.2

|

Dear Fellow Shareholders,

We invite you to attend the Special Meeting of shareholders (the “Meeting”) of Seabridge Gold Inc. (“Seabridge” or the “Company”) at Salon 1, 19th Floor, Fairmont Royal York Hotel, 100 Front Street West, Toronto, Ontario, Canada at 10:00 a.m. Eastern Daylight Time on May 22, 2026. The attached Circular provides important information enabling you to make informed decisions in the exercise of your rights as a shareholder.

Seabridge has proposed to reorganize its corporate structure through a plan of arrangement under which the Company’s interest in the Courageous Lake gold project, located in the Northwest Territories, Canada, will be transferred to a newly created company, Valor Gold Corp. (“Valor”). Upon completion of the arrangement, shareholders of Seabridge will receive shares of Valor on a pro-rata basis and Valor will become an independent, publicly traded company focused on advancing the Courageous Lake project.

The proposed spin-out is intended to allow each company to pursue a more focused strategy. Seabridge will continue to concentrate its resources and management efforts on the advancement of the KSM project in British Columbia, while Valor will be dedicated to the exploration, evaluation and development of the Courageous Lake project. The board of directors of Seabridge believes that separating the assets into two specialized companies will provide value accretion, enhance strategic focus, improve access to capital tailored to each project, and provide shareholders with direct exposure to the value and development potential of Courageous Lake.

I hope to see you at the Meeting. If you cannot attend, please return your proxy and let your voice be counted.

On behalf of the Board,

“Rudi P. Fronk”

Rudi P. Fronk Chairman and C.E.O. March 30, 2026 |

| The Seabridge Board UNANIMOUSLY recommends that the shareholders of Seabridge Gold Inc. vote FOR the Arrangement Resolution. |

These materials are important and require your immediate attention. They require shareholders of Seabridge Gold Inc. to make important decisions. If you are in doubt as to how to make such decisions, please contact your financial, legal, tax or other professional advisors. This document does not constitute an offer or a solicitation to any person in any jurisdiction in which such offer or solicitation is unlawful.

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

| Type: | Special Meeting |

| Date: | May 22, 2026 |

| Time: | 10:00 a.m. Eastern Daylight Time |

| Place: | Salon 1, 19th Floor, Fairmont Royal York Hotel, 100 Front Street West, Toronto, Ontario, Canada |

NOTICE IS HEREBY GIVEN that a Special Meeting (the “Meeting”) of the shareholders of Seabridge Gold Inc. (the “Company” or “Seabridge”) will be held at Salon 1, 19th Floor, Fairmont Royal York Hotel, 100 Front Street West, Toronto, Ontario, Canada, on May 22, 2026, at 10:00 a.m. Eastern Daylight Time.

Matters For Consideration at the Meeting

| 1. | To consider and, if thought fit, to pass a special resolution (the “Arrangement Resolution”) approving an arrangement (the “Arrangement”) under section 192 of the Canada Business Corporations Act (the “Act”) between the Company, its securityholders and Valor Gold Corp. (“Valor”), pursuant to which the Company and the Company’s shareholders will receive shares of Valor. |

| 2. | If the Arrangement Resolution is passed, to consider and, if thought fit, to pass an ordinary resolution approving the proposed restricted share unit and deferred share unit plan of Valor. |

| 3. | To transact such further or other business as may properly come before the Meeting and any adjournment(s) thereof. |

The specific details of the foregoing matters to be put before the Meeting are set forth in the Circular.

This notice is accompanied by the Circular, a form of proxy and a letter of transmittal.

The board of directors of the Company (the “Board”) has by resolution fixed the close of business on March 30, 2026 as the record date, being the date for the determination of the registered holders of common shares of the Company entitled to notice of and to vote at the Meeting and any adjournment(s) thereof.

Shareholders are encouraged to vote on the matters BEFORE the Meeting by proxy to ensure that their votes are properly counted. Those Shareholders who are unable to attend the Meeting are requested to read the notes to the enclosed form of proxy and then to complete, sign and mail the enclosed form of proxy in accordance with the instructions set out in the proxy and in the Circular accompanying this notice.

All shareholders are entitled to attend and vote at the Meeting in person or by proxy. Shareholders who do not wish to attend in person will also be able to listen to the Meeting via Microsoft Teams by visiting www.microsoft.com/microsoft-teams/join-a-meeting and using the Meeting ID and Passcode below, but will not be able to participate or vote their shares unless they attend in person or vote their shares by proxy.

ii

To LISTEN TO the Meeting, please refer to the following Microsoft Teams instructions:

Meeting ID: 254 434 303 795 816

Meeting Passcode: Gs3Yy2Dw

Proxies to be used at the Meeting must be completed, dated, signed and returned to Computershare Investor Services Inc., Proxy Department, at 14th Floor, 320 Bay Street, Toronto, Ontario M5H 4A6 by 10:00 a.m. Eastern Time on May 20, 2026, or if the Meeting is adjourned or postponed, not less than 48 hours (excluding Saturdays, Sundays and holidays) before the date to which the Meeting is adjourned or postponed. Telephone voting can be completed at 1-866-732-8683, and Internet voting can be completed at www.investorvote.com.

Non-Registered Shareholders who receive these materials through their broker or other intermediary are requested to follow the instructions for voting provided by their broker or intermediary, which may include the completion and delivery of a voting instruction form.

AND TAKE NOTICE that dissenting shareholders in respect of the proposed Arrangement are entitled to be paid the payout value of their shares in accordance with section 190 of the CBCA. Pursuant to the Interim Order (as defined in the Circular) of the Supreme Court of British Columbia dated April 10, 2026 and the CBCA, a registered holder of common shares of the Company may until 4:00 p.m. Pacific Time on the day which is two days immediately preceding the date of the Meeting give the Company a notice of dissent in the manner provided for in the Interim Order with respect to the Arrangement Resolution. As a result of giving a notice of dissent, a shareholder may, on receiving a notice of implementation of the Arrangement Resolution, require the Company to purchase all of the common shares held by such shareholder in respect of which the notice of dissent was given. These dissent rights are described in the Circular. As described in the Circular, it is a condition precedent to the completion of the Arrangement that less than 1% of the Seabridge Shareholders shall have validly exercised dissent rights in respect of the Arrangement.

DATED at Toronto, Ontario, this 30th day of March, 2026.

BY ORDER OF THE BOARD

SEABRIDGE GOLD INC.

“Rudi P. Fronk”

Rudi P. Fronk

Chairman and CEO

iii

Table of Contents

| NOTICE OF SPECIAL MEETING OF SHAREHOLDERS | ii |

| GENERAL DISCLOSURE INFORMATION | 4 |

| CAUTIONARY NOTE REGARDING FORWARD-LOOKING INFORMATION | 4 |

| DATE OF INFORMATION | 6 |

| REPORTING CURRENCIES AND ACCOUNTING PRINCIPLES | 6 |

| GLOSSARY | 7 |

| SUMMARY OF CIRCULAR | 15 |

| The Meeting | 15 |

| The Arrangement | 15 |

| Fairness Opinion | 15 |

| Steps in the Arrangement | 16 |

| INFORMATION CIRCULAR | 22 |

| APPOINTMENT OF PROXYHOLDER | 22 |

| VOTING BY PROXY | 23 |

| COMPLETION AND RETURN OF PROXY | 23 |

| REVOCABILITY OF PROXY | 23 |

| NON-REGISTERED HOLDERS | 24 |

| LETTER OF TRANSMITTAL | 25 |

| VOTING SECURITIES AND PRINCIPAL HOLDERS THEREOF | 25 |

| PARTICULARS OF OTHER MATTERS TO BE ACTED UPON | 26 |

| The Arrangement | 26 |

| Background to the Arrangement | 26 |

| Arrangement | 27 |

| Fairness Opinion | 27 |

| Steps in the Arrangement | 28 |

| Recommendation of the Board | 29 |

| Approval of the Arrangement Resolution | 30 |

| The Arrangement Agreement | 31 |

| Completion of the Arrangement | 34 |

| Effect of the Arrangement | 34 |

| Court Approval of the Arrangement | 34 |

| Regulatory Approvals | 36 |

| Canadian Securities Laws and Resale of Securities | 36 |

| U.S. Securities Laws and Resale of Securities | 37 |

| No Collateral Benefit | 39 |

| Significant Positions and Shareholdings | 39 |

| Arrangement Risk Factors | 43 |

| Dissent Rights | 46 |

| Exchange of Securities | 49 |

| Proxy Solicitation Requirements | 50 |

| Valor Incentive Plan Resolution | 50 |

| PRINCIPAL CANADIAN FEDERAL INCOME TAX CONSEQUENCES | 51 |

| Holders Resident in Canada | 52 |

| Holders Not Resident in Canada | 57 |

| MATERIAL UNITED STATES FEDERAL INCOME TAX CONSIDERATIONS | 60 |

| ADDITIONAL INFORMATION | 75 |

| Interest of Informed Persons in Material Transactions | 75 |

| Management Contracts | 75 |

| Response to Shareholders | 75 |

| Information Relating to the Company | 76 |

| APPROVAL | 76 |

| APPENDICES | A-1 |

| Appendix “A” Arrangement Resolution | A-1 |

| Appendix “B” Arrangement Agreement and Plan of Arrangement | B-1 |

| Schedule “1” to Appendix “B” Plan of Arrangement | B-1-1 |

| Schedule “2” to Appendix “B” Arrangement Resolution | B-2-1 |

| Schedule “3” to Appendix “B” Gold Stream Agreement | B-3-1 |

| Appendix “C” Interim Order | C-1 |

| Appendix “D” Notice of Petition and Petition | D-1 |

| Appendix “E” Dissent Provisions of the CBCA | E-1 |

| Appendix “F” Fairness Opinion | F-1 |

| Appendix “G” Information Regarding Valor | G-1 |

| Schedule “1” to Appendix “G” Summary of the Courageous Lake Project | G-1-1 |

| Schedule “2” to Appendix “G” Valor Incentive Plan | G-2-1 |

| Schedule “3” to Appendix “G” Valor Form of Audit Committee Charter | G-3-1 |

| Appendix “H” Carve-Out Financial Statements of Valor for the years ended December 31, 2024 and 2023 | H-1 |

| Appendix “I” Carve-Out MD&A of Valor for the years ended December 31, 2024 and 2023 | I-1 |

| Appendix “J” Condensed Interim Carve-Out Financial Statements of Valor for the three and nine months ended September 30, 2025 | J-1 |

| Appendix “K” Condensed Interim Carve-Out MD&A of Valor for the three and nine months ended September 30, 2025 | K-1 |

3

Capitalized terms hereinafter used are defined in the Glossary of Terms or elsewhere in the Circular.

GENERAL DISCLOSURE INFORMATION

No person has been authorized by the Company to give any information or make any representations in connection with the Arrangement herein described other than those contained in this Circular and, if given or made, any such information or representation must not be relied upon as having been authorized by Seabridge or Valor, as applicable.

References to “management” in this Circular mean the executive officers of Seabridge, as applicable. Any statements in this Circular made by or on behalf of management are made in such persons’ capacities as officers of the Company, as applicable, and not in their personal capacities.

A Shareholder should rely only on the information contained in this Circular and should not rely on certain parts of this Circular to the exclusion of others. The information contained in this Circular is accurate only as of the date of this Circular, regardless of the time of delivery of this Circular.

This Circular does not constitute an offer to sell, or a solicitation of an offer to purchase, any securities, by any person in any jurisdiction in which such an offer or solicitation is not authorized or in which the person making such offer or solicitation is not qualified to do so or to any person to whom it is unlawful to make such an offer or solicitation. Neither delivery of this Circular nor any distribution of the securities referred to in this Circular shall, under any circumstances, create an implication that there has been no change in the information set forth herein since the date of this Circular.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING INFORMATION

This Circular and the documents incorporated into this Circular by reference contain forward-looking statements and forward-looking information (collectively, “forward-looking statements”) within the meaning of applicable Canadian and U.S. securities legislation, including the United States Private Securities Litigation Reform Act of 1995. All statements, other than statements of historical fact, included herein including, without limitation, statements with respect to the Arrangement, the covenants of Seabridge, the timing for the implementation of the Arrangement and the potential benefits of the Arrangement, the likelihood of the Arrangement being completed, principal steps of the Arrangement, the timing of future activities of and developments related to, Seabridge and Valor, Seabridge’s and Valor’s anticipated business plans, Shareholder approval of the Arrangement, regulatory approval of the Arrangement, listing of the Valor Shares on the Toronto Stock Exchange (the “TSX”), listing of the Valor Shares on the OTCQB Venture Market (USA), participation of the Shareholders in the Spin-Out Assets, ability of Valor to develop the Spin-Out Assets, the liquidity of Seabridge Shares and Valor Shares following the Effective Time, costs and timing of exploration and development and capital expenditures related thereto, planned exploration activities, success of exploration activities, estimated exploration budgets, market position, financial and business prospects and financial outlooks of Seabridge and Valor are forward-looking statements.

Any statements that involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often but not always using phrases such as “expects”, or “does not expect”, “is expected”, “anticipates” or “does not anticipate”, “plans”, “budget”, “scheduled”, “forecasts”, “estimates”, “believes” or “intends” or variations of such words and phrases or stating that certain actions, events or results “may” or “could”, “would”, “might”, or “will” be taken to occur or be achieved) are not statements of historical fact and may be forward-looking statements and are intended to identify forward-looking statements, which include statements relating to, among other things, the ability of Seabridge or Valor to continue to successfully compete in the market.

4

These forward-looking statements are based on the beliefs of Seabridge’s management, as well as on assumptions, which such management believes to be reasonable based on information currently available at the time such statements were made. However, there can be no assurance that the forward-looking statements will prove to be accurate. Such assumptions and factors include, among other things, the satisfaction of the terms and conditions of the Arrangement including the approval of the Arrangement’s fairness by the Court, and the receipt of the required governmental and regulatory approvals and consents.

By their nature, forward-looking statements are based on assumptions and involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Seabridge or Valor to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Forward-looking statements are subject to a variety of risks, uncertainties and other factors which could cause actual events or results to differ from those expressed or implied by the forward-looking statements, including, without limitation: the Arrangement Agreement may be terminated in certain circumstances, general business, economic, competitive, political, regulatory and social uncertainties, gold price volatility, uncertainty related to mineral exploration properties, risks related to the ability to finance the continued exploration of mineral properties, risks related to Seabridge and Valor not having any proven or provable mineral reserves, history of losses of Seabridge and expectation of future losses for Seabridge and Valor, risks related to factors beyond the control of Seabridge or Valor, limited business history of Valor, risks and uncertainties associated with exploration and mining operations, risks related to the ability to obtain adequate financing for planned development activities, lack of infrastructure at mineral exploration properties, risks and uncertainties relating to the interpretation of drill results and the geology, grade and continuity of mineral deposits, uncertainties related to title to mineral properties and the acquisition of surface rights, risks related to governmental regulations, including environmental laws and regulations and liability and obtaining permits and licences, future changes to environmental laws and regulations, unknown environmental risks for past activities, commodity price fluctuations, risks related to reclamation activities on mineral properties, risks related to political instability and unexpected regulatory change, currency fluctuations and risks associated with a fixed exchange ratio, influence of third party stakeholders, conflicts of interest, risks related to dependence on key individuals, risks related to the involvement of some of the directors and officers of Seabridge and Valor with other natural resource companies, enforceability of claims, the ability to maintain adequate control over financial reporting, risks related to the Seabridge Shares and Valor Shares, including price volatility due to events that may or may not be within such parties’ control, disruptions or changes in the credit or security markets, risks related to joint venture operations, actual results of current exploration activities, reserve and resource estimate risk, actual results of current reclamation activities, conclusions of economic evaluations, changes in project parameters as plans continue to be refined, changes in labour costs or other costs of production, labour disputes and other risks of the mining industry, delays in obtaining governmental approvals or financing or in the completion of development or construction activities, the ability to renew existing licenses or permits or obtain required licenses and permits, mining operational and development risk, litigation risks, speculative nature of gold exploration, risks relating to the possibility that such number of Shareholders may exercise their dissent rights so as to cause the Board to believe that completion of the Arrangement would not be in the best interests of Seabridge, risks related to instability in the global economic climate, and community and non-governmental actions and regulatory risks.

5

This list is not exhaustive of the factors that may affect any of forward-looking statements of Seabridge and Valor. Forward-looking statements are statements about the future and are inherently uncertain. Actual results could differ materially from those projected in the forward-looking statements as a result of the matters set out or incorporated by reference in this Circular generally and certain economic and business factors, some of which may be beyond the control of Seabridge and Valor. Some of the important risks and uncertainties that could affect forward-looking statements are described further below under the heading “Particulars of Other Matters to be Acted Upon – The Arrangement – Arrangement Risk Factors” and in Appendix “G” to this Circular under the heading “Information Regarding Valor – Risk Factors”.

Certain of the forward-looking statements and forward-looking information and other information contained herein concerning the mining industry and Seabridge’s general expectations concerning the mining industry, Seabridge, and Valor, are based on estimates prepared by Seabridge or Valor using data from publicly available industry sources as well as from market research and industry analysis and on assumptions based on data and knowledge of this industry which Seabridge believes to be reasonable. However, although generally indicative of relative market positions, market shares and performance characteristics, these data are inherently imprecise. While Seabridge is not aware of any misstatement regarding any industry data presented herein, the mining industry involves risks and uncertainties that are subject to change based on various factors.

All forward-looking information attributable to Seabridge or Valor, or persons acting on their behalf, is expressly qualified in their entirety by the cautionary statements set forth above. Readers of this Circular are cautioned not to place undue reliance on the forward-looking information contained in this Circular which reflect the analysis of the management of Seabridge and Valor, as applicable, as of the date of this Circular. Neither Seabridge nor Valor undertakes any obligation to update forward-looking information except as required by applicable securities laws.

At the Meeting, you will be asked to consider and, if deemed advisable, approve the Arrangement Resolution, the full text of which is reproduced in Appendix “A” of this Circular in respect of the Arrangement. If the Arrangement Resolution is passed, Seabridge Shareholders will also be asked to consider and, if deemed advisable, approve the Valor Incentive Plan Resolution, the full text of which is set out under the heading “Particulars of Matters to be Acted Upon – Valor Incentive Plan Resolution” on page 50.

DATE OF INFORMATION

Information contained in this Circular is as at March 30, 2026, unless otherwise indicated.

REPORTING CURRENCIES AND ACCOUNTING PRINCIPLES

The historical financial statements of Valor contained in this Circular are reported in Canadian dollars and have been prepared in accordance with IFRS. All references to dollar amounts in this Circular are to Canadian dollars unless stated otherwise or the context otherwise requires.

6

GLOSSARY

For the purposes of this section, the following terms shall have the meanings ascribed thereto:

“ACB” has the meaning ascribed thereto under “Principal Canadian Federal Income Tax Consequences – Holders Resident in Canada – Alterations to Share Structure and the Seabridge Articles and Re-Designation of the Seabridge Shares”;

“allowable capital loss” has the meaning ascribed thereto under “Principal Canadian Federal Income Tax Consequences – Holders Resident in Canada – Taxation of Capital Gains and Capital Losses”;

“Arrangement” means an arrangement under the provisions of Section 192 of the CBCA, on the terms and conditions set forth in the Plan of Arrangement;

“Arrangement Agreement” means the arrangement agreement between Seabridge and Valor dated March 23, 2026, including the Exhibits and the Appendices thereto as the same may be supplemented or amended from time to time;

“Arrangement Provisions” means Part XV, Section 192 of the Act;

“Arrangement Resolution” means the resolution to be approved by the Shareholders, substantially in the form and content set out in Appendix “A” to this Circular;

“Award” has the meaning ascribed thereto under “Appendix ‘G’ – Information Regarding Valor – Valor Incentive Plan”;

“Beneficial Seabridge Shareholder” means a beneficial owner of Seabridge Shares who holds such shares through an Intermediary and whose name does not appear on the share register of Seabridge as the registered holder of such shares;

“Board” means the board of directors of Seabridge;

“Business Day” means a day which is not a Saturday, Sunday or statutory holiday in Toronto, Ontario;

“CBCA” means Canada Business Corporations Act and the regulations promulgated thereunder, as amended from time to time;

“CDS” means the Canadian Depository for Securities; “CEO” means the Chief Executive Officer;

“CFO” means the Chief Financial Officer; “Chairman” means the chairman of the Board;

“Circular” means this management information circular, together with the accompanying Notice of Meeting and form of proxy;

“Code of Conduct and Ethics” means Valor’s code of business conduct and ethics as outlined under the heading “Code of Ethics, Governance Policies and Corporate Policies on page G-27 of Appendix “G”;

“Convention” has the meaning ascribed thereto under “Principal Canadian Federal Income Tax Consequences – Holders Not Resident in Canada - Taxation of Dividends”;

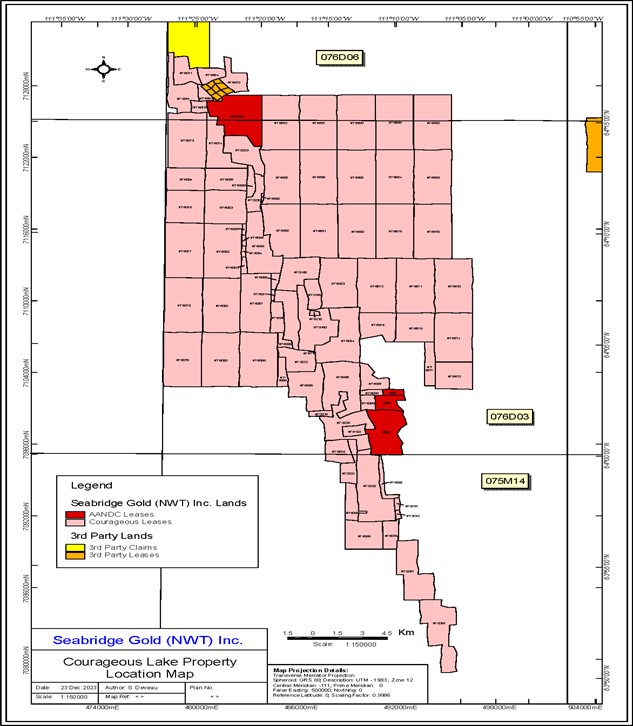

“Courageous Lake Project” or the “Project” means the Courageous Lake project comprising 50,228 hectares of mineral leases and mining claims located 240 km northeast of Yellowknife, NWT, currently held indirectly by Seabridge through SNWT and which will be owned and advanced by Valor indirectly through SNWT after the Arrangement;

7

“Court” means the Supreme Court of British Columbia;

“CRA” means the Canada Revenue Agency;

“Demand for Payment” has the meaning ascribed thereto under “Particulars of Other Matters to be Acted Upon – The Arrangement – Dissent Rights”;

“Depositary” means Computershare Investor Services Inc.;

“Director” means a director of Seabridge;

“Dissent Procedures” means the rules pertaining to the exercise of Dissent Rights as set forth in Section 190 of Part XV of the CBCA and Article 5 of the Plan of Arrangement;

“Dissent Rights” means the rights of dissent granted in favour of registered holders of Seabridge Shares in accordance with Article 5 of the Plan of Arrangement;

“Dissent Share” has the meaning ascribed thereto under “Particulars of Other Matters to be Acted Upon – The Arrangement – Steps in the Arrangement”;

“Dissenting Non-Resident Holder” has the meaning ascribed thereto under “Principal Canadian Federal Income Tax Consequences – Holders Not Resident in Canada – Dissenting Non-Resident Holders”;

“Dissenting Resident Holder” has the meaning ascribed thereto under “Principal Canadian Federal Income Tax Consequences – Holders Resident in Canada – Dissenting Shareholders”;

“Dissenting Shareholder” means a registered holder of Seabridge Shares who dissents in respect of the Arrangement in strict compliance with the Dissent Procedures and who has not withdrawn or been deemed to have withdrawn such exercise of Dissent Rights;

“DRS Advices” means Direct Registration System Advices;

“DSU” means deferred share units granted pursuant to the Valor Incentive Plan;

“Effective Date” means the date upon which the Arrangement becomes effective in accordance with the Plan of Arrangement and the Final Order, as the Board may determine;

“Effective Time” means 12:01 a.m. Pacific Time on the Effective Date or such other time on the Effective Date as agreed to in writing by Seabridge or Valor;

“Electing U.S. Shareholder” has the meaning ascribed thereto under “Material United States Federal Income Tax Considerations – U.S. Federal Income Tax Considerations Applicable to U.S. Holders Regarding the Arrangement – Potential Application of the Passive Foreign Investment Company Rules to the Arrangement”;

“Eligible Director” has the meaning ascribed thereto under “Appendix ‘G’ – Information Regarding Valor – Valor Incentive Plan “;

“ESG” means environmental, social and governance;

“Exchanged Securities” has the meaning ascribed thereto under “Particulars of Other Matters to be Acted Upon – The Arrangement – U.S. Securities Laws and Resale of Securities”;

“Executives” has the meaning ascribed thereto under “Appendix ‘G’ – Information Regarding Valor – Corporate Governance Disclosure – Compensation Committee”;

8

“Extension Period” has the meaning ascribed thereto under “Appendix ‘G’ – Information Regarding Valor – Valor Incentive Plan “;

“Fairness Opinion” means the fairness opinion delivered by RBC to the Board, a full copy of which is attached as Appendix “F”;

“Final Order” means the final order of the Court approving the Arrangement;

“First Tax Return” has the meaning ascribed thereto under “Principal Canadian Federal Income Tax Consequences – Holders Resident in Canada – Eligibility for Investment – New Seabridge Shares and Valor Shares”;

“Foreign Tax Credit Regulations” has the meaning ascribed thereto under “Material United States Federal Income Tax Considerations – Additional Tax Considerations – Foreign Tax Credit”;

“GAAP” means the Generally Accepted Accounting Principles;

“Gold Stream Agreement” means the Gold Purchase Agreement to be entered into between Seabridge and Valor on the Effective Date, in substantially the form attached hereto as Schedule “3” to the Arrangement Agreement, pursuant to which Valor, in consideration for the payment by Seabridge of an upfront deposit of US$3,591,000 (approximately C$4,900,000), shall sell and deliver to Seabridge 10% of the refined gold produced from the Courageous Lake Project at a cash Purchase Price (as defined in the Gold Stream Agreement) of US$4,000 per ounce, in each case when the quarterly average market price of gold equals or exceeds US$4,000 per ounce, provided that Valor shall have no right to convert, buy back, or otherwise reacquire Seabridge’s rights under the agreement;

“Guarantees” means, collectively, (i) the Guarantee Agreement dated July 26, 2002 between Seabridge and Newmont, pursuant to which Seabridge guarantees the secured obligations of SNWT under an Instrument of Delivery dated effective July 26, 2002 between SNWT and Newmont relating to a SNWT Debenture dated July 26, 2002 held by Newmont in the principal amount of US$21,420,000, which was subsequently assigned by Newmont to Franco Nevada, and (ii) the Guarantee Agreement dated July 26, 2002 between Seabridge and Total Resources, pursuant to which Seabridge guarantees the secured obligations of SNWT under an Instrument of Delivery dated effective July 26, 2002 between SNWT and Total Resources relating to a SNWT Debenture dated July 26, 2002 held by Total Resources in the principal amount of US$20,580,000;

“Holder” has the meaning ascribed thereto under “Principal Canadian Federal Income Tax Consequences”;

“ICD” means the Institute of Corporate Directors;

“IFRS” means the International Financial Reporting Standards;

“Intercorporate Debt” has the meaning ascribed thereto under “Particulars of Other Matters to be Acted Upon – The Arrangement – The Arrangement Agreement”;

“Interim Order” means the interim order of the Court approving the Meeting to approve the Arrangement;

“IRS” has the meaning ascribed thereto under “Material United States Federal Income Tax Considerations”;

“Intermediary” has the meaning ascribed thereto under “Non-Registered Holders”;

9

“KSM” means KSM Mining Inc, a company existing under the laws of British Columbia and a wholly owned subsidiary of Seabridge;

“KSM Project” means the Kerr-Sulphurets-Mitchell project comprising mining leases and mineral claims located in British Columbia, Canada, held indirectly by Seabridge through KSM;

“Latest RSU Expiry Date” has the meaning ascribed thereto under “Appendix ‘G’ – Information Regarding Valor – Valor Incentive Plan “;

“LTI” has the meaning ascribed thereto under “Appendix ‘G’ - Information Regarding Valor - Executive Compensation”;

“Management Proxyholders” has the meaning ascribed thereto under “Appointment of Proxyholder”;

“Mark-to-Market Election” has the meaning ascribed thereto under “Material United States Federal Income Tax Considerations – U.S. Federal Income Tax Considerations Applicable to U.S. Holders Regarding the Arrangement – Potential Application of the Passive Foreign Investment Company Rules to the Arrangement”;

“MD&A” means management’s discussion and analysis relating to Valor’s financial statements;

“Meeting” means the special meeting of Shareholders, including any adjournment or postponement thereof, to be held on May 22, 2026 for the purposes of, among other things, obtaining Shareholder approval of the Arrangement;

“MLI” has the meaning ascribed thereto under “Principal Canadian Federal Income Tax Consequences – Holders Not Resident in Canada - Exchange of Old Seabridge Shares for New Seabridge Shares and Valor Shares”;

“Named Executive Officer” or “NEO” has the meaning ascribed thereto under “Executive Compensation “;

“New Seabridge Shares” has the meaning ascribed thereto under “Summary of Circular – Steps in the Arrangement”;

“Newmont” means Newmont Canada Limited;

“Franco Nevada” means Franco Nevada Canada Corporation;

“NI 52-110” means National Instrument 52-110 – Audit Committees;

“Non-Electing Shareholder” has the meaning ascribed thereto under “Material United States Federal Income Tax Considerations – U.S. Federal Income Tax Considerations Applicable to U.S. Holders Regarding the Arrangement – Potential Application of the Passive Foreign Investment Company Rules to the Arrangement”;

“NOBO” has the meaning ascribed thereto under “Non-Registered Holders”;

“Non-Resident Holder” has the meaning ascribed thereto under “Principal Canadian Federal Income Tax Consequences – Holders Not Resident in Canada”;

“Non-Registered Shareholder” means a Seabridge Shareholder who is not a Registered Seabridge Shareholder;

“Notice of Meeting” means the notice of meeting to be sent to Shareholders in connection with the Meeting;

10

“NYSE” means the New York Stock Exchange;

“OBO” has the meaning ascribed thereto under “Non-Registered Holders”;

“Offer to Pay” has the meaning ascribed thereto under “Particulars of Other Matters to be Acted Upon – The Arrangement – Dissent Rights”;

“Old Seabridge Shares” has the meaning ascribed thereto under “Particulars of Other Matters to be Acted Upon – The Arrangement – Steps in the Arrangement”;

“Order” has the meaning ascribed thereto under “Appendix ‘G’ – Information Regarding Valor – Directors and Officers - Corporate Cease Trade Orders, Bankruptcies, Penalties or Sanctions or Individual Bankruptcies”;

“party” means either Seabridge or Valor and “parties” means, collectively, Seabridge and Valor;

“person” means and includes a party, individuals, corporations, bodies corporate, limited or general partnerships, joint stock companies, limited liability corporations, joint ventures, associations, companies, trusts, banks, trust companies, government or any other type of organization, whether or not a legal entity;

“PFIC” has the meaning ascribed thereto under “Material United States Federal Income Tax Considerations – U.S. Federal Income Tax Considerations Applicable to U.S. Holders Regarding the Arrangement – Potential Application of the Passive Foreign Investment Company Rules to the Arrangement”;

“PFIC asset test” has the meaning ascribed thereto under “Material United States Federal Income Tax Considerations – U.S. Federal Income Tax Considerations Applicable to U.S. Holders Regarding the Arrangement – Potential Application of the Passive Foreign Investment Company Rules to the Arrangement”;

“PFIC income test” has the meaning ascribed thereto under “Material United States Federal Income Tax Considerations – U.S. Federal Income Tax Considerations Applicable to U.S. Holders Regarding the Arrangement – Potential Application of the Passive Foreign Investment Company Rules to the Arrangement”;

“Plan of Arrangement” means the plan of arrangement attached as Schedule “1” to the Arrangement Agreement and any amendment or variation thereto made in accordance thereof;

“QEF” has the meaning ascribed thereto under “Material United States Federal Income Tax Considerations – U.S. Federal Income Tax Considerations Applicable to U.S. Holders Regarding the Arrangement – Potential Application of the Passive Foreign Investment Company Rules to the Arrangement”;

“QEF Election” has the meaning ascribed thereto under “Material United States Federal Income Tax Considerations – U.S. Federal Income Tax Considerations Applicable to U.S. Holders Regarding the Arrangement – Potential Application of the Passive Foreign Investment Company Rules to the Arrangement”;

“PUC” has the meaning ascribed thereto under “Principal Canadian Federal Income Tax Consequences – Holders Resident in Canada - Exchange of Old Seabridge Shares for New Seabridge Shares and Valor Shares”;

“RBC” means RBC Dominion Securities Inc.;

11

“RDSP” has the meaning ascribed thereto under “Principal Canadian Federal Income Tax Consequences – Holders Resident in Canada - Eligibility for Investment – New Seabridge Shares and Valor Shares “;

“Record Date” has the meaning ascribed thereto under “Voting Securities and Principal Holders Thereof”;

“Registered Plans” has the meaning ascribed thereto under “Principal Canadian Federal Income Tax Consequences – Holders Resident in Canada - Eligibility for Investment – New Seabridge Shares and Valor Shares “;

“Registered Seabridge Shareholder” means a registered holder of Seabridge Shares;

“Resident Holder” has the meaning ascribed thereto under “Principal Canadian Federal Income Tax Consequences – Holders Resident in Canada”;

“RESP” has the meaning ascribed thereto under “Principal Canadian Federal Income Tax Consequences – Holders Resident in Canada - Eligibility for Investment – New Seabridge Shares and Valor Shares “;

“RRIF” has the meaning ascribed thereto under “Principal Canadian Federal Income Tax Consequences – Holders Resident in Canada - Eligibility for Investment – New Seabridge Shares and Valor Shares “;

“RRSP” has the meaning ascribed thereto under “Principal Canadian Federal Income Tax Consequences – Holders Resident in Canada - Eligibility for Investment – New Seabridge Shares and Valor Shares “;

“RSU” means restricted share units granted pursuant to the Valor Incentive Plan;

“RSU Participant” means a holder of RSUs under the Valor Incentive Plan;

“Seabridge” or “Company” means Seabridge Gold Inc.;

“Seabridge Articles” means the articles of the Company;

“Seabridge Class A Shares” has the meaning ascribed thereto under “Summary of Circular – Steps in the Arrangement”;

“Seabridge Shareholders” or “Shareholders” means the holders of Seabridge Shares;

“Seabridge Shares”, “Seabridge Common Shares” or “Shares” means the common shares of Seabridge;

“Section 3(a)(10) Exemption” means the exemption from the registration requirements of the U.S. Securities Act provided by Section 3(a)(10) of the U.S. Securities Act;

“securities” has the meaning ascribed thereto under “Appendix ‘G’ – Information Regarding Valor – Corporate Governance Disclosure - Code of Ethics, Governance Policies and Corporate Policies “;

“Securities Laws” means all applicable securities laws of Canada and the United States, including the Securities Act, the U.S. Securities Act and the U.S. Exchange Act, together with all other applicable provincial and state securities laws, rules and regulations and published policies thereunder, as now in effect and as they may be promulgated or amended from time to time;

12

“Security Holders” means Seabridge Shareholders; for certain procedural descriptions following the Effective Time, the term may also refer to holders of Valor Shares as the context requires;

“SEDAR+” means the System for Electronic Document Analysis and Retrieval;

“Share Exchange” has the meaning ascribed thereto under “Principal Canadian Federal Income Tax Consequences – Holders Resident in Canada - Exchange of Old Seabridge Shares for New Seabridge Shares and Valor Shares”;

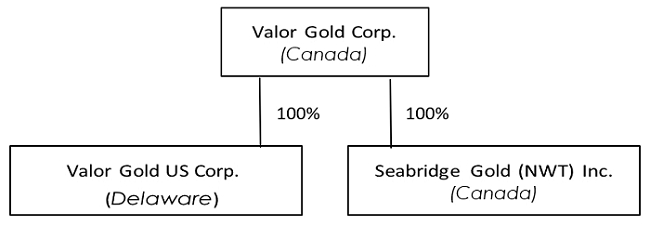

“SNWT” means Seabridge Gold (NWT) Inc., a company existing under the laws of Canada and a wholly owned subsidiary of Seabridge;

“Spin-Out Assets” means the 100% interest of Seabridge in the Courageous Lake Project;

“STI” has the meaning ascribed thereto under “Appendix ‘G’ – Information Regarding Valor – Executive Compensation”;

“Subject Securities” has the meaning ascribed thereto under “Principal Canadian Federal Income Tax Consequences”;

“Subsidiary PFIC” has the meaning ascribed thereto under “Material United States Federal Income Tax Considerations – U.S. Federal Income Tax Considerations Applicable to U.S. Holders Regarding the Ownership and Disposition of New Seabridge Shares and Valor Spin-Out Shares – Potential Application of the Passive Foreign Investment Company Rules to the Arrangement – Passive Foreign Investment Company Rules”;

“Tax Act” means the Income Tax Act (Canada);

“Tax Proposals” has the meaning ascribed thereto under “Principal Canadian Federal Income Tax Consequences”;

“taxable capital gain” has the meaning ascribed thereto under “Principal Canadian Federal Income Tax Consequences – Holders Resident in Canada – Taxation of Capital Gains and Capital Losses”;

“Technical Report” has the meaning ascribed thereto under “Appendix ‘G’ – Information Regarding Valor – Description of the Courageous Lake Project”;

“TFSA” has the meaning ascribed thereto under “Principal Canadian Federal Income Tax Consequences – Holders Resident in Canada - Eligibility for Investment – New Seabridge Shares and Valor Shares “;

“Total Resources” means Total Resources (Canada) Limited;

“Treasury Regulations” has the meaning ascribed thereto under “Material United States Federal Income Tax Considerations”;

“TSX” means the Toronto Stock Exchange;

“U.S. Exchange Act” means the United States Securities Exchange Act of 1934, as amended;

“U.S. Holder” has the meaning ascribed thereto under “Material United States Federal Income Tax Considerations – U.S. Holders”;

“U.S. Securities Act” means the United States Securities Act of 1933, as amended;

13

“U.S. Tax Code” has the meaning ascribed thereto under “Material United States Federal Income Tax Considerations”;

“Valor” means “Valor Gold Corp.”, a company existing under the laws of Canada and a wholly owned subsidiary of Seabridge;

“Valor Board” means the board of directors of Valor;

“Valor Incentive Plan” has the meaning ascribed thereto under “Appendix ‘G’ – Information Regarding Valor – Consolidated Capitalization”;

““Valor Incentive Plan Resolution” means the ordinary resolution of Seabridge Shareholders approving the Valor Incentive Plan, as it may be amended or varied at or at any time prior to the Meeting, to be considered at the Meeting, and the full text of which is set out under “Particulars of Matters to be Acted Upon – Valor Incentive Plan Resolution”;

“Valor Shareholders” means the holders of Valor Shares;

“Valor Shares” means the common shares of Valor; and

“Valor Spin-Out Shares” means the Valor Shares to be issued to Seabridge as consideration for the common shares of Valor, which shares will be subsequently distributed by Seabridge to Seabridge Shareholders in accordance with the Plan of Arrangement.

14

SUMMARY OF CIRCULAR

The following summary is qualified in its entirety by the more detailed information appearing elsewhere in this Circular, including the Appendices which form part of this Circular. Capitalized terms used in this Summary are defined in the Glossary of Terms immediately preceding this summary.

THE MEETING

The Meeting will be held in Salon 1, 19th Floor, Fairmont Royal York Hotel, 100 Front Street West, Toronto, Ontario, Canada on May 22, 2026, at 10:00 a.m. Eastern Daylight Time for the purposes set forth in the Notice of Meeting. At the Meeting, Seabridge Shareholders will consider and vote upon the Arrangement under section 192 of the CBCA involving Seabridge, its securityholders and Valor pursuant to the Arrangement Resolution. See “Particulars of Other Matters to be Acted Upon” on page 26. If the Arrangement Resolution is passed, Seabridge Shareholders will also be asked to consider and, if deemed advisable, approve the Valor Incentive Plan Resolution, the full text of which is set out under the heading “Particulars of Matters to be Acted Upon – Valor Incentive Plan Resolution” on page 50.

THE ARRANGEMENT

The purpose of the Arrangement and the related transactions is to reorganize Seabridge into two separate companies:

| 1. | Seabridge, which will continue to advance the KSM Project and its remaining exploration portfolio; and |

| 2. | Valor, which will focus on the exploration and development of the Courageous Lake Project. |

The Arrangement would result in, among other things, participating Seabridge Shareholders holding, immediately following completion of the Arrangement, the New Seabridge Shares and Valor Shares in proportion to their holdings of Seabridge Shares at the Effective Time.

FAIRNESS OPINION

Based upon and subject to the assumptions, limitations and qualifications set out in the Fairness Opinion, RBC is of the opinion that, as of March 4, 2026, the consideration to be received under the Arrangement is fair, from a financial point of view, to the Seabridge Shareholders.

The full text of the Fairness Opinion, setting out the assumptions made, matters considered and limitations and qualifications on the review undertaken in connection with the Fairness Opinion, is attached as Appendix “F” to this Circular. The summary of the Fairness Opinion in this Circular is qualified in its entirety by reference to the full text of the Fairness Opinion.

15

STEPS IN THE ARRANGEMENT

Under the Plan of Arrangement, commencing at the Effective Time, each of the events set out below shall occur and shall be deemed to occur in the following sequence or as otherwise provided below or herein, without any further act or formality, notwithstanding anything contained in the provisions attaching to any of the securities of Seabridge or Valor, but subject to the provision of Article 5 of the Arrangement Agreement:

| (a) | each Seabridge Common Share in respect of which a Seabridge Shareholder has exercised Dissent Rights and for which the Seabridge Shareholder is ultimately entitled to be paid fair value (each a “Dissent Share”) shall be deemed to have been repurchased by Seabridge for cancellation in consideration for a debt-claim against Seabridge to be paid the fair value of such Dissent Share in accordance with Article 3 of the Plan of Arrangement, net of any applicable withholding tax, and such Dissent Share shall thereupon be cancelled; |

| (b) | the share capital of Seabridge shall be reorganized by: |

| (i) | renaming and redesignating all of the issued and unissued Seabridge Common Shares as “Class A common shares without par value” and amending the rights and restrictions attached to those shares to provide the holders thereof with two (2) votes in respect of each share held, being the “Seabridge Class A Shares”; and |

| (ii) | creating a new class consisting of an unlimited number of “common shares without par value” with terms and rights and restrictions identical to those of the Seabridge Common Shares (except each share will provide the holder with one (1) vote instead of two (2)) immediately prior to the Effective Time, being the “New Seabridge Shares”; |

| (c) | the Seabridge Articles shall be amended to reflect the alterations in Section 2.1(b) of the Plan of Arrangement; |

| (d) | (i) each issued and outstanding Seabridge Class A Share outstanding on the close of business on the Business Day immediately preceding the Effective Date held by a Seabridge Shareholder shall be exchanged, as part of the reorganization of the share capital of Seabridge and in accordance with Section 86 of the Tax Act, for: (A) one New Seabridge Share; and (B) that number or fraction of Valor Shares equal to such Shareholder’s pro rata portion of the 55,000,000 Valor Shares held by Seabridge on the close of business on the Business Day immediately preceding the Effective Date divided by the number of Seabridge Class A Shares held by such Seabridge Shareholder immediately before the exchange described in this paragraph; (ii) the holders of the Seabridge Class A Shares will be removed from the central securities register of Seabridge as the holders of such Seabridge Class A Shares and will be added to the central securities register of Seabridge as the holders of the number of New Seabridge Shares that they have received on the exchange set forth in Section 2.1(d) of the Plan of Arrangement, and (iii) the Valor Shares transferred to the then holders of the Seabridge Class A Shares will be registered in the name of the former holders of the Seabridge Class A Shares and Seabridge will provide Valor and its registrar and transfer agent notice to make the appropriate entries in the central securities register of Valor; |

| (e) | all of the issued Seabridge Class A Shares shall be cancelled with the appropriate entries being made in the central securities register of Seabridge, and the aggregate paid-up capital (as that term is used for purposes of the Tax Act) of the New Seabridge Shares will be equal to that of the Seabridge Common Shares immediately prior to the Effective Time less the fair market value of the Valor Shares distributed pursuant to Section 2.1(d) of the Plan of Arrangement; and |

| (f) | the Seabridge Articles shall be amended to reflect the alteration in Section 2.1(e) of the Plan of Arrangement. |

See “Particulars of Other Matters to be Acted Upon – The Arrangement – Steps in the Arrangement” on page 28.

16

RECOMMENDATION OF THE BOARD

The Board, having reviewed the Plan of Arrangement and related transactions and considered, among other things, the reasons for the Arrangement, has unanimously determined that the Arrangement is in the best interests of Seabridge and the Seabridge Shareholders. The Board recommends that Seabridge Shareholders vote FOR the Arrangement Resolution.

See further details under the section entitled “Particulars of Other Matters to be Acted Upon – The Arrangement – Recommendation of the Board” on page 29.

CONDITIONS TO THE ARRANGEMENT

Completion of the Arrangement is subject to a number of specified mutual conditions being met on or before the Effective Time, including, but not limited to:

| (a) | the Interim Order shall have been granted in form and substance satisfactory to Seabridge; |

| (b) | the Arrangement Resolution, with or without amendment, shall have been approved at the Meeting, in accordance with the Interim Order; |

| (c) | the Court shall have determined that the terms and conditions of the Arrangement are substantively and procedurally fair to the Seabridge Shareholders and the Final Order shall have been granted in form and substance satisfactory to Seabridge, and shall not have been set aside or modified in a manner unacceptable to Seabridge, on appeal or otherwise; |

| (d) | the Issuable Securities (as defined in the Arrangement Agreement) to be issued in the United States pursuant to the Arrangement shall be issued in accordance with and exempt from registration requirements under the U.S. Securities Act provided by Section 3(a)(10) thereunder; |

| (e) | Seabridge shall have made a cash payment to Valor in the amount of C$10,000,000 in consideration for the following: |

| (i) | C$5,100,000 in respect of the issuance of 700,000 common shares of Valor to Seabridge; and |

| (ii) | C$4,900,000 as a deposit paid in consideration for the entering into of the Gold Stream Agreement; |

| (f) | Seabridge and Valor shall have executed and delivered the Gold Stream Agreement; |

| (g) | Seabridge shall have been fully, unconditionally, and irrevocably released and discharged from all of its obligations, liabilities, and duties as guarantor under the Guarantees, effective as of the Effective Time, pursuant to written agreements executed by Franco Nevada and Total Resources, respectively; |

| (h) | Seabridge shall have transferred all of the issued and outstanding common shares of SNWT to Valor in consideration for Valor issuing 54,299,900 common shares to Seabridge; |

17

| (i) | the Intercorporate Debt shall have been discharged, released or otherwise settled by Seabridge; |

| (j) | the TSX and the NYSE shall have conditionally approved the Arrangement, including the listing of the New Seabridge Shares in substitution for the Seabridge Common Shares as of the Effective Date, subject to compliance with the requirements of the TSX and the NYSE; |

| (k) | the TSX shall have conditionally approved the Arrangement, including the listing of the Valor Shares before the end of Valor’s taxation year, as defined in the Tax Act, that includes the exchange referred to in section 2.1(d) of the Plan of Arrangement, subject to the requirements of the TSX; |

| (l) | the number of Seabridge Common Shares held by the Seabridge Shareholders that have validly exercised Dissent Rights (and not withdrawn such exercise) shall not exceed 1% of the Seabridge Common Shares issued and outstanding as of the date hereof; |

| (m) | all governmental, court, regulatory, third party and other approvals, consents, expiry of waiting periods, waivers, permits, exemptions, orders and agreements and all amendments and modifications to, and terminations of, agreements, indentures and arrangements considered by Seabridge to be necessary or desirable for the Arrangement to become effective shall have been obtained or received on terms that are satisfactory to Seabridge; |

| (n) | no action shall have been instituted and be continuing on the Effective Date for an injunction to restrain, a declaratory judgment in respect of, or damages on account of or relating to the Arrangement and there shall not be in force any order or decree restraining or enjoining the consummation of the transactions contemplated by the Arrangement Agreement and no cease trading or similar order with respect to any securities of any of the parties shall have been issued and remain outstanding; |

| (o) | none of the consents, orders, rulings, approvals or assurances required for the implementation of the Arrangement shall contain terms or conditions or require undertakings or security deemed unsatisfactory or unacceptable by Seabridge; |

| (p) | no law, regulation or policy shall have been proposed, enacted, promulgated or applied that interferes or is inconsistent with the completion of the Arrangement and Plan of Arrangement; and |

| (q) | the Arrangement Agreement shall not have been terminated pursuant to Section 6.2 of the Arrangement Agreement. |

See further details under “Particulars of Other Matters to be Acted Upon – The Arrangement – The Arrangement Agreement – Conditions to the Arrangement” on page 31.

COURT APPROVAL

An arrangement under the CBCA requires approval of the Court. Prior to mailing this Circular, Seabridge obtained the Interim Order, which provides for the calling and holding of the Meeting, Dissent Rights and certain other procedural matters. A copy of the Interim Order is attached as Appendix “C”.

18

Subject to the approval of the Arrangement Resolution by Seabridge Shareholders at the Meeting, the hearing for the Final Order is currently scheduled to take place on May 27, 2026 at 9:45 a.m. Pacific Time in Vancouver, British Columbia. At the hearing, any Security Holder who wishes to participate or be represented or present arguments or evidence may do so by serving a response to petition in compliance with the Interim Order.

See further details under “Particulars of Other Matters to be Acted Upon – The Arrangement – The Arrangement Agreement – Court Approval of the Arrangement” on page 34.

REGULATORY APPROVALS

The Seabridge Shares are listed and posted for trading on the TSX. The Arrangement is subject to the acceptance of the TSX and Seabridge will not proceed with the Arrangement if regulatory acceptance or approval is not obtained.

Seabridge intends to apply to the TSX to have the Valor Shares listed and posted for trading on the TSX. Listing is subject to the approval of the TSX. There can be no assurance as to if, or when, the Valor Shares will be listed or traded on the TSX or any other stock exchange. It is a condition of the Arrangement that the TSX shall have conditionally approved the listing of the Valor Shares, however such condition may be mutually waived by Seabridge and Valor at any time.

SEABRIDGE FOLLOWING THE ARRANGEMENT

Following completion of the Arrangement, Seabridge will continue its current business as a mineral acquisition and exploration company. The New Seabridge Shares will trade on the TSX under the symbol “SEA” and on the NYSE under the symbol “SA”.

VALOR FOLLOWING THE ARRANGEMENT

Upon completion of the Arrangement, Valor will own and operate the Spin-Out Assets. For a detailed description of Valor following the completion of the Arrangement, see Appendix “G” – Information Regarding Valor.

CANADIAN SECURITIES LAWS AND RESALE OF SECURITIES

Valor will be a reporting issuer in each of the provinces and territories in which Seabridge is a reporting issuer on completion of the Arrangement, and Valor intends to apply to the TSX to have the Valor Shares listed and posted for trading on the TSX.

The issuance of the Valor Shares to Shareholders pursuant to the Arrangement will constitute a distribution of securities which is exempt from the registration and prospectus requirements of Canadian securities legislation. The Valor Shares received by Shareholders pursuant to the Arrangement may be resold in each of the provinces and territories of Canada provided that (i) the trade is not a “control distribution” as defined in National Instrument 45-102 - Resale of Securities; (ii) no unusual effort is made to prepare the market or create a demand for those securities; (iii) no extraordinary commission or consideration is paid in respect of that sale; and (iv) if the selling securityholder is an insider or officer of Valor, the selling securityholder has no reasonable grounds to believe that Valor is in default of securities legislation.

See further details under “Particulars of Other Matters to be Acted Upon – The Arrangement – Canadian Securities Laws and Resale of Securities” on page 36.

19

U.S. SECURITIES LAWS AND RESALE OF SECURITIES

The Exchanged Securities to be received by Security Holders pursuant to the Arrangement have not been and will not be registered under the U.S. Securities Act or applicable state securities laws, and are being issued in reliance on the exemption from the registration requirements of the U.S. Securities Act set forth in Section 3(a)(10) thereof on the basis of the approval of the Court, and similar exemptions from registration under applicable state securities laws. Section 3(a)(10) of the U.S. Securities Act exempts the issuance of any securities issued in exchange for one or more bona fide outstanding securities from the general requirement of registration under the U.S. Securities Act where the terms and conditions of the issuance and exchange of such securities have been approved by a court of competent jurisdiction that is expressly authorized by law to grant such approval, after a hearing upon the procedural and substantive fairness of the terms and conditions of such issuance and exchange to those to whom the securities will be issued, at which all persons to whom it is proposed to issue the securities have the right to appear and receive timely and adequate notice thereof. The Court is authorized to conduct a hearing at which the procedural and substantive fairness of the terms and conditions of the Arrangement will be considered. The Court issued the Interim Order on April 10, 2026 and, subject to the approval of the Arrangement by the Shareholders, a hearing of the application for the Final Order will be held on or about May 27, 2026 at 9:45 a.m. Pacific Time. All Security Holders are entitled to appear and be heard at this hearing and there will not be any improper impediments to the appearance by those securityholders at the hearing. The Final Order will constitute a basis for the exemption from the registration requirements of the U.S. Securities Act provided by Section 3(a)(10) thereof and comparable state securities laws with respect to the Exchanged Securities. Prior to the hearing on the Final Order, the Court will be informed of this effect of the Final Order. The Final Order approving the Arrangement that is obtained from the Court will state substantially to the effect that the terms and conditions of the Arrangement are approved by the Court as being fair, substantively and procedurally, to the Security Holders entitled to receive Exchanged Securities.

The New Seabridge Shares and the Valor Spin-Out Shares will be freely tradable under U.S. federal Securities Laws, except by persons who are “affiliates” of Seabridge or Valor, as applicable, within 90 days prior to completion of the Arrangement or “affiliates” of Seabridge or Valor, as applicable, following completion of the Arrangement. Persons who may be deemed to be “affiliates” of an issuer include individuals or entities that control, are controlled by, or are under common control with, the issuer, and generally include executive officers and directors of the issuer as well as principal shareholders of the issuer.

See further details under “Particulars of Other Matters to be Acted Upon – The Arrangement – U.S. Securities Laws and Resale of Securities” on page 37.

SIGNIFICANT POSITIONS AND SHAREHOLDINGS

In considering the recommendation of the Board with respect to the Arrangement, Shareholders should be aware that certain members of Seabridge’s senior management and the Board have certain interests in connection with the Arrangement that may present them with actual or potential conflicts of interest in connection with the Arrangement.

See further details under “Particulars of Other Matters to be Acted Upon – The Arrangement – Significant Positions and Shareholdings” on page 39.

RISK FACTORS

Shareholders should be aware that there are various known and unknown risk factors in connection with the Arrangement and the ownership of New Seabridge Shares and Valor Shares following the completion of the Arrangement. Shareholders should carefully consider the risks identified in this Circular under the heading “Particulars of Other Matters to be Acted Upon – The Arrangement – Arrangement Risk Factors” and under Appendix “G” – “Information Regarding Valor – Risk Factors” before deciding whether or not to approve the Arrangement Resolution.

20

DISSENT RIGHTS

Registered Seabridge Shareholders are entitled to exercise Dissent Rights by providing written notice to the Company no later than 4:00 p.m. Pacific Time on May 20, 2026 or two Business Days immediately preceding any date to which the Meeting may be postponed or adjourned in the manner described under the heading “Dissent Rights”. If a Seabridge Shareholder exercises Dissent Rights in strict compliance with the Dissent Procedures (attached as Appendix “E” hereto) and Interim Order and the Arrangement is completed, such Dissenting Shareholder is entitled to be paid the fair value of the Seabridge Shares with respect to which the Dissent Rights were exercised, calculated as of the close of business the day before the approval of the Arrangement Resolution. Seabridge Shareholders should carefully read the section of this Circular entitled “Dissent Rights” and consult with their advisors if they wish to exercise Dissent Rights.

CERTAIN CANADIAN INCOME TAX CONSIDERATIONS

A summary of certain Canadian federal income tax considerations for Seabridge Shareholders who participate in the Arrangement is set out under the heading “Principal Canadian Federal Income Tax Consequences”.

Seabridge Shareholders should carefully review the tax considerations applicable to them under the Arrangement and are urged to consult their own legal, tax and financial advisors in regard to their particular circumstances.

CERTAIN U.S. FEDERAL INCOME TAX CONSIDERATIONS

A summary of certain U.S. federal income tax considerations for Seabridge Shareholders who are U.S. taxpayers and who participate in the Arrangement is set out under the heading “Material U.S. Federal Income Tax Considerations”.

Seabridge Shareholders should carefully review the tax considerations applicable to them under the Arrangement and are urged to consult their own legal, tax and financial advisors in regard to their particular circumstances.

FINANCIAL STATEMENTS OF SEABRIDGE AND VALOR

The financial statements of Seabridge for the year ending December 31, 2025 are available on Seabridge’s SEDAR+ profile at www.sedarplus.ca.

The Carve-Out Financial Statements of Valor for the years ended December 31, 2024 and 2023, and the Condensed Interim Carve-Out Financial Statements of Valor for the three and nine months ended September 30, 2025 are set forth in 1)Appendix “H” and 1)Appendix “J”“, respectively.

21

SEABRIDGE GOLD INC.

106 Front St. East, Suite

400 Toronto, Ontario, M5A 1E1

INFORMATION CIRCULAR

Capitalized terms hereinafter used are defined in the Glossary of Terms or elsewhere in the Circular.

Seabridge Gold Inc. (the “Company”) is providing this Circular (the “Circular”) and a form of proxy in connection with management’s solicitation of proxies for use at the Special Meeting (the “Meeting”) of shareholders of the Company (the “Shareholders”) to be held at Salon 1, 19th Floor, Fairmont Royal York Hotel, 100 Front Street West, Toronto, Ontario, Canada, at 10:00 a.m. Eastern Daylight Time on May 22, 2026 and at any adjournment(s) or postponement(s) thereof. The Company will conduct its solicitation by mail and officers and employees of the Company may, without receiving special compensation, also telephone or make other personal contact. The Company will pay the cost of solicitation.

All dollar amounts referenced herein are expressed in Canadian Dollars unless otherwise stated.

All shareholders are entitled to attend and vote at the Meeting in person or by proxy. Shareholders will also be able to attend and listen to the Meeting via Microsoft Teams by visiting www.microsoft.com/microsoft-teams/join-a-meeting and using the Meeting ID and Passcode below, but will not be able to participate or vote their shares unless they attend in person or vote their shares by proxy.

To LISTEN TO the Meeting, please refer to the following Microsoft Teams instructions:

Meeting ID: 254 434 303 795 816

Meeting Passcode: Gs3Yy2Dw

APPOINTMENT OF PROXYHOLDER

The purpose of a proxy is to designate persons who will vote the proxy on a Shareholder’s behalf in accordance with the instructions given by the Shareholder in the proxy. The persons whose names are printed in the enclosed form of proxy are officers or directors of the Company (the “Management Proxyholders”).

A Shareholder has the right to appoint a person other than a Management Proxyholder to represent the Shareholder at the Meeting by striking out the names of the Management Proxyholders and by inserting the desired person’s name in the blank space provided or by executing a proxy in a form similar to the enclosed form. A proxyholder need not be a Shareholder.

22

VOTING BY PROXY

Only registered Shareholders or duly appointed proxyholders are permitted to vote at the Meeting. Common shares of the Company (“Shares”) represented by a properly executed proxy will be voted for or against or withheld from voting on each matter referred to in the Notice of Meeting in accordance with the instructions of the Shareholder on any ballot that may be called for and if the Shareholder specifies a choice with respect to any matter to be acted upon, the Shares will be voted accordingly.

If a Shareholder does not specify a choice and the Shareholder has appointed one of the Management Proxyholders as proxyholder, the Management Proxyholder will vote in favour of the matters specified in the Notice of Meeting and in favour of all other matters proposed by management at the Meeting.

The enclosed form of proxy also gives discretionary authority to the person named therein as proxyholder with respect to amendments or variations to matters identified in the Notice of the Meeting and with respect to other matters which may properly come before the Meeting. As at the date of this Circular, management of the Company knows of no such amendments, variations or other matters to come before the Meeting.

COMPLETION AND RETURN OF PROXY

A proxy will not be valid unless the completed, dated and signed proxy is received by Computershare Investor Services Inc., Proxy Department, at 14th Floor, 320 Bay Street, Toronto, Ontario M5H 4A6 by 10:00 a.m. Eastern Time on May 20, 2026 or if the Meeting is adjourned or postponed, not less than 48 hours (excluding Saturdays, Sundays and holidays) before the date to which the Meeting is adjourned or postponed. Telephone voting can be completed at 1-866-732-8683, voting by fax can be sent to 1-866-249-7775 or 416-263-9524 and Internet voting can be completed at www.investorvote.com.

Late proxies may be accepted or rejected by the Chairman of the Meeting at their discretion and the Chairman of the Meeting is under no obligation to accept or reject any particular late proxy. The Chairman of the Meeting may waive or extend the proxy cut-off without notice.

REVOCABILITY OF PROXY

A Shareholder who has given a proxy may revoke it by an instrument in writing executed by the Shareholder or by the Shareholder’s attorney authorized in writing or, if the Shareholder is a corporation, by a duly authorized officer or attorney of the corporation, and delivered either to the Company, at 106 Front St. East, Suite 400, Toronto, Ontario M5A 1E1 at any time up to and including the last business day preceding the day of the Meeting or any adjournment of it or to the Chairman of the Meeting on the day of the Meeting or any adjournment of it. A revocation of a proxy does not affect any matter on which a vote has been taken prior to the revocation.

If you are a Non-Registered Shareholder (as defined below), please follow the instructions from your bank, broker or other financial intermediary for instructions on how to revoke your voting instructions.

23

NON-REGISTERED HOLDERS

Only registered Shareholders of the Company or the persons they appoint as their proxies are permitted to vote at the Meeting. Registered shareholders are holders of Shares whose names appear on the share register of the Company and are not held in the name of a brokerage firm, bank or trust company through which they purchased Shares. Whether or not you are able to attend the Meeting, Shareholders are requested to vote their proxy in accordance with the instructions on the proxy. Most Shareholders are “non-registered” Shareholders (“Non-Registered Shareholders”) because the Shares they own are not registered in their names but are instead registered in the name of the brokerage firm, bank or trust company through which they purchased the Shares. The Company’s Shares beneficially owned by a Non-Registered Shareholder are registered either: (i) in the name of an intermediary (an “Intermediary”) that the Non-Registered Shareholder deals with in respect of their Shares of the Company (Intermediaries include, among others, banks, trust companies, securities dealers or brokers and trustees or administrators of self-administered RRSPs, RRIFs, RESPs and similar plans), or (ii) in the name of a clearing agency (such as The Canadian Depository for Securities Limited or The Depository Trust & Clearing Corporation) of which the Intermediary is a participant.

There are two kinds of beneficial owners: those who object to their name being made known to the issuers of securities which they own (called “OBOs” for Objecting Beneficial Owners) and those who do not object (called “NOBOs” for Non-Objecting Beneficial Owners).

Intermediaries are required to forward the Meeting materials to Non-Registered Shareholders unless a Non-Registered Shareholder has waived the right to receive them. Intermediaries often use service companies to forward the Meeting materials to Non-Registered Shareholders. Generally, Non-Registered Shareholders who have not waived the right to receive Meeting materials will either:

| (a) | be given a voting instruction form which is not signed by the Intermediary and which, when properly completed and signed by the Non-Registered Shareholder and returned to the Intermediary or its service company, will constitute voting instructions (often called a “voting instruction form”) which the Intermediary must follow; or |

| (b) | be given a form of proxy which has already been signed by the Intermediary (typically by a facsimile, stamped signature), which is restricted as to the number of Shares beneficially owned by the Non-Registered Shareholder but which is otherwise not completed by the Intermediary. Because the Intermediary has already signed the form of proxy, this form of proxy is not required to be signed by the Non-Registered Shareholder when submitting the proxy. In this case, the Non-Registered Shareholder who wishes to submit a proxy should properly complete the form of proxy and deposit it in accordance with the instructions under “Completion and Return of Proxy” above. |

In either case, the purpose of these procedures is to permit Non-Registered Shareholders to direct the voting of their Shares which they beneficially own. Should a Non-Registered Shareholder who receives one of the above forms wish to vote at the Meeting in person (or have another person attend and vote on behalf of the Non-Registered Shareholder), the Non-Registered Shareholder should strike out the persons named in the form of proxy and insert their own name or such other person’s name in the blank space provided. Non-Registered Shareholders should carefully follow the instructions of their Intermediary, including those regarding when and where the proxy or voting instruction form is to be delivered.

A Non-Registered Shareholder may revoke a voting instruction form or a waiver of the right to receive Meeting materials and to vote which has been given to an Intermediary at any time by written notice to the Intermediary provided that an Intermediary is not required to act on a revocation of a voting instruction form or of a waiver of the right to receive Meeting materials and to vote which is not received by the Intermediary at least seven days prior to the Meeting.

24

In accordance with applicable Securities Laws requirements, the Company has elected to send the Meeting materials to NOBOs. If you are a NOBO, and the Company or its agent has sent these materials to you, your name and address and information about your holdings of securities have been obtained in accordance with applicable securities regulatory requirements from the Intermediary on your behalf. The Company does not intend to pay for Intermediaries to forward the Meeting materials, including proxies or voting information forms, to OBOs and therefore an OBO will not receive the materials with respect to the Meeting unless that OBO’s Intermediary assumes the cost of delivery.

The Company is not sending the Meeting materials to Shareholders using “notice-and-access” as defined under NI 54-101 Communication with Beneficial Owners of Securities of a Reporting Issuer.

LETTER OF TRANSMITTAL

If you are a registered shareholder, you are encouraged to complete and return the enclosed Letter of Transmittal together with the certificate(s) representing your common shares and any other required documents and instruments, to the Depositary, Computershare Investor Services Inc. (at its principal offices in Toronto), in accordance with the instructions set out in the Letter of Transmittal so that if the Arrangement is approved, the consideration for your common shares can be sent to you as soon as possible following the Arrangement becoming effective. The Letter of Transmittal contains other procedural information related to the Arrangement and should be reviewed carefully.

If you hold your common shares through a broker or other person, please contact that broker or other person for instructions and assistance in receiving the new Company shares and Valor shares in exchange for your common shares upon completion of the Arrangement.

This Circular contains a detailed description of the Arrangement and includes certain other information to assist you in considering the matters to be voted upon. You are urged to carefully consider all of the information in the accompanying Circular including the documents incorporated by reference therein. If you require assistance, you should consult your financial, legal, or other professional advisors.

VOTING SECURITIES AND PRINCIPAL HOLDERS THEREOF

The Company is authorized to issue an unlimited number of common shares and an unlimited number of preferred shares, of which 107,373,183 common shares were issued and outstanding as at March 30, 2026 (the “Record Date”). Persons who are registered shareholders at the close of business on the Record Date will be entitled to receive notice of and vote at the Meeting and will be entitled to one vote for each share held. The Company has only one class of shares outstanding, being the common shares of the Company.

Under the Company’s constating documents, the quorum for the transaction of business at the Meeting is three (3) persons who are, or who represent by proxy, shareholders entitled to vote at the meeting who hold, in the aggregate, at least thirty-three and one third percent (33 1/3%) of the votes entitled to be cast at the meeting.

25

To the knowledge of the directors and executive officers of the Company as of the date of this Circular, the only persons who beneficially own, or control or direct, directly or indirectly, voting securities carrying 10% or more of the voting rights attached to any class of voting securities of the Company are as follows.