6901 Rockledge Drive, Suite 800, Bethesda, Maryland20817

(301)564-3200

Securities registered pursuant to Section 12(b) of the Act:

Title of each class

Trading Symbol

Name of each exchange on which registered

Class A Common Stock, par value $0.10 per share

LEU

NYSE

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes☒. No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐.No☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer

☒

Smaller reporting company

☐

Accelerated filer

☐

Emerging growth company

☐

Non-accelerated filer

☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No☒

The aggregate market value of Common Stock held by non-affiliates computed by reference to the price at which the Common Stock was last sold as reported on the New York Stock Exchange as of June 30, 2025, was $3.2 billion. As of February 2, 2026, there were 18,945,365 shares of the registrant’s Class A Common Stock, par value $0.10 per share, and 719,200 shares of the registrant’s Class B Common Stock, par value $0.10 per share, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive proxy statement for the 2026 annual meeting of shareholders to be filed with the Securities and Exchange Commission within 120 days after the end of fiscal year 2025 are incorporated by reference into Part III of this Annual Report on Form 10-K.

American Centrifuge Operating LLC, a subsidiary of Centrus

Board

Centrus Energy Corp.’s Board of Directors

Centrus

Centrus Energy Corp.

Enrichment Board

Separate Board of Directors at Enrichment Corp., a subsidiary of Centrus Energy Corp.

Enrichment Corp.

United States Enrichment Corporation, a subsidiary of Centrus

Oak Ridge

Technology and Manufacturing Center in Oak Ridge, Tennessee

Paducah GDP

Paducah Gaseous Diffusion Plant, an enrichment plant in Paducah, Kentucky formerly operated by Enrichment Corp.

Piketon

Production facility in Piketon, Ohio

Portsmouth GDP

Portsmouth Gaseous Diffusion Plant, an enrichment plant near Portsmouth, Ohio, formerly operated by Enrichment Corp.

USEC-Government

Enrichment Corp. prior to 1993, a wholly-owned government corporation prior to its privatization in July 1998

Other Terms and Abbreviations

0% Convertible Notes

0% Convertible Senior Notes, maturing August 2032 unless repurchased, redeemed or converted

2.25% Convertible Notes

2.25% Convertible Senior Notes maturing November 2030 unless repurchased, redeemed or converted

2002 DOE-USEC Agreement

June 17, 2002 agreement between Centrus (then known as USEC Inc.) and the DOE

2014 Plan

The Company’s 2014 Equity Incentive Plan

2019 Plan

The Company’s 2019 Executive Incentive Plan

5B Cylinders

Storage cylinders for HALEU UF6 produced by the HALEU demonstration cascade

8.25% Notes

8.25% Notes, originally maturing February 2027, redeemed in March 2025

American Centrifuge

Advanced uranium enrichment gas centrifuge technology previously developed, based on the proven workable U.S. centrifuge technology developed by DOE in the mid-1980s and utilized in a demonstration facility in 2012-2013

American Centrifuge Plant

Refers to a demonstration facility in Piketon, Ohio where USEC planned to install a lead cascade of centrifuge machines to demonstrate the American Centrifuge technology under the terms of the 2002 DOE-USEC Agreement

Annual Meeting

The Company’s annual meeting of shareholders

ARDP

DOE’s Advanced Reactor Demonstration Program

ATM

At the Market

Atomic Energy Act

Atomic Energy Act of 1954 is the fundamental U.S. law on both the civilian and the military uses of nuclear materials and provides for both the development and the regulation of the uses of nuclear materials and facilities in the United States

Centrifuge IP

Centrifuge Technology Intellectual Property

Class A Common Stock

Class A common stock, $0.10 par value per share

Class B Common Stock

Class B common stock, $0.10 par value per share

3

CNEIC

China Nuclear Energy Industry Corporation

COBC

Centrus’ Code of Business Conduct

Code

Internal Revenue Code of 1986

Common Stock

Class A Common Stock and Class B Common Stock

Consent Solicitation

Consent solicitation related to the results of the 2021 tender offer

COVID-19

2019 Novel Coronavirus

D&D

Decontamination and Decommissioning

DOC

U.S. Department of Commerce

DOE

U.S. Department of Energy

EU

European Union

Exchange Act

Securities Exchange Act of 1934, as amended

FAR

U.S. Government’s Federal Acquisition Regulation is the primary regulation for use by all executive agencies in their acquisition of supplies and services with appropriated funds.

HALEU

High Assay Low-Enriched Uranium

HALEU Deconversion Contract

An IDIQ Contract awarded by DOE to ACO on October 4, 2024 for the deconversion of HALEU

HALEU Demonstration Contract

Three-year, $115.0 million cost-share contract with DOE signed in 2019 by Centrus’ subsidiary, ACO

HALEU Production Contract

An IDIQ Contract awarded by DOE to ACO on October 16, 2024 for the production of HALEU

HALEU Operation Contract

HALEU production contract with DOE signed in 2022

IDIQ

Indefinite Delivery, Indefinite Quantity, a type of government contract that provides for an indefinite quantity, within stated limits, of supplies or services during a fixed period under which the government places orders for individual requirements.

IEA

International Energy Agency

Import Ban Act

The “Prohibiting Russian Uranium Imports Act” enacted on May 13, 2024 that bans imports of LEU from Russia into the U.S., effective August 11, 2024, subject to issuance of waivers by the DOE

IT

Information Technology

LEU

Low-Enriched Uranium; term is also used to refer to the Centrus Energy Corp. business segment which supplies commercial customers with various components of nuclear fuel

LEU Production Contract

An IDIQ Contract awarded by DOE to ACO on December 10, 2024 for expansion of domestic LEU production

MB Group

Mr. Morris Bawabeh, Kulayba LLC and M&D Bawabeh Foundation, Inc.

Natural Uranium

Raw material needed to produce LEU and HALEU

NAV

Net asset value

NOL

Net Operating Loss

NRC

U.S. Nuclear Regulatory Commission

NRV

Net realizable value

NUBIL

Net unrealized built-in loss

Orano

Orano Cycle

Orano Supply Agreement

Long-term supply of SWU contained in LEU, signed by Enrichment Corp. with Orano in 2018

Power MOU

Memorandum of understanding between the DOE and USEC-Government

4

Price-Anderson Act

Price-Anderson Nuclear Industries Indemnity Act (Section 170 of the U.S. Atomic Energy Act of 1954, as amended)

RFP

Request for Proposal

Rights Agreement

Section 382 Rights Agreement, dated as of April 6, 2016, by and among the Company and Computershare Trust Company, N.A. and Computershare Inc., as rights agent, as amended

Series A Preferred Stock

Series A Participating Cumulative Preferred Stock, par value $1.00 per share

Series B Preferred Stock

Series B Senior Preferred Stock, par value $1.00 per share

Rosatom

Russian State Atomic Energy Corporation, which is a multi-industry holding company which comprises assets in power engineering, machine building, and construction.

RSA

1992 Russian Suspension Agreement, as amended

Russian Decree

Russian Federal Decree No. 1544, enacted on November 14, 2024, that rescinded TENEX’s general license to export LEU to the United States or to entities registered in the United States, effective through December 31, 2025 and extended through December 31, 2027 by Russian Federal Decree No. 1516, enacted on October 2, 2025

SARs

Stock appreciation rights are a form of equity-based compensation giving employees the right to receive an amount of stock or cash, the value of which equals the appreciation in a company’s stock price between the award’s grant date and its vesting/exercise date.

SEC

U.S. Securities & Exchange Commission

SWU

Separative work unit which represents the level of effort required to increase the concentration of U235 in natural uranium.

Technical Solutions

The Centrus business segment focused on uranium enrichment for the nuclear industry and the U.S. government and advanced manufacturing, engineering and other technical services to government and private sector customers.

TENEX

Russian government-owned entity TENEX, Joint-Stock Company

TENEX Supply Contract

March 23, 2011 Enriched Product Transitional Supply Contract with TENEX through 2028

U.S. GAAP

Generally Accepted Accounting Principles in the United States

U235

Uranium-235 isotope

U238

Uranium-238 isotope

U3O8

Uranium oxide, aka “yellowcake”

UF6

Uranium hexafluoride

URENCO

Urenco, Limited, a consortium owned or controlled by the British and Dutch governments and two German utilities which provides uranium enrichment and associated services, and sells uranium components of enriched uranium product.

USW

United Steelworkers Local 689-5 union

WNA

World Nuclear Association

5

FORWARD-LOOKING STATEMENTS

CAUTIONARY STATEMENTS REGARDING FORWARD-LOOKING INFORMATION

This Annual Report on Form 10-K of Centrus (the “Company,” “we” or “us”) contains “forward-looking statements” within the meaning of Section 21E of the Exchange Act of 1934 and the Private Securities Litigation Reform Act of 1995. In this context, forward-looking statements mean statements related to future events, which may impact our expected future business and financial performance, and often contain words such as “expects”, “anticipates”, “intends”, “plans”, “believes”, “will”, “should”, “could”, “would” or “may” and other words of similar meaning. These forward-looking statements are based on information available to us as of the date of this Annual Report on Form 10-K and represent management’s current views and assumptions with respect to future events and operational, economic and financial performance. Forward-looking statements are not guarantees of future performance, events or results and involve known and unknown risks, uncertainties and other factors, which may be beyond our control, and which may be exacerbated by any worsening of the global business and economic environment, including but not limited to, risks and uncertainties related to the following:

•the war in Ukraine and other geopolitical conflicts, including the resulting bans, laws, tariffs, sanctions or other government measures, and actions by third parties, including contractual counterparties, as a result of such conflicts that could directly or indirectly impact our ability to obtain, deliver, transport, sell or collect payment for, LEU or the SWU and natural uranium hexafluoride components of LEU;

•our reliance on third party suppliers to provide essential products and services to us;

•restrictions on imports and exports, including those imposed under the RSA, and related international trade legislation;

•our government contracts, including related to government shutdowns, changes to the U.S. government’s appropriated funding levels for HALEU and the government’s inability to satisfy its obligations, and our lease to our facility in Piketon, Ohio;

•our receipt of additional task orders under the HALEU Production Contract, LEU Production Contract and HALEU Deconversion Contract and, if awarded, the nature, timing and amount thereof;

•our ability to obtain new contracts or funding to be able to continue operations;

•whether or when government demand for HALEU or LEU for government or commercial uses will materialize and at what level;

•the impact and potential extended duration of a supply/demand imbalance in the market for LEU;

•significant competition from major LEU producers, including foreign competitors, who may be less cost sensitive than we are;

•limitations on our ability to compete in foreign markets;

•pricing trends and demand in the uranium and enrichment markets, especially in light of the potential of limited supply and our dependence on others for deliveries of LEU;

•our ability to successfully implement our planned expansion projects in Piketon, Ohio and Oak Ridge, Tennessee;

•natural and other disasters;

•pandemics and other health crises;

•the fact that our revenue is largely dependent on our largest customers and our sales backlog;

•our long-term liabilities, including our postretirement health and life benefit obligations, our 0% Convertible Notes and our 2.25% Convertible Notes;

•failures or security, including cybersecurity, breaches of our information technology systems; and

6

•the impact of, or changes to, government regulation and policies or interpretation of laws or regulations, including by the SEC, DOE, DOC and the NRC.

For a more detailed discussion of these risks and others that could cause actual results to differ materially from those contained in our forward-looking statements, please see (a) Part I, Item 1A, Risk Factors, (b) Part II, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, (c) Part II, Item 8, Financial Statements and Supplementary Data: Note 17, Commitments and Contingencies, and (d) other factors discussed in our filings with the SEC. These factors may not constitute all factors that could cause actual results to differ from those discussed in any forward-looking statement. Accordingly, forward-looking statements should not be relied upon as a predictor of actual results, and readers are cautioned not to place undue reliance on these forward-looking statements, which apply only as of the date of this Annual Report. The Company does not undertake any obligation to publicly release any revision to its forward-looking statements to reflect events or circumstances that may arise after the date of this Annual Report on Form 10-K unless required by law.

7

PART I

Item 1.Business

Overview

Centrus Energy Corp., a Delaware corporation, is a trusted supplier of nuclear fuel components for the nuclear power industry, which provides a reliable source of carbon-free energy, and provides enrichment and technical services for public and private customers. References to “Centrus”, the “Company”, “our”, or “we” include Centrus Energy Corp. and its wholly-owned subsidiaries as well as the predecessor to Centrus, unless the context indicates otherwise.

Centrus operates two business segments: (a) LEU, which supplies various components of nuclear fuel to commercial customers from our global network of suppliers, and (b) Technical Solutions, which provides advanced uranium enrichment for the nuclear industry and the U.S. government and advanced manufacturing and other technical services to government and private sector customers. Our current uranium enrichment involves HALEU production and other capabilities necessary for production of advanced nuclear fuel to power existing and next-generation reactors around the world.

Our LEU segment provides most of the Company’s revenue and involves the sale of LEU, the fissile component of nuclear fuel, primarily to utilities that operate commercial nuclear power plants. The majority of these sales are for the enrichment component of LEU, which is measured in SWU. Centrus also sells natural uranium hexafluoride (the raw material needed to produce LEU) and occasionally sells uranium concentrates, uranium conversion, or LEU with the natural uranium hexafluoride and SWU components combined into one sale.

LEU is a critical component in the production of nuclear fuel for reactors that produce electricity. We supply LEU and its components to both domestic and international utilities for use in nuclear reactors worldwide. We provide LEU from multiple sources, including medium- and long-term supply contracts, spot purchases and our inventory. As a long-term supplier of LEU to our customers, our objective is to provide value through the reliability and diversity of our supply sources.

Our LEU segment backlog includes medium and long-term sales contracts and contingent sales commitments with major utilities through 2040. We have secured cost-competitive supplies of SWU under long-term contracts through the end of this decade designed to allow us to fill our existing customer orders and make new sales. However, supply chain disruptions may impact our ability to fill existing customer orders. A market-related price reset provision in the TENEX Supply Contract, which is our largest supply contract, became effective in 2019 – when market prices for SWU were near historic lows – which has significantly lowered our cost of sales and contributed to improved margins since 2019.

Our Technical Solutions segment is focused on uranium enrichment for the nuclear industry and the U.S. government and advanced manufacturing, engineering and other technical services to government and private sector customers. Under a contract with the DOE, our Technical Solutions segment is operating uranium enrichment capacity for HALEU production, and other capabilities necessary for production of advanced nuclear fuel to meet the evolving needs of the global nuclear industry and the U.S. government. We are also leveraging our unique technical expertise, operational experience, and specialized facilities to expand and diversify our business beyond uranium enrichment, offering new services to existing and new customers in complementary markets.

Our Technical Solutions segment is committed to the restoration of America’s domestic uranium enrichment capabilities for LEU and HALEU, in order to play a critical role in meeting U.S. national security and energy security requirements and advancing America’s clean energy, energy security, and national security objectives. Our Technical Solutions segment is also focused on repairing broken and vulnerable supply chains, providing clean energy jobs, and supporting the communities in which we operate. Our goal is to deliver major components of the next-generation nuclear fuels that will provide reliable carbon-free power around the world.

8

The United States has not had domestic uranium enrichment capability suitable to meet U.S. national security requirements since the Paducah GDP shut down in 2013. DOE continues to draw down its finite stockpile of Cold War-era enriched uranium but is expected to need a new source of U.S.-origin enrichment in the future. Longstanding U.S. policy and binding nonproliferation agreements prohibit the use of foreign-origin civilian enrichment technology for U.S. national security missions. Our AC100M centrifuge currently is the only deployment-ready U.S. uranium enrichment technology that can meet these national security requirements.

Centrus is pioneering U.S. production of HALEU, enabling the deployment of a new generation of HALEU-fueled reactors to meet the world’s growing need for carbon-free power. On October 11, 2023, the Company began enrichment operations at its HALEU production facility in Piketon, Ohio under its contract with DOE. On November 7, 2023, the Company made its first delivery of HALEU to the DOE, completing Phase 1 by successfully demonstrating its HALEU production process. HALEU is a high-performance nuclear fuel component that will be required by a number of advanced reactor and fuel designs that are now under development for commercial and government uses. While existing reactors typically operate on LEU with the U235 concentration below 5%, HALEU is further enriched so that the U235 concentration is between 5% and 20%. The higher U235 concentration offers a number of potential advantages, which may include better fuel utilization, improved performance, fewer refueling outages, simpler reactor designs, reduced waste volumes, and greater nonproliferation resistance.

The lack of HALEU supply is a major obstacle to the successful commercialization of these new reactors. For example, in surveys of advanced reactor developers conducted by the U.S. Nuclear Industry Council in 2020 and 2021, respondents indicated that the number one issue that “keeps you up at night” was access to HALEU. As the only company with a license from the NRC actively enriching up to 20% U235 assay HALEUand that is operating a small scaled HALEU production facility, Centrus is uniquely positioned to fill a critical gap in the supply chain and facilitate the deployment of these promising next-generation reactors.

The war in Ukraine, along with the Import Ban Act and the Russian Decree, have contributed to a significant increase in market prices for enrichment and have prompted calls for public and private investment in new, domestic uranium enrichment capacity not only for HALEU production but also for LEU production to support the existing fleet of reactors. As a result, Centrus is exploring the opportunity to deploy LEU enrichment alongside HALEU enrichment to meet a range of commercial and U.S. government requirements, which would bring cost synergies while increasing revenue opportunities. On September 25, 2025, we announced plans for a major expansion of our uranium enrichment capacity in Piketon, Ohio, including plans for large-scale production of both LEU and HALEU. In December 2025, we initiated design work on a 150,000 square foot training, operations and maintenance Facility in Piketon, Ohio and began domestic centrifuge manufacturing to support commercial LEU enrichment activities at our Piketon, Ohio, facility. Our ability to deploy LEU and/or HALEU enrichment, and the timing, sequencing, and scale of those capabilities, is subject to our continued ability to obtain public and private funding.

The Company’s work on HALEU began under the HALEU Demonstration Contract executed with the DOE in 2019, to construct a cascade of 16 AC100M centrifuges in Piketon, Ohio to demonstrate HALEU production. The DOE funded the HALEU Demonstration Contract up to $173.0 million with a period of performance that ended November 30, 2022. On November 10, 2022, the DOE awarded the HALEU Operation Contract to the Company with a base contract value of approximately $150.0 million in two phases through 2024. Phase 1 included an approximately $30.0 million cost-share contribution from Centrus matched by approximately $30.0 million from the DOE to complete construction of the cascade, begin operations and produce the initial 20 kilograms of HALEU UF6. On November 7, 2023, the Company made its first contractual delivery of HALEU to the DOE, completing Phase 1 of the contract.

9

The Company transitioned to Phase 2 of the HALEU Operation Contract in November 2023 which included continued operations and maintenance of the cascade and production for a full year at an annual production rate of 900 kilograms of HALEU UF6. Under Phase 2, Centrus produced and contractually delivered the Phase 2 production target of 900 kilograms of HALEU UF6 to DOE, and was compensated on a cost-plus-incentive-fee basis, with an initial Phase 2 contract value of approximately $90.0 million. As of December 31, 2025, DOE has increased the Phase 2 contract value and related funding to $170.1 million and extended the Phase 2 period of performance to January 31, 2026.

On June 17, 2025, the DOE amended the HALEU Operation Contract to divide the first three-year option period into a first option period of one year (“Option 1a”) and a second option period of two years (“Option 1b”). The amendment established a target cost and fee for Option 1a of approximately $99.3 million and $8.7 million, respectively, and a target cost and fee for Option 1b of $163.5 million and $15.2 million, respectively. The DOE exercised Option 1a and extended the period of performance to June 30, 2026. As of December 31, 2025, Option 1a is funded for the contract value of $108.2 million. Additionally, the amendment acknowledged that the estimated cost associated with Option 1b is insufficient to support full performance due to known cost increases since the award of the HALEU Operation Contract and indicated that the Company will need to submit a revised cost proposal for review and negotiation prior to DOE’s consideration of Option 1b.

The DOE continues to pursue the availability of HALEU for the ARDP and for the advanced reactor market and the availability of domestically enriched uranium in a quantity that would be sufficient to address a supply disruption and gaps in domestic production and enrichment. Congress appropriated a total of approximately $3.4 billion to the DOE to jumpstart U.S. nuclear fuel production, including both LEU and HALEU enrichment. Based on this funding, the DOE issued a series of three RFPs covering HALEU production, HALEU deconversion, and LEU production. In late 2024, the DOE made initial selections under each of the RFPs. Centrus was among the awardees for all three RFPs under IDIQ structures (the HALEU Deconversion Contract, HALEU Production Contract, and the LEU Production Contract).

Each of these IDIQ awards carries a $2.0 million contract minimum for each awardee and is subject to an overall contract ceiling covering all awardees. Under the IDIQ awards, the DOE can issue task orders to the awardees and then allocate available funding to those task orders. The ultimate value of the awards to Centrus, and the scale of the expansion supported, will depend upon the scope of task orders that DOE may subsequently issue to Centrus under the contracts for which Centrus intends to compete.

On November 6, 2024, DOE issued requests for task order proposals under the HALEU Deconversion Contract and the HALEU Production Contract, respectively. The requests for proposals contemplated the DOE issuing the task orders on a time-and-material basis with a two year period of performance for the purpose of describing the technical approach and price in an optimization study to support DOE in establishing the commercial production of HALEU and commercial deconversion of HALEU, respectively. On January 9, 2025, we submitted our proposals in response to these requests for task order proposals. On August 14, 2025, DOE, without making any awards under the first task order proposal request, issued a second request for task order proposals under the HALEU Production Contract. The second request provided $900.0 million to support the deployment of commercial HALEU enrichment capacity. On January 5, 2026, the DOE announced that ACO was selected for award a $900.0 million task order to expand its uranium enrichment facility in Piketon, Ohio, to include commercial-scale production of HALEU. The task order is subject to negotiation of a definitive agreement and there are no guarantees about whether or when funding by the DOE for such expansion would be awarded. The award also includes options, at the DOE’s discretion, for up to $170.0 million to produce and deliver HALEU to the DOE. The Company and DOE are working to finalize the contract that will govern the award.

On March 30, 2025, the Company submitted its proposal in response to a request for task order proposals from the DOE for a report and additional deliverables under the LEU Production Contract. On April 11, 2025, the Company was awarded a time and materials task order with a total award ceiling of approximately $0.5 million.

10

There is no assurance that we will be awarded any additional task orders under any of our contracts and, if awarded, the nature, timing and amount of the task orders that may be issued under any award.

On November 20, 2024, we announced the resumption of centrifuge manufacturing activities and expansion of the manufacturing capacity at our facility in Oak Ridge, Tennessee. This was followed with an announcement on January 23, 2026 that the Company plans to invest more than $560.0 million over the next several years to transition the facility to a high-rate manufacturing plant and support the production of thousands of advanced centrifuges in Oak Ridge, Tennessee. The first new centrifuges produced in Oak Ridge are expected to come online in Ohio in 2029. We are investing an additional $60.0 million over an 18 month period to lay the groundwork to support a potential large-scale expansion of uranium enrichment in Piketon, Ohio.

On September 25, 2025, we announced plans for a major expansion of our uranium capacity in Piketon, Ohio, including plans for large-scale production of both LEU and HALEU to meet commercial and government requirements. In December 2025, we initiated design work on a 150,000 square foot training, operations and maintenance facility in Piketon, Ohio – a critical piece of site infrastructure necessary to support the Company's plans for a major expansion of its uranium enrichment capacity in Piketon. The project involves a significant renovation and rehabilitation of an existing, largely vacant building on the site of the American Centrifuge Plant, with construction activities set to begin in early 2026. The facility is expected to include a mix of office space, training facilities, and maintenance bays to support plant operations. Also in December 2025, we began domestic centrifuge manufacturing to support commercial LEU enrichment activities at our Piketon, Ohio, facility. This strategic move enables the Company to capitalize on its many first-mover advantages in U.S.-owned domestic uranium enrichment, and marks one of the most consequential transformations in the Company's and the United States' uranium enrichment history. Centrus plans to leverage its multi-billion-dollar uranium enrichment expansion to meet its growing backlog of $2.3 billion in contingent LEU sales to U.S. and international customer contracts, and targets future commercial-scale production of HALEU, as well. For further details, refer to Part 1, Item 1, Business -Low Enriched Uranium – LEU Backlog and Technical Solutions - Technical Solutions Backlog.

The Qualifying Advanced Energy Project Credit (“§48C”) was established by the American Recovery and Reinvestment Act of 2009 and renewed and expanded under the IRA. The §48C program aims to strengthen U.S. industrial competitiveness and clean energy supply chains. On October 18, 2024, the Company submitted an application for a clean energy manufacturing and recycling project associated with re-equipping our manufacturing property at our manufacturing facility in Oak Ridge. This will recreate a viable enrichment supply chain and allow ACO to manufacture centrifuge parts to be used in centrifuge machines to enrich uranium. Our application requested an allocation of $62.4 million based on a qualified investment in eligible property of $208.0 million made by Centrus. On January 10, 2025, the Company was informed that the Internal Revenue Service (“IRS”) granted our request for a $62.4 million credit allocation for this facility. Centrus has two years from that date to provide evidence that the requirements of the credit have been met thus certifying our credit allocation. Upon certification of our credit allocation, we then have two years from that date to notify the DOE that the qualified investment in eligible property is placed in service to receive the credit allocation. It is uncertain how Executive Order 14154 will impact the IRS determination regarding our application request. For further details refer to Part II, Item 7, Liquidity and Capital Resources in this Annual Report on Form 10-K.

Section 6418 was added to the Code as part of the IRA and allows certain eligible taxpayers to elect to transfer certain clean energy tax credits to unrelated taxpayers for cash rather than use the credits to offset their U.S. federal income tax liability. The Company expects to monetize all credit allocations received from §48C by transferring them to unrelated taxpayers for cash. It is uncertain how Executive Order 14154 will impact the IRS determination regarding our application request.

For further details, refer to Part II, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations - Market Conditions and Outlook. For a discussion of the potential risks and uncertainties facing our business, see Part I, Item 1A, Risk Factors.

11

Backlog

The Company’s backlog across both segments was $3.8 billion and $3.7 billion as of December 31, 2025 and 2024, respectively, and extends to 2040. The backlog is recognized as revenue in future periods as work is performed or deliveries of SWU and uranium are made. For further details, refer to Part 1, Item 1, Business - Low Enriched Uranium - LEU Backlog and Technical Solutions - Technical Solutions Backlog.

Low Enriched Uranium

LEU consists of two components: SWU and natural uranium hexafluoride. Revenue from our LEU segment is derived primarily from:

•sales of the SWU component of LEU,

•sales of natural uranium hexafluoride, uranium concentrates, or uranium conversion, and

•sales of enriched uranium product that include both the natural uranium hexafluoride and SWU components of LEU.

Our LEU segment accounted for approximately 77% of our total revenue for the year ended December 31, 2025. The majority of our customers are domestic and international utilities that operate nuclear power plants. Our agreements with electric utilities are primarily medium and long-term, fixed-commitment contracts under which customers are obligated to purchase a specified quantity of the SWU component of LEU from us. Contracts where we sell both the SWU and natural uranium hexafluoride components of LEU to utilities or where we sell natural uranium hexafluoride to utilities and other nuclear fuel related companies are generally shorter-term, fixed-commitment contracts.

Uranium and Enrichment

Uranium is a naturally occurring element and is mined from deposits located in Kazakhstan, Canada, Australia, and several other countries, including the United States. According to the WNA, there are adequate measured resources of natural uranium to fuel nuclear power at current usage rates for about 90 years. In its natural state, uranium is principally comprised of two isotopes: U235 and U238. The concentration of U235 in natural uranium is only 0.711% by weight. Uranium enrichment is the process by which the concentration of U235 is increased. Most commercial nuclear power reactors require LEU fuel with a U235 concentration greater than natural uranium of up to 5% by weight. Future reactor designs currently under development will likely require higher U235 concentration levels of up to 20%.

SWU is a standard unit of measurement that represents the effort required to separate natural uranium between enriched uranium, having a higher percentage of U235, and depleted uranium, having a lower percentage of U235. The SWU contained in LEU is calculated using an industry standard formula based on the physics of enrichment. The amount of enrichment deemed to be contained in LEU under this formula is commonly referred to as its SWU component and the quantity of natural uranium hexafluoride deemed to be contained in LEU under this formula is referred to as its uranium or “feed” component.

While in some cases customers purchase both the SWU and uranium components of LEU from us, utility customers typically provide the natural uranium hexafluoride to us as part of their enrichment contracts and in exchange we deliver LEU to these customers and charge for the SWU component. Title to natural uranium hexafluoride provided by customers generally remains with the customer until Centrus delivers the LEU, at which time title to the LEU is transferred to the customer, and Centrus takes title to the natural uranium hexafluoride.

12

The following outlines the steps for converting natural uranium into LEU fuel, commonly known as the nuclear fuel cycle:

Mining and Milling. Natural, or unenriched, uranium is removed from the earth in the form of ore and then crushed and concentrated.

Conversion. U3O8 is combined with fluorine gas to produce UF6, a solid at room temperature and a gas when heated. UF6 is shipped to an enrichment plant.

Enrichment. UF6 is enriched in a process that increases the concentration of the U235 isotope in the UF6 from its natural state of 0.711% up to 5%, or LEU, which is usable as a fuel for current light water commercial nuclear power reactors. Future commercial reactor designs may use uranium enriched up to 20% U235, or HALEU.

Fuel Fabrication. LEU is then converted to uranium oxide and formed into small ceramic pellets by fabricators. The pellets are loaded into metal tubes that form fuel assemblies, which are shipped to nuclear power plants. As the advanced reactor market develops, HALEU may be converted to uranium oxide, metal, chloride or fluoride salts, or other forms and loaded into a variety of fuel assembly types optimized for the specific reactor design.

Nuclear Power Plant. The fuel assemblies are loaded into nuclear reactors to create energy from a controlled chain reaction. Nuclear power plants generate approximately 18% of U.S. electricity and 9% of the world’s electricity.

Used Fuel Storage. After the nuclear fuel has been in a reactor for several years its efficiency is reduced and the assembly is removed from the reactor’s core. The used fuel is warm and radioactive and is kept in a deep pool of water for several years. Many utilities have elected to then move the used fuel into steel or concrete and steel casks for interim storage.

13

LEU Backlog

Our backlog in the LEU segment extends to 2040. As of December 31, 2025 and 2024, our backlog is approximately $2.9 billion and $2.8 billion, respectively. The backlog is the estimated aggregate dollar amount of revenue for future SWU and uranium deliveries primarily under medium and long-term contracts with fixed commitments. Of the $2.9 billion, approximately $2.3 billion represents contingent LEU sales contracts and commitments, with $2.1 billion of the total under definitive agreements and $0.2 billion of the total subject to entering into definitive agreements, in support of potential construction of LEU production capacity at the Piketon, Ohio facility. The contingent LEU sales contracts and commitments also depend on our ability to secure substantial public and private investment necessary to build new enrichment capacity. The LEU segment backlog also includes approximately $0.1 billion of deferred revenue and advances from customers as of December 31, 2025, whereby customers have made advance payments to be applied against future deliveries. No orders in our backlog are considered at risk, in material respect, related to customer operations. However, these medium and long-term contracts are subject to significant risks and uncertainties, including existing import and export laws and restrictions, such as the RSA and Import Ban Act, which limit imports of Russian uranium products into the United States, and the Russian Decree, which limits exports of Russian uranium products to the United States. These risks and uncertainties apply to our sales using material procured under the TENEX Supply Contract, as well as the potential for additional sanctions and other restrictions affecting the Company or its suppliers, in response to the evolving situation regarding the war in Ukraine or international diplomatic relations. If any of our LEU contracts were to be terminated, our remaining backlog would be reduced by the expected value of the cancelled contracts or forgone options. There is no assurance that the revenues projected will be realized, or, if realized, will result in profits.

Most of our customer contracts provide for fixed purchases of SWU during a given year. Our backlog estimate is based partially on customers’ estimates of the timing and size of their fuel requirements and other assumptions that are subject to change. For example, depending on the terms of specific contracts, the customer may be able to increase or decrease the quantity delivered within an agreed range. Our backlog estimate is also based on our estimates of selling prices, which may be subject to change. For example, depending on the terms of specific contracts, prices may be adjusted based on escalation using a general inflation index, published SWU price indicators prevailing at the time of delivery, and other factors, all of which are variable. We use external composite forecasts of future market prices and inflation rates in our pricing estimates. Refer to Part I, Item 1A, Risk Factors, for a discussion of risks related to our backlog.

Suppliers

We have a diverse base of firm and prospective supply that includes:

•existing inventory of LEU (Refer to Part II, Item 8, Financial Statements and Supplemental Data: Note 4, Inventories, in the Consolidated Financial Statements in Part IV of this Annual Report);

•long-term contracts with enrichment producers;

•purchases and loans from secondary sources, including fabricators and utility operators of nuclear power plants that may have excess inventory; and

•spot purchases of SWU, uranium, and LEU.

We aim to continue to further diversify this base of supply and take advantage of opportunities to obtain additional short and long-term supplies of LEU. Currently, our largest supplier of SWU is TENEX followed by the French government-owned company, Orano.

14

Under the TENEX Supply Contract, we purchase SWU contained in LEU, and we deliver natural uranium hexafluoride to TENEX for the LEU’s uranium component. The TENEX Supply Contract extends through 2028. We typically pay for the SWU contained in the LEU and supply natural uranium to TENEX for the natural uranium component. SWU pricing is determined by a formula using a combination of market-related price points and other factors. The LEU that we obtain from TENEX under the TENEX Supply Contract currently is subject to quotas and other restrictions under the RSA between the United States and the Russian Federation which governs imports of Russian uranium products into the United States. These quotas allow us to supply Russian LEU to our customers through 2028. However, as discussed below, supply under the TENEX Supply Contract has been impacted by the Import Ban Act and the Russian Decree. The terms of the RSA, as extended, were adopted into law by the U.S. Congress in the Consolidated Appropriations Act, 2021. Refer to Item 1A, Risk Factors - Operational Risks for further discussion.

Centrus will need to make additional sales to place all the Russian LEU required to meet our SWU purchase obligations to TENEX. Although the RSA quotas cover most of the Russian LEU that we must order to fulfill our purchase obligations under the TENEX Supply Contract, we expect that a small portion of the LEU that we expect to order during the term of the TENEX Supply Contract will need to be delivered to customers that will use it in non-U.S. reactors.

The war in Ukraine escalated tensions between Russia and the international community. As a result, the United States and other countries imposed, including through the United States’ enactment of the Import Ban Act discussed below, and may continue imposing, additional sanctions, tariffs, and export controls against certain Russian products, services, organizations and/or individuals, and Russia passed the Russian Decree as discussed below. Such additional restrictions, and Russian response thereto, could affect our ability to purchase, take delivery of, transport, or re-sell Russian uranium enrichment, engage in transactions with TENEX, or implement the TENEX Supply Contract, which would have a negative material impact on our business. Refer to Part I, Item 1, Business -Competition and Foreign Trade - War in Ukraine and Part I, Item 1A, Risk Factors - Economic and Industry Risks - Dependence on our largest customers or suppliers could adversely affect us, for further discussion.

In addition to limitations targeted specifically at imports of LEU or exports of natural uranium back to Russia, the evolving sanctions imposed by the United States and foreign governments on the mechanisms used to make payments to Russia and to obtain services, including transportation, have increased the risk that implementation of the TENEX Supply Contract may be disrupted frequently. If the U.S. government were to prohibit companies and individuals from engaging in transactions with Rosatom and its subsidiaries, including TENEX, the Company and its suppliers could not implement the TENEX Supply Contract absent a license or other authorization from the sanctioning government.

Given all of the foregoing, we continue to monitor the situation closely and assess the potential impact of any new sanctions or restrictions and how the impact on the Company might be mitigated. Refer to Part I, Item 1A, Risk Factors - Operational Risks and - War in Ukraine Risks, for further discussion.

We also have an agreement with Orano for the long-term supply of SWU contained in LEU, with deliveries that commenced in 2023 and extend through 2030. Under the Orano Supply Agreement, we purchase SWU contained in LEU received from Orano, and then deliver natural uranium to Orano for the natural uranium feed component of LEU. The Orano Supply Agreement provides flexibility to adjust purchase volumes, subject to annual minimums and maximums, in fixed amounts that vary year by year. The pricing for the purchased SWU is determined by a formula that uses a combination of market-related price points and other factors, and is subject to certain floors and ceilings. Prices are payable in a combination of U.S. dollars and euros.

We procure LEU from other sources under short-term and long-term contracts and have inventories available that diversify our supply portfolio and provide flexibility to help us meet the needs of our customers. We also have agreements to borrow SWU that we can use to optimize our purchases and deliveries over time.

15

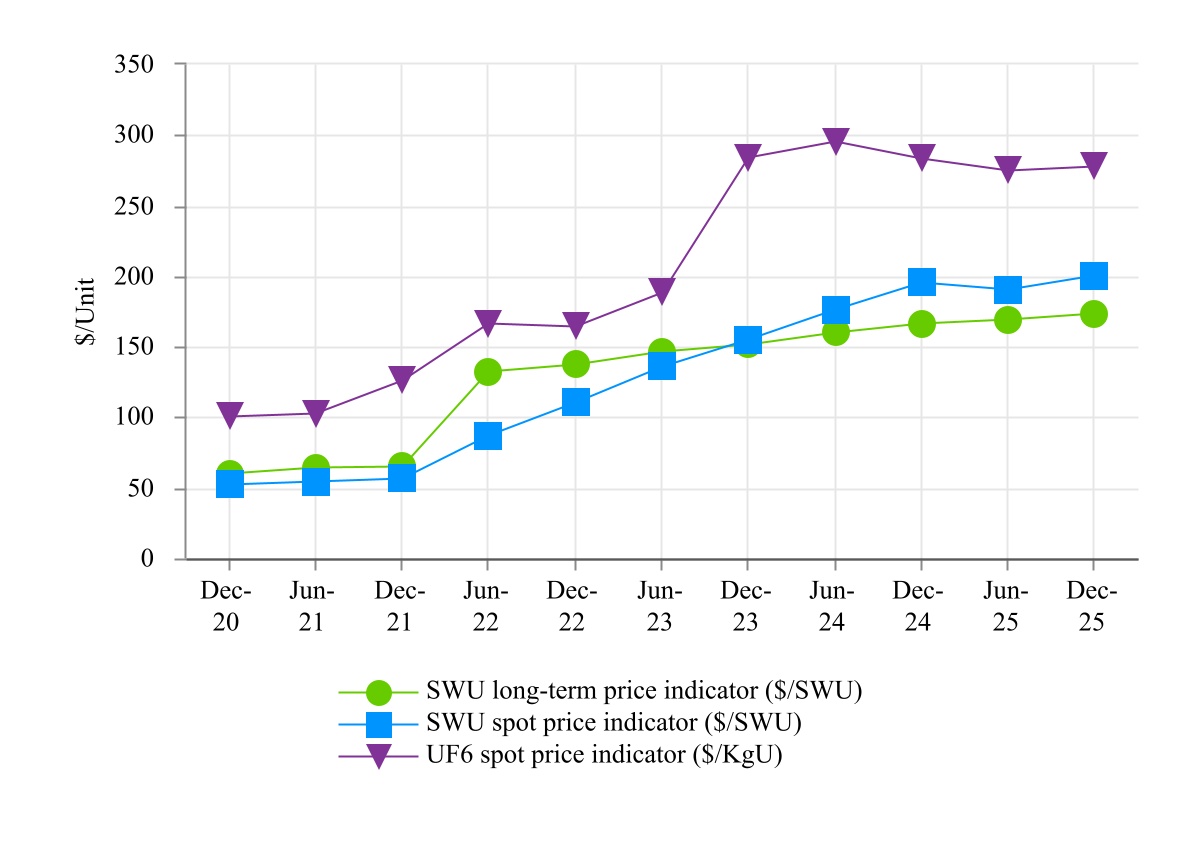

Market prices for SWU fell substantially in the aftermath of the nuclear incident at Fukushima, Japan in 2011, bottoming out in 2018. Since 2018, SWU prices have steadily increased and, following the Russian invasion of Ukraine, have increased to levels consistent with those prior to the 2011 Fukushima incident. Centrus’ purchase prices under the TENEX Supply Contract were adjusted to reflect the lower market prices that prevailed in 2018, based on a one-time market related price reset. The 2018 price reset reduced the cost for our purchases from 2019 through 2028. Similarly, Centrus’ SWU purchases under our long-term contract with Orano reflect the lower market prices that prevailed in 2018, when Centrus signed the long-term contract with Orano.

Technical Solutions

Our Technical Solutions segment reflects our technical, manufacturing, engineering, and operations services offered to public and private sector customers, including the American Centrifuge engineering, procurement, construction, manufacturing, and operations services being performed under the HALEU Operation Contract. Subject to the availability of sufficient funding and offtake commitments, our goal is to expand our uranium enrichment capacity to meet the full range of U.S. government and commercial requirements for enriched uranium. With our government and private sector customers, we seek to leverage our domestic enrichment experience, as well as our engineering know-how and precision manufacturing facility to assist customers with a range of engineering, design and advanced manufacturing projects, including the production of fuel-related components for next-generation nuclear reactors and the development of related facilities. We continue to invest in advanced technology because of the potential for future growth into new areas of business for the Company, while also preserving our unique workforce at our Technology and Manufacturing Center in Oak Ridge, Tennessee, and our production facility near Piketon, Ohio. Refer to Part II, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, for additional information.

Government Contracting

The Company’s work on HALEU began under the HALEU Demonstration Contract, executed with the DOE in 2019, to construct a cascade of 16 AC100M centrifuges in Piketon, Ohio to demonstrate HALEU production. The DOE has funded the HALEU Demonstration Contract up to $173.0 million with a period of performance that ended November 30, 2022.

On November 10, 2022, the DOE awarded the HALEU Operation Contract to the Company with a base contract value of approximately $150.0 million in two phases through 2024. Phase 1 included an approximately $30.0 million cost-share contribution from Centrus matched by approximately $30.0 million from the DOE to complete construction of the cascade, begin operations and produce the initial 20 kilograms of HALEU UF6. On November 7, 2023, the Company made its first contractual delivery of HALEU to the DOE, completing Phase 1 of the contract.

During November 2023, the Company transitioned to Phase 2 of the HALEU Operation Contract, which included production of 900 kilograms of HALEU UF6 for one production year, as well as continued operations and maintenance of the cascade. Phase 2 included an initial contract value of approximately $90.0 million and compensation on a cost-plus-incentive-fee-basis. The DOE owns the HALEU produced from the demonstration cascade. On November 5, 2024, the HALEU Operation Contract was modified to extend the Phase 2 period of performance to June 30, 2025, which allowed the Company to produce and contractually deliver the Phase 2 production target of 900 kilograms of HALEU UF6 to DOE. The DOE further extended the Phase 2 period of performance through January 31, 2026, to allow the Company to complete outstanding change orders. As of December 31, 2025, the total Phase 2 contract value and funded value is $170.1 million. The fee for the Phase 2 period of performance that was extended beyond November 30, 2024 was not definitized and is subject to negotiation. Pursuant to an amendment to the Piketon facility lease, the DOE assumed all D&D liabilities arising out of the HALEU Operation Contract.

16

The HALEU Operation Contract also gives DOE the ability to exercise three optional periods to contract for up to nine additional years of production from the cascade beyond the base contract; those options are at the DOE’s sole discretion and subject to the availability of Congressional appropriations. On June 17, 2025, the DOE issued an amendment to the HALEU Operation Contract that divided the first three-year option period into a first option period of one year (“Option 1a”) and a second option period of two years (“Option 1b”). The amendment established a target cost and fee for Option 1a of approximately $99.3 million and $8.7 million, respectively, and a target cost and fee for Option 1b of $163.5 million and $15.2 million, respectively. The DOE exercised Option 1a and extended the period of performance to June 30, 2026. As of December 31, 2025, Option 1a is funded for the contract value of $108.2 million. Additionally, the Amendment acknowledges that the estimated cost associated with Option 1b is insufficient to support full performance due to known cost increases since award of the HALEU Operation Contract and indicates that the Company will need to submit a revised cost proposal for review and negotiation prior to DOE’s consideration of Option 1b.

Under the HALEU Operation Contract, the DOE is contractually required to provide the 5B Cylinders necessary to collect the output of the cascade, but supply chain challenges created difficulties for the DOE in securing enough 5B Cylinders for the entire Phase 2 production year. During time periods when 5B Cylinders were insufficient, the Company was not able to produce HALEU as it did not have 5B Cylinders to store the enriched uranium. Due to these delays, Centrus was unable to achieve contractual delivery of the 900 kilograms of HALEU UF6 by November 2024, which was the date set for the end of Phase 2 performance. As indicated above, on November 5, 2024, the HALEU Operation Contract was modified to extend the Phase 2 period of performance to June 30, 2025, which allowed the Company to produce and contractually deliver the Phase 2 production target of 900 kilograms of HALEU UF6 to DOE.

Under the HALEU Operation Contract, the Company has submitted several change order requests for work being performed on infrastructure, facility repairs, and 5B Cylinders. The additional work is being performed under the DOE Contracting Officer’s approval or contract modifications. On September 28, 2023, the DOE modified the HALEU Operation Contract to incorporate additional scope for infrastructure and facility repairs, and costs associated with 5B Cylinder refurbishment, for an estimated additional contract value of $5.8 million, without a cost-share provision. As of December 31, 2025, DOE was obligated for costs up to the contract value of $8.8 million for the additional scope work. The DOE modified the HALEU Operation Contract and increased funding in January 2026 and is now obligated for costs up to the current contract value of $9.7 million.

Centrus believes it is well positioned to compete for any follow-on contract(s) to expand HALEU production capability at the Piketon site. As discussed above, on October 4, 2024 and October 16, 2024, the DOE selected ACO and other awardees under competitive solicitations aimed at HALEU deconversion and expanding domestic commercial production of HALEU, respectively. On December 10, 2024, DOE selected ACO and other awardees under a competitive solicitation aimed at expanding domestic commercial production of LEU. On January 5, 2026, the DOE announced that ACO was selected for award of a $900.0 million task order under the HALEU Production Contract to expand its uranium enrichment facility in Piketon, Ohio, to include commercial-scale production of HALEU. The task order is subject to negotiation of a definitive agreement and there are no guarantees about whether or when funding by the DOE for such expansion would be awarded. The ultimate dollar amount under each contract and the potential scale of the expansion supported will depend upon the scope of any further task orders that DOE may subsequently issue under the contracts for which we will compete. There is no assurance that we will be awarded any additional task orders under any of our contracts and, if awarded, the nature, timing and amount of the task orders that may be issued under an award is uncertain.

For further details, refer to Part II, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations - Market Conditions and Outlook.

17

Technical Solutions Backlog

Our backlog in the Technical Solutions segment extends to 2034. As of both December 31, 2025 and 2024, our backlog was approximately $0.9 billion. Our backlog includes both funded amounts (services for which funding has been both authorized and appropriated by the customer), unfunded amounts (services for which funding has not been appropriated), and unexercised options in our contracts. If any of our contracts were to be terminated or options not being exercised by DOE, our remaining backlog would be reduced by the expected value of the cancelled contracts or forgone options.

Competition and Foreign Trade

It is estimated that the enrichment industry market for commercial nuclear reactors powered by LEU is currently about 50 million SWU per year. Our global market share of enrichment for the LEU market is less than 5%. Global LEU suppliers in our highly competitive industry compete on the basis of price and reliability of supply. The four largest LEU suppliers comprising over 95% of market share combined are as follows:

•Rosatom, a Russian government entity, which sells LEU through its wholly-owned subsidiary TENEX;

•Urenco, a consortium of companies owned or controlled by the British and Dutch governments and two German utilities;

•CNEIC, a company owned by the Chinese government; and

•Orano, a company largely owned by the French government, and formerly part of the French government.

According to the WNA, as of 2025, the production capacity for the major LEU suppliers is as follows:

•Rosatom/TENEX was approximately 27 million SWU per year. Imports of LEU and other uranium products produced in the Russian Federation are subject to restrictions as described below under — Russian Suspension Agreement and Ukraine War;

•Urenco has reported installed capacity at its European and U.S. enrichment facilities of approximately 17 million SWU per year;

•CNEIC has emerged as a significant producer primarily focused on supplying domestic requirements in China. CNEIC’s commercial SWU production capacity was approximately 11 million SWU per year; and

•Orano’s gas centrifuge enrichment plant in France began commercial operations in 2011 and the plant has SWU production capacity of approximately 8 million SWU per year.

All of our current competitors are owned or controlled, in whole or in part, by foreign governments, and operate enrichment technologies developed with the financial support of foreign governments. These competitors may make business decisions in both domestic and international markets that are influenced by political or economic policy considerations rather than exclusively by commercial considerations.

LEU also may be produced by down-blending government stockpiles of highly-enriched uranium. Governments control the timing and availability of highly-enriched uranium released for this purpose, and the release of this material to the market could impact market conditions. Any additional LEU released into the market from down-blended highly-enriched uranium could exert downward pressure on prices for LEU. However, without Russian supply, the global market would be undersupplied for uranium enrichment.

Our LEU supply to foreign customers is exported under the terms of international agreements governing nuclear cooperation between the United States and the government of the country of destination or other entities, such as the EU or the International Atomic Energy Agency. The LEU supplied to us is subject to the terms of cooperation agreements between the country in which the material is produced and the country of destination or other entities.

18

Russian Suspension Agreement

Imports into the United States of LEU and other uranium products produced in the Russian Federation, including LEU imported by Centrus under the TENEX Supply Contract, are subject, through December 31, 2040, to quotas imposed under U.S. legislation enacted into law in September 2008 and December 2020, and under the RSA, as amended in 2008 and 2020. These quotas limit the amount of Russian LEU that can be imported into the United States for U.S. consumption1.

The RSA is a trade agreement between the DOC and Rosatom originally signed in 1992 that suspended an anti-dumping duty investigation of Russian uranium and imposed quantitative limits on exports of Russian uranium products, including LEU, to the United States. Under an amendment signed on October 5, 2020, the RSA’s limits on shipments of Russian uranium product to the United States were extended through at least 2040. Additionally, under legislation passed by the U.S. Congress shortly after the amendment was signed, the material terms of the extended RSA were enacted into law.

Under this law and the RSA, import quotas for Russian uranium products peaked in 2023 at an amount equivalent to 24% of the forecasted U.S. demand for enrichment and then began to decline, reaching a quota amount equivalent to 15% by 2028. Despite the fact that overall limits will ramp down, the RSA, as amended in 2020, explicitly sets aside sufficient quota in 2021 through 2028 for Centrus. The RSA and the legislation provide for a revision of the quotas in 2023, 2029, and 2035 to take account of SWU demand forecasts that will be published by the WNA in the future. Accordingly, in November 2023, the DOC calculated a small increase in the quota through 2024. The adjustment does not affect the quota allocated to Centrus. Any quota adjustment or other change to the RSA that reduces our quota allocations could affect our ability to implement the TENEX Supply Contract through sales to customers who take delivery in the United States, which is our most significant market.

The actual size of the annual quotas allocated to Centrus for the TENEX Supply Contract are confidential, but a public version of the quotas shows that they represent a significant portion of the total quotas provided under the RSA in 2021 through 2028. The quotas provided for the TENEX Supply Contract are expected to be adequate to support the Company’s long-term strategic goals and to permit enriched uranium procured from TENEX during the remaining term of the TENEX Supply Contract to be imported to supply U.S. utilities subject to potential supply chain disruptions as a result of the Import Ban Act, the Russian Decree and other impacting restrictions.

For further details, refer to Part I, Item 1A, Risk Factors - Restrictions on imports or sales of SWU or uranium that we buy from our Russian supplier and our other sources of supply could adversely affect profitability and the viability of our business.

1 The term “quota” is used herein for simplicity. The amounts of Russian uranium products that can be shipped to the United States are referred to as export limits in the RSA and import limits in the legislation, but from a practical perspective the terms have identical effect.

19

Ukraine War

The war in Ukraine escalated tensions between Russia and the international community. As a result, the United States and other countries imposed, including through the United States’ enactment of the Import Ban Act discussed below, and may continue imposing, additional sanctions, tariffs, and export controls against certain Russian products, services, organizations and/or individuals, and Russia passed the Russian Decree as discussed below. Such additional restrictions, and any Russian response thereto, could affect our ability to purchase, take delivery of, transport, or re-sell Russian uranium enrichment, engage in transactions with TENEX, or implement the TENEX Supply Contract, which would have a negative material impact on our business. Further, tariffs, sanctions or other restrictions by the United States, Russia or other countries may impact our ability and the cost to transport, export, import, deliver, take delivery, or make payments related to the LEU we purchase and may require us to increase purchases from non-Russian sources to the extent available. For example, due to restrictions imposed by Canada on the ability of Canadian persons and entities to provide ocean transportation services to Russia, a permit is required for our shipper, a Canadian company, to transport the LEU that we procure under the TENEX Supply Contract to the United States. A Canadian permit issued to our shipper was extended to March 2027, but for so long as the sanctions remain in place, the shipper will require further extensions beyond the current validity of the permit for continued shipments of LEU imports.

In response to the war in Ukraine, on May 13, 2024, the U.S enacted the Import Ban Act which banned imports of LEU from Russia into the U.S. beginning August 11, 2024, subject to issuance of waivers by the DOE. In accordance with the instructions published by the DOE, in 2024, the Company filed waiver request applications with the DOE and has received waivers allowing importation of LEU from Russia for deliveries already committed by the Company to its (i) U.S. customers in years 2024 through 2027 (ii) foreign customers for processing and reexport. On December 11, 2024, the Company filed a third waiver request application to allow for importation of LEU from Russia in 2026 and 2027 for use in future sales to our U.S. customers. The U.S. ban on imports of Russian LEU, without the grant of additional timely waivers, would have a negative material impact on our business. Through 2027, well over one-half of the LEU that we expect to deliver to customers was sourced under the TENEX Supply Contract. While we have other sources of supply, they are not sufficient to replace the TENEX supply. It is uncertain whether any waiver would be granted in response to our pending or any potential future applications and, if granted, whether any waiver would be granted in a timely manner for us to benefit from it.

On November 14, 2024 the government of the Russian Federation passed the Russian Decree, effective through December 31, 2027, that rescinded TENEX’s general license to export LEU to the United States, including to us under the TENEX Supply Contract or to entities registered in the United States. TENEX, is required to obtain a specific export license from the Russian authorities for each shipment to Centrus through 2027. Except for isolated delays, TENEX has received specific licenses to satisfy shipments to Centrus in the regular course of business. However, Centrus has been informed that there is no certainty whether additional licenses will be issued by the Russian authorities and if issued, whether they will be issued in a timely manner or rescinded prior to the shipment taking place. Through 2027, well over one-half of the LEU that we expect to deliver to customers was sourced under the TENEX Supply Contract. While we have other sources of supply, they are not sufficient to replace the TENEX supply. Refer to Item 1A, Risk Factors - Economic and Industry Risks - Dependence on our largest customers or suppliers could adversely affect us, for further discussion.

In addition to limitations targeted specifically at imports of LEU into the U.S. or export of LEU out of Russia, the evolving sanctions or restrictions imposed by the United States and foreign governments on the mechanisms used to make payments to Russia and to obtain services, including transportation, have increased the risk that implementation of the TENEX Supply Contract may be disrupted frequently. If the U.S. government were to prohibit companies and individuals from engaging in transactions with Rosatom and its subsidiaries, including TENEX, the Company and its suppliers could not implement the TENEX Supply Contract absent a license or other authorization from the sanctioning government.

20

Given all of the foregoing, we continue to monitor the situation closely and assess the potential impact of any new sanctions and how the impact on the Company might be mitigated. For further details, refer to Part I, Item 1A, Risk Factors - The current war in Ukraine and related international or U.S. sanctions, tariffs and restrictions on trade, and the Russian response thereto, could have a material adverse impact on our business, results of operations, and financial condition.

Other Actions Adversely Affecting International Trade

In 2018, in connection with the withdrawal by the United States from a 2015 multilateral agreement known as the Joint Comprehensive Plan of Action, the U.S. government re-imposed sanctions on the Atomic Energy Organization of Iran and a number of its subsidiaries. Waivers were granted to allow non-Iranian entities to continue to work on certain programs that, among other things, allowed affiliates of Rosatom to continue work on nuclear projects in Iran. These waivers have expired or been terminated and, as a result, the U.S. government could decide to impose sanctions on Russian entities that may be involved in nuclear work in Iran, including Rosatom or its subsidiaries. These sanctions could affect companies owned by Rosatom, including TENEX, even if they are not doing work in Iran. To date, no sanctions have been imposed or announced on TENEX or any other Rosatom subsidiary involved in the TENEX Supply Contract, with respect to the work of Rosatom or its subsidiaries in Iran. For further details, refer to Part I, Item 1A, Risk Factors - Tariffs and other changes in international trade policy could adversely affect our business, financial condition and results of operations.

DOE Facilities

We produced LEU through 2001 at the former Portsmouth GDP in Piketon, Ohio and through 2013 at the former Paducah GDP in Paducah, Kentucky, both of which facilities we had leased from the DOE. The Portsmouth GDP and Paducah GDP were operated by agencies of the U.S. government for more than 40 years prior to the creation of the Company through privatization of the government enterprise in 1998. As a result of such operation, there are contamination and other potential environmental liabilities associated with the U.S. government’s prior operation of the plants. The USEC Privatization Act and the terms of our leases of the plants provide that DOE remains responsible for the D&D of the gaseous diffusion plants. Further, the DOE continued operations as well as cleanup activities, both during and subsequent to our operations at the facilities.

We lease facilities and related personal property near Piketon from the DOE. In connection with a letter agreement that preceded the HALEU Demonstration Contract, the DOE and Centrus amended the lease agreement, which initially was scheduled to expire by its terms on June 30, 2019, but was extended through December 31, 2025. On November 30, 2022 the lease was further amended to ensure all D&D liabilities created under the HALEU Operation Contract reside with the DOE. With the DOE exercise of Option 1a of Phase 3 of the HALEU Operation Contract, the lease was further extended to June 30, 2027. DOE may exercise further options to extend the term of the HALEU Operation Contract, in which case the expiration of the lease shall extend to one calendar year beyond the last day of the HALEU Operation Contract period. Any facilities or equipment constructed or installed will be owned by the DOE and may be returned to the DOE in an “as is” condition at the end of the lease term. The DOE will be responsible for the D&D of any returned facilities or equipment. If we determine the equipment and facilities may benefit Centrus after completion of the HALEU program, we can seek to extend the facility lease, subject to mutual agreement regarding D&D and other terms.

Human Capital Management

Our employees in Maryland, Ohio, and Tennessee are dedicated to our corporate philosophy based on honesty, trust, and the highest levels of integrity, safety, and security. Every day these values drive how we operate our business; govern how we interact with each other and our customers, partners, and suppliers; guide the way that we treat our workforce; and determine how we connect with our communities. Our commitment to ethical business practices is outlined in our COBC. Each employee is required to acknowledge receipt, understanding of, and compliance with our standards.

21

Due to the highly specialized nature of our business we need to hire and train skilled and qualified personnel to design, build, operate our state-of-the-art equipment, and to provide a broad range of services to support our country and our customers. Our work requires that we attract individuals who are dedicated to consistently performing quality work and for many of our positions, can obtain a security clearance. We recognize that our success as a company depends on our ability to attract, develop, and retain such a workforce. We are dedicated to promoting the health, welfare, and safety of our employees. Part of our responsibility includes treating all employees with dignity, respect and providing them with fair, competitive, market-based, and equitable compensation. We recognize and reward the performance of our employees in line with our pay-for-performance philosophy and provide a comprehensive suite of benefit options that are designed to enable our employees and their dependents to live healthy and productive lives.

Workplace safety is our top priority. We strive to proactively address potential hazards, promote safe practices, and foster a culture of continuous improvement to prevent incidents and injuries while ensuring compliance with health and safety laws and regulations.

We are committed to building a workforce that reflects a wide range of experience and viewpoints in thought, experience, perspectives, backgrounds, and capabilities, recognizing that our differences drive innovation and strengthen the solutions we deliver to our customers. To this end, we cultivate an inclusive environment that respects diverse opinions, values individual talents, and celebrates the unique contributions of each of our employees. We partner with a Human Resource Consulting firm to assist us in hiring. These efforts underscore our dedication to opportunity, and the principles of inclusive excellence.

Our core values inspire us to foster a workplace culture that values professional growth, skill development and leadership excellence. We are committed to providing opportunities for training and development to empower our workforce with job skills needed to excel in their roles.

Additionally, we emphasize cultivating leadership attributes that align with our organizational philosophy, to assist our employees in not only succeeding individually but also contributing to the broader success of our teams and business. Through these efforts, we aim to create a dynamic and knowledgeable workforce capable of diving innovation and achieving sustainable success.

A summary of our employees by location is as follows:

No. of Employees

at December 31,

Location

2025

2024

Piketon, OH

250

153

Oak Ridge, TN

165

116

Bethesda, MD

52

53

Total Employees

467

322

In May 2024, the Company and the United Steelworkers Local 689-5 union agreed to extend their collective bargaining agreement to October 2026. In September 2025, the Company entered into a collective bargaining agreement with the International Union, Security, Police, and Fire Professionals of America, which extends until 2030.

22

Information about our Executive Officers

Executive officers are elected by and serve at the discretion of the Board of Directors. Our executive officers as of February 11, 2026, are as follows:

Name

Age

Position

Amir V. Vexler

53

President and Chief Executive Officer

Todd M. Tinelli

45

Senior Vice President, Chief Financial Officer, and Treasurer

Richard D. Emery

53

Senior Vice President, General Counsel, Chief Compliance Officer and Corporate Secretary

Patrick S. Brown

46

Senior Vice President, Field Operations

John M.A. Donelson

61

Senior Vice President and Chief Marketing Officer

Neal K. Nagarajan

40

Senior Vice President, Head of Investor Relations

Amir V. Vexler joined Centrus on December 4, 2023, as a Special Advisor to the Board. On January 1, 2024, Mr. Vexler assumed the role of President and Chief Executive Officer. Mr. Vexler has extensive experience in the nuclear fuel industry and a strong background in manufacturing, engineering services, commercial operations, and business development. Prior to joining the Company, he served as President and Chief Executive Officer of Orano USA, overseeing sales of nuclear fuel, decommissioning services, used nuclear fuel management, and medical isotopes as well as engineering and technology services for the federal government. Previously, Mr. Vexler spent 20 years at General Electric Company, where he served in a number of leadership positions, including Chief Executive Officer, Chairman of the Board, and Chief Operating Officer of Global Nuclear Fuel, a joint venture of General Electric Company and Hitachi.