Please wait

TRANSALTA CORPORATION

Management’s Discussion and Analysis

This Management’s Discussion and Analysis (MD&A) contains forward-looking statements. These statements are based on certain estimates and assumptions and involve risks and uncertainties. Actual results may differ materially. Refer to the "Forward-Looking Statements" section of this MD&A for additional information.

Table of Contents

This MD&A should be read in conjunction with our 2025 audited annual consolidated financial statements (the consolidated financial statements) and our 2025 Annual Information Form (AIF), each for the fiscal year ended Dec. 31, 2025. In this MD&A, unless the context otherwise requires, “we”, “our”, “us”, the “Company” and “TransAlta” refer to TransAlta Corporation and its subsidiaries. The consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) for Canadian publicly accountable enterprises as issued by the International Accounting Standards Board (IASB) and in effect at Dec. 31, 2025. All tabular amounts in the following discussion are in millions of Canadian dollars unless otherwise noted, except amounts per share, which are in whole dollars to the nearest two decimals. This MD&A is dated Feb. 26, 2026. Additional information respecting TransAlta, including our AIF for the year ended Dec. 31, 2025, is available on SEDAR+ at www.sedarplus.ca, on EDGAR at www.sec.gov and on our website at www.transalta.com. Information on or connected to our website is not incorporated by reference herein.

| | | | | | | | |

| TransAlta Corporation | 2025 Annual Report | M1 |

Forward-Looking Statements

This MD&A includes "forward-looking information" within the meaning of applicable Canadian securities laws and "forward-looking statements" within the meaning of applicable U.S. securities laws, including the Private Securities Litigation Reform Act of 1995 (collectively referred to herein as "forward-looking statements").

Forward-looking statements are not facts, but only predictions and generally can be identified by the use of statements that include phrases such as "may", "will", "can", "could", "would", "shall", "believe", "expect", "estimate", "anticipate", "intend", "plan", "forecast", "foresee", "potential", "enable", "continue" or other comparable terminology.

In particular, this MD&A contains forward-looking statements about the following, among other things:

•The strategic objectives of the Company and that the execution of the Company’s strategy will realize value for shareholders;

•Our capital allocation and financing strategy;

•Our 2026 Outlook;

•Our financial and operational performance, including our hedge position;

•The optimization and diversification of our existing assets;

•The increasingly contracted nature of our fleet;

•Expectations about strategies for growth and expansion;

•Execution of a data centre memorandum of understanding and its framework for phased development of the Keephills site, including the execution of definitive binding agreements with our counterparties for phase 1, the evaluation of opportunities for additional phases of development and the potential for such additional phases of development to aggregate to 1GW of load;

•Expected costs and schedules for planned projects, including the Centralia coal-to-gas conversion project;

•Expected regulatory processes and outcomes, including in respect of the U.S. Department of Energy Order regarding Centralia Unit 2;

•The power generation industry and the supply of, and demand for, electricity;

•Our CEO and CFO succession plans;

•The cyclicality of our business;

•Expected outcomes with respect to legal proceedings;

•The expected impact of future tax and accounting changes; and

•Expected industry, market and economic conditions.

The forward-looking statements contained in this MD&A are based on many assumptions including, but not limited to, the following:

•No significant changes to applicable laws and regulations, including carbon pricing, renewable energy incentives, royalty rates and climate-related regulations;

•No unexpected delays in obtaining required regulatory and other third-party approvals;

•No material adverse impacts to investment and credit markets;

•No significant changes to power price and hedging assumptions;

•No significant changes to gas commodity price assumptions and transport costs;

•No significant changes to interest or foreign exchange rates;

•No significant changes to the demand for, and growth of, electricity generation;

•No significant changes to the integrity and reliability of our facilities;

•No significant changes to the Company's debt and credit ratings;

•No unforeseen changes to economic and market conditions;

•No significant event occurring outside the ordinary course of business;

•No significant changes to the Company's ability to develop, access or implement, on a timely basis and on reasonable terms, the technology necessary to efficiently and effectively operate the Company's assets and achieve expected future results;

•No significant supply chain disruptions or shortages of raw materials or skilled labour;

•No significant changes to the Company's ability to access the capital markets on reasonable terms; and

•No material changes to international trade laws, regulations, agreements, treaties, taxes, tariffs, duties or policies of Canada, the United States or other countries.

These assumptions are based on information currently available to TransAlta, including information obtained from third-party sources. Actual results may differ materially from those predicted by such assumptions.

Factors that may adversely impact what is expressed or implied by forward-looking statements contained in this MD&A include, but are not limited to:

•Fluctuations in power prices;

•Changes in supply and demand for electricity;

•Our ability to contract our electricity generation for prices that will provide expected returns;

•Our ability to replace contracts as they expire;

•Risks associated with development projects and acquisitions;

•Our ability to develop, access or implement, on a timely basis and on reasonable terms, the technology necessary to efficiently and effectively operate our assets and achieve expected future results;

| | | | | | | | |

M2 | TransAlta Corporation | 2025 Annual Report |

•Any difficulty raising needed capital in the future on reasonable terms;

•Long-term commitments on gas transportation capacity that may not be fully utilized over time;

•Changes to legislative, regulatory and political environments, including changes to carbon pricing, renewable energy policies and emissions regulations in Canada, the United States and Australia;

•Environmental requirements and changes in, or liabilities under, these requirements;

•Operational risks involving our facilities, including unplanned outages and equipment failure;

•Disruptions in the transmission and distribution of electricity;

•Grid reliability;

•Reductions in production;

•Impairments and/or writedowns of assets;

•Adverse impacts on our information technology systems and our internal control systems, including increased cybersecurity threats;

•Commodity risk management and energy-trading risks;

•Reduced labour availability, ability to continue to staff our operations and facilities and other labour relations matters;

•Disruptions to our supply chains;

•Weather conditions and their impact on electricity generation and demand;

•Climate change-related risks, including the increased frequency and severity of extreme weather events;

•Reductions to our generating units' relative efficiency or capacity factors;

•General economic risks, including deterioration of equity markets, increasing interest rates, changes to foreign exchange rates or rising inflation;

•General domestic and international economic and political developments, including potential trade tariffs;

•Industry risk and competition, including from emerging technologies affecting the demand, generation, distribution or storage of electricity;

•Counterparty credit risks;

•Inadequacy or unavailability of insurance coverage;

•Increases in the Company's income taxes and any risk of reassessments;

•Legal, regulatory and contractual disputes and proceedings involving the Company;

•Reputational and stakeholder-related risks; and

•Reliance on key personnel.

The foregoing risk factors, among others, are described in further detail in the "Risk Management" section of this MD&A.

Readers are urged to consider these factors carefully when evaluating the forward-looking statements, which reflect the Company's expectations only as of the date of this MD&A and are cautioned not to place undue reliance on them. The forward-looking statements included in this document are made only as of the date of its release and we do not undertake to publicly update these forward-looking statements to reflect new information, future events or otherwise, except as required by applicable laws. The purpose of the financial outlooks contained in this document is to give the reader information about management's current expectations and plans and readers are cautioned that such information may not be appropriate for other purposes. In light of these risks, uncertainties and assumptions, the forward-looking statements might occur to a different extent or at a different time than we have described, or might not occur at all. We cannot assure that projected results or events will be achieved.

| | | | | | | | |

| TransAlta Corporation | 2025 Annual Report | M3 |

Description of the Business

TransAlta Corporation is one of Canada’s largest publicly traded power generators, owning and operating a diverse fleet across Canada, the United States (U.S.) and Western Australia. Our portfolio includes hydro, wind, solar, battery storage and thermal generation, complemented by our asset optimization and energy marketing capabilities. As one of Canada’s largest producers of wind and thermal generation and Alberta’s largest producer of hydroelectric power, TransAlta remains committed to a diverse generation mix. With strong cash flows underpinned by a high-quality portfolio, TransAlta strives to deliver sustainable long-term shareholder value in an evolving energy landscape.

Portfolio of Assets

Our asset portfolio is geographically diversified with operations across our core markets.

Our Hydro, Wind and Solar, Gas and Energy Transition segments are responsible for operating and maintaining our generation facilities. Our Energy Marketing segment is responsible for marketing and scheduling our merchant asset fleet in North America (excluding Alberta) along with the procurement, transport and storage of natural gas, providing knowledge to support our growth team, and

generating a stand-alone gross margin separate from our asset business through a leading North American energy marketing and trading platform.

Our diversified portfolio consists of both high-quality contracted assets and merchant assets. Our contracted assets provide stable long-term cash flow and earnings, balancing our merchant fleet. Our merchant assets include our unique hydro merchant portfolio and our merchant legacy thermal portfolio and wind assets. Our merchant exposure is primarily in Alberta, where 58 per cent of our capacity is located and 77 per cent of our Alberta capacity is available to participate in the merchant market.

In Alberta, the Company manages its merchant exposure by executing hedging strategies that include a significant base of commercial and industrial customers, supplemented with financial hedges. A significant portion of our thermal and hydro generation capacity in Alberta may be hedged to provide greater cash flow certainty while also being available to capture upside through the optimization of our merchant generation portfolio. Refer to the "2026 Outlook" section and the "Optimization of the Alberta Portfolio" section of this MD&A for further details.

| | | | | | | | |

M4 | TransAlta Corporation | 2025 Annual Report |

The following table provides our consolidated ownership by segment of our facilities across the regions in which we operate as at Dec. 31, 2025:

| | | | | | | | | | | | | | | | | | | | | | |

As at Dec. 31, 2025 | Hydro | Wind & Solar | Gas | Energy Transition(2) | | | Total |

| Alberta | Gross installed capacity (MW)(1) | 834 | | 764 | | 3,650 | | — | | | | 5,248 | |

Number of facilities | 17 | | 14 | | 15 | | — | | | | 46 | |

Weighted average contract life (years) | — | | 16 | | 8 | | — | | | | 10 | |

Contracted capacity (MW) | — | | 336 | | 887 | | — | | | | 1,223 | |

Contracted capacity as a % of total capacity (%) | — | | 44 | | 24 | | — | | | | 23 | |

| | | | | | | |

| Canada, excluding Alberta | Gross installed capacity (MW)(1) | 88 | | 751 | | 705 | | — | | | | 1,544 | |

Number of facilities | 7 | | 9 | | 4 | | — | | | | 20 | |

Weighted average contract life (years) | 14 | | 8 | | 6 | | — | | | | 7 | |

Contracted capacity (MW) | 88 | | 751 | | 705 | | — | | | | 1,544 | |

Contracted capacity as a % of total capacity (%) | 100 | 100 | 100 | — | | | | 100 |

| | | | | | | |

| U.S. | Gross installed capacity (MW)(1) | — | | 1,024 | | 29 | | 671 | | | | 1,724 | |

Number of facilities | — | | 10 | | 1 | | 2 | | | | 13 | |

Weighted average contract life (years) | — | | 12 | | — | | — | | | | 9 | |

Contracted capacity (MW) | — | | 1,024 | | 29 | | 301 | | | | 1,354 | |

Contracted capacity as a % of total capacity (%) | — | | 100 | | 100 | | 45 | | | | 79 | |

| | | | | | | |

Western Australia | Gross installed capacity (MW)(1) | — | | 48 | | 450 | | — | | | | 498 | |

Number of facilities | — | | 3 | | 6 | | — | | | | 9 | |

Weighted average contract life (years) | — | | 13 | | 13 | | — | | | | 13 | |

Contracted capacity (MW) | — | | 48 | | 450 | | — | | | | 498 | |

Contracted capacity as a % of total capacity (%) | — | | 100 | | 100 | | — | | | | 100 | |

| Total | Gross installed capacity (MW)(1) | 922 | | 2,587 | | 4,834 | | 671 | | | | 9,014 | |

Number of facilities | 24 | | 36 | | 26 | | 2 | | | | 88 | |

Weighted average contract life (years) | 14 | | 11 | | 8 | | — | | | | 9 | |

Contracted capacity (MW) | 88 | | 2,159 | | 2,071 | | 301 | | | | 4,619 | |

Contracted capacity as a % of total capacity (%)(3) | 10 | | 83 | | 43 | | 45 | | | | 51 | |

| | | | | | | | |

(1)Gross installed capacity for consolidated reporting is based on a proportionate interest held in a facility. Refer to the "Plant Summary" section of the 2025 Annual Report for details.

(2)Includes the Centralia coal facility and the Skookumchuck hydro facility.

(3)Approximately 51 per cent of our total installed capacity is contracted with creditworthy counterparties.

| | | | | | | | |

| TransAlta Corporation | 2025 Annual Report | M5 |

Highlights

The Company demonstrated strong operational performance for the year ended Dec. 31, 2025. Lower power pricing in Alberta, subdued market volatility and lower wind resource impacted the Company's results year-over-year, with Adjusted EBITDA coming in below the lower end of the range of management's expectations. Free cash flow, while lower year-over-year, came in slightly above the midpoint of the Company's 2025

Outlook, primarily due to lower current tax expense and lower distributions paid to non-controlling interests. The Company partially mitigated the impact of lower power pricing in Alberta by settling a higher volume of hedges at prices that were significantly above the spot market and also benefited from the integration of Heartland assets, acquired at the end of 2024.

| | | | | | | | | | | | | | |

| | |

| 3 months ended Dec. 31, | Year ended Dec. 31 |

| (in millions of Canadian dollars except where noted) | 2025 | 2024 | 2025 | 2024 |

Operational information(1) | | | | |

| Availability (%) | 90.1 | | 87.8 | | 92.3 | | 91.2 | |

| Production (GWh) | 6,725 | | 6,199 | | 24,521 | | 22,811 | |

Select financial information(1) | | | | |

| Revenues | 599 | | 678 | | 2,405 | | 2,845 | |

| | | | |

| | | | |

| | | | |

Adjusted EBITDA(2) | 247 | | 282 | | 1,104 | | 1,255 | |

Adjusted Earnings before income taxes(2) | 14 | | 38 | | 181 | | 396 | |

(Loss) earnings before income taxes | (42) | | (51) | | (141) | | 319 | |

Adjusted Net (Loss) Earnings Attributable to Common Shareholders(2) | (19) | | 3 | | 57 | | 236 | |

Net (loss) earnings attributable to common shareholders | (62) | | (65) | | (190) | | 177 | |

Cash flows(1) | | | | |

| Cash flow from operating activities | 231 | | 215 | | 646 | | 796 | |

Funds from operations(2) | 162 | | 135 | | 749 | | 816 | |

Free cash flow(2) | 93 | | 46 | | 514 | | 575 | |

Per share(1) | | | | |

Weighted average number of common shares outstanding | 297 | | 298 | | 297 | | 302 | |

Adjusted Net (Loss) Earnings Attributable to Common Shareholders per share(2)(3) | (0.06) | | 0.01 | | 0.19 | | 0.78 | |

Net (loss) earnings per share attributable to common shareholders, basic and diluted | (0.21) | | (0.22) | | (0.64) | | 0.59 | |

| Dividends declared per common share | 0.13 | | 0.13 | | 0.26 | | 0.24 | |

| Dividends declared per preferred share | 0.68 | | 0.69 | | 1.36 | | 1.36 | |

Cash flow from operating activities per share(4) | 0.78 | | 0.72 | | 2.18 | | 2.64 | |

Funds from operations per share(2)(3) | 0.55 | | 0.45 | | 2.52 | | 2.70 | |

Free cash flow per share(2)(3) | 0.31 | | 0.15 | | 1.73 | | 1.90 | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

(1)On Dec. 4, 2024, the Company completed the acquisition of Heartland Generation, which added 1,747 MW to gross installed capacity, excluding the Poplar Hill and Rainbow Lake facilities (collectively, the Required Divestitures). Refer to the "Significant and Subsequent Events" section of this MD&A. IFRS financial statements include the results attributable to the Required Divestitures up until the date of disposal, in accordance with a consent agreement entered into with the Commissioner of Competition for Canada. Our non-IFRS measures and operational Key Performance Indicators exclude the results of the Required Divestitures.

(2)These are non-IFRS measures and ratios, which are not defined and have no standardized meaning under IFRS and may not be comparable to similar measures presented by other issuers. Refer to the "Segmented Financial Performance and Operating Results" section of this MD&A for further discussion of these items. Also, refer to the "Non-IFRS and Supplementary Financial Measures" section of this MD&A for more information regarding these non-IFRS measures and ratios, including, where applicable, reconciliations to measures calculated in accordance with IFRS.

(3)Adjusted Net (Loss) Earnings Attributable to Common Shareholders per share, funds from operations (FFO) per share and free cash flow (FCF) per share are calculated using the weighted average number of common shares outstanding during the period. Refer to the "Non-IFRS and Supplementary Financial Measures" section of this MD&A for more information regarding these non-IFRS measures and ratios.

(4)Represents a supplementary financial measure and is calculated as cash flow from operating activities for the period divided by the weighted average number of common shares outstanding during the period.

| | | | | | | | |

M6 | TransAlta Corporation | 2025 Annual Report |

| | | | | | | | |

| (in millions of Canadian dollars except where noted) | | |

As at Dec. 31 | 2025 | 2024 |

| Liquidity and capital resources | | |

Available liquidity(1) | 1,500 | | 1,616 | |

Adjusted Net Debt to Adjusted EBITDA (times)(2)(3) | 4.0 | | 3.6 | |

Total Consolidated Net Debt(2)(4) | 3,725 | | 3,798 | |

| Assets and liabilities | | |

| Total assets | 8,661 | | 9,499 | |

Total long-term liabilities(5) | 5,366 | | 5,087 | |

Total liabilities | 7,196 | | 7,656 | |

(1)Available liquidity is a supplementary financial measure and is calculated as the sum of total available capacity under the committed credit and term facilities and cash and cash equivalents less bank overdraft and the amounts drawn under the non-committed demand facilities.

(2)These are non-IFRS measures and ratios, which are not defined and have no standardized meaning under IFRS and may not be comparable to similar measures presented by other issuers. Refer to the "Segmented Financial Performance and Operating Results" section of this MD&A for further discussion of these items. Also, refer to the "Non-IFRS and Supplementary Financial Measures" section of this MD&A for more information regarding these non-IFRS measures and ratios, including, where applicable, reconciliations to measures calculated in accordance with IFRS.

(3)The most directly comparable IFRS ratio to Adjusted Net Debt to Adjusted EBITDA (times) is calculated as credit facilities, long-term debt and lease liabilities of $3,593 million (Dec. 31, 2024 — $3,808 million) divided by loss before income taxes for the last four quarters of $141 million (Dec. 31, 2024 — earnings before income taxes $319 million) and is equal to (25) times (Dec. 31, 2024 — 12 times). Refer to the "Key Non-IFRS Financial Ratios" section of this MD&A for details of the calculation.

(4)The most directly comparable IFRS measure to Total Consolidated Net Debt is total credit facilities, long-term debt and lease liabilities, which is equal to $3,593 million (Dec. 31, 2024 — $3,808 million). Refer to the table in the "Financial Condition" section of this MD&A for more details on the composition of Total Consolidated Net Debt.

(5)Total long-term liabilities are equal to total non-current liabilities in the consolidated statements of financial position under IFRS.

Significant and Subsequent Events

Memorandum of Understanding for Data Centre Development at Keephills Site Signed

On Feb. 26, 2026, the Company entered into a Memorandum of Understanding (MOU) with Canada Pension Plan Investments and Brookfield to advance data centre development in Alberta, for which TransAlta is the exclusive site and power provider. The MOU establishes a framework for phased development at the Company's Keephills site in Parkland County, including an initial long-term power purchase agreement for approximately 230 MW and the evaluation of additional development aggregating up to 1 Gigawatt of load. Development is subject to regulatory approvals and the parties reaching definitive agreements.

Declared Increase in Common Share Dividend

The Company’s Board has approved a $0.02 annualized (eight per cent) increase to the common share dividend and declared a dividend of $0.07 per common share on Feb. 25, 2026 to be payable on July 1, 2026 to shareholders of record at the close of business on June 1, 2026. The quarterly dividend of $0.07 per common share

represents an annualized dividend of $0.28 per common share.

Acquisition of Far North

On Feb. 2, 2026, the Company closed the acquisition of Far North Power Corporation (Far North) for a purchase price of $95 million from an affiliate of Hut 8 Corporation, subject to working capital and other adjustments. The net cash payment for the transaction was funded through a combination of cash on hand and borrowings under TransAlta's credit facilities.

The transaction adds 310 MW of capacity from four natural gas-fired facilities in our core market of Ontario, increasing the Company's total installed capacity in the province to 1,384 MW.

US$400 Million Senior Notes Offering and Early Redemption of the 7.8% Senior Notes

On Dec. 22, 2025, the Company issued US$400 million senior notes with a fixed annual coupon rate of 5.9 per cent, maturing on Feb. 1, 2034. The notes are unsecured and rank equally in right of payment with all existing and future senior indebtedness and senior in right of payment

| | | | | | | | |

| TransAlta Corporation | 2025 Annual Report | M7 |

to all future subordinated indebtedness. The notes were issued at 99.4 per cent of par value, resulting in net proceeds of $541 million (US$393 million), and are callable in three years. Interest payments on the notes are made semi-annually, on Feb. 1 and Aug. 1, with the first payment scheduled for Aug. 1, 2026.

The proceeds from the offering were used to redeem all of the Company's outstanding 7.8 per cent US$400 million senior notes for the total redemption price of $573 million (US$416 million) in advance of the scheduled maturity date of Nov. 15, 2029.

Mothballing of Sheerness Unit 1

On Dec. 18, 2025, the Company provided notice to the Alberta Electric System Operator (AESO) that Sheerness Unit 1 will be mothballed effective April 1, 2026, for a period of up to two years. The Company maintains the flexibility to return the mothballed unit to service when market fundamentals improve or contracting opportunities are secured. The unit will remain available and fully operational through the first quarter of 2026 and Sheerness Unit 2 will remain fully in service.

Centralia Unit 2 Mandated to Remain Available

On Dec. 16, 2025, the Company received an order from the United States Department of Energy (the Order) requiring that our 700 MW Centralia Unit 2 facility remain available if called upon to operate for a period of 90 days, until March 16, 2026. The Company is currently compliant with the Order and continues to work with the state and federal governments in relation thereto.

Centralia Tolling Agreement Signed

On Dec. 9, 2025, the Company announced it had entered into a long-term tolling agreement (Tolling Agreement) with Puget Sound Energy to convert our 700 MW Centralia Unit 2 facility from coal to natural gas. The conversion extends the operating life of facility and will leverage existing turbines, transmission and infrastructure, while also lowering emissions.

The Tolling Agreement provides a fixed-price capacity payment through 2044 for the facility. The coal-to-gas conversion project is expected to require approximately US$600 million in capital and, once in service, will generate contracted cash flow over the life of the Tolling Agreement. The Company expects to declare a final investment decision for the project in early 2027, after receiving required regulatory approvals. Permitting work will continue through 2026, followed by construction in 2027–2028, with converted natural gas-fired operations expected to begin in late 2028.

Chief Executive Officer Succession

On Nov. 6, 2025, the Company announced that John Kousinioris, President and Chief Executive Officer and a Director of TransAlta, plans to retire effective April 30, 2026. Concurrent with this announcement, the Board of Directors appointed Joel Hunter, TransAlta’s Executive Vice President, Finance and Chief Financial Officer, to succeed Mr. Kousinioris as President and Chief Executive Officer and be nominated to join the Board effective April 30, 2026. Mr. Kousinioris has agreed to serve as a strategic advisor to Mr. Hunter and the Board for a period of six months following his retirement. The Company’s Chief Financial Officer successor will be announced in the coming months.

Demand Transmission Service Contract

On Oct. 3, 2025, the Company entered into a 230 MW Demand Transmission Service Contract with the AESO, representing the full allocation awarded to the Company through Phase I of the AESO's Data Centre Large Load Integration Program.

Completion of Required Divestitures

On Aug. 1, 2025, the Company completed the sale of its 100 per cent interest in the 48 MW Poplar Hill facility, followed by the completion of the sale of its 50 per cent interest in the 97 MW Rainbow Lake facility on Oct. 2, 2025. Both divestitures were required by the consent agreement entered into with the federal Competition Bureau as part of its regulatory approval for the Company's acquisition of Heartland Generation. Energy Capital Partners received the proceeds from the sale of both facilities, net of certain adjustments.

Credit Facility Extension

On July 16, 2025, the Company strengthened its liquidity profile by executing agreements with its lending syndicate to extend its committed credit facilities totalling $2.1 billion by one year. The revised agreements reduced the syndicated facility size from $1.95 billion to $1.90 billion, and extended its maturity to June 30, 2029. The bilateral credit facilities of $240 million were extended by one year to June 30, 2027. The amended agreements enhance financial flexibility, which is a strategic priority.

Recontracting of Ontario Wind Facilities

During the second quarter of 2025, the Company successfully recontracted its Melancthon 1, Melancthon 2 and Wolfe Island wind facilities through the Ontario Independent Electricity System Operator Five-Year Medium-Term 2 Energy Contract (MT2e). MT2e will replace current energy contracts for the three wind

| | | | | | | | |

M8 | TransAlta Corporation | 2025 Annual Report |

facilities when they expire, extending the contract dates until April 30, 2031, for Melancthon 1 and April 30, 2034, for Melancthon 2 and Wolfe Island.

Senior Notes Offering

On March 24, 2025, the Company issued $450 million of senior notes with a fixed annual coupon of 5.625 per cent, maturing on March 24, 2032. The notes are unsecured and rank equally in right of payment with all existing and future senior indebtedness and are senior in right of payment to all future subordinated indebtedness. Interest payments on the notes are made semi-annually, on March 24 and Sept. 24, with the first payment made on Sept. 24, 2025.

On March 25, 2025, the Company repaid its $400 million variable rate term loan facility in advance of the scheduled maturity date of Sept. 7, 2025, with the proceeds received from the senior notes offering.

Nova Clean Energy, LLC

During the first quarter of 2025, the Company made a strategic investment in Nova Clean Energy, LLC (Nova), a developer of renewable energy projects. The investment includes a US$75 million term loan and US$100 million revolving facility. As at Dec. 31, 2025, US$106 million was drawn by Nova under the credit facilities. The outstanding principal under the term loan and the revolving facility bear interest at seven per cent per year with interest due quarterly. The terms of the term loan and the revolving

facility are six and five years, respectively, unless accelerated. The term loan is convertible to a minority equity interest at any time, prior to maturity, at the option of the Company and any remaining unused term loan commitments at the time of conversion would be terminated. This investment provides the Company with the exclusive right to purchase Nova's late-stage development projects in the western U.S.

Normal Course Issuer Bid (NCIB)

On May 27, 2025, the Company announced that it had received approval from the Toronto Stock Exchange to repurchase up to a maximum of 14 million common shares during the 12-month period that commenced May 31, 2025 and will terminate on May 30, 2026.

For the year ended Dec. 31, 2025, the Company purchased and cancelled a total of 1,932,800 common shares, at an average price of $12.42 per common share, for a total cost of $24 million, including taxes.

Mothballing of Sundance 6

On April 1, 2025, the Company mothballed the Sundance Unit 6 facility for a period of up to two years depending on market conditions. TransAlta maintains the flexibility to return the mothballed unit to service when market fundamentals improve or opportunities to contract are secured.

Operating and Financial Performance

Operating Performance

The following table provides availability (%) by segment:

| | | | | | | | | | | | | | | |

| 3 months ended Dec. 31, | Year ended Dec. 31 | |

| 2025 | 2024 | 2025 | 2024 | |

| Hydro | 94.4 | | 85.8 | | 92.0 | | 90.7 | | |

| Wind and Solar | 94.6 | | 92.2 | | 94.4 | | 93.4 | | |

| Gas | 85.9 | | 84.1 | | 91.8 | | 92.2 | | |

Energy Transition | 92.5 | | 91.7 | | 88.5 | | 80.0 | | |

| Availability (%) | 90.1 | | 87.8 | | 92.3 | | 91.2 | | |

Availability is an important measure for the Company as it represents the percentage of time a facility is available to produce electricity, and is an indicator of the overall performance of the fleet.

Availability is impacted by planned and unplanned outages, and derates. The Company schedules planned outages to maintain, repair or make improvements to the facilities at times chosen to minimize operational impacts. In high price environments, outage schedules may be adjusted to accelerate the unit's return to service.

| | | | | | | | |

| TransAlta Corporation | 2025 Annual Report | M9 |

Three months ended Dec. 31, 2025

Availability for the three months ended Dec. 31, 2025, was 90.1 per cent compared to 87.8 per cent for the same period in 2024, primarily due to:

•Lower planned maintenance outages in the Hydro, Gas and Energy Transition segments; and

•Lower unplanned maintenance outages in the Wind and Solar segment.

Year ended Dec. 31, 2025

Availability for the year ended Dec. 31, 2025, was 92.3 per cent compared to 91.2 per cent in 2024. Higher availability compared to the prior year was primarily due to:

•Lower planned and unplanned outages at the Centralia facility in the Energy Transition segment;

•The impact from the White Rock and Horizon Hill wind facilities which achieved commercial operation in the first half of 2024 and operated at higher availability in 2025; and

•Lower planned and unplanned maintenance outages in the Hydro segment; partially offset by

•Higher unplanned outages and derates in the Gas segment.

Production and Long-Term Average Generation

The following table provides the production and long-term average generation (LTA generation) on a consolidated basis for each of our segments:

| | | | | | | | | | | | | | | | | | | | | | | |

| 2025 | | 2024 |

3 months ended Dec. 31 | Actual production (GWh) | LTA generation (GWh) | Production as a % of LTA | | Actual production (GWh) | LTA generation (GWh) | Production as a % of LTA |

| Hydro | 336 | | 447 | | 75 | % | | 452 | | 447 | | 101 | % |

Wind and Solar | 2,008 | | 2,175 | | 92 | % | | 1,831 | | 2,175 | | 84 | % |

| | | | | | | |

| | | | | | | |

Gas | 3,499 | | | | | 2,875 | | | |

| Energy Transition | 882 | | | | | 1,041 | | | |

| | | | | | | |

| | | | | | | |

| Total | 6,725 | | | | | 6,199 | | | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| 2025 | 2024 | |

| Year ended Dec. 31 | Actual production (GWh) | LTA generation (GWh) | Production as a % of LTA | Actual production (GWh) | LTA generation (GWh) | Production as a % of LTA | | | | |

| Hydro | 1,914 | | 2,015 | | 95 | % | 1,723 | | 2,015 | | 86 | % | | | | | | |

Wind and Solar(1) | 6,454 | | 7,457 | | 87 | % | 5,949 | | 6,876 | | 87 | % | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

Gas | 13,003 | | | | 12,317 | | | | | | | | | |

| Energy Transition | 3,150 | | | | 2,822 | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Total | 24,521 | | | | 22,811 | | | | | | | | | |

| | | | | | | | | | | | |

(1)LTA generation for Wind and Solar increased as a result of new wind facilities, including the White Rock and the Horizon Hill wind facilities commissioned in the first half of 2024.

In addition to availability, the Company uses LTA generation as another indicator of performance for its renewable facilities, whereby actual production levels are compared against expected long-term average production levels. In the short term, for each of the Hydro and Wind and Solar segments, the conditions will vary from one period to the next. Over longer durations, facilities are expected to produce in-line with their long-term averages, which is broadly considered a reliable indicator of performance.

LTA generation is calculated on an annualized basis from the average annual energy yield predicted from our simulation model based on historical resource data performed over a period of typically greater than 25 years.

The LTA generation for Gas and Energy Transition is not applicable as these facilities are dispatchable and their production largely depends on market conditions and merchant demand.

| | | | | | | | |

M10 | TransAlta Corporation | 2025 Annual Report |

Three months ended Dec. 31, 2025

Total production for the three months ended Dec. 31, 2025, increased by 526 GWh, or eight per cent, compared to the same period in 2024, primarily due to:

•Addition of production from the Heartland gas facilities acquired in December 2024;

•Higher production at the Sarnia gas facility due to higher availability compared to the same period in 2024, when the facility experienced a planned outage during a portion of the quarter; and

•Higher availability and wind resource across Canada and the U.S. partially offset by

•Higher dispatch optimization in Alberta in the Gas segment due to lower market prices;

•Lower production in the Hydro segment due to lower market prices and water conservation; and

•Lower production at Centralia due to lower Mid-Columbia prices.

Year ended Dec. 31, 2025

Total production for 2025 increased by 1,710 GWh, or seven per cent, compared to 2024, primarily due to:

•Addition of production from the Heartland gas facilities acquired in December 2024;

•Production impact from the White Rock and Horizon Hill wind facilities which achieved commercial operation in the first half of 2024;

•Higher production at the Sarnia gas facility due to higher availability compared to 2024, when the facility experienced a planned outage during a portion of the fourth quarter;

•Improved availability at Centralia;

•Higher production in the Hydro segment due to higher water reserves and optimization of water supply; and

•Higher wind resource in Eastern Canada; partially offset by

•Higher dispatch optimization in Alberta in the Gas segment due to lower market prices.

Market Pricing

| | | | | | | | | | | | | | | |

| 3 months ended Dec. 31, | Year ended Dec. 31 | |

| 2025 | 2024 | 2025 | 2024 | |

Alberta spot power price ($/MWh) | 43 | | 52 | | 44 | | 63 | | |

Mid-Columbia spot power price (US$/MWh) | 38 | | 41 | | 42 | | 56 | | |

Ontario spot power price(1) ($/MWh) | 78 | | 34 | | 60 | | 32 | | |

Natural gas price (AECO) per GJ ($) | 2.15 | | 1.42 | | 1.61 | | 1.29 | | |

(1)Ontario spot power prices through to the end of April 2025 were based on the hourly Ontario energy price (HOEP). Starting May 1, 2025 prices are based on the settled day ahead hourly Ontario zonal energy prices.

For the three months and year ended Dec. 31, 2025, spot power prices in Alberta were 17 and 30 per cent lower, respectively, compared to the same periods in 2024, driven by generally milder weather and increased supply from new renewable and gas-fired facilities.

For the three months and year ended Dec. 31, 2025, Mid-Columbia spot power prices in the Pacific Northwest were seven and 25 per cent lower, respectively, compared to the same periods in 2024, due to the impact of milder weather.

Ontario spot power prices were higher on average compared to the three months and year ended Dec. 31, 2024, due to nuclear refurbishments occurring in 2025 and higher natural gas prices.

For the three months and year ended Dec. 31, 2025, AECO natural gas prices were 51 and 25 per cent higher, respectively, compared to the same periods in 2024, mainly due to lower gas production and lower storage levels in Alberta and throughout North America, as well as stronger demand.

| | | | | | | | |

| TransAlta Corporation | 2025 Annual Report | M11 |

Financial Performance Review of Consolidated Information

| | | | | | | | | | | | | | | |

| | | |

| 3 months ended Dec. 31, | Year ended Dec. 31 | |

| 2025 | 2024 | 2025 | 2024 | |

| Revenues | 599 | | 678 | | 2,405 | | 2,845 | | |

| Fuel and purchased power | (258) | | (249) | | (935) | | (939) | | |

Carbon compliance costs | (40) | | (39) | | (50) | | (112) | | |

| Operations, maintenance and administration | (186) | | (234) | | (711) | | (655) | | |

| Depreciation and amortization | (148) | | (143) | | (579) | | (531) | | |

Asset impairment reversals (charges) | 68 | | (20) | | 13 | | (46) | | |

| | | | | |

| | | | | |

Interest expense | (81) | | (92) | | (347) | | (324) | | |

| | | | | |

(Loss) earnings before income taxes | (42) | | (51) | | (141) | | 319 | | |

Income tax recovery (expense) | 2 | | 8 | | (17) | | (80) | | |

Net (loss) earnings attributable to common shareholders | (62) | | (65) | | (190) | | 177 | | |

Net (loss) earnings attributable to non-controlling interests | (4) | | (4) | | (20) | | 10 | | |

Three months ended Dec. 31, 2025

Revenues for the three months ended Dec. 31, 2025 decreased by $79 million, or 12 per cent, compared to the same period in 2024, primarily due to:

•Lower spot power prices in the Alberta market;

•Higher dispatch optimization in the Gas segment driven by lower power prices in Alberta;

•Higher unrealized mark-to-market losses on the long-term wind energy sales related to the Oklahoma facilities in the Wind and Solar segment;

•Lower revenues in the Energy Transition segment due to lower Mid-Columbia prices, reduced production and a lower volume of favourable hedge positions settled;

•Lower realized mark-to-market gains on settled trades in the Gas segment; partially offset by

•The addition of the Heartland facilities in the Gas segment;

•Lower unrealized mark-to-market losses in the Gas segment due to favourable changes in forward prices;

•Higher revenue from the Sarnia gas facility in the current period as the facility experienced a planned outage during a portion of the quarter in 2024;

•Lower unrealized mark-to-market losses in the Energy Marketing segment due to more favourable forward positions across North American power and natural gas markets; and

•Higher revenues in the Wind and Solar segment due to higher wind resource in Alberta and the U.S..

Fuel and purchased power costs for the three months ended Dec. 31, 2025 increased by $9 million, or four per cent, compared to the same period in 2024, primarily due to:

•The full quarter impact from the addition of the Heartland facilities in the fourth quarter of 2024;

•Higher natural gas prices; and

•Higher production at the Sarnia gas facility as the facility experienced a planned outage during a portion of the quarter in 2024; partially offset by

•Lower purchased power costs driven by lower Mid-Columbia prices on repurchases of power and lower production in the Energy Transition segment.

Carbon compliance costs for the three months ended Dec. 31, 2025 were comparable to the same period of 2024 primarily due to:

•The full quarter impact from the addition of the Heartland facilities in the fourth quarter of 2024;

•Higher production at the Sarnia gas facility in the current period as the facility experienced a planned outage during a portion of the quarter in 2024; and

•An increase in the carbon price from $80 to $95 per tonne; partially offset by

•Favourable impact on carbon compliance cost from higher production at lower-carbon-emitting cogeneration facilities.

OM&A expenses for the three months ended Dec. 31, 2025 decreased by $48 million, or 21 per cent, compared to the same period in 2024, primarily due to:

•No penalties recognized in the current period compared to the same period in 2024, when the Company recognized the penalties assessed by the Alberta Market Surveillance Administrator for self-reported contraventions pertaining to Brazeau hydro ancillary services provided during 2021 and 2022;

•Lower acquisition-related transaction and restructuring costs;

| | | | | | | | |

M12 | TransAlta Corporation | 2025 Annual Report |

•Lower spending related to the planning, design and implementation of an upgrade to our Enterprise Resource Planning (ERP) system; and

•Lower incentive costs; partially offset by

•The full quarter impact from the addition of the Heartland facilities in the fourth quarter of 2024 and associated corporate costs.

Depreciation and amortization for the three months ended Dec. 31, 2025 increased by $5 million, or three per cent, compared to the same period in 2024, primarily due to full quarter impact from the addition of Heartland facilities in the fourth quarter of 2024.

Asset impairment reversals for the three months ended Dec. 31, 2025 increased by $88 million, from asset impairment charges for the same period in 2024, primarily due to:

•A change in the decommissioning and restoration provisions driven by the revisions in estimated cash flows, timing of cash flows and discount rates in the Energy Transition segment; and

•Lower impairment charges related to development projects that are no longer proceeding.

Interest expense for the three months ended Dec. 31, 2025 decreased by $11 million, or 12 per cent, compared to 2024, primarily due to:

•Lower interest on exchangeable debentures due to the financing costs amortization completion in 2024; and

•Net gain on early redemption of the US$400 million senior notes; partially offset by

•Higher interest on debt driven by the addition of the Heartland term facility.

Loss before income taxes for the three months ended Dec. 31, 2025 totalling $42 million, decreased by $9 million, or 18 per cent, compared to the same period in 2024, due to:

•The items noted above; partially offset by

•Realized foreign exchange loss on early redemption of the US$400 million senior notes; and

•Lower unrealized foreign exchange gains due to unfavourable changes in foreign exchange rates.

Income tax recovery for the three months ended Dec. 31, 2025 decreased by $6 million, or 75 per cent, compared to the same period in 2024 due to a decrease in loss before income taxes.

Net loss attributable to common shareholders for the three months ended Dec. 31, 2025 increased by $3 million, or 5 per cent, compared to the same period of 2024 due to the above noted items.

Year ended Dec. 31, 2025

Revenues totalled $2,405 million, a decrease of $440 million, or 15 per cent, compared to 2024, primarily due to:

•Lower Alberta and Mid-Columbia power prices;

•Higher dispatch optimization in the Gas segment driven by lower power prices in Alberta;

•Higher unrealized mark-to-market losses in the Wind and Solar, Gas and Energy Transition segments primarily related to unfavourable changes in forward prices; and

•Lower realized mark-to-market gains on settled trades in the Energy Marketing, Gas and Energy Transition segments; partially offset by

•The full year impact from the addition of the Heartland facilities in the fourth quarter of 2024;

•Higher revenues from the Sarnia gas facility in the current period as the facility experienced a planned outage during a portion of the fourth quarter in 2024; and

•The impact from the White Rock and Horizon Hill wind facilities which achieved commercial operation in the first half of 2024.

Fuel and purchased power costs totalled $935 million, which is comparable to 2024, primarily due to:

•Lower purchased power costs driven by higher availability in the Energy Transition segment; partially offset by

•The full year impact from the addition of the Heartland facilities in the fourth quarter of 2024;

•Higher natural gas prices;

•Higher production in the Energy Transition segment due to higher availability; and

•Higher production at the Sarnia gas facility in the fourth quarter of 2025 compared to the same period in 2024, when the facility experienced a planned outage during a portion of the fourth quarter in 2024.

Carbon compliance costs totalled $50 million, a decrease of $62 million, or 55 per cent, compared to 2024, primarily due to:

•Higher utilization of internally generated and externally purchased emission credits in the current period compared to the same period in 2024 to settle a portion of our GHG obligation and a portion of the 2024 GHG obligation assumed with the Heartland acquisition; and

•The favourable impact on carbon compliance costs due to increased production from lower-carbon-emitting cogeneration facilities; partially offset by

•The addition of carbon compliance costs from the Heartland facilities acquired in the fourth quarter of 2024; and

| | | | | | | | |

| TransAlta Corporation | 2025 Annual Report | M13 |

•An increase in the carbon price from $80 per tonne in 2024 to $95 per tonne in 2025.

OM&A expenses totalled $711 million, an increase of $56 million, or nine per cent, compared to 2024, primarily due to:

•The full year impact from the addition of the Heartland facilities in the fourth quarter of 2024 and associated corporate costs;

•Higher spending to support strategic and growth initiatives;

•Higher spending related to the planning, design and implementation of an upgrade to our ERP system; and

•The full year impact from the White Rock and Horizon Hill wind facilities which achieved commercial operation in the first half of 2024; partially offset by

•No penalties recognized in 2025 compared to 2024, when the Company recognized the penalties assessed by the Alberta Market Surveillance Administrator for Brazeau self-reported contraventions pertaining to hydro ancillary services provided during 2021 and 2022; and

•Lower acquisition-related transaction and restructuring costs.

Depreciation and amortization totalled $579 million, an increase of $48 million, or nine per cent, compared to 2024, primarily due to:

•The full year impact from the addition of the Heartland facilities in the fourth quarter of 2024; and

•The full year impact from the White Rock and Horizon Hill wind facilities which achieved commercial operation in the first half of 2024; partially offset by

•Revisions to the useful lives of certain gas facilities in the fourth quarter of 2024.

Asset impairment reversals totalled $13 million, an increase of $59 million compared to asset impairment charges in the same period in 2024, primarily due to:

•A change in decommissioning and restoration provisions driven by the revisions in estimated cash flows, timing of cash flows and discount rates, and higher impairment reversals related to generation equipment in the Energy Transition segment; partially offset by

•An impairment charge on Required Divestiture assets previously classified as Assets Held for Sale; and

•An impairment charge, net of impairment reversals, related to certain Wind and Solar facilities due to changes in expected production volumes and price assumptions.

Interest expense totalled $347 million, an increase of $23 million, or seven per cent, compared to 2024, primarily due to:

•Higher interest on debt driven by the addition of the Heartland term facility;

•No capitalized interest during 2025 due to lower construction activity compared to the same period in 2024; partially offset by

•Lower interest on debt due to the refinancing of senior notes at lower interest rates during 2025;

•Lower interest on exchangeable debentures due to the financing costs amortization completion in 2024; and

•Net gain on early redemption of the US$400 million senior notes.

Loss before income taxes totalled $141 million, an increase of $460 million, or 144 per cent from earnings before income taxes of $319 million for the same period in 2024, primarily due to:

•The items noted above;

•Realized foreign exchange loss on early redemption of the US$400 million senior notes; and

•Higher unrealized foreign exchange losses due to unfavourable changes in foreign currency rates.

Income tax expense totalled $17 million, a decrease of $63 million, or 79 per cent, compared to 2024, due to the increase in loss before income taxes, partially offset by a higher valuation allowance on U.S. operations.

Net loss attributable to non-controlling interests totalled $20 million an increase of $30 million from net earnings of $10 million for the same period in 2024, primarily due to lower net earnings for TA Cogen resulting from lower merchant pricing in the Alberta market.

Refer to the "Segment Financial Performance and Operating Results" section for additional information.

| | | | | | | | |

M14 | TransAlta Corporation | 2025 Annual Report |

Adjusted EBITDA

For the three months ended Dec. 31, 2025, the Company's Adjusted EBITDA was $247 million compared to $282 million for the same period in 2024, a decrease of $35 million, or 12 per cent.

The major factors impacting Adjusted EBITDA for the three months ended Dec. 31, 2025 are summarized in the following table:

| | | | | |

| 3 months ended Dec. 31 |

Adjusted EBITDA(1) for the three months ended Dec. 31, 2024(2) | 282 | |

Hydro: Lower due to lower spot and ancillary services power prices in the Alberta market and lower merchant volumes in Alberta driven by lower market prices and water conservation. | (18) | |

Wind and Solar: Higher due to higher wind resource and availability across Canada and the U.S. and higher environmental and tax attributes revenues driven by an increase in sales of emission credits to third parties. | 7 | |

Gas: Lower primarily due to higher dispatch optimization driven by lower market prices, lower spot power prices in the Alberta market, lower hedge power prices compared to the same period in 2024 and an increase in the carbon price, partially offset by the positive contribution from the addition of the Heartland facilities, higher production at the Sarnia gas facility due to higher availability compared to the same period in 2024, when the facility experienced a planned outage during a portion of the quarter, and favourable hedge positions settled, which generated positive contributions over settled spot prices in Alberta. | (20) | |

Energy Transition: Lower primarily due to lower Mid-Columbia power prices, partially offset by lower purchased power costs due to fewer repurchases to fulfil contractual obligations during outages and favourable hedge positions settled, which generated positive contributions over settled spot prices. | (10) | |

Energy Marketing: Lower primarily due to comparatively subdued market volatility across North American natural gas and power markets and lower realized gains. | (5) | |

Corporate: Higher primarily due to lower incentive costs, partially offset by the addition of corporate costs related to Heartland. | 11 | |

Adjusted EBITDA(1) for the three months ended Dec. 31, 2025 | 247 | |

(1)Adjusted EBITDA is a non-IFRS measure. Refer to the "Non-IFRS and Supplementary Financial Measures" section of this MD&A. The most directly comparable IFRS measure is loss before income taxes of $42 million for the three months ended Dec. 31, 2025 ($51 million for the three months ended Dec. 31, 2024). Refer to the "Reconciliation of Non-IFRS Measures on a Consolidated Basis by Segments" section of this MD&A.

(2)During the first quarter of 2025, our Adjusted EBITDA composition was amended to exclude the impact of realized gain (loss) on closed exchange positions and Australian interest income. The Company has therefore applied this composition to all previously reported periods. Refer to the "Non-IFRS and Supplementary Financial Measures" section of this MD&A for more details.

| | | | | | | | |

| TransAlta Corporation | 2025 Annual Report | M15 |

For the year ended Dec. 31, 2025, the Company's Adjusted EBITDA was $1,104 million compared to $1,255 million in 2024, a decrease of $151 million, or 12 per cent.

The major factors impacting Adjusted EBITDA for the year ended Dec. 31, 2025 are summarized in the following table:

| | | | | |

| Year ended Dec. 31 |

Adjusted EBITDA(1) for the year ended Dec. 31, 2024(2) | 1,255 | |

Hydro: Lower primarily due to lower spot and ancillary services power prices in the Alberta market, partially offset by higher merchant and contract volumes, higher volume of favourable hedge positions settled (which generated positive contributions over settled spot prices in Alberta), higher regulated transmission revenues related to the reimbursement of costs incurred in prior periods and higher environmental and tax attributes revenue due to increased intercompany sales of emission credits to the Gas segment to fulfil our 2024 GHG obligation. | (31) | |

Wind and Solar: Higher primarily due to the positive contribution from the impact of the White Rock and Horizon Hill wind facilities, which achieved commercial operation in the first half of 2024; higher environmental and tax attributes revenue due to increased sales of emission credits to third parties and intercompany sales to the Gas segment; and higher production volumes due to higher availability across the fleet and higher wind resource in Eastern Canada and the U.S.; partially offset by lower Alberta spot power prices, lower wind resource in Alberta and lower liquidated damages recognized at various wind facilities. | 22 | |

Gas: Lower primarily due to higher dispatch optimization driven by lower market prices, lower spot power prices in the Alberta market, lower hedge power prices compared to the same period in 2024, higher natural gas prices and an increase in the carbon price, partially offset by the positive contributions from the addition of the Heartland facilities, favourable hedge positions settled (which generated positive contributions over settled spot prices in Alberta and the reduction of carbon compliance costs driven by using internally generated and externally purchased emission credits to settle a portion of our GHG obligation and a portion of the 2024 GHG obligation assumed in the Heartland acquisition) and an increase of production from lower carbon-emitting cogeneration facilities. | (86) | |

Energy Transition: Higher primarily due to lower purchased power costs driven by higher availability and favourable hedge positions settled, which generated positive contributions over settled spot prices, partially offset by lower revenue due to lower Mid-Columbia prices and higher OM&A related to community fund spending. | 11 | |

Energy Marketing: Lower primarily due to comparatively subdued market volatility across North American natural gas and power markets and lower realized gains in 2025 compared to 2024. | (61) | |

Corporate: Lower primarily due to increased spending to support strategic and growth initiatives and the addition of corporate costs related to Heartland, partially offset by cost saving initiatives. | (6) | |

Adjusted EBITDA(1) for the year ended Dec. 31, 2025 | 1,104 | |

(1)Adjusted EBITDA is a non-IFRS measure. Refer to the "Non-IFRS and Supplementary Financial Measures" section of this MD&A. The most directly comparable IFRS measure is loss before income taxes of $141 million for the year ended Dec. 31, 2025 (earnings before income taxes were $319 million for the year ended Dec. 31, 2024). Refer to "Reconciliation of Non-IFRS Measures on a Consolidated Basis by Segments" section of this MD&A.

(2)During the first quarter of 2025, our Adjusted EBITDA composition was amended to exclude the impact of realized gain (loss) on closed exchange positions and Australian interest income. The Company has therefore applied this composition to all previously reported periods. Refer to the "Non-IFRS and Supplementary Financial Measures" section of this MD&A for more details.

| | | | | | | | |

M16 | TransAlta Corporation | 2025 Annual Report |

Free Cash Flow

For the three months ended Dec. 31, 2025, the Company's free cash flow (FCF) increased by $47 million, or 102 per cent, compared to the same period in 2024.

The major factors impacting FCF for the three months ended Dec. 31, 2025 are summarized in the following table:

| | | | | |

| 3 months ended Dec. 31 |

FCF(1) for the three months ended Dec. 31, 2024. | 46 | |

Lower Adjusted EBITDA(2) due to the items noted above. | (35) | |

| |

Higher current income tax recovery due to the higher loss before income taxes in 2025. | 28 | |

Lower sustaining capital expenditures(3) due to lower major maintenance for our Canadian gas facilities and lower major maintenance at our Hydro facilities in Alberta due to timing of spend. | 22 | |

| |

| |

Higher provisions settled, resulting in lower FCF. | (8) | |

Lower realized foreign exchange losses from operating activities. | 20 | |

Other(4) | 6 | |

Other non-cash items(5) | 14 | |

FCF(1) for the three months ended Dec. 31, 2025 | 93 | |

(1)FCF is a non-IFRS measure, is not defined and has no standardized meaning under IFRS and may not be comparable to similar measures presented by other issuers. Refer to the "Non-IFRS and Supplementary Financial Measures" section of this MD&A for more information regarding this measure. The most directly comparable IFRS measure is cash flow from operating activities, which was $231 million and $215 million for the three months ended Dec. 31, 2025 and 2024, respectively. Refer to the "Cash Flows" section of this MD&A.

(2)During the first quarter of 2025, our Adjusted EBITDA composition was amended to exclude the impact of realized gain (loss) on closed exchange positions and Australian interest income. The Company has therefore applied this composition to all previously reported periods. Refer to the "Non-IFRS and Supplementary Financial Measures" section of this MD&A.

(3)Sustaining capital expenditures is a supplementary financial measure. Refer to "Capital Expenditures" section of this MD&A for more information regarding this measure.

(4)Other consists primarily of lower decommissioning and restoration costs settled, lower Net Interest Expense, and lower dividends paid on preferred shares, partially offset by higher loan advances and higher distributions paid to subsidiaries' non-controlling interests relating to TA Cogen.

(5)Other non-cash items primarily consist of changes in deferred payments, contract assets and liabilities, onerous contracts and long-term incentive accruals.

| | | | | | | | |

| TransAlta Corporation | 2025 Annual Report | M17 |

For the year ended Dec. 31, 2025, the Company's FCF decreased by $61 million, or 11 per cent, compared to 2024, but was within the range of our expected full-year financial guidance.

The major factors impacting FCF for the year ended Dec. 31, 2025 are summarized in the following table:

| | | | | |

| Year ended Dec. 31 |

FCF(1) for the year ended Dec. 31, 2024 | 575 | |

Lower Adjusted EBITDA(2) due to the items noted above. | (151) | |

Lower current income tax expense due to loss before income taxes in 2025 compared to earnings before income taxes in the same period in 2024. | 94 | |

Higher Net Interest Expense(3) due to higher interest on debt primarily driven by the addition of the Heartland term facility and lower capitalized interest resulting from lower construction activity compared to the same period in 2024. | (33) | |

Lower distributions paid to subsidiaries' non-controlling interests relating to lower TA Cogen net earnings resulting from lower merchant pricing in the Alberta market. | 29 |

Higher provisions settled in the current year compared to the prior year, resulting in lower FCF. | (14) | |

Higher sustaining capital expenditures due to higher major maintenance at our Canadian gas facilities due to timing of spend and the addition of maintenance for the gas facilities acquired from Heartland, and higher major maintenance in the Wind and Solar segment, partially offset by no major maintenance occurring in the Energy Transition segment in the current period and lower major maintenance at our Hydro facilities in Alberta due to timing of spend. In addition, the first quarter of 2024 was impacted by the receipt of a lease incentive related to the Company's head office. | (20) | |

Lower realized foreign exchange losses from operating activities. | 27 | |

| |

| |

| |

Other non-cash items(4) | 8 | |

Other(5) | (1) | |

FCF(1) for the year ended Dec. 31, 2025 | 514 | |

(1)FCF is a non-IFRS measure, is not defined and has no standardized meaning under IFRS and may not be comparable to similar measures presented by other issuers. Refer to the "Non-IFRS and Supplementary Financial Measures" section of this MD&A for more information regarding this measure. The most directly comparable IFRS measure is cash flow from operating activities, which was $646 million and $796 million for the years ended Dec. 31, 2025 and 2024, respectively. Refer to the "Cash Flows" section of this MD&A.

(2)During the first quarter of 2025, our Adjusted EBITDA composition was amended to exclude the impact of realized gain (loss) on closed exchange positions and Australian interest income. The Company has therefore applied this composition to all previously reported periods. Refer to the "Non-IFRS and Supplementary Financial Measures" section of this MD&A.

(3)Net Interest Expense is a non-IFRS measure, is not defined and has no standardized meaning under IFRS and may not be comparable to similar measures presented by other issuers. Refer to "Non-IFRS and Supplementary Financial Measures" section of this MD&A for more information regarding this measure. The most directly comparable IFRS measure is interest expense of $347 million for the year ended Dec. 31, 2025 (Dec. 31, 2024 — $324 million).

(4)Other non-cash items primarily consist of changes in deferred payments, contract assets and liabilities, onerous contracts and long-term incentive accruals.

(5)Other primarily consists of lower decommissioning and restoration costs settled and lower principal payments on lease liabilities, partially offset by higher loan advances.

| | | | | | | | |

M18 | TransAlta Corporation | 2025 Annual Report |

2026 Outlook

For 2026, the Company expects Adjusted EBITDA to be in the range of $950 million to $1,050 million and FCF to be in the range of $350 million to $450 million, based on the following expectations:

•Lower contribution from the Energy Transition segment due to the Centralia facility ceasing dispatchable coal-fired generation at the end of 2025;

•Lower contribution from the Alberta merchant gas portfolio as a result of lower average hedge prices and higher fuel costs, partially offset by lower carbon compliance costs due to a higher utilization of internally generated low-cost environmental credits;

•Lower contributions from Sarnia, reflecting a step down in contracted pricing and the expiry of the contract and decommissioning of the Ada Cogeneration facility;

•Higher contributions within the Hydro, Gas and Wind and Solar segments due to the expected realization of carbon credits against in-year, in addition to 2025, carbon compliance costs in Alberta;

•Higher contributions from the Gas segment due to the acquisition of the Far North Ontario gas facilities;

•Higher contributions from the Wind and Solar segment as a result of higher expected production;

•Higher income tax expense; and

•Lower Net Interest Expense as a result of lower interest rates on refinanced debt and lower interest on non-recourse debt as a result of amortizing repayments.

The following table outlines our expectations on key financial targets and related assumptions for 2026 and should be read in conjunction with the narrative discussion that follows and the "Risk Management" section of this MD&A:

| | | | | | | | | | | | |

| Measure | 2026 Target(2) | 2025 Target | | 2025 Actual(3) |

Adjusted EBITDA(1) | $950 million to $1,050 million | $1,150 million to $1,250 million | | $1,104 million |

FCF(1) | $350 million to $450 million | $450 million to $550 million | | $514 million |

FCF per share(1) | $1.18 to $1.51 | $1.51 to $1.85 | | $1.73 |

Dividend per share | $0.28 annualized | $0.26 annualized | | $0.26 annualized |

(1)These are non-IFRS measures, which are not defined and have no standardized meaning under IFRS and may not be comparable to similar measures presented by other issuers. Refer to the "Reconciliation of Non-IFRS Measures" section of this MD&A for further discussion of these items, including, where applicable, reconciliations to measures calculated in accordance with IFRS. See also the "Non-IFRS and Supplementary Financial Measures" section of this MD&A.

(2)Represents forward-looking information.

(3)The actual 2025 amounts for the most directly comparable IFRS measures for Adjusted EBITDA and FCF were as follows: Loss before income taxes of $141 million and Cash flow from operating activities of $646 million. The most directly comparable IFRS ratio to FCF per share is cash flow from operating activities per share of $2.18, which is calculated as cash flow from operating activities for the period divided by the weighted average number of common shares outstanding during the period. Refer to the "Non-IFRS and Supplementary Financial Measures" section of the MD&A for additional information.

The Company's outlook for 2026 may be impacted by a number of factors as detailed further below.

Range of key 2026 power and gas price assumptions

| | | | | | | | | | | | | |

| Market | | 2026 Assumptions | 2025 Assumptions | 2025 Actual | |

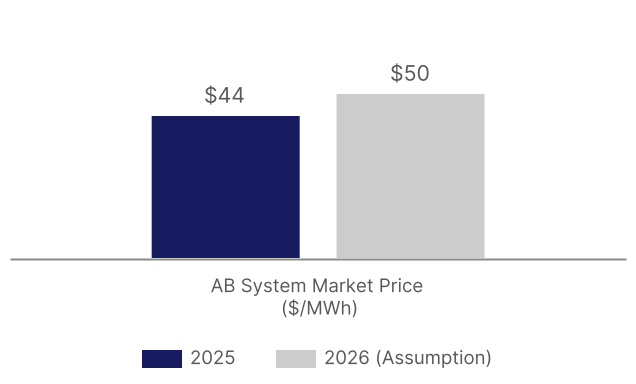

| Alberta spot ($/MWh) | | $40 to $60 | $40 to $60 | $44 | |

| | | | | |

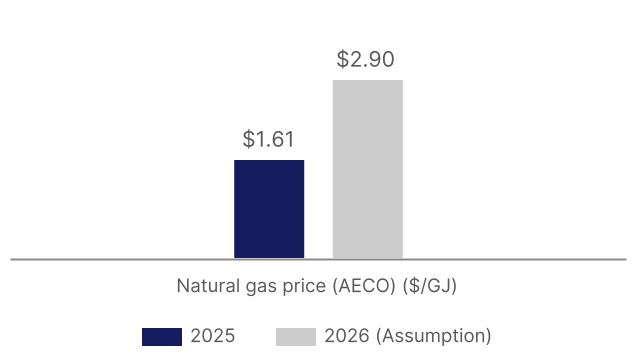

| AECO gas price ($/GJ) | | $2.65 to $3.15 | $1.60 to $2.10 | $1.61 | |

Alberta spot price sensitivity: a +/- $1 per MWh change in spot price is expected to have a +/- $2 million impact on Adjusted EBITDA for 2026.

| | | | | | | | |

| TransAlta Corporation | 2025 Annual Report | M19 |

Other assumptions relevant to the 2026 outlook

| | | | | | | | | | | | | |

| Measure | 2026 Expectations | 2025 Expectations | | 2025 Actual | |

Energy Marketing Adjusted Revenues(1) | $110 million to $130 million | $110 million to $130 million | | $122 million | |

Sustaining capital expenditures(2) | $140 million to $160 million | $145 million to $165 million | | $162 million | |

Current income tax expense | $70 million to $100 million | $95 million to $130 million | | $49 million | |

Net Interest Expense(1) | $240 million to $260 million | $255 million to $275 million | | $264 million | |

(1)Energy Marketing Adjusted Revenues and Net Interest Expense are non-IFRS measures, are not defined, have no standardized meaning under IFRS and may not be comparable to similar measures presented by other issuers. The most directly comparable IFRS measure to Energy Marketing Adjusted Revenues is revenues of $130 million for the year ended Dec. 31, 2025 and to Net Interest Expense — interest expense of $347 million for the year ended Dec. 31, 2025.

(2)Sustaining capital expenditures is a supplementary financial measure. Refer to "Capital Expenditures" section of this MD&A for more information regarding this measure.

Alberta Hedging

| | | | | | | | | | | | | | | | | | |

| Range of hedging assumptions | Q1 2026 | Q2 2026 | Q3 2026 | Q4 2026 | 2027 | |

| Hedged production (GWh) | 2,302 | | 1,990 | | 2,172 | | 2,027 | | 3,967 | | |

| Hedge price ($/MWh) | $65 | $65 | $65 | $65 | $71 | |

Hedged gas amounts (GJ) | 12 million | 7 million | 8 million | 7 million | 19 million | |

| Hedge gas prices ($/GJ) | $3.21 | $3.33 | $3.29 | $3.39 | $3.04 | |

| | | | | | |

| | | | | | |

Market Pricing

The following graphs include 2026 pricing assumptions and are subject to change:

Annual Average Spot Electricity Prices

Annual Average Gas (AECO) Prices

For 2026, spot electricity prices in Alberta are expected to be higher compared to 2025, driven by ongoing load growth and slowing additions of new supply in the province. Where power prices settle in relationship to 2025 prices, will ultimately depend on actual weather conditions.

AECO natural gas prices are expected to be higher than in 2025.

The objective of our portfolio management strategy in Alberta is to balance opportunity and risk and to deliver optimization strategies that contribute to our total

investment, which includes a return on invested capital. We can be more or less hedged in a given period, and we expect to realize our annual targets through a combination of forward hedging and selling generation into the spot market. The assets within the Alberta electricity portfolio are managed as a portfolio to maximize the overall value of generation and capacity from our hydro, wind, energy storage and thermal facilities. Hedging is a key component of cash flow certainty and the hedges are primarily tied to our portfolio of gas facilities and also allocated to our portfolio of hydro facilities rather than a single facility.

| | | | | | | | |

M20 | TransAlta Corporation | 2025 Annual Report |

Sustaining Capital Expenditures

Our estimate for total sustaining capital is as follows:

| | | | | | | | | |

| | Expected spend in 2026 | Spent in 2025 |

| Total sustaining capital | | $140 million to $160 million | $162 million |

The Company expects sustaining capital to be in the range of $140 million to $160 million in 2026. The Gas segment is expected to incur higher sustaining capital related to planned major maintenance, offset by lower spend in the Hydro segment.

Liquidity and Capital Resources

We maintain adequate available liquidity under our committed credit facilities. As at Dec. 31, 2025, we had access to $1.5 billion in liquidity, including $205 million in cash, which exceeds the funds required for committed growth, sustaining capital and productivity projects.

Segmented Financial Performance and Operating Results

Segmented information is prepared on the same basis that the Company manages its business, evaluates financial results and makes key operating decisions. The following table reflects the summary financial information on a consolidated basis for the three months and year ended Dec. 31:

| | | | | | | | | | | | | | | |

| 3 months ended Dec. 31, | Year ended Dec. 31 | |

| 2025 | 2024 | 2025 | 2024 | |

| Hydro | 39 | | 57 | | 285 | | 316 | | |

| Wind and Solar | 102 | | 95 | | 338 | | 316 | | |

Gas | 96 | | 116 | | 438 | | 524 | | |

| Energy Transition | 16 | | 26 | | 100 | | 89 | | |

| Energy Marketing | 21 | | 26 | | 85 | | 146 | | |

Corporate | (27) | | (38) | | (142) | | (136) | | |

Total Adjusted EBITDA(1)(2) | 247 | | 282 | | 1,104 | | 1,255 | | |

Adjusted Earnings before income taxes(1) | 14 | | 38 | | 181 | | 396 | | |

(Loss) earnings before income taxes | (42) | | (51) | | (141) | | 319 | | |

Adjusted Net (Loss) Earnings Attributable to Common Shareholders(1) | (19) | | 3 | | 57 | | 236 | | |

Net (loss) earnings attributable to common shareholders | (62) | | (65) | | (190) | | 177 | | |

(1)These are non-IFRS measures, which are not defined, have no standardized meaning under IFRS and may not be comparable to similar measures presented by other issuers. Refer to the "Non-IFRS and Supplementary Financial Measures" section of this MD&A for more information regarding these measures. The most directly comparable IFRS measure to Adjusted EBITDA and Adjusted Earnings before income taxes is (loss) earnings before income taxes. The most directly comparable IFRS measure to Adjusted Net (Loss) Earnings Attributable to Common Shareholders is Net (loss) earnings attributable to common shareholders. Refer to "Reconciliation of Non-IFRS Measures on a Consolidated Basis by Segments" section of this MD&A.

(2)During the first quarter of 2025, our Adjusted EBITDA composition was amended to exclude the impact of realized gain (loss) on closed exchange positions and Australian interest income. Therefore, the Company has applied this composition to all previously reported periods. Refer to the "Non-IFRS and Supplementary Financial Measures" section of this MD&A.

Three months ended Dec. 31, 2025

Adjusted Earnings before income taxes for the three months ended Dec. 31, 2025 decreased by $24 million, or 63 per cent, from Adjusted Earnings before income taxes for the same period in 2024, primarily due to:

•The factors causing lower Adjusted EBITDA described in the "Adjusted EBITDA" section of this MD&A; and

•Higher depreciation due to the addition of the Heartland gas facilities in December 2024; partially offset by

•Lower interest expense as explained in the Corporate segment of the "Segmented Financial Performance and Operating Results" section of this MD&A.

| | | | | | | | |

| TransAlta Corporation | 2025 Annual Report | M21 |

Adjusted Net Loss attributable to common shareholders for the three months ended Dec. 31, 2025 increased by $22 million from Adjusted Earnings Attributable to Common Shareholders for the same period in 2024, primarily due to:

•The factors causing higher Adjusted Earnings before Income Taxes described above; and

•Lower calculated tax expense on adjustments and reclassifications compared to the same period in 2024; partially offset by

•Lower income tax recovery compared to the same period in 2024 due to a decrease in loss before income taxes.