SHINHAN FINANCIAL GROUP CO., LTD.

Separate Financial Statements

December 31, 2025 and 2024

(With Independent Auditor’s Report Thereon)

SHINHAN FINANCIAL GROUP CO., LTD.

Separate Financial Statements

December 31, 2025 and 2024

(With Independent Auditor’s Report Thereon)

Contents

|

|

Page |

|

|

|

Independent Auditors’ Report |

|

1 |

|

|

|

Separate Statements of Financial Position |

|

4 |

|

|

|

Separate Statements of Comprehensive Income |

|

5 |

|

|

|

Separate Statements of Changes in Equity |

|

6 |

|

|

|

Separate Statements of Cash Flows |

|

8 |

|

|

|

Notes to the Separate Financial Statements |

|

10 |

|

|

|

Independent Auditors’ Report on Internal Control over Financial Reporting |

|

74 |

|

|

|

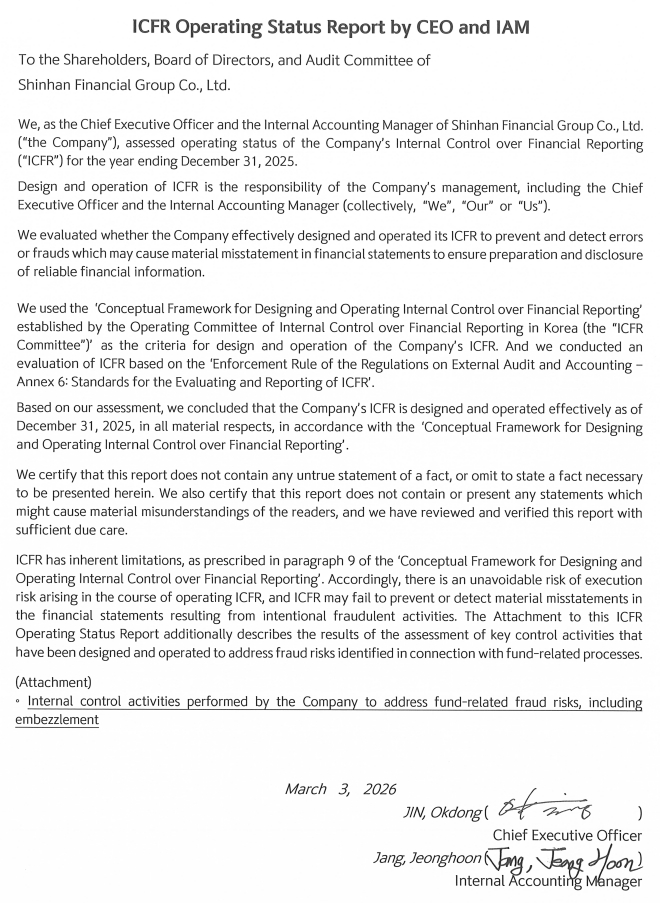

ICFR Operating Status Report by CEO and IAM |

|

76 |

Independent Auditors’ Report

Based on a report originally issued in Korean

The Board of Directors and Stockholders

Shinhan Financial Group Co., Ltd.

Opinion

We have audited the separate financial statements of Shinhan Financial Group Co., Ltd. (“the Company”), which comprise the separate statements of financial position as of December 31, 2025 and 2024, the separate statements of comprehensive income, changes in equity and cash flows for the years then ended, and notes, comprising a summary of material accounting policies and other explanatory information.

In our opinion, the accompanying separate financial statements present fairly, in all material respects, the separate financial position of the Company as of December 31, 2025 and 2024, and its separate financial performance and its cash flows for the years then ended in accordance with Korean International Financial Reporting Standards (“KIFRS”).

We have also audited, in accordance with Korean Standards on Auditing (“KSAs”), the Company’s Internal Control over Financial Reporting (“ICFR”) as of December 31, 2025 based on the criteria established in Conceptual Framework for Designing and Operating Internal Control over Financial Reporting issued by the Operating Committee of Internal Control over Financial Reporting in the Republic of Korea, and our report dated March 3, 2026 expressed an unmodified opinion on the effectiveness of the Company’s internal control over financial reporting.

Basis for Opinion

We conducted our audits in accordance with KSAs. Our responsibilities under those standards are further described in the Auditors’ Responsibilities for the Audit of the Separate Financial Statements section of our report. We are independent of the Company in accordance with the ethical requirements that are relevant to our audits of the separate financial statements in the Republic of Korea, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinions.

Key Audit Matters

We have determined that there are no key audit matters to communicate in our report.

Other Matters

The procedures and practices utilized in the Republic of Korea to audit such separate financial statements may differ from those generally accepted and applied in other countries.

1

Responsibilities of Management and Those Charged with Governance for the Separate Financial Statements

Management is responsible for the preparation and fair presentation of the separate financial statements in accordance with K-IFRS, and for such internal control as management determines is necessary to enable the preparation of separate financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the separate financial statements, management is responsible for assessing the Company’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Company or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Company’s financial reporting process.

Auditors’ Responsibilities for the Audit of the Separate Financial Statements

Our objectives are to obtain reasonable assurance about whether the separate financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditors’ report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with KSAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these separate financial statements.

As part of an audit in accordance with KSAs, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

2

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in the internal controls that we identify during our audit.

We also provide those charged with governance with a statement that we have complied with relevant ethical requirements regarding independence, and communicate with them all relationships and other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards.

From the matters communicated with those charged with governance, we determine those matters that were of most significance in the audit of the separate financial statements of the current period and are therefore the key audit matters. We describe these matters in our auditors’ report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of such communication.

The engagement partner on the audit resulting in this independent auditors’ report is Jung-Soo Bok.

KPMG Samjong Accounting Corp.

Seoul, Korea

March 3, 2026

This report is effective as of March 3, 2026, the audit report date. Certain subsequent events or circumstances, which may occur between the audit report date and the time of reading this report, could have a material impact on the accompanying separate financial statements and notes thereto. Accordingly, the readers of the audit report should understand that the above audit report has not been updated to reflect the impact of such subsequent events or circumstances, if any. |

3

SHINHAN FINANCIAL GROUP CO., LTD.

Separate Statements of Financial Position

As of December 31, 2025 and 2024

(In millions of won) |

|

Notes |

|

2025 |

|

2024 |

|

|

|

|

|

|

|

Assets |

|

|

|

|

|

|

Cash and due from banks at amortized cost |

|

4, 6, 8, 33 |

W |

2,589 |

|

151,143 |

Financial assets at fair value through profit or loss |

|

4, 7, 33 |

|

3,160,174 |

|

2,552,750 |

Loans at amortized cost |

|

4, 8, 33 |

|

2,951,878 |

|

3,837,298 |

Property and equipment |

|

9, 11, 33 |

|

4,833 |

|

6,509 |

Intangible assets |

|

10 |

|

7,114 |

|

6,488 |

Investments in subsidiaries |

|

12 |

|

30,723,705 |

|

30,623,651 |

Net defined benefit assets |

|

16 |

|

9,676 |

|

5,622 |

Deferred tax assets |

|

29 |

|

6,388 |

|

- |

Other assets |

|

4, 8, 13, 33 |

|

927,470 |

|

488,842 |

Total assets |

|

|

W |

37,793,827 |

|

37,672,303 |

|

|

|

|

|

|

|

Liabilities |

|

|

|

|

|

|

Borrowings |

|

4, 14 |

|

9,975 |

|

19,914 |

Debt securities issued |

|

4, 15, 33 |

|

10,457,205 |

|

10,731,336 |

Deferred tax liabilities |

|

29 |

|

- |

|

20,518 |

Other liabilities |

|

4, 17, 33 |

|

991,187 |

|

552,360 |

Total liabilities |

|

|

|

11,458,367 |

|

11,324,128 |

|

|

|

|

|

|

|

Equity |

|

18 |

|

|

|

|

Capital stock |

|

|

|

2,969,641 |

|

2,969,641 |

Hybrid bonds |

|

|

|

4,749,837 |

|

4,600,121 |

Capital surplus |

|

|

|

11,350,744 |

|

11,350,744 |

Capital adjustments |

|

|

|

(647,347) |

|

(296,024) |

Accumulated other comprehensive loss |

|

|

|

(11,363) |

|

(9,307) |

Retained earnings |

|

|

|

7,923,948 |

|

7,733,000 |

Total equity |

|

|

|

26,335,460 |

|

26,348,175 |

Total liabilities and equity |

|

|

W |

37,793,827 |

|

37,672,303 |

See accompanying notes to the separate financial statements.

4

SHINHAN FINANCIAL GROUP CO., LTD.

Separate Statements of Comprehensive Income

For the years ended December 31, 2025 and 2024

(In millions of won, except earnings per share data) |

|

Notes |

|

2025 |

|

2024 |

|

|

|

|

|

|

|

Interest income |

|

28, 33 |

W |

89,331 |

|

98,770 |

Interest expense |

|

33 |

|

(335,753) |

|

(334,798) |

Net interest expense |

|

20 |

|

(246,422) |

|

(236,028) |

|

|

|

|

|

|

|

Fees and commission income |

|

28, 33 |

|

71,038 |

|

71,053 |

Fees and commission expense |

|

33 |

|

(810) |

|

(617) |

Net fees and commission income |

|

21 |

|

70,228 |

|

70,436 |

|

|

|

|

|

|

|

Dividend income |

|

22, 28, 33 |

|

2,624,112 |

|

2,025,956 |

Net gain on financial assets at fair value through profit or loss |

|

24, 28 |

|

71,959 |

|

89,244 |

Net foreign currency transaction loss |

|

28 |

|

(291) |

|

(2,128) |

Reversal of credit loss allowance |

|

8, 23, 28, 33 |

|

266 |

|

215 |

General and administrative expenses |

|

25, 33 |

|

(155,536) |

|

(146,832) |

|

|

|

|

|

|

|

Operating income |

|

|

|

2,364,316 |

|

1,800,863 |

|

|

|

|

|

|

|

Non-operating expenses |

|

27 |

|

(3,788) |

|

(169,111) |

|

|

|

|

|

|

|

Profit before income taxes |

|

|

|

2,360,528 |

|

1,631,752 |

|

|

|

|

|

|

|

Income tax expense (benefit) |

|

29 |

|

(24,929) |

|

11,885 |

Profit for the year |

|

|

|

2,385,457 |

|

1,619,867 |

|

|

|

|

(2,056) |

|

(2,665) |

Other comprehensive loss for the year, net of income tax |

|

16, 18 |

|

|

||

Items that will not be reclassified subsequently to profit or loss: Re-measurements of the defined benefit asset |

|

|

|

(2,056) |

|

(2,665) |

|

|

|

|

|

|

|

Total comprehensive income for the year |

|

|

W |

2,383,401 |

|

1,617,202 |

|

|

|

|

|

|

|

Basic and diluted earnings per share in Korean won |

30 |

W |

4,497 |

|

2,850 |

|

|

|

|

|

|

|

|

See accompanying notes to the separate financial statements.

5

SHINHAN FINANCIAL GROUP CO., LTD.

Separate Statements of Changes in Equity

For the years ended December 31, 2025 and 2024

(In millions of won) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Capital stock |

|

Hybrid bonds |

|

Capital surplus |

|

Capital adjust-ments |

|

Accumulated other comprehensive loss |

|

Retained earnings |

|

Total equity |

Balance at January 1, 2024 |

W |

2,969,641 |

|

4,001,731 |

|

11,350,744 |

|

(148,464) |

|

(6,642) |

|

7,932,131 |

|

26,099,141 |

Total comprehensive income for the year: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Profit for the year |

|

- |

|

- |

|

- |

|

- |

|

- |

|

1,619,867 |

|

1,619,867 |

Other comprehensive income |

|

- |

|

- |

|

- |

|

- |

|

(2,665) |

|

- |

|

(2,665) |

Remeasurements of the net defined benefit assets |

|

- |

|

- |

|

- |

|

- |

|

(2,665) |

|

- |

|

(2,665) |

|

|

- |

|

- |

|

- |

|

- |

|

(2,665) |

|

1,619,867 |

|

1,617,202 |

Transactions with owners: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dividends |

|

- |

|

- |

|

- |

|

- |

|

- |

|

(268,697) |

|

(268,697) |

Interim dividends |

|

- |

|

- |

|

- |

|

- |

|

- |

|

(820,287) |

|

(820,287) |

Dividend to hybrid bonds |

|

- |

|

- |

|

- |

|

- |

|

- |

|

(176,945) |

|

(176,945) |

Redemption of hybrid bonds |

|

- |

|

(199,476) |

|

- |

|

(524) |

|

- |

|

- |

|

(200,000) |

Transfer to retained earnings of redemption loss of hybrid bonds |

|

- |

|

- |

|

- |

|

102,667 |

|

- |

|

(102,667) |

|

- |

Issuance of hybrid bonds |

|

- |

|

797,866 |

|

- |

|

- |

|

- |

|

- |

|

797,866 |

Acquisition of treasury stock |

|

- |

|

- |

|

- |

|

(700,300) |

|

- |

|

- |

|

(700,300) |

Disposal of treasury stock |

|

- |

|

- |

|

- |

|

297 |

|

- |

|

- |

|

297 |

Retirement of treasury stock |

|

- |

|

- |

|

- |

|

450,300 |

|

- |

|

(450,402) |

|

(102) |

|

|

- |

|

598,390 |

|

- |

|

(147,560) |

|

- |

|

(1,818,998) |

|

(1,368,168) |

Balance at December 31, 2024 |

|

2,969,641 |

|

4,600,121 |

|

11,350,744 |

|

(296,024) |

|

(9,307) |

|

7,733,000 |

|

26,348,175 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6

SHINHAN FINANCIAL GROUP CO., LTD.

Separate Statements of Changes in Equity (Continued)

For the years ended December 31, 2025 and 2024

(In millions of won) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Capital stock |

|

Hybrid bonds |

|

Capital surplus |

|

Capital adjust-ments |

|

Accumulated other comprehensive loss |

|

Retained earnings |

|

Total equity |

Balance at January 1, 2025 |

W |

2,969,641 |

|

4,600,121 |

|

11,350,744 |

|

(296,024) |

|

(9,307) |

|

7,733,000 |

|

26,348,175 |

Total comprehensive income for the year: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Profit for the year |

|

- |

|

- |

|

- |

|

- |

|

- |

|

2,385,457 |

|

2,385,457 |

Other comprehensive income |

|

- |

|

- |

|

- |

|

- |

|

(2,056) |

|

- |

|

(2,056) |

Remeasurements of the net defined benefit assets |

|

- |

|

- |

|

- |

|

- |

|

(2,056) |

|

- |

|

(2,056) |

|

|

- |

|

- |

|

- |

|

- |

|

(2,056) |

|

2,385,457 |

|

2,383,401 |

Transactions with owners: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dividends |

|

- |

|

- |

|

- |

|

- |

|

- |

|

(267,755) |

|

(267,755) |

Interim dividends |

|

- |

|

- |

|

- |

|

- |

|

- |

|

(828,228) |

|

(828,228) |

Dividend to hybrid bonds |

|

- |

|

- |

|

- |

|

- |

|

- |

|

(197,932) |

|

(197,932) |

Redemption of hybrid bonds |

|

- |

|

(648,154) |

|

- |

|

(1,846) |

|

- |

|

- |

|

(650,000) |

Transfer to retained earnings of redemption loss of hybrid bonds |

|

- |

|

- |

|

- |

|

524 |

|

- |

|

(524) |

|

- |

Issuance of hybrid bonds |

|

- |

|

797,870 |

|

- |

|

- |

|

- |

|

- |

|

797,870 |

Acquisition of treasury stock |

|

- |

|

- |

|

- |

|

(1,250,001) |

|

- |

|

- |

|

(1,250,001) |

Retirement of treasury stock |

|

- |

|

- |

|

- |

|

900,000 |

|

- |

|

(900,070) |

|

(70) |

|

|

- |

|

149,716 |

|

- |

|

(351,323) |

|

- |

|

(2,194,509) |

|

(2,396,116) |

Balance at December 31, 2025 |

W |

2,969,641 |

|

4,749,837 |

|

11,350,744 |

|

(647,347) |

|

(11,363) |

|

7,923,948 |

|

26,335,460 |

See accompanying notes to the separate financial statements.

7

SHINHAN FINANCIAL GROUP CO., LTD.

Separate Statements of Cash Flows

For the years ended December 31, 2025 and 2024

(In millions of won) |

|

Notes |

|

2025 |

|

2024 |

|

|

|

|

|

|

|

Cash flows from operating activities |

|

|

|

|

|

|

Profit for the year |

|

|

W |

2,385,457 |

|

1,619,867 |

Adjustments for: |

|

|

|

|

|

|

Interest income |

|

20 |

|

(89,331) |

|

(98,770) |

Interest expense |

|

20 |

|

335,753 |

|

334,798 |

Dividend income |

|

22 |

|

(2,624,112) |

|

(2,025,956) |

Income tax expense (benefit) |

|

29 |

|

(24,929) |

|

11,885 |

Net gain on financial instruments at fair value through profit or loss |

|

24 |

|

(29,334) |

|

(39,427) |

Reversal of credit loss allowance |

|

|

|

(266) |

|

(215) |

Employee benefits |

|

|

|

12,825 |

|

6,364 |

Depreciation and amortization |

|

25 |

|

4,450 |

|

5,137 |

Net foreign currency translation loss (gain) |

|

|

|

(37,848) |

|

4,201 |

Non-operating expense |

|

|

|

2,272 |

|

167,731 |

|

|

|

|

(2,450,520) |

|

(1,634,252) |

Changes in assets and liabilities: |

|

|

|

|

|

|

Financial instruments at fair value through profit or loss |

|

|

|

(564,963) |

|

(330,111) |

Other assets |

|

|

|

(886) |

|

235 |

Net defined benefit assets |

|

|

|

(8,916) |

|

(4,625) |

Other liabilities |

|

|

|

(2,699) |

|

(4,021) |

|

|

|

|

(577,464) |

|

(338,522) |

|

|

|

|

|

|

|

Income tax paid |

|

|

|

(594) |

|

792 |

Interest received |

|

|

|

88,220 |

|

97,366 |

Interest paid |

|

|

|

(328,744) |

|

(326,008) |

Dividend received |

|

|

|

2,624,048 |

|

2,025,368 |

Net cash inflow from operating activities |

|

|

|

1,740,403 |

|

1,444,611 |

|

|

|

|

|

|

|

Cash flows from investing activities |

|

|

|

|

|

|

Acquisition of financial instruments at fair value through profit or loss |

|

|

|

(100,000) |

|

(150,000) |

Decrease in financial instruments at fair value through profit or loss |

|

|

|

100,000 |

|

- |

Lending of loans at amortized cost |

|

|

|

(1,575,697) |

|

(179,304) |

Collection of loans at amortized cost |

|

|

|

2,480,890 |

|

615,000 |

Acquisition of property and equipment |

|

|

|

(292) |

|

(2,162) |

Disposal of property and equipment |

|

|

|

- |

|

(10) |

Acquisition of intangible assets |

|

|

|

(1,806) |

|

(1,840) |

Disposal of intangible assets |

|

|

|

- |

|

2,387 |

Increase in other assets |

|

|

|

(8,225) |

|

(620) |

Decrease in other assets |

|

|

|

- |

|

71 |

Acquisition of investment in subsidiary |

|

|

|

(100,054) |

|

(100,000) |

Disposal of investments in subsidiaries |

|

|

|

- |

|

32,804 |

Net cash inflow from investing activities |

|

|

W |

794,816 |

|

216,326 |

8

SHINHAN FINANCIAL GROUP CO., LTD.

Separate Statements of Cash Flows (Continued)

For the years ended December 31, 2025 and 2024

9

SHINHAN FINANCIAL GROUP CO., LTD.

Separate Statements of Cash Flows (Continued)

For the years ended December 31, 2025 and 2024

(In millions of won) |

|

Notes |

|

2025 |

|

2024 |

|

|

|

|

|

|

|

Cash flows from financing activities |

|

|

|

|

|

|

Issuance of hybrid bonds |

|

|

|

797,870 |

|

797,867 |

Redemption of hybrid bonds |

|

|

|

(650,000) |

|

(200,000) |

Issuance of debt securities |

|

|

|

2,738,224 |

|

1,836,934 |

Redemption of debt securities |

|

|

|

(3,015,000) |

|

(1,770,000) |

Increase in borrowings |

|

|

|

109,700 |

|

29,316 |

Decrease in borrowings |

|

|

|

(120,000) |

|

(235,000) |

Dividends paid |

|

|

|

(1,293,828) |

|

(1,267,146) |

Acquisition of treasury stock |

|

|

|

(1,250,001) |

|

(700,300) |

Disposal of treasury stock |

|

|

|

- |

|

297 |

Expense for retirement of treasury stock |

|

|

|

(69) |

|

(102) |

Repayments of lease liabilities |

|

|

|

(731) |

|

(1,619) |

Net cash outflow from financing activities |

|

|

|

(2,683,835) |

|

(1,509,753) |

|

|

|

|

|

|

|

Net increase (decrease) in cash and cash equivalents |

|

|

|

(148,616) |

|

151,184 |

|

|

|

|

|

|

|

Cash and cash equivalents at the beginning of year |

|

32 |

|

151,203 |

|

19 |

Cash and cash equivalents at the end of year |

|

32 |

W |

2,587 |

|

151,203 |

See accompanying notes to the separate financial statements.

10

SHINHAN FINANCIAL GROUP CO., LTD.

Notes to the Separate Financial Statements

December 31, 2025 and 2024

1. Reporting entity

Shinhan Financial Group Co., Ltd. (hereinafter referred to as "the Company") was established on September 1, 2001 for the main business purposes such as control and management of companies operating in the financial industry, and financial support for subsidiaries. In addition, the stocks were listed on the Korea Exchange on September 10, 2001, and the Company was registered with the Securities and Exchange Commission (SEC) on September 16, 2003, and on the same date, ADS (American Depositary Shares) was listed on the New York Stock Exchange (NYSE).

2. Basis of preparation

(a) Statement of compliance

The Company maintains its accounting records in Korean won and prepares statutory financial statements in the Korean language (Hangul) in accordance with International Financial Reporting Standards as adopted by the Republic of Korea (K-IFRS) The accompanying separate financial statements have been restructured and translated into English from the Korean language financial statements.

Certain information attached to the Korean language financial statements, but not required for a fair presentation of the Company's financial position, financial performance or cash flows, is not presented in the accompanying separate financial statements.

These financial statements are separate financial statements prepared in accordance with K-IFRS No. 1027 ‘Separate Financial Statements’ in which presented on the basis of direct equity investments, not on that the controlling company, equity interests in associates and joint ventures does not base the investment on the investee’s reported performance and net assets.

(b) Basis of measurement

The separate financial statements have been prepared on the historical cost basis except for the following major items in the separate statement of financial position.

(c) Functional and presentation currency

These separate financial statements are presented in Korean won which is the Company’s functional currency and the currency of the primary economic environment in which the Company operates.

11

SHINHAN FINANCIAL GROUP CO., LTD.

Notes to the Separate Financial Statements

December 31, 2025 and 2024

2. Basis of preparation (continued)

(d) Use of estimates and judgments

The preparation of the separate financial statements in conformity with K-IFRS requires management to make judgments, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets, liabilities, income and expenses. If the estimates and assumptions based on management's judgment as of the end of the annual reporting period differ from the actual circumstances, the related actual results may differ from these estimates.

Estimates and underlying assumptions about estimates are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the period in which the estimates are revised and in any future periods affected.

(e) Changes in accounting policy

Except for the following new standard, which has been applied from January 1, 2025, the accounting policies applied by the Company in these separate financial statements are the same as those applied by the Company in its separate financial statements as of and for the year ended December 31, 2024.

i) Amendments to K-IFRS No. 1021 'Effects of Changes in Foreign Exchange Rates' and No. 1101 ‘First-time adoption of K-IFRS’ – Lack of Exchangeability

These amendments define scenarios where exchanges with other currencies are considered possible for accounting purposes, clarify the assessment of exchangeability with other currencies, and specify requirements for estimating and disclosing the spot exchange rate in cases where no exchangeability exists.

If exchange with other currencies is not possible, the spot exchange rate must be estimated on the measurement date using observable exchange rates without adjustment or employing alternative estimation techniques. There is no significant impact on the separate financial statements from these amendments.

ii) Amendments to K-IFRS No. 1117 ‘Insurance Contracts’ - Disclosure requirements related to lapse rates for insurance products with no or low surrender value

A paragraph has been added to require disclosure of any differences and their effects on the financial statements when the estimation techniques used for input variables in measuring insurance contracts differ from the principles for estimation required under insurance-related laws and regulations, provided that such information is considered relevant and material to users of the financial statements. These amendments are effective from December 31, 2025, and are applicable to the first annual reporting period ending after the effective date. The amendments will remain in effect until the annual reporting period ending December 31, 2029. There is no significant impact on the separate financial statements from these amendments.

(f) Approval of separate financial statements

These separate financial statements were approved by the Board of Directors on February 5, 2026, which will be submitted for approval to shareholders’ meeting on March 26, 2026.

12

SHINHAN FINANCIAL GROUP CO., LTD.

Notes to the Separate Financial Statements

December 31, 2025 and 2024

3. Material accounting policies

The material accounting policies applied by the Company in preparation of its separate financial statements are included below. The Company applies the same accounting policies applied as when preparing the annual separate financial statements for the years ended December 31, 2025 and 2024, except for the following amendments that have been applied for the first time since January 1, 2025 and as described in Note 2.

(a) Investments in subsidiaries

The accompanying separate financial statements have been prepared on a stand-alone basis in accordance with K-IFRS No. 1027 Separate Financial Statements. The Company’s investments in subsidiaries are recorded at cost less impairment, if any, in accordance with K-IFRS No. 1027. The Company applied K-IFRS No. 1101 First-time Adoption of K-IFRS, and considered the amount reported previously in separate financial statements prepared in accordance with previous K-GAAP as deemed cost at the date of transition. Dividends received from its subsidiaries are recognized in profit or loss when the Company is entitled to receive the dividend.

(b) Cash and cash equivalents

Cash and cash equivalents comprise cash on hand, demand deposits, and short-term, highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value and are used by the Company in management of its short-term commitments with maturities of three months or less from the date of acquisition.

(c) Non-derivative financial assets

Financial assets are recognized in the separate statement of financial position when the Company becomes a party to the contract. In addition, a standardized purchase or sale (a purchase or sale of a financial asset under a contract whose terms require delivery of the asset within the time frame established generally by regulation or convention in the market concerned) is recognized on the trade date.

i) Financial assets designated at FVTPL

Financial assets can be irrevocably designated as measured at FVTPL despite classification standards stated below, if doing so eliminates or significantly reduces an accounting mismatch that would otherwise arise from measuring assets or liabilities or recognizing the gains or losses on them on different bases. However, once the financial assets are designated at FVTPL, it is irrevocable.

ii) Equity instruments

For the equity instruments that are not held for short-term trading, at initial recognition, the Company may make an irrevocable election to present subsequent changes in fair value in other comprehensive income. Equity instruments that are not classified as financial assets at Fair Value through Other Comprehensive Income (“FVOCI”) are classified as financial assets at FVTPL.

The Company subsequently measures all equity investments at fair value. Valuation gains or losses of the equity instruments that are classified as financial assets at FVOCI previously recognized as other comprehensive income is not reclassified as profit or loss on derecognition. The Company recognizes dividends in profit or loss when the Company’s right to receive payments of the dividend is established.

Valuation gains or losses due to changes in fair value of the financial assets at FVTPL are recognized as gains or losses on financial assets at FVTPL. Impairment loss (reversal) on equity instruments at FVOCI is not recognized separately.

13

SHINHAN FINANCIAL GROUP CO., LTD.

Notes to the Separate Financial Statements

December 31, 2025 and 2024

3. Material accounting policies (continued)

(c) Non-derivative financial assets (continued)

iii) Debt instruments

Subsequent measurement of debt instruments depends on the Company’s business model in which the asset is managed and the contractual cash flow characteristics of the asset. Debt instruments are classified as financial assets at amortized cost, at FVOCI, or at FVTPL. Debt instruments are reclassified only when the Company’s business model changes.

iii-1) Financial assets at amortized cost

Assets that are held within a business model whose objective is to hold assets to collect contractual cash flows where those cash flows represent solely payments of principal and interest are measured at amortized cost. Impairment losses, and gains or losses on derecognition of the financial assets at amortized cost are recognized in profit or loss. Interest income on the effective interest method is included in the ‘Interest income’ in the separate statement of comprehensive income.

iii-2) Financial asset at FVOCI

Assets that are held within a business model whose objective is achieved by both collecting contractual cash flows and selling financial assets, where the assets’ cash flows represent solely payments of principal and interest, are measured at FVOCI. Other than impairment losses, interest income amortized using effective interest method and foreign exchange differences, gains or losses of the financial assets at FVOCI are recognized as other comprehensive income in equity. On removal, gains or losses accumulated in other comprehensive income are reclassified to profit or loss. The interest income on the effective interest method is included in the ‘Interest income’ in the separate statement of comprehensive income. Foreign exchange differences and impairment losses are included in the ‘Net foreign currency transaction gain’ and ‘Provision for credit losses allowance’ in the separate statement of comprehensive income, respectively.

iii-3) Financial asset at FVTPL

Debt securities other than financial assets at amortized costs or FVOCI are classified at FVTPL. Unless hedge accounting is applied, gains or losses from financial assets at FVTPL are recognized as profit or loss and are included in ‘Net gain on financial instruments at fair value through profit or loss’ in the separate statement of comprehensive income.

iv) Embedded derivatives

Financial assets with embedded derivatives are classified regarding the entire hybrid contract, and the embedded derivatives are not separately recognized. The entire hybrid contract is considered when it is determined whether the contractual cash flows represent solely payments of principal and interest.

14

SHINHAN FINANCIAL GROUP CO., LTD.

Notes to the Separate Financial Statements

December 31, 2025 and 2024

3. Material accounting policies (continued)

(d) Expected credit losses of financial assets

The Company recognizes provision for credit loss allowance for debt instruments measured at amortized cost and fair value through other comprehensive income, using the expected credit loss impairment model.

Financial assets migrate through the following three stages based on the change in credit risk since initial recognition and loss allowances for the financial assets are measured at the 12-month expected credit losses (“ECL”) or the lifetime ECL, depending on the stage.

Category |

|

Provision for credit loss allowance |

||

STAGE 1 |

|

When credit risk has not increased significantly since the initial recognition |

|

12-month ECL: the ECL associated with the probability of default events occurring within the next 12 months

|

STAGE 2 |

|

When credit risk has increased significantly since the initial recognition |

|

Lifetime ECL: a lifetime ECL associated with the probability of default events occurring over the remaining lifetime |

STAGE 3 |

|

When assets are impaired |

|

Same as above |

The Company, meanwhile, only recognizes the cumulative changes in lifetime expected credit losses since the initial recognition as a loss allowance for purchased or originated credit-impaired financial assets.

The total period refers to the expected life of the financial instrument up to the contractual maturity date.

i) Reflection of forward-looking information

The Company incorporates forward-looking information when assessing whether credit risk has increased significantly and when measuring expected credit losses.

Assuming that the measurement factor of expected credit losses has a certain correlation with economic fluctuations, the expected credit losses are calculated by reflecting forward-looking information through modeling between macroeconomic variables and measurement factors.

ii) Measurement of amortization cost regarding the expected credit loss of financial assets

The expected credit loss of amortized financial assets is measured as the difference between the present value of the cash flows expected to be received and the cash flow to be received in accordance with loan agreements. For this purpose, the Company calculates expected cash flows for individually significant financial assets.

For financial assets that are not individually significant, the Company collectively measures the expected credit losses thereof with similar credit risk characteristics.

Expected credit losses are deducted from financial assets at amortized cost using ACL, which are written off along with the assets if the assets are not recoverable. The allowance for credit loss is increased when the written-off loan receivables are subsequently collected, and the changes in the allowance for credit loss are recognized in profit or loss.

iii) Measurement of expected credit loss of financial assets at FVOCI

The calculation of expected credit loss of financial assets at FVOCI is the same as for financial assets measured at amortized cost, but changes in allowance for credit loss are recognized in other comprehensive income. In the case of disposal and redemption of financial assets at FVOCI, the allowance for credit loss is reclassified from other comprehensive income to profit or loss and recognized in profit or loss.

15

SHINHAN FINANCIAL GROUP CO., LTD.

Notes to the Separate Financial Statements

December 31, 2025 and 2024

16

SHINHAN FINANCIAL GROUP CO., LTD.

Notes to the Separate Financial Statements

December 31, 2025 and 2024

3. Material accounting policies (continued)

(e) Property and equipment

Depreciation is recognized in profit or loss on a straight-line basis over the estimated useful lives of 5 years, since this most closely reflects the expected pattern of consumption of the future economic benefits embodied in the asset.

(f) Intangible assets

Intangible assets are measured initially at cost and, subsequently, are carried at cost less accumulated amortization and accumulated impairment losses, if any.

Amortization of intangible assets is calculated on a straight-line basis over the estimated useful lives of 5 years from the date that they are available for use. The residual value of intangible assets is zero. However, if there are no foreseeable limits to the periods over which certain intangible assets are expected to be available for use, they are determined to have indefinite useful lives and are not amortized.

(g) Impairment of non-financial assets

The carrying amounts of the Company’s non-financial assets, other than assets arising from employee benefits and deferred tax assets, are reviewed at the end of the reporting period to determine whether there is any indication of impairment. If any such indication exists, then the asset’s recoverable amount is estimated. Intangible assets that have indefinite useful lives or that are not yet available for use, irrespective of whether there is any indication of impairment, are tested for impairment annually by comparing their recoverable amount to their carrying amount.

The Company estimates the recoverable amount of an individual asset, if it is impossible to measure the individual recoverable amount of an asset, then the Company estimates the recoverable amount of cash-generating unit (“CGU”). A CGU is the smallest identifiable group of assets that generates cash inflows that are largely independent of the cash inflows from other assets or groups of assets. The recoverable amount of an asset or CGU is the greater of its value in use and its fair value less costs to sell. The value in use is estimated by applying a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset or CGU for which estimated future cash flows have not been adjusted, to the estimated future cash flows expected to be generated by the asset or CGU.

An impairment loss is recognized if the carrying amount of an asset or a CGU exceeds its recoverable amount. Impairment losses are recognized in profit or loss.

17

SHINHAN FINANCIAL GROUP CO., LTD.

Notes to the Separate Financial Statements

December 31, 2025 and 2024

3. Material accounting policies (continued)

(h) Non-derivative financial liabilities

The Company recognizes financial liabilities in the separate statement of financial position when the Company becomes a party to the contractual provisions of the financial liability in accordance with the substance of the contractual arrangement and the definitions of financial liabilities. Transaction costs on the financial liabilities at FVTPL are recognized in profit or loss as incurred.

i) Financial liabilities designated at FVTPL

Financial liabilities can be irrevocably designated as measured at FVTPL if doing so eliminates or significantly reduces an accounting mismatch that would otherwise arise from measuring assets or liabilities or recognizing the gains and losses on them on different bases, or a group of financial instruments is managed and its performance is evaluated on a fair value basis, in accordance with a documented risk management or investment strategy. The amount of change in the fair value of the financial liabilities designated at FVTPL that is attributable to changes in the credit risk of that liabilities shall be presented in other comprehensive income.

ii) Financial liabilities at FVTPL

Since initial recognition, financial liabilities at FVTPL are measured at fair value, and changes in the fair value are recognized as profit or loss.

iii) Other financial liabilities

Non-derivative financial liabilities other than financial liabilities at fair value through profit or loss are classified as other financial liabilities. At the date of initial recognition, other financial liabilities are measured at fair value minus transaction costs that are directly attributable to the acquisition. Subsequent to initial recognition, other financial liabilities are at amortized cost using the effective interest method.

The Company derecognizes a financial liability from the separate statement of financial position when it is extinguished (i.e. when the obligation specified in the contract is discharged, cancelled or expires).

(i) Paid-in capital

i) Hybrid bond

The Company classifies issued financial instrument, or its component parts, as a financial liability or an equity instrument depending on the substance of the contractual arrangement of such financial instrument. Hybrid bond where the Company has an unconditional right to avoid delivering cash or another financial asset to settle a contractual obligation are classified as an equity instrument and presented in equity.

18

SHINHAN FINANCIAL GROUP CO., LTD.

Notes to the Separate Financial Statements

December 31, 2025 and 2024

3. Material accounting policies (continued)

(j) Employee benefits

i) Short-term employee benefits

Short-term employee benefits are employee benefits that are due to be settled within 12 months after the end of the period in which the employees render the related service. When an employee has rendered service to the Company during an accounting period, the Company recognizes the undiscounted amount of short-term employee benefits expected to be paid in exchange for that service.

ii) Other long-term employee benefits

The Company’s net obligation in respect of long-term employee benefits other than pension plans is the amount of future benefit that employees have earned in return for their service in the current and prior periods; that benefit is discounted to determine its present value, and the fair value of any related assets is deducted. The discount rate is the yield at the reporting date on AA credit-rated bonds that have maturity dates approximating the terms of the Company’s obligations. The calculation is performed using the projected unit credit method. Any actuarial gains and losses are recognized in profit or loss in the period in which they arise.

iii) Retirement benefits: defined benefit plans

For the year ended December 31, 2024, defined benefit liabilities related to the defined benefit plan are recognized by deducting the fair value of external reserve from the present value of the defined benefit plan debt.

Defined benefit liabilities are calculated annually by independent actuaries using the predicted unit credit method. If the net present value of the defined benefit obligation less the fair value of the plan assets is an asset then the present value of the economic benefits available to the entity in the form of a refund from the plan or a reduction in future contributions to the plan.

(k) Provisions

A provision is recognized if, as a result of a past event, the Company has a present legal or constructive obligation that can be estimated reliably, and it is probable that an outflow of economic benefits will be required to settle the obligation.

The risks and uncertainties that inevitably surround many events and circumstances are taken into account in reaching the best estimate of a provision. Where the effect of the time value of money is material, provisions are determined at the present value of the expected future cash flows.

Provisions are reviewed at the end of each reporting period and adjusted to reflect the current best estimate. If it is no longer probable that an outflow of resources embodying economic benefits will be required to settle the obligation, the provision is reversed.

Provision shall be used only for expenditures for which the provision is originally recognized.

19

SHINHAN FINANCIAL GROUP CO., LTD.

Notes to the Separate Financial Statements

December 31, 2025 and 2024

3. Material accounting policies (continued)

(l) Recognition of revenues and expenses

The Company recognizes revenue by applying the following five-step revenue recognition model:

① Identify the contract → ② Identify performance obligations → ③ Determine the transaction price → ④ Allocate the transaction price to the performance obligations → ⑤ Recognize revenue once performance obligations are satisfied

i) Interest income and expenses

Interest income and expense are recognized in profit or loss using the effective interest method.

ii) Fees and commissions

The recognition of revenue for financial service fees depends on the purposes for which the fees are assessed and the basis of accounting for any associated financial instrument.

ii-1) Fees that are an integral part of the effective interest rate of a financial instrument

Such fees are generally treated as an adjustment to the effective interest rate. Such fees may include compensation for activities such as evaluating the borrower’s financial condition, evaluating and recording guarantees, collateral and other security arrangements, preparing and processing documents, closing the transaction and the origination fees received on issuing financial liabilities. However, when the financial instrument is measured at fair value with the change in fair value recognized in profit or loss, the fees are recognized as revenue when the instrument is initially recognized.

ii-2) Fees earned as services are provided

Fees and commission income, including investment management fees, sales commission, and account servicing fees, are recognized as the related services are provided.

ii-3) Fees that are earned on the execution of a significant act

The fees that are earned on the execution of a significant act including commission on the allotment of shares or other securities to a client, placement fee for arranging a loan between a borrower and an investor and sales commission, are recognized as revenue when the significant act has been completed.

iii) Dividend income

Dividend income is recognized when the shareholder’s right to receive payment is established.

20

SHINHAN FINANCIAL GROUP CO., LTD.

Notes to the Separate Financial Statements

December 31, 2025 and 2024

3. Material accounting policies (continued)

(m) Income tax

Income tax expense comprises current and deferred tax. Current tax and deferred tax are recognized in profit or loss except to the extent that it relates to a business combination, or items recognized directly in equity or in other comprehensive income.

The Company applies the consolidated tax payment system, under which the Company, as the parent corporation, and its domestic subsidiaries subject to the parent’s consolidated control (hereinafter referred to as the “Consolidated Subsidiaries”) are treated as a single taxable unit for purposes of calculating a single tax base and tax liability.

The Company evaluates the probability of realizing temporary differences by considering the future taxable profit of each entity and the consolidated group and recognizes changes in deferred tax assets (liabilities), except those recognized directly in equity, in profit or loss as income tax expense. In addition, given the Company, as the consolidated parent corporation, files a corporate tax return and pays corporate tax, it recognizes total consolidated income taxes payables and income tax allocated to each subsidiary as liabilities and receivables from subsidiaries, respectively, within its stand-alone financial statements.

The carrying value of deferred tax assets is reviewed at the end of each reporting period. The carrying value of deferred tax assets is reduced when it is no longer likely that sufficient taxable income will be generated to use benefits from deferred tax assets.

Because of the tax polices taken by the Company, tax uncertainties arise from the complexity of transactions and differences in tax law analysis. Also, it arises from a tax refund suit, tax investigation, or a refund suit against the tax authorities' tax amount. The Company paid the tax amount by the tax authorities in accordance with K-IFRS No. 2123. However, it will be recognized as the corporate tax assets if there is a high possibility of a refund in the future. In addition, the amount expected to be paid as a result of the tax investigation is recognized as the tax liability.

The company is subject to the Global Minimum Corporate Tax Act and has applied the temporary exception for deferred taxes under K-IFRS No. 1012. Accordingly, the company does not recognize deferred tax assets and liabilities related to the Global Minimum Corporate Tax Act and does not disclose information related to deferred tax. However, the company separately discloses details of the current income tax expense (income) related to the Global Minimum Corporate Tax Act.

21

SHINHAN FINANCIAL GROUP CO., LTD.

Notes to the Separate Financial Statements

December 31, 2025 and 2024

3. Material accounting policies (continued)

(n) New standards and amendments not yet adopted by the Company

The following new accounting standards and amendments have been published that are not mandatory for annual periods beginning on or after January 1, 2025, and have not been early adopted by the Company.

i) Amendments to K-IFRS No. 1109 ‘Financial Instruments’ and K-IFRS No. 1107 ‘Financial Instruments: Disclosures’ – Classification and measurement requirements of financial instruments

i -1) Derecognition of financial liabilities settled through electronic transfers

The amendments permit an entity, subject to specified criteria, to consider a financial liability (or a portion thereof) that is settled through an electronic payment system as extinguished (and derecognized) prior to the settlement date. When this accounting policy is elected, it must be applied consistently to all settlements made through the same electronic payment system.

i -2) Classification of financial assets

- Contractual terms and conditions consistent with a basic lending arrangement

The amendments provide guidance on how to assess whether the contractual cash flows of a financial asset are consistent with a basic lending arrangement. This guidance is intended to support entities in applying the contractual cash flow characteristics assessment to financial assets with features linked to environmental, social and governance (ESG) factors.

- Non-recourse financial assets

The amendments enhance the explanation of the term ‘non-recourse’, clarifying in particular that a financial asset has non-recourse characteristics when the entity’s ultimate contractual right to receive cash flows is limited to the cash flows generated from specified assets.

- Contractually linked instruments

The amendments clarify the characteristics that distinguish contractually linked instruments from other transactions. Specifically, they emphasize that, in such instruments, the priority of payments to holders of multiple contractually linked instruments (tranches) is established through a waterfall payment structure, resulting in the concentration of credit risk and the uneven allocation of losses among holders of different tranches. In addition, the amendments explain that not all transactions involving multiple debt instruments meet the criteria for contractually linked instruments and clarify that the pool of underlying assets may include financial assets that are outside the scope of the classification requirements of this standard.

i -3) Disclosures

- Investments in equity instruments designated at fair value through other comprehensive income (FVOCI)

The requirements of K-IFRS No. 1107 have been amended to require entities to separately present fair value gains or losses related to investments derecognized during the reporting period and those related to investments held at the end of the reporting period, as well as to disclose fair value gains or losses recognized in other comprehensive income during the reporting period.

- Contractual terms that may change the timing or amount of contractual cash flows

The amendments require disclosure of contractual terms that may change the timing or amount of contractual cash flows as a result of the occurrence (or non-occurrence) of contingent features that are not directly related to changes in basic lending risks or costs. These disclosure requirements apply to each class of financial assets at amortized cost or at fair value through other comprehensive income, and to each class of financial liabilities measured at amortized cost.

22

SHINHAN FINANCIAL GROUP CO., LTD.

Notes to the Separate Financial Statements

December 31, 2025 and 2024

3. Material accounting policies (continued)

(n) New standards and amendments not yet adopted by the Company (continued)

The amendments are effective for annual reporting periods beginning on or after 1 January 2026 with earlier application permitted. The Company expects that there will be no material impact on the separate financial statements from these amendments.

ii) K-IFRS No. 1118 ‘Presentation and Disclosure in Financial Statements’

K-IFRS No. 1118 supersedes K-IFRS No. 1001 . While K-IFRS No. 1118 carries forward many of the requirements of K-IFRS No. 1001 without change, it also introduces new requirements. Certain paragraphs of K-IFRS No. 1001 have been relocated to K-IFRS No. 1008 and K-IFRS No. 1107, and K-IFRS No. 1007 and K-IFRS No. 1033 have been amended.

K-IFRS No. 1118 introduces the following new requirements:

- Presentation of specified categories and defined subtotals in the statement of profit or loss

- Disclosure of management-defined performance measures (MPMs) in the notes to the financial statements

- Improvements to aggregation and disaggregation requirements

The new Standard is effective for annual reporting periods beginning on or after 1 January 2027, with early application permitted. The amendments to K-IFRS No. 1007 and K-IFRS No. 1033, as well as the amended K-IFRS No. 1008 and K-IFRS No. 1107, are effective when K-IFRS No. 1118 is applied. K-IFRS No. 1118 requires retrospective application and provides specific transitional provisions. In accordance with the retrospective application requirements of the Standard, the comparative information for the year ended December 31, 2026 will be restated in accordance with K-IFRS No. 1118.

The Company is currently assessing the impact of the new Standard on its financial statements. The adoption of the Standard is not expected to affect net income. However, it is expected to affect the determination and presentation of operating profit, as income and expenses in the statement of profit or loss will be classified into new categories.

ⅲ) Annual Improvements to Korean International Financial Reporting Standards (K-IFRS)

K-IFRS annual improvements are effective for annual reporting periods beginning on or after 1 January 2026 with earlier application permitted. The Company expects that there will be no material impact on the separate financial statements from these amendments.

- K-IFRS No. 1101 ‘First-time adoption of Korean International Financial Reporting Standards’ – Hedging accounting by a first-time adopter

- K-IFRS No. 1107 ‘Financial Instruments: Disclosures’ – Gain or loss on derecognition

and Guidance on implementing K-IFRS No. 1107

- K-IFRS No. 1109 ‘Financial Instruments’ – Derecognition of lease liabilities and transaction price

- K-IFRS No. 1110 ‘Consolidated Financial Statements’ – Determination of ‘de facto agent’

- K-IFRS No. 1007 ‘Statement of Cash Flows’ – Cost method

- K-IFRS No. 1109 ‘Financial Instruments’ and K-IFRS No. 1107 ‘Financial Instruments: Disclosures’ - Contracts referencing nature-dependent electricity

23

SHINHAN FINANCIAL GROUP CO., LTD.

Notes to the Separate Financial Statements

December 31, 2025 and 2024

4. Financial risk management

(a) Overview

As a financial services provider, Shinhan Financial Group Co., Ltd. and its subsidiaries (hereinafter referred to as the “Group”) manage various risks that may arise within business area, and the main risks are credit risk, market risk, interest rate risk and liquidity risk. These risks are recognized, measured, controlled and reported in accordance with the basic risk management policies established by the controlling company and each subsidiary.

i) Risk management principles

The risk management principles of the Group are as follows:

- All business activities take into account the balance of risks and profits within a predetermined risk appetite.

- The controlling company shall present the Group Risk Management Model Standard, supervise their compliance, and have responsibility and authority for group-level monitoring.

- Operate a risk-related decision-making system that enhances management's involvement.

- Organize and operate risk management organizations independent of the business sector.

- Operate a performance management system that clearly considers risks when making business decisions.

- Aim for preemptive and practical risk management functions.

- Share a cautious view to prepare for possible deterioration of the situation.

ii) Risk management organization

The fundamental policies for risk management of the Group are established by the Board of Directors of the controlling company, while the basic risk management strategies are established by the Risk Management Committee (the “Group Risk Management Committee”) within the controlling company’s Board of Directors. The Group's Chief Risk Officer (CRO) assists the Group Risk Management Committee and consults the risk management policies and strategies of the group and each subsidiary through the Group Risk Council, which includes the Chief Risk Officer of each subsidiary. The subsidiary implements the risk management policies and strategies of the Group through each company's risk management committee, risk-related committee, and risk management organization, and consistently establishes and implements the detailed risk management policies and strategies of the subsidiary. The risk management team of the controlling company assists the Group's Chief Risk Officer for risk management and supervision.

The Company has a hierarchical limit system to manage the risks of the Group to an appropriate level. The Group Risk Management Committee sets the risk limits that can be acceptable by the Group and each subsidiary, while the Risk Management Committee and the management-level risk Commitees of each subsidiary set and manage detailed risk limits by risk, department, desk, and product types.

ii-1) Group Risk Management Committee

The Committee establishes the risk management framework for the controlling company and each of its subsidiaries and comprehensively manages Group-wide risk-related matters, including the establishment of the Group’s fundamental risk management policies and strategies and the approval of limits. The Committee consists of directors of the controlling company.

The Committee's resolutions are as follows.

- Establish risk management basic policy in line with management strategy

- Determine the level of risk that can be assumed by the Group and each subsidiary

- Approve appropriate investment limit or loss allowance limit

- Enact and amend the Group Risk Management Regulations and the Group Risk Council Regulations

- Matters concerning risk management organization structure and division of duties

- Matters concerning the operation of the risk management system

- Matters concerning the establishment of various limits and approval of limits

24

SHINHAN FINANCIAL GROUP CO., LTD.

Notes to the Separate Financial Statements

December 31, 2025 and 2024

- Make decisions on approval of the FSS's internal rating based approach for non-retail and retail credit rating systems

4. Financial risk management (continued)

(a) Overview (continued)

ii-1) Group Risk Management Committee(continued)

- Matters concerning risk disclosure policy

- Analysis of crisis situation, related capital management plan and financing plan

- Matters deemed necessary by the board of directors

- Matters required by external regulations such as the Financial Services Commission and other regulations and guidelines

- Matters deemed necessary by the Chairman

ii-2) Group Risk Management Council

In order to maintain the Group's risk policies and strategies consistently, discuss all risk-related matters of the Group and make resolutions on matters necessary to implement the policies prescribed by the Group Risk Management Committee. The members shall be chaired by the chief risk officer of the group and shall be comprised of the chief risk officer of the major subsidiaries.

iii) Risk management framework

iii-1) Management of the Risk Capital

Risk capital refers to the capital required to compensate for the potential loss (risk) if it is actually realized. Risk capital management refers to the management of the risk assets considering its risk appetite, which is a datum point on the level of risk burden compared to available capital, so as to maintain the risk capital at an appropriate level. The controlling company and subsidiaries establish and operate a risk planning process to reflect the risk plan in advance when establishing financial and business plans for risk capital management, and establish a risk limit management system to control risk to an appropriate level.

iii-2) Risk monitoring

In order to proactively manage risks by periodically identifying risk factors that can affect the Group's business environment, the Company has established a multi-dimensional risk monitoring system. Each subsidiary is required to report to the Company on key issues that affect risk management at the Group level. The Company prepares weekly, monthly and ad-hoc monitoring reports for Group management, including the CRO.

In addition, the Risk Dashboard is operated to derive abnormal symptoms through three-dimensional monitoring of major portfolios, increased risks, and external environmental changes of assets for each subsidiary. If necessary, the Company takes preemptive risk management to establish and implement countermeasures.

iii-3) Risk review

When conducting new product, new business and major policy changes, risk factors are reviewed by using a pre-defined checklist to prevent indiscriminate promotion of business that is not easy to judge risk and to support rational decision making. The subsidiary's risk management department conducts a preliminary review and post-monitoring process on products, services, and projects to be pursued in the business division. In case of matters that are linked or jointly promoted with other subsidiaries, the risk reviews are carried out after prior-consultation with the risk management department of the controlling company.

25

SHINHAN FINANCIAL GROUP CO., LTD.

Notes to the Separate Financial Statements

December 31, 2025 and 2024

4. Financial risk management (continued)

(a) Overview (continued)

iii) Risk management framework (continued)

iii-4) Crisis management

The Company maintains a group-wide risk management system to detect the signals of any risk crisis and, in the event of a crisis actually happening, to respond on a timely, efficient and flexible basis so as to ensure the Group’s survival as a going concern. Each subsidiary maintains crisis planning for four levels of contingencies, namely, “cautious’, “alert”, “imminent crisis” and “crisis”, determination of which is made based on quantitative and qualitative monitoring and consequence analysis, and upon the happening of any such contingency, is required to respond according to a prescribed contingency plan. At the controlling company level, the Company maintains and installs crisis detection and response system which is applied consistently group-wide, and upon the happening of any contingency at two or more subsidiary levels, the Company directly takes charge of the situation so that the Company manages it on a concerted group wide basis.

(b) Credit risk

i) Credit risk management

Credit risk is the risk of potential economic loss that may be caused if a customer or counterparty to a financial instrument fails to meet its contractual obligations, and is the largest risk which the Company faces. The Company’s credit risk management encompasses all areas of credit that may result in potential economic loss, including not just transactions that are recorded on the balance sheet, but also off-balance-sheet transactions such as guarantees, loan commitments and derivative transactions.

< Techniques, assumptions and input variables used to measure impairment>

i-1) Determining significant increases in credit risk since initial recognition

At the end of each reporting period, the Company assesses whether the credit risk on a financial instrument has increased significantly since initial recognition. When making the assessment, the Company uses the change in the risk of a default occurring over the expected life of the financial instrument instead of the change in the amount of expected credit losses. To make that assessment, the Company compares the risk of a default occurring on the financial instrument as at the reporting date with the risk of a default occurring on the financial instrument as at the date of initial recognition and consider reasonable and supportable information, that is available without undue cost or effort, that is indicative of significant increases in credit risk since initial recognition. This information includes the default experience data we have and the analysis results of internal credit rating experts.

① Measuring the risk of default

The Company assigns an internal credit risk rating to each individual exposure based on observable data and historical experiences that have been found to have a reasonable correlation with the risk of default. The internal credit risk rating is determined by considering both qualitative and quantitative factors that indicate the risk of default, which may vary depending on the nature of the exposure and the type of borrower.

② Measuring term structure of probability of default

Internal credit rating is a key input variable for determining term structure of probability of default. The Company accumulates information after analyzing the information regarding exposure to credit risk and default information by the type of product and borrower and results of internal credit risk assessment. For some portfolios, the Company uses information obtained from external credit rating agencies when performing these analyses.

26

SHINHAN FINANCIAL GROUP CO., LTD.

Notes to the Separate Financial Statements

December 31, 2025 and 2024

4. Financial risk management (continued)

(b) Credit risk (continued)

i) Credit risk management (continued)

i-1) Determining significant increases in credit risk since initial recognition (continued)

② Measuring term structure of probability of default (continued)

The Company applies statistical techniques to estimate the probability of default for the remaining life of the exposure from the accumulated data and to estimate changes in the estimated probability of default over time.

③ Significant increases in credit risk

The Company uses the indicators defined as per portfolio to determine the significant increase in credit risk, and such indicators generally consist of changes in the risk of default estimated from changes in the internal credit risk rating, qualitative factors, days of delinquency, and others.

i-2) Risk of default

The Company considers a financial asset to be in default if it meets one or more of the following conditions:

- if a borrower is overdue by 90 days or more from the contractual payment date

- if the Company judges that it is not possible to recover principal and interest without enforcing the collateral on a financial asset

The Company uses the following indicators when determining whether a borrower is in default:

- Qualitative factors (e.g. breach of contractual terms),

- Quantitative factors (e.g. if the same borrower does not perform more than one payment obligations to the Company, the number of days past due per payment obligation. However, in the case of a specific portfolio, the Company uses the number of days past due for each financial instrument),

- Internal observation data and external data

The definition of default applied by the Company generally conforms to the definition of default defined for regulatory capital management purposes; however, depending on the situations, the information used to determine whether a default has incurred, and the extent thereof may vary.

27

SHINHAN FINANCIAL GROUP CO., LTD.

Notes to the Separate Financial Statements

December 31, 2025 and 2024

4. Financial risk management (continued)

(b) Credit risk (continued)

i) Credit risk management (continued)

i-3) Reflection of forward-looking information

The Company reflects forward-looking information presented by internal experts based on a variety of information when measuring expected credit losses. For the purpose of estimating this forward-looking information, the Company utilizes the economic outlook published by domestic and overseas research institutes or government and public agencies.

The Company identified the key macroeconomic variables needed to forecast credit risk and credit losses for each portfolio as follows by analyzing data obtained from past experience and drew correlations across credit risk for each variable. After that, the Company has reflected the forward-looking information through a regression estimation.

Key macroeconomic variables |

|

Correlation with credit risk |

GDP growth rate |

|

(-) |

Private consumption growth rate |

|

(-) |

Facility investment growth rate |

|

(-) |

Consumer price index growth rate |

|

(+) |

Balance on current account |

|

(-) |

The predicted correlations between the macroeconomic variables and the risk of default, used by the Company, are derived based on data from over past ten years.