Please wait

|

.2

MANAGEMENT’S DISCUSSION & ANALYSIS

|

MANAGEMENT’S DISCUSSION & ANALYSIS

FOR THE YEAR ENDED DECEMBER 31, 2019

|

|

|

|

TABLE OF CONTENTS

|

|

|

2019 PERFORMANCE

HIGHLIGHTS

|

2

|

|

ABOUT

DENISON

|

3

|

|

URANIUM INDUSTRY

OVERVIEW

|

4

|

|

RESULTS OF

OPERATIONS

|

7

|

|

Wheeler River

Project

|

11

|

|

Exploration Pipeline

Properties

|

24

|

|

OUTLOOK FOR

2020

|

35

|

|

ADDITIONAL

INFORMATION

|

37

|

|

CAITIONARY

STATEMENT REGARDING FORWARD-LOOKING

STATEMENTS

|

49

|

|

|

|

This

Management’s Discussion and Analysis (‘MD&A’)

of Denison Mines Corp. and its subsidiary companies, joint

arrangements, and contractual arrangements (collectively,

‘Denison’ or the ‘Company’) provides a

detailed analysis of the Company’s business and compares its

financial results with those of the previous year. This MD&A is

dated as of March 5, 2020 and should be read in conjunction with

the Company’s audited consolidated financial statements and

related notes for the year ended December 31, 2019. The audited

consolidated financial statements are prepared in accordance with

International Financial Reporting Standards (‘IFRS’) as

issued by the International Accounting Standards Board

(‘IASB’). All dollar amounts in this MD&A are

expressed in Canadian dollars, unless otherwise noted.

Additional

information about Denison, including the Company’s press

releases, quarterly and annual reports, Annual Information Form and

Form 40-F is available through the Company’s filings with the

securities regulatory authorities in Canada at www.sedar.com

(‘SEDAR’) and the United States at

www.sec.gov/edgar.shtml (‘EDGAR’).

|

|

MANAGEMENT’S DISCUSSION & ANALYSIS

|

2019 PERFORMANCE

HIGHLIGHTS

■

Initiation of the Environmental Assessment (‘EA’) at

Wheeler River

During the first

quarter of 2019, Denison submitted a Project Description

(‘PD’) to the Canadian Nuclear Safety Commission

(‘CNSC’) and a Technical Proposal to the Saskatchewan

Ministry of Environment (‘SK MOE’) to support the

advancement of an In-Situ Recovery (‘ISR’) uranium mine

at the Company’s 90% owned Wheeler River Uranium Project

(‘Wheeler River’ or ‘the Project’). The

documents were accepted in the second quarter of 2019, initiating

the EA process for the project in accordance with the requirements

of both the Canadian Environmental Assessment Act, 2012

(‘CEAA 2012’) and the Saskatchewan Environmental

Assessment Act. The submission of the PD followed a decision by

Denison’s Board of Directors to approve the advancement of

the Phoenix ISR operation outlined in the Pre-Feasibility Study

(‘PFS’) completed for Wheeler River in 2018. In late

December 2019, Denison received a Record of Decision from the CNSC

on the scope of the factors to be taken into account for the

Wheeler EA, which indicate that the EA will follow the CNSC’s

generic guidelines.

■

Completion of Highly Successful 2019 ISR Field Test at

Phoenix

In December 2019,

Denison reported the completion of a highly successful ISR field

test program, which was carried out at the high-grade Phoenix

uranium deposit (‘Phoenix’) on the Wheeler River

property. The ISR field test program was designed to validate the

permeability of Phoenix, and to collect an extensive database of

hydrogeological data to further evaluate the ISR mining conditions

present at Phoenix. This detailed data is expected to facilitate

detailed mine planning as part of the completion of a future

Feasibility Study (‘FS’). The ISR field test program

included preliminary hydrogeological tests completed by using a

series of small diameter and large diameter test wells to move

water through two test areas defined within the Phoenix ore zone.

The ISR field test successfully achieved each of the

program’s planned objectives, and is highlighted by several

key de-risking accomplishments, including the

following:

●

Confirmation of significant

hydraulic connectivity within the Phoenix ore zone;

●

Installation of the Athabasca

Basin’s first Commercial Scale Wells (‘CSWs’) for

ISR;

●

Confirmation of limited

hydraulic connectivity within the underlying basement units;

and

●

Demonstration of the

effectiveness of MaxPerf to increase access to existing

permeability from a CSW.

Extensive

hydrogeological data sets were collected during the 2019 ISR field

program, and are being incorporated into a hydrogeological model

being developed for Phoenix. In February 2020, Denison reported

that the results from the hydrogeological test work, completed

to-date, have confirmed the ability to achieve bulk hydraulic

conductivity values (a measure of permeability) consistent with the

PFS (see Denison press release dated February 24,

2020).

■

Denison Initiates ISR

Metallurgical

Testing for the Phoenix Deposit and Reports Uranium Concentrations

from Initial Core Leach Tests up to Four Times the Amount Assumed

in PFS for Phoenix ISR

In December 2019,

Denison announced the initiation of the next phase of ISR

metallurgical laboratory testing for uranium recovery, which will

utilize the mineralized drill core recovered through the

installation of various test wells during the 2019 ISR field test

program. The metallurgical laboratory test program builds upon the

laboratory tests completed for the recovery of uranium as part of

the project’s PFS and is expected to further increase

confidence and reduce risk associated with the application of ISR.

The results are expected to facilitate detailed mine and process

plant planning as part of a future FS, and will provide key inputs

for the EA process. Significant components of the metallurgical

laboratory test program include core leach tests, column leach

tests, bench-scale tests and metallurgical modelling.

In February 2020,

Denison reported that initial data from core leach tests includes

elemental uranium concentrations, after test startup, in the range

of 13.5 grams per litre (‘g/L’) to 39.8 g/L, with an

average of 29.8 g/L over 20 days of testing (see Denison’s

press release dated February 19, 2020). This compares favourably to

the previous metallurgical test work completed to assess the use of

the ISR mining method at Phoenix – which supported a uranium

concentration of 10 g/L for the ISR processing plant design used in

the PFS.

■

Denison Reports Favorable Results from Exploration at Wheeler River

and Waterbury Lake

Denison conducted

winter and summer diamond drilling programs at Wheeler River during

2019 – totaling 10,573 metres in 20 holes. The programs were

focused on initial testing of regional target areas (K West, Q

South East, K South, O Zone) with the potential to result in the

discovery of additional high-grade deposits that could form

satellite ISR operations. During the 2019 winter program,

unconformity-hosted uranium mineralization was discovered along the

southern portion of the K West trend (approximately 2 kilometres

southwest of the Gryphon deposit) accompanied by strong sulphide

mineralization and other geological features commonly associated

with unconformity-related uranium deposits.

|

|

MANAGEMENT’S DISCUSSION & ANALYSIS

|

Drill hole WR-756

was highlighted by 0.03% U3O8 over 1.5 metres,

1.3% Cu over 4.0 metres, 0.13% Ni over 4.0 metres, and 0.18% Co

over 6.0 metres, located immediately above the sub-Athabasca

unconformity. Additional follow-up drilling during the 2019 summer

program at K West intersected strong hydrothermal alteration

associated with highly anomalous geochemistry within the basal

Athabasca sandstone, indicative of a fertile uranium mineralizing

system along the K West trend and providing evidence for additional

exploration targets.

At Waterbury Lake

a winter diamond drilling program was completed during 2019 –

totaling 5,735 metres in 15 holes. The program was focused on drill

testing priority target areas (GB Zone, Oban South, GB Northeast

and the Midwest Extension) associated with the regional Midwest

Structure, which is interpreted to be located along the eastern

portion of the Waterbury Lake property. The program was highlighted

by intersections of basement-hosted uranium mineralization at the

GB Zone including 0.15% U3O8 over 6.0 metres

in drill hole WAT19-480, and 0.25% U3O8 over 2.0 metres

and 0.22% U3O8 over 1.5 metres

in drill hole WAT19-486.

■

Execution of Memoranda of Understanding (‘MOUs’) with

Local Communities for Wheeler River

As reported in

the PD, Denison executed a series of MOUs, in support of the

advancement of Wheeler River, with certain Indigenous communities

who assert that Wheeler River falls partially or entirely within

their traditional territories and where traditional land use

activities are currently practiced within the local and regional

area surrounding the project. These non-binding MOUs formalize the

signing parties’ intent to work together in the spirit of

mutual respect and cooperation, in order to collectively identify

practical means by which to avoid, mitigate, or otherwise address

potential impacts of the project upon the exercise of Indigenous

rights, Treaty rights, and other interests, as well as to

facilitate sharing in the benefits that are expected to flow from

the project.

■

Renewal of Management Services Agreement with Uranium Participation

Corp.

The Company,

through its wholly owned subsidiary Denison Mines Inc., entered

into a new five year agreement to provide management services to

Uranium Participation Corp. (‘UPC’). The new agreement

has the potential to generate $10,000,000 in management fees to

Denison over the five year term.

■

Denison’s Closed Mines Group Renews Cornerstone Environmental

Services Contract with BHP Group Limited

(‘BHP’)

Effective July 1,

2019, Denison’s Closed Mines group entered into a new two

year services agreement with Rio Algom Limited, a subsidiary of

BHP. Under the terms of the agreement, the Closed Mines group is

responsible for carrying out the management and operation of nine

of BHP’s decommissioned mine sites in Ontario and

Quebec.

■

Obtained Financing for the Company’s 2020 Canadian

Exploration Activities

In December 2019,

the Company completed a $4,715,000 bought deal private placement

equity offering for the issuance of 6,934,500 common shares on a

flow-through basis at a price of $0.68 per share. The proceeds from

the financing will be used to fund Canadian exploration activities

through to the end of 2020.

Denison Mines

Corp. was formed under the laws of Ontario and is a reporting

issuer in all Canadian provinces. Denison’s common shares are

listed on the Toronto Stock Exchange (the ‘TSX’) under

the symbol ‘DML’ and on the NYSE American exchange

under the symbol ‘DNN’.

Denison is a

uranium exploration and development company with interests focused

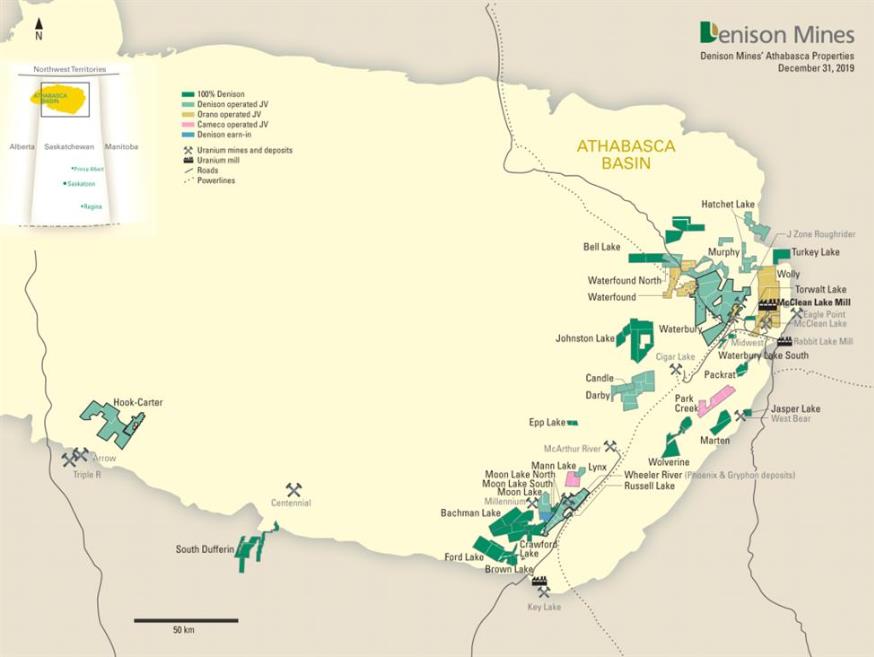

in the Athabasca Basin region of northern Saskatchewan, Canada. The

Company’s flagship project is the 90% owned Wheeler River

Uranium Project, which is the largest undeveloped uranium project

in the infrastructure rich eastern portion of the Athabasca Basin

region of northern Saskatchewan. A PFS was completed for Wheeler

River in late 2018, considering the potential economic merit of

developing the Phoenix deposit as an ISR operation and the Gryphon

deposit as a conventional underground mining operation. Denison's

interests in Saskatchewan also include a 22.5% ownership interest

in the McClean Lake Joint Venture (‘MLJV’), which

includes several uranium deposits and the McClean Lake uranium

mill, which is currently processing ore from the Cigar Lake mine

under a toll milling agreement, plus a 25.17% interest in the

Midwest deposits and a 66.57% interest in the J Zone and Huskie

deposits on the Waterbury Lake property. The Midwest, J Zone and

Huskie deposits are located within 20 kilometres of the McClean

Lake mill. In addition, Denison has an extensive portfolio of

exploration projects in the Athabasca Basin region.

|

|

MANAGEMENT’S DISCUSSION & ANALYSIS

|

Denison is

engaged in mine decommissioning and environmental services through

its Closed Mines group (formerly Denison Environmental Services),

which manages Denison’s Elliot Lake reclamation projects and

provides post-closure mine and maintenance services to a variety of

industry and government clients.

Denison is also

the manager of Uranium Participation Corporation

(‘UPC’), a publicly traded company listed on the TSX

under the symbol ‘U’, which invests in uranium oxide in

concentrates (‘U3O8’) and

uranium hexafluoride (‘UF6’).

STRATEGY

Denison’s

strategy is focused on leveraging its uniquely diversified asset

base to position the Company to take advantage of the strong

long-term fundamentals of the uranium market. The Company has built

a portfolio of strategic uranium deposits, properties, and

investments highlighted by a 90% interest in Wheeler River and a

minority interest in an operating and licensed uranium milling

facility in the MLJV, both located in the infrastructure rich

eastern portion of the Athabasca Basin region. While active in

exploring for new uranium discoveries in the region,

Denison’s present focus is on advancing Wheeler River to a

development decision, with the potential to become the next large

scale uranium producer in Canada. With a shortage of low cost

uranium development projects in the global project pipeline,

Denison offers shareholders exposure to value creation through the

potential future development of Wheeler River as well as an

anticipated increase in future uranium prices.

URANIUM INDUSTRY

OVERVIEW

Much of 2019 was

defined and influenced by policy matters in the United States

(‘US’), which effectively created an overhang of

uncertainty throughout the uranium market. In July 2019, the US

Presidential Administration completed an investigation into a trade

petition, launched under Section 232 of the Trade Expansion Act of

1962 (‘Section 232’), and no trade actions were

implemented. The US President indicated that the

Administration’s investigation did not agree with findings of

the US Department of Commerce (‘DOC’) that uranium

imports threaten to impair US national security. This announcement

was expected to provide clarity to the uranium market; however, the

Administration followed the decision with an order to review the

nuclear fuel supply chain in the US. Accordingly, a Nuclear Fuel

Working Group (‘NFWG’) was commissioned to examine the

current state of domestic nuclear fuel production to reinvigorate

the entire nuclear fuel supply chain, consistent with United States

national security and nonproliferation goals and to make

recommendations, if needed, to further enable US domestic nuclear

fuel production. A report from the NFWG was submitted, after a

brief extension, to the White House in late 2019. To date, no

official recommendations have been made public, however, the

President’s recent Budget Request for Fiscal Year 2021

included $150 million in the Department of Energy budget to

establish a uranium reserve. The budget request also set out a

schedule for a similar amount to be approved in the budget in each

of the next ten years.

Another source of

uranium market uncertainty stems from policies relating to Russian

deliveries of nuclear fuel into the US. Since breaking from the

Joint Comprehensive Plan of Action with Iran, commonly known as the

Iran Nuclear Deal, the US Administration has put in place sanctions

against Iran. The US has also issued waivers to certain of

Iran’s trading partners, allowing entities from particular

nations, including Russia, to continue working with Iran on

civilian nuclear programs. On December 15, 2019, one of those

waivers, related to Iran’s Fordow Fuel Enrichment Plant, was

lifted, which raised concern among market participants regarding

the possibility of other waivers being revoked. The waiver causing

uranium market participants particular concern relates to the

Bushehr nuclear power plant, which Russia is involved in

building. If this waiver is removed, there is concern that

Russia could face sanctions in the US, which would halt deliveries

of Russian nuclear fuel to US utilities and represent a significant

supply-side development.

Also relevant to

Russian nuclear fuel supply into the US is the Agreement Suspending

the Antidumping Investigation on Uranium from the Russian

Federation (also known as the Russian Suspension Agreement, or the

‘RSA’), which established annual quotas limiting the

delivery of nuclear fuel into the US from Russia, Kazakhstan,

Kyrgyzstan, Tajikistan, Ukraine and Uzbekistan. This agreement is

set to expire at the end of 2020 and is currently under review.

Before the agreement expires, a decision needs to be made by the US

DOC as to whether there will be an extension and, if so, whether an

extension will be under existing or revised terms. If the RSA

expires, Russian-origin uranium products and services could be sold

into the US without any restrictions - adding further uncertainty

to the uranium market.

These market dynamics contributed to a soft

uranium price throughout the year. In 2019, the spot uranium price

traded within a narrow band, beginning the year at USD$28.50 per

pound U3O8

and ending it down over 12% at

USD$25.00 per pound U3O8.

Lower prices near the end of the year were attributed to limited

demand in the spot market. While spot uranium volumes did not match

the historic high reached in 2018 (almost 89 million pounds

U3O8),

2019 spot buying remained reasonably strong at 65 million pounds

U3O8.

Similar to 2018, however, despite seeing fairly robust spot market

volumes, long-term utility contracting remained low in

2019.

|

|

MANAGEMENT’S DISCUSSION & ANALYSIS

|

Despite the

impact of these policy matters, there are several indications that

uranium supply and demand fundamentals continue to improve

underneath the cloud of uncertainty that has dominated the market

in 2019. This was underscored in the bi-annual Nuclear Fuel Report

released by the World Nuclear Association (‘WNA’) at

its annual symposium in September 2019. The report evaluates

nuclear fuel demand and supply scenarios for the period from 2019

to 2040, using reference, low and high cases. For the first time in

several years, the WNA’s outlook for global uranium demand

increased for all three scenarios, which is positive for the future

outlook on demand and reflects industry consensus that the demand

picture has improved significantly in recent years. This has been

supported by many positive news stories on the demand side,

including increasing public recognition of the critical role

nuclear energy has to play in combatting climate change. One of the

most significant acknowledgments of this was made by the European

Union (‘EU’), with its leaders recently agreeing that

nuclear energy must be included as part of the solution required to

meet the EU’s goal of becoming carbon neutral by 2050. The

EU’s ‘European Green Deal’ officially

acknowledged the importance of nuclear energy in meeting the

region’s comprehensive climate action goals.

●

In the US, there were a

number of positive announcements through the course of 2019. In

Ohio, a long-awaited energy bill was passed supporting the

continued operation of the Davis-Besse and Perry nuclear power

plants. Previous attempts to secure subsidies for these plants were

unsuccessful, which had led most in the industry to believe the

plants would be shut down by calendar year 2021. Recognizing the

long-term viability of existing nuclear power plants, the Turkey

Point nuclear units 3 and 4 received approval for an additional 20

years of operating life from the US Nuclear Regulatory Commission

(‘NRC’). This additional extension will take the

reactors to a total of 80 years of operating life, which is the

longest license ever issued by the NRC. Turkey Point 3 and 4 are

now licensed to operate to 2052 and 2053, respectively. In the US

Midwest, the life of the Monticello nuclear plant was extended by

another decade to 2040.

●

In Mexico, the

country’s national nuclear utility, the Federal Electricity

Commission (‘CFE’), is considering building four new

nuclear reactors, to add to its existing two units at Laguna Verde.

CFE shared its plans to present a feasibility study to management

and the government in 2020. The study will examine a project to

build 1,400 megawatts electric (‘MWe’) reactors, with

an estimated cost of US$7 billion each.

●

In Canada, with the

longer-term future of nuclear in mind, the provincial governments

of New Brunswick, Ontario and Saskatchewan demonstrated support for

future nuclear new builds. The leaders of these provinces announced

that they had joined efforts to collaborate on advancing small

modular reactor (‘SMR’) technologies. The leaders see

SMRs as a practical solution to help curb carbon emissions, move

away from coal-fired power generation, and create an opportunity

for new economic growth in the provinces.

●

In India, the government

continued to demonstrate its commitment to increase its use of

nuclear energy. At a recent nuclear conference, the Chairman of

India’s Atomic Energy Commission and Secretary of the

Department of Atomic Energy reinforced the country’s

aggressive pursuit of new nuclear power plants in order to improve

the reliability of the country’s power supply. The

government’s Union Minister for Atomic Energy also confirmed

that there are currently nine reactors under construction in India

and indicated that the government had given administrative and

financial support to build an additional 12 new reactors with a

capacity of 9,000 MWe.

●

In the United Kingdom

(‘UK’), a leaked government analysis stressed the need

to build a fleet of new nuclear or carbon capture power plants in

order to meet climate targets. The UK government believes that up

to 40,000 MWe of low carbon power stations could be needed in 2050

to reduce Britain’s emissions to ‘net zero’ and

currently there is just one nuclear power plant under construction

– EDF Energy’s 3,200 MWe Hinkley Point C in

England.

●

In South Korea, Korea Hydro

& Nuclear Power (‘KHNP’) announced the successful

start-up of its Shin Kori 4 nuclear power plant. Initial

criticality was reached and the unit was connected to the grid in

April 2019. The Shin Kori 4 unit is a 1,400 MWe APR-1400, which is

the same design as those currently under construction in the United

Arab Emirates at the Barakah nuclear power plant, which is expected

to begin supplying electricity early in 2020.

●

In Taiwan, sentiment has

shifted away from a previous policy to eliminate nuclear power from

the Taiwan energy mix. In May 2019, the country passed an amendment

to eliminate the ‘Nuclear Free Homeland 2025’ mandate

that was imposed by the anti-nuclear Democratic Progressive Party

in early 2017. This amendment has opened the door for future

pro-nuclear decisions to be made regarding extending the lives of

existing nuclear power plants in the country, as well as the

possible completion of the Lungmen nuclear power plant, where

construction was halted in 2014.

|

|

MANAGEMENT’S DISCUSSION & ANALYSIS

|

●

In Germany, positive

sentiment towards nuclear also appears to be growing. In 2019 the

government received escalating calls from several of the

country’s most prominent businesses to delay the

country’s plans to implement a full-scale nuclear phase-out

by the end of 2022. Some of these businesses emphasized the

importance of nuclear power, highlighting that Germany needs to run

its nuclear power plants longer if climate protection really

matters to the country.

Though much of

the nuclear news out of Asia was positive, news emerged from Japan

early in 2019 that the requirements set by the country’s

Nuclear Regulation Authority (‘NRA’) for utilities to

complete anti-terrorism protection work on each reactor’s

emergency facilities were unlikely to be met on schedule. All three

utilities currently operating units in Japan have said they require

between one and two and a half additional years to complete the

required work. The NRA has indicated, however, that it will not

extend the deadline. Due to this, it was recently announced that

reactors 3 and 4 at the Takahama nuclear power plant will stop

operating by the summer of 2020, with work aimed at meeting the NRA

commitment about one year behind schedule.

Overall, uranium

demand has grown in recent years, having now exceeded the annual

levels that existed prior to Japan shutting all of its nuclear

units following the 2011 Fukushima Daichii nuclear

incident.

The supply side

of the uranium market has also been progressing in the right

direction. This has resulted in a growing gap between annual

utility requirements and primary production, which continues to be

filled by drawing down on inventories and other secondary sources

of supply. Some of the positive supply indicators

include:

●

The world’s largest and

lowest cost uranium producer, National Atomic Company Kazatomprom

announced in August 2019, that it was reaffirming its commitment to

reach and maintain a more commercial balance between supply and

demand by extending its previously announced 20% production

curtailment through to 2021.

●

Other important supply side

changes included Rio Tinto finalizing the sale of its Rössing

operation in Namibia to China’s China National Uranium

Corporation (‘CNUC’). Taken together with the slow wind

down of Rio Tinto’s Ranger operation in Australia, we expect

to see Rio Tinto, one of the world’s largest mining companies

and a long-term major producer in the uranium industry, completely

exit the market.

●

In Niger, it was announced

that the Cominak mine will cease operation in March 2021 due to

depletion of ore. The operation has been a source of supply to the

industry since 1978.

With a

significant shortfall having developed between annual nuclear

utility requirements and primary production, inventories and other

secondary sources of supply are being drawn down to meet utility

needs. This process of inventory drawdowns suggests that we are

nearing an inflection point – where end-users of uranium

begin to question where long-term uranium supplies will come from

and how secure that supply will be over the long lives of their

nuclear reactors. There is already a growing sense that market

participants are beginning to look beyond near-term market

conditions in an attempt to understand what the supply environment

will look like in the mid-2020s and beyond. With a renewed focus on

nuclear energy as a critical element in battling climate change, it

is expected that global utilities will be looking to source future

supply from operations that are not only low-cost, reliable, and

situated in stable jurisdictions (the typical criteria for a good

supplier), but also those which are flexible and environmentally

responsible.

SELECTED ANNUAL FINANCIAL INFORMATION

|

(in

thousands, except for per share amounts)

|

|

|

|

Year

Ended

December

31,

2019

|

|

Year Ended

December 31,

2018

|

|

Year Ended

December 31,

2017

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Continuing Operations:

|

|

|

|

|

|

|

|

|

|

Total

revenues

|

|

|

$

|

15,549

|

$

|

15,550

|

$

|

16,067

|

|

Exploration and

evaluation

|

|

|

$

|

(15,238)

|

$

|

(15,457)

|

$

|

(16,643)

|

|

Operating

expenses

|

|

|

$

|

(14,436)

|

$

|

(15,579)

|

$

|

(13,687)

|

|

Impairment

reversal (expense)

|

|

|

$

|

-

|

$

|

(6,086)

|

$

|

331

|

|

Net

loss

|

|

|

$

|

(18,141)

|

$

|

(30,077)

|

$

|

(19,454)

|

|

Basic and diluted

loss per share

|

$

|

(0.03)

|

$

|

(0.05)

|

$

|

(0.04)

|

|

Discontinued Operations:

|

|

|

|

|

|

|

|

Net

loss

|

$

|

-

|

$

|

-

|

$

|

(109)

|

|

Basic and diluted

loss per share

|

$

|

-

|

$

|

-

|

$

|

-

|

|

|

MANAGEMENT’S DISCUSSION & ANALYSIS

|

|

(in

thousands)

|

|

|

|

As at

December 31,

2019

|

|

As at

December 31,

2018

|

|

As at

December 31,

2017

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Financial Position:

|

|

|

|

|

|

|

|

|

|

Cash and cash

equivalents

|

|

|

$

|

8,190

|

$

|

23,207

|

$

|

3,636

|

|

Investments in

debt instruments (GICs)

|

|

|

$

|

-

|

$

|

-

|

$

|

37,807

|

|

Cash, cash

equivalents and GICs

|

|

|

$

|

8,190

|

$

|

23,207

|

$

|

41,443

|

|

|

|

|

|

|

|

|

|

|

|

Working

capital

|

$

|

1,597

|

$

|

19,221

|

$

|

34,756

|

|

Property, plant

and equipment

|

$

|

257,259

|

$

|

258,291

|

$

|

249,002

|

|

Total

assets

|

$

|

299,998

|

$

|

312,187

|

$

|

326,300

|

|

Total long-term

liabilities

|

$

|

74,903

|

$

|

77,455

|

$

|

80,943

|

SELECTED QUARTERLY FINANCIAL INFORMATION

|

|

|

|

|

2019

|

|

2019

|

|

2019

|

|

2019

|

|

(in

thousands, except for per share amounts)

|

|

Q4

|

|

Q3

|

|

Q2

|

|

Q1

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total

revenues

|

$

|

3,956

|

$

|

3,478

|

$

|

4,139

|

$

|

3,976

|

|

Net

loss

|

$

|

(1,498)

|

$

|

(6,424)

|

$

|

(4,884)

|

$

|

(5,335)

|

|

Basic and diluted

loss per share

|

$

|

(0.00)

|

$

|

(0.01)

|

$

|

(0.01)

|

$

|

(0.01)

|

|

|

|

|

|

2018

|

|

2018

|

|

2018

|

|

2018

|

|

(in

thousands, except for per share amounts)

|

|

Q4

|

|

Q3

|

|

Q2

|

|

Q1

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total

revenues

|

$

|

4,144

|

$

|

3,729

|

$

|

4,104

|

$

|

3,573

|

|

Net

loss

|

$

|

(13,642)

|

$

|

(3,884)

|

$

|

(5,583)

|

$

|

(6,968)

|

|

Basic and diluted

loss per share

|

$

|

(0.02)

|

$

|

(0.01)

|

$

|

(0.01)

|

$

|

(0.01)

|

|

|

|

|

|

|

|

|

|

|

Significant items causing variations in quarterly

results

●

The Company’s toll

milling revenues fluctuate due to the timing of uranium processing

at the McClean Lake uranium mill as well as changes to the

estimated mineral resources of the Cigar Lake mine.

●

Revenues from the Closed

Mines group fluctuate due to the timing of projects, which vary

throughout the year in the normal course of business.

●

Operating expenses fluctuate

due to the timing of projects at both the MLJV and the Closed Mines

group, which vary throughout the year in the normal course of

business.

●

Exploration expenses are

generally largest in the first and third quarters, due to the

timing of the winter and summer exploration programs in

Saskatchewan.

●

The Company’s results

are also impacted, from time to time, by other non-recurring events

arising from its ongoing activities, as discussed below where

applicable.

RESULTS OF OPERATIONS

REVENUES

McClean Lake Uranium Mill

The McClean Lake

property is located on the eastern edge of the Athabasca Basin in

northern Saskatchewan, approximately 750 kilometres north of

Saskatoon. Denison holds a 22.5% ownership interest in the MLJV and

the McClean Lake uranium mill, one of the world’s largest

uranium processing facilities. The mill has licensed annual

production capacity of 24.0 million pounds U3O8, and is currently

operating under a 10-year license expiring in 2027. The mill is

currently processing ore from the Cigar Lake mine under a toll

milling agreement.

|

|

MANAGEMENT’S DISCUSSION & ANALYSIS

|

The MLJV is a

unincorporated contractual arrangement between Orano Canada Inc.

(‘Orano Canada’) with a 70% interest, Denison with a

22.5% interest, and OURD (Canada) Co. Ltd. with a 7.5%

interest.

In February 2017,

Denison completed a transaction with Anglo Pacific Group PLC and

one of its wholly owned subsidiaries (the ‘APG

Arrangement’), under which Denison received an upfront

payment of $43,500,000 in exchange for its right to receive future

toll milling cash receipts from the MLJV under the current toll

milling agreement with the Cigar Lake Joint Venture

(‘CLJV’) from July 1, 2016 onwards. The APG Arrangement

consists of certain contractual obligations of Denison to forward

to APG the cash proceeds of future toll milling revenue earned by

the Company related to the processing of the specified Cigar Lake

ore through the McClean Lake mill, and as such, the upfront payment

was accounted for as deferred revenue.

During the year

ended December 31, 2019, the McClean Lake mill processed 18.0

million pounds U3O8 for the CLJV

(2018 – 18.0 million pounds U3O8). In 2019, the

Company recorded toll milling revenue of $4,609,000 (2018 –

$4,239,000). The increase in toll milling revenue in 2019 compared

to the prior year is predominantly the result of an update to the

published Cigar Lake mineral resource estimate in the first quarter

of 2018, which resulted in the Company recording a negative

non-cash cumulative catch-up accounting adjustment of $332,000,

which reduced the recorded toll milling revenue in 2018. During the

first quarter of 2019, the Company recorded a nominal $26,000

positive non-cash cumulative accounting adjustment related to the

Cigar Lake mineral resource estimate update published in that

quarter.

During the year

ended December 31, 2019, the Company also recorded an accretion

expense of $3,203,000 on the toll milling deferred revenue balance

(2018 – $3,314,000). The annual accretion expense will

decrease over the life of the contract as the deferred revenue

liability decreases over time.

During the fourth

quarter of 2019, the McClean Lake Union Unifor Local 48-S ratified

a new collective bargaining agreement. The new three-year agreement

includes the implementation of a new two-weeks-in two-weeks-out

rotation, which will be implemented early in 2020.

Denison Closed Mines Services

Mine

decommissioning and environmental services are provided through

Denison’s Closed Mines group, which has provided long-term

care and maintenance for closed mine sites since 1997. With offices

in Ontario, the Yukon Territory and Quebec, the Closed Mines group

manages Denison’s Elliot Lake reclamation projects and

provides post-closure mine care and maintenance services to various

customers.

Revenue from

Closed Mines services during 2019 was $8,974,000 (2018 -

$9,298,000). The decrease in revenue in 2019, as compared to 2018,

was due to a decrease in activity at certain care and maintenance

sites, as well as a decrease in environmental consulting activities

during the year.

Management Services Agreement with UPC

Denison provides

general administrative and management services to UPC pursuant to a

management services agreement. The current agreement has an

effective date of April 1, 2019, and is for a five year term.

Management fees and commissions earned by Denison provide a source

of cash flow to partly offset corporate administrative expenditures

incurred by the Company.

During 2019,

revenue from the Company’s management contract with UPC was

$1,966,000 (2018 - $2,013,000). The decrease in revenues during

2019, compared to the prior year, was due to a decrease in

commission-based and discretionary fees, partly offset by an

increase in NAV-based management fees. UPC’s balance sheet

consists primarily of uranium held either in the form of

U3O8 or UF6, which is

accounted for at its fair value. The increase in NAV-based

management fees during the year, as compared to the prior period,

was due to the increase in the average fair value of UPC’s

uranium holdings, resulting from both increased uranium spot prices

and increased uranium holdings. The decrease in commission-based

fees in the year was due to a decrease in uranium purchases, and a

decrease in sales of conversion services, by UPC during the current

period, as compared to the prior year. Denison earns a 1%

commission on the gross value of UPC’s uranium purchases and

sales.

|

|

MANAGEMENT’S DISCUSSION & ANALYSIS

|

OPERATING EXPENSES

Mining

Operating

expenses of the mining segment include depreciation and development

costs.

Operating

expenses in 2019 were $6,090,000 (2018 - $7,159,000). In 2019,

operating expenses included depreciation of the McClean Lake mill

of $3,165,000 (2018 - $3,264,000), as a result of processing

approximately 18.0 million pounds U3O8 for the CLJV

(2018 – 18.0 million pounds). The decrease in depreciation

during 2019 was primarily driven by a reduction in the

units-of-production depreciation rate due to an increase in the

estimate of the future CLJV production to be processed through the

mill.

In 2019,

operating expenses also included development and other operating

costs related to the MLJV of $2,925,000 (2018 – $3,893,000),

which relate predominantly to the multi-year test mining program,

operated by Orano Canada within the MLJV, to support the

advancement of the novel Surface Access Borehole Resource

Extraction (‘SABRE’) mining technology.

Closed Mines Services

Operating

expenses during 2019 totaled $8,346,000 (2018 - $8,211,000). The

expenses relate primarily to care and maintenance services provided

to clients, and include labour and other costs. The increase in

operating expenses in 2019, compared to 2018, is predominantly due

to a restructuring that was undertaken in the fourth quarter of

2019, to discontinue environmental consulting activities in order

to focus on the providing care and maintenance services, resulting

in a reduction in headcount and associated severance

expenditures.

CANADIAN MINERAL PROPERTY EXPLORATION & EVALUATION

During 2019, the

Company continued to focus on its high priority projects in the

Athabasca Basin region in Saskatchewan. Denison’s share of

exploration and evaluation expenditures in 2019 was $15,238,000

(2018 – $15,457,000). Exploration spending in Canada is

seasonal, with spending higher during the winter exploration season

(January to mid-April) and summer exploration season (June to

mid-October) in the Athabasca Basin. During 2019, the

Company’s exploration and evaluation expenditures decreased,

primarily due to decreased exploration activity, partially offset

by increased evaluation activities at Wheeler River.

The following

tables summarize the 2019 exploration and evaluation activities

completed through the middle of February 2020. The exploration

drilling relates to the Company’s summer and winter 2019

exploration programs, while the evaluation drilling relates to the

Wheeler River ISR field test which ran from June to December 2019

and included the installation of preliminary ISR test wells in

small diameter diamond drill holes and the completion of two large

diameter drill holes used for the installation of two commercial

scale wells (CSWs).

All exploration

and evaluation expenditure information in this MD&A covers the

twelve months ending December 31, 2019.

|

|

MANAGEMENT’S DISCUSSION & ANALYSIS

|

|

EXPLORATION ACTIVITIES

|

|

Property

|

Denison’s

Ownership(1)

|

Exploration

Drilling(6)

|

|

Wheeler

River

|

90%(2)

|

10,573 m (20

holes)

|

|

Waterbury

Lake

|

66.57%(3)

|

5,735 m (15

holes)

|

|

Hook-Carter

|

80%(4)

|

4,797 m (6

holes)

|

|

Waterfound

River

|

12.32%(5)

|

5,110 m (7

holes)

|

|

Total

|

|

26,215 m (48 holes)

|

Notes:

(1) The

Company’s ownership as at December 31, 2019.

(2) JCU (Canada)

Exploration Company Limited (‘JCU’) funded their 10%

portion of exploration and evaluation expenditures during 2019 and

ownership interests are unchanged for 2019.

(3) Denison

earned an additional 0.65% interest in the Waterbury Lake property

during 2019. The partner, Korea Waterbury Uranium Limited

Partnership (‘KWULP’), elected not to fund the 2019

exploration program and therefore diluted its ownership interest.

Refer to RELATED PARTY TRANSACTIONS for further

details.

(4) The Company

acquired an 80% ownership in the Hook-Carter project in November

2016 from ALX Uranium Corp. (‘ALX’) and has agreed to

fund

ALX’s share

of the first $12.0 million in expenditures on the project. See

below for further details.

(5) Denison

elected not to fund its 14.42% share of the $1,508,286 2019

drilling program implemented by the operator, Orano Canada.

Accordingly, Denison’s ownership interest decreased by 2.1%

to 12.32%.

(6) The Company

reports total exploration metres drilled and the number of holes

that were successfully completed to their target

depth.

|

EVALUATION ACTIVITIES

|

|

Property

|

Denison’s

Ownership(1)

|

Evaluation Drilling

|

Other Activities

|

|

Wheeler

River

|

90%(2)

|

9,632 m (30 small

diameter wells)(3)

821 m (2 large

diameter wells)(4)

|

ISR Field

Testing,

Engineering,

Environmental Assessment

|

|

Total

|

|

10,453 m (32 holes)

|

|

Notes:

(1) The

Company’s ownership as at December 31, 2019.

(2) JCU (Canada)

Exploration Company Limited (‘JCU’) funded their 10%

portion of exploration and evaluation expenditures during 2019 and

ownership interests are unchanged for 2019.

(3) Small

diameter evaluation drilling includes HQ/PQ sized diamond drilling

either as the widening (reaming) of existing exploration drill

holes, or the drilling of new holes, for the purposes of installing

test wells for ISR field testing at Phoenix. Figures include total

evaluation metres drilled and total number of holes

completed.

(4) Large

diameter evaluation drilling relates to the drilling and

installation of new large diameter CSWs from surface for the

purposes of ISR field testing at Phoenix. Figures include total

evaluation metres drilled and total number of holes

completed.

The

Company’s Athabasca land package decreased during the fourth

quarter of 2019 from 305,658 hectares (213 claims) to 279,883

hectares (214 claims) due to area reductions of claims belonging to

the Darby, Epp Lake, Hatchet Lake, Johnston Lake, Murphy Lake and

South Dufferin properties, and lapsing of claims belonging to the

Perpete Lake and Waterbury North properties. Claim area reductions

allow the Company to extend tenure of the higher priority portions

of claims and reduce the annual expenditure requirements going

forward.

|

|

MANAGEMENT’S DISCUSSION & ANALYSIS

|

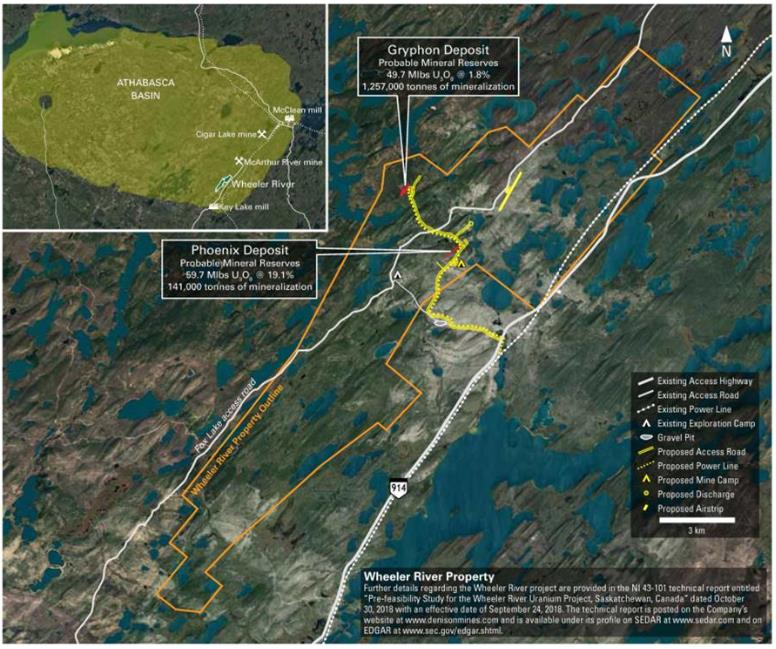

Wheeler River Project

Project Highlights:

●

PFS

results suggest Phoenix could become one of the lowest-cost uranium

mining operation globally

On September 24,

2018, the Company announced the results of the PFS for Wheeler

River. The PFS was completed in accordance with NI 43-101 and is

highlighted by the selection of the ISR mining method for the

development of the Phoenix deposit, with an estimated average

operating cost of $4.33 (USD$3.33) per pound U3O8.

The PFS considers

the potential economic merit of co-developing the Phoenix and

Gryphon deposits. The high-grade Phoenix deposit is designed as an

ISR mining operation, with associated processing to a finished

product occurring at a plant to be built on site at Wheeler River.

The Gryphon deposit is designed as an underground mining operation,

utilizing a conventional long hole mining approach with processing

of mine production assumed at Denison’s 22.5% owned McClean

Lake mill. Taken together, the project is estimated to have mine

production of 109.4 million pounds U3O8 over a 14-year

mine life, with a base case pre-tax net present value

(‘NPV’) of $1.31 billion (8% discount rate), internal

rate of return (‘IRR’) of 38.7%, and initial

pre-production capital expenditures of $322.5 million.

The PFS was

prepared on a project (100% ownership) and pre-tax basis. Denison

completed an indicative post-tax assessment based on a 90%

ownership interest, yielding a base case post-tax NPV of $755.9

million and post-tax IRR of 32.7%, with initial capital costs to

Denison of $290.3 million.

On December 18,

2018, Denison reported that the Company's Board of Directors and

the Wheeler River Joint Venture (‘WRJV’) approved the

advancement of Wheeler River, following a detailed assessment of

the PFS results. In support of the decision to advance Wheeler

River, in 2019 the WRJV initiated the EA process as well as

engineering studies and related programs required to advance the

high-grade Phoenix deposit as an ISR mining operation.

|

|

MANAGEMENT’S DISCUSSION & ANALYSIS

|

●

Environmental

advantages of the proposed Wheeler River ISR mine

The Company's

evaluation of the ISR mining method in the PFS has identified

several significant environmental and permitting advantages –

particularly when compared to the impacts associated with

conventional uranium mining in Canada. The Project's ISR mining

operation is expected to produce no tailings, generate very small

volumes of waste rock, and has the potential for low volumes or

possibly no water discharge to surface water bodies, as well as the

potential to use the existing power grid to operate on a near zero

carbon emissions basis. The planned use of a freeze wall to

encapsulate the ore zone and contain the mining solution used in

the ISR operation streamlines the mining process, minimizes

interaction with the environment, and facilitates controlled

reclamation of the site at decommissioning. Taken together, the

Project has the potential to be one of the most environmentally

friendly uranium mining and processing operations in the world.

Owing largely to these benefits, engagement with local Indigenous

communities, the public, and federal and provincial

representatives, to date, has been encouraging regarding the use of

ISR mining.

●

The

largest undeveloped uranium project in the eastern Athabasca

Basin

Upon completion

of the PFS and in accordance with NI 43-101 standards, the Company

has declared the following mineral reserves and

resources.

●

Probable mineral reserves of 109.4 million

pounds U3O8

(Phoenix 59.7 million pounds U3O8 from 141,000

tonnes at 19.1% U3O8; Gryphon 49.7

million pounds U3O8 from 1,257,000

tonnes at 1.8% U3O8);

●

Indicated mineral resources (inclusive of

reserves) of 132.1 million pounds U3O8

(1,809,000 tonnes at an average grade of 3.3% U3O8);

plus

●

Inferred mineral resources of 3.0 million

pounds U3O8 (82,000

tonnes at an average grade of 1.7% U3O8).

●

Potential

for resource growth

Potential exists

for resource growth, outside of the currently defined mineral

resources, at both the Phoenix and Gryphon deposits. At Phoenix,

potential exists particularly around Zone B, where previous

mineralized results remain open on section or the interpreted

optimal exploration target remains untested, and at Zone C, which

is not currently included in the mineral resource estimate, where

similar targets exist. At Gryphon, potential exists to expand

mineral resources both along strike and down-plunge of the

currently defined A Series Lenses.

Outside of the

Phoenix and Gryphon deposits, Wheeler River has significant

exploration potential for the discovery of additional high-grade

uranium deposits. The Project’s significant repository of

geophysical and historic drilling data has facilitated the

identification of numerous high-priority regional target areas in

accordance with the Company’s latest exploration models. Many

of the target areas have the potential to host high-grade

sandstone-hosted deposits, similar to Phoenix, that may be amenable

to the use of the low-cost ISR mining method. Following almost ten

years of exploration drilling focused largely on the Phoenix and

Gryphon deposits, a multi-year plan has been developed to explore

the regional target areas, which commenced in 2018, and continued

in 2019.

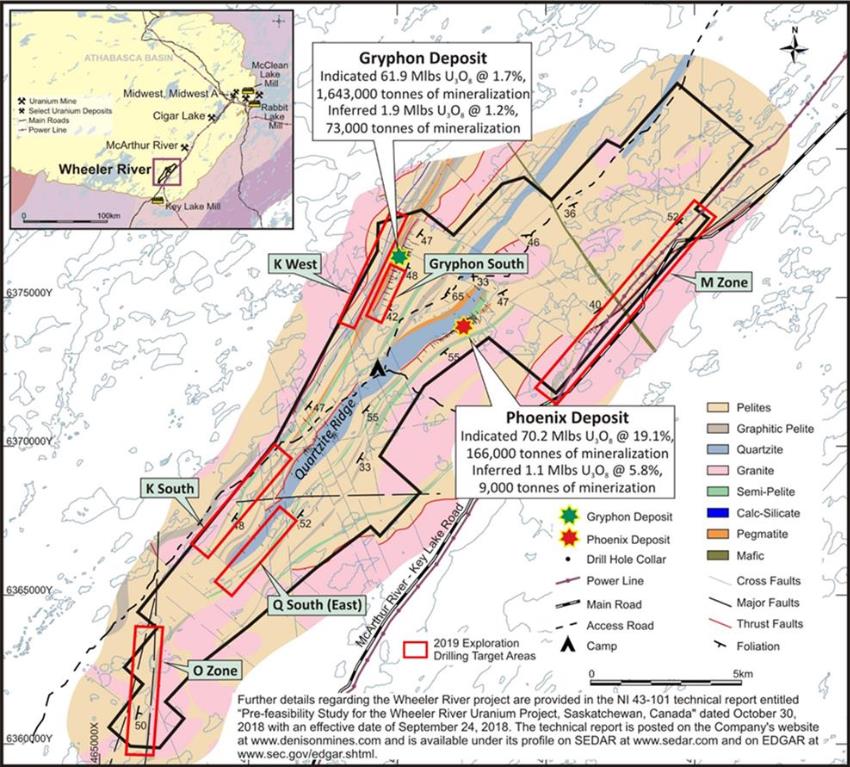

Further details

regarding Wheeler River, including the estimated mineral reserves

and resources and PFS, are provided in the Technical Report for the

Wheeler River project titled ‘Pre-feasibility Study Report

for the Wheeler River Uranium Project, Saskatchewan, Canada’

prepared by Mark Liskowich, P.Geo. of SRK Consulting (Canada) Inc.

with an effective date of September 24, 2018 (‘PFS Technical

Report’). A copy of the PFS Technical Report is available on

Denison’s website and under its profile on each of SEDAR and

EDGAR.

|

|

MANAGEMENT’S DISCUSSION & ANALYSIS

|

The location of

the Wheeler River property, as well as the Phoenix and Gryphon

deposits, and existing and proposed infrastructure, is shown on the

map provided below.

Evaluation Program

During 2019,

Denison’s share of evaluation costs at Wheeler River amounted

to $9,867,000 (2018 - $3,130,000), which consisted primarily of

work related to the ISR field test program, other engineering

activities (including metallurgical testing) in support of a future

FS, and activities related to the EA process.

Engineering Activities

ISR Field Test

The

ISR field test program was designed to assess the permeability of

Phoenix, and to collect an extensive database of hydrogeological

data to further evaluate the ISR mining conditions present at

Phoenix (see Figure 1). This data is of critical importance to the

advancement of Phoenix as an ISR mining operation – as it is

expected to support a detailed assessment of the ISR requirements

related to permeability, and to be further incorporated into a

detailed ISR mine plan as part of the completion of a future

FS.

The

Company successfully completed the planned ISR field test work and

safely concluded operations on site at Wheeler River during the

fourth quarter of 2019 (see Denison’s press release dated

December 18, 2019). The field activities associated with the 2019

ISR field test program were completed over a period of

approximately 23 weeks (starting in June and completed in late

November), and required the support of approximately 40 Denison

employees and contractor staff.

|

|

MANAGEMENT’S DISCUSSION & ANALYSIS

|

The

objectives of the program were extensive, and the scope of the work

completed on site during the program was considerable. The

following represent the key components of field work completed as

part of the 2019 ISR field test program:

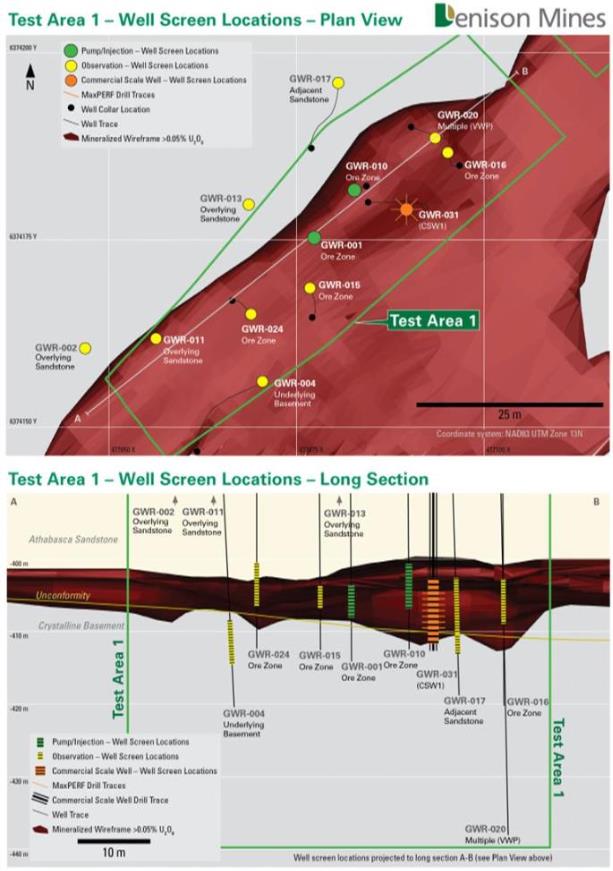

●

Installation

of 4 small-diameter pump/injection (‘P/I’) wells with a

2.5-inch diameter PVC pipe and slotted well-screen set within the

ore zone of Test Area 1 and Test Area 2.

●

Installation

of 5 small-diameter observation wells with a 1.5-inch diameter PVC

pipe and slotted well-screen set at various depths within the ore

zone of Test Area 1 and Test Area 2.

●

Installation

of 6 small-diameter observation wells with a 1.5 inch diameter PVC

pipe and slotted well-screen set at various depths outside of the

ore zone of Test Area 1 and Test Area 2, including wells situated

in the basement formation below Phoenix and in the sandstone above

and adjacent to Phoenix.

●

Installation

of 2 test wells containing Vibrating Wire Piezometers

(‘VWPs’) in each of Test Area 1 and Test Area 2,

equipped with pressure transducers at five different depth

locations – including the overburden (1 transducer),

overlying sandstone (2 transducers), ore zone (1 transducer), and

underlying basement (1 transducer).

●

Installation

of 12 small-diameter regional observation wells with a 1.5 inch

diameter PVC pipe and slotted well-screen set at various depths and

located approximately between 100 metres and 700 metres outside of

the boundaries of the ore zone at Phoenix, for the purposes of

environmental monitoring and baseline data collection.

●

Installation

of 1 re-charge well with a 2.5-inch diameter PVC pipe and slotted

well-screen set within the ore zone horizon for the purposes of

recharging formation test waters.

●

Completion of

a series of short-duration preliminary hydrogeological tests, using

the P/I wells to pump water from or inject water into the ore zone

to collect hydrogeological data and identify hydraulic connectivity

between test wells – validating the ability to move water,

and the existence of significant permeability, within the Phoenix

ore zone.

●

Installation

of 2 large-diameter CSWs within the ore zone – one located in

each of Test Area 1 and Test Area 2 and both designed to meet

expected regulatory and environmental requirements such that they

can ultimately form part of the production ISR well field at

Phoenix.

●

Completion of

a series of short-duration preliminary hydrogeological tests, using

the CSWs to pump water from or inject water into the ore zone to

collect further hydrogeological data and assess the extent of

permeability prior to testing the MaxPERF Drilling

Tool.

●

Deployment of

the MaxPERF Drilling Tool in each of CSW1 and CSW2 to complete an

array of lateral drill holes (penetration tunnels) designed to

enhance access from each CSW to the existing permeability within

the ore zone.

●

Completion of

a further series of short-duration preliminary hydrogeological

tests, using each of CSW1 and CSW2 to pump water from or inject

water into the ore zone following the deployment of the MaxPERF

Drilling Tool – indicating potential increased flow rates

following the application of the MaxPERF drilling.

●

Completion of

long-duration hydrogeological tests, using each of CSW1 and CSW2 to

pump water from or inject water into the ore zone for an extended

period of time, to collect further detailed hydrogeological data

designed to simulate fluid flow under conditions similar to an

envisioned commercial production environment.

●

Completion of

approximately 23 individual hydraulic conductivity tests (downhole

packer testing) in 15 boreholes at various depths within and

adjacent to the ore zone of Test Area 1 and Test Area 2 –

including hydraulic conductivity tests within the underlying

basement formation below Phoenix and in the sandstone above and

adjacent to Phoenix.

●

Completion of

downhole geophysics including nuclear magnetic resonance, dual

neutron, and cement-bond log in CSW2 and dual neutron in GWR-001,

GWR-010, GWR-019 and GWR-022.

●

Recovery of

approximately 100 metres of mineralized drill core in 14 individual

drill holes from the installation of P/I and observation wells, as

well as CSWs, within Test Area 1 and Test Area 2 – subject to

detailed on-site geological and geotechnical logging as well as

permeability (permeameter) testing, prior to portions of the core

being preserved for laboratory-based metallurgical test

work.

●

Completion of

extensive permeameter testing in the field, utilizing a portable

nitrogen gas probe permeameter adapted for testing whole drill core

pieces. Permeameter measurements were taken on core at approximate

10 centimetre intervals, resulting in a total of over 1,200

measurements collected from the 2019 ISR field test

program.

|

|

MANAGEMENT’S DISCUSSION & ANALYSIS

|

The

ISR field test successfully achieved each of the program’s

planned objectives, and is highlighted by several key de-risking

accomplishments, including the following:

Confirmation of significant hydraulic connectivity within the

Phoenix ore zone:

●

85% of test

wells located within Test Area 1 and Test Area 2 of the Phoenix

deposit showed hydraulic connectivity with another test well (see

Figure 2 and Figure 3);

●

Hydraulic

connectivity was observed over 77% of the total strike length

tested in Test Area 1 and Test Area 2 combined, and over 100% of

the total across-strike length tested;

●

Taken

together, the extent of hydraulic connectivity observed during the

ISR field test program is supportive of the permeability of the ore

zone and the potential suitability for ISR mining.

Installation of the Athabasca Basin’s first CSWs for

ISR:

●

ISR mining of

the Phoenix deposit is expected to require the installation of

approximately 300 large-diameter/commercial-scale vertical wells

into and surrounding the Phoenix deposit at approximately 400

metres below surface;

●

The

installation of CSW1 (GWR-031) and CSW2 (GWR-032) represent a

historic milestone for the advancement of ISR mining within the

Athabasca Basin – as the first wells to have been installed

for the purpose of ISR mining (see Figure 2 and Figure

3);

●

Completion of

these wells represents a notable de-risking accomplishment for the

project, as it confirms the ability to drill these large-diameter

holes and install the materials necessary for ISR mining in a

complex and highly altered geological setting that has not

previously been tested for the suitability of the installation of

ISR wells.

Confirmation of limited hydraulic connectivity within the

underlying basement units:

●

During

preliminary tests in Test Area 1 and Test Area 2, negligible

hydraulic responses were observed in the observation wells situated

in the basement rock units underlying the Phoenix

deposit;

●

This result

is indicative of the basement units having relatively low

permeability and is supportive of the PFS design for the Phoenix

ISR operation, which relies on the basement units providing

containment of the ISR mining solution in conjunction with the

planned freeze dome.

Demonstration of the effectiveness of MaxPERF to increase CSW

access to existing permeability:

●

The MaxPERF

Drilling Tool was successfully deployed in CSW1 and CSW2 to create

a series of lateral drill holes (penetration tunnels) roughly 0.7

inches (1.78 centimetres) in diameter, which extend up to 72 inches

(1.83 metres) from the CSW;

●

Initial

short-duration hydrogeological tests confirmed increased flow rates

in Test Area 1 following the completion of the MaxPERF drilling

(see Denison’s press release dated August 27, 2019). In Test

Area 2, initial short-duration hydrogeological tests confirmed

similar flow rates both before and after the completion of the

MaxPERF drilling (See Denison’s press release dated December

18, 2019);

●

These results

confirm that the MaxPERF Drilling Tool can be deployed successfully

within a CSW to mechanically engineer increased access to the

existing permeability of the ore formation. This tool could be of

significant utility in areas of the Phoenix deposit where natural

access to permeability is challenged.

Confirmation of ability to achieve hydraulic conductivity values

consistent with PFS

●

In February

2020, the Company reported further results of the pump and

injection tests performed on the two CSWs. These tests were

designed to allow for the simulation of fluid flow under conditions

similar to an envisioned commercial ISR production environment

– ultimately facilitating a quantitative assessment of the

bulk hydraulic conductivity of the Phoenix orebody and surrounding

rock formations.

●

For ISR

mining operations, the term ‘hydraulic conductivity’ is

used to describe the ease with which a fluid can move through the

pore spaces or fractures within a host rock. Hydraulic

conductivity, commonly represented by the symbol ‘K’,

is often stated as a rate of flow (under a unit hydraulic gradient

through a unit cross-sectional area of aquifer) and is typically

reported in units of metres/sec (‘m/s’) or metres/day

(‘m/d’).

●

The Pump and injection tests completed during the

2019 Field Test from CSW2 (drill hole GWR-032), after deployment of

the MaxPerf Drilling Tool, produced K values ranging from 3.7 x

10-7

to 9.6 x 10-7

(or 0.033 m/d to 0.084 m/d –

consistent with the K values used in the PFS.

The

extensive hydrogeological data sets collected during the 2019 field

program will be incorporated into the hydrogeological model being

developed for Phoenix, which is expected to facilitate detailed

mine planning. The hydrogeological testing and modelling are being

undertaken by Petrotek Corporation (‘Petrotek’) –

specialists in the technical evaluation and field operation of

subsurface fluid flow and injection projects, including significant

ISR experience in various jurisdictions. Denison expects the

hydrogeological model and final report to be completed in Q1

2020.

|

|

MANAGEMENT’S DISCUSSION & ANALYSIS

|

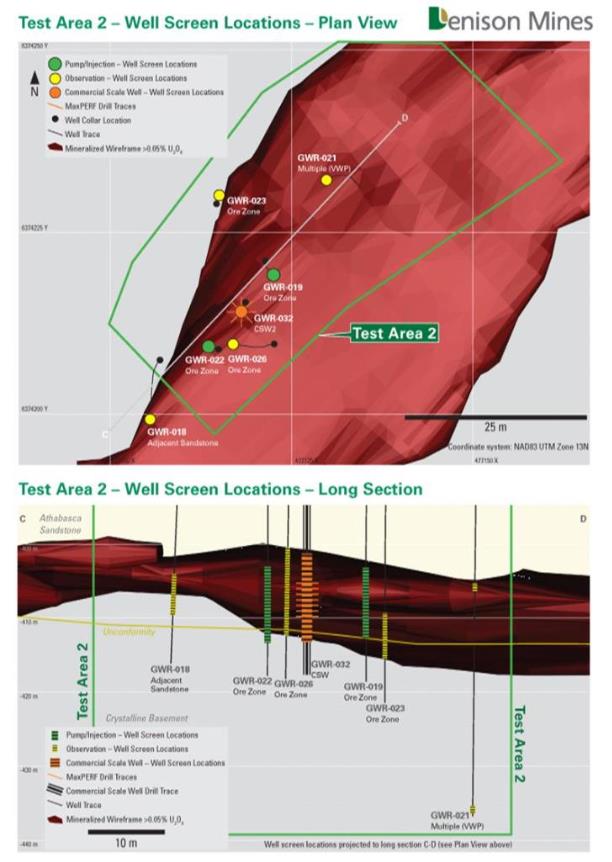

Figure 1: Phoenix Zone A plan view showing Test Areas and well

installations completed during 2019.

|

|

MANAGEMENT’S DISCUSSION & ANALYSIS

|

Figure 2: Plan map and long section showing Pump/Injection wells,

Observation wells and CSW1 completed

for ISR field testing in Test Area 1.

|

|

MANAGEMENT’S DISCUSSION & ANALYSIS

|

Figure 3:

Plan map and long section showing Pump/Injection wells, Observation

wells and CSW2

completed for ISR field testing in Test Area 2.

|

|

MANAGEMENT’S DISCUSSION & ANALYSIS

|

Other Engineering Activities

Metallurgical Testing

Metallurgical

test work commenced in the fourth quarter of 2019, utilizing core

samples collected during the ISR field test program. The

metallurgical test program is expected to include the

following:

Core Leach Tests:

These specialized tests involve the

testing of intact mineralized core samples, representative of the

in-situ conditions at Phoenix, to evaluate uranium recovery

specifically for the ISR mining method. Mineralized core samples of

between 0.75 metres and 1.5 metres in length were obtained from the

2019 ISR field test program. A triple-tube method of core recovery

was employed to ensure the core could be recovered with minimal

breakage and would be representative of the in-situ Phoenix ore.

Core samples were collected to represent the various ore types and

grade ranges (~1% to 60% U3O8)

at Phoenix.

A specialized laboratory apparatus will be

utilized to completely seal the outer diameter of the intact

mineralized core, thus ensuring that the leach solution travels

through the intact core sample (25 centimetres to 50 centimetres in

length). The tests are expected to utilize mining solution (or

lixiviant) with acid and oxidant concentrations, and injection

pressures, similar to those envisaged during commercial ISR

operations. Denison considers this type of specialized test

of intact competent core samples to be the most representative

available laboratory test of the natural leach conditions of the

host rock. Accordingly, these tests

are expected to provide important detailed metallurgical recovery

data that is expected to inform the Company’s understanding

of the potential scope of the start-up, steady state, and closure

of ISR wells.

In February 2020,

the Company reported on the results from the initial core leach

tests (see Denison press release dated February 19, 2020). At that

time, over 50 days of testing had been completed on a mineralized

core sample recovered from drill hole GWR-016. The core sample was

recovered from between 405 and 407 metres below surface within the

extent of the high-grade core of Phoenix Zone A. Various parameters

for lixiviant composition (including both acid and oxidant

concentration) have been tested to date. In all cases, the

lixiviant is injected into the core continuously and only

interrupted periodically if a change in the lixiviant composition

is required. After the initial test startup, uranium bearing

solution recovered from the core sample returned uranium content in

the range of 13.5 g/L to 39.8 g/L. The average uranium

concentration returned over the last 20 days of testing was 29.8

g/L – which represents a uranium content that is

approximately 200% higher than (or three times) the minimum level

used for the ISR process plant design in the PFS of 10

g/L.

Column Leach Tests:

Additional core samples in the same

grade ranges (~1% to 60% U3O8)

were obtained from the 2019 ISR field test program and preserved

for metallurgical tests. These samples will be crushed and packed

into test columns at the test facility in order to complete

traditional column leach tests utilizing the same mining solutions

as the Core Leach Tests. The testing is expected to provide

additional data on the recovery of uranium, and any other metals,

from the various ore types and grade ranges associated with the

Phoenix deposit under the envisaged ISR mining conditions. The

purpose of the Column Leach Tests is to correlate data from the

specialized Core Leach Tests to the traditional ISR laboratory

testing methods used during the PFS. Additionally, the Column Leach

Tests are able to generate uranium bearing solutions in larger

quantities for further laboratory testing of the process plant

flowsheet.

Bench-Scale Tests:

Upon completion of the Core Leach

Tests and Column Leach Tests (together, the ‘Leach

Tests’), Bench-Scale Tests of each unit operation in the

proposed flowsheet is planned. These tests are expected to use the

uranium-bearing solution produced from the Leach Tests. The data

from the Bench-Scale Tests will provide key details to proceed with

the next stage of process plant design for impurity removal,

uranium precipitation, solid liquid separation, reagent usage and

water treatment.

Metallurgical Modelling:

Concurrent with these tests, Denison

is building a metallurgical simulation model with the basic

parameters for mass, energy and water balances. The data from all

laboratory tests will be incorporated into a model update once

testing is completed.

The

timing of the above noted elements of the metallurgical test

program will be contingent on the Company raising sufficient

capital.

Electrical Power Studies

In July 2019,

Denison submitted a request to the provincial power utility

(SaskPower) for the completion of an interconnection study. The

study is expected to provide Denison with guidance on the

connection schedule, as well as capital and engineering costs

expected to be required to connect the Wheeler River site to the

existing overhead power lines located approximately six kilometres

from the proposed Phoenix ISR operation.

|

|

MANAGEMENT’S DISCUSSION & ANALYSIS

|

Additional Engineering Activities

Certain

additional engineering activities have commenced to complement the

environmental program, including those required to confirm the

water, heat and mass balances for the ISR operation and process

plant. These efforts will provide valuable inputs to the

EA.

Environmental and Sustainability Activities

Project Description and Environmental Assessment

In 2019, the

Company submitted a PD to the CNSC and a Technical Proposal

to the SK MOE to support the advancement of an ISR uranium mine at

Wheeler River. Acceptance of these

documents was announced by both the SK MOE and the CNSC on June

1st,

2019. This milestone marked the official commencement of the EA

process. Additionally, in December 2019, final confirmation of the

EA scope for the Project was received from the

CNSC.

The

Company identified the EA process as a key element of the Project's

critical path. Accordingly, Denison has initiated various studies

and assessments as part of the EA process, which is intended to

culminate in the preparation of the Project EIS. The EA is a

planning and decision-making tool, which involves predicting

potential environmental effects throughout the project lifecycle

(construction, operation, decommissioning and post-decommissioning)

at the site, and within the local and regional assessment

areas.

In

late December 2019, Denison received a Record of Decision from the

CNSC on the scope of the factors to be taken into account for the

Wheeler EA, which indicate that the EA will follow the CNSC’s

generic guidelines.

Environmental Baseline Data Collection

Baseline work

completed during 2019 included ongoing monitoring of ambient radon

and dust in the air, groundwater quality, and waste rock barrel

leachate chemistry. In addition, ambient gamma, sulphur dioxide and

nitrogen dioxide monitoring programs were initiated during the

year, and aquatic, terrestrial and heritage baseline surveys were

conducted to build upon the work completed to date, improving

Denison’s understanding of the existing environment around

the Project area, and supporting the completion of the

EA.

In 2019, 12

regional observation wells were also installed for the purpose of