|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Investor Company |

|

Investee Company |

|

Location |

|

Main Businesses and Products |

|

Original Investment Amount |

|

|

Balance as of December 31, 2025 |

|

|

Net Income

(Loss) of the

Investee |

|

|

Recognized

Gain (Loss)

(Notes 1

and 2) |

|

|

Note |

| |

December 31,

2025 |

|

|

December 31,

2024 |

|

|

Shares

(Thousands) |

|

|

Percentage of

Ownership (%) |

|

|

Carrying

Value |

|

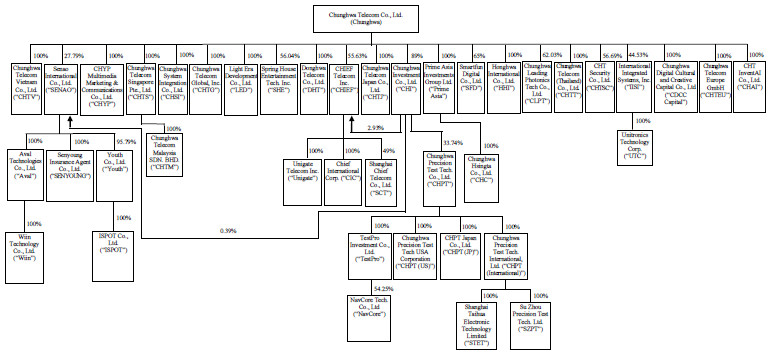

| Chunghwa Telecom Co., Ltd. |

|

Senao International Co., Ltd. |

|

Taiwan |

|

Handset and peripherals retailer; sales of CHT mobile phone plans as an

agent |

|

$ |

1,065,813 |

|

|

$ |

1,065,813 |

|

|

|

71,773 |

|

|

|

28 |

|

|

$ |

1,745,625 |

|

|

$ |

445,292 |

|

|

$ |

117,446 |

|

|

Subsidiary (Notes 3 and 5) |

|

|

Light Era Development Co., Ltd. |

|

Taiwan |

|

Planning and development of real estate and intelligent buildings, and property management |

|

|

3,000,000 |

|

|

|

3,000,000 |

|

|

|

300,000 |

|

|

|

100 |

|

|

|

3,830,021 |

|

|

|

18,892 |

|

|

|

10,771 |

|

|

Subsidiary (Note 5) |

|

|

Donghwa Telecom Co., Ltd. |

|

Hong Kong |

|

International private leased circuit, IP VPN service, and IP transit services |

|

|

691,163 |

|

|

|

691,163 |

|

|

|

178,590 |

|

|

|

100 |

|

|

|

990,245 |

|

|

|

101,622 |

|

|

|

101,622 |

|

|

Subsidiary (Note 5) |

|

|

Chunghwa Telecom Singapore Pte., Ltd. |

|

Singapore |

|

International private leased circuit, IP VPN service, and IP transit services |

|

|

574,112 |

|

|

|

574,112 |

|

|

|

26,383 |

|

|

|

100 |

|

|

|

1,349,725 |

|

|

|

266,078 |

|

|

|

266,082 |

|

|

Subsidiary (Note 5) |

|

|

Chunghwa System Integration Co., Ltd. |

|

Taiwan |

|

Providing system integration services and telecommunications equipment |

|

|

838,506 |

|

|

|

838,506 |

|

|

|

60,000 |

|

|

|

100 |

|

|

|

689,976 |

|

|

|

38,140 |

|

|

|

33,678 |

|

|

Subsidiary (Note 5) |

|

|

CHIEF Telecom Inc. |

|

Taiwan |

|

Network integration, internet data center (“IDC”), communications integration and cloud

application services |

|

|

459,652 |

|

|

|

459,652 |

|

|

|

43,368 |

|

|

|

56 |

|

|

|

2,210,297 |

|

|

|

1,227,441 |

|

|

|

699,241 |

|

|

Subsidiary (Note 5) |

|

|

Chunghwa Investment Co., Ltd. |

|

Taiwan |

|

Investment |

|

|

639,559 |

|

|

|

639,559 |

|

|

|

68,085 |

|

|

|

89 |

|

|

|

3,736,466 |

|

|

|

311,080 |

|

|

|

277,049 |

|

|

Subsidiary (Note 5) |

|

|

Prime Asia Investments Group Ltd. |

|

British Virgin Islands |

|

Investment |

|

|

385,274 |

|

|

|

385,274 |

|

|

|

1 |

|

|

|

100 |

|

|

|

180,965 |

|

|

|

(3,408 |

) |

|

|

(3,408 |

) |

|

Subsidiary (Note 5) |

|

|

Honghwa International Co., Ltd. |

|

Taiwan |

|

Telecommunication engineering, sales agent of mobile phone plan application and other business

services, etc. |

|

|

180,000 |

|

|

|

180,000 |

|

|

|

18,000 |

|

|

|

100 |

|

|

|

725,618 |

|

|

|

365,125 |

|

|

|

362,788 |

|

|

Subsidiary (Notes 3 and 5) |

|

|

CHYP Multimedia Marketing & Communications Co., Ltd. |

|

Taiwan |

|

Digital information supply services and advertisement services |

|

|

150,000 |

|

|

|

150,000 |

|

|

|

15,000 |

|

|

|

100 |

|

|

|

195,379 |

|

|

|

7,096 |

|

|

|

5,315 |

|

|

Subsidiary (Note 5) |

|

|

Chunghwa Telecom Vietnam Co., Ltd. |

|

Vietnam |

|

Intelligent energy saving solutions, international circuit, and information and communication

technology (“ICT”) services |

|

|

148,275 |

|

|

|

148,275 |

|

|

|

— |

|

|

|

100 |

|

|

|

76,025 |

|

|

|

5,113 |

|

|

|

5,113 |

|

|

Subsidiary (Note 5) |

|

|

Chunghwa Telecom Global, Inc. |

|

United States |

|

International private leased circuit, internet services, and transit services |

|

|

70,429 |

|

|

|

70,429 |

|

|

|

6,000 |

|

|

|

100 |

|

|

|

919,632 |

|

|

|

98,703 |

|

|

|

98,703 |

|

|

Subsidiary (Note 5) |

|

|

CHT Security Co., Ltd. |

|

Taiwan |

|

Computing equipment installation, wholesale of computing and business machinery equipment and

software, management consulting services, data processing services, digital information supply services and internet identify services |

|

|

230,580 |

|

|

|

230,580 |

|

|

|

23,058 |

|

|

|

57 |

|

|

|

1,106,750 |

|

|

|

436,927 |

|

|

|

291,121 |

|

|

Subsidiary (Note 5) |

|

|

Chunghwa Telecom (Thailand) Co., Ltd. |

|

Thailand |

|

International private leased circuit, IP VPN service, ICT and cloud VAS services |

|

|

119,624 |

|

|

|

119,624 |

|

|

|

1,300 |

|

|

|

100 |

|

|

|

163,667 |

|

|

|

7,293 |

|

|

|

7,293 |

|

|

Subsidiary (Note 5) |

|

|

Spring House Entertainment Tech. Inc. |

|

Taiwan |

|

Software design services, internet contents production and play, and motion picture production and

distribution |

|

|

62,209 |

|

|

|

62,209 |

|

|

|

8,251 |

|

|

|

56 |

|

|

|

164,226 |

|

|

|

28,577 |

|

|

|

16,015 |

|

|

Subsidiary (Note 5) |

|

|

Chunghwa Leading Photonics Tech Co., Ltd. |

|

Taiwan |

|

Production and sale of electronic components and finished products |

|

|

70,500 |

|

|

|

70,500 |

|

|

|

7,050 |

|

|

|

62 |

|

|

|

218,164 |

|

|

|

68,355 |

|

|

|

47,568 |

|

|

Subsidiary (Note 5) |

|

|

Smartfun Digital Co., Ltd. |

|

Taiwan |

|

Providing diversified family education digital services |

|

|

65,000 |

|

|

|

65,000 |

|

|

|

6,500 |

|

|

|

65 |

|

|

|

86,103 |

|

|

|

21,604 |

|

|

|

13,142 |

|

|

Subsidiary (Note 5) |

|

|

Chunghwa Telecom Japan Co., Ltd. |

|

Japan |

|

International private leased circuit, IP VPN service, and IP transit services |

|

|

17,291 |

|

|

|

17,291 |

|

|

|

1 |

|

|

|

100 |

|

|

|

358,331 |

|

|

|

101,299 |

|

|

|

93,387 |

|

|

Subsidiary (Note 5) |

|

|

International Integrated Systems, Inc. |

|

Taiwan |

|

IT solution provider, IT application consultation, system integration and package solution |

|

|

503,369 |

|

|

|

507,363 |

|

|

|

35,920 |

|

|

|

45 |

|

|

|

764,721 |

|

|

|

152,442 |

|

|

|

69,391 |

|

|

Subsidiary (Note 5) |

|

|

Chunghwa Digital Cultural and Creative Capital Co., Ltd |

|

Taiwan |

|

Investment and management consulting |

|

|

50,000 |

|

|

|

50,000 |

|

|

|

5,000 |

|

|

|

100 |

|

|

|

28,300 |

|

|

|

(10,715 |

) |

|

|

(10,900 |

) |

|

Subsidiary (Note 5) |

|

|

Chunghwa Telecom Europe GmbH |

|

Germany |

|

International private leased circuit, internet services, transit services and ICT services |

|

|

122,675 |

|

|

|

122,675 |

|

|

|

3,500 |

|

|

|

100 |

|

|

|

114,274 |

|

|

|

(11,360 |

) |

|

|

(11,360 |

) |

|

Subsidiary (Note 5) |

|

|

CHT InventAI Co., Ltd. |

|

Taiwan |

|

AI software, system development, application services, and enterprise consulting |

|

|

120,000 |

|

|

|

— |

|

|

|

12,000 |

|

|

|

100 |

|

|

|

119,237 |

|

|

|

(763 |

) |

|

|

(763 |

) |

|

Subsidiary (Note 5) |