QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended September 30, 2025

Or

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number 1-14037

____________________

Moody’s Corporation

(Exact name of registrant as specified in its charter)

Delaware

13-3998945

(State of Incorporation)

(I.R.S. Employer Identification No.)

7 World Trade Center at 250 Greenwich Street, New York, New York10007

(Address of Principal Executive Offices)

(Zip Code)

Registrant’s telephone number, including area code:

(212)553-0300

Securities registered pursuant to Section 12(b) of the Act:

Title of each class

Trading Symbol(s)

Name of each exchange on which registered

Common Stock, par value $0.01 per share

MCO

New York Stock Exchange

1.75% Senior Notes Due 2027

MCO 27

New York Stock Exchange

0.950% Senior Notes Due 2030

MCO 30

New York Stock Exchange

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Sections 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically, every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large Accelerated Filer

☑

Accelerated filer

☐

Non-accelerated filer

☐

Smaller reporting company

☐

Emerging growth company

☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☑

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date:

Amortization expense relating to definite-lived intangible assets acquired by the Company from all business combination transactions

Adjusted Diluted EPS

Diluted EPS excluding the impact of certain items as detailed in the section entitled “Non-GAAP Financial Measures”

Adjusted Net Income

Net Income excluding the impact of certain items as detailed in the section entitled “Non-GAAP Financial Measures”

Adjusted Operating Income

Operating income excluding the impact of certain items as detailed in the section entitled “Non-GAAP Financial Measures”

Adjusted Operating Margin

Adjusted Operating Income divided by revenue

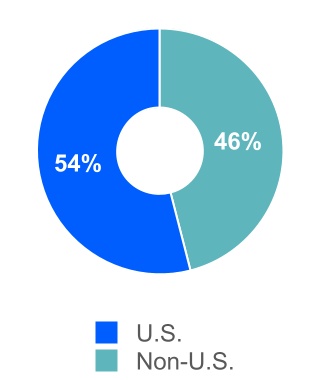

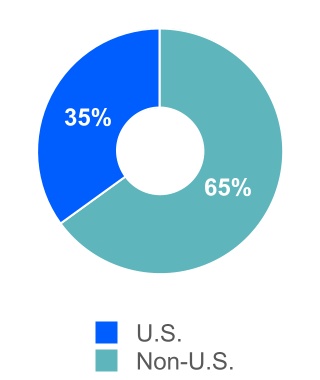

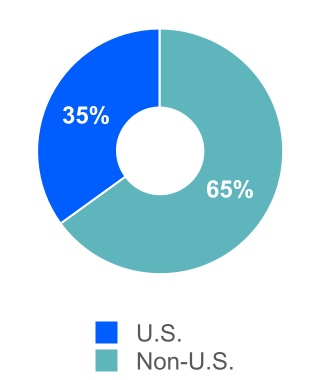

Americas

Represents countries within North and South America, excluding the U.S.

AOCI(L)

Accumulated other comprehensive income/loss; a separate component of shareholders’ equity

ARR

Annualized Recurring Revenue; a supplemental performance metric to provide additional insight on the estimated value of MA's recurring revenue contracts at a given point in time, excluding the impact of FX and contracts related to acquisitions

ASC

The FASB Accounting Standards Codification; the sole source of authoritative GAAP as of July 1, 2009, except for rules and interpretive releases of the SEC, which are also sources of authoritative GAAP for SEC registrants

Asia-Pacific

Represents Australia and countries in Asia including but not limited to: China, India, Indonesia, Japan, Republic of South Korea, Malaysia, Singapore, Sri Lanka and Thailand

ASU

The FASB Accounting Standards Update to the ASC. Provides background information for accounting guidance and the bases for conclusions on the changes in the ASC. ASUs are not considered authoritative until codified into the ASC

BitSight

A provider that helps global market participants understand cyber risk through ratings, analytics, and performance management tools; the Company acquired a minority investment in BitSight in 2021

Board

The board of directors of the Company

BPS

Basis points

CAD

Canadian dollar

CAPE Analytics

A provider of AI-powered property risk intelligence; the Company acquired CAPE Analytics in January 2025

CCXI

China Cheng Xin International Credit Rating Co. Ltd.; the first and largest domestic credit rating agency approved by the People’s Bank of China; the Company acquired a 49% interest in 2006 and currently owns 30% of CCXI

CEO

Chief Executive Officer

CFG

Corporate finance group; an LOB of MIS

CLO

Collateralized loan obligation

CMBS

Commercial mortgage-backed securities; an asset class within SFG

CODM

Chief Operating Decision Maker; identified as the Company's CEO

COLI

Corporate-Owned Life Insurance

Common Stock

The Company’s common stock

Company

Moody’s Corporation and its subsidiaries; MCO; Moody’s

Compensation expense

Compensation expenses include salaries, benefits, incentive and stock-based compensation and other related expenses for employees. These expenses are charged to income as incurred

CP

Commercial Paper

CP Program

A program entered into on August 3, 2016 allowing the Company to privately place CP up to a maximum of $1 billion for which the maturity may not exceed 397 days from the date of issue, and which is backstopped by the 2024 Facility

CRAs

Credit rating agencies

Data and Information (D&I)

LOB within MA which provides vast data sets on companies and securities via data feeds and data applications products

LOB within MA that provides subscription-based solutions supporting banking, insurance, and KYC workflows. This LOB utilizes components from the Data & Information and Research & Insights LOBs to provide risk assessment solutions

EMEA

Represents countries within Europe, the Middle East and Africa

EPS

Earnings per share

ESTR

Euro Short-Term Rate

ETR

Effective tax rate

EU

European Union

EUR

Euros

Excess Tax Benefits

The difference between the tax benefit realized at exercise of an option or delivery of a restricted share and the tax benefit recorded at the time the option or restricted share is expensed under GAAP

Exchange Act

The Securities Exchange Act of 1934, as amended

External Revenue

Revenue excluding any intersegment amounts

FASB

Financial Accounting Standards Board

FIG

Financial institutions group; an LOB of MIS

Free Cash Flow

Net cash provided by operating activities less cash paid for capital additions

FX

Foreign exchange

GAAP

U.S. Generally Accepted Accounting Principles

GBP

British pounds

GCR (Global Credit Rating Company Limited and subsidiaries)

A domestic credit rating agency with operations spanning Africa; the Company acquired a controlling financial interest in GCR in July 2024; the Company previously accounted for GCR as an equity method investment

GDP

Gross domestic product

GLoBE

Global Anti-Base Erosion, also known as "Pillar II;" tax model issued by the OECD in 2023

HKD

Hong Kong Dollars

ICRA

ICRA Limited; a provider of credit ratings and research in India

INR

Indian rupee

JPY

Japanese yen

KYC

Know-your-customer

LOB

Line of business

MA

Moody’s Analytics - a reportable segment of MCO; consists of three LOBs - Decision Solutions; Research and Insights; and Data and Information

MAKS

Moody’s Analytics Knowledge Services; formerly known as Copal Amba; provided offshore research and analytic services to the global financial and corporate sectors; business was divested in the fourth quarter of 2019 and was formerly a reporting unit within the MA reportable segment

MCO

Moody’s Corporation and its subsidiaries; the Company; Moody’s

MD&A

Management’s Discussion and Analysis of Financial Condition and Results of Operations

M&A

Mergers and acquisitions

MIS

Moody’s Investors Service - a reportable segment of MCO; consists of five LOBs - CFG; SFG; FIG; PPIF; and MIS Other

MIS Other

Consists of financial instruments pricing services in the Asia-Pacific region, ICRA non-ratings revenue, and revenue from professional services. These businesses are components of MIS; MIS Other is an LOB of MIS

Moody’s

Moody’s Corporation and its subsidiaries; MCO; the Company

MSS

Moody's Shared Services; primarily consists of information technology and support staff such as finance, human resources and legal that support both MA and MIS

Net Income

Net income attributable to Moody’s Corporation, which excludes net income from consolidated noncontrolling interests belonging to the minority interest holder

Non-compensation expenses include costs incurred that are not related to employee compensation. This includes, but is not limited to, consulting and professional service fees, hosting expenses, rent, and marketing expenses. These expenses are charged to income as incurred

Non-GAAP

A financial measure not in accordance with GAAP; these measures, when read in conjunction with the Company’s reported results, can provide useful supplemental information for investors analyzing period-to-period comparisons of the Company’s performance, facilitate comparisons to competitors’ operating results and to provide greater transparency to investors of supplemental information used by management in its financial and operational decision making

NRSRO

Nationally Recognized Statistical Rating Organization, which is a credit rating agency registered with the SEC

Numerated

A provider of commercial lending platforms; the Company acquired Numerated in November 2024

OBBBA

The “One Big Beautiful Bill Act” enacted into U.S. law on July 4, 2025

OCI(L)

Other comprehensive income (loss); includes gains and losses on cash flow and net investment hedges, certain gains and losses relating to pension and other retirement benefit obligations and foreign currency translation adjustments

OECD

Organization for Economic Co-operation and Development

Operating segment

Term defined in the ASC relating to segment reporting; the ASC defines an operating segment as a component of a business entity that has each of the three following characteristics: i) the component engages in business activities from which it may recognize revenue and incur expenses; ii) the operating results of the component are regularly reviewed by the entity’s CODM; and iii) discrete financial information about the component is available

Pillar II

Tax model issued by the OECD in 2023; also referred to as the "Global Anti-Base Erosion" or "GLoBE" rules

PPIF

Public, project and infrastructure finance; an LOB of MIS

Praedicat

A provider of casualty insurance analytics; the Company acquired a controlling financial interest in Praedicat in September 2024; the Company previously accounted for Praedicat as an equity method investment

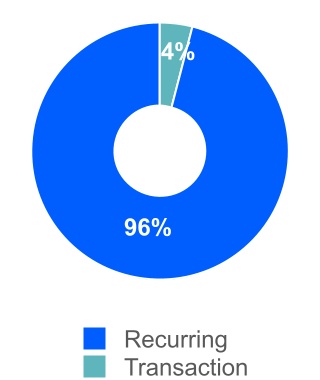

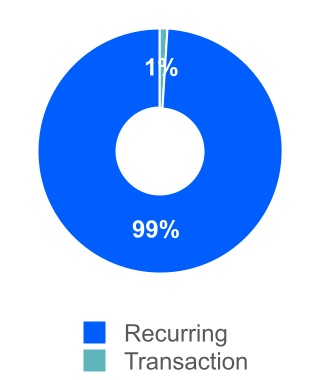

Recurring Revenue

For MA, represents subscription-based revenue and software maintenance revenue. For MIS, represents recurring monitoring fees of a rated debt obligation and/or entities that issue such obligations, as well as revenue from programs such as commercial paper, medium-term notes and shelf registrations. For MIS Other, represents financial instrument pricing services.

Reporting unit

The level at which Moody’s evaluates its goodwill for impairment under GAAP; defined as an operating segment or one level below an operating segment

Research and Insights (R&I)

LOB within MA thatprovides models, scores, expert insights and commentary. This LOB includes credit research; credit models and analytics; economics data and models; and structured finance solutions

RMBS

Residential mortgage-backed securities; an asset class within SFG

ROU Asset

Assets which represent the Company’s right to use an underlying asset for the term of a lease

SaaS

Software-as-a-Service

SEC

U.S. Securities and Exchange Commission

SFG

Structured finance group; an LOB of MIS

SG&A

Selling, general and administrative expenses

SGD

Singapore dollar

SOFR

Secured Overnight Financing Rate

Strategic and Operational Efficiency Restructuring Program

Multi-year restructuring program approved by the CEO of Moody’s on December 19, 2024 relating to the Company's strategy to realign the business toward high priority growth areas and to consolidate certain functions to simplify the organizational structure to enable efficiency and improved operating leverage; includes a reduction in staff, the rationalization and exit of certain real estate leases and incremental amortization of certain software

Tax Act

The “Tax Cuts and Jobs Act” enacted into U.S. law on December 22, 2017, which significantly amends the tax code in the U.S.

For MA, represents revenue from one-time sales, including those from perpetual software license fees, software implementation services, risk management advisory projects, and training and certification services. For MIS (excluding MIS Other), represents the initial rating of a new debt issuance as well as other one-time fees. For MIS Other, represents revenue from professional services.

(Amounts in millions, except share and per share data)

September 30, 2025

December 31, 2024

ASSETS

Current assets:

Cash and cash equivalents

$

2,181

$

2,408

Short-term investments

78

566

Accounts receivable, net of allowance for credit losses of $33 in 2025 and $32 in 2024

1,774

1,801

Other current assets

566

515

Total current assets

4,599

5,290

Property and equipment, net of accumulated depreciation of $1,506 in 2025 and $1,453 in 2024

712

656

Operating lease right-of-use assets

300

216

Goodwill

6,465

5,994

Intangible assets, net

1,916

1,890

Deferred tax assets, net

288

293

Other assets

1,135

1,166

Total assets

$

15,415

$

15,505

LIABILITIES AND SHAREHOLDERS' EQUITY

Current liabilities:

Accounts payable and accrued liabilities

$

1,032

$

1,344

Current portion of operating lease liabilities

98

102

Current portion of long-term debt

—

697

Deferred revenue

1,369

1,454

Total current liabilities

2,499

3,597

Non-current portion of deferred revenue

58

57

Long-term debt

6,983

6,731

Deferred tax liabilities, net

348

449

Uncertain tax positions

232

211

Operating lease liabilities

282

216

Other liabilities

901

517

Total liabilities

11,303

11,778

Contingencies (Note 16)

Shareholders' equity:

Preferred stock, par value $0.01 per share; 10,000,000 shares authorized; no shares issued and outstanding

—

—

Series common stock, par value $0.01 per share; 10,000,000 shares authorized; no shares issued and outstanding

—

Common stock, par value $0.01 per share; 1,000,000,000 shares authorized; 342,902,272 shares issued at September 30, 2025 and December 31, 2024, respectively

3

3

Capital surplus

1,617

1,451

Retained earnings

17,410

16,071

Treasury stock, at cost; 164,507,047 and 162,593,213 shares of common stock at September 30, 2025 and December 31, 2024, respectively

(14,535)

(13,322)

Accumulated other comprehensive loss

(538)

(638)

Total Moody's shareholders' equity

3,957

3,565

Noncontrolling interests

155

162

Total shareholders' equity

4,112

3,727

Total liabilities, noncontrolling interests and shareholders' equity

$

15,415

$

15,505

The accompanying notes are an integral part of the consolidated financial statements.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

(tabular dollar and share amounts in millions, except per share data)

NOTE 1. DESCRIPTION OF BUSINESS AND BASIS OF PRESENTATION

Moody’s is a global provider of integrated perspectives on risk that empowers organizations and investors to make better decisions. Moody’s reports in two reportable segments: MA and MIS.

MA is a global provider of: i) decision solutions; ii) research and insights; and iii) data and information, which help companies make better and faster decisions. MA leverages its industry expertise across multiple risks such as credit, market, financial crime, supply chain, catastrophe and climate to deliver integrated risk assessment solutions that enable business leaders to identify, measure and manage the implications of interrelated risks and opportunities.

MIS publishes credit ratings and provides assessment services on a wide range of debt obligations, programs and facilities, and the entities that issue such obligations in markets worldwide, including various corporate, financial institution and governmental obligations, and structured finance securities.

These interim financial statements have been prepared in accordance with the instructions to Form 10-Q and should be read in conjunction with the Company’s consolidated financial statements and related notes in the Company’s 2024 annual report on Form 10-K filed with the SEC on February 14, 2025. The results of interim periods are not necessarily indicative of results for the full year or any subsequent period. In the opinion of management, all adjustments (including normal recurring accruals) considered necessary for a fair presentation of financial position, results of operations and cash flows at the dates and for the periods presented have been included. The year-end consolidated balance sheet data was derived from audited financial statements, but does not include all disclosures required by GAAP.

Certain reclassifications have been made to prior period amounts to conform to the current presentation.

Recently Issued Accounting Standards

In December 2023, the FASB issued ASU 2023-09, "Income Taxes (Topic 740): Improvements to Income Tax Disclosures" ("ASU No. 2023-09"), which is intended to enhance the transparency and decision usefulness of income tax disclosures. The amendments in ASU No. 2023-09 require entities to disclose additional income tax information, primarily related to greater disaggregation of the entity's ETR reconciliation and income taxes paid by jurisdiction disclosures. This ASU is effective for annual periods beginning after December 15, 2024, and should be applied on a prospective basis; however, retrospective application is permitted. The Company is prepared to adopt and comply with the disclosure requirements set forth in this ASU upon its effective date.

In November 2024, the FASB issued ASU 2024-03, "Income Statement—Reporting Comprehensive Income—Expense Disaggregation Disclosures (Subtopic 220-40): Disaggregation of Income Statement Expenses" ("ASU No. 2024-03"). The amendments in this ASU require more detailed disclosures about specific expense categories in the notes to financial statements (including employee compensation, depreciation and intangible asset amortization) and apply to both interim and annual reporting periods. ASU No. 2024-03 also requires disclosure of total selling expenses for both interim and annual reporting periods, with an additional requirement to provide an entity’s definition of selling expenses in annual reporting. This ASU is effective in fiscal years beginning after December 15, 2026, and interim periods within fiscal years beginning after December 15, 2027. Early adoption is permitted. The amendments in this ASU should be applied either (1) prospectively for annual and interim reporting periods beginning after the aforementioned effective dates or (2) retrospectively to any or all prior periods presented in the financial statements. The Company is currently evaluating the impact of adopting this ASU on its consolidated financial statements and disclosures.

In July 2025, the FASB issued ASU 2025-05, "Financial Instruments—Credit Losses (Topic 326): Measurement of Credit Losses for Accounts Receivable and Contract Assets", which amends Topic 326 to provide a practical expedient and an accounting policy election related to the estimation of expected credit losses for current accounts receivable and current contract assets that arise from transactions accounted for under ASC 606. Specifically, in developing reasonable and supportable forecasts as part of estimating expected credit losses on accounts receivable, entities may elect a practical expedient that assumes that current conditions as of the balance sheet date do not change for the remaining life of the asset. This ASU is effective for annual reporting periods beginning after December 15, 2025, and interim reporting periods within those annual reporting periods, with early adoption permitted. Entities should apply the new guidance prospectively. The Company does not expect the adoption of this ASU to have a material impact on its financial statements.

In September 2025, the FASB issued ASU 2025-06 "Intangibles—Goodwill and Other—Internal-Use Software (Subtopic 350-40): Targeted Improvements to the Accounting for Internal-Use Software" ("ASU No. 2025-06"). This ASU eliminates prescriptive software development stages and requires capitalization of software costs when (1) management commits to funding the project, and (2) completion and intended use are probable, with consideration to when significant uncertainty associated with the development activities of the software no longer exists. This ASU also clarifies the disclosure requirements for internal-use software costs and supersedes prior guidance on website development costs. This ASU is effective for annual reporting periods beginning after December 15, 2027, with early adoption permitted. Entities may transition using prospective, modified prospective, or retrospective approaches. The Company is currently evaluating the impact of adopting this ASU on its consolidated financial statements and disclosures.

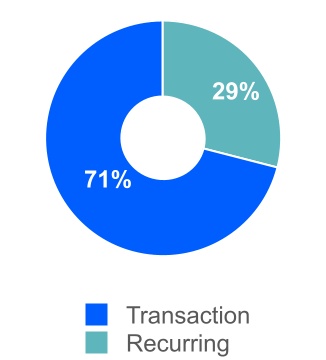

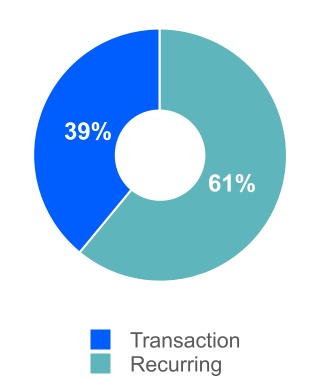

Reclassification of Previously Reported Transaction and Recurring Revenue

In the first quarter of 2025, the Company reclassified certain prior-year transaction and recurring revenue amounts to align with a refined classification methodology. The impact of the reclassifications was not material, and the reclassified amounts for 2024 are reflected in Note 3.

NOTE 2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

This update should be read in conjunction with the summary of significant accounting policies disclosures made in the Company's Form 10-K for the year ended December 31, 2024. All significant accounting policies described in the Form 10-K for the year ended December 31, 2024 remain unchanged with the exception of the following update:

Goodwill

Moody’s evaluates its goodwill for impairment at the reporting unit level, defined as an operating segment (i.e., MA and MIS), or one level below an operating segment (i.e., a component of an operating segment). Prior to 2025, MA's reporting unit structure consisted of two reporting units comprised of businesses that offer: i) data and data-driven analytical solutions; and ii) risk-management software, workflow and CRE solutions. During the first quarter of 2025, MA reorganized its management and reporting structure, which affected the composition of the reporting units within the MA reportable segment. As a result, MA's reporting unit structure now consists of one reporting unit, which is consistent with the segment's current management structure and operating model. This reorganization did not result in a change to the Company's reportable segments. The Company performed assessments of the reporting units impacted by the reorganization immediately before and after the reorganization became effective and determined that it was not more likely than not that the fair value of any reporting unit was less than its carrying amount.

Subsequent to the aforementioned reorganization of the MA reporting unit structure, the Company now has three reporting units: two within the Company’s ratings business (one for the ICRA business and one that encompasses all of Moody’s other ratings operations) and one reporting unit within MA.

The following table presents the Company’s revenues disaggregated by LOB:

Three Months Ended

September 30,

Nine Months Ended September 30,

2025

2024

2025

2024

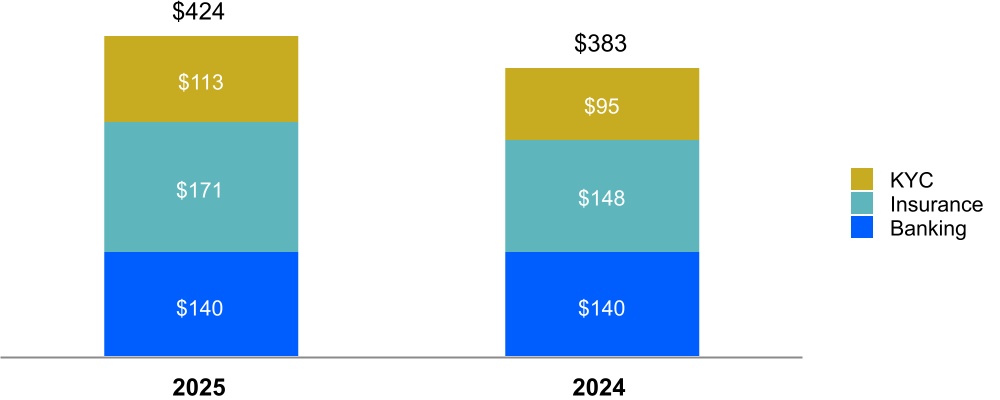

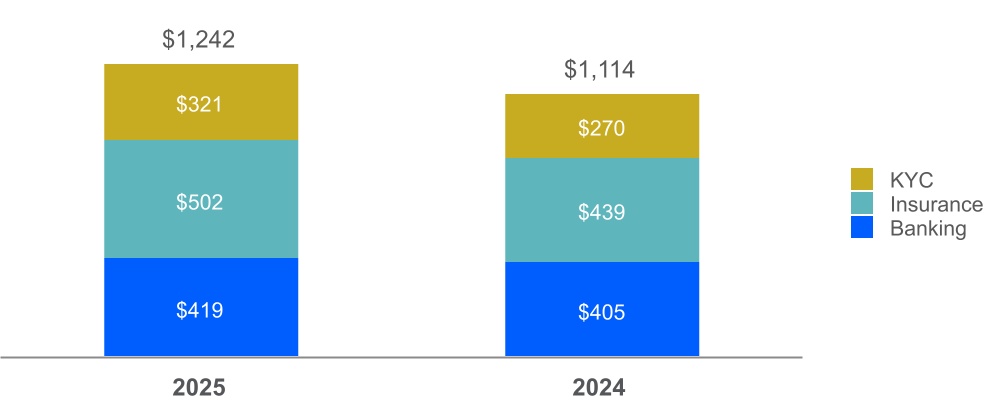

MA:

Decision Solutions (DS)

Banking

$

140

$

140

$

419

$

405

Insurance

171

148

502

439

KYC

113

95

321

270

Total DS

424

383

1,242

1,114

Research and Insights (R&I)

252

235

737

683

Data and Information (D&I)

233

213

677

635

Total external revenue

909

831

2,656

2,432

Intersegment revenue

3

3

9

10

Total MA

912

834

2,665

2,442

MIS:

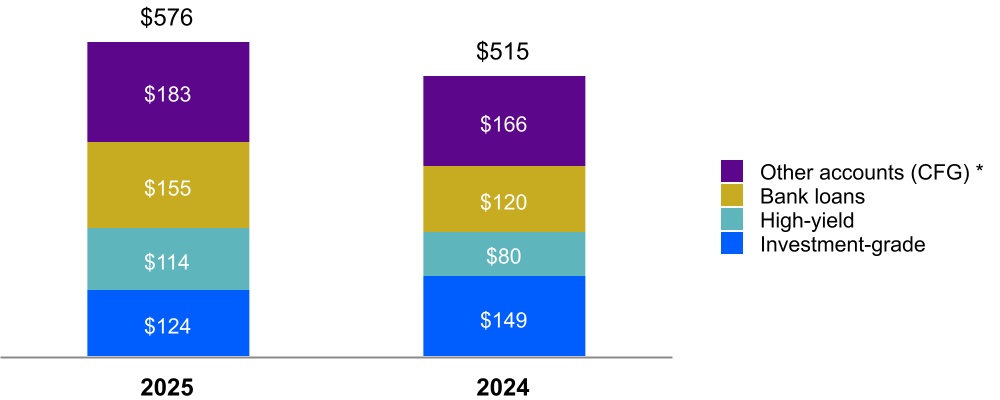

Corporate Finance (CFG)

Investment-grade

124

149

431

416

High-yield

114

80

266

232

Bank loans

155

120

413

422

Other accounts (1)

183

166

542

499

Total CFG

576

515

1,652

1,569

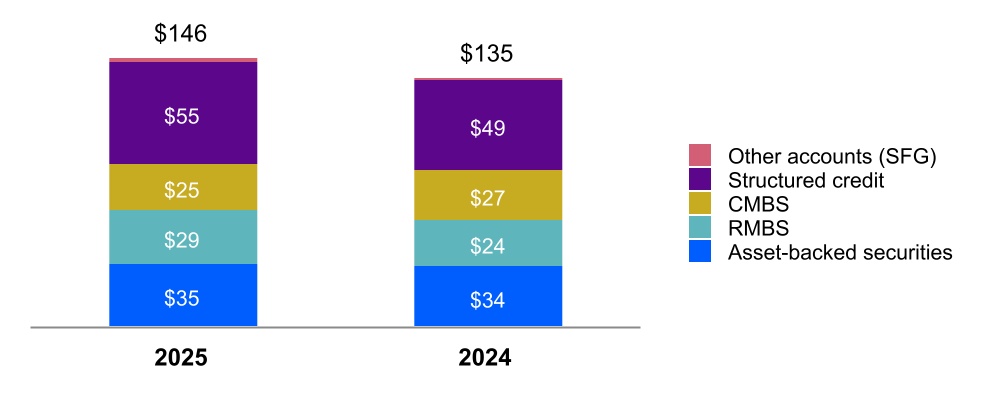

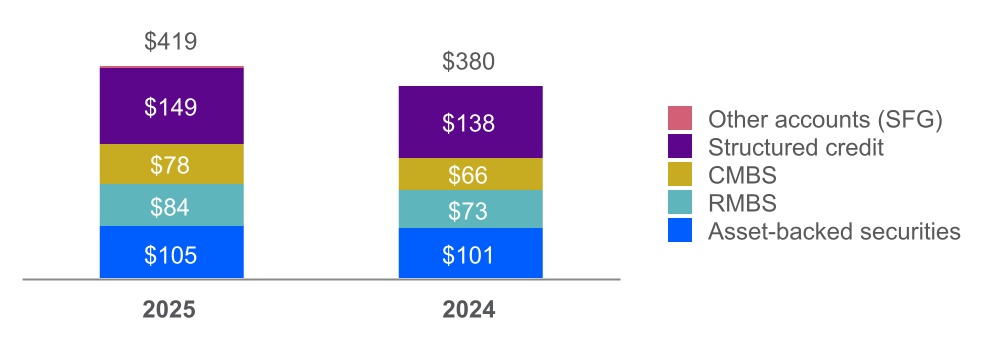

Structured Finance (SFG)

Asset-backed securities

35

34

105

101

RMBS

29

24

84

73

CMBS

25

27

78

66

Structured credit

55

49

149

138

Other accounts

2

1

3

2

Total SFG

146

135

419

380

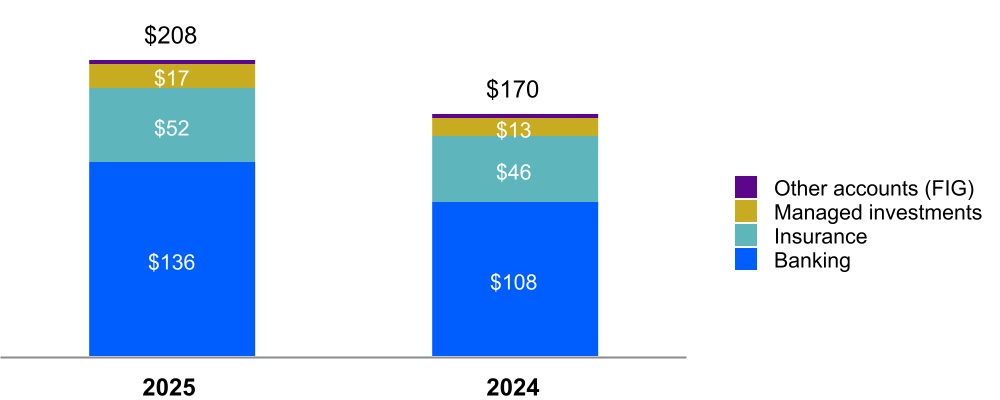

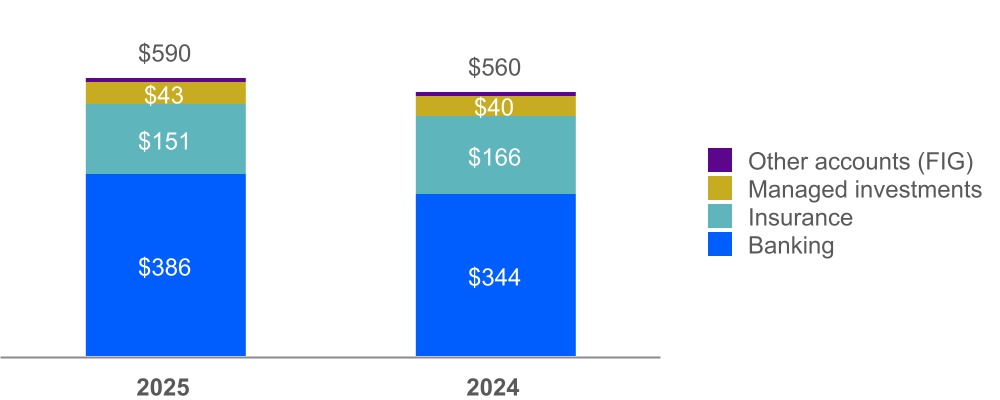

Financial Institutions (FIG)

Banking

136

108

386

344

Insurance

52

46

151

166

Managed investments

17

13

43

40

Other accounts

3

3

10

10

Total FIG

208

170

590

560

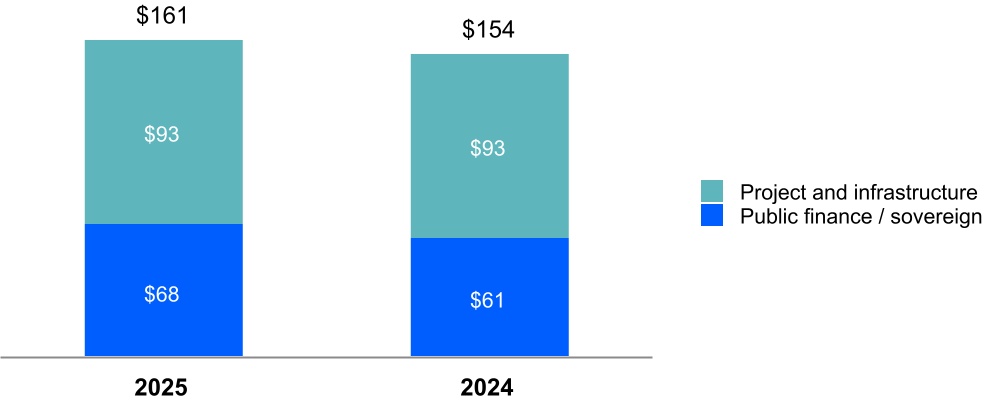

Public, Project and Infrastructure Finance (PPIF)

Public finance / sovereign

68

61

215

187

Project and infrastructure

93

93

271

262

Total PPIF

161

154

486

449

Total ratings revenue

1,091

974

3,147

2,958

MIS Other

7

8

26

26

Total external revenue

1,098

982

3,173

2,984

Intersegment revenue

50

48

149

144

Total MIS

1,148

1,030

3,322

3,128

Eliminations

(53)

(51)

(158)

(154)

Total MCO

$

2,007

$

1,813

$

5,829

$

5,416

(1) Other includes: recurring monitoring fees of a rated debt obligation and/or entities that issue such obligations as well as fees from programs such as commercial paper, medium term notes, and ICRA corporate finance revenue.

(1) Revenue from software implementation services and risk management advisory projects, while classified by management as transactional revenue, is recognized over time under GAAP.

The following tables present the timing of revenue recognition:

Unbilled receivables, deferred revenue and remaining performance obligations

Unbilled receivables

For certain MA arrangements, the timing of when the Company has the unconditional right to consideration and recognizes revenue occurs prior to invoicing the customer. In addition, certain MIS arrangements contain contractual terms whereby the customers are billed in arrears for annual monitoring services, requiring revenue to be accrued as an unbilled receivable as such services are provided.

The following table presents the Company's unbilled receivables, which are included within accounts receivable, net, at September 30, 2025 and December 31, 2024:

As of September 30, 2025

As of December 31, 2024

MA

MIS

MA

MIS

Unbilled Receivables

$

114

$

530

$

122

$

426

Deferred revenue

The Company recognizes deferred revenue when a contract requires a customer to pay consideration to the Company in advance of when revenue related to that contract is recognized. This deferred revenue is relieved when the Company satisfies the related performance obligation and revenue is recognized.

Significant changes in the deferred revenue balances during the three and nine months ended September 30, 2025 and 2024 are as follows:

Three Months Ended September 30, 2025

Three Months Ended September 30, 2024

MA

MIS

Total

MA

MIS

Total

Balance at June 30,

$

1,285

$

350

$

1,635

$

1,146

$

336

$

1,482

Changes in deferred revenue:

Revenue recognized that was included in the deferred revenue balance at the beginning of the period

(612)

(123)

(735)

(551)

(120)

(671)

Increases due to amounts billable excluding amounts recognized as revenue during the period

491

87

578

410

92

502

Reclassification to liabilities held-for-sale (1)

$

(23)

—

(23)

—

—

—

Increases due to acquisitions during the period

—

—

—

5

5

Effect of exchange rate changes

(27)

(1)

(28)

37

4

41

Total changes in deferred revenue

(171)

(37)

(208)

(99)

(24)

(123)

Balance at September 30,

$

1,114

$

313

$

1,427

$

1,047

$

312

$

1,359

(1) The 2025 reclassification to liabilities held-for-sale for the MA segment in the table above relate to the planned divestiture of the MA Learning Solutions business, more fully discussed in Note 12.

Revenue recognized that was included in the deferred revenue balance at the beginning of the period

(1,074)

(205)

(1,279)

(950)

(197)

(1,147)

Increases due to amounts billable excluding amounts recognized as revenue during the period

910

239

1,149

860

238

1,098

Reclassification to liabilities held-for-sale (1)

$

(23)

—

(23)

—

—

—

Increases due to acquisitions during the period

15

15

5

—

5

Effect of exchange rate changes

43

11

54

21

1

22

Total changes in deferred revenue

(129)

45

(84)

(64)

42

(22)

Balance at September 30,

$

1,114

$

313

$

1,427

$

1,047

$

312

$

1,359

Deferred revenue - current

$

1,113

$

256

$

1,369

$

1,047

$

253

$

1,300

Deferred revenue - non-current

$

1

$

57

$

58

$

—

$

59

$

59

(1) The 2025 reclassification to liabilities held-for-sale for the MA segment in the table above relate to the planned divestiture of the MA Learning Solutions business, more fully discussed in Note 12

For the MA segment, the decrease in deferred revenue for the three months ended September 30, 2025 and 2024 was primarily due to the recognition of annual subscription and maintenance revenue for the period, for which billing occurs in December and January. For the nine months ended September 30, 2025 and 2024, the decrease in the deferred revenue balance is attributable to recognition of revenues related to the aforementioned December billings being mostly offset by the impact of the high concentration of billings in the first quarter..

For the MIS segment, the change in the deferred revenue balance for all periods presented was primarily related to the significant portion of contract renewals that occur during the first quarter and are generally recognized over a one year period.

Remaining performance obligation

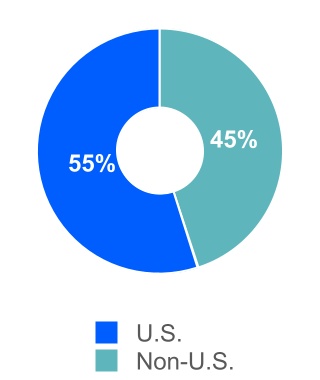

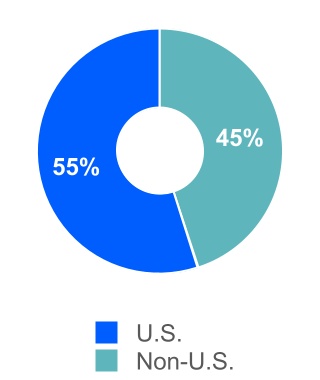

Remaining performance obligations in the MA segment include both amounts recorded as deferred revenue on the balance sheet as of September 30, 2025 as well as amounts not yet invoiced to customers as of September 30, 2025, largely reflecting future revenue related to signed multi-year arrangements for hosted and installed subscription-based products. As of September 30, 2025, the aggregate amount of the transaction price allocated to remaining performance obligations was approximately $4.1 billion. The Company expects to recognize into revenue approximately 55% of this balance within one year, approximately 25% of this balance between one to two years and the remaining amount thereafter.

Remaining performance obligations in the MIS segment largely reflect deferred revenue related to monitoring fees for certain structured finance products, primarily CMBS, where the issuers can elect to pay the monitoring fees for the life of the security in advance. As of September 30, 2025, the aggregate amount of the transaction price allocated to remaining performance obligations was approximately $87 million. The Company expects to recognize into revenue approximately 25% of this balance within one year, approximately 50% of this balance between one to five years and the remaining amount thereafter. With respect to the remaining performance obligations for the MIS segment, the Company has applied a practical expedient set forth in ASC Topic 606 permitting the omission of unsatisfied performance obligations relating to contracts with an original expected length of one year or less.

Presented below is a summary of the stock-based compensation cost and associated tax benefit included in the accompanying consolidated statements of operations:

Three Months Ended September 30,

Nine Months Ended September 30,

2025

2024

2025

2024

Stock-based compensation cost

$

58

$

57

$

176

$

166

Tax benefit

$

13

$

12

$

38

$

36

During the first nine months of 2025, the Company granted 0.1 million employee stock options, which had a weighted average grant date fair value of $163.59 per share. The Company also granted 0.4 million shares of restricted stock in the first nine months of 2025, which had a weighted average grant date fair value of $512.07 per share. Both the employee stock options and restricted stock generally vest ratably over four years. Additionally, the Company granted 0.1 million shares of performance-based awards whereby the number of shares that ultimately vest is based on the achievement of certain non-market-based performance metrics of the Company over three years. The weighted average grant date fair value of these awards was $501.88 per share.

The following weighted average assumptions were used in determining the fair value using the Black-Scholes option-pricing model for options granted in 2025:

Expected dividend yield

0.73

%

Expected stock volatility

27

%

Risk-free interest rate

4.51

%

Expected holding period

5.6 years

Unrecognized stock-based compensation expense at September 30, 2025 was $11 million and $287 million for unvested stock options and restricted stock, respectively, which is expected to be recognized over a weighted average period of 2.0 years and 2.5 years, respectively. Additionally, there was $59 million of unrecognized stock-based compensation expense relating to the aforementioned non-market-based performance-based awards, which is expected to be recognized over a weighted average period of 1.8 years.

The following table summarizes information relating to stock option exercises and restricted stock vesting:

Nine Months Ended September 30,

2025

2024

Exercise of stock options:

Proceeds from stock option exercises

$

26

$

44

Aggregate intrinsic value

$

42

$

60

Tax benefit realized upon exercise

$

9

$

10

Number of shares exercised

0.1

0.3

Vesting of restricted stock:

Fair value of shares vested

$

245

$

183

Tax benefit realized upon vesting

$

60

$

45

Number of shares vested

0.5

0.5

Vesting of performance-based restricted stock:

Fair value of shares vested

$

8

$

40

Tax benefit realized upon vesting

$

1

$

9

Number of shares vested (1)

—

0.1

(1) The number of shares vested in 2025 was approximately 15 thousand.

Moody’s ETR was 25.4% and 24.0% for the three months ended September 30, 2025 and 2024, respectively. The increase of 1.4% primarily reflects tax benefits recognized in the third quarter of 2024, which resulted from the resolutions of uncertain tax positions, coupled with an increase in current year state income taxes.

Moody’s ETR was 24.2% and 23.5% for the nine months ended September 30, 2025 and 2024, respectively. The year-to-date ETR as of September 30, 2025 was generally in line with the same period in the prior year. The Company’s provision for income taxes for the nine months ended September 30, 2025 differs from the tax computed by applying its estimated annual ETR to the pre-tax earnings primarily due to the excess tax benefits from stock-based compensation of $30 million.

The Company classifies interest related to UTPs in interest expense, net in its consolidated statements of operations. Penalties, if incurred, would be recognized in other non-operating income, net. The Company had an increase in its UTP reserves of $5 million, during the third quarter of 2025 (both on a gross basis and net of federal tax benefits) and an increase of $21 million ($19 million, net of federal tax benefits) during the first nine months of 2025.

Moody’s is subject to U.S. federal income tax as well as income tax in various state, local and foreign jurisdictions. The Company's U.S. federal income tax returns for 2021 through 2024 remain open to examination. The Company’s New York City tax returns for 2018 through 2022 are currently under examination, and 2023 is open to examination. The Company's U.K. corporate income tax returns are currently under audit for years 2017 through 2021, while years 2022 through 2023 remain open to examination.

In the fourth quarter of 2025, pursuant to a lapse of a statute of limitations, the Company expects to reverse $64 million in reserves (and $15 million in related interest) for uncertain tax positions that it had assumed as part of a prior year M&A transaction, for which the sellers had indemnified Moody's. This tax benefit and related reduction to Interest expense, net will be offset by the release of the related indemnification asset within Other non-operating income, net, with no impact to net income. For ongoing audits, it is possible the balance of UTPs could decrease in the next twelve months as a result of the settlement of such audits, which might involve the payment of additional taxes, the adjustment of certain deferred taxes and/or the recognition of tax benefits. It is also possible that new issues will be raised by tax authorities which could necessitate increases to the balance of UTPs. As the Company is unable to predict the timing or outcome of these audits, it is unable to estimate the amount of future changes to the balance of UTPs at this time. However, the Company believes that it has adequately provided for its financial exposure relating to all open tax years, by tax jurisdiction, in accordance with the applicable provisions of ASC Topic 740 regarding UTPs.

The following table shows the amount the Company paid for income taxes:

Nine Months Ended September 30,

2025

2024

Income taxes paid

$

644

$

391

On July 4, 2025, the One Big Beautiful Bill Act was enacted in the U.S. Key provisions of the OBBBA include making permanent certain aspects of the Tax Act, modifying certain international tax rules, and restoring provisions that accelerate deductions for certain business investments and expenditures. The legislation has multiple effective dates, with certain provisions effective in 2025 and others implemented in subsequent years. The OBBBA did not have material impact on the Company’s consolidated financial statements for the period ended September 30, 2025, and the Company does not expect the changes to have a material impact on the provision for income taxes or net income in future periods.

Effective in 2024, multiple foreign jurisdictions in which the Company operates enacted legislation to adopt a minimum tax rate described in the Global Anti-Base Erosion tax model rules (referred to as GloBE or Pillar II) issued by the OECD. A minimum ETR of 15% applies to multinational companies with consolidated revenue above €750 million. Under the GloBE rules, a company is required to determine a combined ETR for all entities located in a jurisdiction. If the jurisdictional effective tax rate is less than 15%, an additional tax generally will be due to bring the jurisdictional ETR up to 15%. We have evaluated the impact of the Pillar II global minimum tax rules on our consolidated financial statements and related disclosures. As of September 30, 2025, the Pillar II minimum tax requirement is not expected to have a material impact on our full-year results of operations or financial position.

NOTE 6. RECONCILIATION OF WEIGHTED AVERAGE SHARES OUTSTANDING

Below is a reconciliation of basic to diluted shares outstanding:

Three Months Ended September 30,

Nine Months Ended September 30,

2025

2024

2025

2024

Basic

178.9

181.7

179.5

182.2

Dilutive effect of shares issuable under stock-based compensation plans

0.7

0.8

0.7

0.8

Diluted

179.6

182.5

180.2

183.0

Anti-dilutive options to purchase common shares and restricted stock as well as contingently issuable restricted stock which are excluded from the table above

0.2

0.3

0.2

0.4

The calculation of basic shares outstanding is based on the weighted average number of shares of common stock outstanding during the reporting period. The calculation of diluted EPS requires certain assumptions regarding the use of both cash proceeds and assumed proceeds that would be received upon the exercise of stock options and vesting of restricted stock outstanding as of September 30, 2025 and 2024.

NOTE 7. CASH EQUIVALENTS AND INVESTMENTS

The table below provides additional information on the Company’s cash equivalents and investments:

As of September 30, 2025

Balance sheet location

Cost

Gains/(Losses)

Fair Value

Cash and cash equivalents

Short-term investments

Other assets

Certificates of deposit and money market deposit accounts/funds (1)

$

1,228

$

—

$

1,228

$

1,149

$

78

$

1

Mutual funds

$

91

$

14

$

105

$

—

$

—

$

105

As of December 31, 2024

Balance sheet location

Cost

Gains/(Losses)

Fair Value

Cash and cash equivalents

Short-term investments

Other assets

Certificates of deposit and money market deposit accounts/funds (1)

$

1,911

$

—

$

1,911

$

1,345

$

566

$

—

Mutual funds

$

88

$

10

$

98

$

—

$

—

$

98

(1) Consists of time deposits, money market deposit accounts and money market funds. The remaining contractual maturities for the certificates of deposits classified as short-term investments are one month to 12 months at both September 30, 2025 and December 31, 2024. The remaining contractual maturities for the certificates of deposits classified in other assets are 16 months to 23 monthsat September 30, 2025. Time deposits with a maturity of less than 90 days at time of purchase are classified as cash and cash equivalents.

In addition, the Company invested in COLI. As of September 30, 2025 and December 31, 2024, the contract value of the COLI was $50 million and $48 million, respectively.

NOTE 8. DERIVATIVE INSTRUMENTS AND HEDGING ACTIVITIES

The Company is exposed to global market risks, including risks from changes in FX rates and changes in interest rates. Accordingly, the Company uses derivatives in certain instances to manage financial exposures that occur in the normal course of business. The Company does not hold or issue derivatives for speculative purposes.

Derivatives and non-derivative instruments designated as accounting hedges:

Fair Value Hedges

Interest Rate Swaps

The Company has entered into interest rate swaps to convert the fixed interest rate on certain of its long-term debt to a floating interest rate based on the SOFR. The purpose of these hedges is to mitigate the risk associated with changes in the fair value of the long-term debt, thus the Company has designated these swaps as fair value hedges. The fair value of the swaps is adjusted quarterly with a corresponding adjustment to the carrying value of the debt. The changes in the fair value of the swaps and the underlying hedged item generally offset and the net cash settlements on the swaps are recorded each period within interest expense, net in the Company’s consolidated statements of operations.

The following table summarizes the Company’s interest rate swaps designated as fair value hedges:

Notional Amount

Hedged Item

Nature of Swap

As of

September 30, 2025

As of December 31, 2024

Floating Interest Rate

2014 Senior Notes due 2044

Pay Floating/Receive Fixed

$

300

$

300

SOFR

2017 Senior Notes due 2028

Pay Floating/Receive Fixed

500

500

SOFR

2018 Senior Notes due 2029

Pay Floating/Receive Fixed

400

400

SOFR

2018 Senior Notes due 2048

Pay Floating/Receive Fixed

300

300

SOFR

2020 Senior Notes due 2025

Pay Floating/Receive Fixed

—

300

SOFR

2022 Senior Notes due 2052

Pay Floating/Receive Fixed

500

500

SOFR

2022 Senior Notes due 2032

Pay Floating/Receive Fixed

250

250

SOFR

Total

$

2,250

$

2,550

Refer to Note 14 for information on the cumulative amount of fair value hedging adjustments included in the carrying amount of the above hedged items.

The following table summarizes the impact to the statements of operations of the Company’s interest rate swaps designated as fair value hedges:

Total amounts of financial statement line item presented in the statements of operations in which the effects of fair value hedges are recorded

Amount of income/(loss) recognized in the consolidated statements of operations

Three Months Ended September 30,

Nine Months Ended September 30,

2025

2024

2025

2024

Interest expense, net

$

(58)

$

(60)

$

(180)

$

(185)

Description

Location on Consolidated Statements of Operations

Net interest settlements and accruals on interest rate swaps

The Company has designated €500 million of the 2015 Senior Notes Due 2027 and €750 million of the 2019 Senior Notes due 2030 as net investment hedges to mitigate FX exposure related to a portion of the Company’s euro net investment in certain foreign subsidiaries against changes in euro/USD exchange rates. These hedges are designated as accounting hedges under the applicable sections of ASC Topic 815 and will end upon the repayment of the notes in 2027 and 2030, respectively, unless terminated early at the discretion of the Company.

Cross currency swaps designated as net investment hedges

The Company enters into cross-currency swaps to mitigate FX exposure related to a portion of the Company’s net investment in certain foreign subsidiaries against changes in exchange rates. The following tables provide information on the cross-currency swaps designated as net investment hedges under ASC Topic 815:

September 30, 2025

Pay

Receive

Nature of Swap

Notional Amount (1)

Weighted Average Interest Rate

Notional Amount

Weighted Average Interest Rate

Pay Fixed/Receive Fixed

€

1,997

2.48%

$

2,114

3.98%

Pay Floating/Receive Floating

€

1,688

Based on ESTR

$

1,750

Based on SOFR

Pay Fixed/Receive Fixed

HK$

3,907

—%

$

500

0.64%

Pay Fixed/Receive Fixed

S$

389

—%

HK$

2,350

0.62%

(1) € = euro, HK$ = Hong Kong dollar, S$ = Singapore dollar

As of September 30, 2025 these hedges will expire and the notional amounts will be settled as follows unless terminated early at the discretion of the Company:

EUR/USD

HKD/USD

SGD/HKD

Years Ending December 31,

Notional Amount (Pay) (1)

Notional Amount (Receive)

Notional Amount (Pay) (1)

Notional Amount (Receive)

Notional Amount (Pay) (1)

Notional Amount (Receive) (1)

2027

€

530

$

550

HK$

—

$

—

S$

—

HK$

—

2028

588

600

—

—

—

—

2029

573

614

—

—

—

—

2030

662

700

—

—

—

—

2031

481

500

—

—

—

—

2032

481

500

3,907

500

389

2,350

2033

370

400

—

—

—

—

Total

€

3,685

$

3,864

HK$

3,907

$

500

S$

389

HK$

2,350

(1) € = euro, HK$ = Hong Kong dollar, S$ = Singapore dollar

The following table provides information on the gains/(losses) on the Company’s net investment and cash flow hedges:

Derivative and Non-Derivative Instruments in Net Investment Hedging Relationships

Amount of Gain/(Loss) Recognized in AOCL on Derivative, net of Tax

Amount of Loss Reclassified from AOCL into Income, net of Tax

Gain Recognized in Income on Derivative (Amount Excluded from Effectiveness Testing)

Three Months Ended

September 30,

Three Months Ended

September 30,

Three Months Ended

September 30,

2025

2024

2025

2024

2025

2024

Cross currency swaps

$

6

$

(95)

$

—

$

—

$

17

$

12

Long-term debt

(1)

(41)

—

—

—

—

Total net investment hedges

$

5

$

(136)

$

—

$

—

$

17

$

12

Derivatives in Cash Flow Hedging Relationships

Cross currency swap

$

—

$

—

$

1

$

—

$

—

$

—

Interest rate contracts

$

—

$

—

$

(1)

$

(1)

$

—

$

—

Total cash flow hedges

$

—

$

—

$

—

$

(1)

$

—

$

—

Total

$

5

$

(136)

$

—

$

(1)

$

17

$

12

Derivative and Non-Derivative Instruments in Net Investment Hedging Relationships

Amount of Gain/(Loss) Recognized in AOCL on Derivative, net of Tax

Amount of Loss Reclassified from AOCL into Income, net of Tax

Gain Recognized in Income on Derivative (Amount Excluded from Effectiveness Testing)

The cumulative amount of net investment hedge and cash flow hedge gains (losses) remaining in AOCL is as follows:

Cumulative Gains (Losses), net of tax

September 30, 2025

December 31, 2024

Net investment hedges

Cross currency swaps

$

(181)

$

178

FX forwards

29

29

Long-term debt

(62)

68

Total net investment hedges

$

(214)

$

275

Cash flow hedges

Interest rate contracts

$

(41)

$

(43)

Cross currency swaps

—

1

Total cash flow hedges

(41)

(42)

Total net gain in AOCL

$

(255)

$

233

Derivatives not designated as accounting hedges:

Foreign exchange forwards

The Company also enters into foreign exchange forward contracts to mitigate the change in fair value on certain assets and liabilities denominated in currencies other than a subsidiary’s functional currency. These forward contracts are not designated as accounting hedges under the applicable sections of ASC Topic 815. Accordingly, changes in the fair value of these contracts are recognized immediately in other non-operating income, net, in the Company’s consolidated statements of operations along with the FX gain or loss recognized on the assets and liabilities denominated in a currency other than the subsidiary’s functional currency. These contracts have expiration dates at various times through December 2025.

The following table summarizes the notional amounts of the Company’s outstanding foreign exchange forwards:

September 30, 2025

December 31, 2024

Notional amount of currency pair (1):

Sell

Buy

Sell

Buy

Contracts to sell USD for GBP

$

597

£

442

$

604

£

470

Contracts to sell USD for JPY

$

24

¥

3,500

$

29

¥

4,000

Contracts to sell USD for CAD

$

38

C$

53

$

35

C$

50

Contracts to sell USD for SGD

$

74

S$

95

$

45

S$

59

Contracts to sell USD for EUR

$

105

€

89

$

—

€

—

Contracts to sell USD for INR

$

20

₹

1,729

$

23

₹

1,900

Contracts to sell EUR for USD

€

—

$

—

€

12

$

12

(1) € = euro, £ = British pound, S$ = Singapore dollar, $ = U.S. dollar, ¥ = Japanese yen, C$ = Canadian dollar, ₹= Indian Rupee

Total Return Swaps

The Company has entered into total return swaps to mitigate market-driven changes in the value of certain liabilities associated with the Company's deferred compensation plans. The fair value of these swaps at September 30, 2025 and related gains in the three and nine months ended September 30, 2025 were not material. The notional amount of the total return swaps as of September 30, 2025 and December 31, 2024 was $72 million and $66 million, respectively.

The following table summarizes the impact to the consolidated statements of operations relating to the gains (losses) on the Company’s derivatives which are not designated as hedging instruments:

The table below shows the classification between assets and liabilities on the Company’s consolidated balance sheets for the fair value of the derivative instrument as well as the carrying value of its non-derivative debt instruments designated and qualifying as net investment hedges:

Derivative and Non-Derivative Instruments

Balance Sheet Location

September 30, 2025

December 31, 2024

Assets:

Derivatives designated as accounting hedges:

Cross-currency swaps designated as net investment hedges

Other assets

$

—

$

58

Derivatives not designated as accounting hedges:

FX forwards on certain assets and liabilities

Other current assets

2

—

Total assets

$

2

$

58

Liabilities:

Derivatives designated as accounting hedges:

Interest rate swaps designated as fair value hedges

Accounts payable and accrued liabilities

$

4

$

3

Cross-currency swaps designated as net investment hedges

Other liabilities

480

26

Interest rate swaps designated as fair value hedges

NOTE 9. GOODWILL AND OTHER ACQUIRED INTANGIBLE ASSETS

The following table summarizes the activity in goodwill for the periods indicated:

Nine Months Ended September 30, 2025

MA

MIS

Consolidated

Gross goodwill

Accumulated impairment charge

Net goodwill

Gross goodwill

Accumulated impairment charge

Net goodwill

Gross goodwill

Accumulated impairment charge

Net goodwill

Balance at beginning of year

$

5,626

$

(12)

$

5,614

$

380

$

—

$

380

$

6,006

$

(12)

$

5,994

Additions/

adjustments (1)

136

—

136

8

—

8

144

—

144

Foreign currency translation adjustments

336

—

336

—

—

—

336

—

336

Reclassification to assets held-for-sale (2)

(9)

—

(9)

—

—

—

(9)

—

(9)

Ending balance

$

6,089

$

(12)

$

6,077

$

388

$

—

$

388

$

6,477

$

(12)

$

6,465

Year Ended December 31, 2024

MA

MIS

Consolidated

Gross goodwill

Accumulated

impairment

charge

Net

goodwill

Gross goodwill

Accumulated impairment

charge

Net

goodwill

Gross goodwill

Accumulated

impairment

charge

Net

goodwill

Balance at beginning of year

$

5,681

$

(12)

$

5,669

$

287

$

—

$

287

$

5,968

$

(12)

$

5,956

Additions/

adjustments (3)

112

—

112

97

—

97

209

—

209

Foreign currency translation adjustments

(167)

—

(167)

(4)

—

(4)

(171)

—

(171)

Ending balance

$

5,626

$

(12)

$

5,614

$

380

$

—

$

380

$

6,006

$

(12)

$

5,994

(1) The 2025 additions relate to the acquisition of CAPE Analytics and ICR Chile in 2025.

(2) The 2025 reclassification to assets held-for-sale for the MA segment in the table above relate to the planned divestiture of the MA Learning Solutions business, more fully discussed in Note 12.

(3) The 2024 additions/adjustments primarily relate to certain immaterial acquisitions in 2024 (most notably GCR, Numerated and Praedicat).

Acquired intangible assets and related amortization consisted of:

September 30, 2025

December 31, 2024

Customer relationships

$

2,149

$

2,035

Accumulated amortization

(686)

(631)

Net customer relationships

1,463

1,404

Software/product technology

774

695

Accumulated amortization

(507)

(419)

Net software/product technology

267

276

Database

163

166

Accumulated amortization

(99)

(89)

Net database

64

77

Trade names

200

199

Accumulated amortization

(91)

(83)

Net trade names

109

116

Other (1)

63

67

Accumulated amortization

(50)

(50)

Net other

13

17

Total acquired intangible assets, net (2)

$

1,916

$

1,890

(1) Other intangible assets primarily consist of trade secrets, covenants not to compete, and acquired ratings methodologies and models.

(2) Excludes approximately $15M of net acquired intangible assets, which were reclassified to assets held-for-sale related to the planned divestiture of the MA Learning Solutions business, more fully discussed in Note 12.

Amortization expense relating to acquired intangible assets is as follows:

Three Months Ended

September 30,

Nine Months Ended September 30,

2025

2024

2025

2024

Amortization expense

$

55

$

51

$

163

$

148

NOTE 10. RESTRUCTURING

On December 19, 2024, the CEO of Moody’s approved the Strategic and Operational Efficiency Restructuring Program. The Company estimates that upon completion, the program will result in annualized savings of $250 million to $300 million. This program relates to the Company's strategy to realign its operations toward high priority growth areas and to consolidate certain functions to simplify the organization to enable improved operating efficiency and leverage. This program will primarily include a reduction in staff, the rationalization and exit of certain leased office spaces and the retirement of certain legacy software applications. The program includes $170 million to $200 million of expected pre-tax personnel-related restructuring charges, an amount that includes severance costs, expense related to the modification of equity awards and other related costs primarily determined under the Company’s existing severance plans. In addition, the program is expected to result in $10 million to $20 million of non-cash charges from the exit from certain leased office spaces and $20 million to $30 million of non-cash charges related to incremental amortization of internally developed software due to a reduction in the useful life of the software assets. The savings generated from the Strategic and Operational Efficiency Restructuring Program are expected to strengthen the Company's operating margin, with a portion being deployed to support strategic investments. The Strategic and Operational Efficiency Restructuring Program is expected to be substantially complete by the end of 2026. Cash outlays associated with this program are expected to be $170 million to $200 million, which are expected to be paid through 2027.

Total expense included in the accompanying consolidated statements of operations relating to the aforementioned restructuring program is below:

Three months ended September 30,

Nine months ended September 30,

Cumulative expense incurred

2025

2024

2025

2024

Strategic and Operational Efficiency Restructuring Program

Employee termination and other related costs (1)

$

21

$

—

$

75

$

—

$

120

Real estate related costs (2)

—

—

4

—

4

Internally developed software-related charges (3)

—

—

2

—

2

Total Restructuring

$

21

$

—

$

81

$

—

$

126

(1) Primarily includes severance costs, expense related to the modification of equity awards and professional service fees related to execution of the restructuring program.

(2) Includes the non-cash acceleration of amortization of ROU Assets that have been abandoned or for which abandonment is planned in future periods.

(3) Includes the non-cash acceleration of amortization of internally developed software that has been abandoned.

Changes to the restructuring liability for the aforementioned restructuring program were as follows:

Balance as of December 31, 2024

$

39

Strategic and Operational Efficiency Restructuring Program:

Cost incurred and adjustments

72

Cash payments

(79)

Balance as of September 30, 2025 (1)

$

32

(1) Restructuring liability is primarily comprised of employee termination costs and other severance-related charges.

As of September 30, 2025, substantially all of the remaining $32 million restructuring liability is expected to be paid out in the next twelve months.

The tables below present information about items that are carried at fair value at September 30, 2025 and December 31, 2024:

Fair Value Measurement as of September 30, 2025

Description

Balance

Level 1

Level 2

Assets:

Derivatives (1)

$

2

$

—

$

2

Money market funds/mutual funds

115

115

—

Total

$

117

$

115

$

2

Liabilities:

Derivatives (1)

$

578

$

—

$

578

Total

$

578

$

—

$

578

Fair Value Measurement as of December 31, 2024

Description

Balance

Level 1

Level 2

Assets:

Derivatives (1)

$

58

$

—

$

58

Money market funds/mutual funds

108

108

—

Total

$

166

$

108

$

58

Liabilities:

Derivatives (1)

$

216

$

—

$

216

Total

$

216

$

—

$

216

(1) Represents fair value of certain derivative contracts as more fully described in Note 8 to the consolidated financial statements.

The following are descriptions of the methodologies utilized by the Company to estimate the fair value of its derivative contracts, money market mutual funds and mutual funds:

Derivatives:

In determining the fair value of the derivative contracts in the table above, the Company utilizes industry standard valuation models. Where applicable, these models project future cash flows and discount the future amounts to a present value using spot rates, forward points, currency volatilities, interest rates as well as the risk of non-performance of the Company and the counterparties with whom it has derivative contracts. The Company established strict counterparty credit guidelines and only enters into transactions with financial institutions that adhere to these guidelines. Accordingly, the risk of counterparty default is deemed to be minimal.

Money market funds and mutual funds:

The mutual funds in the table above are deemed to be equity securities with readily determinable fair values with changes in the fair value recognized through net income under ASC Topic 321. The fair value of these instruments is determined using Level 1 inputs as defined in the ASC Topic 820.

Derivative instruments designated as accounting hedges

570

192

Other

41

52

Total other liabilities

$

901

$

517

Assets and Liabilities Held-for-Sale

In August 2025, the Company entered into a definitive agreement to sell the MA Learning Solutions business. As of September 30, 2025, the assets and liabilities related to this business, which are not material, are classified as held-for-sale. The Company expects the transaction to close during the fourth quarter of 2025.

Investments in non-consolidated affiliates:

The following table provides additional detail regarding Moody's investments in non-consolidated affiliates, as included in other assets in the consolidated balance sheets:

September 30, 2025

December 31, 2024

Equity method investments (1)

$

119

$

127

Investments measured using the measurement alternative (2)

350

328

Other

14

10

Total investments in non-consolidated affiliates

$

483

$

465

(1) Equity securities in which the Company has significant influence over the investee but does not have a controlling financial interest in accordance with ASC Topic 323.

(2) Equity securities without readily determinable fair value for which the Company has elected to apply the measurement alternative in accordance with ASC Topic 321.

Moody's holds various investments accounted for under the equity method, the most significant of which is the Company's minority investment in CCXI. Moody's also holds various investments measured using the measurement alternative, the most significant of which is the Company's minority interest in BitSight.

Earnings from non-consolidated affiliates, which are included within other non-operating income, net, are disclosed within the table below.

Other non-operating income, net:

The following table summarizes the components of other non-operating income, net:

Three months ended September 30,

Nine Months Ended September 30,

2025

2024

2025

2024

FX gains (losses)

$

(7)

$

—

$

(10)

$

(7)

Net periodic pension income - non-service and non-interest cost components

9

9

27

25

Income from investments in non-consolidated affiliates

4

8

18

10

Gain on previously held equity method investments (1)

—

7

—

7

Gain on investments

3

4

8

12

Other

(1)

(3)

(1)

(2)

Total

$

8

$

25

$

42

$

45

(1) The amounts for the three and nine months ended September 30, 2024 reflect non-cash gains relating to the step-acquisitions of Praedicat and GCR.

Charges related to asset abandonment:

During the three and nine months ended September 30, 2025, the Company recorded severance charges pursuant to a reduction in staff due to the Company's decision in 2024 to outsource the production of certain sustainability content utilized in our product offerings. During the three and nine months ended September 30, 2024, the Company incurred severance charges and

incremental amortization expense related to the change in estimated useful lives of certain internally developed software and amortizable intangible assets that are associated with the sustainability content offerings for which production is being outsourced. Cumulative charges relating to this action as of September 30, 2025 were $47 million.

NOTE 13. COMPREHENSIVE INCOME AND ACCUMULATED OTHER COMPREHENSIVE LOSS

The amounts reclassified out of AOCL, as shown in the consolidated statements of comprehensive income, were not material for all periods presented.

The following tables show changes in AOCL by component (net of tax):

Three Months Ended September 30,

2025

2024

Gains/(Losses)

Pension and Other Retirement Benefits

Cash Flow Hedges

Foreign Currency Translation Adjustments

Net Investment Hedges

Total

Pension and Other Retirement Benefits

Cash Flow Hedges

Foreign Currency Translation Adjustments

Net Investment Hedges

Total

Balance at June 30,

$

(41)

$

(41)

$

(218)

$

(219)

$

(519)

$

(59)

$

(43)

$

(674)

$

159

$

(617)

Other comprehensive income (loss) before reclassifications

—

—

(24)

5

(19)

—

—

249

(136)

113

Amounts reclassified from AOCL

—

—

—

—

—

—

1

—

—

1

Other comprehensive income (loss)

—

—

(24)

5

(19)

—

1

249

(136)

114

Balance at September 30,

$

(41)

$

(41)

$

(242)

$

(214)

$

(538)

$

(59)

$

(42)

$

(425)

$

23

$

(503)

Nine Months Ended September 30,

2025

2024

Pension and Other Retirement Benefits

Cash Flow Hedges

Foreign Currency Translation Adjustments

Net Investment Hedges

Total

Pension and Other Retirement Benefits

Cash Flow Hedges

Foreign Currency Translation Adjustments

Net Investment Hedges

Total

Balance at December 31,

$

(39)

$

(42)

$

(832)

$

275

$

(638)

$

(56)

$

(44)

$

(520)

$

53

$

(567)

Other comprehensive income (loss) before reclassifications

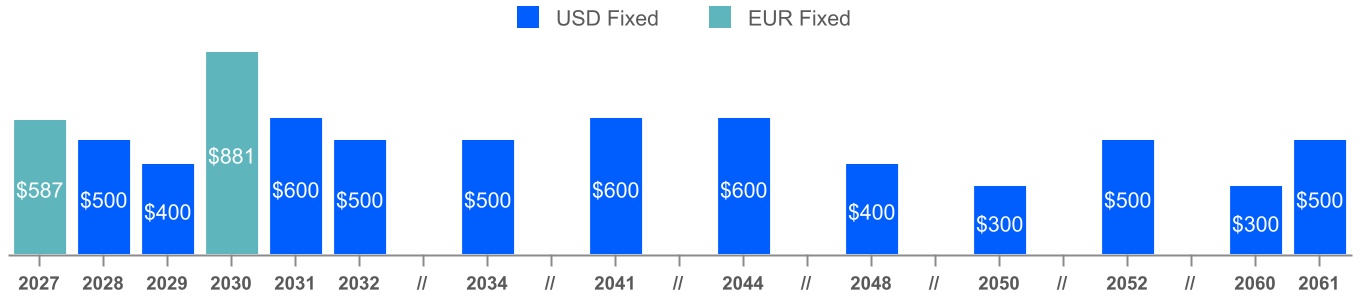

The Company’s debt is recorded at its carrying value, which represents the issuance amount plus or minus any issuance premium or discount, except for certain debt as depicted in the table below, which is recorded at the carrying value adjusted for the fair value of an interest rate swap used to hedge the fair value of the note.

The following table summarizes total indebtedness:

September 30, 2025

Notes Payable:

Principal Amount

Fair Value of Interest Rate Swaps (1)

Unamortized (Discount) Premium

Unamortized Debt Issuance Costs

Carrying Value

5.25% 2014 Senior Notes, due 2044

$

600

$

(20)

$

3

$

(4)

$

579

1.75% 2015 Senior Notes, due 2027

587

—

—

(1)

586

3.25% 2017 Senior Notes, due 2028

500

(4)

(1)

(1)

494

4.25% 2018 Senior Notes, due 2029

400

(21)

(1)

(1)

377

4.875% 2018 Senior Notes, due 2048

400

(23)

(6)

(3)

368

0.950% 2019 Senior Notes, due 2030

881

—

(1)

(3)

877

3.25% 2020 Senior Notes, due 2050

300

—

(4)

(3)

293

2.55% 2020 Senior Notes, due 2060

300

—

(2)

(3)

295

2.00% 2021 Senior Notes, due 2031

600

—

(5)

(3)

592

2.75% 2021 Senior Notes, due 2041

600

—

(12)

(4)

584

3.10% 2021 Senior Notes, due 2061

500

—

(6)

(5)

489

3.75% 2022 Senior Notes, due 2052

500

(23)

(8)

(4)

465

4.25% 2022 Senior Notes, due 2032

500

(3)

(2)

(3)

492

5.00% 2024 Senior Notes, due 2034

500

—

(4)

(4)

492

Total long-term debt

$

7,168

$

(94)

$

(49)

$

(42)

$

6,983

December 31, 2024

Notes Payable:

Principal Amount

Fair Value of Interest Rate Swaps (1)

Unamortized (Discount) Premium

Unamortized Debt Issuance Costs

Carrying Value

5.25% 2014 Senior Notes, due 2044

$

600

$

(32)

$

3

$

(4)

$

567

1.75% 2015 Senior Notes, due 2027

518

—

—

(1)

517

3.25% 2017 Senior Notes, due 2028

500

(13)

(2)

(1)

484

4.25% 2018 Senior Notes, due 2029

400

(35)

(1)

(1)

363

4.875% 2018 Senior Notes, due 2048

400

(35)

(6)

(3)

356

0.950% 2019 Senior Notes, due 2030

776

—

(1)

(3)

772

3.75% 2020 Senior Notes, due 2025

700

(3)

—

—

697

3.25% 2020 Senior Notes, due 2050

300

—

(4)

(3)

293

2.55% 2020 Senior Notes, due 2060

300

—

(2)

(3)

295

2.00% 2021 Senior Notes, due 2031

600

—

(6)

(4)

590

2.75% 2021 Senior Notes, due 2041

600

—

(12)

(5)

583

3.10% 2021 Senior Notes, due 2061

500

—

(7)

(5)

488

3.75% 2022 Senior Notes, due 2052

500

(43)

(8)

(5)

444

4.25% 2022 Senior Notes, due 2032

500

(8)

(2)

(3)

487