REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered | ||

| Ordinary Participation Certificates (Certificados de Participación Ordinarios), or CPOs, each CPO representing two Series A shares and one Series B share, traded in the form of CPOs. |

☑ |

Accelerated filer | ☐ |

Non-accelerated filer |

☐ | ||||||

| Emerging growth company | ||||||||||

U.S. GAAP ☐ |

by the International Accounting Standards Board ☑ |

Other ☐ |

|

| ||||

TABLE OF CONTENTS

| 11 | ||||

| Item 1. Identity of Directors, Senior Management and Advisors |

11 | |||

| 11 | ||||

| 11 | ||||

| 59 | ||||

| 156 | ||||

| 157 | ||||

| 231 | ||||

| 274 | ||||

| 277 | ||||

| 278 | ||||

| 280 | ||||

| Item 11. Quantitative and Qualitative Disclosures About Market Risk |

295 | |||

| Item 12. Description of Securities Other Than Equity Securities |

295 | |||

| 295 | ||||

| 295 | ||||

| 295 | ||||

| 295 | ||||

| Part II | 297 | |||

| 297 | ||||

| Item 14. Material Modifications to the Rights of Security Holders and Use of Proceeds |

297 | |||

| 297 | ||||

| 298 | ||||

| 298 | ||||

| 298 | ||||

| 300 | ||||

| Item 16D. Exemptions from the Listing Standards for Audit Committees |

301 | |||

| Item 16E. Purchases of Equity Securities by the Issuer and Affiliated Purchasers |

301 | |||

| 301 | ||||

| 301 | ||||

| 307 | ||||

| Item 16I. Disclosure Regarding Foreign Jurisdictions that Prevent Inspections |

307 | |||

| 307 | ||||

| 307 | ||||

| Part III | III-1 | |||

| III-1 | ||||

| III-1 | ||||

| III-1 | ||||

| INTRODUCTION | ||||

INTRODUCTION

Cemex, S.A.B. de C.V. is incorporated as a publicly traded variable stock corporation (sociedad anónima bursátil de capital variable) organized under the laws of the United Mexican States (“Mexico”). Except as the context otherwise may require, references in this annual report to “Cemex,” the “Company,” “we,” “us” or “our” refer to Cemex, S.A.B. de C.V. and its consolidated entities. See note 1 to Cemex, S.A.B. de C.V.’s 2025 audited consolidated financial statements included elsewhere in this annual report.

Presentation of Financial Information

The audited consolidated financial statements of Cemex, S.A.B. de C.V. included elsewhere in this annual report have been prepared in accordance with IFRS Accounting Standards (“IFRS”), as issued by the International Accounting Standards Board (“IASB”).

The regulations of the U.S. Securities and Exchange Commission (the “SEC”) do not require foreign private issuers that prepare their financial statements based on IFRS (as issued by the IASB) to reconcile such financial statements to United States Generally Accepted Accounting Principles (“U.S. GAAP”).

Unless otherwise indicated, references in this annual report to “$” and “Dollars” are to United States Dollars, references to “€” are to Euros, references to “£,” “Pounds Sterling” and “Pounds” are to British Pounds, and references to “Ps,” “Mexican Pesos” and “Pesos” are to Mexican Pesos. References to “billion” mean one thousand million. References in this annual report to “CPOs” are to Cemex, S.A.B. de C.V.’s Ordinary Participation Certificates (Certificados de Participación Ordinarios), each CPO represents two Series A shares (as defined below) and one Series B share (as defined below) of Cemex, S.A.B. de C.V. References to “ADSs” are to American Depositary Shares of Cemex, S.A.B. de C.V., each ADS represents 10 CPOs.

Unless otherwise indicated, all information in this annual report excludes (i) our operations in Guatemala and the Philippines, which we disposed of in September 2024 and December 2024 and (ii) our operations in the Dominican Republic and Panama, which we disposed of in January 2025 and October 2025, respectively. For the year ended December 31, 2023 and for the period from January 1 to September 10, 2024, our operations in Guatemala are reported in the income statements, net of income tax, in the single line item “Discontinued operations.” For the year ended December 31, 2023 and for the period from January 1 to December 2, 2024, our operations in the Philippines are reported in the income statements, net of income tax, in the single line item “Discontinued operations.” For the years ended December 31, 2023 and 2024 and for the period from January 1 to January 30, 2025, our operations in the Dominican Republic are reported in the income statements, net of income tax, in the single line item “Discontinued operations.” For the years ended December 31, 2023 and 2024 and for the period from January 1 to October 6, 2025, our operations in Panama are reported in the income statements, net of income tax, in the single line item “Discontinued operations.” See “Item 5. Operating and Financial Review and Prospects—Results of Operations—Significant Transactions,” “Item 5. Operating and Financial Review and Prospects—Results of Operations—Discontinued Operations” and note 5.2 to Cemex, S.A.B. de C.V.’s 2025 audited consolidated financial statements included elsewhere in this annual report for more information.

See notes 3.4, 18.1 and 18.2 to Cemex, S.A.B. de C.V.’s 2025 audited consolidated financial statements included elsewhere in this annual report for a detailed description of our debt and other financial obligations. Total debt plus other financial obligations differs from the calculation of debt under our main credit agreements, being the Credit Agreement, dated as of October 29, 2021 (as last amended on October 30, 2023 and as further amended and/or restated from time to time, the “2023 Credit Agreement”), the Credit Agreement dated as of October 7, 2022 (as last

CEMEX • 2025 20-F REPORT • 1

| INTRODUCTION | ||||

amended on April 11, 2024 and as further amended and/or restated from time to time, the “Euro Credit Agreement”) and the Credit Agreement dated as of December 20, 2021 (as last amended on December 6, 2023 and as further amended and/or restated from time to time, the “Peso Bilateral Term Loan”) (collectively, the “Credit Agreements”). See “Item 5. Operating and Financial Review and Prospects—Liquidity and Capital Resources—Our Indebtedness” for more information.

Under IAS 32, Financial Instruments: Presentation (“IAS 32”), we concluded that our outstanding 5.125% Subordinated Notes and our 7.200% Subordinated Notes (together, the “Subordinated Notes”) do not meet the definition of financial liability, and consequently are classified in controlling interest stockholders’ equity within Other equity reserves. See note 22.2 to Cemex, S.A.B. de C.V.’s 2025 audited consolidated financial statements included elsewhere in this annual report for a detailed description of the Subordinated Notes.

We also refer in various places within this annual report to non-IFRS measures, including “Operating EBITDA.” Operating EBITDA equals operating earnings before other expenses, net, plus depreciation and amortization expenses, as more fully explained in “Item 5. Operating and Financial Review and Prospects—Results of Operations—Selected Consolidated Financial Information.” Additionally, we refer to “Operating EBITDA Margin,” which is calculated by dividing our Operating EBITDA by our revenues. The presentation of these non-IFRS measures is not meant to be considered in isolation or as a substitute for Cemex, S.A.B. de C.V.’s 2025 audited consolidated financial results prepared in accordance with IFRS as issued by the IASB.

We have approximated certain numbers in this annual report to their closest round numbers or a given number of decimal places. Due to rounding, figures shown as totals in tables may not be arithmetic aggregations of the figures preceding them.

CEMEX • 2025 20-F REPORT • 2

| INTRODUCTION | ||||

Certain Technical Terms

When used in this annual report, the terms set forth below mean the following:

| • | Additives refer to any material (primarily inorganic) that is added to either cement/binders or concrete to achieve a specific target (e.g., alter flow properties, substitute clinker/cement, etc.). In the United States, these materials are often referred to as “inorganic processing additions,” while in Europe, these materials are commonly known as “other constituents.” |

| • | Admixtures refer to any chemical product (primarily organic molecules) that is added or applied to (our core business products) cement/binders, concrete, or aggregates to achieve a targeted performance. |

| • | Aggregates are inert granular materials, such as stone, sand, and gravel, which are obtained from land-based sources (mainly mined from quarries) or by dredging marine deposits. While they can influence concrete’s strength, aggregates play a key role in optimizing the mix by occupying volume and reducing the amount of cement needed, allowing the concrete to achieve the required strength more efficiently and cost-effectively. |

| • | Cement is a hydraulic binder, a finely engineered powder that activates upon contact with water, hardening to bond the core components of concrete: sand and aggregates. Its production begins with the crushing of limestone or chalk, blended with carefully selected materials such as clay, shale and iron ore. This raw mix is then fed into a rotary kiln, where it is subjected to temperatures reaching 1,450°C, comparable to the intensity of volcanic lava and triggering the chemical transformations that give cement its binding properties. |

| • | Concrete is a mixture of cement, water and aggregates (e.g., sand and gravel, crushed stone or recycled concrete) and often includes small amounts of admixtures. The exact ratios and mix and type of aggregate used depend on the intended use. Concrete is an extremely strong, durable and resilient material that can be used in a variety of ways (i.e., shelter, housing, providing clean water and sanitation, transport, business and commerce). |

| • | Cement mill (also called “finish mill” in the United States) is a piece of equipment used to reduce the size of the materials needed for cement production, usually to microns size (1 micron is equal to 0.001 millimeters). Traditionally, cement mills have adopted the form of ball mills. Vertical roller mills, which are more effective in terms of energy consumption compared to ball mills, have been gradually introduced to our operations in the United States, Mexico, Europe, the Middle East, and other regions where Cemex operates. |

| • | Clinker is the essential raw material in the production of portland cement, composed of at least two-thirds calcium silicates by mass. It is formed through a high-temperature process known as clinkering, in which a precisely proportioned raw mix, typically limestone, clay, and iron oxide, is fired in a rotary kiln at approximately 1,450°C. The resulting nodular material is then ground and blended to produce cement, with each ton of cement containing approximately 70% clinker, though this value can vary significantly depending on the cement type, ranging from 95% down to 50%. |

| • | CO2, or carbon dioxide, is a chemical compound with the chemical formula CO2. It is a greenhouse gas, which means it contributes to the warming of the Earth’s atmosphere by trapping heat that would otherwise escape into space. |

| • | CO2 emissions refer to the release of CO2 into the atmosphere as a result of our direct and indirect activities. These activities, which are responsible for most of our CO2 that is released, include fuel emissions from the burning of fossil fuels (such as coal, gas, diesel, tires, biomass, etc.) and emissions derived from the decarbonization of limestone (altogether known as process emissions). |

| • | Fly ash is a combustion residue from coal-fired power plants with cementitious capabilities when mixed with clinker and can be used as a supplementary cementitious material. |

CEMEX • 2025 20-F REPORT • 3

| INTRODUCTION | ||||

| • | Gray Ordinary Portland Cement or Gray Cement is a hydraulic binding agent with a traditional composition by weight of approximately 90% to 95% clinker and up to 5% of a minor component (usually calcium sulfate and limestone) when mixed with sand, stone or other aggregates and water, produce concrete. Blended portland cement has lower clinker factor, usually below 90%, which results in lower CO2 emissions. Both traditional and blended portland cement, when mixed with sand, stone or other aggregates and water, produce concrete. |

| • | Ground Granulated Blast Furnace Slag is a by-product generated in blast furnaces used for smelting to produce pig-iron. When mixed with clinker, it exhibits cementitious properties and can be used as a supplementary cementitious material. |

| • | Petroleum coke or pet coke is a by-product of the oil refining coking process that can be incorporated into the cement production process as fuel, in substitution of other primary fuels such as natural gas or coal. |

| • | Ready-mix concrete is a mixture of cement, aggregates, admixtures and water that is produced through a central batching process and transferred to a ready-mix truck for delivery or is mixed directly in the ready-mix truck and produced through a dry batching process. |

| • | Tons means metric tons. One metric ton equals 1.102 short tons. |

| • | Urbanization Solutions refers to a portfolio of complementary products designed to address urbanization opportunities and evolving industry trends. These solutions are organized around four relevant businesses: construction chemicals, mortars, concrete products and asphalt. |

| • | White cement is a special portland cement used primarily for decorative purposes with the same or higher performance of gray portland cement. The white color of the cement is typically achieved by reducing the iron-bearing phases in clinker to a minimum. |

CEMEX • 2025 20-F REPORT • 4

| INTRODUCTION | ||||

Cautionary Statement Regarding Forward-Looking Statements

This annual report contains, and the reports we will file or furnish in the future may contain, forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). We intend these forward-looking statements to be covered by the “safe harbor” provisions for forward-looking statements within the meaning of applicable securities laws and regulations in all jurisdictions where such provisions exist, including but not limited to the United States Private Securities Litigation Reform Act of 1995. In some cases, these statements can be identified by the use of forward-looking words such as, but not limited to, “will,” “may,” “assume,” “might,” “should,” “could,” “continue,” “would,” “can,” “consider,” “anticipate,” “estimate,” “expect,” “envision,” “plan,” “believe,” “foresee,” “predict,” “potential,” “target,” “goal,” “strategy,” “intend,” “aimed,” or other forward-looking words. Unless otherwise indicated, these forward-looking statements reflect our current expectations and projections about the future, which are based on certain assumptions and on our knowledge of facts and circumstances as of the date such forward-looking statements are made. These forward-looking statements and information necessarily involve risks, uncertainties and assumptions, including, but not limited to, statements related to our plans, objectives, goals, targets and expectations (operative, financial or otherwise) and other important factors that could cause results and any estimate, projection and/or guidance presented in this annual report to differ materially from historical results, performance and/or achievements or those anticipated by forward-looking statements. Although we believe that our expectations are reasonable, we can give no assurance that these expectations will prove to be correct, and actual results, performance and/or achievements may vary, including materially, from historical results, performance and/or achievements or those anticipated by forward-looking statements due to various factors. Among others, such risks, uncertainties, assumptions, and other important factors that could cause results and any estimate, projection and/or guidance presented in this annual report to differ or fail to materialize, or that otherwise could have an impact on us include those discussed in this annual report and those detailed from time to time in our other filings with the SEC, the Mexican National Banking and Securities Commission (Comisión Nacional Bancaria y de Valores) (the “CNBV”) and the Mexican Stock Exchange (Bolsa Mexicana de Valores) (the “MSE”), including, but not limited to:

| • | changes in general economic, political and social conditions, including government shutdowns, new governments or regimes and decisions implemented by such new governments or regimes, changes in laws or regulations in the countries in which we do business, elections, changes in inflation, interest and foreign exchange rates, employment levels, population growth, any slowdown in the flow of remittances into countries where we operate, consumer confidence, and the liquidity of the financial and capital markets in Mexico, the United States, the European Union (the “EU”), the United Kingdom or other countries in which we operate; |

| • | the cyclical activity of the construction sector and reduced construction activity in our end markets or reduced use in our end markets for our products; |

| • | our exposure to sectors that impact our and our clients’ businesses, particularly those operating in the commercial and residential construction sectors, and the public and private infrastructure and energy sectors; |

| • | volatility in pension plan asset values and liabilities, which may require cash or other contributions to the pension plans; |

| • | changes in spending levels for residential and commercial construction and general infrastructure projects; |

| • | the availability of short-term credit lines or working capital facilities, which can assist us in connection with market cycles; |

| • | any impact of not maintaining investment grade debt rating or not obtaining investment grade debt ratings from additional rating agencies on our cost of capital and on the cost of the products and services we purchase; |

CEMEX • 2025 20-F REPORT • 5

| INTRODUCTION | ||||

| • | availability of raw materials and related fluctuating prices of raw materials, as well as of general goods and services, in particular increases in prices of raw materials, goods and services, as a result of inflation, trade barriers, measures imposed by governments or as a result of conflicts between countries that disrupt supply chains; |

| • | our ability to maintain and expand our distribution network and maintain favorable relationships with third parties who supply us with equipment, services and essential supplies; |

| • | competition in the markets in which we offer our products and services; |

| • | the impact of environmental cleanup costs and other remedial actions, and other environmental, climate and related liabilities relating to existing and/or divested businesses, assets and/or operations; |

| • | our ability to secure and permit aggregates reserves in strategically located areas in amounts that our operations require to operate or operate in a cost-efficient manner; |

| • | the timing and amount of federal, state, and local funding for infrastructure; |

| • | changes in our effective tax rate; |

| • | our ability to comply with regulations and implement technologies and other initiatives that aim to reduce and/or capture CO2 emissions and comply with related carbon emissions regulations in place in the jurisdictions where we have operations; |

| • | the legal and regulatory environment, including environmental, climate, trade, energy, tax, antitrust, sanctions, import and export controls, construction, human rights, and labor welfare, and acquisition-related rules and regulations in the countries and regions in which we have operations; |

| • | the effects of currency fluctuations on our results of operations and financial condition; |

| • | our ability to satisfy our obligations under our debt agreements, the indentures that govern our outstanding Notes (as defined herein) and our other debt instruments and financial obligations, and also regarding our subordinated notes with no fixed maturity and other financial obligations; |

| • | adverse legal or regulatory proceedings or disputes, such as class actions or enforcement or other proceedings brought by third parties, government and regulatory agencies, including antitrust investigations and claims; |

| • | our ability to protect our reputation and intellectual property; |

| • | our ability to consummate asset sales or consummate asset sales in terms favorable to us, fully integrate newly acquired businesses, achieve cost-savings from our cost-reduction initiatives, implement our pricing and commercial initiatives for our products and services, and generally meet our business strategy’s goals; |

| • | the increasing reliance on information technology infrastructure for our sales, invoicing, procurement, financial statements, and other processes that can adversely affect our sales and operations in the event that the infrastructure does not work as intended, experiences technical difficulties, or is subjected to invasion, disruption, or damage caused by circumstances beyond our control, including cyber-attacks, catastrophic events, power outages, natural disasters, computer system or network failures, or other security breaches; |

| • | the effects of climate change, in particular reflected in weather conditions, including, but not limited to, excessive rain and snow, shortage of usable water, wildfires and natural disasters, such as earthquakes, hurricanes, tornadoes and floods, that could affect our facilities or the markets in which we offer our products and services or from where we source our raw materials; |

| • | trade barriers, including, but not limited to, tariffs or import taxes, including those imposed by the United States to key markets in which we operate, in particular, Mexico, China and the EU, and changes in existing trade |

CEMEX • 2025 20-F REPORT • 6

| INTRODUCTION | ||||

| policies or changes to, or withdrawals from, free trade agreements, including the United States-Mexico-Canada Agreement (the “USMCA”), and the overall impact that the imposition or threat of trade barriers may cause on the overall economy of the countries in which we do business or that are part of our global supply chain; |

| • | availability and cost of trucks, railcars, barges, and ships, terminals, warehouses, as well as their licensed operators, drivers, staff and workers, for transport, loading and unloading of our materials or that are otherwise a part of our supply chain; |

| • | labor shortages and constraints; |

| • | our ability to hire, effectively compensate and retain our key personnel and maintain satisfactory labor relations; |

| • | our ability to detect and prevent money laundering, terrorism financing and corruption, as well as other illegal activities and how any measures implemented by governments to detect and prevent money laundering, terrorism financing and corruption, and other illegal activities, affect our customers, suppliers and countries in which we do business; |

| • | defaults, losses or disruptions in agreements, financial transactions or operations resulting from sanctions or restrictions imposed on any financial institution, including, but not limited to, banks, common representatives, trustees, payment processors, paying agents or other financial intermediaries, or any related parties; |

| • | terrorist and organized criminal activities, social unrest, as well as geopolitical events, such as global, regional or national instability, hostilities, war, and armed conflicts, including the current war between Russia and Ukraine, the ongoing war among Israel, the United States and the Islamic Republic of Iran, conflicts in the Middle East and any insecurity and hostilities in Mexico related to illegal activities or organized crime and any actions any government takes to prevent these illegal activities and organized crime; |

| • | the impact of pandemics, epidemics, or outbreaks of infectious diseases and the response of governments and other third parties, which could adversely affect, among other matters, the ability of our operating facilities to operate at full or any capacity, supply chains, international operations, availability of liquidity, investor confidence and consumer spending, as well as the availability of, and demand for, our products and services; |

| • | changes in the economy that affect demand for consumer goods, consequently affecting demand for our products and services; |

| • | the depth and duration of an economic slowdown or recession, instability in the business landscape and lack of availability of credit; |

| • | declarations of insolvency or bankruptcy, or becoming subject to similar proceedings; |

| • | natural disasters and other unforeseen events (including global health hazards such as COVID-19); |

| • | our ability to implement our climate action program in effect at any given time, if any, including our current “Future in Action” climate action and nature program, and to achieve our sustainability goals and objectives in effect at any given time, if any, including under our current “Future in Action” climate action and nature program; and |

| • | the other risks and uncertainties described under “Item 3. Key Information—Risk Factors” and elsewhere in this annual report. |

Many factors could cause our expectations, expected results, and/or projections expressed in this annual report not being reached and/or not producing the expected benefits and/or results, as any such benefits or results are subject to uncertainties, costs, performance, and rate of success and/or implementation of technologies, some of which are not yet proven, among other factors. Should one or more of these risks or uncertainties materialize, or should

CEMEX • 2025 20-F REPORT • 7

| INTRODUCTION | ||||

underlying assumptions prove incorrect, actual results, performance and/or achievements may vary materially from historical results, performance, and/or achievements and/or results, performance, or achievements expressly or implicitly anticipated by the forward-looking statements, or otherwise could have an impact on us. Forward-looking statements should not be considered guarantees of future performance, and past results or developments are not indicative of results or developments in subsequent periods. Actual results, performance and/or achievements of our operations and the development of market conditions in which we operate, or other circumstances that may materialize, may differ materially from those described in, or suggested by, the forward-looking statements contained herein, and events referenced therein. Any or all of our forward-looking statements may turn out to be inaccurate and the factors identified above are not exhaustive. Accordingly, readers should not place undue reliance on forward-looking statements, as such forward-looking statements speak only as of the date on which they are made. The forward-looking statements and the information disclosed in this annual report are made as of the dates specified in this annual report and are subject to change without notice; and, except to the extent legally required, we expressly disclaim any obligation or undertaking to update or correct the information contained in this annual report, or revise any forward-looking statements in this annual report, whether to reflect new information, the occurrence of anticipated or unanticipated future events or circumstances, any change in our expectations regarding those forward-looking statements, any change in events, conditions, or circumstances on which any such statement is based, or otherwise. Readers should review future reports filed or furnished by us with the SEC, the CNBV and the MSE.

This annual report contains statistical data regarding, but not limited to, the production, distribution, marketing, and sale of cement, ready-mix concrete, clinker, aggregates, and Urbanization Solutions. We generated some of this data internally, and some was obtained from independent industry publications and reports, available as of the date of this annual report, that we believe to be reliable sources. We have not independently verified this data nor sought the consent of any organizations to refer to their reports in this annual report.

We act in strict compliance with antitrust laws and as such, among other measures, maintain an independent pricing policy that has been independently developed. Our policy’s core element is to price our products and services based on their quality and characteristics as well as their value to our customers. We do not accept any communications or agreements of any type with competitors regarding the determination of our prices for our products and services. Unless the context indicates otherwise, all references to pricing initiatives, price increases or price decreases, refer to our prices for our products.

This annual report includes certain non-IFRS financial measures that differ from financial information presented by Cemex in accordance with IFRS in its financial statements and reports containing financial information. These aforementioned non-IFRS financial measures include “Operating EBITDA” (operating earnings before other expenses, net plus depreciation and amortization) and “Operating EBITDA Margin.” The closest financial measure to Operating EBITDA in our financial statements under IFRS is the line item of “Operating earnings before other expenses, net,” as Operating EBITDA adds depreciation and amortization to this line item. Our Operating EBITDA Margin is calculated by dividing our Operating EBITDA for the period by our revenues as reported in our financial statements for the same period. We believe there is no close IFRS financial measure to compare Operating EBITDA Margin. These non-IFRS financial measures are designed to complement and should not be considered superior to financial measures calculated in accordance with IFRS. Although Operating EBITDA and Operating EBITDA Margin are not measures of operating performance, an alternative to cash flows or a measure of financial position under IFRS, Operating EBITDA is the financial measure used by our management to review operating performance and profitability, for decision-making purposes and to allocate resources. Moreover, our Operating EBITDA is a measure used by our creditors to review our ability to internally fund capital expenditures, to service or incur debt and to comply with financial covenants under our financing agreements. Furthermore, our management regularly reviews our Operating EBITDA Margin by reportable segment and on a consolidated basis as a measure of performance and profitability. These non-IFRS financial measures do not have any standardized meaning and are therefore unlikely to be comparable to

CEMEX • 2025 20-F REPORT • 8

| INTRODUCTION | ||||

similarly titled measures presented by other companies. Non-IFRS financial measures presented in this annual report are being provided for informative purposes only and shall not be construed as investment, financial, or other advice.

The information, statements, and opinions contained in this annual report are for informational purposes and do not constitute a public offer under any applicable legislation, an offer to sell, or solicitation of any offer to buy any securities or financial instruments, or any advice or recommendation with respect to such securities or other financial instruments. You should not construe any such information or other material as legal, tax, investment, financial, or other advice. We are not responsible for any third-party information referenced in this annual report.

Cautionary Statement Regarding Environmental, Social, and Governance (“ESG”) and Sustainability-Related Data, Metrics, and Methodologies

This annual report includes non-financial metrics, estimates, or other information related to ESG and sustainability matters that are subject to significant uncertainties, which may include the methodology, collection, and verification of data, various estimates, and assumptions, and/or underlying data that is obtained from third parties, some of which cannot be independently verified.

The preparation of certain information on ESG and sustainability matters contained in this annual report requires the application of a number of key judgments, assumptions, and estimates. The reported measures in this annual report reflect good faith estimates, assumptions, and judgments at the given point in time. There is a risk that these judgments, estimates, or assumptions may subsequently prove to be incorrect and/or, to the extent legally required, may need to be restated or changed. The disclosure of information on sustainability-related matters is not yet subject to the same recognized or accepted reporting or accounting principles and rules as traditional financial information. Consequently, there are no commonly accepted reporting practices for us to follow, and ESG metrics among organizations in our industry may not be comparable. In addition, the underlying data, systems, and controls that support non-financial reporting are generally considerably less sophisticated than the systems and internal control for financial reporting and rely on manual processes. This may result in non-comparable information between organizations and/or between reporting periods within organizations as methodologies continue to develop and/or be socialized. The further development of or changes to accounting and/or reporting standards could materially impact the performance metrics, data points, and targets contained in this annual report, and the reader may not be able to compare non-financial information performance metrics, data points, or targets between reporting periods on a direct like-for-like basis.

Additionally, the information disclosed in this annual report contains references to “green,” “social,” “sustainable,” or equivalent-labelled activities, products, assets, or projects. There is currently no single globally recognized or accepted, consistent and comparable set of definitions or standards (legal, regulatory, or otherwise) of, nor widespread cross-market consensus (i) as to what constitutes, a “green,” “social,” “sustainable,” or having equivalent-labelled activity, product, or asset; (ii) as to what precise attributes are required for a particular activity, product, or asset to be defined as “green,” “social,” “sustainable” or such other equivalent label; or (iii) as to climate and sustainable funding and financing activities and their classification and reporting.

Therefore, there is little certainty, and no assurance or representation is given, that such activities, products, assets, or projects and/or reporting of such activities, products, assets or projects will meet any present or future expectations or requirements for describing or classifying such activities, products, assets or projects as “green,” “social,” “sustainable,” or attributing similar labels. We expect policies, regulatory requirements, standards, and definitions to be developed and continuously evolve over time.

CEMEX • 2025 20-F REPORT • 9

| INTRODUCTION | ||||

Cautionary Statement Regarding Forward-Looking ESG or Sustainability Statements

Certain sections in this annual report contain ESG- or sustainability-related forward-looking statements, such as aims, ambitions, estimates, forecasts, plans, projections, targets, goals and other metrics, including but not limited to: climate and emissions, business and human rights, corporate governance, research and development (“R&D”) and partnerships, development of products and services that intend to address sustainability-related concerns and sustainability related targets/ ambitions when finalized, including the implementation of technologies and other initiatives that aim to reduce and/or capture CO2 emissions. These forward-looking statements also include references to specific programs, such as our current “Future in Action” climate action and nature program, as well as various ESG-related indicators, objectives or metrics disclosed previously or that may be disclosed in the future, none of which are guarantees and any and all of which may ultimately not be achieved or may be abandoned at any time, whether in part, in full, or within any specific timeframe. There are many significant uncertainties, assumptions, judgements, opinions, estimates, forecasts and statements made of future expectations underlying these forward-looking statements which could cause actual results, performance, outcomes or events to differ materially from those expressed or implied in these forward-looking statements, which include, but are not limited to:

| • | the extent and pace of climate change, including the timing and manifestation of physical and transition risks; |

| • | the macroeconomic environment; |

| • | uncertainty around future climate-related policy and regulations, including the timely implementation and integration of adequate government policies; |

| • | the effectiveness of actions of governments, legislators, regulators, businesses, investors, customers, and other stakeholders to mitigate the impact of climate and sustainability-related risks; |

| • | changes in customer behavior and demand, changes in the available technology for mitigation and the effectiveness of any such technologies, as some of these new technologies may be unproven; |

| • | excessive costs and expenses related to acquire and/or develop technology for mitigation; |

| • | the roll-out of low carbon infrastructure; |

| • | the availability and adoption of renewable energy in our value chain; |

| • | the development of carbon capture, circular utilization, and sequestration technologies, including the adoption of cost-effective carbon-related technologies such as carbon capture, utilization, and storage (“CCUS”); |

| • | the availability of accurate, verifiable, reliable, consistent, and comparable climate-related data; |

| • | lack of transparency and comparability of climate-related forward-looking methodologies; |

| • | variation in approaches and outcomes, as variations in methodologies may lead to under or overestimates and consequently present exaggerated indication of climate-related risk; and |

| • | reliance on assumptions and future uncertainty (calculations of forward-looking metrics are complex and require many methodological choices and assumptions). |

Accordingly, undue reliance should not be placed on these forward-looking statements. Furthermore, changing national and international standards, industry and scientific practices, regulatory requirements, and market expectations regarding climate change, which remain under continuous development, are subject to different interpretations.

There can be no assurance that these standards, practices, requirements, and expectations will not be interpreted differently than our understanding when defining sustainability-related ambitions and targets or change in a manner that substantially increases the cost or effort for us to achieve such ambitions and targets.

CEMEX • 2025 20-F REPORT • 10

| PART I | ||||

Part I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISORS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

Pursuing Excellence

In 2025, we underwent a significant operational and strategic transformation, delivering strong results despite a complex global environment marked by geopolitical shifts, trade policy adjustments and persistent macroeconomic headwinds. Under the leadership of our new Chief Executive Officer and a renewed senior management team, we shifted our focus to operational excellence, increasing free cash flow and enhancing shareholder returns. To achieve these renewed priorities, we launched “Project Cutting Edge,” a comprehensive initiative focused on reducing costs, pursuing operational excellence and improving profitability. As part of our transformation, we reconfigured our organizational structure to simplify decision-making and grant greater operational authority to our regional teams. This decentralized approach, coupled with in-depth business performance reviews across all operating regions, is designed to instill an ownership mentality throughout the organization and focus on accountability in an effort to improve results. We also established new criteria for capital allocation, prioritizing investments with a goal of increasing free cash flow and improving contribution margins. Among other results, Project Cutting Edge generated approximately $200 million in recurring savings during the year, with targeted cumulative savings of $400 million by 2027. These results reflect the discipline and commitment of our employees worldwide.

For the year ended December 31, 2025, we had revenues of $16,132 million, remaining stable compared to 2024. Throughout 2025, we continued to strengthen our financial position and our leverage ratio, which, as calculated under the Credit Agreements, was 1.63x as of December 31, 2025. We also continued executing our portfolio rebalancing strategy, completing the divestment of our operations in the Dominican Republic and most of our operations in Panama. A portion of the proceeds from the divestment of our Panama operations was deployed toward the acquisition of a majority stake in Couch Aggregates, LLC (“Couch”) in the United States, reinforcing our growth strategy in a market we believe offers strong long-term potential and higher returns. We also continued delivering on our progressive shareholder return program with a cash dividend of $130 million declared in 2025, compared to the $120 million declared in 2024.

In 2025, we continued advancing our current “Future in Action” climate action and nature program, with a renewed focus on profitable decarbonization. Our operations in Europe achieved the net CO2 emissions target for 2030 established by the European Cement Association and we further optimized our fuel mix and reduced our clinker factor through innovations such as micronization and greater use of alternative cementitious materials and additives.

Beyond our financial and operational results, we maintained our strong commitment to health and safety. In 2025, our employee Lost Time Injury (“LTI”) Frequency Rate improved to 0.3, with approximately 97% of our plants and facilities recording zero incidents, positioning us as one of the global industry leaders. We remain committed to our goal of achieving zero incidents across all operations. We look forward to continuing the transformation of our Company, building on the strong foundation established this year, with a clear focus on operational excellence, disciplined capital allocation and the generation of greater returns for our shareholders.

CEMEX • 2025 20-F REPORT • 11

| PART I | ||||

As required pursuant to the laws of Mexico, the following is a description of our debt securities listed in Mexico:

CEMEX • 2025 20-F REPORT • 12

| PART I | ||||

INFORMATION ABOUT THE LONG-TERM NOTES (CERTIFICADOS BURSÁTILES A TASA VARIABLE)

(“Long-Term Notes 1”) ISSUED BY CEMEX, S.A.B. DE C.V.

AS OF DECEMBER 31, 2025

Amount of the Issuance of Original Long-Term Notes 1: Ps 1,000,000,000.00.

Amount of the Issuance of Additional Long-Term Notes 1: Ps 2,000,000,000.00.

Name of the Issuer: Cemex, S.A.B. de C.V.

Ticker: “CEMEX 23L”

Issue Number under the Program: First Issuance and First Reopening of First Issuance.

Issue Date of Original Long-Term Notes 1: October 5, 2023.

Issue Date of Additional Long-Term Notes 1: February 20, 2024.

Maturity Date: October 1, 2026.

Term of Original Long-Term Notes 1: 1,092 days.

Term of Additional Long-Term Notes 1: 954 days.

Interest Rate and Interest Calculation Method: The annual gross interest rate will be calculated by adding 0.45 percentage points to the rate known as the Mexican Interbank Equilibrium Interest Rate at a 28-day term.

Interest Payment Frequency: Every 28 days starting November 2, 2023.

Place and Form of Payment of Principal and Interest: The principal and ordinary interest accrued will be paid by electronic transfer of funds to the address of S.D. Indeval Institución para el Depósito de Valores, S.A. de C.V. (“Indeval”), or, where appropriate, at the offices of Cemex, S.A.B. de C.V.

Redemption and Early Redemption: A single payment at their nominal value or, if applicable, at their Adjusted Nominal Value (as defined in the Long-Term Notes 1).

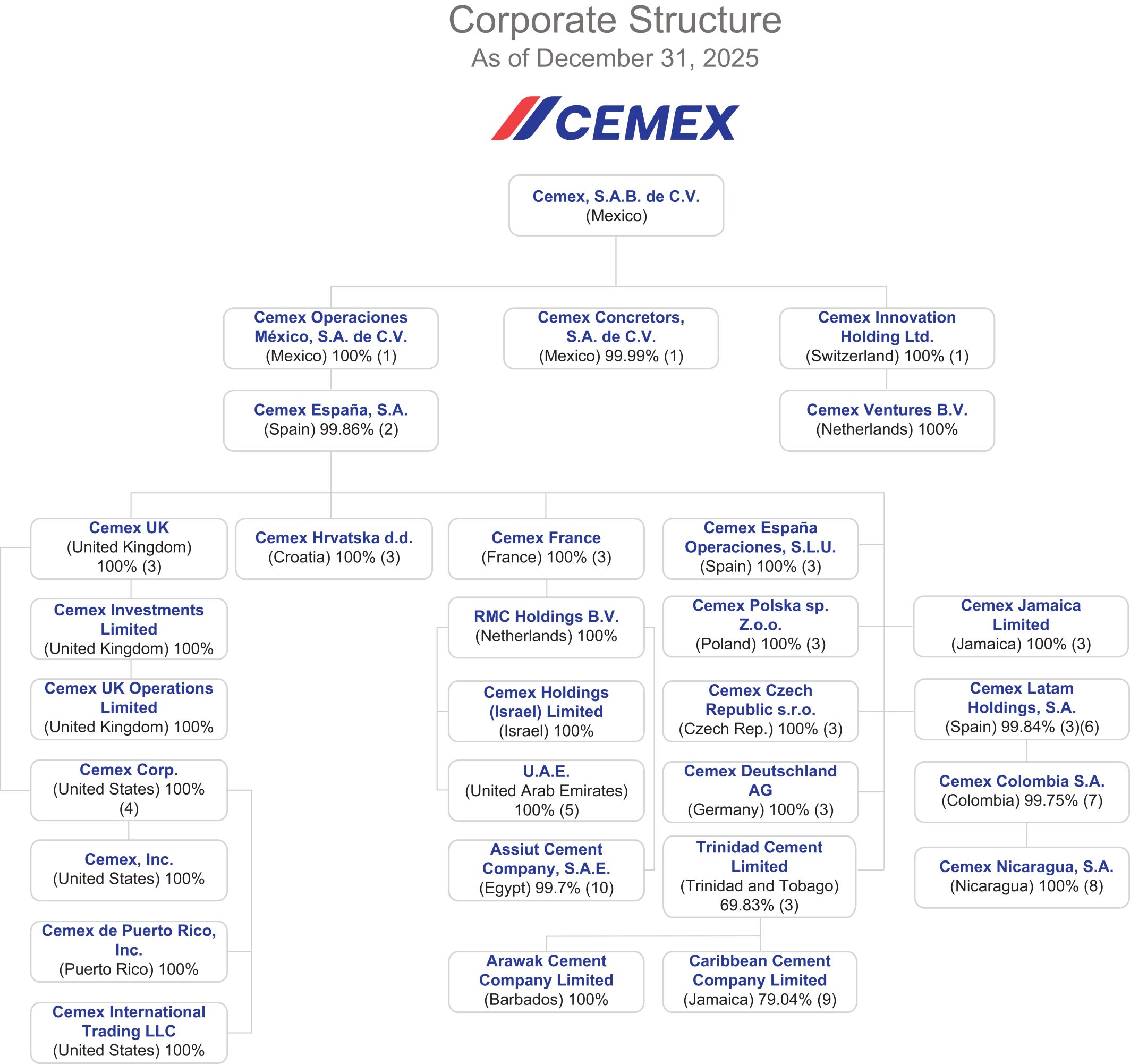

Guarantee: The Long-Term Notes 1 will be guaranteed, initially, by the following entities (the “Long-Term Notes 1 Guarantors” or “Refinancing Guarantors”): Cemex Concretos, S.A. de C.V. (“Cemex Concretos”), Cemex Corp. (“Cemex Corp”), Cemex Operaciones México, S.A. de C.V. (“COM”), and Cemex Innovation Holding Ltd. (“CIH”), but are not secured. Cemex, S.A.B. de C.V. shall have the right to release or replace any Long-Term Notes 1 Guarantor, or add new guarantors, provided that after such release, addition or replacement takes effect, the Minimum Endorsement (as defined in the Long-Term Notes 1) is satisfied.

Rating: Standard & Poor’s, S.A. de C.V. “mxAA” (payment capacity of Cemex, S.A.B. de C.V. to satisfy its financial commitments within the obligation is very strong compared to other issuers in the domestic market). Fitch México, S.A. de C.V. “AA (mex)” (very low risk level of default compared to other issuers or obligations in the same country).

Common Representative: Banco Multiva, S.A., Institución de Banca Múltiple, Grupo Financiero Multiva (“Multiva”) (formerly CIBanco S.A., Institución de Banca Múltiple).

CEMEX • 2025 20-F REPORT • 13

| PART I | ||||

Depositary: Indeval.

Tax Regime: The applicable withholding rate with respect to interest paid under the Long-Term Notes 1 is subject: (i) for individuals or legal entities residing in Mexico for tax purposes, to the provisions of Articles 54, 55, 135, and other applicable laws of the current Income Tax Law; and (ii) for individuals and legal entities resident abroad for tax purposes, the provisions of Articles 153, 166, and other applicable laws of the current Income Tax Law. The current tax regime may be amended throughout the term of the issue.

Cemex, S.A.B. de C.V.’s policy on making decisions regarding changes of control during the term of the issue: Not applicable.

Cemex, S.A.B. de C.V.’s policy on making decisions regarding corporate restructurings, including acquisitions, mergers and spin-offs during the term of the issue: Cemex, S.A.B. de C.V. and the Long-Term Notes 1 Guarantors cannot merge, unless: (i) the merged or acquiring company assumes the obligations of the Issuer or the Long-Term Notes 1 Guarantor, as appropriate, under the Long-Term Notes 1, (ii) a Cause of Early Termination (as defined in the Long-Term Notes 1) does not occur under the Long-Term Notes 1 as a result of the merger or transfer, and (iii) the merged or acquiring company delivers to the Common Representative (as defined in the Long-Term Notes 1) a legal opinion stating that said merger or transfer complies with (i) and (ii) above.

Cemex, S.A.B. de C.V.’s policy on making decisions on the sale or creation of encumbrances on essential assets, specifying what such concept will include during the term of the issue: According to the provisions of the Long-Term Notes 1, Cemex, S.A.B. de C.V. shall not permit the constitution of any encumbrance on its assets, except (i) for Permitted Encumbrances (as defined in the Long-Term Notes 1), or (ii) where the Issuer’s obligations under the Long-Term Notes 1 are simultaneously guaranteed.

The net proceeds from the issuance of the Long-Term Notes 1 were applied towards total or partial repayment of the then-outstanding amounts under the Credit Agreements as in effect at the time and/or the Notes, other than the CEBURES.

CEMEX • 2025 20-F REPORT • 14

| PART I | ||||

INFORMATION ABOUT THE LONG-TERM NOTES (CERTIFICADOS BURSÁTILES A TASA FIJA) (“Long-Term Notes 2”) ISSUED BY CEMEX, S.A.B. DE C.V.

AS OF DECEMBER 31, 2025

Amount of the Issuance of Original Long-Term Notes 2: Ps 5,000,000,000.00.

Amount of the Issuance of Additional Long-Term Notes 2: Ps 3,500,000,000.00.

Name of the Issuer: Cemex, S.A.B. de C.V.

Ticker: “CEMEX 23-2L”

Issue Number under the Program: Second Issuance and First Reopening of Second Issuance.

Issue Date of Original Long-Term Notes 2: October 5, 2023.

Issue Date of Additional Long-Term Notes 2: February 20, 2024.

Maturity Date: September 26, 2030.

Term of Original Long-Term Notes 2: 2,548 days.

Term of Additional Long-Term Notes 2: 2,410 days.

Interest Rate and Interest Calculation Method: Annual gross interest of 11.48%, which will remain fixed during the term of the issue, except in the event that such rate is substituted by the Adjusted Gross Annual Interest Rate (as defined in the Long-Term Notes 2).

Interest Payment Frequency: Every 182 days starting April 4, 2024.

Place and Form of Payment of Principal and Interest: The principal and ordinary interest accrued will be paid by electronic transfer of funds to the address of Indeval, or, where appropriate, at the offices of Cemex, S.A.B. de C.V.

Redemption and Early Redemption: A single payment at their nominal value or, if applicable, at their Adjusted Nominal Value (as defined in the Long-Term Notes 2).

Guarantee: The Long-Term Notes 2 will be guaranteed, initially, by Long-Term Notes 1 Guarantors, but are not secured. The Issuer shall have the right to release or replace any Long-Term Note 1 Guarantor, or add new guarantors, provided that after such release, addition or replacement takes effect, the Minimum Endorsement (as defined in the Long-Term Notes 2) is satisfied.

Rating: Standard & Poor’s, S.A. de C.V. “mxAA” (payment capacity of the Cemex, S.A.B. de C.V. to satisfy its financial commitments within the obligation is very strong compared to other issuers in the domestic market). Fitch México, S.A. de C.V. “AA (mex)” (very low risk level of default compared to other issuers or obligations in the same country).

Common Representative: Multiva (formerly CIBanco S.A., Institución de Banca Múltiple).

CEMEX • 2025 20-F REPORT • 15

| PART I | ||||

Depositary: Indeval.

Tax Regime: The applicable withholding rate with respect to interest paid under the Long-Term Notes 2 is subject: (i) for individuals or legal entities residing in Mexico for tax purposes, to the provisions of Articles 54, 55, 135, and other applicable laws of the current Income Tax Law; and (ii) for individuals and legal entities resident abroad for tax purposes, the provisions of Articles 153, 166, and other applicable laws of the current Income Tax Law. The current tax regime may be amended throughout the term of the issue.

Cemex, S.A.B. de C.V.’s policy on making decisions regarding changes of control during the term of the issue: Not applicable.

Cemex, S.A.B. de C.V.’s policy on making decisions regarding corporate restructurings, including acquisitions, mergers and spin-offs during the term of the issue: Cemex, S.A.B. de C.V. and the Long-Term Notes 1 Guarantors cannot merge, unless: (i) the merged or acquiring company assumes the obligations of Cemex, S.A.B. de C.V. or the Long-Term Notes 1 Guarantor, as appropriate, under the Long-Term Notes 2, (ii) a Cause of Early Termination (as defined in the Long-Term Notes 2) does not occur under the Long-Term Notes 2 as a result of the merger or transfer, and (iii) the merged or acquiring company delivers to the Common Representative (as defined in the Long-Term Notes 2) a legal opinion stating that said merger or transfer complies with (i) and (ii) above.

Cemex, S.A.B. de C.V.’s policy on making decisions on the sale or creation of encumbrances on essential assets, specifying what such concept will include during the term of the issue: According to the set forth on the Long-Term Notes 2, Cemex, S.A.B. de C.V. shall not permit the constitution of any encumbrance on its assets, except (i) for Permitted Encumbrances (as defined in the Long-Term Notes 2), or (ii) where the Issuer’s obligations under the Long-Term Notes 2 are simultaneously guaranteed.

The net proceeds from the issuance of the Long-Term Notes 2 were applied towards total or partial repayment of the then-outstanding amounts under the Credit Agreements as in effect at the time and/or the Notes, other than the CEBURES.

CEMEX • 2025 20-F REPORT • 16

| PART I | ||||

INFORMATION ABOUT THE LONG-TERM NOTES (CERTIFICADOS BURSÁTILES A TASA VARIABLE)

(“Long-Term Notes 3”) ISSUED BY CEMEX, S.A.B. DE C.V.

Amount of the Issuance of Long-Term Notes 3: Ps 5,500,000,000.

Name of the Issuer: Cemex, S.A.B. de C.V.

Ticker: “CEMEX 26”

Issue Number under the Program: Third Issuance.

Issue Date of Long-Term Notes 3: February 19, 2026.

Maturity Date: February 13, 2031.

Term of Long-Term Notes 3: 1,820 days.

Interest Rate and Interest Calculation Method: The annual gross interest rate will be calculated by adding 0.70 percentage points to the rate known as the Mexican Overnight Interbank Equilibrium Interest Rate (TIIE de Fondeo).

Interest Payment Frequency: Every 28 days starting March 19, 2026.

Place and Form of Payment of Principal and Interest: The principal and ordinary interest accrued will be paid by electronic transfer of funds to the address of Indeval, or, where appropriate, at the offices of Cemex, S.A.B. de C.V.

Redemption and Early Redemption: A single payment at their Nominal Value or, if applicable, at their Adjusted Nominal Value (as defined in the Long-Term Notes 3).

Guarantee: The Long-Term Notes 3 will be guaranteed, initially, by the Refinancing Guarantors, but are not secured. Cemex, S.A.B. de C.V. shall have the right to release or replace any Long-Term Notes 1 Guarantor, or add new guarantors, provided that after such release, addition or replacement takes effect, the Minimum Endorsement (as defined in the Long-Term Notes 3) is satisfied.

Rating: Standard & Poor’s, S.A. de C.V. “mxAAA” (payment capacity of Cemex, S.A.B. de C.V. to satisfy its financial commitments within the obligation is extremely strong compared to other issuers in the domestic market). Fitch México, S.A. de C.V. “AA+ (mex)” (very low risk level of default compared to other issuers or obligations in the same country).

Common Representative: Multiva.

Depositary: Indeval.

Tax Regime: The applicable withholding rate with respect to interest paid under the Long-Term Notes 3 is subject: (i) for individuals or legal entities residing in Mexico for tax purposes, to the provisions of Articles 54, 55, 135, and other applicable laws of the current Income Tax Law; and (ii) for individuals and legal entities resident abroad for tax purposes, the provisions of Articles 153, 166, and other applicable laws of the current Income Tax Law. The current tax regime may be amended throughout the term of the issue.

CEMEX • 2025 20-F REPORT • 17

| PART I | ||||

Cemex, S.A.B. de C.V.’s policy on making decisions regarding changes of control during the term of the issue: Not applicable.

Cemex, S.A.B. de C.V.’s policy on making decisions regarding corporate restructurings, including acquisitions, mergers and spin-offs during the term of the issue: Cemex, S.A.B. de C.V. and the Refinancing Guarantors cannot merge, unless: (i) the merged or acquiring company assumes the obligations of the Issuer or the Long-Term Notes 1 Guarantor, as appropriate, under the Long-Term Notes 3, (ii) a Cause of Early Termination (as defined in the Long-Term Notes 3) does not occur under the Long-Term Notes 3 as a result of the merger or transfer, and (iii) the merged or acquiring company delivers to the Common Representative (as defined in the Long-Term Notes 3) a legal opinion stating that said merger or transfer complies with (i) and (ii) above.

Cemex, S.A.B. de C.V.’s policy on making decisions on the sale or creation of encumbrances on essential assets, specifying what such concept will include during the term of the issue: According to the provisions of the Long-Term Notes 3, Cemex, S.A.B. de C.V. shall not permit the constitution of any encumbrance on its assets, except (i) for Permitted Encumbrances (as defined in the Long-Term Notes 3), or (ii) where the Issuer’s obligations under the Long-Term Notes 3 are simultaneously guaranteed.

The net proceeds from the issuance of the Long-Term Notes 3 were applied towards general corporate purposes, including towards the total or partial repayment, redemption or repurchase, as applicable, of the outstanding amounts under the 2023 Credit Agreement, the Euro Credit Agreement and/or the Notes, other than the CEBURES.

CEMEX • 2025 20-F REPORT • 18

| PART I | ||||

RISK FACTORS

We are subject to various risks mainly resulting from changing economic, environmental, political, industry, business, legal, regulatory, financial and climate conditions, as well as risks related to ongoing legal proceedings and investigations. The following risk factors are not the only risks we face, and any of the risk factors described below could significantly and adversely affect our business, liquidity, results of operations or financial condition, as well as, in certain instances, our reputation.

Risk Factor Summary

Risks Relating to Ownership of Our Securities

| • | Non-Mexicans may not hold Cemex, S.A.B. de C.V.’s Series A shares directly and must have them held in a trust at all times. |

| • | ADS holders may only indirectly vote the Series B shares represented by the CPOs deposited with the ADS depositary through the ADS depositary and are not entitled to vote the Series A shares represented by the CPOs deposited with the ADS depositary or to attend shareholders’ meetings. |

| • | Corporate rights, mainly voting rights, may not be available to any person that acquires or otherwise becomes entitled to vote 2% or more of Cemex, S.A.B. de C.V.’s shares with voting rights without the previous approval of Cemex, S.A.B. de C.V.’s Board of Directors. |

| • | Preemptive rights generally available under Mexican law may be unavailable to ADS holders. |

| • | The protections afforded to shareholders in Mexico are different from those in other countries and may be more difficult to enforce. |

Risks Relating to Our Business and Operations

| • | Economic conditions globally, including persistently elevated inflation and interest rates, particularly in countries where we operate, have affected and may continue to adversely affect our business, financial condition, liquidity, and results of operations. |

| • | Political, social, and geopolitical events, changes in public policies and other risks in some of the countries where we operate, which are inherent to the operations of an international company, could have a material adverse effect on our business, financial condition, liquidity, and results of operations. |

| • | The emergence or continued escalation of geopolitical conflicts may have a material adverse effect on our business, financial condition, liquidity, and results of operation. |

| • | Potential political, economic, and military instability in Israel and the Middle East could materially and adversely affect our business, financial condition, liquidity, and results of operation. |

| • | Complications in relationships with local communities and different stakeholder perspectives could lead to social actions against our industry or company, including legal actions, on-the-ground protests, attacks on our assets or facilities, negative media campaigns, strikes, and social unrest. All these events could disrupt our operations, affect our capacity to serve our clients, damage our assets and/or reputation and may materially and adversely affect our business continuity, reputation, liquidity, and results of operations. |

| • | Labor activism and unrest, or failure to maintain satisfactory labor relations, could materially and adversely affect our reputation and results of operations. |

| • | We are subject to restrictions and reputational risks resulting from non-controlling interests held by third parties in our consolidated subsidiaries. As of the date of this annual report, we control publicly listed companies in Trinidad and Tobago and in Jamaica, where this risk is heightened. |

CEMEX • 2025 20-F REPORT • 19

| PART I | ||||

| • | High energy and fuel costs have had and may continue to have a material adverse effect on our business, financial condition, liquidity, and results of operation. |

| • | We are increasingly dependent on information technology and our systems and infrastructure, as well as those provided by third-party service providers, face certain risks, including cyber-security risks, which if materialized, could materially and adversely affect our business, financial condition, liquidity, and results of operation. |

| • | The development and adoption of AI, including generative AI, and its use by us or use or misuse by third parties, may increase the financial and operational risks or create new financial or operational risks that we are not currently anticipating. |

| • | We may not be able to realize the expected benefits from our portfolio rebalancing or any divestments, acquisitions, investments or joint ventures, some of which may have a material impact on our reputation, business, financial condition, liquidity, and results of operations. Any failure to realize expected benefits from the bolt-on acquisitions of our business strategy heightens this risk. |

| • | We have adopted a sustainability strategy we consider to be ambitious. Our sustainability strategy includes the targets of our current “Future in Action” climate action and nature program and some of these targets are replicated as key performance indicators in our sustainability-linked financing arrangements. Failure to reach these goals may expose us to certain risks that could have a material adverse effect on our reputation, business, financial condition, liquidity, and results of operations. |

| • | A substantial amount of our total assets consists of intangible assets, including goodwill. We have recognized charges for goodwill impairment in the past, and during 2025, we recognized a non-cash goodwill impairment loss. If market or industry conditions deteriorate further in the future, additional impairment charges may be recognized. |

| • | The failure of any bank in which we deposit our funds could have an adverse effect on our financial condition. |

| • | Activities in our business can be hazardous and can cause injury to people or damage to property in certain circumstances. They are also subject to significant regulations, including as relates to the protection of human health, safety and the environment. These regulations continue to evolve and, in some locations, are becoming increasingly stringent. Compliance with existing or future regulations could have a material adverse effect on our reputation, business, financial condition, liquidity, and results of operations. |

| • | The introduction of or failure to introduce construction material substitutes or alternative forms of cement, ready-mix concrete, or aggregates into the market and the development of or failure to develop new construction techniques and technologies could have a material adverse effect on our business, financial condition, liquidity, and results of operations and could have an impact in our sustainability targets. |

| • | We operate in highly competitive markets with numerous players employing different competitive strategies and if we do not compete effectively, our revenues, market share, business and results of operations may be affected. |

| • | We may fail to secure certain materials required to run our business, or could secure them at higher prices, which could have a material adverse effect on our business, financial condition, liquidity, and results of operations. |

| • | Our operations and ability to source products and materials can be affected by adverse weather conditions, hydrometeorological and geological hazards such as hurricanes, flash floods, earthquakes, and/or natural disasters, including climate change, which could have a material adverse effect on our business, financial condition, liquidity, and results of operations. |

| • | We could be materially and adversely affected by any significant or prolonged disruption to our production facilities, which could impact our business, financial condition, liquidity, and results of operations. |

| • | Our insurance coverage may not cover all the risks to which we, our board members, officers and employees may be exposed or may cover them to an amount that may not be sufficient to satisfy our requirements. |

CEMEX • 2025 20-F REPORT • 20

| PART I | ||||

| • | Our success depends largely on the strategic vision and actions of Cemex, S.A.B. de C.V.’s Board of Directors and on key members of our executive management team and the availability of a specialized workforce. |

| • | Future pandemics and epidemics could materially adversely affect our financial condition and results of operations. |

Risks Relating to Our Indebtedness and Certain Other Obligations

| • | The Credit Agreements, the indentures governing our 3.125% Euro-denominated notes due 2026 (the “March 2026 Euro Notes”), 5.450% Dollar denominated notes due 2029 (the “November 2029 Dollar Notes”), 5.200% Dollar denominated notes due 2030 (the “September 2030 Dollar Notes”), 3.875% Dollar denominated notes due 2031 (the “July 2031 Dollar Notes”), and the Long-Term Notes 1 and Long-Term Notes 2 in the Mexican market (the “CEBURES” and, collectively with the March 2026 Euro Notes, the November 2029 Dollar Notes, the September 2030 Dollar Notes and the July 2031 Dollar Notes, the “Notes”) and our other debt agreements and/or instruments and other agreements contain several restrictions and covenants. Our failure to comply with such restrictions and covenants or any inability to capitalize on business opportunities or refinance our debt resulting from them could have a material adverse effect on our business and financial conditions. |

| • | We have a substantial amount of debt and other financial obligations. If we are unable to secure refinancing on favorable terms or at all, we may not be able to comply with our payment obligations upon their maturity. Our ability to comply with our principal maturities and financial covenants may depend on us implementing certain strategic initiatives, including, but not limited to, making asset sales, and there is no assurance that we will be able to implement any such initiatives or execute such sales, if needed, on terms favorable to us or at all. |

| • | We may not be able to generate sufficient cash to service our indebtedness or satisfy our short-term liquidity needs, and we may be forced to take other actions to do so, which may not be successful. |

| • | Cemex, S.A.B. de C.V.’s ability to repay debt and execute any shareholder returns is highly dependent on its subsidiaries’ ability to transfer income and dividends to us. As of the date of this annual report, we control publicly listed companies in Trinidad and Tobago and in Jamaica, where this risk is heightened. |

| • | We have to service part of our debt and other financial obligations denominated in Dollars and Euros with revenues generated in Mexican Pesos or other currencies, as we do not generate sufficient revenue in Dollars and Euros from our operations to service all our debt and other financial obligations denominated in Dollars and Euros. This could adversely affect our ability to service our obligations in the event of a devaluation of the Mexican Peso, or any of the other currencies of the countries in which we operate, compared to the Dollar and Euro. In addition, our consolidated reported results and outstanding indebtedness are significantly affected by fluctuations in exchange rates between the Dollar (our reporting currency) vis-à-vis the Mexican Peso and other significant currencies within our operations. |

| • | Increases in liabilities related to our pension plans could adversely affect our results of operations. |

| • | Our use of derivative financial instruments could negatively affect our net income and liquidity, especially in volatile and uncertain markets. |

Risks Relating to Regulatory and Legal Matters

| • | We are subject to the laws and regulations of the countries where we operate and do business. Non-compliance with laws and regulations and/or any material changes in such laws and regulations and/or any significant delays in assessing the impact and/ or adapting to such changes in laws and regulations may have a material adverse effect on our reputation, business, financial condition, liquidity, and results of operations. |

CEMEX • 2025 20-F REPORT • 21

| PART I | ||||

| • | We or our third-party providers may fail to maintain, obtain, or renew, or may experience material delays in obtaining, requisite governmental or other approvals, licenses, and permits for the conduct of our or their business. |

| • | We are subject to litigation proceedings, including, but not limited to, government investigations relating to corruption, antitrust, and other proceedings that could harm our business and our reputation. |

| • | We are subject to human rights, anti-corruption, anti-bribery, anti-money laundering, antitrust, anti-boycott, economic sanctions, anti-terrorism, trade embargoes, and import and export control laws and regulations in the countries in which we operate and do business, a considerable number of which are considered high and medium risk countries for purposes of corruption, money laundering, and other matters. Any violation of any such laws or regulations could have a material adverse impact on our reputation, results of operations, and financial condition, as well as harm our reputation. |

| • | Certain tax matters have had and may have a material adverse effect on our cash flow, financial condition, and net income, as well as on our reputation. |

| • | Our operations are subject to environmental laws and regulations, including those relating to greenhouse gas emissions, and new reporting requirements that are or could become effective and increasingly stringent. Compliance with existing or future regulations could have material adverse effect on our reputation, business, financial condition, liquidity, and results of operations. |

| • | It may be difficult to enforce civil liabilities against us or the members of Cemex, S.A.B. de C.V.’s Board of Directors, our senior management, and controlling persons. |

Risks Relating to Ownership of Our Securities

Non-Mexicans may not hold Cemex, S.A.B. de C.V.’s Series A shares directly and must have them held in a trust at all times.

Any person acquiring shares, CPOs or ADSs of Cemex, S.A.B. de C.V. should be aware that Cemex, S.A.B. de C.V.’s by-laws provide that non-Mexican investors and Mexican companies without a foreign investment-exclusion clause in their by-laws may not directly hold the Series A shares of Cemex, S.A.B. de C.V. Notwithstanding the provisions of Cemex, S.A.B. de C.V.’s by-laws, non-Mexican investors and Mexican companies without a foreign investment-exclusion clause in their by-laws may hold the Series A shares underlying Cemex, S.A.B. de C.V.’s CPOs or ADSs indirectly through Cemex, S.A.B. de C.V.’s CPO trust. Upon the early termination or expiration of the term of Cemex, S.A.B. de C.V.’s CPO trust on September 6, 2029, the Series A shares underlying the CPOs held by non-Mexican investors or by Mexican companies without a foreign investment-exclusion clause in their by-laws must be placed into a new trust similar to the current CPO trust. We cannot guarantee that a trust similar to the CPO trust will exist or that the relevant authorization for the transfer of Cemex, S.A.B. de C.V.’s Series A shares to such a trust will be obtained. In that event, such investors might be required to sell their Series A shares to a Mexican individual or corporation that has a foreign investment-exclusion clause in its by-laws, which could expose shareholders to a loss in the sale of the corresponding Series A shares and may cause the price of Cemex, S.A.B. de C.V.’s shares, CPOs and ADSs to decrease.

ADS holders may only indirectly vote the Series B shares represented by the CPOs deposited with the ADS depositary through the ADS depositary and are not entitled to vote the Series A shares represented by the CPOs deposited with the ADS depositary or to attend shareholders’ meetings.

Any person acquiring ADSs should be aware of the terms of the ADSs, the corresponding deposit agreement pursuant to which the ADSs are issued (the “Deposit Agreement”), the CPO Trust (as defined in the Deposit

CEMEX • 2025 20-F REPORT • 22

| PART I | ||||

Agreement) and Cemex, S.A.B. de C.V.’s by-laws. Under such terms, in relation to shareholders’ meetings of Cemex, S.A.B. de C.V., a holder of an ADS has the right to instruct the ADS depositary to exercise voting rights only with respect to Series B shares represented by the CPOs deposited with the depositary, but not with respect to the Series A shares represented by the CPOs deposited with the depositary. ADS holders will not be able to directly exercise their right to vote unless they withdraw the CPOs underlying their ADSs (and, in the case of non-Mexican holders, even if they do so, they may not vote the Series A shares represented by the CPOs) and may not receive voting materials in time to ensure that they are able to instruct the depositary to vote the CPOs underlying their ADSs or receive sufficient notice of a shareholders’ meeting of Cemex, S.A.B. de C.V. to permit them to withdraw their CPOs to allow them to cast their vote with respect to any specific matter. Holders of ADSs will not have the right to instruct the ADS depositary as to the exercise of voting rights in respect of Series A shares underlying CPOs held in the CPO Trust. Under the terms of the CPO Trust, Series A shares underlying CPOs held by non-Mexican nationals, including all Series A shares underlying CPOs represented by ADSs, will be voted by the CPO Trustee (as defined in the Deposit Agreement), according to the majority of all Series A shares held by Mexican nationals and Series B shares voted at a shareholders meeting of Cemex, S.A.B. de C.V. In addition, the depositary and its agents may not be able to send out voting instructions on time or carry them out in the manner an ADS holder has instructed. As a result, ADS holders may not be able to exercise their right to vote and they may lack recourse if the CPOs underlying their ADSs are not voted as they requested. ADS holders will also not be permitted to vote the CPOs underlying the ADSs directly at a shareholders’ meeting of Cemex, S.A.B. de C.V. or to appoint a proxy to do so without withdrawing the CPOs. If the ADS depositary does not receive voting instructions from a holder of ADSs in a timely manner, such holder will nevertheless be treated as having instructed the ADS depositary to give a proxy to a person the corresponding CPO trust’s technical committee, which is formed by our employees, designates, to vote the Series B shares underlying the CPOs represented by the ADSs in his/her discretion. The ADS depositary or the custodian for the CPOs on deposit may represent the CPOs at any meeting of holders of CPOs of Cemex, S.A.B. de C.V. even if no voting instructions have been received. The CPO trustee may represent the Series A shares and the Series B shares represented by the CPOs at any meeting of holders of Series A shares or Series B shares of Cemex, S.A.B. de C.V. even if no voting instructions have been received. By so attending, the ADS depositary, the custodian or the CPO trustee, as applicable, may contribute to the establishment of a quorum at a meeting of holders of CPOs, Series A shares or Series B shares, as appropriate. In addition, even though every shareholder of Cemex, S.A.B. de C.V. is entitled to attend shareholders’ meetings pursuant to Cemex, S.A.B. de C.V.’s by-laws and Mexican law, ADS holders are generally not able to attend shareholders’ meetings because they are not the registered holders of the CPOs underlying the ADSs they hold; and, consequently, they are generally unable to satisfy the procedural requirements to attend a shareholders’ meeting pursuant to Cemex, S.A.B. de C.V.’s by-laws and the CPO Trust unless they withdraw the CPOs underlying their ADSs (and, in the case of non-Mexican holders, even if they do so, they may not vote the Series A shares represented by the CPOs). Generally, as only registered holders of CPOs are able to satisfy the requirements to attend a shareholders’ meeting of Cemex, S.A.B. de C.V. pursuant to Cemex, S.A.B. de C.V.’s by-laws and the CPO Trust, only the ADS depositary (as the registered holder of the CPOs underlying ADSs) or the CPO trustee (at the direction of the ADS depositary) will be able to satisfy such requirements and attend shareholders’ meetings of Cemex, S.A.B. de C.V. to represent the CPOs underlying ADSs at a shareholders’ meeting of Cemex, S.A.B. de C.V.