Please wait

Management’s Discussion and Analysis

Table of Contents

| | | | | |

| Forward-Looking Statements | |

| Description of the Business | |

| Alberta Electricity Portfolio | |

| Accelerated Clean Electricity Growth Plan | |

| Highlights | |

| Significant and Subsequent Events | |

| Segmented Financial Performance and Operating Results | |

| Fourth Quarter Highlights | |

| Segmented Financial Performance and Operating Results for the Fourth Quarter | |

| Selected Quarterly Information | |

| Financial Position | |

| Financial Capital | |

| Other Consolidated Analysis | |

| Cash Flows | |

| Financial Instruments | |

| Additional IFRS Measures and Non-IFRS Measures | |

| Financial Highlights on a Proportional Basis of TransAlta Renewables | |

| Key Non-IFRS Financial Ratios | |

| 2022 Financial Outlook | |

| Critical Accounting Policies and Estimates | |

| Accounting Changes | |

| Environment, Social and Governance ("ESG") | |

Transforming Our Business Model to Become Carbon Neutral by 2050 | |

| 2022+ Sustainable Targets | |

| Our 2021 Sustainability Performance | |

| Decarbonizing Our Energy Mix | |

| Engaging with Our Stakeholders to Create Positive Relationships | |

| Building a Diverse and Inclusive Workforce | |

Progressive Environmental Stewardship | |

| Reliable, Low-Cost and Sustainable Energy Production | |

Technology Adoption and Innovation Focus | |

| Sustainability Governance | |

| Governance and Risk Management | |

| Disclosure Controls and Procedures | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

This Management’s Discussion and Analysis (“MD&A”) should be read in conjunction with our 2021 audited annual consolidated financial statements (the "consolidated financial statements") and our 2021 annual information form ("AIF"), each for the fiscal year ended Dec. 31, 2021. The consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) for Canadian publicly accountable enterprises as issued by the International Accounting Standards Board (“IASB”) and in effect at Dec. 31, 2021. All dollar amounts in the tables are in millions of Canadian dollars unless otherwise noted and except amounts per share, which are in whole dollars to the nearest two decimals. All other dollar amounts in this MD&A are in Canadian dollars, unless otherwise noted. This MD&A is dated February 23, 2022. Additional information respecting TransAlta Corporation (“TransAlta”, “we”, “our”, “us” or the “Company”), including our AIF, is available on SEDAR at www.sedar.com, on EDGAR at www.sec.gov and on our website at www.transalta.com. Information on or connected to our website is not incorporated by reference herein.

Management’s Discussion and Analysis

Forward-Looking Statements

This MD&A includes "forward-looking information" within the meaning of applicable Canadian securities laws, and "forward-looking statements" within the meaning of applicable US securities laws, including the US Private Securities Litigation Reform Act of 1995 (collectively referred to herein as "forward-looking statements"). All forward-looking statements are based on our beliefs as well as assumptions based on information available at the time the assumption was made, and on management's experience and perception of historical trends, current conditions and expected future developments, as well as other factors deemed appropriate in the circumstances. Forward-looking statements are not facts, but only predictions and generally can be identified by the use of statements that include phrases such as "may," "will," "can," "could," "would," "shall," "believe," "expect," "estimate," "anticipate," "intend," "plan," "forecast," "foresee," "potential," "enable," "continue" or other comparable terminology. These statements are not guarantees of our future performance, events or results and are subject to risks, uncertainties and other important factors that could cause our actual performance, events or results to be materially different from that set out in or implied by the forward-looking statements.

In particular, this MD&A contains forward-looking statements including, but not limited to, statements relating to: our Clean Electricity Growth Plan and ability to achieve the target of 2 gigawatts ("GW") of incremental renewables capacity with an investment of $3 billion by 2025; the Company's future growth pipeline, including the timing of commercial operations and the costs of the advanced and early-stage projects; expansion of the Company's development pipeline to 5 GW; the White Rock East and White Rock West Wind Power Projects ("White Rock Wind Projects"), including the total construction costs, ability to secure tax equity financing, the timing of commercial operation and expected average earnings before interest, taxes, depreciation and amortization ("EBITDA"); the proportion of EBITDA to be generated from renewable sources by the end of 2025; the suspension of the Sundance 5 repowering project; expected average annual EBITDA of the North Carolina Solar (as defined below) portfolio; the incident at the Kent Hills 1 and 2 wind facilities and the extent of any remediation, the timing and cost of such remediation, the ability to secure waivers in respect of the Kent Hills bonds for any potential event of default, and the impact such incident could have on the Company's revenues and contracts; the Northern Goldfields Solar Project, including the total construction capital and expected average annual EBITDA; the Garden Plain wind project, including construction capital and expected average annual EBITDA; expected increases to our cost per tonne of coal at Centralia; the expected impact and quantum of carbon compliance costs; the ability to realize future growth opportunities with BHP (as defined below); regulatory developments and their expected impact on the Company, including the Canadian federal climate plan and the implementation of the major aspects thereof (including increased carbon pricing and increased funding for clean technology); the ability of the Company to realize benefits from Canadian, US and Australian regulatory developments, including receiving funding for clean electricity projects; the potential increase in value of emission reduction credits; the 2022 financial outlook, including adjusted EBITDA, free cash flow ("FCF") and annualized dividend in 2022; increased gross margin contribution from Energy Marketing; hedged production and price for the full year 2022; hedged gas volume and gas price for 2022; sustaining and productivity capital in 2022, including routine capital, planned major maintenance and mine capital; significant planned major outages for 2022 and lost production due to planned major maintenance for 2022; expected power prices in Alberta, Ontario and the Pacific Northwest; the cyclicality of the business, including as it relates to maintenance costs, production and loads; expectations regarding refinancing the debt maturing in 2022; the liquidated damages potentially payable in respect of the Sarnia cogeneration facility outages in the second quarter of 2021; and the Company continuing to maintain a strong financial position and significant liquidity.

Management’s Discussion and Analysis

The forward-looking statements contained in this MD&A are based on many assumptions including, but not limited to, the following: the impacts arising from COVID-19 not becoming significantly more onerous on the Company; no significant changes to applicable laws and regulations beyond those that have already been announced; no significant changes to the fuel and purchased power costs; no material adverse impacts to the long-term investment and credit markets; Alberta spot prices of $80/MWh to $90/MWh in 2022; Mid-Columbia spot prices of US$45/MWh to US$55/MWh in 2022; sustaining capital of $150 million to $170 million; the Company's proportionate ownership of TransAlta Renewables Inc. ("TransAlta Renewables") not changing materially; no decline in the dividends to be received from TransAlta Renewables; and the growth of TransAlta Renewables. Forward-looking statements are subject to a number of significant risks and uncertainties that could cause actual plans, performance, results or outcomes to differ materially from current expectations. Factors that may adversely impact what is expressed or implied by forward-looking statements contained in this MD&A include risks relating to: the impact of COVID-19, including more restrictive directives of government and public health authorities; increased force majeure claims; reduced labour availability and ability to continue to staff our operations and facilities; disruptions to our supply chains, including our ability to secure necessary equipment; our ability to obtain regulatory approvals on the expected timelines or at all in respect of our growth projects; restricted access to capital and increased borrowing costs; changes in short-term and/or long-term electricity supply and demand; fluctuations in market prices, including lower merchant pricing in Alberta, Ontario and Mid-Columbia; reductions in production; increased costs; a higher rate of losses on our accounts receivables due to credit defaults; impairments and/or write-downs of assets; adverse impacts on our information technology systems and our internal control systems, including increased cybersecurity threats; commodity risk management and energy trading risks, including the effectiveness of the Company’s risk management tools associated with hedging and trading procedures to protect against significant losses; changes in demand for electricity and capacity and our ability to contract our generation for prices that will provide expected returns and replace contracts as they expire; changes to the legislative, regulatory and political environments in the jurisdictions in which we operate; environmental requirements and changes in, or liabilities under, these requirements; operational risks involving our facilities, including unplanned outages; disruptions in the transmission and distribution of electricity; the effects of weather, including man-made or natural disasters and other climate-change related risks; unexpected increases in cost structure; reductions to our generating units’ relative efficiency or capacity factors; disruptions in the source of fuels, including natural gas and coal, as well as the extent of water, solar or wind resources required to operate our facilities; general economic risks, including deterioration of equity markets, increasing interest rates or rising inflation; failure to meet financial expectations; general domestic and international economic and political developments, including armed hostilities, the threat of terrorism, including cyberattacks, diplomatic developments or other similar events that could adversely affect our business; equipment failure and our ability to carry out or have completed the repairs in a cost-effective manner or timely manner or at all, including if the remediation at the Kent Hills 1 and 2 wind facilities is more costly or takes longer than expected; industry risk and competition; fluctuations in the value of foreign currencies; structural subordination of securities; counterparty credit risk; changes to our relationship with, or ownership of, TransAlta Renewables; changes in the payment or receipt of future dividends, including from TransAlta Renewables; risks associated with development projects and acquisitions, including capital costs, permitting, labour and engineering risks, and delays in the construction or commissioning of projects; inadequacy or unavailability of insurance coverage; our provision for income taxes; legal, regulatory and contractual disputes and proceedings involving the Company; reliance on key personnel; and labour relations matters. The foregoing risk factors, among others, are described in further detail in the Governance and Risk Management section of this MD&A and the Risk Factors section in our AIF for the year ended Dec. 31, 2021.

Readers are urged to consider these factors carefully in evaluating the forward-looking statements, which reflect the Company's expectations only as of the date hereof, and are cautioned not to place undue reliance on them. The forward-looking statements included in this document are made only as of the date hereof and we do not undertake to publicly update these forward-looking statements to reflect new information, future events or otherwise, except as required by applicable laws. The purpose of the financial outlooks contained herein is to give the reader information about management's current expectations and plans and readers are cautioned that such information may not be appropriate for other purposes. In light of these risks, uncertainties and assumptions, the forward-looking statements might occur to a different extent or at a different time than we have described, or might not occur at all. We cannot assure that projected results or events will be achieved.

Management’s Discussion and Analysis

Description of the Business

Portfolio of Assets

TransAlta is a Canadian corporation and one of Canada's largest publicly traded power generators with over 110 years of operating experience. We own, operate and manage a geographically diversified portfolio of assets utilizing a broad range of fuels that includes water, wind, solar, natural gas and thermal coal.

The following table provides our consolidated ownership of our facilities across the regions in which we operate as at Dec. 31, 2021:

| | | | | | | | | | | | | | | | | | | | | | |

| As at Dec. 31, 2021 | Hydro | Wind and Solar(4) | Gas(4)(5) | Energy Transition(6) | | | Total |

| Alberta | Gross installed capacity (MW)(1) | 834 | | 636 | | 1,960 | | 801 | | | | 4,231 | |

| | | | | | | |

| Number of facilities | 17 | | 13 | | 7 | | 2 | | | | 39 | |

Weighted average contract life(2) | — | | 7 | | 1 | | — | | | | 2 | |

| Canada, Excl. Alberta | Gross installed capacity (MW)(1) | 91 | | 751 | | 645 | | — | | | | 1,487 | |

| | | | | | | |

| Number of facilities | 9 | | 9 | | 3 | | — | | | | 21 | |

Weighted average contract life(3) | 7 | | 10 | | 6 | | — | | | | 8 | |

| US | Gross installed capacity (MW)(1) | — | | 519 | | 29 | | 671 | | | | 1,219 | |

| | | | | | | |

| Number of facilities | — | | 7 | | 1 | | 2 | | | | 10 | |

Weighted average contract life(3) | — | | 12 | | 4 | | 4 | | | | 8 | |

| Australia | Gross installed capacity (MW)(1) | — | | — | | 450 | | — | | | | 450 | |

| | | | | | | |

| Number of facilities | — | | — | | 6 | | — | | | | 6 | |

Weighted average contract life(3) | — | | — | | 17 | | — | | | | 17 | |

| | | | | | | |

| Total | Gross installed capacity (MW)(1) | 925 | | 1,906 | | 3,084 | | 1,472 | | | | 7,387 | |

| | | | | | | |

| Number of facilities | 26 | | 29 | | 17 | | 4 | | | | 76 | |

Weighted average contract life(3) | 1 | | 9 | | 5 | | 2 | | | | 5 | |

(1) Gross installed capacity for consolidated reporting represents 100 per cent output of a facility. Capacity figures for Wind and Solar includes 100 per cent of the Kent Hills wind facilities; Gas includes 100 per cent of the Ottawa and Windsor facilities, 100 per cent of the Poplar Creek facility, 50 per cent of the Sheerness facility and 60 per cent of the Fort Saskatchewan facility.

(2) The weighted average contract life for the assets in Alberta are nil as it is operating primarily on a merchant basis in the Alberta market. Refer to the Alberta Electricity Portfolio section for more information.

(3) For power generated under long-term power purchase agreements ("PPA"), power hedge contracts and short- and long-term industrial contracts, the PPAs have a weighted average remaining contract life (based on gross long-term average gross installed capacity).

(4) The weighted average remaining contract life is related to the contract period for the McBride Lake (38 MW), the Windrise facility (206 MW), Poplar Creek facility (115 MW) and the Fort Saskatchewan facility (71 MW), with remaining wind and gas facilities operated on a merchant basis.in the Alberta market.

(5) Gas segment includes the segments previously known as Australian Gas and North American Gas and the coal generation assets converted to gas from the segment previously known as Alberta Thermal.

(6) Energy Transition segment includes the segment previously known as Centralia and the coal generation assets not converted to gas (including Sundance 4) and mining assets from the segment previously known as Alberta Thermal.

Our Clean Energy Investment Plan, announced in 2019, included converting our existing Alberta coal assets to natural gas and advancing our leadership position in renewable electricity. To date, we have retired 4,064 MW of coal-fired generation capacity since 2018 while converting 1,659 MW to natural gas, significantly reducing our carbon footprint. During 2021, we increased our renewable fleet by 334 MW through acquisitions and construction of renewable wind and solar facilities and on Sept 28, 2021, we announced a Clean Electricity Growth Plan that includes strategic growth targets. Please refer to the Accelerated Clean Electricity Growth Plan section of this MD&A for further information.

Approximately 57 per cent of our gross installed capacity is located in Alberta. Our portfolio of merchant assets in Alberta is a combination of hydro facilities, wind facilities, a battery storage facility and converted natural-gas-fired thermal facilities. This balance of fuel types provides us with portfolio generation diversification. It also provides us with capacity that can be monetized as ancillary services or dispatched into the energy market during times of supply tightness. We also enter into financial contracts to reduce our exposure to variable power prices on our merchant generation. Please refer to the Alberta Electricity Portfolio section of this MD&A for further information.

Management’s Discussion and Analysis

Clean Energy Transition

The Company has completed the conversion to gas at its Alberta facilities that were formerly fuelled by coal; these facilities are now running solely on gas. The Company retired the Highvale coal mine effective Dec. 31, 2021, and is no longer mining coal. Our Centralia coal-fired facility in Washington State is committed to be retired under the TransAlta Energy Transition Bill by 2025. Centralia Unit 1 retired on Dec. 31, 2020, and the remaining unit, Centralia Unit 2, is scheduled to retire on Dec. 31, 2025.

The following table shows the Company's completed conversions to gas:

| | | | | | | | | | | |

| Project | MW | Cumulative Conversion Project Spend(1) | Project Completion Date |

| Keephills Unit 3 | 463 | | $31 | | Q4 2021 |

| Keephills Unit 2 | 395 | | $34 | | Q2 2021 |

| Sundance Unit 6 | 401 | | $39 | | Q1 2021 |

Sheerness Unit 1(2) | 200 | $7 | | Q1 2021 |

Sheerness Unit 2(2) | 200 | $14 | | Q1 2020 |

(1) Conversion project spend only includes costs associated with the conversion to gas-burning technology. Any additional planned major maintenance has been included as part of sustaining capital spend.

(2) These facilities are jointly owned by TransAlta Cogeneration L.P. ("TA Cogen") and Heartland Generation Ltd. This represents the portion of the 400 MW facility consolidated by the Company.

During the 2021 Investor Day, the Company announced its decision to retire Keephills Unit 1 and Sundance Unit 4 effective Dec. 31, 2021, and April 1, 2022, respectively. The retirement decisions were largely driven by TransAlta's assessment of future market conditions, the age and condition of the units and the Company's strategic focus on customer-centred renewable energy solutions. As a result of the decision to retire these units, the Company recorded impairment charges of $94 million and $56 million, respectively, on these units based on the estimated salvage value.

Following an in-depth evaluation and assessment of the Sundance Unit 5 repowering project, the Company suspended the project. The decision was made due to escalating costs, changing supply and demand dynamics and forecasted power prices in the Alberta market, as well as risks associated with carbon pricing and the evolving regulatory environment. With the suspension of the project, the Company will redeploy the capital previously allocated to the Sundance Unit 5 repowering project to renewable growth projects. The Company recorded an impairment charge of $191 million in 2021 in relation to the project. The total remaining estimated recoverable amount and salvage value for the Sundance Unit 5 repowering project was $33 million. Of this amount, $25 million was related to assets held for sale. Included in the impairment charge was $141 million for assets under construction and $50 million for the balance of the plant steam equipment. An additional $20 million was expensed for amounts due under contracts as a result of the suspension of the project.

With the suspension of the Sundance Unit 5, we have also impaired a previously recognized deferred asset, as it is no longer likely that we will incur sufficient capital or operating expenditures to utilize the remaining credit. The Company impaired the remaining balance of the credit of $10 million (US$8 million) in 2021.

The Highvale mine is no longer considered to be providing significant economic benefit to the Alberta Merchant cash-generating unit ("CGU") and it has been removed from the CGU, which resulted in an impairment recognized in 2021 of $195 million. An onerous contract provision of $14 million relating to future Highvale mine royalty payments (2022 and 2023), has also been recognized as an expense in 2021.

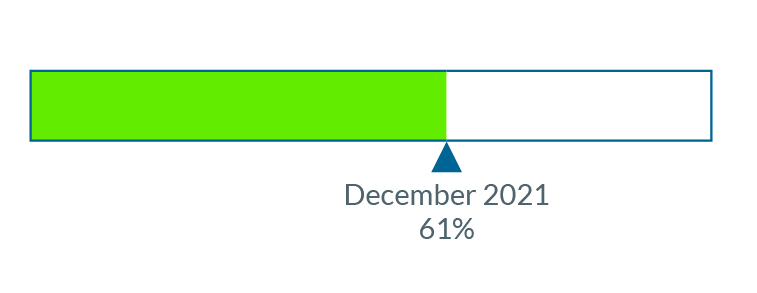

With the successful completion of the Keephills Unit 3 conversion on Dec. 29, 2021, and the planned closure of the Highvale coal mine effective Dec. 31, 2021, TransAlta’s thermal facilities in Alberta have been fully transitioned to 100 per cent natural gas operation. We have reduced our CO2 emissions by 61 per cent from 2015 levels.

Management’s Discussion and Analysis

Reporting Segment Changes

With the completion of the Clean Energy Transition plan and the announcement of our strategic focus on customer-centred renewable generation, the Company has realigned its current operating segments to better reflect its current strategic focus and to align with the Company's Clean Electricity Growth Plan. The segment reporting changes reflect a corresponding change in how the Chief Executive Officer assesses the performance of the Company.

The primary changes are the elimination of the Alberta Thermal and the Centralia segments and the reorganization of the North American Gas and Australia Gas segments into a new "Gas" segment. The Alberta Thermal facilities that have been converted to gas are included in the Gas segment. The remaining assets previously included in Alberta Thermal, including the mining assets and those facilities not converted to gas and the remaining Centralia unit, are included in a new "Energy Transition" segment. No changes have been made to the Hydro, Wind and Solar, Energy Marketing or the Corporate and Other segments. Please refer to the Segmented Financial Performance and Operating Results section of this MD&A for further information.

Performance by Segment with Supplemental Geographical Information

The following table provides the performance of our facilities across the regions we operate in as at Dec. 31, 2021, and Dec. 31, 2020:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

| Year ended Dec. 31, 2021 | | Hydro | Wind and Solar | Gas(1) | Energy Transition(2) | Energy Marketing | Corporate and Other | Total |

| | | | | | | | |

| Alberta | | 308 | | 63 | | 269 | | 59 | | — | | (85) | | 614 | |

| | | | | | | | |

| Canada, excl. Alberta | | 14 | | 120 | | 75 | | — | | 137 | | — | | 346 | |

| | | | | | | | |

| US | | — | | 79 | | 10 | | 74 | | — | | — | | 163 | |

| | | | | | | | |

| Australia | | — | | — | | 140 | | — | | — | | — | | 140 | |

Total adjusted EBITDA(3) | | 322 | | 262 | | 494 | | 133 | | 137 | | (85) | | 1,263 | |

| | | | | | | | |

| Loss before income taxes | | | | | | | | (380) | |

| | | | | | | | |

| Year ended Dec. 31, 2020 | | Hydro | Wind and Solar | Gas(1) | Energy Transition(2) | Energy Marketing | Corporate and Other | Total |

| | | | | | | | |

| Alberta | | 88 | | 18 | | 151 | | 36 | | — | | (81) | | 212 | |

| | | | | | | | |

| Canada, excl. Alberta | | 17 | | 153 | | 88 | | — | | 113 | | — | | 371 | |

| | | | | | | | |

| US | | — | | 77 | | 4 | | 139 | | — | | — | | 220 | |

| | | | | | | | |

| Australia | | — | | — | | 124 | | — | | — | | — | | 124 | |

| | | | | | | | |

Total adjusted EBITDA(3) | | 105 | | 248 | | 367 | | 175 | | 113 | | (81) | | 927 | |

| Loss before income taxes | | | | | | | | (303) | |

(1) Gas segment includes the segments previously known as Australian Gas and North American Gas and the coal generation assets converted to gas from the segment previously known as Alberta Thermal.

(2) Energy Transition segment includes the segment previously known as Centralia and the coal generation assets not converted to gas and mining assets from the segment previously known as Alberta Thermal.

(3) Adjusted EBITDA is not defined and has no standardized meaning under IFRS. Presenting this from period to period provides management and investors with the ability to evaluate earnings trends more readily in comparison with prior periods’ results. Please refer to the Segmented Financial Performance and Operating Results section of this MD&A for further discussion of these items, including, where applicable, reconciliations to measures calculated in accordance with IFRS. See also the Additional IFRS Measures and Non-IFRS Measures section of this MD&A.

Management’s Discussion and Analysis

Alberta Electricity Portfolio

Generating capacity in Alberta is subject to market forces, rather than rate regulation. Power from commercial generation is cleared through a wholesale electricity market. Power is dispatched in accordance with an economic merit order administered by the Alberta Electric System Operator ("AESO"), based upon offers by generators to sell power in the real-time energy-only market. Our merchant Alberta fleet operates under this framework and we internally manage our offers to sell power.

On Dec. 31, 2020, the legislated Alberta Power Purchase Arrangements ("Alberta PPA") for our Alberta hydro assets ("Alberta Hydro Assets"), Sheerness 1 and 2 Units, and the Keephills 1 and 2 Units expired. Effective Jan. 1, 2021, these facilities began operating on a fully merchant basis in the Alberta market and form a core part of our Alberta portfolio optimization activities.

The Alberta Electricity Portfolio generated gross margin of $864 million, an increase of $405 million compared to the same period in 2020. This performance was driven by strengthened power prices in the province, optimization of production during periods of favourable pricing, partially offset by higher natural gas and carbon pricing and higher transmission costs. Optimization of facilities is driven by the diversity in fuel types, which enables portfolio management and allows for maximization of operating margins. A portion of the baseload generation in the portfolio is hedged to provide cash flow certainty. The portfolio consists of hydro, wind, energy storage and natural gas units operating, primarily, on a merchant basis in the Alberta market. Prior to 2022, the Alberta Electricity Portfolio also included coal units, which are now either retired, have been converted to natural gas or will only operate on gas. Sundance Unit 4 will continue to operate within the portfolio, fuelled only by gas, until its retirement date on April 1, 2022.

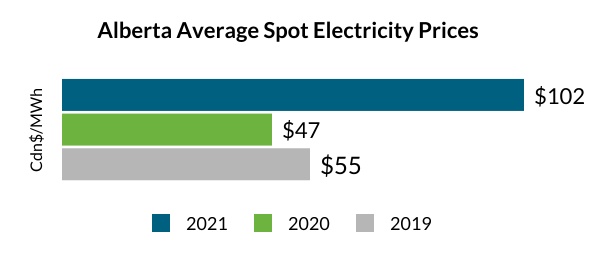

Alberta's annual demand expanded approximately 3.0 per cent from 2020 to 2021 as the economy recovered from the impacts of the COVID-19 pandemic and stronger market conditions for energy commodities supported power demand in the province. The average pool price increased from $47/MWh in 2020 to $102/MWh in 2021. Pool prices were higher in each quarter compared to 2020, generally as a result of competition among generators, higher demand in the province, tighter supply conditions due to higher planned outages, and higher natural gas and carbon prices. In addition, in 2021, Alberta experienced very strong weather-driven demand in February, June, July and December.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 2021 | 2020 | 2019 | |

| Year ended Dec. 31 | Hydro | Wind & Solar | Gas | Energy Transition | Total | Hydro | Wind & Solar | Gas | Energy Transition | Total | Hydro | Wind & Solar | Gas | Energy Transition | Total | |

Total Production (GWh)(1) | 1,586 | | 1,319 | | 7,281 | | 2,591 | | 12,777 | | 1,779 | | 1,320 | | 7,732 | | 2,865 | | 13,696 | | 1,715 | | 1,058 | | 8,691 | | 4,698 | | 16,162 | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| Revenues | 358 | | 97 | | 680 | | 257 | | 1,392 | | 126 | | 57 | | 482 | | 207 | | 872 | | 132 | | 59 | | 519 | | 334 | | 1,044 | | |

| Fuel and purchased power | 13 | | 9 | | 258 | | 92 | | 372 | | 6 | | 15 | | 151 | | 73 | | 245 | | 4 | | 6 | | 151 | | 84 | | 245 | | |

| Carbon compliance | — | | — | | 96 | | 60 | | 156 | | — | | — | | 120 | | 48 | | 168 | | — | | — | | 138 | | 77 | | 215 | | |

| Gross margin | 345 | | 88 | | 326 | | 105 | | 864 | | 120 | | 42 | | 211 | | 86 | | 459 | | 128 | | 53 | | 230 | | 173 | | 584 | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

(1) Units in the Gas and Energy Transition segment in the current and prior years may have operated on coal.

Management’s Discussion and Analysis

The following table provides information for the Company's Alberta Electricity Portfolio:

| | | | | | | | | | | |

| Year ended Dec. 31 | 2021 | 2020 | 2019 |

| Spot power price average per MWh | $102 | | $47 | | $55 | |

| Natural gas price (AECO) per GJ | $3.39 | | $2.11 | | $1.68 | |

| Carbon cost per tonne | $40 | | $30 | | $20 | |

| | | |

Realized power price per MWh(1) | $109 | | $64 | | $65 | |

| Hydro energy realized power price per MWh | $122 | | $51 | | $61 | |

| Hydro ancillary realized price per MWh | $55 | | $23 | | $30 | |

| Wind energy realized power price per MWh | $63 | | $33 | | $38 | |

| Gas and Energy Transition realized power price per MWh | $102 | | $71 | | $64 | |

| | | |

Hedged volume (MW)(2) | 6,992 | | 5,395 | | 5,187 | |

Hedge position (percentage)(3) | 75 | | 100 | | 87 | |

Hedged power price average per MWh(2) | $72 | | $54 | | $55 | |

| | | |

Fuel and purchased power per MWh(4) | $38 | | $23 | | $18 | |

Carbon compliance cost per MWh(4) | $16 | | $16 | | $16 | |

(1) Realized power price for the Alberta Electricity Portfolio is the average price realized as a result of the Company's commercial contracted sales and portfolio optimization activities divided by total GWh produced.

(2) In 2020 and 2019, much of the portfolio in Alberta was still under PPAs and the PPA volumes are not included in the total hedged volumes listed above.

(3) Represents the percentage of production sold forward at the end of the reporting period for the Gas assets only. The hedge program is focused primarily on generation from the merchant Gas and Energy Transition assets.

(4) Fuel and purchased power per MWh and carbon compliance cost per MWh are calculated over production from carbon-emitting generation segments in Gas and Energy Transition.

For the year ended Dec. 31, 2021, the realized power price per MWh of production increased by $45 per MWh, compared with the same period in 2020, primarily due to the optimization of production during periods of favourable pricing. The realized prices include gains and losses from hedging positions that are entered into in order to mitigate the impact of unfavourable market pricing.

For the year ended Dec. 31, 2021, the fuel and purchased power cost per MWh of production increased by $15 per MWh compared to the same period in 2020. Cost per MWh increased due to higher natural gas pricing, higher coal mine depreciation and coal inventory write-downs at the Highvale mine and higher transmission costs.

For the year ended Dec. 31, 2021, carbon compliance costs per MWh of production were consistent with the same period in 2020. Carbon compliance costs have increased in 2021 primarily due to an increase in carbon price from $30 per tonne to $40 per tonne; however, this was substantially offset by changes in fuel ratios as we increased our natural gas combustion compared to coal. The shift in fuel ratio effectively lowered our greenhouse gas ("GHG") compliance costs as natural gas combustion produces fewer GHG emissions than coal combustion.

Management’s Discussion and Analysis

Accelerated Clean Electricity Growth Plan

On Sept. 28, 2021, TransAlta announced its strategic growth targets and Accelerated Clean Electricity Growth Plan. Our goal is to be a leading customer-centred electricity company, committed to a sustainable future, focused on increasing shareholder value by growing our portfolio of high quality generation facilities with stable and predictable cash flows. Our strategy includes meeting our customers' needs for clean, low-cost, reliable electricity and providing operational excellence and continuous improvement in everything we do.

The Company's enhanced focus on renewable generation and storage solutions for customers is driven largely by global decarbonization policies and the increase in demand and growth projections in the renewable sector, namely for companies to achieve their environment, social and governance ("ESG") ambitions. For additional information on regulatory developments, see the ESG section of this MD&A.

We are primarily evaluating greenfield opportunities in Alberta, Western Australia and the US along with acquisitions in markets in which we have existing operations. We maintain highly qualified and experienced development teams to identify and develop these opportunities.

Our Accelerated Clean Electricity Growth Plan has established the following strategic priorities and targets to guide our path from 2021 to 2025. These include:

▪Deliver 2 GW of incremental renewable capacity with a targeted capital investment of $3 billion by the end of 2025. These new assets, once fully operational are targeted to deliver incremental average annual EBITDA1 of $250 million;

▪Accelerate growth into customer-centred renewables and storage through the deployment of our 3 GW development pipeline;

▪Expand the Company's development pipeline to 5 GW by 2025 to enable a two-fold increase in its renewables fleet between 2025 and 2030;

▪Realize targeted diversification and value creation by focusing on expanding our platform in each of our core geographies (Canada, United States and Australia);

▪Lead in ESG policy development to enable the successful evolution of the markets in which we operate and compete; and

▪Define the next generation of power solutions and technologies and potential for parallel investments in new complementary sectors by the end of 2025.

We expect the Company's EBITDA generated from renewable sources, including hydro, wind, and solar technologies, to increase from 35 per cent to 70 per cent by the end of 2025.

The Clean Electricity Growth Plan will largely be funded from current cash balances, cash generated from operations, and asset-level financing.

Growth

In 2021, the Company announced 600 MW of new build projects and asset acquisitions and has 240 MW in advanced-stage development. In addition, the current growth pipeline has a potential capacity ranging from 2,085 MW to 2,685 MW from projects in the early stages of development.

Announced Acquisition

North Carolina Solar

On Nov. 5, 2021, the Company closed the previously announced acquisition of a 122 MW portfolio of operating solar sites located in North Carolina (collectively, “North Carolina Solar”). The North Carolina Solar facility consists of 20 solar photovoltaic sites across North Carolina. The sites were commissioned between November 2019 and May 2021 and are all operational. The facility is secured by long-term PPAs with Duke Energy, which have an average remaining term of 12 years. Under the PPAs, Duke Energy receives the renewable electricity, capacity and environmental attributes from each site. The North Carolina Solar facility is expected to generate an average annual EBITDA1 of approximately US$9 million and average annual cash available for distribution of approximately US$7 million.

1 Average annual EBITDA is not defined and has no standardized meaning under IFRS, and is forward-looking. Please refer to the Additional IFRS Measures and Non-IFRS Measures section of this MD&A for further discussion.

Management’s Discussion and Analysis

Projects under Construction

The following projects have been approved by the Board of Directors ("the Board"), have executed PPAs and are currently under construction. The projects under construction will be financed through existing liquidity in the near term. We will continue to explore project financing or tax equity as a long-term financing solution on an asset-by-asset basis.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | Total project | | Target completion date(1) | | | | | | |

| Project | Type | Region | MW | Estimated

spend | Spent to

date | PPA Term | | Average annual EBITDA(2) | | | Status |

| Projects Under Construction or Approved for Construction |

| Canada | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

Garden Plain(3) | Wind | AB | 130 | $190 | | | — | $200 | $37 | | H2 2022 | 18 | | $14 - $18 | | | •Secured all required permits and approvals •Construction activities commenced in Q4 2021 •On track to be completed on schedule |

| United States | | | | | | | | | | | | | | | |

| White Rock Wind | Wind | OK | 300 | US$460 | | | — | US$470 | US$30 | | H2 2023 | | | US$42 - US$46 | | | •Long-term PPA executed •All major equipment supply and EPC agreements executed •Detailed design and final permitting on track |

| Australia | | | | | | | | | | | | | | | | |

| Northern Goldfields Solar | Hybrid Solar | WA | 48 | AU$69 | | — | AU$73 | AU$15 | | H2 2022 | 16 | | AU$9 - AU$10 | | | •Final Notice to Proceed issued on Sept. 28, 2021 •On track to be completed on schedule |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

(1) H2 is defined as the second half of the year

(2) This item is not defined and has no standardized meaning under IFRS and is forward-looking. Please refer to the Additional IFRS measures and Non-IFRS Measures section of this MD&A for further discussion.

(3) The Garden Plain PPA with Pembina Pipeline Corporation ("Pembina") is for 100 MW of the total 130 MW capacity of the facility.

Advanced-Stage Development

These projects have detailed engineering, advanced position in the interconnection queue and are progressing offtake opportunities. The following table shows the pipeline of future growth projects currently under advanced-stage development:

| | | | | | | | | | | | | | | | | |

| Project | Type | Region | Gross Installed Capacity (MW) | Estimated Spend | Average Annual EBITDA(1) |

| Advanced-Stage Development | | |

| | | | | |

| Horizon Hill | Wind | Oklahoma | 200 | US$290 - US$310 | US$25 - US$35 |

| | | | | |

| Mount Keith 132kV Expansion | Transmission | Western Australia | n/a | AU$50 - AU$53 | AU$6 - AU$7 |

| Mount Keith Capacity Expansion | Gas | Western Australia | 40 | AU$80 - AU$100 | AU$9 - AU$12 |

| | | | | |

(1) This item is not defined and has no standardized meaning under IFRS and is forward-looking. Please refer to the Additional IFRS measures and Non-IFRS Measures section of this MD&A for further discussion.

TRANSALTA CORPORATION M10

Management’s Discussion and Analysis

Early-Stage Development

These projects are in the early stages and may or may not move ahead. Generally, these projects will have:

▪Collected meteorological data;

▪Begun securing land control;

▪Started environmental studies;

▪Confirmed appropriate access to transmission; and

▪Started preliminary permitting and other regulatory approval processes.

The following table shows the pipeline of future growth projects currently under early-stage development:

| | | | | | | | | | | |

| Project | Type | Region | Gross Installed Capacity (MW) |

|

| | | |

| | | |

| | | |

| | | |

| | | |

| Early-Stage Development |

| Canada | | | |

| Riplinger Wind | Wind | Alberta | 300 | |

| Willow Creek 1 | Wind | Alberta | 70 | |

| Willow Creek 2 | Wind | Alberta | 70 | |

| Tempest | Wind | Alberta | 100 | |

| WaterCharger | Battery Storage | Alberta | 180 | |

| | | |

| Sunhills Solar | Solar | Alberta | 85 | |

| Alberta Solar Opportunities | Solar | Alberta | 35 | |

| Canadian Wind Opportunities | Wind | Various | 200 | |

| Brazeau Pumped Hydro | Hydro | Alberta | 300 - 900 |

| | Total | 1,340 - 1,940 |

| US | | | |

| Prairie Violet | Wind | Illinois | 130 | |

| Old Town | Wind | Illinois | 185 | |

| Big Timber | Wind | Pennsylvania | 50 | |

| | | |

| Other US Wind Prospects | Wind | Various | 240 | |

| | | |

| | Total | 605 | |

| Australia | | | |

| Goldfields Expansions | Gas, Solar and Wind | Western Australia | 90 | |

| South Hedland Solar | Solar | Western Australia | 50 | |

| | | |

| | Total | 140 | |

| Canada, US and Australia | | Total | 2,085 - 2,685 |

| | | |

| | | |

| | | |

| | | |

TRANSALTA CORPORATION M11

Management’s Discussion and Analysis

Highlights

Consolidated Financial Highlights | | | | | | | | | | | |

| Year ended Dec. 31 | 2021 | 2020 | 2019 |

| Adjusted availability (%) | 86.6 | | 90.7 | | 90.0 | |

| Production (GWh) | 22,105 | | 24,980 | | 29,071 | |

| Revenues | 2,721 | | 2,101 | | 2,347 | |

Fuel and purchased power(1) | 1,054 | | 805 | | 881 | |

Carbon compliance(1) | 178 | | 163 | | 205 | |

| Operations, maintenance and administration | 511 | | 472 | | 475 | |

Adjusted EBITDA(2,3,7) | 1,263 | | 927 | | 984 | |

| Earnings (loss) before income tax | (380) | | (303) | | 193 | |

| Net earnings (loss) attributable to common shareholders | (576) | | (336) | | 52 | |

| Cash flow from operating activities | 1,001 | | 702 | | 849 | |

Funds from operations(2,3) | 971 | | 685 | | 757 | |

Free cash flow(2,3) | 562 | | 358 | | 435 | |

Net earnings (loss) per share attributable to common shareholders, basic and

diluted | (2.13) | | (1.22) | | 0.18 | |

Dividends declared per common share(4) | 0.19 | | 0.22 | | 0.12 | |

Dividends declared per preferred share(5) | 1.02 | | 1.27 | | 0.78 | |

Funds from operations per share(2,3,8) | 3.58 | | 2.49 | | 2.67 | |

Free cash flow per share(2,3,8) | 2.07 | | 1.30 | | 1.54 | |

| | | |

| As at Dec. 31 | 2021 | 2020 | 2019 |

| Total assets | 9,226 | | 9,747 | | 9,508 | |

Total consolidated net debt(3,6) | 2,636 | | 2,974 | | 3,110 | |

Total long-term liabilities | 4,702 | | 5,376 | | 4,329 | |

| Total liabilities | 6,633 | | 6,311 | | 5,446 | |

(1) Carbon compliance costs have been reclassified from fuel and purchase power costs and disclosed separately. Prior periods have been adjusted for comparative purposes and did not impact previously reported net earnings.

(2) Includes $56 million received on settlement of the dispute with the Balancing Pool in the third quarter of 2019.

(3) These items are not defined and have no standardized meaning under IFRS. Presenting these items from period to period provides management and investors with the ability to evaluate earnings trends more readily in comparison with prior periods’ results. Please refer to the Segmented Financial Performance and Operating Results section of this MD&A for further discussion of these items, including, where applicable, reconciliations to measures calculated in accordance with IFRS. See also the Additional IFRS Measures and Non-IFRS Measures section of this MD&A.

(4) No dividends were declared in the first quarter of 2021 as the quarterly dividend related to the period covering the first quarter of 2021 was declared in December 2020.

(5) Weighted average of the Series A, B, C, E and G preferred share dividends declared. Dividends declared vary year over year due to timing of dividend declarations.

(6) Total consolidated net debt includes long-term debt, including current portion, amounts due under credit facilities, exchangeable securities, US tax equity financing and lease liabilities, net of available cash and cash equivalents, the principal portion of restricted cash on our subsidiary TransAlta OCP LP ("TransAlta OCP") and the fair value of economic hedging instruments on debt. See the table in the Financial Capital section of this MD&A for more details on the composition of total consolidated net debt.

(7) In the fourth quarter of 2021, comparable EBITDA was relabelled as adjusted EBITDA to align with industry standard terminology.

(8) Funds from operations ("FFO") per share and free cash flow per share are calculated using the weighted average number of common shares outstanding during the period. The weighted average number of common shares outstanding at Dec. 31, 2021 was 271 million shares (2020 - 275 million shares and 2019 - 283 million shares). Please refer to the Additional IFRS Measures and Non-IFRS Measures section in this MD&A for the purpose of these non-IFRS ratios.

We have seen exceptional performance from our Alberta Electricity Portfolio, driving overall strong performance for the Company. Both the Hydro and Gas segments had high availability on the merchant assets during periods of peak pricing, which resulted from abnormally warm summer and cold winter weather and periods of province-wide planned thermal outages. The Alberta merchant portfolio was positioned to capture opportunities from these strong spot market conditions through both energy and ancillary service revenues. This was further supplemented by strong performance in our Energy Marketing segment.

Adjusted availability for 2021 was 86.6 per cent compared to 90.7 per cent in 2020. The decrease was primarily due to higher planned and unplanned outages in the Energy Transition segment. The unplanned outages at Centralia Unit 2 and Sundance Unit 4 adversely impacted availability. In addition, adjusted availability was reduced by the planned outages for the Keephills Unit 2 and Keephills Unit 3 boiler conversions. The unplanned outage at the Kent Hills 1 and 2 wind facilities further contributed to reduced adjusted availability.

TRANSALTA CORPORATION M12

Management’s Discussion and Analysis

Production for 2021 was 22,105 gigawatt hours ("GWh") compared to 24,980 GWh in 2020. Overall, the decrease in production was primarily due to the planned retirement of Centralia Unit 1, portfolio optimization activities in Alberta, lower wind resources, the outage at the Kent Hills 1 and 2 wind facilities in the Wind and Solar segment and lower capacity loads in the Gas segment. This was partially offset by higher incremental production at our Ada facility within our Gas segment and higher incremental production from the Skookumchuck wind facility, the Windrise wind facility and the North Carolina Solar facility in the Wind and Solar segment.

Revenues for 2021 increased by $620 million compared to 2020, mainly as a result of capturing higher realized prices within the Alberta market through our optimization and operating activities and the elimination of the net payment obligations under the Alberta Hydro PPA required in the prior period. Revenues also increased due to the strong performance from the Energy Marketing segment, an increase in revenues within the Gas segment from the addition of the Ada facility and an increase within the Wind and Solar segment from the addition of the North Carolina Solar facility and the Windrise wind facility. These increases were partially offset by lower production in the Energy Transition, Hydro, Wind and Solar, and Gas segments.

Fuel and purchased power costs in 2021 increased by $249 million compared to 2020. In our Energy Transition segment, our fuel and purchased power costs increased compared to 2020 due to higher fuel transportation costs and the acquisition of higher-priced power during periods of higher merchant pricing to fulfil our contractual obligations during planned and unplanned outages at the Centralia facility. In addition, the Gas and Energy Transition segments experienced higher natural gas pricing, higher coal mine depreciation and coal inventory write-downs at the Highvale mine, all of which contributed to higher fuel costs.

Carbon compliance costs increased by $15 million compared to 2020, due to an increase in the carbon price per tonne, partially offset by reductions in GHG emissions stemming from changes in the fuel mix ratio as we operated more on natural gas and fired less with coal. Additionally, carbon compliance costs were partially offset by lower production in the Gas and Energy Transition segments. Operating with natural gas reduces carbon compliance costs as we produce fewer GHG emissions than by using coal.

Operations, maintenance and administration ("OM&A") expenses for 2021 increased by $39 million compared to 2020. A write-down of $28 million was recorded on parts and material inventory related to the Highvale mine and coal operations at our natural gas converted facilities. In addition, variability caused by the total return swap resulted in a favourable change of $7 million. During 2021, we received a Canada Emergency Wage Subsidy ("CEWS") of $8 million. Excluding the impact of the total return swap, CEWS funding and inventory write-down, OM&A expenses were higher compared to the same periods in 2020, primarily due to increased staffing costs for growth and strategic initiatives and higher incentive costs. In addition, there were additional costs associated with the legal fees and the settlement of outstanding legal issues. As previously committed, the CEWS funding continues to be used to support incremental employment within the Company.

Adjusted EBITDA increased by $336 million compared to 2020. Adjusted EBITDA increased largely due to higher gross margin, driven by higher realized prices and dispatch optimization in the Alberta market from our merchant facilities residing in the Alberta Electricity Portfolio across the Hydro, Wind and Solar, Gas, and Energy Transition segments. In addition, the Energy Marketing segment also increased adjusted EBITDA due to favourable short-term trading of both physical and financial power and natural gas products across North American markets. This increase was partially offset by the retirement of Centralia Unit 1, unplanned outages at Centralia Unit 2 in the Energy Transition segment and the extended site outage at the Kent Hills 1 and 2 wind facilities. Significant changes in segmented adjusted EBITDA are highlighted in the Segmented Financial Performance and Operating Results section within this MD&A.

Loss before income taxes for 2021 increased by $77 million compared to 2020. Net loss attributable to common shareholders for 2021 was $576 million compared to a loss of $336 million in 2020. The higher loss before income taxes and the higher net loss attributable to common shareholders in 2021 was largely driven by higher asset impairments related to decisions to shut down the Highvale mine, suspend the Sundance 5 repowering project and planned retirements of Sundance Unit 4 and Keephills Unit 1. These higher asset impairments were partially offset by higher adjusted EBITDA largely resulting from the strong performance of the Alberta Electricity Portfolio across all of our fuel segments, higher gains on sale of assets due to the gain on sale of equipment in the Energy Transition segment and the gain from the sale of the Pioneer Pipeline in the Gas segment and lower depreciation. The higher net loss attributable to common shareholders was also impacted by higher income tax expense in 2021 due to higher earnings in the Energy Marketing segment and from the Alberta Electricity Portfolio.

Cash flow from operating activities increased by $299 million compared with 2020, primarily due to higher revenues being realized in Alberta on the merchant assets and changes in non-cash working capital, partially offset by higher fuel and purchased power and OM&A costs as the Company transitioned off coal.

TRANSALTA CORPORATION M13

Management’s Discussion and Analysis

FCF, one of the Company's key financial metrics, totalled $562 million compared to $358 million in 2020. This represents an increase of $204 million, driven primarily by higher adjusted EBITDA, partially offset by an increase in sustaining capital spending related to higher planned maintenance and facility turnarounds, settlement of provisions and higher distributions paid to subsidiaries' non-controlling interests.

Sustaining Capital

We are in a long-cycle, capital-intensive business that requires significant capital expenditures. Our goal is to undertake sustaining capital expenditures that ensures our facilities operate reliably and safely over a long period of time.

| | | | | | | | | | | |

| Year ended Dec. 31 | 2021 | 2020 | 2019 |

| | | |

| | | |

| | | |

| Total sustaining capital expenditures | 199 | | 157 | | 141 | |

| | | |

| | | |

| | | |

| | | |

Total sustaining capital expenditures were $42 million higher compared to 2020, mainly due to higher planned major maintenance turnarounds related to Keephills Unit 2 and 3 and Sheerness Unit 1 and distributed planned maintenance expenditures across the entire hydro and wind fleet, with a focus on planned component replacements in the wind fleet.

Ability to Deliver Financial Results

The metrics we use to track our performance are adjusted EBITDA and FCF. The following table compares target to actual amounts for each of the three past fiscal years:

| | | | | | | | | | | | | | |

| Year ended Dec. 31 | | 2021 | 2020 | 2019 |

Adjusted EBITDA (1) | Target(2) | 1,200-1,300 | 925-1000 | 875-975 |

| Actual | 1,263 | | 927 | | 984 | |

| | | | |

| | | | |

| | | | |

| | | | |

FCF (1) | Target(2) | 500-560 | 325-375 | 350-380 |

| Actual | 562 | | 358 | | 435 | |

| | | |

(1) These items are not defined and have no standardized meaning under IFRS. Please refer to the Additional IFRS Measures and Non-IFRS Measures section of this MD&A for further discussion of these items, including, where applicable, reconciliations to measures calculated in accordance with IFRS.

(2) This represents our revised outlook, as a result of strong performance in the second and third quarters of 2021, the Company revised the following 2021 targets: Adjusted EBITDA from the previously announced target range of $960 million - $1,080 million to the target range of $1,200 million - $1,300 million and FCF target range from $340 million - $440 million to the target range of $500 million - $560 million. In addition, during the fourth quarter of 2019, we revised our FCF target from a range of $270 million to $330 million to a range of $350 million to $380 million.

Significant and Subsequent Events

White Rock Wind Projects and Fully Executed Corporate PPAs

On Dec. 22, 2021, TransAlta executed two long-term PPAs with a new customer with an AA credit rating from S&P Global Ratings for 100 per cent of the generation from its 300 MW White Rock Wind Projects to be located in Caddo County, Oklahoma. The White Rock Wind Projects will consist of a total of 51 Vestas turbines. Construction is expected to begin in late 2022 with a target commercial operation date in the second half of 2023. TransAlta will construct, operate and own the facilities. Total construction capital is estimated at approximately US$460 million to US$470 million and is expected to be financed with a combination of existing liquidity and tax equity financing. Over 90 per cent of the project costs are captured under executed fixed price turbine supply agreements and fixed price engineering, procurement and construction agreements. The project is expected to generate average annual EBITDA2 of approximately US$42 million to US$46 million including production tax credits.

North Carolina Solar Acquisition

On Nov. 5, 2021, the Company closed the acquisition of a 122 MW portfolio of 20 solar photovoltaic sites located in North Carolina. The assets were acquired from a fund managed by Copenhagen Infrastructure Partners for approximately US$99 million (including working capital adjustments) and the assumption of existing tax equity obligations. The acquisition was funded using existing liquidity.

At the closing of the acquisition, TransAlta Renewables acquired a 100 per cent economic interest in North Carolina Solar from a wholly owned subsidiary of TransAlta through a tracking share structure for aggregate consideration of approximately US$102 million.

2 Average annual EBITDA is not defined and has no standardized meaning under IFRS, and is forward-looking. Please refer to the Additional IFRS Measures and Non-IFRS Measures section of this MD&A for further discussion.

TRANSALTA CORPORATION M14

Management’s Discussion and Analysis

The facilities are all operational and were commissioned between November 2019 and May 2021. The facilities are secured by PPAs with Duke Energy, which have an average remaining term of 12 years. Under the PPAs, Duke Energy receives the renewable electricity, capacity and environmental attributes from each facility. North Carolina Solar is expected to generate an average annual EBITDA3 of approximately US$9 million.

Kent Hills Wind Facilities Outage

On Sept. 27, 2021, the Company's subsidiary, Kent Hills Wind LP, experienced a single tower failure at its 167 MW Kent Hills wind facilities in Kent Hills, New Brunswick. The failure involved a collapsed tower located within the Kent Hills 2 site. There were no injuries as a result of the collapse. No one was in the area when the incident occurred and there are no homes in the immediate vicinity. The Company's emergency response team secured the area to ensure safety. The Company recorded an impairment charge of $2 million on the collapsed tower.

The facilities consist of 50 turbines at the Kent Hills 1 and 2 wind facilities and five turbines at Kent Hills 3. Following extensive independent engineering assessments and root cause failure analysis, the Company announced on Jan. 11, 2022, that all 50 turbine foundations at the Kent Hills 1 and 2 wind facilities require a full foundation replacement. The root cause failure analysis indicates that deficiencies in the original design of the foundations had led to subsurface crack propagation within the foundations and that the foundations must be replaced. The Company is in the process of planning the rehabilitation of the wind sites and currently expects the wind facility foundations to be fully replaced by the end of 2023. Based on the recommendations of independent engineers, and in order to maintain the safety of the affected facilities and turbines, the wind turbines will cease to operate until their associated foundations are replaced. The Company has recorded $12 million of accelerated depreciation relating to the 50 foundations that will be replaced.

Foundation replacements will require expenditures of approximately $75 million to $100 million, in aggregate. The remediation plan is expected to begin to be implemented in 2022. The outage is expected to result in foregone revenue of approximately $3.4 million per month on an annualized basis so long as all 50 turbines are offline, based on average historical wind production, with revenue expected to be earned as the wind turbines are returned to service.

TransAlta and New Brunswick Power Corporation continue discussions to enable the safe return to service of the facilities.

The foundation issues at the Kent Hills 1 and 2 wind facilities are unique to the design of those sites and there is no indication of any foundation issue at the Kent Hills 3 facility or any other wind facility in the fleet. The Company is maintaining communication with all key stakeholders and is keeping them fully apprised of the situation. The Company is actively evaluating any options that may be available to recover these costs from third parties and insurance.

As a result of the determination that all 50 foundations require replacement, as well as certain resulting amendments to applicable insurance policies, the Company's operating subsidiary, Kent Hills Wind LP, has provided notice to BNY Trust Company of Canada, as trustee (the “Trustee”), for the approximately $221 million outstanding non-recourse project bonds (the “KH Bonds”) secured by, among other things, the Kent Hills 1, 2 and 3 wind facilities, that events of default may have occurred under the trust indenture governing the terms of the KH Bonds. Upon the occurrence of any event of default, holders of more than 50 per cent of the outstanding principal amount of the KH Bonds have the right to direct the Trustee to declare the principal and interest on the KH Bonds and all other amounts due, together with any make-whole amount as at Dec. 31, 2021 — $39 million, to be immediately due and payable and to direct the Trustee to exercise rights against certain collateral. The Company is in discussions with the Trustee and holders of the KH Bonds to negotiate required waivers and amendments while the Company works to remedy the matters described in the notice. Although the Company expects that it will reach agreement with the Trustee and holders of the KH Bonds with respect to terms of an acceptable waiver and amendment, there can be no assurance that the Company will receive such waivers and amendments. Accordingly, the Company has classified the entire carrying value of the KH Bonds as a current liability as at Dec. 31, 2021.

Investor Day

On Sept. 28, 2021, TransAlta held our 2021 Investor Day and announced our Clean Electricity Growth Plan. The Company has established targets to deliver 2 GW of incremental renewables capacity with a targeted investment of $3 billion by 2025. TransAlta will accelerate its growth with a focus on customer-centred renewables and storage through the execution of its 3 GW development pipeline. Please see the Accelerated Clean Electricity Growth Plan section of this MD&A.

3 Average annual EBITDA is not defined and has no standardized meaning under IFRS, and is forward-looking. Please refer to the Additional IFRS Measures and Non-IFRS Measures section of this MD&A for further discussion.

TRANSALTA CORPORATION M15

Management’s Discussion and Analysis

Retirement of Sundance Unit 4, Keephills Unit 1 and Sundance Unit 5 Coal-Fired Units

The Company announced, during its recent Investor Day, its decision to suspend the Sundance Unit 5 repowering project and retire Keephills Unit 1 on Jan. 1, 2022 and Sundance Unit 4 in 2022.

On July 29, 2021, in accordance with applicable regulatory requirements, the Company gave notice to the AESO of its intention to retire the currently mothballed coal-fired Sundance Unit 5 effective Nov. 1, 2021, and to terminate the associated transmission service agreement. Refer to the Clean Energy Transition section within the Description of the Business section of this MD&A for additional details on these thermal assets.

TransAlta Achieves Full Phase-Out of Coal in Canada

During the year, the Company completed the full conversion of Keephills Unit 2, Keephills Unit 3 and Sundance Unit 6 from thermal coal to natural gas. Keephills Unit 2, Keephills Unit 3 and Sundance Unit 6 will maintain the same generator nameplate capacity of 395 MW, 463 MW and 401 MW, respectively. These conversion to gas projects will reduce our CO2 emissions by more than half and completes our plan to generate 100 per cent clean electricity in Alberta by the end of 2021. As of Dec. 31, 2021, the Company has fully transitioned to natural gas in Canada.

Highvale Mine Impairment

During the third quarter of 2020, the Board approved the accelerated shutdown of the Highvale mine by the end of 2021 and, accordingly, the useful life of the related assets was adjusted to align with the Company's conversion to gas plans. During the third quarter of 2021, with all of TransAlta's remaining coal-fired units having been converted, in the process of being converted to natural gas or being retired, the Highvale mine was no longer considered to be providing significant economic benefit to the Alberta Merchant CGU and was removed from the CGU. This resulted in an impairment being recognized during 2021 of $195 million. Effective Dec. 31, 2021, the mine has entered its reclamation phase.

Announced Common Dividend Increase

On Sept. 28, 2021, the Company announced that the Board approved an 11 per cent increase on its common share dividend and declared a dividend of $0.05 per common share paid on Jan. 1, 2022, to shareholders of record at the close of business on Dec. 1, 2021. The quarterly dividend of $0.05 per common share represents an annualized dividend of $0.20 per common share.

Northern Goldfields Solar Project

On July 29, 2021, TransAlta Renewables announced that Southern Cross Energy ("SCE"), a subsidiary of the Company and an entity in which TransAlta Renewables owns an indirect economic interest, had reached an agreement to provide BHP Billiton Nickel West Pty Ltd. ("BHP") with renewable electricity to its Goldfields-based operations through the construction of the Northern Goldfields Solar Project. The project consists of the 27 MW Mount Keith Solar Farm, 11 MW Leinster Solar Farm, 10 MW/5MWh Leinster Battery Energy Storage System and interconnecting transmission infrastructure, all of which will be integrated into our existing 169 MW Southern Cross Energy North remote network in Western Australia. Construction commenced in the first quarter of 2022 with completion of the projects expected in the second half of 2022. Total construction capital for the project is estimated at approximately AU$69 million to AU$73 million. The project is expected to generate average annual EBITDA4 of approximately AU$9 million to AU$10 million.

On Oct. 22, 2020, SCE replaced and extended its current PPA with BHP. SCE is composed of four generation facilities with a combined capacity of 245 MW in the Goldfields region of Western Australia. The new agreement was effective Dec. 1, 2020, and replaces the previous contract that was scheduled to expire Dec. 31, 2023. The amendment to the PPA extends the term to Dec. 31, 2038, and provides SCE with the exclusive right to supply thermal and electrical energy from the Southern Cross Facilities for BHP's mining operations located in the Goldfields region of Western Australia. The extension will provide SCE a return on new capital investments, which will be required to support BHP's future power requirements and recently announced emission reduction targets. The amendments within the PPA also provide BHP with participation rights in integrating renewable electricity generation, including solar and wind, with energy storage technologies, subject to the satisfaction of certain conditions. In addition to the Northern Goldfields Solar Project, evaluation of further renewable energy supply and carbon emissions reduction initiatives under the extended PPA with BHP are underway, including wind generation and lower emission firming generation to support BHP's future power requirements.

4 Average annual EBITDA is not defined and has no standardized meaning under IFRS, and is forward-looking. Please refer to the Additional IFRS Measures and Non-IFRS Measures section of this MD&A for further discussion.

TRANSALTA CORPORATION M16

Management’s Discussion and Analysis

Sale of the Pioneer Pipeline

On June 30, 2021, the Company closed the sale of the Pioneer Pipeline to ATCO Gas and Pipelines Ltd. ("ATCO") for the aggregate sale price of $255 million. The net cash proceeds to TransAlta from the sale of its 50 per cent interest was approximately $128 million. Pioneer Pipeline has been integrated into the NOVA Gas Transmission Ltd. ("NGTL") and ATCO Alberta natural gas transmission systems to provide reliable natural gas supply to the Company's power generation stations at Sundance and Keephills. As part of the transaction, TransAlta has entered into additional long-term gas transportation agreements with NGTL for new and existing transportation service of 400 TJ per day by the end of 2023.

Sarnia Cogeneration Facility Contract Extension

On May 12, 2021, the Company executed an Amended and Restated Energy Supply Agreement with one of its large industrial customers at the Sarnia cogeneration facility, which provides for the supply of electricity and steam. This agreement will extend the term of the original agreement from Dec. 31, 2022 to Dec. 31, 2032. The agreement provides that if the Company is unable to enter into a new contract with the Ontario Independent Electricity System Operator (“IESO”) or enter into agreements with its other industrial customers at the Sarnia cogeneration facility that extend past Dec. 31, 2025, then the Company has the option to provide notice of termination in 2022 that would terminate the Amended and Restated Energy Supply Agreement four years following such notice. The Company is in active discussions with the three other existing industrial customers regarding extensions to their supply of electricity and steam from the Sarnia cogeneration facility on comparable terms. The current contract with the IESO in respect of the Sarnia cogeneration facility expires on Dec. 31, 2025. On July 19, 2021, the IESO released its Annual Acquisition Report, which included draft details for medium- and long-term procurement mechanisms for capacity for 2026 and beyond for existing and new generation. The medium-term procurement process is scheduled to be run in 2022. The Company plans to bid into the process, seeking to secure a contract extension for the Sarnia cogeneration facility following the end of the current contract.

Garden Plain Wind Project

On May 3, 2021, the Company announced that it entered into a long-term PPA with Pembina pursuant to which Pembina has contracted for the renewable electricity and environmental attributes for 100 MW of the 130 MW Garden Plain project. Under a separate agreement, Pembina has the option to purchase a 37.7 per cent interest in the project (49 per cent of the quantity under the PPA). The option must be exercised no later than 30 days after the commercial operational date. TransAlta would remain the operator of the facility and earn a management fee if Pembina exercises this option. Garden Plain will be located approximately 30 kilometres north of Hanna, Alberta. Construction activities started in the fall of 2021 with completion of the project expected in the second half of 2022. Total construction capital for the project is estimated at approximately $195 million. The project is expected to contribute between $14 million and $18 million of average annual EBITDA5.

TransAlta Renewables is Named on the Best 50 Corporate Citizens List

During the second quarter of 2021, TransAlta Renewables was recognized by Corporate Knights as one of the Best 50 Corporate Citizens for 2021. The Best 50 Corporate Citizens list evaluates and ranks Canadian corporations against a set of 24 key performance indicators covering ESG indicators relative to their industry peers and using publicly available information. The Company is committed to continuous improvement on key ESG issues and to ensuring its economic value creation is balanced with a value proposition for the environment and its communities.

Equity, Diversity and Inclusion Program

On May 3, 2021, TransAlta announced that it received certification from a third party that specializes in measuring and tracking equity, diversity and inclusion ("ED&I") metrics for organizations, due to its continued commitment to and meaningful performance on ED&I in the workplace. The Company developed a five-year ED&I strategy that was approved by the Board in August 2021, and is now executing the first year of that ED&I strategy.

5 Average annual EBITDA is not defined and has no standardized meaning under IFRS, and is forward-looking. Please refer to the Additional IFRS Measures and Non-IFRS Measures section of this MD&A for further discussion.

TRANSALTA CORPORATION M17

Management’s Discussion and Analysis

Sustainability-Linked Loan

In March 2021, TransAlta extended its $1.3 billion syndicated credit facility to June 30, 2025, and converted the facility into a Sustainability-Linked Loan (“SLL”). The facility's financing terms will align the cost of borrowing to TransAlta's GHG emission reductions and gender diversity targets, which are part of the Company's overall ESG strategy. The SLL will have a cumulative pricing adjustment to the borrowing costs on the facilities and a corresponding adjustment to the standby fee (the "Sustainability Adjustment"). Depending on performance against interim targets that have been set for each year of the credit facility term, the Sustainability Adjustment is structured as a two-way mechanism and could move either up, down or remain unchanged for each sustainability performance target based on performance. The SLL further underscores TransAlta's dedication to sustainability, including ED&I and emissions reduction.

Mangrove Claim

On April 23, 2019, the Mangrove Partners Master Fund Ltd. ("Mangrove") commenced an action in the Ontario Superior Court of Justice naming the Company, the members of the Board of the Company on such date, and Brookfield BRP Holdings (Canada) ("Brookfield") as defendants. Mangrove was seeking to set aside the 2019 Brookfield transaction. The parties reached a confidential settlement and the action was discontinued in the Ontario Superior Court of Justice on April 30, 2021.

Fortescue Metals Group Ltd. ("FMG") Dispute at South Hedland Power Station

On May 2, 2021, the Company entered into a conditional settlement with FMG. The settlement was concluded and the actions were formally dismissed in the Supreme Court of Western Australia on Dec. 7, 2021. The settlement amount has been recorded as revenue in the fourth quarter of 2021, while all other balances previously provided for have been reversed. The settlement has resulted in FMG continuing as a customer of the South Hedland facility.

Keephills 1 Superheater Force Majeure

Keephills Unit 1 was taken offline from March 17, 2015, to May 17, 2015, as a result of a large leak in the secondary superheater. TransAlta claimed force majeure under the PPA. ENMAX Energy Corporation ("ENMAX"), the purchaser under the PPA at the time, did not dispute the force majeure but the Balancing Pool attempted to do so, seeking to recover $12 million in capacity payment charges it paid to TransAlta while the unit was offline. The parties reached a confidential settlement on April 21, 2021, and this matter is now resolved.

TransAlta Renewables Acquisitions

The Company completed the sale of its 100 per cent direct interest in the 206 MW Windrise wind project ("Windrise") to TransAlta Renewables on Feb. 26, 2021, for $213 million. The remaining construction costs for Windrise were paid by TransAlta Renewables. On Nov. 10, 2021, Windrise achieved commercial operations. On Dec. 6, 2021, the Company's indirect wholly owned subsidiary, Windrise Wind LP, secured green bond financing by way of private placement for $173 million. The bonds will be amortizing and will bear interest from their date of issue at a rate of 3.41 per cent per annum and mature on Sept. 30, 2041.

On April 1, 2021, the Company completed the sale of its 100 per cent economic interest in the 29 MW Ada cogeneration facility ("Ada") and its 49 per cent economic interest in the 137 MW Skookumchuck wind facility ("Skookumchuck") to TransAlta Renewables for $43 million and $103 million, respectively. Both facilities are fully operational. Pursuant to the transaction, a TransAlta subsidiary owns Ada and Skookumchuck directly and has issued to TransAlta Renewables tracking preferred shares reflecting its economic interest in the facilities. The Ada facility is under a PPA until 2026. The Skookumchuck wind facility is contracted under a PPA until 2040 with an investment grade counterparty.

Normal Course Issuer Bid

On May 25, 2021, the Toronto Stock Exchange ("TSX") accepted the notice filed by the Company to implement a normal course issuer bid ("NCIB") for a portion of our common shares. Pursuant to the NCIB, TransAlta may repurchase up to a maximum of 14,000,000 common shares, representing approximately 7.16 per cent of its public float of common shares as at May 18, 2021. Purchases under the NCIB may be made through open market transactions on the TSX and any alternative Canadian trading platforms on which the common shares are traded, based on the prevailing market price. Any common shares purchased under the NCIB will be cancelled. The period during which TransAlta is authorized to make purchases under the NCIB commenced on May 31, 2021, and ends on May 30, 2022, or such earlier date on which the maximum number of common shares are purchased under the NCIB or the NCIB is terminated at the Company’s election.