![]()

Year Ended December 31, 2025

| INTRODUCTION |

The following Management's Discussion and Analysis ("MD&A") of IAMGOLD Corporation ("IAMGOLD" or the "Company"), dated February 17, 2026, should be read in conjunction with IAMGOLD's audited consolidated financial statements and related notes as at and for the fiscal year ended December 31, 2025. All figures in this MD&A are in U.S. dollars and tabular dollar amounts are in millions, unless stated otherwise. Additional information on IAMGOLD can be found at www.iamgold.com. However, the information on the website is not in any way incorporated in or made a part of this MD&A.

| ABOUT IAMGOLD |

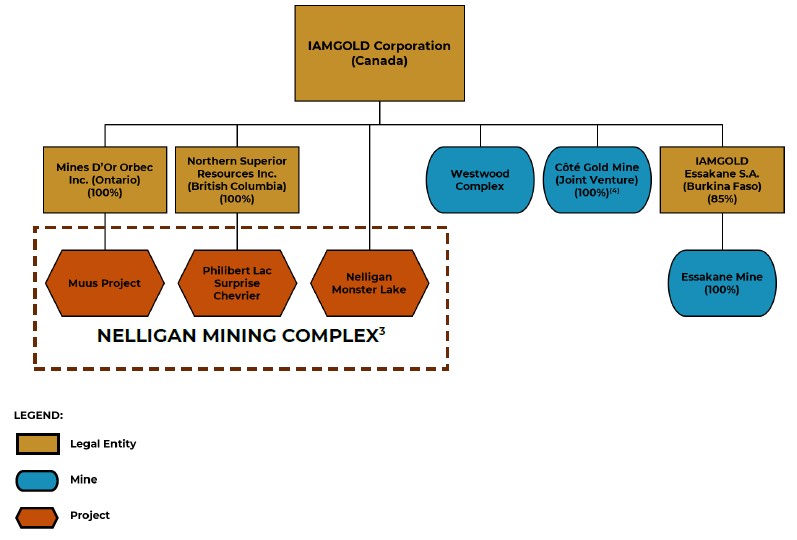

IAMGOLD is an intermediate gold producer and developer based in Canada with operating mines in North America and West Africa, including Côté Gold (Canada), Westwood (Canada) and Essakane (Burkina Faso). The Côté Gold Mine ("Côté" or "Côté Gold") is among the largest gold mines in production in Canada, which IAMGOLD operates in a 70|30 partnership with Sumitomo Metal Mining Co. Ltd. ("SMM"). In addition, the Company has an established portfolio of early stage and advanced exploration projects within high potential mining districts, including the large-scale Nelligan Mining Complex located in Quebec, Canada.

IAMGOLD employs approximately 3,700 people and is committed to maintaining its culture of accountable mining through high standards of Environmental, Social and Governance ("ESG") practices. IAMGOLD is listed on the New York Stock Exchange (NYSE:IAG) and the Toronto Stock Exchange (TSX:IMG).

| HIGHLIGHTS |

Operating and financial results

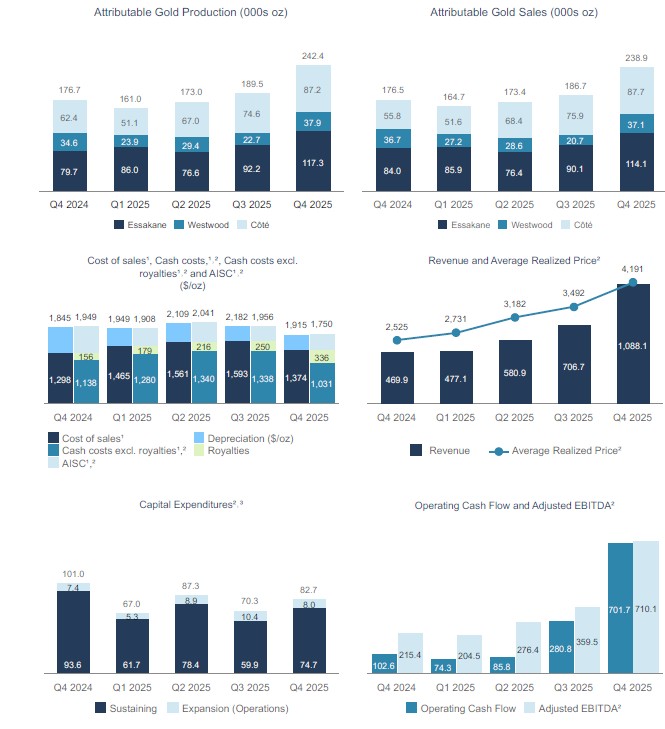

• Attributable gold production for the fourth quarter was 242,400 ounces and 765,900 ounces for the year, achieving the mid-point of the Company's 2025 production guidance of 735,000 to 820,000 ounces, following record quarterly production at all of its operations, including at Côté Gold which achieved the top end of its guidance target.

• Côté produced a record 87,200 attributable ounces (124,600 ounces | 100%) in the fourth quarter, and 279,900 attributable ounces (399,800 ounces | 100%) for the full year, achieving the top end of the attributable 2025 production guidance range of 250,000 to 280,000 ounces (360,000 to 400,000 ounces | 100%).

• Westwood produced a record 37,900 ounces in the fourth quarter and 113,900 ounces for the full year, below the bottom end of the 2025 guidance range of 125,000 to 140,000 ounces.

• Essakane produced 117,300 attributable ounces (a record 138,100 ounces | 100%) in the fourth quarter and 372,100 attributable ounces (427,200 ounces | 100%) for the full year, exceeding the mid-point of the production guidance range on a 100% basis.

• Revenues in the fourth quarter totaled $1,088.1 million from sales of 259,000 ounces at an average realized gold price of $4,191 per ounce1. For the year, revenues were $2,852.8 million from sales of 817,800 ounces at an average realized gold price of $3,482 per ounce1. The average realized gold price for the year ended 2025, excluding the impact of the 2024 gold prepay arrangement, was $3,549 per ounce (see "Financial Condition - Gold prepay arrangements").

• Cost of sales per ounce sold was $1,374 for the fourth quarter and $1,489 for the year.

• Cash cost1 per ounce sold, excluding royalties, was $1,031 for the fourth quarter and $1,230 for the year.

• Cash cost1 per ounce sold, including royalties, was $1,367 for the fourth quarter and $1,484 for the year, compared to the guidance range of $1,375 to $1,475.

• AISC1 per ounce sold was $1,750 for the fourth quarter and $1,900 for the year, within the guidance range of $1,830 to $1,930.

• Net earnings and adjusted net earnings attributable to equity holders1 was $406.6 million and $405.8 million for the fourth quarter, and $664.4 million and $709.2 million for the year, respectively.

• Net earnings and adjusted net earnings per share attributable to equity holders1 of $0.70 and $0.70 for the fourth quarter, respectively; for the year, net earnings and adjusted net earnings per share attributable to equity holders1 of $1.16 and $1.23 respectively.

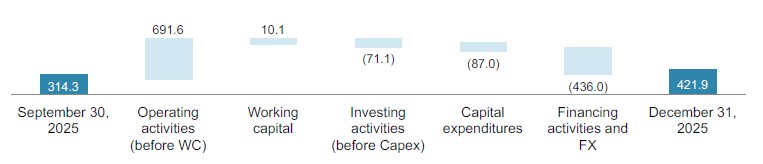

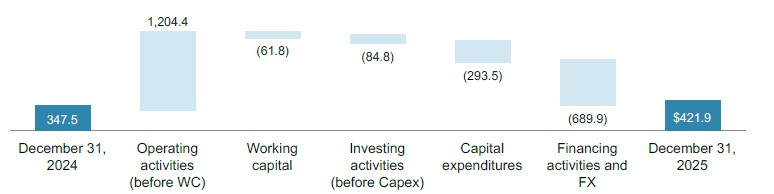

• Net cash from operating activities was $701.7 million for the fourth quarter, and $1,142.6 million for the year. Net cash from operating activities, before movements in working capital and non-current ore stockpiles1, was $691.6 million for the fourth quarter and $1,204.4 million for the year.

___________________________

1. This is a non-GAAP financial measure. See "Non-GAAP Financial Measures".

• Earnings before interest, income taxes, depreciation and amortization ("EBITDA")1 was $685.5 million for the fourth quarter and $1,502.9 million for the year, and Adjusted EBITDA1 was $710.1 million for the fourth quarter and $1,550.5 million for the year.

• Record mine-site free cash flow1 of $626.6 million for the fourth quarter and $1,199.0 million for the year, including attributable mine-site free cash flow from Côté of $197.0 million for the fourth quarter.

• The Company has available liquidity1 of $868.6 million, mainly comprised of cash and cash equivalents of $421.9 million and the available balance of the revolving credit facility ("Credit Facility") of $445.7 as at December 31, 2025. Net debt was $344.4 million at December 31, 2025, a reduction of $514.9 million during the year.

• In health and safety, for the year ended December 31, 2025, the Company reported a total recordable injuries frequency rate ("TRIFR") of 0.60 for the year, tracking below the prior year performance. IAMGOLD is continuing to advance its critical risk management and visible leadership to improve safety and reduce high-potential incidents.

2026 Outlook

• Total attributable production for IAMGOLD in 2026 is expected to be in the range of 720,000 to 820,000 ounces, as operations at Côté Gold focus on sustainable operations at nameplate operating rates ahead of the technical report outlining the expansion plans which is expected to be announced in the fourth quarter 2026.

• Cash costs1, excluding royalties, are expected to average $1,100 to $1,250 per ounce sold. With the current strong gold price environment, royalties account for an average of approximately $325 per ounce sold - based on a gold price assumption for 2026 of $4,000 per ounce. Cash costs1, including royalties, are expected to average $1,425 to $1,575 per ounce sold.

Mineral Reserves and Resources Update

• On February 17, 2026, IAMGOLD announced its updated Mineral Reserves and Resources statement as of December 31, 2025.

• Proven and Probable ("P&P") Mineral Reserves (100% basis) total 9.9 million ounces of gold in 279.6 million tonnes ("Mt") at 1.10 g/t Au (7.5 million ounces attributable). P&P Mineral Reserves decreased 7%, or 796,000 ounces, from the prior year, primarily due to depletion at Côté Gold and Essakane partially offset by an increase in Mineral Reserves at Westwood.

• Measured and Indicated ("M&I") Mineral Resources (100% basis) increased 16% to 31.0 million ounces of gold in 1.0 billion tonnes ("Bt") at 0.94 g/t Au (24.6 million ounces attributable). The increase was primarily associated with the conversion of Inferred Mineral Resources in the Gosselin deposit at Côté Gold and Nelligan deposit, coupled with the inclusion of the Philibert and Chevrier deposits as part of the Northern Superior transaction towards the end of the year.

Corporate

• Allocated $400 million of free cash flows generated in the fourth quarter to repay the remaining balance of $300 million of the second lien term loan, repay $50 million of the Credit Facility and purchased 3 million shares for $50 million as part of the share buyback program. Subsequent to quarter end, the Company has purchased an additional 2.6 million shares for $50 million. Essakane's attributable free cash flow for 2026 is expected to be approximately $400 to $500 million at a $4,000 per ounce gold price. The Company intends to use this free cash flow to repurchase shares under its share buyback program as the cash is generated and repatriated from Essakane over the course of 2026.

• $291 million of cash was repatriated from Essakane in the fourth quarter and an additional $171 million subsequent to quarter end, using the new structure that enables payments to be made at any time of the year based on the cash generated in excess of working capital requirements by Essakane.

• Consolidation of Nelligan Mining Complex with the closing of the previously announced acquisitions of all of the issued and outstanding shares of each of Northern Superior Resources Inc. ("Northern Superior") and Mines d'Or Orbec Inc. ("Orbec") by way of a plan of arrangement on December 19, 2025, and December 22, 2025, respectively. The transactions consolidated the Chibougamau region with a dominant land position of approximately 134,000 hectares. The Northern Superior acquisition with the Philibert, Chevrier and Croteau2 projects together with Orbec acquisition with the Muus project are combined with IAMGOLD's Nelligan and Monster Lake Projects (together, the "Nelligan Mining Complex"). The newly combined assets, together, rank as one of the largest pre-production gold camps in Canada with Measured and Indicated Mineral Resources of 4.3 million ounces ("Moz Au") and Inferred Mineral Resources of 7.5 Moz Au. The close proximity of the primary deposits to each other supports the conceptual vision of a central processing facility being fed from multiple ore sources within a 17-kilometre radius.

____________________________

1. This is a non-GAAP financial measure. See "Non-GAAP Financial Measures".

2. At the time of the Northern Superior acquisition, disclosed estimates were 3.75 Moz Au Measured and Indicated Mineral Resources and 8.65 Moz Au Inferred Mineral Resources, which included Croteau. As at December 31, 2025, the Company opted to exclude the mineral resources previously associated with the Croteau property in its year end update, resulting in reported totals of 4.34 Moz Au Measured and Indicated Mineral Resources and 7.50 Moz Au Inferred Mineral Resources.

| OPERATING AND FINANCIAL RESULTS |

For more details and the Company's overall outlook for 2026, see "Outlook", and for individual mines performance, see "Operations". The following table summarizes certain operating and financial results for the three months ended December 31, 2025 (Q4 2025), December 31, 2024 (Q4 2024) and the years ended December 31 for 2025, 2024 and 2023.

| Q4 2025 | Q4 2024 | 2025 | 2024 | 2023 | |||||||||||

| Key Operating Statistics | |||||||||||||||

| ($ millions) | |||||||||||||||

| Gold production - attributable (000s oz) | 242.4 | 176.7 | 765.9 | 666.5 | 465.0 | ||||||||||

| - Côté Gold1 | 87.2 | 62.4 | 279.9 | 124.0 | - | ||||||||||

| - Westwood | 37.9 | 34.6 | 113.9 | 133.7 | 93.4 | ||||||||||

| - Essakane2 | 117.3 | 79.7 | 372.1 | 408.8 | 371.6 | ||||||||||

| Gold sales - attributable (000s oz) | 238.9 | 176.5 | 763.7 | 653.7 | 462.1 | ||||||||||

| - Côté Gold1 | 87.7 | 55.8 | 283.6 | 111.1 | - | ||||||||||

| - Westwood | 37.1 | 36.7 | 113.6 | 133.9 | 90.2 | ||||||||||

| - Essakane2 | 114.1 | 84.0 | 366.5 | 408.7 | 371.9 | ||||||||||

| Cost of sales3 ($/oz sold) | $ | 1,374 | $ | 1,298 | $ | 1,489 | $ | 1,156 | $ | 1,291 | |||||

| - Côté Gold1 | $ | 1,271 | $ | 1,083 | $ | 1,272 | $ | 1,035 | $ | - | |||||

| - Westwood | $ | 1,307 | $ | 1,155 | $ | 1,547 | $ | 1,177 | $ | 1,600 | |||||

| - Essakane2 | $ | 1,475 | $ | 1,504 | $ | 1,640 | $ | 1,182 | $ | 1,216 | |||||

| Cash costs4 - excluding royalties ($/oz sold) | $ | 1,031 | $ | 1,138 | $ | 1,230 | $ | 1,007 | $ | 1,158 | |||||

| - Côté Gold1 | $ | 949 | $ | 902 | $ | 1,020 | $ | 875 | $ | - | |||||

| - Westwood | $ | 1,288 | $ | 1,148 | $ | 1,530 | $ | 1,164 | $ | 1,588 | |||||

| - Essakane2 | $ | 1,011 | $ | 1,291 | $ | 1,300 | $ | 991 | $ | 1,053 | |||||

| Cash costs4 ($/oz sold) | $ | 1,367 | $ | 1,294 | $ | 1,484 | $ | 1,152 | $ | 1,261 | |||||

| - Côté Gold1 | $ | 1,265 | $ | 1,080 | $ | 1,268 | $ | 1,032 | $ | - | |||||

| - Westwood | $ | 1,288 | $ | 1,148 | $ | 1,530 | $ | 1,167 | $ | 1,591 | |||||

| - Essakane2 | $ | 1,471 | $ | 1,501 | $ | 1,636 | $ | 1,179 | $ | 1,181 | |||||

| AISC4 ($/oz sold) | $ | 1,750 | $ | 1,949 | $ | 1,900 | $ | 1,716 | $ | 1,783 | |||||

| - Côté Gold1 | $ | 1,688 | $ | 1,685 | $ | 1,636 | $ | 1,658 | $ | - | |||||

| - Westwood | $ | 1,719 | $ | 1,688 | $ | 2,117 | $ | 1,702 | $ | 2,344 | |||||

| - Essakane2 | $ | 1,674 | $ | 2,118 | $ | 1,888 | $ | 1,625 | $ | 1,521 | |||||

| Average realized gold price4,5 ($/oz) | $ | 4,191 | $ | 2,525 | $ | 3,482 | $ | 2,330 | $ | 1,955 |

1. Attributable portion for Côté Gold is based on IAMGOLD's ownership of 70%. Prior to November 30, 2024, IAMGOLD's attributable portion was 60.3%. See "Operations - Côté Gold, Canada" for more details.

2. IAMGOLD's Essakane ownership interest decreased from 90% to 85% effective June 20, 2025. See "Operations - Essakane, Burkina Faso" for more details. The attributable portion for Essakane is presented as 90% for the first half of 2025 and 85% for the second half of 2025 throughout this MD&A.

3. Throughout this MD&A, cost of sales, excluding depreciation, and cost of sales, excluding depreciation and royalties are disclosed in the segment note in the consolidated financial statements.

4. Refer to the "Non-GAAP Financial Measures" disclosure at the end of this MD&A for a description and calculation of these measures.

5. All prepay delivery obligations were completed by the end of the second quarter 2025. The average realized gold price for the year ended 2025, excluding the impact of the 2024 prepay arrangement (see "Financial Condition - Gold prepay arrangements"), was $3,549 per ounce.

| Q4 2025 | Q4 2024 | 2025 | 2024 | 2023 | ||||||||||||

| Financial Results | ||||||||||||||||

| ($ millions) | ||||||||||||||||

| Revenues | $ | 1,088.1 | $ | 469.9 | $ | 2,852.8 | $ | 1,633.0 | $ | 987.1 | ||||||

| Gross profit | $ | 593.6 | $ | 130.9 | $ | 1,206.2 | $ | 549.9 | $ | 124.1 | ||||||

| EBITDA1 | $ | 685.5 | $ | 259.5 | $ | 1,502.9 | $ | 1,323.0 | $ | 381.0 | ||||||

| - Continuing operations | $ | 685.5 | $ | 259.5 | $ | 1,502.9 | $ | 1,323.0 | $ | 366.6 | ||||||

| - Discontinued operations | $ | - | $ | - | $ | - | $ | - | $ | 14.4 | ||||||

| Adjusted EBITDA1 | $ | 710.1 | $ | 215.4 | $ | 1,550.5 | $ | 780.6 | $ | 338.5 | ||||||

| - Continuing operations | $ | 710.1 | $ | 215.4 | $ | 1,550.5 | $ | 780.6 | $ | 315.1 | ||||||

| - Discontinued operations | $ | - | $ | - | $ | - | $ | - | $ | 23.4 | ||||||

| Net earnings (loss) attributable to equity holders | $ | 406.6 | $ | 86.2 | $ | 664.4 | $ | 819.6 | $ | 94.3 | ||||||

| - Continuing operations | $ | 406.6 | $ | 86.2 | $ | 664.4 | $ | 819.6 | $ | 88.7 | ||||||

| - Discontinued operations | $ | - | $ | - | $ | - | $ | - | $ | 5.6 | ||||||

| Adjusted net earnings (loss) attributable to equity holders1 | $ | 405.8 | $ | 57.2 | $ | 709.2 | $ | 296.0 | $ | 59.3 | ||||||

| - Continuing operations | $ | 405.8 | $ | 57.2 | $ | 709.2 | $ | 296.0 | $ | 44.7 | ||||||

| - Discontinued operations | $ | - | $ | - | $ | - | $ | - | $ | 14.6 | ||||||

| Net earnings (loss) per share attributable to equity holders | $ | 0.70 | $ | 0.15 | $ | 1.16 | $ | 1.52 | $ | 0.18 | ||||||

| to equity holders1 | $ | 0.70 | $ | 0.10 | $ | 1.23 | $ | 0.55 | $ | 0.09 | ||||||

| Net cash from operating activities before changes in working capital1 - continuing operations | $ | 691.6 | $ | 127.2 | $ | 1,204.4 | $ | 600.4 | $ | 158.9 | ||||||

| Net cash from operating activities | $ | 701.7 | $ | 102.6 | $ | 1,142.6 | $ | 486.0 | $ | 159.4 | ||||||

| - Continuing operations | $ | 701.7 | $ | 102.6 | $ | 1,142.6 | $ | 486.0 | $ | 144.0 | ||||||

| - Discontinued operations | $ | - | $ | - | $ | - | $ | - | 15.4 | |||||||

| Mine-site free cash flow1 | $ | 626.6 | $ | 78.2 | $ | 1,199.0 | $ | 385.1 | $ | 54.1 | ||||||

| - Continuing operations | $ | 626.6 | $ | 78.2 | $ | 1,199.0 | $ | 385.1 | $ | 48.2 | ||||||

| - Discontinued operations | $ | - | $ | - | $ | - | $ | - | $ | 5.9 | ||||||

| Capital expenditures1,2 - sustaining | $ | 74.7 | $ | 93.6 | $ | 274.7 | $ | 290.8 | $ | 200.3 | ||||||

| Capital expenditures1,2 - expansion | $ | 8.0 | $ | 7.4 | $ | 32.6 | $ | 196.1 | $ | 656.8 | ||||||

| December 31 | December 31 | December 31 | ||||||||

| 2025 | 2024 | 2023 | ||||||||

| Financial Position ($ millions) | ||||||||||

| Cash and cash equivalents | $ | 421.9 | $ | 347.5 | $ | 367.1 | ||||

| Long-term debt | $ | 649.8 | $ | 1,028.9 | $ | 830.8 | ||||

| Net cash (debt)1 | $ | (344.4 | ) | $ | (859.3 | ) | $ | (649.5 | ) | |

| Available Credit Facility | $ | 445.7 | $ | 418.5 | $ | 387.0 | ||||

1. Refer to the "Non-GAAP Financial Measures" disclosure at the end of this MD&A for a description and calculation of these measures.

2. Sustaining and expansion capital expenditures represent incurred expenditures for property, plant and equipment and exploration and evaluation assets, and exclude right-of-use assets and working capital impacts.

____________________________

1. Cost of sales, including depreciation, cash costs and AISC are expressed on an attributable ounce sold basis (excluding the non-controlling interests at Essakane). See "Operations - Essakane, Burkina Faso".

2. This is a non-GAAP financial measure. See "Non-GAAP Financial Measures".

3. Côté capital expenditures reflect the proportionate interest in Côté Gold UJV on an incurred basis.

| OUTLOOK |

Production (000 oz)

| Actual 2025 | Full Year Guidance 2026 | |

| Côté Gold - (70%) | 279.9 | 270 - 310 |

| Westwood - (100%) | 113.9 | 110 - 130 |

| Essakane - (90% H1 2025 | 85% - H2 2025 and thereafter) | 372.1 | 340 - 380 |

| Total attributable production (000s oz) | 765.9 | 720 - 820 |

Total attributable production for IAMGOLD in 2026 is expected to be in the range of 720,000 to 820,000 ounces, as operations at Côté Gold focus on sustainable operations at nameplate operating rates ahead of the technical report outlining the expansion plans which is expected to be announced in the fourth quarter 2026. For further details, refer to the "Operations" section of each mine below.

The attributable guidance for Essakane is estimated according to IAMGOLD's 85% ownership interest. See "Operations - Essakane, Burkina Faso" for more details.

Costs

| Actual 2025 | Full Year Guidance 2026 | |

| Côté Gold | ||

| Cash costs - excluding royalties ($/oz sold) | $1,020 | $900 - $1,050 |

| Cash costs - including royalties ($/oz sold) | $1,268 | $1,200 - $1,350 |

| AISC ($/oz sold) | $1,636 | $1,775 - $1,925 |

| Westwood | ||

| Cash costs ($/oz sold) | $1,530 | $1,500 - $1,650 |

| AISC ($/oz sold) | $2,117 | $1,950 - $2,100 |

| Essakane | ||

| Cash costs - excluding royalties ($/oz sold) | $1,300 | $1,150 - $1,300 |

| Cash costs - including royalties ($/oz sold) | $1,636 | $1,600 - $1,750 |

| AISC ($/oz sold) | $1,888 | $2,000 - $2,150 |

| Consolidated | ||

| Cost of sales1 ($/oz sold) | $1,489 | $1,425 - $1,575 |

| Cash costs1,2 - excluding royalties ($/oz sold) | $1,230 | $1,100 - $1,250 |

| Cash costs1,2 - including royalties ($/oz sold) | $1,484 | $1,425 - $1,575 |

| AISC1,2 ($/oz sold) | $1,900 | $2,000 - $2,150 |

1. Consists of Côté Gold and Westwood on an attributable basis of 70% and 100%, respectively, and an attributable basis of 90% at Essakane for the first half of 2025 and 85% thereafter.

2. This is a non-GAAP financial measure. See "Non-GAAP Financial Measures".

Cash costs on a consolidated basis, excluding royalties, are expected to be in the range of $1,100 to $1,250 per ounce sold. With the current strong gold price environment, royalties account for an average of approximately $325 per ounce sold - based on a gold price assumption for 2026 of $4,000 per ounce. Cash costs, including royalties, are expected to average $1,425 to $1,575 per ounce sold. AISC for IAMGOLD are expected to be in the range of $2,000 and $2,150 per ounce sold.

The full year guidance for 2026 is based on the following assumptions (before the impact of hedging): an average realized gold price of $4,000 per ounce, USD/CAD exchange rate of 1.35, EUR/USD exchange rate of 1.18, average Brent oil price of $65 per barrel and West Texas Intermediate (WTI) price of $65 per barrel. For expected impacts from fluctuation in these assumptions, refer to the Sensitivity Impact table included in the "Financial Condition" section.

Royalty Sensitivities

| $ per ounce sold | |||

| Gold Price | Consolidated | Côté Gold | Essakane |

| $3,500 | $270 | $245 | $350 |

| $4,000 (guidance price) | $325 | $300 | $450 |

| $4,500 | $390 | $340 | $540 |

| $5,000 | $440 | $385 | $600 |

Capital Expenditures

| Actual 20251 | Full Year Guidance 20262 | |||||||||||||||||

| ($ millions) | Sustaining | Expansion | Total | Sustaining | Expansion | Total | ||||||||||||

| Côté Gold (IMG share) | $ | 103.8 | $ | 23.7 | $ | 127.5 | $ | 160 | $ | 85 | $ | 245 | ||||||

| Westwood | 63.9 | 1.5 | 65.4 | 55 | 30 | 85 | ||||||||||||

| Essakane | 106.9 | 7.4 | 114.3 | 165 | 5 | 170 | ||||||||||||

| $ | 274.6 | $ | 32.6 | $ | 307.2 | $ | 380 | $ | 120 | $ | 500 | |||||||

| Corporate | 0.1 | - | 0.1 | - | - | - | ||||||||||||

| Total3 | $ | 274.7 | $ | 32.6 | $ | 307.3 | $ | 380 | $ | 120 | $ | 500 | ||||||

1. 100% basis, for Westwood and Essakane, 70% for Côté Gold, all on an incurred basis.

2. Capital expenditures guidance (±5%).

3. Includes $7 million of capitalized exploration and evaluation expenditures also included in the Exploration Outlook guidance table.

Sustaining capital expenditures are expected to be approximately $380 million ±5%. Sustaining capital at Côté Gold, on an attributable basis, is expected to total $160 million ±5%, an increase from the prior year due to additional non-recurring plant and infrastructure design changes and improvements identified during the ramp-up to optimize operations and operating costs.

Expansion capital expenditures are expected to total $120 million ±5% in 2026. The Company intends to accelerate spending to de-risk the contemplated Côté expansion; early works include basic mill infrastructure and a significant pushback to expand the operating area of the pit. Additional expansion capital is associated with development works at Westwood to support the study of options to expand the mine in the eastern parts of Westwood underground that could be amenable to bulk mining.

Exploration Outlook

| Actual 2025 | Full Year Guidance 2026 | |||||||||||||||||

| ($ millions) | Capitalized | Expensed | Total | Capitalized | Expensed | Total | ||||||||||||

| Exploration projects - greenfield | $ | 0.2 | $ | 22.0 | $ | 22.2 | $ | 11 | $ | 34 | $ | 45 | ||||||

| Exploration projects - brownfield | 10.8 | 2.1 | 12.9 | 7 | 2 | 9 | ||||||||||||

| $ | 11.0 | $ | 24.1 | $ | 35.1 | $ | 18 | $ | 36 | $ | 54 | |||||||

Exploration expenditures for 2026 are expected to be approximately $54 million, the majority of which will be expensed. The largest exploration spend in 2026 is expected to be the Nelligan complex of approximately $24 million including the construction of certain infrastructure to support an expanding program, Côté Gold of approximately $5 million attributed to IAMGOLD, and Essakane at approximately $6 million.

Income Taxes Paid and Depreciation Outlook

| ($ millions) | Actual 2025 | Full Year Guidance 2026 |

| Depreciation expense | $420.9 | $480 (±5%) |

| Income taxes paid | $171.5 | $205 - $215 |

The Company expects to pay cash taxes in the range of $205 to $215 million during 2026. Cash tax payments do not occur evenly by quarter, as amounts paid in a quarter can include payments of the final balance of the prior year taxes and payments of instalments for the current year, both required to be made at times as prescribed by different countries. There are no significant cash taxes expected in respect of the new global minimum top-up taxes ("GloBE").

Depreciation expense for 2026 is expected to be $480 million (±5%) corresponding with production levels and depletion of certain pit phases for which waste stripping costs have been capitalized

| ENVIRONMENTAL, SOCIAL AND GOVERNANCE |

The Company is committed to maintaining its culture of accountable mining through high standards of Environmental, Social and Governance practices, in every aspect of its business. The Company tracks its ESG performance to understand progress and achievements across a range of material topics and indicators and draws upon various ESG frameworks and standards and internationally recognized methodologies such as the Global Reporting Initiative and Sustainability Accounting Standards Board to guide its Sustainability Report:

• On May 6, 2025, the Company released its annual Sustainability Report, outlining the Company's 2024 sustainability performance.

• On December 16, 2025, the Company released its 2024 Scope 3 Emissions Report. As a member of the Mining Association of Canada ("MAC"), the Company participates in the Towards Sustainable Mining ("TSM") initiative at its Westwood operation, as well as internationally at Essakane (Burkina Faso), which exceeds MAC's requirements of reporting only on Canadian operations. The Company conducted internal assessments of the 2024 TSM results for the Westwood and Essakane mines that were also externally verified and achieved an 'A' level or higher for all indicators within all protocols. The 2025 self-assessment reported improvement on some indicators.

In 2025, the Company set and achieved most of its ESG targets related to health and safety; equity, diversity, and inclusion; and environment, including:

• Integration of Critical Risk Management into operational processes including the development of a control verification tool,

• Embed cost of carbon into decision-making processes,

• Advance the catchment-based Water Framework at sites through the development of roadmaps, and

• Zero significant environmental and community incidents¹.

Health and Safety

IAMGOLD's TRIFR was 0.60 as of December 31, 2025, compared to 0.63 as of December 31, 2024. IAMGOLD is continuing to advance its critical risk management and visible leadership to improve safety and reduce high-potential incidents. This includes the integration of contractors in the critical risk management program. The Company continues to track a range of leading indicators around critical risk management, contractor management, and incident investigation quality.

Environmental

In 2025, the Company's key environmental focus areas were water and biodiversity. Building on the water stewardship framework developed in 2024, activities during the year focused on advancing initiatives identified in site-level water roadmaps, developing water performance scorecards, and re-assessing each operation's maturity against the Company's water stewardship framework. Following the establishment of the corporate biodiversity roadmap in 2024, the Company initiated work in 2025 on the development of site-specific regional biodiversity strategies. The Company also initiated work on determining a value of carbon approach for incorporating carbon considerations into decision-making.

The Company's three operating sites all have closure plans filed with the authorities supported by associated financial assurance to secure future restoration funds. In 2025, work to update each closure plan was undertaken to reflect current disturbance conditions and restoration concepts.

Essakane has been certified ISO 14001 for many years and conducted a management review of its environmental management system. The site continued to run an environmental 'stop incident' campaign to educate and empower employees to recognize and respond to environmental risks.

Westwood completed the pilot water recycling projects to reduce water withdrawal from the Bousquet River, and full-scale implementation is planned for 2026.

There were zero significant environmental or community incidents reported during 20251.

Social Performance

Throughout 2025, each operation continued to engage with their communities of interest and support community investment initiatives.

At Essakane, key engagements and activities included discussions on economic, social, security, and resettlement topics. In the fourth quarter 2024, IAMGOLD partnered with Project CURE to deliver two 40-foot containers of medical supplies to seven health centers in the Dori and Gorom-Gorom districts. After a needs assessment, IAMGOLD committed to funding two additional containers and four containers will be distributed in 2026 - three funded by IAMGOLD and one by Resource Capital Funds Foundation.

At Côté Gold, the Company hosted site tours with both elected local municipal and provincial officials, as well as Indigenous partner communities to share information about the mine and IAMGOLD's approach to responsible mining. The Company maintained ongoing communication with our neighbouring First Nation communities, local land users, communities' groups and government agencies through meetings, email, social media and school presentations.

At Westwood, the team continued to meet with Abitibiwinni First Nation related to the negotiation of an Impact Benefit Agreement.

________________________

1. IAMGOLD defines significant incidents as those assessed as Level 4 or 5 based on the Company's risk matrix, and/or resulting in fines greater than US$100,000. The Company's risk matrix includes a consequence matrix to determine incident severity that considers environmental, health and safety, social, and financial aspects.

Indigenous Relations

As a Canadian business committed to responding to the Truth and Reconciliation Commission of Canada's Calls to Action1, IAMGOLD launched a company-wide initiative in the first quarter 2025, that will help the Company articulate how it works with Indigenous peoples beyond reconciliation, towards a future that builds upon the Company's experiences and reflects its values. This work will lead to the creation of a coherent vision for reconciliation and a roadmap to help guide the Company's actions as an organization. During the fourth quarter 2025, IAMGOLD continued its work, supported by an Indigenous-owned business, to define a five-year plan for action in support of reconciliation.

Equity, Diversity and Inclusion

IAMGOLD includes annual objectives to support its efforts in integrating Equity, Diversity and Inclusion ("EDI") into the strategy and corporate scorecard, for the annual objectives, and tracks EDI metrics in site and corporate reports for visibility and measurement. IAMGOLD's executive leadership team has a 40% women representation.

Governance

The Board of Directors of IAMGOLD (the "Board") maintains diversity and renewal guidelines that reflect governance best practices. Membership should comprise, at a minimum, of the greater of (i) two women directors, or (ii) 30% women directors. The average tenure of the Board should not exceed ten years, and no director should serve as the chair of the Board or the chair of any committee for more than ten consecutive years.

Women represent 44% of all directors and 50% of independent directors. The average tenure of directors on the Board is approximately three years.

__________________________

1. The Truth and Reconciliation Commission of Canada (2015) released its Calls to Action report, which included a call to the Canadian corporate sector to support reconciliation

| OPERATIONS |

| Côté Gold, Canada |

The Côté District is located 125 kilometres southwest of Timmins and 175 kilometres north of Sudbury, Ontario, Canada. The mine is being operated through an unincorporated joint venture (the "Côté Gold UJV" or "UJV") between IAMGOLD, as the operator, and SMM. On November 30, 2024, the Company repurchased a 9.7% temporarily transferred interest (the "Funding Agreement with SMM") which returned IAMGOLD to its full 70% interest in the Côté Gold UJV. See "Funding Agreement with SMM" below.

Côté Gold Mine (IAMGOLD interest - 70% for 2025, 60.3% from January 2024 to November 2024 and 70% for December 2024)

| Q4 2025 | Q4 2024 | 2025 | 2024 | |||||||||

| Key Operating Statistics (100% basis, unless otherwise stated) | ||||||||||||

| Ore mined (000s t) | 4,514 | 3,637 | 14,640 | 10,849 | ||||||||

| Grade mined (g/t) | 1.04 | 1.07 | 0.94 | 0.97 | ||||||||

| Operating waste mined (000s t) | 6,555 | 4,765 | 24,830 | 16,666 | ||||||||

| Capital waste mined (000s t) | 12 | 2,445 | 5,638 | 11,821 | ||||||||

| Total material mined (000s t) | 11,081 | 10,847 | 45,108 | 39,336 | ||||||||

| Strip ratio1 | 1.5 | 2.0 | 2.1 | 2.6 | ||||||||

| Ore milled (000s t) | 2,874 | 2,433 | 10,889 | 4,948 | ||||||||

| Head grade (g/t) | 1.44 | 1.34 | 1.22 | 1.37 | ||||||||

| Recovery (%) | 94 | 91 | 93 | 92 | ||||||||

| Gold production (000s oz) - 100% | 124.6 | 96.1 | 399.8 | 199.1 | ||||||||

| Gold production (000s oz) - attributable | 87.2 | 62.4 | 279.9 | 124.0 | ||||||||

| Gold sales (000s oz) - 100% | 127.8 | 87.4 | 407.7 | 179.4 | ||||||||

| Gold sales (000s oz) - attributable | 87.7 | 55.8 | 283.6 | 111.1 | ||||||||

| Average realized gold price2,3 ($/oz) | $ | 4,212 | $ | 2,644 | $ | 3,572 | $ | 2,555 | ||||

| Financial Results ($ millions - attributable interest) | ||||||||||||

| Revenues4 | $ | 370.4 | $ | 147.9 | $ | 1,014.4 | $ | 284.3 | ||||

| Cost of sales4 | 111.7 | 60.6 | 360.8 | 115.0 | ||||||||

| Production costs | 80.5 | 52.8 | 286.7 | 107.2 | ||||||||

| (Increase)/decrease in finished goods | 3.4 | (2.1 | ) | 3.6 | (9.6 | ) | ||||||

| Royalties5 | 27.8 | 9.9 | 70.5 | 17.4 | ||||||||

| Cash costs2 | 111.1 | 60.4 | 359.6 | 114.7 | ||||||||

| Sustaining capital expenditures2 | 30.7 | 25.6 | 103.8 | 42.7 | ||||||||

| Expansion capital expenditures2 | 5.7 | 5.4 | 23.7 | 191.0 | ||||||||

| Total sustaining and expansion capital expenditures2 | 36.4 | 31.0 | 127.5 | 233.7 | ||||||||

| Earnings from operations | 203.0 | 44.2 | 464.6 | 105.6 | ||||||||

| Mine-site free cash flow2 | 197.0 | 16.9 | 484.1 | 40.2 | ||||||||

| Unit costs per tonne2 | ||||||||||||

| Mine costs per operating tonne mined2 | $ | 4.72 | $ | 4.19 | $ | 4.20 | $ | 3.90 | ||||

| Mill costs per tonne milled2 | $ | 20.91 | $ | 17.59 | $ | 20.00 | $ | 17.32 | ||||

| G&A costs per tonne milled2 | $ | 7.62 | $ | 7.35 | $ | 6.97 | $ | 8.49 | ||||

| Operating costs per ounce6 | ||||||||||||

| Cost of sales excluding depreciation ($/oz sold) | $ | 1,271 | $ | 1,083 | $ | 1,272 | $ | 1,035 | ||||

| Cash costs2 - excluding royalties ($/oz sold) | $ | 949 | $ | 902 | $ | 1,020 | $ | 875 | ||||

| Cash costs2 ($/oz sold) | $ | 1,265 | $ | 1,080 | $ | 1,268 | $ | 1,032 | ||||

| AISC2 ($/oz sold) | $ | 1,688 | $ | 1,685 | $ | 1,636 | $ | 1,658 |

1. Strip ratio is calculated as waste mined divided by ore mined.

2. This is a non-GAAP financial measure. See "Non-GAAP Financial Measures".

3. Average gold price realized on the attributable portion of sales excludes the impact of gold delivered into prepayment arrangements.

4. As per note 35 of the consolidated financial statements for revenues and cost of sales. Cost of sales is net of depreciation expense.

5. Includes the 7.5% gross margin royalty and various net smelter return royalties.

6. Cost of sales, cash costs excluding royalties cash costs and AISC per ounce sold may not be calculated based on amounts presented in this table due to rounding.

Operational Insights

• In its first full year of operations, Côté's attributable production was 279,900 ounces (399,800 ounces | 100%), achieving the top-end of the annual guidance range. The mine completed the ramp-up and achieved nameplate plant throughput of 36,000 tonnes per day ("tpd") over a period of thirty consecutive days ahead of schedule in June.

• Attributable gold production in the fourth quarter 2025 was a record 87,200 ounces (124,600 ounces | 100%), a 40% increase from the prior year period.

• Mining activity totaled 11.1 million tonnes in the fourth quarter 2025. Ore tonnes mined increased to a record 4.5 million tonnes, or 24% over the prior year period, with an associated strip ratio of 1.5:1 waste to ore. The average grade mined was 1.04 g/t in the fourth quarter 2025, in line with expectations, and the highest quarterly grade mined to date for the operation.

• Mill throughput in the fourth quarter 2025 totaled 2.9 million tonnes, an increase of 18% over the prior year period. The installation of the additional secondary crusher was completed in November and commissioned in December with both cone crushers tested and operating in parallel. The Company used a temporary contractor aggregate crusher to supplement crushing capacity during 2025 due to high wear caused by the abrasive ore impacting the availability of the secondary crushing circuit. The Company plans to phase out the temporary aggregate crushing circuit over the first half of 2026. The additional secondary cone crusher is expected to increase overall crushing capacity, optimize the particle size entering the high pressure grinding rolls (HPGR) allowing for improved maintenance cycles on the dry side, as well as the particle size entering the ball mill which has the potential to increase capacity in the wet side of the plant.

• Head grade for the fourth quarter was a record 1.44 g/t as a result of the combination of higher grade direct feed ore, a low strip ratio over the quarter and stockpiling of lower grade ore. Recoveries in the plant averaged a record 94% in the quarter. The reconciliation between the reserve models, grade control models, mill feed and production continues to be in line with expected tolerances.

Financial Highlights (attributable basis) - Q4 and 2025

• Revenue and cost of sales for the year are recognized at 70% in accordance with IAMGOLD's ownership interest.

• Production costs were $80.5 million and $286.7 million during the three and twelve months ended December 31, 2025, respectively. As outlined below, mining and milling per tonne unit costs continue to be elevated in part due to the ongoing reliance on the contractor aggregate crushing described above.

• Mining costs averaged $4.72 and $4.20 per tonne mined during the three and twelve months ended December 31, 2025, respectively. Mining costs in the fourth quarter continued to be impacted by the contractor aggregate crushing that increased rehandling and utilization of haul trucks. The impact is expected to reduce in 2026 as the contractor aggregate is phased out over the first half of 2026. Additional improvements to mining cost per tonne are expected through various measures including the continued transition to bulk mining, the improvement of the expected average life on haul truck tires and improving drilling practices to reduce the amount of redrilling required.

• Milling costs were $20.91 and $20.00 per tonne milled during the three and twelve months ended December 31, 2025, respectively. Unit costs remained higher in the fourth quarter as the temporary aggregate crusher was used extensively during the integration and commissioning of the additional secondary crusher. Milling costs were also higher due to the expensing of certain capital spares in 2025 as the life of the spares is expected to be less than a year until the benefits from the installation of the second secondary crusher are realized. Unit costs are expected to decline over the course of 2026 as the contractor aggregate crushing is phased out over the first half of the year.

• G&A costs were $7.62 and $6.97 per tonne milled during the three and twelve months ended December 31, 2025, respectively.

• Cost of sales, excluding depreciation, during the three and twelve months ended December 31, 2025, totaled $111.7 million and $360.8 million, respectively. Cost of sales per ounce sold, excluding depreciation, for the three and twelve months ended December 31, 2025, was $1,271 and $1,272, respectively.

• Cash costs, excluding royalties, during the three and twelve months ended December 31, 2025, totaled $83.3 million and $289.1 million, respectively, and cash cost per ounce sold, excluding royalties, was $949 and $1,020, respectively.

• Royalties during the three and twelve months ended December 31, 2025, were $27.8 million or $316 per ounce (25% of cash cost) and $70.5 million or $248 per ounce (20% of cash cost), respectively.

• Cash costs during the three and twelve months ended December 31, 2025, totaled $111.1 million and $359.6 million, respectively, and cash cost per ounce sold was $1,265 and $1,268, respectively.

• AISC during the three and twelve months ended December 31, 2025, was $1,688 and $1,636 per ounce sold, respectively.

• Capital expenditures, on a 100% and incurred basis, totaled $51.7 million in the fourth quarter 2025. Sustaining capital expenditures totaled $43.7 million ($30.7 million | 70%), including $29.2 million of capital projects related to operational improvements and ramp-up, $10.2 million of mobile equipment and critical spares, $2.3 million of other capital projects and $2.0 million of tailings infrastructure and related earthworks. Expansion capital of $8.0 million ($5.7 million | 70%) was primarily associated with the installation and commissioning of the additional secondary cone crusher completed during the fourth quarter of this year.

• Capital expenditures for the year, on a 100% and incurred basis, totaled $181.6 million. Sustaining capital expenditures totaled $148.0 million, ($103.8 million | 70%), including $46.0 million of capital projects related to operational improvements and ramp-up, $37.4 million of tailings expansion and related earthworks, $36.9 million of mobile equipment and critical spares, $21.1 million of capitalized stripping, and $6.6 million of other capital projects. Expansion capital of $33.6 million ($23.7 million | 70%) was primarily associated with the installation and commissioning of the additional secondary cone crusher during the fourth quarter of this year.

• Mine-site free cash flow was a record $197.0 million on an attributable basis for the three months ended December 31, 2025, on the strength of record revenues of $370.4 million with gold sales of 87,700 ounces at the realized gold price of $4,212 per ounce, resulting in operating cash flows of $241.8 million offset by capital expenditures totaling $44.8 million. For the year, mine-site free cash flow was $484.1 million on an attributable basis, with revenues of $1,014.4 million from the sale of 283,600 ounces at a realized gold price of $3,572 per ounce, resulting in operating cash flows of $606.8 million offset by capital expenditures totaling $122.7 million.

2026 Outlook

Côté Gold attributable production in 2026 is expected to be in the range of 270,000 to 310,000 ounces (390,000 to 440,000 ounces | 100%). The focus in 2026, now that the plant is operating at nameplate throughput, is on stabilization and optimization, improving the cost structure and preparing for the contemplated expansion of Côte. Short to medium term capital investment is planned to improve the operating efficiency and cost structure while also systematically investing in the expansion to derisk the larger build.

Mining activities in 2026 are planning a total of approximately 52 million tonnes of material mined. This includes a large pushback to open up the pit to improve mine efficiency and prepare for the contemplated expansion. Mill throughput is expected to average 36,000 tpd (nameplate) over the course of the year after the successful installation of the additional secondary crusher in the fourth quarter 2025. Plant head grades are expected to average between 1.00 g/t and 1.10 g/t. Gold production is expected to be higher in the second half of the year based on expected lower grades in the first half of the year followed by higher grades in the second half - as determined by the scheduled mine sequence.

Cash costs, excluding royalties, at Côté Gold are expected to be in the range of $900 to $1,050 per ounce sold, and including royalties (assuming a $4,000 per ounce gold price) in the range of $1,200 to $1,350 per ounce sold. AISC is expected to be in the range of $1,775 to $1,925 per ounce sold.

Sustaining capital expenditures guidance for Côté Gold is approximately $160 million ±5% ($230 million | 100%) that includes $50 million ($70 million | 100%) of non-recurring capital to improve the operating efficiency and the long-term operating cost structure.

Expansion capital of $85 million ±5% ($120 million | 100%) mainly relates to the planned strategic pit pushback that will provide both operational flexibility in the near term and optionality for the expansion, as well as the acceleration of certain expansion related plant construction activities, including an additional Vertimill in early 2027.

Exploration

The Gosselin zone is located immediately to the northeast of the Côté zone. Following the completion of the expansion and delineation diamond drilling program in 2024, the 2025 drilling plan was to continue with diamond drilling activities aimed at increasing the confidence in the existing resource and converting a large part of the Inferred Resource to the Indicated Resource category. A total of 45,000 metres was planned initially but this program was increased to approximately 53,750 metres for the year. Approximately 3,600 metres were completed in the fourth quarter 2025. In addition, approximately 5,550 metres tested the area to the north-east of the Gosselin zone.

The results of the Gosselin exploration program will be included in an updated Mineral Reserves and Mineral Resources estimate in the second quarter 2026 and will inform the planned updated technical report which will consider a larger scale Côté Gold Mine with a conceptual mine plan targeting both the Côté and Gosselin zones over the life of mine. This updated technical report is expected to be completed by the end of 2026.

Côté Zone Drilling

An infill drilling program of 20,000 metres was planned on the Côté zone which was initiated in the second quarter of 2025. Approximately 1,350 metres were completed in the fourth quarter 2025, for approximately 20,650 metres for the year. This infill drilling program was planned to improve resource confidence within the northeastern extension of the Côté deposit and convert Inferred Resources into the Indicated Resources category.

Mineral Resources and Reserves

Mineral Reserves decreased 301,000 ounces from the prior year period as updated estimates partially offset depletion (based on 10.9 Mt at 1.22 g/t for contained ounces of 428,100 ounces at 100% interest). The Côté Gold Mineral Reserve block model will be updated this year resulting in an updated mine plan incorporating both Côté and Gosselin.

Côté Gold (Côté and Gosselin) Measured & Indicated Mineral Resources, inclusive of Mineral Reserves and on a 100% basis, increased 12%, or approximately 2.0 million ounces, to an estimated 18.2 million ounces (12.7 million ounces attributable) as of December 31, 2025. Inferred Mineral Resources decreased approximately 2.0 million ounces to 2.2 million ounces.

The 2025 drilling plan at Côté and Gosselin prioritized increasing the confidence in the existing resource and converting a large part of the Inferred Resource to the Indicated Resource category. The program was increased to approximately 53,750 metres for the year at Gosselin. The results of the Gosselin drilling program will inform the planned updated technical report which will consider a larger scale Côté Gold Mine with a mine plan targeting both the Côté and Gosselin zones over the life of mine. (See "Mineral Resources and Reserves")

Funding Agreement with SMM

On December 19, 2022, the Company announced it had entered into the JV Funding and Amending Agreement with SMM, whereby SMM contributed the Company's funding obligations to the Côté Gold UJV and as a result, the Company transferred 9.7% of its interest in Côté Gold to SMM with a right to repurchase these transferred interests to return to its full 70% interest in the Côté Gold Mine.

On November 30, 2024, the Company exercised its right to repurchase the 9.7% interest in Côté Gold returning IAMGOLD to its full 70% interest in Côté Gold.

| Westwood Complex, Canada |

The Westwood Complex is located 35 kilometres northeast of Rouyn-Noranda and 80 kilometres west of Val d'Or in southwestern Québec, Canada. The Westwood Complex includes the Westwood underground mine and the Grand Duc open pit mine.

Westwood Complex (IAMGOLD interest - 100%)

| Q4 2025 | Q4 2024 | 2025 | 2024 | 2023 | |||||||||||

| Key Operating Statistics | |||||||||||||||

| Underground lateral development (metres) | 891 | 1,086 | 3,856 | 4,591 | 5,271 | ||||||||||

| Ore mined (000s t) - underground | 105 | 98 | 382 | 354 | 280 | ||||||||||

| Ore mined (000s t) - open pit | 174 | 283 | 996 | 662 | 742 | ||||||||||

| Ore mined (000s t) - total | 279 | 381 | 1,378 | 1,016 | 1,022 | ||||||||||

| Grade mined (g/t) - underground | 9.87 | 9.65 | 7.55 | 9.19 | 7.11 | ||||||||||

| Grade mined (g/t) - open pit | 1.02 | 1.33 | 1.09 | 1.75 | 1.71 | ||||||||||

| Grade mined (g/t) - total | 4.35 | 3.47 | 2.88 | 4.34 | 3.19 | ||||||||||

| Ore milled (000s t) | 299 | 267 | 1,154 | 1,107 | 1,034 | ||||||||||

| Head grade (g/t) - underground | 9.78 | 9.51 | 7.59 | 9.17 | 7.12 | ||||||||||

| Head grade (g/t) - open pit | 1.19 | 1.17 | 1.22 | 1.60 | 1.51 | ||||||||||

| Head grade (g/t) - total | 4.21 | 4.34 | 3.32 | 4.04 | 3.03 | ||||||||||

| Recovery (%) | 93 | 93 | 92 | 93 | 93 | ||||||||||

| Gold production (000s oz) | 37.9 | 34.6 | 113.9 | 133.7 | 93.4 | ||||||||||

| Gold sales (000s oz) | 37.1 | 36.7 | 113.6 | 133.9 | 90.2 | ||||||||||

| Average realized gold price1,2 ($/oz) | $ | 4,151 | $ | 2,652 | $ | 3,531 | $ | 2,403 | $ | 1,946 | |||||

| Financial Results ($ millions) | |||||||||||||||

| Revenues3 | $ | 155.0 | $ | 97.6 | $ | 403.0 | $ | 323.0 | $ | 176.6 | |||||

| Cost of sales3 | 48.5 | 42.3 | 175.7 | 157.5 | 144.6 | ||||||||||

| Production costs | 45.1 | 39.0 | 177.3 | 155.3 | 148.5 | ||||||||||

| (Increase)/decrease in finished goods | 3.4 | 3.3 | (1.6 | ) | 1.9 | (4.1 | ) | ||||||||

| Royalties | - | - | - | 0.3 | 0.2 | ||||||||||

| Cash costs1 | 47.8 | 42.2 | 173.8 | 156.3 | 143.7 | ||||||||||

| Sustaining capital expenditures1 | 15.1 | 18.5 | 63.9 | 66.1 | 65.0 | ||||||||||

| Expansion capital expenditures1 | 1.5 | (0.1 | ) | 1.5 | - | 0.6 | |||||||||

| Total sustaining and expansion capital expenditures1 | 16.6 | 18.4 | 65.4 | 66.1 | 65.6 | ||||||||||

| Earnings/(loss) from operations4 | 91.2 | 45.1 | 171.4 | 578.9 | (9.7 | ) | |||||||||

| Mine-site free cash flow1 | 89.2 | 41.3 | 148.6 | 94.4 | (42.8 | ) | |||||||||

| Unit costs per tonne1 | |||||||||||||||

| Underground mining cost per tonne mined | $ | 264.72 | $ | 233.72 | $ | 287.85 | $ | 250.86 | $ | 281.76 | |||||

| Open pit mining cost per operating tonne mined | $ | 6.82 | $ | 6.88 | $ | 7.29 | $ | 8.75 | $ | 8.86 | |||||

| Milling cost per tonne milled | $ | 25.53 | $ | 28.55 | $ | 27.32 | $ | 24.25 | $ | 23.56 | |||||

| G&A cost per tonne milled | $ | 22.69 | $ | 19.70 | $ | 20.31 | $ | 18.44 | $ | 21.30 | |||||

| Operating costs per ounce5 | |||||||||||||||

| Cost of sales excluding depreciation6 ($/oz sold) | $ | 1,307 | $ | 1,155 | $ | 1,547 | $ | 1,177 | $ | 1,600 | |||||

| Cash costs1 - excluding royalties ($/oz sold) | $ | 1,288 | $ | 1,148 | $ | 1,530 | $ | 1,164 | $ | 1,588 | |||||

| Cash costs1 ($/oz sold) | $ | 1,288 | $ | 1,148 | $ | 1,530 | $ | 1,167 | $ | 1,591 | |||||

| AISC1 ($/oz sold) | $ | 1,719 | $ | 1,688 | $ | 2,117 | $ | 1,702 | $ | 2,344 |

1. This is a non-GAAP financial measure. See "Non-GAAP Financial Measures".

2. Average realized gold price excludes the impact of gold delivered into prepayment arrangements.

3. As per note 35 of the consolidated financial statements for revenues and cost of sales. Cost of sales is net of depreciation expense.

4. Included in 2024 net earnings from operations is a $455.5 million gain on the reversal of the previously recorded impairment of the Westwood CGU.

5. Cost of sales, cash costs excluding royalties, cash costs and AISC per ounce sold may not be calculated based on amounts presented in this table due to rounding.

6. Includes non-cash ore stockpile and finished goods inventories NRV write-down of $3.2 million in 2023, which had an impact on cost of sales, excluding depreciation, per ounce sold of $36 for 2023).

Operational Insights

• Production was 113,900 ounces for the full year, below the bottom end of the guidance range of 125,000 to 140,000 ounces, due to lower grade stopes being mined earlier in the year after changes in the mine sequence to accommodate challenging ground conditions, combined with higher than expected underground dilution and lower mining recovery in certain areas.

• Production in the fourth quarter 2025 was 37,900 ounces, higher by 3,300 ounces or 10% compared with the same prior year period, a record level since the mine restarted in the second half of 2021. The fourth quarter included higher grade stopes which had been re-sequenced earlier in 2025 as described above.

• Mining activity for the year totaled 1.4 million tonnes of ore, an increase over the prior year of 0.4 million tonnes or 36% due to increased tonnes from both the underground mine and open pit. Mining activity in the fourth quarter 2025 of 279,000 tonnes of ore was lower by 102,000 tonnes or 27% than the same prior year period, primarily due to decreased volumes at the Grand Duc open pit. Underground mining activities in the fourth quarter averaged 1,139 tpd, translating to 105,000 tonnes in the quarter, a record volume from underground since the mine restart, with an average underground mined grade of 9.87 g/t Au.

• Mill throughput for the year was 1.2 million tonnes at an average head grade of 3.32 g/t, 4% higher and 18% lower, respectively, than the prior year. The lower head grades are due to a decrease in the grade from the underground mine as described above. Mill throughput in the fourth quarter 2025 was 299,000 tonnes, at an average grade of 4.21 g/t, 12% higher and 3% lower than the same prior year period, respectively.

• The mill achieved recoveries of 93% in the fourth quarter 2025, in line with the same prior year period.

• A renewed Collective Bargaining Agreement was ratified in the quarter extending through November 2030.

Financial Performance - Q4 2025 Compared to Q4 2024

• Production costs of $45.1 million were higher by $6.1 million or 16% than the same prior year period, due to increased underground mining activities. Underground mining costs per tonne mined were $264.72, the lowest level for the year due to the higher volumes mined. Mining costs included in production costs were higher due to an increased proportion of development activities in the fourth quarter supporting extraction and stope preparation activities relative to the same prior year period where there was a higher proportion of capital development activities, alongside an increase in the consumption of tires, explosives and related ground support components. Maintenance costs, increased over the fourth quarter 2025, continued in line with the year-to-date run rate as the mine continues to transition certain maintenance activities in house.

• Cost of sales, excluding depreciation, of $48.5 million was higher by $6.2 million or 15% compared to the same prior year period due to higher production costs. Cost of sales per ounce sold, excluding depreciation, of $1,307, was higher by $152 or 13% as a result, with sales volume in line with the same year prior period.

• Cash costs of $47.8 million were higher by $5.6 million or 13% compared to the prior year period. Cash costs per ounce sold of $1,288 were higher by $140 per ounce or 12%, due to the increase in production costs, with sales volume in line with the same year prior period.

• AISC per ounce sold of $1,719 was higher by $31 per ounce or 2%, primarily due to higher cash costs, partially offset by lower sustaining capital spend, with sales volume in line with the same year prior period.

• Sustaining capital expenditures of $15.1 million included mill and mobile equipment of $6.3 million, underground development and rehabilitation of $5.9 million, capitalized stripping at Grand Duc of $2.0 million, and other sustaining capital projects of $0.9 million. During the fourth quarter a work program commenced on the adjacent Eastwood deposit, with $1.5 million incurred in the period, to support the study of options to expand the mine in the eastern parts of Westwood underground that could be amenable to bulk mining.

• Mine-site free cash flow was $89.2 million for the three months ended December 31, 2025, based on the record revenues of $155.0 million with gold sales of 37,100 ounces at a realized gold price of $4,151 per ounce, generating operating cash flows of $106.1 million offset by capital expenditures totaling $16.9 million.

Financial Performance - 2025 Compared to 2024

• Production costs of $177.3 million were higher by $22.0 million or 14%, primarily due to higher mining costs due to an increase in underground mining activity resulting in increased consumption of explosives, tires and related components for required ventilation and ground support, alongside increasing maintenance and labour costs. Milling cost increased due to the rental cost of a mobile ore crusher to support higher mill throughput, and increased cost of mill consumables.

• Cost of sales, excluding depreciation, of $175.7 million was higher by $18.2 million or 12%, primarily due to higher production costs. Cost of sales per ounce sold, excluding depreciation, of $1,547 was higher by $370 or 31%, primarily due to higher production costs and lower production and sales volumes.

• Cash costs of $173.8 million were higher by $17.5 million or 11%, primarily due to higher production costs. Cash costs per ounce sold of $1,530 were higher by $363 or 31%, primarily due to higher production costs and lower production and sales volumes.

• AISC per ounce sold of $2,117 was higher by $415 or 24%, primarily due to higher cash costs, partially offset by lower production and sales volumes.

• Sustaining capital expenditures of $63.9 million included mill and mobile equipment of $29.7 million, underground development and rehabilitation of $28.0 million, capitalized stripping at Grand Duc of $2.0 million, and other sustaining capital projects of $4.2 million.

• Mine-site free cash flow was $148.6 million for the twelve months ended December 31, 2025, with record revenues of $403.0 million with gold sales of 113,600 ounces at a realized gold price of $3,531 per ounce, resulting in operating cash flows of $214.1 million offset by capital expenditures totaling $65.5 million. This increase of $54.2 million compared to the prior year period is primarily attributed to $80.0 million in higher revenues due to the higher realized gold price, partially offset by lower production and sales.

2026 Outlook

Westwood production is expected to be in the range of 110,000 to 130,000 ounces in 2026. Underground mining is planned for between 900 to 1,000 tonnes per day and the Grand Duc open pit life has been extended into 2027 based on the improved economics in the current gold price environment. Mill throughput is expected to average 1.2 million tonnes in 2026 with blended head grades expected to average 3.44 g/t over the course of the year.

Cash costs at Westwood are expected to be in the range of $1,500 to $1,650 per ounce sold and AISC in the range of $1,950 to $2,100 per ounce sold.

Sustaining capital expenditures guidance is $55 million (±5%), primarily consisting of underground development in support of the mine plan, the continued renewal of the mobile fleet and fixed equipment, and certain asset integrity projects at the Westwood mill. Expansion capital of $30 million is primarily associated with development works to support the study of options to expand the mine in the eastern parts of Westwood underground that could be amenable to bulk mining. Additional extensions to the Grand Duc pit will also be investigated this year.

Brownfield Exploration

During the three and twelve months ended December 31, 2025, approximately 7,700 metres and 28,400 metres respectively, of underground diamond drilling (including approximately 1,600 metres for the year of geotechnical drilling) were completed to support the continued ramp-up of underground mining operations. The Company is investigating high priority underground targets which could offer potential additional sources of high-grade material.

Mineral Resources and Reserves

Mineral Reserves from the underground increased 125,000 ounces and 20,000 ounces from the Grand Duc open pit, more than offsetting depletion, primarily as a result of the change in resource model and increased gold price assumption and reduction in the underground cut-off grade to 6.40 g/t Au (down from 6.82 g/t Au previously). (See "Mineral Resources and Reserves")

| Essakane, Burkina Faso |

The Essakane District is located in north-eastern Burkina Faso, West Africa approximately 330 kilometres northeast of the capital, Ouagadougou. The Essakane District includes the Essakane mine and the surrounding mining lease and exploration concessions totaling approximately 600 square kilometres. Effective June 20, 2025, in accordance with the amended Burkina Faso Mining Code, the government of Burkina Faso increased its ownership interest in the Essakane mine from 10% to 15%. As a result, the Company's interest decreased thereafter from 90% to 85%.

Essakane Mine (IAMGOLD interest - 90% for H1 2025 and prior, 85% thereafter)

| Q4 2025 | Q4 2024 | 2025 | 2024 | 2023 | |||||||||||

| Key Operating Statistics1 | |||||||||||||||

| Ore mined (000s t) | 4,123 | 2,170 | 11,910 | 9,714 | 9,586 | ||||||||||

| Grade mined (g/t) | 1.44 | 1.14 | 1.25 | 1.44 | 1.35 | ||||||||||

| Operating waste mined (000s t) | 4,649 | 4,036 | 22,087 | 13,315 | 19,530 | ||||||||||

| Capital waste mined (000s t) | 620 | 6,168 | 5,651 | 23,895 | 14,233 | ||||||||||

| Total material mined (000s t) | 9,392 | 12,374 | 39,648 | 46,924 | 43,349 | ||||||||||

| Strip ratio2 | 1.3 | 4.7 | 2.3 | 3.8 | 3.5 | ||||||||||

| Ore milled (000s t) | 3,241 | 2,948 | 12,560 | 12,087 | 11,283 | ||||||||||

| Head grade (g/t) | 1.50 | 1.07 | 1.18 | 1.33 | 1.26 | ||||||||||

| Recovery (%) | 88 | 87 | 90 | 88 | 90 | ||||||||||

| Gold production (000s oz) - 100% | 138.1 | 88.4 | 427.2 | 454.2 | 412.9 | ||||||||||

| Gold production (000s oz) - attributable | 117.3 | 79.7 | 372.1 | 408.8 | 371.6 | ||||||||||

| Gold sales (000s oz) - 100% | 134.2 | 92.9 | 420.6 | 454.0 | 413.2 | ||||||||||

| Average realized gold price3,4 ($/oz) | $ | 4,188 | $ | 2,680 | $ | 3,538 | $ | 2,383 | $ | 1,957 | |||||

| Financial Results ($ millions)1 | |||||||||||||||

| Revenues5 | $ | 562.7 | $ | 249.3 | $ | 1,489.5 | $ | 1,083.2 | $ | 809.6 | |||||

| Cost of sales5 | 198.0 | 139.7 | 689.2 | 536.8 | 502.4 | ||||||||||

| Production costs | 131.1 | 121.9 | 544.7 | 458.3 | 450.5 | ||||||||||

| (Increase)/decrease in finished goods | 5.2 | (1.7 | ) | 2.2 | (6.8 | ) | (0.8 | ) | |||||||

| Royalties6 | 61.7 | 19.5 | 142.3 | 85.3 | 52.7 | ||||||||||

| Cash costs3 | 197.4 | 139.4 | 687.7 | 535.5 | 488.0 | ||||||||||

| Sustaining capital expenditures3 | 28.9 | 49.0 | 106.9 | 180.4 | 134.9 | ||||||||||

| Expansion capital expenditures3 | 0.8 | 2.1 | 7.4 | 5.1 | 1.7 | ||||||||||

| Total sustaining and expansion capital expenditures3 | 29.7 | 51.1 | 114.3 | 185.5 | 136.6 | ||||||||||

| Earnings from operations | 297.0 | 77.4 | 608.1 | 384.4 | 92.0 | ||||||||||

| Mine-site free cash flow3 | 340.4 | 20.0 | 566.3 | 250.5 | 91.0 | ||||||||||

| Unit costs per tonne3 | |||||||||||||||

| Open pit mining cost per operating tonne mined | $ | 6.66 | $ | 5.37 | $ | 6.36 | $ | 5.34 | $ | 5.02 | |||||

| Milling cost per tonne milled | $ | 17.95 | $ | 20.35 | $ | 19.35 | $ | 19.26 | $ | 18.94 | |||||

| G&A cost per tonne milled | $ | 10.67 | $ | 9.83 | $ | 9.52 | $ | 8.50 | $ | 9.07 | |||||

| Operating costs per ounce7 | |||||||||||||||

| Cost of sales excluding depreciation ($/oz sold) | $ | 1,475 | $ | 1,504 | $ | 1,640 | $ | 1,182 | $ | 1,216 | |||||

| Cash costs3 - excluding royalties ($/oz sold) | $ | 1,011 | $ | 1,291 | $ | 1,300 | $ | 991 | $ | 1,053 | |||||

| Cash costs3 ($/oz sold) | $ | 1,471 | $ | 1,501 | $ | 1,636 | $ | 1,179 | $ | 1,181 | |||||

| AISC3 ($/oz sold) | $ | 1,674 | $ | 2,118 | $ | 1,888 | $ | 1,625 | $ | 1,521 |

1. 100% basis, unless otherwise stated.

2. Strip ratio is calculated as waste mined divided by ore mined.

3. This is a non-GAAP financial measure. See "Non-GAAP Financial Measures".

4. Average realized gold price excludes the impact of gold delivered into prepayment arrangements.

5. As per note 35 of the consolidated financial statements for revenues and cost of sales. Cost of sales is net of depreciation expense.

6. Includes contributions made by the Essakane mine to the development fund for local communities, equating to 1% of total revenues.

7. Cost of sales, cash costs excluding royalties, cash costs and AISC per ounce sold may not be calculated based on amounts presented in this table due to rounding.

Operational Insights

• Essakane delivered full year production of 427,200 ounces on a 100% basis, exceeding the midpoint of the guidance range when expressed on a 100% basis; on an attributable basis Essakane produced 372,100 ounces that include the impact of the mid-year change in ownership from 90% to 85%. During the fourth quarter 2025, Essakane produced a record 138,100 ounces, or 117,300 ounces on an attributable basis, an increase of 37,600 ounces or 47% from the prior year period, due to higher head grades compared to the same prior year period.

• Mining for the year totaled 39.6 million tonnes, 7.3 million tonnes or 16% lower than the prior year period in line with the mine plan, and included ore mined totaling 11.9 million tonnes at an average grade of 1.25 g/t, an increase of 23% and decrease of 13%, respectively over the prior year. Mining in the fourth quarter 2025 totaled 9.4 million tonnes, lower by 3.0 million tonnes or 24% compared to the same prior year period and included ore mined totaling 4.1 million tonnes in the quarter at an average grade of 1.44 g/t, an increase of 90% and 26%, respectively over the same year prior period. The average grade of mined ore in the fourth quarter was the highest grade mined in the year as the mine sequences deeper into Phase 7.

• Mill throughput for the year totaled 12.6 million tonnes at an average head grade of 1.18 g/t, 4% higher and 11% lower than prior year levels, respectively. Mill throughput in the fourth quarter 2025 was 3.2 million tonnes at an average head grade of 1.50 g/t, 10% higher and 40% higher than the same prior year period, respectively.

• The mill achieved recoveries of 90% for the year, 2% higher than the prior year. Recoveries were 88% in the fourth quarter 2025, 1% higher than the same prior year period.

• The security situation in Burkina Faso continues to be a focus for the Company. Security-related incidents are still occurring in the country, and more broadly, the West African region, which pressure supply chains. The Company continues to take proactive measures to ensure the safety and security of in-country personnel and is constantly adjusting its protocols and activity levels at the site in response to the security environment. The Company continues to invest in the security and supply chain infrastructure in the region and at the mine site. It is also incurring additional costs to bring employees, contractors, supplies, and inventory to the mine. The situation has placed the Government of Burkina Faso under significant financial constraint due to the high cost of funding its initiatives to defend itself against militant attacks. See "Risks and Uncertainties".

• Essakane declared a record dividend of approximately $855 million in June 2025. This dividend represents the full distribution of past undistributed retained earnings up to and including 2024. IAMGOLD's 85% portion of the dividend, net of taxes, is approximately $680 million at a foreign exchange rate of EUR/USD 1.15. See "Financial Condition - Dividend Payments from Essakane".

• On April 7, 2025, the Government of Burkina Faso enacted an update to the royalty decree increasing the minimum royalty rate applicable to gold prices above $3,000/oz to 8%, with the rate increasing by an additional 1% for each $500/oz thereafter. The previous rate was 7% on all gold sold at or above $2,000/oz. The average royalty rate was 10.0% in the fourth quarter and 8.6% for the full year 2025, in addition to the contributions to the development fund for local communities equating to 1% of total revenues.

Financial Performance - Q4 2025 Compared to Q4 2024

• Production costs of $131.1 million were higher by $9.2 million or 8%, primarily resulting from a higher proportion of mining costs being expensed, due to the lower strip ratio during the period due to the increased proportion of ore tonnes mined described above. Costs were also impacted by USD equivalent labour, contractor and facility costs, which have increased compared to the same prior year period due to the appreciation of the local XOF currency, which is pegged to the Euro.

• Cost of sales, excluding depreciation, of $198.0 million was higher by $58.3 million or 42%, primarily due to higher production costs and a 216% increase in royalties resulting from higher gold prices and the new royalty decree. Cost of sales per ounce sold, excluding depreciation, of $1,475 was lower by $29 per ounce or 2% primarily due to higher production and sales volumes due to higher average head grade in the quarter offsetting the impact of higher production costs and royalties. Royalties accounted for $460 per ounce, an increase of $250 per ounce.

• Cash costs, excluding royalties, of $135.7 million were higher by $15.8 million or 13%, primarily due to higher production costs. Cash costs per ounce sold, excluding royalties, of $1,011 per ounce were lower by $280 per ounce or 22%, primarily due to higher production and sales volumes offsetting the impact of higher production costs.

• Cash costs, including royalties, of $197.4 million were higher by $58.0 million or 42%, and total cash costs per ounce sold of $1,471 per ounce were lower by $30 or 2%.

• AISC per ounce sold of $1,674 was lower by $444 per ounce or 21% primarily due to lower sustaining capital expenditures and higher production and sales volumes, partially offset by higher production costs and royalties compared to the prior period.

• Total capitalized stripping of $4.2 million was lower by $28.9 million or 87%, as the mine fleet prioritized ore mining, resulting in lower overall waste tonnes mined in the period increasing the proportion of waste tonnes classified as operating waste consistent with the 2025 mine plan.

• Sustaining capital expenditures, excluding capitalized stripping, of $24.7 million included mobile and mill equipment of $13.3 million, capital spares of $4.9 million, tailings management of $2.8 million, resource development of $1.4 million, and other sustaining projects of $2.3 million.

• Mine-site free cash flow was $340.4 million for the three months ended December 31, 2025, with record revenues of $562.7 million with gold sales of 134,200 ounces at a realized gold price of $4,188 per ounce, resulting in operating cash flows of $367.2 million offset by capital expenditures totaling $26.8 million. This increase of $320.4 million compared to the same prior year period is primarily due to higher revenues from the higher realized gold price and higher production and sales volume, partially offset by higher production costs and royalty payments.

Financial Performance - 2025 Compared to 2024

• Production costs of $544.7 million were higher by $86.4 million or 19% than the prior year period, primarily resulting from a higher proportion of mining costs being expensed, due to the lower overall waste tonnages mined reducing the lower strip ratio and amount of deferred stripping during the period. Costs were also impacted by higher maintenance costs and higher energy costs.

• Cost of sales, excluding depreciation, of $689.2 million was higher by $152.4 million or 28%, primarily due to higher production costs and a 67% increase in royalties resulting from the higher gold prices and new royalty decree. Cost of sales per ounce sold, excluding depreciation, of $1,640 was higher by $458 or 39%, primarily due to higher production costs and increased royalties as well as lower production and sales volumes. Royalties were $336 per ounce, an increase of $148 per ounce due to higher realized gold prices.

• Cash costs, excluding royalties, of $545.4 million were higher by $95.2 million or 21%, primarily due to the higher cost of sales. Cash costs per ounce sold, excluding royalties, of $1,300 were higher by $309 or 31%, primarily due to higher production costs as described above.

• Cash costs, including royalties, of $687.7 million were higher by $152.2 million or 28%, and total cash costs per ounce sold of $1,636 were higher by $457 or 39% than the prior year period.

• AISC per ounce sold of $1,888 was higher by $263 per ounce or 16%, primarily due to higher cash cost and lower production and sales volume, partially offset by lower sustaining capital expenditures.

• Total capitalized stripping of $32.5 million was lower by $93.6 million or 74%, as the mine fleet continued to prioritize ore mining in Phase 7 and sequencing through mining phases with higher life of phase strip ratios, resulting in a higher proportion of waste tonnes classified as operating waste consistent with the 2025 mine plan.

• Sustaining capital expenditures, excluding capitalized stripping, of $74.4 million included mobile and mill equipment of $23.7 million, capital spares of $20.0 million, tailings management of $10.6 million, resource development of $8.6 million, generator overhaul of $1.9 million and other sustaining projects of $9.6 million.

• Mine-site free cash flow was $566.3 million for the twelve months ended December 31, 2025, with record revenues of $1,489.5 million from the sale of 420,600 ounces at a realized gold price of $3,538 per ounce resulting in operating cash flows of $672.9 million offset by capital expenditures totaling $106.6 million. This increase of $315.8 million compared to the prior year period is primarily due to higher revenues from the higher realized gold price, partially offset by lower production and sales and higher production costs of $86.4 million described above, $57.0 million in higher royalty payments in the year and higher cash tax payments of $66.5 million due to higher taxation based on higher profits in 2024.

2026 Outlook

Essakane attributable production is expected to be in the range of 340,000 to 380,000 ounces (400,000 to 440,000 ounces | 100%). Mining activities will predominantly target Phase 6 and 7 and the Lao pit that is adjacent to the Essakane Main Zone, with an estimated target of 42 to 43 million tonnes of material mined at a strip ratio between 2.5 to 3:1. Mill throughput is expected to total near 13 million tonnes with head grades averaging 1.10 g/t Au.

Cash costs, excluding royalties, are expected to be in the range of $1,150 to $1,300 per ounce sold, and including royalties, in the range of $1,600 to $1,750. AISC is expected to be in the range of $2,000 to $2,150 per ounce sold. Costs at Essakane are impacted by the Burkinabe royalty structure described above which are uncapped and tied to gold prices.

Sustaining capital expenditures guidance is approximately $165 million (±5%), including approximately $90 million of capitalized waste stripping to progress Phase 6 and into the Lao pit, as well as the ongoing replacement of certain equipment to improve efficiency and maintenance costs at Essakane, and the annual tailings dam program. The capitalized waste stripping is higher than estimated in the December 2023 technical report due to inclusion of the Lao pit and extension of estimated mine life into 2029.

Continued security incidents or related concerns could have a material adverse impact on future operating performance. In response to the security situation noted above, the Company continues to actively work with authorities and suppliers to mitigate potential impacts and manage supply continuity, while also investing in additional infrastructure and supply inventory levels designed to secure operational continuity. See "Risks and Uncertainties."

Brownfield Exploration

During the three and twelve months ended December 31, 2025, approximately 3,800 metres and 40,300 metres respectively, of diamond and reverse circulation drilling were completed as part of a step-out and infill drilling program to extend known mineralization and improve resource confidence within selected areas of Essakane North, Essakane Main Zone and the Lao satellite deposit and southern extension. The deposits remain open along strike and at depth. Exploration activities on concessions surrounding the mine lease continue to be suspended due to regional security constraints.

Mineral Resources and Reserves