As described above, the Transactions Involving TMC, including the Tender Offer for Own

Shares, involve a potential risk of conflicts of interest between Mr. Toyoda and the Company. As such, Mr. Toyoda has not participated in the Company’s consideration of the Transactions Involving TMC and discussions with the relevant

parties in his capacity representing the Company. However, his written consent for the written resolution of June 3, 2025 in lieu of a resolution of the board of directors, the written resolution of March 6, 2026 in lieu of a resolution of

the board of directors, and the written resolution of today in lieu of a resolution of the board of directors, has been obtained because, under the Companies Act, a written resolution requires the written consent of all directors who are eligible to

vote on matters relating to a proposal, and since it may be construed that Mr. Toyoda does not have a special interest prescribed in Article 369, Paragraph 2 of the Companies Act with respect to the relevant proposal and is eligible to vote,

and in such case, his written consent is also required.

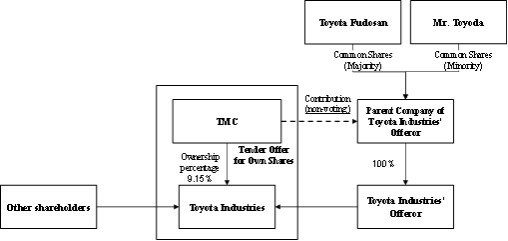

With respect to the funds required for the Tender Offer for Own Shares, the

Company plans to allocate all funds from its own capital. The Company’s consolidated on-hand liquidity (cash and cash equivalents; the same applies hereinafter for the calculation of on-hand liquidity) as of December 31, 2025, as stated in the FY2025 Third Quarter Consolidated Financial Results (IFRS) announced by the Company on February 6, 2026 (“FY2025 3Q Financial

Results”), was 7,918,907 million yen (on-hand liquidity ratio: 1.9 months) (Note 4), and is expected to be 4,262,010 million yen (on-hand liquidity

ratio: 1.0 months) (Note 5) even after appropriating the funds required for the Tender Offer for Own Shares (3,656,897 million yen). Therefore, since on-hand liquidity can be sufficiently secured, it is

considered that the Company’s financial health and security can be maintained in the future.

| |

(Note 4) |

This was obtained by dividing the Company’s consolidated on-hand

liquidity as of December 31, 2025 stated in the FY2025 3Q Financial Results by monthly operating revenue (which refers to the figure obtained by dividing the consolidated operating revenue for the nine months ended December 31 by 9 months;

hereinafter the same) calculated from the FY2025 3Q Financial Results (rounded to one decimal place). |

| |

(Note 5) |

This was obtained by deducting the amount of funds required for repurchase in the Tender Offer for Own Shares

from the Company’s consolidated on-hand liquidity as of December 31, 2025 stated in the FY2025 3Q Financial Results and dividing such figure by the monthly operating revenue calculated from the

FY2025 3Q Financial Results (rounded to one decimal place). |

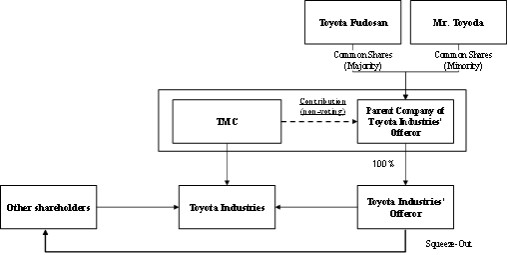

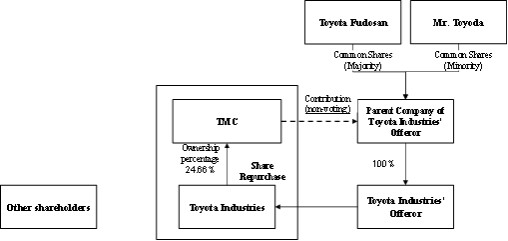

The Tender Offer for Own Shares is to be conducted as part

of the delisting of Toyota Industries, as described above. The Company believes that the significance and purpose of participating in the delisting of Toyota Industries and the series of transactions are as follows.

The Company originated from the Automobile Department, which was established in 1933 within Toyoda Automatic Loom Works, Ltd. (now Toyota

Industries Corporation), which was founded in November 1926 in Kariya-shi, Aichi to manufacture “Type G Automatic Looms” invented by Sakichi Toyoda. Ever since its founding, the Company has sought to contribute to “a more

prosperous society through the manufacture of automobiles,” operating its business with a focus on vehicle production and sales. Currently, the automotive industry is in a once-in-a-century period of change, and with its mission of “producing happiness for all,” as a member of the Toyota Group, the Company is taking on challenges to “transform into a

mobility company” and aiming to contribute to the development of the mobility industry in Japan and the world through these challenges. Mobility involves four perspectives (namely, people, goods, information, and energy); among these, the

Company is working on the evolution of cars from the perspective of movement of people and is aiming to contribute to the realization of a “mobility society” full of smiles. On the other hand, the Company believes that in order for the

Toyota Group to “transform into a mobility company,” it is necessary to focus not only on movement of people but also on movement of goods. Under these circumstances, the Company believes that Toyota Industries, which engages in

materials handling equipment business within the Toyota Group for development, manufacture, and sale of products and services of wide-ranging domains, from lift trucks to logistics equipment and systems, and which is a globally remarkable leading

company regarding movement of goods, is indispensable for these transformations, and that it is important to further strengthen its competitiveness.

22

Not for distribution in or into the United States.