UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

|

Form 6-K |

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 Or 15d-16 Of

The Securities Exchange Act Of 1934

For the month of March 2026

Commission File Number: 001-14950

ULTRAPAR HOLDINGS INC.

(Translation of Registrant’s Name into English)

Brigadeiro Luis Antonio Avenue, 1343, 9th Floor

São Paulo, SP, Brazil 01317-910

(Address of Principal Executive Offices)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F ____X____ Form 40-F ________

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Yes ________ No ____X____

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes ________ No ____X____

ULTRAPAR HOLDINGS INC.

TABLE OF CONTENTS

|

|

|

|

Ultrapar Participações S.A. and Subsidiaries |

|

(Convenience Translation into English from the Original Previously Issued in Portuguese)

Ultrapar Participações S.A.

Individual and Consolidated Financial Statements

for the Year Ended December 31, 2025 and Independent Auditor’s Report

Deloitte Touche Tohmatsu Auditores Independentes Ltda.

|

Deloitte Touche Tohmatsu Av. Dr. Chucri Zaidan, 1.240 - 4o ao 12o andares - Golden Tower 04711-130 - São Paulo - SP Brazil

Tel.: + 55 (11) 5186-1000 Fax: + 55 (11) 5181-2911 www.deloitte.com.br |

(Convenience Translation into English from the Original Previously Issued in Portuguese)

INDEPENDENT AUDITOR’S REPORT ON THE INDIVIDUAL AND CONSOLIDATED FINANCIAL STATEMENTS

To the Shareholders, Directors and Management of

Ultrapar Participações S.A.

Opinion

We have audited the accompanying individual and consolidated financial statements of Ultrapar Participações S.A. (“Company”), identified as Parent and Consolidated, respectively, which comprise the individual and consolidated statements of financial position as at December 31, 2025, and the related individual and consolidated statements of income, of comprehensive income, of changes in equity and of cash flows for the year then ended, and notes to the financial statements, including material accounting policies.

In our opinion, the individual and consolidated financial statements referred to above present fairly, in all material respects, the individual and consolidated financial position of Ultrapar Participações S.A. as at December 31, 2025, and its individual and consolidated financial performance and its individual and consolidated cash flows for the year then ended in accordance with accounting practices adopted in Brazil and International Financial Reporting Standards (“IFRS Accounting Standards”) issued by the International Accounting Standards Board (“IASB”).

Basis for opinion

We conducted our audit in accordance with Brazilian and International Auditing Standards. Our responsibilities under those standards are further described in the “Auditor’s responsibilities for the audit of the individual and consolidated financial statements” section of our report. We are independent of the Company in accordance with the relevant ethical requirements set out in the Code of Ethics for Professional Accountants and the professional standards issued by the Brazilian Federal Accounting Council, applicable to audits of financial statements of public interest entities in Brazil. We also comply with other ethical responsibilities in accordance with these standards. We believe that the audit evidence obtained is sufficient and appropriate to provide a basis for our opinion.

Key audit matters

Key audit matters (“KAM”) are those matters that, in our professional judgment, were of most significance in our audit of the current year. These matters were addressed in the context of our audit of the individual and consolidated financial statements as a whole, and in forming our opinion thereon, and, therefore, we do not provide a separate opinion on these matters.

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (DTTL), its global network of member firms, and their related entities (collectively, the “Deloitte organization”). DTTL

(also referred to as “Deloitte Global”) and each of its member firms and related entities are legally separate and independent entities, which cannot obligate or bind each other in respect

of third parties. DTTL and each DTTL member firm and related entity is liable only for its own acts and omissions, and not those of each other. DTTL does not provide services to clients.

Please see www.deloitte.com/about to learn more.

Deloitte provides leading professional services to nearly 90% of the Fortune Global 500® and thousands of private companies. Our people deliver measurable and lasting results that

help reinforce public trust in capital markets and enable clients to transform and thrive. Building on its 180-year history, Deloitte spans more than 150 countries and territories. Learn

how Deloitte’s approximately 470,000 people worldwide make an impact that matters at www.deloitte.com.

© 2026. For information, contact Deloitte Global.

Business Combination - Hidrovias

Why is it a KAM?

As disclosed in note 28 to the individual and consolidated financial statements, in May 2025, the Company acquired control of Hidrovias do Brasil S.A., now holding 50.15% of its capital. This transaction requires, in accordance with the applicable accounting standards, the recognition by the Company of the business combination, including the measurement, at fair value, of the assets acquired and liabilities assumed, as well as the determination and recognition of goodwill. The determination of these values involves valuation techniques and subjective estimates – such as cash flow projections, discount rates, useful lives and operational assumptions – that require significant judgments by the Management.

This topic was considered a key audit matter due to: (i) the materiality of the balances involved; (ii) the complexity of the required estimates; (iii) the relevant judgment by the Management in concluding that it was a business combination in phases, considering that the Parent Company already had significant influence over Hidrovias before the acquisition of control; and (iv) the high degree of subjectivity inherent to the assumptions used in the measurement of fair value and in the determination of goodwill.

How the Key Audit Matter Was Addressed in the Audit

Our audit procedures included, among others: (i) evaluation of design and implementation of internal controls over the method, assumptions and data used in the business combination; (ii) evaluation of the accounting policy applied to the business combination and the identification of the assets and liabilities recorded at fair value; (iii) understanding and reading of the documents and contracts of the acquisition transactions; (iv) involvement of our valuation specialists in the evaluation of the methodologies used, (v) evaluation of the relevant data and assumptions used by the Management; (vi) recalculation of the revaluation of the investment in the Parent Company; (vii) involvement of our accounting standards experts for the evaluation of the business combination in phases; and (v) review and evaluation of the disclosures included in the individual and consolidated financial statements;

Based on the evidence obtained through our procedures described above, we consider that the accounting treatment adopted by the Management for the business combination of the subsidiary Hidrovias and the respective disclosures presented in the notes are acceptable in the context of the individual and consolidated financial statements taken as a whole.

Recoverability of tax credits (PIS and COFINS)

Why is it a KAM?

As disclosed in the Note nº 7.a.2, as of December 31, 2025, the Company carries tax credits related to PIS and COFINS (Federal Value Added Taxes) at R$ 3,863,682 may be utilized for offset against other federal taxes or may be refunded by the Federal Revenue Service through requests if they are filed within the applicable regulatory period.

The recognition and measurement of PIS and COFINS credits for the Company’s subsidiary Ipiranga Produtos de Petróleo S.A. require a high degree of judgment by Management, given the complexity underlying the interpretations of the applicable tax laws, as well as the uncertainties involving the expected realization of amounts and considerable efforts made by Management in preparing the calculations used to measure and to recognize those tax credits.

Such matter was considered a key audit matter due to (i) the significance of the amounts involved, and (ii) the complexity and high degree of judgment involved in assessing and challenging Management’s assumptions and judgments regarding the realizability of tax credits.

© 2026. For information, contact Deloitte Global.

How the Key Audit Matter Was Addressed in the Audit

Our audit procedures included, among others: (i) evaluation of design and implementation of internal controls over the method, assumptions and data used in the projections to support the realization of the tax credits; (ii) the analysis, challenges and tests on the methodology and assumptions used for the projections that support the realization of the credits, including inquiries to the business, treasury and controllership areas about the assumptions and projections that support the projected results and historical performance, retrospective analysis of results, history of offsets and tax refunds, including the evaluation of contradictory evidence; (iii) inquiries to the Management; and (vi) the analysis and evaluation of the disclosures made in the individual and consolidated financial statements.

Based on the evidence obtained from performing our procedures described previously, we consider that the accounting treatment applied to the aforesaid transaction and related disclosures made in the notes are acceptable in the context of the individual and consolidated financial statements taken as a whole.

Other matters

Statements of value added

The individual and consolidated statements of value added for the year ended December 31, 2025 prepared under the responsibility of the Company’s Management and disclosed as supplemental information for purposes of the IFRS Accounting Standards, were subject to audit procedures performed together with the audit of the Company’s financial statements. In forming our opinion, we assess whether these statements of value added are reconciled with the financial statements and accounting records, as applicable, and whether their form and content are in accordance with the criteria set out in technical pronouncement CPC 09 - Statement of Value Added. In our opinion, these statements of value added were appropriately prepared, in all material respects, in accordance with the criteria set out in such technical pronouncement and are consistent in relation to the individual and consolidated financial statements taken as a whole.

Other information accompanying the individual and consolidated financial statements and the independent auditor’s report

The Company's Management is responsible for this other information that comprises the Management Report.

Our opinion on the individual and consolidated financial statements does not cover the Management Report and we do not express any form of audit conclusion thereon.

In connection with our audit of the individual and consolidated financial statements, our responsibility is to read the Management Report and, in doing so, consider whether this report is materially inconsistent with the financial statements or our knowledge obtained in the audit or otherwise appears to be materially misstated. If, based on the work we have performed, we conclude that there is a material misstatement in the Management Report, we are required to report that fact. We have nothing to report in this regard.

Responsibilities of Management and those charged with governance for the individual and consolidated financial statements

Management is responsible for the preparation and fair presentation of the individual and consolidated financial statements in accordance with accounting practices adopted in Brazil and IFRS Accounting Standards, issued by IASB, and for such internal control as Management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the individual and consolidated financial statements, Management is responsible for assessing the Company’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless Management either intends to liquidate the Company and its subsidiaries or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Company’s and its subsidiaries’ financial reporting process.

© 2026. For information, contact Deloitte Global.

| 8 |

Auditor’s responsibilities for the audit of the individual and consolidated financial statements

Our objectives are to obtain reasonable assurance about whether the individual and consolidated financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with Brazilian and International Standards on Auditing will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with Brazilian and International Standards on Auditing, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

- Identify and assess the risks of material misstatement of the individual and consolidated financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

- Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the internal control of the Company and its subsidiaries.

- Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by Management.

- Conclude on the appropriateness of Management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the ability of the Company and its subsidiaries to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the individual and consolidated financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the Company and its subsidiaries to cease to continue as a going concern.

- Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the individual and consolidated financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

- Plan and perform the group audit to obtain appropriate and sufficient audit evidence regarding the financial information of the entities or business units within the group to express an opinion on the consolidated financial statements. We are responsible for the direction, supervision and review of the audit work performed for purposes of the group audit. We remain solely responsible for our audit opinion.

© 2026. For information, contact Deloitte Global.

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any eventual significant deficiencies in internal control that we identify during our audit.

We also provide those charged with governance a statement that we have complied with the relevant ethical requirements, including the applicable independence requirements, and we have communicated all possible relationships or matter that may considerably affect our independence, including, when applicable, the respective safeguards.

From the matters communicated with those charged with governance, we determine those matters that were of most significance in the audit of the financial statements of the current period and are therefore the key audit matters. We describe these matters in our auditor’s report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of such communication.

The accompanying individual and consolidated financial statements have been translated into English for the convenience of readers outside Brazil.

São Paulo, March 4, 2026

| DELOITTE TOUCHE TOHMATSU | Daniel Corrêa de Sá |

| Auditores Independentes Ltda. | Engagement Partner |

© 2026. For information, contact Deloitte Global.

|

Ultrapar Participações S.A. and Subsidiaries |

|

|

Statements of financial position as of December 31, 2025 and 2024

|

|

| (In thousands of Brazilian Reais) |

|

|

|

Parent |

|

Consolidated |

|||||

|

|

Note |

12/31/2025 |

12/31/2024 |

|

12/31/2025 |

12/31/2024 |

|||

|

Assets |

|

|

|

|

|

|

|||

|

Current assets |

|

|

|

|

|

|

|||

|

Cash and cash equivalents |

4.a |

42,145 |

4,186 |

|

3,175,125 |

2,071,593 |

|||

|

Financial investments |

4.b |

6,515 |

20,100 |

|

3,851,758 |

2,306,927 |

|||

|

Derivative financial instruments |

26.f |

‐ |

‐ |

|

127,254 |

246,084 |

|||

|

Trade receivables |

5.a |

‐ |

‐ |

|

3,703,954 |

3,540,266 |

|||

|

Reseller financing |

5.a |

‐ |

‐ |

|

573,093 |

511,979 |

|||

|

Inventories |

6 |

‐ |

‐ |

|

4,244,164 |

3,917,076 |

|||

|

Recoverable taxes |

7.a |

1,589 |

1,323 |

|

1,685,426 |

2,040,008 |

|||

|

Recoverable income and social contribution taxes |

7.b |

25,490 |

16,734 |

|

317,963 |

151,930 |

|||

|

Energy trading futures contracts |

26.h |

‐ |

‐ |

|

371,241 |

141,257 |

|||

|

Dividends receivable |

|

- |

‐ |

|

923 |

3,415 |

|||

|

Other receivables and other assets |

|

107,552 |

95,859 |

|

294,068 |

294,769 |

|||

|

Prepaid expenses |

|

7,519 |

5,506 |

|

165,392 |

163,846 |

|||

|

Contractual assets with customers - exclusivity rights |

10 |

‐ |

‐ |

|

666,109 |

658,571 |

|||

|

Total current assets |

|

190,810 |

143,708 |

|

19,176,470 |

16,047,721 |

|||

|

|

|

|

|

|

|

|

|||

|

Non-current assets |

|

|

|

|

|

|

|||

|

Financial investments |

4.b |

1,411,213 |

300,001 |

|

2,381,597 |

2,819,179 |

|||

|

Derivative financial instruments |

26.f |

‐ |

‐ |

|

773,063 |

585,294 |

|||

|

Trade receivables |

5.a |

‐ |

‐ |

|

33,282 |

27,003 |

|||

|

Reseller financing |

5.a |

‐ |

‐ |

|

800,927 |

766,045 |

|||

|

Related parties |

8 |

7,524 |

7,076 |

|

105,196 |

48,309 |

|||

|

Deferred income and social contribution taxes |

9.a |

164,441 |

142,630 |

|

1,007,291 |

936,941 |

|||

|

Recoverable taxes |

7.a |

74 |

74 |

|

3,717,815 |

2,650,269 |

|||

|

Recoverable income and social contribution taxes |

7.b |

10,914 |

7,196 |

|

346,093 |

346,137 |

|||

|

Energy trading futures contracts |

26.h |

‐ |

‐ |

|

724,121 |

263,438 |

|||

|

Escrow deposits |

18.a |

14,375 |

12,615 |

|

471,609 |

446,076 |

|||

|

Indemnification asset - business combination |

18.c |

‐ |

‐ |

|

92,524 |

126,098 |

|||

|

Other receivables and other assets |

|

1,743 |

2,607 |

|

185,726 |

117,076 |

|||

|

Prepaid expenses |

|

21,459 |

18,989 |

|

80,643 |

40,904 |

|||

|

Contractual assets with customers - exclusivity rights |

10 |

‐ |

‐ |

|

1,518,987 |

1,473,331 |

|||

|

Investments in subsidiaries, joint ventures and associates |

11 |

13,987,459 |

14,898,466 |

|

521,381 |

2,148,633 |

|||

|

Right-of-use assets, net |

12 |

5,619 |

7,664 |

|

1,928,694 |

1,671,324 |

|||

|

Property, plant and equipment, net |

13 |

63,323 |

68,447 |

|

12,167,097 |

7,135,966 |

|||

|

Intangible assets, net |

14 |

276,157 |

273,674 |

|

3,316,478 |

1,908,330 |

|||

|

Total non-current assets |

|

15,964,301 |

15,739,439 |

|

30,172,524 |

23,510,353 |

|||

|

Total assets |

|

16,155,111 |

15,883,147 |

|

49,348,994 |

39,558,074 |

|||

|

Ultrapar Participações S.A. and Subsidiaries |

|

|

Statements of financial position as of December 31, 2025 and 2024 |

|

| (In thousands of Brazilian Reais) |

|

|

|

Parent |

|

Consolidated |

|||||

|

|

Note |

12/31/2025 |

12/31/2024 |

|

12/31/2025 |

12/31/2024 |

|||

|

Liabilities |

|

|

|

|

|

|

|||

|

Current liabilities |

|

|

|

|

|

|

|||

|

Trade payables |

16 |

27,779 |

25,423 |

|

4,643,344 |

3,518,385 |

|||

|

Trade payables – reverse factoring |

|

‐ |

‐ |

|

3,785 |

1,014,504 |

|||

|

Loans, financing and debentures |

15 |

‐ |

‐ |

|

4,251,131 |

3,478,673 |

|||

|

Derivative financial instruments |

26.f |

‐ |

‐ |

|

246,064 |

74,087 |

|||

|

Salaries and related charges |

|

47,379 |

44,191 |

|

576,674 |

480,285 |

|||

|

Taxes payable |

|

379 |

903 |

|

236,928 |

151,230 |

|||

|

Energy trading futures contracts |

26.h |

‐ |

‐ |

|

303,455 |

66,729 |

|||

|

Dividends payable |

20.h |

21,738 |

293,165 |

|

23,073 |

327,471 |

|||

|

Income and social contribution taxes payable |

|

6,508 |

175 |

|

358,685 |

322,074 |

|||

|

Post-employment benefits |

17.b |

‐ |

‐ |

|

19,067 |

24,098 |

|||

|

Provisions for tax, civil and labor risks |

18.a |

220 |

431 |

|

49,175 |

47,788 |

|||

|

Leases payable |

12.b |

2,921 |

3,012 |

|

343,725 |

316,460 |

|||

|

Financial liabilities of customers |

|

‐ |

‐ |

|

63,445 |

117,090 |

|||

|

Other payables |

|

1,044 |

2,069 |

|

728,793 |

554,327 |

|||

|

Total current liabilities |

|

107,968 |

369,369 |

|

11,847,344 |

10,493,201 |

|||

|

|

|

|

|

|

|

|

|||

|

Non-current liabilities |

|

|

|

|

|

|

|||

|

Loans, financing and debentures |

15 |

‐ |

‐ |

|

15,842,130 |

10,381,837 |

|||

|

Derivative financial instruments |

26.f |

‐ |

‐ |

|

334,851 |

367,513 |

|||

|

Energy trading futures contracts |

26.h |

‐ |

‐ |

|

431,418 |

48,047 |

|||

|

Related parties |

8 |

2,875 |

2,875 |

|

2,875 |

3,516 |

|||

|

Deferred income and social contribution taxes |

9.a |

‐ |

‐ |

|

637,897 |

132,825 |

|||

|

Post-employment benefits |

17.b |

1,776 |

1,517 |

|

196,549 |

198,778 |

|||

|

Provisions for tax, civil and labor risks |

18.a |

131,923 |

197,396 |

|

485,439 |

610,572 |

|||

|

Leases payable |

12.b |

3,706 |

5,698 |

|

1,395,908 |

1,168,692 |

|||

|

Financial liabilities of customers |

|

‐ |

‐ |

|

10,881 |

63,135 |

|||

|

Subscription warrants – indemnification |

19 |

53,911 |

47,745 |

|

53,911 |

47,745 |

|||

|

Provision for loss on investment |

11 |

130,897 |

68,530 |

|

76,059 |

349 |

|||

|

Other payables |

|

55,783 |

31,299 |

|

303,115 |

218,420 |

|||

|

Total non-current liabilities |

|

380,871 |

355,060 |

|

19,771,033 |

13,241,429 |

|||

|

|

|

|

|

|

|

|

|||

|

Equity |

|

|

|

|

|

|

|||

|

Share capital |

20.a |

7,987,100 |

6,621,752 |

|

7,987,100 |

6,621,752 |

|||

|

Equity instrument granted |

20.b |

144,694 |

108,253 |

|

144,694 |

108,253 |

|||

|

Capital reserve |

20.d |

617,009 |

612,048 |

|

617,009 |

612,048 |

|||

|

Treasury shares |

20.c |

(822,526) |

(596,400) |

|

(822,526) |

(596,400) |

|||

|

Revaluation reserve |

20.e |

3,476 |

3,632 |

|

3,476 |

3,632 |

|||

|

Profit reserves |

20.f |

7,662,403 |

8,195,221 |

|

7,662,403 |

8,195,221 |

|||

|

Accumulated other comprehensive income |

|

223,355 |

214,212 |

|

223,355 |

214,212 |

|||

|

Acquisition of shares from shareholders |

28.b |

(149,239) |

‐ |

|

(149,239) |

‐ |

|||

|

Equity attributable to: |

|

|

|

|

|

|

|||

|

Ultrapar shareholders’ equity |

|

15,666,272 |

15,158,718 |

|

15,666,272 |

15,158,718 |

|||

|

Non-controlling interests |

11 |

‐ |

‐ |

|

2,064,345 |

664,726 |

|||

|

Total equity |

|

15,666,272 |

15,158,718 |

|

17,730,617 |

15,823,444 |

|||

|

Total liabilities and equity |

|

16,155,111 |

15,883,147 |

|

49,348,994 |

39,558,074 |

|||

The accompanying notes are an integral part of the financial statements.

|

Ultrapar Participações S.A. and Subsidiaries |

|

| For the years ended December 31, 2025 and 2024 | |

| (In thousands of Brazilian Reais, except earnings per thousand shares) |

|

|

|

Parent |

|

Consolidated |

|||||

|

|

Note |

01/01/2025 to 12/31/2025 |

01/01/2024 to 12/31/2024 |

|

01/01/2025 to 12/31/2025 |

01/01/2024 to 12/31/2024 |

|||

|

Continuing operations |

|

|

|

|

|

|

|||

|

Net revenue from sales and services |

21 |

‐ |

‐ |

|

142,369,540 |

133,498,913 |

|||

|

Cost of products and services sold |

22 |

‐ |

‐ |

|

(133,010,699) |

(123,811,893) |

|||

|

|

|

|

|

|

|

|

|||

|

Gross profit |

|

‐ |

‐ |

|

9,358,841 |

9,687,020 |

|||

|

|

|

|

|

|

|

|

|||

|

Operating income (expenses) |

|

|

|

|

|

|

|||

|

Selling and marketing |

22 |

‐ |

‐ |

|

(2,517,894) |

(2,499,547) |

|||

|

General and administrative |

22 |

(53,165) |

(48,834) |

|

(2,249,413) |

(1,872,092) |

|||

|

Results from disposal of assets |

|

90 |

59 |

|

99,570 |

171,837 |

|||

|

Other operating income (expenses), net |

22 |

55,637 |

18,343 |

|

354,664 |

(414,092) |

|||

|

|

|

|

|

|

|

|

|||

|

Operating result before share of profit (loss) of subsidiaries, joint ventures and associates, financial result and income and social contribution taxes |

|

2,562 |

(30,432) |

|

5,045,768 |

5,073,126 |

|||

|

Share of profit (loss) of subsidiaries, joint ventures and associates |

11 |

2,549,952 |

2,380,009 |

|

(155,999) |

(127,182) |

|||

|

Amortization of fair value adjustments on associates acquisition |

11 |

‐ |

‐ |

|

(1,611) |

(2,493) |

|||

|

Gain on acquisition of control of associate |

28.b |

‐ |

‐ |

|

91,105 |

‐ |

|||

|

Total share of profit (loss) of subsidiaries, joint ventures and associates |

|

2,549,952 |

2,380,009 |

|

(66,505) |

(129,675) |

|||

|

|

|

|

|

|

|

|

|||

|

Income before financial result and income and social contribution taxes |

|

2,552,514 |

2,349,577 |

|

4,979,263 |

4,943,451 |

|||

|

|

|

|

|

|

|

|

|||

|

Financial income |

23 |

45,798 |

68,869 |

|

1,580,842 |

881,074 |

|||

|

Financial expenses |

23 |

(19,835) |

(20,959) |

|

(2,748,196) |

(1,813,008) |

|||

|

Financial result, net |

23 |

25,963 |

47,910 |

|

(1,167,354) |

(931,934) |

|||

|

Income before income and social contribution taxes |

|

2,578,477 |

2,397,487 |

|

3,811,909 |

4,011,517 |

|||

|

|

|

|

|

|

|

|

|||

|

Income and social contribution taxes |

|

|

|

|

|

|

|||

|

Current |

9.b |

(25,311) |

(13,217) |

|

(1,054,797) |

(1,124,664) |

|||

|

Deferred |

9.b |

21,840 |

(21,530) |

|

(8,892) |

(360,953) |

|||

|

|

|

(3,471) |

(34,747) |

|

(1,063,689) |

(1,485,617) |

|||

|

|

|

|

|

|

|

|

|||

|

Net income from continuing operations |

|

2,575,006 |

2,362,740 |

|

2,748,220 |

2,525,900 |

|||

|

|

|

|

|

|

|

|

|||

|

Discontinued operations |

|

|

|

|

|

|

|||

|

Net income (loss) from discontinued operations |

29 |

(121,153) |

‐ |

|

(206,312) |

‐ |

|||

|

|

|

|

|

|

|

|

|||

|

Net income for the year |

|

2,453,853 |

2,362,740 |

|

2,541,908 |

2,525,900 |

|||

|

Income attributable to: |

|

|

|

|

|

|

|||

|

Shareholders of Ultrapar |

|

2,453,853 |

2,362,740 |

|

2,453,853 |

2,362,740 |

|||

|

Non-controlling interests in subsidiaries |

11 |

‐ |

‐ |

|

88,055 |

163,160 |

|||

|

|

|

|

|

|

|

|

|||

|

Total earnings per share from continuing operations (based on the weighted average number of shares outstanding) – R$ |

|

|

|

|

|

|

|||

|

Basic |

24 |

2.4027 |

2.1438 |

|

2.4027 |

2.1438 |

|||

|

Diluted |

24 |

2.3513 |

2.1141 |

|

2.3513 |

2.1141 |

|||

|

|

|

|

|

|

|

|

|||

|

Earnings per share from discontinued operations (based on the weighted average number of shares outstanding) – R$ |

|

|

|

|

|

|

|||

|

Basic |

24 |

(0.1130) |

‐ |

|

(0.1130) |

‐ |

|||

|

Diluted |

24 |

(0.1106) |

‐ |

|

(0.1106) |

‐ |

|||

|

|

|

|

|

|

|

|

|||

|

Total earnings per share (based on the weighted average number of shares outstanding) – R$ |

|

|

|

|

|

|

|||

|

Basic |

24 |

2.2896 |

2.1438 |

|

2.2896 |

2.1438 |

|||

|

Diluted |

24 |

2.2407 |

2.1141 |

|

2.2407 |

2.1141 |

|||

The accompanying notes are an integral part of the financial statements.

|

Ultrapar Participações S.A. and Subsidiaries |

|

| For the years ended December 31, 2025 and 2024 | |

| (In thousands of Brazilian Reais) |

|

|

|

|

Parent |

|

Consolidated |

||||

|

|

Note |

|

01/01/2025 to 12/31/2025 |

01/01/2024 to 12/31/2024 |

|

01/01/2025 to 12/31/2025 |

01/01/2024 to 12/31/2024 |

||

|

Net income for the year, attributable to shareholders of Ultrapar |

|

|

2,453,853 |

2,362,740 |

|

2,453,853 |

2,362,740 |

||

|

Net income for the year, attributable to non-controlling interests in subsidiaries |

|

|

‐ |

‐ |

|

88,055 |

163,160 |

||

|

Net income for the year |

|

|

2,453,853 |

2,362,740 |

|

2,541,908 |

2,525,900 |

||

|

|

|

|

|

|

|

|

|

||

|

Items that will be subsequently reclassified to profit or loss: |

|

|

|

|

|

|

|

||

|

Fair value adjustments of financial instruments of subsidiaries, joint ventures and associates, net of income and social contribution taxes |

20.g |

|

65,526 |

8,495 |

|

117,760 |

8,495 |

||

|

Translation adjustments of subsidiaries |

20.g |

|

(57,479) |

36,134 |

|

(78,712) |

36,134 |

||

|

|

|

|

|

|

|

|

|

||

|

Items that will not be subsequently reclassified to profit or loss: |

|

|

|

|

|

|

|

||

|

Actuarial gains of post-employment benefits, net of income and social contribution taxes |

20.g |

|

1,096 |

15,475 |

|

3,865 |

25,218 |

||

|

|

|

|

|

|

|

|

|

||

|

Total comprehensive income for the year |

|

|

2,462,996 |

2,422,844 |

|

2,584,821 |

2,595,747 |

||

|

|

|

|

|

|

|

|

|

||

|

Total comprehensive income for the year attributable to shareholders of Ultrapar |

|

|

2,462,996 |

2,422,844 |

|

2,462,996 |

2,422,844 |

||

|

Total comprehensive income for the year attributable to non-controlling interests in subsidiaries |

|

|

‐ |

‐ |

|

121,825 |

172,903 |

||

The accompanying notes are an integral part of the financial statements.

|

Ultrapar Participações S.A. and Subsidiaries |

|

| For the years ended December 31, 2025 and 2024 | |

| (In thousands of Brazilian Reais, except dividends per share) |

|

|

|

|

|

|

|

|

|

|

|

|

Equity attributable to: |

|

|

||||||||||||

|

|

Note |

Share capital |

Equity instrument granted |

Capital reserve |

Treasury shares |

Revaluation reserve |

Profit reserves |

Accumulated other comprehensive income |

Acquisition of shares from shareholders |

Retained earnings |

Shareholders of Ultrapar |

|

Non-controlling interests (i) |

|

Total equity |

||||||||||

|

Balance as of December 31, 2023 |

|

6,621,752 |

75,925 |

597,828 |

(470,510) |

3,802 |

6,523,590 |

154,108 |

‐ |

‐ |

13,506,495 |

|

523,331 |

|

14,029,826 |

||||||||||

|

Net income for the year |

- |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

2,362,740 |

2,362,740 |

|

163,160 |

|

2,525,900 |

||||||||||

|

Other comprehensive income |

- |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

60,104 |

‐ |

‐ |

60,104 |

|

9,743 |

|

69,847 |

||||||||||

|

Total comprehensive income for the year |

|

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

60,104 |

‐ |

2,362,740 |

2,422,844 |

|

172,903 |

|

2,595,747 |

||||||||||

|

Issuance of shares related to the subscription warrants - indemnification |

- |

‐ |

‐ |

6,452 |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

6,452 |

|

‐ |

|

6,452 |

||||||||||

|

Equity instrument granted |

8.d; 20.b |

‐ |

32,328 |

2,069 |

23,055 |

‐ |

‐ |

‐ |

‐ |

‐ |

57,452 |

|

6 |

|

57,458 |

||||||||||

|

Purchase of treasury shares |

- |

‐ |

‐ |

‐ |

(148,945) |

‐ |

‐ |

‐ |

‐ |

‐ |

(148,945) |

|

‐ |

|

(148,945) |

||||||||||

|

Realization of revaluation reserve of subsidiaries |

- |

‐ |

‐ |

‐ |

‐ |

(170) |

‐ |

‐ |

‐ |

170 |

‐ |

|

‐ |

|

‐ |

||||||||||

|

Setting up of reserves |

20.a |

‐ |

‐ |

5,699 |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

5,699 |

|

(36) |

|

5,663 |

||||||||||

|

Shareholder transaction - changes of ownership interest |

- |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

534 |

534 |

|

309 |

|

843 |

||||||||||

|

Dividends prescribed |

- |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

3,369 |

3,369 |

|

‐ |

|

3,369 |

||||||||||

|

Non-controlling interest in acquired subsidiary |

|

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

|

112,160 |

|

112,160 |

||||||||||

|

Allocation of net income: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

Legal reserve |

20.f |

‐ |

‐ |

‐ |

‐ |

‐ |

118,137 |

‐ |

‐ |

(118,137) |

‐ |

|

‐ |

|

‐ |

||||||||||

|

Investments statutory reserve |

20.f |

‐ |

‐ |

‐ |

‐ |

‐ |

1,479,404 |

‐ |

‐ |

(1,479,404) |

- |

|

‐ |

|

- |

||||||||||

|

Additional minimum mandatory dividend for the year (R$ 0.26 per share) |

20.h |

- |

- |

- |

- |

- |

- |

- |

- |

(285,180) |

(285,180) |

|

- |

|

(285,180) |

||||||||||

|

Additional dividends (R$ 0.19 per share) |

20.f |

‐ |

‐ |

‐ |

‐ |

‐ |

208,121 |

‐ |

‐ |

(208,121) |

‐ |

|

‐ |

|

‐ |

||||||||||

|

Interest on equity attributable to non-controlling interests |

|

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

|

(105,590) |

|

(105,590) |

||||||||||

|

Dividends attributable to non-controlling interests |

- |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

|

(38,357) |

|

(38,357) |

||||||||||

|

Interim dividends (R$ 0.25 per share) |

20.h |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

(275,971) |

(275,971) |

|

‐ |

|

(275,971) |

||||||||||

|

Approval of additional dividends by the Ordinary General Shareholders’ Meeting |

20.h |

‐ |

‐ |

‐ |

‐ |

‐ |

(134,031) |

‐ |

‐ |

‐ |

(134,031) |

|

‐ |

|

(134,031) |

||||||||||

|

Balance as of December 31, 2024 |

|

6,621,752 |

108,253 |

612,048 |

(596,400) |

3,632 |

8,195,221 |

214,212 |

‐ |

‐ |

15,158,718 |

|

664,726 |

|

15,823,444 |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

Net income for the year |

|

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

2,453,853 |

2,453,853 |

|

88,055 |

|

2,541,908 |

||||||||||

|

Other comprehensive income |

|

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

9,143 |

‐ |

‐ |

9,143 |

|

33,770 |

|

42,913 |

||||||||||

|

Total comprehensive income for the year |

|

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

9,143 |

‐ |

2,453,853 |

2,462,996 |

|

121,825 |

|

2,584,821 |

||||||||||

|

Issuance of shares related to the subscription warrants - indemnification |

|

‐ |

‐ |

7,863 |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

7,863 |

|

‐ |

|

7,863 |

||||||||||

|

Equity instrument granted |

8.d; 20.b |

‐ |

36,441 |

(7,351) |

40,828 |

‐ |

‐ |

‐ |

‐ |

‐ |

69,918 |

|

(1,563) |

|

68,355 |

||||||||||

|

Purchase of treasury shares |

20.c |

‐ |

‐ |

‐ |

(266,954) |

‐ |

‐ |

‐ |

‐ |

‐ |

(266,954) |

|

‐ |

|

(266,954) |

||||||||||

|

Realization of revaluation reserve |

- |

‐ |

‐ |

‐ |

‐ |

(156) |

‐ |

‐ |

‐ |

156 |

‐ |

|

‐ |

|

‐ |

||||||||||

|

Capital increase with reserves |

20.a |

1,365,348 |

‐ |

‐ |

‐ |

‐ |

(1,365,348) |

‐ |

‐ |

‐ |

‐ |

|

‐ |

|

‐ |

||||||||||

|

Capital increase of non-controlling shareholders |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

|

12,184 |

|

12,184 |

||||||||||

|

Shareholder transaction |

28.b |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

(149,239) |

(45) |

(149,284) |

|

‐ |

|

(149,284) |

||||||||||

|

Setting up of reserves |

20.d |

‐ |

‐ |

4,449 |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

4,449 |

|

‐ |

|

4,449 |

||||||||||

|

Non-controlling interest in the equity of acquired subsidiary – Hidrovias |

28.b |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

|

1,658,270 |

|

1,658,270 |

||||||||||

|

Variation in change of ownership interest of non-controlling shareholders |

- |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

|

(190,462) |

|

(190,462) |

||||||||||

|

Non-controlling interest in the equity of acquired subsidiary |

- |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

|

45,633 |

|

45,633 |

||||||||||

|

Payment of dividends for the prior year |

20.h |

‐ |

‐ |

‐ |

‐ |

‐ |

(208,121) |

‐ |

‐ |

‐ |

(208,121) |

|

‐ |

|

(208,121) |

||||||||||

|

Allocation of net income: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

Legal reserve |

20.f |

‐ |

‐ |

‐ |

‐ |

‐ |

122,692 |

‐ |

‐ |

(122,692) |

‐ |

|

- |

|

- |

||||||||||

|

Investments statutory reserve |

20.f |

‐ |

‐ |

‐ |

‐ |

‐ |

917,959 |

‐ |

‐ |

(917,959) |

‐ |

|

- |

|

- |

||||||||||

|

Minimum mandatory dividends for the year |

20.h |

‐ |

‐ |

‐ |

‐ |

‐ |

- |

‐ |

‐ |

(582,790) |

(582,790) |

|

- |

|

(582,790) |

||||||||||

|

Additional dividends to the minimum mandatory dividends |

20.h |

‐ |

‐ |

‐ |

‐ |

‐ |

- |

‐ |

‐ |

(830,523) |

(830,523) |

|

- |

|

(830,523) |

||||||||||

|

Dividends and interest on equity attributable to non-controlling interests |

- |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

‐ |

|

(246,268) |

|

(246,268) |

||||||||||

|

Balance as of December 31, 2025 |

|

7,987,100 |

144,694 |

617,009 |

(822,526) |

3,476 |

7,662,403 |

223,355 |

(149,239) |

- |

15,666,272 |

|

2,064,345 |

|

17,730,617 |

||||||||||

(i) Are substantially represented by non-controlling shareholders of Iconic and Hidrovias.

The accompanying notes are an integral part of the financial statements.

|

Ultrapar Participações S.A. and Subsidiaries |

|

| For the years ended December 31, 2025 and 2024 | |

| (In thousands of Brazilian Reais) |

|

|

|

Parent |

|

Consolidated |

|||||

|

|

Note |

12/31/2025 |

12/31/2024 |

|

12/31/2025 |

12/31/2024 |

|||

|

CASH FLOWS FROM CONTINUING OPERATING ACTIVITIES |

|

|

|

|

|

|

|||

|

Net income from continuing operations |

|

2,575,006 |

2,362,740 |

|

2,748,220 |

2,525,900 |

|||

|

Adjustments to reconcile net income to cash provided (consumed) by operating activities |

|

|

|

|

|

|

|||

|

Share of profit (loss) of subsidiaries, joint ventures and associates and amortization of fair value adjustments on associates acquisition |

11 |

(2,549,952) |

(2,380,009) |

|

157,610 |

129,675 |

|||

|

Amortization of contractual assets with customers - exclusivity rights |

10 |

‐ |

‐ |

|

469,766 |

555,083 |

|||

|

Amortization of right-of-use assets |

12 |

2,955 |

2,864 |

|

367,129 |

312,060 |

|||

|

Depreciation and amortization |

13; 14 |

14,491 |

15,808 |

|

1,219,034 |

900,673 |

|||

|

Interest, monetary variations and foreign exchange variations |

|

25,506 |

13,122 |

|

1,472,633 |

1,557,814 |

|||

|

Current and deferred income and social contribution taxes |

9.b |

3,471 |

34,747 |

|

1,063,689 |

1,485,617 |

|||

|

Gain (loss) on disposal or write-off of assets |

|

(90) |

(35,298) |

|

(110,259) |

(207,076) |

|||

|

Equity instrument granted |

|

22,837 |

32,959 |

|

40,564 |

57,458 |

|||

|

Gain (loss) on the fair value of energy contracts |

|

‐ |

‐ |

|

(71,121) |

(64,287) |

|||

|

Provision for decarbonization - CBIO |

|

‐ |

‐ |

|

370,823 |

584,371 |

|||

|

Revaluation of investment in associates |

28.b |

‐ |

‐ |

|

(91,105) |

‐ |

|||

|

Provisions for tax, civil and labor risks |

|

(55,323) |

8,164 |

|

(103,901) |

(4,708) |

|||

|

Other provisions and adjustments |

|

(466) |

6,916 |

|

(18,431) |

(11,361) |

|||

|

|

|

38,435 |

62,013 |

|

7,514,651 |

7,821,219 |

|||

|

(Increase) decrease in assets |

|

|

|

|

|

|

|||

|

Trade receivables and reseller financing |

5 |

‐ |

‐ |

|

(185,611) |

180,339 |

|||

|

Inventories |

6 |

‐ |

‐ |

|

(151,282) |

371,244 |

|||

|

Recoverable taxes |

|

4,191 |

8,869 |

|

(171,126) |

(585,254) |

|||

|

Dividends received from subsidiaries, associates and joint ventures |

|

3,395,567 |

1,584,885 |

|

11,141 |

2,028 |

|||

|

Other assets |

|

(17,166) |

(30,090) |

|

167,931 |

(114,528) |

|||

|

|

|

|

|

|

|

|

|||

|

Increase (decrease) in liabilities |

|

|

|

|

|

|

|||

|

Trade payables and trade payables - reverse factoring |

16 |

2,355 |

(1,349) |

|

(31,818) |

(1,209,636) |

|||

|

Salaries and related charges |

|

3,188 |

(6,957) |

|

47,615 |

(17,019) |

|||

|

Taxes payable |

|

(524) |

(554) |

|

8,963 |

(23,512) |

|||

|

Income and social contribution taxes payable |

|

(13,823) |

(9,667) |

|

(949,442) |

(1,057,460) |

|||

|

Other liabilities |

|

36,104 |

(57) |

|

189,931 |

(160,331) |

|||

|

Acquisition of CBIO and carbon credits |

14 |

‐ |

‐ |

|

(370,501) |

(713,453) |

|||

|

Payments of contractual assets with customers - exclusivity rights |

10 |

‐ |

‐ |

|

(455,567) |

(418,250) |

|||

|

Payment of contingencies |

|

(12,707) |

‐ |

|

(78,537) |

(30,896) |

|||

|

Income and social contribution taxes paid |

|

(706) |

(3,433) |

|

(124,077) |

(308,915) |

|||

|

Net cash provided by continuing operating activities |

|

3,434,914 |

1,603,660 |

|

5,422,271 |

3,735,576 |

|||

|

Net cash provided by discontinued operating activities |

|

- |

- |

|

30,231 |

- |

|||

|

Net cash provided by operating activities |

|

3,434,914 |

1,603,660 |

|

5,452,502 |

3,735,576 |

|||

|

|

|

|

|

|

|

|

|||

|

CASH FLOWS FROM INVESTING ACTIVITIES |

|

|

|

|

|

|

|||

|

Financial investments, net of redemptions |

4.b |

(1,123,954) |

(213,003) |

|

(1,510,857) |

(4,202,032) |

|||

|

Acquisition of property, plant and equipment and intangible assets |

13; 14 |

(11,910) |

(81,479) |

|

(2,005,243) |

(1,787,175) |

|||

|

Sale of investments and other assets |

|

136 |

264,564 |

|

429,283 |

1,386,252 |

|||

|

Capital increase and decrease in subsidiaries, associates and joint ventures |

11 |

(53,014) |

(1,124,230) |

|

- |

- |

|||

|

Acquisition of investments and other assets |

|

(44,284) |

‐ |

|

(937,457) |

(1,785,517) |

|||

|

Cash acquired in business combination |

|

‐ |

‐ |

|

1,213,510 |

522 |

|||

|

Net cash consumed by continuing investing activities |

|

(1,233,026) |

(1,154,148) |

|

(2,810,764) |

(6,387,950) |

|||

|

Net cash consumed by discontinued investing activities |

|

- |

- |

|

(34,948) |

- |

|||

|

Net cash consumed by investing activities |

|

(1,233,026) |

(1,154,148) |

|

(2,845,712) |

(6,387,950) |

|||

|

|

|

|

|

|

|

|

|||

|

CASH FLOWS FROM FINANCING ACTIVITIES |

|

|

|

|

|

|

|||

|

Loans, financing and debentures |

|

|

|

|

|

|

|||

|

Proceeds |

15 |

‐ |

‐ |

|

8,669,139 |

4,179,974 |

|||

|

Repayments |

15 |

‐ |

‐ |

|

(5,134,131) |

(2,718,953) |

|||

|

Interest and derivatives (paid) or received |

|

‐ |

7,838 |

|

(1,899,251) |

(1,117,562) |

|||

|

Payments of lease |

|

|

|

|

|

|

|||

|

Principal and interest paid |

12.b |

(3,666) |

(3,595) |

|

(480,722) |

(433,488) |

|||

|

Dividends paid |

|

(1,892,861) |

(713,066) |

|

(2,172,132) |

(833,658) |

|||

|

Payments of financial liabilities of customers |

|

‐ |

‐ |

|

(123,122) |

(159,897) |

|||

|

Capital increase made by non-controlling shareholders and redemption of shares |

|

‐ |

‐ |

|

(12,300) |

13,500 |

|||

|

Repurchase of treasury shares |

|

(266,954) |

(148,945) |

|

(266,954) |

(148,945) |

|||

|

Related parties |

|

(448) |

(398) |

|

(43,521) |

(15,073) |

|||

|

|

|

|

|

|

|

|

|||

|

Net cash consumed by continuing financing activities |

|

(2,163,929) |

(858,166) |

|

(1,462,994) |

(1,234,102) |

|||

|

Net cash consumed by discontinued financing activities |

|

- |

- |

|

(6,596) |

- |

|||

|

Net cash consumed by financing activities |

|

(2,163,929) |

(858,166) |

|

(1,469,590) |

(1,234,102) |

|||

|

|

|

|

|

|

|

|

|||

|

Effect of exchange rate changes on cash and cash equivalents in foreign currency - continuing operations |

|

‐ |

‐ |

|

(44,981) |

32,381 |

|||

|

Increase (decrease) in cash and cash equivalents - continuing operations |

|

37,959 |

(408,654) |

|

1,103,532 |

(3,854,095) |

|||

|

Increase (decrease) in cash and cash equivalents - discontinued operations |

|

- |

- |

|

(11,313) |

- |

|||

|

Cash and cash equivalents at the beginning of the year - continuing operations |

4.a |

4,186 |

412,840 |

|

2,071,593 |

5,925,688 |

|||

|

Cash and cash equivalents at the beginning of the year - discontinued operations |

|

- |

- |

|

11,313 |

- |

|||

|

Cash and cash equivalents at the end of the year - continuing operations |

4.a |

42,145 |

4,186 |

|

3,175,125 |

2,071,593 |

|||

|

|

|

|

|

|

|

|

|||

|

Non-cash transactions: |

|

|

|

|

|

|

|||

|

Addition and remeasurement on right-of-use assets and leases payable |

12 |

‐ |

‐ |

|

400,758 |

342,332 |

|||

|

Addition on contractual assets with customers - exclusivity rights |

10 |

‐ |

‐ |

|

67,393 |

5,627 |

|||

|

Reclassification between financial assets and investment in associates |

|

‐ |

‐ |

|

‐ |

645,333 |

|||

|

Issuance of shares related to the subscription warrants - indemnification - Extrafarma acquisition |

|

‐ |

6,452 |

|

‐ |

6,452 |

|||

|

Acquisition of property, plant and equipment and intangible assets without cash effect |

|

‐ |

‐ |

|

23,478 |

42,180 |

|||

|

Capital increase in subsidiaries with shares |

|

‐ |

133,552 |

|

‐ |

- |

|||

The accompanying notes are an integral part of the financial statements.

|

Ultrapar Participações S.A. and Subsidiaries |

|

| For the years ended December 31, 2025 and 2024 | |

| (In thousands of Brazilian Reais) |

|

|

|

Parent |

|

Consolidated |

|||||

|

|

Note |

12/31/2025 |

|

12/31/2024 |

|

12/31/2025 |

|

12/31/2024 |

|

|

Revenues |

|

|

|

|

|

|

|

|

|

|

Gross revenue from sales and services, except rents and royalties |

21 |

‐ |

|

‐ |

|

147,327,691 |

|

138,927,497 |

|

|

Rebates, discounts and returns |

21 |

‐ |

|

‐ |

|

(1,063,429) |

|

(1,122,338) |

|

|

Allowance for expected credit losses |

5 |

‐ |

|

‐ |

|

2,684 |

|

(3,744) |

|

|

Amortization of contractual assets with customers - exclusivity rights |

10; 21 |

‐ |

|

‐ |

|

(469,766) |

|

(555,083) |

|

|

Gain (loss) on disposal of assets and other operating income (expenses), net |

|

55,727 |

|

18,402 |

|

454,234 |

|

(242,255) |

|

|

|

|

55,727 |

|

18,402 |

|

146,251,414 |

|

137,004,077 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Materials purchased from third parties |

|

|

|

|

|

|

|

|

|

|

Cost of products and services sold |

|

‐ |

|

‐ |

|

(133,062,345) |

|

(124,034,095) |

|

|

Materials, energy, third-party services and others |

|

237,446 |

|

207,435 |

|

(1,836,555) |

|

(1,775,717) |

|

|

Provision for assets losses |

|

‐ |

|

‐ |

|

(8,481) |

|

735 |

|

|

|

|

237,446 |

|

207,435 |

|

(134,907,381) |

|

(125,809,077) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross value added |

|

293,173 |

|

225,837 |

|

11,344,033 |

|

11,195,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Retentions |

|

|

|

|

|

|

|

|

|

|

Depreciation and amortization of intangible assets and right-of-use assets |

12.a; 13; 14 |

(17,444) |

|

(18,672) |

|

(1,586,163) |

|

(1,212,733) |

|

|

|

|

(17,444) |

|

(18,672) |

|

(1,586,163) |

|

(1,212,733) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Net value added produced by the Company |

|

275,729 |

|

207,165 |

|

9,757,870 |

|

9,982,267 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Value added received in transfer |

|

|

|

|

|

|

|

|

|

|

Total share of profit (loss) of subsidiaries, joint ventures and associates |

|

2,549,952 |

|

2,380,009 |

|

(66,505) |

|

(129,675) |

|

|

Rents and royalties |

21 |

‐ |

|

‐ |

|

138,091 |

|

319,809 |

|

|

Financial income |

23 |

45,798 |

|

68,869 |

|

1,580,842 |

|

881,074 |

|

|

|

|

2,595,750 |

|

2,448,878 |

|

1,652,428 |

|

1,071,208 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Value added from continuing operations available for distribution |

|

2,871,479 |

|

2,656,043 |

|

11,410,298 |

|

11,053,475 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Value added from discontinued operations available for distribution |

|

(121,153) |

|

‐ |

|

(156,215) |

|

‐ |

|

|

|

|

|

|

|

|

|

|

|

|

|

Total value added available for distribution |

|

2,750,326 |

|

2,656,043 |

|

11,254,083 |

|

11,053,475 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Distribution of value added |

|

|

|

|

|

|

|

|

|

|

Personnel and related charges |

|

|

|

|

|

|

|

|

|

|

Salaries and wages |

|

205,158 |

|

167,659 |

|

1,777,134 |

|

1,494,898 |

|

|

Benefits |

|

28,511 |

|

27,473 |

|

489,709 |

|

434,927 |

|

|

Government Severance Indemnity Fund for Employees (FGTS) |

|

9,038 |

|

7,656 |

|

111,113 |

|

107,666 |

|

|

Others |

|

1,786 |

|

7,413 |

|

136,150 |

|

268,559 |

|

|

|

|

244,493 |

|

210,201 |

|

2,514,106 |

|

2,306,050 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Taxes, fees and contributions |

|

|

|

|

|

|

|

|

|

|

Federal |

|

27,059 |

|

62,228 |

|

2,615,598 |

|

3,671,136 |

|

|

State |

|

‐ |

|

‐ |

|

548,866 |

|

519,824 |

|

|

Municipal |

|

366 |

|

305 |

|

226,047 |

|

162,873 |

|

|

|

|

27,425 |

|

62,533 |

|

3,390,511 |

|

4,353,833 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Financial expenses and rents |

|

|

|

|

|

|

|

|

|

|

Interest, foreign exchange variations and financial instruments |

|

3,381 |

|

75 |

|

2,488,627 |

|

1,650,376 |

|

|

Rents |

|

5,089 |

|

4,178 |

|

128,559 |

|

113,328 |

|

|

Others |

|

16,085 |

|

16,316 |

|

140,275 |

|

103,988 |

|

|

|

|

24,555 |

|

20,569 |

|

2,757,461 |

|

1,867,692 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Remuneration of own capital |

|

|

|

|

|

|

|

|

|

|

Interest on capital and dividends |

|

1,621,434 |

|

275,971 |

|

1,658,830 |

|

666,741 |

|

|

Retained earnings |

|

953,572 |

|

2,086,769 |

|

1,089,390 |

|

1,859,159 |

|

|

|

|

2,575,006 |

|

2,362,740 |

|

2,748,220 |

|

2,525,900 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Value added from continuing operations distributed |

|

2,871,479 |

|

2,656,043 |

|

11,410,298 |

|

11,053,475 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Value added from discontinued operations distributed |

|

(121,153) |

|

‐ |

|

(156,215) |

|

‐ |

|

|

|

|

|

|

|

|

|

|

|

|

|

Value added distributed |

|

2,750,326 |

|

2,656,043 |

|

11,254,083 |

|

11,053,475 |

|

The accompanying notes are an integral part of the financial statements.

|

Ultrapar Participações S.A. and Subsidiaries |

|

|

Notes to the financial statements |

|

| For the year ended December 31, 2025 |

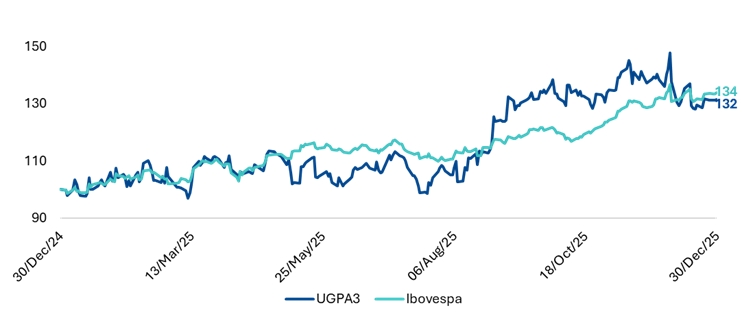

Ultrapar Participações S.A. (“Ultrapar” or “Company”) is a publicly-traded company headquartered at the Brigadeiro Luís Antônio Avenue, 1343 in the city of São Paulo – SP, Brazil, listed on B3 S.A. – Brasil, Bolsa, Balcão (“B3”), in the Novo Mercado listing segment under the ticker “UGPA3” and on the New York Stock Exchange (“NYSE”) in the form of level III American Depositary Receipts (“ADRs”) under the ticker “UGP”.

The Company engages in the investment of its own capital in services, commercial and industrial activities, through the subscription or acquisition of shares of other companies. Through its subsidiaries, it operates on liquefied petroleum gas distribution and other energies (“Ultragaz”), fuel distribution and related businesses (“Ipiranga” or “IPP”), storage services for liquid bulk (“Ultracargo”) and logistics and waterway and multimodal infrastructure (“Hidrovias”). The information on segments is disclosed in Note 25.

These financial statements were authorized for issuance by the Board of Directors on March 4, 2026.

a. Principles of consolidation and interest in subsidiaries

a.1 Principles of consolidation

In the preparation of the consolidated financial statements the investments of one company in another, balances of asset and liability accounts, revenue transactions, costs and expenses were eliminated, as well as the effects of transactions conducted between the companies. Non-controlling interests in subsidiaries are presented within consolidated equity and net income.

Consolidation of a subsidiary begins when the Company obtains direct or indirect control over an entity and ceases when the company loses control. Income and expenses of a subsidiary acquired are included in the consolidated statements of income and of comprehensive income from the date the Company gains control. Income and expenses of a subsidiary, in which the Company loses control, are included in the consolidated statements of income and of comprehensive income until the date the Company loses control.

When necessary, adjustments are made to the financial statements of subsidiaries to bring their accounting policies into line with the Company’s accounting policies.

|

Ultrapar Participações S.A. and Subsidiaries |

|

|

Notes to the financial statements |

|

| For the year ended December 31, 2025 |

a.2 Interest in subsidiaries

The consolidated financial statements include the following direct and indirect subsidiaries:

|

|

|

|

|

|

Interest % rounded |

||||||

|

|

|

|

|

|

12/31/2025 |

|

12/31/2024 |

||||

|

|

|

|

|

|

Control |

|

Control |

||||

|

|

|

Location |

Segment |

|

Direct |

|

Indirect |

|

Direct |

|

Indirect |

|

Ultra Mobilidade S.A. (1) |

|

Brazil |

Ipiranga |

|

100 |

|

- |

|

100 |

|

- |

|

Centro de Conveniências Millennium Ltda. and subsidiaries (2) |

|

Brazil |

Ipiranga |

|

- |

|

- |

|

- |

|

100 |

|

am/pm Comestíveis Ltda. (3) |

|

Brazil |

Ipiranga |

|

- |

|

100 |

|

- |

|

- |

|

Glazed Brasil S.A. (“Krispy Kreme”) |

|

Brazil |

Ipiranga |

|

- |

|

55 |

|

- |

|

- |

|

Centro de Conveniências Millennium Ltda. and subsidiaries (2) |

|

Brazil |

Ipiranga |

|

- |

|

100 |

|

- |

|

- |

|

Neodiesel Ltda. |

|

Brazil |

Ipiranga |

|

- |

|

100 |

|

- |

|

100 |

|

Serra Diesel Transportador Revendedor Retalhista Ltda. |

|

Brazil |

Ipiranga |

|

- |

|

60 |

|

- |

|

60 |

|

Neoagro Diesel S.A. (4) |

|