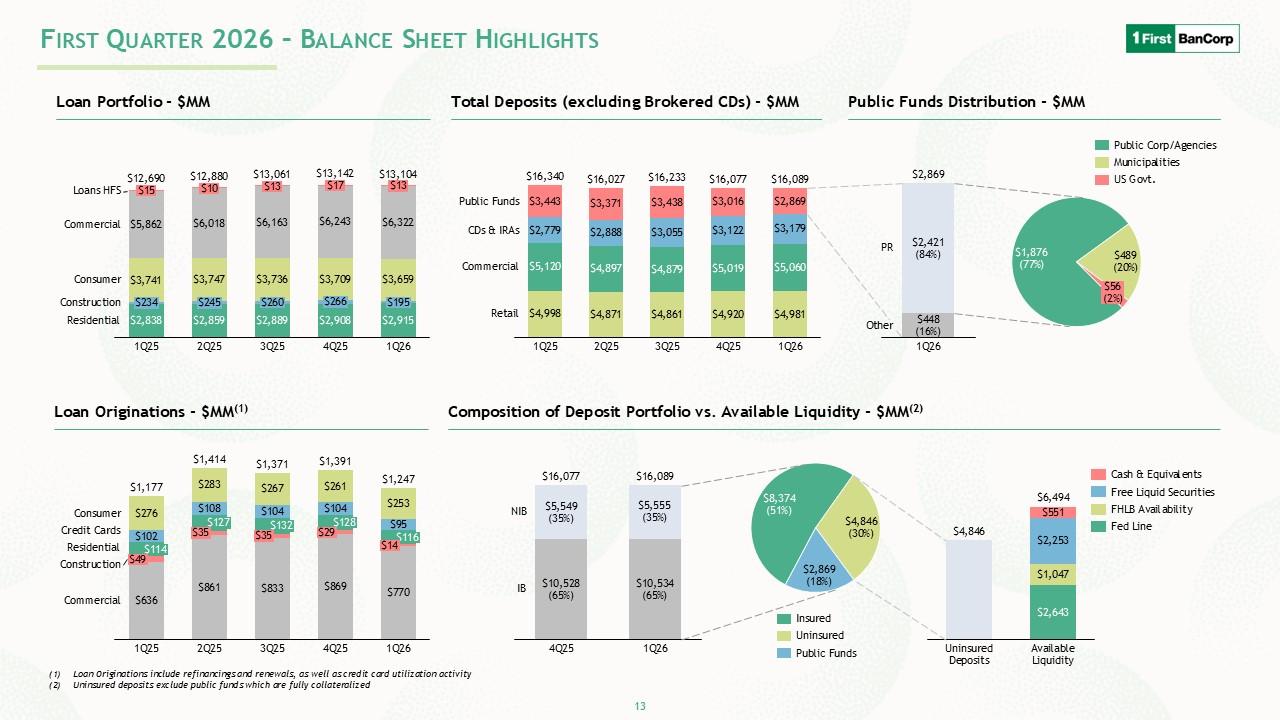

First Quarter 2026 – Balance Sheet Highlights Loan Portfolio - $MM $12,690.0 $12,880.0 $13,061.0 $13,142.0 $13,104.0 Loans HFS $15 $10 $13 $17 $13 Commercial $5,862 $6,018 $6,163 $6,243 $6,322 Consumer $3,741 $3,747 $3,736 $3,709 $3,659 Construction $234 $245 $260 $260 $195 Residential $2,838 $2,859 $2,889 $2,908 $2,915 1Q25 2Q25 3Q25 4Q25 1Q26 Total Deposits (excluding Brokered CDs) - $MM $16 $16,027 $16,233 $16,077 $16,089 Public Funds $3,443 $3,371 $3,438 $3,016 $2,869 CDs & IRAs $2,779 $2,888 $3,055 $3,122 $3,179 Commercial $5,120 $4,897 $4,879 $5,019 $5,060 Retail $4,998 $4,871 $4,861 $4,920 $4,981 1Q25 2Q25 3Q25 4Q25 1Q26 Public Funds Distribution - $MM $2 -84% PR $448 Other -16% 1Q26 $1,876 $489 $56 -77% -20% -2% Public Corp/Agencies Municipalities US Govt. Loan Originations - $MM(1) $1,177 $1,414 $1,371 $1,391 $1,247 Consumer $276 $283 $267 $261 $253 Credit Card $102 $106 $104 $104 $95 Residential $114 $127 $132 $128 $116 Construction $49 $35 $35 $29 $14 Commercial $4,998 $861 $833 $869 $770 1Q25 2Q25 3Q25 4Q25 1Q26 Composition of Deposit Portfolio vs. Available Liquidity - $MM(2) $16,077 $16,089 $5,549 $5,555 -35% -35% NIB $10,528 $10,534 IB -65% -65% 4Q25 1Q26 $8,374 $4,846 $2,869 -51% -30% -18% Cash & Equivalents Free Liquid Securities PHLB Avaialbility Fed Line (1) Loan Originations include refinancing and renewals, as well as credit card utilization activity (2) Uninsured deposits exclude public funds which are fully collateralized 13

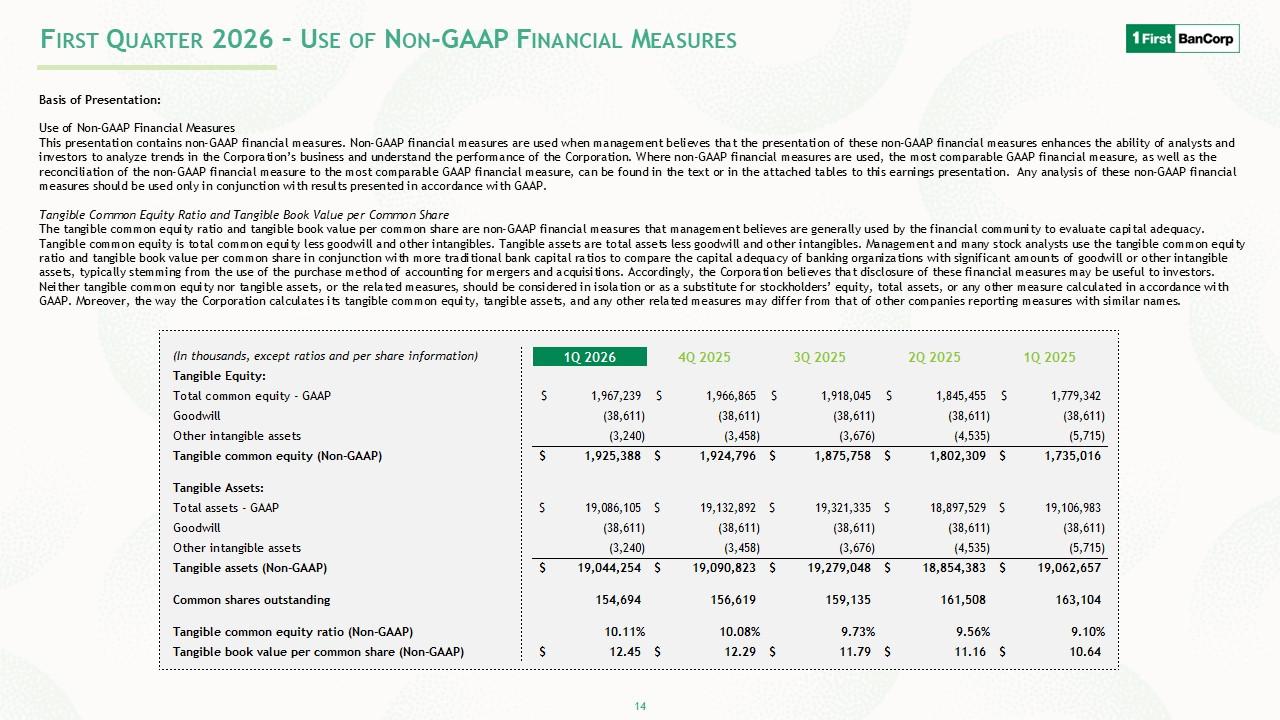

First Quarter 2026 – Use of Non-GAAP Financial Measures Basis of Presentation: Use of Non-GAAP Financial Measures This presentation contains non-GAAP financial measures. Non-GAAP financial measures are used when management believes that the presentation of these non-GAAP financial measures enhances the ability of analysts and investors to analyze trends in the Corporation’s business and understand the performance of the Corporation. Where non-GAAP financial measures are used, the most comparable GAAP financial measure, as well as the reconciliation of the non-GAAP financial measure to the most comparable GAAP financial measure, can be found in the text or in the attached tables to this earnings presentation. Any analysis of these non-GAAP financial measures should be used only in conjunction with results presented in accordance with GAAP. Tangible Common Equity Ratio and Tangible Book Value per Common Share The tangible common equity ratio and tangible book value per common share are non-GAAP financial measures that management believes are generally used by the financial community to evaluate capital adequacy. Tangible common equity is total common equity less goodwill and other intangibles. Tangible assets are total assets less goodwill and other intangibles. Management and many stock analysts use the tangible common equity ratio and tangible book value per common share in conjunction with more traditional bank capital ratios to compare the capital adequacy of banking organizations with significant amounts of goodwill or other intangible assets, typically stemming from the use of the purchase method of accounting for mergers and acquisitions. Accordingly, the Corporation believes that disclosure of these financial measures may be useful to investors. Neither tangible common equity nor tangible assets, or the related measures, should be

considered in isolation or as a substitute for stockholders’ equity, total assets, or any other measure calculated in accordance with GAAP. Moreover, the way the Corporation calculates its tangible common equity, tangible assets, and any other related measures may differ from that of other companies reporting measures with similar names. (In thousands, except ratios and per share information) 10 2026 1 40 2025 3Q2025 20 2025 10 2025 Tangible Equity: Total common equity - GAAP s 1,967,239 S 1,966,865 S 1,918,045 S 1,845,455 S 1,779,342 Goodwill (38,611) (38,611) (38,611) (38,611) (38,611) Other intangible assets (3,240) (3,458) (3,676) (4,535) (5,715) Tangible common equity (Non-GAAP) $ 1,925,388 $ 1,924,796 $ 1,875,758 $ 1,802,309 $ 1,735,016 Tangible Assets: Total assets - GAAP s 19,086,105 S 19,132,892 S 19,321,335 S 18,897,529 S 19,106,983 Goodwill (38,611) (38,611) (38,611) (38,611) (38,611) Other intangible assets (3,240) (3,458) (3,676) (4,535) (5,715) Tangible assets (Non-GAAP) $ 19,044,254 $ 19,090,823 $ 19,279,048 $ 18,854,383 $ 19,062,657 Common shares outstanding 154,694 156,619 159,135 161,508 163,104 Tangible common equity ratio (Non-GAAP) 10.11% 10.08% 9.73% 9.56% 9.10% Tangible book value per common share (Non-GAAP) $ 12.45 $ 12.29 $ 11.79 $ 11.16 $ 10.64 14

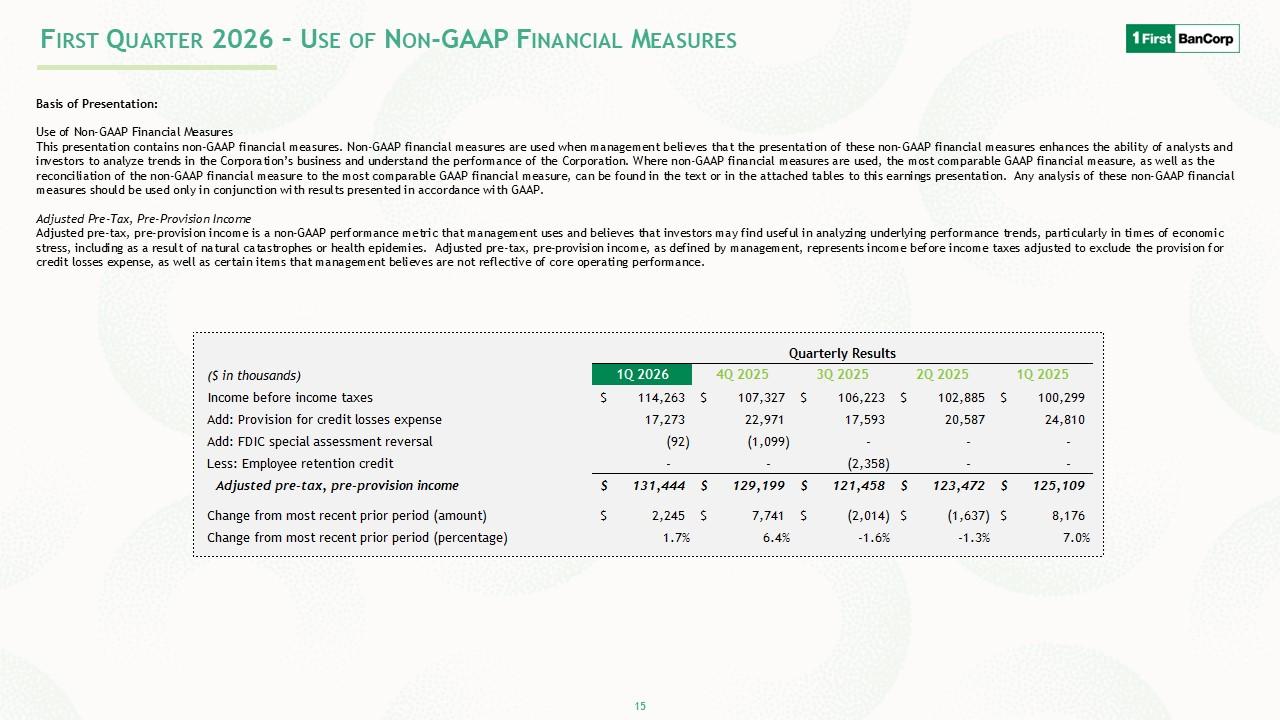

First Quarter 2026 – Use of Non-GAAP Financial Measures Basis of Presentation: Use of Non-GAAP Financial Measures This presentation contains non-GAAP financial measures. Non-GAAP financial measures are used when management believes that the presentation of these non-GAAP financial measures enhances the ability of analysts and investors to analyze trends in the Corporation’s business and understand the performance of the Corporation. Where non-GAAP financial measures are used, the most comparable GAAP financial measure, as well as the reconciliation of the non-GAAP financial measure to the most comparable GAAP financial measure, can be found in the text or in the attached tables to this earnings presentation. Any analysis of these non-GAAP financial measures should be used only in conjunction with results presented in accordance with GAAP. Adjusted Pre-Tax, Pre-Provision Income Adjusted pre-tax, pre-provision income is a non-GAAP performance metric that management uses and believes that investors may find useful in analyzing underlying performance trends, particularly in times of economic stress, including as a result of natural cat astrophes or health epidemies. Adjusted pre-tax, pre-provision income, as defined by management, represents income before income taxes adjusted to exclude the provision for credit losses expense, as well as certain items that management believes are not reflective of core operating performance. (S in thousands) Income before income taxes Add: Provision for credit losses expense Add: FDIC special assessment reversal Less: Employee retention credit Adjusted pre-tax, pre-provision income Change from most recent prior period (amount) Change from most recent prior period (percentage) Quarterly Results 10 2026 ! 40 2025 3Q2025 20 2025 1Q2025 S 114,263 S 107,327 S 106,223 S 102,885 S 100,299 17,273 22,971 17,593 20,587

24,810 (92) (1,099) - -s - - (-5 (2,358) - S 131,444 S 129,199 S 121,458 S 123,472 S 125,109 s 2,245 s 7,741 s (2,014) S (1,637) S 8,176 1.7% 6.4% -1.6% -1.3% 7.0% 15

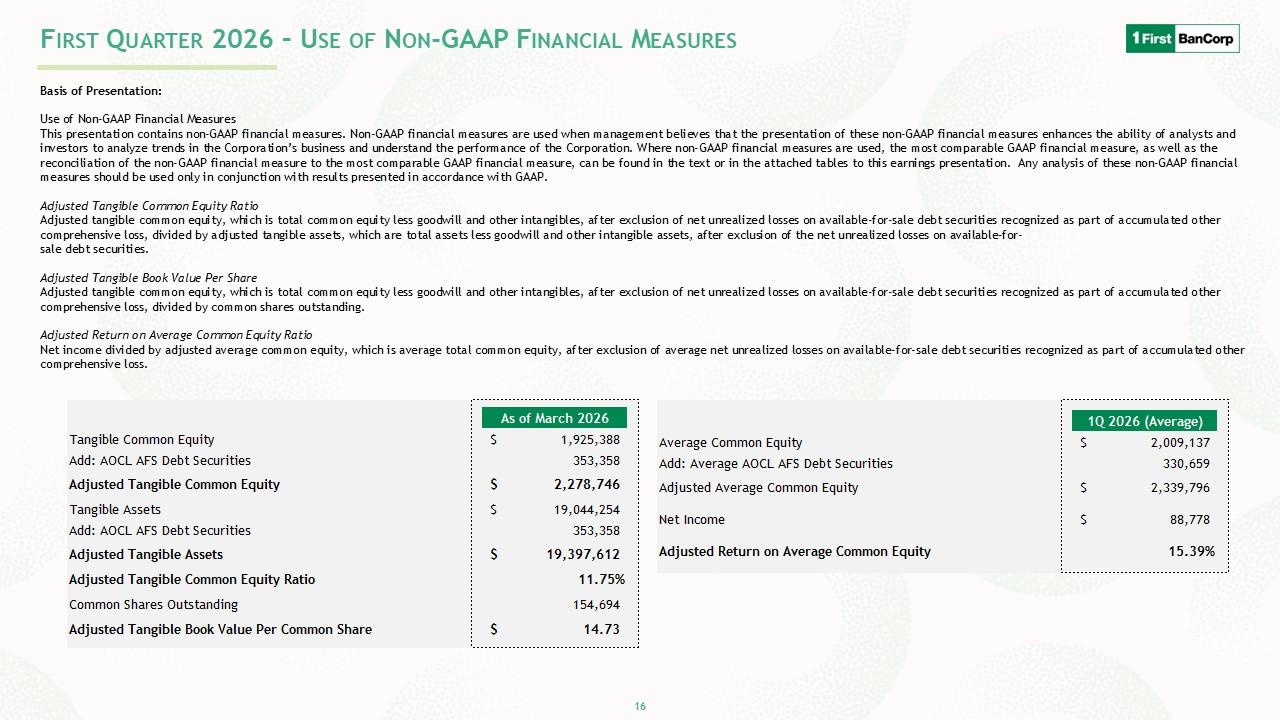

First Quarter 2026 – Use of Non-GAAP Financial Measures Basis of Presentation: Use of Non-GAAP Financial Measures This presentation contains non-GAAP financial measures. Non-GAAP financial measures are used when management believes that the presentation of these non-GAAP financial measures enhances the ability of analysts and investors to analyze trends in the Corporation’s business and understand the performance of the Corporation. Where non-GAAP financial measures are used, the most comparable GAAP financial measure, as well as the reconciliation of the non-GAAP financial measure to the most comparable GAAP financial measure, can be found in the text or in the attached tables to this earnings presentation. Any analysis of these non-GAAP financial measures should be used only in conjunction with results presented in accordance with GAAP. Adjusted Tangible Common Equity Ratio Adju sted tangible common equity, which is total common equity less goodwill and other intangibles, after exclusion of net unreali zed losses on available-for-sale debt securities recognized as part of accumulated other comprehensive loss and Special Items, divided by adjusted tangible assets, which are total assets less goodwill and other intangible assets, after exclusion of the net unrealized losses on available-for- sale debt securities. Adjusted Tangible Book Value Per Share Adjusted tangible common equity, which is total common equity less goodwill and other intangibles, after exclusion of net unrealized losses on available-for-sale debt securities recognized as part of accumulated other comprehensive loss, divided by common shares outstanding. Adjusted Return on Average Common Equity Ratio Net income divided by adjusted average common equity, which is average total common equity, after exclusion of average net unrealized losses on available-for-sale debt securities recognized as

part of accumulated other comprehensive loss. Tangible Common Equity Add: AOCL AFS Debt Securities Adjusted Tangible Common Equity Tangible Assets Add: AOCL AFS Debt Securities Adjusted Tangible Assets Adjusted Tangible Common Equity Ratio Common Shares Outstanding Adjusted Tangible Book Value Per Common Share As of March 2026 S 1,925,388 353,358 $ 2,278,746 s 19,044,254 353,358 $ 19,397,612 11.75% 154,694 s 14.73 Average Common Equity Add: Average AOCL AFS Debt Securities Adjusted Average Common Equity Net Income Adjusted Return on Average Common Equity 1Q2026 (Average) S 2,009,137 330,659 $ 2,339,796 s 88,778 15.39% 16

Financial Results First Quarter 2026 April 22, 2026