| Management Report 2025 Gerdau S.A. Videoconference February 24 (Tuesday) 12:00 p.m. BRT 11:00 a.m. NY Click here to access the videoconference RI.GERDAU.COM RI.GERDAU.COM |

| Management Report 2025 | Gerdau S.A. 2 MESSAGE FROM MANAGEMENT We ended 2025 with results that reaffirm the resilience of our operations and the relevance of our global presence. People's safety remains our non-negotiable value and top priority, guiding decisions and reinforcing a culture built on our employees’ care and well-being. The global steel scenario in 2025 remained challenging, marked by heightened competition and persistent production overcapacity in various regions. In Brazil, the market remains impacted by the rising steel imports under unfair conditions, hitting a record level of 6 million tonnes and putting pressure on operations’ profitability in the domestic market. Conversely in the United States, the adjustments of Section 232 tariffs contributed to rebalancing supply and demand, boosting the performance of our operations in the region. Despite the challenges posed by this complex environment, our ability to adapt and our financial discipline have provided us with a key competitive advantage, while geographic diversification remained a strategic pillar for delivering consistent results. We ended 2025 with Net sales of R$69.9 billion, Adjusted EBITDA of R$10.1 billion, and Adjusted Net Income of R$3.4 billion. North America North America operations stood out in the Company's results, reflecting a more favorable business environment with results benefiting from a consistent decline in imports, which contributed to rebalancing local supply, boosting shipment volume and higher prices in the domestic market. With high asset capacity utilization, a competitive cost structure, and strategic investments underway, North America ended 2025 with its highest-ever share of consolidated EBITDA (62%), reinforcing its pivotal role in the Company's strategy and value creation. Brazil In Brazil, we faced another year of fierce competition in the domestic market, due to the rising and unfair level of steel imports, which still put pressure on prices, shipment volumes, and our operations’ profitability throughout the year. In spite of this scenario, we bolstered our position in the domestic market, enhanced operational efficiency, and continued to seek to defend a market with fair conditions for the industry by improving trade defense mechanisms. We also advanced our strategic projects, such as the new hot-rolled coil mill in Ouro Branco, enhancing our portfolio with higher value-added products and accelerating the physical progress of the Miguel Burnier Sustainable Mining platform. South America In South America, 2025 was marked by a gradual recovery in steel shipment volumes. However, throughout the year, demand for steel remained weak in the region, coupled with a market also constrained by rising steel imports and ongoing price pressure, negatively impacting our operating results. Financial results Throughout 2025, we maintained a solid capital structure, with healthy leverage levels and adequate financial flexibility to sustain the continuity of our strategic projects and generate returns for our shareholders. We invested R$6.1 billion in CAPEX, advancing relevant initiatives such as the completion of the new hot-rolled coil line in Ouro Branco (MG), investments in renewable energy self-generation, and the expansion of the Midlothian (TX) industrial unit, bolstering the competitiveness of our North America’s main asset. We also moved forward with the physical progress of the Miguel Burnier Sustainable Mining platform – which reached 91% in 4Q25 – and which will add 5.5 million tonnes/year of iron ore capacity. For 2026, we estimate R$4.7 billion in CAPEX, with a focus on our assets’ maintenance and competitiveness, ensuring the disciplined execution of key projects. In 2025, we distributed roughly R$1.2 billion in dividends. We also completed the 2025 Share Buyback Program, acquiring 64.5 million shares, equivalent to 3.0% of outstanding shares. In addition to a robust investment cycle, capital allocation discipline in 2025 considered a total of R$2.4 billion in shareholder remuneration, including dividends and share buybacks, or a payout of 182%. Keeping this commitment to return value to our shareholders, on February 23, 2026, the Company's Board of Directors approved a new share buyback program of up to 55 million preferred shares, and up to 1.4 million common shares, equivalent to 2,9% of outstanding shares (GGBR and/or GGB), with a 18-month term. With 125 years of history completed in January 2026, we remain firmly committed to enhancing the Company's competitiveness, swiftly adapting to market changes, and generating a positive impact in the regions where we operate. Once again, we would like to thank our employees, customers, suppliers, partners, shareholders, and other stakeholders for their trust and support in building our history and continuously creating value. THE MANAGEMENT |

| Management Report 2025 | Gerdau S.A. 3 WHO WE ARE LARGEST BRAZILIAN STEEL PRODUCER With 125 years of history, Gerdau is Brazil’s largest producer of steel, and a leading supplier of long and special steel globally. In Brazil, Gerdau also produces flat steel and iron ore. Dedicated to empowering individuals who shape the future, the Company is a benchmark for internationalization in the Brazilian industrial sector. It is present in several countries in the Americas and relies on 30,000 employees across all its operations. Gerdau has 29 steel production units, including 13 industrial units in North America. Recognized as the largest recycler in Latin America, Gerdau utilizes scrap as a significant raw material, with nearly 70% of its steel production derived from scrap. Annually, it transforms 10 million tonnes of scrap into a diverse range of steel products. As a result of its sustainable production matrix, Gerdau currently has one of the lowest average greenhouse gas (CO₂e) emissions, accounting for half the global average for the sector. Gerdau shares are listed on the São Paulo (B3) and New York (NYSE) stock exchanges. For more information, visit the Investor Relations website: https://ri.gerdau.com/ |

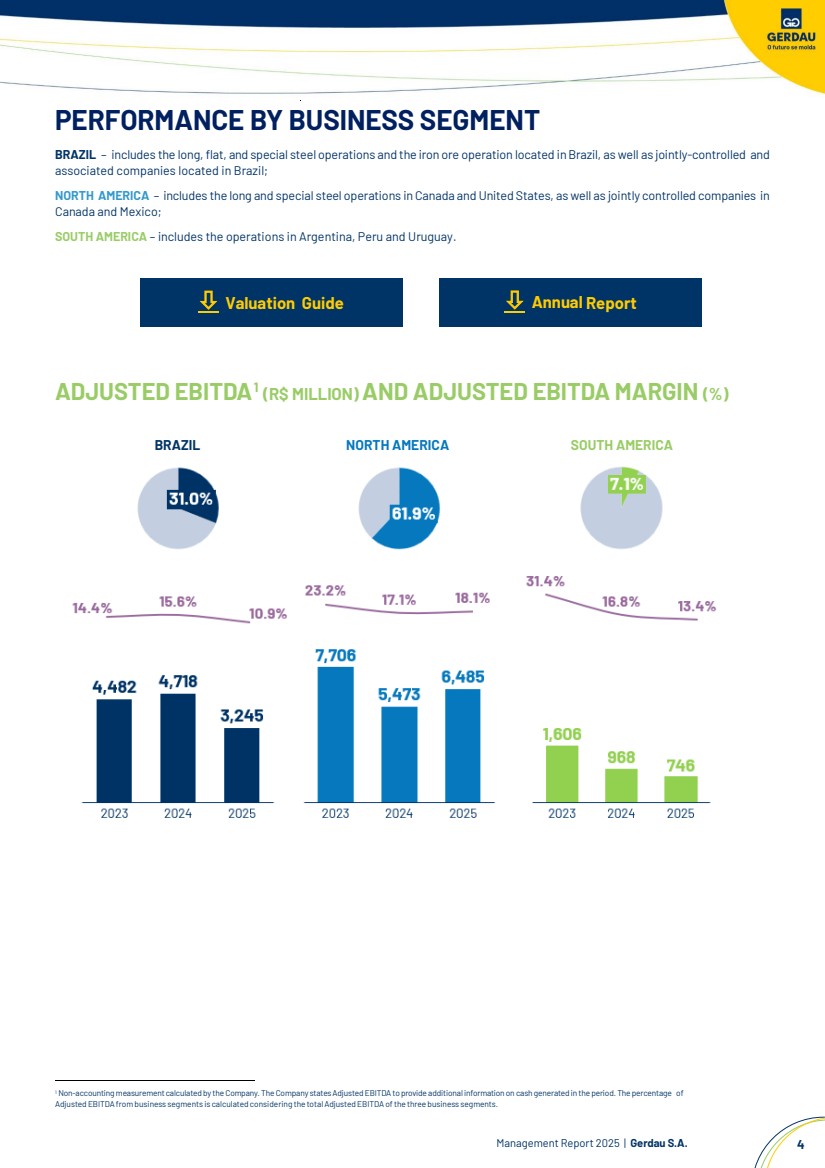

| Management Report 2025 | Gerdau S.A. 4 PERFORMANCE BY BUSINESS SEGMENT BRAZIL – includes the long,flat, and special steel operations and the iron ore operation located inBrazil, as well as jointly-controlled and associated companies located in Brazil; NORTH AMERICA – includes the long and special steel operations in Canada and United States, as well as jointly controlled companies in Canada and Mexico; SOUTH AMERICA – includes the operations in Argentina, Peru and Uruguay. Valuation Guide ADJUSTED EBITDA3F0F 1 (R$ MILLION) AND ADJUSTED EBITDA MARGIN (%) BRAZIL NORTH AMERICA SOUTH AMERICA 1 Non-accounting measurement calculatedby the Company. TheCompany statesAdjusted EBITDA toprovide additional information on cash generatedin the period. The percentage of AdjustedEBITDAfrombusiness segments is calculated considering the totalAdjustedEBITDAofthe three business segments. Annual Report |

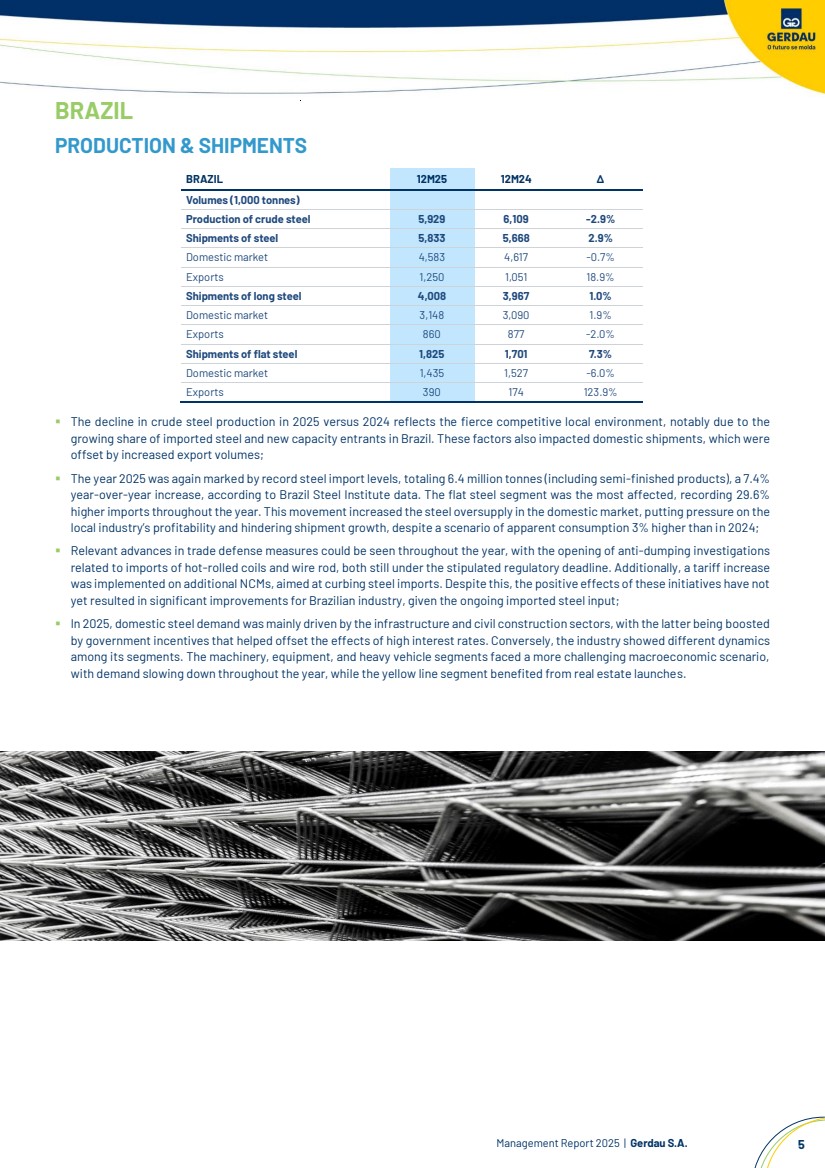

| Management Report 2025 | Gerdau S.A. 5 BRAZIL PRODUCTION & SHIPMENTS ▪ The decline in crude steel production in 2025 versus 2024 reflects the fierce competitive local environment, notably due to the growing share of imported steel and new capacity entrants in Brazil. These factors also impacted domestic shipments, which were offset by increased export volumes; ▪ The year 2025 was again marked by record steel import levels, totaling 6.4 million tonnes (including semi-finished products), a 7.4% year-over-year increase, according to Brazil Steel Institute data. The flat steel segment was the most affected, recording 29.6% higher imports throughout the year. This movement increased the steel oversupply in the domestic market, putting pressure on the local industry’s profitability and hindering shipment growth, despite a scenario of apparent consumption 3% higher than in 2024; ▪ Relevant advances in trade defense measures could be seen throughout the year, with the opening of anti-dumping investigations related to imports of hot-rolled coils and wire rod, both still under the stipulated regulatory deadline. Additionally, a tariff increase was implemented on additional NCMs, aimed at curbing steel imports. Despite this, the positive effects of these initiatives have not yet resulted in significant improvements for Brazilian industry, given the ongoing imported steel input; ▪ In 2025, domestic steel demand was mainly driven by the infrastructure and civil construction sectors, with the latter being boosted by government incentives that helped offset the effects of high interest rates. Conversely, the industry showed different dynamics among its segments. The machinery, equipment, and heavy vehicle segments faced a more challenging macroeconomic scenario, with demand slowing down throughout the year, while the yellow line segment benefited from real estate launches. BRAZIL 12M25 12M24 ∆ Volumes (1,000 tonnes) Production of crude steel 5,929 6,109 -2.9% Shipments of steel 5,833 5,668 2.9% Domestic market 4,583 4,617 -0.7% Exports 1,250 1,051 18.9% Shipments of long steel 4,008 3,967 1.0% Domestic market 3,148 3,090 1.9% Exports 860 877 -2.0% Shipments of flat steel 1,825 1,701 7.3% Domestic market 1,435 1,527 -6.0% Exports 390 174 123.9% |

| Management Report 2025 | Gerdau S.A. 6 OPERATING RESULT 1- Includes iron ore and co-products sales. 2- Non-accounting measurement reconciled with information stated in the Note 27 to the Company’s Financial Statements, as set forth by CVM Resolution No. 156 of June 23, 2022. ▪ In 2025, Net sales went down 1.8% from 2024, due to a fierce competitive environment in the domestic market, marked by rising steel imports and the entry of new capacity players, which pressured prices in the common long and flat steel segments throughout the year. Despite shipment volume growth, the greater share of exports in the mix also contributed to the decline in Net sales in the period; ▪ The cost of goods sold came 5.7% higher in 2025 versus 2024, driven by increased shipment volume and, mainly, by scheduled shutdowns and structural and operational adjustments necessary throughout the year to implement improvements and prepare for new investments at the Ouro Branco industrial unit. These factors temporarily raised fixed costs, raw materials, and maintenance. However, during the second half of the year, the industrial unit then recorded greater operational stability. In addition, the higher occupancy rate of mini mills contributed to cost dilution and efficiency gains, partially mitigating the effects seen earlier in the year. It is worth noting that, in 2024, costs of goods sold benefited from optimization initiatives and hibernations, which reduced the basis for comparison; ▪ As a result of the operational effects mentioned above, adjusted EBITDA was 31.2% lower than in 2024. BRAZIL 12M25 12M24 ∆ Results (R$ million) Net sales¹ 29,688 30,218 -1.8% Domestic market 24,897 26,396 -5.7% Exports 4,792 3,822 25.4% Cost of goods sold (27,807) (26,319) 5.7% Gross profit 1,881 3,898 -51.7% Gross margin (%) 6.3% 12.9% -6.6 p.p Selling, general and administrative expenses (952) (939) 1.4% Other operating income (expenses) (62) (145) -57.6% Depreciation and amortization 2,144 1,761 21.8% Proportional EBITDA of associated companies and jointly controlled entities 234 143 63.7% Adjusted EBITDA² 3,245 4,718 -31.2% Adjusted EBITDA Margin² (%) 10.9% 15.6% -4.7 p.p |

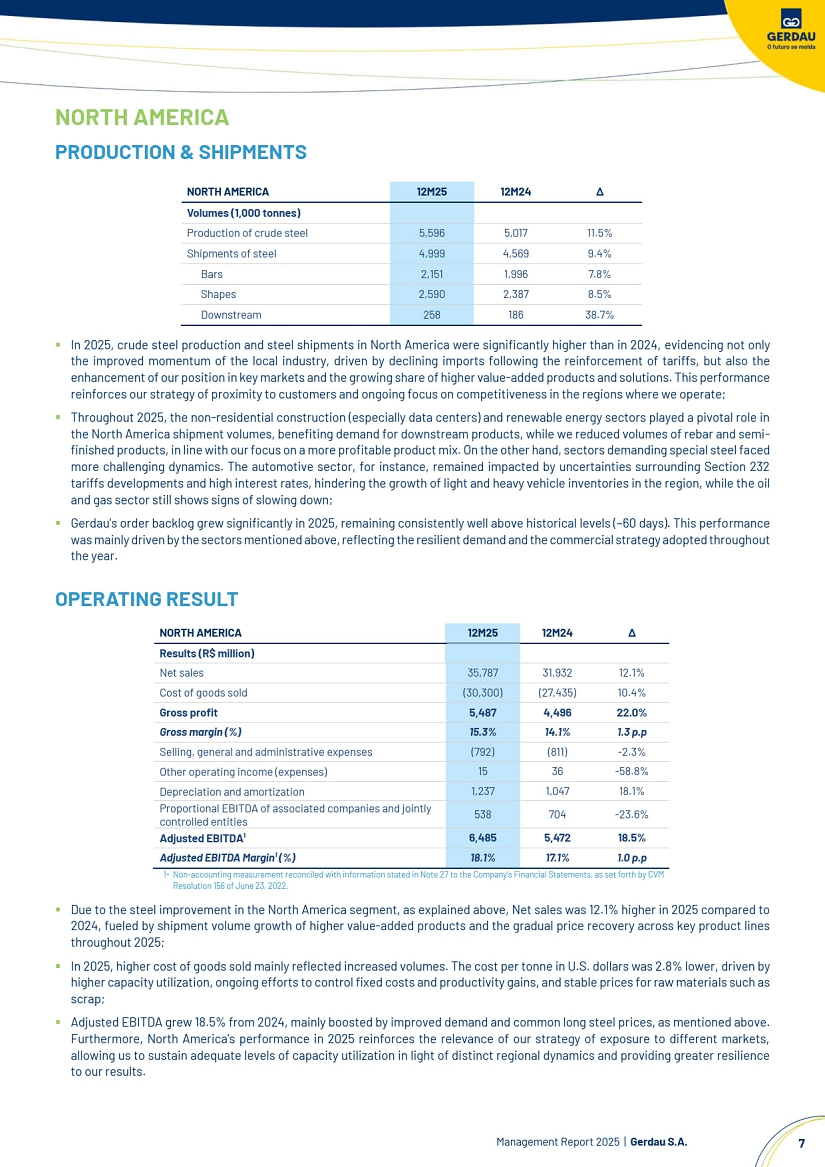

| Management Report 2025 | Gerdau S.A. 7 NORTH AMERICA PRODUCTION & SHIPMENTS ▪ In 2025, crude steel production and steel shipments in North America were significantly higher than in 2024, evidencing not only the improved momentum of the local industry, driven by declining imports following the reinforcement of tariffs, but also the enhancement of our position in key markets and the growing share of higher value-added products and solutions. This performance reinforces our strategy of proximity to customers and ongoing focus on competitiveness in the regions where we operate; ▪ Throughout 2025, the non-residential construction (especially data centers) and renewable energy sectors played a pivotal role in the North America shipment volumes, benefiting demand for downstream products, while we reduced volumes of rebar and semi-finished products, in line with our focus on a more profitable product mix. On the other hand, sectors demanding special steel faced more challenging dynamics. The automotive sector, for instance, remained impacted by uncertainties surrounding Section 232 tariffs developments and high interest rates, hindering the growth of light and heavy vehicle inventories in the region, while the oil and gas sector still shows signs of slowing down; ▪ Gerdau's order backlog grew significantly in 2025, remaining consistently well above historical levels (~60 days). This performance was mainly driven by the sectors mentioned above, reflecting the resilient demand and the commercial strategy adopted throughout the year. OPERATING RESULT 1- Non-accounting measurement reconciled with information stated in Note 27 to the Company’s Financial Statements, as set forth by CVM Resolution 156 of June 23, 2022. ▪ Due to the steel improvement in the North America segment, as explained above, Net sales was 12.1% higher in 2025 compared to 2024, fueled by shipment volume growth of higher value-added products and the gradual price recovery across key product lines throughout 2025; ▪ In 2025, higher cost of goods sold mainly reflected increased volumes. The cost per tonne in U.S. dollars was 2.8% lower, driven by higher capacity utilization, ongoing efforts to control fixed costs and productivity gains, and stable prices for raw materials such as scrap; ▪ Adjusted EBITDA grew 18.5% from 2024, mainly boosted by improved demand and common long steel prices, as mentioned above. Furthermore, North America's performance in 2025 reinforces the relevance of our strategy of exposure to different markets, allowing us to sustain adequate levels of capacity utilization in light of distinct regional dynamics and providing greater resilience to our results. NORTH AMERICA 12M25 12M24 ∆ Volumes (1,000 tonnes) Production of crude steel 5,596 5,017 11.5% Shipments of steel 4,999 4,569 9.4% Bars 2,151 1,996 7.8% Shapes 2,590 2,387 8.5% Downstream 258 186 38.7% NORTH AMERICA 12M25 12M24 ∆ Results (R$ million) Net sales 35,787 31,932 12.1 Cost of goods sold (30,300) (27,435) 10.4% Gross profit 5,487 4,496 22.0% Gross margin (%) 15.3% 14.1% 1.3 p.p Selling, general and administrative expenses (792) (811) -2.3% Other operating income (expenses) 15 36 -58.8% Depreciation and amortization 1,237 1,047 18.1% Proportional EBITDA of associated companies and jointly controlled entities 538 704 -23.6% Adjusted EBITDA¹ 6,485 5,472 18.5% Adjusted EBITDA Margin¹ (%) 18.1% 17.1% 1.0 p.p |

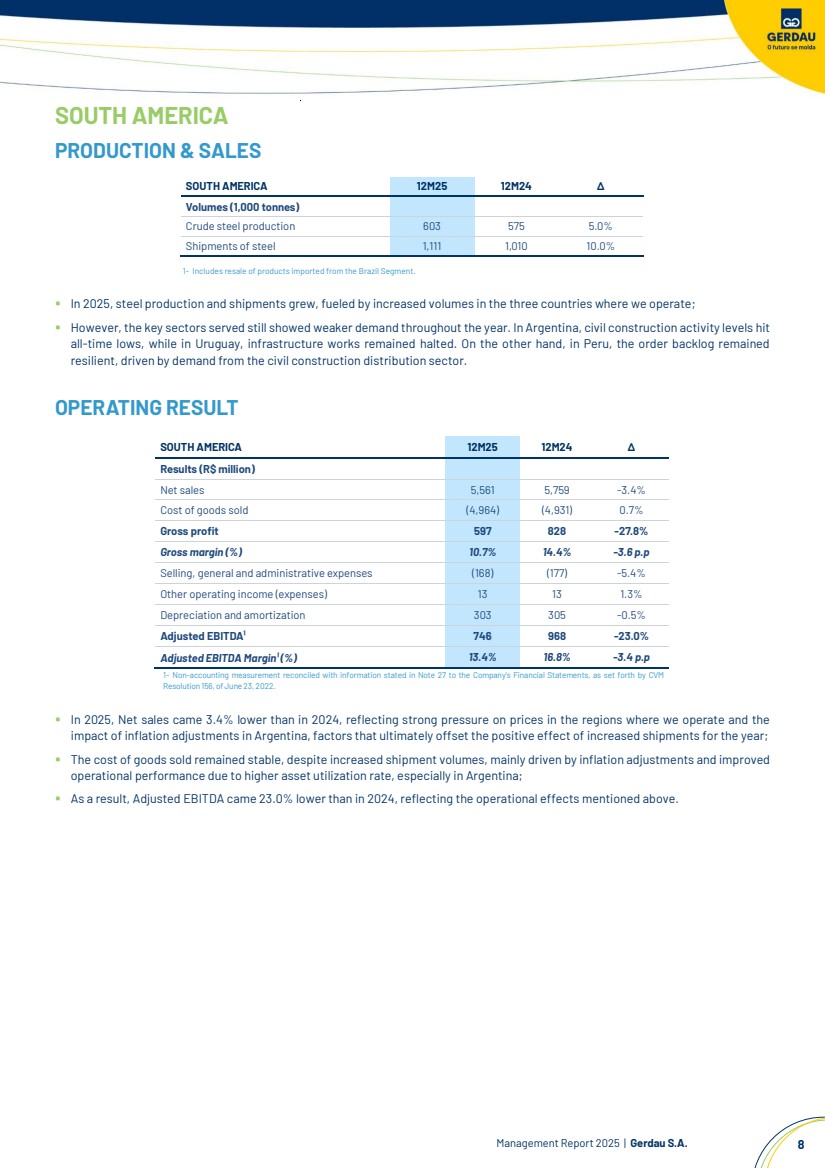

| Management Report 2025 | Gerdau S.A. 8 SOUTH AMERICA PRODUCTION & SALES 1- Includes resale of products imported from the Brazil Segment. ▪ In 2025, steel production and shipments grew, fueled by increased volumes in the three countries where we operate; ▪ However, the key sectors served still showed weaker demand throughout the year. In Argentina, civil construction activity levels hit all-time lows, while in Uruguay, infrastructure works remained halted. On the other hand, in Peru, the order backlog remained resilient, driven by demand from the civil construction distribution sector. OPERATING RESULT 1- Non-accounting measurement reconciled with information stated in Note 27 to the Company’s Financial Statements, as set forth by CVM Resolution 156,ofJune 23, 2022. ▪ In 2025, Net sales came 3.4% lower than in 2024, reflecting strong pressure on prices in the regions where we operate and the impact of inflation adjustments in Argentina, factors that ultimately offset the positive effect of increased shipments for the year; ▪ The cost of goods sold remained stable, despite increased shipment volumes, mainly driven by inflation adjustments and improved operational performance due to higher asset utilization rate, especially in Argentina; ▪ As a result, Adjusted EBITDA came 23.0% lower than in 2024, reflecting the operational effects mentioned above. SOUTH AMERICA 12M25 12M24 ∆ Volumes (1,000 tonnes) Crude steel production 603 575 5.0% Shipments of steel 1,111 1,010 10.0% SOUTH AMERICA 12M25 12M24 ∆ Results (R$ million) Net sales 5,561 5,759 -3.4% Cost of goods sold (4,964) (4,931) 0.7% Gross profit 597 828 -27.8% Gross margin (%) 10.7% 14.4% -3.6 p.p Selling, general and administrative expenses (168) (177) -5.4% Other operating income (expenses) 13 13 1.3% Depreciation and amortization 303 305 -0.5% Adjusted EBITDA¹ 746 968 -23.0% Adjusted EBITDA Margin¹ (%) 13.4% 16.8% -3.4 p.p |

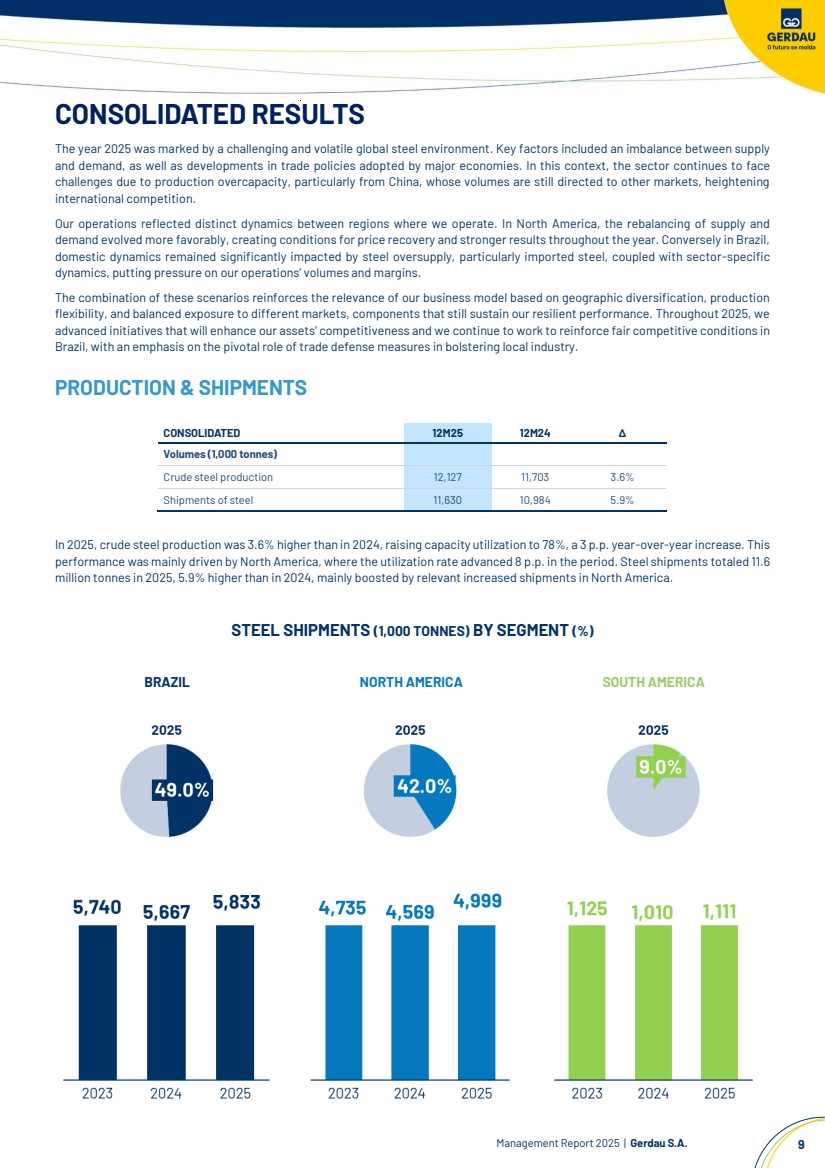

| Management Report 2025 | Gerdau S.A. 9 CONSOLIDATED RESULTS The year 2025 was marked by a challenging and volatile global steel environment. Key factors included an imbalance between supply and demand, as well as developments in trade policies adopted by major economies. In this context, the sector continues to face challenges due to production overcapacity, particularly from China, whose volumes are still directed to other markets, heightening international competition. Our operations reflected distinct dynamics between regions where we operate. In North America, the rebalancing of supply and demand evolved more favorably, creating conditions for price recovery and stronger results throughout the year. Conversely in Brazil, domestic dynamics remained significantly impacted by steel oversupply, particularly imported steel, coupled with sector-specific dynamics, putting pressure on our operations’ volumes and margins. The combination of these scenarios reinforces the relevance of our business model based on geographic diversification, production flexibility, and balanced exposure to different markets, components that still sustain our resilient performance. Throughout 2025, we advanced initiatives that will enhance our assets’ competitiveness and we continue to work to reinforce fair competitive conditions in Brazil, with an emphasis on the pivotal role of trade defense measures in bolstering local industry. PRODUCTION & SHIPMENTS CONSOLIDATED 12M25 12M24 ∆ Volumes (1,000 tonnes) Crude steel production 12,127 11,703 3.6% Shipments of steel 11,630 10,984 5.9% In 2025, crude steel production was 3.6% higher than in 2024, raising capacity utilization to 78%, a 3 p.p. year-over-year increase. This performance was mainly driven by North America, where the utilization rate advanced 8 p.p. in the period. Steel shipments totaled 11.6 million tonnes in 2025, 5.9% higher than in 2024, mainly boosted by relevant increased shipments in North America. STEEL SHIPMENTS (1,000 TONNES) BY SEGMENT (%) BRAZIL NORTH AMERICA SOUTH AMERICA |

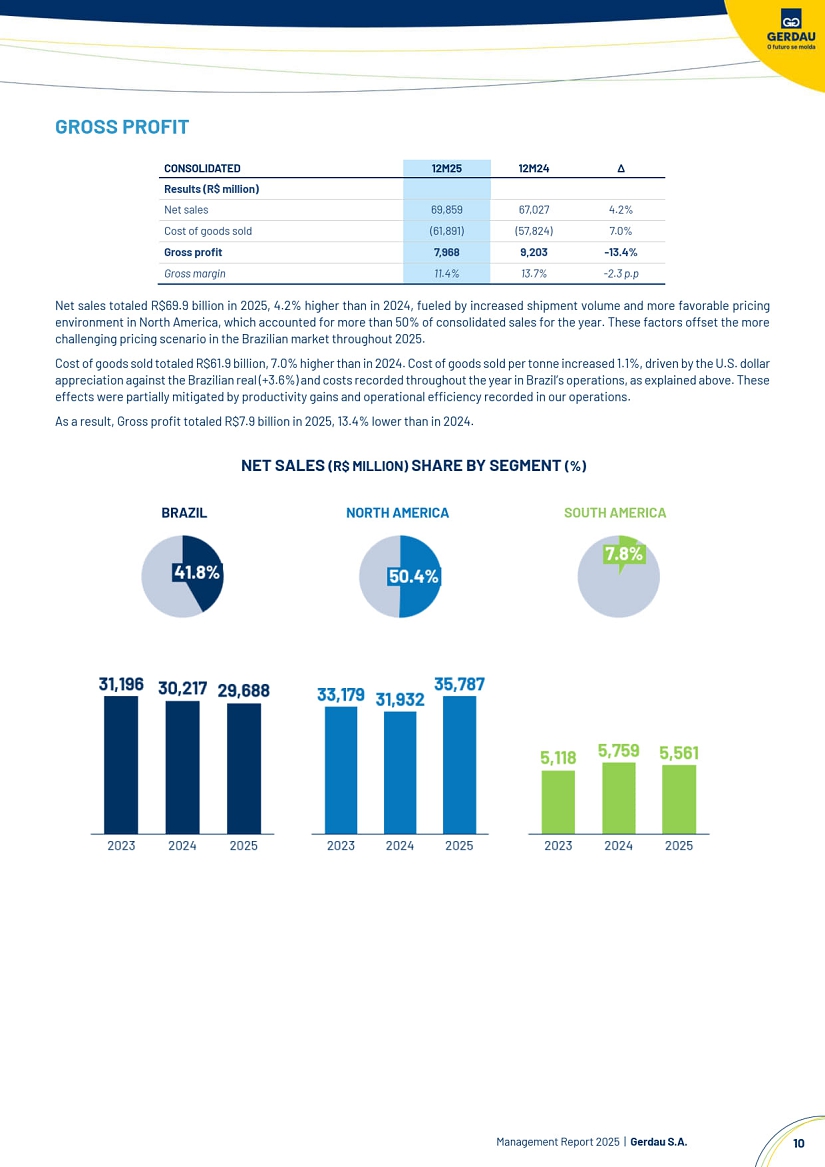

| Management Report 2025 | Gerdau S.A. 10 GROSS PROFIT Net sales totaled R$69.9 billion in 2025, 4.2% higher than in 2024, fueled by increased shipment volume and more favorable pricing environment in North America, which accounted for more than 50% of consolidated sales for the year. These factors offset the more challenging pricing scenario in the Brazilian market throughout 2025. Cost of goods sold totaled R$61.9 billion, 7.0% higher than in 2024. Cost of goods sold per tonne increased 1.1%, driven by the U.S. dollar appreciation against the Brazilian real (+1.2%) and costs recorded throughout the year in Brazil’s operations, as explained above. These effects were partially mitigated by productivity gains and operational efficiency recorded in our operations. As a result, Gross profit totaled R$7.9 billion in 2025, 13.4% lower than in 2024. NET SALES (R$ MILLION) SHARE BY SEGMENT (%) CONSOLIDATED 12M25 12M24 ∆ Results (R$ million) Net sales 69,859 67,027 4.2% Cost of goods sold (61,891) (57,824) 7.0% Gross profit 7,968 9,203 -13.4% Gross margin 11.4% 13.7% -2.3 p.p BRAZIL NORTH AMERICA SOUTH AMERICA |

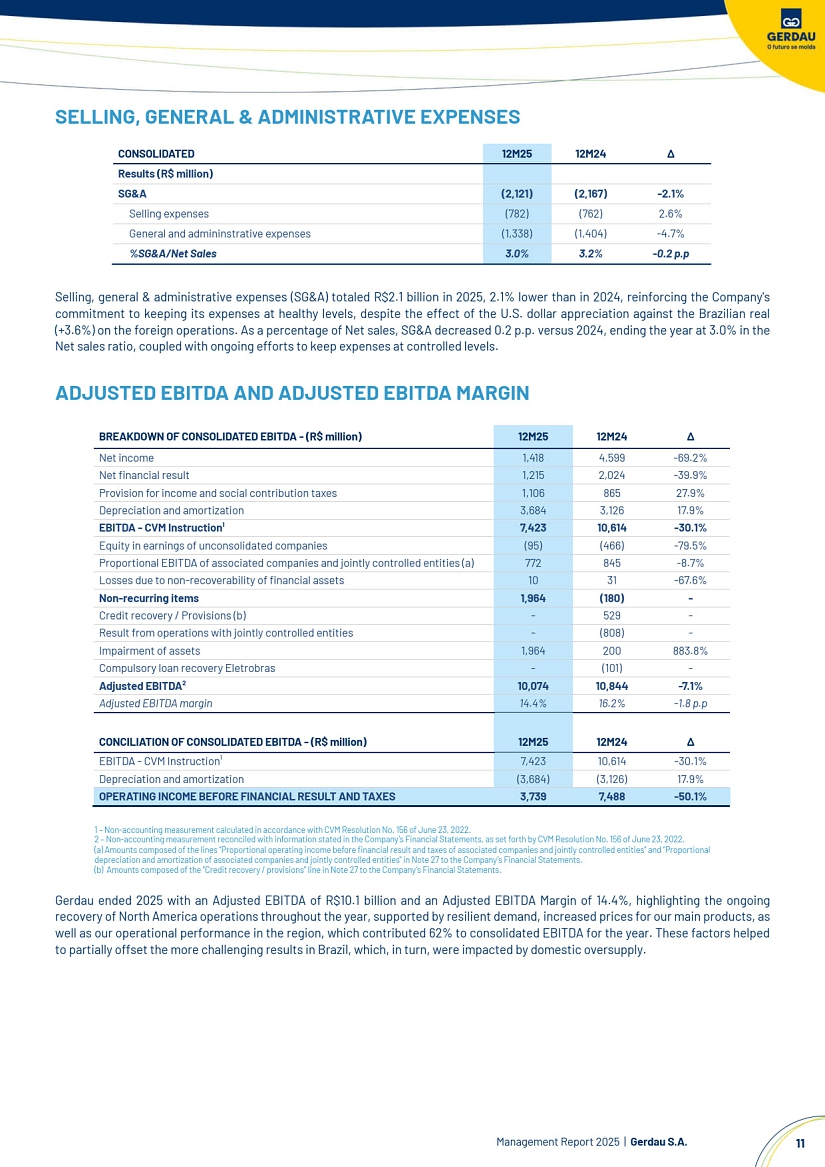

| Management Report 2025 | Gerdau S.A. 11 SELLING, GENERAL & ADMINISTRATIVE EXPENSES Selling, general & administrative expenses (SG&A) totaled R$2.1 billion in 2025, 2.1% lower than in 2024, reinforcing the Company's commitment to keeping its expenses at healthy levels, despite the effect of the U.S. dollar appreciation against the Brazilian real (+1.2%) on the foreign operations. As a percentage of Net sales, SG&A decreased 0.2 p.p. versus 2024, ending the year at 3.0% in the Net sales ratio, coupled with ongoing efforts to keep expenses at controlled levels. ADJUSTED EBITDA AND ADJUSTED EBITDA MARGIN 1 – Non-accounting measurement calculated in accordance with CVM Resolution No. 156 of June 23, 2022. 2 – Non-accounting measurement reconciled with information stated in the Company’s Financial Statements, as set forth by CVM Resolution No. 156 of June 23, 2022. (a) Amounts composed of the lines “Proportional operating income before financial result and taxes of associated companies and jointly controlled entities” and “Proportional depreciation and amortization of associated companies and jointly controlled entities" in Note 27 to the Company’s Financial Statements. (b) Amounts composed of the “Credit recovery / provisions” line in Note 27 to the Company’s Financial Statements. Gerdau ended 2025 with an Adjusted EBITDA of R$10.1 billion and an Adjusted EBITDA Margin of 14.4%, highlighting the ongoing recovery of North America operations throughout the year, supported by resilient demand, increased prices for our main products, as well as our operational performance in the region, which contributed 62% to consolidated EBITDA for the year. These factors helped to partially offset the more challenging results in Brazil, which, in turn, were impacted by domestic oversupply. CONSOLIDATED 12M25 12M24 ∆ Results (R$ million) SG&A (2,121) (2,167) -2.1% Selling expenses (782) (762) 2.6% General and admininstrative expenses (1,338) (1,404) -4.7% %SG&A/Net Sales 3.0% 3.2% -0.2 p.p BREAKDOWN OF CONSOLIDATED EBITDA - (R$ million) 12M25 12M24 ∆ Net income 1,418 4,599 -69.2% Net financial result 1,215 2,024 -39.9% Provision for income and social contribution taxes 1,106 865 27.9% Depreciation and amortization 3,684 3,126 17.9% EBITDA - CVM Instruction¹ 7,423 10,614 -30.1% Equity in earnings of unconsolidated companies (95) (466) -79.5% Proportional EBITDA of associated companies and jointly controlled entities (a) 772 845 -8.7% Losses due to non-recoverability of financial assets 10 31 -67.6% Non-recurring items 1,964 (180) - Credit recovery / Provisions (b) - 529 - Result from operations with jointly controlled entities - (808) - Impairment of assets 1,964 200 883.8% Compulsory loan recovery Eletrobras - (101) - Adjusted EBITDA² 10,074 10,844 -7.1% Adjusted EBITDA margin 14.4% 16.2% -1.8 p.p CONCILIATION OF CONSOLIDATED EBITDA - (R$ million) 12M25 12M24 ∆ EBITDA - CVM Instruction¹ 7,423 10,614 -30.1% Depreciation and amortization (3,684) (3,126) 17.9% OPERATING INCOME BEFORE FINANCIAL RESULT AND TAXES 3,739 7,488 -50.1% |

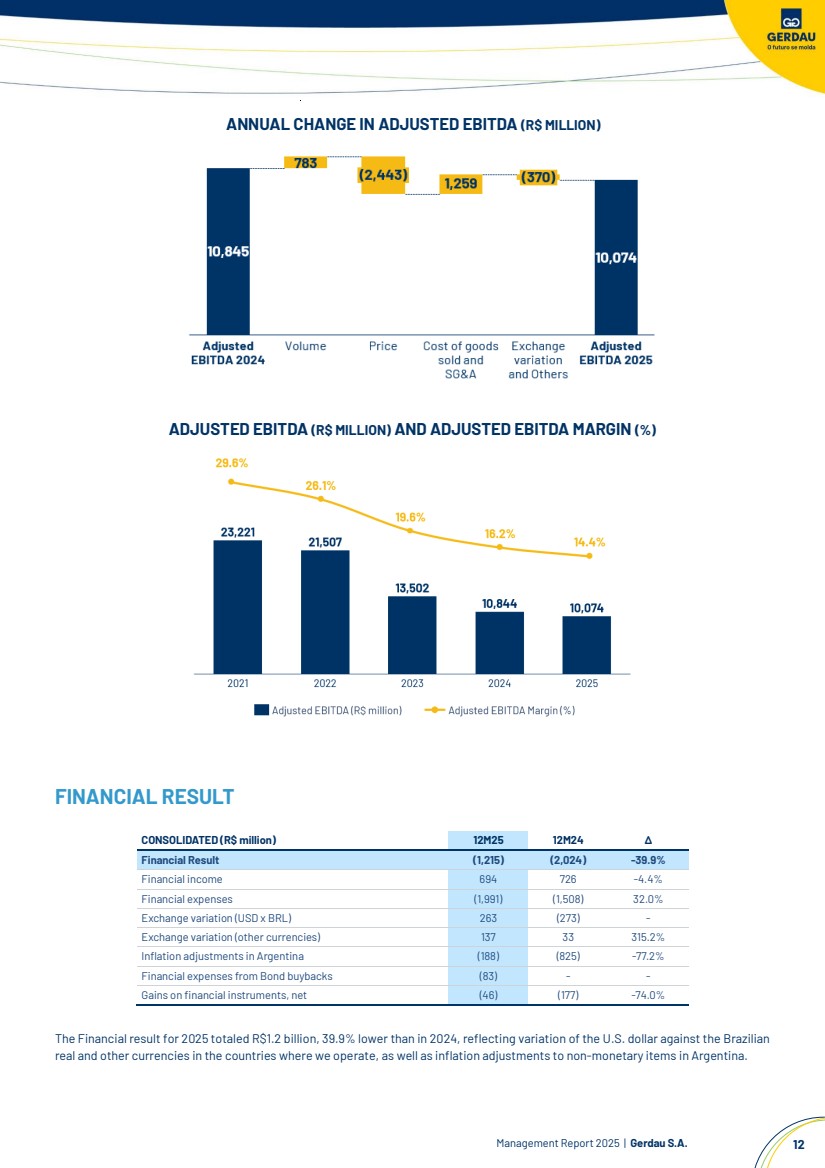

| Management Report 2025 | Gerdau S.A. 12 ANNUAL CHANGE IN ADJUSTED EBITDA (R$ MILLION) ADJUSTED EBITDA (R$ MILLION) AND ADJUSTED EBITDA MARGIN (%) FINANCIAL RESULT CONSOLIDATED (R$ million) 12M25 12M24 ∆ Financial Result (1,215) (2,024) -39.9% Financial income 694 726 -4.4% Financial expenses (1,991) (1,508) 32.0% Exchange variation (USD x BRL) 263 (273) - Exchange variation (other currencies) 137 33 315.2% Inflation adjustments in Argentina (188) (825) -77.2% Financial expenses from Bond buybacks (83) - - Gains on financial instruments, net (46) (177) -74.0% The Financial result for 2025 totaled R$1.2 billion, 39.9% lower than in 2024, reflecting variation of the U.S. dollar against the Brazilian real and other currencies in the countries where we operate, as well as inflation adjustments to non-monetary items in Argentina. |

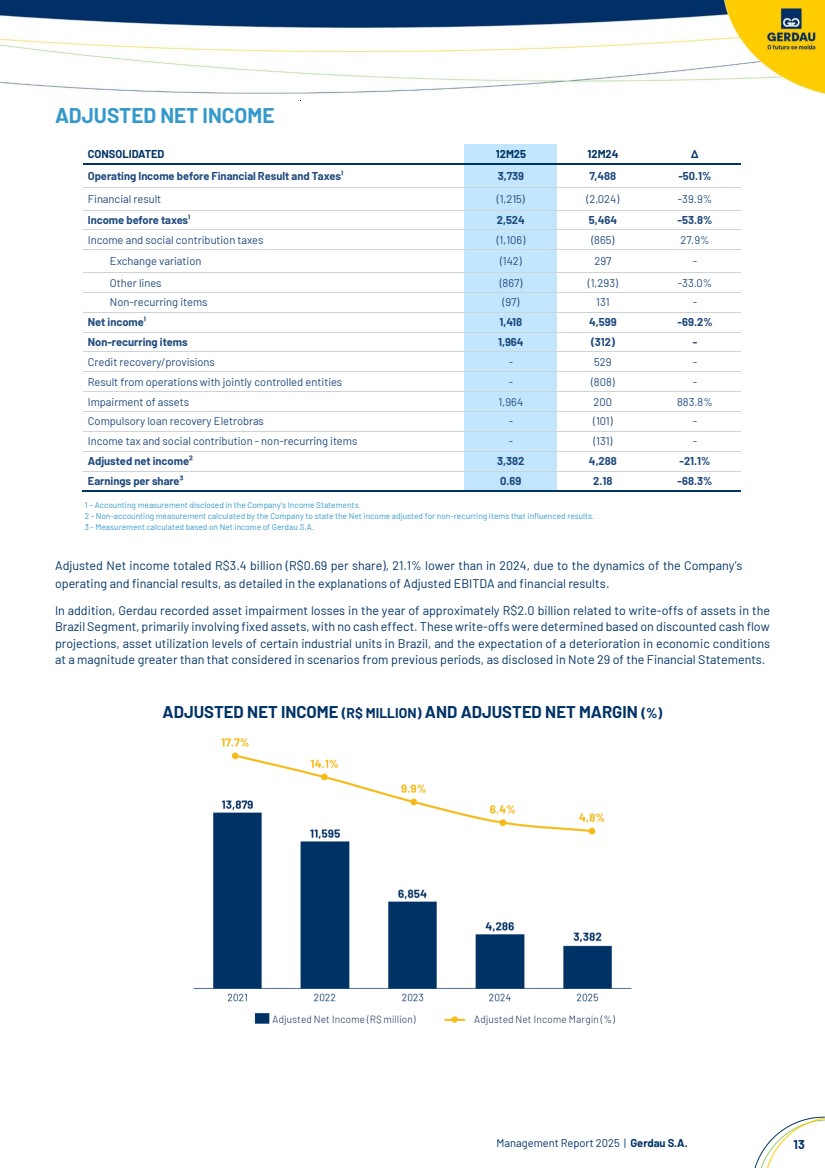

| Management Report 2025 | Gerdau S.A. 13 ADJUSTED NET INCOME 1 – Accounting measurement disclosed in the Company’s Income Statements. 2 - Non-accounting measurement calculated by the Company to state the Net income adjusted for non-recurring items that influenced results. 3 - Measurement calculated based on Net income of Gerdau S.A. Adjusted Net income totaled R$3.4 billion (R$0.69 per share), 21.1% lower than in 2024, due to the dynamics of the Company’s operating and financial results, as detailed in the explanations of Adjusted EBITDA and financial results. In addition, Gerdau recorded asset impairment losses in the year of approximately R$2.0 billion related to write-offs of assets in the Brazil Segment, primarily involving fixed assets, with no cash effect. These write-offs were determined based on discounted cash flow projections, asset utilization levels of certain industrial units in Brazil, and the expectation of a deterioration in economic conditions at a magnitude greater than that considered in scenarios from previous periods, as disclosed in Note 29 of the Financial Statements. ADJUSTED NET INCOME (R$ MILLION) AND ADJUSTED NET MARGIN (%) CONSOLIDATED 12M25 12M24 ∆ Operating Income before Financial Result and Taxes¹ 3,739 7,488 -50.1% Financial result (1,215) (2,024) -39.9% Income before taxes¹ 2,524 5,464 -53.8% Income and social contribution taxes (1,106) (865) 27.9% Exchange variation (142) 297 - Other lines (867) (1,293) -33.0% Non-recurring items (97) 131 - Net income¹ 1,418 4,599 -69.2% Non-recurring items 1,964 (312) - Credit recovery/provisions - 529 - Result from operations with jointly controlled entities - (808) - Impairment of assets 1,964 200 883.8% Compulsory loan recovery Eletrobras - (101) - Income tax and social contribution - non-recurring items - (131) - Adjusted net income² 3,382 4,288 -21.1% Earnings per share³ 0.69 2.18 -68.3% |

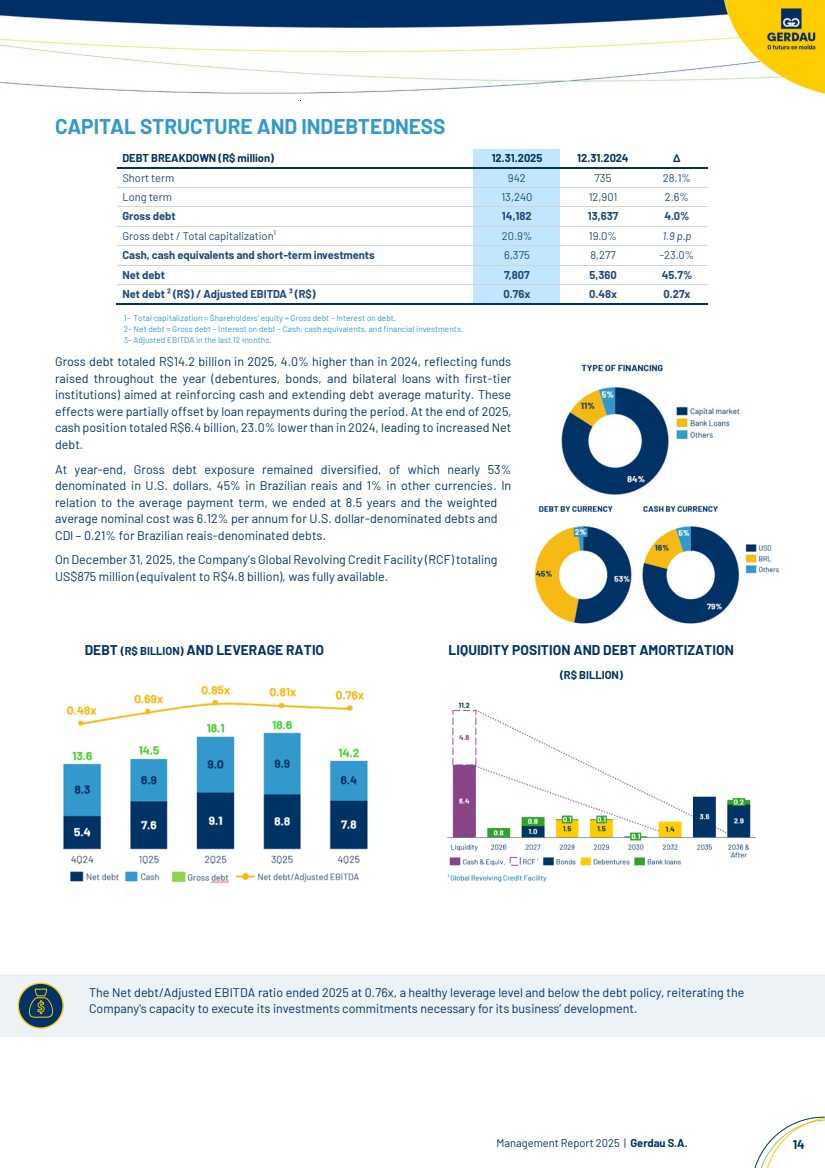

| Management Report 2025 | Gerdau S.A. 14 The Net debt/Adjusted EBITDA ratio ended 2025 at 0.76x, a healthy leverage level and below the debt policy, reiterating the Company's capacity to execute its investments commitments necessary for its business’ development. CAPITAL STRUCTURE AND INDEBTEDNESS DEBT BREAKDOWN (R$ million) 12.31.2025 12.31.2024 ∆ Short term 942 735 28.1% Long term 13,240 12,901 2.6% Gross debt 14,182 13,637 4.0% Gross debt / Total capitalization¹ 20.9% 19.0% 1.9 p.p Cash, cash equivalents and short-term investments 6,375 8,277 -23.0% Net debt 7,807 5,360 45.7% Net debt² (R$) / Adjusted EBITDA ³ (R$) 0.76x 0.48x 0.27x 1- Total capitalization = Shareholders’ equity + Gross debt – Interest on debt. 2- Net debt = Gross debt – Interest on debt – Cash, cash equivalents, and financial investments. 3- Adjusted EBITDA in the last 12 months. Gross debt totaled R$14.2 billion in 2025, 4.0% higher than in 2024, reflecting funds raised throughout the year (debentures, bonds, and bilateral loans with first-tier institutions) aimed at reinforcing cash and extending debt average maturity. These effects were partially offset by loan repayments during the period. At the end of 2025, cash position totaled R$6.4 billion, 23.0% lower than in 2024, leading to increased Net debt. At year-end, Gross debt exposure remained diversified, of which nearly 53% denominated in U.S. dollars, 45% in Brazilian reais and 1% in other currencies. In relation to the average payment term, we ended at 8.5 years and the weighted average nominal cost was 6.12% per annum for U.S. dollar-denominated debts and CDI – 0.21% for Brazilian reais-denominated debts. On December 31, 2025, the Company’s Global Revolving Credit Facility (RCF) totaling US$875 million (equivalent to R$4.8 billion), was fully available. DEBT (R$ BILLION) AND LEVERAGE RATIO LIQUIDITY POSITION AND DEBT AMORTIZATION (R$ BILLION) |

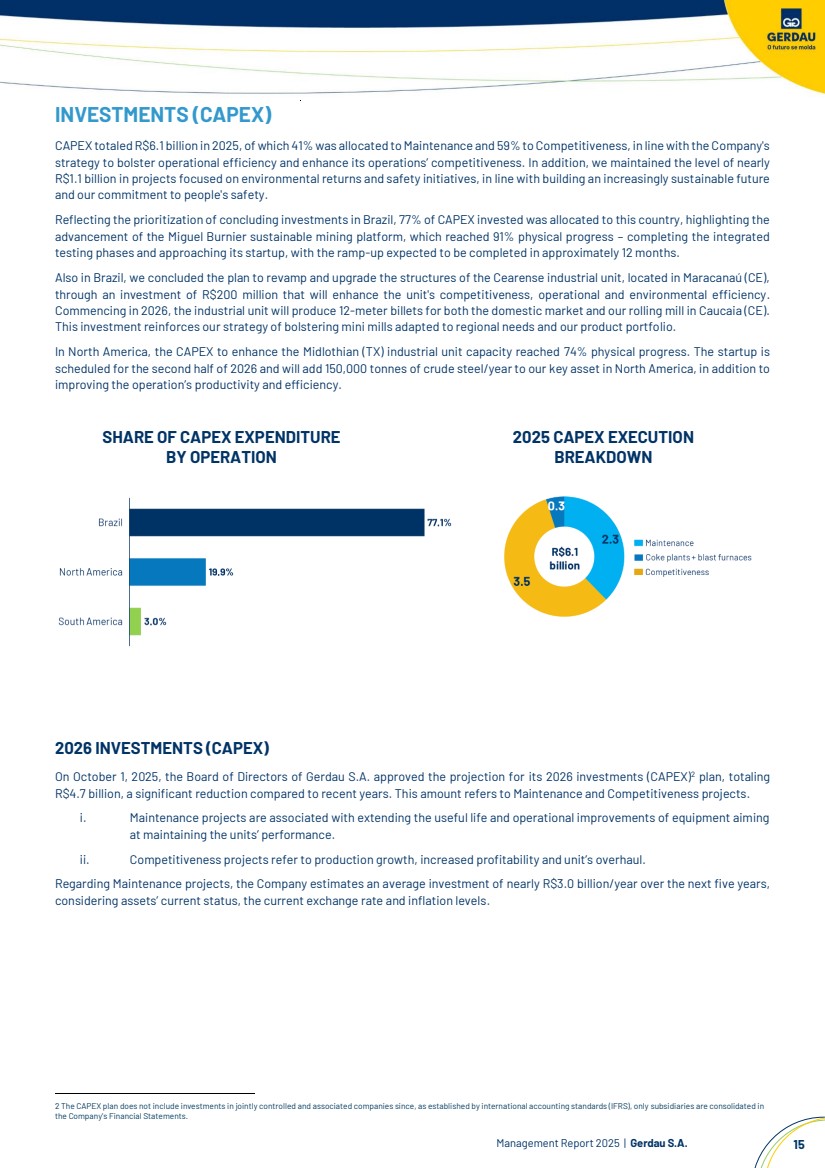

| Management Report 2025 | Gerdau S.A. 15 INVESTMENTS (CAPEX) CAPEX totaled R$6.1 billion in 2025, of which 41% was allocated to Maintenance and 59% to Competitiveness, in line with the Company's strategy to bolster operational efficiency and enhance its operations’ competitiveness. In addition, we maintained the level of nearly R$1.1 billion in projects focused on environmental returns and safety initiatives, in line with building an increasingly sustainable future and our commitment to people's safety. Reflecting the prioritization of concluding investments in Brazil, 77% of CAPEX invested was allocated to this country, highlighting the advancement of the Miguel Burnier sustainable mining platform, which reached 91% physical progress – completing the integrated testing phases and approaching its startup, with the ramp-up expected to be completed in approximately 12 months. Also in Brazil, we concluded the plan to revamp and upgrade the structures of the Cearense industrial unit, located in Maracanaú (CE), through an investment of R$200 million that will enhance the unit's competitiveness, operational and environmental efficiency. Commencing in 2026, the industrial unit will produce 12-meter billets for both the domestic market and our rolling mill in Caucaia (CE). This investment reinforces our strategy of bolstering mini mills adapted to regional needs and our product portfolio. In North America, the CAPEX to enhance the Midlothian (TX) industrial unit capacity reached 74% physical progress. The startup is scheduled for the second half of 2026 and will add 150,000 tonnes of crude steel/year to our key asset in North America, in addition to improving the operation’s productivity and efficiency. SHARE OF CAPEX EXPENDITURE BY OPERATION 2025 CAPEX EXECUTION BREAKDOWN 2026 INVESTMENTS (CAPEX) On October 1, 2025, the Board of Directors of Gerdau S.A. approved the projection for its 2026 investments (CAPEX) 2 plan, totaling R$4.7 billion, a significant reduction compared to recent years. This amount refers to Maintenance and Competitiveness projects. i. Maintenance projects are associated with extending the useful life and operational improvements of equipment aiming at maintaining the units’ performance. ii. Competitiveness projects refer to production growth, increased profitability and unit’s overhaul. Regarding Maintenance projects, the Company estimates an average investment of nearly R$3.0 billion/year over the next five years, considering assets’ current status, the current exchange rate and inflation levels. 2 The CAPEX plan does not include investments in jointly controlled and associated companies since, as established by international accounting standards (IFRS), only subsidiaries are consolidated in the Company's Financial Statements. |

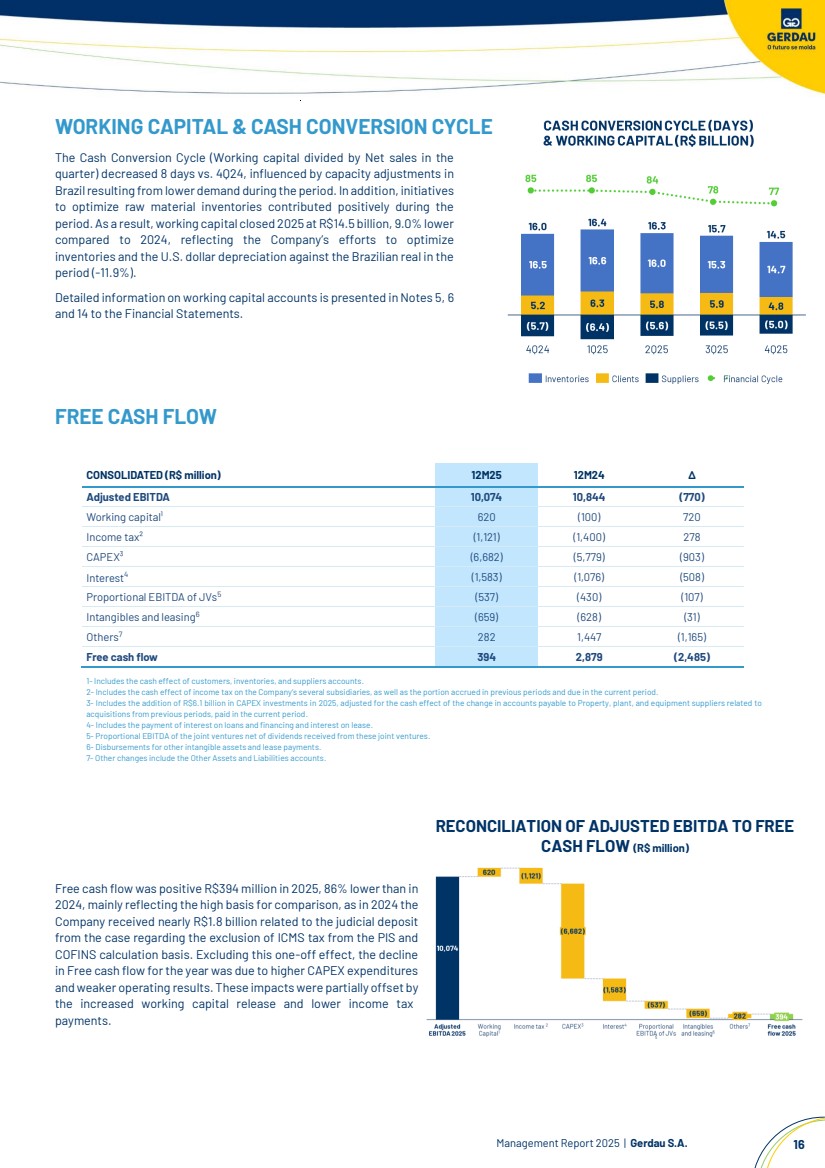

| Management Report 2025 | Gerdau S.A. 16 WORKING CAPITAL & CASH CONVERSION CYCLE The Cash Conversion Cycle (Working capital divided by Net sales in the quarter) decreased 8 days vs. 4Q24, influenced by capacity adjustments in Brazil resulting from lower demand during the period. In addition, initiatives to optimize raw material inventories contributed positively during the period. As a result, working capital closed 2025 at R$14.5 billion, 9.0% lower compared to 2024, reflecting the Company’s efforts to optimize inventories and the U.S. dollar depreciation against the Brazilian real in the period (-11.9%). Detailed information on working capital accounts is presented inNotes 5, 6 and 14 to the Financial Statements. FREE CASH FLOW CONSOLIDATED (R$ million) 12M25 12M24 ∆ Adjusted EBITDA 10,074 10,844 (770) Working capital¹ 620 (100) 720 Income tax² (1,121) (1,400) 278 CAPEX³ (6,682) (5,779) (903) Interest4 (1,583) (1,076) (508) Proportional EBITDA of JVs5 (537) (430) (107) Intangibles and leasing6 (659) (628) (31) Others7 282 1,447 (1,165) Free cash flow 394 2,879 (2,485) 1- Includes the cash effect of customers, inventories, and suppliers accounts. 2- Includes the cash effect of income tax on the Company’s several subsidiaries, as well as the portion accrued in previous periods and due in the current period. 3- Includes the addition of R$6.1 billion in CAPEX investments in 2025, adjusted for the cash effect of the change in accounts payable to Property, plant, and equipment suppliers related to acquisitions from previous periods, paid in the current period. 4- Includes the payment of interest on loans and financing and interest on lease. 5- Proportional EBITDA of the joint ventures net of dividends received from these joint ventures. 6- Disbursements for other intangible assets and lease payments. 7- Other changes include the Other Assets and Liabilities accounts. RECONCILIATION OF ADJUSTED EBITDA TO FREE CASH FLOW (R$ million) Free cash flow was positive R$394 million in 2025, 86% lower than in 2024, mainly reflecting the high basis for comparison, as in 2024 the Company received nearly R$1.8 billion related to the judicial deposit from the case regarding the exclusion of ICMS tax from the PIS and COFINS calculation basis. Excluding this one-off effect, the decline in Free cash flow for the year was due to higher CAPEX expenditures and weaker operating results. These impacts were partially offset by the increased working capital release and lower income tax payments. |

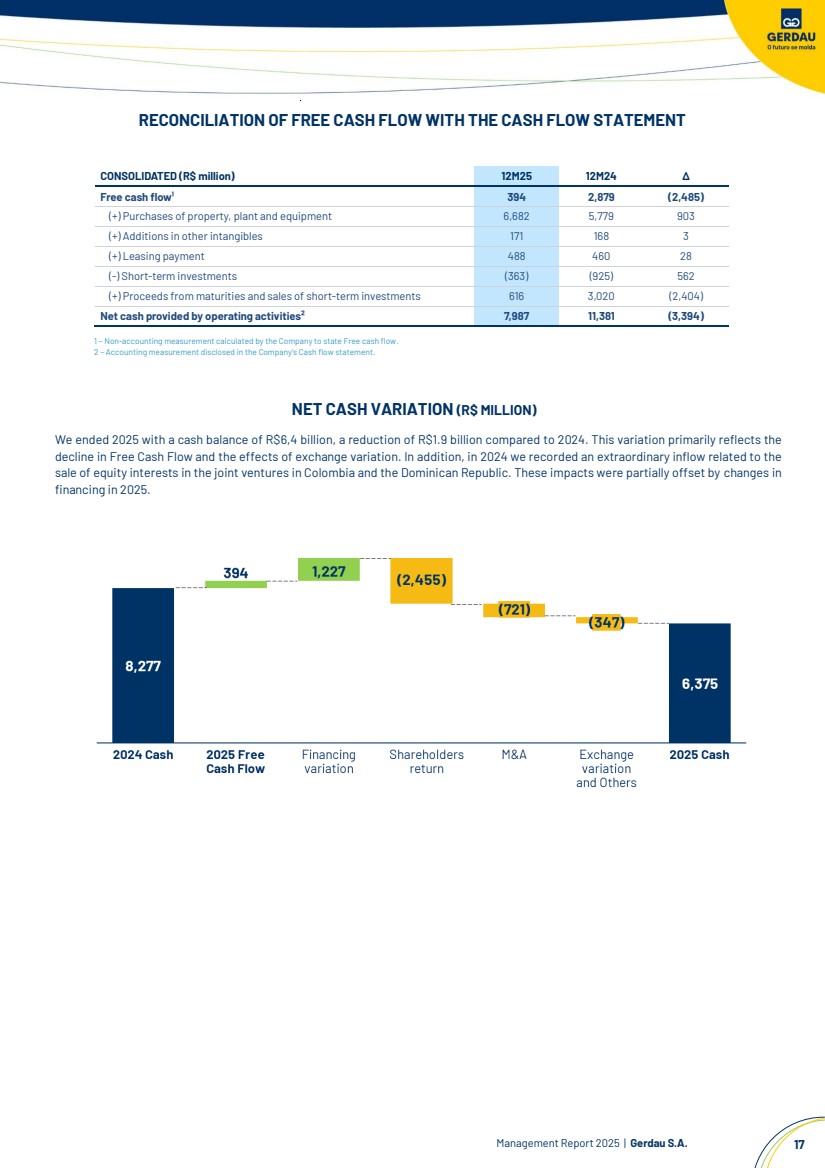

| Management Report 2025 | Gerdau S.A. 17 RECONCILIATION OF FREE CASH FLOW WITH THE CASH FLOW STATEMENT 1 – Non-accounting measurement calculated by the Company to state Free cash flow. 2 – Accounting measurement disclosed in the Company’s Cash flow statement. NET CASH VARIATION (R$ MILLION) We ended 2025 with a cash balance of R$6,4 billion, a reduction of R$1.9 billion compared to 2024. This variation primarily reflects the decline in Free Cash Flow and the effects of exchange variation. In addition, in 2024 we recorded an extraordinary inflow related to the sale of equity interests in the joint ventures in Colombia and the Dominican Republic. These impacts were partially offset by changes in financing in 2025. CONSOLIDATED (R$ million) 12M25 12M24 ∆ Free cash flow¹ 394 2,879 (2,485) (+) Purchases of property, plant and equipment 6,682 5,779 903 (+) Additions in other intangibles 171 168 3 (+) Leasing payment 488 460 28 (-) Short-term investments (363) (925) 562 (+) Proceeds from maturities and sales of short-term investments 616 3,020 (2,404) Net cash provided by operating activities² 7,987 11,381 (3,394) |

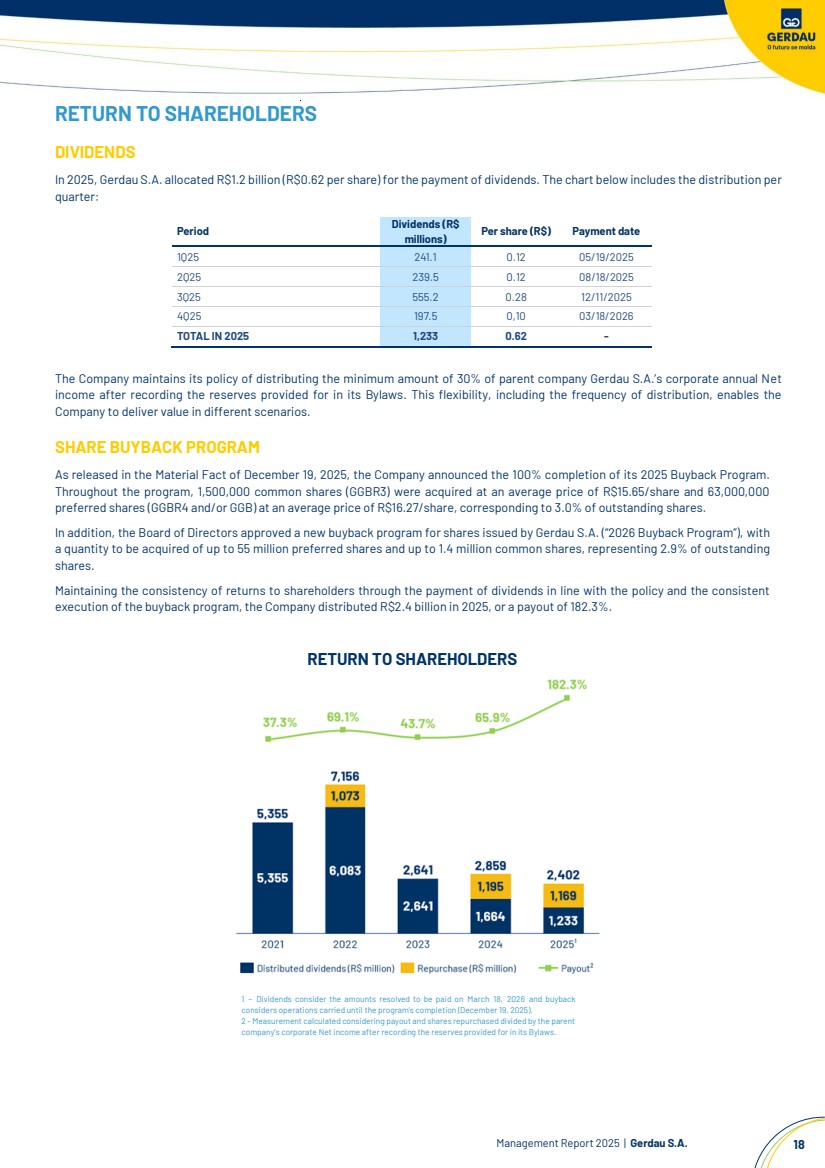

| Management Report 2025 | Gerdau S.A. 18 RETURN TO SHAREHOLDERS DIVIDENDS In 2025, Gerdau S.A. allocated R$1.2 billion (R$0.62 per share) for the payment of dividends. The chart below includes the distribution per quarter: The Company maintains its policy of distributing the minimum amount of 30% of parent company Gerdau S.A.’s corporate annual Net income after recording the reserves provided for in its Bylaws. This flexibility, including the frequency of distribution, enables the Company to deliver value in different scenarios. SHARE BUYBACK PROGRAM As released in the Material Fact of December 19, 2025, the Company announced the 100% completion of its 2025 Buyback Program. Throughout the program, 1,500,000 common shares (GGBR3) were acquired at an average price of R$15.65/share and 63,000,000 preferred shares (GGBR4 and/or GGB) at an average price of R$16.27/share, corresponding to 3.0% of outstanding shares. In addition, the Board of Directors approved a new buyback program for shares issued by Gerdau S.A. (“2026 Buyback Program”), with a quantity to be acquired of up to 55 million preferred shares and up to 1.4 million common shares, representing 2.9% of outstanding shares. Maintaining the consistency of returns to shareholders through the payment of dividends in line with the policy and the consistent execution of the buyback program, the Company distributed R$2.4 billion in 2025, or a payout of 182.3%. RETURN TO SHAREHOLDERS 1 – Dividends consider the amounts resolved to be paid on March 18, 2026 and buyback considers operations carried until the program’s completion (December 19, 2025). 2 - Measurement calculated considering payout and shares repurchased divided by the parent company’s corporate Net income after recording the reserves provided for in its Bylaws. Period Dividends (R$ millions) Per share (R$) Payment date 1Q25 241.1 0.12 05/19/2025 2Q25 239.5 0.12 08/18/2025 3Q25 555.2 0.28 12/11/2025 4Q25 197.5 0,10 03/18/2026 TOTAL IN 2025 1,233 0.62 - |

| Management Report 2025 | Gerdau S.A. 19 SUSTAINABILITY Gerdau, with its 125 years of history, is dedicated to shaping a future in which it will contribute to solutions for the planet's challenges, recognizing the relevance of low-carbon steel as an indispensable element for the energy transition and the construction of a more sustainable world. It will also remain committed to Brazil’s industry and socio-economic development. Gerdau's more than 30,000 employees are dedicated to achieving the Company’s goals daily, who share a vision of the future based on delivering exceptional products and solutions to customers while making a positive impact on the communities in which the Company operates. As a result of all these efforts, Gerdau was again recognized in 2025 by prominent national and international awards for its environmental, social, and governance practices. In addition, the Company reaffirms the strength of its environmental management by sustaining CDP high scores, a global benchmark organization for environmental transparency, with an A- score in the Climate Change module report, leadership rating that recognizes companies with advanced practices in managing climate-related risks and opportunities, surpassing the sector’s global average score, and a B score in Water Security, reflecting consistent water resource management and mitigation of risks related to this issue. In addition, the Governance Report (ICVM 586) shows that the Company achieved 72% adhesion to practices, 2 p.p. higher than in 2024. Furthermore, in 2025, various Company programs were reinforced to enhance participation in building an even more diverse and inclusive world. Looking ahead, Gerdau reaffirms its commitment to sustainability across all its dimensions, as a cross-cutting issue in its long-term business strategy. The Company recognizes that sustainable development is paramount to ensuring a prosperous future for its operations and for generations to come. RATINGS Credit Rating Agencies Reports AGENCY NATIONAL SCALE GLOBAL SCALE OUTLOOK LAST UPDATE Standard & Poors brAAA BBB Stable October, 2024 Fitch Ratings brAAA BBB Stable July, 2025 Moody’s - Baa2 Stable April, 2025 |

| Management Report 2025 | Gerdau S.A. 20 PARENT COMPANY INFORMATION A substantial amount of Gerdau S.A.'s results comes from investments in subsidiaries, jointly controlled and associated companies. The value of these investments as of December 31, 2025, totaled R$53.0 billion, resulting in Equity in the earnings of unconsolidated companies of R$1.4 billion in 2025. Steel products in 2025 generated Net sales of R$4.8 billion, with cost of goods sold of R$3.8 billion, resulting in a Gross margin of 21.5% in 2025. In 2025, the Financial result (Financial income less Financial expenses, Exchange variation, and losses on Financial instruments) was negative R$411 million (R$601 million in 2024). This variation in the Financial result mainly derived from exchange variation effects in the period. Gerdau S.A. recorded Net income of R$1.4 billion in 2025, equivalent to R$0.69 per share, versus Net income of R$4.6 billion in 2024, equivalent to R$2.18 per share. The Net income decline mainly reflects lower operating result in the period. In compliance with the Company’s policy, on December 31, 2025, Gross debt totaled R$4.7 billion, versus R$3.8 billion on December 31, 2024. The increase reflects the issuance of debentures during the year, which totaled R$900 million. On December 31, 2025, the Company’s Shareholders’ equity totaled R$53.6 billion, corresponding to a book value of R$27.13 per share. RELATIONSHIP WITH EXTERNAL AUDITORS The Company’s policy for hiring any services from the independent auditor unrelated to external audit is based on principles that preserve the independence of the auditor, namely (a) auditors must not audit their own work; (b) auditors must not perform managerial duties at their customers; and (c) auditors must not promote the interests of their customers. The audit fees refer to professional services rendered in the audit of the Company's consolidated financial statements, quarterly reviews of the Company's consolidated financial statements, corporate audits, and interim reviews of certain subsidiaries, as required by the appropriate legislation. Audit fees refer to services traditionally performed by an external auditor in acquisitions and advisory on accounting standards and transactions. Non-audit fees correspond mainly to services rendered to the Company’s subsidiaries abroad to comply with tax requirements. In order to comply with CVM Resolutions 80/2022 and 162/2022, Gerdau S.A. announces that PricewaterhouseCoopers Auditores Independentes Ltda., the Company’s external audit firm, has not provided any services other than auditing that could lead to a conflict of interest, loss of independence, or loss of objectivity of the auditing services provided. DECLARATION OF THE EXECUTIVE BOARD In compliance with the provisions in Article 27 of CVM Resolution 80/2022, the Executive Board declares that it has reviewed, discussed, and agreed with the Financial Statements for the fiscal year ended December 31, 2025, and with the opinion expressed in the Independent Auditors' Report on the Financial Statements, issued on this date. São Paulo, February 23,2026. THE MANAGEMENT |

| Rafael Japur Vice President and Investor Relations Officer Mariana Velho Dutra IR Manager Ariana Pereira Renata Albuquerque Arthur Alves Trovo Adriana Costa Adriana Costa Siga a Gerdau nas Redes Sociais IR CONTACTS Investor Relations website: http://ri.gerdau.com/ IR e-mail: inform@gerdau.com Press e-mail: atendimentogerdau.br@bcw-global.com |