.5

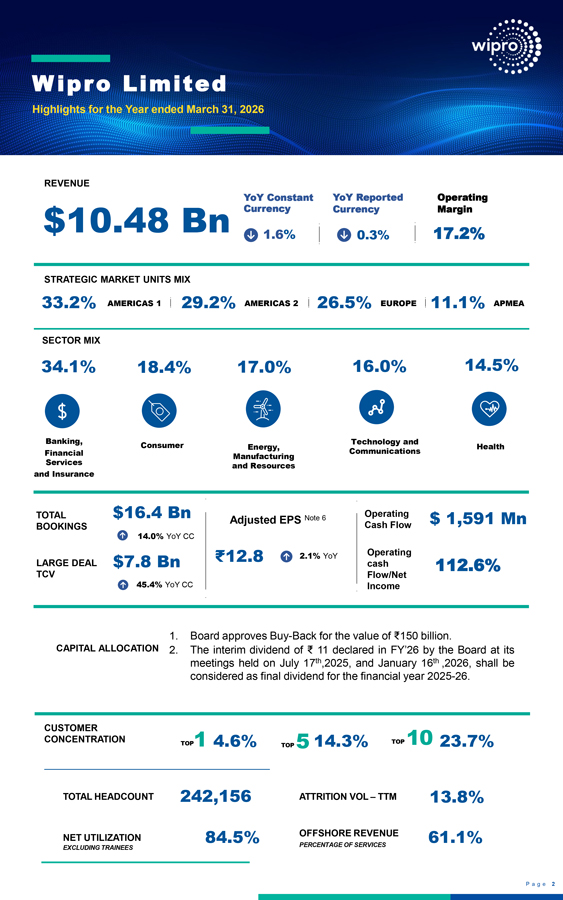

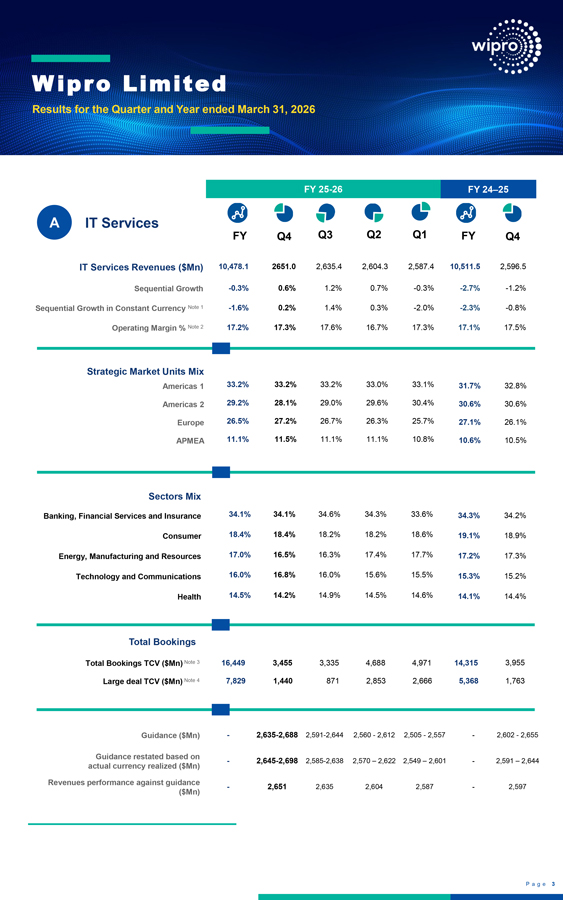

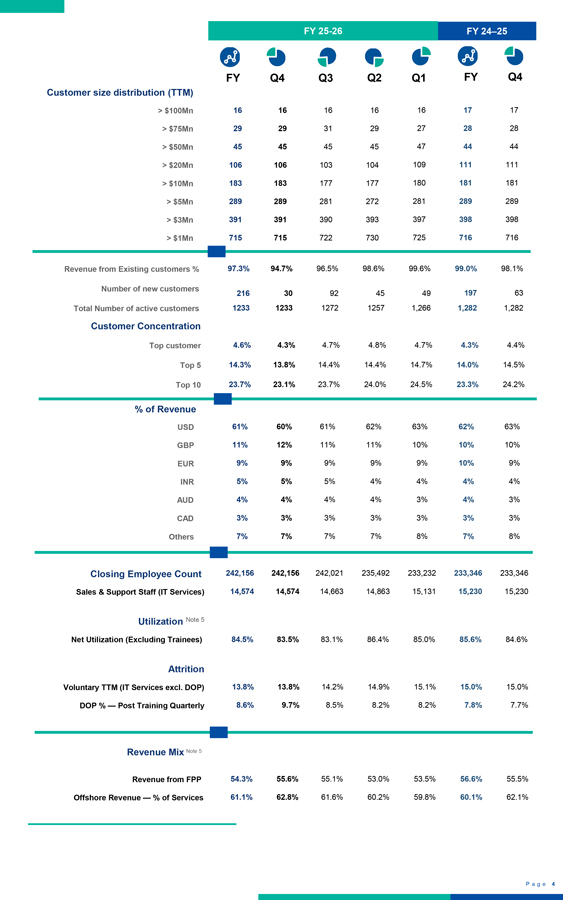

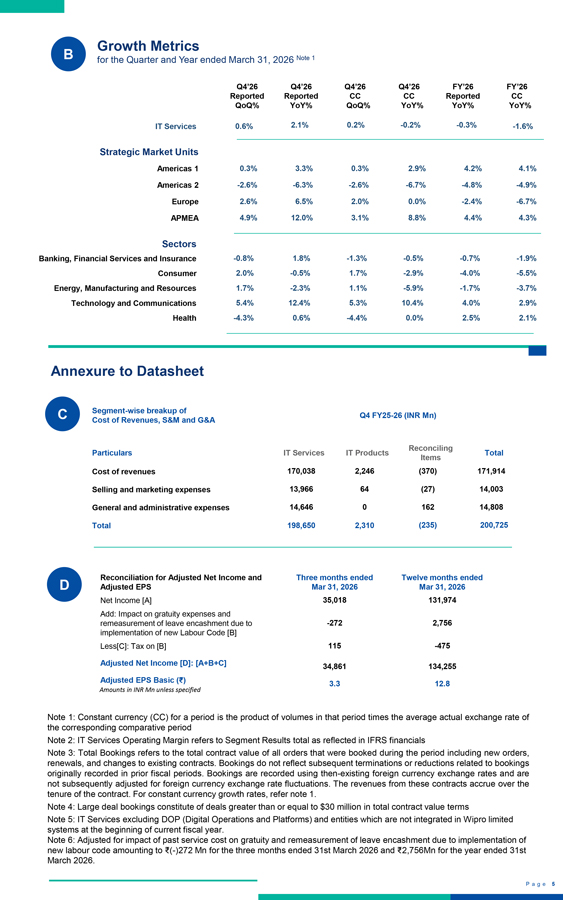

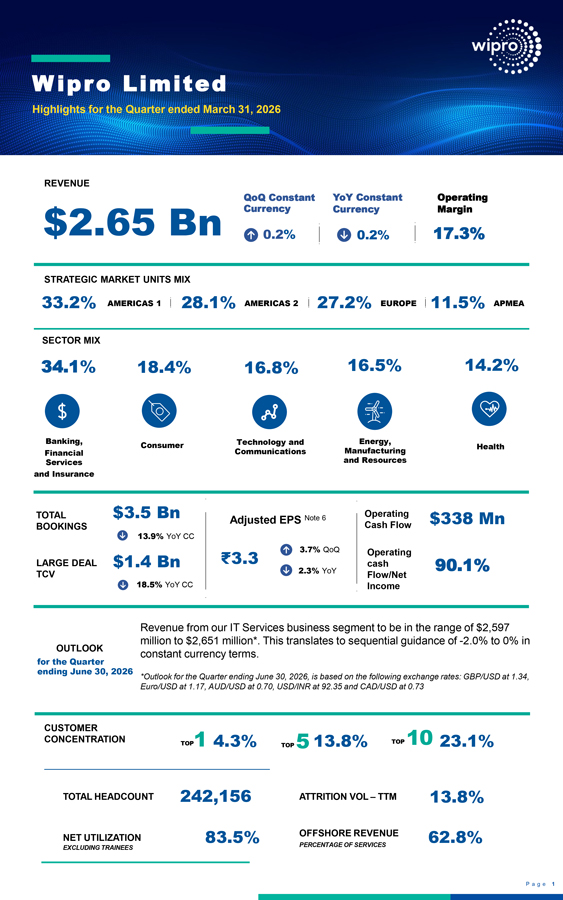

Wipro Limited Highlights for the Quarter ended March 31, 2026 REVENUE QoQ Constant YoY Constant Operating $2.65 Bn Currency Currency Margin 0.2% 0.2% 17.3% STRATEGIC MARKET UNITS MIX 33.2% AMERICAS 1 28.1% AMERICAS 2 27.2% EUROPE 11.5% APMEA SECTOR MIX 34.1% 18.4% 16.8% 16.5% 14.2% Banking, Consumer Technology and Energy, Health Financial Communications Manufacturing Services and Resources and Insurance TOTAL $3.5 Bn Operating Adjusted EPS Note 6 Cash Flow $338 Mn BOOKINGS 13.9% YoY CC ₹ 3.3 3.7% QoQ Operating LARGE DEAL $1.4 Bn cash 90.1% TCV 2.3% YoY Flow/Net 18.5% YoY CC Income Revenue from our IT Services business segment to be in the range of $2,597 million to $2,651 million*. This translates to sequential guidance of -2.0% to 0% in OUTLOOK constant currency terms. for the Quarter ending June 30, 2026 *Outlook for the Quarter ending June 30, 2026, is based on the following exchange rates: GBP/USD at 1.34, Euro/USD at 1.17, AUD/USD at 0.70, USD/INR at 92.35 and CAD/USD at 0.73 CUSTOMER CONCENTRATION TOP1 4.3% 13.8% TOP 10 23.1% TOP 5 TOTAL HEADCOUNT 242,156 ATTRITION VOL – TTM 13.8% OFFSHORE REVENUE NET UTILIZATION 83.5% 62.8% PERCENTAGE OF SERVICES EXCLUDING TRAINEES P a g e 1