Please wait

Management Discussion & Analysis

Management of Algonquin Power & Utilities Corp. ("AQN", the "Company" or the "Corporation") has prepared the following discussion and analysis to provide information to assist its securityholders' understanding of the financial results for the three and twelve months ended December 31, 2025. This Management Discussion & Analysis ("MD&A") should be read in conjunction with AQN's audited consolidated financial statements for the years ended December 31, 2025 and 2024. This material is available on SEDAR+ at www.sedarplus.com, on EDGAR at www.sec.gov/edgar and on the AQN website at www.algonquinpower.com. Additional information about AQN, including the most recent Annual Information Form ("AIF"), can be found on SEDAR+ at www.sedarplus.com and on EDGAR at www.sec.gov/edgar.

Contents

| | | | | |

| Explanatory Notes | |

| Caution Concerning Forward-Looking Statements and Forward-Looking Information | |

| Caution Concerning Non-GAAP Measures | |

| Overview and Business Strategy | |

| Financial Outlook | |

| Significant Updates | |

2025 Fourth Quarter Results From Operations | |

2025 Annual Results From Operations | |

| |

| |

| |

| Regulated Services Group | |

| |

Corporate Group Net Earnings and Adjusted Earnings | |

Hydro Group Net Earnings | |

| |

Discontinued Operations: Renewable Energy Group | |

| Non-GAAP Financial Measures | |

| |

| Summary of Property, Plant and Equipment Expenditures | |

| Liquidity and Capital Reserves | |

| Share-Based Compensation Plans | |

| Enterprise Risk Management | |

| Quarterly Financial Information | |

| |

| Disclosure Controls and Procedures | |

| |

| Critical Accounting Estimates and Policies | |

| | | | | |

| |

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 1 |

Explanatory Notes

Unless otherwise indicated, financial information provided for the years ended December 31, 2025 and 2024 has been prepared in accordance with generally accepted accounting principles in the United States ("U.S. GAAP"). As a result, the Company's financial information may not be comparable with financial information of other Canadian companies that provide financial information on another basis.

All monetary amounts are in U.S. dollars, except where otherwise noted. We denote any amounts denominated in Canadian dollars with "C$" immediately prior to the stated amount. Certain amounts in this MD&A may not total due to rounding.

Capitalized terms used herein and not otherwise defined have the meanings assigned to them in the Company's most recent AIF.

The term "rate base" is used in this document. Rate base is a measure specific to rate-regulated utilities that is not intended to represent any financial measure as defined by U.S. GAAP. The measure is used by the regulatory authorities in the jurisdictions where the Company's rate-regulated subsidiaries operate. The calculation of this measure may not be comparable to similarly-titled measures used by other companies.

Unless noted otherwise, this MD&A is based on information available to management as of March 6, 2026.

Renewables business sale

On January 8, 2025, the Company completed the previously announced sale of its renewable energy business (excluding hydro) (the "Renewables Sale") to a wholly-owned subsidiary of LS Power ("LS Buyer") for proceeds of approximately $2.1 billion, after subtracting taxes, transaction fees and other preliminary closing adjustments, including an adjustment for estimated remaining completion costs for in-construction assets. Approximately $1.95 billion of such proceeds were received upon the closing of the transaction and an additional approximately $115 million in proceeds were received in 2025 upon monetization of tax attributes on certain in-construction projects. The remaining $35 million of proceeds are currently expected to be received in 2026 upon monetization of tax attributes on additional in-construction projects. Additionally, the Company can receive up to $220 million in cash pursuant to an earn out agreement relating to certain wind assets (the "Earn Out"). The amount and timing of the ultimate net cash proceeds will be dependent on final completion costs for in-construction assets, the associated monetization of tax credits on certain of these projects (including, but not limited to, future events which could cause recapture of part or all of the tax attributes monetized and refund of the associated proceeds), and other final closing adjustments.

During the third quarter of 2024, the Company concluded that the consolidated assets within its former renewable energy group (excluding hydro) met the accounting requirements to be presented as "Held for Sale". As a result, the renewable energy group (excluding hydro) was classified as "discontinued operations" until closing of the Renewables Sale on January 8, 2025. The Company recorded a total impairment loss of $1,357.3 million in 2024 as a result of the classification of the renewable energy group (excluding hydro) as "discontinued operations". Further, the Company recorded loss from discontinued operations of $11.0 million and $37.7 million during the three and twelve months ended December 31, 2025, respectively.

The discontinued operations operated as a distinct segment and had no impact on the operations of the Regulated Services Group operating segment, other than sharing certain corporate support functions and benefiting from corporate debt and equity funding. This MD&A reflects the results of continuing operations, unless otherwise noted.

| | | | | | |

| | |

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 2 | |

Caution Concerning Forward-Looking Statements and Forward-Looking Information

This document may contain statements that constitute "forward-looking information" within the meaning of applicable securities laws in each of the provinces and territories of Canada and the respective policies, regulations and rules under such laws or "forward-looking statements" within the meaning of the U.S. Private Securities Litigation Reform Act of 1995 (collectively, "forward-looking information"). The words "aims", "anticipates", "believes", "budget", "could", "estimates", "expects", "forecasts", "intends", "may", "might", "plans", "projects", "schedule", "seeks", "should", "strives", "targets", "will", "would", "pursue", "outlook" (and grammatical variations of such terms) and similar expressions are often intended to identify forward-looking information, although not all forward-looking information contains these identifying words. Specific forward-looking information in this document includes, but is not limited to, statements relating to: expected future investments and growth, earnings (including 2026 and 2027 Adjusted Net Earnings per common share) and results of operations; expected tax rates and tax optimization strategies; the timing and costs of gas operational excellence activities; expectations regarding the timing and amount of certain proceeds and the Earn Out in connection with the Renewables Sale; the Company’s integrated customer solution technology platform; future plans and the expected outcomes thereof; liquidity, capital resources and operational requirements; sources of funding, including adequacy and availability of credit facilities, cash flows from operations, capital markets financing, and asset dispositions; potential acquisitions, dispositions, projects, initiatives or other transactions; financing plans; expectations regarding future macroeconomic conditions; expectations regarding the Company's corporate development activities and the results thereof; expectations regarding regulatory hearings, motions, orders, settlements, proposals, filings, appeals and approvals, including rate reviews, and the timing, impacts and outcomes thereof; expectations regarding the redemption of outstanding notes; expected future generation, capacity and production of the Company's energy facilities; expectations regarding future capital investments, including expected timing, investment plans, sources of funds and impacts; capital management plans and objectives; expectations regarding the outcome of legal claims and disputes; expectations regarding the April 9, 2025 gas incident in Lexington, Missouri, including regulatory actions arising therefrom and availability of insurance coverage; strategy and goals; dividends to shareholders; share price appreciation; credit ratings and equity credit from rating agencies; expectations regarding debt repayment and refinancing; the impact on the Company of actual or proposed laws, regulations and rules; accounting estimates; interest rates, including the anticipated effect of an increase thereof; financing costs; the expected impact of tariffs imposed by the U.S. and Canada and possible changes thereto; and currency exchange rates. All forward-looking information is given pursuant to the "safe harbour" provisions of applicable securities legislation.

The forecasts and projections that make up the forward-looking information contained herein are based on certain factors or assumptions which include, but are not limited to: the receipt of applicable regulatory approvals and requested rate decisions; the absence of material adverse regulatory decisions being received and the expectation of regulatory stability; the absence of any material equipment breakdown or failure; availability of financing including self-monetization transactions for U.S. federal tax credits on commercially reasonable terms; the stability of credit ratings of the Corporation and its subsidiaries; the absence of unexpected material liabilities or uninsured losses; the continued availability of commodity supplies and stability of commodity prices; the absence of interest rate increases or significant currency exchange rate fluctuations; the absence of significant operational, financial or supply chain disruptions or liability, including relating to additional import controls and tariffs; the continued ability to maintain systems and facilities to ensure their continued performance; the absence of a severe and prolonged downturn in general economic, credit, social or market conditions; the successful and timely development and construction of new projects; the absence of capital project or financing cost overruns; sufficient liquidity and capital resources; the continuation of long-term weather patterns and trends; the absence of significant counterparty defaults; the continued competitiveness of electricity pricing when compared with alternative sources of energy; the realization of the anticipated benefits of the Corporation's dispositions, acquisitions and joint ventures; the absence of a change in applicable laws, political conditions, public policies and directions by governments materially negatively affecting the Corporation; the ability to obtain, comply with and maintain licenses and permits; maintenance of adequate insurance coverage; the absence of material fluctuations in market energy prices; the absence of material disputes with taxation authorities or changes to applicable tax laws; continued maintenance of information technology infrastructure and the absence of a material breach of cybersecurity; the successful implementation and operation of new information technology systems and infrastructure; favourable relations with external stakeholders; favourable labour relations; that the Corporation will be able to successfully integrate newly acquired entities, and the absence of any material adverse changes to such entities prior to closing; the absence of undisclosed liabilities of entities being acquired; the absence of any significant indemnification claims arising from the Renewables Sale; the absence of any reputational harm to the Corporation as a result of the Renewables Sale; the absence of adverse reactions or changes in business relationships or relationships with employees following the Renewables Sale; and the ability of the Corporation to realize the anticipated benefits from the Renewables Sale.

The forward-looking information contained herein is subject to risks, uncertainties and other factors that could cause actual results to differ materially from historical results or results anticipated by the forward-looking information. Factors which could cause results or events to differ materially from current expectations include, but are not limited to: changes in general economic, credit, social or market conditions; changes in customer energy usage patterns and energy demand; reductions in the liquidity of energy markets; global climate change; the incurrence of environmental liabilities; natural

| | | | | |

| |

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 3 |

disasters, diseases, pandemics, public health emergencies and other force majeure events and the collateral consequences thereof, including the disruption of economic activity, volatility in capital and credit markets and legislative and regulatory responses; critical equipment breakdown or failure; supply chain disruptions; the impact of existing import controls and tariffs and the imposition of additional import controls or tariffs; the failure of information technology infrastructure and other cybersecurity measures to protect against data, privacy and cybersecurity breaches; failure to successfully implement and operate, and cost overruns and delays in connection with, new information technology systems and infrastructure; physical security breach; the loss of key personnel and/or labour disruptions; seasonal fluctuations and variability in weather conditions and natural resource availability; reductions in demand for electricity, natural gas and water due to developments in technology; reliance on transmission systems owned and operated by third parties; issues arising with respect to land use rights and access to the Corporation's facilities; terrorist attacks; fluctuations in commodity and energy prices; capital expenditures; reliance on subsidiaries; the incurrence of an uninsured loss; a credit rating downgrade; an increase in financing costs or limits on access to credit and capital markets; inflation; increases and fluctuations in interest rates and failure to manage exposure to credit and financial instrument risk; currency exchange rate fluctuations; restricted financial flexibility due to covenants in existing credit agreements; an inability to refinance maturing debt on favourable terms; disputes with taxation authorities or changes to applicable tax laws; requirement for greater than expected contributions to post-employment benefit plans; default by a counterparty; inaccurate assumptions, judgments and/or estimates with respect to asset retirement obligations; failure to maintain required regulatory authorizations; changes in, or failure to comply with, applicable laws and regulations; failure of compliance programs; failure to dispose of assets (at all or at a competitive price) to fund the Company’s operations and strategic objectives; delays and cost overruns in the design and construction of projects; loss of key customers; a third party joint venture partner acting in a manner contrary to the Corporation’s interests; facilities being condemned or otherwise taken by governmental entities; increased external stakeholder activism adverse to the Corporation's interests; fluctuations in the price and liquidity of the Corporation's common shares and the Corporation's other securities; and the failure to implement the Corporation's strategic objectives or achieve expected benefits relating to acquisitions, dispositions or other initiatives. Although the Corporation has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking information, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. Some of these and other factors are discussed in more detail under the heading "Enterprise Risk Management" in this MD&A and under the heading "Enterprise Risk Factors" in the Corporation's most recent AIF.

Forward-looking information contained herein (including any financial outlook) is provided for the purposes of assisting the reader in understanding the Corporation and its business, operations, risks, financial performance, financial position and cash flows as at and for the periods indicated and to present information about management's current expectations and plans relating to the future, and the reader is cautioned that such information may not be appropriate for other purposes. Forward-looking information contained herein is made as of the date of this document and based on the plans, beliefs, estimates, projections, expectations, opinions and assumptions of management on the date hereof. There can be no assurance that forward-looking information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such forward-looking information. Accordingly, readers should not place undue reliance on forward-looking information. While subsequent events and developments may cause the Corporation's views to change, the Corporation disclaims any obligation to update any forward-looking information or to explain any material difference between subsequent actual events and such forward-looking information, except to the extent required by applicable law. All forward-looking information contained herein is qualified by these cautionary statements.

Caution Concerning Non-GAAP Measures

AQN uses a number of financial measures to assess the performance of its business lines. Some measures are calculated in accordance with U.S. GAAP, while other measures do not have a standardized meaning under U.S. GAAP. These non-GAAP measures include non-GAAP financial measures and non-GAAP ratios, each as defined in Canadian National Instrument 52-112 Non-GAAP and Other Financial Measures Disclosure. AQN's method of calculating these measures may differ from methods used by other companies and therefore may not be comparable to similar measures presented by other companies.

The terms "Adjusted Net Earnings", "Earnings Before Interest and Taxes" ("EBIT"), and "Net Utility Sales", which are used throughout this MD&A, are non-GAAP financial measures. An explanation of each of these non-GAAP financial measures is set out below and a reconciliation to the most directly comparable U.S. GAAP measure, in each case, can be found in this MD&A. In addition, "Adjusted Net Earnings" is presented throughout this MD&A on a per common share basis. Adjusted Net Earnings per common share is a non-GAAP ratio and is calculated by dividing Adjusted Net Earnings by the weighted average number of common shares outstanding during the applicable period. As a pure-play regulated utility, as of the first quarter of 2025, the Company no longer presents "Adjusted Earnings Before Interest, Taxes, Depreciation and Amortization" or "Adjusted Funds from Operations" as these metrics were relevant mainly to the Company's former renewable energy group (excluding hydro) that was sold in connection with the Renewables Sale.

AQN does not provide reconciliations for forward-looking non-GAAP financial measures as AQN is unable to provide a meaningful or accurate calculation or estimation of reconciling items and the information is not available without

| | | | | |

| |

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | |

unreasonable effort. This is due to the inherent difficulty of forecasting the timing or amount of various events that have not yet occurred, are out of AQN's control and/or cannot be reasonably predicted, and that would impact the most directly comparable forward-looking U.S. GAAP financial measure. For these same reasons, AQN is unable to address the probable significance of the unavailable information. Forward-looking non-GAAP financial measures may vary materially from the corresponding U.S. GAAP financial measures.

EBIT

EBIT is a non-GAAP financial measure used by many investors to assess the Company's core operational profitability by measuring the profit generated from day-to-day business activities, excluding interest and tax expenses. AQN uses EBIT to assess its operating performance without the effects of (as applicable): income tax expense or recoveries, interest expense and earnings attributable to non-controlling interests. Earnings attributable to non-controlling interests includes Hypothetical Liquidation at Book Value ("HLBV") income (which represents the value of net tax attributes earned in the period from electricity generated by certain of AQN's U.S. wind power and U.S. solar generation facilities). AQN believes that presentation of this measure will enhance an investor's understanding of AQN's operating performance. EBIT is not intended to be representative of cash provided by operating activities or results of operations determined in accordance with U.S. GAAP, and can be impacted positively or negatively by these items. For a reconciliation of EBIT to net earnings attributable to common shareholders, see Non-GAAP Financial Measures starting on page 38 of this MD&A. For reconciliations of EBIT by business segments, see 2025 Fourth Quarter and Annual Regulated Services Group Net Earnings starting on page 20, Corporate Group Net Earnings and Adjusted Net Earnings on page 34 and Hydro Group Net Earnings on page 36. Adjusted Net Earnings

Adjusted Net Earnings is a non-GAAP financial measure used by many investors to compare net earnings attributable to common shareholders from operations without the effects of certain volatile primarily non-cash items that generally have no current economic impact or items such as acquisition expenses or certain litigation expenses that are viewed as not directly related to a company’s operating performance. AQN uses Adjusted Net Earnings to assess its performance without the effects of (as applicable): gains or losses on foreign exchange, foreign exchange forward contracts, interest rate swaps, acquisition and transition costs, one-time costs of arranging tax equity financing, certain litigation expenses and write down of intangibles and property (including restructuring costs related to the Company's transition to a pure-play utility), plant and equipment, earnings or loss from discontinued operations, unrealized mark-to-market revaluation impacts, costs related to management succession and executive retirement, costs related to prior period adjustments due to changes in tax law, costs related to condemnation proceedings, changes in value of investments carried at fair value, gains and losses on disposition of assets, prior period adjustments included in the gain (loss) from equity method investments not operated by the Company and other typically non-recurring or unusual items as these are not reflective of the performance of the underlying business of AQN. AQN believes that analysis and presentation of net earnings or loss on this basis will enhance an investor’s understanding of the operating performance of its businesses. Adjusted Net Earnings is not intended to be representative of net earnings or loss determined in accordance with U.S. GAAP, and can be impacted positively or negatively by these items. For a reconciliation of Adjusted Net Earnings to net earnings attributable to common shareholders, see Non-GAAP Financial Measures starting on page 39 and Corporate Group Net Earnings and Adjusted Net Earnings on page 34 of this MD&A. The composition of Adjusted Net Earnings has been changed from that previously disclosed in the Company's most-recently filed quarterly interim MD&A to exclude dividends on the Company's Series A and Series D preferred shares. Management believes this change better aligns the measure with industry practice and improves the metric's usefulness to investors. Comparative figures for this metric have been adjusted for the new composition.

Net Utility Sales

Net Utility Sales is a non-GAAP financial measure used by investors to identify utility revenue after commodity costs, either water, natural gas or electricity, where these commodity costs are generally included as a pass through in rates to its utility customers. AQN uses Net Utility Sales to assess its utility revenues without the effects of fluctuating commodity costs as such costs are predominantly passed through and paid for by utility customers. AQN believes that analysis and presentation of Net Utility Sales on this basis will enhance an investor's understanding of the revenue generation of the Regulated Services Group. It is not intended to be representative of revenue as determined in accordance with U.S. GAAP. For a reconciliation of Net Utility Sales to revenue, see 2025 Fourth Quarter and Annual Regulated Services Group Net Earnings on page 20 of this MD&A. | | | | | |

| |

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 5 |

Overview and Business Strategy

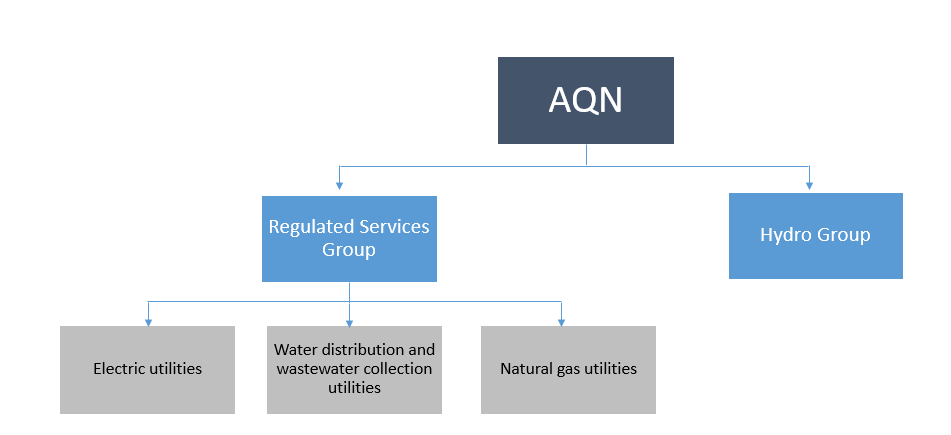

AQN is incorporated under the Canada Business Corporations Act. The Company's operations are organized across two business units consisting of (i) the Regulated Services Group, which primarily owns and operates a portfolio of regulated electric, water distribution and wastewater systems and natural gas utility systems and transmission operations in the United States, Canada, Bermuda and Chile; and (ii) the Hydro Group, which consists of hydroelectric generation facilities located in Canada that were not sold as part of the Renewables Sale. Additionally, the Company has a corporate function, the Corporate Group, consisting of corporate debt and corporate and shared services that primarily support the Regulated Services Group and the Hydro Group. The Company's investment in Atlantica Sustainable Infrastructure plc ("Atlantica"), which previously formed part of the Corporate Group, was sold during the fourth quarter of 2024. The Company’s former renewable energy group (excluding hydro) is reported as discontinued operations (see Note 23 to the audited consolidated financial statements - Disposition of Renewable Energy Business) and was sold by the Company on January 8, 2025. The Company's business units align with how the Company assesses financial performance and makes decisions regarding resource allocations. Through its activities, the Company aims to drive growth in earnings and cash flows to support a sustainable dividend and share price appreciation. AQN strives to achieve these results while also seeking to maintain a business risk profile consistent with its investment grade credit ratings.

Summary Structure of the Business

The following chart depicts, in summary form, AQN's key operating business units. A more detailed description of AQN's organizational structure as of the date of the AIF can be found in the most recent AIF.

| | | | | |

| |

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 6 |

Regulated Services Group

The Regulated Services Group primarily operates a diversified portfolio of regulated utility systems located in the United States, Canada, Bermuda and Chile serving approximately 1,272,000 customer connections as at December 31, 2025 (using an average of 2.5 customers per connection, this translates into approximately 3,170,000 customers). The Regulated Services Group seeks to provide safe, high quality, and reliable services to its customers and to deliver stable and predictable earnings to AQN. The Regulated Services Group seeks to deliver long-term growth within its service territories, including through the pursuit of capital investment opportunities and other initiatives.

The Regulated Services Group's regulated electrical distribution utility systems and related generation assets are located in the U.S. states of Arkansas, California, Kansas, Missouri, Nevada, New Hampshire and Oklahoma, as well as in Bermuda, which together served approximately 311,000 electric customer connections as at December 31, 2025. The group also owns and operates generating assets with a gross capacity of approximately 2.0 GW and has investments in generating assets with approximately 0.3 GW of net generation capacity.

The Regulated Services Group's regulated water distribution and wastewater utility systems are located in the U.S. States of Arizona, Arkansas, California, Illinois, Missouri, New York, and Texas as well as in Chile which together served approximately 583,000 customer connections as at December 31, 2025.

The Regulated Services Group's regulated natural gas distribution utility systems are located in the U.S. States of Georgia, Illinois, Iowa, Massachusetts, Missouri New Hampshire, and New York, and in the Canadian Province of New Brunswick, which together served approximately 378,000 natural gas customer connections as at December 31, 2025.

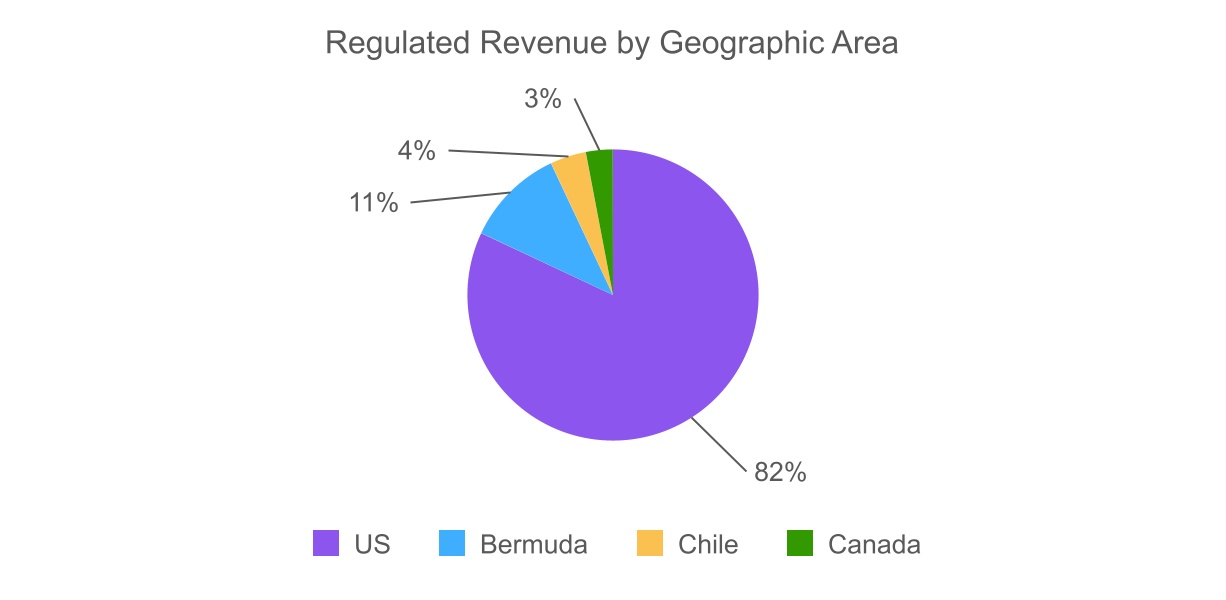

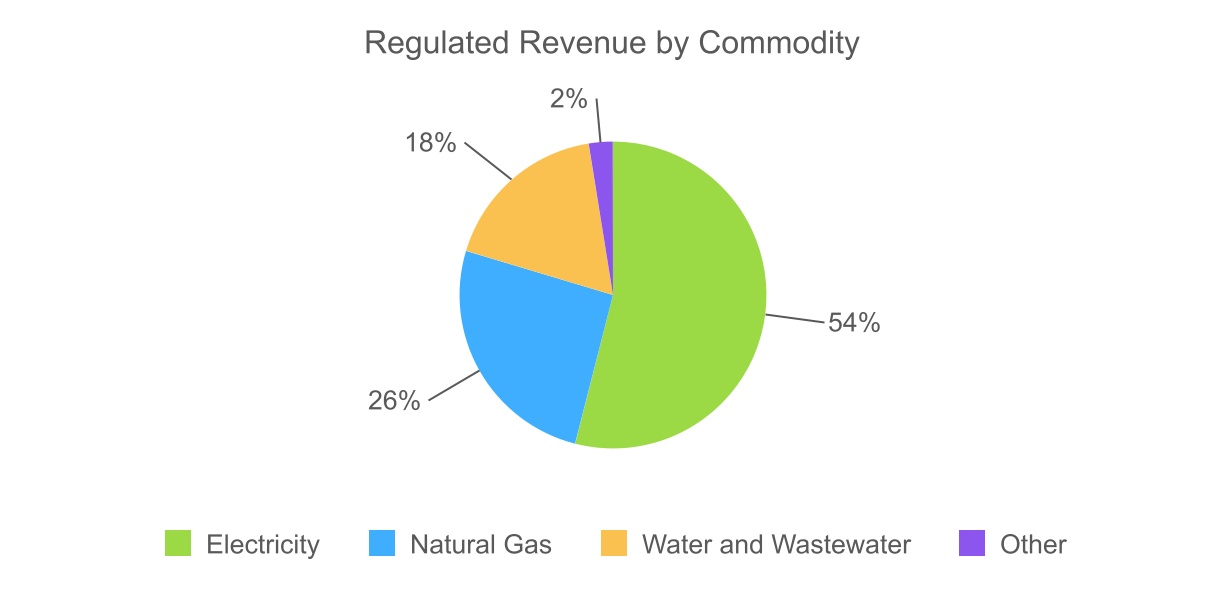

Below is a breakdown of the Regulated Services Group's Revenue by geographic area and by commodity for the twelve months ended December 31, 2025.

| | | | | |

| |

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | |

Hydro Group

The Hydro Group is comprised of 14 hydroelectric generating facilities located in the Canadian provinces of Alberta, Ontario, New Brunswick and Quebec with a combined gross generating capacity of approximately 112 MW and a net generating capacity of approximately 104 MW.

Corporate Group

The Corporate Group primarily consists of AQN’s corporate and shared services and corporate debt, in addition to certain ancillary investments. Prior to the sale of the Company's investment in Atlantica on December 12, 2024, the Corporate Group also included the Company’s interest in Atlantica.

The Company’s former renewable energy group (excluding hydro) is reported as "discontinued operations" and was sold by the Company on January 8, 2025.

| | | | | |

| |

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | |

Financial Outlook

The following discussion should be read in conjunction with the Caution Concerning Forward-Looking Statements and Forward-Looking Information section in this MD&A. Actual results may differ materially from the estimates below. Accordingly, investors are cautioned not to place undue reliance on these estimates.

The Company estimates that its Adjusted Net Earnings per common share will be within a range of $0.35 - $0.37 for 2026 (see Caution Concerning Non-GAAP Measures). With respect to the Company's previously disclosed Adjusted Net Earnings per common share outlook for 2027, the Company now expects its effective tax rate in 2027 to be in the mid-to-high twenties as compared to the previously anticipated low-to-mid twenties estimate, resulting in a decrease to anticipated 2027 Adjusted Net Earnings per common share of slightly more than $0.03 compared to the Company's previous estimate. The Company also now expects the timing of gas operational excellence activities to extend into 2027. When combined, these factors result in an updated expected Adjusted Net Earnings per common share range of $0.38 - $0.42 for 2027. The Company continues to evaluate various tax strategies to optimize its effective tax rate but expects the majority of the benefits from such strategies to be realized after 2027. The Company also expects the costs of gas operational excellence activities assumed in 2027 to normalize thereafter.

The Company is focused on organic capital investment, with utility capital expenditures of approximately $3.2 billion expected for 2026 through 2028 including approximately $0.8 billion in 2026.

The foregoing financial outlook, including estimated Adjusted Net Earnings per common share and expectations regarding capital expenditures, is based on the following key assumptions, as well as those set out under Caution Concerning Forward-Looking Statements and Forward-Looking Information:

•resolution of customer billing matters, regulatory investigations and rate decisions in line with expectations, including absence of material write downs of assets;

•normalized weather patterns in the geographical areas in which the Company operates;

•insurance coverage remains effective and sufficient;

•capital projects being completed on time, substantially in line with budgeted costs, and without adverse tariff impacts;

•timely receipt of required regulatory approvals and permits;

•the absence of material disruptions to supply chains or labour availability affecting pricing, operations or project execution;

•realization of company-wide efficiency initiatives in line with expectations;

•the absence of significant changes in applicable political or macroeconomic environments or capital markets, including with respect to legislation, interest rates or inflation;

•a Canadian dollar/U.S. dollar exchange rate and a Chilean peso/U.S. dollar exchange rate in line with expectations;

•receipt of anticipated proceeds under the Earn Out;

•a low twenties percentage effective tax rate in 2026, and a mid-to-high twenties percentage effective tax rate in 2027;

•the timing and amount of gas operational excellence activities costs in line with expectations;

•energy production consistent with long-term averages and realized pricing in line with expectations;

•the absence of significant adverse litigation outcomes, fines, penalties, losses and inverse condemnation rulings; and

•access to capital markets at pricing consistent with current market levels.

| | | | | |

| |

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 9 |

Significant Updates

Operating Results

AQN's operating results relative to the same period last year are as follows:

| | | | | | | | | | | | | | | | | | | | | | | |

| Three months ended December 31 | | Twelve months ended December 31 |

(all dollar amounts in $ millions except per share information) | 2025 | 2024 | Change | | 2025 | 2024 | Change |

Net earnings (loss) attributable to shareholders from continuing operations | $ | 32.0 | | $ | (107.5) | | 130 | % | | $ | 218.5 | | $ | 65.3 | | 235 | % |

Net earnings (loss) attributable to common shareholders from continuing operations | 29.4 | | (110.2) | | 127 | % | | 208.0 | | 54.8 | | 280 | % |

Net earnings (loss) attributable to common shareholders from continuing operations and discontinued operations | 18.4 | | (189.1) | | 110 | % | | 170.3 | | (1,391.0) | | 112 | % |

| | | | | | | |

| | | | | | | |

Adjusted Net Earnings1 | 47.2 | | 42.5 | | 11 | % | | 258.8 | | 221.6 | | 17 | % |

EBIT1 | 93.2 | | 115.8 | | (20) | % | | 493.5 | | 540.8 | | (9) | % |

Net earnings (loss) per common share from continuing operations | $ | 0.04 | | $ | (0.14) | | 129 | % | | $ | 0.27 | | $ | 0.07 | | 286 | % |

Net earnings per common share from continuing operations and discontinued operations | $ | 0.02 | | $ | (0.25) | | 108 | % | | $ | 0.22 | | $ | (1.90) | | 112 | % |

Adjusted Net Earnings per common share1 | $ | 0.06 | | $ | 0.06 | | — | % | | $ | 0.34 | | $ | 0.30 | | 13 | % |

1 See Caution Concerning Non-GAAP Measures. | | | | | | | |

Management Changes

On February 16, 2026, the Company appointed Kristin von Fischer as Chief Human Resources Officer, effective as of such date.

On January 5, 2026, the Company announced the appointment of Peter Norgeot as Chief Operating Officer, effective as of such date.

On November 7, 2025, the Company announced the appointment of Robert Stefani as Chief Financial Officer. Mr. Stefani's appointment was effective January 5, 2026. Brian Chin acted as Interim Chief Financial Officer until January 5, 2026 and after such date, has continued with the Company in his Vice President, Investor Relations role.

On June 18, 2025, the Company announced the appointment of Amy Walt as Chief Customer Officer, effective June 30, 2025.

On June 9, 2025, the Company announced the appointment of Noel Black as Chief Regulatory and External Affairs Officer, effective June 30, 2025.

On January 31, 2025, the Company announced that Roderick West would join the Company as Chief Executive Officer. Mr. West’s appointment as Chief Executive Officer was effective as of 12:00 p.m. (Eastern time) on March 7, 2025. Chris Huskilson stepped down as Chief Executive Officer as of such date and continued in his role as a director of the Company until November 24, 2025.

Sale of Renewable Energy Business

On January 8, 2025, the Company completed the sale of its renewable energy business (excluding hydro) to LS Buyer. Please refer to the section titled “Explanatory Notes” above for additional details regarding the Renewables Sale.

| | | | | |

| |

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 10 |

2025 Fourth Quarter Results From Operations

| | | | | | | | | |

Key Financial Information1 | Three months ended December 31 |

| (all dollar amounts in $ millions except per share information) | 2025 | 2024 | |

| Revenue | $ | 630.7 | | $ | 584.8 | | |

Net revenue | 446.8 | | 432.6 | | |

Net earnings (loss) attributable to shareholders | 32.0 | | (107.5) | | |

Net earnings (loss) attributable to common shareholders | 29.4 | | (110.2) | | |

| | | |

| Net earnings (loss) attributable to common shareholders from continuing operations and discontinued operations | 18.4 | | (189.1) | | |

Adjusted Net Earnings2 | 47.2 | | 42.5 | | |

Dividends declared to common shareholders | 50.5 | | 50.4 | | |

| Weighted average number of common shares outstanding | 768,429,981 | | 767,465,543 | | |

Per common share | | | |

Basic and diluted net earnings (loss) | $ | 0.04 | | $ | (0.14) | | |

Basic and diluted net earnings from continuing operations and discontinued operations | $ | 0.02 | | $ | (0.25) | | |

| Basic and diluted net loss from discontinued operations | $ | (0.01) | | $ | (0.10) | | |

Adjusted Net Earnings2 | $ | 0.06 | | $ | 0.06 | | |

| Dividends declared to common shareholders | $ | 0.07 | | $ | 0.07 | | |

| | | | | |

| 1 | Reflects results of continuing operations unless marked otherwise (see Explanatory Notes). |

| 2 | See Caution Concerning Non-GAAP Measures. |

| |

For the three months ended December 31, 2025, AQN reported revenue of $630.7 million as compared to $584.8 million in the comparative period, an increase of $45.9 million. This increase was mainly driven by higher pass through commodity costs across all gas systems, as well as the implementation of approved rates of $10.3 million.

The following table outlines the changes to Adjusted Net Earnings1 for the three months ended December 31, 2025 as compared to the same period in 2024, including the breakdown of net earnings attributable to common shareholders by the Company's main business units and the discussion below outlines the changes to net earnings attributable to common shareholders:

| | | | | | | | | | | |

Net Earnings by business units2 and Total Adjusted Net Earnings1 | Three months ended December 31 |

| (all dollar amounts in $ millions) | 2025 | 2024 | Change |

| Net earnings for Regulated Services Group | $ | 73.6 | | $ | 60.5 | | $ | 13.1 | |

| Net earnings for Hydro Group | 2.1 | | 2.5 | | $ | (0.4) | |

| Net loss for Corporate Group | (46.3) | | (173.2) | | $ | 126.9 | |

| Total Net Earnings (Loss) | 29.4 | | (110.2) | | 139.6 | |

Add: Adjusted items | 17.8 | | 152.7 | | (134.9) | |

Total Adjusted Net Earnings1 | $ | 47.2 | | $ | 42.5 | | $ | 4.7 | |

| | | |

| | | |

| | | | | |

| 1 | See Caution Concerning Non-GAAP Measures. |

| 2 | Reflects results of continuing operations unless marked otherwise (see Explanatory Notes). |

| | | | | |

| |

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 11 |

| | | | | | | | | | | | | | |

Change in Net Earnings and Adjusted Net Earnings1 Breakdown2 | Three months ended December 31, 2025 |

| (all dollar amounts in $ millions) | Regulated Services | Hydro | Corporate | Total |

Change in Net Earnings attributable to common shareholders | | | | |

Net earnings (loss) attributable to common shareholders - Prior period balances | $ | 60.5 | | $ | 2.5 | | $ | (173.2) | | $ | (110.2) | |

| | | | |

EBIT1,3 | | | | |

Electricity | (4.7) | | — | | — | | (4.7) | |

Natural Gas | 6.4 | | — | | — | | 6.4 | |

Water | (1.0) | | — | | — | | (1.0) | |

Other | (1.6) | | (0.3) | | (21.4) | | (23.3) | |

Total change in EBIT1 | (0.9) | | (0.3) | | (21.4) | | (22.6) | |

| | | | |

| Interest expense | 10.6 | | — | | 7.3 | | 17.9 | |

Income tax expense | 1.4 | | — | | 140.9 | | 142.3 | |

Net effect of non-controlling interests | 2.0 | | (0.1) | | — | | 1.9 | |

Series A Shares and Series D Shares dividend | — | | — | | 0.1 | | 0.1 | |

Total change in net earnings (loss) | 13.1 | | (0.4) | | 126.9 | | 139.6 | |

| | | | |

Net earnings (loss) attributable to common shareholders - Current period balances | 73.6 | | 2.1 | | (46.3) | | 29.4 | |

| | | | |

Change in Adjusted Net Earnings1 | | | | |

Adjusted Net Earnings (Loss)1 - Prior period balance3 | 60.5 | | 2.5 | | (20.5) | | 42.5 | |

Total change in net earnings (loss) | 13.1 | | (0.4) | | 126.9 | | 139.6 | |

Total change in adjusted items,3 | — | | — | | (134.9) | | (134.9) | |

Adjusted Net Earnings (loss)1 - Current period balances | $ | 73.6 | | $ | 2.1 | | $ | (28.5) | | $ | 47.2 | |

| | | | | |

| 1 | See Caution Concerning Non-GAAP Measures. |

| 2 | Reflects results of continuing operations unless marked otherwise (see Explanatory Notes). |

| 3 | See Corporate Group Net Earnings and Adjusted Net Earnings. |

For the three months ended December 31, 2025, AQN reported net earnings attributable to common shareholders of $29.4 million and basic net earnings per common share of $0.04. During the comparative period in 2024, the Company reported net loss attributable to common shareholders of $110.2 million and basic net loss per common share of $0.14. The net earnings attributable to common shareholders increased by $139.6 million and the basic net earnings per common share increased by $0.18. These increases were primarily driven by:

•an increase of $13.1 million in the net earnings of the Regulated Services Group primarily due to:

–an increase in net earnings of $26.3 million primarily driven by the implementation of approved rates of $10.3 million, an increase in net earnings of $5.4 million due to favorable weather normalization, lower interest expense of $10.6 million as a result of the repayment of debt with the proceeds from the Renewables Sale and the proceeds from the sale of the Company’s investment in Atlantica; partially offset by;

–a decrease of $13.2 million primarily driven by higher operating expenses of $2.4 million (unfavorable operating expenses such as a targeted relief initiative for customers of $8.5 million agreed to as part of the Empire District Electric System (MO) rate case settlement and a non-recoverable write-off of $2.0 million pertaining to the Lexington gas incident; partially offset by favorable labour and maintenance expenses), higher depreciation expense of $3.7 million due to additional assets placed in service, and other non-recurring expenses primarily due to a $7.3 million write-off related to the discontinuation of a solar project at the CalPeco Electric System; and

| | | | | |

| |

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | |

•an increase of $126.9 million in the net earnings of the Corporate Group primarily due to:

–an increase in net earnings of $148.2 million primarily driven by a decrease in income tax expenses of $140.9 million due to valuation allowance recorded in 2024 on Canadian deferred tax assets and the effect from the restructuring of certain intercompany financing arrangements which were executed in advance of the implementation of global minimum tax rules in the various jurisdictions in which the Company operates, as well as a $7.3 million decrease in interest expense as a result of the repayment of debt with the proceeds of the Renewables Sale and the proceeds from the sale of the Company's investment in Atlantica; partially offset by;

–a decrease of $24.9 million primarily driven by a decrease of $10.9 million owing to decreased dividends received from the Company’s investment in Atlantica during the fourth quarter of 2024, which was sold in the fourth quarter of 2024, as well as a $14.0 million increase in non-recurring charges primarily due to restructuring.

For the three months ended December 31, 2025 and December 31, 2024, AQN reported Adjusted Net Earnings per common share of $0.06 (see Caution Concerning Non-GAAP Measures). Adjusted Net Earnings increased by $4.6 million period over period (see Caution Concerning Non-GAAP Measures). This increase was primarily driven by the factors noted above (see Reconciliation of Adjusted Net Earnings to Net Earnings).

For the three months ended December 31, 2025, cash provided by operating activities increased by $127.9 million as compared to the same period in 2024, primarily as a result of an increase in Net Earnings of $139.6 million and changes in working capital items of $157.7 million (see Note 21 to the audited consolidated financial statements - Non Cash Operating Items). For the three months ended December 31, 2025 cash provided by investing activities decreased by $1,005.0 million as a result of non-recurring proceeds from the sale of the Company's investment in Atlantica in the prior year. For the three months ended December 31, 2025 cash provided by financing activities increased by $890.4 million primarily because in the fourth quarter of the 2024, the Company repaid debt using the proceeds from the sale of the investment in Atlantica.

| | | | | |

| |

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | |

2025 Annual Results From Operations1

| | | | | | | | | | | | |

Key Financial Information | Twelve months ended December 31 |

| (all dollar amounts in $ millions except per share information) | 2025 | 2024 | 2023 | |

| Revenue | $ | 2,433.6 | | $ | 2,319.5 | | $ | 2,403.9 | | |

Net Revenue | 1,793.8 | | 1,718.7 | | 1,686.9 | | |

Net earnings (loss) attributable to shareholders | 218.5 | | 65.3 | | (14.4) | | |

Net earnings attributable to common shareholders | 208.0 | | 54.8 | | (22.8) | | |

| | | | |

Net earnings (loss) attributable to common shareholders from continuing operations and discontinued operations | 170.3 | | (1,391.0) | | 20.3 | | |

| | | | |

| | | | |

Adjusted Net Earnings2 | 258.8 | | 221.6 | | 271.0 | | |

| Dividends declared to common shareholders | 201.8 | | 260.0 | | 301.8 | | |

| Weighted average number of common shares outstanding | 768,098,435 | | 731,721,239 | | 688,738,717 | | |

Per common share | | | | |

Basic and diluted net earnings (loss) | $ | 0.27 | | $ | 0.07 | | $ | (0.03) | | |

Basic and diluted net earnings (loss) from continuing operations and discontinued operations | $ | 0.22 | | $ | (1.90) | | 0.03 | | |

| | | | |

Adjusted Net Earnings2 | $ | 0.34 | | $ | 0.30 | | $ | 0.39 | | |

| Dividends declared to common shareholders | $ | 0.26 | | $ | 0.35 | | $ | 0.43 | | |

| | | | |

| Total assets - Continuing and discontinued operations | 14,136.2 | | 16,961.7 | | 18,374.0 | | |

| Long-term debt - Continuing and discontinued operations | 6,532.9 | | 8,047.5 | | 8,516.0 | | |

| | | | | |

| |

| |

| 1 | Reflects results of continuing operations unless marked otherwise (see Explanatory Notes). |

| 2 | See Caution Concerning Non-GAAP Measures. |

For the twelve months ended December 31, 2025, AQN reported revenue of $2,433.6 million as compared to $2,319.5 million in the comparative period, an increase of $114.1 million. This increase was mainly driven by the implementation of approved rates of $41.6 million, favourable weather which resulted in an increase in revenue of approximately $13.9 million at the Empire Electric System, as well as higher pass-through costs driven by increased commodity prices.

The following table outlines the changes to Adjusted Net Earnings1 for the twelve months ended December 31, 2025 as compared to the same period in 2024, including the breakdown of net earnings attributable to common shareholder by the Company's main business units, and the discussion below outlines the changes to net earnings attributable to common shareholders:

| | | | | | | | | | | |

Net Earnings and Adjusted Net Earnings1 by business unit2 | Twelve months ended December 31 |

| (all dollar amounts in $ millions) | 2025 | 2024 | Change |

Net earnings for Regulated Services Group | $ | 351.0 | | $ | 260.1 | | $ | 90.9 | |

Net earnings for Hydro Group | 31.1 | | 12.0 | | 19.1 | |

Net loss for Corporate Group | (174.1) | | (217.3) | | 43.2 | |

Total Net Earnings | 208.0 | | 54.8 | | 153.2 | |

Add: Adjusted items | 50.8 | | 166.8 | | (116.0) | |

Total Adjusted Net Earnings1 | $ | 258.8 | | $ | 221.6 | | $ | 37.2 | |

| | | |

| | | |

| | | | | |

| |

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 14 |

| | | | | | | | | | | | | | |

Change in Net Earnings and Adjusted Net Earnings1 Breakdown2 | Twelve months ended December 31, 2025 |

| (all dollar amounts in $ millions) | Regulated Services | Hydro | Corporate | Total |

Change in Net Earnings attributable to common shareholders | | | | |

Net earnings (loss) attributable to common shareholders- Prior period balances | $ | 260.1 | | $ | 12.0 | | $ | (217.3) | | $ | 54.8 | |

EBIT1 | | | | |

Electricity | 14.4 | | — | | — | | 14.4 | |

Natural Gas | 35.9 | | — | | — | | 35.9 | |

Water | 11.8 | | — | | — | | 11.8 | |

Other | 9.2 | | (0.2) | | (118.4) | | (109.4) | |

Total change in EBIT1 | 71.3 | | (0.2) | | (118.4) | | (47.3) | |

| | | | |

Interest expense | 50.4 | | — | | 30.7 | | 81.1 | |

Income tax expense | (29.2) | | 20.1 | | 130.9 | | 121.8 | |

Net effect of non-controlling interests | (1.6) | | (0.8) | | — | | (2.4) | |

Total change in net earnings | 90.9 | | 19.1 | | 43.2 | | 153.2 | |

| | | | |

Net earnings (loss) attributable to common shareholders - Current period balances | 351.0 | | 31.1 | | (174.1) | | 208.0 | |

| | | | |

Change in Adjusted Net Earnings1 | | | | |

Adjusted Net Earnings (Loss)1 - Prior period balance3 | 260.1 | | 12.0 | | (50.5) | | 221.6 | |

Total change in net earnings | 90.9 | | 19.1 | | 43.2 | | 153.2 | |

Total change in adjusted items3 | — | | — | | (116.0) | | (116.0) | |

Adjusted Net Earnings (loss)1 - Current period balances | $ | 351.0 | | $ | 31.1 | | $ | (123.3) | | $ | 258.8 | |

| | | | | |

| |

| |

| 1 | See Caution Concerning Non-GAAP Measures. |

| 2 | Reflects results of continuing operations unless marked otherwise (see Explanatory Notes). |

| 3 | See Corporate Group Net Earnings and Adjusted Net Earnings. |

For the twelve months ended December 31, 2025, AQN reported net earnings attributable to common shareholders of $208.0 million and basic net earnings per common share of $0.27. During the comparative period in 2024, the Company reported net earnings attributable to common shareholders of $54.8 million and basic net earnings per common share of $0.07. The net earnings attributable to common shareholders increased by $153.2 million, and basic net earnings per common share increase by $0.20. The increases were primarily driven by:

•an increase of $90.9 million in the net earnings of the Regulated Services Group, primarily due to:

–an increase in net earnings of $105.9 million primarily due to the implementation of approved rates of $41.6 million, favourable weather normalization, which resulted in an increase in net earnings of $13.9 million, and lower interest expense of $50.4 million as a result of the repayment of debt with the proceeds from the Renewables Sale and the proceeds from the sale of the Company’s investment in Atlantica; partially offset by;

–a decrease in net earnings of $14.8 million primarily due to higher depreciation of $5.3 million due to higher organic depreciation, net of $11.9 million due to depreciation deferral adjustments related to the Granite State Electric and EnergyNorth Gas Systems, lower net operating expenses of $2.2 million due to lower labour and maintenance expenses across all systems, partially offset by a targeted relief initiative for customers of $8.5 million agreed to as part of the Empire District Electric System (MO) rate case settlement, and a write-off of $7.3 million related to the discontinuation of a solar project at the CalPeco Electric System.

•an increase of $19.1 million in the net earnings of the Hydro Group primarily due to a tax recovery; and

•an increase in the net earnings of the Corporate Group of $43.2 million, primarily due to:

| | | | | |

| |

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | |

–an increase in net earnings of $161.6 million primarily due to a decrease in income tax expense of $130.9 million primarily driven by valuation allowance recorded in 2024 on Canadian deferred tax assets and the effect from the restructuring of certain intercompany financing arrangements which were executed in advance of the implementation of global minimum tax rules in the various jurisdictions in which the Company operates, as well as a $30.7 million decrease in interest expense as a result of the repayment of debt with the proceeds of the Renewables Sale and the proceeds from the sale of the Company's investment in Atlantica; partially offset by;

–a decrease in net earnings of $97.7 million primarily driven by a $21.4 million fair value mark to market gain recorded in 2024, a decrease of $76.3 million owing to decreased dividends received from the Company’s investment in Atlantica, which was sold in the fourth quarter of 2024, and an increase of $18.4 million in foreign exchange losses due to fluctuations in USD-CAD exchange rates.

•The above increases were offset by common share dilution upon the issuance of 77,293,314 common shares in the second quarter of 2024, which issuance was almost entirely due to common shares that were issued in connection with the settlement of the purchase contracts that were a component of the Company's equity units.

For the twelve months ended December 31, 2025, AQN reported Adjusted Net Earnings per common share of $0.34 as compared to $0.30 per common share during the same period in 2024, an increase of $0.04 (see Caution Concerning Non-GAAP Measures). Adjusted Net Earnings per common share exceeded the top end of Company’s previously provided guidance range by $0.02. This was driven by accelerated realization of operating expense savings, lower depreciation expense resulting from authorized deferrals, and tax adjustments. These benefits were partially offset by costs associated with a targeted relief initiative for customers agreed to as part of the Empire District Electric System (MO) settlement as well as costs associated with the discontinuation of a solar project at the CalPeco Electric System. Adjusted Net Earnings increased by $37.2 million year over year (see Caution Concerning Non-GAAP Measures). This increase was primarily driven by the factors noted above, excluding the impact of the $21.4 million fair value mark to market gain (See Reconciliation of Adjusted Net Earnings to Net Earnings).

For the twelve months ended December 31, 2025, cash provided by operating activities increased by $111.9 million as compared to the same period in 2024, primarily due to changes in working capital items of $93.8 million (See Note 16 to the audited consolidated financial statements - Non Cash Operating Items); partially offset by an increase in net earnings. Cash flow provided by investing activities increased by $1,030.6 million mainly due to proceeds received from the Renewables Sale and the sale of the Company's investment in Atlantica. These proceeds were used for the repayment of debt, which was the primary factor leading to an increase of $1,254.8 million in the cash flow used in financing activities.

| | | | | |

| |

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | |

REGULATED SERVICES GROUP

The Regulated Services Group primarily operates rate-regulated utilities that as of December 31, 2025 provided electric generation and transmission services as well as distribution services in the electric, natural gas and water and wastewater sectors to approximately 1,272,000 customer connections, which is an increase of approximately 7,000 customer connections as compared to December 31, 2024.

The Regulated Services Group seeks to deliver long-term growth within its service territories, including through the pursuit of capital investment opportunities and other initiatives.

| | | | | | | | | | | | | | | | | | | | | | | |

| Utility System Type | As at December 31 |

| 2025 | | 2024 |

| (all dollar amounts in $ millions) | Assets | Net Utility Sales1 | Total Customer Connections2 | | Assets | Net Utility Sales1 | Total Customer Connections2 |

| Electricity | 5,566.5 | | 934.9 | | 311,000 | | | 5,454.5 | | 910.4 | | 310,000 | |

| Natural Gas | 2,018.1 | | 387.4 | | 378,000 | | | 1,921.4 | | 363.2 | | 378,000 | |

| Water and Wastewater | 1,895.4 | | 400.0 | | 583,000 | | | 1,786.3 | | 378.0 | | 577,000 | |

| Other | 98.6 | | 32.3 | | | | 122.2 | | 30.5 | | |

| Other revenue | | 60.7 | | | | | 54.0 | | |

| Less: Cost of Sales | | (28.4) | | | | | (23.5) | | |

| Total | $ | 9,578.6 | | $ | 1,754.6 | | 1,272,000 | | | $ | 9,284.4 | | $ | 1,682.1 | | 1,265,000 | |

| | | | | | | |

| Accumulated Deferred Income Taxes Liability | $ | 929.4 | | | | | $ | 833.6 | | | |

| | | | | |

| 1 | Net Utility Sales for the twelve months ended December 31, 2025 and 2024. See Caution Concerning Non-GAAP Measures. |

| 2 | Total Customer Connections represents the sum of all active and vacant customer connections. |

| |

The Regulated Services Group aggregates the performance of its utility operations by utility system type – electricity, natural gas, and water and wastewater systems.

The electric distribution, generation and transmission systems are comprised of regulated electrical distribution utility systems that served approximately 311,000 customer connections in the U.S. States of Arkansas, California, Kansas, Missouri, New Hampshire and Oklahoma, as well as in Bermuda as at December 31, 2025.

The natural gas distribution systems are comprised of regulated natural gas distribution utility systems that served approximately 378,000 customer connections located in the U.S. States of Georgia, Illinois, Iowa, Massachusetts, Missouri, New Hampshire and New York, and in the Canadian Province of New Brunswick as at December 31, 2025.

The water and wastewater distribution systems are comprised of regulated water distribution and wastewater utility systems that served approximately 583,000 customer connections located in the U.S. States of Arizona, Arkansas, California, Illinois, Missouri, New York, and Texas, as well as in Chile, as at December 31, 2025.

| | | | | |

| |

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 17 |

2025 Fourth Quarter and Annual Usage Results

| | | | | | | | | | | | | | | | | | | | | | | |

| Electric Distribution Systems | Three months ended December 31 | | Twelve months ended December 31 |

| | 2025 | | 2024 | | 2025 | | 2024 |

| Average Active Electric Customer Connections For The Period | | | | | | | |

| Residential | 263,500 | | | 263,300 | | | 263,400 | | | 263,400 | |

| Commercial and industrial | 43,500 | | | 43,200 | | | 43,400 | | | 43,000 | |

| Total Average Active Electric Customer Connections For The Period | 307,000 | | | 306,500 | | | 306,800 | | | 306,400 | |

| | | | | | | |

| Customer Usage (GW-hrs) | | | | | | | |

| Residential | 653.3 | | | 583.3 | | | 2,858.2 | | | 2,777.5 | |

| Commercial and industrial | 922.9 | | | 954.6 | | | 3,856.2 | | | 3,866.7 | |

| Total Customer Usage (GW-hrs) | 1,576.2 | | | 1,537.9 | | | 6,714.4 | | | 6,644.2 | |

For the three months ended December 31, 2025, the electric distribution systems' usage totaled 1,576.2 GW-hrs as compared to 1,537.9 GW-hrs for the same period in 2024, an increase of 38.3 GW-hrs or 2.5%. The increase in electricity consumption is primarily due to favourable weather at the Empire District Electric System.

For the twelve months ended December 31, 2025, the electric distribution systems' usage totaled 6,714.4 GW-hrs as compared to 6,644.2 GW-hrs for the same period in 2024, an increase of 70.2 GW-hrs or 1.1%. The increase in electricity consumption is primarily due to favourable weather and customer growth at the Empire District Electric System.

| | | | | | | | | | | | | | | | | | | | | | | |

| Natural Gas Distribution Systems | Three months ended December 31 | | Twelve months ended December 31 |

| 2025 | | 2024 | | 2025 | | 2024 |

| Average Active Natural Gas Customer Connections For The Period | | | | | | | |

| Residential | 322,100 | | | 322,700 | | | 322,700 | | | 323,000 | |

| Commercial and industrial | 40,300 | | | 40,300 | | | 40,300 | | | 40,000 | |

| Total Average Active Natural Gas Customer Connections For The Period | 362,400 | | | 363,000 | | | 363,000 | | | 363,000 | |

| | | | | | | |

| Customer Usage (MMBTU) | | | | | | | |

| Residential | 5,182,000 | | | 4,941,000 | | | 20,789,000 | | | 19,770,000 | |

| Commercial and industrial | 6,864,000 | | | 5,114,000 | | | 22,799,000 | | | 20,301,000 | |

| Total Customer Usage (MMBTU) | 12,046,000 | | | 10,055,000 | | | 43,588,000 | | | 40,071,000 | |

For the three months ended December 31, 2025, usage at the natural gas distribution systems totaled 12,046,000 MMBTU as compared to 10,055,000 MMBTU during the same period in 2024, an increase of 1,991,000 MMBTU, or 19.8%. The increase is primarily due to favourable weather at all distributions systems.

For the twelve months ended December 31, 2025, usage at the natural gas distribution systems totaled 43,588,000 MMBTU as compared to 40,071,000 MMBTU during the same period in 2024, an increase of 3,517,000 MMBTU, or 8.8%. The increase is primarily due to favourable weather at all distributions systems.

| | | | | |

| |

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 18 |

| | | | | | | | | | | | | | | | | | | | | | | |

| Water and Wastewater Distribution Systems | Three months ended December 31 | | Twelve months ended December 31 |

| 2025 | | 2024 | | 2025 | | 2024 |

| Average Active Customer Connections For The Period | | | | | | | |

| Water distribution customer connections | 519,200 | | | 513,300 | | | 516,700 | | | 510,600 | |

| Wastewater customer connections | 55,700 | | | 55,600 | | | 55,800 | | | 55,700 | |

| Total Average Active Customer Connections For The Period | 574,900 | | | 568,900 | | | 572,500 | | | 566,300 | |

| | | | | | | |

| Gallons Provided (millions of gallons) | | | | | | | |

| Water provided | 9,747 | | | 10,204 | | | 41,153 | | | 39,747 | |

| Wastewater treated | 927 | | | 963 | | | 3,694 | | | 3,716 | |

| Total Gallons Provided (millions of gallons) | 10,674 | | | 11,167 | | | 44,847 | | | 43,463 | |

For the three months ended December 31, 2025, the water and wastewater distribution systems provided approximately 9,747 million gallons of water to customers and treated approximately 927 million gallons of wastewater. This is compared to 10,204 million gallons of water provided and 963 million gallons of wastewater treated during the same period in 2024, a decrease in total gallons provided of 457 million or 4.5% and a decrease in total gallons treated of 36 million or 3.7%. The decrease in water is primarily due lower usage at the Park Water and Litchfield Park Water Systems.

For the twelve months ended December 31, 2025, the water and wastewater distribution systems provided approximately 41,153 million gallons of water to customers and treated approximately 3,694 million gallons of wastewater. This is compared to 39,747 million gallons of water provided and 3,716 million gallons of wastewater treated during the same period in 2024, an increase in total gallons provided of 1,406 million or 3.5% and decrease in total gallons treated of 22 million or 0.6%. The increase in water is primarily due to favourable weather at the New York Water System.

| | | | | |

| |

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | |

2025 Fourth Quarter and Annual Regulated Services Group Net Earnings

| | | | | | | | | | | | | | | | | | | | | | | |

| Three months ended | | Twelve months ended |

| December 31 | | December 31 |

| (all dollar amounts in $ millions) | 2025 | | 2024 | | 2025 | | 2024 |

| Revenue | | | | | | | |

| Regulated electricity distribution | $ | 309.5 | | | $ | 304.6 | | | $ | 1,292.7 | | | $ | 1,276.1 | |

| Less: Regulated electricity purchased | (87.2) | | | (85.1) | | | (357.8) | | | (365.7) | |

Net Utility Sales – electricity1 | 222.3 | | | 219.5 | | | 934.9 | | | 910.4 | |

| Regulated gas distribution | 191.1 | | | 152.5 | | | 614.4 | | | 546.4 | |

| Less: Regulated gas purchased | (82.1) | | | (51.1) | | | (227.0) | | | (183.2) | |

Net Utility Sales – natural gas1 | 109.0 | | | 101.4 | | | 387.4 | | | 363.2 | |

| Regulated water reclamation and distribution | 103.0 | | | 104.0 | | | 426.6 | | | 406.1 | |

| Less: Regulated water purchased | (6.2) | | | (8.4) | | | (26.6) | | | (28.1) | |

Net Utility Sales – water reclamation and distribution1 | 96.8 | | | 95.6 | | | 400.0 | | | 378.0 | |

| | | | | | | |

Other revenue2 | 17.8 | | | 15.8 | | | 60.7 | | | 54.0 | |

Less: Other Cost of Sales | (8.4) | | | (7.6) | | | (28.4) | | | (23.5) | |

Net Utility Sales1,3 | 437.5 | | | 424.7 | | | 1,754.6 | | | 1,682.1 | |

| Operating expenses | 224.1 | | | 221.7 | | | 853.9 | | | 855.2 | |

| Depreciation and amortization | 101.3 | | | 97.6 | | | 392.1 | | | 386.8 | |

| Interest, dividend and other income | 7.4 | | | 10.1 | | | 28.8 | | | 33.4 | |

Other expenses | | | | | | | |

| Pension and post-employment non-service costs | $ | (1.9) | | | $ | (3.7) | | | (3.7) | | | $ | (14.1) | |

Other net losses | $ | (16.3) | | | $ | (10.3) | | | (30.4) | | | $ | (17.8) | |

| Gain/(Loss) on derivative financial instruments | $ | (0.3) | | | $ | 0.4 | | | 8.9 | | | $ | (0.7) | |

EBIT1,4 | $ | 101.0 | | | $ | 101.9 | | | $ | 512.2 | | | $ | 440.9 | |

| Interest expense | (36.0) | | | (46.6) | | | (141.4) | | | (191.8) | |

| Income tax expense | $ | (13.9) | | | $ | (15.3) | | | (96.2) | | | (67.0) | |

Net effect of non-controlling interests6 | $ | 22.5 | | | $ | 20.5 | | | 76.4 | | | 78.0 | |

| Net Earnings | $ | 73.6 | | | $ | 60.5 | | | $ | 351.0 | | | $ | 260.1 | |

| | | | | |

| 1 | See Caution Concerning Non-GAAP Measures. |

| 2 | See Note 19 in the audited consolidated financial statements. |

| 3 | This table contains a reconciliation of Net Utility Sales to revenue for the Regulated Services Group. The relevant sections of the table are derived from and should be read in conjunction with the audited consolidated statement of operations and Note 19 in the audited consolidated financial statements, "Segmented Information". This supplementary disclosure is intended to more fully explain disclosures related to Net Utility Sales and provides additional information related to the operating performance of the Regulated Services Group. Investors are cautioned that Net Utility Sales should not be construed as an alternative to revenue. |

| 4 | This table contains a reconciliation of EBIT to net earnings for the Regulated Services Group. The relevant sections of the table are derived from and should be read in conjunction with the audited consolidated statement of operations and Note 19 in the audited consolidated financial statements, "Segmented Information". This supplementary disclosure is intended to more fully explain disclosures related to EBIT and provides additional information related to the operating performance of the Regulated Services Group. Investors are cautioned that EBIT should not be construed as an alternative to net earnings. |

| 6 | Net effect of non-controlling interests primarily includes HLBV income from Empire Electric. |

| |

| | | | | |

| |

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 20 |

2025 Fourth Quarter Regulated Services Group Operating Results

For the three months ended December 31, 2025, the Regulated Services Group reported revenue of $603.6 million (comprised of $309.5 million of regulated electricity distribution, $191.1 million of regulated gas distribution and $103.0 million of regulated water reclamation and distribution) as compared to revenue of $561.1 million in the comparable period in the prior year (comprised of $304.6 million of regulated electricity distribution, $152.5 million of regulated gas distribution and $104.0 million of regulated water reclamation and distribution).

For the three months ended December 31, 2025, the Regulated Services Group reported net earnings of $73.6 million as compared to $60.5 million for the comparable period in the prior year.

Highlights of the changes are summarized in the following table:

| | | | | |

| (all dollar amounts in $ millions) | Three months ended December 31 |

Prior Period Net Earnings | $ | 60.5 | |

| |

Regulated Services Group EBIT1: | |

Electricity: Decrease is primarily due to: –favourable weather, which resulted in an increase to net earnings of approximately $5.4 million –lower operating expenses of approximately $9.7 million, including a $4.0 million favourable impact from an adjustment recorded in 2024 (benefiting the fourth quarter of 2024), with the remaining decrease driven by lower labour and maintenance expenses

More than offset by: –additional expense of $8.5 million in respect of a targeted relief initiative for customers of agreed to as part of the Empire District Electric System (MO) rate case settlement –unrecoverable fuel costs of approximately $2.3 million at the Empire District Electric System –a write-off of $7.3 million related to the discontinuation of a solar project at the CalPeco Electric System | (4.7) | |

Gas: Increase is primarily due to: –the implementation of approved rates of $4.0 million at Midstates (MO) and Peach State (GA) Gas Systems –higher net revenue of approximately $2.0 million due to billing cycle changes at the Midstates (MO) Gas System –net items totaling $4.8 million recorded in the fourth quarter of 2024, primarily related to the EnergyNorth (NH) and Empire District (MO) Gas Systems.

Partially offset by: –items totaling $3.5 million, consisting of a $1.0 million fuel inventory write-off at the Midstates (MO) Gas System and $2.5 million of operating expenses associated with the Lexington gas incident | 6.4 | |

Water: Decrease is primarily due to: –the implementation of approved rates of $4.2 million at the New York (NY), Missouri Water (MO), Bella Vista (AZ), Beardsley (AZ), Cordes Lake (AZ) Water System and Rio Rico (AZ) Water and Sewer System

More than offset by: –higher depreciation expense of $3.2 million due to organic growth –lower revenue at the New York (NY) Water system of approximately $1.0 million related to timing | (1.0) | |

Other: decrease primarily due to non-recurring expenses | (1.6) | |

Interest expense: Decrease primarily due to the repayment of debt with the proceeds of the Renewables Sale and the sale of the Company's investment in Atlantica which were partially pushed down into the Regulated Services Group | 10.6 | |

Income tax expense: Lower income tax expense primarily due to tax adjustment recorded during the quarter as a result of the enacted Tax Credits Act 2025 in Bermuda | 1.4 | |

Net effect of non-controlling interests: Increase due to higher wind production resulting in higher HLBV | 2.0 | |

Current Period Net Earnings | $ | 73.6 | |

| | | | | |

| 1 | See Caution Concerning Non-GAAP Measures. |

| | | | | |

| |

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 21 |

2025 Annual Regulated Services Group Operating Results

For the twelve months ended December 31, 2025, the Regulated Services Group reported revenue of $2,333.7 million (comprised of $1,292.7 million of regulated electricity distribution revenue, $614.4 million of regulated natural gas distribution revenue and $426.6 million of regulated water reclamation and distribution revenue) as compared to revenue of $2,228.6 million in the same period in the prior year (comprised of $1,276.1 million of regulated electricity distribution revenue, $546.4 million of regulated natural gas distribution revenue and $406.1 million of regulated water reclamation and distribution revenue).

For the twelve months ended December 31, 2025, the Regulated Services Group reported net earnings of $351.0 million as compared to $260.1 million in the comparable period in the prior year.

Highlights of the changes are summarized in the following table:

| | | | | |

| (all dollar amounts in $ millions) | Twelve months ended December 31 |

| Prior Period Net Earnings | $ | 260.1 | |

| |

Regulated Services Group EBIT1: | |

Electricity: Increase is primarily due to: –a $5.5 million true-up recorded in the first quarter of 2024 at the Empire District Electric System –favourable weather, which resulted in an increase of net earnings of approximately $13.9 million at the Empire District Electric System –the implementation of approved rates at the BELCO Electric System of $6.3 million (2024 approved rates were effective in the second quarter of 2024) –lower operating expenses of approximately $11.0 million including $4.0 million favourable impact from an adjustment recorded in 2024, with the remaining decrease driven by lower labour and maintenance expenses

Partially offset by: –additional expense of $8.5 million in respect of a targeted relief initiative for customers agreed to as part of the Empire District Electric System (MO) rate case settlement –a write-off of $7.3 million related to the discontinuation of a solar project at the CalPeco Electric System –higher depreciation across all utilities of $5.6 million partially offset by a depreciation deferral adjustment of $4.8 million related to Granite State Electric System –lower interest income on regulatory asset accounts of approximately $3.0 million | 14.4 | |

Gas: Increase is primarily due to: –the implementation of approved rates of $16.8 million at the Midstates (MO) and Peach State (GA) Gas Systems –higher net revenue of $1.9 million from the Gas System Enhancement Program at the New England (MA) Gas System –lower bad debt expense of $6.9 million –a depreciation deferral adjustment of $7.1 million related to the EnergyNorth (NH) Gas System in 2025 and a depreciation adjustment in 2024 at the Peach State (GA) Gas System of $1.9 million, partly offset by higher depreciation across the majority of gas systems of $6.2 million –increase in other income of $5.6 million at the Empire (MO) Gas System relating to a rate case adjustment due to over-amortization of pension and Other Post-Employment Benefits balance –a write-off of $6.8 million at the EnergyNorth (NH) Gas System in the fourth quarter of 2024

Partially offset by: –expenses of approximately $3.2 million relating to the Lexington gas incident –higher property taxes of approximately $3.1 million | 35.9 | |

| | | | | |

| |

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 22 |

| | | | | |

| (all dollar amounts in $ millions) | Twelve months ended December 31 |

Water: Increase is primarily due to: –the implementation of approved rates of $18.5 million at the Arkansas (AR), Missouri Water (MO), New York (NY) (2024 approved rates were effective to the third quarter of 2024, retroactive to the second quarter of 2024) and Bella Vista (AZ), Beardsley (AZ), Cordes Lake (AZ) Water Systems and Rio Rico (AZ) Water and Sewer System –lower operating expenses of approximately $6.5 million at the New York Water (NY) Water System primarily due to lower labour expenses and a write off of $1.7 million recorded in 2024

Partially offset by: –higher depreciation expenses of $7.0 million –rate case adjustment of $3.3 million at the Litchfield Park (AZ) Water and Sewer System –lower interest income of approximately $1.2 million | 11.8 | |

Other: Increase is primarily due to the gain of $9.1 million on the settlement of a swap at the BELCO Electric System | 9.2 | |

Interest expense: Decrease primarily due to the repayment of debt with the proceeds of the Renewables Sale and the sale of the Company's investment in Atlantica which were partially pushed down into the Regulated Services Group | 50.4 | |

| Income tax expense: Increase primarily due to higher earnings before tax | (29.2) | |

Net effect of non-controlling interests: Decrease primarily due to lower wind production resulting in lower HLBV | (1.6) | |

| Current Period Net Earnings | $ | 351.0 | |

1 See Caution Concerning Non-GAAP Measures. | |

| | | | | |

| |

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | |

Regulatory Proceedings

The following table summarizes the major regulatory proceedings currently underway or completed or effective in 2025 within the Regulated Services Group.