Annual Report 2024

March 6, 2025

Term |

Definition | |

AI |

Artificial intelligence | |

“Big 3” segments |

Our combined Legal Professionals, Corporates and Tax & Accounting Professionals segments | |

Blackstone’s consortium |

The Blackstone Group and its subsidiaries, and private equity funds affiliated with Blackstone | |

bp |

Basis points – one basis point is equal to 1/100th of 1%,“100bp” is equivalent to 1% | |

constant currency |

A non-IFRS measure derived by applying the same foreign currency exchange rates to the financial results of the current and equivalent prior-year period | |

EBITDA |

Earnings before interest, tax, depreciation and amortization | |

EPS |

Earnings per share | |

IFRS |

International Financial Reporting Standards | |

LSEG |

London Stock Exchange Group plc | |

ML |

Machine learning | |

n/a |

Not applicable | |

n/m |

Not meaningful | |

organic or organically |

A non-IFRS measure that represents changes in revenues of our existing businesses at constant currency. The metric excludes the distortive impacts of acquisitions and dispositions from not owning the business in both comparable periods | |

Woodbridge |

The Woodbridge Company Limited, our principal and controlling shareholder | |

YPL |

York Parent Limited, the entity that owned LSEG shares, which is jointly owned by our company and the Blackstone consortium. References to YPL also include its subsidiaries. | |

$ and US$ |

U.S. dollars | |

2 |

||||

| 2 | ||||

| 5 | ||||

| 5 | ||||

| 5 | ||||

| 6 | ||||

| 6 | ||||

| 6 | ||||

| 7 | ||||

| 10 | ||||

| 10 | ||||

| 10 | ||||

| 10 | ||||

| 10 | ||||

| 10 | ||||

| 11 | ||||

| 11 | ||||

| 11 | ||||

| 12 | ||||

| 13 | ||||

| 15 | ||||

16 |

||||

28 |

||||

81 |

||||

142 |

||||

| 142 | ||||

| 144 | ||||

| 147 | ||||

| 148 | ||||

| 149 | ||||

| 149 | ||||

| 150 | ||||

| 151 | ||||

| 151 | ||||

| 151 | ||||

152 |

||||

| 152 | ||||

| 153 | ||||

| 154 | ||||

| 155 | ||||

| 155 | ||||

| 156 | ||||

| 156 | ||||

| 159 | ||||

| 160 | ||||

| 160 | ||||

162 |

||||

| 162 | ||||

| 163 | ||||

|

Legal Professionals Serves law firms and governments with research and workflow products powered by leading-edge technologies, including generative AI, focusing on intuitive legal research and integrated legal workflow solutions that combine content, tools and analytics. | |

|

Corporates Serves corporations, ranging from small businesses to multinational organizations, including the seven largest global accounting firms, with our full suite of content-driven products, powered by leading-edge technologies, including generative AI, and integrated compliance workflow solutions to help them achieve their business outcomes. | |

|

Tax & Accounting Professionals Serves tax, audit and accounting firms (other than the seven largest, which are served by our Corporates segment) with research and workflow products powered by leading-edge technologies, including generative AI. | |

|

Reuters News Supplies business, financial and global news and data to the world’s media organizations, professionals and news consumers through Reuters News Agency, Reuters.com, Reuters Events, Thomson Reuters products and to financial firms exclusively via LSEG products. | |

|

Global Print Provides legal and tax information primarily in print format to customers around the world and provides commercial printing services to a wide range of book publishers. |

| Page 2 | Thomson Reuters Annual Report 2024 |

Attractive Industry • Currently our “Big 3” segments operate in an estimated $28 billion market expected to grow between 8% and 11% over the next 5 years• Legal, Tax & Risk markets are prime for content-driven innovation |

Balanced and Diversified Leadership • A leader in key Legal Professionals, Corporates, Tax & Accounting Professionals and News segments• Resilient businesses, historically stable, through periods of macroeconomic uncertainty• Approximately 450,000 customers; largest customer is approximately 5% of revenues* |

Attractive Business Model • 81% of revenues were recurring in 2024• Fixed cost model supports operating leverage as we grow• Strong and consistent cash generation capabilities |

Strong Competitive Positioning • Proprietary content plus data and human expertise combined with AI and ML are key differentiators• Products deeply embedded in customers’ daily workflows• 91% retention rate in 2024 |

Disciplined Financial Policies • Focused and incentivized on organic revenue growth and free cash flow growth• Balance investing in business and returning capital to shareholders• Committed to maintaining investment grade rating with stable capital structure• · Significant potential capital capacity affords optionality |

| * | The news agreement with the Data & Analytics business of LSEG. |

• |

2022 two-year Change Program (an initiative that focused on transforming our company from a holding company to an operating company and from a content provider into a content-driven technology company) was completed by the end of 2022. We achieved $540 million of annualized run-rate operating expense savings and made significant progress transforming Thomson Reuters into a more streamlined and scalable business that we believe has a strong foundation for sustainable future growth. In 2022, LSEG repurchased approximately 1.2 million ordinary shares from YPL under a buyback program announced by LSEG in August 2022. We received proceeds of $43 million, for approximately 0.5 million shares, related to our portion of the buyback. In 2022, we also launched Westlaw Precision, a new version of Westlaw designed to dramatically improve research speed and quality by enabling lawyers to target precisely what they are looking for. |

• |

2023 AI-based initiatives, including generative AI. In November 2023, we announced a series of generative AI initiatives designed to assist in the transformation of the legal profession. Most notably, the commercial releases of AI-Assisted Research on Westlaw Precision and CoCounsel Core AI Assistant for lawyers. In 2023, we further deepened our focus on content-enabled technology with the acquisitions of SurePrep, LLC, Imagen Ltd., Casetext, Inc., and the remaining interest in Westlaw Japan. |

• |

2024 AI-enabled tools to automate internal processes, including in the Reuters newsroom and our editorial and go-to-market |

Thomson Reuters Annual Report 2024 |

Page 3 |

| Page 4 | Thomson Reuters Annual Report 2024 |

• |

Continue evolving our transformative AI capabilities through ongoing product innovation and enhancements to our flagship products |

• |

Continue to roll out our AI assistant, CoCounsel, across our customer base |

• |

Maintain and build on our deep domain expertise and comprehensive collection of richly enhanced data and content |

• |

Further enhance our go-to-market |

• |

Extend our channel partnerships to integrate our products and services into broader ecosystems |

• |

Ongoing expansion of our international offerings |

• |

Accelerate our pace of execution to move fast and win in a competitive market |

• |

Leverage our significant capital capacity to fund organic investment and execute a balanced capital allocation approach including annual dividend growth, strategic acquisitions and shareholder returns |

Thomson Reuters Annual Report 2024 |

Page 5 |

| Page 6 | Thomson Reuters Annual Report 2024 |

Brand |

Type of Product/Service |

Legal Professionals |

Corporates |

Tax & Accounting Professionalss | ||||

Westlaw Westlaw Edge (U.S., U.K. & Canada) Westlaw Precision (U.S.) |

Legal, regulatory and compliance information-based products and services. Westlaw is our primary online legal research delivery platform. Westlaw offers authoritative content, powerful search functionality and research organization, team collaboration features and navigation tools to find and share specific points of law and search for analytical commentary. Westlaw employs proprietary, innovative technology including generative AI. Localized country-specific online legal research platforms are provided for Argentina, Australia, Brazil, Canada, Chile, Ireland, Japan, New Zealand, the United Kingdom, United States, Uruguay and other countries. Through Westlaw International and Westlaw Asia, we offer our region-based online legal research platforms to customers in markets where we do not offer a country-specific Westlaw service. |

|

|

|||||

Practical Law Practical Law Practical Law Connect Practical Law Dynamic Tool Set |

Legal know-how, current awareness and workflow tools with embedded guidance from expert practitioners. Practice notes, standard documents, checklists and What’s Market tools cover a wide variety of practice areas such as commercial, corporate, labor and employment, intellectual property, finance and litigation. Practical Law currently has localized product offerings in the United Kingdom, United States, Canada and Australia. Through Practical Law Global and our local Practical Law offerings, we offer our online products and services to customers in markets where we do not have a fully localized service. |

|

|

|||||

CoCounsel CoCounsel Drafting |

Our professional-grade generative AI assistant that is trained by TR domain experts and leverages our TR proprietary content in generating answers to users across the legal, tax, risk & fraud, and media domains. This AI assistant also integrates functionality from other software products across the TR estate, allowing users to navigate seamlessly from one application to another. It also has the capability to integrate customer content directly to help ground the responses in customer proprietary content in addition to TR’s world-class content assets. |

|

|

| ||||

Thomson Reuters Annual Report 2024 |

Page 7 |

Brand |

Type of Product/Service |

Legal Professionals |

Corporates |

Tax & Accounting Professionalss | ||||

CLEAR CLEAR Risk Inform CLEAR ID Confirm CLEAR Adverse Media Sanctions PeopleMap |

Prevent fraud, detect risk and investigate crime with powerful online software. |

|

|

|||||

HighQ |

Cloud-based collaboration and workflow platform for the legal and regulatory market segment. |

|

|

|||||

Case Center |

Cloud-based evidence-sharing platform for sharing documents and multimedia between justice agencies for trial preparation and courtroom presentation. |

|

||||||

Fraud Analytics Fraud Detect ID Risk Analytics Case Tracking |

A suite of data and analytics solutions to help auditors, investigators and managers detect fraud, waste and abuse in healthcare and large government subsidy programs. |

|

|

|||||

Checkpoint Checkpoint Edge (U.S. & Canada) |

Integrated tax, audit and accounting research solution that delivers news, editorial insights, advisory tools, authoritative content and linked primary sources integrated throughout Thomson Reuters workflow productivity tools, applications and software. |

|

|

| ||||

Legal Tracker |

Online spend and matter management, e-billing, legal analytics services and document storage, search and retrieval. |

|

||||||

ONESOURCE |

Global cloud-based tax and trade solutions that reduce risk and regulatory complexity, improving the accuracy of a company’s entire tax or trade lifecycle. Integrating openly with existing technology and ecosystem solutions to manage direct and indirect tax compliance, indirect tax determination, statutory reporting, trust taxation, tax information reporting, tax planning, trade compliance, trade operations, trade special programs, trade regulatory content and overall data and process management. |

|

| |||||

Confirmation |

Cloud-based platform to automate the workflow of the confirmations process of an audit. Used by a global network of audit firms, banks and law firms to increase efficiency and reduce risk. |

|

| |||||

Pagero |

A provider of e-invoicing and continuous transaction controls compliance solutions for the global market. Pagero provides a Smart Business Network that connects buyers and sellers for automated, compliant and secure exchange of orders, invoices, payment instructions and other business documents. |

|

||||||

Dominio |

Accounting management and tax management software solutions for accounting firms and micro and small companies in Brazil. |

| ||||||

| Page 8 | Thomson Reuters Annual Report 2024 |

Brand |

Type of Product/Service |

Legal Professionals |

Corporates |

Tax & Accounting Professionalss | ||||

Cloud Audit Suite |

End-to-end |

| ||||||

UltraTax & CS Professional Suite |

Scalable, integrated suite of desktop and online software applications that encompass key aspects of a professional accounting firm’s operations, from collecting client data and preparing and filing tax returns to the overall management of the accounting practice. |

| ||||||

SafeSend |

Cloud-based software that automates assembly, review, e-signature and secure delivery of tax returns for individuals and entities. |

|

| |||||

SurePrep |

Software and services that automate tax preparation, supporting a digital tax workflow for accounting firms and their clients. Solutions TaxCaddy, 1040SCAN and SPbinder streamline the entire 1040 tax process for tax professionals and taxpayers. |

|

| |||||

Thomson Reuters Annual Report 2024 |

Page 9 |

| Page 10 | Thomson Reuters Annual Report 2024 |

Thomson Reuters Annual Report 2024 |

Page 11 |

By Region |

||||

Americas |

14,100 | |||

Asia Pacific |

8,300 | |||

Europe, Middle East and Africa (EMEA) |

4,000 | |||

By Unit |

||||

Legal Professionals |

700 | |||

Corporates |

1,900 | |||

Tax & Accounting Professionals |

1,300 | |||

Global Print |

800 | |||

Government |

650 | |||

Reuters News |

3,500 | |||

Product & Editorial |

3,300 | |||

Operations & Technology |

9,100 | |||

Corporate Center (Enabling Functions) |

1,300 | |||

Commercial Functions (1) |

1,200 | |||

Other (2) |

2,650 | |||

Thomson Reuters |

26,400 |

| (1) | Reflects employees in Marketing, Commercial Excellence and Strategy. |

| (2) | Reflects employees in our Latin America, Asia and Emerging Markets businesses. |

| Page 12 | Thomson Reuters Annual Report 2024 |

We post a Social Impact & ESG Report annually on our website, www.tr.com/social-impact-report, which summarizes our strategy, includes stories of progress and tracks performance, tying our efforts to our business strategy and commercial expertise. We encourage you to review the Social Impact & ESG Report to gain a better understanding of our accomplishments and practices in these areas. |

Thomson Reuters Annual Report 2024 |

Page 13 |

| Page 14 | Thomson Reuters Annual Report 2024 |

Facility |

Approx. Sq. Ft. |

Owned/Leased |

Principal Use | |||

610 Opperman Drive, Eagan, Minnesota, United States |

1,331,130 | Owned | Global Print operating facility | |||

2900 Ames Crossing Rd. Eagan, Minnesota, United States |

308,070 | Subleased | Legal Professionals operating facility | |||

6300 Interfirst Drive, Ann Arbor, Michigan, United States |

247,210 | Owned | Tax & Accounting Professionals operating facility | |||

Knowledge Court, Bangalore, India |

150,760 | Leased | Thomson Reuters shared services center | |||

5 Canada Square, London, United Kingdom |

133,400 | Subleased | Legal Professionals, Tax & Accounting Professionals and Reuters News operating facility | |||

Hyderabad, Bldg. 11 Madhapur, Hyderabad, India |

130,320 | Leased | Global shared service center | |||

19 Duncan Street Toronto, Ontario, Canada |

129,950 | Leased | Thomson Reuters headquarters | |||

Reforma Cuarzo 26 Paseo de la Reforma, Mexico City, Mexico |

118,200 | Leased | Global shared service center | |||

6160 Warren Parkway Frisco, TX, United States |

56,700 | Leased (1) |

Tax & Accounting Professionals and Corporates operating facility | |||

3 Times Square, New York, New York, United States |

46,100 | Owned/leased (2) |

Reuters News, Legal Professionals and Corporates operating facility | |||

Landis & Gyr 3, Zug, Switzerland |

31,870 | Leased | Enterprise Centre | |||

| (1) | New Tax & Accounting Professionals operating facility lease which replaces former Thomson Reuters-owned Carrolton TX facility. |

| (2) | The landlord (3XSQ Associates) is an entity owned by one of our subsidiaries and Rudin Times Square Associates LLC. 3XSQ Associates was formed to build and operate the 3 Times Square property. |

Thomson Reuters Annual Report 2024 |

Page 15 |

Risk Category |

Page |

|||

| 16 | ||||

| 20 | ||||

| 22 | ||||

| 23 | ||||

| 26 | ||||

| 27 | ||||

• |

We have seen an increase in well-funded new competitors focused on leveraging technological advancements, particularly generative AI, which has reduced barriers to entry. Some of these new entrants also differentiate themselves by being specialized, with a narrower focus than our company, and therefore may be able to adopt and implement newer technology faster than we can or at lower price points. |

• |

The application of generative AI technologies across public sources of free or relatively inexpensive information which is available online increases the competition risk and can diminish the perceived value of packaging this content for our target customers. |

• |

Some of our customers may independently develop products and services that compete with ours, including through the formation of partnerships or consortia. In addition, the growing awareness and understanding of use cases of transformative AI technologies may see us facing displacement from our own customers as they explore internal development of products and services that compete with our offerings. If customers become internally self-sufficient, demand for our products may be reduced. |

• |

Some of our competitors aggressively market their products as a lower cost alternative and offer price incentives to acquire new business. As some of our competitors offer products and services that may be viewed as more cost effective than ours or which may be seen as having greater functionality or performance than ours, the relative value of some of our products or services could be diminished. Competition may require us to reduce the price of some of our products and services (which may result in lower revenues) or make additional capital investments (which might result in lower profit margins). If we are unable or unwilling to reduce prices or make additional investments for some of our products and services in the future, we may lose customers and our financial results may be adversely affected. |

| Page 16 | Thomson Reuters Annual Report 2024 |

• |

Some of our principal competitors are established companies and firms that have substantial financial resources, recognized brands in certain product segments, or have more established positions in certain geographic regions than we do. Some larger companies that compete with us, such as enterprise resource planning companies, have large installed customer bases and may change or expand the focus of their business strategies to target our customers. |

• |

Law firms continue to be challenged by corporate counsels, which are seeking to keep more work in-house to deliver greater business value and insights internally, limit increases in billing rates and hours, and insist on increased transparency and efficiency from law firms. The emergence of generative AI as a tool in the legal space could also have significant impacts on law firms, such as their headcount, service delivery, and pricing. While generative AI introduces productivity and efficiency improvement opportunities for law firms, it also adds uncertainties to how law firms and legal professionals need to evolve with technology in the future. These trends could impact the future ability to spend by a select set of our law firm customers on our products which in turn could adversely affect our revenues as well as our cash flows. |

• |

Accounting firms are also adapting their business models related to service offerings, technology and pricing to address their clients’ evolving needs, priorities and expectations. Amid an ongoing talent shortage and increasing regulatory complexity, accounting firms continue to increase efficiency and automation while ongoing commoditization of tax and audit work is driving expansion into more profitable advisory services. |

• |

Corporations continue to be under pressure to become more efficient and drive margins which may put pressure on their ability to spend on our products. Their behavior is also closely linked to economic cycles with spending pressures tied to periods of economic downturn. Their focus on data privacy and cybersecurity continues to increase, requiring additional security reviews of our products and lengthening sales cycles. Corporations are also focusing on consolidating vendors which adds an additional dimension of competition. |

• |

Relative to our Reuters News business, the media sector continues to transform, with the traditional news agency market under pressure due to audiences’ shift to digital and streaming services. |

• |

We continue to expect revenue declines in our Global Print business as customers migrate to online delivery, which has been compounded by the influence of the virtual and hybrid work environment. |

Thomson Reuters Annual Report 2024 |

Page 17 |

| Page 18 | Thomson Reuters Annual Report 2024 |

Thomson Reuters Annual Report 2024 |

Page 19 |

• |

Cyber-attacks on our own and third-party information technology systems and infrastructure that we rely upon, including without limitation attacks using and incidents arising from computer viruses or other malware, distributed denial of service attacks, ransomware, data theft, phishing, social engineering, destructive attacks against information systems, and other attacks or incidents. This also includes those cyber-attacks and incidents that have in the past resulted in, and could in the future result in, the unauthorized access to, loss, manipulation, destruction of, or disclosure of personal and business information and/or the temporary or sustained unavailability of personal and business information, content, or information technology systems and infrastructure. As technologies like AI develop rapidly, malicious third parties are using these technologies to create new sophisticated attack methods that are increasingly automated, widespread and coordinated making these cyber-attacks more difficult to defend against; |

• |

The introduction or exploitation of vulnerabilities existing in our own and third-party information technology systems and infrastructure, including without limitation the products and services of our key brands and generative AI products and services, some of which may be undetected and only discovered after an extended period of time (including after exploitation) and after installation or integration by our company or our customers. This also includes vulnerabilities in purchased or licensed third-party software, adopted open source software, or in newly integrated technologies resulting from an acquisition or partnership; |

• |

Unauthorized access or attacks obtaining access to sensitive data, including compromise or manipulation of AI, ML and large language model (LLM) solutions embedded in product offerings; |

• |

Actions taken by individuals, groups of hackers, or sophisticated organizations, including without limitation nation-states, state-sponsored, state-aligned, or criminal organizations; |

• |

Attacks on, incidents affecting, or vulnerabilities in underlying cloud service provider environments, communication networks, services, and other technologies or infrastructure that support the Internet, power and water supply, and other utilities, most of which are not under our direct control or the control of our suppliers, partners or customers but can adversely affect our company and our business; |

• |

Insider threats that compromise our security measures, including without limitation malicious acts and human errors by employees, contractors, third-party providers, or others with access to our information technology systems and infrastructure; |

• |

Unauthorized persons could gain access to customer accounts if customers do not maintain effective security or access controls of their systems and software. Inadvertent exposure of data or access to our systems may also be caused by members of our workforce, including by their error or use of AI; and |

• |

Attacks against or incidents involving employee or contractor work from home or hybrid working environments (e.g., home networks, residential internet service providers) that allow an unauthorized party to gain remote or physical access to an employee’s or contractor’s devices or information used to access our information technology systems and infrastructure. |

| Page 20 | Thomson Reuters Annual Report 2024 |

Thomson Reuters Annual Report 2024 |

Page 21 |

• |

Difficulties in penetrating new markets due to established and entrenched competitors or unavailability of local companies for acquisition or joint venture partners or restrictions on foreign ownership; |

• |

Difficulties in developing products and services that are tailored to the needs of local customers; |

• |

Local lack of recognition of our brands or acceptance or knowledge of our products and services; |

• |

The impact of geopolitical tensions in local markets, including the impact of the Russian invasion of Ukraine and related government sanctions and the ongoing Israel-Hamas conflict, potential new tariffs and ongoing protectionism measures due to a decline in global alignment (including retaliatory measures related to the imposition of tariffs), changes in monetary policy, weaker global demand, supply chain disruptions, labour shortages and other events; |

• |

Challenges protecting the safety, security and wellbeing of staff in all locations; |

| Page 22 | Thomson Reuters Annual Report 2024 |

• |

Economic, political or social instability in local markets; |

• |

Exposure to possibly adverse governmental or regulatory actions in countries where we operate or conduct business; |

• |

Higher inflation rates and increased credit risk; |

• |

The impact of foreign currency fluctuations on prices charged to local customers, notably when there is strengthening of the U.S. dollar, and other controls, regulations and orders that might restrict our ability to repatriate cash or limit our ability to move or invest cash freely; |

• |

Difficulties hiring and retaining staff for foreign operations and protecting their safety, differing employee/employer relationships and workplace cultures, and other challenges caused by distance, language and cultural differences; |

• |

Reduced protection for intellectual property rights; |

• |

Changes in laws and policies affecting trade and investment in other jurisdictions; and |

• |

Managing compliance with local laws and regulations (notably related to data privacy, data use and data protection) and varying and sometimes conflicting laws and regulations across the countries in which we do business. |

Thomson Reuters Annual Report 2024 |

Page 23 |

• |

Impose limits on our collection, retention and use of certain kinds of information or data and our ability to communicate such information effectively to our customers; |

• |

Impose limits on our ability to develop and offer our products, services, and content in certain countries; |

• |

Frustrate or disrupt our ability to do business with certain customers and other third parties or collect or pay third parties, including without limitation as a result of newly issued sanctions and export/import restrictions; |

• |

Increase compliance complexity and add more compliance related costs; |

• |

Increase our cost of doing business or require us to change some of our existing products, services or business practices; and |

• |

Conflict or increase complexity on a global basis (such as the U.S. Foreign Corrupt Practices Act, the U.K. Bribery Act and similar laws). |

| Page 24 | Thomson Reuters Annual Report 2024 |

Thomson Reuters Annual Report 2024 |

Page 25 |

| Page 26 | Thomson Reuters Annual Report 2024 |

Thomson Reuters Annual Report 2024 |

Page 27 |

| Page 28 | Thomson Reuters Annual Report 2024 |

|

|

Legal Professionals Serves law firms and governments with research and workflow products powered by leading-edge technologies, including generative AI, focusing on intuitive legal research and integrated legal workflow solutions that combine content, tools and analytics. |

2024 Revenues  | ||

|

Corporates Serves corporations, ranging from small businesses to multinational organizations, including the seven largest global accounting firms, with our full suite of content-driven products, powered by leading-edge technologies, including generative AI, and integrated compliance workflow solutions to help them achieve their business outcomes. | |||

|

Tax & Accounting Professionals Serves tax, audit and accounting firms (other than the seven largest, which are served by our Corporates segment) with research and workflow products powered by leading-edge technologies, including generative AI. | |||

|

Reuters News Supplies business, financial and global news to the world’s media organizations, professionals and news consumers through Reuters News Agency, Reuters.com, Reuters Events, Thomson Reuters products and to financial firms exclusively via LSEG products. | |||

|

|

Global Print Provides legal and tax information primarily in print format to customers around the world and provides commercial printing services to a wide range of book publishers. |

Thomson Reuters Annual Report 2024 |

Page 29 |

Attractive Industry |

Balanced and Diversified Leadership |

Attractive Business Model |

Strong Competitive Positioning |

Disciplined Financial Policies | ||||

• Currently our “Big 3” segments operate in an estimated $28 billion market expected to grow between 8% and 11% over the next 5 years• Legal, Tax & Risk markets are prime for content-driven innovation |

• A leader in key Legal Professionals, Corporates, Tax & Accounting Professionals and News segments• Resilient businesses, historically stable, through periods of macroeconomic uncertainty• Approximately 450,000 customers; largest customer is approximately 5% of revenues* |

• 81% of revenues were recurring in 2024• Fixed cost model supports operating leverage as we grow• Strong and consistent cash generation capabilities |

• Proprietary content plus data and human expertise combined with AI and ML are key differentiators• Products deeply embedded in customers’ daily workflows• 91% retention rate in 2024 |

• Focused and incentivized on organic revenue growth and free cash flow growth• Balance investing in business and returning capital to shareholders• Committed to maintaining investment grade rating with stable capital structure• Significant potential capital capacity affords optionality | ||||

|

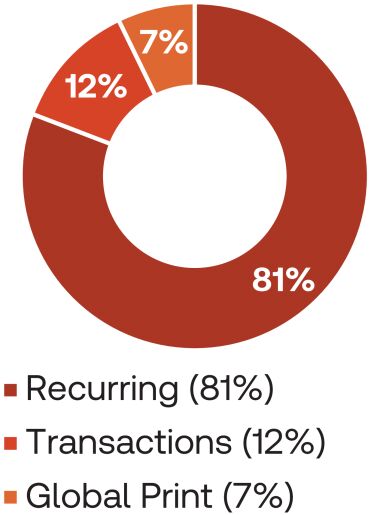

Revenues by type Recurring revenues one-off arrangements. However, as we generally recognize recurring revenues ratably over the contract term, there is a lag in realizing the impact of current sales or cancellations in our reported revenues. As a result, our revenues are typically slower to decline when economic conditions worsen, but slower to return to growth when economic activity improves, compared to other businesses that are not subscription-based.Transactions revenues Global Print revenues | |

|

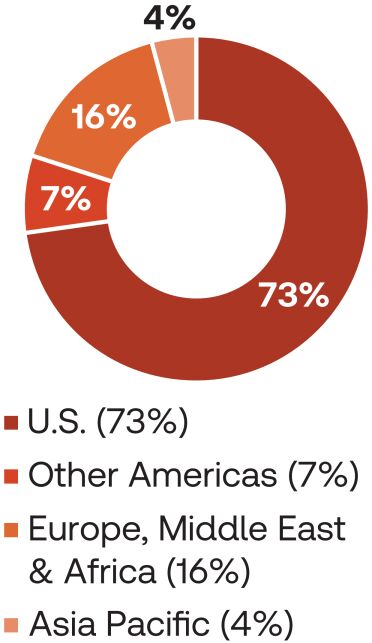

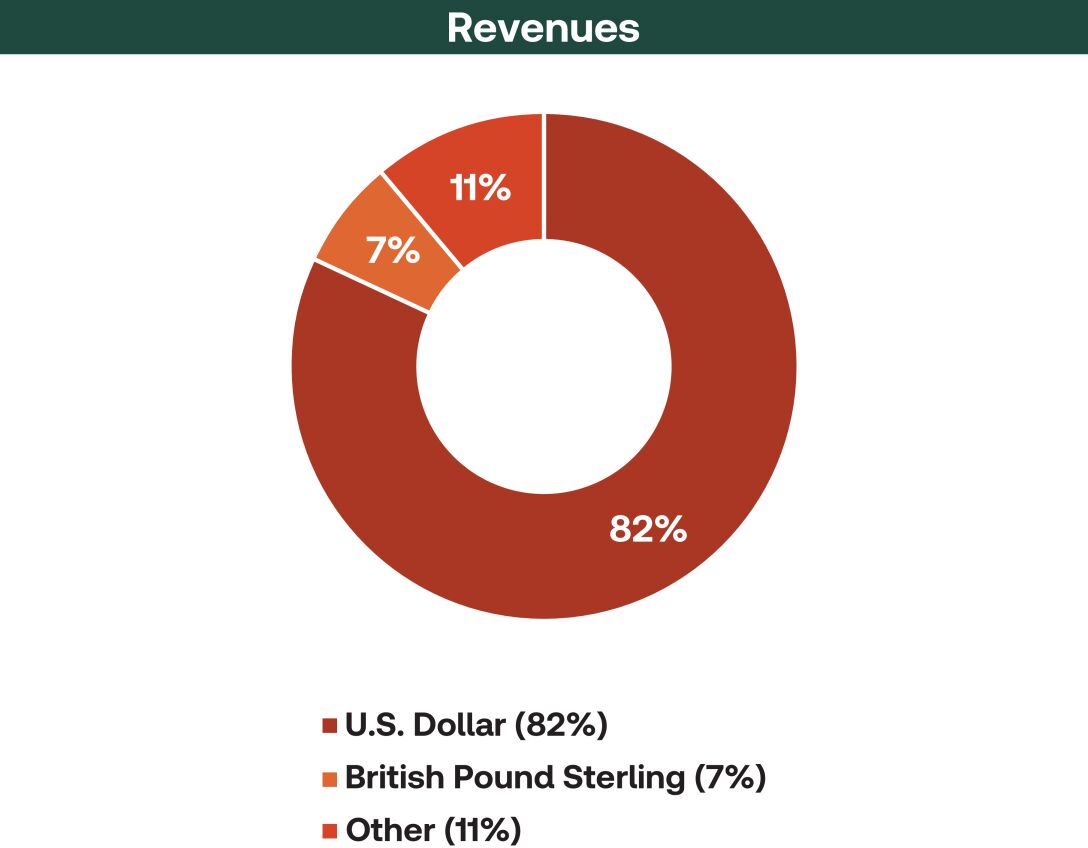

Revenues by geography In 2024, 73% of our revenues were U.S.-based. We also operate regional teams outside of the U.S., including in emerging markets, where we serve regional customers by either modifying existing products and services for their needs or developing specific products for the local market. Changes in foreign currency exchange rates relative to our business outside the U.S. may cause variation in our revenue performance from period to period. In 2024, however, changes in foreign exchange rates had a less than 1% negative impact on our revenue growth compared to the prior year. |

| Page 30 | Thomson Reuters Annual Report 2024 |

|

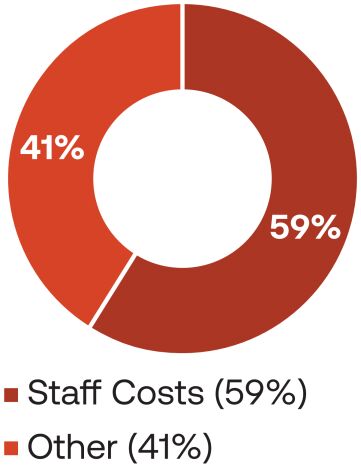

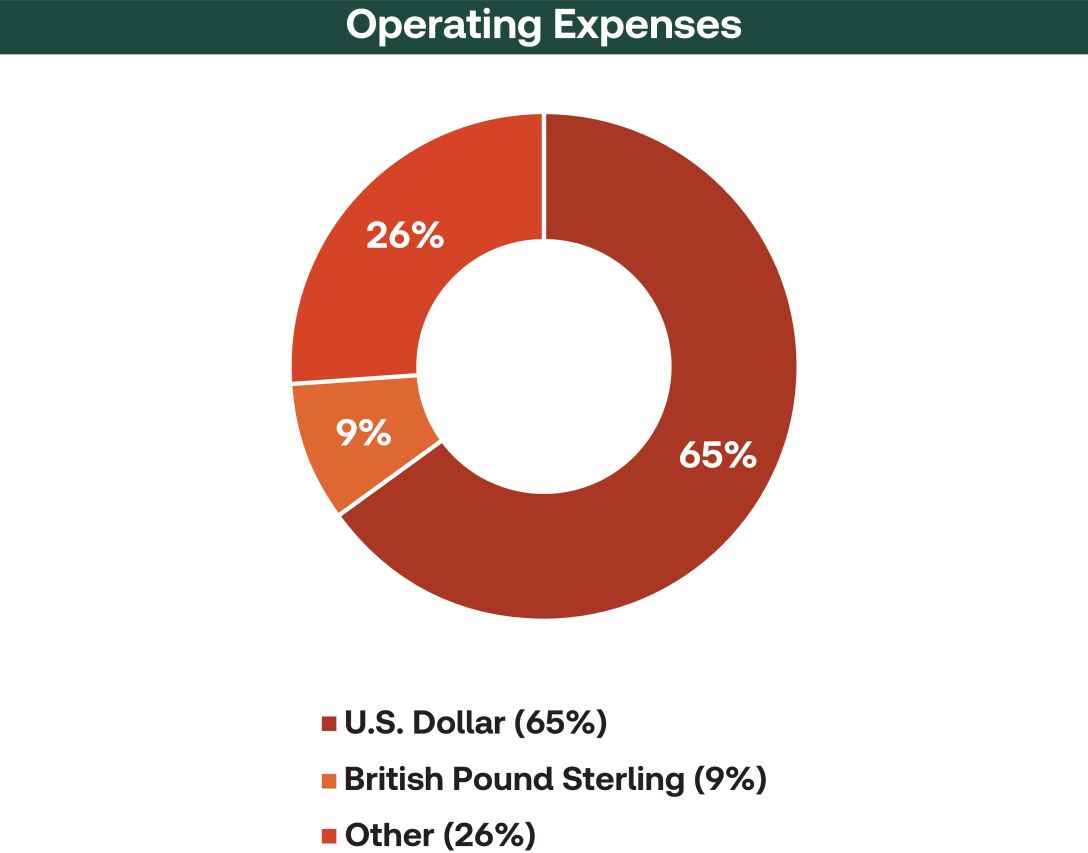

Operating Expenses Most of our expenses are fixed in the short-to-medium |

Thomson Reuters Annual Report 2024 |

Page 31 |

Total Thomson Reuters |

2024 Updated Outlook |

2024 Actual Performance (Before currency) (1) |

||||

Revenue growth |

~7.0% | 7.1% |

✓ | |||

Organic revenue growth ( 2) |

~7.0% |

7.1% |

✓ | |||

Adjusted EBITDA margin (2) |

~38% | 38.1% |

✓ | |||

Corporate costs |

$120-$130 million | $108 million |

✓ | |||

Free cash flow (2) |

~$1.8 billion | $1.8 billion |

✓ | |||

Accrued capital expenditures as a percentage of revenues (2) |

~8.5% | 8.4% |

✓ | |||

Depreciation and amortization of computer software |

$730-$750 million |

$732 million |

✓ | |||

Depreciation and amortization of internally developed software |

$580-$600 million |

$585 million |

✓ | |||

Amortization of acquired software |

~$150 million | $147 million |

✓ | |||

Interest expense |

$125-$145 million |

$125 million |

✓ | |||

Effective tax rate on adjusted earnings (2)(3) |

~18% |

17.9% |

✓ | |||

“Big 3” Segments (2) |

2024 Updated Outlook |

2024 Actual Performance (Before currency) (1) |

||||

Revenue growth |

~8.5% | 8.4% |

✓ | |||

Organic revenue growth |

~8.5% |

8.7% |

✓ | |||

Adjusted EBITDA margin |

~43% |

42.0% |

× | |||

Legend |

||||||

✓ - Achieved or exceeded updated outlook. × - Did not meet updated outlook. |

• |

January 2024: Pagero, a global leader in e-invoicing and indirect tax solutions; |

• |

January 2024: World Business Media Limited (The Insurer), a cross-platform and subscription-based provider of editorial coverage for the global P&C and specialty (re)insurance industry; |

• |

August 2024: Safe Sign Technologies, a U.K.-based startup that is developing legal-specific large language models; and |

• |

October 2024: Credere Technologies, Inc., doing business as Materia, a U.S.-based startup that specializes in the development of an agentic AI assistant for the tax, audit and accounting profession. |

| Page 32 | Thomson Reuters Annual Report 2024 |

• |

January 2023: SurePrep LLC, a provider of tax automation software and services; |

• |

July 2023: Imagen Ltd, a media asset management company now part of our Reuters News segment; and |

• |

August 2023: Casetext, a business that uses AI and ML to enable legal professionals to work more efficiently. |

Year ended December 31, |

||||||||||||||||

Change |

||||||||||||||||

(millions of U.S. dollars, except per share amounts and margins) |

2024 |

2023 |

Total |

Constant Currency |

||||||||||||

| IFRS Financial Measures | ||||||||||||||||

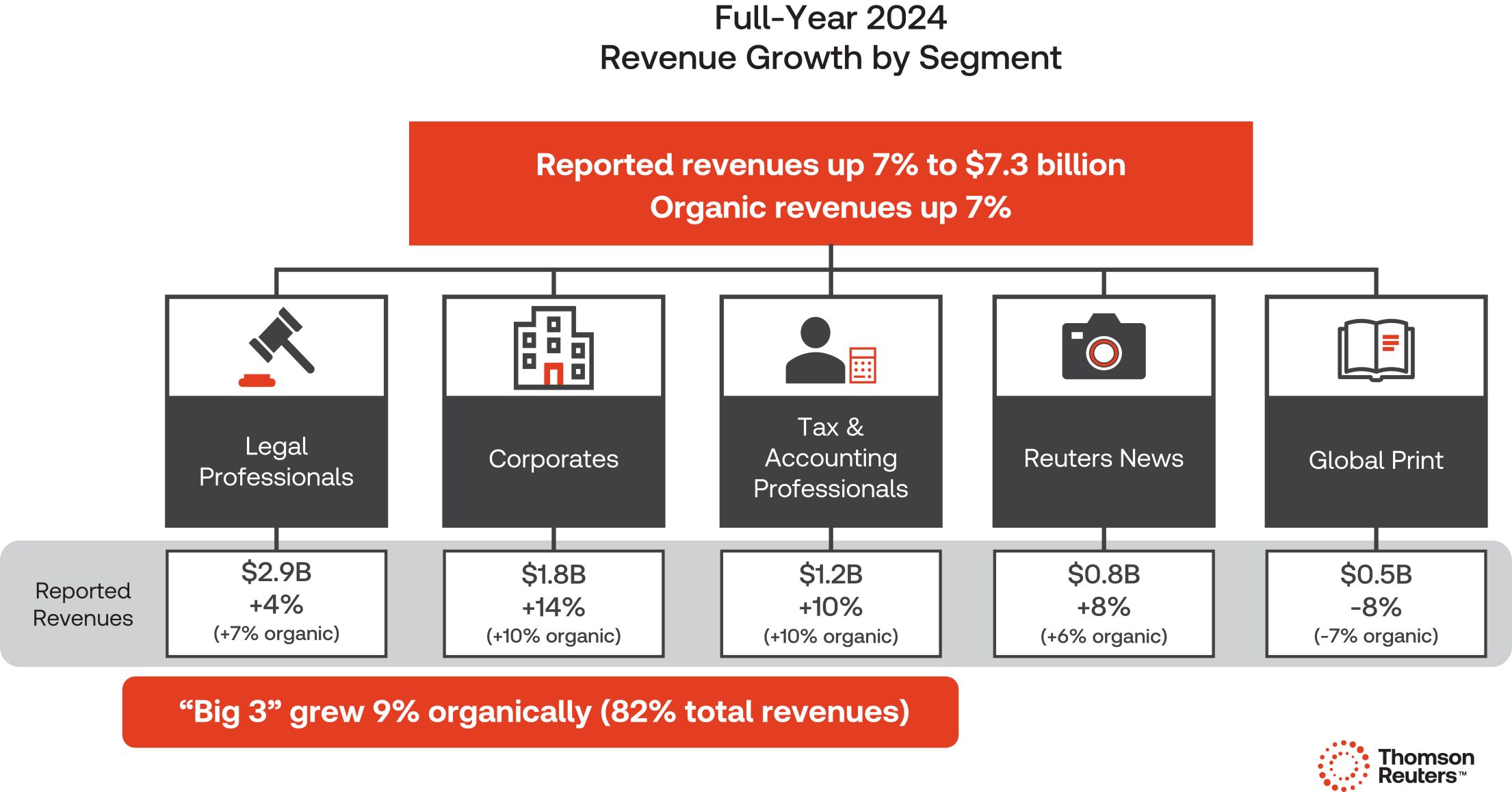

| Revenues | 7,258 |

6,794 | 7% | |||||||||||||

| Operating profit | 2,109 |

2,332 | (10%) | |||||||||||||

| Diluted EPS | $4.89 |

$5.80 | (16%) | |||||||||||||

Non-IFRS Financial Measures |

||||||||||||||||

| Revenues | 7,258 |

6,794 | 7% | 7% | ||||||||||||

Organic revenue growth |

7% |

|||||||||||||||

| Adjusted EBITDA | 2,779 |

2,678 | 4% | 4% | ||||||||||||

| Adjusted EBITDA margin | 38.2% |

39.3% | (110)bp | (130)bp | ||||||||||||

| Adjusted EBITDA less accrued capital expenditures | 2,170 |

2,146 | 1% | |||||||||||||

| Adjusted EBITDA less accrued capital expenditures margin | 29.9% |

31.5% | (160)bp | |||||||||||||

| Adjusted EPS | $3.77 |

$3.51 | 7% | 7% | ||||||||||||

| “Big 3” Segments | ||||||||||||||||

| Revenues | 5,931 |

5,485 | 8% | 8% | ||||||||||||

Organic revenue growth |

9% |

|||||||||||||||

| Adjusted EBITDA | 2,500 |

2,408 | 4% | 4% | ||||||||||||

| Adjusted EBITDA margin | 42.1% |

43.8% | (170)bp | (180)bp | ||||||||||||

Thomson Reuters Annual Report 2024 |

Page 33 |

Year ended December 31, | ||||||||||

Change | ||||||||||

(millions of U.S. dollars) |

2024 |

2023 |

Total |

Constant Currency |

Organic | |||||

Recurring revenues |

5,882 |

5,458 | 8% | 8% | 8% | |||||

Transactions revenues |

857 |

774 | 11% | 11% | 10% | |||||

Global Print revenues |

519 |

562 | (8%) | (7%) | (7%) | |||||

Revenues |

7,258 |

6,794 | 7% | 7% | 7% | |||||

Year ended December 31, |

||||||||||||||||

Change |

||||||||||||||||

(millions of U.S. dollars) |

2024 |

2023 |

Total |

Constant Currency |

||||||||||||

Operating expenses |

4,471 |

4,134 | 8% | 9% | ||||||||||||

Remove fair value adjustments (1) |

17 |

(2) | ||||||||||||||

Operating expenses excluding fair value adjustments |

4,488 |

4,132 | 9% | 9% | ||||||||||||

| (1) | Fair value adjustments primarily represent gains or losses due to changes in foreign currency exchange rates on intercompany balances that arise in the ordinary course of business. |

| Page 34 | Thomson Reuters Annual Report 2024 |

Year ended December 31, | ||||||

(millions of U.S. dollars) |

2024 |

2023 |

Change | |||

Depreciation |

113 |

116 | (2%) | |||

Amortization of computer software |

||||||

Internally developed |

471 |

440 | 7% | |||

Acquisition related |

147 |

72 | 104% | |||

Total amortization of computer software |

618 |

512 | 21% | |||

Amortization of other identifiable intangible assets |

91 |

97 | (6%) | |||

• |

Depreciation decreased primarily due to assets acquired in previous years becoming fully depreciated. |

• |

Total amortization of computer software increased primarily due to acquisitions, and to a lesser extent, internal product development. |

• |

Amortization of other identifiable intangible assets decreased as the completion of amortization of assets acquired in previous years more than offset expenses associated with recent acquisitions. |

Year ended December 31, |

||||||||

(millions of U.S. dollars) |

2024 |

|||||||

Other operating gains, net |

144 |

397 | ||||||

Year ended December 31, | ||||||

(millions of U.S. dollars) |

2024 |

2023 |

Change | |||

Net interest expense |

125 |

152 | (18%) | |||

Year ended December 31, |

||||||||

(millions of U.S. dollars) |

2024 |

2023 |

||||||

Other finance income (costs) |

45 |

(192 | ) | |||||

Thomson Reuters Annual Report 2024 |

Page 35 |

Year ended December 31, |

||||||||

(millions of U.S. dollars) |

2024 |

|||||||

YPL |

68 |

1,099 | ||||||

Other equity method investments |

(28) |

(24) | ||||||

Share of post-tax earnings in equity method investments |

40 |

1,075 | ||||||

Year ended December 31, |

||||||||

(millions of U.S. dollars) |

2024 (1) |

2023 |

||||||

(Decrease) increase in LSEG share price |

(86) |

785 | ||||||

Foreign exchange (losses) gains on LSEG shares |

(3) |

251 | ||||||

Dividend income |

6 |

58 | ||||||

Loss from forward contract |

- |

(77) | ||||||

Gain (loss) from call options |

22 |

(15) | ||||||

Historical excluded equity adjustment (2) |

129 |

97 | ||||||

YPL – Share of post-tax earnings in equity method investments |

68 |

1,099 | ||||||

| (1) | Activity through May 2024, when the investment was fully divested. |

| (2) | Represents income from the recognition of the remaining cumulative impact of equity transactions that were excluded from our investment in YPL. |

Year ended December 31, |

||||||||

(millions of U.S. dollars) |

2024 |

2023 |

||||||

Tax (benefit) expense |

(123 |

) |

417 | |||||

| Page 36 | Thomson Reuters Annual Report 2024 |

Year ended December 31, |

||||||||

(millions of U.S. dollars) |

2024 |

|||||||

(Benefit) expense |

||||||||

Tax items impacting comparability: |

||||||||

| Recognition of deferred tax asset (1) |

(468) |

- | ||||||

| Discrete changes to uncertain tax positions (2) |

(15) |

(61) | ||||||

| Corporate tax laws and rates (3) |

7 |

(100) | ||||||

| Deferred tax adjustments (4) |

(2) |

(11) | ||||||

| Subtotal | (478) |

(172) | ||||||

Tax related to: |

||||||||

| Amortization of acquired computer software | (33) |

(17) | ||||||

| Amortization of other identifiable intangible assets | (22) |

(22) | ||||||

| Other operating gains, net | 56 |

81 | ||||||

| Other finance income (costs) | (19) |

(31) | ||||||

| Share of post-tax earnings in equity method investments |

7 |

253 | ||||||

| Other items | 2 |

1 | ||||||

| Subtotal | (9) |

265 | ||||||

Total |

(487) |

93 | ||||||

| (1) | Relates to new tax legislation enacted in Canada. |

| (2) | In 2024, relates to the release of tax reserves that are no longer required due to the settlement of a tax dispute. In 2023, relates to tax reserves no longer required due to the expiration of statutes of limitation. |

| (3) | Relates primarily to adjustments to deferred tax balances due to changes in the applicable statutory tax rate in a jurisdiction outside of the U.S. and adjustments to deferred tax balances due to changes in effective state tax rates. |

| (4) | Relates primarily to adjustments to deferred tax assets attributable to a non-U.S. subsidiary. |

Year ended December 31, |

||||||||

(millions of U.S. dollars) |

2024 |

|||||||

Tax (benefit) expense |

(123) |

417 | ||||||

| Remove: Items from above impacting comparability | 487 |

(93) | ||||||

Total tax expense on adjusted earnings |

364 |

324 | ||||||

Year ended December 31, |

||||||||

Income taxes paid (millions of U.S. dollars) |

2024 |

|||||||

Operating activities – continuing operations |

234 |

163 | ||||||

Investing activities – continuing operations |

317 |

705 | ||||||

Investing activities – discontinued operations |

- |

1 | ||||||

Total income taxes paid |

551 |

869 | ||||||

Thomson Reuters Annual Report 2024 |

Page 37 |

Year ended December 31, |

||||||||

(millions of U.S. dollars) |

2024 |

|||||||

Earnings from discontinued operations, net of tax |

15 |

49 | ||||||

Year ended December 31, |

||||||||||||||||

Change |

||||||||||||||||

(millions of U.S. dollars, except per share amounts) |

2024 |

2023 |

Total |

Constant Currency |

||||||||||||

IFRS Financial Measures |

||||||||||||||||

| Net earnings | 2,207 |

2,695 | (18%) | |||||||||||||

| Diluted EPS | $4.89 |

$5.80 | (16%) | |||||||||||||

Non- IFRS Financial Measures |

||||||||||||||||

| Adjusted earnings | 1,701 |

1,629 | 4% | |||||||||||||

| Adjusted EPS | $3.77 |

$3.51 | 7% | 7% | ||||||||||||

Year ended December 31, | ||||||||||

Change | ||||||||||

(millions of U.S. dollars, except margins) |

2024 |

2023 |

Total |

Constant Currency |

Organic | |||||

Recurring revenues |

2,828 |

2,674 | 6% | 6% | 8% | |||||

Transactions revenues |

94 |

133 | (29%) | (28%) | (2%) | |||||

Revenues |

2,922 |

2,807 | 4% | 4% | 7% | |||||

Segment adjusted EBITDA |

1,302 |

1,299 | - | - | ||||||

Segment adjusted EBITDA margin |

44.6% |

46.2% | (160)bp | (180)bp | ||||||

| Page 38 | Thomson Reuters Annual Report 2024 |

Year ended December 31, | ||||||||||

Change | ||||||||||

(millions of U.S. dollars, except margins) |

2024 |

2023 |

Total |

Constant Currency |

Organic | |||||

Recurring revenues |

1,543 |

1,373 | 12% | 13% | 10% | |||||

Transactions revenues |

301 |

247 | 22% | 22% | 11% | |||||

Revenues |

1,844 |

1,620 | 14% | 14% | 10% | |||||

Segment adjusted EBITDA |

671 |

619 | 8% | 8% | ||||||

Segment adjusted EBITDA margin |

36.3% |

38.1% | (180)bp | (220)bp | ||||||

Year ended December 31, | ||||||||||

Change | ||||||||||

(millions of U.S. dollars, except margins) |

2024 |

2023 |

Total |

Constant Currency |

Organic | |||||

Recurring revenues |

867 |

808 | 7% | 9% | 9% | |||||

Transactions revenues |

298 |

250 | 19% | 19% | 14% | |||||

Revenues |

1,165 |

1,058 | 10% | 11% | 10% | |||||

Segment adjusted EBITDA |

527 |

490 | 8% | 9% | ||||||

Segment adjusted EBITDA margin |

45.2% |

45.8% | (60)bp | (50)bp | ||||||

Thomson Reuters Annual Report 2024 |

Page 39 |

Year ended December 31, | ||||||||||

Change | ||||||||||

(millions of U.S. dollars, except margins) |

2024 |

2023 |

Total |

Constant Currency |

Organic | |||||

Recurring revenues |

668 |

625 | 7% | 7% | 5% | |||||

Transactions revenues |

164 |

144 | 14% | 13% | 9% | |||||

Revenues |

832 |

769 | 8% | 8% | 6% | |||||

Segment adjusted EBITDA |

196 |

172 | 14% | 16% | ||||||

Segment adjusted EBITDA margin |

23.6% |

22.4% | 120bp | 150bp | ||||||

Year ended December 31, | ||||||||||

Change | ||||||||||

(millions of U.S. dollars, except margins) |

2024 |

2023 |

Total |

Constant Currency |

Organic | |||||

Revenues |

519 |

562 | (8%) | (7%) | (7%) | |||||

Segment adjusted EBITDA |

188 |

213 | (12%) | (12%) | ||||||

Segment adjusted EBITDA margin |

36.2% |

38.0% | (180)bp | (180)bp | ||||||

Year ended December 31, |

||||||||

(millions of U.S. dollars) |

2024 |

2023 |

||||||

Corporate costs |

105 |

115 | ||||||

| Page 40 | Thomson Reuters Annual Report 2024 |

Three months ended December 31, | ||||||||

Change | ||||||||

(millions of U.S. dollars, except per share amounts and margins) |

2024 |

2023 |

Total |

Constant Currency | ||||

IFRS Financial Measures |

||||||||

| Revenues | 1,909 |

1,815 | 5% | |||||

| Operating profit | 722 |

558 | 29% | |||||

| Net earnings | 587 |

678 | (14%) | |||||

| Diluted EPS | $1.30 |

$1.49 | (13%) | |||||

| Net cash provided by operating activities | 564 |

705 | (20%) | |||||

| Net cash used in investing activities | (69) |

(223) | (71%) | |||||

| Net cash used in financing activities | (252) |

(1,702) | (85%) | |||||

Non-IFRS Financial Measures(1) |

||||||||

| Revenues | 1,909 |

1,815 | 5% | 5% | ||||

| Organic revenue growth |

5% | |||||||

| Adjusted EBITDA | 718 |

707 | 2% | 1% | ||||

| Adjusted EBITDA margin | 37.6% |

38.9% | (130)bp | (160)bp | ||||

| Adjusted EBITDA less accrued capital expenditures | 546 |

554 | (1%) | |||||

| Adjusted EBITDA less accrued capital expenditures margin | 28.6% |

30.5% | (190)bp | |||||

| Adjusted earnings | 454 |

446 | 2% | |||||

| Adjusted EPS | $1.01 |

$0.98 | 3% | 1% | ||||

| Free cash flow | 425 |

613 | (31%) | |||||

| “Big 3” Segments | ||||||||

| Revenues | 1,553 |

1,446 | 7% | 7% | ||||

| Organic revenue growth | 8% | |||||||

| Adjusted EBITDA | 648 |

624 | 4% | 3% | ||||

| Adjusted EBITDA margin | 41.7% |

43.1% | (140)bp | (190)bp | ||||

| (1) | Refer to Appendices A and B of this management’s discussion and analysis for additional information and reconciliations of our non-IFRS financial measures to the most directly comparable IFRS financial measures. |

Thomson Reuters Annual Report 2024 |

Page 41 |

| Page 42 | Thomson Reuters Annual Report 2024 |

Three months ended December 31, | ||||||||||

Change | ||||||||||

(millions of U.S. dollars, except margins) |

2024 |

2023 |

Total |

Constant Currency (1) |

Organic (1) | |||||

Revenues |

||||||||||

| Legal Professionals | 729 |

700 | 4% | 4% | 7% | |||||

| Corporates | 458 |

402 | 14% | 15% | 10% | |||||

| Tax & Accounting Professionals | 366 |

344 | 6% | 7% | 7% | |||||

| “Big 3” Segments Combined (1) |

1,553 |

1,446 | 7% | 7% | 8% | |||||

| Reuters News | 218 |

220 | (1%) | (1%) | (3%) | |||||

| Global Print | 144 |

154 | (6%) | (6%) | (6%) | |||||

| Eliminations/ Rounding | (6) |

(5) | ||||||||

Revenues |

1,909 |

1,815 | 5% | 5% | 5% | |||||

Adjusted EBITDA (1) |

||||||||||

| Legal Professionals | 299 |

298 | - | (1%) | ||||||

| Corporates | 153 |

138 | 11% | 8% | ||||||

| Tax & Accounting Professionals | 196 |

188 | 4% | 5% | ||||||

| “Big 3” Segments Combined | 648 |

624 | 4% | 3% | ||||||

| Reuters News | 45 |

61 | (26%) | (26%) | ||||||

| Global Print | 55 |

55 | (1%) | (1%) | ||||||

| Corporate costs | (30) |

(33) | ||||||||

Adjusted EBITDA |

718 |

707 | 2% | 1% | ||||||

Adjusted EBITDA margin (1) |

||||||||||

| Legal Professionals | 41.0% |

42.5% | (150)bp | (200)bp | ||||||

| Corporates | 33.5% |

34.5% | (100)bp | (190)bp | ||||||

| Tax & Accounting Professionals | 53.4% |

54.6% | (120)bp | (90)bp | ||||||

| “Big 3” Segments Combined | 41.7% |

43.1% | (140)bp | (190)bp | ||||||

| Reuters News | 20.8% |

27.9% | (710)bp | (670)bp | ||||||

| Global Print | 38.2% |

36.4% | 180bp | 190bp | ||||||

Adjusted EBITDA margin |

37.6% |

38.9% | (130)bp | (160)bp | ||||||

| (1) | Refer to Appendices A and B of this management’s discussion and analysis for additional information and reconciliations of our non-IFRS financial measures to the most directly comparable IFRS financial measures. |

Thomson Reuters Annual Report 2024 |

Page 43 |

| Page 44 | Thomson Reuters Annual Report 2024 |

Year ended December 31, | ||||||

(millions of U.S. dollars) |

2024 |

2023 |

$ Change | |||

Net cash provided by operating activities |

2,457 |

2,341 | 116 | |||

Net cash provided by investing activities |

680 |

3,513 | (2,833) | |||

Net cash used in financing activities |

(2,459) |

(5,626) | 3,167 | |||

Translation adjustments |

(8) |

1 | (9) | |||

Increase in cash and cash equivalents |

670 |

229 | 441 | |||

Cash and cash equivalents at beginning of period |

1,298 |

1,069 | 229 | |||

Cash and cash equivalents at end of period |

1,968 |

1,298 | 670 | |||

Non-IFRS Financial Measure(1): |

||||||

Free cash flow |

1,828 |

1,871 | (43) | |||

| (1) | Refer to Appendices A and B of this management’s discussion and analysis for additional information and reconciliations of our non-IFRS financial measures to the most directly comparable IFRS financial measures. |

Thomson Reuters Annual Report 2024 |

Page 45 |

• |

Commercial paper program. |

• |

Credit facility. |

We guarantee borrowings by our subsidiaries under the credit facility. We must also maintain a ratio of net debt as defined in the credit agreement (total debt after swaps less cash and cash equivalents) as of the last day of each fiscal quarter to EBITDA as defined in the credit agreement (earnings before interest, income taxes, depreciation and amortization and other modifications described in the credit agreement) for the last four quarters ended of not more than 4.5:1. If we complete an acquisition with a purchase price of over $500 million, we may elect, subject to notification, to temporarily increase the ratio of net debt to EBITDA to 5.0:1 at the end of the quarter within which the transaction closed and for each of the three immediately following fiscal quarters. At the end of that period, the ratio would revert to 4.5:1. As of December 31, 2024, we complied with this covenant as our ratio of net debt to EBITDA, as calculated under the terms of our syndicated credit facility, was 0.3:1. |

• |

Long-term debt |

| Page 46 | Thomson Reuters Annual Report 2024 |

In June 2024, we filed a new base shelf prospectus pursuant to which Thomson Reuters Corporation (TRC) and one of its U.S. subsidiaries, TR Finance LLC (TR Finance), may collectively issue up to $3.0 billion of unsecured debt securities from time to time through July 19, 2026. Any debt securities issued by TR Finance LLC will be fully and unconditionally guaranteed on an unsecured basis by TRC and three U.S. subsidiary guarantors, which are also indirect 100%-owned and consolidated subsidiaries of TRC. Except for TR Finance and the subsidiary guarantors, none of Thomson Reuters Corporation’s other subsidiaries have guaranteed or would otherwise become obligated with respect to any issued TR Finance debt securities. As of December 31, 2024, neither TRC nor TR Finance have issued any debt securities under the prospectus. Please refer to Appendix G of this management’s discussion and analysis for condensed consolidating financial information of the Company, including TR Finance and the subsidiary guarantors. |

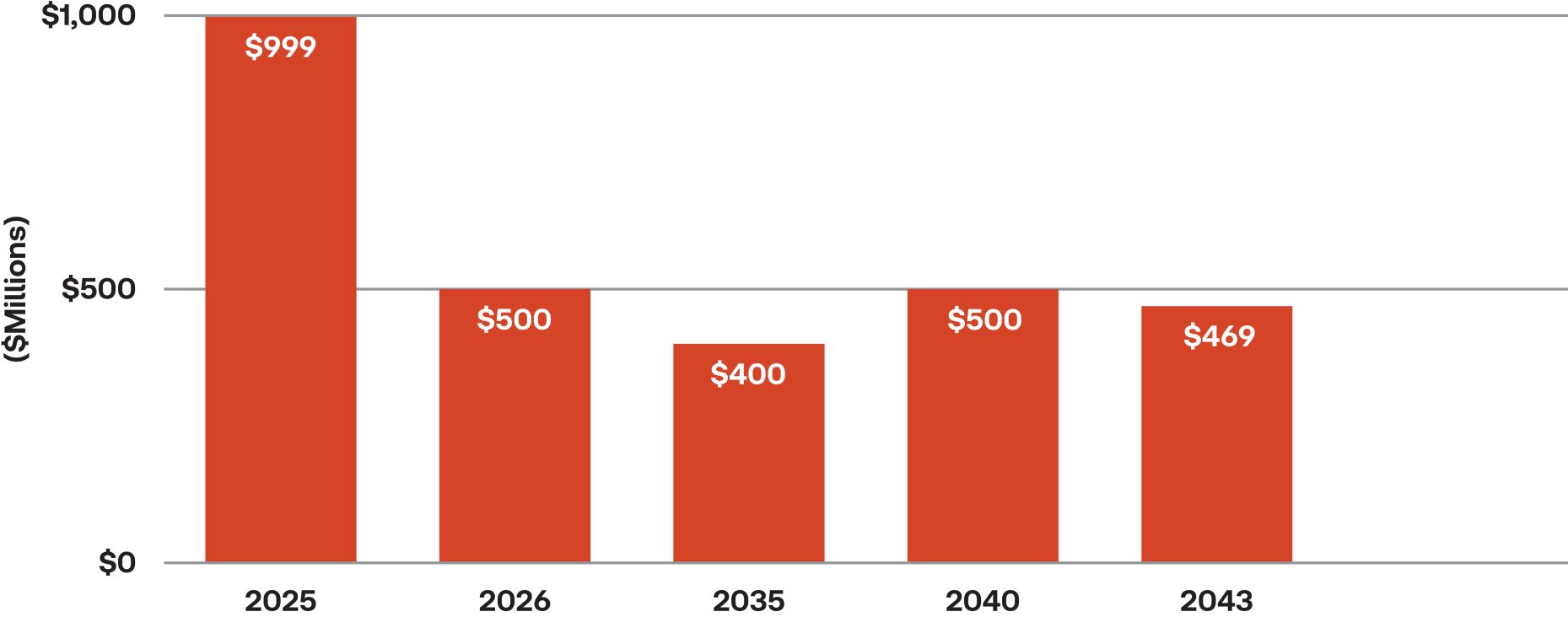

On February 11, 2025, we commenced offers to exchange any or all validly tendered and accepted notes of TRC of the series of notes below for new notes issued by TR Finance, an indirect 100% owned U.S. subsidiary of TRC in order to optimize the Thomson Reuters group capital structure, align revenue generation to indebtedness, and give existing holders of the existing notes the option to receive notes issued by TR Finance with the same financial terms and substantially similar covenants as the applicable series of the existing notes: |

• |

$500 million 3.35% Notes due 2026; |

• |

$500 million 5.85% Notes due 2040; |

• |

$119 million 4.50% Notes due 2043; |

• |

$350 million 5.65% Notes due 2043; and |

• |

$400 million 5.50% Debentures due 2035. |

The exchange offers will not have a significant impact on our annual interest expense and will not change our debt maturity profile. Following completion of the exchange offers, we plan to update our base shelf prospectus to reflect the finalized terms of the TR Finance indenture and the guarantee of the TRC notes by the three U.S. subsidiary guarantors. |

• |

Credit ratings. |

In May 2024, S&P Global Ratings upgraded our long-term debt to BBB+ from BBB. |

The following table sets forth the credit ratings from rating agencies in respect of our outstanding securities as of the date of this management’s discussion and analysis: |

Moody’s |

S&P Global Ratings |

DBRS Limited |

Fitch | |||||

Long-term debt |

Baa1 | BBB+ | BBB (high) | BBB+ | ||||

Commercial paper |

P-2 |

A-2 |

R-2 (high) |

F1 | ||||

Trend/Outlook |

Stable | Stable | Stable | Stable | ||||

These credit ratings are not recommendations to purchase, hold, or sell securities and do not address the market price or suitability of a specific security for a particular investor. Credit ratings may not reflect the potential impact of all risks on the value of securities. We cannot ensure that our credit ratings will not be lowered in the future or that rating agencies will not issue adverse commentaries regarding our securities. |

• |

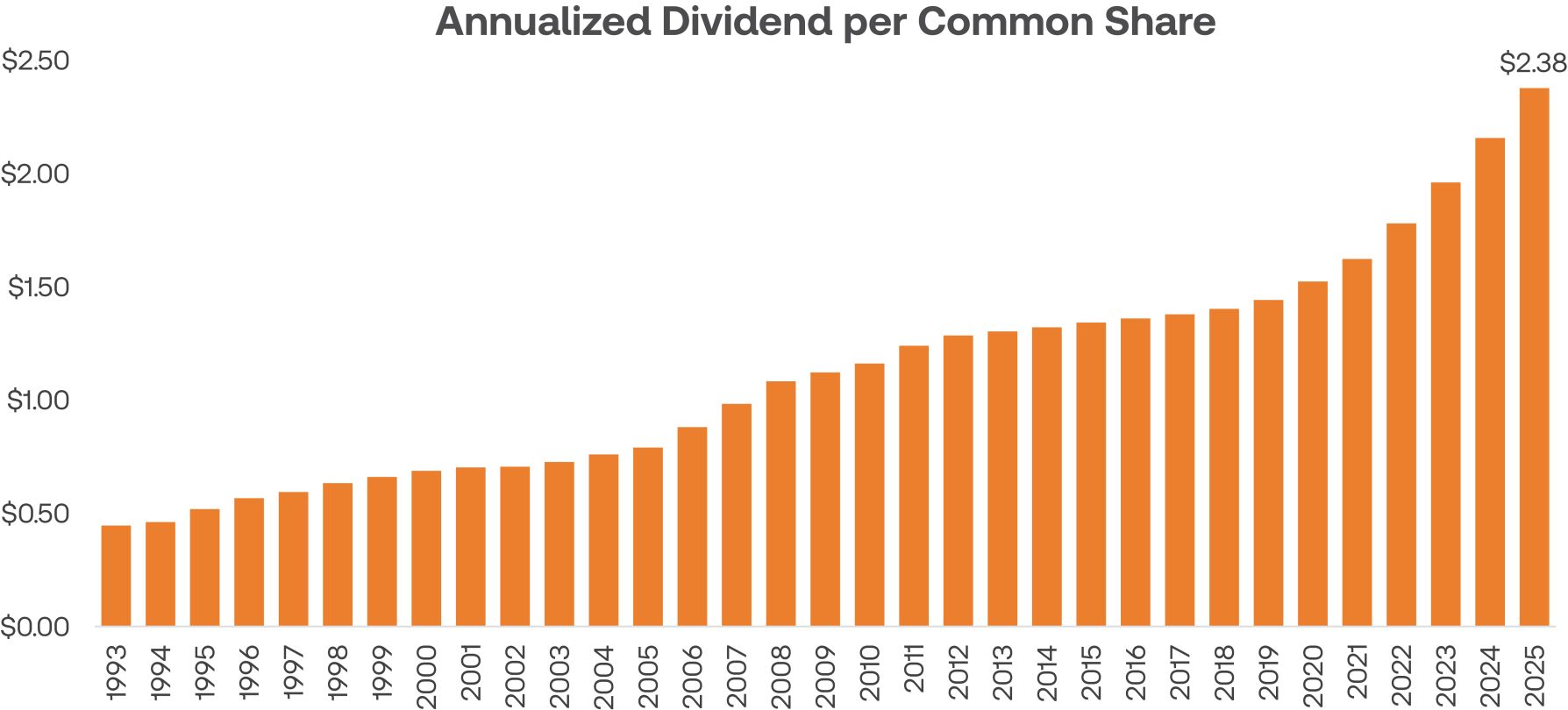

Dividends. |

Details of dividends declared per common share and dividends paid on common shares are as follows: |

Year ended December 31, | ||||

(millions of U.S. dollars, except per share amounts) |

2024 |

2023 | ||

Dividends declared per common share |

$2.16 |

$1.96 | ||

Dividends declared |

973 |

908 | ||

Dividends reinvested |

(29) |

(21) | ||

Dividends paid |

944 |

887 | ||

In February 2025, we announced a 10% or $0.22 per share increase in the annualized dividend rate to $2.38 per common share (beginning with the common share dividend that we plan to pay in March 2025). See the “Subsequent Events” section of this management’s discussion and analysis for additional information. |

Thomson Reuters Annual Report 2024 |

Page 47 |

• |

Share repurchases - Normal Course Issuer Bid (NCIB). |

Year ended December 31, | ||||

2024 |

2023 | |||

Share repurchases (millions of U.S. dollars) |

639 |

1,079 | ||

Shares repurchased (number in millions) |

4.1 |

8.6 | ||

Share repurchases – average price per share |

$156.92 |

$125.07 | ||

From time to time when we do not possess material nonpublic information about ourselves or our securities, we may enter into a pre-defined plan with our broker to allow for the repurchase of shares at times when we ordinarily would not be active in the market due to our own internal trading blackout periods, insider trading rules or otherwise. Any such plans entered into with our broker will be adopted in accordance with applicable Canadian securities laws and the requirements of Rule 10b5-1 under the U.S. Securities Exchange Act of 1934, as amended. |

• |

Return of capital and share consolidation. pre-consolidated share for 0.963957 post-consolidated shares. Shareholders who were subject to income tax in a jurisdiction other than Canada were given the opportunity to opt-out of the transaction. The share consolidation was proportional to the cash distribution and the share consolidation ratio was based on the volume weighted-average trading price of the shares on the New York Stock Exchange (NYSE), the stock exchange on which our shares were listed at the time (see the “Subsequent Events” section of this management’s discussion and analysis for additional information) for the five-trading day period immediately preceding June 23, 2023, the effective date for the return of capital transaction. Woodbridge, our principal shareholder, participated in this transaction. As a result of the share consolidation, our company’s outstanding common shares were reduced by 15.8 million common shares. |

December 31, | ||||

(millions of U.S. dollars) |

2024 |

2023 | ||

Net debt (1) |

1,156 |

2,207 | ||

Leverage ratio of net debt to adjusted EBITDA: |

||||

Adjusted EBITDA (1) |

2,779 |

2,678 | ||

Net debt/adjusted EBITDA (1) |

0.4:1 |

0.8:1 | ||

| (1) | Represent non-IFRS financial measures. Refer to Appendices A and B of this management’s discussion and analysis for additional information and reconciliations of our non-IFRS financial measures to the most directly comparable IFRS financial measures. |

| Page 48 | Thomson Reuters Annual Report 2024 |

|

|

Thomson Reuters Annual Report 2024 |

Page 49 |

(millions of U.S. dollars) |

2025 |

2026 |

2027 |

2028 |

2029 |

Thereafter |

Total | |||||||

Notes/debentures (1) |

973 | 500 | - | - | - | 1,369 | 2,842 | |||||||

Interest payable (1) |

104 | 84 | 76 | 76 | 76 | 791 | 1,207 | |||||||

Debt-related hedges outflows (2) |

1,011 | - | - | - | - | - | 1,011 | |||||||

Debt-related hedges inflows (1) |

(984) | - | - | - | - | - | (984) | |||||||

Lease obligations (3) |

74 | 61 | 47 | 37 | 31 | 127 | 377 | |||||||

Unconditional purchase obligations |

479 | 267 | 92 | 34 | 7 | 4 | 883 | |||||||

Defined benefit obligations |

33 | - | - | - | - | - | 33 | |||||||

Total |

1,690 | 912 | 215 | 147 | 114 | 2,291 | 5,369 | |||||||

| (1) | Represents contractual cash flows calculated using spot foreign exchange rates as of December 31, 2024. |

| (2) | Represents contractual U.S. dollar cash flows. |

| (3) | Includes leases with a term of 12 months or less, certain low-value assets and lease commitments that have not commenced, all of which are not recognized in the consolidated statement of financial position. |

• |

Subsidiary guarantees |

• |

Guarantees |

• |

Unconditional purchase obligations |

• |

Defined benefit obligations |

The amount and timing of any future required contributions to pension plans could differ significantly from our estimates as of December 31, 2024. We cannot estimate contributions beyond 2025 because they depend on future economic conditions, plan performance and potential future government legislation. For certain plans, the trustees have the right to call for special valuations, which could subsequently result in us having to make an unexpected contribution. Additionally, from time to time, we may elect to make voluntary contributions to improve the funded status of the plans. |

• |

Disposition contingencies |

| Page 50 | Thomson Reuters Annual Report 2024 |

Thomson Reuters Annual Report 2024 |

Page 51 |

• |

Legal Professionals: |

• |

Corporates: |

• |

Tax & Accounting Professionals: on-premises tax, audit, accounting, and practice management systems are gradually being replaced by cloud-based offerings. |

| Page 52 | Thomson Reuters Annual Report 2024 |

• |

Continue evolving our transformative AI capabilities through ongoing product innovation and enhancements to our flagship products |

• |

Continue to roll out our AI assistant, CoCounsel, across our customer base |

• |

Maintain and build on our deep domain expertise and comprehensive collection of richly enhanced data and content |

• |

Further enhance our go-to-market |

• |

Extend our channel partnerships to integrate our products and services into broader ecosystems |

• |

Ongoing expansion of our international offerings |

• |

Accelerate our pace of execution to move fast and win in a competitive market; and |

• |

Leverage our significant capital capacity to fund organic investment and execute a balanced capital allocation approach including annual dividend growth, strategic acquisitions, and shareholder returns. |

Total Thomson Reuters |

2024 Actual |

2025 Outlook | ||

Revenue growth Organic revenue growth (1) |

7% 7% |

3.0% – 3.5% (2) 7.0% – 7.5% | ||

Adjusted EBITDA margin (1) |

38.2% | ~39% | ||

Corporate costs |

$105 million | $120 – $130 million | ||

Free cash flow (1) |

$1.8 billion | ~$1.9 billion | ||

Accrued capital expenditures as a percentage of revenues (1) |

8.4% | ~8% | ||

Depreciation and amortization of computer software Depreciation and amortization of internally developed software Amortization of acquired software |

$731 million $584 million $147 million |

$835 – $855 million $635 – $655 million ~$200 million | ||

Interest expense |

$125 million | ~$150 million | ||

Effective tax rate on adjusted earnings (1) |

17.6% | ~19% | ||

“Big 3” Segments (1) |

2024 Actual |

2025 Outlook | ||

Revenue growth Organic revenue growth |

8% 9% |

~4% ~9% | ||

Adjusted EBITDA margin |

42.1% | ~43% | ||

| (1) | Non-IFRS financial measures. Refer to Appendices A and B of this management’s discussion and analysis for additional information and reconciliations of our non-IFRS financial measures to the most directly comparable IFRS financial measures. |

| (2) | Total revenue growth reflects the impact of the divestitures of FindLaw and other non-core businesses in December 2024. |

Thomson Reuters Annual Report 2024 |

Page 53 |

• |

Organic revenue growth to be in the range of 5% to 6%; and |

• |

Adjusted EBITDA margin to be approximately 40%. |

Revenues | ||

Material assumptions |

Material risks | |

• Uncertain macroeconomic and geopolitical conditions will continue to disrupt the economy and cause periods of volatility• Continued need for trusted products and services that help customers navigate evolving and complex legal, tax, accounting, regulatory, geopolitical and commercial changes, developments and environments, and for cloud-based digital tools that drive productivity• Continued ability to deliver innovative products that meet evolving customer demands• Acquisition of new customers through expanded and improved digital platforms, simplification of the product portfolio and through other sales initiatives• Improvement in customer retention through commercial simplification efforts and customer service improvements |

• Ongoing geopolitical and macroeconomic uncertainty continue to impact the global economy. The severity and duration of this uncertainty could lead to lower demand for our products and services (beyond our assumption that these disruptions will cause periods of volatility)• Uncertainty in the legal regulatory regime relating to AI. Potential future legislation may make it harder for us to conduct business using AI, lead to regulatory fines or penalties, require us to change product offerings or business practices, or prevent or limit our use of AI• Demand for our products and services could be reduced by changes in customer buying patterns, or our inability to execute on key product design or customer support initiatives• Competitive pricing actions and product innovation could impact our revenues• Our sales, commercial simplification and product design initiatives may be insufficient to retain customers or generate new sales | |

Adjusted EBITDA margin | ||

Material assumptions |

Material risks | |

• Our ability to achieve revenue growth targets• Business mix continues to shift to higher-growth product offerings• Integration expenses associated with recent acquisitions will reduce margins |

• Same as the risks above related to the revenue outlook• Higher than expected inflation may lead to greater than anticipated increase in labor costs, third-party supplier costs and costs of print materials• Acquisition and disposal activity may dilute adjusted EBITDA margin | |

Free Cash Flow | ||

Material assumptions |

Material risks | |

• Our ability to achieve our revenue and adjusted EBITDA margin targets• Accrued capital expenditures expected to approximate 8% of revenues in 2025 and 2026 |

• Same as the risks above related to the revenue and adjusted EBITDA margin outlook• A weaker macroeconomic environment could negatively impact working capital performance, including the ability of our customers to pay us• Accrued capital expenditures may be higher than currently expected• The timing and amount of tax payments to governments may differ from our expectations | |

| Page 54 | Thomson Reuters Annual Report 2024 |

Effective tax rate on adjusted earnings | ||

Material assumptions |

Material risks | |

• Our ability to achieve our adjusted EBITDA target• The mix of taxing jurisdictions where we recognized pre-tax profit or losses in 2024 does not significantly change in 2025 or 2026• Minimal changes in currently enacted tax laws and treaties within the jurisdictions where we operate• No significant charges or benefits from the finalization of prior tax years• Depreciation and amortization of internally developed computer software of $835 - $855 million in 2025• Interest expense of approximately $150 million in 2025 |

• Same as the risks above related to adjusted EBITDA• A material change in the geographical mix of our pre-tax profits and losses• A material change in current tax laws or treaties to which we are subject, and did not expect• Depreciation and amortization of internally developed computer software as well as interest expense may be significantly higher or lower than expected | |

Thomson Reuters Annual Report 2024 |

Page 55 |

Year ended December 31, |

||||||||

(millions of U.S. dollars) |

2024 |

2023 |

||||||

Salaries and other benefits |

25 |

23 | ||||||

Share-based payments |

19 |

17 | ||||||

Total compensation |

44 |

40 | ||||||

• |

$500 million 3.35% Notes due 2026; |

• |

$500 million 5.85% Notes due 2040; |

• |

$119 million 4.50% Notes due 2043; |

• |

$350 million 5.65% Notes due 2043; and |

• |

$400 million 5.50% Debentures due 2035. |

| Page 56 | Thomson Reuters Annual Report 2024 |

• |

The consolidated income statement to be structured according to operating, investing and financing categories, and include additional subtotals for “Operating Profit” and “Profit Before Financing and Income Taxes”; |

• |

Management-defined performance measurements (MPM’s), which represent certain of our non-IFRS measures, to be identified, defined, and have an explanation why each one is useful. Each MPM must be reconciled to the most directly comparable IFRS subtotal. All disclosures related to MPM’s must be disclosed in a single footnote within the consolidated financial statements; and |

• |

The application of enhanced guidance related to the grouping of financial information associated with amounts presented within the financial statements, otherwise known as aggregation or disaggregation. |

• |

An election permitting derecognition of financial liabilities that are settled through an electronic payment system before the actual settlement date, if certain conditions are met; and |

• |

Expanded disclosures for (a) investments in equity instruments and (b) financial liabilities that have features unrelated to basic lending risks, such as achieving sustainability targets, that could affect the cash flows of those liabilities. |

Thomson Reuters Annual Report 2024 |

Page 57 |

| Page 58 | Thomson Reuters Annual Report 2024 |

Thomson Reuters Annual Report 2024 |

Page 59 |

How We Define It |

Why We Use It and Why It Is Useful to Investors |

Most Directly Comparable IFRS Measure | ||

Adjusted EBITDA and the related margin | ||||

Represents earnings or losses from continuing operations before tax expense or benefit, net interest expense, other finance costs or income, depreciation, amortization of computer software and other identifiable intangible assets, our share of post-tax earnings or losses in equity method investments, other operating gains and losses, certain asset impairment charges and fair value adjustments, including those related to acquired deferred revenue.The related margin is adjusted EBITDA expressed as a percentage of revenues. For purposes of this calculation, revenues are before fair value adjustments to acquired deferred revenue. |

Provides a consistent basis to evaluate operating profitability and performance trends by excluding items that we do not consider to be controllable activities for this purpose. Also represents a measure commonly reported and widely used by investors as a valuation metric, as well as to assess our ability to incur and service debt. |

Earnings from continuing operations | ||

Adjusted EBITDA less accrued capital expenditures and the related margin | ||||

Represents adjusted EBITDA less accrued capital expenditures, where accrued capital expenditures include amounts that remain unpaid at the reporting date. The related margin is adjusted EBITDA less accrued capital expenditures expressed as a percentage of revenues. For purposes of this calculation, revenues are before fair value adjustments to acquired deferred revenue. |

Provides a basis for evaluating the operating profitability and capital intensity of a business in a single measure. This measure captures investments regardless of whether they are expensed or capitalized, and reflects the basis on which management measures capital spending. | Earnings from continuing operations | ||

Accrued capital expenditures as a percentage of revenues | ||||

Accrued capital expenditures expressed as a percentage of revenues. For purposes of this calculation, revenues are before fair value adjustments to acquired deferred revenue. |

Reflects the basis on how we manage capital expenditures for internal budgeting purposes. | Capital expenditures | ||

| Page 60 | Thomson Reuters Annual Report 2024 |

How We Define It |

Why We Use It and Why It Is Useful to Investors |

Most Directly Comparable IFRS Measure | ||

Adjusted earnings and adjusted EPS | ||||

Net earnings or loss including dividends declared on preference shares but excluding the post-tax impacts of fair value adjustments, including those related to acquired deferred revenue, amortization of acquired intangible assets (attributable to other identifiable intangible assets and acquired computer software), other operating gains and losses, certain asset impairment charges, other finance costs or income, our share of post-tax earnings or losses in equity method investments, discontinued operations and other items affecting comparability. Acquired intangible assets contribute to the generation of revenues from acquired companies, which are included in our computation of adjusted earnings.The post-tax amount of each item is excluded from adjusted earnings based on the specific tax rules and tax rates associated with the nature and jurisdiction of each item.Adjusted EPS is calculated from adjusted earnings using diluted weighted-average shares and does not represent actual earnings or loss per share attributable to shareholders. |

Provides a more comparable basis to analyze earnings. These measures are commonly used by shareholders to measure performance. |

Net earnings and diluted EPS | ||

Effective tax rate on adjusted earnings | ||||

Adjusted tax expense divided by pre-tax adjusted earnings. Adjusted tax expense is computed as income tax (benefit) expense plus or minus the income tax impacts of all items impacting adjusted earnings (as described above), and other tax items impacting comparability. |

Provides a basis to analyze the effective tax rate associated with adjusted earnings. | Tax benefit (expense) | ||

In interim periods, we also make an adjustment to reflect income taxes based on the estimated full-year effective tax rate. Earnings or losses for interim periods under IFRS reflect income taxes based on the estimated effective tax rates of each of the jurisdictions in which we operate. The non-IFRS adjustment reallocates estimated full-year income taxes between interim periods but has no effect on full-year income taxes. |

Our effective tax rate computed in accordance with IFRS may be more volatile by quarter because the geographical mix of pre-tax profits and losses in interim periods may be different from that for the full year. Therefore, we believe that using the expected full-year effective tax rate provides more comparability among interim periods. |

|||

Thomson Reuters Annual Report 2024 |

Page 61 |

How We Define It |

Why We Use It and Why It Is Useful to Investors |