CONFIDENTIAL Discussion Materials March 2026

CONFIDENTIAL Disclaimer This confidential information presentation (this “Presentation”) contains certain information pertaining to Beasley Media Group, LLC (including any successor thereto, the “Company” doing business as “Beasley”). The Presentation is provided to the recipient at the recipient’s request for informational purposes only and is not, and may not be relied on in any manner as, legal, tax or investment advice or as an offer to sell or a solicitation of an offer to buy an interest in any securities of the Company. Neither the Company nor any of its advisors or agents intend for this Presentation to form the sole basis of any transaction decision. The recipient should conduct its own investigation and analysis of the Company in connection with any transaction. The information in this Presentation was provided by the Company or is from public or other sources. Neither the Company nor any of its advisors or agents assumes any responsibility for independently verifying such information and each of them expressly disclaims any liability to any purchaser in connection with such information or any transaction with the Company. Neither the Company nor any of its advisors or agents make any representation or warranty, express or implied, or accept any responsibility or liability for the accuracy or completeness of this Presentation or any other written or oral information that the Company or any other person makes available to any recipient. Neither the Company nor any of its advisors or agents makes any representation or warranty as to the achievement or reasonableness of any projections, management estimates, prospects or returns. This Presentation speaks only as of the date of the information herein and neither the Company nor any of its advisors or agents has any obligation to update or correct any information herein. Forward-Looking Statements: This Presentation, contains “forward-looking statements” about the Company, which relate to future, not past, events. All statements other than statements of historical fact included in this Presentation are forward-looking statements. These forward-looking statements are based on the current beliefs and expectations of the Company’s management and are subject to known and unknown risks and uncertainties. Forward-looking statements, which address the Company’s expected business and financial performance and financial condition, among other matters, contain words such as: “expects,” “anticipates,” “intends,” “plans,” “believes,” “estimates,” “may,” “will,” “plans,” “projects,” “could,” “should,” “would,” “seek,” “forecast,” or other similar expressions. Forward-looking statements, by their nature, address matters that are, to different degrees, uncertain. Although the Company believes the expectations reflected in such forward-looking statements are based upon reasonable assumptions, it can give no assurance that the expectations will be attained or that any deviation will not be material. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date on which they are made. The Company undertakes no obligation to update or revise any forward-looking statements. Forward-looking statements involve a number of risks and uncertainties, and actual results or events may differ materially from those projected or implied in those statements. Factors that could cause actual results or events to differ materially from these forward- looking statements include, but are not limited to: • risks associated with the exchange of less than 100% of the Existing Notes pursuant to the Offers and the ability of the Supporting Holders to waive the TSA Minimum Participation Condition; • the ability of the Company to comply with the continued listing standards of Nasdaq, remain listed on Nasdaq, and make periodic filings with the SEC; • risks from health epidemics, natural disasters, terrorism, and other catastrophic events; • adverse effects of inflation; • external economic forces and conditions that could have a material adverse impact on the Company’s advertising revenues and results of operations; • the ability of the Company’s stations to compete effectively in their respective markets for advertising revenues; • the ability of the Company to develop compelling and differentiated digital content, products and services; • audience acceptance of the Company’s content, particularly its audio programs; • the ability of the Company to adapt or respond to changes in technology, standards and services that affect the audio industry; • the Company’s dependence on federally issued licenses subject to extensive federal regulation; • actions by the Federal Communications Commission (“FCC”) or new legislation affecting the audio industry; • increases to royalties the Company pays to copyright owners or the adoption of legislation requiring royalties to be paid to record labels and recording artists; • the Company’s dependence on selected market clusters of stations for a material portion of its net revenue; • credit risk on the Company’s accounts receivable; • the risk that the Company’s FCC licenses could become impaired; • the Company’s substantial debt levels and the potential effect of restrictive debt covenants on the Company’s operational flexibility and ability to pay dividends; • the 2027 PIK Notes will be structurally subordinated to all obligations of the Issuer’s existing and future subsidiaries that are not and do not become Guarantors; • the Issuer may not be able to repurchase the 2027 PIK Notes upon a change of control; • certain corporate events may not trigger a change of control; • holders of the 2027 PIK Notes may not be able to determine when a change of control has occurred; • federal and state fraudulent transfer laws may permit a court to void the 2027 PIK Notes and/or the Guarantees; • a lowering or withdrawal of the ratings assigned to our debt securities by rating agencies; • many of the covenants in the 2027 PIK Notes Indenture governing the 2027 PIK Notes will not apply during any period in which the 2027 PIK Notes are rated investment grade by two of S&P, Moody’s and Fitch; • our ability to comply with debt covenants and service our debt, including the 2027 PIK Notes; • restrictions on the ability to transfer or resell the 2027 PIK Notes; • absence of an active trading market for the 2027 PIK Notes; • impacts to the value of collateral assets; • our ability to consummate the Offers; • the potential effects of hurricanes, extreme weather and other climate change conditions on the Company’s corporate offices and station; • the failure or destruction of the internet, satellite systems and transmitter facilities that the Company depends upon to distribute its programming; • modifications or interruptions of the Company’s information technology infrastructure and information systems; • the loss of key executives and other key employees; • the Company’s ability to identify, consummate and integrate acquired businesses and stations; • the fact that the Company is controlled by the Beasley family, which creates difficulties for any attempt to gain control of the Company; and • other economic, business, competitive, and regulatory factors affecting the businesses of the Company, as discussed in more detail in the Company’s filings with the SEC. Our actual performance and results could differ materially because of these factors and other factors discussed in the “Management’s Discussion and Analysis of Results of Operations and Financial Condition” in our SEC filings, including but not lC imo ite ndf ide to on urt ial | 1 annual reports on Form 10-K or quarterly reports on Form 10-Q, copies of which can be obtained from the SEC website, www.sec.gov, or our website, www.bbgi.com. While forward-looking statements reflect our good faith beliefs, they are not guarantees of future performance. All information in this Presentation is as of the date of this Presentation, and we undertake no obligation to update the information contained herein to actual results or changes to our expectations.

CONFIDENTIAL Disclaimer Projections: This Presentation contains projected financial information (the “Projections”) with respect to the business of the Company, including net revenue and adjusted EBITDA for 2025-2028. Such Projections constitute forward-looking information, is for illustrative purposes only and should not be relied upon as being necessarily indicative of future results. The assumptions and estimates underlying Projections are inherently uncertain and are subject to a wide variety of significant business, economic and competitive risk and uncertainties that could cause actual results to differ materially from those contained in the Projections. See “Forward Looking Statements” above. Actual results may differ materially from the results contemplated by the Projections contained in this Presentation, and the inclusion of such information in this Presentation should not be regarded as a representation by the Company that the results reflected in such projections will be achieved. The auditors of the Company have not audited, reviewed, compiled or performed any procedures with respect to the Projections for the purpose of their inclusion in this Presentation, and, accordingly, have not expressed an opinion or provided any other form of assurance with respect thereto for the purpose of this Presentation. Use of Non-GAAP Financial Metrics: This Presentation includes certain financial measures that have not been prepared in a manner that complies with generally accepted accounting principles in the United States (“GAAP”), including, without limitation, EBITDA, Adjusted EBITDA, Total Station Operating Income, Audio Station Operating Income, Compound Annual Growth Rate, and Unlevered Free Cash Flow (collectively, the “non-GAAP financial measures”). We believe that the presentation of these Non-GAAP Financial Measures enhances an investor’s understanding of our financial performance. We further believe that these Non-GAAP Financial Measures are useful financial metrics to assess our operating performance from period to period by excluding certain items that we believe are not representative of our core business or adjusting for the effect of acquisitions or dispositions. We use these Non-GAAP Financial Measures for business planning purposes and in measuring our performance relative to that of our competitors. We believe these Non- GAAP Financial Measures are commonly used by investors to evaluate our performance and that of our competitors. However, our use of such Non-GAAP Financial Measures may vary from that of others in our industry. These Non-GAAP Financial Measures should not be considered as alternatives to net revenue, operating income (loss), net income (loss), net cash provided by operating activities or any other performance measures presented in accordance with GAAP. EBITDA consists of net income (loss) before interest income or expense, income tax expense or benefit, depreciation, and amortization. No reconciliation of other non-GAAP financial measures in the Projections to GAAP measures were created or used in connection with preparing the Projections, and there would be inherent difficulty in forecasting and quantifying the measures that would be necessary for such reconciliation. Confidential | 2

CONFIDENTIAL Executive Summary Beasley Broadcasting Group, Inc. (“Beasley” or the “Company”) is well positioned to generate long-term value from its high-quality assets and participate in post deregulation portfolio optimization once its capital structure is right-sized • Despite secular headwinds, Beasley consistently ranks as a top audio provider in all of its rated markets o In addition, while agency trends have challenged the industry broadly, Beasley has been actively transitioning towards direct business in both Digital and Spot, in order to create a more resilient top-line and benefit from higher margins • Beasley continues to evolve its business model, with a sustained focus on shifting its revenue mix to digital where margins are significantly higher o Digital represents ~24.3% of revenue as of FY2025E, compared to 18.8% of revenue for FY2023 o High margins driven by shifting to O&O and programmatic • In response to industry contraction, Beasley has executed substantial cost reduction initiatives, lowering total station operating and corporate expenses by $30MM annually • The Company also sees promising opportunities ahead in various key areas with the potential to drive material (~$50MM) revenue enhancements • Finally, de-regulation will be a critical catalyst for Beasley to unlock future value where restructurings across the industry will allow attractive in-market buyers to emerge Confidential | 3

1. Financial Performance Confidential | 4

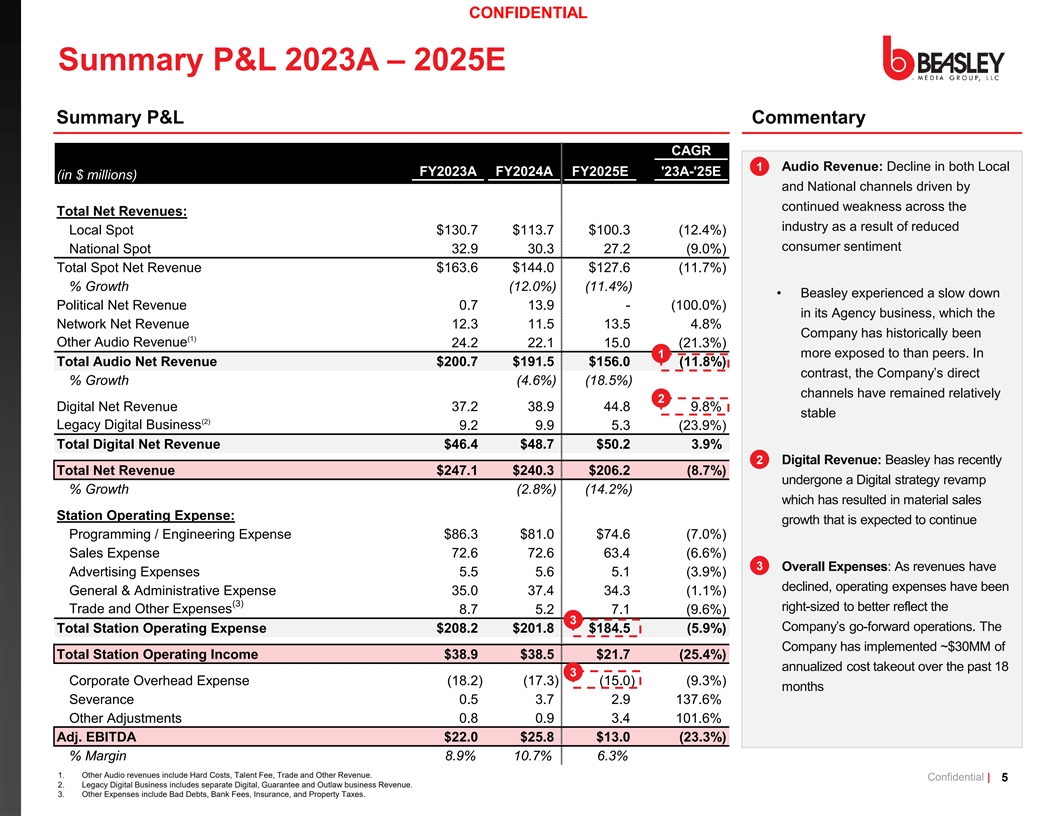

CONFIDENTIAL Summary P&L 2023A – 2025E Summary P&L Commentary CAGR 1 • Audio Revenue: Decline in both Local FY2023A FY2024A FY2025E '23A-'25E (in $ millions) and National channels driven by continued weakness across the Total Net Revenues: industry as a result of reduced Local Spot $130.7 $113.7 $100.3 (12.4%) consumer sentiment National Spot 32.9 30.3 27.2 (9.0%) Total Spot Net Revenue $163.6 $144.0 $127.6 (11.7%) % Growth (12.0%) (11.4%) • Beasley experienced a slow down Political Net Revenue 0.7 13.9 - (100.0%) in its Agency business, which the Network Net Revenue 12.3 11.5 13.5 4.8% Company has historically been (1) Other Audio Revenue 24.2 22.1 15.0 (21.3%) more exposed to than peers. In 1 Total Audio Net Revenue $200.7 $191.5 $156.0 (11.8%) contrast, the Company’s direct % Growth (4.6%) (18.5%) channels have remained relatively 2 Digital Net Revenue 37.2 38.9 44.8 9.8% stable (2) Legacy Digital Business 9.2 9.9 5.3 (23.9%) Total Digital Net Revenue $46.4 $48.7 $50.2 3.9% 2 • Digital Revenue: Beasley has recently Total Net Revenue $247.1 $240.3 $206.2 (8.7%) undergone a Digital strategy revamp % Growth (2.8%) (14.2%) which has resulted in material sales Station Operating Expense: growth that is expected to continue Programming / Engineering Expense $86.3 $81.0 $74.6 (7.0%) Sales Expense 72.6 72.6 63.4 (6.6%) 3 • Overall Expenses: As revenues have Advertising Expenses 5.5 5.6 5.1 (3.9%) declined, operating expenses have been General & Administrative Expense 35.0 37.4 34.3 (1.1%) (3) right-sized to better reflect the Trade and Other Expenses 8.7 5.2 7.1 (9.6%) 3 Company’s go-forward operations. The Total Station Operating Expense $208.2 $201.8 $184.5 (5.9%) Company has implemented ~$30MM of Total Station Operating Income $38.9 $38.5 $21.7 (25.4%) annualized cost takeout over the past 18 3 Corporate Overhead Expense (18.2) (17.3) (15.0) (9.3%) months Severance 0.5 3.7 2.9 137.6% Other Adjustments 0.8 0.9 3.4 101.6% Adj. EBITDA $22.0 $25.8 $13.0 (23.3%) % Margin 8.9% 10.7% 6.3% 1. Other Audio revenues include Hard Costs, Talent Fee, Trade and Other Revenue. Confidential | 5 2. Legacy Digital Business includes separate Digital, Guarantee and Outlaw business Revenue. 3. Other Expenses include Bad Debts, Bank Fees, Insurance, and Property Taxes.

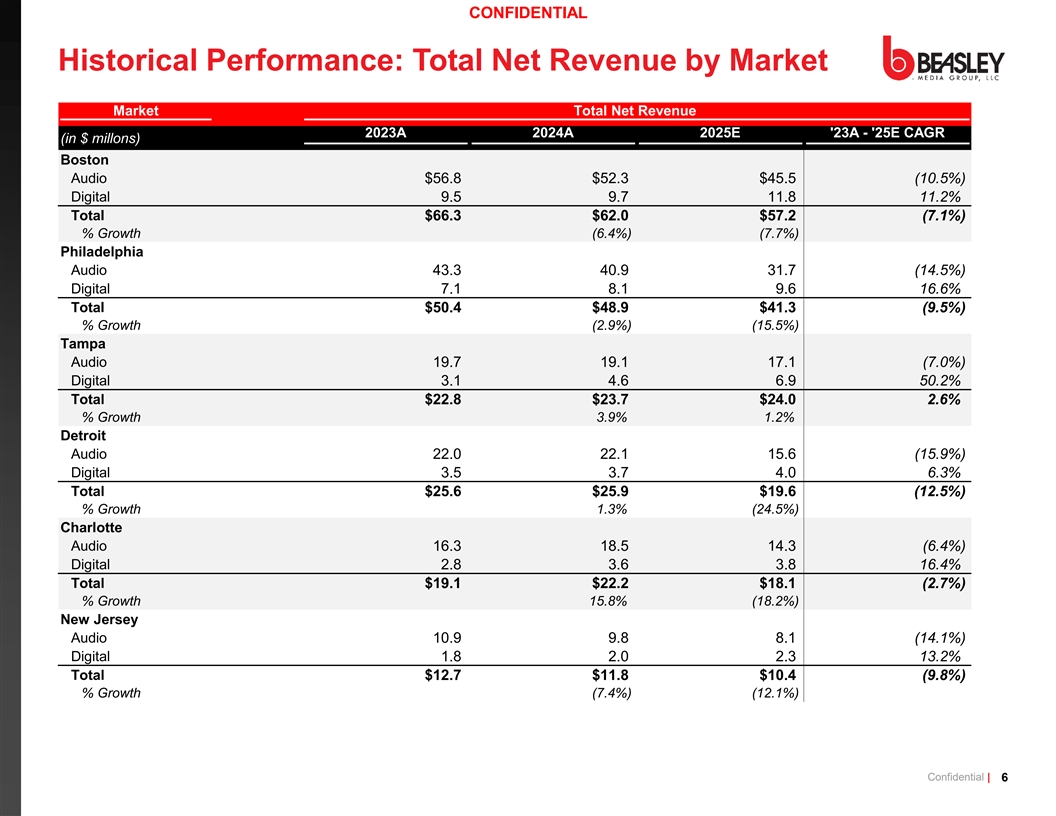

CONFIDENTIAL Historical Performance: Total Net Revenue by Market Market Total Net Revenue 2023A 2024A 2025E '23A - '25E CAGR (in $ millons) Boston Audio $56.8 $52.3 $45.5 (10.5%) Digital 9.5 9.7 11.8 11.2% Total $66.3 $62.0 $57.2 (7.1%) % Growth (6.4%) (7.7%) Philadelphia Audio 43.3 40.9 31.7 (14.5%) Digital 7.1 8.1 9.6 16.6% Total $50.4 $48.9 $41.3 (9.5%) % Growth (2.9%) (15.5%) Tampa Audio 19.7 19.1 17.1 (7.0%) Digital 3.1 4.6 6.9 50.2% Total $22.8 $23.7 $24.0 2.6% % Growth 3.9% 1.2% Detroit Audio 22.0 22.1 15.6 (15.9%) Digital 3.5 3.7 4.0 6.3% Total $25.6 $25.9 $19.6 (12.5%) % Growth 1.3% (24.5%) Charlotte Audio 16.3 18.5 14.3 (6.4%) Digital 2.8 3.6 3.8 16.4% Total $19.1 $22.2 $18.1 (2.7%) % Growth 15.8% (18.2%) New Jersey Audio 10.9 9.8 8.1 (14.1%) Digital 1.8 2.0 2.3 13.2% Total $12.7 $11.8 $10.4 (9.8%) % Growth (7.4%) (12.1%) Confidential | 6

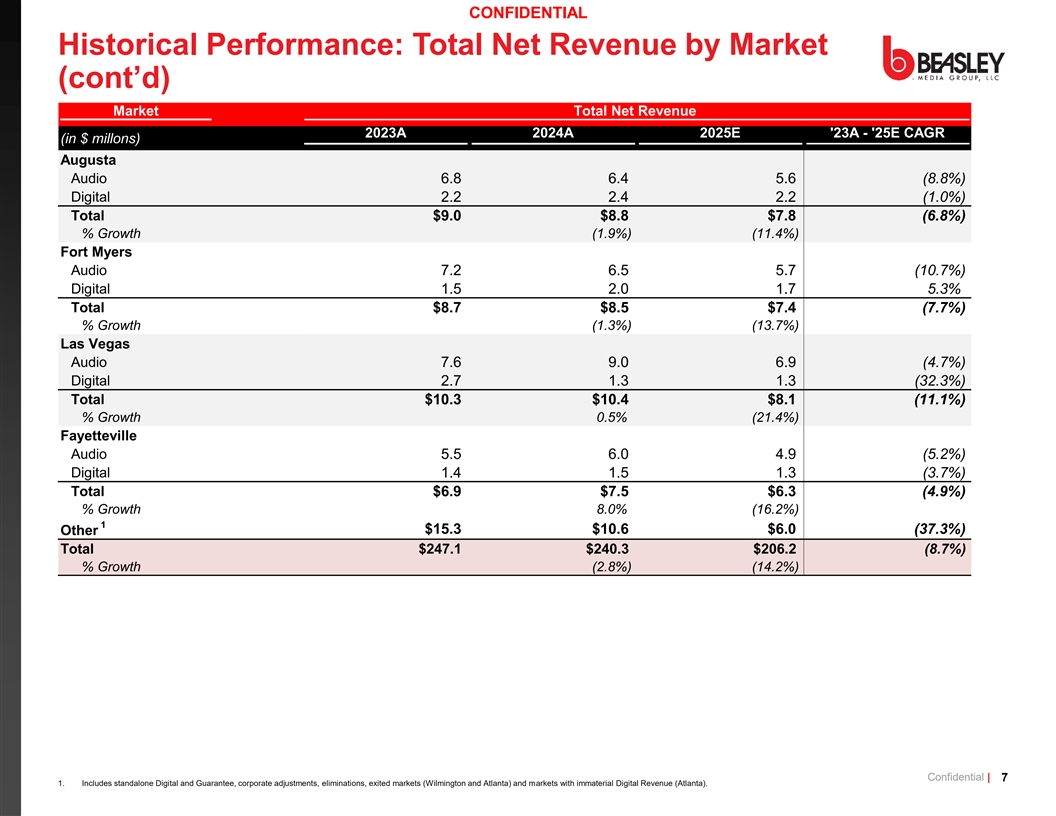

CONFIDENTIAL Historical Performance: Total Net Revenue by Market (cont’d) Market Total Net Revenue 2023A 2024A 2025E '23A - '25E CAGR (in $ millons) Augusta Audio 6.8 6.4 5.6 (8.8%) Digital 2.2 2.4 2.2 (1.0%) Total $9.0 $8.8 $7.8 (6.8%) % Growth (1.9%) (11.4%) Fort Myers Audio 7.2 6.5 5.7 (10.7%) Digital 1.5 2.0 1.7 5.3% Total $8.7 $8.5 $7.4 (7.7%) % Growth (1.3%) (13.7%) Las Vegas Audio 7.6 9.0 6.9 (4.7%) Digital 2.7 1.3 1.3 (32.3%) Total $10.3 $10.4 $8.1 (11.1%) % Growth 0.5% (21.4%) Fayetteville Audio 5.5 6.0 4.9 (5.2%) Digital 1.4 1.5 1.3 (3.7%) Total $6.9 $7.5 $6.3 (4.9%) % Growth 8.0% (16.2%) 1 $15.3 $10.6 $6.0 (37.3%) Other Total $247.1 $240.3 $206.2 (8.7%) % Growth (2.8%) (14.2%) Confidential | 7 1. Includes standalone Digital and Guarantee, corporate adjustments, eliminations, exited markets (Wilmington and Atlanta) and markets with immaterial Digital Revenue (Atlanta).

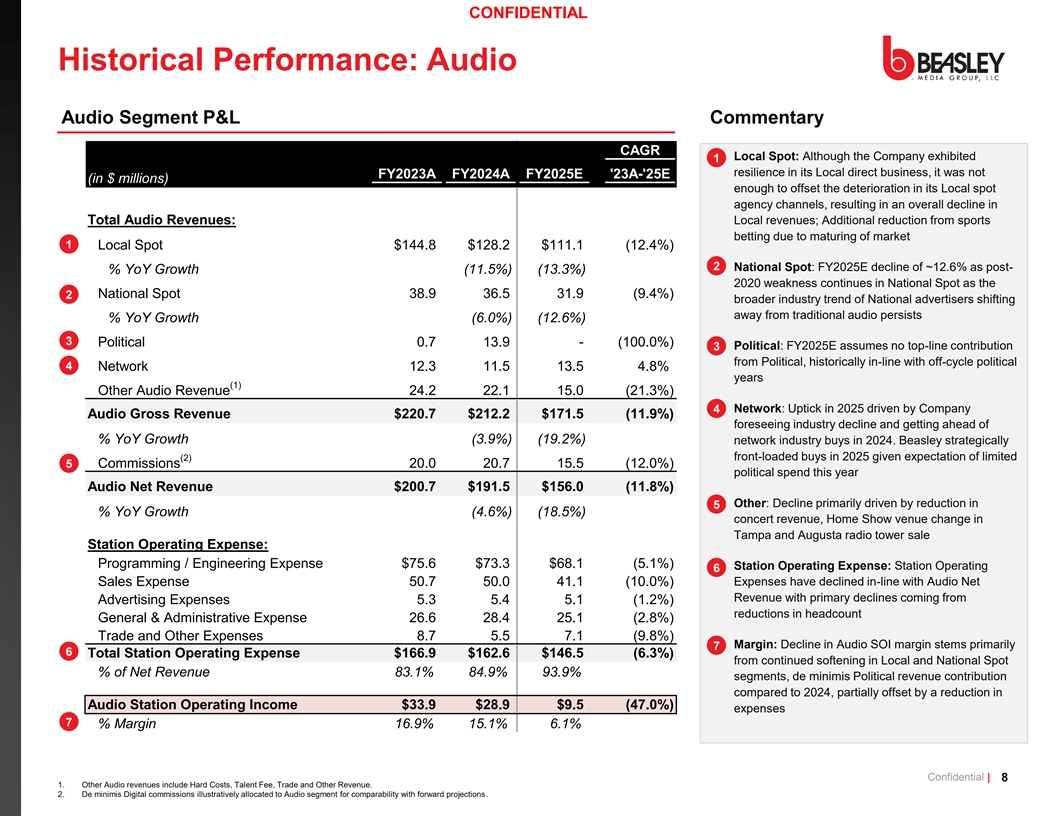

CONFIDENTIAL Historical Performance: Audio Audio Segment P&L Commentary CAGR • Local Spot: Although the Company exhibited 1 resilience in its Local direct business, it was not FY2023A FY2024A FY2025E '23A-'25E (in $ millions) enough to offset the deterioration in its Local spot agency channels, resulting in an overall decline in Local revenues; Additional reduction from sports Total Audio Revenues: betting due to maturing of market 1 Local Spot $144.8 $128.2 $111.1 (12.4%) 2 • National Spot: FY2025E decline of ~12.6% as post- % YoY Growth (11.5%) (13.3%) 2020 weakness continues in National Spot as the 2 National Spot 38.9 36.5 31.9 (9.4%) broader industry trend of National advertisers shifting away from traditional audio persists % YoY Growth (6.0%) (12.6%) 3 Political 0.7 13.9 - (100.0%) • Political: FY2025E assumes no top-line contribution 3 from Political, historically in-line with off-cycle political 4 Network 12.3 11.5 13.5 4.8% years (1) Other Audio Revenue 24.2 22.1 15.0 (21.3%) • Network: Uptick in 2025 driven by Company 4 Audio Gross Revenue $220.7 $212.2 $171.5 (11.9%) foreseeing industry decline and getting ahead of % YoY Growth (3.9%) (19.2%) network industry buys in 2024. Beasley strategically front-loaded buys in 2025 given expectation of limited (2) 5 Commissions 20.0 20.7 15.5 (12.0%) political spend this year Audio Net Revenue $200.7 $191.5 $156.0 (11.8%) • Other: Decline primarily driven by reduction in 5 % YoY Growth (4.6%) (18.5%) concert revenue, Home Show venue change in Tampa and Augusta radio tower sale Station Operating Expense: Programming / Engineering Expense $75.6 $73.3 $68.1 (5.1%) • Station Operating Expense: Station Operating 6 Expenses have declined in-line with Audio Net Sales Expense 50.7 50.0 41.1 (10.0%) Revenue with primary declines coming from Advertising Expenses 5.3 5.4 5.1 (1.2%) reductions in headcount General & Administrative Expense 26.6 28.4 25.1 (2.8%) Trade and Other Expenses 8.7 5.5 7.1 (9.8%) • Margin: Decline in Audio SOI margin stems primarily 7 6 Total Station Operating Expense $166.9 $162.6 $146.5 (6.3%) from continued softening in Local and National Spot % of Net Revenue 83.1% 84.9% 93.9% segments, de minimis Political revenue contribution compared to 2024, partially offset by a reduction in Audio Station Operating Income $33.9 $28.9 $9.5 (47.0%) expenses 7 % Margin 16.9% 15.1% 6.1% Confidential | 8 1. Other Audio revenues include Hard Costs, Talent Fee, Trade and Other Revenue. 2. De minimis Digital commissions illustratively allocated to Audio segment for comparability with forward projections.

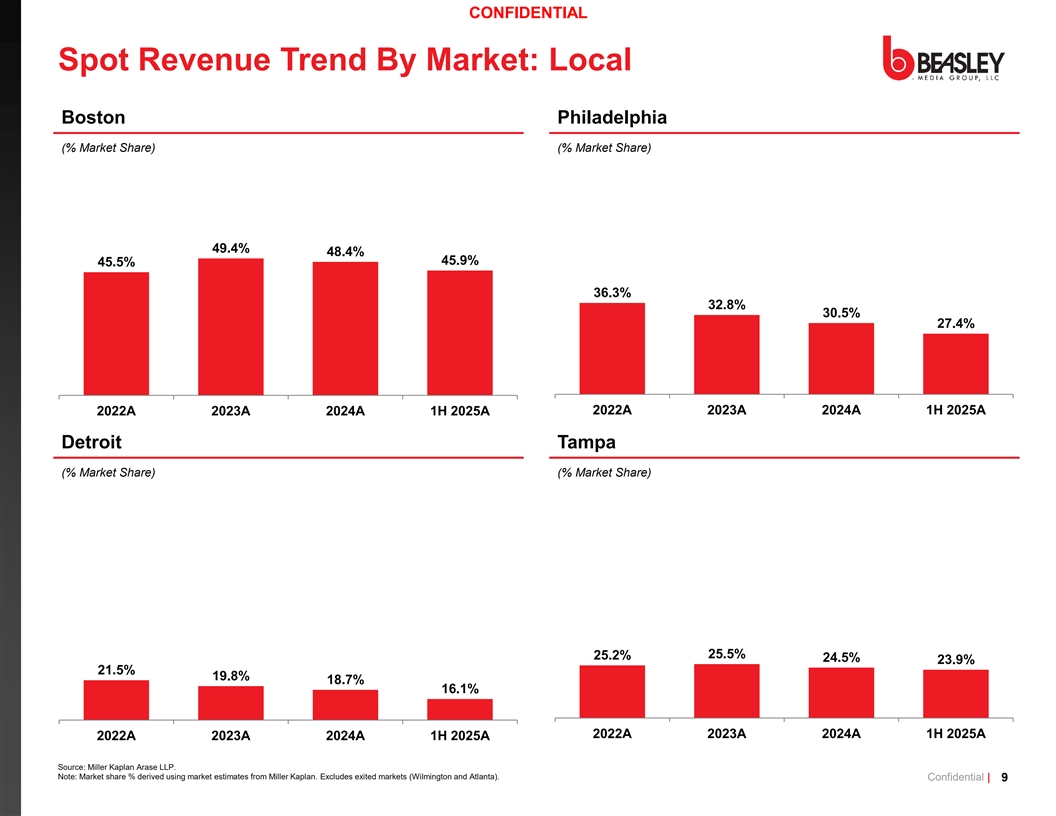

CONFIDENTIAL Spot Revenue Trend By Market: Local Boston Philadelphia (% Market Share) (% Market Share) 49.4% 48.4% 45.9% 45.5% 36.3% 32.8% 30.5% 27.4% 2022A 2023A 2024A 1H 2025A 2022A 2023A 2024A 1H 2025A Detroit Tampa (% Market Share) (% Market Share) 49.4% 48.4% 45.9% 45.5% 25.5% 25.2% 24.5% 23.9% 21.5% 19.8% 18.7% 16.1% 2022A 2023A 2024A 1H 2025A 20 2022A 22A 20 2023A 23A 20 2024A 24A 1H 1H 2025 2025A A Source: Miller Kaplan Arase LLP. Note: Market share % derived using market estimates from Miller Kaplan. Excludes exited markets (Wilmington and Atlanta). Confidential | 9

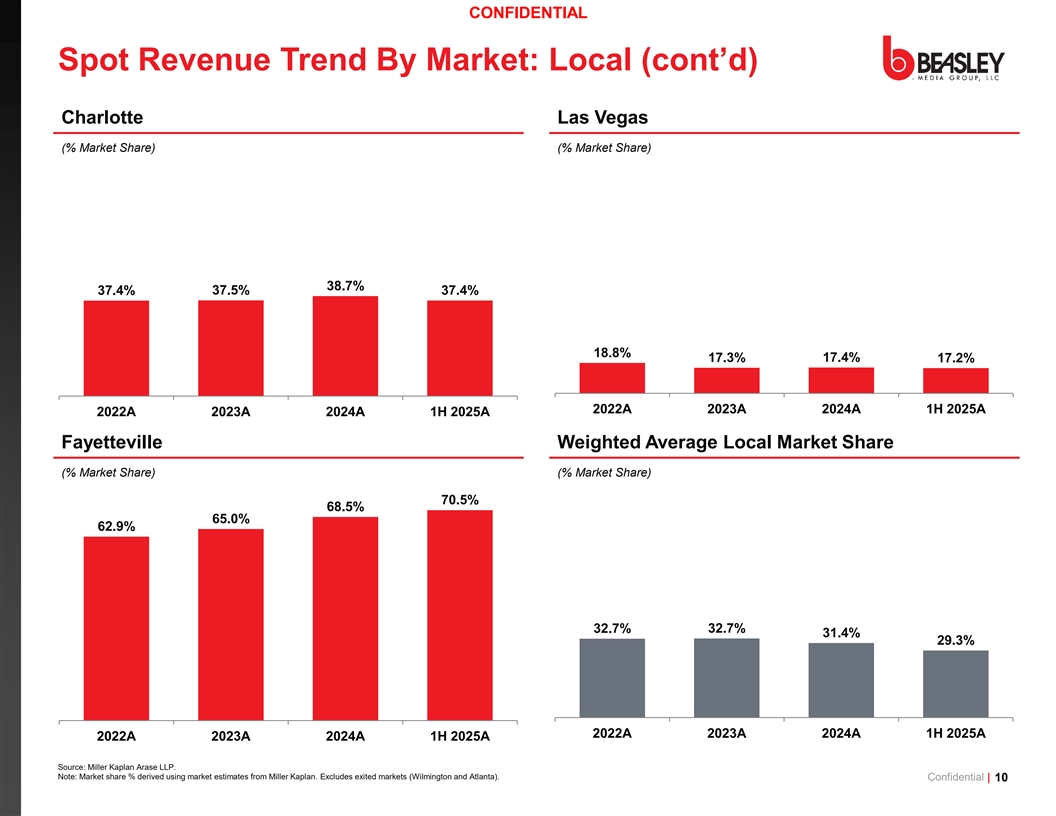

CONFIDENTIAL Spot Revenue Trend By Market: Local (cont’d) Charlotte Las Vegas (% Market Share) (% Market Share) 38.7% 37.4% 37.5% 37.4% 18.8% 17.3% 17.4% 17.2% 2022A 2023A 2024A 1H 2025A 2022A 2023A 2024A 1H 2025A Fayetteville Weighted Average Local Market Share (% Market Share) (% Market Share) 70.5% 68.5% 38.7% 65.0% 62.9% 37.5% 37.4% 37.4% 32.7% 32.7% 31.4% 29.3% 2022A 2023A 2024A 1H 2025A 2022A 2023A 2024A 1H 2025A 2022A 2023A 2024A 1H 2025A Source: Miller Kaplan Arase LLP. Note: Market share % derived using market estimates from Miller Kaplan. Excludes exited markets (Wilmington and Atlanta). Confidential | 10

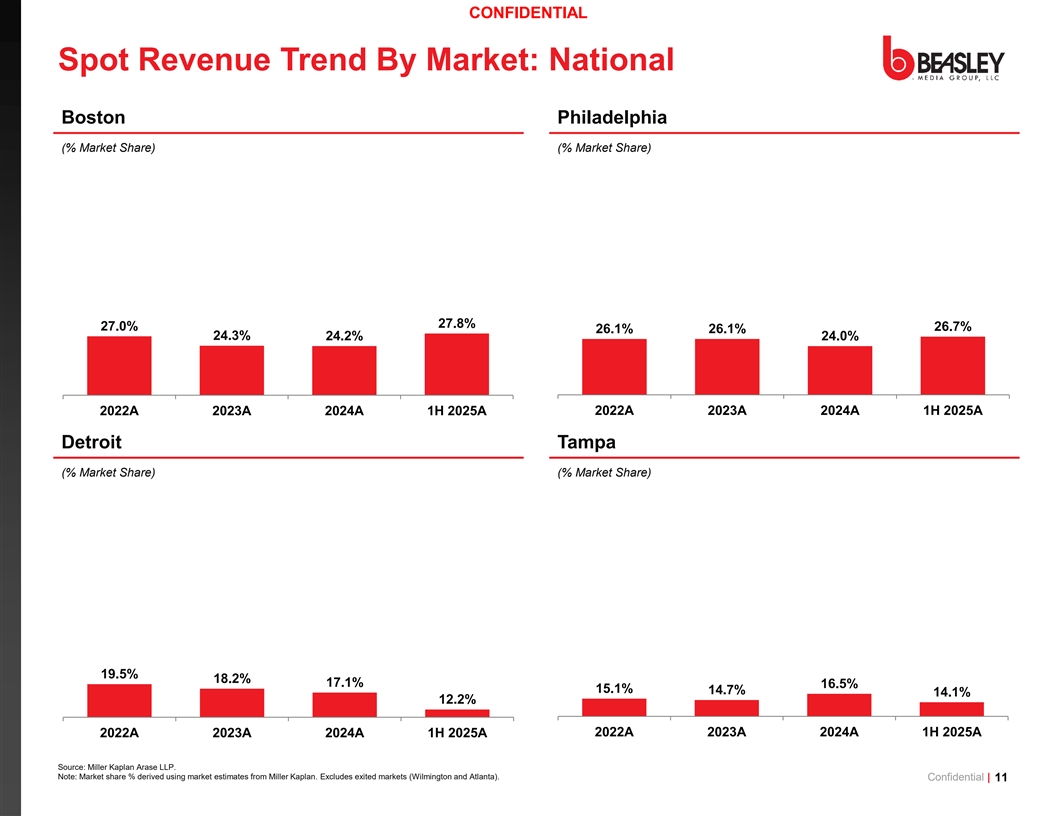

CONFIDENTIAL Spot Revenue Trend By Market: National Boston Philadelphia (% Market Share) (% Market Share) 27.8% 27.0% 26.7% 26.1% 26.1% 24.3% 24.2% 24.0% 2022A 2023A 2024A 1H 2025A 2022A 2023A 2024A 1H 2025A Detroit Tampa (% Market Share) (% Market Share) 49.4% 48.4% 45.9% 45.5% 19.5% 18.2% 17.1% 16.5% 15.1% 14.7% 14.1% 12.2% 2022A 2023A 2024A 1H 2025A 2022A 2023A 2024A 1H 2025A 2022A 2023A 2024A 1H 2025A Source: Miller Kaplan Arase LLP. Note: Market share % derived using market estimates from Miller Kaplan. Excludes exited markets (Wilmington and Atlanta). Confidential | 11

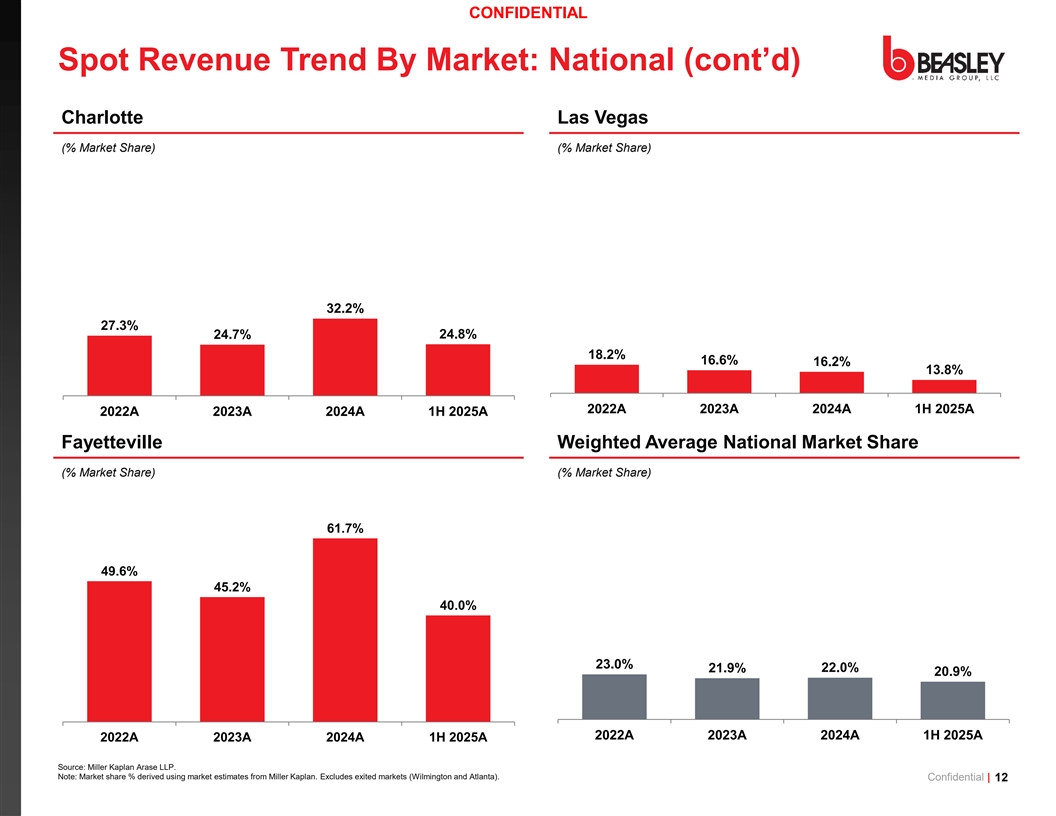

CONFIDENTIAL Spot Revenue Trend By Market: National (cont’d) Charlotte Las Vegas (% Market Share) (% Market Share) 32.2% 27.3% 24.7% 24.8% 18.2% 16.6% 16.2% 13.8% 2022A 2023A 2024A 1H 2025A 2022A 2023A 2024A 1H 2025A Fayetteville Weighted Average National Market Share (% Market Share) (% Market Share) 38.7% 61.7% 49.6% 45.2% 40.0% 37.5% 37.4% 37.4% 23.0% 22.0% 21.9% 20.9% 20 2022A 22A 20 2023A 23A 20 2024A 24A 1H 1H 2025 2025A A 2022A 2023A 2024A 1H 2025A Source: Miller Kaplan Arase LLP. Note: Market share % derived using market estimates from Miller Kaplan. Excludes exited markets (Wilmington and Atlanta). Confidential | 12

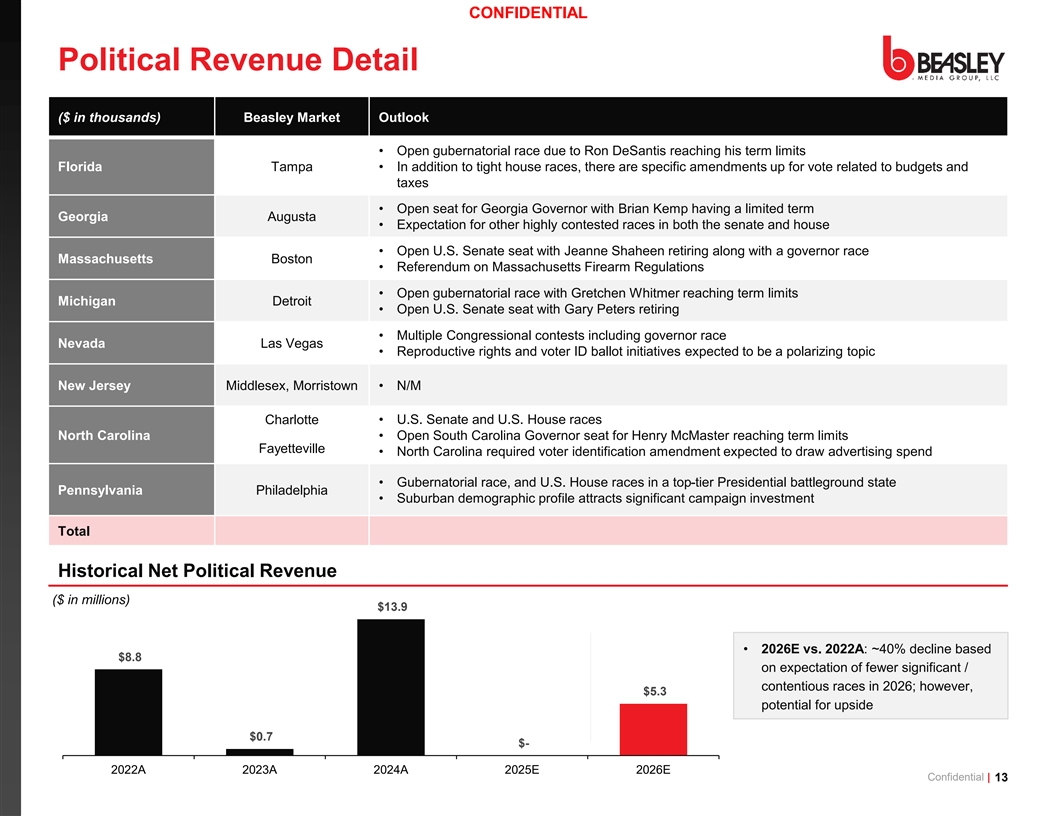

CONFIDENTIAL Political Revenue Detail ($ in thousands) Beasley Market Outlook • Open gubernatorial race due to Ron DeSantis reaching his term limits Florida Tampa • In addition to tight house races, there are specific amendments up for vote related to budgets and taxes • Open seat for Georgia Governor with Brian Kemp having a limited term Georgia Augusta • Expectation for other highly contested races in both the senate and house • Open U.S. Senate seat with Jeanne Shaheen retiring along with a governor race Massachusetts Boston • Referendum on Massachusetts Firearm Regulations • Open gubernatorial race with Gretchen Whitmer reaching term limits Michigan Detroit • Open U.S. Senate seat with Gary Peters retiring • Multiple Congressional contests including governor race Nevada Las Vegas • Reproductive rights and voter ID ballot initiatives expected to be a polarizing topic New Jersey Middlesex, Morristown • N/M Charlotte • U.S. Senate and U.S. House races North Carolina • Open South Carolina Governor seat for Henry McMaster reaching term limits Fayetteville • North Carolina required voter identification amendment expected to draw advertising spend • Gubernatorial race, and U.S. House races in a top-tier Presidential battleground state Pennsylvania Philadelphia • Suburban demographic profile attracts significant campaign investment Total Historical Net Political Revenue ($ in millions) $13.9 • 2026E vs. 2022A: ~40% decline based $8.8 on expectation of fewer significant / contentious races in 2026; however, $5.3 potential for upside $0.7 $- 2022A 2023A 2024A 2025E 2026E Confidential | 13

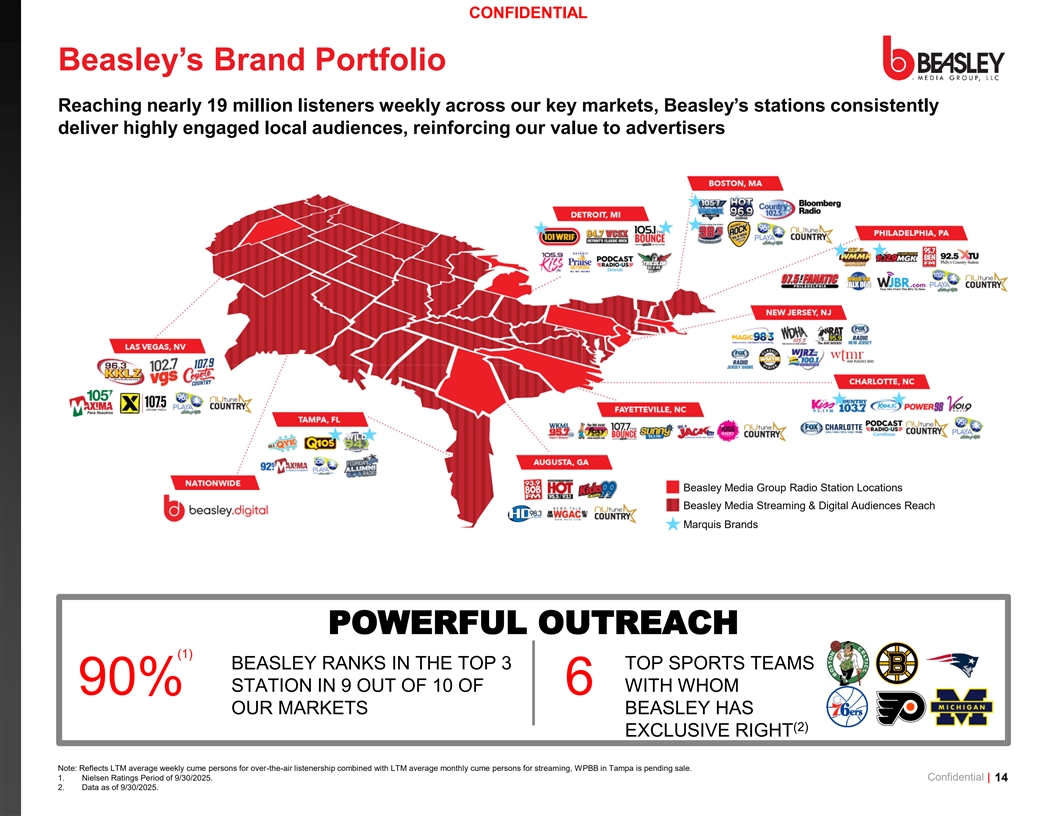

CONFIDENTIAL Beasley’s Brand Portfolio Reaching nearly 19 million listeners weekly across our key markets, Beasley’s stations consistently deliver highly engaged local audiences, reinforcing our value to advertisers Beasley Media Group Radio Station Locations Beasley Media Streaming & Digital Audiences Reach Marquis Brands POWERFUL OUTREACH (1) BEASLEY RANKS IN THE TOP 3 TOP SPORTS TEAMS STATION IN 9 OUT OF 10 OF WITH WHOM 90% 6 OUR MARKETS BEASLEY HAS (2) EXCLUSIVE RIGHT Note: Reflects LTM average weekly cume persons for over-the-air listenership combined with LTM average monthly cume persons for streaming, WPBB in Tampa is pending sale. 1. Nielsen Ratings Period of 9/30/2025. Confidential | 14 2. Data as of 9/30/2025.

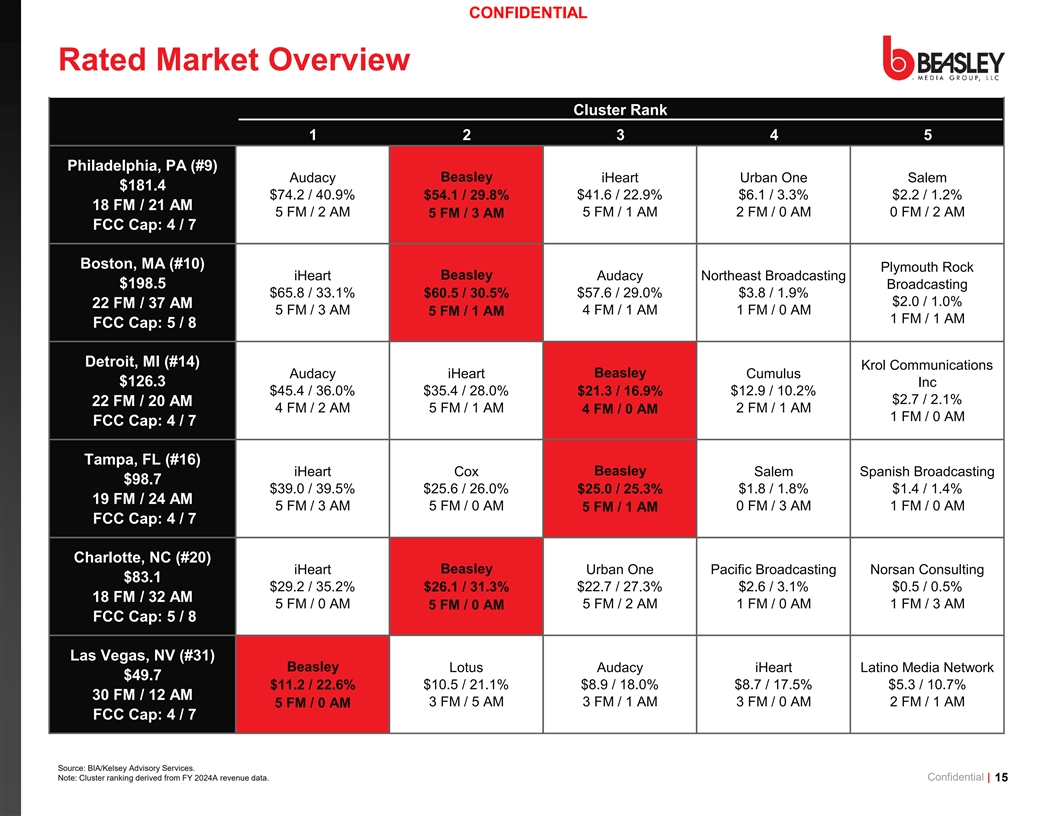

CONFIDENTIAL Rated Market Overview Cluster Rank 1 2 3 4 5 Philadelphia, PA (#9) Beasley Audacy iHeart Urban One Salem $181.4 $74.2 / 40.9% $54.1 / 29.8% $41.6 / 22.9% $6.1 / 3.3% $2.2 / 1.2% 18 FM / 21 AM 5 FM / 2 AM 5 FM / 3 AM 5 FM / 1 AM 2 FM / 0 AM 0 FM / 2 AM FCC Cap: 4 / 7 Boston, MA (#10) Plymouth Rock iHeart Beasley Audacy Northeast Broadcasting $198.5 Broadcasting $65.8 / 33.1% $60.5 / 30.5% $57.6 / 29.0% $3.8 / 1.9% $2.0 / 1.0% 22 FM / 37 AM 5 FM / 3 AM 4 FM / 1 AM 1 FM / 0 AM 5 FM / 1 AM 1 FM / 1 AM FCC Cap: 5 / 8 Detroit, MI (#14) Krol Communications Beasley Audacy iHeart Cumulus $126.3 Inc $45.4 / 36.0% $35.4 / 28.0% $21.3 / 16.9% $12.9 / 10.2% $2.7 / 2.1% 22 FM / 20 AM 4 FM / 2 AM 5 FM / 1 AM 4 FM / 0 AM 2 FM / 1 AM 1 FM / 0 AM FCC Cap: 4 / 7 Tampa, FL (#16) iHeart Cox Beasley Salem Spanish Broadcasting $98.7 $39.0 / 39.5% $25.6 / 26.0% $25.0 / 25.3% $1.8 / 1.8% $1.4 / 1.4% 19 FM / 24 AM 5 FM / 3 AM 5 FM / 0 AM 0 FM / 3 AM 1 FM / 0 AM 5 FM / 1 AM FCC Cap: 4 / 7 Charlotte, NC (#20) Beasley iHeart Urban One Pacific Broadcasting Norsan Consulting $83.1 $29.2 / 35.2% $26.1 / 31.3% $22.7 / 27.3% $2.6 / 3.1% $0.5 / 0.5% 18 FM / 32 AM 5 FM / 0 AM 5 FM / 2 AM 1 FM / 0 AM 1 FM / 3 AM 5 FM / 0 AM FCC Cap: 5 / 8 Las Vegas, NV (#31) Beasley Lotus Audacy iHeart Latino Media Network $49.7 $11.2 / 22.6% $10.5 / 21.1% $8.9 / 18.0% $8.7 / 17.5% $5.3 / 10.7% 30 FM / 12 AM 3 FM / 5 AM 3 FM / 1 AM 3 FM / 0 AM 2 FM / 1 AM 5 FM / 0 AM FCC Cap: 4 / 7 Source: BIA/Kelsey Advisory Services. Note: Cluster ranking derived from FY 2024A revenue data. Confidential | 15

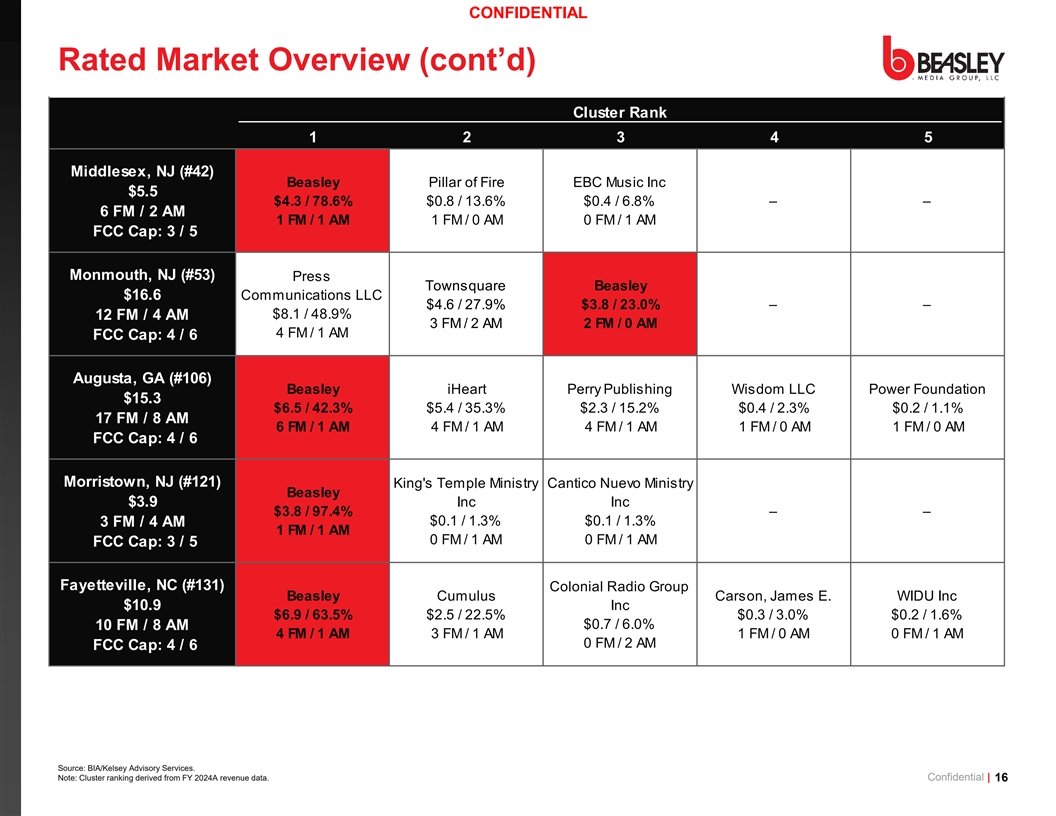

CONFIDENTIAL Rated Market Overview (cont’d) Cluster Rank 1 2 3 4 5 Middlesex, NJ (#42) Beasley Pillar of Fire EBC Music Inc $5.5 $4.3 / 78.6% $0.8 / 13.6% $0.4 / 6.8% – – 6 FM / 2 AM 1 FM / 1 AM 1 FM / 0 AM 0 FM / 1 AM FCC Cap: 3 / 5 Monmouth, NJ (#53) Press Townsquare Beasley $16.6 Communications LLC $4.6 / 27.9% $3.8 / 23.0% – – $8.1 / 48.9% 12 FM / 4 AM 3 FM / 2 AM 2 FM / 0 AM 4 FM / 1 AM FCC Cap: 4 / 6 Augusta, GA (#106) Beasley iHeart Perry Publishing Wisdom LLC Power Foundation $15.3 $6.5 / 42.3% $5.4 / 35.3% $2.3 / 15.2% $0.4 / 2.3% $0.2 / 1.1% 17 FM / 8 AM 6 FM / 1 AM 4 FM / 1 AM 4 FM / 1 AM 1 FM / 0 AM 1 FM / 0 AM FCC Cap: 4 / 6 Morristown, NJ (#121) King's Temple Ministry Cantico Nuevo Ministry Beasley $3.9 Inc Inc $3.8 / 97.4% – – $0.1 / 1.3% $0.1 / 1.3% 3 FM / 4 AM 1 FM / 1 AM 0 FM / 1 AM 0 FM / 1 AM FCC Cap: 3 / 5 Fayetteville, NC (#131) Colonial Radio Group Beasley Cumulus Carson, James E. WIDU Inc $10.9 Inc $6.9 / 63.5% $2.5 / 22.5% $0.3 / 3.0% $0.2 / 1.6% $0.7 / 6.0% 10 FM / 8 AM 4 FM / 1 AM 3 FM / 1 AM 1 FM / 0 AM 0 FM / 1 AM 0 FM / 2 AM FCC Cap: 4 / 6 Source: BIA/Kelsey Advisory Services. Note: Cluster ranking derived from FY 2024A revenue data. Confidential | 16

CONFIDENTIAL Beasley’s Continued Digital Transformation Beasley’s continued growth initiatives within its Digital segment should provide for enhanced growth and scale while increasing margins via developing new products, expanding O&O, focusing on podcasting and video and leveraging existing relationships to cross sell bundled packages via a recalibrated sales force 1 Development of New Products • Company rolled-out market level infrastructure including newsletters and websites to capitalize on long-standing audience base in markets, reduce go-forward expenses, optimize content delivery, and enable enhanced network expansion • Company recently launched its self-serve portal for smaller AOV sales in Tampa, with broader launch expected in Q1’26, yielding higher margins via minimizing touchpoints and allowing the Company to concentrate sales force efforts around larger transactions • Sports viewers have proven to be more engaged with the platform and remain a focus on a go-forward basis through partnerships 2 Expanding Sales of O&O Products • Vast O&O product inventory in conjunction with increased incentives and Digital product training, should yield additional higher-margin top-line upside • Sales commissions reduced on TPP, incentivizing shift to O&O and leading to improved margins • Combination of O&O and programmatic availability for direct attribution dashboards / reporting for clients • Centralized all customer reporting to decrease the reliance on reporting from vendors and increase O&O performance visibility 3 Podcasting and Video Offering Focus • Podcasting makes up ~11% of Beasley’s digital audio product with video making up one of the biggest growth levers • Podcasting and Plus products allows for a waterfall approach starting with high margin O&O and then dropping to programmatic at a lower rate • Production and implementation of full-scale video content for sports in process • Opportunities for quality partnerships which could raise CPMs and increase distribution 4 Sales Force Recalibration and Cross Selling • Train existing Sales Force on consultative selling to refocus sales efforts around optimizing client results across Digital and Audio, while emphasizing accountability • Shift Sales Development Representative concentration to developing further digital advertiser relationships • Revamped commission plans to incentive the sale of Beasley’s direct products, such as O&O digital and direct spot business • Moved SEO product to internal team to increase margins, utilize labor on owned and operated properties, and increase quality Confidential | 17

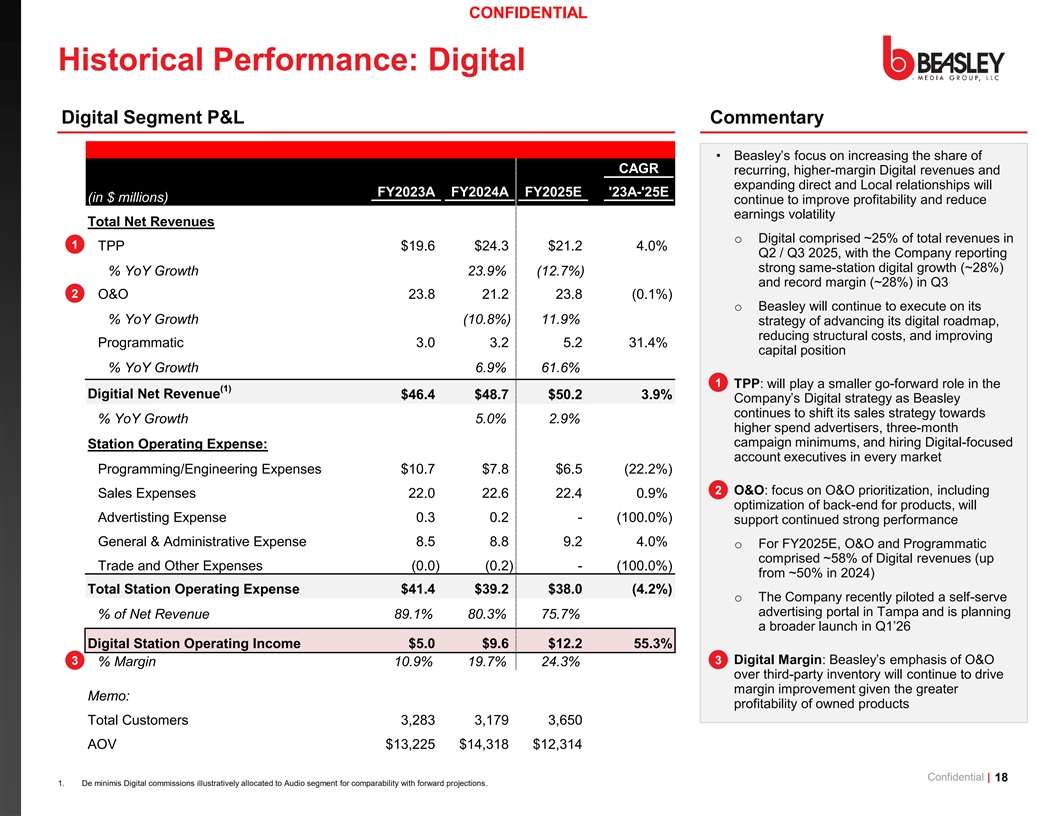

CONFIDENTIAL Historical Performance: Digital Digital Segment P&L Commentary • Beasley’s focus on increasing the share of CAGR recurring, higher-margin Digital revenues and expanding direct and Local relationships will FY2023A FY2024A FY2025E '23A-'25E (in $ millions) continue to improve profitability and reduce earnings volatility Total Net Revenues o Digital comprised ~25% of total revenues in 1 TPP $19.6 $24.3 $21.2 4.0% Q2 / Q3 2025, with the Company reporting strong same-station digital growth (~28%) % YoY Growth 23.9% (12.7%) and record margin (~28%) in Q3 2 O&O 23.8 21.2 23.8 (0.1%) o Beasley will continue to execute on its % YoY Growth (10.8%) 11.9% strategy of advancing its digital roadmap, reducing structural costs, and improving Programmatic 3.0 3.2 5.2 31.4% capital position % YoY Growth 6.9% 61.6% 1 • TPP: will play a smaller go-forward role in the (1) Digitial Net Revenue $46.4 $48.7 $50.2 3.9% Company’s Digital strategy as Beasley continues to shift its sales strategy towards % YoY Growth 5.0% 2.9% higher spend advertisers, three-month campaign minimums, and hiring Digital-focused Station Operating Expense: account executives in every market Programming/Engineering Expenses $10.7 $7.8 $6.5 (22.2%) 2 • O&O: focus on O&O prioritization, including Sales Expenses 22.0 22.6 22.4 0.9% optimization of back-end for products, will Advertisting Expense 0.3 0.2 - (100.0%) support continued strong performance General & Administrative Expense 8.5 8.8 9.2 4.0% o For FY2025E, O&O and Programmatic comprised ~58% of Digital revenues (up Trade and Other Expenses (0.0) (0.2) - (100.0%) from ~50% in 2024) Total Station Operating Expense $41.4 $39.2 $38.0 (4.2%) o The Company recently piloted a self-serve advertising portal in Tampa and is planning % of Net Revenue 89.1% 80.3% 75.7% a broader launch in Q1’26 Digital Station Operating Income $5.0 $9.6 $12.2 55.3% 3 • Digital Margin: Beasley’s emphasis of O&O 3 % Margin 10.9% 19.7% 24.3% over third-party inventory will continue to drive margin improvement given the greater Memo: profitability of owned products Total Customers 3,283 3,179 3,650 AOV $13,225 $14,318 $12,314 Confidential | 18 1. De minimis Digital commissions illustratively allocated to Audio segment for comparability with forward projections.

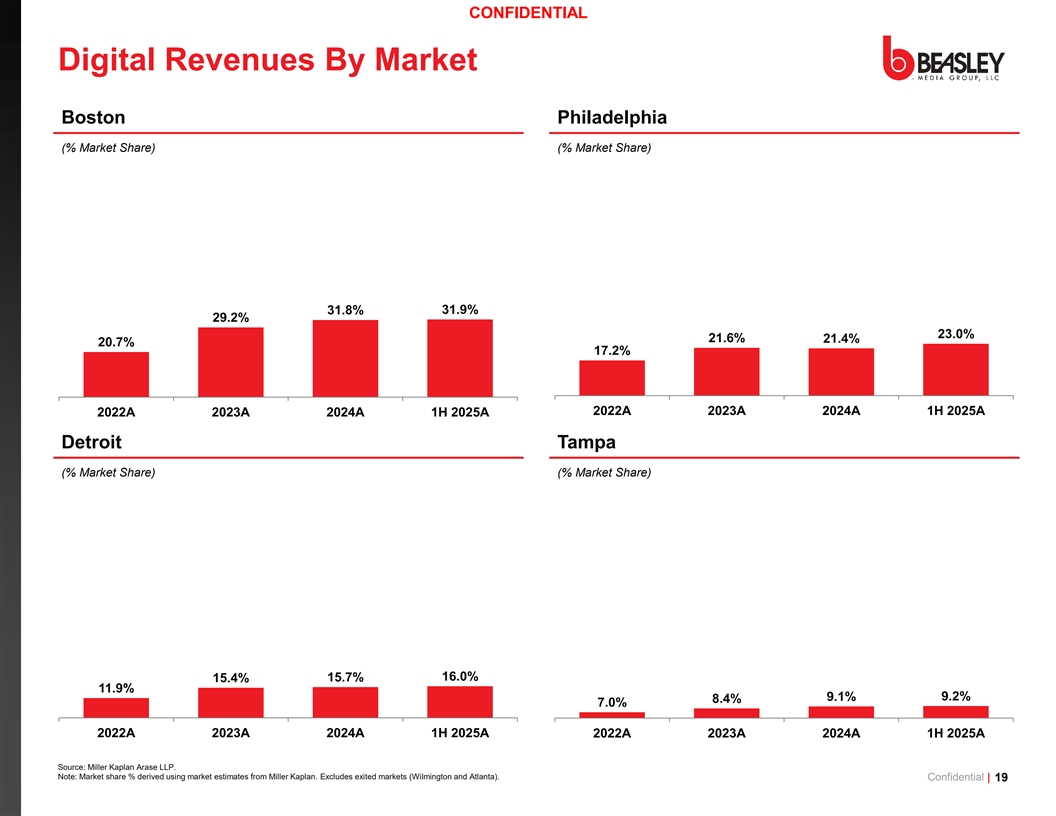

CONFIDENTIAL Digital Revenues By Market Boston Philadelphia (% Market Share) (% Market Share) 49.4% 48.4% 45.9% 45.5% 31.9% 31.8% 31.8% 31.9% 29.2% 24.5% 23.0% 22.5% 23.0% 21.4% 21.6% 21.4% 20.7% 20.7% 17.2% 17.2% 20 2022A 22A 20 2023A 23A 20 2024A 24A 1H 1H 2025A 2025A 2022A 2023A 2024A 1H 2025A 20 2022A 22A 20 2023A 23A 20 2024A 24A 1H 1H 2025A 2025A Detroit Tampa (% Market Share) (% Market Share) 49.4% 48.4% 45.9% 45.5% 21.5% 19.8% 16.0% 15.7% 15.7% 16.0% 15.4% 18.7% 14.3% 11.9% 11.9% 16.1% 9.1% 9.2% 9.1% 9.2% 8.4% 7.0% 7.0% 6.6% 20 2022A 22A 20 2023A 23A 20 2024A 24A 1H 1H 2025 2025A A 20 2022A 22A 20 2023A 23A 20 2024A 24A 1H 1H 2025A 2025A 20 2022A 22A 20 2023A 23A 20 2024A 24A 1H 1H 2025 2025A A Source: Miller Kaplan Arase LLP. Note: Market share % derived using market estimates from Miller Kaplan. Excludes exited markets (Wilmington and Atlanta). Confidential | 19

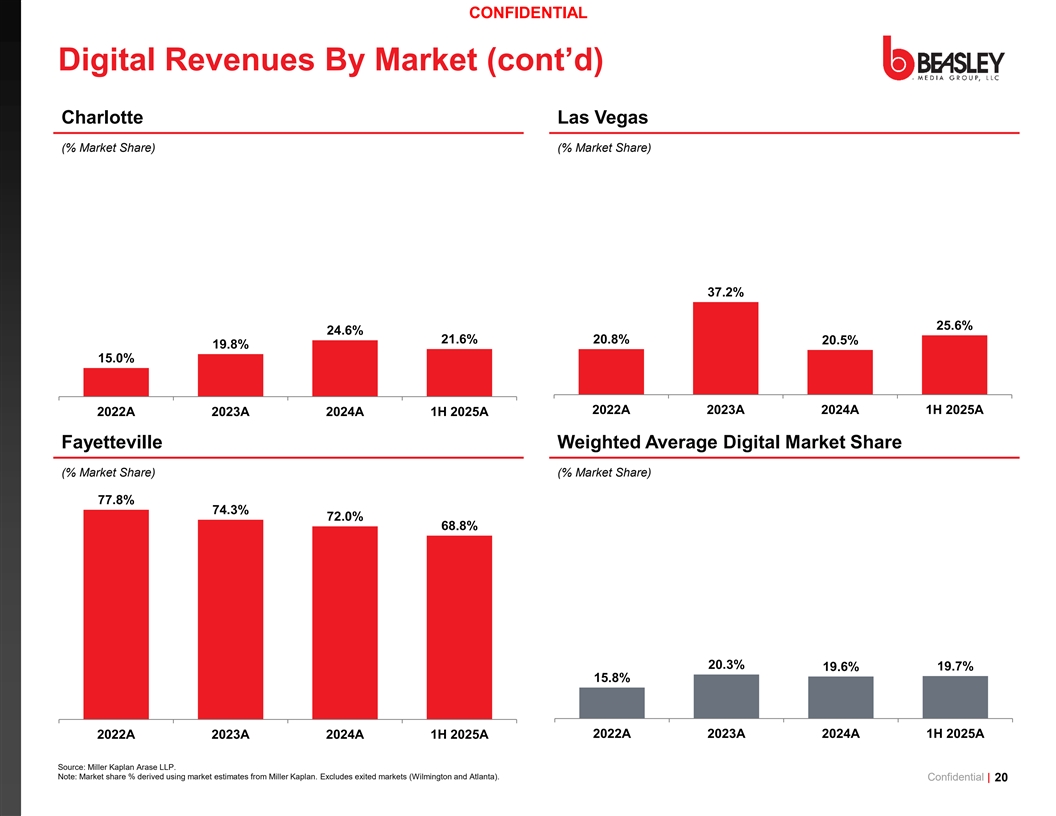

CONFIDENTIAL Digital Revenues By Market (cont’d) Charlotte Las Vegas (% Market Share) (% Market Share) 37.2% 27.5% 25.6% 25.6% 24.6% 24.6% 21.6% 21.6% 20.8% 20.8% 20.5% 20.5% 19.8% 16.7% 15.0% 15.0% 20 2022A 22A 20 2023A 23A 20 2024A 24A 1H 1H 2025A 2025A 20 2022A 22A 20 2023A 23A 20 2024A 24A 1H 1H 2025A 2025A Fayetteville Weighted Average Digital Market Share (% Market Share) (% Market Share) 77.8% 77.8% 74.3% 38.7% 72.9% 72.0% 72.0% 68.8% 68.8% 37.5% 37.4% 37.4% 32.7% 32.7% 31.4% 29.3% 20.3% 19.7% 19.6% 19.6% 19.7% 18.1% 15.8% 15.8% 2022A 2023A 2024A 1H 2025A 20 2022A 22A 20 2023A 23A 20 2024A 24A 1H 1H 2025A 2025A 20 2022A 22A 20 2023A 23A 20 2024A 24A 1H 1H 2025A 2025A 2022A 2023A 2024A 1H 2025A Source: Miller Kaplan Arase LLP. Note: Market share % derived using market estimates from Miller Kaplan. Excludes exited markets (Wilmington and Atlanta). Confidential | 20

2. Business Plan Overview Confidential | 21

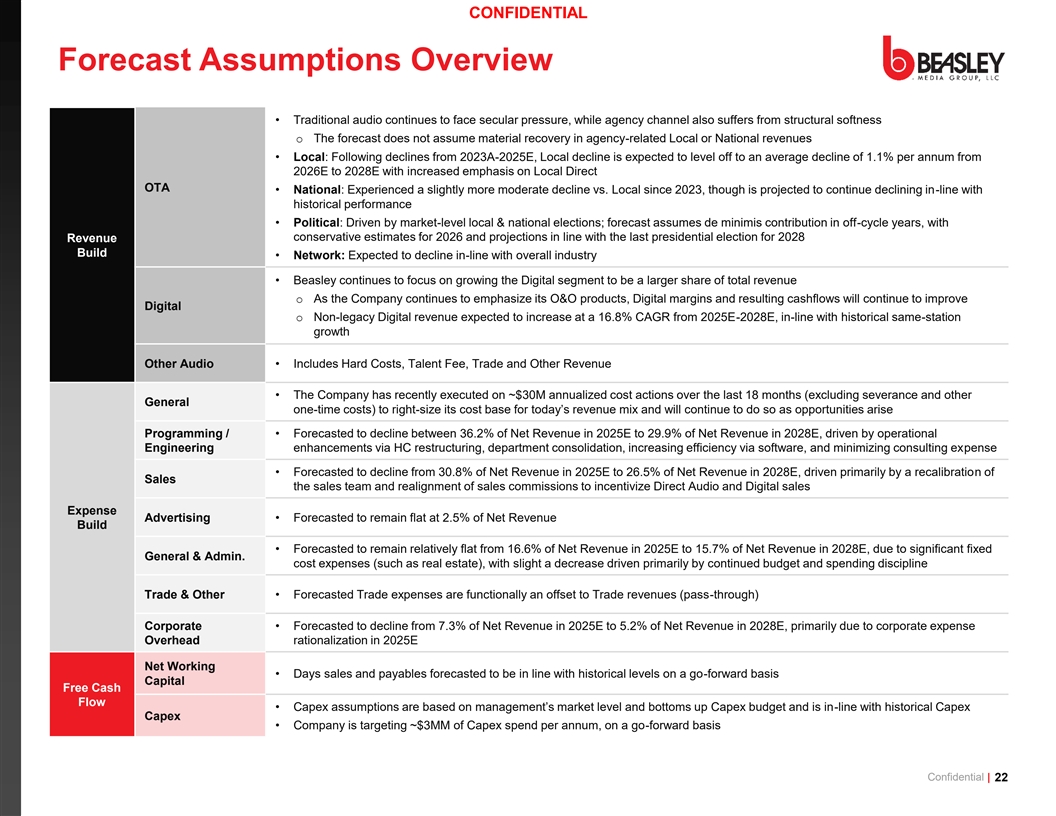

CONFIDENTIAL Forecast Assumptions Overview • Traditional audio continues to face secular pressure, while agency channel also suffers from structural softness o The forecast does not assume material recovery in agency-related Local or National revenues • Local: Following declines from 2023A-2025E, Local decline is expected to level off to an average decline of 1.1% per annum from 2026E to 2028E with increased emphasis on Local Direct OTA • National: Experienced a slightly more moderate decline vs. Local since 2023, though is projected to continue declining in-line with historical performance • Political: Driven by market-level local & national elections; forecast assumes de minimis contribution in off-cycle years, with conservative estimates for 2026 and projections in line with the last presidential election for 2028 Revenue Build • Network: Expected to decline in-line with overall industry • Beasley continues to focus on growing the Digital segment to be a larger share of total revenue o As the Company continues to emphasize its O&O products, Digital margins and resulting cashflows will continue to improve Digital o Non-legacy Digital revenue expected to increase at a 16.8% CAGR from 2025E-2028E, in-line with historical same-station growth Other Audio • Includes Hard Costs, Talent Fee, Trade and Other Revenue • The Company has recently executed on ~$30M annualized cost actions over the last 18 months (excluding severance and other General one-time costs) to right-size its cost base for today’s revenue mix and will continue to do so as opportunities arise Programming / • Forecasted to decline between 36.2% of Net Revenue in 2025E to 29.9% of Net Revenue in 2028E, driven by operational Engineering enhancements via HC restructuring, department consolidation, increasing efficiency via software, and minimizing consulting expense • Forecasted to decline from 30.8% of Net Revenue in 2025E to 26.5% of Net Revenue in 2028E, driven primarily by a recalibration of Sales the sales team and realignment of sales commissions to incentivize Direct Audio and Digital sales Expense Advertising • Forecasted to remain flat at 2.5% of Net Revenue Build • Forecasted to remain relatively flat from 16.6% of Net Revenue in 2025E to 15.7% of Net Revenue in 2028E, due to significant fixed General & Admin. cost expenses (such as real estate), with slight a decrease driven primarily by continued budget and spending discipline Trade & Other • Forecasted Trade expenses are functionally an offset to Trade revenues (pass-through) Corporate • Forecasted to decline from 7.3% of Net Revenue in 2025E to 5.2% of Net Revenue in 2028E, primarily due to corporate expense Overhead rationalization in 2025E Net Working • Days sales and payables forecasted to be in line with historical levels on a go-forward basis Capital Free Cash Flow • Capex assumptions are based on management’s market level and bottoms up Capex budget and is in-line with historical Capex Capex • Company is targeting ~$3MM of Capex spend per annum, on a go-forward basis Confidential | 22

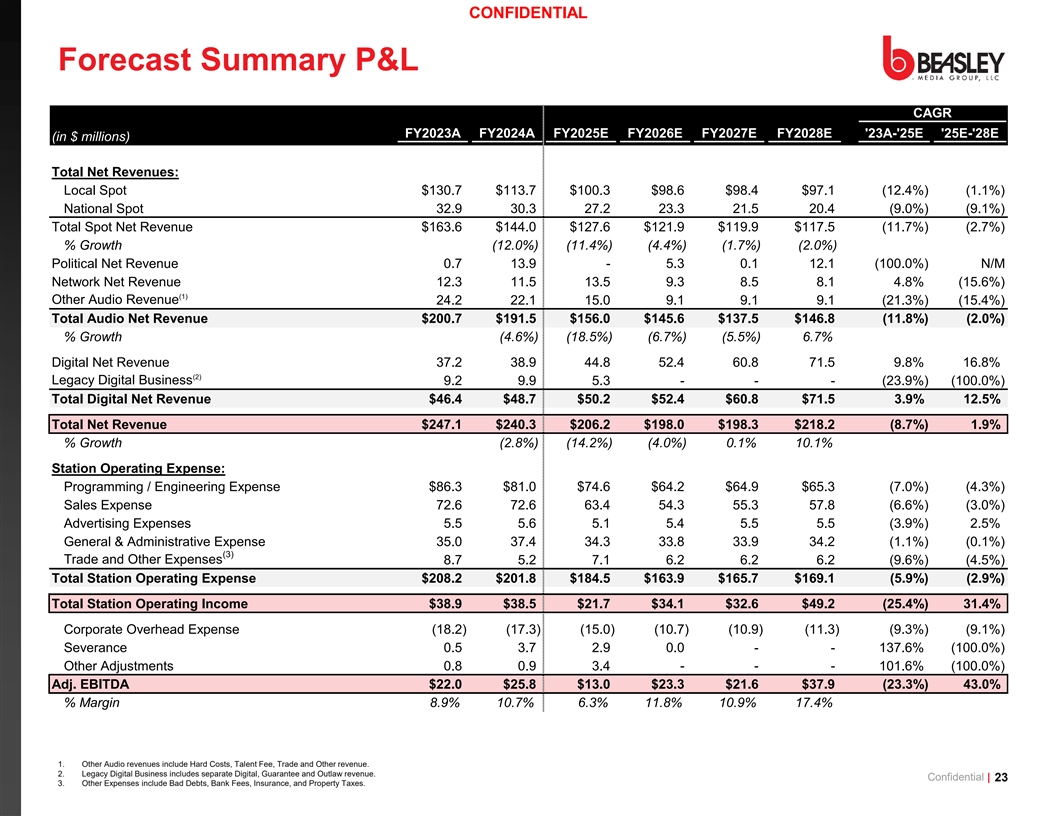

CONFIDENTIAL Forecast Summary P&L CAGR FY2023A FY2024A FY2025E FY2026E FY2027E FY2028E '23A-'25E '25E-'28E (in $ millions) Total Net Revenues: Local Spot $130.7 $113.7 $100.3 $98.6 $98.4 $97.1 (12.4%) (1.1%) National Spot 32.9 30.3 27.2 23.3 21.5 20.4 (9.0%) (9.1%) Total Spot Net Revenue $163.6 $144.0 $127.6 $121.9 $119.9 $117.5 (11.7%) (2.7%) % Growth (12.0%) (11.4%) (4.4%) (1.7%) (2.0%) Political Net Revenue 0.7 13.9 - 5.3 0.1 12.1 (100.0%) N/M Network Net Revenue 12.3 11.5 13.5 9.3 8.5 8.1 4.8% (15.6%) (1) Other Audio Revenue 24.2 22.1 15.0 9.1 9.1 9.1 (21.3%) (15.4%) Total Audio Net Revenue $200.7 $191.5 $156.0 $145.6 $137.5 $146.8 (11.8%) (2.0%) % Growth (4.6%) (18.5%) (6.7%) (5.5%) 6.7% Digital Net Revenue 37.2 38.9 44.8 52.4 60.8 71.5 9.8% 16.8% (2) Legacy Digital Business 9.2 9.9 5.3 - - - (23.9%) (100.0%) Total Digital Net Revenue $46.4 $48.7 $50.2 $52.4 $60.8 $71.5 3.9% 12.5% Total Net Revenue $247.1 $240.3 $206.2 $198.0 $198.3 $218.2 (8.7%) 1.9% % Growth (2.8%) (14.2%) (4.0%) 0.1% 10.1% Station Operating Expense: Programming / Engineering Expense $86.3 $81.0 $74.6 $64.2 $64.9 $65.3 (7.0%) (4.3%) Sales Expense 72.6 72.6 63.4 54.3 55.3 57.8 (6.6%) (3.0%) Advertising Expenses 5.5 5.6 5.1 5.4 5.5 5.5 (3.9%) 2.5% General & Administrative Expense 35.0 37.4 34.3 33.8 33.9 34.2 (1.1%) (0.1%) (3) Trade and Other Expenses 8.7 5.2 7.1 6.2 6.2 6.2 (9.6%) (4.5%) Total Station Operating Expense $208.2 $201.8 $184.5 $163.9 $165.7 $169.1 (5.9%) (2.9%) Total Station Operating Income $38.9 $38.5 $21.7 $34.1 $32.6 $49.2 (25.4%) 31.4% Corporate Overhead Expense (18.2) (17.3) (15.0) (10.7) (10.9) (11.3) (9.3%) (9.1%) Severance 0.5 3.7 2.9 0.0 - - 137.6% (100.0%) Other Adjustments 0.8 0.9 3.4 - - - 101.6% (100.0%) Adj. EBITDA $22.0 $25.8 $13.0 $23.3 $21.6 $37.9 (23.3%) 43.0% % Margin 8.9% 10.7% 6.3% 11.8% 10.9% 17.4% 1. Other Audio revenues include Hard Costs, Talent Fee, Trade and Other revenue. 2. Legacy Digital Business includes separate Digital, Guarantee and Outlaw revenue. Confidential | 23 3. Other Expenses include Bad Debts, Bank Fees, Insurance, and Property Taxes.

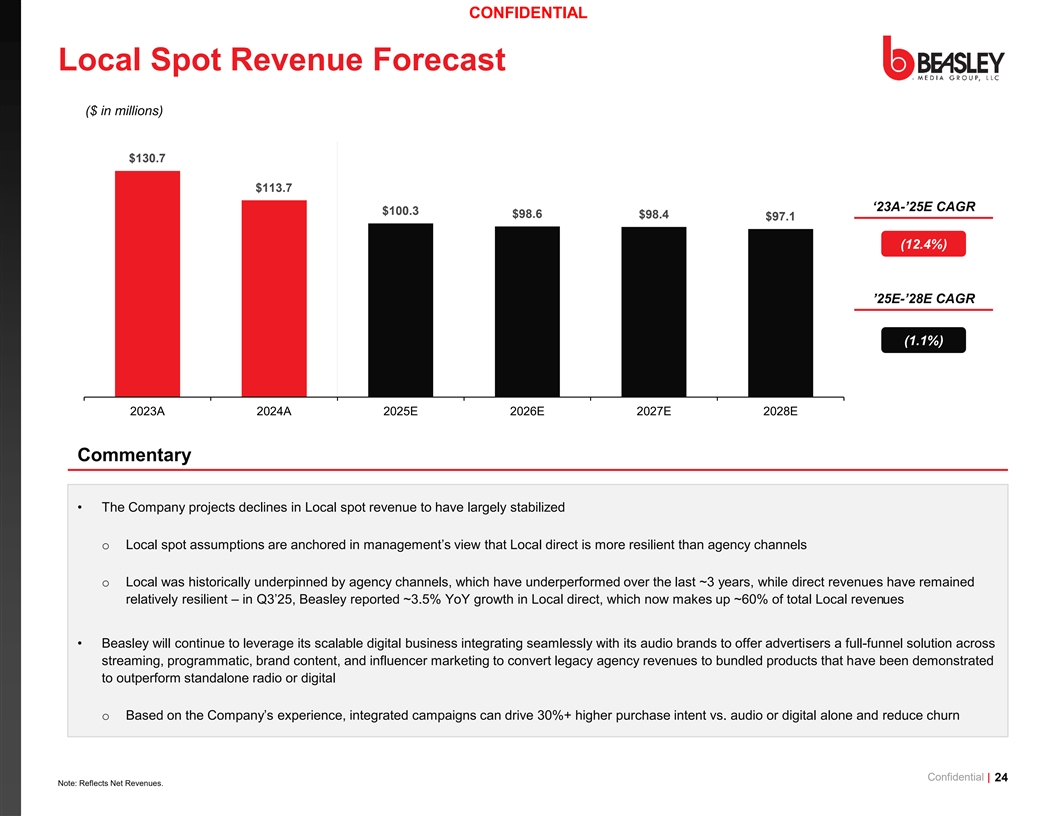

CONFIDENTIAL Local Spot Revenue Forecast ($ in millions) $130.7 $113.7 ‘23A-’25E CAGR $100.3 $98.6 $98.4 $97.1 (12.4%) ’25E-’28E CAGR (1.1%) 2023A 2024A 2025E 2026E 2027E 2028E Commentary • The Company projects declines in Local spot revenue to have largely stabilized o Local spot assumptions are anchored in management’s view that Local direct is more resilient than agency channels o Local was historically underpinned by agency channels, which have underperformed over the last ~3 years, while direct revenues have remained relatively resilient – in Q3’25, Beasley reported ~3.5% YoY growth in Local direct, which now makes up ~60% of total Local revenues • Beasley will continue to leverage its scalable digital business integrating seamlessly with its audio brands to offer advertisers a full-funnel solution across streaming, programmatic, brand content, and influencer marketing to convert legacy agency revenues to bundled products that have been demonstrated to outperform standalone radio or digital o Based on the Company’s experience, integrated campaigns can drive 30%+ higher purchase intent vs. audio or digital alone and reduce churn Confidential | 24 Note: Reflects Net Revenues.

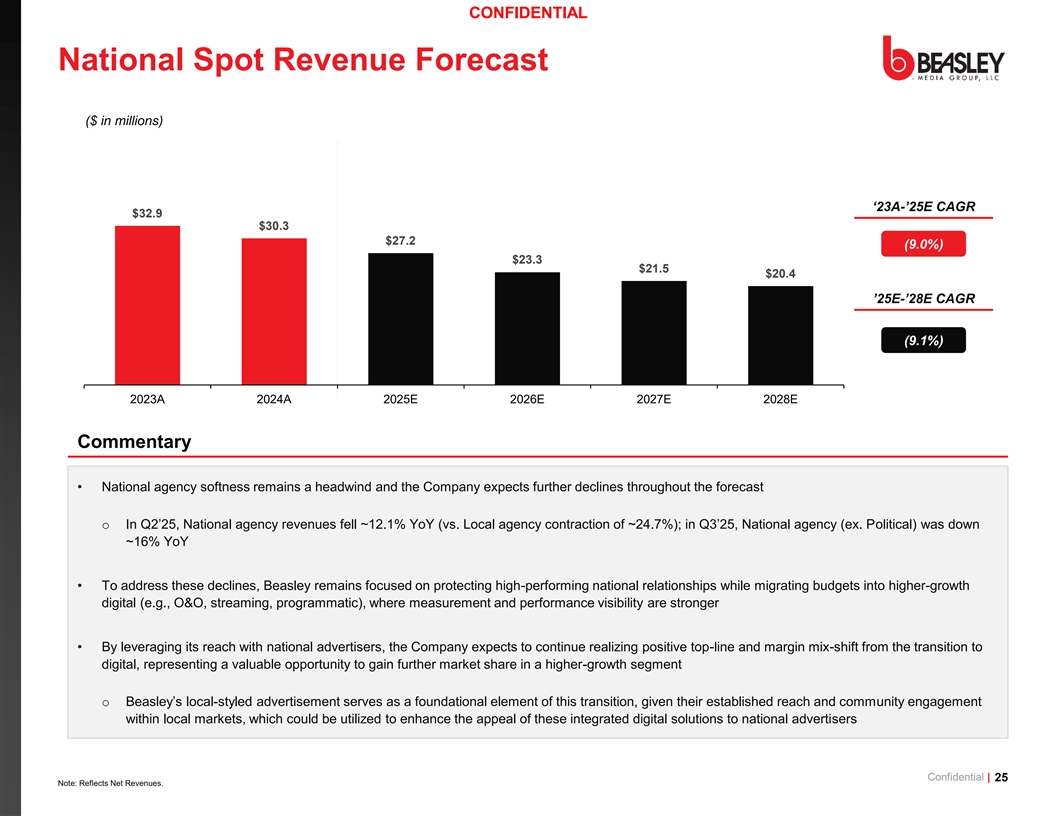

CONFIDENTIAL National Spot Revenue Forecast ($ in millions) ‘23A-’25E CAGR $32.9 $30.3 $27.2 (9.0%) $23.3 $21.5 $20.4 ’25E-’28E CAGR (9.1%) 2023A 2024A 2025E 2026E 2027E 2028E Commentary • National agency softness remains a headwind and the Company expects further declines throughout the forecast o In Q2’25, National agency revenues fell ~12.1% YoY (vs. Local agency contraction of ~24.7%); in Q3’25, National agency (ex. Political) was down ~16% YoY • To address these declines, Beasley remains focused on protecting high-performing national relationships while migrating budgets into higher-growth digital (e.g., O&O, streaming, programmatic), where measurement and performance visibility are stronger • By leveraging its reach with national advertisers, the Company expects to continue realizing positive top-line and margin mix-shift from the transition to digital, representing a valuable opportunity to gain further market share in a higher-growth segment o Beasley’s local-styled advertisement serves as a foundational element of this transition, given their established reach and community engagement within local markets, which could be utilized to enhance the appeal of these integrated digital solutions to national advertisers Confidential | 25 Note: Reflects Net Revenues.

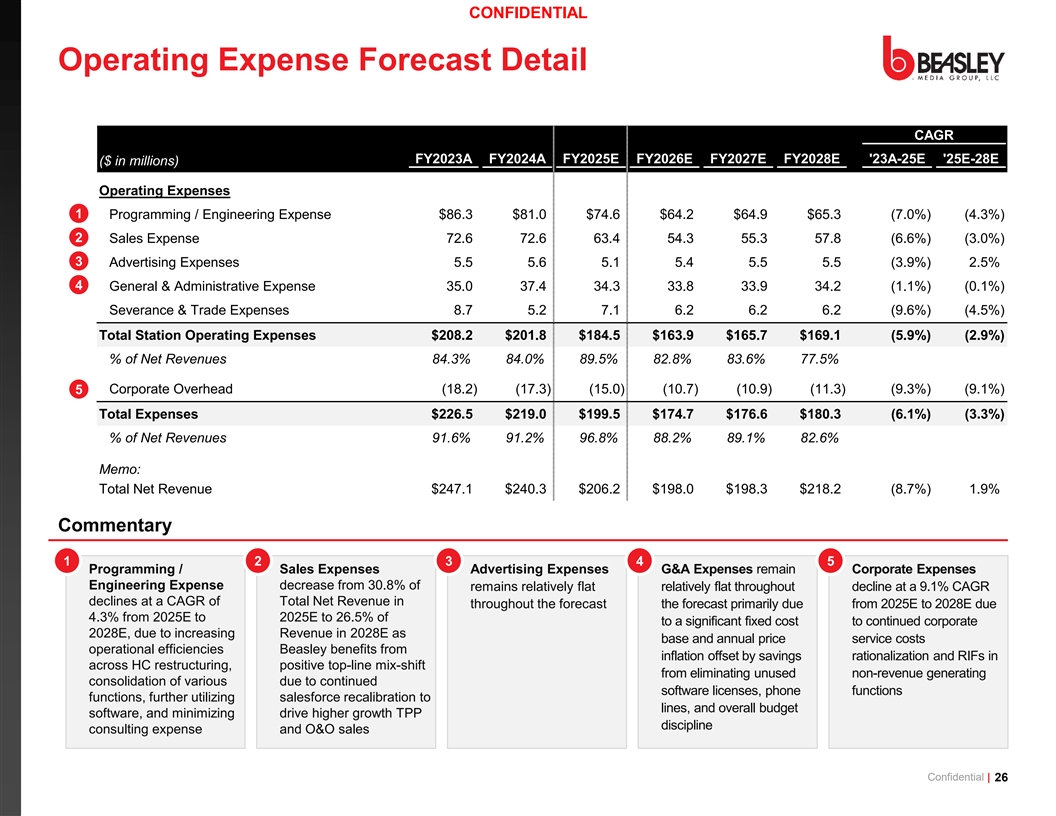

CONFIDENTIAL Operating Expense Forecast Detail CAGR FY2023A FY2024A FY2025E FY2026E FY2027E FY2028E '23A-25E '25E-28E ($ in millions) Operating Expenses 1 Programming / Engineering Expense $86.3 $81.0 $74.6 $64.2 $64.9 $65.3 (7.0%) (4.3%) 2 Sales Expense 72.6 72.6 63.4 54.3 55.3 57.8 (6.6%) (3.0%) 3 Advertising Expenses 5.5 5.6 5.1 5.4 5.5 5.5 (3.9%) 2.5% 4 General & Administrative Expense 35.0 37.4 34.3 33.8 33.9 34.2 (1.1%) (0.1%) Severance & Trade Expenses 8.7 5.2 7.1 6.2 6.2 6.2 (9.6%) (4.5%) Total Station Operating Expenses $208.2 $201.8 $184.5 $163.9 $165.7 $169.1 (5.9%) (2.9%) % of Net Revenues 84.3% 84.0% 89.5% 82.8% 83.6% 77.5% Corporate Overhead (18.2) (17.3) (15.0) (10.7) (10.9) (11.3) (9.3%) (9.1%) 5 Total Expenses $226.5 $219.0 $199.5 $174.7 $176.6 $180.3 (6.1%) (3.3%) % of Net Revenues 91.6% 91.2% 96.8% 88.2% 89.1% 82.6% Memo: Total Net Revenue $247.1 $240.3 $206.2 $198.0 $198.3 $218.2 (8.7%) 1.9% Commentary 1 2 3 4 5 • Programming / • Sales Expenses • Advertising Expenses • G&A Expenses remain • Corporate Expenses Engineering Expense decrease from 30.8% of remains relatively flat relatively flat throughout decline at a 9.1% CAGR declines at a CAGR of Total Net Revenue in throughout the forecast the forecast primarily due from 2025E to 2028E due 4.3% from 2025E to 2025E to 26.5% of to a significant fixed cost to continued corporate 2028E, due to increasing Revenue in 2028E as base and annual price service costs operational efficiencies Beasley benefits from inflation offset by savings rationalization and RIFs in across HC restructuring, positive top-line mix-shift from eliminating unused non-revenue generating consolidation of various due to continued software licenses, phone functions functions, further utilizing salesforce recalibration to lines, and overall budget software, and minimizing drive higher growth TPP discipline consulting expense and O&O sales Confidential | 26

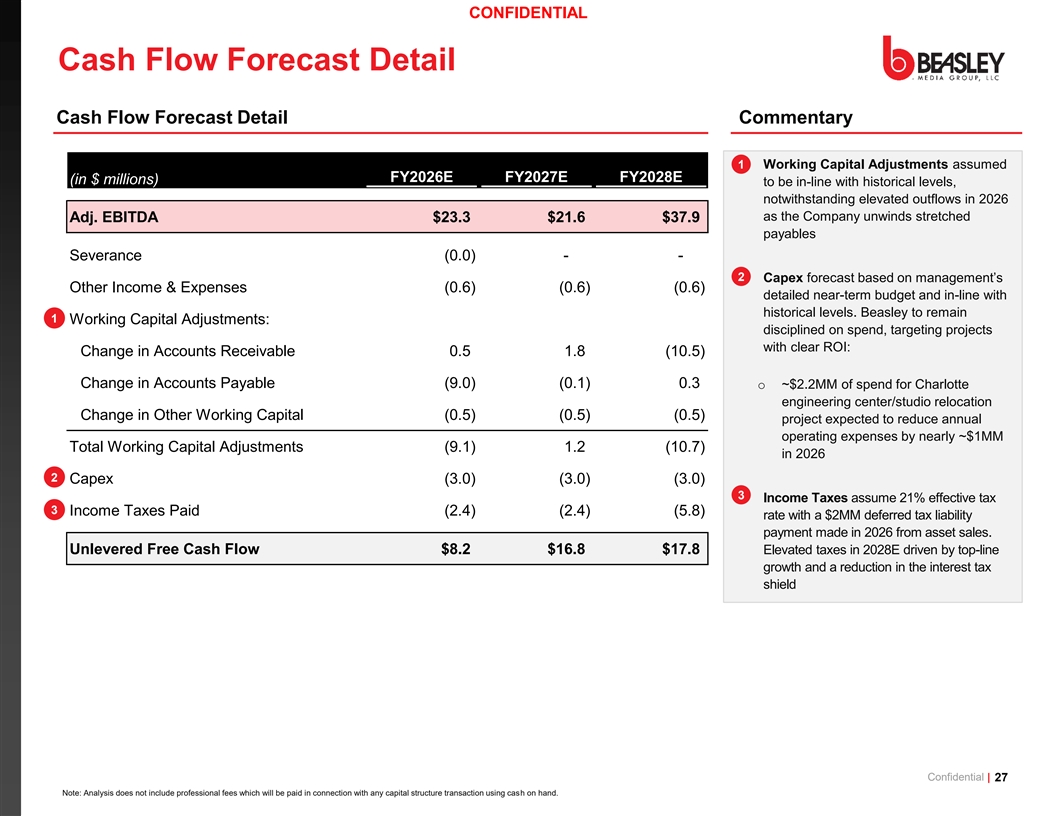

CONFIDENTIAL Cash Flow Forecast Detail Cash Flow Forecast Detail Commentary 1 • Working Capital Adjustments assumed FY2026E FY2027E FY2028E (in $ millions) to be in-line with historical levels, notwithstanding elevated outflows in 2026 as the Company unwinds stretched Adj. EBITDA $23.3 $21.6 $37.9 payables Severance (0 .0) - - 2 • Capex forecast based on management’s Other Income & Expenses (0 .6) (0 .6) (0 .6) detailed near-term budget and in-line with historical levels. Beasley to remain 1 Working Capital Adjustments: disciplined on spend, targeting projects with clear ROI: Change in Accounts Receivable 0.5 1.8 (10.5) Change in Accounts Payable (9 .0) (0 .1) 0.3 o ~$2.2MM of spend for Charlotte engineering center/studio relocation Change in Other Working Capital (0 .5) (0 .5) (0 .5) project expected to reduce annual operating expenses by nearly ~$1MM Total Working Capital Adjustments (9 .1) 1.2 (1 0.7) in 2026 2 Capex (3 .0) (3 .0) (3 .0) 3 • Income Taxes assume 21% effective tax 3 Income Taxes Paid (2 .4) (2 .4) (5 .8) rate with a $2MM deferred tax liability payment made in 2026 from asset sales. Unlevered Free Cash Flow $8.2 $16.8 $17.8 Elevated taxes in 2028E driven by top-line growth and a reduction in the interest tax shield Confidential | 27 Note: Analysis does not include professional fees which will be paid in connection with any capital structure transaction using cash on hand.

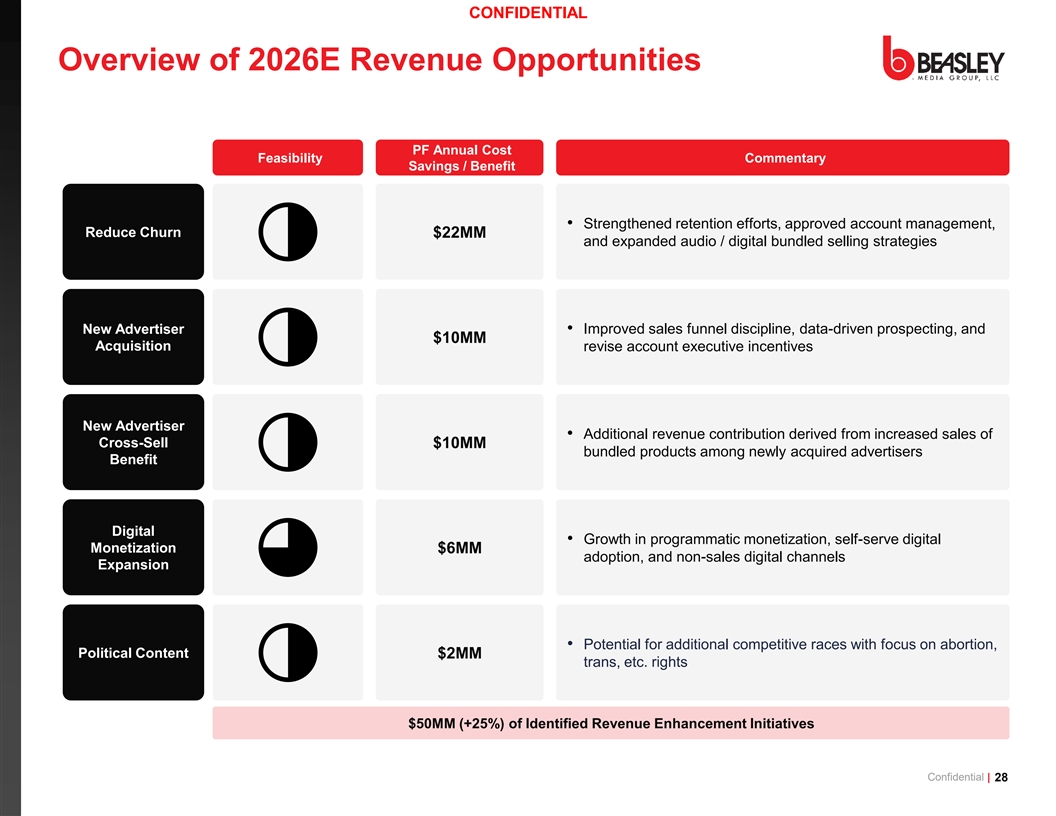

CONFIDENTIAL Overview of 2026E Revenue Opportunities PF Annual Cost Feasibility Commentary Savings / Benefit • Strengthened retention efforts, approved account management, Reduce Churn $22MM and expanded audio / digital bundled selling strategies • Improved sales funnel discipline, data-driven prospecting, and New Advertiser $10MM Acquisition revise account executive incentives New Advertiser • Additional revenue contribution derived from increased sales of Cross-Sell $10MM bundled products among newly acquired advertisers Benefit Digital • Growth in programmatic monetization, self-serve digital Monetization $6MM adoption, and non-sales digital channels Expansion • Potential for additional competitive races with focus on abortion, Political Content $2MM trans, etc. rights $50MM (+25%) of Identified Revenue Enhancement Initiatives Confidential | 28

3. Transaction Overview Confidential | 29

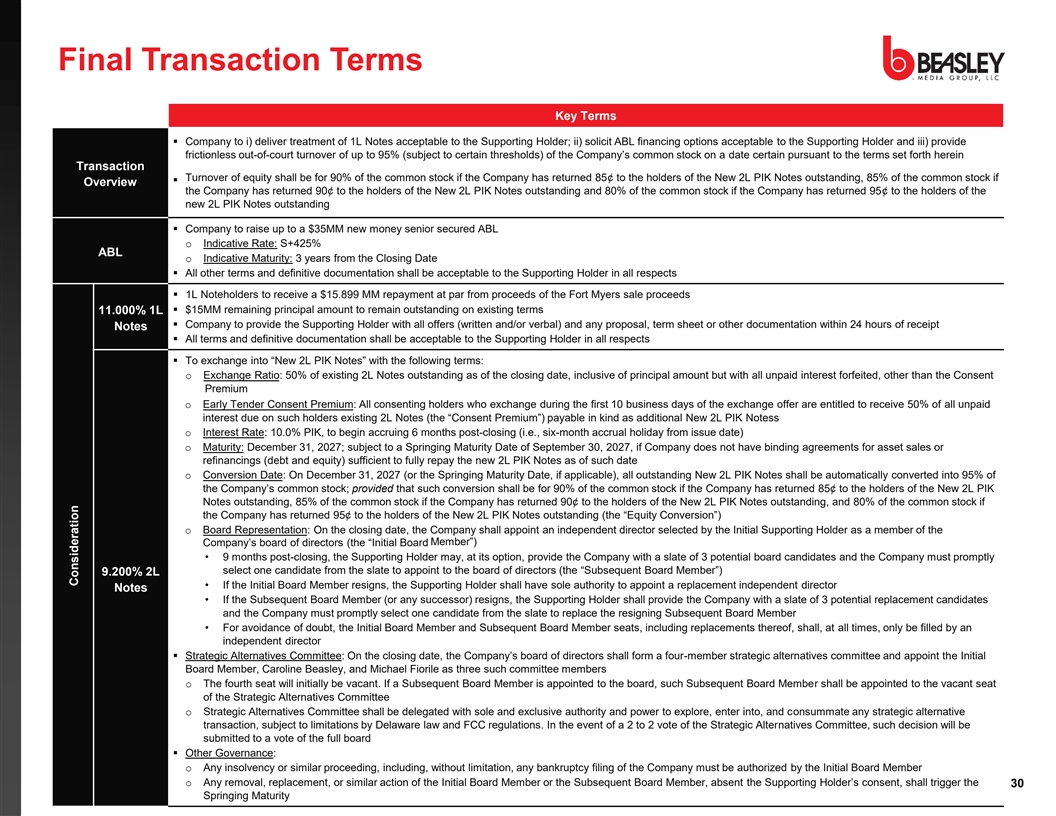

Final Transaction Terms Key Terms ▪ Company to i) deliver treatment of 1L Notes acceptable to the Supporting Holder; ii) solicit ABL financing options acceptable to the Supporting Holder and iii) provide frictionless out-of-court turnover of up to 95% (subject to certain thresholds) of the Company’s common stock on a date certain pursuant to the terms set forth herein Transaction Turnover of equity shall be for 90% of the common stock if the Company has returned 85¢ to the holders of the New 2L PIK Notes outstanding, 85% of the common stock if ▪ Overview the Company has returned 90¢ to the holders of the New 2L PIK Notes outstanding and 80% of the common stock if the Company has returned 95¢ to the holders of the new 2L PIK Notes outstanding ▪ Company to raise up to a $35MM new money senior secured ABL o Indicative Rate: S+425% ABL o Indicative Maturity: 3 years from the Closing Date ▪ All other terms and definitive documentation shall be acceptable to the Supporting Holder in all respects ▪ 1L Noteholders to receive a $15.899 MM repayment at par from proceeds of the Fort Myers sale proceeds ▪ $15MM remaining principal amount to remain outstanding on existing terms 11.000% 1L ▪ Company to provide the Supporting Holder with all offers (written and/or verbal) and any proposal, term sheet or other documentation within 24 hours of receipt Notes ▪ All terms and definitive documentation shall be acceptable to the Supporting Holder in all respects ▪ To exchange into “New 2L PIK Notes” with the following terms: o Exchange Ratio: 50% of existing 2L Notes outstanding as of the closing date, inclusive of principal amount but with all unpaid interest forfeited, other than the Consent Premium o Early Tender Consent Premium: All consenting holders who exchange during the first 10 business days of the exchange offer are entitled to receive 50% of all unpaid interest due on such holders existing 2L Notes (the “Consent Premium”) payable in kind as additional New 2L PIK Notess o Interest Rate: 10.0% PIK, to begin accruing 6 months post-closing (i.e., six-month accrual holiday from issue date) o Maturity: December 31, 2027; subject to a Springing Maturity Date of September 30, 2027, if Company does not have binding agreements for asset sales or refinancings (debt and equity) sufficient to fully repay the new 2L PIK Notes as of such date o Conversion Date: On December 31, 2027 (or the Springing Maturity Date, if applicable), all outstanding New 2L PIK Notes shall be automatically converted into 95% of the Company’s common stock; provided that such conversion shall be for 90% of the common stock if the Company has returned 85¢ to the holders of the New 2L PIK Notes outstanding, 85% of the common stock if the Company has returned 90¢ to the holders of the New 2L PIK Notes outstanding, and 80% of the common stock if the Company has returned 95¢ to the holders of the New 2L PIK Notes outstanding (the “Equity Conversion”) o Board Representation: On the closing date, the Company shall appoint an independent director selected by the Initial Supporting Holder as a member of the Member”) Company’s board of directors (the “Initial Board • 9 months post-closing, the Supporting Holder may, at its option, provide the Company with a slate of 3 potential board candidates and the Company must promptly select one candidate from the slate to appoint to the board of directors (the “Subsequent Board Member”) 9.200% 2L • If the Initial Board Member resigns, the Supporting Holder shall have sole authority to appoint a replacement independent director Notes • If the Subsequent Board Member (or any successor) resigns, the Supporting Holder shall provide the Company with a slate of 3 potential replacement candidates and the Company must promptly select one candidate from the slate to replace the resigning Subsequent Board Member • For avoidance of doubt, the Initial Board Member and Subsequent Board Member seats, including replacements thereof, shall, at all times, only be filled by an independent director ▪ Strategic Alternatives Committee: On the closing date, the Company’s board of directors shall form a four-member strategic alternatives committee and appoint the Initial Board Member, Caroline Beasley, and Michael Fiorile as three such committee members o The fourth seat will initially be vacant. If a Subsequent Board Member is appointed to the board, such Subsequent Board Member shall be appointed to the vacant seat of the Strategic Alternatives Committee o Strategic Alternatives Committee shall be delegated with sole and exclusive authority and power to explore, enter into, and consummate any strategic alternative transaction, subject to limitations by Delaware law and FCC regulations. In the event of a 2 to 2 vote of the Strategic Alternatives Committee, such decision will be submitted to a vote of the full board ▪ Other Governance: o Any insolvency or similar proceeding, including, without limitation, any bankruptcy filing of the Company must be authorized by the Initial Board Member Confidential | o Any removal, replacement, or similar action of the Initial Board Member or the Subsequent Board Member, absent the Supporting Holder’s consent, shall trigger the 30 Springing Maturity Consideration

CONFIDENTIAL Final Transaction Terms (cont’d) Key Terms ▪ Retain existing economic interests of the Company at Close ▪ Upon the occurrence of the Equity Conversion, holders of New 2L PIK Notes shall automatically receive 95% of existing equity interests on a pro rata basis and existing Existing Equity equity holders shall retain 5% of existing equity interests, provided that pro rata equity to New 2L PIK Notes shall be for 90% of the common stock if the Company has returned 85¢ to the holders of the New 2L PIK Notes outstanding, 85% of the common stock if the Company has returned 90¢ to the holders of the New 2L PIK Notes outstanding, and 80% of the common stock if the Company has returned 95¢ to the holders of the New 2L PIK Notes Outstanding ▪ 100%, may be waived in the Supporting Holder’s sole and absolute discretion Min. Participation ▪ Payment of all Supporting Holder advisor fees and expenses ▪ New 2L PIK Notes shall be secured by all of the Company’s assets, including any currently encumbered or unencumbered property, and including all economic interests and value of any of the foregoing, subject to carveouts for the ABL Facility (which, for the avoidance of doubt, shall only be senior on ABL priority collateral (receivables and proceeds thereof) and shall be junior on all non-ABL priority collateral) and any other reasonable exceptions to be agreed in definitive documentation, in each case, acceptable to the Supporting Holder ▪ Negative covenants in New 2L PIK Notes Indenture: No non-ordinary course capacity, subject to reasonable exceptions required for business operations and other exceptions to be agreed in definitive documentation, in each case, acceptable to the Supporting Holder ▪ Liability management protections in New 2L PIK Notes Indenture: Liability management protections acceptable to the Supporting Holder, including, for the avoidance of doubt, an omni-LME blocker ▪ Holders of existing 2L Notes participating in New 2L PIK Notes exchange shall provide exit consents, including amendments, on terms acceptable to the Supporting Conditions / Other Holder, to, among other things, strip collateral and/or covenants in existing 2L Notes Indenture ▪ Company and consenting 2L Noteholders to enter into support agreement with interim operating covenants ▪ Tax structuring and implementation of transaction shall be tax-efficient and mutually acceptable to Company and the Supporting Holder ▪ Satisfaction of diligence acceptable to the Supporting Holder ▪ Gibson Dunn to identify any other conditions precedent that are customary or otherwise requested by the Supporting Holder ▪ 100% of all net proceeds of any and all asset sales after repayment of the 1L Notes and any required repayment of ABL Facility (which shall be solely as to ABL priority collateral), as necessary, shall be used to immediately pay down the New 2L PIK Notes with no reinvestment right; all definitions related to asset sale provisions, including, without limitation, definition of “net proceeds,” shall be acceptable to the Supporting Holder ▪ The 1L Notes and New 2L PIK Notes trustees shall enter into an intercreditor agreement in form and substance acceptable to the Supporting Holder (including, for the avoidance of doubt, among other things, that the New 2L PIK Notes trustee shall control remedies) Confidential | 31